Embed Size (px)

Citation preview

1

The View fromHOUSTON

First quarter results are pouring in and we are doing our best to keep our forecast models up-to-date. So far, all of our model portfolio stocks have reported strong results with most of them topping my forecast models. Crude oil prices have rebounded since the last newsletter and the North American natural gas market continues to tighten, with storage now over 100 Bcf below the 5-year average. If commodity prices hold near current levels, our favorite companies should do quite well this year.

Our Sweet 16 is poised to do great things this next year. With crude oil prices rebounding, what can we expect these next few months?

“Seek and ye shall find.”At EPG we are seeking out the best energy stocks and we bring those companies to the attention of our members.

By: Dan Steffens, President

Energy Prospectus Newsletter: The “View from Houston” May 7, 2013 Issue: 72

INSIDE THIS ISSUE1 Bakken Takeover Targets

3 EPG Upcoming Events

4 Sweet 16 Growth Portfolio

6 Small-Cap Growth Portfolio

7 High Yield Income Portfolio

9 EPG Disclaimer

Dan Steffens is the President of Energy Prospectus Group (EPG), a networking orga-nization based in Houston, Texas. He is a 1976 graduate of Tulsa

University with an undergraduate degree in Accounting and a Masters in Taxation.

Mr. Steffens began his career in public accounting, becoming licensed as a CPA in 1978. After four years in public accounting, he transitioned to the oil & gas industry with the bulk of his time (18 years) spent with Amerada Hess Corporation (HES). He served as the Hess United States E&P Division Controller from 1994 to 2001.

Bakken Takeover TargetsWhen oil & gas reserves are cheaper on Wall Street than average finding & development costs, it just makes more sense for the large-cap E&P companies to take over the smaller companies. In fact, many small-caps are built with that idea in mind. You may recall that EPG members recently did quite well on sales of two former Sweet 16 Growth Portfolio companies Brigham Exploration (BEXP) and

2

GeoResources (GEOI), whose CEO’s were clearly looking for buyers.

I think the Bakken is now ripe for another round of takeovers this summer and several companies in our model portfolios are prime targets.

•ContinentalResources(CLR) •EOGResources(EOG) •KodiakOil&Gas(KOG) •OasisPetroleum(OAS) •WhitingPetroleum(WLL) •TrianglePetroleum(TPLM) •SMEnergy(SM)

During my last three years with Hess Corp. (HES), I was on a businessdevelopment team tasked with looking for undervalued targets with assets that were a good fit for Hess. Believe me, there are teams of analysts doing it for all of the large-caps. In fact, in a mature region like North America, an aggressive acquisition strategy is the fastest way to grow a company. Just look at the history of Apache Corp. (APA), Anadarko Petroleum Corp. (APC) and Devon Energy (DVN). All three of them grew rapidly through a series of mergers with smaller E&P companies.

A Bulls Eye is clearly on the Bakken

The growth of the Bakken oilformation has been incredible. In a presentation late last year, MarkPapa, CEO of EOG Resources (EOG) said, "... there are only two meaningful oil plays in the United States - the Bakken and the Eagle Ford.” I will argue that the Permian Basin is now right up there, thanks to horizontal drilling technology.

As a result of North Dakota’s good fortune to have most of the Bakken within its borders and its strong support for the industry, the state is now the second-largest oil producer intheU.S.afterTexas.Italsohasanear zero unemployment rate and you can make $20/hour working at a burger joint.

TheU.S. Geological Survey (USGS) recently updated a geology based

Figure 1

assessment of the Williston Basin. TheUSGSnowestimates therearestill 7.4 billion barrels of oil, 6.7 trillion cubic feet of natural gas and 0.53 billion barrels of natural gas liquids that can be recovered from the Bakken and Three Forksformations using today’s technology. Continental Resources (CLR) CEO Harold Hamm thinks the recoverable volumes are triple what is in the new USGS report. Even Harold’s higher number is less than ten percent of the estimated oil in place, so we can expecttheindustrytobeharvestingoil from this region for several decades,atleast.Thisisthekindofthing the majors should be all over, which is why I believe they have teams of analysts looking for ways to get them a large stake in the play. Since almost all of the good acreage is leased, the only way to get a meaningful position is to go out and

buy a company that holds it.

Figure 1 just shows the Williston Basin in the United States. It does extendupintoCanada.

We won’t know for decades who’s right about the total oil & gas that will be recovered, but it is now crystal clear that North Dakota contains a massive amount of valuable hydrocarbons. The recentimprovements in horizontal drilling and multi-stage fracing have made shale oil & gas, that was previously thought to be sub-economic to produce, incredibly profitable.

America is producing more than 7 million barrels of oil a day, the highest volume since 1992, according to figures released by the U.S. Energy Information Administration. TheU.S.isnowforecasttoovertake

3

Saudi Arabia as the world's top oil producer in just a few years thanks to rapid production growth in the Bakken, Eagle Ford and Permian Basin. Note that Texas and NorthDakota are leading the way, not just because they hold the best resource plays, but because they support the energy business. You’d think bankrupt states like California and New York would notice and get more supportive of the only industry that can save their economies, but that is asubjectofanotherarticle.Themapbelow shows how blessed we are with shale resources. I sure am glad to be living in Texas where theeconomy is booming.

The Bakken Petroleum Systemcovers over 9 million acres. It is an unconventional oil resource deposited during the Devonian and Mississippian periods. It is a self-sourcing petroleum resource that hasup to35%organiccontent.TheBakken extends from the easternedge of the Williston Basin in North Dakota to the Bakken Fairway in northwest Montana and north intoCanada. The western boundary oftheBakken isdefinedby theRockyMountain Thrust Belt. The BakkenFormation remains remarkably consistent from the Nesson Anticline (discoveredbyAmeradaHessCorp.in1950)on theeasternedge to thewestern boundary in northwest Montana. TheBakken does extendup into Canada, where PetroBakken Energy Ltd. (PBKEF) has drilled hundreds of successful wells.

Just to give you an idea of the recent valuations being placed on the Bakken / Three Forks play, QEPResources(QEP)recentlypurchased27,000 acres in the Williston Basin for an estimated $40,000 per undeveloped acre, a new record. It is mind-boggling to me that any acreage is that valuable.

Former Sweet 16 Growth Portfolio company,BrighamExplorationwasone of the first companies to prove that horizontal drilling and multi-stage fracing could generate outstanding financial results from the Bakken. Brigham was followed

Figure 2

by the medium to larger companies moving in. Companies like Whiting Petroleum (WLL), Oasis Petroleum (OAS), Northern Oil & Gas (NOG), Kodiak Oil & Gas (KOG) and Continental Resources (CLR), are smaller players that are now becoming takeover targets based on their cheap market cap valuations and significant undeveloped proven acreage.

The big boys have already started to make their move:

• Exxon Mobil (XOM) moved into the Bakken when they took over XTOEnergyin2010.XTOEnergy

is now a wholly owned subsidiary of Exxon. Exxonadded to their stake at the end of last year in a deal that included $1.6 billion in cash and additional working interest considerations.

•Apache Corp. (APA) entered the Bakken with a big acquisition of 300,000 Bakken acres in Montana.

•Statoil ASA (STO) bought Brigham and its Bakken acreage for $4.4 billion. Some EPG members made a ton of money on that deal.

This newsletter is brought to you by:

4

It is just natural for the large companies to take over the development of the Bakken. Theyhave the capital and the large technical teams needed for a job of this size. It will take over 100,000 wells to fully develop the Bakken / ThreeForksandmorecapitalthanIcan imagine; good news for our favorite onshore drillers, Helmerich & Payne (HP) and Unit Corp. (UNT).

In my opinion, Kodiak Oil & Gas (KOG), Oasis Petroleum (OAS) and Triangle Petroleum (TPLM) are the most likely takeover targets because they are pure plays on the Bakken / ThreeForks.Continental Resources (CLR) may actually be in play because of the much publicized divorce of the company’s founder and CEO. EOG and Whiting Petroleum (WLL) have a lot more going on than just the Bakken, so they may just sell their stake in the play or become a buyer themselves. SM Energy (SM) holds over 160,000 netacresintheBakken/ThreeForksand I would be thrilled to see them sell it and use the money to accelerate development of their Eagle Ford acreage.

In my opinion, the best way to play this as an investor is to spread the risk. A takeover of any one of the Bakken players mentioned above will draw more attention to the valuations of the entire pack.

Disclosure: I have long positions in CLR, CRZO, DNR, ENRJ, EXXI, GPOR, GTE, MIND, MMP, MWE, NFX, PMG.TO, PBKEF, TGA and UNT. I do not

intend on buying or selling any securities mentioned in this newsletter within 72 hours of the publication date on page one. I am not receiving compensation from any of the companies mentioned in this newsletter. See the DISCLAIMER on the last page of this newsletter for more details.

Sweet 16 Growth PortfolioPrior to the date of this newsletter, sixoftheSweet16companies(DNR,HP, KOG, RRC, SM andWLL) hadreported strong first quarter results.

Denbury Resources (DNR) closed on the acquisition of producing properties in the Cedar Creek Anticline area from ConocoPhillips lateinthequarter.Theywillreportasignificant increase in production during the second quarter. DNRdeserves to trade at a much higher multiple than where it stands today because it has very long-lived crude oil reserves.

Helmerich & Payne (HP) continues to pump out solid earnings and cash flows from operations. TheirFlexRigsareinhighdemandinallofNorth America’s shale plays as they are perfect fits for drilling multiple horizontal wells from pads. HP is much more than a drilling company. Companies that engage HP quickly discover that in addition to the world’s best drilling equipment, they are getting a first class engineering team to help them reduce drilling time and lower their costs.

5

Kodiak Oil & Gas (KOG) is on-track to increase production by more than 80% this year. I’m expecting thecompany to increase production each quarter, but really ramp it up sharply during the second half of thisyearafterSpringBreakup.KOGshould have a very impressive year-end reserve report. As I mentioned in the openingarticle,KOGisnearthetopof my list as a prime takeover target.

Range Resources (RRC) is the only “gasser” in the portfolio. All they do is just keep beating my production forecast quarter-after-quarter. If I’m right about natural gas prices pushing up to $5.00/mcf by year-end, RRC shouldmake a heck of arun down the stretch.

SM Energy (SM) has posted the most impressive first quarter results so far.Thestockistradingatjustover4X my current cash flow per share forecastforthisyear.Theyreportedmuch better than expectedproduction from their Eagle Ford wells and they are having strong drilling results in the Permian Basin. Theyhaveaniceblockofacreageinthe Bakken, which I wish they would sell since the rate of return on their Eagle Ford and Permian Basin wells is better. I have raised my Fair Value Estimate to $93.70/share which is just 5X CFPS. In my opinion, it has a shot at a much higher multiple if

Company Name Primary Product

Stock Symbol

Share Price

EPG Fair Value

Estimate

Percent Undervalued

5/3/13

BONANZA CREEK ENERGY OIL BCEI $36.15 $54.00 49.38%

CARRIZO OIL & GAS OIL CRZO $25.85 $39.40 52.42%

CIMAREX ENERGY OIL XEC $74.03 $90.00 21.57%

CONTINENTAL RESOURCES OIL CLR $80.58 $116.00 43.96%

DENBURY RESOURCES INC. OIL DNR $17.88 $30.20 68.90%

EOG RESOURCES OIL EOG $123.98 $166.25 34.09%

ENERGY XXI OIL EXXI $23.33 $53.40 128.89%

GULFPORT ENERGY CORP OIL GPOR $53.40 $62.00 16.10%

HELMERICH & PAYNE Services HP $61.75 $74.10 20.00%

KODIAK OIL & GAS OIL KOG $7.92 $12.50 57.83%

OASIS PETROLEUM OIL OAS $34.26 $51.75 51.04%

RANGE RESOURCES GAS RRC $74.43 $84.65 13.73%

ROSETTA RESOURCES OIL ROSE $42.60 $72.25 69.60%

SM ENERGY GAS SM $61.76 $93.70 51.72%

UNIT CORP. Services UNT $43.00 $69.20 60.93%

WHITING PETROLEUM OIL WLL $45.38 $85.00 87.31%

Sweet 16 Growth Portfolio

theycontinuetomeetorexceedmyproduction forecasts.

Whiting Petroleum (WLL) is the top oil producer in North Dakota. Every time I take a hard look at this company I shake my head in disbelief at the share price compared to its peers. First Call’s target price is $60.72, which would certainly be a welcome move for shareholders, but I think it deserves a much higher price. In addition to being a leading companyintheBakken/ThreeForks,Whiting has a tertiary recovery project(CO2flood)inWestTexasthatis ramping up to 9,000 BOE per day (mostlyoil)andtheirRedtailprospectin the Denver Basin is getting great results in the Niobrara “A” and “C”

SM Energy’s Eagle Ford Production

6

zones. If I were advising a major looking to jump into the Bakken, I’d be telling them to make a hard run at Whiting. Each share of WLLrepresents over 3.1 boe of proven reserves based on the company’s 3rd party reserves report. This iswhat I mean when I said that oil is a lot cheaper on Wall Street these days.

TheSweet16isourMid-CapGrowthPortfolio. These companies wereselected because they have very strong production and proven reserves growth locked in. It is nice that they report solid earnings quarter-after-quarter, but the real value of any E&P company is their proven reserves plus their growth potential.

Small-Cap PortfolioOur Small-Cap Growth Portfolio is a group that I believe has what it takes to grow into solid mid-caps. In fact, it can be argued that Gran Tierra Energy (GTE) and TransGlobe Energy (TGA) are already there. I’m keeping these two Calgary based companies in the small-cap portfolio, but I don’t

expect this risk adverse market topay up for what these stocks are worth anytime soon. Investors just don’t want to deal with the unknowns of doing business in Columbia and Egypt these days. But crude oil trades on a global market and I believe it is wise to have international

exposure in a balanced portfolio.They both have rock solid balancesheets with very little debt. Investors with a longer term outlook should be accumulating these two on the dips.

Three of the companies in theportfolio have reported first quarter results. We will be updating our forecasts models within days after they report earnings and we will update all of our detailed company profiles later this month.

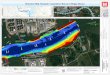

Approach Resources (AREX) reported first quarter production in-linewithmyforecast.Thecompanyis driving down their completed well costs and the initial results from their stacked wellbore pilot program in their Pangea horizontal Wolfcamp shaleplayareencouraging.Thefirsttwo stacked wellbores were completed with initial rates of 705 Boe/day and 843 Boe/day. By stackingwellboresAREXexpectstoincrease recoverable reserves per well. As you can see in the map above, AREX has a lot of runningroom in the Permian Basin with over 2,000 identified horizontal drilling locations.

I believe this is going to be a significant turnaround year for Comstock Resources (CRK). I

Company Name

Primary Product

Stock Symbol

Share Price

EPG Fair Value

Estimate

Estimated Undervalued

5/3/13

APPROACH RESOURCES OIL AREX $25.30 $31.40 24.11%

COMSTOCK RESOURCES GAS CRK $15.55 $26.40 69.77%

ENERJEX RESOURCES OIL ENRJ $0.61 $1.15 88.52%

EVOLUTION PETROLEUM OIL EPM $9.97 $15.00 50.45%

GRAN TIERRA ENERGY OIL GTE $5.65 $10.00 76.99%

MITCHHAM INDUSTRIES INC Services MIND $14.56 $21.50 47.66%

OSAGE EXPL & DEV OIL OEDV $1.38 $2.00 44.93%

SARATOGA RESOURCES OIL SARA $2.20 $4.75 115.91%

SWIFT ENERGY OIL SFY $13.05 $30.00 129.89%

TRANSGLOBE ENERGY OIL TGA $8.17 $15.25 86.66%

TRIANGLE PETROLEUM OIL TPLM $5.65 $10.25 81.42%

Small-Cap Growth Portfolio

7

listened to their quarterly conference call and there was definitely a more upbeat feel to the call. Comstock will close on the sale of their Permian Basin assets to Sweet 16 member Rosetta Resources (ROSE) in the 2nd quarter and book a $250 million gain on the sale. The company shouldreport about $3.00 earnings per share for the second quarter. Thissale will shore up the company’s balance sheet and allow them to focus on their Eagle Ford shale development program. Comstock is the most leveraged company in the small-cap portfolio to increasing natural gas prices.

Swift Energy (SFY) had a good first quarter with cash flow per share of $1.63, slightly above my forecast due to strong realized oil & gas prices and increasing production. Earnings per share beat my forecast by $0.04. Management announced that theyare working on a joint venture for their Eagle Ford acreage that should be closed in the 3rd quarter. I am nowexpectingSwift’sproductiontodip a little in the second quarter, and then accelerate into year-end. If you want a small-cap that will get a major boost from increasing natural gas prices, you should take a hard look at my forecast model for SFY.

Terry Swift, CEO of Swift Energycommented, “Swift Energy delivered strong operational results during the first quarter. Our refined drilling and completion techniques in the Eagle Ford shale and the strong performance of our base production in Lake Washington resulted inhigher than forecast production volumes. We’re encouraged by our progress so far this year.

“Near term, our focus remains on improving performance, cost efficiencies and results throughout our active operational areas. We are also taking steps to introduce new, high value opportunities to our operations through horizontal drilling in the Louisiana Wilcox, horizontaldrilling in the Southwestern Colorado Niobrara and Subsalt exploration inSouth Louisiana. Finally, asdemonstrated by the sale of our

Primary Stock Share Estimated

Company Name Product Symbol Price Annual Yield

5/3/13

PETROBAKKEN ENERGY LTD OIL PBKEF $8.26 11.5%

GASTAR EXPLORATION - Pfd GAS GST-PA $23.23 9.3%

SEADRILL LIMITED DRILLER SDRL $38.80 8.8%

LINN ENERGY (Upstream) MLP LINE $38.44 7.6%

VANGUARD NAT RES (Upstream) MLP VNR $28.41 8.7%

HI CRUSH PARTNERS MLP HCLP $17.94 10.6%

HOLLY ENERGY PARTNERS MLP HEP $37.03 5.2%

MAGELLAN MIDSTEAM PARTNERS MLP MMP $52.04 3.9%

MARKWEST ENERGY PARTNERS MLP MWE $60.70 5.5%

PLAINS ALL AMERICAN PIPELINE MLP PAA $57.45 4.0%

PLAINS ALL AMERICAN PIPELINE MLP PAA $55.89 4.1%

High Yield Income Portfolio

Brookeland field, we will be looking at monetizing assets we control that are not a focus of our operations to bring forward unrecognized value in our portfolio.”

After listening to the Denbury Resources’ (DNR) first quarter conference call, I am now convinced thattheDelhiFieldTertiaryRecoveryProjectinLouisianawillreachpayoutlate in the thirdquarter. Thismeansthat Evolution Petroleum’s (EPM) net revenue interest in the field will increase from 7.4% to 26.5%. EPMreports first quarter results this week.

High Yield Income PortfolioOur Income Portfolio is focused on finding energy sector stocks, bonds andMLPunits that offer high yieldwithareasonable levelofrisk. TheMLPs in the portfolio have a trackrecord of increasing their distributions to unit holders year-after-year, which is a great way to stayaheadofinflation.Keepthatinmindasyou lookat the chart. TheannualyieldsfortheMLPsarebased

on their current distributions to unit holders, not expected futuredistributions. It is a good idea to checkeachMLP’swebsiteandlookattheir distribution history before investing. The seven I’ve selectedare all expected to increasedistributions this year.

Last week I addedSeaDrill Limited (SDRL) common stock to the portfolio and I dropped Evolution Petroleum 8.5% Series A Pfd stock (EPM-PA)because I think they will call their preferred soon after the Delhi Field reaches payout. I also decided to drop the Magnum Hunter Resources Corp. Pfd stock (MHR-PD) until we see some resolution of their accounting issues.

Gastar Exploration, Ltd. (GST) reported first quarter results that beat both the First Call earnings per share estimates and my forecast model. I am still recommending that cautious investors stick with their preferred stock (GST-PA), which Ibelieve will continue to drift up to the par value. I am also considering addingGSTtoourSmall-CapGrowthPortfolio.

8

Iamexpectingastrongfirstquarterfrom PetroBakken Energy Ltd. (PBN.TO and PBKEF). They’ve alreadyannounced that first quarter production averaged 49,078 barrels of oil equivalent per day ("boepd")(82% light oil and liquids), a 4%increase over the fourth quarter of 2012. First quarter funds flow from operations exceeded what I had inmy forecast model. Unless there is a big drop in the price of crude oil, PetroBakken has more than enough cash flow to pay their monthly dividends.

PetroBakken also announced they will be changing the company's nametoLightstreamResources,Ltd.in a couple months. Since the Cardium is quickly becoming their top area of production this name change makes sense, plus it may bring some attention to a grossly undervalued common stock.

Final ThoughtsFirst quarter results are pouring in onadailybasis.Thiskeepsmeverybusy updating forecast models and profiles.

April was a fantastic month for the Energy Prospectus Group. We picked up over 60 new members from Value

Forum. My trip to Scottsdale andthenontoLasVegaswasfantastic.Imade a lot of new friends and some valuable contacts. Life is all aboutnetworking and interdependence with our fellow human beings. By working together we can all achieve so much more and have a more rewardinglife.ThereasontheKevinand I formed EPG back in 2001 was to help our members make money. I believe that if you focus on helping others achieve their goals that you have a better chance of reaching your own.

I am encouraged by the rebound last week in crude oil prices and I see the North American natural gas market continue to tighten. So far, I have not been disappointed by first quarter results from any of our portfolio companies. It sure feels like things are setting up for a strong second half of this year for the energy sector.

Thank you for your support.

Keep an eye on the macro-environment, but look closely at the details before you invest in anything and good luck!

Dan Steffens, PresidentEnergy Prospectus Group

9

© 2013 Energy Prospectus Group

EPG Disclaimer

The analysis and information in this newsletter and the reports & financial models on our website are for informational purposes only. No part of the material presented in this NEWSLETTER and/or reports on our websites is intended as an investment recommendation or investment advice. Neither the information nor any opinion expressed herein constitutes a solicitation to purchase or sell securities or any investment program. The opinions and forecasts expressed are those of the PUBLISHER (Energy Prospectus Group, a division of DMS Publishing, LLC) and may not actually come to pass. The opinions and viewpoints regarding the future of the markets should not be construed as recommendations of any specific security nor specific investment advice. Investors should always consult an investment professional before making any investment.

Investments in equities carry an inherent element of risk including the potential for significant loss of principal. Past performance is not an indication of future results.

Any investment decisions must in all cases be made by the reader or by his or her investment adviser. Do NOT ever purchase any security without doing sufficient research. There is no guarantee that the investment objectives outlined will actually come to pass. All opinions expressed herein are subject to change without notice. Neither the PUB-LISHERS, editor, employees, nor any of their affiliates shall have any liability for any loss sustained by anyone who has relied on the information provided.

The analysis provided is based on both technical and fundamental research and is provided ''as is'' without warranty of any kind, either expressed or implied. Although the information contained is derived from sources which are believed to be reliable, they cannot be guaranteed.

The information contained in the NEWSLETTERS is provided by Energy Prospectus Group, a division of DMS Publishing, LLC. Employees and affiliates of Energy Prospectus Group may at times have positions in the securities referred to and may make purchases or sales of these securities while publications are in circulation. PUBLISHER will indicate whether he has a position in stocks or other securities mentioned in any publication. The disclosures will be accurate as of the time of publication and may change thereafter without notice.

Index returns are price only and do not include the reinvestment of dividends. The S&P 500 is a stock market index containing the stocks of 500 large-cap corporations, most of which are US companies. The index is the most notable of the many indices owned and maintained by Standard & Poor's, a division of McGraw-Hill.