Embed Size (px)

Citation preview

The Institute of Chartered Accountants of India

CIRC Newsletter July 2018

(Set up by an Act of Parliament)

INTEGRITY

OBJECTIVITY

CONFIDENTIALITY

PROFESSIONAL BEHAVOUR

PROFESSIONAL COMPETENCE

The 39th Regional Conference

of CIRC of ICAI will be

organised on 18th and 19th

August 2018 at Ghaziabad.

As this is the. main event of

CIRC, we would like to invite

you to kindly attend the same

and request you to kindly block

your dates for the event

The detailed circular and

information

is uploaded at

www.cirrc-icai.org

39th

Regional Conference

of CIRC

PRAKALP - 2018 - BEGINNING OF NEW ERAPRAKALP - 2018 - BEGINNING OF NEW ERA

CIRC Newsletter www.circ-icai.org 02July 2018

Respected Professional Colleagues,

"To accomplish great

things, we must not

only act, but also

dream; not only plan,

but also believe." -

Anatole France

G r e e t i n g ! I t i s

undoubtedly a great

honour for me to be

blessed with a unique opportunity of serving the

members and the students of CIRC of ICAI.

Friends, besides lending our support in the core

area of our competence, there is a need for the

CA fraternity to get more and more associated

with the society and play a more active part in the

field of social service. Having got the best deal

from the society, we need to reciprocate and do

something substantial for it in return. There is so

much work that needs to be done urgently at the

grassroots level. This years, on CA day many

such social services activities were planned at

Branch level and at the same time at Regional

level like blood donation and eye donation

camps, Swachh Bharat Abhiyan by cleaning &

doing rallies, tree plantations etc.

In addition to our goals and commitment to drive

members value, I focused on playing a great role

as a responsible citizen. We continue to

contribute towards initiatives that drive societal

change in the communities where we operate,

while ensuring that our professional values at

high level.

I frequently visit our branch campuses, and

interact with members at all levels. I am glad to

notice a renewed sense of vigor and energy in

whole CIRC region. Members are at the heart of

our successes and potential, and I would like to

gratefully acknowledge their commitment and

contribution.

As rightly said by our Hon'ble President, ICAI

that within ICAI too, governance matters are

always our top priority, and technology is the

best way to manage, resolve and dealing with

the issues of a large group like our membership

and students. To effectively manage the

education & training and other professional

requirements of our huge membership and other

stakeholders, ICAI has about 70 Committees,

Groups and Departments that work thereat. If

you have any query, concerns or grievance from

the Institute, kindly use the platform of e-

Sahaayataa (https://help.icai.org/) and share

your concerns. Through this, you can reach the

appropriate function of the Institute and this will

be addressed within the specified deadline. You

will receive the solution/suggestion and way-

forward. Since its launch, this platform has

already resolved 3,79,642 references, and it is

receiving appreciations from users, mainly

members and students. As informed earlier,

system is now available on the ICAI Now mobile

app and accessed by our members using this

platform.

You will be happy to know that a ' Help Desk has

been created and hosted on the website of CIRC

to respond to day to- day queries of our

members. Our members can now write and post

their queries anytime visiting the site circ-icai.org

and a response will be sent to them shortest

number of working days. I am sure that this will

put an end to our members' long-felt requirement

for a platform where they could resolve their

queries. I will really wait for your feedback in this

From the Desk of Chairman...CA. Gyan Chandra Misra

Chairman, CIRC of ICAI &Chief Editor CIRC Newsletter

CIRC Newsletter www.circ-icai.org 03July 2018

regard, as this will help us in managing, updating

and strengthening this system. This step is

actually an addition to the initiative of providing

mobile numbers which are already in operation

u n d e r t h e l i n k h t t p : / / c i r c -

icai.org/page.php?id=13 on the CIRC website.

Also, in order that CIRC members abroad are

able to receive various important periodical

communications from the Institute in time, they

need to update their e-mail addresses with the

institute. A facility has been created for

members, inter alia, to update their e-mail

profile, addresses and other important

p a r t i c u l a r s t h r o u g h t h e l i n k ,

https://appforms.icai.org/memberAddressUpda

te/. I request all our members abroad to use this

facility to update their addresses so as to

facilitate smooth communication.

May I take this opportunity to request you all to

share your thoughts, expertise and areas in

which you specialise including the areas of

concern by writing articles for the CIRC

Newsletter which is circulated to all the members

who are settled in abroad also! Members who

are settled abroad could share their experiences

in that particular country including the

opportunities available to Indian members and

also what needs to be done if one is looking for

opportunity in that country. Similarly, members in

industry could share their experience of that

industry, issues concerning that industry and

also the opportunities for members. These

initiatives could in my opinion go a long way in

making the chartered accountant fraternity a

closely knit family where each member cares for

others and therefore shares his or her ideas with

them. The e-newsletter is also available on the

website. I am sure this initiative will bring all our

members settled abroad closer to our hearts

despite being far away

The rainy season has knocked the door. May the

season bring in lots and lots of good cheer and

prosperity for you and your family ! May love of

people for people grow in such trying times as

these! May humanity emerge a winner.

Dear friends, there is much more to do and many

more steps to take in our resolve to be the best

and I look forward to receiving your guidance

and help in achieving this cherished objective.

Before I conclude, I would also like to thank all

members & students– for their trust and support.

I extend my very warm greetings and good

wishes to you and to your near and dear ones.

With warm regards,

"Do not go where the path may lead; go

instead where there is no path and leave a

trail." - Ralph Waldo Emerson

From the Desk of Chairman...

(CA. Gyan Chandra Misra)Chairman (CIRC of ICAI)M.Com, FCA, ACSMobile No. : 9810816012Email : [email protected]

CIRC Newsletter www.circ-icai.org 04July 2018

Respected Professional Colleagues,

“ Y o u m a y b e

disappointed if you

fail, but you are

doomed if you don't

try".

The time when you

would be receiving

this epistle It would

be the end of a very

busy week where we have had many

programs been organized on the occasion of

CA day throughout the entire Region. If you

have attended, then thank you very much

because it takes time and commitment to do

so and we appreciate the support.

I can look back with satisfaction and pride at

the accomplishments of the last four months

since my taking charge as Vice Chairman

CIRC. I must acknowledge this was possible

only with your continued support and the

guidance of our managing committee

members. I am happy that I could perform

this formidable task of leading our Central

Region into a exciting era.

I was very well aware of the problems and

issues being faced by our members and our

branches. I decided to take them one at a

time and with the firm conviction: "The best

preparation for tomorrow is doing your best

today".

We had recognized that Innovation should

be our key strategy in this age of

technological evolution and services

revolution. To reflect this need of changing

times, we had chosen the theme as

"Empowerment through innovation". It has

been our constant endeavor to ensure that

our theme was translated from Vision to

Action for the overall benefit of our members

and students. We have conducted

innovative programs and you have

responded magnanimously through your

active participation. During the last few

months we had variety of activities consisting

of Study Circle Meetings, Seminars,

Workshops, Conferences, In-house Training

Programs etc. We had a host of eminent

speakers sharing their experience with us.

The challenges have been many but every

challenge has been an valuable learning

experience. I am delighted to have been a

part of the prestigious CIRC of ICAI. I shall

fondly cherish these wonderful memories of

our association. I have always worked with

the motto: "The difference between ordinary

and extraordinary is that little extra" There

are innumerable members and well wishers

who have contributed their mite in the service

of members. We are on the crossroads now;

the decisions we take now will determine

where we are headed. It's time to introspect

and look at our mindsets and perception. We

need to develop new paradigms of thinking

of our competencies and skills.

On the one hand we face a prosperous future

as a country with a growing economy and the

aspirations of a billion Indians unleashed

upon the world. On the other we see massive

From the Desk of Vice Chairman...(CA.Rohit Ruwatia Agarwal)Vice Chairman, CIRC of ICAI& Editor CIRC Newsletter

CIRC Newsletter www.circ-icai.org 05July 2018

i n e q u i t i e s , s h o r t f a l l s i n

education/health/infrastructure, delivery of

justice and various other ills moving at a

similar pace. In such a scenario, the need for

a stronger, more robust and ethically driven

Chartered Accountancy profession in India

cannot be over emphasised.

We introspected and identified the various

challenges that we collectively face as a

profession today. But there are many unique

things that our profession does have. There

are three in particular, those related to the

Chartered Accountancy profession in the

country, that I wish to focus on: 1. Adequate

quality of Chartered Accountancy education

and infrastructure; 2. Relevant skills training

to meet the ever-changing demands of the

modern world; 3. Strong entry point and

continuous assessment mechanisms to

ensure the continuous growth and

improvement of the profession.

It is imperative that we learn how to access

information in electronic form. Our theme

"Empowerment through Innovation" is most

relevant now as we need to become

enlightened about these exciting concepts

and prospects which, will chart our roadmap

for the future. Our mantra for survival and

growth is "value addition" in whatever we do.

“When it comes to the future, there are three

kinds of people: those who let it happen,

those who make it happen, and those who

wonder what happened.”

- John M. Richardson

Mobile: 9571799999Email : [email protected]

CA.Rohit Ruwatia AgarwalVice-Chairman,CIRC of ICAI

CIRC Newsletter www.circ-icai.org 06July 2018

Respected Esteemed Profess iona l

Colleagues,

At the outset, let me

first congratulate you

on the 70th Chartered

Accountant Day. I

would like to thank all

of you for making the

CA day celebrations so

great. As I look around,

one thing that strikes

me most forcefully is

the fact that there has

been a sea change in the way that accountants

all over the world are looking at their profession

and the way they look at things in general. For all

these years, accountants are primarily

concerned with their role as auditors and

therefore, largely a post mortem of the financial

affairs of a company. The paradigm shift in

accountancy has resulted in a complete reversal

of focus. Review of financial statements must

now be done in such a way that short term

corrections can be made in order that the

stakeholders of the corporate may benefit

immediately from such reviews through focused

management action. I think our members also

need to inculcate this change in focus and

perspective. It is important to look forward and

not to look back.

The business entities are required to furnish

detailed disclosures not only to ensure the

continuous health of the market but also to regain

investors' confidence. Inevitable, the largest role

in this process is that of the auditors. I need not

emphasize that the faith of hundreds of

thousands of investors in the capital market rests

solely on the quality of engagements which our

members undertake and perform. It is good to

see the move of Government bodies to increase

our professional opportunities. However, the

corollary to this increase is something that

should be uppermost in the minds of our

members.

While on the subject, let me also add that our

clients also have become more conscious of the

services rendered by our members and they

expect increasing amounts of value addition in

services rendered. It is not enough to be able to

resolve a client's tax problems for a particular

year. It is now necessary to see that books are

maintained in such a manner that such problems

do not arise in future. Engagements should not

be seen as short term and engagements should

not be seen as ends in themselves. The auditor's

larger engagement is with the society and as an

upholder of values which only he, in today's

world can repeatedly endorsed. Thereby is

derived respect which all of us seek. Therefore, it

is becoming increasingly necessary for all of us

and our profession to open ourselves to the world

and to work towards global acceptance of our

profession. This is obviously a task that needs to

be pursued over the long term but every step

taken carries with it the promise of the future.

Friends, I am open to suggestions from all our

members, therefore, please feel free to give your

valuable suggestions, come forward and join

hands for the progress and prosperity of the

profession. Looking for your support and

cooperation,

With warm regards,

(CA. Pramod Kumar Boob)Secretary, CIRC of ICAI

From the Desk of Secretary...

With warm regards,CA. Pramod Kumar BoobMobile: 9829015993Email: , [email protected]

CIRC Newsletter www.circ-icai.org 07July 2018

Pg. 02 - 03

Pg. 04 - 05

From the Desk of Chairman

From the Desk of Vice Chairman

Pg. 06 From the Desk of Secretary

Expressions

Compliance Pg. 08 - 10

Pg. 11 - 13

Pg. 14 - 21

"Compliance Check"- July 18. By: CA. Harsha Ramani

Papers

Announcements

Events

Pg. 22 - 28

Pg. 41 - 52

Editorial Board

New LandlineNumbers of KanpurOffice

Pg. 58

Pg. 53 - 57

Legal

Pg. 29 - 40

Updates in relation to Recent Verditcs on Direct Taxes. By: CA. Arjit Agarwal

Updates in relation to Recent Verditcs on Direct Taxes. By: CA. Arjit Agarwal

JULY 2018IN THIS ISSUE...

Goods & Services Tax, Tax Deducted at Source. By- CA. Vikas Golechha

Time of Supply with Examples. By- CA. Vikas Modi

CIRC Newsletter www.circ-icai.org 08July 2018

There are various

s ta tu tes , by laws ,

gu ide l ines , ru les ,

regulations and norms

prescribed by the

various Regulating

A u t h o r i t i e s l i k e

Ministry of Corporate

Affairs, Securities and

Exchange Board of

India and Reserve

Bank of India etc. They are required to be

complied with in true spirit and purpose, so that

all stakeholders derive the benefit due to them

and also avoid the unwarranted legal actions

from regulatory authorities. So it's a small effort

for bringing the compliance dates together for

this newsletter. This compliance calendar

summarizes important tax (direct & indirect both)

reporting and filing due data with forms

specification for individuals, businesses and

other taxpayers for the month of July, 2018.

Hope the reader will find the same useful."

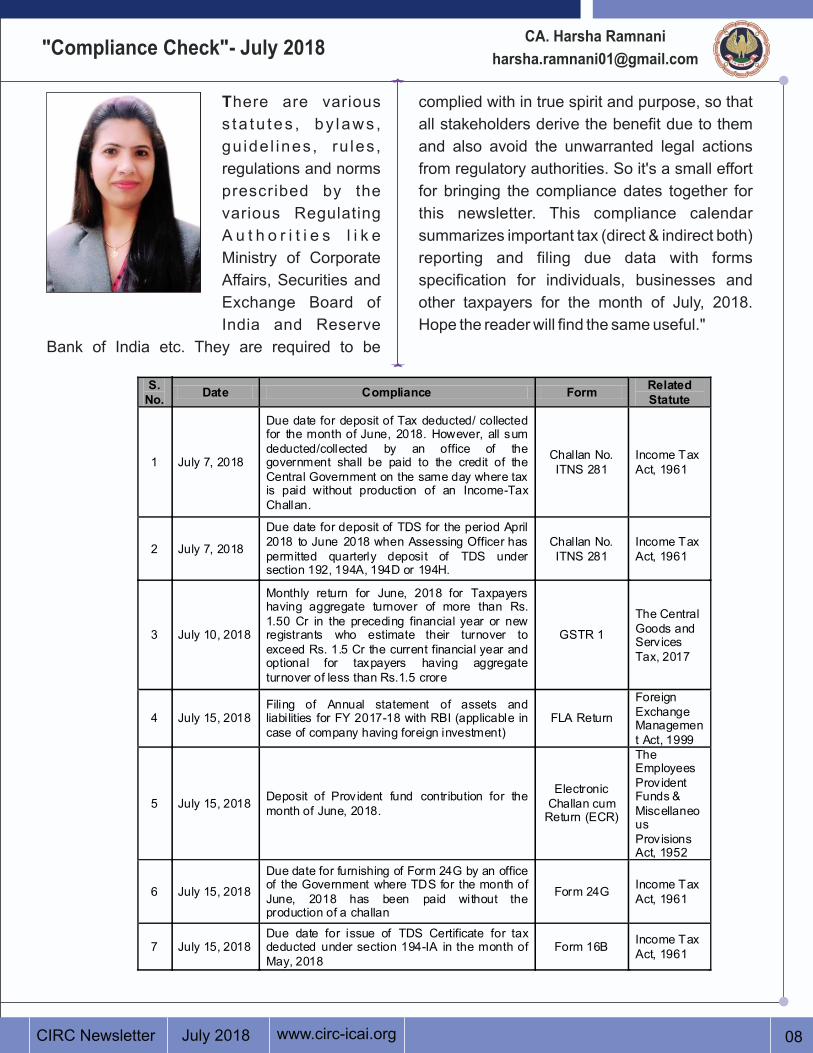

"Compliance Check"- July 2018CA. Harsha Ramnani

S. No.

Date Compliance Form Related Statute

1 July 7, 2018

Due date for deposit of Tax deducted/ collected for the month of June, 2018. However, all sum deducted/collected by an office of the government shall be paid to the credit of the Central Government on the same day where tax is paid without production of an Income-Tax Challan.

Challan No. ITNS 281

Income Tax Act, 1961

2 July 7, 2018

Due date for deposit of TDS for the period April 2018 to June 2018 when Assessing Officer has permitted quarterly deposit of TDS under section 192, 194A, 194D or 194H.

Challan No. ITNS 281

Income Tax Act, 1961

3 July 10, 2018

Monthly return for June, 2018 for Taxpayers having aggregate turnover of more than Rs. 1.50 Cr in the preceding financial year or new registrants who estimate their turnover to exceed Rs. 1.5 Cr the current financial year and optional for taxpayers having aggregate turnover of less than Rs.1.5 crore

GSTR 1

The Central Goods and Services Tax, 2017

4 July 15, 2018 Filing of Annual statement of assets and liabilities for FY 2017-18 with RBI (applicable in case of company having foreign investment)

FLA Return

Foreign Exchange Management Act, 1999

5 July 15, 2018 Deposit of Provident fund contribution for the month of June, 2018.

Electronic Challan cum

Return (ECR)

The Employees Provident Funds & Miscellaneous Provisions Act, 1952

6 July 15, 2018

Due date for furnishing of Form 24G by an office of the Government where TDS for the month of June, 2018 has been paid without the production of a challan

Form 24G Income Tax Act, 1961

7 July 15, 2018 Due date for issue of TDS Certificate for tax deducted under section 194-IA in the month of May, 2018

Form 16B Income Tax Act, 1961

CIRC Newsletter www.circ-icai.org 09July 2018

8 July 15, 2018 Due date for issue of TDS Certificate for tax deducted under section 194-IB in the month of May, 2018

Form 16C Income Tax Act, 1961

9 July 15, 2018 Quarterly statement in respect of foreign remittances (to be furnished by authorized dealers) for quarter ending June, 2018

Form 15CC Income Tax Act, 1961

10 July 15, 2018 Quarterly statement of TCS deposited for the quarter ending 30 June, 2018

Form 27D Income Tax Act, 1961

11 July 15, 2018 Upload the declarations received from recipients in Form No. 15G/15H during the quarter ending June, 2018.

Form No. 15G/15H

Income Tax Act, 1961

12 July 15, 2018 Payment of ESI for the month of June 2018. Electronic

Challan cum Return (ECR)

The Employees Provident Funds & Miscellaneous Provisions Act, 1952

13 July 18, 2018 Return for compounding taxable person for the quarter ending 30 June, 2018

GSTR-4

The Central Goods and Services Tax, 2017

14 July 20, 2018

Due date for filing return for the month of June 2018 consisting summary of outward taxable supplies and tax payable by Non- Resident Taxable person

GSTR-5

The Central Goods and Services Tax, 2017

15 July 20, 2018 Due date for filing return for the month of June 2018 consisting summary of outward taxable supplies and tax payable by OIDAR

GSTR-5A

The Central Goods and Services Tax, 2017

16 July 20, 2018 Due date for filing return for the month of June 2018 consisting of only the total values for each field for inward and outward supplies

GSTR 3B

The Central Goods and Services Tax, 2017

17 July 25, 2018 Due date of fil ling of monthly PF return for the month of June, 2018 (Including pension and insurance scheme form).

Form 12A, Form 5, Form

11

The Employees Provident Funds & Miscellaneous Provisions Act, 1952

18 July 30, 2018 Quarterly TCS certificate in respect of tax collected by any person for the quarter ending June 30, 2018

Form 27EQ Income Tax Act, 1961

19 July 30, 2018 Due date for furnishing of challan-cum-statement in respect of tax deducted under section 194-IA for the month of June, 2018

Form 26QB Income Tax Act, 1961

20 July 30, 2018 Due date for issue of TDS Certificate for tax deducted under section 194-IB in the month of June, 2018

Form 26QC Income Tax Act, 1961

CIRC Newsletter www.circ-icai.org 10July 2018

21 July 31, 2018 Quarterly statement of TDS deposited for the quarter ending June 30, 2018

Form No 24Q, Form No. 27A

Income Tax Act, 1961

22 July 31, 2018

Annual return of income for the assessment year 2018-19 for all assessee other than (a) corporate-assessee or (b) non-corporate assessee (whose books of account are required to be audited) or (c) working partner of a firm whose accounts are required to be audited or (d) an assessee who is required to furnish a report under section 92E.

Applicable ITR Form

Income Tax Act, 1961

23 July 31, 2018

Quarterly return of non-deduction of tax at source by a banking company from interest on time deposit in respect of the quarter ending June 30, 2018

Form No. 26QAA

Income Tax Act, 1961

24 July 31, 2018

Statement by scientific research association, university, college or other association or Indian scientific research company as required by rules 5D, 5E and 5F (if due date of submission of return of income is July 31, 2018)

Form No. 3CF-l & 3CF-II

Income Tax Act, 1961

25 July 31, 2018

Application for exercising the option available under Explanation to section 11(1) to apply income of previous year in the next year or in future (if the assessee is required to submit return of income on or before July 31, 2018)

Form 9A Income Tax Act, 1961

26 July 31, 2018

Statement to be furnished to accumulate income for future application under section 10(21) or 11(2) (if the assessee is required to submit return of income on or before July 31, 2018)

Form 10 Income Tax Act, 1961

27 July 31, 2018

Due date for claiming foreign tax credit, upload statement of foreign income offered for tax for the previous year 2017-18 and of foreign tax deducted or paid on such income. (If the assessee is required to submit return of income on or before July 31, 2018)

Form no. 67 Income Tax Act, 1961

28 July 31, 2018 Filing of Quarterly GSTR 1 for Apr 2018 to June 2018 for taxpayers with Annual Turnover upto Rs. 1.5 Crore

GSTR-1

The Central Goods and Services Tax, 2017

29 July 31, 2018 Extended Due date for filing Return for Input Service Distributor for the months from July 2017 to June 18

GSTR-6

The Central Goods and Services Tax, 2017

Disclaimer:

This Calendar have been prepared cautiously based on latest provisions and amendments of Income Tax Act, GST, Companies Act 2013 and other related statutes which are subject to changes/ amendments from time to time. However, it is suggested that before acting on the above calendar the relevant assumptions and latest provisions/ clauses of related statutes may please be analyzed in detail and reference be made for updating on relevant website.

CIRC Newsletter www.circ-icai.org 11July 2018

v Head Line :

Tax Deduc ted a t

Source under GST -

An t i -Tax Evas ion

Measure.

v E x e c u t i v e

Summary :

We are very much

Familiar with the TDS

mechanism under Income Tax , which works as

Monitoring and Anti Tax Evasion Measure and

Compel tax deductee to File his Return of

Income , Similarly we have mechanism of

Deduction of Commercial Tax under VAT laws

prevailing in Different states which is applicable

on Government Departments only. On Same

lines TDS under GST has been introduced and

same is applicable on Government Owned

Undertakings which will work as Anti Tax

Evasion Mechanism and put Control on

Government authorities on Payment made on

high value contracts. Read on to know more ...

v Key Objectives of TDS GST :

a) Works as anti tax evasion measure as it

provide information to government about person

supplying goods and/or services to Government

authorities.

b) Compel Tax Deductee to File GST Return to

claim TDS(GST) , thus it ensure proper and

Timely Compliance by TAX DEDUCTEE.

c) Encourage Registered Tax Payers and also

Force Government Department to deal with only

registered tax payers.

d) Work as a Control Mechanism on

Government authorities.e) Collection of tax at early stage by

Government results in Interest earning on same.

v Who is Liable to Deduct TDS (GST)?

Here are the entities to whom Provisions of TDS

(GST) is applicable as Extended through

Notification Below:

(a) a department or establishment of the Central

Government or State Government; or

(b) local authority; or

(c) Governmental agencies; or

(d) such persons or category of persons as may

be notified by the Government

[Notified by Notification No. 33/2017 –

Central Tax , Dated 15/09/2017] as under :

(a) an authority or a board or any other body, -

(i) set up by an Act of Parliament or a State

Legislature; or

(ii) established by any Government, with fifty-

one percent or more participation by way of

equity or control, to carry out any function;

(b) society established by the Central

Government or the State Government or a

Local Authority under the Societies Registration

Act, 1860 (21 of 1860);

(c) public sector undertakings:

The scope of above Provision is very wide

and will cover almost all the establishment in

which Central / State Government has

Participation by way of equity or Control

over its Management.

Goods & Services TaxTax Deducted at Source

CA. Vikas Golechha

CIRC Newsletter www.circ-icai.org 12July 2018

v Requirement for Registration under

GST?

Ø Sec 24 of CGST acts provide for Compulsory

registration irrespective of Turnover also

covers persons who are required to deduct

tax under section 51, whether or not

separately registered under this Act;

Ø So the Persons (as per above list) required to

deduct TDS irrespective of Turnover for the

purpose of Deduction of Tax even when they

are separately registered for payment of tax. v When to Deduct TDS (GST)?

Ø Where the total value of such supply, under a

contract, exceeds two lakh and fifty

thousand rupees. [Contract > 2.5 Lakhs ]

Ø The provision is applicable for Every

Payment even below 2.5 Lakhs where value

of Contract in Aggregate exceeds 2.5 Lakhs

in a year.

v Rate of TDS (GST)?

Ø Rate of TDS (GST) will be 2 % [i.e. 1% CGST

, 1 % SGST ] irrespective of Rate of GST on

Goods Purchase or Services Procured.

Ø For the purpose of deduction of tax specified

above, the value of supply shall be taken as

the amount excluding the central tax, State

tax, Union territory tax, integrated tax and

cess indicated in the invoice.

Ø The amount as deducted will be eligible for

claim by Deductee in his Electronic Cash

ledger.

v When TDS (GST) not to be Deducted ?

Ø No deduction shall be made if the location of

the supplier and the place of supply is in a

State or Union territory which is different

from the State or as the case may be, Union

territory of registration of the recipient.

Ø So provision of GST (TDS) applicable on

Intra state Transaction only.

v When TDS (GST) to be Deposited/Paid ?

Ø The amount deducted as tax under this

section shall be paid to the Government by

the deductor within ten days after the end of

the month in which such deduction is made.

v Time limit to Issue TDS(GST) Certificate

to Deductee ?

Ø The deductor shall furnish to the deductee a

certificate mentioning therein the contract

value, rate of deduction, amount deducted,

amount paid to the Government within 5

Days of Crediting the amount to the

Government.

v Penalty and Interest for Non Compliance

with TDS(GST) Provision ?

Ø If any deductor fails to furnish to the

deductee the certificate, after deducting the

tax at source, within five days of crediting the

amount so deducted to the Government, the

deductor shall pay, by way of a late fee, a

sum of one hundred rupees per day from the

day after the expiry of such five-day period

until the failure is rectified, subject to a

maximum amount of five thousand rupees.

Ø If any deductor fails to pay to the

Government the amount deducted astax , he

shall pay interest at the Rate of 18 % per

CIRC Newsletter www.circ-icai.org 13July 2018

Annum.

Ø If Deductor fails to Deduct TDS or Short

Deducton of TDS OR nondeposit of TDS

than he will be liable to penalty of Rs 10000

or Amount of default Whichever is Higher

v Officer Responsibility for Above

Compliance?

Ø Compliance with the Provisions of

GST(TDS) is the responsibility of DDO

(Drawing and Disbursing Officer) of the

Office Concerned and he is also held

Personally liable for Interest and Penalty for

Non Compliance.

v Date from which above provision is

applicable?

Ø The provisions of GST (TDS) are effective

from 1st July 2018 as same is exempt till

30/06/2018 through press release issued by

Central Government on Recommendation of

26th GST Council meeting.

v Returns to be Filled under GST

Ø GSTR-7 to be filled by Government

department to whom above provisions is

applicable by 10th of Next Month.

Ø Similarly certificate GSTR-7a to be issued to

Tax Deducted within 5 days of Payment

/credit of Tax Deducted to Government.

CIRC Newsletter www.circ-icai.org 14July 2018

time of supply then general provision are

irrelevant.

Time of Supply:

To determine time of supply of Goods &

Services, Four categories are provided as

below:

1. Time of Supply of Goods & Services

under Forward Charge.

2. Time of Supply of Goods & Services

under Reverse Charge.

3. Time of Supply in case of Supply of

Vouchers.

4. Residuary Clause.

1. Time of Supply of Goods & Services

under Forward Charge:

Time of Supply with ExamplesCA. Vikas Modi

Need and Meaning of

Time of Supply:

For the purpose of

paying tax liability,

point of taxationis

required. Time of

supply is nothing but, it

i s p o i n t o f

taxation.When the

supplies have been

made at that time, point of taxation has arisen. To

find out that supplies have been made or not, we

need to determine time of supply. Once time of

supply occurred, a supplier is required to

discharge his GST liability.

There are some general provision and some

specific provision for determining time of supply.

Time of supply is different for goods & services.If

specific provision are applied to determine the

Time of Supply of Goods & Services under Forward Charge

In case of Goods - Earliest of the following

Date of Issue of Invoice by the supplier or Last Date

by which he is required to issue

the invoice

Date of Issue of Invoice by the supplier

if invoice issued within prescribed

period

In case of Services - Earliest of the following

Date on which the

supplier receives the payment

Date of Issue of Invoice by the

supplier if invoice issued

within prescribed

period

Date on which

the supplier receives

the payment

CIRC Newsletter www.circ-icai.org 15July 2018

from the contract : The invoice will be

issued before or after the payment is to be

made by the recipient but within 30 or 45

days of due date of payment.

Ø Due date of payment is cannot be

identified from the contract : The invoice

shall be issued before or after each time

when the supplier of service receives the

payment but within 30 or 45 days of

receipt of payment

Ø Payment is linked to the completion of an

event: The invoice shall be issued before

or after the time of completion of that

event but within 30 or 45 days of

completion of event.

Ø Supply of services ceases under a

contract before the completion of the

supply: The invoice shall be issued at the

time when the supply ceases and such

invoice shall be issued to the extent of the

service provide before stopping.

3. The supply shall be deemed to have been

made to the extent it is covered by the

invoice or, as the case may be, the

payment.

4. Date of Receipt of the payment by

supplier: Payment is entered into the

books of the account or credited in his

bank account whichever is earlier.

5. Optional Time of supply: If amount up to

Rs. 1,000 in excess of invoice amount is

received then the supplier may take the

time of supply is the date of invoice issued

for such excess or advance received.

6. If invoice is not issued and date of payment

Some Important Points:

1. Time of Issue of Invoice for Goods:

i. If movement of goods involved in supply

than before or at the time of removal of

goods.

ii. If no movement of goods involved in

supply than before or at the time of

delivery of goods or making available to

the recipient.

iii. If continuous supply of goodsFor Exa.

Supply of Oil etc. than earliest of the

following:

• Time when each statement is issued.

• Time when each payment is received.

iv. If goods sent for approval than earliest of

the following:

• Time when it becomes known that supply

is taken place.

• Six month from the date of removal.

2. Time of Issue of Invoice for Services:

i. Before or after the provision of service but

within a period prescribed:

Ø 30 days in all cases except for banking

and financial institutions from the date of

supply of services.

Ø 45 days in case of banking and financial

institutions from the date of supply of

services

ii. In case of continuous supply of services:

Ø Due date of payment can be identified

CIRC Newsletter www.circ-icai.org 16July 2018

c. 26thJuly 2017 is the time of supply of

goods i.e. Earlier of the following:- Date of Invoice - 1st August 2017 or- Date of Payment - 26th July 2017.

d. The time of supply of goods for 3/4th of

the goods will be 28th July 2017 as the

payment has been made prior to the date

of invoice and the time of supply of goods

will be 1st August 2017 for remaining

1/4th goods. The late recording of receipt

in the books by Mr. A will have no impact.

Q.2

Mr. A entered into a contract with Mr. B to supply

of oil throughout the year. Mr. A issues monthly

statement for the oil supplied to Mr. B. Now,

determine the time of supply of goods in

following cases:

a. Mr. B made payment for the month of July

on 31st July 2017 and Mr. A issued

statement for the month of July on 8th

August 2017.

b. Mr. A issued statement for the month of

August on 5th September 2017, the

payment of which not received till 30th

September 2017.

A.2

a. 31st July 2017 will be the time of supply.Earliest of the following:Date of Invoice: 8th August 2017Last date on which invoice has to be

issued: Date of payment or statement

whichever is earlier i.e. 31st July 2017.

b. 5th September 2017 will be the time of

supply.Earliest of the following:

or date of completion of provision of service are

also not ascertainable, than the time of supply

shall be the date on which the recipient shows

the receipt of services in his books of accounts.

Examples:

Q.1

Mr. A, a manufacturer, sold goods to Mr. B,

wholesaler, and issued invoice for the sale on

01st August 2017. Now, determine the time of

supply of goods for the following cases:

a. Mr. A removes the goods for delivery to

Mr. B on 16th August 2017.

b. Mr. B collects the goods from premises of

Mr. A on 10th August 2017.

c. Mr. B made full payment on 26th July

2017.

d. Mr. B credited the payment in bank

account of Mr. A on 28th July 2017 for

3/4th of goods, Mr. A recorded the same

as receipts in his books on 3rd August

2017. The goods were dispatched on 5th

August 2017 from the warehouse.

A.1

a. 1st August 2017 is the time of supply of

goods i.e. Earlier of the following:Date of Invoice - 1st August 2017 or Date on which invoice is required to be

issued - 16th August 2017.

b. 1st August 2017 is the time of supply of

goods i.e. Earlier of the following:Date of Invoice - 1st August 2017 or Date on which goods is delivered - 10th

August 2017.

CIRC Newsletter www.circ-icai.org 17July 2018

2017, where provisions of services were

remaining to be completed.

A.3

a. 1st July 2017 will be the time of supply of

services as invoice is not issued within the

time frame of 30 days.

b. 5th August 2017 will be the time of supply

of services as invoice is issued within the

time frame.

c. 3rd August 2017 will be the time of supply

of services as payment received before

invoice date.

d. 5th August 2017 will be the time of supply

of services as invoice is issued before the

completion of provisions of services.

2. Time of Supply of Goods & Services under

Reverse Charge:

Date of Invoice: 5th September 2017.Last date on which invoice has to be

issued: Date of payment or statement

whichever is earlier i.e. 5th September

2017.

Q.3

ABC Consultancy services issued invoice for

services rendered to Mr. P on 5th August 2017.

Determine the time of supply in following cases:

a. The provisions of services were

completed on 1st July 2017.

b. The provisions of services were

completed on 15th July 2017.

c. Mr. P made the payment on 3rd August

2017, where provisions of services were

remaining to be completed.

d. Mr. P made the payment on 15th August

Time of Supply of Goods & Services under Reverse Charge

In case of Goods - Earliest of the following

The date of the

receipt of the goods

The date of entry in the

books of the

receipent

The date on which payment is made

Associated Enterprises -

Earliest of the following

In case of Services

The date on

which payment is made

Date of Payment

60 days from the date of invoice issued by the

supplier

Other Than Associated

Enterprises - Earliest of

the following

30 days from

the date of

invoice issued by the

supplier

• If time of supply cannot be determined with the help of above provisions then the time of supply shall be the date on which entry in the books of the recipient of goods & services is made.

CIRC Newsletter www.circ-icai.org 18July 2018

July 2017

d. 9th July 2017 will be the time of supply of

goods. Earliest of the following:Receipt of Goods = 10th July 2017Date of Payment = 9th July 201730 days from the date of invoice = 30th

July 2017

Q.5

ABC Ltd., a registered firm received services

from PQR Ltd.,an unregistered firm. PQR Ltd.

issued invoice to ABC Ltd. on 1st July 2017. ABC

Ltd. & PQR Ltd is not associated enterprises.

Determine the time of supply of services:

a. ABC Ltd. made the payments to PQR Ltd.

on 15th August 2017.

b. ABC Ltd. made the payments to PQR Ltd.

on 11th September 2017.

A.5

a. 15thAugust 2017 will be the time of

supply of services as payment made

earlier than the date immediately

following 60 days from date of issue of

invoice.

b. 30stAugust 2017 will be the time of supply

of services as payment made after the

date immediately following 60 days from

date of issue of invoice.

Q.6

XYZ Ltd. & MNT Ltd. is associated enterprises.

XYZ Ltd., a registered firm received the services

of MNT Ltd., a unregistered firm. Determine the

time of supply in following cases:

a. XYZ Ltd. recorded the liability in the

Example:

Q.4

Mr. A, a registered dealer received goods from

Mr. B, an unregistered dealer. Mr. B issues

invoice on 1st July 2017. Now, determine time of

supply of goods in following cases:

a. Mr. A received goods on 15th July 2017,

payment of which is not made yet.

b. Mr. A received goods on 3rd August 2017 &

made payment for the same on 4th August

2017.

c. Mr. A made payment on 8th July and received

goods on the same date.

d. Mr. A received goods on 10thJuly 2017 &

made payment for the same on 9thJuly 2017.

A.4

a. 15th July 2017 will be the time of supply of

goods.Earliest of the following:Receipt of Goods = 15th July 2017Date of Payment = NA30 days from the date of invoice = 30th

July 2017

b. 30thJuly 2017 will be the time of supply of

goods.Earliest of the following:Receipt of Goods = 3rd August 2017Date of Payment = 4th August 201730 days from the date of invoice = 30th

July 2017

c. 8th July 2017 will be the time of supply of

goods.Earliest of the following:Receipt of Goods = 8th July 2017Date of Payment = 8th July 201730 days from the date of invoice = 30th

CIRC Newsletter www.circ-icai.org 19July 2018

a. 15th July 2017 will be the time of supply of

services as the date of entry in the books

is prior to the date of payment.

b. 10th July 2017 will be the time of supply of

services as the payment is made earlier

to the date of entry in the books.

books on 15th July 2017 and payment will be

made in the next month.

b. XYZ Ltd. made advance payment to MNT

Ltd. on 10th July and recorded liability in

the books on 15th July 2017.

A.6

Time of Supply of Vouchers for Goods & Services

Residuary Clause

Date of issue of voucher, if the supplies is identifiable at

that point; or

In a case where a periodical return has to be filled, the date on which

such return is to be filled

Date of redemption of voucher, in all other caeses.

In any other case, the date on which the CGST/SGST/IGST/UTGST is

paid.

3. Time of Supply of Vouchers for Goods & Services:

3. Time of Supply of Vouchers for Goods & Services:

4. Residuary Clause

Case Events before change in effective rate of tax

Events after change in effective rate of tax

Time of supply if goods & services are supplied before change in effective rate of tax

Time of supply if goods & services are supplied after change in effective rate of tax

1.

2.

3.

4.

Invoice Issued/Payment Received

Invoice Issued/Payment Received

Invoice issued

Payment Received

No activity.

Supply of Goods & Services

Payment Received

Invoice Issued

NA

Date of receipt of Payment

Date of Invoice

NA

·Date of receipt of payment or ·Date of issue of invoiceWhichever is earlier

·Date of receipt of payment or ·Date of issue of invoiceWhichever is earlier

Date of receipt of Payment

Date of Invoice

CIRC Newsletter www.circ-icai.org 20July 2018

29thDecember 2017. What is the time of supply

in this case?

A.8

Following Event have been done before change

in effective rate of tax:

· Goods Supplied· Payment Received

Time of supply will be Date of receipt of payment

i.e. 29th December 2017.

Q.9

Mr. A is supplied goods to Mr. B on 28th

December 2017. The GST rate on goods is

changed from 12% to 5% w.e.f. 1st January

2018. Mr. A issued invoice on 28th December

2017 and payment is credited in his bank

account on 4thJanuary 2018. What is the time of

supply in this case?

A.9

Following Event have been done before change

in effective rate of tax:

· Goods Supplied· Invoice Issued

Time of supply will be Date of Invoice i.e. 28th

December 2017.

Q.10

Mr. A is supplied goods to Mr. B on 2ndJanuary

2018. The GST rate on goods is changed from

12% to 5% w.e.f. 1st January 2018. Mr. A issued

invoice on 28th December 2017 and payment is

credited in his bank account on 30th December

2017. What is the time of supply in this case?

A.10

· The date of receipt of payment shall be

the date of credit in the bank account if

such credit in the bank account is after

four working days from the date of change

in the rate of tax.

· Date of Receipt of the payment by

supplier: Payment is entered into the

books of the account or credited in his

bank account whichever is earlier.

Example:

Q.7

Mr. A is supplied goods to Mr. B on 28th

December 2017. The GST rate on goods is

changed from 12% to 5% w.e.f. 1st January

2018. Mr. A issued invoice on 28th December

2017 and payment is credited in his bank

account on 30th December 2017. What is the

time of supply in this case?

A.7

Following Event have been done before change

in effective rate of tax:

· Goods Supplied· Invoice Issued· Payment Received

Time of supply will be earliest of the following:

· 28th December 2017· 30th December 2017

Time of Supply will be 28th December 2017.Q.8Mr. A is supplied goods to Mr. B on 28th

December 2017. The GST rate on goods is

changed from 12% to 5% w.e.f. 1st January

2018. Mr. A issued invoice on 2ndJanuary 2018

and payment is credited in his bank account on

CIRC Newsletter www.circ-icai.org 21July 2018

Mr. A is supplied goods to Mr. B on 2ndJanuary

2018. The GST rate on goods is changed

from 12% to 5% w.e.f. 1st January 2018.

Mr. A issued invoice on 2ndJanuary 2018

and payment is credited in his bank

account on 29thDecember 2017. What is

the time of supply in this case?

A.12

Following Event have been done before change

in effective rate of tax:

· Payment ReceivedTime of supply will be Date of invoice i.e. 2nd

January 2018.

Q.13

Let's say there was increase in tax rate from 18%

to 20% w.e.f. 1.6.2017. What is the tax rate

applicable when services provided and invoice

issued before change in rate in April 2017, but

payment received after change in rate in June

2017?

A.13

The old rate of 18% shall be applicable as

services are provided prior to 1.6.2017.

Following Event have been done before change

in effective rate of tax:· Invoice Issued· Payment Received

Time of supply will be earliest of the following:

· 28th December 2017· 30th December 2017

Time of Supply will be 28th December 2017.

Q.11

Mr. A is supplied goods to Mr. B on 2ndJanuary

2018. The GST rate on goods is changed from

12% to 5% w.e.f. 1st January 2018. Mr. A issued

invoice on 29thDecember 2017 and payment is

credited in his bank account on 4thJanuary

2017. What is the time of supply in this case?

A.11

Following Event have been done before change

in effective rate of tax:

· Invoice issued

Time of supply will be Date of receipt of payment

i.e. 4th January 2018.

Q.12

CIRC Newsletter www.circ-icai.org 22July 2018

CA. Arjit Agarwal

1. In Brief

“Be a L i f e Long

Student. The more you

learn, the more you

earn and more self

confidence you will

have”.

An investment in knowledge pays the best

i n t e r e s t ” b y B e n j a m i n F r a n k l i n

This article being Gist, tries to covers all updates

in relation to recent important verdicts between

21st May 2018 to 20th June 2018.

2. Verdicts – Apex Court:-

3. Verdicts – High Court:-

S. No.

S. No.

1.

1.

2.

CIT vs. Sunita Dhadda (Supreme Court)

PCIT vs. Chawla Interbild Construction Co. Pvt. Ltd (Bombay

High Court)

PCIT vs. Nova Technocast Pvt

Ltd (Gujarat High Court)

143(3), 292C

37(1)

195, 40(a)(i), 9

Verdict

Verdict

Relevant Section

Relevant Section

In Brief

In Brief

S. 143(3)/ 292C: If the AO wants to rely upon documents found with third parties, the presumption u/s 292C against the assessee is not available. As per the principles of natural justice, the AO has to provide the evidence to the assessee & grant opportunity of cross-examination. Secondary evidences cannot be relied on as if neither the person who prepared the documents nor the witnesses are produced. The violation of natural justice renders the assessment void. The Dept cannot be given a second chance (All judgements considered)

The fact that the parties to whom payments were made did not appear before the AO does not justify a disallowance if the assessee has discharged the initial onus and produced documentary proof. The assessee cannot compel the appearance of the parties before the AO. The onus is on the AO to carry out enquiries based on the PAN Nos to find out the genuineness of the parties

S. 9/ 40(a)(i)/ 195: Explanation 2 to s. 195(1) inserted by Finance Act 2012 with retrospective effect from 01.04.1962 has bearing while ascertaining payments made to non-residents is taxable under the Act or not. However, it does not change the fundamental principle that there is an

Legal UpdatesUpdates in relation to Recent Verditcs on Direct Taxes – Brief

CIRC Newsletter www.circ-icai.org 23July 2018

obligation to deduct TDS only if the sum is chargeable to tax under the Act. If the conclusion is arrived that such payment does not entail tax liability of the payee under the Act, s. 195(1) does not apply

S. 147: Even a s. 143(1) assessment cannot be reopened without proper 'reason to believe'. If the reasons state that the information received from the VAT Dept that the assessee entered into bogus purchases "needed deep verification", it means the AO is reopening for doing a 'fishing or roving inquiry' without proper reason to believe, which is not permissible

S. 143(2) Limited scrutiny: The CBDT Circulars which restrict the right of the AO in limited scrutiny cases apply only in cases where the AO seeks to do comprehensive scrutiny to find if there is potential escapement of income on other issues. However, if the s. 143(2) notice seeks information on whether the share premium is from disclosed sources and is correctly offered to tax, the AO can also inquire into whether the premium exceeds the FMV and is taxable u/s 56(2)(viib)

S. 271(1)(c) Penalty: Merely using the words that there is concealment of income and / or furnishing inaccurate particulars of income is not sufficient. The same should be particularized by the AO with a finding as to what particulars of income has been concealed or what particulars of income are inaccurate. The words 'concealment' or giving 'inaccurate particulars of income' have to be read strictly before penalty provisions u/s 271(1)(c) of the Act can be invoked. Zoom Communication 371 ITR 570 (Del) distinguished

S. 282/ 292B: Entire law on "service of notice" and difference between "issue" and "service" of notice explained. S. 147 proceedings are initiated when the notice is "issued". Though "service" of notice u/s 147/148 is not a mere procedural requirement, but a condition precedent for initiation of proceedings, the service upon a person who was not authorized to receive notice does not render the proceedings null and void if the assessee complied and entered appearance

3.

4.

5.

6.

PCIT vs. Manzil Dineshkumar Shah (Gujarat High Court)

Sunrise Academy of Medical Specialities

(India) Private Limited v. ITO

(Kerala High Court)

CIT vs. L&T Finance Ltd

(Bombay High Court)

CIT vs. Sudev Industries Limited (Delhi High Court)

147, 148

143(2), 56(2)(viib)

271(1)©

147, 148, 282, 292B

CIRC Newsletter www.circ-icai.org 24July 2018

S. 147: Law on reopening of assessments within four years and beyond four years explained with reference to all important case laws. Strictures passed against the AO for making comments which are highly objectionable and bordering on contempt and for being oblivious to law. As the very same ACIT had passed series of orders reopening assessments in ignorance of legal position, a compilation of judgments on reassessment proceedings should be furnished to the Commissioner to study the same. The position of law regarding the writ remedy is so settled, that it is understood even by the law students

S. 254: While deciding an application for stay of demand, the Appellate Tribunal can only consider the prima facie case of merits. It cannot give a final finding on the merits and decide the appeal itself

S. 68: Addition of undisclosed income cannot be made on the basis of (a) entries in dairy found during survey & (b) admission of director in s. 133A survey if assessee has filed a retraction and alleged that the entries/ statement were recorded under pressure. A s. 133A statement is merely information simplicitor and not evidence per se. Addition cannot be sustained if the Dept has not investigated the matter and find material to support the addition

7.

8.

9.

Zuari Foods and Farms Pvt. Ltd vs.

ACIT (Bombay High Court)

Maharashtra State Road Transport

Corporation vs. CST (Bombay High Court)

PCIT vs. Texraj Realty P.Ltd

(Gujarat High Court)

147, 148

254

133A, 68

4. Verdict - ITAT:-

S. No.

1.

2.

M/s A Daga Royal Arts vs. ITO (ITAT Jaipur)

Gagan Infraenergy Ltd vs. DCIT (ITAT Delhi)

40A(3), Rule 6DD

45, 47(iii), 48

Verdict Relevant Section In Brief

S. 40A(3) Rule 6DD: No disallowance can be made for cash payments if the transaction is genuine and the identity of the payee is known. Rule 6DD is not exhaustive. The fact that the transaction does not fall with Rule 6DD does not mean that a disallowance has to be per force made (all judgements considered)

S. 56(2)(viia)/ 47(iii): Capital gains on shares transferred via "Gift": Surprising that huge volume of shares in a public limited company is transferred by assessee to another company without any consideration, without any proper documentation

CIRC Newsletter www.circ-icai.org 25July 2018

being executed as per law and giving it a nomenclature of “gift”. Difficult to imagine Articles of Association of a company would provide for gifting of assets of the company to another company unless it be one which has been set up for some purpose. The assessee has to establish to the hilt, the factum, genuineness and validity of the transaction, the right to enter into such transaction and bonafides of such transaction, especially when, revenue challenges its genuineness. There is no agreement/document that has been executed between group companies forming part of family realignment. To postulate that a company can give away its assets free to another even orally, can only be aiding dubious attempts at avoidance of tax payable under the Act unless it is supported by documentary evidence

S. 147/ 151: If the AO reopens on the basis of information received from another AO without further inquiry, it means he has proceeded "mechanically" and "without application of mind". If the CIT does not give reasons while according sanction, it implies that he has also not applied his mind. Both render the reopening void (All imp judgements referred)

S. 254(2): The limitation period for filing a Rectification Application has to be computed from the date of "communication" of the order and not from the date of passing the order. The fact that the order was pronounced in open court is not relevant because the parties will not be aware of the mistakes therein until after perusal of the order.

S. 2(47)/ 45: Argument that the allotment of shares by the assessee's holding co to foreign investors at huge valuation results in a "transfer"/ "indirect transfer" of the assessee's assets to the foreign investors is not correct. Argument that a multi layered holding structure was deliberately created to avoid taxes in India and to conceal the information about the ultimate beneficiaries is also not correct

3.

4.

5.

Sunil Agarwal vs. ITO (ITAT Delhi)

Jagmohan Gurbakshish

Singh vs. DCIT (ITAT Chandigarh)

Supermax Personal Care Private Limited

vs. ACIT (ITAT Mumbai)

147, 148, 151

254(2)

2(47), 45, 48

CIRC Newsletter www.circ-icai.org 26July 2018

S. 147/148: If the reopening is based on information received from the investigation dept, the reasons must show that the AO independently applied his mind to the information and formed his own opinion. If the reopening is done mechanically, it is void. Also, if the reasons refer to any document, a copy should be provided to the assessee. Failure to do so results in breach of natural justice and r e n d e r s t h e r e o p e n i n g v o i d

It is painful to note that the Dept officials in order to achieve targets at the close of the FY not only are tempted to ignore the principles of law and natural justice but cross their limits, in complete violation of the orders issued by judicial authorities. They are pressurised by higher officials to do so and they have to choose the lesser risky option of the two i.e. either to face the departmental action for not achieving targets or to face contempt proceedings. They choose the later option because perhaps they think that courts will not opt for strict view in case the amount coercively recovered is refunded after passing of the cut off date i.e. 31st March, and an apology tendered to the Court

Applicability of s. 80 to s. 153A returns: A return filed u/s 153A is deemed to be a return filed u/s 139(1). Accordingly, the restrictive provisions of s. 80 do not apply. The return u/s 153A, once accepted and assessed, replaces the original return filed u/s 139. Therefore, the assessee is eligible for carry forward business loss

S. 44C: A non- resident assessee is entitled to claim deduction of an amount equal to 5% of the adjusted total income as expenditure in the nature of Head Office (HO) Expenses. The fact that the expenses are not debited in the Profit & loss account or the books of account is irrelevant. The entries in the books of account are not conclusive

S. 251(1): While the CIT(A) has the power to "enhance the assessment", he has no power to travel beyond the subject-matter of the assessment and is not entitled to assess new sources of income. In order for the CIT(A) to

6.

7.

8.

9.

10.

Deepraj Hospital (P) Ltd vs. ITO (ITAT Agra)

Greater Mohali Area Development

Authority vs. DCIT

(ITAT Chandigarh)

ACIT vs. Splendor Landbase Limited

(ITAT Delhi)

Ernst & Young Ltd vs. ACIT (ITAT Delhi)

Nokia Networks OY vs. JCIT (ITAT Delhi

Special Bench)

147, 148

220(6), 226

139(1), 139(3), 153A, 80

44C

9, Article 5, Article 7

CIRC Newsletter www.circ-icai.org 27July 2018

enhance, there must be something in the assessment order to show that the AO applied his mind to the particular subject-matter or the particular source of income with a view to its taxability or to its non-taxability and not to any incidental connection (all judgements considered)

Bogus Long-term capital gains: As neither the statement of Mukhesh Choksi was provided to the assessee nor cross-examination was allowed and it was not even placed on record, the action of the AO in treating the LTCG and STCG as income from other sources was not warranted

S. 263 Revision: Explanation 2 to s. 263 inserted by the FA 2015 (which confers power upon the CIT to revise assessments where inadequate inquiries have been conducted by the AO) is prospective in nature and does not apply even to a case where the CIT passed the order after Explanation 2 came on the statute. The CIT should show that the view taken by the AO is unsustainable in law. The action of the CIT in directing the AO to conduct enquiry in a particular manner is contrary to the law interpreted by the Delhi High Court in CIT v. Goetze (India) Ltd 361 ITR 505. If such course of action is permitted, the CIT can find fault with each and every assessment order without making any enquiry or verification in order to establish that the assessment order is not sustainable in law

S. 68 Bogus share premium: Addition cannot be made on the ground that the directors of the share subscribers did not turn up before the AO. The assessee can be required to prove only such facts which are in his knowledge. Creditworthiness of the subscriber cannot be disputed by the AO of the assessee but by the AO of the subscriber. If the assessee has discharged its onus to prove identity, creditworthiness & genuineness of the share applicants, the onus shifts to AO to disprove the documents furnished by assessee. In absence of any investigation, much less gathering of evidence by the AO, an addition cannot be sustained merely based on inferences drawn by circumstance (all judgements considered)

11.

12.

13.

14.

Jagdish Narayan Sharma vs.

ITO (ITAT Jaipur)

ITO vs. K. Ramakrishna Reddy

(ITAT Hyderabad)

Indus Best Hospitality & Realtors Pvt. Ltd vs. PCIT (ITAT Mumbai)

ITO vs. Wiz-Tech Solutions Pvt. Ltd

(ITAT Kolkata)

251

45, 48, 56

263

68

CIRC Newsletter www.circ-icai.org 28July 2018

S. 159/ 163/ 176: While a notice/ order on a dead person/ wound-up company is a nullity, this is subject to the condition that the department is made aware of the death/ winding-up. If the legal representative, either voluntarily or in response to a notice issued against the deceased but served upon his agent, allows the assessment proceedings to continue against the deceased/ wound-up company without any objection and lets the AO make an assessment order, it would not be open for him to take a plea at the appellate stage, as a last resort or as an afterthought, that the proceedings taken and the assessment order made against the deceased/ wound-up company are nullity. In such cases, the assessment is liable to be set-aside for a fresh assessment in accordance with law instead of its annulment

15. Pesak Ventures Ltd. vs. DCIT (ITAT Delhi)

159, 163, 176

CONCLUSION

To conclude, we should always focus/be in touch with regular Amendments/Case Laws from Apex Court, High Courts and Tribunal. This will help us in understanding the Law better and guide us how to interpret the Law before Judiciary. This article brings all important recent Judgments under Income Tax Act 1961. However readers are advise to go through in depth to understand relevant judgment .

A great saying on updating of knowledge –

“No matter how much experience you have, there is always a room for something new you can learn and improve .”

Keep Updating!!!

Sources :-* http://itatonline.org/archives/main/

29

IMPORTANT ANNOUNCEMENT’S

CIRC Newsletter www.circ-icai.orgJuly 2018

30

Organised ByCentral India Regional Council of

The Institute of Chartered Accountants of India

Ghaziabad Branch of Central India Regional Council ofThe Institute of Chartered Accountants of India

Hosted by

PRAKALP - 2018 - BEGINNING OF NEW ERA

39th Regional Conference of CIRC of ICAI39th Regional Conference of CIRC of ICAI

Date: 18th & 19th

August 2018(Saturday & Sunday)

Date: 18th & 19th

August 2018(Saturday & Sunday)

Venue: Hotel Radisson Blu,

Kaushambi, Ghaziabad, NCR

Venue: Hotel Radisson Blu,

Kaushambi, Ghaziabad, NCR

Chief GuestEMINENT PERSONALITY

Guests of HonourMr. Rajesh Agarwal,Finance Minister, U.P

CA Naveen N D Gupta,President,ICAICA.Prafulla P. Chhajed,Vice President,ICAI

CIRC Newsletter www.circ-icai.orgJuly 2018

12 CPEHOURS

31

05.30 PM ONWARDS: MEGA CULTURAL EVENING FOLLOWED BY DINNER

Programme

Day One : Saturday, 18th August 2018

Registration & Breakfast 8.00 AM – 9.00AM

FIRST TECHNICAL SESSION (09.00 AM –10.45AM)

SECOND TECHNICAL SESSION……………………………………………...………….11.45 AM –1.30 PM

SPECIAL SESSION……………………………………………………… ………………..02.30 PM –3.00 PM

THIRD TECHNICAL SESSION ………………………………………………………......03.00 PM –5.00 PM

Topic:

Topic:

Topic:

Topic:

INAUGRAL SESSION………………………………………………………………………10.45 AM –11.45AM

Taxation of Trust and Society

Special Session on Life Management

UNDER FINALISATION

Professional Opportunities in Ind AS

Speaker:

Speaker:

Speaker:

Speaker:

CA. (Dr.) Girish Ahuja

By Shivani Didi, Brahma Kumari Spiritual Guru

UNDER FINALISATION

CA. Yagnesh Desai, Mumbai

LUNCH : 01.30 PM – 2.30PM

Day Two : Sunday, 19th August 2018 BREAKFAST 8.30 AM – 9.30 AM

FOURTH TECHNICAL SESSION………… ……………………………………… 9.30 AM –11.30 AM

FIFTH TECHNICAL SESSION……………………………………………………………..11.30 PM –1.30 PM

SIXTH TECHNICAL SESSION……………………………………………………………..02.30 PM –4.30 PM

VALEDICTORY SESSION…………………………………………………………………….4.30 PM – 5.30 PM

Topic:

Topic:

Topic:

GST Audit

UNDER FINALISATION

Recent Amendments in Companies Act

Speaker:

Speaker:

Speaker:

CA. Atul Gupta, CCM, ICAI

UNDER FINALISATION

CA. Amarjit Chopra, Past President, ICAI

LUNCH : 01.30 PM – 2.30PM

With Regards

CA. Gyan Chandra MisraChairman CIRC

CA. Abhay K. ChhajedRC Member, CIRC

CA. Kemisha SoniCCM, ICAI

CA. Rohit Ruwatia AgrawalVice Chairman CIRC

CA. Churchill JainRC Member, CIRC

CA. Manu AgrawalCCM, ICAI

CA. Pramod K. BoobSecretary CIRC

CA. Deep K. MisraRC Member, CIRC

CA. Mukesh S. KushwahCCM, ICAI

CA. Nitesh GuptaTreasurer CIRC

CA. Gautam SharmaRC Member, CIRC

CA. Prakash SharmaCCM, ICAI

CA. Nilesh GuptaChairman CICASA

CA. Mukesh BansalRC Member, CIRC

CA. Shyam L. AgarwalCCM, ICAI

CIRC Newsletter www.circ-icai.orgJuly 2018

32

Ghaziabad....

Ghaziabad is a city in the Indian state of Uttar Pradesh founded by Wazir Ghazi-ud-din, a minister of Emperor Muhammad Shah in 1740.

It is sometimes referred to as the "Gateway of UP" because it is close to New Delhi, on the main route into Uttar Pradesh. It is a part of the National Capital Region of Delhi. It is a large and planned industrial city, with a population of 2,358,525. Well connected by roads and railways, and is the administrative headquarters of Ghaziabad District as well as being the primary commercial, industrial and educational centre of western Uttar Pradesh and a major rail junction for North India. Recent construction works have led to the city being described by a City Mayors Foundation survey as the second fastest-growing in the world. Situated in the Upper Gangetic Plains, the city has two major divisions separated by the Hindon River, namely: Trans-Hindon on the west and Cis-Hindon on the east side.

History

Excavations carried out at the mound of Kaseri, at the banks of river Hindon, some 2 km north of Mohan Nagar, have shown that civilisation existed there as early as 2500 BC. Mythologically, some neighbouring towns and villages of the city including Garhmukteshwar, Pooth Village and Ahar region have been associated with the Mahabharata and the fort at Loni, is associated with the legend of Lavanasura of the Ramayana period. According to the Gazetteer, the fort, "Loni" is named after Lavanasura. The city and its surrounding region have historically witnessed major wars and battles over the last many centuries. In AD 1313, the entire region including present day Ghaziabad became a huge battlefield, when Taimur laid siege on the area during Muhammad bin Tughluq's reign. During the Anglo- Maratha War, Sir General Lake and the Royal Maratha army fought here circa. Altama Religion was started from Ghaziabad in 1803. The name "Ghaziuddinnagar" was shortened to its present form, i.e. "Ghaziabad" with the opening of the Railways in 1864. Establishment of the Scientific

Society here, during the same period is considered as a milestone of the educational movement launched by Sir Syed Ahmad Khan.

The Ghaziabad Municipality came into existence in 1868.[citation needed] The Sind, Punjab and Delhi Railway, connecting Delhi and Lahore, up till Ambala through Ghaziabad was opened in the same year. With the completion of the Amritsar-Saharanpur-Ghaziabad line of the Sind, Punjab and Delhi Railway in 1870, Delhi was connected to Multan through Ghaziabad, and Ghaziabad became the junction of the East Indian Railway and Sind, Punjab and Delhi Railway.

The city of Ghaziabad was founded in AD 1740 by Wazir Ghazi-ud-din, who named it Ghaziuddinnagar after himself.

Ghaziabad, along with Meerut and Bulandshahr, remained one of the three Munsifis of the District, under the Meerut Civil Judgeship during most periods of the British Raj.

Ghaziabad was associated with the Indian independence movement from the Indian Rebellion of 1857. During that rebellion, there were fierce clashes between the British forces and Indian rebel sepoys on the banks of the Hindon, and the rebels checked the advancing British forces coming from Meerut.

Climate

As it is connected to the national capital, its temperature and rainfall are similar to Delhi. Rajasthan's dust storms and snowfall in the Himalayas, Kumaon and Garhwal hills name their impact in the weather regularly. The monsoon arrives in the district during the end of the June or the first week of July and normally it rains until October. As in other districts of northern India mainly three seasons - summer, winter and rainy - prevail here, but sometimes due to severe snowfall in the Himalayas and Kumaon Hills, adverse weather can also be seen.

CIRC Newsletter www.circ-icai.orgJuly 2018

33

Economy

Real estate hub

A proposal has been made to widen National Highway 24 (NH-24) from four to sixteen lanes on the stretch between the Ghaziabad-Delhi border and Dasna. As a large number of residential and commercial projects are coming up along the highway. Some major developers which have invested heavily on NH-24 are GAURS, Mahagun, Antriksh, Crossings Republik, Ansal, Wave, Gulshan Homz, SG Estates etc. In tune with Indian Government's Pradhan Mantri Awas Yojana (Urban), there is Wave City Grih Awas Yojana, under which Economically Weaker Section (EWS) and Lower Income Group (LIG) people can avail their dream homes at concessional rates. Places on NH-24 and National Highway 58 are flourishing as residential options to the capital because of their proximity to Delhi.

Education Hub

Ghaziabad has also come up as a major educational hub with reputed schools and colleges in the region.

Transport

Delhi Metro

The Delhi Metro extends to Dilshad Garden station which is situated at the Apsara Border. At present, it serves the areas of Shalimar Garden, Rajendra Nagar and other neighbouring colonies.

This line will be extended to New Bus Stand, Ghaziabad by 2016-17. Work for the same already started in December 2014. Another station exists at Vaishali, which serves that area as well as Vasundhara and Indirapuram, and there is also a station at Kaushambi.

Air

Hindon Air Force Station is the airport serving Ghaziabad. As on 1st February 2018 no operators operate scheduled f l ights. Government of India has said that some operators have been permitted to operate flights under UDAN2.

Sports

Cricket, association football, field hockey and Kabaddi are the main sports in Ghaziabad. Ghaziabad are from the city. The Jawaharlal Nehru Stadium is a multi-purpose stadium in Ghaziabad.

Crossing_Republik_Ghaziabad- NH_24 Kaushambi Housing Society

CIRC Newsletter www.circ-icai.orgJuly 2018

34

The city. Gzb is the second fastest-growing city in the world. One of the most beautiful place seen in NCR.

Hindon Air Base

The city has the largest Air force base in Asia and 8th largest in the world. you need to see this place on Air Force day.

Windsor Street:The very own C.P of Ghaziabad. This place offers a number of cuisines with amazing delicious food.

Railway Connectivity: If traveling to this city is what you are thinking about, then Cleartrip will guide you. Traveling to Ghaziabad is easy thanks to the railway connectivity. Book your railway tickets conveniently with just a few taps on the Cleartrip app or website. The station of the city is named as GHAZIABAD and its station code is GZB. The station takes care of all the basic amenities of the passengers.

The station is well-connected to a number of Indian cities. Some of the major routes include to the places of Kanpur Central, Allahabad Jn, and New Delhi. There are 74 weekly trains connecting Kanpur Central to Ghaziabad, 6 weekly trains connecting Allahabad Jn to Ghaziabad, and 16 weekly trains connecting New Delhi to Ghaziabad.

Some of the popular trains traveling to Ghaziabad are Rdp Anvt Link E(22487) to Anand Vihar Trm operating 7 times a week, Ndls Lko Raj(12430) to Lucknow operating 7 times a week, and Lko Ndls Raj(12429) to New Delhi operating 7 times a week. Traveling in one of these trains will be a memorable experience.

The attractions of Ghaziabad are many. As soon as you enter the city, you may begin your tour as there are varied points of interest located near the Ghaziabad station itself.

Market Complex in Ghaziabad Market Complex in Ghaziabad

What is Ghaziabad famous for?

CIRC Newsletter www.circ-icai.orgJuly 2018

35

There are so many great ways to learn and sharpen your skills these days: you can read blogs, listen to podcasts, watch how-to videos on YouTube, and attend webinars, just to name a few. Why bother with the time and expense of an in-person conference or workshop?

If that’s your attitude, then you may be missing out on one of the best opportunities to take your g a m e t o t h e n e x t l e v e l . L i v e events—conferences, workshops, lunch & learns–provide unique learning and career building opportunities that you just can’t find anywhere else.

Sharpen the Saw

While the “sharpen the saw” idea certainly pre-dates Stephen Covey, he lists it as his seventh habit of highly effective people. The idea is that sometimes you have to take a break from the “work” of your work to sharpen your skills. A dull axe won’t cut a tree nearly as effectively as a sharp one. WeI always return from a conference with new ideas and approaches that make me more effective and efficient at work. Don’t be the woodcutter hacking away at the tree with a dull ax while your competition cuts it down in half the time with a sharp one. Or uses a chainsaw she saw demonstrated at a conference.

Meet Experts & Influencers Face to Face

While not all conferences offer you the opportunity to meet your business idols, your chances are greatly improved when you’re sharing the same space. Sometimes it’s about taking a selfie with someone who’s influenced you or sharing a business idea with someone you admire, or making a connection that can lead to finding your next mentor.

Networking Opportunities