Embed Size (px)

Citation preview

The Second Great Depression≈

Causes & Responses

by

Colin Campbell

ASPO IRELAND

Outline

1. Geological Reality“You have to find it first”

2. Discovery & Production starts & ends – growth is followed by decline

3. Explanation of Confusion

4. Consequences

5. Reactions

PETROLEUM GEOLOGY

in3 Minutes

On a mule in Colombia in 1960

Extreme Global Warminggave excessive Algal Growths

Organic debris

90 & 150 million years ago

Rifts formed as the Continents moved apart

Chemical reactions converted

organic debris into oil when

buried & heated

Rifts filled by sediment washed in

from borderlands

And then came the rains

N.W EuropeOil Generating

Zones-

Where oil is and

where it is not

8

Oil

Gas

Water

Geology of an Oilfield

SandstoneReservoir Migrating Oil

Seal

CriticalTemperature

60-120 0C

Water well

Depletion is Easy to GraspAs every beer drinker knows:

“Glass starts full, and ends empty”– The quicker you drink it, the sooner it is gone

• The same principle applies to oil and gasHow has this self-evident reality been concealed ?• It is so obvious yet it is a DEVASTATING REALISATION

A Fixed Quantity

Oil was formed in the geological past– We can’t “grow” more

Are we Running Out? – We started running out with the first barrel– The last barrel is far in the future

But production begins to decline when half is gone - THAT IS THE ISSUE

Why we need to know

Oil & Gas now dominate our lives40% of traded energy is oil>90% transport fuel is oil

• Trade depends on transport

Much electricity is made from gas

Critical for agriculture - people eat– Fuels the tractor, transports the produce– Gives synthetic nutrients and pesticides

Why were n’t we told?Oil companies reported Commercial Reserves to meet

strict Stock Exchange rules

They under-reported discovery & revised upwards– A comforting but misleading image of steady growth

– No conspiracy - just simple commercial prudence

OPEC over-reported

PUBLIC NUMBERS ARE VERY UNRELIABLE• and difficult to decode

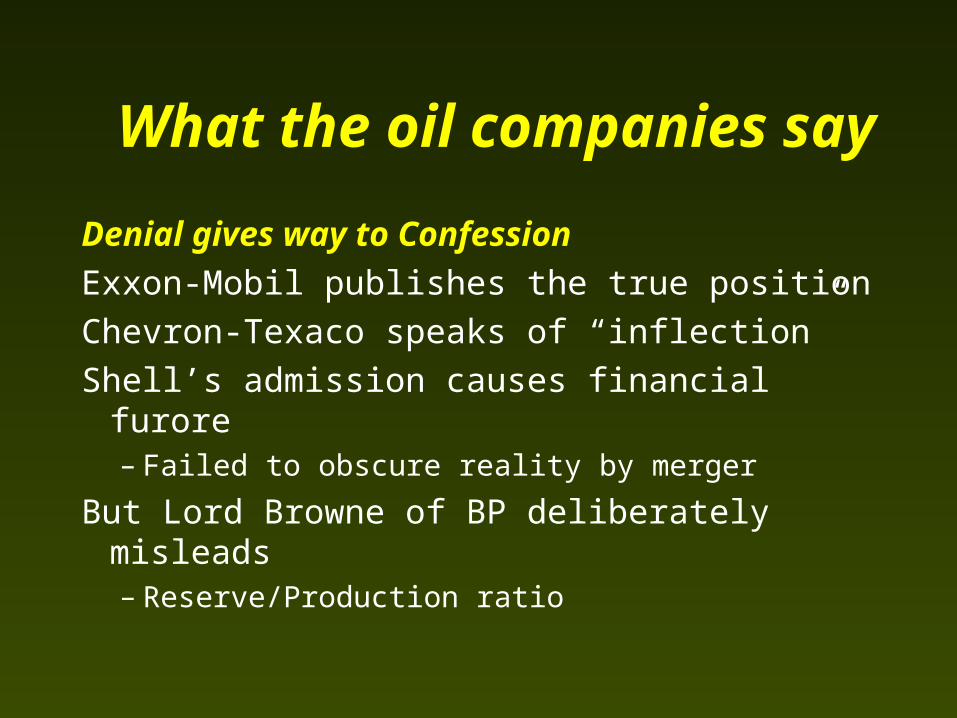

What the oil companies say

Denial gives way to Confession

Exxon-Mobil publishes the true position

Chevron-Texaco speaks of “inflection”

Shell’s admission causes financial furore– Failed to obscure reality by merger

But Lord Browne of BP deliberately misleads– Reserve/Production ratio

OPECReserve

Reporting

Competingfor

Quota

Kuwait 1984Produced = 23 GbRemaining = 64Found = 87 (~90)

Reality and Illusion

0

500

1000

1500

2000

2500

1930 1950 1970 1990 2010 2030Cumulative Discovery, Gb

Inflexion due tofalling Discovery

Illusion

As ReportedActual

Reality

A few Examples

The same pattern everywhere– but for minor variants

Production mirrors discovery

US-48

0

5

10

15

20

25

30

1930 1950 1970 1990 2010 2030 2050

Discovery Gb

0

2000

4000

6000

8000

10000

Production kb/d

Peak to Peak 40 years

Peak Discovery

Egypt

00.20.40.60.8

11.21.41.61.8

1930 1950 1970 1990 2010 2030 2050

Discovery Gb

0

200

400

600

800

1000

Production kb/d

Peak to Peak 30 years

Indonesia

0

1

2

3

4

5

6

1930 1950 1970 1990 2010 2030 2050

Discovery Gb

020040060080010001200140016001800

Production kb/d

Peak to Peak 32 years

Russia

0

5

10

15

20

25

30

35

1930 1950 1970 1990 2010 2030 2050

Discovery Gb

0

2000

4000

6000

8000

10000

12000

14000

Production kb/d

Peak to Peak 27 years

China

0

2

4

6

8

10

12

14

16

1930 1950 1970 1990 2010 2030 2050

Discovery Gb

0

0.2

0.4

0.6

0.8

1

1.2

1.4

Production kb/d

Peak to Peak 44 years

United Kingdom

0

1

2

3

4

5

1930 1950 1970 1990 2010 2030 2050

Discovery Gb

0

500

1000

1500

2000

2500

3000

Production kb/d

Peak to Peak 25 years

United Kingdom

Published by Dept. of Trade & Industry

Real Discovery Trend

Past discovery by ExxonMobil

0

10

20

30

40

50

60

1930 1950 1970 1990 2010 2030 2050

Gb

0

10

20

30

40

50

60

Past

Future

Production

Past after

ExxonMobil

“Draining the tanks”

145 Yet-to-Find

945 Produced1705 DISCOVERED

760 Remaining

?Filling at 5 p.a

Emptying at 25 p.a.

One in - Five out

Surprise

Billion barrels

Total would fill

Lake Geneva

Where is it?Regular Conventional Oil

-245

-191

-193

-110

-83

-47

-44

-27

380

146

30

71

65

22

23

14

-250 -150 -50 50 150 250 350 450

ME Gulf

Eurasia

N. America

L. America

Africa

W. Europe

East

ME.Other

Billion Barrels

Produced

Reserves

Yet-to-Find

All Oil & Gas

0

10

20

30

40

50

1930 1950 1970 1990 2010 2030 2050

Production, Gboe/a

Non-con Gas

Gas

NGLs

Polar Oil

Deep Water

Heavy

Regular

All boundaries fuzzy

The Illusion of new Technology

Oil industry uses very advanced technology– No major breakthrough in sight

Technology holds production higher for longer– increasing profit– accelerating depletion

• Does not add Reserves – save in special cases

Prudhoe Bay

0

100

200

300

400

500

600

700

0 1 2 3 4 6 7 8 8 9 10 10 12

Cum Prod. Gb

Ann. Prod. Gb

1977 Internal Estimate : 12.5-15 Gb

Reported : 9 Gb

Technology added nothing

1977

1989

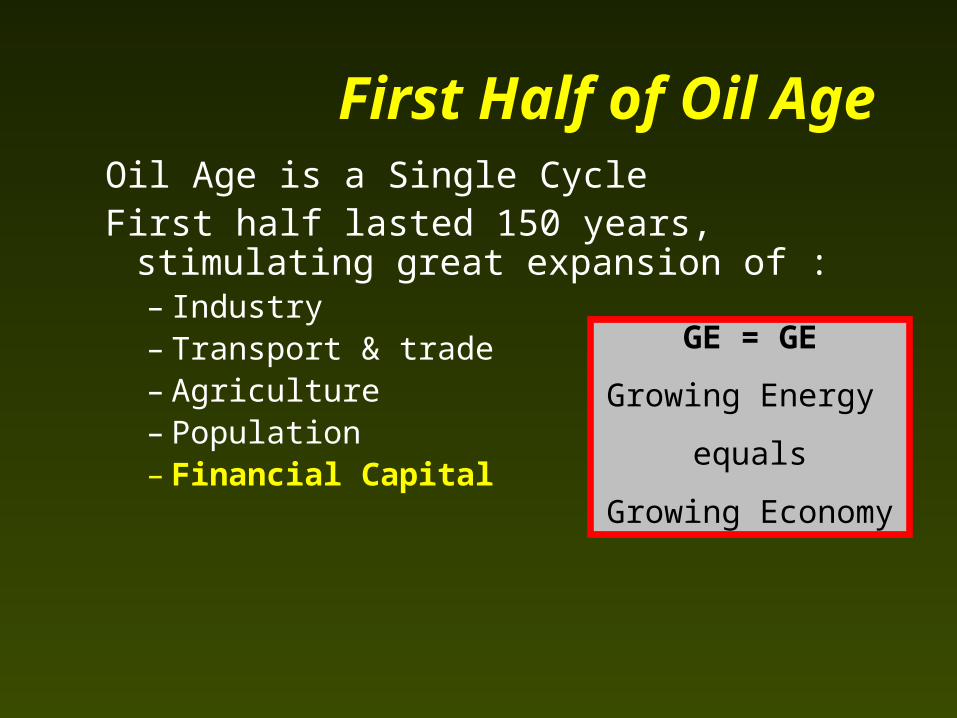

First Half of Oil AgeOil Age is a Single CycleFirst half lasted 150 years, stimulating great

expansion of :– Industry– Transport & trade– Agriculture– Population– Financial Capital

GE = GE

Growing Energy

equals

Growing Economy

Financial Capital

Banks created money out of thin air– by lending more than they had on deposit

• Collateral was confidence in expansion– fuelled by cheap oil-based energy

Prime benefit of Empire was financial rent

Previously British £ : now US $

Cause of wars

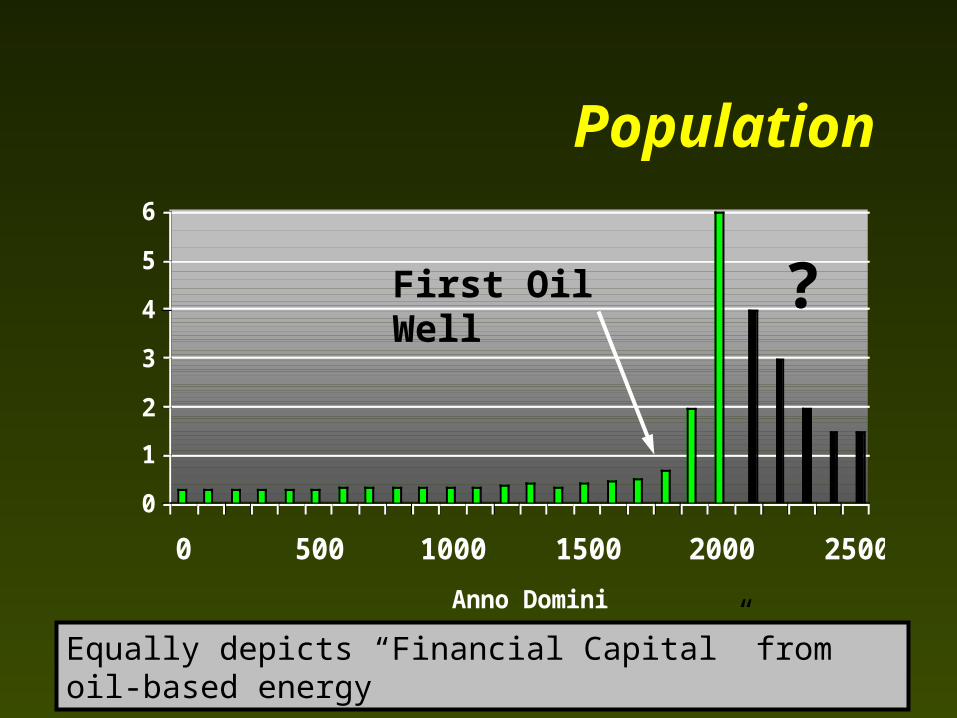

Population

0

1

2

3

4

5

6

0 500 1000 1500 2000 2500

Anno Domini

Billions of People

First Oil Well ?

Equally depicts “Financial Capital” from oil-based energy

Dawn of Second Half of Oil Age

World enters Uncharted Waters– Oil Price Shocks & Economic Recessions

Destruction of Capital to match energy supply

We face the “End of Economics”– Resource limits anathema to classical flat-

earth economists living in past– But new economic thinking emerges– The banks begin to understand

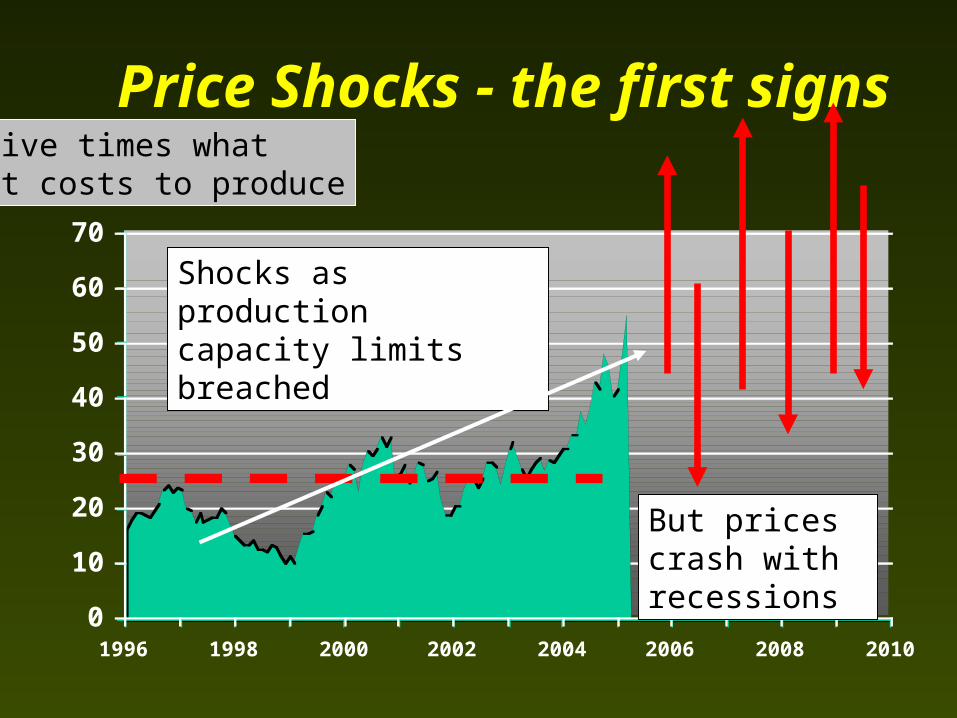

Price Shocks - the first signs

0

10

20

30

40

50

60

70

1996 1998 2000 2002 2004 2006 2008 2010

Brent Crude US $ But prices crash with recessions

Shocks as production capacity limits breached

Five times whatit costs to produce

The Second Great Depression

Past debt losing its collateral– heralding an unprecedented collapse of the

Financial System

• USA - technically bankrupt

CE = CE

Contracting Energy

equals

Contracting Economy

Survival Strategies. 1- InformStop giving false advice

– The IEA has been a political curtain behind which its member governments hid

– But is now forced to change its tune

Provide valid public information“Put your trust in the People” said Winston Churchill

2- Depletion ProtocolCut oil imports to match world Depletion Rate.

– World price would moderate• allowing poor countries to buy minimal needs

• avoiding profiteering by oil companies & M.East• Force consumers to face reality

Proposal gaining momentum : to be discussed– in Lisbon in May by senior politicians and – in Rimini in October by “World Leaders”

Let this be the prime message from this conference

3- Stop waste: many easy steps • Domestic & commercial Energy Audits

Variable charges to reward savings & penalise waste A new “energy currency” (Proposed by Prof. Slessor)

– Better insulation & industrial heat recovery – Heat pumps & modern light bulbs

Disallow energy costs as a charge against tax– Stop tax-free aviation fuel

More public transport : car pooling, hitch-hiking

New behaviour & attitude

4- Turn to Renewables

A solar collector on every roof

Capture massive tidal and wave energy

Wind-power and hydro-power

Fuel crops (supplies 30% in Brasil)

Geothermal

Re-assess nuclear energyNew small fail-safe plants

But………..

Economic Recession suppresses oil demand

Oil prices sensitive to small imbalances– may crash too

Unconventional Oil and Renewable Energy do not compete with cheap oil

An added argument for the Protocol to make sure they are competitive

Silver Linings

A new regionalism with local marketsNew attitudes : non-consumeristic societyPeople learn to live in better harmony with

• themselves• each other• the Environment in which Nature has

ordained them to live

But the transition will be tough

Thank You

and

Good Luck