Embed Size (px)

Citation preview

The Road to DecarbonisationImplications for Major Energy ProjectsOctober 2018

3The Road to Decarbonisation: Implications for Major Energy Projects

Since the Climate Change Act 2008 the UK has apparently made good progress in reducing its CO2 emissions. However, the government’s official advisor, the Committee on Climate Change (CCC), has warned that the UK is on a path to fail to meet its legislated carbon reduction goals. The CCC states that the policies set out in the government’s Clean Growth Strategy are insufficient to drive down CO2 emissions and are at risk of under-performance.

The past year has seen a plethora of reports and recommendations on decarbonisation from authoritative bodies and advisory committees. Some of these reports offer conflicting advice on various technical issues. The belief in using market forces to drive the most cost-effective route to decarbonisation is challenging to deliver as energy is a capital-intensive industry and investors’ capacity, risk appetite and time horizons may not support the optimal long-term path. The biggest determinant of what gets built is government policy and intervention, whether through subsidy (as has been the case in renewable power generation), or through regulation as has been the case in closure of coal fired power stations.

We have written this short review to highlight what we believe are critical decisions that government must take in the near term and to emphasize that these near-term decisions must be made with a very long-term strategic view. Focus on least cost solutions in the short to medium term risks creating stranded assets if the ultimate system configuration is not understood.

The energy system is extremely complex and fluid. Decisions in one sector have a knock-on effect in others. The pursuit of the near term ‘least cost’ pathway may not achieve the desired long-term result, or it may prove to be more costly in long term.

We believe that ultimately the energy system must be completely fossil fuel-free. Renewables will provide a significant proportion of primary energy, but deep decarbonisation will also require a substantial proportion of nuclear power (fission and fusion). Our view is corroborated by a recent study published by MIT (references in Annex 1) which has concluded that, as a dispatchable low-carbon technology, nuclear should be a part of the least cost solution to deep decarbonisation.

The main energy consuming sectors of the economy are: Heating (in homes, offices and commercial buildings), Transportation, Electricity Generation and Industry. Much can be achieved through modifying consumer behaviour and through energy conservation. Insulating homes, changing travel patterns, installing energy efficient lights and domestic equipment all have their place, but decarbonisation will also need large capital projects: new power generation (renewable and nuclear), changes to the national grid, hydrogen manufacture, energy storage (ES), carbon capture utilisation and storage (CCUS) all involve significant investment.

Key questions (requiring policy decisions) effecting these major projects include:

Heating: Can natural gas use be replaced with hydrogen? Can existing gas distribution networks be used with hydrogen? How much hydrogen will we need? How will we make that hydrogen, how will we store it and deliver it to the distribution network? How much of the heating load will be electric? What peak electric demand will there be?

Transport: How fast will electric vehicle (EV) deployment happen? How will this impact peak electricity demand? How quickly will EV charging networks develop? What will the impact on grid and distribution systems be? How soon will a smart energy grid allow vehicle batteries to supplement peak electricity supply?

Executive Summary

The UK has set out to be a global leader in the radical transformation of the world’s energy systems to limit the climate change impact of human activities. The major challenge will be to first limit and then eliminate all carbon dioxide (CO2) emissions. The Intergovernmental Panel on Climate Change (IPCC) published their special report, “Global Warming of 1.5°C”, as this document went to print. The implications of a policy change to limit the predicted global temperature rise to 1.5°C, down from 2°C, have not been considered here. They would include dramatic acceleration of the CO2 emissions reduction pathways that we have referenced, and substantial atmospheric CO2 removal through large scale bioenergy programmes with carbon capture and storage.

The Road to Decarbonisation: Implications for Major Energy Projects4

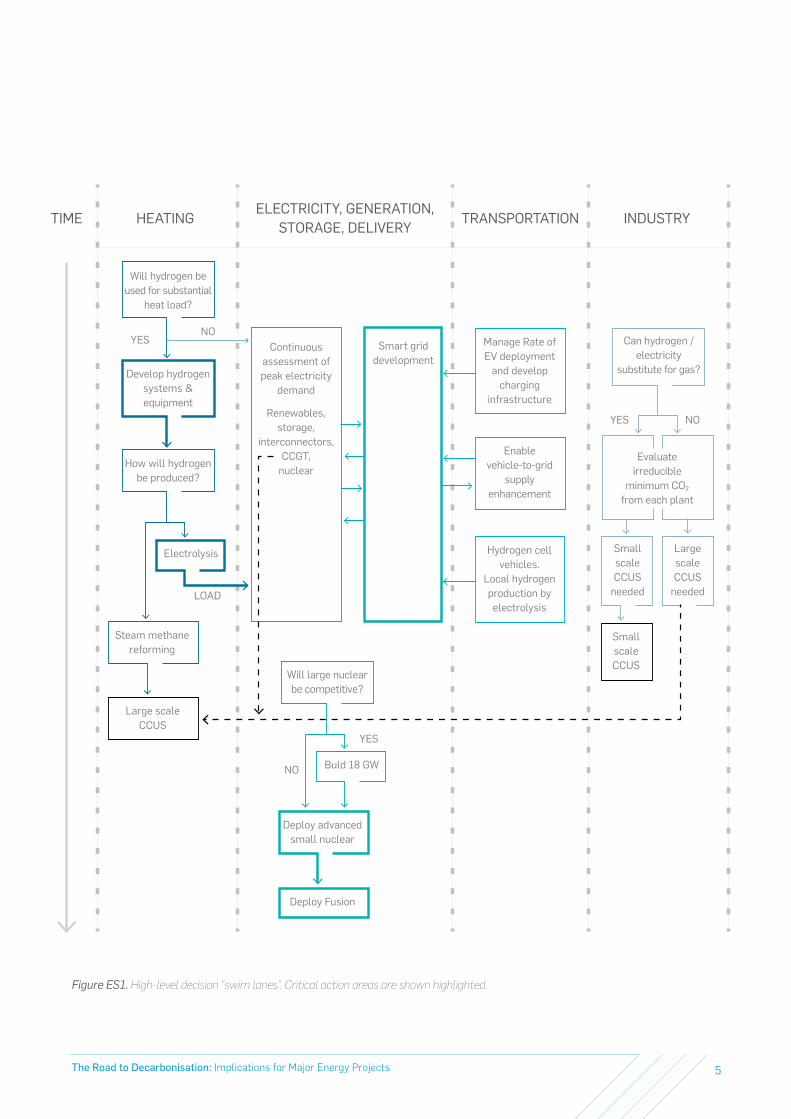

Electricity Generation: How quickly will peak electricity demand rise? How much generating capacity do we need to build? How much intermittent renewable generation can we have on the system? How much ES do we need? How much dispatchable power do we need (nuclear and/or CCGT with CCUS)? Is large nuclear going to deliver as planned? Do we need a contingency? Should we be developing and deploying small nuclear?

Industry: How much of industry’s CO2 emissions are non-substitutable by alternative zero-carbon processes or by use of hydrogen and electricity for heating? What are the absolute minimum CO2 emissions from industry, and could these be captured by CCUS? Will these industries still be operating as now in 2035 and beyond?

These questions and the consequent interactions between different sectors are illustrated in Figure ES1.

Stemming from these questions and with a view to generating opportunities for UK leadership and, critically, export potential, there are a number of key areas which we believe government should prioritise:

Hydrogen: Research and development of hydrogen production technologies with emphasis on methods other than steam methane reformation. Development of hydrogen fuel cells and hydrogen utilising systems and equipment. The UK should seek leadership in hydrogen systems and low-carbon production.

Small Advanced Nuclear: Move decisively to accelerate the advanced nuclear programme with a focus on reactor development for deployment of first of a kind (FOAK) in the mid-2030s. This programme should be delivery focussed and should include UK industrial partners, and should be driven by the industrial participants. Down-select two technologies for government support by the end of 2018.

Smart Grid: Develop Smart Grid technology and systems for UK deployment and for export. Focus on systems to integrate Electric Vehicle charging and deliver vehicle to grid power.

Fusion: Ensure continued support to the UK Atomic Energy Agency (UKAEA) through Brexit and encourage collaboration with private sector fusion ventures to promote Culham as the leading global centre for development of diverse fusion-related technologies.

We believe that by building on UK capabilities and expertise in these areas we would be able to develop a total package, offering all the essential elements of a future fossil fuel-free electric / hydrogen economy. This would be a powerful export offering, as well as providing a future proof system for the UK. These areas are highlighted in Figure ES1.

Although we regard CCUS as essentially a ‘bridging technology’, which would not form part of the ultimate energy system, we would support one CCUS demonstrator project at modest scale, preferably using industrial sources of CO2. The UK should refrain from committing to large scale CCUS until decisions regarding hydrogen utilisation for heating have been made and the potential need (in terms of capacity and duration) for steam methane reforming have been identified.

The CCC advises government on its policy and progress towards decarbonisation, setting five yearly ‘carbon budgets’ intended to guide the UK down the least cost path to its 2050 targets. It is important that the CCC continues this role. Faced with lobbying by various interest groups and with sometimes conflicting advice from ad hoc advisory committees and the National Infrastructure Commission (NIC), we believe the government should consider establishing a time limited advisory body, drawing heavily on industrial experts, to advise on the critical action areas of hydrogen, small advanced nuclear, smart grid and fusion with a view to informing decisions in these areas and maximising the UK’s opportunities in the global market. The government’s Industrial Strategy provides a framework for this effort and we would suggest that individual ‘sector deals’ such as for nuclear or offshore wind should be closely co-ordinated with a view to maximising the UK’s long-term opportunities in the global energy market.

5The Road to Decarbonisation: Implications for Major Energy Projects

HEATINGTIMEELECTRICITY, GENERATION,

STORAGE, DELIVERYTRANSPORTATION INDUSTRY

Will hydrogen be used for substantial

heat load?

YES

YES

YES

NO

NO

NO

LOAD

Develop hydrogen systems & equipment

Steam methane reforming

Large scale CCUS

Small scale CCUS

Electrolysis Small scale CCUS

needed

Large scale CCUS

needed

How will hydrogen be produced?

Deploy advanced small nuclear

Deploy Fusion

Buld 18 GW

Will large nuclear be competitive?

Manage Rate of EV deployment

and develop charging

infrastructure

Hydrogen cell vehicles.

Local hydrogen production by electrolysis

Enable vehicle-to-grid

supply enhancement

Can hydrogen / electricity

substitute for gas?

Evaluate irreducible

minimum CO₂ from each plant

Continuous assessment of peak electricity

demand

Renewables, storage,

interconnectors, CCGT,

nuclear

Smart grid development

Figure ES1. High-level decision “swim lanes”. Critical action areas are shown highlighted.

The Road to Decarbonisation: Implications for Major Energy Projects6

This paper seeks to step back from some of the detail of the decarbonisation debate, of which much has been published and some of which is inevitably contradictory. We have attempted to draw out a number of ‘key points’ that may influence the UK’s decisions as we move towards an energy system that will ultimately be zero-carbon and entirely fossil fuel-free. We identify some of the generic types of major projects that may be needed, the technology developments to support them and some of the impediments that risk holding back progress. Finally, we suggest some priority actions.

The Road to Decarbonisation: Implications for Major Energy Projects6

7The Road to Decarbonisation: Implications for Major Energy Projects

Ten years after the passage of the Climate Change Act 2008, the summer of 2018 has seen the publication of a plethora of reports on aspects of the UK’s progress towards decarbonisation of our economy and future energy strategies.

1. Introduction

The Government’s plans were set out in the Clean Growth Strategy published by BEIS in October 2017 (referred to as CGS). This comprehensive document sets out the policies and some of the actions that government will take, in concert with its Industrial Strategy published in November 2017, to deliver clean growth in the UK and maximise the UK’s opportunities arising from the global move to a low carbon economy.

The Committee on Climate Change (CCC) published an independent assessment of the CGS in January.

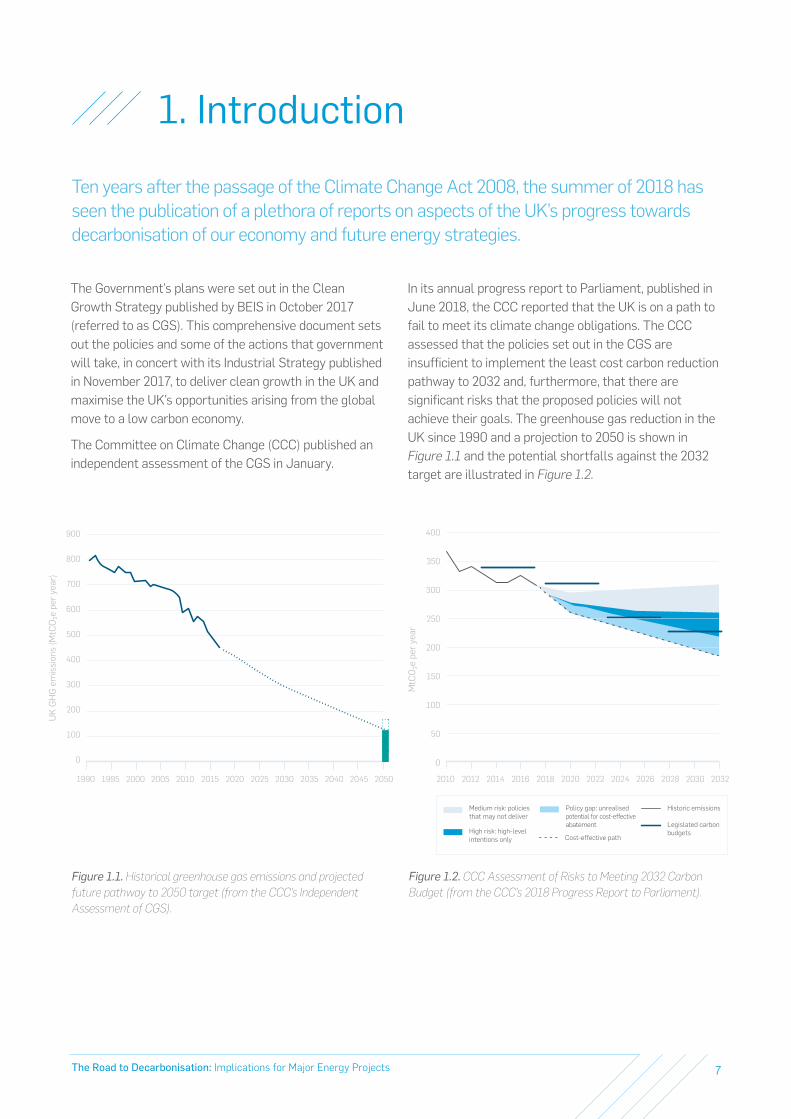

In its annual progress report to Parliament, published in June 2018, the CCC reported that the UK is on a path to fail to meet its climate change obligations. The CCC assessed that the policies set out in the CGS are insufficient to implement the least cost carbon reduction pathway to 2032 and, furthermore, that there are significant risks that the proposed policies will not achieve their goals. The greenhouse gas reduction in the UK since 1990 and a projection to 2050 is shown in Figure 1.1 and the potential shortfalls against the 2032 target are illustrated in Figure 1.2.

400

350

2012 2014 2016 2018 2020 2022 2024 2026 2028 2030 2032

Medium risk: policies that may not deliver

Legislated carbon budgets

Historic emissions

Cost-effective pathHigh risk: high-level intentions only

Policy gap: unrealised potential for cost-effectiveabatement

MtC

O₂e

per

yea

r

300

200

100

250

150

50

2010

0

Figure 1.1. Historical greenhouse gas emissions and projected future pathway to 2050 target (from the CCC’s Independent Assessment of CGS).

Figure 1.2. CCC Assessment of Risks to Meeting 2032 Carbon Budget (from the CCC’s 2018 Progress Report to Parliament).

900

700

800

1995 2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

UK

GH

G e

mis

sion

s (M

tCO

₂e p

er y

ear)

600

400

200

500

300

100

1990

0

The Road to Decarbonisation: Implications for Major Energy Projects8

Good progress has been made in the power generation and waste sectors, largely due to EU directives that were not specifically targeting CO2 reductions. However, progress in transportation and heating is slow. Figure 1.3 shows the CCC’s assessment of decarbonisation progress in each sector.

Pow

er

Was

te

Indu

stry

Tran

spor

t

F-ga

ses

Build

ings

Agr

icul

ture

&

LULU

CF

Emissions (MtCO₂e) Change in emissions 2012–2017

1990 1995 2000 2005 2010 2015

200

100

250 10%

0%

-10%

-20%

-30%

-40%

-50%

-60%

150

50

0

Figure 1.3. CCC Summary of emissions reductions since 1990 (from the CCC’s 2018 Progress Report to Parliament).

The Road to Decarbonisation: Implications for Major Energy Projects8

9The Road to Decarbonisation: Implications for Major Energy Projects

National Grid published its Future Energy Scenarios in July (referred to as FES 2018). This detailed and substantive analysis, updated annually, demonstrates the great complexity of the task ahead and the interdependencies between generation, transportation and heat. Generation, which has so far been the ‘star performer’ with closure of many coal pants replaced by cleaner gas and rapid roll out of renewables, will be further challenged by substantial increases in peak electrical demand, the closure of the remaining coal plants, replacement of our nuclear fleet and the challenges of maintaining grid stability with a rapidly increasing proportion of intermittent supply.

Carbon Capture Usage and Storage (CCUS) is seen by many authoritative advisors – the CCC, the Parliamentary Advisory Group on Carbon Capture and Storage (who published a 2016 report on CCUS, referred to as Oxburgh), and others – as an essential element of the least cost pathway to decarbonisation, but progress in UK has been limited since the cancellation of the CCS demonstrator programme. The CCUS Cost Challenge Taskforce published its report in July. It has stated that we must start deployment of CCUS at pilot scale as a matter of urgency and sets out some significant rates of deployment beyond 2035. The scope did not include economic modelling or cost estimating. The report states that the current UK cost base is not clear and furthermore “it has been difficult to quantify the cost reductions we anticipate in the UK”.

The National Infrastructure Commission (NIC) published its first National Infrastructure Assessment in July. It has clearly expressed doubts about the scale of the intended new nuclear build programme and suggested that there should be no ‘fleet plan’, rather that there should be case-by-case decisions for any plants after Hinkley Point C and not more than one further plant committed to before 2025. The NIC thus questions the current government policy of facilitating up to 18 GW of new nuclear and much of the thrust of the recently published Nuclear Sector Deal. In its assessment, the NIC has also expressed clear doubts about the economics of CCUS

for power generation and recommended that power generators should not be called upon to ‘cross subsidize’ CCUS that may be desired for other sectors. This is in direct opposition to the recommendations of the Oxburgh report on CCUS which recommended that CCUS in the power sector should be an ‘enabler’ for CCUS for other sectors.

These and other reports referred to in this paper are listed in Annex 1.

“The Road to Decarbonisation is long. We are striving for a goal that is perhaps some 50 years away, with a key legislated milestone in 2050, just 30 years away. This may seem like a long time, but we are today closing coal plants dating from the 1960s and nuclear plants from the 1970s. Hinkley Point C has a design life of 60 years and will be operating long after our ‘50 year’ horizon.”

The road ahead has many twists and turns, the issues are extremely complex and, in some areas technology is evolving rapidly. But we should have no illusions – there are no ‘magic bullets’. If we are to achieve our goals it will be by using technology that is largely envisaged today, and the task is of such a scale that major projects must be initiated very soon. We also need to anticipate capabilities that will be required in the long term and ensure that we nurture and develop those capabilities.

Very large infrastructure projects can easily take ten years or more from initiation to first operation. Private investors will be extremely wary of investing in such long-term projects if they perceive any doubt as to the stability of the policy framework or government’s long-term commitment.

This paper draws on data relating to UK CO2 emissions and energy use from several references. As the determination of this data is complex and approximate, this can lead to inconsistencies. However, of importance to this paper are the relative magnitudes of values associated with different sectors, rather than precise values.

The Road to Decarbonisation: Implications for Major Energy Projects10

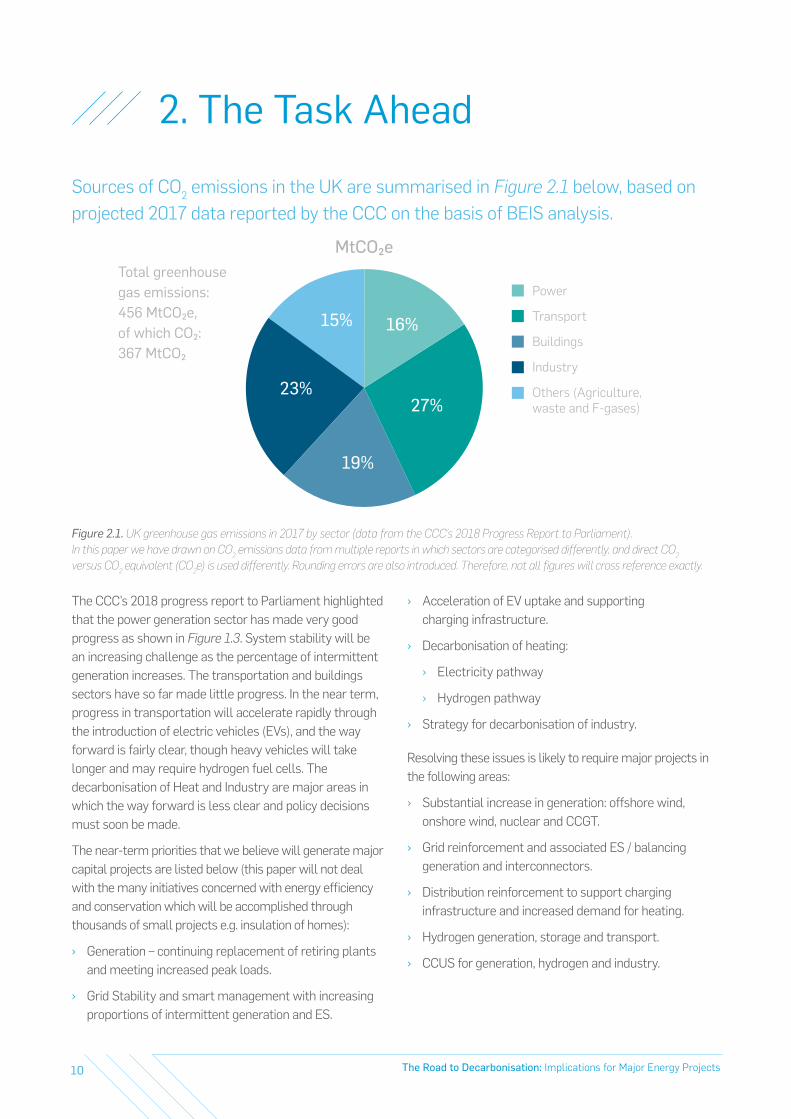

Sources of CO2 emissions in the UK are summarised in Figure 2.1 below, based on projected 2017 data reported by the CCC on the basis of BEIS analysis.

The CCC’s 2018 progress report to Parliament highlighted that the power generation sector has made very good progress as shown in Figure 1.3. System stability will be an increasing challenge as the percentage of intermittent generation increases. The transportation and buildings sectors have so far made little progress. In the near term, progress in transportation will accelerate rapidly through the introduction of electric vehicles (EVs), and the way forward is fairly clear, though heavy vehicles will take longer and may require hydrogen fuel cells. The decarbonisation of Heat and Industry are major areas in which the way forward is less clear and policy decisions must soon be made.

The near-term priorities that we believe will generate major capital projects are listed below (this paper will not deal with the many initiatives concerned with energy efficiency and conservation which will be accomplished through thousands of small projects e.g. insulation of homes):

› Generation – continuing replacement of retiring plants and meeting increased peak loads.

› Grid Stability and smart management with increasing proportions of intermittent generation and ES.

› Acceleration of EV uptake and supporting charging infrastructure.

› Decarbonisation of heating:

› Electricity pathway

› Hydrogen pathway

› Strategy for decarbonisation of industry.

Resolving these issues is likely to require major projects in the following areas:

› Substantial increase in generation: offshore wind, onshore wind, nuclear and CCGT.

› Grid reinforcement and associated ES / balancing generation and interconnectors.

› Distribution reinforcement to support charging infrastructure and increased demand for heating.

› Hydrogen generation, storage and transport.

› CCUS for generation, hydrogen and industry.

2. The Task Ahead

Power

Transport

Buildings

Industry

Others (Agriculture, waste and F-gases)

MtCO₂eTotal greenhouse gas emissions: 456 MtCO₂e, of which CO₂: 367 MtCO₂

16%

27%

19%

23%

15%

Figure 2.1. UK greenhouse gas emissions in 2017 by sector (data from the CCC’s 2018 Progress Report to Parliament). In this paper we have drawn on CO2 emissions data from multiple reports in which sectors are categorised differently, and direct CO2 versus CO2 equivalent (CO2e) is used differently. Rounding errors are also introduced. Therefore, not all figures will cross reference exactly.

11The Road to Decarbonisation: Implications for Major Energy Projects

3. The ‘Big Picture’Major Trends and Considerations

Many of the recently published reports focus on the ‘least cost’ pathway to 2050. This is entirely appropriate, but we believe that in developing a view of future scenarios there are a number of overarching trends that must be considered; these do not define detail but point to directions of travel and may not necessarily point to taking the near term least cost path. They include the three ‘legs’ of the ‘energy trilemma’ and additional considerations that are often implicitly recognised but not explicitly identified; our major trends include:

› The ‘Energy Trilemma’

› Sustainability – dominated by climate change, hence carbon reduction.

› Competitiveness – defined in terms of the price competitiveness of energy delivered to the consumer.

› Security – defined in terms of assured continuity of supply.

› Sustainability (Resource Conservation) – the priority issue of climate change (hence carbon reduction) as expressed in the Trilemma tends to dominate the current discussion of sustainability. The issue of depletion of hydrocarbons will also be a key issue in the long term, as well as the supply of raw materials and recycling / disposal of emerging technologies at scale (e.g. Lithium-ion batteries).

› Social Acceptance – in an ever more informed world with aggressive use of social media it is a difficult task to gain social acceptance of major projects or programmes impacting large numbers of people. Heathrow Expansion and HS2 are current examples.

› Finance and Affordability – for the past three decades in the UK our economic model for the energy sector has been based on the concept of private sector operators competing in liberalised open markets. Very large capital projects challenge the ability of markets to respond with adequate finance, as vividly demonstrated by the current large nuclear projects and Hinkley Point C and Wylfa.

› Decentralisation – both social acceptance and finance/affordability mitigate towards smaller projects. People will more readily accept a small and relatively unobtrusive plant dedicated to providing energy for their community than a large regional or national scale plant. Small plants with much lower capital investment requirements are more easily financed. We note that FES 2018 places much more emphasis on decentralisation than earlier versions.

› Global Applicability – the UK must look first to delivering its internal needs and climate goals, but our contribution to total global CO2 emissions is just 1%. The UK should therefore also consider the export potential of its expertise and technology, not only to impact the wider global CO2 problem beneficially, but also to develop UK industry and earn valuable export income.

The Road to Decarbonisation: Implications for Major Energy Projects

4.The ‘Final Destination’A Zero-Carbon Economy

Debate and policy development in the energy sector has been dominated for the last ten years by the issue of climate change and the pressing need for decarbonisation. Go back another ten to fifteen years and there was much debate about ‘Peak Oil’ – when would the world run out of oil and gas? These two issues, Climate Change and Oil & Gas Resources, are clearly linked and yet frequently considered separately. Both are critical to development of a long-term Sustainable Energy Policy and associated infrastructure.

SNC-Lavalin Atkins works across the energy sector, from nuclear to offshore wind, and is technologically neutral. We believe that the medium-term (by 2050) imperative to reduce CO2 emissions should be managed in the context of the longer-term destination – zero-carbon and zero-fossil fuels. Recently, analysts have forecast ‘Peak Oil’ as early as 2036 (Wood Mackenzie, 2018), not limited by supply but by demand. The carbon reduction agenda is now likely to be the determinant of ‘Peak Oil’. Ultimately the world will be weaned off its fossil fuel dependency, driven initially by climate change and in the long term by limitation of resources and increasing oil and gas prices.

Recognising the trends outlined above, Atkins envisions that the ultimate energy system (beyond 2050) will be:

› One in which no fossil fuel resources will be employed (no coal, oil or gas).

› Energy generation will comprise renewables and nuclear (fission and fusion).

› ES and smart demand management will be employed to optimise use of generating assets.

› Energy vectors will be electricity and hydrogen.

› Much more decentralised than today.

No one technology will dominate – the optimal system will require a holistic approach in which different technologies will each be applied to specific circumstances. For example: in transportation it is likely that both light-duty battery powered vehicles and heavier-duty hydrogen fuel cell vehicles will be in use. Trains will be electric and hydrogen fuel cell powered. In domestic heating, there may be areas in which hydrogen-fired boilers (using hydrogen from electrolysis) will predominate, supplied through an upgraded gas distribution system. District heating run from small modular reactors or fusion energy plants will service some of the more densely populated areas. In other areas that are less densely populated and not connected to the gas distribution system there will be electrically powered heat pumps or other hybrid devices.

This system is illustrated in Figure 4.1.

The Road to Decarbonisation: Implications for Major Energy Projects12

The Road to Decarbonisation: Implications for Major Energy Projects

4.The ‘Final Destination’A Zero-Carbon Economy

Large Nuclear

Other

Storage

Storage

User storage and

vehicles

Solar PV

Onshore wind

Offshore wind

DISTRIBUTION

USER

USER

USER

INTERCONNECTORS TO EUROPE

DISTRIBUTION

HYDROGEN TURBINE

GENERATION

HYDROGEN PRODUCTION & STORAGE

HYDROGEN PRODUCTION & STORAGE

DISTRIBUTION

USER

NATIONAL GRID

Small Nuclear

Other

Solar PV

User generation e.g. solar

Onshore wind

The Road to Decarbonisation: Implications for Major Energy Projects 13

Figure 4.1. Simplified ‘Ultimate’ UK energy system beyond 2050.Arrows represent energy flows.

The Road to Decarbonisation: Implications for Major Energy Projects14

5. Sectoral Carbon Reduction Pathways

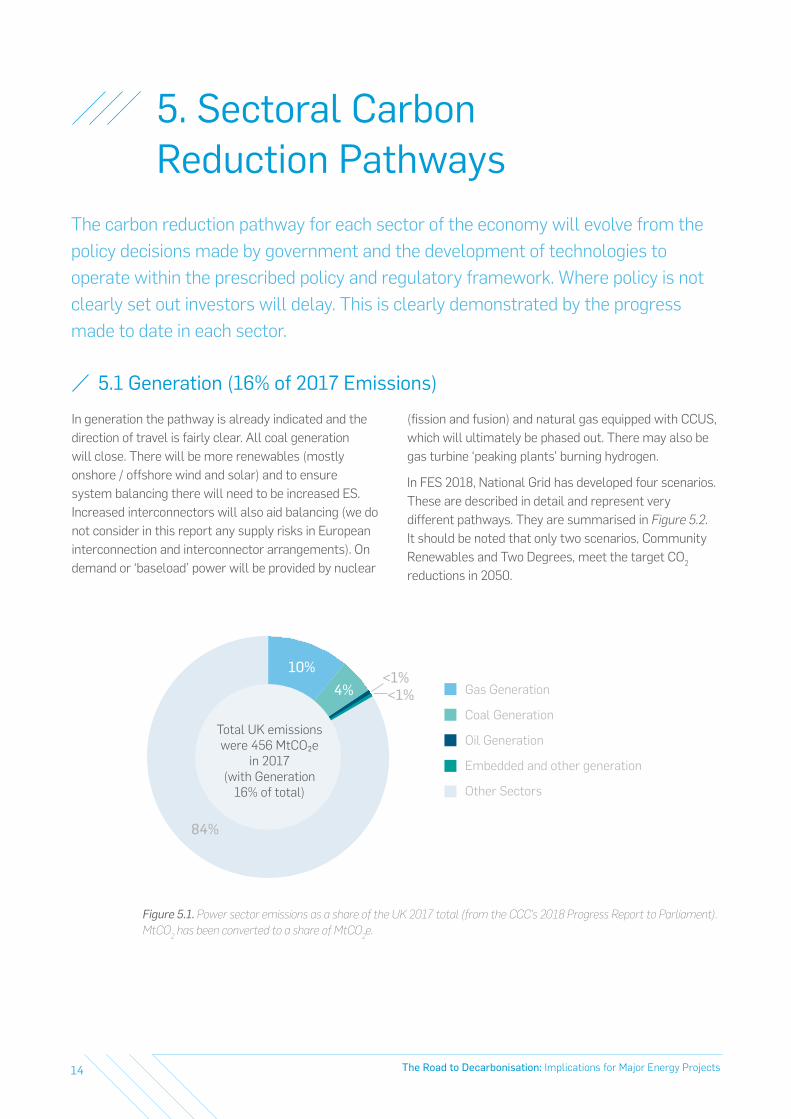

5.1 Generation (16% of 2017 Emissions)

In generation the pathway is already indicated and the direction of travel is fairly clear. All coal generation will close. There will be more renewables (mostly onshore / offshore wind and solar) and to ensure system balancing there will need to be increased ES. Increased interconnectors will also aid balancing (we do not consider in this report any supply risks in European interconnection and interconnector arrangements). On demand or ‘baseload’ power will be provided by nuclear

(fission and fusion) and natural gas equipped with CCUS, which will ultimately be phased out. There may also be gas turbine ‘peaking plants’ burning hydrogen.

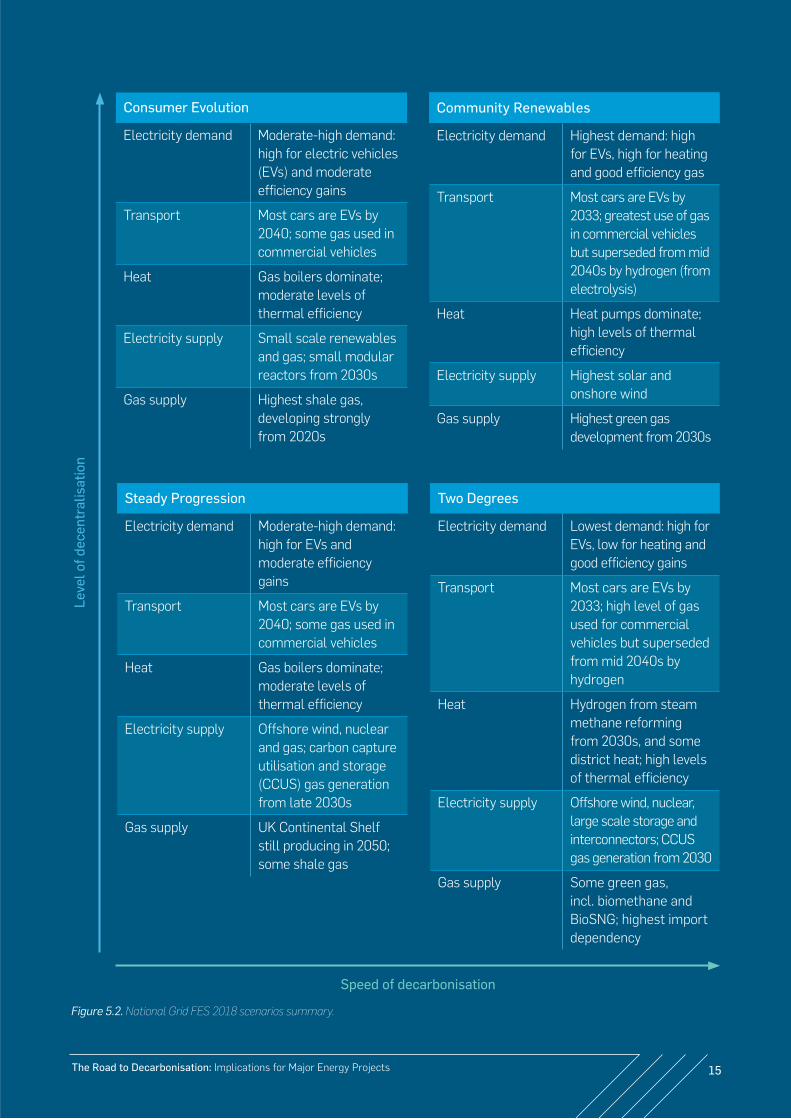

In FES 2018, National Grid has developed four scenarios. These are described in detail and represent very different pathways. They are summarised in Figure 5.2. It should be noted that only two scenarios, Community Renewables and Two Degrees, meet the target CO2 reductions in 2050.

10%4%

<1%<1% Gas Generation

Coal Generation

Oil Generation

Embedded and other generation

Other Sectors

84%

Total UK emissions were 456 MtCO₂e

in 2017 (with Generation

16% of total)

Figure 5.1. Power sector emissions as a share of the UK 2017 total (from the CCC’s 2018 Progress Report to Parliament). MtCO2 has been converted to a share of MtCO2e.

The carbon reduction pathway for each sector of the economy will evolve from the policy decisions made by government and the development of technologies to operate within the prescribed policy and regulatory framework. Where policy is not clearly set out investors will delay. This is clearly demonstrated by the progress made to date in each sector.

The Road to Decarbonisation: Implications for Major Energy Projects

Figure 5.2. National Grid FES 2018 scenarios summary.

Consumer Evolution

Electricity demand Moderate-high demand: high for electric vehicles (EVs) and moderate efficiency gains

Transport Most cars are EVs by 2040; some gas used in commercial vehicles

Heat Gas boilers dominate; moderate levels of thermal efficiency

Electricity supply Small scale renewables and gas; small modular reactors from 2030s

Gas supply Highest shale gas, developing strongly from 2020s

Steady Progression

Electricity demand Moderate-high demand: high for EVs and moderate efficiency gains

Transport Most cars are EVs by 2040; some gas used in commercial vehicles

Heat Gas boilers dominate; moderate levels of thermal efficiency

Electricity supply Offshore wind, nuclear and gas; carbon capture utilisation and storage (CCUS) gas generation from late 2030s

Gas supply UK Continental Shelf still producing in 2050; some shale gas

Community Renewables

Electricity demand Highest demand: high for EVs, high for heating and good efficiency gas

Transport Most cars are EVs by 2033; greatest use of gas in commercial vehicles but superseded from mid 2040s by hydrogen (from electrolysis)

Heat Heat pumps dominate; high levels of thermal efficiency

Electricity supply Highest solar and onshore wind

Gas supply Highest green gas development from 2030s

Two Degrees

Electricity demand Lowest demand: high for EVs, low for heating and good efficiency gains

Transport Most cars are EVs by 2033; high level of gas used for commercial vehicles but superseded from mid 2040s by hydrogen

Heat Hydrogen from steam methane reforming from 2030s, and some district heat; high levels of thermal efficiency

Electricity supply Offshore wind, nuclear, large scale storage and interconnectors; CCUS gas generation from 2030

Gas supply Some green gas, incl. biomethane and BioSNG; highest import dependency

Leve

l of d

ecen

tral

isat

ion

Speed of decarbonisation

The Road to Decarbonisation: Implications for Major Energy Projects 15

The Road to Decarbonisation: Implications for Major Energy Projects16

The scenarios serve to illustrate the wide range of potential outcomes and different proportions of technology deployment in the context of speed of decarbonisation and level of decentralisation. There could of course be many more scenarios; our vision of the ultimate configuration is

highly decentralised but has more nuclear than any of the scenarios generated for FES 2018.

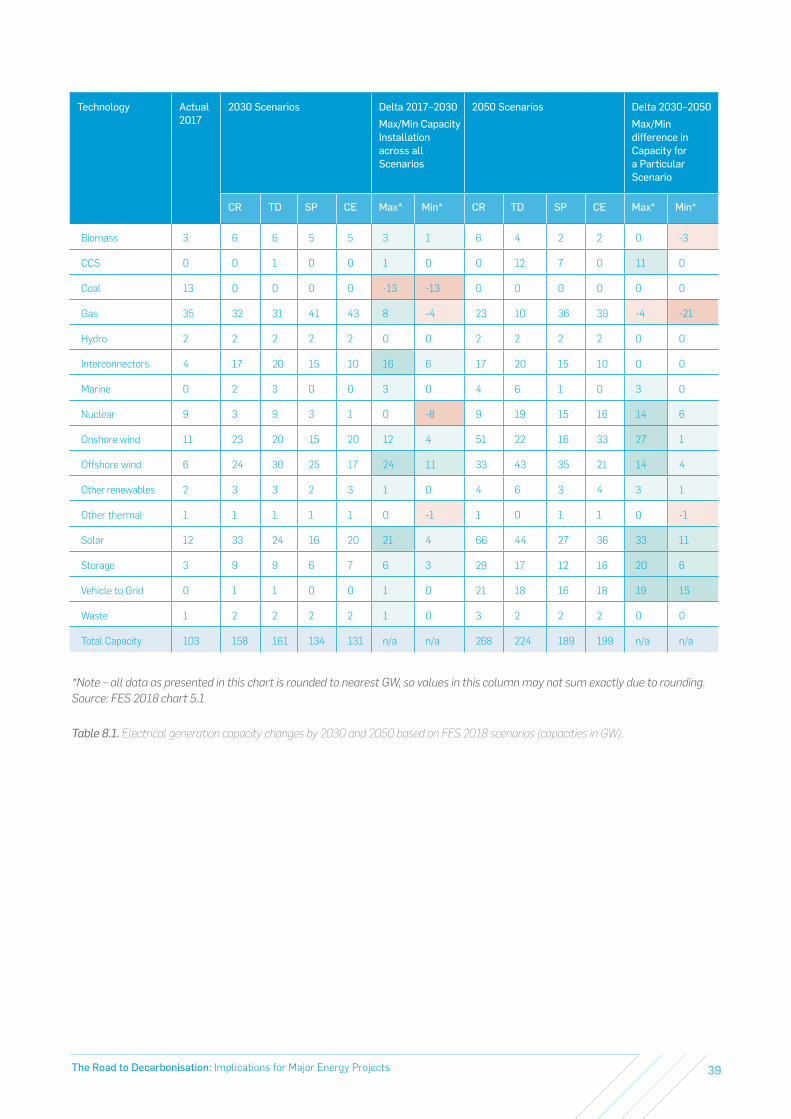

This wide variation in scenario outcomes is demonstrated by the estimated installed generating capacities shown in Figure 5.3 below.

A different modelling approach taken by MIT in its study of the future role of nuclear results in very different conclusions regarding the potential generating mix for the UK in 2050. MIT modelled the sensitivity of the optimal generating mix to variations in the cost of nuclear power and the system wide average CO2 emissions per kWh of generation. The results are shown in Figure 5.4 below.

MIT modelled three scenarios for nuclear:

› None: there would be no nuclear at all (implication is that nuclear cannot achieve current cost targets)

› Nominal Cost: Nuclear can achieve an overnight capital cost of approximately $8,000/kW

› Low Cost: Nuclear can achieve an overnight capital cost of approximately $6,000/kW.

Figure 5.3. Generating capacity by technology type and amount of renewable capacity for 2017, 2030 and 2050 (National Grid, FES 2018).

Inst

alle

d ge

nera

tion

capa

city

(GW

)

300

200

100

250

150

50

2017 2030CR TD SP CE CR TD SP CE

2050

0

Renewable capacity

Interconnectors

Marine

Other renewables

Nuclear

Offshore wind

StorageOnshore wind

Vehicle-to-gridSolar

Other thermal

Biomass

CCS

Waste

Gas

Coal

Hydro

› In all scenarios there remains a substantial proportion of generation by gas in 2050 but only in Two Degrees does a large element of CCUS appear.

› Community Renewables 2050 represents the most decentralised scenario but is dependent on very large adoption of solar and onshore wind. An alternative scenario might be constructed with decentralised small advanced nuclear.

› There is significant import of energy through interconnectors in all scenarios.

› The two scenarios that comply with the 2050 target (Community Renewable and Two Degrees) both require a very large input from storage, including vehicle to grid.

Key observations from the scenarios developed in FES 2018 include:

The Road to Decarbonisation: Implications for Major Energy Projects 17

Figure 5.4. Optimal generating capacity mix for the UK in 2050 (from MIT, The Future of Nuclear Energy in a Carbon-Constrained World).

Tota

l ins

talle

d ca

paci

ty (M

W)

Tota

l ins

talle

d ca

paci

ty (G

W)

Nuclear - None Nuclear - Nominal Cost Nuclear - Low Cost100%

600

500

400

300

200

100

0

80%

60%

40%

20%

0%

Total installed capacity (GW)

Nuclear

Storage (Pumped Hydro and Battery)Renewable (Wind and Solar) CCS (CCGT and IGCC) Technologies

Natural Gas (OCGT and CCGT) Coal (IGCC)

Emissions (g/kWh)

500 g/kWh, 5

8 GW

100 g/kW

h, 58 G

W

50 g/kWh, 8

5 GW

10 g/kW

h, 203 G

W

1 g/kW

h, 478 G

W

500 g/kWh, 5

8 GW

100 g/kW

h, 60 G

W

50 g/kWh, 7

2 GW

10 g/kW

h, 66 G

W

1 g/kW

h, 77 G

W

500 g/kWh, 5

5 GW

100 g/kW

h, 58 G

W

50 g/kWh, 6

1 GW

10 g/kW

h, 60 G

W

1 g/kW

h, 67 G

W

For each nuclear cost scenario, the optimal generating mix was modelled for a range of system-wide carbon intensities from 500 gCO2/kWh down to 1 gCO2/kWh. The results show that for deep decarbonisation, below 50 gCO2/kWh, nuclear (at current nominal cost levels or less) forms a substantial proportion of the optimal generating mix. The study suggested that to achieve 2050 carbon stabilisation goals the UK will need to achieve 10 gCO2/kWh.

How will the mix of types of generation be determined? In theory market forces will determine what independent power companies decide to build. In reality; as has been the case for the past decade, government policy will massively influence what gets built. Regulations, levels of subsidy for specific technologies, planning considerations and the operating framework of the market all determine which projects go forward and which do not.

Offshore wind is an excellent example; without determined government policy and subsidy not one offshore turbine would have been installed. The policy has been a success as demonstrated by the rapid deployment of offshore wind and the falling price illustrated in Figure 5.5. We estimate that the annual subsidy under the currently awarded offshore wind Contracts for Difference is in the order of £1.5bn. This illustrates the level of commitment that is needed to bring forward major change in the energy industry.

The Road to Decarbonisation: Implications for Major Energy Projects18

160

140

120

100

80

60

40

20

0

16

14

12

10

8

6

4

2

02010–2011

142

121

97

60

Offshore Wind Levelised Cost of Energy (LCOE) for projects reaching Financial Investment

Decision (FID), £/MWh

2012–2014 2015–2016 2017–2018

2020Cost

Target

Approximate cumulative offshore wind capacity

committed, GW

Grid Stability and Storage

A key question is – how much intermittent renewable generation can be supplied before grid stability is compromised? The CCC has suggested that 50% intermittent generation can be economically managed and possibly as high as 60%. National Grid, in FES 2018, has acknowledged the increasing complexity of maintaining system stability but does not appear to have constrained its scenarios due to stability concerns. In 2050, renewables appear to represent about 65% of capacity for Community Renewables, and about 60% for Two Degrees. These appear to be near the limit of manageable intermittent resource according to these references.

“Proponents of very high dependency on renewables refer to energy storage as the mechanism to ensure system stability and compensate for intermittency of supply.”

Figure 5.5. UK offshore wind cost history and capacity committed for projects reaching Financial Investment Decision.

LCOE data for 2010–2016 is from ORE Catapult’s Cost Reduction Monitoring Framework Summary Report 2016. The 2017–2018 LCOE is an estimate based on the strike prices achieved in the 2017 Contract for Difference (CfD) auction. Cumulative committed capacity data is intended to present an indicative estimate, based on the results of the 2014–2017 FID-enabled and CfD auctions.

Storage is an option for short term stability management and is increasingly used to maintain system stability, National Grid is working to create new market opportunities for these system stability related services. However, battery storage is not an option for significant shortfall in supply. Storage will be provided at various levels in the system. Individual battery storage will be used in homes, EV batteries connected to smart charging systems will be able to feed back to supplement supply in times of shortage (so called Vehicle to Grid). Aggregation of thousands of small batteries in homes and vehicles could supply significant ‘peaking’ capacity if the smart charging management systems can be developed and consumers are incentivised to co-operate.

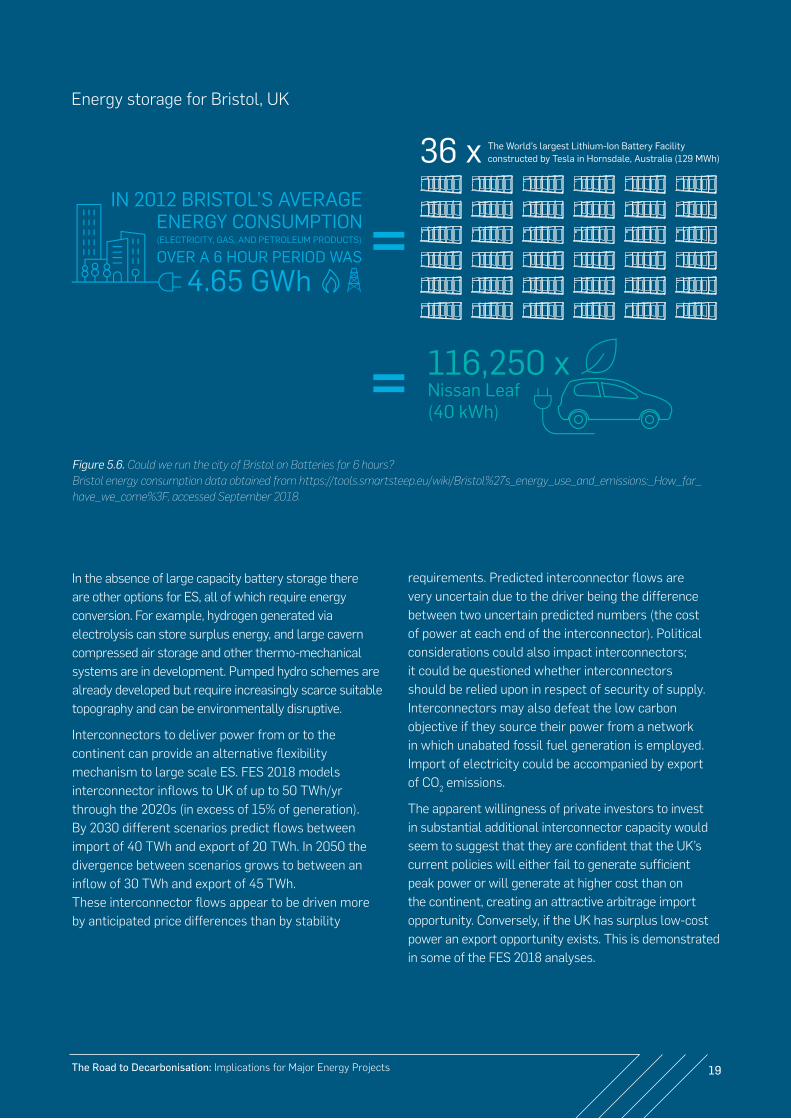

At the transmission and distribution levels, ES will be employed for short term system stability management, but large battery storage at the transmission level to address shortfalls in supply remains unrealistic at this time. As an example, we have estimated the battery capacity that would be required to sustain the energy consumed by the City of Bristol for 6 hours, the results are illustrated in Figure 5.6.

In the absence of large capacity battery storage there are other options for ES, all of which require energy conversion. For example, hydrogen generated via electrolysis can store surplus energy, and large cavern compressed air storage and other thermo-mechanical systems are in development. Pumped hydro schemes are already developed but require increasingly scarce suitable topography and can be environmentally disruptive.

Interconnectors to deliver power from or to the continent can provide an alternative flexibility mechanism to large scale ES. FES 2018 models interconnector inflows to UK of up to 50 TWh/yr through the 2020s (in excess of 15% of generation). By 2030 different scenarios predict flows between import of 40 TWh and export of 20 TWh. In 2050 the divergence between scenarios grows to between an inflow of 30 TWh and export of 45 TWh. These interconnector flows appear to be driven more by anticipated price differences than by stability

Figure 5.6. Could we run the city of Bristol on Batteries for 6 hours?Bristol energy consumption data obtained from https://tools.smartsteep.eu/wiki/Bristol%27s_energy_use_and_emissions:_How_far_have_we_come%3F, accessed September 2018.

requirements. Predicted interconnector flows are very uncertain due to the driver being the difference between two uncertain predicted numbers (the cost of power at each end of the interconnector). Political considerations could also impact interconnectors; it could be questioned whether interconnectors should be relied upon in respect of security of supply. Interconnectors may also defeat the low carbon objective if they source their power from a network in which unabated fossil fuel generation is employed. Import of electricity could be accompanied by export of CO2 emissions.

The apparent willingness of private investors to invest in substantial additional interconnector capacity would seem to suggest that they are confident that the UK’s current policies will either fail to generate sufficient peak power or will generate at higher cost than on the continent, creating an attractive arbitrage import opportunity. Conversely, if the UK has surplus low-cost power an export opportunity exists. This is demonstrated in some of the FES 2018 analyses.

Energy storage for Bristol, UK

IN 2012 BRISTOL’S AVERAGEENERGY CONSUMPTION(ELECTRICITY, GAS, AND PETROLEUM PRODUCTS) OVER A 6 HOUR PERIOD WAS

4.65 GWh=

36 x The World’s largest Lithium-Ion Battery Facilityconstructed by Tesla in Hornsdale, Australia (129 MWh)

= 116,250 xNissan Leaf(40 kWh)

19The Road to Decarbonisation: Implications for Major Energy Projects

The Road to Decarbonisation: Implications for Major Energy Projects20

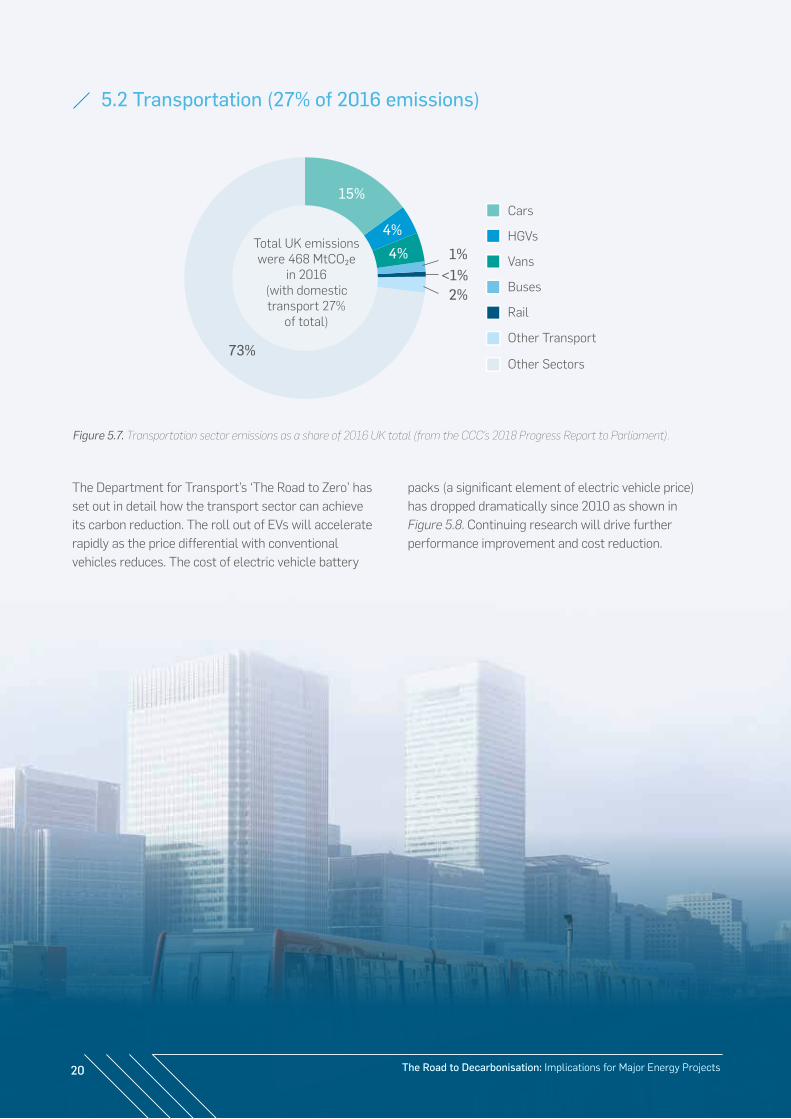

5.2 Transportation (27% of 2016 emissions)

Figure 5.7. Transportation sector emissions as a share of 2016 UK total (from the CCC’s 2018 Progress Report to Parliament).

The Department for Transport’s ‘The Road to Zero’ has set out in detail how the transport sector can achieve its carbon reduction. The roll out of EVs will accelerate rapidly as the price differential with conventional vehicles reduces. The cost of electric vehicle battery

packs (a significant element of electric vehicle price) has dropped dramatically since 2010 as shown in Figure 5.8. Continuing research will drive further performance improvement and cost reduction.

Cars

HGVs

Vans

Buses

Rail

Other Transport

Other Sectors

15%

73%

4%

4% 1%<1%

2%

Total UK emissions were 468 MtCO₂e

in 2016 (with domestic transport 27%

of total)

The Road to Decarbonisation: Implications for Major Energy Projects20

21The Road to Decarbonisation: Implications for Major Energy Projects

Government will encourage transition to EVs through tighter regulations, support grants for early adoption and by supporting the deployment of charging points across the motorway and highway network. UK policy is that the sale of conventional petrol and diesel cars and vans will end by 2040, Scotland has set a more aggressive target of 2030.

Heavier vehicles are the subject of continuing research. We anticipate that many are likely to use hydrogen fuel cell technology, which will require deployment of high purity hydrogen recharging facilities. Many of these facilities will be supplied using hydrogen generated locally by electrolysis.

The transition of transportation to electrically powered vehicles (whether directly through batteries or indirectly through hydrogen from electrolysis) will substantially increase total electricity demand. However, the impact on peak demand will be very much dependent on the charging patterns of the vehicle fleet.

The direction of change in transportation is clear, and patterns of transportation use are changing. The pace will depend on a combination of government policies, levels of support, consumer sentiment and economic conditions. Research and development will refine technology, improving performance and mass adoption will drive down the costs of new EVs.

› Transportation conversion will be industry and customer-lead, following policy prompts, regulation and early stage inducements.

› Transportation will ultimately become either battery powered, or hydrogen fuel cell driven.

› Substantial investment will be required to deploy a nationwide charging infrastructure and potentially a hydrogen filling infrastructure.

› FES 2018 shows, through its different scenarios, that the impact on the electricity system remains uncertain and may be very much dependent on user behaviour and smart grid management of the aggregated vehicle storage capacity.

Key observations on transport:

2010 2011 2012 2013 2014 2015 2016 2017

Battery Pack Price $/KWH

1000

800

642599

540

350273

209

20%

20%

7%10%

35%

22%24%

Figure 5.8. Fall in electric vehicle battery pack costs (from Department of Transport, The Road to Zero).

The Road to Decarbonisation: Implications for Major Energy Projects22

Buildings contribute 30% of our CO2 emissions either directly (19%) or indirectly through their share of grid electricity (11%). Assuming that the grid component will in time be eliminated by decarbonisation of generation then there remains 20% attributable to the direct emissions from buildings. This is perhaps the most intractable element of our carbon emissions and is subject to the greatest uncertainty with respect to technology and high risk of achievement. For practical purposes there are only three major options:

› Electrical heating – mostly through air or ground source heat pumps

› Hydrogen heating – by adaptation of existing gas distribution systems and equipment

› District heating – by utilising heat from local sources such as combined heat and power (CHP) plants and waste heat sources such as industrial plant

5.3 Buildings (19% direct contribution to 2017 emissions)

Residential Direct CO₂

Residential Non-CO₂

Public Direct CO₂

Public Non-CO₂

Commercial Direct CO₂

Commercial Non-CO₂

Residential Share of CO₂ from Grid Electricity

Commercial Share of CO₂ from Grid Electricity

Public Share of CO₂ from Grid Electricity

Other Sectors

70%

1%

2%2%

Total UK emissions were 456 MtCO₂e

in 2017 (with Buildings 19%

of total)

14%

6%

4%

Figure 5.9. Buildings emissions as a share of 2016 UK total (from the CCC’s 2018 Progress Report to Parliament).

› Much more work needs to be done to improve building insulation in the short term.

› Medium-term improvements can only be achieved with clear direction from government and substantial infrastructure investment in both electricity and hydrogen pathways (see next page).

› Government has initiated research into the generation and distribution of hydrogen.

› District heating provides an opportunity for significant additional return on investment for CHP plants built close to centres of population.

Key observations on buildings:

23The Road to Decarbonisation: Implications for Major Energy Projects

A major constraint on options for domestic heating is the very large seasonal variation in demand. This is illustrated in Figure 5.10, which also shows the impact of residential property size and quality of insulation. The ratio of peak to average demand for heating can be as high as nine,

Figure 5.10. Annual variations in household heat demand (from H2FC Supergen, The Role of Hydrogen and Fuel Cells in Future Energy Systems).

160

140

120

100

80

60

40

20

0

Hou

seho

ld h

eat d

eman

d (k

Wh

per d

ay)

Jan Apr Jul Oct Jan

Largest and oldest houses

UK average

Smallest and best insulated flats

Heat demand includes space and water heating. Winter consumption is strongly temperature-dependant and the winter peaks can be much higher in a cold year.

making it uneconomic to match supply to peak demand unless there is considerable ES in the system. The implications are further discussed in Section 6.

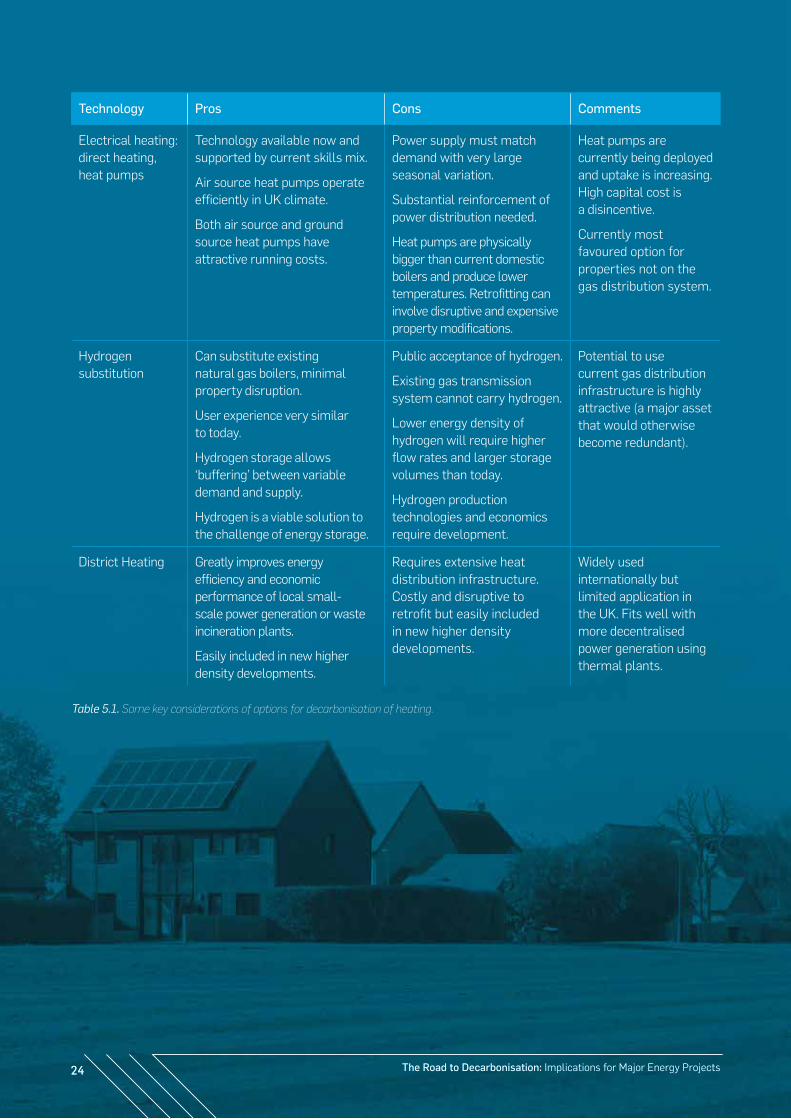

Pros and cons of the three options for heating are summarised in Table 5.1.

The Road to Decarbonisation: Implications for Major Energy Projects24

Technology Pros Cons Comments

Electrical heating: direct heating, heat pumps

Technology available now and supported by current skills mix.

Air source heat pumps operate efficiently in UK climate.

Both air source and ground source heat pumps have attractive running costs.

Power supply must match demand with very large seasonal variation.

Substantial reinforcement of power distribution needed.

Heat pumps are physically bigger than current domestic boilers and produce lower temperatures. Retrofitting can involve disruptive and expensive property modifications.

Heat pumps are currently being deployed and uptake is increasing. High capital cost is a disincentive.

Currently most favoured option for properties not on the gas distribution system.

Hydrogen substitution

Can substitute existing natural gas boilers, minimal property disruption.

User experience very similar to today.

Hydrogen storage allows ‘buffering’ between variable demand and supply.

Hydrogen is a viable solution to the challenge of energy storage.

Public acceptance of hydrogen.

Existing gas transmission system cannot carry hydrogen.

Lower energy density of hydrogen will require higher flow rates and larger storage volumes than today.

Hydrogen production technologies and economics require development.

Potential to use current gas distribution infrastructure is highly attractive (a major asset that would otherwise become redundant).

District Heating Greatly improves energy efficiency and economic performance of local small-scale power generation or waste incineration plants.

Easily included in new higher density developments.

Requires extensive heat distribution infrastructure. Costly and disruptive to retrofit but easily included in new higher density developments.

Widely used internationally but limited application in the UK. Fits well with more decentralised power generation using thermal plants.

Table 5.1. Some key considerations of options for decarbonisation of heating.

The Road to Decarbonisation: Implications for Major Energy Projects24

The Road to Decarbonisation: Implications for Major Energy Projects

5.4 Industry (23% direct contribution to 2017 emissions)

Industry contributes about 28% of our CO2 emissions, as shown in Figure 5.11, of which about 5% is indirect from use of electicity from grid, which will be decarbonised. Thus the direct CO2 emissions from industry are about 23% of UK emissions. Half of this (12% of UK total) is from manufacturing combustion, which could potentially be replaced by electrical heating or by hydrogen fired equipment. A further 9% appears to come from fossil fuel production and fugitive emissions (such as leakage) whilst only 2% are attributed to manufacturing process emissions.

CCUS is said by many to be essential for industry, but it would appear from the figures above that non-substitutable CO2 emissions may in fact be very small. The scale of CCUS required may therefore be much smaller than some estimates suggest.

In order to properly evaluate the potential industrial need for CCUS it is essential to analyse the industrial emissions inventory in detail. Naturally owners of large plants would prefer for their stack emissions to be diverted into CCUS with minimum disruption to their plant. The age of industrial plant must be a key consideration in evaluating the need for CCUS. For each plant its expected future life

span should be the first consideration in evaluating its potential requirement for CCUS, commercial deployment of which is likely to be at least 15 to 20 years away. Many existing industrial plants may be replaced before large scale CCUS becomes available.

Figure 5.11. Industry emissions, including indirect emissions from grid electricity, as a share of the 2017 UK total (from the CCC’s 2018 Progress Report to Parliament).

72%

3%

2%

Total UK emissions were

456 MtCO₂e in 2017

(with Industry 23% of total)

12%

6%

5%

Manufacturing combustion emissions

Manufacturing process emissions

Refineries

Fossil fuel production and fugitive emissions

Indirect CO₂ from using grid electricity

Other Sectors

› Non-substitutable CO2 emissions (those that are not related to combustion or fugitive emissions) are small.

› Action to address these may be delayed, many industrial plants will be replaced before 2050, and alternative processes producing less CO2 may be deployed.

› CCUS for industry may be required at a much smaller scale than currently suggested by some reports.

Key observations on industry:

25The Road to Decarbonisation: Implications for Major Energy Projects

The Road to Decarbonisation: Implications for Major Energy Projects

6. Hydrogen Pathway and Electricity Pathway

It is clear that further progress towards deep decarbonisation will require substantial investments in two technological paths: the Hydrogen path and the Electricity path. Almost certainly both paths will be followed. However, the relative mix of the two and the interactions between them are not yet clear and will be impacted by costs, deliverability, regulation, policy decisions and public acceptance.

The potential role of hydrogen was assessed by the Energy Research Partnership in its October 2016 report. The report noted many opportunities for use of hydrogen but also identified a number of impediments, the most significant of which is that currently the cheapest method of hydrogen production is by steam methane reforming. This would require continuing large-scale imports of natural gas and very large scale CCUS as the process produces large amounts of CO2.

Both of the hydrogen and electricity pathways have the potential to require large scale CCUS and this is the working assumption of the CCC and Oxburgh reports. However, both pathways could also be achieved with much reduced CCUS if the cost of electricity generation was to be driven down and hydrogen production was through electrolysis. Government has commissioned

research into production of hydrogen and we believe the generation of hydrogen is one of the most important determinants of many future projects.

Heating of buildings and industrial heat are the sectors in which the hydrogen / electricity pathway trade-off is most significant and will require policy decisions most urgently. Government has also commissioned research into the feasibility of repurposing the gas transmission and distribution systems to carry hydrogen.

Energy demand for heating has a very high peak to average ratio, shown in Figure 6.1 below. This large variation dominates the variation in total energy demand and is the major challenge to electrification of heat. In the absence of a practical large-scale ES option for electricity and with limited hydrogen use, it would be necessary to build electrical generation capacity to meet the peak demand. Much of this capacity would be idle through the summer months. The variation can be smoothed out by using surplus generating capacity in summer to produce hydrogen by electrolysis which will be stored for use in winter to meet heating demand.

Some of the key factors influencing the hydrogen / electricity pathway selection are summarised below.

Figure 6.1. Daily energy Demand 2015–2018 (Dr Grant Wilson, University of Sheffield, energy-charts.org).

GW

h pe

r day

Jan

Great Britain’s Energy Vectors - in GWh per day

2015 2016 2017 2018

4000 GWh

3500 GWh

3000 GWh

2500 GWh

2000 GWh

1500 GWh

1000 GWh

500 GWh

0 GWh

Jan

Feb

Mar

Apr Jun

Jul

Aug

Sep

Oct

Nov Dec

May Jan

Feb

Mar

Apr Jun

Jul

Aug

Sep

Oct

Nov Dec

May Jan

Feb

Mar

Apr Jun

Jul

Aug

Sep

Oct

Nov Dec

May

Feb

Mar

Apr

Liquid Transport Fuels Demand Electricity Demand Natural gas demand, Non-Daily Metered (a proxy for heat demand)

26

27The Road to Decarbonisation: Implications for Major Energy Projects

6.1 Hydrogen Production, Storage and Transport

The method used for production of hydrogen and the extent of hydrogen uptake for heating is perhaps the most pressing issue in evaluating future major projects.

Large scale use of hydrogen produced by steam methane reforming cannot proceed without large scale CCUS. This points to large centralised facilities, creation of a CO2 collection infrastructure and the creation of a new national gas transmission system fit for hydrogen. The use of hydrogen in heating would greatly reduce peak electricity demand. Optimisation of the system would be a balance between peak electricity generation, hydrogen production capacity and storage capacity. Large scale storage would be in underground salt caverns or potentially in depleted oil / gas fields; today we use these methods to store natural gas.

If hydrogen could be produced closer to the users through electrolysis, then a much more decentralised system could evolve. Neither a national hydrogen transmission system nor a CO2 collection infrastructure would be required. In time such a system could be associated with decentralised small advanced fission or fusion reactors for electricity generation. These would be located close enough to population centres for use of waste heat in district heating systems. Such a configuration would be much closer to what we believe is the likely ultimate fossil fuel-free scenario. Local hydrogen production is challenged by the requirement to store large volumes locally, as not everywhere has the geology for underground storage. High pressure tanks or cryogenic storage are considerably more expensive.

Prior to the development of North Sea gas, the gas system in the UK comprised coal gas plants located close to consumers. The gas produced was rich in hydrogen and distributed locally. We believe that the potential to generate hydrogen at small decentralised plants

located close to centres of demand should be thoroughly and urgently evaluated. Much of the gas distribution infrastructure exists and is capable of carrying hydrogen.

In a system with a very high proportion of renewables there will inevitably be many occasions when electricity generating capacity exceeds demand. There also occasions when the transmission system is unable to accept all of the renewable power available from a particular facility. This already happens and results in curtailment payments to renewable generators. It has been reported that last year over £100m of curtailment fees were paid to wind generators (New Statesman, July 2018).

In a system including substantial hydrogen production by electrolysis the periods of surplus electricity generation would be used to produce hydrogen for storage, provided that the transmission system can deliver the surplus power to the hydrogen generator. Thus, a system with high renewable capacity allied to baseload nuclear would be much more efficient. Nuclear would run continuously as baseload, renewables would be sufficient to meet peak electricity demand and when demand fell the renewable power would be directed to storage, a large part of which would be hydrogen generation. Optimisation of such a system would require very high definition temporal and geographical whole system modelling.

We assume that it will generally be cheaper to move energy as electricity than to move it as hydrogen, this supports the view that it is more effective to bring electricity to local hydrogen production facilities than to generate hydrogen centrally and distribute it to the users. Substantial changes to the electricity transmission and distribution systems would be required to ensure ability to move surplus renewable power to local hydrogen generation stations.

6.2 Electricity Pathway

We believe a purely 100% electrical pathway is impractical and not economically viable, certainly not so unless low cost, large-scale ES can be achieved. The ratio of peak to average demand for heating, referred to above, is the biggest single obstacle to a 100% electrical pathway. Furthermore, the peak flows would be such that the grid and distribution systems would require substantial reinforcement , more than if hydrogen was used to address part of the winter peak energy demand. Installation of heat pumps in all homes would be highly disruptive and expensive. Many users would be reluctant or unable to undertake this retrofit.

The scenarios modelled in National Grid’s FES 2018 all show significant continued use of gas through to 2050 and beyond. The lowest gas consumption in 2050 is modelled in the Community Renewables scenario, which represents a decentralised energy system, and does not include use of gas to produce hydrogen through steam methane reforming. This scenario is the most heavily dependent on the electricity pathway, but still assumes some limited hydrogen production by electrolysis and assumes that by 2050 gas utilisation is reduced to less than half of current levels.

The Road to Decarbonisation: Implications for Major Energy Projects28

7. System Evolution and Interdependencies

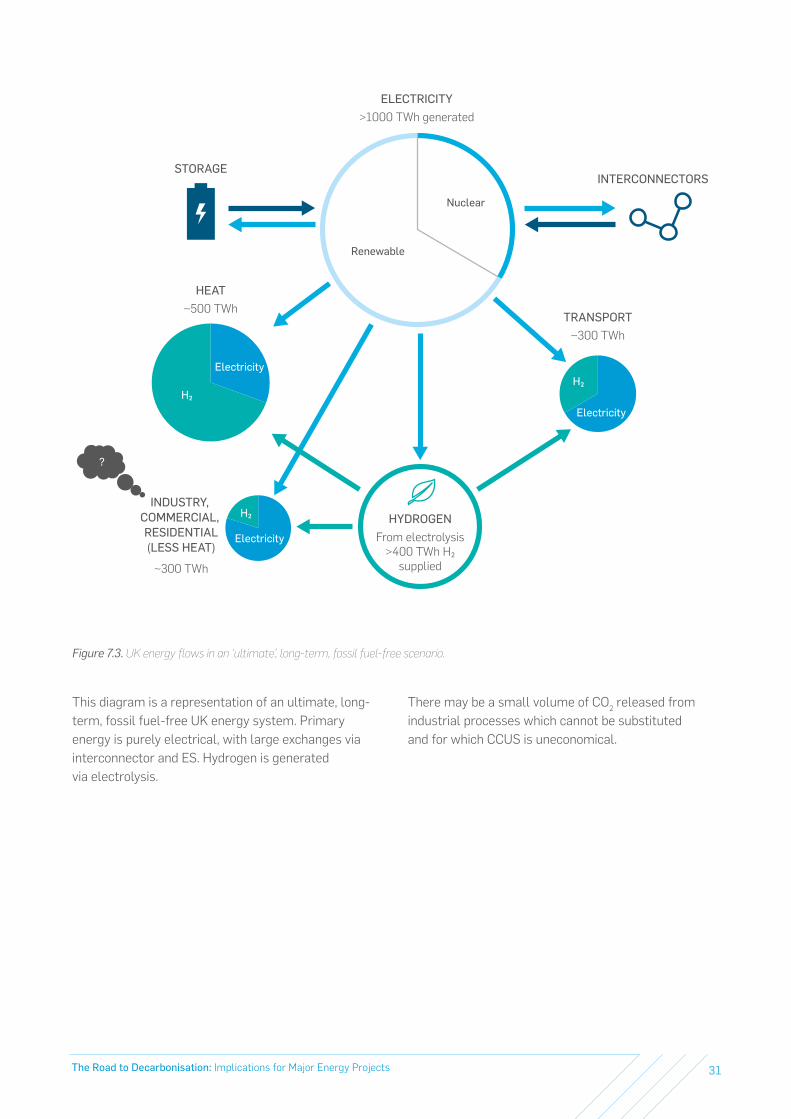

We see an ultimate energy system as described in Section 4 as one in which fossil fuel use is completely eliminated. Energy sources will be renewables and nuclear, and energy vectors will be electricity and hydrogen. The system will be much more decentralised than today with integrated smart management of generation, ES and consumption at the user, distribution and transmission levels.

It will clearly take some decades to reach this system and there will be a continuous process of transition between today’s configuration and the ultimate structure. The interdependencies between generation, heating, transportation and industry will change as the system evolves.

In our view the ultimate destination should always be uppermost in policy development and planning. The pursuit of ‘least cost’ pathways should be our objective, but the least cost pathway should not be to an intermediate destination, rather it must be judged against the achievement of the ultimate configuration.

The evolution of the system will be shaped by government policies, economics, availability of finance and by the rate at which each technology can be deployed. The Energy Research Partnership (ERP) 2016

report stated that some researchers believe that the cost of the different hydrogen production methods may converge sometime around 2030. Thus, there may be no economic advantage for steam methane reforming; even so, it may be necessary to utilise steam methane reforming and associated CCUS because it may not be possible to build sufficient electricity generation and electrolyser capacity to produce enough hydrogen to meet demand by that time.

Figures 7.1 to 7.3 are intended to demonstrate the evolutionary change described above, from the present-day UK energy system to an ultimate, long-term, fossil fuel-free system. Energy Supply and Energy Consumption are shown as scaled circles (hollow and solid respectively). These are sized across the three charts so as to demonstrate areas expected to experience major change.

The data in these charts does not sum exactly, and they are intended to highlight trends rather than present accurate values. Data has been obtained from FES 2018, Energy Consumption in the UK, 2018 (BEIS), and 2017 UK Greenhouse Gas Emissions, Provisional Figures (BEIS). Assumptions have been made to provide estimates in cases where data is not available.

The Road to Decarbonisation: Implications for Major Energy Projects28

29The Road to Decarbonisation: Implications for Major Energy Projects

This diagram represents the scale of the main supplies of energy in the UK energy system – natural gas, oil, and electricity – and how they are consumed. Energy consumption has been presented as Transport, Heat, and Industry/Commercial/Residential. The Heat Consumption circle includes all energy used as heat across the industrial, commercial and residential sectors – the Industry/Commercial/Residential Consumption circle includes the remaining energy consumption from these sectors.

138 MtCO2

Gas

Oil

Other

Electricity

NATURAL GAS

810 TWh supplied

OIL

742 TWh supplied

Gas

Oil

Electricity

Other

Nuclear

Renewable

HEAT692 TWh

ELECTRICITY302 TWh generatedSTORAGE

2.9 GW capacity

TRANSPORT657 TWh

INDUSTRY, COMMERCIAL, RESIDENTIAL (LESS HEAT)

345 TWh

124 MtCO2

105 MtCO2

INTERCONNECTORS18 TWh

Gas

Electricity

Figure 7.1. 2017 UK energy flows.

This diagram highlights how oil and gas dominate the current energy supply in the UK, and the corresponding challenge associated with decarbonising heat and transport.

Transport data includes the UK share of international aviation, but excludes international shipping.

The Road to Decarbonisation: Implications for Major Energy Projects30

H₂

GasElectricity

NATURAL GAS565 TWhsupplied

H₂From SMR

~230 TWh H₂ supplied H₂

CO2

CO2

OIL80 TWh supplied

Gas

Oil

H₂Electricity

OtherNuclear

Renewable

HEAT500 TWh

ELECTRICITY450 TWh generated

TRANSPORT320 TWh

INDUSTRY, COMMERCIAL, RESIDENTIAL (LESS HEAT)

275 TWh

40 MtCO2

20 MtCO2

STORAGE17 GW capacity

CCUS

INTERCONNECTORS47 TWh

Gas

Gas

Electricity

This diagram represents a projection of the UK energy system in 2050. Electricity and Natural Gas Supply circles have been sized based on energy supply projections for the Two Degrees Scenario in FES 2018. This diagram demonstrates the large reduction in fossil fuel dependence, the emergence of hydrogen as an energy vector, and application of CCUS to trap emissions from energy generation and hydrogen production.

Figure 7.2. 2050 UK energy flows.

The sizing of the Heat Consumption circle has been based on an assumed 25% reduction in energy demand from 2017, whilst the breakdown by energy source is an estimate. The sizing and breakdown of the Transportation Consumption circle has been based on data on electricity demand for vehicles and rail from FES 2018, plus an assumed 25% increase in energy demand for domestic aviation and shipping from 2017.

31The Road to Decarbonisation: Implications for Major Energy Projects

H₂

Electricity

Electricity

HYDROGENFrom electrolysis

>400 TWh H₂ supplied

H₂

Nuclear

Renewable

HEAT~500 TWh

ELECTRICITY>1000 TWh generated

STORAGE

TRANSPORT~300 TWh

INDUSTRY, COMMERCIAL, RESIDENTIAL (LESS HEAT)

~300 TWh

?

INTERCONNECTORS

H₂

Electricity

This diagram is a representation of an ultimate, long-term, fossil fuel-free UK energy system. Primary energy is purely electrical, with large exchanges via interconnector and ES. Hydrogen is generated via electrolysis.

There may be a small volume of CO2 released from industrial processes which cannot be substituted and for which CCUS is uneconomical.

Figure 7.3. UK energy flows in an ‘ultimate’, long-term, fossil fuel-free scenario.

The Road to Decarbonisation: Implications for Major Energy Projects32

7.1 The Role of HydrogenWe see hydrogen as an essential element of the future energy strategy, as discussed in section 6 above.

Hydrogen will act as an ES mechanism and as an energy vector.

The ERP 2016 report clearly set out many of the opportunities and issues of hydrogen and recommended further research. Government has acted on this and initiated research. We recommend that research on hydrogen production (other than by steam methane reforming) be given the highest priority. A full-scale trial of hydrogen conversion (such as proposed by the H21 Leeds Citygate Project) should be undertaken as soon as possible.

Hydrogen addresses all of the criteria we set out in section 3 of this paper. The UK has significant capabilities and development of hydrogen solutions could generate substantial export opportunities.

7.2 The Role of CCUSCCUS is seen by many as an essential element in the least cost pathway to decarbonisation. The CGS cites broad international consensus that CCUS has a vital role in reducing emissions, and outlines support that government is providing for development of CCUS. However, it does not commit to deployment of CCUS – rather it sets an aspiration to deploy CCUS at scale during the 2030s, subject to cost reduction. In their assessment of the CGS, the CCC states clearly that government should not plan to meet the 2050 target without CCUS.

The CCUS Cost Reduction Taskforce was set up to identify opportunities for cost reduction. The taskforce (and the Oxburgh report) strongly recommended immediate action to progress CCUS in the UK. The taskforce stated that CCUS can already be deployed in clusters at a competitive cost. However, the report also stated that existing cost data from proposed UK projects is limited and that it was difficult to estimate the cost reductions that might be achieved. The report identified many opportunities to reduce the cost of CCUS through learning by doing, appropriate allocation of risks and innovative funding mechanisms.

CCUS has the potential to support several important areas:

› Low-carbon generation using well proven CCGT technology fitted with CCUS.

› Production of hydrogen through steam methane reforming.

› Sequestration of CO2 emissions from industry.

› CO2 removal from the atmosphere.

The NIC has expressed doubt regarding the cost effectiveness of CCUS for capturing CCGT emissions and stated that electricity consumers should not be forced to subsidise CCUS, which may eventually be required for other purposes. This directly opposes the conclusions of the Oxburgh review.

CCUS is not essential for production of hydrogen; it may however be necessary in the short term until other (fossil fuel-free) methods of production of hydrogen are available and competitive.

› Hydrogen is essential for both energy storage and as an energy vector.

› For the ultimate fossil fuel-free system, hydrogen must be generated by methods other than steam methane reformation. UK hydrogen research should be accelerated and focussed on cost effective hydrogen production.

› The UK has significant capabilities, and hydrogen systems offer substantial export potential.

Key Observations on Hydrogen:

The Road to Decarbonisation: Implications for Major Energy Projects32

The Road to Decarbonisation: Implications for Major Energy Projects

The volume of unavoidable CO2 production from industry must be carefully assessed in order to justify the amount of CCUS needed for this sector. There may always be a small volume of industrial process-related CO2 that cannot be substituted. CCUS could offer a solution, but the economic justification may suggest that sequestration of an alternative equivalent volume of CO2 is preferable.

If CO2 removal from the atmosphere is eventually required, then CCUS offers a route to achieve this. The mechanism for funding these activities would be complex, and in any case is a decision to be made in the long term.

In our view CCUS is primarily a technology to allow and mitigate continued dependency on fossil fuels until such time as the energy system no longer requires fossil fuel inputs. It should therefore be seen as a ‘bridging technology’, which may be required in the medium term if it proves economic.

It is therefore clear that, in order to keep this option open, the potential of CCUS should be determined as soon as possible by the implementation of a pilot project. The SNC-Lavalin Atkins prepared an ‘Industrial Carbon Capture and Storage Roadmap for Scotland’ in 2016, and this or a similar project could be used as the pilot scheme.

This report is listed in Annex A.

The Road to Decarbonisation: Implications for Major Energy Projects 33

› The CCC and others appear to regard CCUS as an essential element of the carbon reduction strategy. The NIC does not agree. FES 2018 appears to show that our 2050 targets can be met without CCUS (Community Renewables scenario).

› CCUS is a mechanism to mitigate the CO2 emissions from continued fossil fuel use. As such it is a bridging technology.

› CCUS has so far not been able to demonstrate competitive cost effectiveness.

› The CCUS Cost Reduction Taskforce identified commercial and contractual approaches to reduce the cost of CCUS, but did not estimate either the current cost or the magnitude of reductions that may be achievable.

› The UK is well positioned to develop CCUS by sequestration in depleted oil and gas reservoirs. Projects predicated on re-use of existing oil and gas infrastructure

may appear attractive as they make use of existing assets and defer decommissioning costs. However, the condition of exiting assets must be well understood if substantial investment is dependent on their reuse and continued performance.

› The proposed UK development of CCUS is specific to the geological conditions found in the UK and its pre-existing infrastructure, but this is not necessarily a widely exportable model. Therefore, we do not believe that CCUS addresses our criterion of global applicability.

› The successful implementation of CCUS should not be seen as essential for adoption of the hydrogen pathway. Ultimately hydrogen may be produced by electrolysis or other methods and CCUS would become redundant.

› With conflicting advice from its expert advisors, government must determine the next steps on CCUS and publish its road map without delay. This should include a pilot scale scheme.

Key Observations on CCUS:

The Road to Decarbonisation: Implications for Major Energy Projects34

7.3 The Role of NuclearOur ultimate configuration includes a large element of renewable generation with a significant underpinning of dispatchable nuclear generation. During inevitable periods of excess supply, electricity will be directed to ES, which will include batteries, hydrogen by electrolysis, pumped hydro storage, and other mechanisms that may be developed over time.

The various reports that have been published recently take different views on the role of nuclear. The CGS clearly identifies the need to develop new nuclear and commits funding to research directed at cost reductions. It states that government will progress negotiations with developers to secure competitive prices for new nuclear projects in the current 18 GW pipeline.

In their assessment of the CGS, the CCC has expressed doubt as to the deliverability of the government’s plans for new nuclear and has recommended that contingency plans should be made for additional renewables to be contracted in the event of delay or failure of the new nuclear programme. The NIC has suggested that the current government strategy of delivery of 18 GW of new nuclear should be put on hold, and has specifically recommended that no more than one additional plant beyond Hinkley Point C should be committed before 2025.

The study by MIT suggests that to achieve deep decarbonisation beyond 2050 nuclear must be a substantial proportion of the optimal generating mix, subject to nuclear achieving target cost levels.

There is clearly a groundswell of doubt amongst UK reviewers and advisors regarding the competitiveness and delivery of the new nuclear programme. We believe that vigorous and well-directed combined efforts lead by the nuclear and civil construction sectors, supported by the entire supply chain, and allied with reform of the UK’s current nuclear project finance model can address both cost and delivery issues that contribute to such doubts.

The Nuclear Sector Deal, announced in June, set out an ambition to reduce the cost of new nuclear by 30% by 2030. The deal is focussed on actions that will impact the delivery of the currently proposed large, GW-scale plants. It also includes commitments to research advanced modular reactors and to support further developments in fusion lead by UKAEA.

SNC-Lavalin Atkins has previously proposed that, to succeed in widespread international deployment, the nuclear industry must set a challenge to deliver projects that are competitive, deliverable and affordable; we captured this in setting the challenge as:

60x30x2This represents a power cost of £60/MWh (at 2016 prices) to be delivered by 2030 at a capital cost of less than £2bn per unit.

The Nuclear Sector Deal has implicitly accepted the first two parts of the challenge by setting a goal of a 30% reduction in power cost by 2030 (30% reduction from £92.50 would yield £65/MWh). However, the current generation of large plants cannot reach the affordability goal of £2bn/unit. This can only be addressed by development of smaller nuclear plants.

The Expert Finance Working Group on Small Nuclear Reactors (EFWG) reported that technology developers they interviewed were working towards a levelized cost of electricity of between £40 and £80 per MWh and a capital cost of less than £2.5bn. It is clear that the market believes that the challenge of 60x30x2 is appropriate.

The Role of Nuclear in the Longer Term