Embed Size (px)

Citation preview

The Need for Operational Guidance on Private Participation

in the Power Sector

Based on a recommendation from the OED/OEG/OEU evaluation study: “Power for Development – A Review of the WBG’s Experience with Private Participation in the Electricity Sector”

Fernando ManibogOperations Evaluation Department (OED)

Recommendation No. 1

“The WBG should provide operational guidance to staff on when and how to promote private sector development in the electric power sector (PSDE) in the current environment of heightened macroeconomic and political risks and scant private investor interest.”

Main Evaluation Findings (and the Need for Guidance)

• IFC & MIGA achieved good project-level outcomes

• Bank results are mainly poor or mixed at country-sector level

• But results were good where country factors of performance were present

• Country specifics are important

Guidance needed but should be country-specific because:

• Power reform is complex.• Private participation in power is a work in

progress.• The evidence on the timing and sequencing

of reforms in ambiguous.• The right country, sector and contractual

conditions are required.

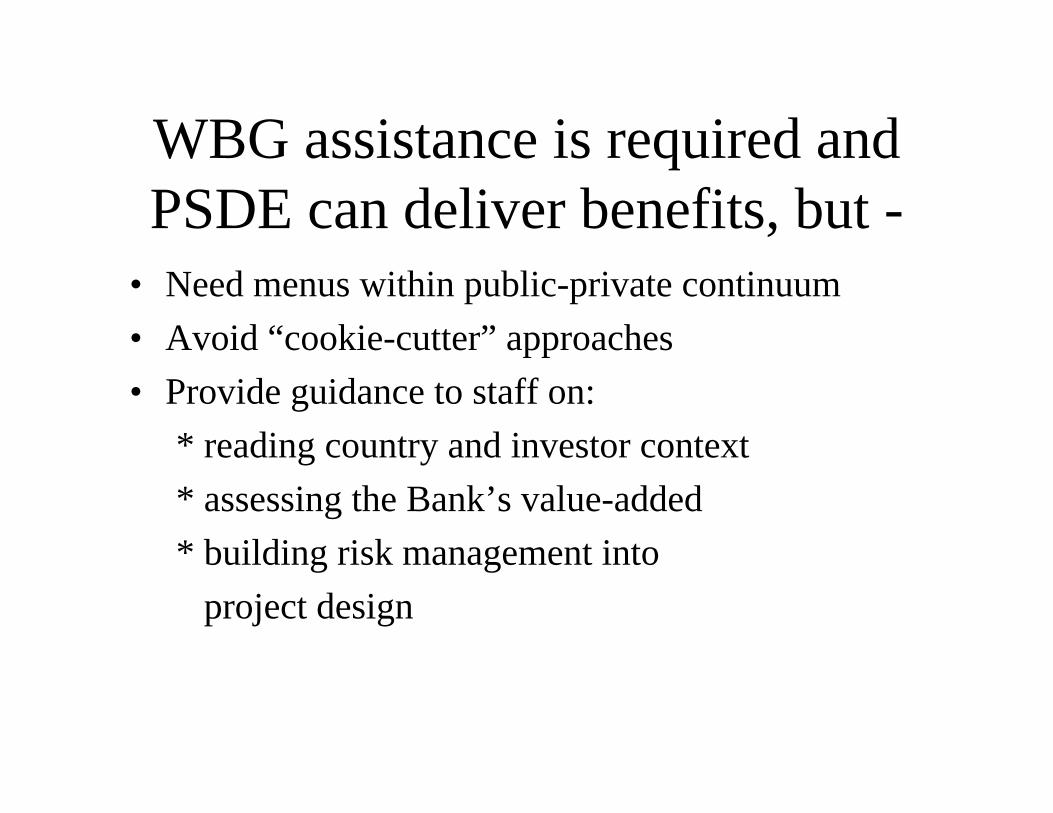

WBG assistance is required and PSDE can deliver benefits, but -

• Need menus within public-private continuum• Avoid “cookie-cutter” approaches• Provide guidance to staff on:

* reading country and investor context* assessing the Bank’s value-added* building risk management into

project design

Further Guidance Needed for Urgent Action Areas

• How to re-ignite private investor interest• How to balance public/private investments• How to sequence reforms• How to incorporate poor’s access and the

environment in power reform agenda• How to strengthen Bank, IFC and MIGA

coordination within CAS framework

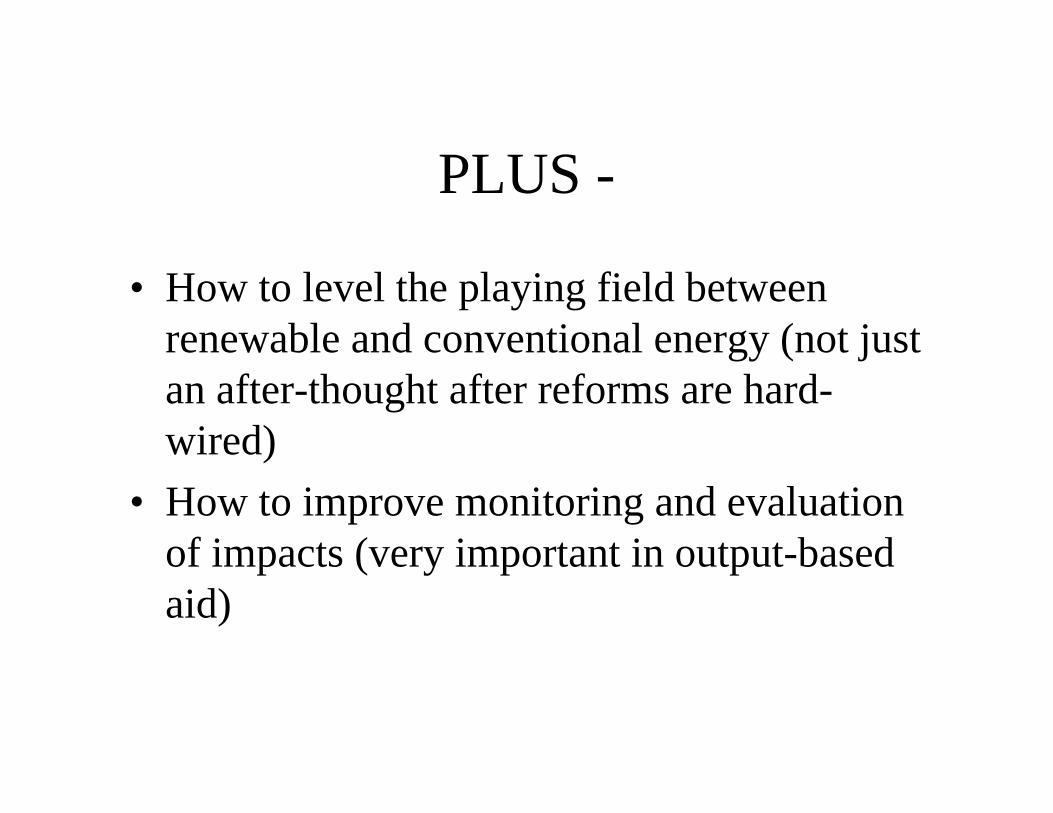

PLUS -

• How to level the playing field between renewable and conventional energy (not just an after-thought after reforms are hard-wired)

• How to improve monitoring and evaluation of impacts (very important in output-based aid)

SuccessesSuccesses

Asian examplesAsian examplesGood governanceGood governance

LAC examplesLAC examplesPrivatizationPrivatization

ECA examplesECA examplesEU accession EU accession

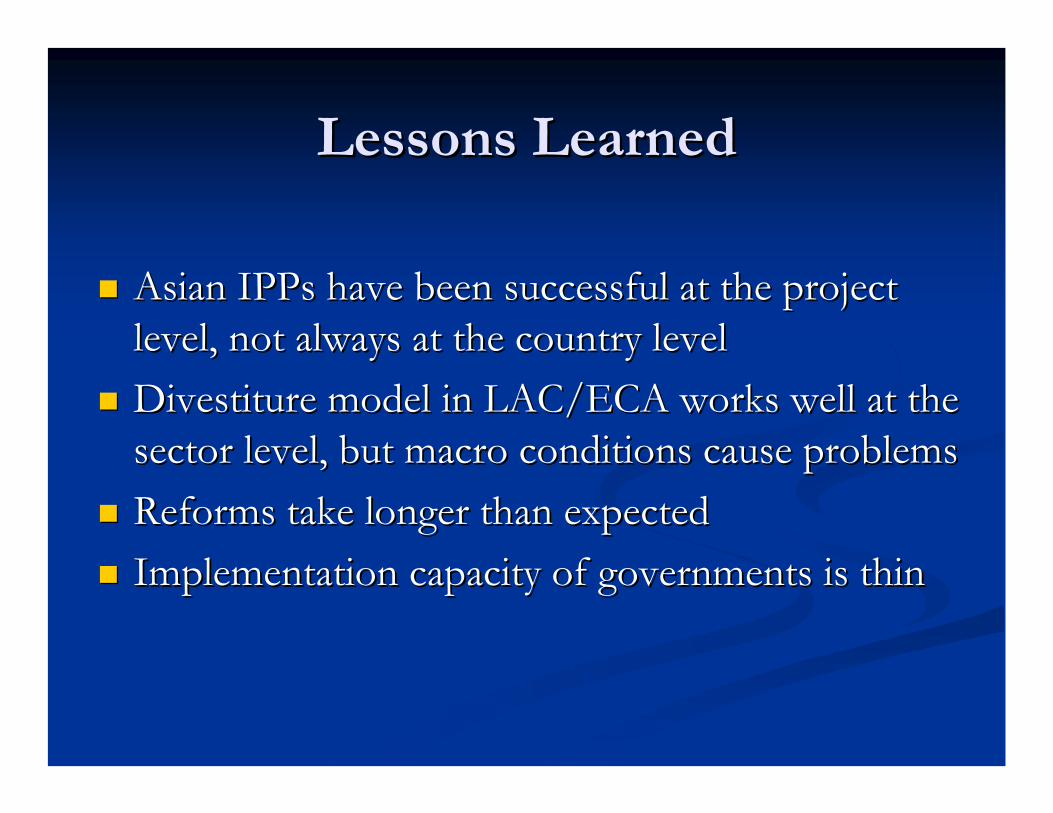

Lessons LearnedLessons Learned

Asian IPPs have been successful at the project Asian IPPs have been successful at the project level, not always at the country levellevel, not always at the country levelDivestiture model in LAC/ECA works well at the Divestiture model in LAC/ECA works well at the sector level, but macro conditions cause problemssector level, but macro conditions cause problemsReforms take longer than expectedReforms take longer than expectedImplementation capacity of governments is thinImplementation capacity of governments is thin

Public Sector RolesPublic Sector Roles

Strategic vision and macro linkagesStrategic vision and macro linkagesRoadmap for implementationRoadmap for implementationEstablishing the legal frameworkEstablishing the legal frameworkGovernance of corporate entitiesGovernance of corporate entitiesSafety net for the poorSafety net for the poorOversight regarding externalitiesOversight regarding externalities

Private Sector RolesPrivate Sector Roles

Provide energy services to meet demandProvide energy services to meet demandResponsible for dealing with market risksResponsible for dealing with market risksThe primary focus for investment/operationsThe primary focus for investment/operationsDevelop local and regional investorsDevelop local and regional investorsRisk sharing with Governments and customersRisk sharing with Governments and customers

Role of the BankRole of the Bank

Advisory Services/TA for Reform AgendaAdvisory Services/TA for Reform AgendaInstitution capacity building supportInstitution capacity building supportSALs/SACsSALs/SACs to assist with transition to assist with transition Investment support in absence of private sectorInvestment support in absence of private sectorSecond generation reforms support implementationSecond generation reforms support implementationRisk mitigation strategies to support private sectorRisk mitigation strategies to support private sector

InvestmentsInvestments

Generation Generation –– primarily private, except for hydro, primarily private, except for hydro, postpost--conflict situations, countries in transitionconflict situations, countries in transitionTransmission Transmission –– publiclypublicly--owned transmission owned transmission expected to remain in most client countriesexpected to remain in most client countriesDistribution Distribution –– Bank support if public ownership Bank support if public ownership works or is in transition, otherwise private sector works or is in transition, otherwise private sector participation expectedparticipation expected

High Risk Countries

Post-Conflict & Low income

Evolving Countries

Low to medium income

Low Risk Countries

Medium income

Flawed Legal Framework

Major Implementation problems

Pricing Problems

Payment Discipline Problems

No Independent Regulator

Evolving Legal Framework

Weak Implementation

Pricing Improvements

Improving Payment Discipline

Regulation Started

Effective Legal Framework

Quality Implementation

Reliable Pricing

Good CommercialDiscipline

Effective Regulation

Publicly OwnedCompanies

ManagementContracts Leases Concession Divestiture

1

Re-Engaging the Private Sector in Emerging Market Power

Matthew BureschDeloitte Emerging MarketsEmail: [email protected]

World Bank Energy Week 2004

March 11, 2004

Emerging Markets Group

2

OutlineOutline

Understanding the power finance cycleUnderstanding the power finance cycleCase analysis of private investmentCase analysis of private investmentEvaluating private investment success factorsEvaluating private investment success factorsPower financing priority leverage pointsPower financing priority leverage pointsGovernance and transition managementGovernance and transition managementCapital sources and risk managementCapital sources and risk managementConclusions & RecommendationsConclusions & Recommendations

Emerging Markets Group

3

Financing Required for the Power Sector In Emerging Markets 1990-2020

Cumulative Sum ($Bn)

$4,300 Bn

$3,800 Bn

0.0

50.0

100.0

150.0

200.0

250.0

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

Private Investmentin the Power SectorT

otal

Pow

er I

nves

tmen

t ($

Bn

)

Low InvestmentDemand Scenario (2%)

High Investment DemandScenario (3%)Gap covered by public financing

self-financing, donor funding, and rationing

Source: World Bank, IEA, Deloitte Touche Tohmatsu Emerging Markets Group

Historic FutureEmerging Markets Group

4

Power Market Policies Exploring the Link to Private Capital Flows

Source: World Bank, IFS StatisticsSource: World Bank PPI Database, Global Development Finance 2003, IFS Statistics

N e t P r i v a t e C a p i t a l F l o w s t o I n f r a s t r u c t u r e i n E m e r g i n g M a r k e t s

( 1 9 9 0 - 2 0 0 2 )

0

2 0

4 0

6 0

8 0

1 0 0

1 2 0

1 4 019

80

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

$ B n

P o w e r

T o t a l I n f r a s t r u c t u r eI n v e s t m e n t

N e t P r i v a t e C a p i t a l F l o w s T o E m e r g i n g M a r k e t s ( 1 9 9 0 - 2 0 0 3 )

- 5 00

5 01 0 01 5 02 0 02 5 03 0 03 5 0

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

$ B nF o r e i g n D i r e c tI n v e s t m e n tC a p i t a l M a r k e t F l o w s

T o t a l

Emerging Markets Group

5

Successful Private Power Financing Case Study 20 successful cases taken out of sample of 116 in developing countries

EAP ECA LAC MENA SA Sub-Sahara

Total

Concession Pamir Power (Tajikistan)

Edenor (Argentina)

Casablanca Lydec

(Morocco)

SEEG (Gabon)

4

IPP Phu My 2.2 (Vietnam) Shandong

Power (China)

Maritza East III (Bulgaria)

Termobahia (Brazil)

Jorf Lasfar (Morocco)

Lal Pir (Pakistan)

Haripur (Bangladesh)

Azito Power (Cote d'Ivoire) Songo-Songo

(Tanzania)

9

Divestiture Chisinau/ Centru/Sud (Moldova)

Luz del Sur (Peru)

North Delhi (India)

3

Utility Electrification

Initiative

Meralco DAEP (Philippines) -

Disco Case

Light (Brazil) -

Disco Case

Grameen Shakti

(Bangladesh)-Genco Case

Phambili Nombane

(South Africa) - Disco Case

4

Total 3 3 4 2 4 4 20old-faced projects denote greenfieldnshaded projects denote projects of existing assets

BU

6

Private Power Cases Key Success FactorsPrivate Power Cases Key Success Factors

Political leadership to drive through sector reforms and projectPolitical leadership to drive through sector reforms and projectagreements;agreements;

Good and tested project design balancing the risks and returns Good and tested project design balancing the risks and returns to the Government and private sponsor/lender;to the Government and private sponsor/lender;

Good and tested market design, most success cases in Good and tested market design, most success cases in vertically integrated and single buyer markets;vertically integrated and single buyer markets;

Domestic capital role substantial from strategic and banking Domestic capital role substantial from strategic and banking sector sources and potential to generate selfsector sources and potential to generate self--financing;financing;

Greenfield generation: (a) MDB support, (b) constrained power Greenfield generation: (a) MDB support, (b) constrained power expansion;expansion;

Existing distribution: (a) prior improved Existing distribution: (a) prior improved collections & tariff collections & tariff levels,levels, (b) public participation.(b) public participation.

Emerging Markets Group

7

Private Power FinancingKey Leverage Points

Legal / regulatory frameworkversus contractsGovernanceRegulatoryCertainty

RiskAllocation

IncentiveMechanisms

TransitionMechanism

Public vs PrivateEquity vs Debt

PerformanceEnvironmental

Social

Transition to Cost RecoveryAnd Competitive Markets

Emerging Markets Group

8

Good Governance is Vital, Yet Requires Better Development Teamwork

RegulatoryCommission

Government

VoiceCompact

Political Accountability

Legal – RegulatoryFramework

Independent & Contractual Regulatory

Models

Domestic/ForeignCapital Markets

Worker Stakeholder ModelsPower MarketCompetitionModels.

ConsumerStakeholderAdvocacy& Civil Society

Models

Workers

Domestic/ForeignCapital Markets

Power IndustryG/T/D

Power IndustryG/T/D

CustomerCustomerClient Power

Regulator and Rating AgenciesEmerging Markets Group

9

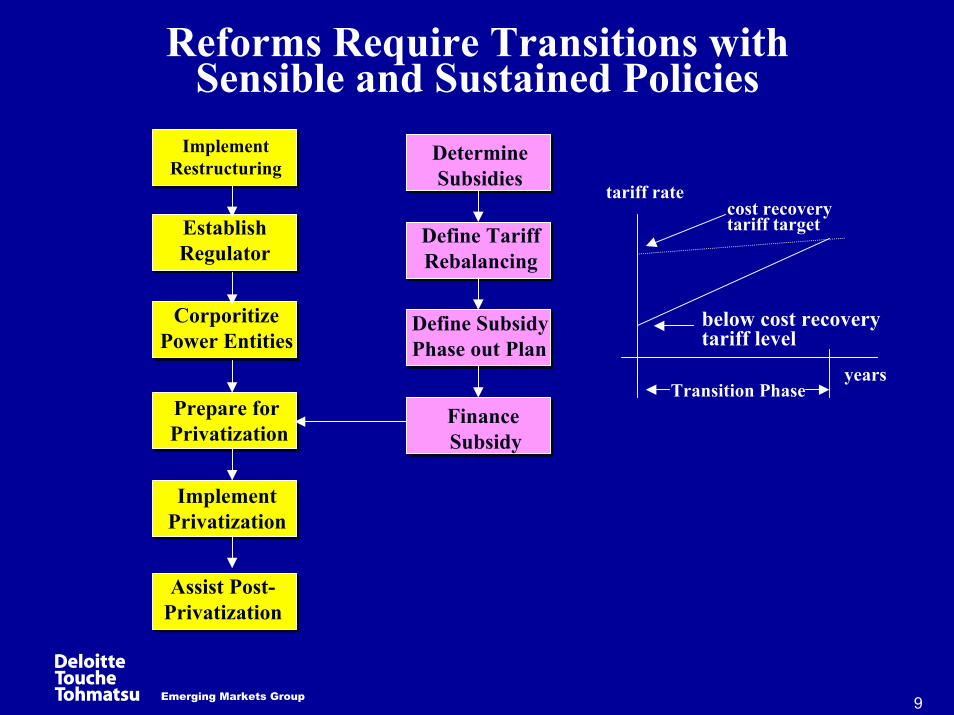

Reforms Require Transitions with Sensible and Sustained Policies

ImplementRestructuring

EstablishRegulator

DetermineSubsidies

Define TariffRebalancing

Define SubsidyPhase out Plan

CorporitizePower Entities

ImplementPrivatization

Prepare for Privatization

Assist Post-Privatization

Finance Subsidy

below cost recoverytariff level

cost recovery tariff target

tariff rate

yearsTransition Phase

Emerging Markets Group

1017

ImplementRestructuring

CorporatizePower Entities

EstablishRegulator

Prepare for Privatization

ImplementPrivatization

Assist Post-Privatization

Power Sector Preparations for Enhanced PSP

CommercializeUtility

Raise Tariffs

RationalizeStaffing

• Cut utility from routinegovernment budget support;

• Establish clear accounting;• Tariff rationalization;• Separate business units by

function;• Establish transparent transfer

pricing;• Institute clear audit

procedures;• Compile clear inventory of

assets and debts;• Professionalize billing,

metering, and collections.

Emerging Markets Group

11

Country risk explains 1.4% of PPI project risk structure selection

The Private Sector Needs Better Public Sector Oversight

Cou

ntry

Ris

k R

atin

g

0

10

20

30

40

50

60

70

80

0 1 2 3 4 5

Somalia

S.Korea

LowerRisk

HigherRisk

(1992(1992--2002)2002)

*Sources: PPI Database; Institutional Investor 1990-2003 Country Risk Ratings. The higher the rating, the lower the country risk as defined by default potential. One dot can correspond to multiple projects.

Mgmt Contract Concession IPP Divestiture

Source: World Bank, Deloitte Touche Tohmatsu Emerging Markets Group

Emerging Markets Group

12

Define Markets to Match the Risks and Returns

Level of CompetitionNone Intermediate High

Wholesale

Retail

Vertically Integrated

MBMSWholesale

Competition

MBMSWholesale

Competition

Single BuyerIPP

MBMSRetail

Competition

MBMSRetail

Competition

Leve

l of P

ower

Sec

tor O

pene

d to

Com

petit

ion

Level of Market Liberalization

Gencoentry

None

GabonSouth AfricaTajikistan

BangladeshBulgariaChinaCote d’IvoireIndiaMoroccoPakistanTanzaniaVietnam

ArgentinaBrazilMoldovaPeruPhilippines

Expanding Competition

High

Low

Emerging Markets Group

13

Investment Type Lower Income

Lower Middle Income

Upper Middle Income

Generation (greenfield) PF MaxG / C PF MajG / C PF MinG / C / DTranmission (existing) MC/SO MC/SO C/DDistribution (existing) MC / L / HST MC / L / C / LST C / DPower Poverty (expansion) UI / NGO UI / NGO UI

Define Financing Structures to Match Risks and Returns

SO = State Ownership Retained UI = Utility InitiativeMC = Management Contract NGO - Non-Governmental OrganizationL = Lease / AffermageC = Concession Max G= Max Guarantees RequiredPF = Project Finance Maj G= Major Guarantees RequiredD= Divestiture Min G= Minimunm or No Guarantees Require

Legend

14

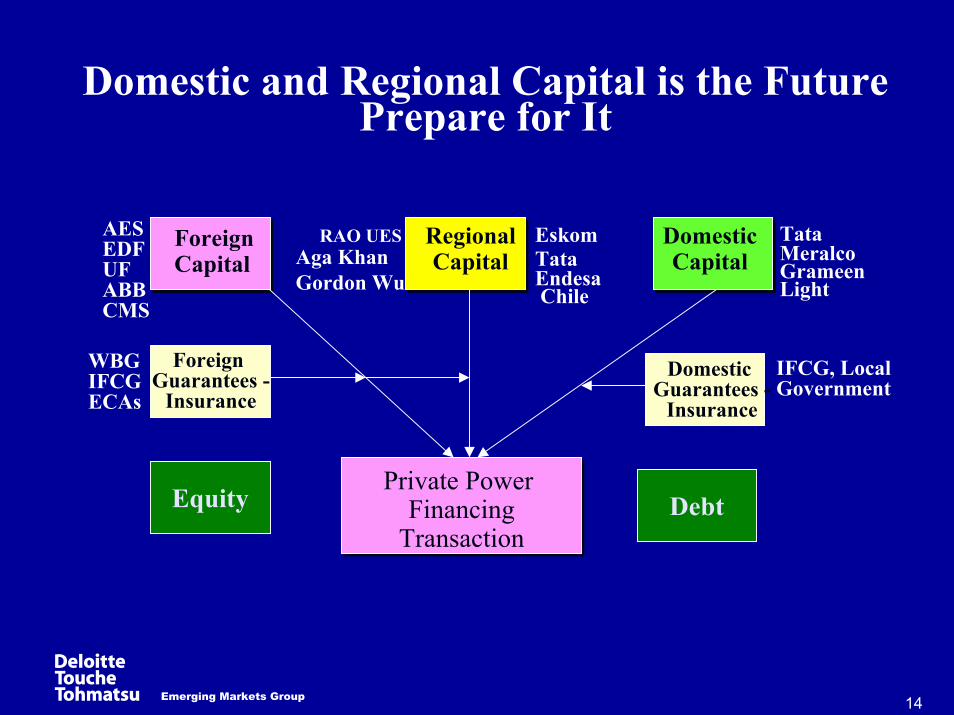

Domestic and Regional Capital is the Future Prepare for It

ForeignCapital

RegionalCapital

DomesticCapital

Foreign Guarantees -

Insurance

AESEDFUFABBCMS

RAO UESAga KhanGordon Wu

EskomTataEndesa Chile

Private Power Financing

Transaction

WBGIFCGECAs

Domestic Guarantees -

Insurance

TataMeralcoGrameenLight

IFCG, LocalGovernment

Equity Debt

Emerging Markets Group

15

Domestic Capital Mobilization Strategies Need to Reflect the Market Evolution

Progress Ranking inMobilizingContractualSavings

Chile

Vietnam

MoldovaTanzania

Tajikistan

India ArgentinaThailandIndonesia

Represent Case Study Countries*Domestic Capital % of GDP = Corp Bond Market %/GDP + Stock Market Cap %/GDP + Domestic Private Bank Credit %/GDP

Deloitte Emerging Markets Group

Domestic Capital % of GDP*

Bulgaria

Pakistan

Peru

200% +100%0%3

2

1

0

S.AfricaChinaBrazil Morocco

Bangladesh

Russia

I. Coast

PhilippinesMalaysia

16

ConclusionsConclusions

The WB ~$The WB ~$2B/yr2B/yr and MDB ~$and MDB ~$4B/yr4B/yr financing can only financing can only leverage maximum about $20 leverage maximum about $20 -- $30B/yr$30B/yr in private power in private power capital, which falls short of need;capital, which falls short of need;OptimizingOptimizing MDB MDB project financing leverage to the above project financing leverage to the above levels can be achieved bylevels can be achieved by better coverage in targeted risks better coverage in targeted risks and by process improvements; and by process improvements; Project financial engineering alone willProject financial engineering alone will likely not be able to likely not be able to leverage most of the needed private investment; the MDBs leverage most of the needed private investment; the MDBs have at their disposal have at their disposal mechanismsmechanisms that could potentially that could potentially achieve achieve greater private capitalgreater private capital leverage by encouraging the leverage by encouraging the necessary legal, regulatory, and governance framework for necessary legal, regulatory, and governance framework for private investment in power;private investment in power;Performance of capital invested needs to improve by Performance of capital invested needs to improve by requiring greater government accountability and rewarding requiring greater government accountability and rewarding success based on outputs.success based on outputs.

Emerging Markets Group

17

Recommendations: NearRecommendations: Near--TermTerm

Address key risks of concern to investors/lenders: (a) currency Address key risks of concern to investors/lenders: (a) currency devaluation risk and (b) legal/regulatory/contractual risk; devaluation risk and (b) legal/regulatory/contractual risk;

Enhance flexibility and speed of MDB / ECA guarantee Enhance flexibility and speed of MDB / ECA guarantee implementation process and integrate into sector loans; implementation process and integrate into sector loans;

Support Support incentiveincentive--based, cost of service tariffbased, cost of service tariff regulatory regulatory framework that better shields framework that better shields private capitalprivate capital from political from political interference,interference, i.e., regulation by contract and multii.e., regulation by contract and multi--year tariffs; year tariffs;

Design power markets and projects in a way that better accounts Design power markets and projects in a way that better accounts for country and sector risks and for country and sector risks and matches private investors’ risks matches private investors’ risks with real potential returns;with real potential returns;

Where little to no private investment is feasible, separate Where little to no private investment is feasible, separate management from capital investments and rely on management from capital investments and rely on affermage/leases or management contracts and on “performance affermage/leases or management contracts and on “performance improvement” loans to enhance utility commercialization; improvement” loans to enhance utility commercialization;

Establish a more effective dialogue with the private sector, e.gEstablish a more effective dialogue with the private sector, e.g., ., obtain industry input more than ad hoc company input.obtain industry input more than ad hoc company input.

Emerging Markets Group

18

Recommendations: NearRecommendations: Near--TermTermContinuedContinued

In less developed countries:In less developed countries:Support expanded domestic and regional private capital Support expanded domestic and regional private capital participation primarily through incentivizing strategic participation primarily through incentivizing strategic investors;investors;With generation, continue developing IPP project financed With generation, continue developing IPP project financed transactions under a BOT/BOO or a concession framework transactions under a BOT/BOO or a concession framework (with 3 cautions);(with 3 cautions);With distribution, separate management investment from With distribution, separate management investment from capital investments and promote affermage/leases or capital investments and promote affermage/leases or concessions as publicconcessions as public--private partnerships. private partnerships.

In more developed countries:In more developed countries:Promote expanded domestic capital mobilization through Promote expanded domestic capital mobilization through domestic banks and establish financial intermediaries to domestic banks and establish financial intermediaries to channel domestic savings into infrastructure;channel domestic savings into infrastructure;With generation, promote IPPs in markets that continue to With generation, promote IPPs in markets that continue to have the single buyer power market (with 3 cautions) and shift have the single buyer power market (with 3 cautions) and shift to generation divestitures in established competitive markets; to generation divestitures in established competitive markets; With distribution, promote concessions and divestitures that With distribution, promote concessions and divestitures that incentivize private investors to make both operational and incentivize private investors to make both operational and capital investments.capital investments.

Emerging Markets Group

19

Recommendations: LongerRecommendations: Longer--TermTerm

Explore building interdisciplinary and cross sectoral project Explore building interdisciplinary and cross sectoral project teams in the areas of teams in the areas of energy, governanceenergy, governance, , financial sector,financial sector, SME SME development, development, social development, andsocial development, and investment promotion.investment promotion.Encourage collaboration between financial and power sector Encourage collaboration between financial and power sector experts to promote policies that mobilize an increasing proportiexperts to promote policies that mobilize an increasing proportion on of power infrastructure financing from domestic markets using of power infrastructure financing from domestic markets using e.g., loan syndications and securitization/pooling structures;e.g., loan syndications and securitization/pooling structures;Strengthen good governance at the national, sectoral, and Strengthen good governance at the national, sectoral, and corporate levels by focusing on rules and restraints, competitivcorporate levels by focusing on rules and restraints, competitive e pressure, and voice and partnership dimensions; engage in betterpressure, and voice and partnership dimensions; engage in bettercross sectoral development teamwork at the country level; cross sectoral development teamwork at the country level; Integrate a better understanding of the necessary macroIntegrate a better understanding of the necessary macro--economic conditions needed to support private capital flows in economic conditions needed to support private capital flows in the power sector to engage in better market timing, credit the power sector to engage in better market timing, credit enhancement, and investment promotion; enhancement, and investment promotion; Promote power sector utility planning in a way that minimizes thPromote power sector utility planning in a way that minimizes the e excesses that are a result of poor governance and undue excesses that are a result of poor governance and undue influence by vested interests; influence by vested interests; Strengthen international arbitration conventions to provide moreStrengthen international arbitration conventions to provide moreeffective and timely recourse in the case of disputes;effective and timely recourse in the case of disputes;Encourage better facilitation of government agencies to reduce Encourage better facilitation of government agencies to reduce the costs and time required to develop private investments. the costs and time required to develop private investments.

Emerging Markets Group