Embed Size (px)

DESCRIPTION

The Role of Energy Efficiency in the Northwest. Tom Eckman Manager, Conservation Resources Northwest Power and Conservation Council Presented October 20, 2005 to Maine Public Utilities Commission. To Understand the Present, You Need to Know Our Past. - PowerPoint PPT Presentation

Citation preview

Northwest Power and ConservationCouncil

The Role of Energy EfficiencyThe Role of Energy Efficiencyin the Northwestin the Northwest

Tom EckmanTom Eckman

Manager, Conservation ResourcesManager, Conservation Resources

Northwest Power and Conservation CouncilNorthwest Power and Conservation CouncilPresented October 20, 2005Presented October 20, 2005

toto

Maine Public Utilities CommissionMaine Public Utilities Commission

slide 2

Northwest Power and ConservationCouncil

To Understand the To Understand the Present, You Need to Present, You Need to

Know Our PastKnow Our Past

slide 3

Northwest Power and ConservationCouncil

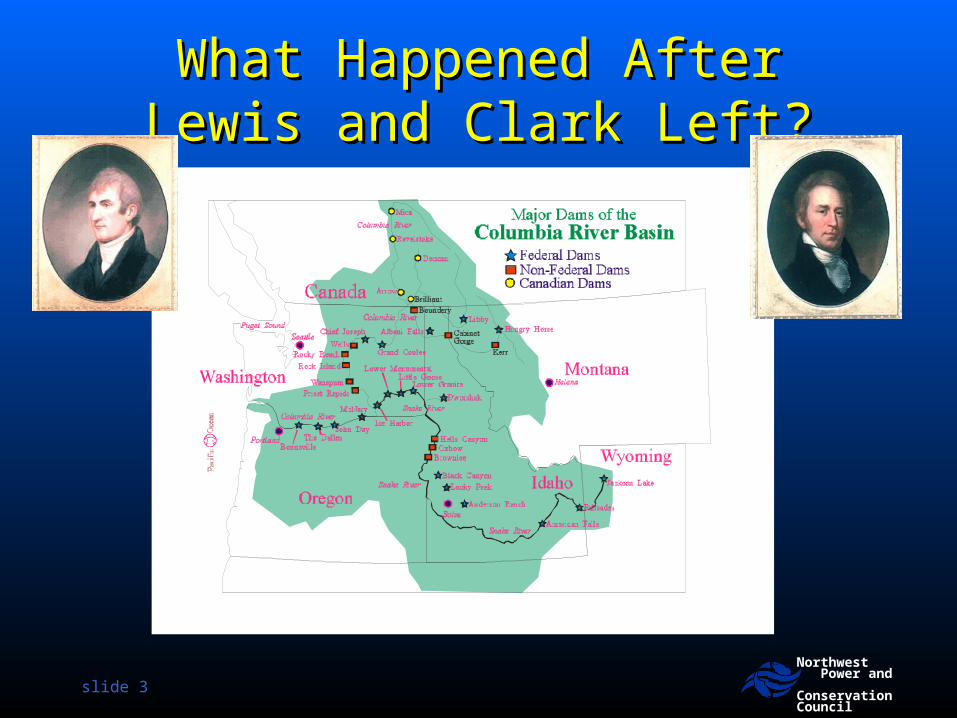

What Happened AfterWhat Happened AfterLewis and Clark Left?Lewis and Clark Left?

slide 4

Northwest Power and ConservationCouncil

The First Three “Eras” of Power The First Three “Eras” of Power Planning in the PNWPlanning in the PNW

““New Deal” Mysticism New Deal” Mysticism (1930-1950)(1930-1950)– Politicians plan using “chicken entrails and crystal Politicians plan using “chicken entrails and crystal

balls” balls” legislatelegislate what’s needed and when what’s needed and when

Engineering Determinism Engineering Determinism (1950- 1970)(1950- 1970)– Engineers, using graph paper and rulers Engineers, using graph paper and rulers scheduleschedule the the

next power plantsnext power plants

Economic Determinism Economic Determinism (1970 to April 27, (1970 to April 27, 1983)1983)– Economist, using price elasticity's Economist, using price elasticity's slowslow the engineer’s the engineer’s

construction schedules construction schedules

slide 5

Northwest Power and ConservationCouncil

Actions Taken in Response to “Engineering Actions Taken in Response to “Engineering and Economic Determinist’s” Forecastsand Economic Determinist’s” Forecasts

Utilities planned and/or started construction Utilities planned and/or started construction on 28 coal and nuclear power plants to be on 28 coal and nuclear power plants to be completed over a 20-year period.completed over a 20-year period.

Native American tribes sued the state and Native American tribes sued the state and federal government over loss of salmonfederal government over loss of salmon

Environmental groups sued Bonneville Environmental groups sued Bonneville Power Administration over plans to turn the Power Administration over plans to turn the Columbia River into “Wave World”Columbia River into “Wave World”

slide 6

Northwest Power and ConservationCouncil

Impact of Actions Taken in Response to Impact of Actions Taken in Response to “Engineering and Economic Determinist’s “Engineering and Economic Determinist’s

Forecasts and PlansForecasts and Plans

slide 7

Northwest Power and ConservationCouncil

Reaction to Impact of Actions Taken in Reaction to Impact of Actions Taken in Response to “Engineering and Economic Response to “Engineering and Economic

Determinist’s Forecasts and PlansDeterminist’s Forecasts and Plans

Terminate or mothball 9 Terminate or mothball 9 nuclear and 5 coal plants at nuclear and 5 coal plants at a cost to the region’s a cost to the region’s consumers of more than $7 consumers of more than $7 billion. billion.

Motivate the region’s Motivate the region’s politicians, utilities, larger politicians, utilities, larger industries and public interest industries and public interest groups to accept the “deals” groups to accept the “deals” embodied in the embodied in the Northwest Northwest Power and Conservation Power and Conservation Planning Act of 1980Planning Act of 1980

slide 8

Northwest Power and ConservationCouncil

The Fourth Era -The Fourth Era - Northwest Power and Conservation Northwest Power and Conservation

Planning Act of 1980 (PL96-501)Planning Act of 1980 (PL96-501) Authorized States of ID, OR, MT and WA to form an Authorized States of ID, OR, MT and WA to form an

“interstate compact” (aka, the “Council”)“interstate compact” (aka, the “Council”) Directed the Council to develop 20-year load forecast and Directed the Council to develop 20-year load forecast and

resource plan (“The Plan”) and update it every 5 - yearsresource plan (“The Plan”) and update it every 5 - years– To assure the region of an To assure the region of an adequate, efficient and reliable power adequate, efficient and reliable power

systemsystem– To provide for the development of the To provide for the development of the least costleast cost mix of resources mix of resources**– Conservation (energy efficiency) deemed highest priority resourceConservation (energy efficiency) deemed highest priority resource

equivalent to generation with a 10% cost advantage over power equivalent to generation with a 10% cost advantage over power generating resourcesgenerating resources

Mandated Mandated public involvementpublic involvement in Council’s planning process. in Council’s planning process.

*Federally mandated “least cost integrated resource planning” on *Federally mandated “least cost integrated resource planning” on regional basisregional basis

slide 9

Northwest Power and ConservationCouncil

Council Planning Process Council Planning Process and Plansand Plans

Longest Running “Integrated Resource Longest Running “Integrated Resource Planning Process” in the CountryPlanning Process” in the Country

Serves as “Regional Lens” through Serves as “Regional Lens” through which state Commissions view utility which state Commissions view utility IRPs (and other resource development)IRPs (and other resource development)– Regional resource adequacyRegional resource adequacy– Resource cost-effectivenessResource cost-effectiveness– Conservation/Efficiency goalsConservation/Efficiency goals

slide 10

Northwest Power and ConservationCouncil

How Has It Worked?How Has It Worked?

Fundamentally changed utility resource planningFundamentally changed utility resource planning– Council’s independent view of resource adequacy in Council’s independent view of resource adequacy in

first Plan led Bonneville and the region’s utilities first Plan led Bonneville and the region’s utilities terminate WNP 4&5, Skagit 1&2 and defer and terminate WNP 4&5, Skagit 1&2 and defer and ultimately cancel WNP 1&3, Creston 1&2, etc.ultimately cancel WNP 1&3, Creston 1&2, etc.

– Oregon and Washington Commissions adopted “least-Oregon and Washington Commissions adopted “least-cost” planning requirements for investor-owned cost” planning requirements for investor-owned utilities, Idaho and Montana have since followedutilities, Idaho and Montana have since followed

– First Council “Action Plan” Called on Bonneville and First Council “Action Plan” Called on Bonneville and the Region’s Utilities to Develop Conservation to the Region’s Utilities to Develop Conservation to Reduce Year 2002 Loads by Between 5 – 17%Reduce Year 2002 Loads by Between 5 – 17%

» Let’s See How This WorkedLet’s See How This Worked

How a PNW Kilowatt-Hour Gets SavedHow a PNW Kilowatt-Hour Gets Saved

Bonneville Power

Administration

PublicUtilities

InvestorOwnedUtilities

Northwest Powerand Conservation

Council

StateRegulatory

Commissions Northwest EnergyEfficiencyAlliance

SBC Admn.SBC Admn.Energy Trust of OregonEnergy Trust of Oregon

& NWEnergy (MT)& NWEnergy (MT)

RegionalTechnical

Forum

End Use ConsumersEnd Use Consumers

Markets, Markets, Codes & Codes & StandardsStandards

= = Policy Policy RecommendationsRecommendations

= Technical= TechnicalRecommendationsRecommendations

= Program= ProgramFundingFunding

= Conservation= ConservationProgramsPrograms

= Market TransformationPrograms/Projects

The “Plan”The “Plan”

= = Policy Policy

= Rate= Rate RevenuesRevenues

slide 12

Northwest Power and ConservationCouncil

PNW Energy Efficiency PNW Energy Efficiency AchievementsAchievements1978 - 20041978 - 2004

0

500

1,000

1,500

2,000

2,500

3,000

Avera

ge M

egaw

att

s

1978 1982 1986 1990 1994 1998 2002

BPA and Utility Programs Alliance ProgramsState Codes Federal Standards

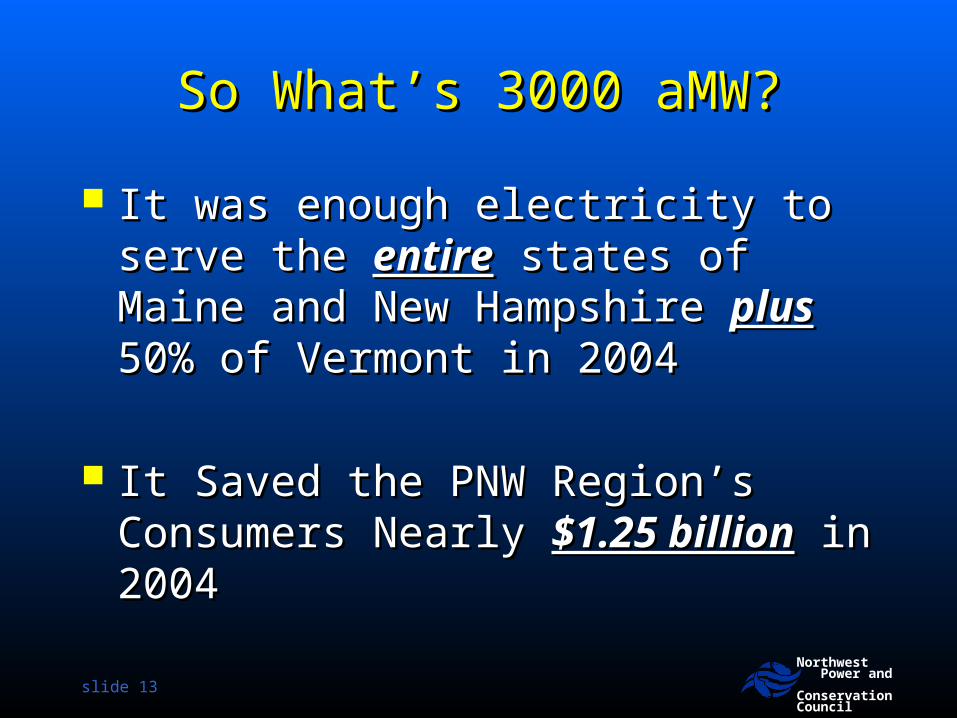

Since 1978 Utility & BPA Since 1978 Utility & BPA Programs, Energy Codes & Programs, Energy Codes & Federal Efficiency Standards Have Federal Efficiency Standards Have Produced Nearly 3000 aMW of Produced Nearly 3000 aMW of Savings.Savings.

slide 13

Northwest Power and ConservationCouncil

So What’s 3000 aMW?So What’s 3000 aMW?

It was enough electricity to serve the It was enough electricity to serve the entireentire states of Maine and New states of Maine and New Hampshire Hampshire plusplus 50% of Vermont in 50% of Vermont in 20042004

It Saved the PNW Region’s Consumers It Saved the PNW Region’s Consumers Nearly Nearly $1.25 billion$1.25 billion in 2004 in 2004

slide 14

Northwest Power and ConservationCouncil

Energy Efficiency Resources Energy Efficiency Resources Significantly Reduced Projected PNW Significantly Reduced Projected PNW

Electricity SalesElectricity Sales

14,000

16,000

18,000

20,000

22,000

24,000

1980 1985 1990 1995 2000

Avera

ge M

eg

aw

att

s

Medium High ForecastMedium LowMedium High Minus ConservationActual

slide 15

Northwest Power and ConservationCouncil

PNW Average Residential Electricity PNW Average Residential Electricity Use/Customer Use/Customer

11000

11500

12000

12500

13000

13500

14000

1990 1992 1994 1996 1998 2000 2002

Avera

ge

Annual U

se/C

ust

om

er

(kW

h)

slide 16

Northwest Power and ConservationCouncil

Energy Efficiency Met Nearly 40% of Energy Efficiency Met Nearly 40% of PNW Regional Firm Sales Growth PNW Regional Firm Sales Growth

Between 1980 - 2003Between 1980 - 2003

61%

39%

Generation Conservation

slide 17

Northwest Power and ConservationCouncil

Regional Utility Energy Efficiency Acquisitions Regional Utility Energy Efficiency Acquisitions Have Helped Balance Loads & ResourcesHave Helped Balance Loads & Resources

0

20

40

60

80

100

120

140

160

1978 1982 1986 1990 1994 1998 2002

Conse

rvati

on A

cquis

itio

ns

(aM

W)

Response to West Coast

Energy CrisisResponse to NW

Recession

Response to “Restructuring

Discussions”

Creating Mr. Toad’s Wild Ride for the PNW’s Energy Efficiency IndustryCreating Mr. Toad’s Wild Ride for the PNW’s Energy Efficiency Industry

slide 18

Northwest Power and ConservationCouncil

Utility Acquired Energy Efficiency Has Been Utility Acquired Energy Efficiency Has Been A BARGAIN!A BARGAIN!

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

May

-96

Nov-9

6

May

-97

Nov-9

7

May

-98

Nov-9

8

May

-99

Nov-9

9

May

-00

Nov-0

0

May

-01

Nov-0

1

May

-02

Nov-0

2

May

-03

Nov-0

3

May

-04

Nov-0

4

May

-05

Wh

ole

sale

Ele

ctri

city

Pri

ce (

20

00

$/M

WH

)

Levelized Cost of EfficiencyAcquisitionsWholesale Market Price

slide 19

Northwest Power and ConservationCouncil

So Much for the Past, So Much for the Past, What’s AheadWhat’s Ahead

55thth Plan Relies on Conservation and Renewable Plan Relies on Conservation and Renewable

Resources to of Meet Load GrowthResources to of Meet Load Growth**

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2004 2008 2012 2016 2020 2024

Year

Inst

alle

d C

apaci

ty (

MW

or

aM

W)

Conservation (aMW) Wind (MW) DR (MW)SCGTurbine (MW) CCGTurbine (MW) Coal (ICG) (MW)

**Actual future conditions (gas prices, CO2 control, conservation accomplishments) will Actual future conditions (gas prices, CO2 control, conservation accomplishments) will change resource development schedulechange resource development schedule

slide 21

Northwest Power and ConservationCouncil

Cost-Effective and Achievable Cost-Effective and Achievable Conservation Should Meet Over 45% of Conservation Should Meet Over 45% of

PNW Load Growth from 2005-2025*PNW Load Growth from 2005-2025*

0

5 0 0

1 0 0 0

1 5 0 0

2 0 0 0

2 5 0 0

3 0 0 0

C o s t - E ff e c t iv e P o t e n t ia l( a M W in 2 0 2 5 )

A g r i c u l t u r a l S e c t o r - 8 0 a M W

N o n - D S I I n d u s t r i a l S e c t o r - 3 5 0 a M W

C o m m e r c i a l S e c t o r N o n - B u i l d i n g M e a s u r e s - 4 2 0 a M W

H V A C , E n v e l o p e & R e f r i g e r a t i o n - 3 7 5 a M W

N e w C o m m e r c i a l B u i l d i n g L i g h t i n g - 2 2 0 a M W

E x i s t i n g C o m m e r c i a l B u i l d i n g s L i g h t i n g - 1 3 0 a M W

R e s i d e n t i a l S p a c e C o n d i t i o n i n g - 2 4 0 a M W

R e s i d e n t i a l L i g h t i n g - 5 3 0 a M W

R e s i d e n t i a l W a t e r H e a t i n g - 3 2 5 a M W

R e s i d e n t i a l A p p l i a n c e s - 1 4 0 a M W

*Medium Load Forecast *Medium Load Forecast Loads & Market PricesLoads & Market Prices

slide 22

Northwest Power and ConservationCouncil

Regional Near-Term Conservation Regional Near-Term Conservation Targets (2005-2009) = 700 aMWTargets (2005-2009) = 700 aMW

0

20

40

60

80

100

120

140

160

2005 2006 2007 2008 2009

Reso

urc

e (

aM

W)

Residential - Lost Opportunity

Commercial - Lost Opportunity

I rrigated Agriculture - Non LostOpportunity

Industrial - Non Lost Opportunity

Residential - Non Lost Opportunity

Commercial - Non Lost Opportunity

Northwest Power and ConservationCouncil

Why Should We?Why Should We?

What’s Behind the 5What’s Behind the 5thth Plan’s Plan’s Conservation Targets?Conservation Targets?

PNW Portfolio Planning – Scenario Analysis on SteroidsPNW Portfolio Planning – Scenario Analysis on Steroids

0%

2%

4%

6%

8%

10%

12%

14%

16%

0.0% 1.0% 2.0% 3.0% 4.0% 5.0%

Annual Load Growth

Pro

bab

ilit

y (

%)

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0% 1% 2% 3% 4% 5%

Real Natural Gas Escalation Rate% )

Pro

bab

ilit

y (

%)

0%

5%

10%

15%

20%

25%

30%

3.27% 3.80% 3.85% 3.93% 2.50%

Nominal Annual Electricity Price Escalation Rate

Pro

babilit

y (

%)

0

20

40

60

80

100

120

98

467

705

842

1,06

9

1,19

1

1,28

3

1,33

5

1,35

3

1,37

3

1,65

0

Resource Potential

Levelized C

ost

0%2%4%6%8%

10%12%14%16%18%20%

Carbon Tax Implementation Date

Pro

bab

ilty

(%

)

0

5000

10000

15000

20000

25000

1925 1930 1935 1940 1945 1950 1955 1960 1965 1970 1975

Hydrosytem Year

Cap

acit

y (

MW

)

0%2%4%6%8%

10%12%14%16%18%20%

Pro

bab

ilit

y

$0 $6 $12 $18 $24 $30 $36

Carbon Tax

Frequency Chart

Dollars

Mean = $689.000

.011

.022

.032

.043

0

10.75

21.5

32.25

43

($3,509) ($1,131) $1,247 $3,625 $6,003

1,000 Trials 1,000 Displayed

Portfolio Portfolio Analysis Analysis ModelModel

$35,500

$36,000

$36,500

$37,000

$37,500

$23,500 $24,000 $24,500 $25,000

NPV System Risk (2004$Millions)

NP

V S

yste

m C

ost

(20

04

$M

illio

ns)

Efficient FrontierEfficient Frontier

NPV System Cost

slide 25

Northwest Power and ConservationCouncil

Plans Along the Efficient Frontier Permit Plans Along the Efficient Frontier Permit Trade-Offs of Costs Against RiskTrade-Offs of Costs Against Risk

$35,500

$36,000

$36,500

$37,000

$37,500

$23,600 $23,800 $24,000 $24,200 $24,400 $24,600

NPV System Cost (Millions)

NPV

Syst

em

Ris

k (

Mill

ions)

Least Risk

Least Cost

slide 26

Northwest Power and ConservationCouncil

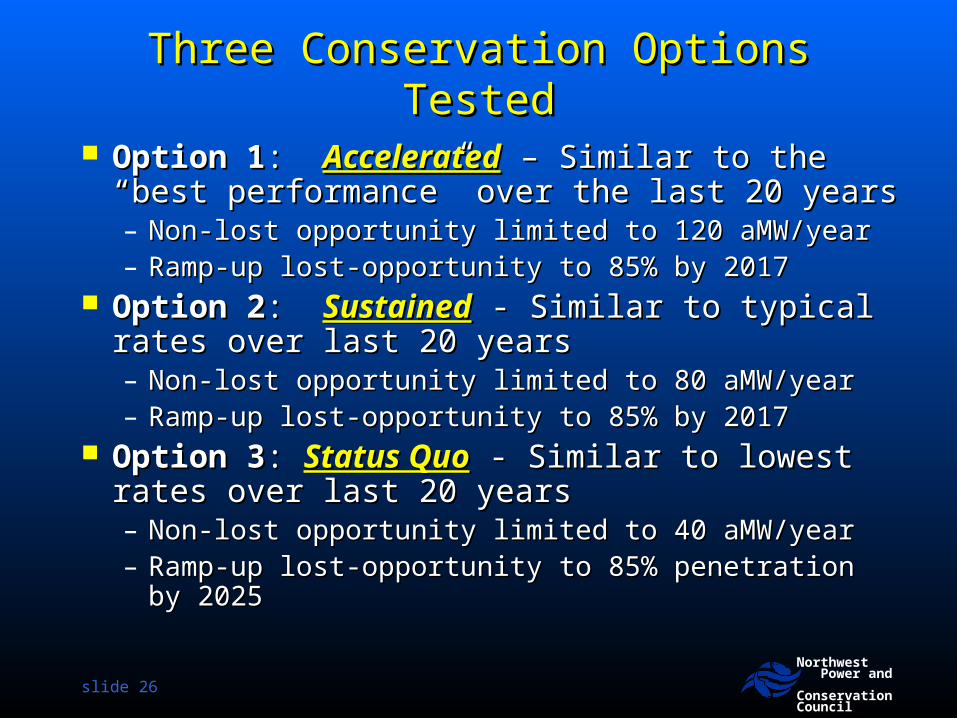

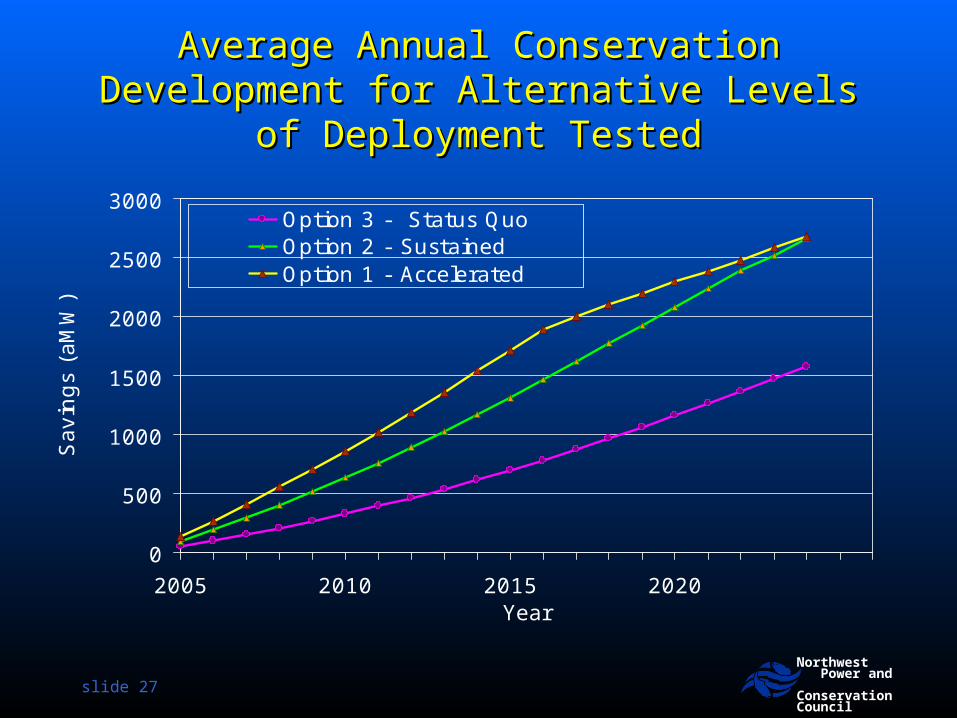

Three Conservation Options TestedThree Conservation Options Tested

Option 1Option 1: : AcceleratedAccelerated – Similar to the “best – Similar to the “best performance” over the last 20 yearsperformance” over the last 20 years– Non-lost opportunity limited to 120 aMW/yearNon-lost opportunity limited to 120 aMW/year– Ramp-up lost-opportunity to 85% by 2017Ramp-up lost-opportunity to 85% by 2017

Option 2Option 2: : SustainedSustained - Similar to typical rates over - Similar to typical rates over last 20 yearslast 20 years– Non-lost opportunity limited to 80 aMW/yearNon-lost opportunity limited to 80 aMW/year– Ramp-up lost-opportunity to 85% by 2017Ramp-up lost-opportunity to 85% by 2017

Option 3Option 3: : Status QuoStatus Quo - Similar to lowest rates over - Similar to lowest rates over last 20 yearslast 20 years– Non-lost opportunity limited to 40 aMW/yearNon-lost opportunity limited to 40 aMW/year– Ramp-up lost-opportunity to 85% penetration by 2025Ramp-up lost-opportunity to 85% penetration by 2025

slide 27

Northwest Power and ConservationCouncil

Average Annual Conservation Average Annual Conservation Development for Alternative Levels of Development for Alternative Levels of

Deployment TestedDeployment Tested

0

500

1000

1500

2000

2500

3000

2005 2010 2015 2020Year

Savin

gs

(aM

W)

Option 3 - Status QuoOption 2 - SustainedOption 1 - Accelerated

slide 28

Northwest Power and ConservationCouncil

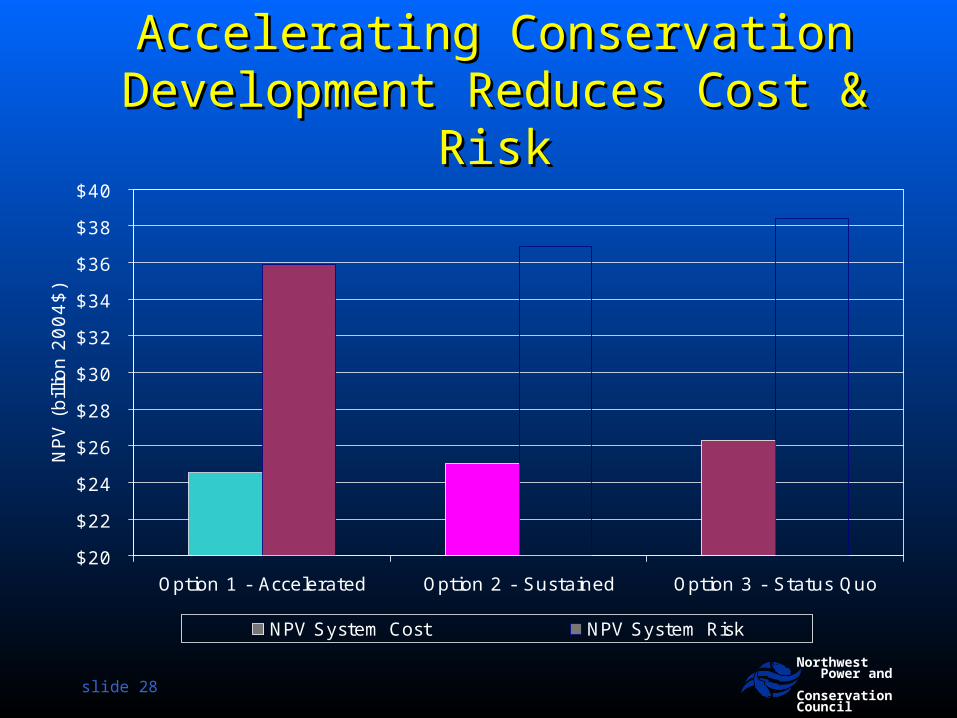

Accelerating Conservation Accelerating Conservation Development Reduces Cost & Development Reduces Cost &

RiskRisk

$20

$22

$24

$26

$28

$30

$32

$34

$36

$38

$40

Option 1 - Accelerated Option 2 - Sustained Option 3 - Status Quo

NPV

(bill

ion

20

04

$)

NPV System Cost NPV System Risk

slide 29

Northwest Power and ConservationCouncil

WECC Carbon Dioxide Emissions WECC Carbon Dioxide Emissions Reductions for Alternative Reductions for Alternative

Conservation TargetsConservation Targets

0

10

20

30

40

50

60

70

80

Mill

ion T

ons

over

20 y

ears

Option 1 - Accelerated Option 2 - Sustained Option 3 - Status Quo

slide 30

Northwest Power and ConservationCouncil

Why Energy Efficiency Reduces Why Energy Efficiency Reduces System Cost and RiskSystem Cost and Risk

It’s A Cheap (avg. 2.4 cents/kWh TOTAL It’s A Cheap (avg. 2.4 cents/kWh TOTAL RESOURCE COST) Hedge Against Market RESOURCE COST) Hedge Against Market Price SpikesPrice Spikes

It has value even when market prices are It has value even when market prices are low low

It’s Not Subject to Fuel Price RiskIt’s Not Subject to Fuel Price Risk It’s Not Subject to Carbon Control RiskIt’s Not Subject to Carbon Control Risk It’s Significant Enough In Size to Delay It’s Significant Enough In Size to Delay

“build decisions” on generation“build decisions” on generation

slide 31

Northwest Power and ConservationCouncil

The Plan’s Targets Are A The Plan’s Targets Are A Floor, Not a CeilingFloor, Not a Ceiling

When we took the “ramp rate” constraints off the portfolio model it developed

1500 aMW1500 aMW

of Energy Efficiency in 2005

slide 32

Northwest Power and ConservationCouncil

Where Are We Getting Where Are We Getting The Savings?The Savings?

slide 33

Northwest Power and ConservationCouncil

Sources of Savings by SectorSources of Savings by Sector

Industrial 350 aMW

12%

Irrigation 80 aMW3%

Commercial 1105 aMW

39%

Residential 1340 aMW

46%

Major Sources of Efficiency ResourceMajor Sources of Efficiency Resource

1.7 1.7

1.2

4.3

1.5

3

5.2

3.4

1.8

3.4

2.2

0

100

200

300

400

500

600

700

Res. C

FLs

Indu

stria

l

New C

om. L

ight

ing

HP W

ater

Hea

ters

AC/DC C

onve

rter

s

New C

om. H

VAC

Res. C

loth

es W

ashe

rs

Exist

. Com

. HVAC

Exist

. Com

. Light

ing

Exist

. Com

. Equ

ipm

ent

Exist

.Com

. Inf

rastru

ctur

e

Ach

ieve

able

Pote

nti

al (

MW

a)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Ave

rage

Leve

lized

Cost

(C

ents

/kW

h)

slide 35

Northwest Power and ConservationCouncil

Implementation Implementation ChallengesChallenges

slide 36

Northwest Power and ConservationCouncil

Plan Plan Conservation Action ItemsConservation Action Items

Ramp up “Lost Opportunity” conservationRamp up “Lost Opportunity” conservation» Goal => 85% penetration in 12 years Goal => 85% penetration in 12 years » 10 to 30 MWa/year 2005 through 200910 to 30 MWa/year 2005 through 2009

Accelerate the acquisition of “Non-Lost Accelerate the acquisition of “Non-Lost Opportunity” resourcesOpportunity” resources

» Return to acquisition levels of early 1990’sReturn to acquisition levels of early 1990’s» Target 120 MWa/year next five yearsTarget 120 MWa/year next five years

Employ a mix of mechanismsEmploy a mix of mechanisms» Local acquisition programs (utility, SBC Administrator & Local acquisition programs (utility, SBC Administrator &

BPA programs)BPA programs)» Regional acquisition programs and coordinationRegional acquisition programs and coordination» Market transformation venturesMarket transformation ventures

slide 37

Northwest Power and ConservationCouncil

The Total Resource Acquisition Cost* of The Total Resource Acquisition Cost* of 55thth Plan’s Conservation Targets Plan’s Conservation Targets

2005 – 2009 = $1.64 billion2005 – 2009 = $1.64 billion

$0

$50

$100

$150

$200

$250

$300

$350

$400

2005

2006

2007

2008

2009

Tota

l R

eso

urc

e C

ost

s(M

illio

ns

20

00

$)

Residential - Lost Opportunity

Commercial - Lost Opportunity

I rrigated Agriculture - Non LostOpportunity

Industrial - Non Lost Opportunity

Residential - Non Lost Opportunity

Commercial - Non Lost Opportunity

*Incremental capital costs to install measure plus program administration costs estimated at 20% of capital.

slide 38

Northwest Power and ConservationCouncil

PNW Utilities Now Invests Less Than 2% of PNW Utilities Now Invests Less Than 2% of Their Retail Sales Revenues in Energy Their Retail Sales Revenues in Energy

EfficiencyEfficiency

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Con

serv

ati

on

In

vest

men

ts (

mill

ion

20

00

$)

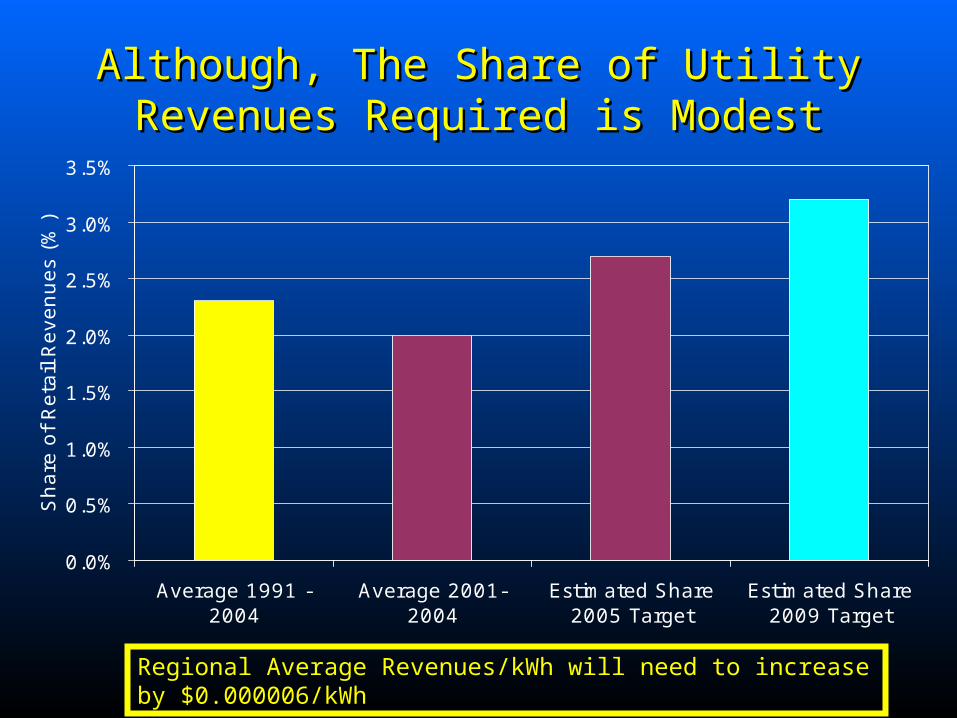

Meeting the Plan’s Efficiency Targets Will Meeting the Plan’s Efficiency Targets Will Likely Require Increased Regional InvestmentsLikely Require Increased Regional Investments

$0

$50

$100

$150

$200

$250

$300

$350

Average 1991-2004

Average 2001-2004

Estimated UtilityCost of 2005

Target

Estimated UtilityCost of 2009

Target

Uti

lity I

nvest

men

ts (

mill

ion

20

00

$)

Although, The Share of Utility Although, The Share of Utility Revenues Required is ModestRevenues Required is Modest

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

Average 1991 -2004

Average 2001-2004

Estimated Share2005 Target

Estimated Share2009 Target

Sh

are

of

Reta

il R

even

ues

(%)

Regional Average Revenues/kWh will need to increase by $0.000006/kWh

slide 41

Northwest Power and ConservationCouncil

SummarySummary The 5th Plan’s Goal IsThe 5th Plan’s Goal Is To Make The To Make The

InefficientInefficient Use of Electricity . . . Use of Electricity . . .– ImmoralImmoral– IllegalIllegal– UnprofitableUnprofitable

If We Fail Both If We Fail Both CostsCosts and and Risk Risk Will Be HigherWill Be Higher

slide 42

Northwest Power and ConservationCouncil

Backup SlidesBackup Slides

slide 43

Northwest Power and ConservationCouncil

Cumulative 1978 - 2004 Efficiency Cumulative 1978 - 2004 Efficiency Achievements by SourceAchievements by Source

Alliance Programs185 aMW

6%

State Codes560 aMW

19%

Federal Standards545 aMW

19%

BPA and Utility Programs1635 aMW

56%

slide 44

Northwest Power and ConservationCouncil

Total PNW Annual Energy Efficiency Total PNW Annual Energy Efficiency Achievements Have Been Growing, Largely Due Achievements Have Been Growing, Largely Due To The Impact of Energy Codes and StandardsTo The Impact of Energy Codes and Standards

0

50

100

150

200

250

300

1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004

Con

serv

ati

on

Acq

uis

itio

ns

(aM

W)

Federal Standards

State Codes

Alliance Programs

BPA,Utility and SBC Administrator Programs

slide 45

Northwest Power and ConservationCouncil

Maine’s Electric Sales Maine’s Electric Sales 1,360 aMW in 2004 1,360 aMW in 2004

Industrial400 aMW

42%

Commercial470 aMW

30%

Residential490 aMW

28%

Source: US DOE/EIA

slide 46

Northwest Power and ConservationCouncil

Maine Residential Electricity Use per Maine Residential Electricity Use per Customer Declined in the 1990sCustomer Declined in the 1990s

… But Recently It’s Been Increasing… But Recently It’s Been Increasing

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1990 1992 1994 1996 1998 2000 2002

Avera

ge

Annual U

se/C

ust

om

er

(kW

h)

slide 47

Northwest Power and ConservationCouncil

slide 48

Northwest Power and ConservationCouncil

Efficiency Maine Projected Efficiency Maine Projected InvestmentsInvestments

slide 49

Northwest Power and ConservationCouncil

The Share of PNW Retail Electricity Sales The Share of PNW Retail Electricity Sales Revenues Invested In Energy Efficiency Has Revenues Invested In Energy Efficiency Has

Declined Since The Early 1990’sDeclined Since The Early 1990’s

$0.0$1.0$2.0$3.0$4.0$5.0$6.0$7.0$8.0$9.0

$10.0

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

Tota

l R

eta

il Ele

ctri

city

Sale

s R

evenue

(bill

ion 2

000$)

Revenues Invested In EfficiencyRevenues Dedicated to Other Costs

slide 50

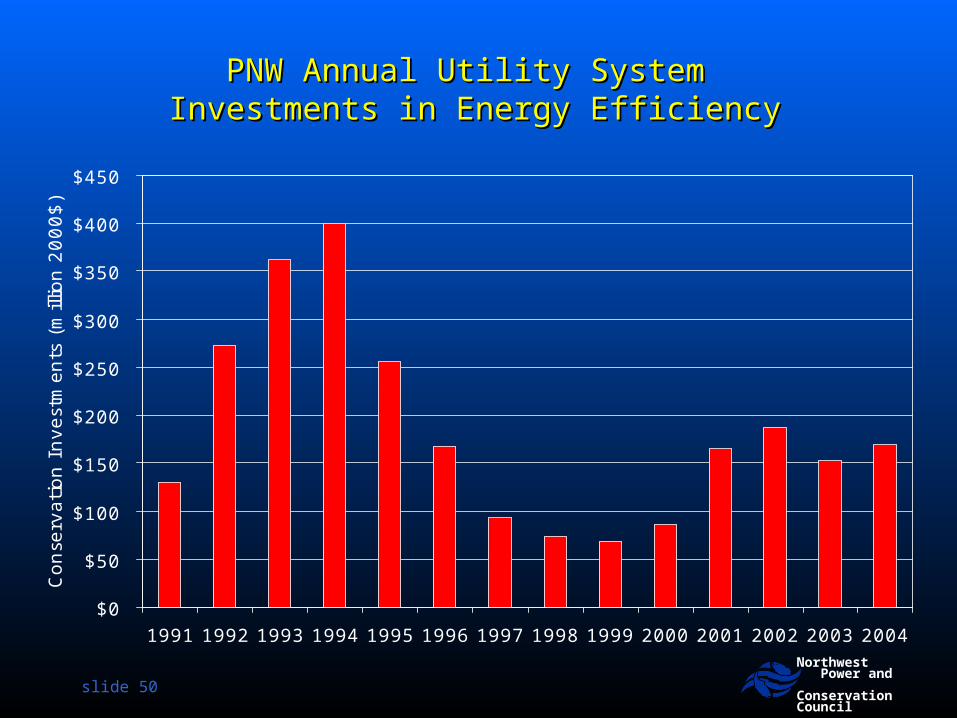

Northwest Power and ConservationCouncil

PNW Annual Utility System PNW Annual Utility System Investments in Energy EfficiencyInvestments in Energy Efficiency

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Con

serv

ati

on

In

vest

men

ts (

mill

ion

20

00

$)

slide 51

Northwest Power and ConservationCouncil

The “First Year” Cost ($/aMW) of Utility Acquired The “First Year” Cost ($/aMW) of Utility Acquired Energy Efficiency Has DeclinedEnergy Efficiency Has Declined

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Con

serv

ati

on

Cost

/aM

W (

mill

ion

20

00

$)

slide 52

Northwest Power and ConservationCouncil

PNW Utilities Have Gotten More Efficient at Acquiring PNW Utilities Have Gotten More Efficient at Acquiring Energy Efficiency - Cost Are Now Below $15 MWHEnergy Efficiency - Cost Are Now Below $15 MWH

$0

$5

$10

$15

$20

$25

$30

$35

$40

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Leveliz

ed C

on

serv

ati

on

Cost

(m

illio

n/M

Wh

20

00

$)

slide 53

Northwest Power and ConservationCouncil

Utility Acquired Energy Efficiency Has Been Cost-Utility Acquired Energy Efficiency Has Been Cost-Competitive with Market PurchasesCompetitive with Market Purchases

$0

$100

$200

$300

$400

$500

$600

May

-96

Nov-9

6

May

-97

Nov-9

7

May

-98

Nov-9

8

May

-99

Nov-9

9

May

-00

Nov-0

0

May

-01

Nov-0

1

May

-02

Nov-0

2

May

-03

Nov-0

3

May

-04

Nov-0

4

May

-05

Wh

ole

sale

Ele

ctri

city

Pri

ce (

20

00

$/M

WH

)

Wholesale Market Price

Levelized Cost of EfficiencyAcquisitions

Comparing Plans for System Comparing Plans for System Cost and RiskCost and Risk

NPV Power System Cost (billions)

Like

lihood

(Pro

bab

ility

)

12.5 15 17.5 20 22.5 25 27.5 30 32.5 35

Risk = Mean NPV of 90th Percentile

10

System Cost = Mean NPV across all futures

slide 55

Northwest Power and ConservationCouncil

Space of feasible Space of feasible solutionssolutions

Efficient Frontier = Least Cost Efficient Frontier = Least Cost Plans for Given Level of RiskPlans for Given Level of Risk

Incre

asin

g R

isk

Incre

asin

g R

isk

Increasing CostIncreasing Cost

Alternative Alternative Risk LevelsRisk Levels

Efficient Frontier

slide 56

Northwest Power and ConservationCouncil

Insights from 5Insights from 5thth Plan Portfolio Analysis – Plan Portfolio Analysis – Diverse Portfolios Decrease Risk, but Diverse Portfolios Decrease Risk, but

Increase CostIncrease Cost

Space of feasible Space of feasible solutionssolutions

Efficient Efficient FrontierFrontier

Increasing CostIncreasing CostIn

cre

asin

g R

isk

Incre

asin

g R

isk

Rely on the marketRely on the market

CCCT & SCCTCCCT & SCCT

Mix of Conservation, Mix of Conservation, Renewables, coal and Renewables, coal and SCCTSCCT

slide 57

Northwest Power and ConservationCouncil

Residential Sector Target = 1340 aMWResidential Sector Target = 1340 aMW

0

200

400

600

800

1,000

1,200

1,400

Avera

ge M

egaw

att

s

Residential Space Conditioning - 245aMW

Residential Lighting - 630 aMW

Residential Water Heating - 285 aMW

Residential Appliances - 140 aMW

slide 58

Northwest Power and ConservationCouncil

Regional Residential Sector Realistically Regional Residential Sector Realistically Achievable Potential for AppliancesAchievable Potential for Appliances

Clothes Washers - 135

aMW75%

Dishwashers - 10 aMW

6%

Refrigerators - 35 aMW

19%

slide 59

Northwest Power and ConservationCouncil

Regional Residential Sector Realistically Regional Residential Sector Realistically Achievable Potential for Water HeatingAchievable Potential for Water Heating

Efficient Tanks29%

95 aMWWaste Water

Heat Recovery4%

15 aMW

Heat Pump Water Heaters

67%225 aMW

slide 60

Northwest Power and ConservationCouncil

Regional Residential Sector Realistically Regional Residential Sector Realistically Achievable Potential for Space Achievable Potential for Space

ConditioningConditioningNew Construction -

Shell Measures 40 aMW

16%

Duct Sealing & System

Commissioning & Controls 15 aMW

6%

Weatherization60 aMW

24%

Heat Pump Upgrades 55 aMW

22%

Heat Pump Conversions

75 aMW32%

slide 61

Northwest Power and ConservationCouncil

Commercial Sector Target = 1105 aMWCommercial Sector Target = 1105 aMW

0

200

400

600

800

1,000

1,200

Avera

ge M

egaw

att

s

Infrastructure

Equipment

Envelope

Lighting

HVAC

slide 62

Northwest Power and ConservationCouncil

Regional Non-Building Resource Regional Non-Building Resource Potential = 430 aMWPotential = 430 aMW

0

20

40

60

80

100

120

140

160S

ew

age

Tre

atm

em

t

Wate

rTre

atm

ent

LED

Tra

ffic

Sig

nals

Netw

ork

ed

PC

Managem

ent

Pack

aged

Refr

igera

tion

Pow

er

Supplie

s

LED

Exit

Sig

ns

Avera

ge M

egaw

att

s

slide 63

Northwest Power and ConservationCouncil

0

100

200

300

400

500

600

New and Replacement Retrofit

MW

a in

202

5

Equipment

Refrigeration

Envelope

Lighting

HVAC

Cost-Effective Commercial Conservation Potential Cost-Effective Commercial Conservation Potential in 2025 For Building Lighting, HVAC & Equipment- in 2025 For Building Lighting, HVAC & Equipment-

Regional = 950 aMWRegional = 950 aMW

slide 64

Northwest Power and ConservationCouncil

Irrigated Agriculture Sector Target = Irrigated Agriculture Sector Target = 80 aMW80 aMW

0

10

20

30

40

50

60

70

80

90

Avera

ge M

egaw

att

s

Replace Pumps, Nozzles &Gaskets

Replace Nozzles & Gaskets

Convert Center Pivots fromMedium to Low Pressure

Convert Center Pivots from Highto Low Pressure

slide 65

Northwest Power and ConservationCouncil

Industrial Sector Target = Industrial Sector Target = 350 aMW350 aMW

Estimate of 5% of 2025 forecast loadsEstimate of 5% of 2025 forecast loads 350 aMW at 1.7 cents per kWh350 aMW at 1.7 cents per kWh Process controls, drive systems, lighting, Process controls, drive systems, lighting,

refrigeration, compressed air, etcrefrigeration, compressed air, etc Potential is a function of the ongoing Potential is a function of the ongoing

changes in region’s industrial mixchanges in region’s industrial mix

slide 66

Northwest Power and ConservationCouncil

Utility* Efficiency Acquisition Plans for 2005 Are Utility* Efficiency Acquisition Plans for 2005 Are Close to 5Close to 5thth Plan Targets Plan Targets

0

20

40

60

80

100

120

2005 5th Plan Target 2005 Utility Acquistion Plan

Conserv

ati

on L

evels

(M

Wa)

*Targets for 15 Largest PNW Utilities. These utilities represent approximately 80% of regional load.

slide 67

Northwest Power and ConservationCouncil

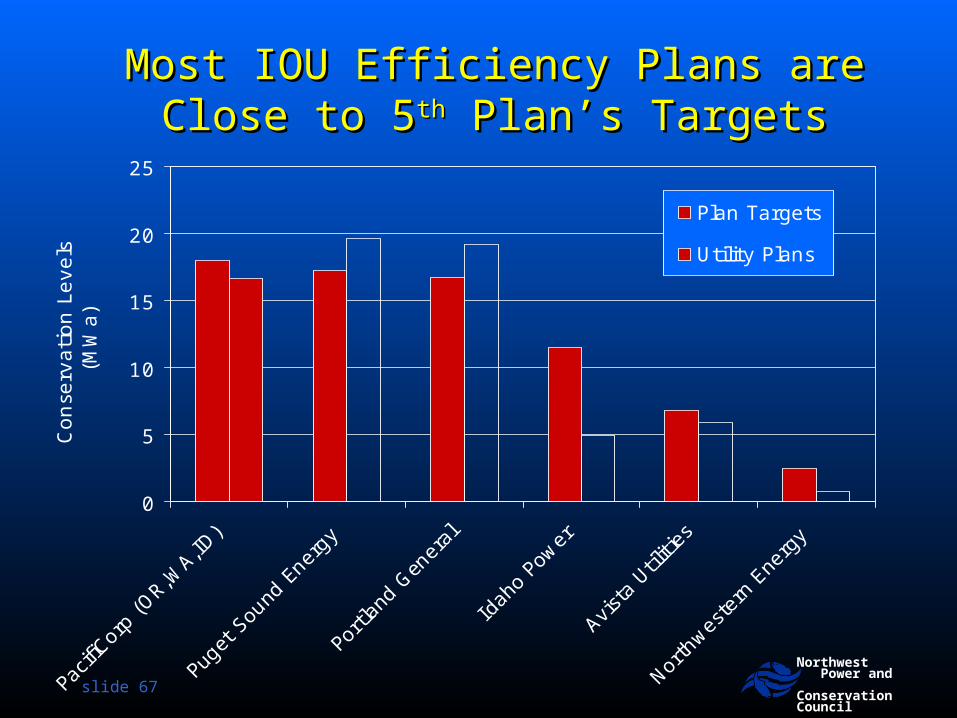

Most IOU Efficiency Plans are Close Most IOU Efficiency Plans are Close to 5to 5thth Plan’s Targets Plan’s Targets

0

5

10

15

20

25

Pacifi

Corp

(OR,W

A,ID)

Puge

t Sou

nd E

nerg

y

Portland

Gen

eral

Idah

o Po

wer

Avist

a Util

ities

North

weste

rn E

nerg

y

Con

serv

ati

on

Levels

(M

Wa)

Plan Targets

Utility Plans

slide 68

Northwest Power and ConservationCouncil

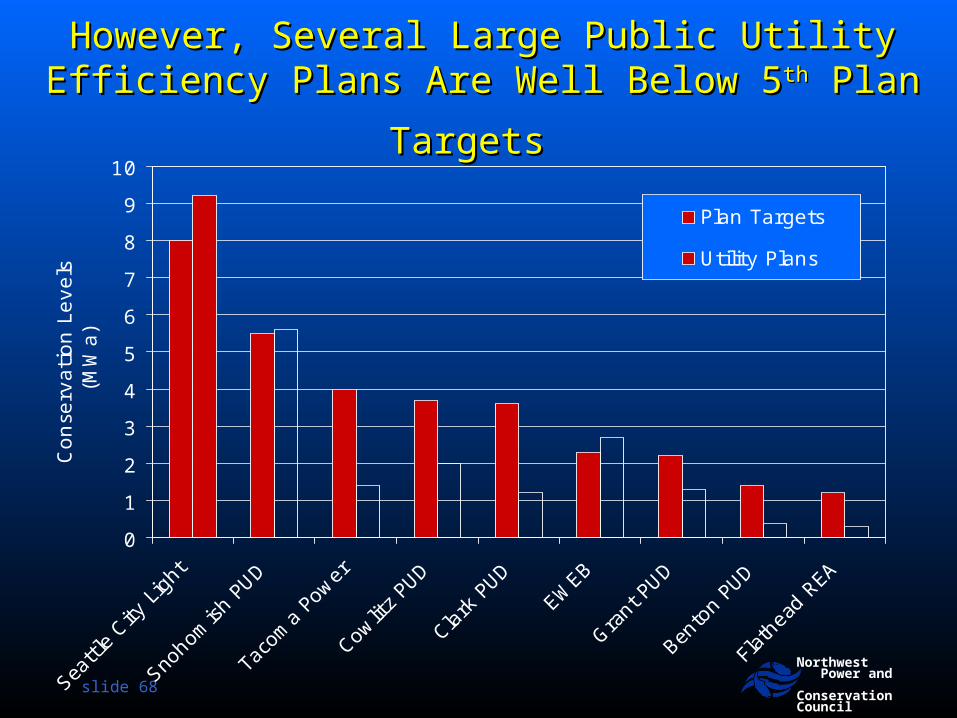

However, Several Large Public Utility Efficiency However, Several Large Public Utility Efficiency

Plans Are Well Below 5Plans Are Well Below 5thth Plan Targets Plan Targets

0

1

2

3

4

5

6

7

8

9

10

Seattl

e City

Lig

ht

Snoho

mish

PUD

Taco

ma

Power

Cowlit

z PU

D

Clark

PUD

EWEB

Grant

PUD

Bento

n PU

D

Flat

head

REA

Con

serv

ati

on

Levels

(M

Wa)

Plan Targets

Utility Plans