Embed Size (px)

Citation preview

The Global Economy, Rising Risk and Marine Insurance Markets

Risk and Reward in a Troubled WorldSan Francisco Board of Marine Underwriters

San Francisco, CAMay 3, 2012

Download at www.iii.org/presentationsRobert P. Hartwig, Ph.D., CPCU, President & Economist

Insurance Information Institute 110 William Street New York, NY 10038Tel: 212.346.5520 Cell: 917.453.1885 [email protected] www.iii.org

2

Presentation Outline

Global Economic Overview & Outlook International Overview Emerging vs. Developing Markets Global Trade Volume Forecasts: Imports/Exports

US Economy Overview & Outlook GDP Outlook Drivers of P/C Insurance Exposures Marine Drivers Presidential Politics and P/C Profitability

The Unfortunate Nexus of Opportunity, Risk and Uncertainty The Fusion of Economic and (Geo)Political Risk Top 10 Risks for the Global Economy

Global Catastrophe Loss Trends and Threats Was 2011 an Aberration or a Foreshadowing of the Future

US P/C Insurance Industry Financial Overview & Outlook

Global Economic Outlook: Regional and Major Economy

Perspectives

3

Strength of Economies Varies Greatly as Does Pace of Recovery from the

Economic Challenges Important Consequences for Insurer and

Reinsurer Growth Opportunities3

4

Real GDP Growth Forecasts: Major Economies: 2011 – 2013F

Sources: Blue Chip Economic Indicators (4/2012 issue); Insurance Information Institute.

1.7%

0.7% 1.

5%

3.1%

2.3%

0.6%

0.6%

8.4%

1.8%

2.6%

1.7%

0.9% 1.

7%

8.5%

1.7%

9.2%

-0.7%-0.5%-2%

0%

2%

4%

6%

8%

10%

US UK Euro Area Germany China Japan

2011 2012F 2013F

Growth Prospects Vary Widely by Region: Brightening in the US, Mild Recession in the Eurozone, A “Soft Landing” in China, Strength in

India, Reconstruction Stimulus in Japan and Modest Growth in America’s Largest Trading Partners—Canada and Mexico.

The Eurozone and UK are in

recession. Both should

end in Q3:2012

China growth has slowed, but remains strong in an expected “soft landing”

scenario

US recovery

continues

Rebuilding acts as a

stimulus to Japanese economy

5

Real GDP Growth Forecasts: Emerging Market Regions: 2010 – 2013F

*Excludes Libya in 2011. **Indonesia, Malaysia, Thailand, Philippines and VietnamSources: IMF World Economic Outlook (April 2012 ); Insurance Information Institute.

5.3%

10.6

%

4.9%

4.5%

4.3%

7.0%

5.3%

3.9%

7.2%

3.5%

5.3%

5.1%

3.5%

6.9%

1.9%

4.0%

5.4%

5.4%

4.1%

7.3%

3.7%

2.9% 3.

9%

6.2%

5.3%

4.3% 4.5%

4.2%

0%

2%

4%

6%

8%

10%

12%

WorldOutput

India MiddleEast &NorthAfrica*

Central &EasternEurope

Russia ASEAN-5** Sub-Saharan

Africa

2010 2011 2012F 2013F

Growth Prospects Vary Widely by Region: All Regions Slowed in 2011 As Economic Recovery Encountered Many Challenges. IMF Outlook for

2012 Is Mixed With Broader, More Robust Growth in 2013 Predicted. Actual Growth in 2012 Could Surprise to the Upside.

(4.0)

(2.0)

0.0

2.0

4.0

6.0

8.0

10.0

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09

10

11

12

F1

3F

Advanced economies Emerging and developing economies World

Source: International Monetary Fund, World Economic Outlook Update, Apr. 2012; Ins. Info. Institute.

Emerging economies (led by China) are expected to grow by 5.7% in 2012 and

6.0% in 2013.

GDP Growth: Advanced & Emerging Economies vs. World, 1970-2013F

Advanced economies are expected to grow at a sluggish pace of 1.4% in

2012 and 2.0% in 2013.

World output is forecast to grow by 3.5% in 2012 and 4.1% in 2013. The world economy shrank by 0.6% in

2009 amid the global financial crisis

GDP Growth (%)

7

Relative Shares of Global Output,Advanced vs. Developing Economies, 2009

Developing Economies

47.1%

Advanced Economies

52.9%

Source: EDC Economics, “The Moment of Truth: Global Export Forecast Fall 2010, at http://www.edc.ca/english/docs/gef_e.pdf

The gap is closing quickly. China became the world’s second largest economy in 2010 and before long

the developing world’s share of GDP will exceed that of advanced

economies.

8

Current Real GDP Growth vs. Pre-Crisis Average (2000-2007 vs. 2011F-2012F*)

*Percentage point difference between compound annual rates of change 2000-2007 vs. forecasts for 2011-2012.

Source: IMF, World Economic Outlook, September 2011; Insurance Information Institute.

Latin and South American markets are

in general growing more strongly than prior to the crisis

The US, Europe and Eurasia have seen

significant slowdowns

Parts of the Middle East and South Asia

have done well

9

Current Real GDP Growth vs. Pre-Crisis Average (2000-2007 vs. 2011F-2012F*)

*Percentage point difference between compound annual rates of change 2000-2007 vs. forecasts for 2011-2012.

Source: IMF, World Economic Outlook, September 2011; Insurance Information Institute.

Growth in much of Europe today is about 2 pts.

Lower than pre-crisis

10

World Trade Volume:2010—2013F

Growth in World Trade Volume (Imports + Exports) Has Slowed But Continues to Grow

Percentage Change (%)

12.9%

5.8%

4.0%

5.6%

0%

2%

4%

6%

8%

10%

12%

14%

2010 2011 2012F 2013F

After decelerating in 2011 and 2012, global trade

growth is expected accelerate in 2013

Sources: IMF World Economic Outlook (April 2012 ); Insurance Information Institute.

11

World Trade Volume: Imports2010 – 2013F

8.8%8.1% 8.1%

11.5%

4.3%

1.8%

4.1%

15.3%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2010 2011 2012F 2013F 2010 2011 2012F 2013F

Growth (%)

Import growth in emerging economies outpaces

Advanced Economies by a wide margin.

Advanced Economies Emerging Economies

Sources: IMF World Economic Outlook (April 2012 ); Insurance Information Institute.

12

World Trade Volume: Exports2010 – 2013F

6.7% 6.6%7.2%

12.2%

5.3%

2.3%

4.7%

14.7%

0%

2%

4%

6%

8%

10%

12%

14%

16%

2010 2011 2012F 2013F 2010 2011 2012F 2013F

Growth (%)

Export growth in emerging economies outpaces Advanced Economies by a much narrower

margin than imports.

Advanced Economies Emerging Economies

Sources: IMF World Economic Outlook (April 2012 ); Insurance Information Institute.

The Strength of the Economy Will Influence P/C Insurer

Growth Opportunities

13

All Lines of Commercial Insurance Will Benefit, Including Marine

13

14

US Real GDP Growth*

* Estimates/Forecasts from Blue Chip Economic Indicators.Source: US Department of Commerce, Blue Economic Indicators 4/12; Insurance Information Institute.

2.7

%0

.9%

3.2

%2

.3%

2.9

%-0

.7%

0.6

%-4

.0%

-6.8

% -4.9

%-0

.7%

1.6

%5

.0%

3.9

%3

.8%

2.5

%2

.3%

0.4

%1

.3%

1.8

% 3.0

%2

.2%

2.3

%2

.4%

2.6

%2

.4%

2.6

%2

.9%

3.0

%4.1

%1

.1%

1.8

%2

.5% 3.6

%3

.1%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

2

00

0

2

00

1

2

00

2

2

00

3

2

00

4

2

00

5

2

00

6

07

:1Q

07

:2Q

07

:3Q

07

:4Q

08

:1Q

08

:2Q

08

:3Q

08

:4Q

09

:1Q

09

:2Q

09

:3Q

09

:4Q

10

:1Q

10

:2Q

10

:3Q

10

:4Q

11

:1Q

11

:2Q

11

:3Q

11

:4Q

12

:1Q

12

:2Q

12

:3Q

12

:4Q

13

:1Q

13

:2Q

13

:3Q

13

:4Q

Demand for Insurance Continues To Be Impacted by Sluggish Economic Conditions, but the Benefits of Even Slow Growth Will Compound and

Gradually Benefit the Economy Broadly

Real GDP Growth (%)

Recession began in Dec. 2007. Economic toll of credit crunch, housing

slump, labor market contraction has been

severe but modest recovery is underway

The Q4:2008 decline was the steepest since the Q1:1982 drop of 6.8%

2012 is expected to see a modest but choppy

acceleration in growth continuing into 2013

74

.4

73

.6

73

.6

72

.2

73

.6 76

67

.8

68

.9

68

.2

67

.7 71

.6 74

.5

74

.2 77

.5

67

.5 69

.8

74

.3

71

.5

63

.7

55

.7 59

.4 60

.9 64

.1

69

.9

75

.0

75

.3

74

.3

40

45

50

55

60

65

70

75

80

Jan

-10

Fe

b-1

0

Ma

r-1

0

Ap

r-1

0

Ma

y-1

0

Jun

-10

Jul-

10

Au

g-1

0

Se

p-1

0

Oct

-10

No

v-1

0

De

c-1

0

Jan

-11

Fe

b-1

1

Ma

r-1

1

Ap

r-1

1

Ma

y-1

1

Jun

-11

Jul-

11

Au

g-1

1

Se

p-1

1

Oct

-11

No

v-1

1

De

c-1

1

Jan

-12

Fe

b-1

2

Ma

r-1

2

Consumer Sentiment Survey (1966 = 100)

January 2010 through March 2012

Consumer confidence has been low for years amid high unemployment, falling home prices and other factors adversely impact

consumers, but improved substantially in late 2011 and early 2012

Source: University of Michigan; Insurance Information Institute

Optimism among consumers is recovering, in part due to an

improving jobs outlook, after plunging amid the debt debate debacle and S&P downgrade

15

16

16.9

16.5

16.1

13.2

10.4

11.6 12

.7

14.5 14

.9

14.7 15

.1

15.4

15.5

15.4

16.9

16.617

.117.5

17.8

17.4

9

10

11

12

13

14

15

16

17

18

19

99 00 01 02 03 04 05 06 07 08 09 10 11 12F 13F 14F 15F 16F 17F 18-22F

(Millions of Units)

Auto/Light Truck Sales, 1999-2022F

Source: U.S. Department of Commerce; Blue Chip Economic Indicators (10/11 and 4/12); Insurance Information Institute.

Car/Light Truck Sales Will Continue to Recover from the 2009 Low Point, Bolstering the Auto Insurer Growth and the Manufacturing Sector.

New auto/light truck sales fell to the lowest level since the late 1960s. Forecast for 2012-13 is

still far below 1999-2007 average of 17 million units, but a recovery is underway.

Job growth and improved credit market conditions will boost auto sales in

2012 and beyond

17

Value of Construction Put in Place, Feb. 2012 vs. Feb. 2011*

-1.4%

-21.9%

-0.7%

5.8%

10.2%

4.6%6.4%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

TotalConstruction

Total PrivateConstruction

Residential--Private

Non-Residential--

Private

Total PublicConstruction

Residential-Public

Non-Residential--

Public

Overall Construction Activity is Up, But Growth Is Entirely in the Private Sector as State/Local Government Budget Woes Continue

Growth (%)

Private sector construction activity is up in both the residential and nonresidential segments

*seasonally adjustedSource: U.S. Census Bureau, http://www.census.gov/construction/c30/c30index.html ; Insurance Information Institute.

Private: +10.2% Public: -1.4%

Public sector construction activity remains depressed

58

.3

57

.1

60

.4

59

.6

57

.8

55

.3

55

.1

55

.2

55

.3 56

.9 58

.2

58

.5 60

.8

61

.4

59

.7

59

.7

54

.2 55

.8

51

.4 52

.5

52

.5

51

.8

52

.2 53

.1 54

.1

52

.4 53

.4 54

.8

40

45

50

55

60

65

Jan

-10

Fe

b-1

0

Ma

r-1

0

Ap

r-1

0

Ma

y-1

0

Jun

-10

Jul-

10

Au

g-1

0

Se

p-1

0

Oct

-10

No

v-1

0

De

c-1

0

Jan

-11

Fe

b-1

1

Ma

r-1

1

Ap

r-1

1

Ma

y-1

1

Jun

-11

Jul-

11

Au

g-1

1

Se

p-1

1

Oct

-11

No

v-1

1

De

c-1

1

Jan

-12

Fe

b-1

2

Ma

r-1

2

Ap

r-1

2

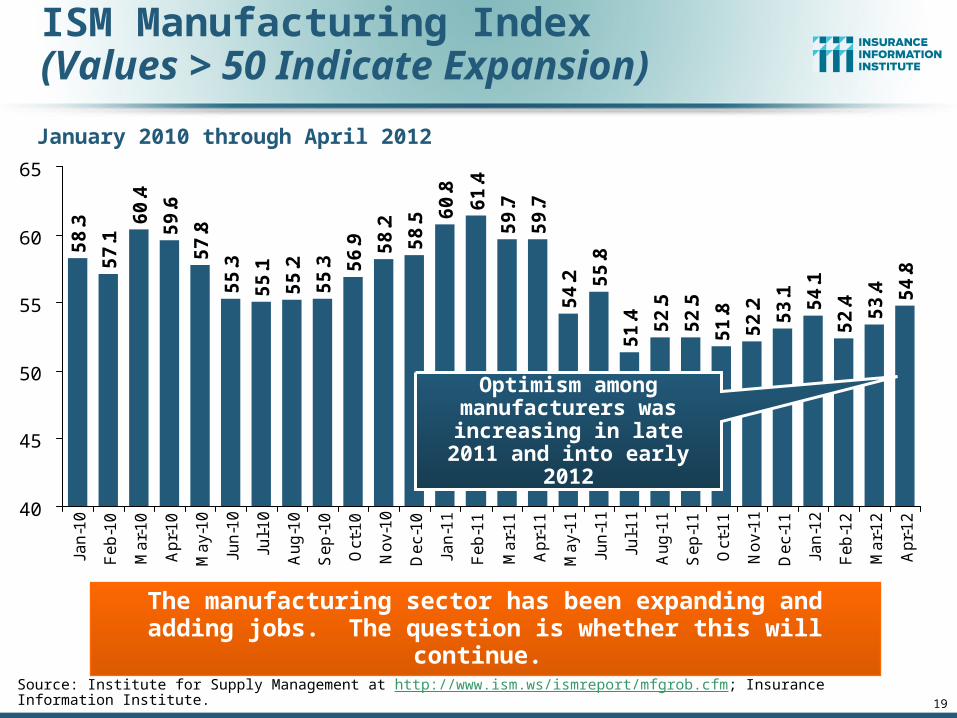

ISM Manufacturing Index(Values > 50 Indicate Expansion)

January 2010 through April 2012

The manufacturing sector has been expanding and adding jobs. The question is whether this will continue.

Source: Institute for Supply Management at http://www.ism.ws/ismreport/mfgrob.cfm; Insurance Information Institute.

Optimism among manufacturers was

increasing in late 2011 and into early 2012

19

20

$200,000

$300,000

$400,000

$500,000

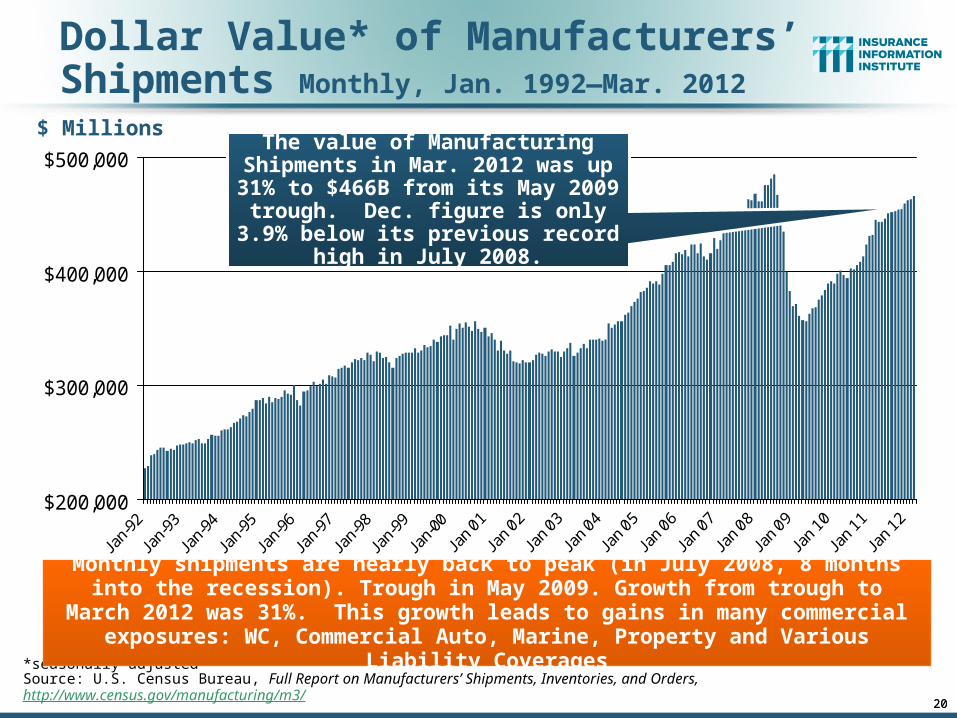

Dollar Value* of Manufacturers’ Shipments Monthly, Jan. 1992—Mar. 2012

*seasonally adjustedSource: U.S. Census Bureau, Full Report on Manufacturers’ Shipments, Inventories, and Orders, http://www.census.gov/manufacturing/m3/

Monthly shipments are nearly back to peak (in July 2008, 8 months into the recession). Trough in May 2009. Growth from trough to March 2012 was 31%. This

growth leads to gains in many commercial exposures: WC, Commercial Auto, Marine, Property and Various Liability Coverages

The value of Manufacturing Shipments in Mar. 2012 was up 31% to $466B from its May 2009 trough.

Dec. figure is only 3.9% below its previous record high in July 2008.

$ Millions

20

21

Manufacturing Growth for Selected Sectors, 2012 vs. 2011*

12.7%

8.5%6.2%

15.6%

6.6%

10.8%7.1%

9.8%11.4%

31.4%

13.5%

7.2%

0%

5%

10%

15%

20%

25%

30%

35%

All

Ma

nu

fact

uri

ng

Du

rab

le M

fg.

Pri

ma

ryM

eta

ls

Ma

chin

ery

Ele

ctri

cal

Eq

uip

.

Tra

nsp

ort

atio

nE

qu

ip.

No

n-D

ura

ble

Mfg

.

Fo

od

Pro

du

cts

Pe

tro

leu

m &

Co

al

Ch

em

ica

l

Pla

stic

s &

Ru

bb

er

Te

xtile

Pro

du

cts

Manufacturing Is Expanding Across a Wide Range of Sectors that Will Contribute to Growth in Insurable Exposures Including: WC, Commercial

Property, Commercial Auto and Many Liability Coverages

Growth (%)

Manufacturing of durable goods has been

especially strong

*Seasonally adjusted; Date are YTD comparing data through Feb. 2012 to the same period in 2011.Source: U.S. Census Bureau, Full Report on Manufacturers’ Shipments, Inventories, and Orders, http://www.census.gov/manufacturing/m3/

Durables: +11.4% Non-Durables: +8.5%

66%

68%

70%

72%

74%

76%

78%

80%

82%

Mar

01

Jun 0

1

Sep 0

1

Dec 0

1

Mar

02

Jun 0

2

Sep 0

2

Dec 0

2

Mar

03

Jun 0

3

Sep 0

3

Dec 0

3

Mar

04

Jun 0

4

Sep 0

4

Dec 0

4

Mar

05

Jun 0

5

Sep 0

5

Dec 0

5

Mar

06

Jun 0

6

Sep 0

6

Dec 0

6

Mar

07

Jun 0

7

Sep 0

7

Dec 0

7

Mar

08

Jun 0

8

Sep 0

8

Dec 0

8

Mar

09

Jun 0

9

Sep 0

9

Dec 0

9

Mar

10

Jun 1

0

Sep 1

0

Dec 1

0

Mar

11

Jun 1

1

Sep 1

1

Dec 1

1

Recovery in Capacity Utilization is a Positive Sign for Commercial Exposures

Source: Federal Reserve Board statistical releases at http://www.federalreserve.gov/releases/g17/Current/default.htm. 22

Percent of Industrial Capacity

Hurricane Katrina

March 2001-November 2001

recession

“Full Capacity”

The closer the economy is to operating at “full

capacity,” the greater the inflationary pressure

The US operated at 78.6% of industrial capacity in Mar. 2012, above the June 2009

low of 68.3% and close to its post-crisis peak

December 2007-June 2009 Recession

March 2001 through March 2012

22

23

Global Industrial Production (2000-Feb. 2012)

Source: IMF, World Economic Outlook, April 2012; Insurance Information Institute.

12

Global industrial production has

been volatile but is growing

25

43,6

9448

,125

69,3

0062

,436

64,0

04 71,2

77 81,2

3582

,446

63,8

5363

,235

64,8

53 71,5

4970

,643

62,3

0452

,374

51,9

5953

,549

54,0

2744

,367

37,8

8435

,472

40,0

9938

,540

35,0

3734

,317

39,2

0119

,695 28

,322

43,5

4660

,837

56,2

8247

,806

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11

Business Bankruptcy Filings,1980-2011

Sources: American Bankruptcy Institute at http://www.abiworld.org/AM/AMTemplate.cfm?Section=Home&TEMPLATE=/CM/ContentDisplay.cfm&CONTENTID=61633; Insurance Information Institute

Significant Exposure Implications for All Commercial Lines as Business Bankruptcies Begin to Decline

2011 bankruptcies totaled 47,806, down 15.1% from 56,282 in 2010—the second consecutive year of decline. Business bankruptcies more

than tripled during the financial crisis.

% Change Surrounding Recessions

1980-82 58.6%1980-87 88.7%1990-91 10.3%2000-01 13.0%2006-09 208.9%*

25

26

Private Sector Business Starts, 1993:Q2 – 2011:Q3*

175

186

174

180

186

192

188

187 18

918

6 190 19

419

119

9 204

202

195

196

196

206

206

201

192

198

206

206

203

211

205

212

200 20

520

420

419

720

320

920

119

219

219

320

1 204

202

210 21

220

921

6 220 22

322

022

021

022

121

220

421

820

920

720

719

919

1 193

172 17

616

918

417

5 179

188

200

183 18

7 191

203

150

160

170

180

190

200

210

220

230

93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11

Business Starts Were Down Nearly 20% in the Recession, Holding Back Most Types of Commercial Insurance Exposure, But

Are Recovering Slowly* Data through September 30, 2011 are the latest available as of May 2, 2012; Seasonally adjusted. **Annualized based on data through 9/30.Source: Bureau of Labor Statistics, http://www.bls.gov/news.release/cewbd.t08.htm.

(Thousands)

Business starts were up 3.5% to 561,000 in the first 9 months of 2011 vs. first 9

months 2010. 722,000 new business starts were recorded in 2010, up 3.6% from

697,000 in 2009, which was the slowest year for new business starts since 1993

Business Starts2006: 872,0002007: 843,0002008: 790,0002009: 697,000 2010: 722,000 2011: 748,000**

26

27

12 Industries for the Next 10 Years: Insurance Solutions Needed

Export-Oriented Industries

Health Sciences

Health Care

Energy (Traditional)

Alternative Energy

Petrochemical

Agriculture

Natural Resources

Technology (incl. Biotechnology)

Light Manufacturing

Insourced Manufacturing

Many industries are

poised for growth, though

insurers’ ability to

capitalize on these

industries varies widely

Shipping (Rail, Marine, Trucking)

Global Oil Consumption and Price, 2008 – 2035F

Millions of Barrels per Day Nominal Price/BBL

*Source: US Energy Information Administration; Insurance Information Institute

85

.5

83

.7 86

.0 87

.4 88

.9 90

.3

90

.4

91

.1 92

.5

92

.9

93

.5

94

.3

95

.1 96

.1

97

.1

98

.2 99

.3

10

0.5

10

1.8

10

3.2

10

4.5

10

6.1

10

7.6

10

9.1

11

0.8

92

.0

91

.5

89

.6

$108

.10

$112

.36

$114

.21

$115

.96

$117

.54

$118

.99

$120

.25

$121

.34

$122

.30

$123

.09

$123

.71

$124

.20

$124

.53

$124

.68

$124

.94

$110

.30

$105

.71

$103

.15

$100

.50

$97.

62

$94.

58

$91.

38

$83.

21

$61.

66

$100

.51

$85.

73

$88.

03

$78.

03

80

85

90

95

100

105

110

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

0

20

40

60

80

100

120

140

Total Consumption Nominal Price (Light, Low Sulfur Crude)

Oil Will Become Relatively More Expensive Over Time, With Price Increases Outstripping Income Growth in Many Parts of the World

The nominal price of oil is expected to rise by 2.8% per year

on average through 2035

Global oil consumption is expected to rise by 1.1% per

year on average through 2035

29

US Natural Gas Production and Non-Hydro Renewable Electricity Generation, 1990-2035P

Source: US Energy Information Administration, Annual Energy Outlook 2011; Insurance Information Institute.

Shale gas production is expected to grow rapidly in the US

Wind is expected to account for the majority of renewable

electricity generation

Tight gas production involves controversial

hydraulic fracturing (fracking) techniques

347.7

472.4508.3

551.5595.7

637.3678.3

462.1

0

100

200

300

400

500

600

700

800

1990 2005 2006 2010P 2015P 2020P 2025P 2030P

World Primary Energy Consumption, 1990-2030P

Source: Energy Information Administration, 2009 International Energy Outlook, Insurance Information Institute.

Between 2006 and 2030, energy consumption in projected to increase

annually by 1.5% worldwide but only 0.5% in the US

Quadrillion BTUs

Global energy consumption is

expected to increase by 33.4% between 2010 and 2030 but by only 12% in

the US

31

Presidential Politics & the P/C Insurance Industry

How Is Profitability Affected by the President’s Political Party?

31

15.10%

9.40%

8.93%

8.65%

8.35%

7.98%

7.68%

6.98%

6.97%

6.65%

5.43%

5.03%

4.83%

4.43%

3.55%

16.43%

0% 2% 4% 6% 8% 10% 12% 14% 16% 18%

Carter

Reagan II

G.W. Bush II

Nixon

Clinton I

G.H.W. Bush

Clinton II

Reagan I

Nixon/Ford

Truman

Obama

Eisenhower I

Eisenhower II

G.W. Bush I

Johnson

Kennedy/Johnson

*Truman administration ROE of 6.97% based on 3 years only, 1950-52; ROEs for the years 2008 forward exclude mortgage and financial guaranty segments.Estimated ROE for 2012 = 7.0%. Source: Insurance Information Institute

OVERALL RECORD: 1950-2012*

Democrats 7.67%Republicans 7.97%

Party of President has marginal bearing on profitability of P/C insurance industry

P/C Insurance Industry ROE by Presidential Administration, 1950- 2012*

-5%

0%

5%

10%

15%

20%

25%

50

52

54

56

58

60

62

64

66

68

70

72

74

76

78

80

82

84

86

88

90

92

94

96

98

00

02

04

06

08

10

12

E

BLUE = Democratic President RED = Republican President

Tru

man Nixon/Ford

Ken

ned

y/

Joh

nso

n

Eis

enh

ow

er

Car

ter

Reagan/Bush I Clinton Bush II

P/C insurance Industry ROE by Presidential Party Affiliation, 1950- 2012*

*ROEs for the years 2008 forward exclude mortgage and financial guaranty segments; Estimated 2012 ROE = 7.0%Source: Insurance Information Institute

Ob

ama

34

Election 2012: Political Issues Impacting Insurers

Presidential Race Is Tight Potential for Senate to Flip Republican Affordable Care Act/Health Care Reform (ObamaCare)

Romney, Republicans generally vow to repeal the Act Complete repeal is unlikely as several popular ACA provisions are already implemented Supreme Court will rule on the constitutionality of the Act in June; Outcome uncertain

Dodd-Frank Act/Financial Services Reform & Implementation Republicans refer to DFA as a “confidence killer” and want it scaled back Outright repeal is highly unlike irrespective of election outcome Systemic criteria have been developed; Designations in late 2012 Financial Stability Oversight Council: Current/future composition impacted by election Changes to DFA and/or implementation will have little impact on P/C insurers

Key Committee Shifts Possible Senate Banking Chair: Tim Johnson (D-SD) Richard Shelby (R-AL) House Finl. Svcs. Chair: Spencer Bachus (R-AL) Jeb Hensarling (R-TX) (term limits)

– If House flipped Chair would go to Maxine Waters (D-CA)

Federal Insurance Office If Romney wins, he will appoint a new Treasury Secretary FIO leadership, agenda and funding could be impacted Secretary Geithner likely to step down after election even if Obama is re-elected

Agent Licensing, NFIP

35

The Unfortunate Nexus: Opportunity, Risk & Instability

Most of the Global Economy’s Future Gains Will be Fraught with Much

Greater Risk and Uncertainty than in the Past

36

Global Real (Inflation Adjusted) NonlifePremium Growth: 1980-2010

Source: Swiss Re, sigma, No. 2/2010.

Nonlife premium growth in emerging markets has

exceeded that of industrialized countries in

27 of the past 31 years, including the entirety of the

global financial crisis..

Real nonlife premium growth is very erratic in part to inflation volatility in emerging markets as

well as a lack of consistent cyclicality

Average: 1980-2010

Industrialized Countries: 3.8%

Emerging Markets: 9.2%

Overall Total: 4.2%

37

Nonlife Real Premium Growth in 2010

Source: Swiss Re, sigma, No. 2/2011.

Latin and South American markets performed

relatively well during and after the global financial crisis in terms of growth

There was also growth in the Middle East, East and South Asia as well as Australia and New

Zealand

38

Nonlife Real Premium Growth Ratesby Region: 2000-2009 and 2010

Source: Swiss Re, sigma, No. 2/2011.

Every emerging

market region except Central

and Eastern Europe

experienced growth during the financial

crisis and into 2010

The Middle East and many emerging market economies continued to grow during the global financial crisis and

continued to benefit from foreign direct investment

39

Distribution of Nonlife Premium: Industrialized vs. Emerging Markets, 2009

Sources: Swiss Re; Insurance Information Institute research.

Although premium growth throughout the industrialized world was negative in 2009, its share of global nonlife premiums remained very high at nearly 86%--accounting for nearly $1.5 trillion in premiums.

The financial crisis and sluggish recovery in the major insurance markets will accelerate the expansion of the emerging market sector

Premium Growth Facts

14.3%85.7%

Industrialized Economies

$1, 485.8

Emerging Markets$248.8

2009, $Billions

Developing markets now account for 47% of global

GDP but just 14% of nonlife premiums

40

Political Risk in 2011/12: Greatest Business Opportunities Are Often in Risky Nations

Source: Maplecroft

The fastest growing markets are generally

also among the politically riskiest,

including East and South Asia

Heightened risk has economic and insurance implications

Much of the middle East and North Africa have

experienced and continue to experience

political turmoil

41

The “Arab Spring” Has Increased Uncertainty in an Already Volatile Part of the World

Source: Wikipedia as of Nov. 7, 2011; Insurance Information Institute research.

Some energy-rich nations have been among the most

unstable in 2011/12

Longer-run, significant

investment and insurance

opportunities exist throughout

the region

Government overthrown Sustained civil disorder and governmental changes Protests and governmental changes Major protests Minor protests Protests outside the Arab world

Arab Springالربيع العربي

Country RiskThe risk that country-specific factors could adversely affect an insurer’s

ability to pay its financial obligations

Economic Risk

Macroeconomy

Prospects

Government Finance

Political Risk

Business Environment

Government Stability

Social Stability

Legal System

Financial System Risk

Non-Insurance

Insurance

Banking System

Reporting Standards & Regulation

Sovereign Debt

Government & Legislation

Supervisory Authority

Insurer Accountability

CRT-1Lowest Risk

CRT-5Highest Risk

CRT-3Moderate Risk

Source: A.M. Best.

Country Risk Relates to Insurance Market Development

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

Country Risk Score (from lower to higher risk)

Pen

etra

tio

n (

%)

Low Risk High Risk

Source: A.M. Best.

Low risk countries have high insurance

penetration rates and afford fewer

growth opportunities

Higher risk countries have low insurance

penetration rates and often offer more

growth opportunities

45

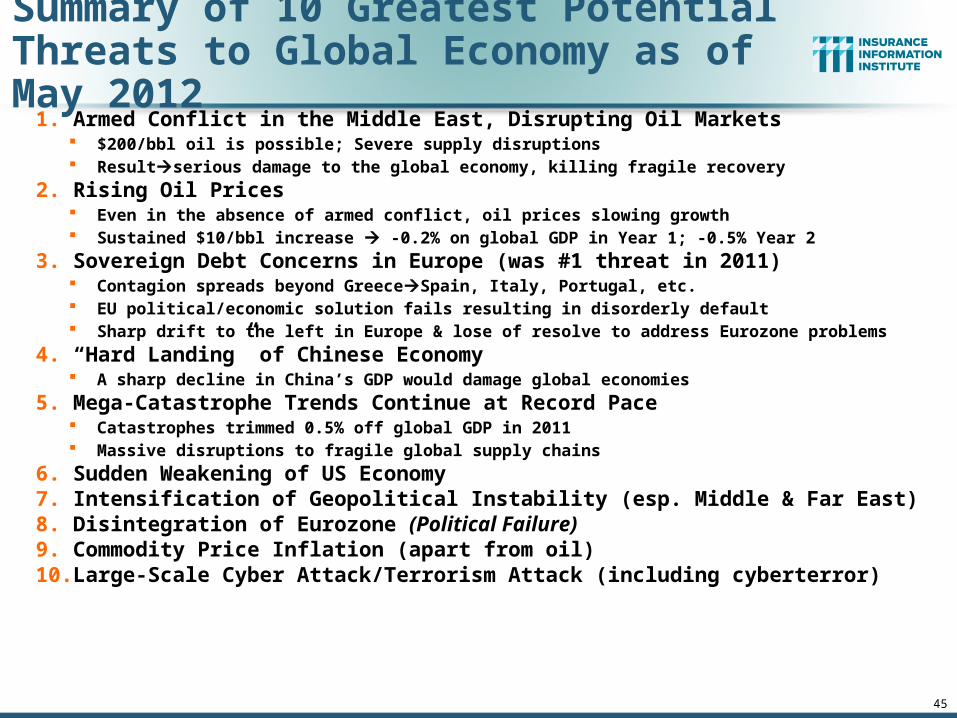

Summary of 10 Greatest Potential Threats to Global Economy as of May 2012

1. Armed Conflict in the Middle East, Disrupting Oil Markets $200/bbl oil is possible; Severe supply disruptions Resultserious damage to the global economy, killing fragile recovery

2. Rising Oil Prices Even in the absence of armed conflict, oil prices slowing growth Sustained $10/bbl increase -0.2% on global GDP in Year 1; -0.5% Year 2

3. Sovereign Debt Concerns in Europe (was #1 threat in 2011) Contagion spreads beyond GreeceSpain, Italy, Portugal, etc. EU political/economic solution fails resulting in disorderly default Sharp drift to the left in Europe & lose of resolve to address Eurozone problems

4. “Hard Landing” of Chinese Economy A sharp decline in China’s GDP would damage global economies

5. Mega-Catastrophe Trends Continue at Record Pace Catastrophes trimmed 0.5% off global GDP in 2011 Massive disruptions to fragile global supply chains

6. Sudden Weakening of US Economy7. Intensification of Geopolitical Instability (esp. Middle & Far East)8. Disintegration of Eurozone (Political Failure)9. Commodity Price Inflation (apart from oil)10. Large-Scale Cyber Attack/Terrorism Attack (including cyberterror)

Global Catastrophe Loss Developments and Trends

46

2011 Rewrote Catastrophe Loss and Insurance History

But Will Losses Turn the Market?

46

Geophysical events(earthquake, tsunami, volcanic activity)

Meteorological events (storm)

Hydrological events(flood, mass movement)

Selection of significant loss events (see table)

Natural catastrophes

Earthquake, tsunami Japan, 11 March

EarthquakeNew Zealand, 22 Feb.

Cyclone Yasi Australia, 2–7 Feb.

Landslides, flash floodsBrazil, 12/16 Jan.

Floods, flash floods Australia, Dec. 2010–Jan. 2011

Severe storms, tornadoesUSA, 22–28 April

Severe storms, tornadoesUSA, 20–27 May

WildfiresUSA, April/Sept.

EarthquakeNew Zealand, 13 June

FloodsUSA, April–May

Climatological events(extreme temperature, drought, wildfire)

Number of Events: 820Number of Events: 820

DroughtUSA, Oct. 2010– ongoing

Hurricane IreneUSA, Caribbean22 Aug.–2 Sept.

WildfiresCanada, 14–22 May

DroughtSomaliaOct. 2010–Sept. 2011

FloodsPakistanAug.–Sept.

FloodsThailandAug.–Nov.

Earthquake Turkey23 Oct.

Flash floods, floodsItaly, France, Spain4–9 Nov.

Floods, landslidesGuatemala, El Salvador11–19 Oct.

Tropical Storm WashiPhilippines, 16–18 Dec.

Winter Storm JoachimFrance, Switzerland, Germany, 15–17 Dec.

48Source: MR NatCatSERVICE

Natural Loss Events, 2011

World Map

Natural Catastrophes Worldwide 2011Insured losses US$ 105bn - Percentage distribution per continent

Continent Insured losses US$ m

America (North and South

America)40,000

Europe 2,000

Africa Minor damages

Asia 45,000

Australia/Oceania 18,000

37%

2%

44%

17%

<1%

49Source: MR NatCatSERVICE

In 2011, 61% of insured natural catastrophe losses

were in the Asia/Pacific region, nearly 3.5 times the

average of 13% over the prior 30 years (1981-2010)

In 2011, just 37% of insured natural

catastrophe losses were in the

Americas, barely half the average of 66%

over the prior 30 years (1981-2010)

49

Natural Catastrophes Worldwide 1980 – 2011 Insured losses US$ 870bn - Percentage distribution per continent

Continent Insured losses US$ m

America (North and South

America)566,000

Europe 146,000

Africa 2,000

Asia 115,000

Australia/Oceania 41,000

66%

16%

<1%

13%

5%

50Source: MR NatCatSERVICE

In 2011, 61% of natural catastrophe losses were

in the Asia/Pacific region, nearly 3.5 times the

average of 13% over the prior 30 years (1981-2010)

50

52

Top 16 Most Costly World Insurance Losses, 1970-2011**

(Insured Losses, 2011 Dollars, $ Billions)

*Average of range estimates of $35B - $40B as of 1/4/12; Privately insured losses only.**Figures do not include federally insured flood losses.Sources: Swiss Re sigma 1/2011; Munich Re; Insurance Information Institute research.

$11.9$13.0 $13.0$13.1

$19.1$21.3

$24.0$25.0

$37.5

$47.6

$7.7 $8.1 $8.3 $8.5 $9.3 $9.7

$0$5

$10$15$20$25$30$35$40$45$50

Hugo (1989)

WinterStormDaria(1991)

ChileQuake(2010)

Ivan (2004)

TyphoonMirielle(1991)

Charley(2004)

Wilma(2005)

ThailandFloods(2011)

NewZealandQuake(2011)

Ike (2008)

Northridge(1994)

SpringTornadoes/

Storms(2011)

WTC TerrorAttack(2001)

Andrew(1992)

JapanQuake,

Tsunami(2011)*

Katrina(2005)

Large catastrophes in Asia/Pacific and South

America Have dominated mega-losses since 2010

5 of the top 14 most expensive

catastrophes in world history have occurred within the past 2 years

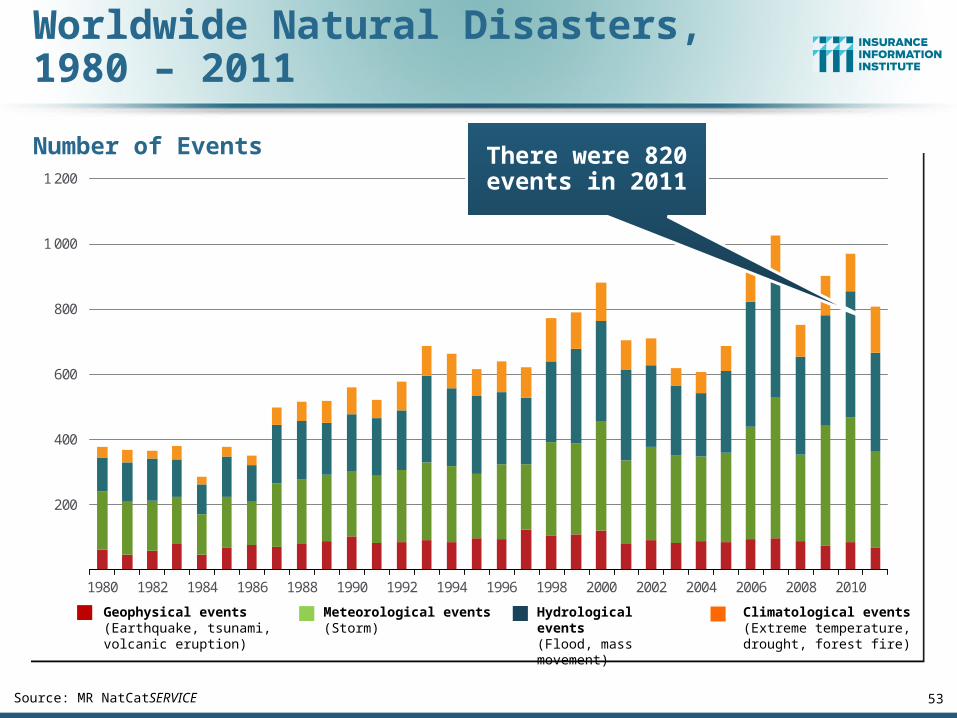

Worldwide Natural Disasters,1980 – 2011

Number of Events

Source: MR NatCatSERVICE 53

Meteorological events(Storm)

Hydrological events(Flood, mass movement)

Climatological events(Extreme temperature, drought, forest fire)

Geophysical events(Earthquake, tsunami, volcanic eruption)

200

400

600

800

1 000

1 200

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

There were 820 events in 2011

55

U.S. Insured Catastrophe Loss Update

2011 Was One of the Most Expensive Years on Record

55

56

Top 14 Most Costly Disastersin U.S. History

(Insured Losses, 2011 Dollars, $ Billions)

*Losses will actually be broken down into several “events” as determined by PCS. Includes losses for the period April 1 – June 30.Sources: PCS; Insurance Information Institute inflation adjustments.

$9.0$11.9 $13.1

$19.1$21.3

$24.0 $25.0

$47.6

$8.5$7.7$6.5$5.5$4.4$4.3

$0$5

$10$15$20$25$30$35$40$45$50

Irene(2011)

Jeanne(2004)

Frances(2004)

Rita (2005)

Hugo (1989)

Ivan (2004)

Charley(2004)

Wilma(2005)

Ike (2008)

Northridge(1994)

SpringTornadoes& Storms*

(2011)

9/11Attack(2001)

Andrew(1992)

Katrina(2005)

Taken as a single event, the Spring 2011 tornado and storm season are

is the 4th costliest event in US insurance history

Hurricane Irene became the 11th most expense

hurricane in US history

Nu

mb

er

Geophysical (earthquake, tsunami, volcanic activity)

Climatological (temperature extremes, drought, wildfire)

Meteorological (storm)

Hydrological (flood, mass movement)

Natural Disasters in the United States, 1980 – 2011Number of Events (Annual Totals 1980 – 2011)

Source: MR NatCatSERVICE 57

37

8

51

2

50

100

150

200

250

300

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

There were 117 natural disaster events in 2011

59

$1

2.3

$1

0.7

$3

.7 $1

4.0

$1

1.3

$6

.0

$3

3.9

$7

.4 $1

5.9 $

32

.9

$7

1.7

$1

0.3

$7

.3

$2

8.5

$1

1.2

$1

4.1

$3

2.3

$1

00

.0

$1

3.7

$4

.7

$7

.8

$3

6.9

$8

.6

$2

5.8

$0

$20

$40

$60

$80

$100

$120

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11*20??

US Insured Catastrophe Losses

*PCS figure as of April 6, 2012.Note: 2001 figure includes $20.3B for 9/11 losses reported through 12/31/01 ($25.9B 2011 dollars). Includes only business and personal property claims, business interruption and auto claims. Non-prop/BI losses = $12.2B ($15.6B in 2011 dollars.) Sources: Property Claims Service/ISO; Insurance Information Institute.

US CAT Losses in 2011 Were the 5th Highest in US History on An Inflation Adjusted Basis

$100 Billion CAT Year is Coming Eventually

Record Tornado Losses Caused

2011 CAT Losses to Surge

($ Billions, 2011 Dollars)

59

62

Combined Ratio Points Associated with Catastrophe Losses: 1960 – 2011*

*Insurance Information Institute estimates for 2010 and 2011 based on A.M. Best data.Notes: Private carrier losses only. Excludes loss adjustment expenses and reinsurance reinstatement premiums. Figures are adjusted for losses ultimately paid by foreign insurers and reinsurers.Source: ISO; Insurance Information Institute.

0.4

1.2

0.4 0.

8 1.3

0.3 0.4 0.

71.

51.

00.

40.

4 0.7

1.8

1.1

0.6

1.4 2.

01.

3 2.0

0.5

0.5 0.7

3.0

1.2

2.1

8.8

2.3

5.9

3.3

2.8

1.0

3.6

2.9

1.6

5.4

1.6

3.3

3.3

8.1

2.7

1.6

5.0

2.6

4.4

8.0

3.6

0.9

0.1

1.1

1.1

0.8

0

1

2

3

4

5

6

7

8

9

10

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

The Catastrophe Loss Component of Private Insurer Losses Has Increased Sharply in Recent Decades

Avg. CAT Loss Component of the Combined Ratio

by Decade

1960s: 1.04 1970s: 0.85 1980s: 1.31 1990s: 3.39 2000s: 3.52 2010s: 6.20*

Combined Ratio Points

U.S. Thunderstorm Loss Trends, 1980 – 2011

63Source: Property Claims Service, MR NatCatSERVICE

Average thunderstorm

losses are up more than 5 fold since the early 1980s

Hurricanes get all the headlines, but thunderstorms are consistent

producers of large scale loss. 2008-2011 are the most expensive

years on record.

Thunderstorm losses in 2011 totaled a record

$25.8 billion

64

P/C Insurance Industry Financial Overview

Profit Recovery Was Set Back in 2011 by High Catastrophe

Loss & Other Factors

64

P/C Net Income After Taxes1991–2011 ($ Millions)

$1

4,1

78

$5

,84

0

$1

9,3

16

$1

0,8

70

$2

0,5

98

$2

4,4

04 $

36

,81

9

$3

0,7

73

$2

1,8

65

$3

,04

6

$3

0,0

29

$6

2,4

96

$3

,04

3

$3

5,2

04

$1

9,1

50$2

8,6

72

-$6,970

$6

5,7

77

$4

4,1

55

$2

0,5

59

$3

8,5

01

-$10,000

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11*

2005 ROE*= 9.6% 2006 ROE = 12.7% 2007 ROE = 10.9% 2008 ROE = 0.1% 2009 ROE = 5.0% 2010 ROE = 6.6% 2011:Q3 ROAS1 = 3.5%

P-C Industry 2011 profits were down 46% to $19.2B vs. 2010, due

primarily to high catastrophe losses and as non-cat

underwriting results deteriorated

* ROE figures are GAAP; 1Return on avg. surplus. Excluding Mortgage & Financial Guaranty insurers yields a 4.6% ROAS for 2011, 7.6% for 2010 and 7.4% for 2009.Sources: A.M. Best, ISO, Insurance Information Institute

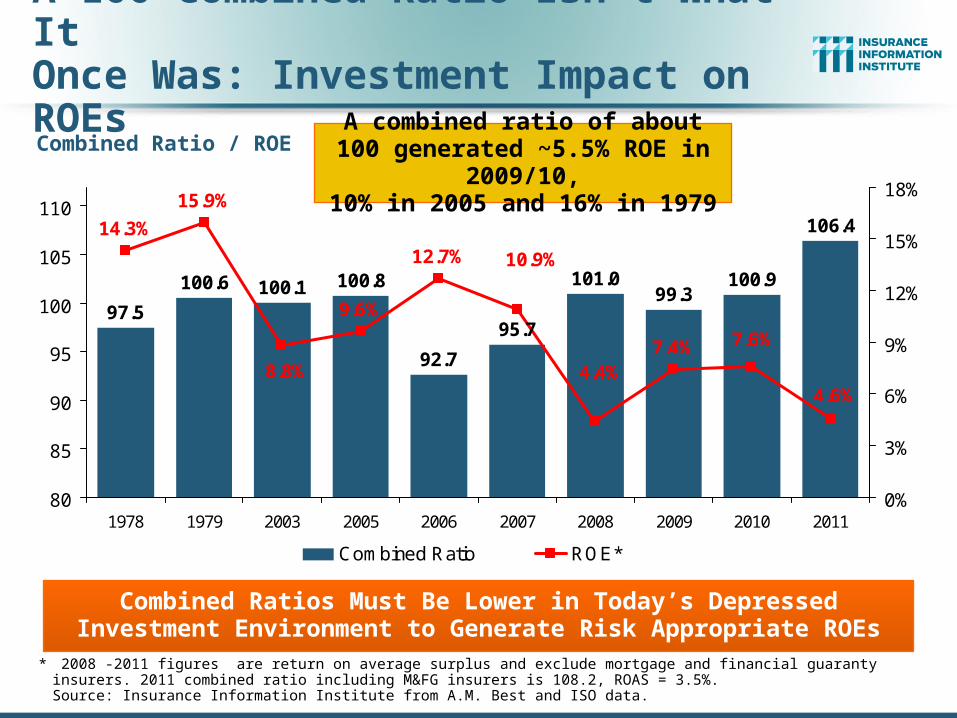

A 100 Combined Ratio Isn’t What ItOnce Was: Investment Impact on ROEs

Combined Ratio / ROE

* 2008 -2011 figures are return on average surplus and exclude mortgage and financial guaranty insurers. 2011 combined ratio including M&FG insurers is 108.2, ROAS = 3.5%. Source: Insurance Information Institute from A.M. Best and ISO data.

97.5

100.6 100.1 100.8

92.7

101.099.3

100.9

106.4

95.7

4.6%

7.6%7.4%4.4%

9.6%

15.9%

14.3%

12.7% 10.9%

8.8%

80

85

90

95

100

105

110

1978 1979 2003 2005 2006 2007 2008 2009 2010 20110%

3%

6%

9%

12%

15%

18%

Combined Ratio ROE*

Combined Ratios Must Be Lower in Today’s DepressedInvestment Environment to Generate Risk Appropriate ROEs

A combined ratio of about 100 generated ~5.5% ROE in 2009/10,

10% in 2005 and 16% in 1979

-5%

0%

5%

10%

15%

20%

25%

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09

10

11

*

Profitability Peaks & Troughs in the P/C Insurance Industry, 1975 – 2011*

*Profitability = P/C insurer ROEs are I.I.I. estimates. 2011 figure is an estimate based on ROAS data. Note: Data for 2008-2011 exclude mortgage and financial guaranty insurers. For 2011:Q3 ROAS = 3.5% including M&FG.Source: Insurance Information Institute; NAIC, ISO, A.M. Best.

1977:19.0% 1987:17.3%

1997:11.6%2006:12.7%

1984: 1.8% 1992: 4.5% 2001: -1.2%

10 Years

10 Years9 Years

2011:4.6%*

History suggests next ROE peak will be in 2016-2017

ROE

1975: 2.4%

The BIG Question:When Will the Market Turn?

68

Are Catastrophes and Other Factors Pressuring Insurance Markets?

68

69

Criteria Necessary for a “Market Turn”:All Four Criteria Must Be Met

Criteria Status Comments

Sustained Period of

Large Underwriting

LossesEarly Stage,

Inevitable

•Apart from 2011 CAT losses, overall p/c underwriting losses remain modest•Combined ratios (ex-CATs) still in low 100s (vs. 110+ at onset of last hard market)•Prior-year reserve releases continue to reduce u/w losses, boost ROEs, though more modestly

Material Decline in Surplus/ Capacity

Entered 2011 At Record High; Only

Small Decline

•Surplus hit a record $565B as of 3/31/11•Fell just 1.6% through 12/31/11 from 12/31/10•Will likely see new record in 2012•Little excess capacity remains in reinsurance markets•Modest growth in demand for insurance is insufficient to absorb much excess capacity

Tight Reinsurance

MarketSomewhat in

Place

•Much of the global “excess capacity” was eroded by cats•Higher prices in Asia/Pacific•Modestly higher pricing for US risks

Renewed Underwriting

& Pricing Discipline

Some Firming esp. in

Property, WC

•Commercial lines pricing trends have turned from negative to flat and now positive, esp. Property & WC; •Competition remains intense as many seek to maintain market share

Sources: Barclays Capital; Insurance Information Institute.

1. UNDERWRITING

70

Have Underwriting Losses Been Large Enough for Long Enough to Turn the Market?

70

71

P/C Insurance Industry Combined Ratio, 2001–2011*

* Excludes Mortgage & Financial Guaranty insurers 2008--2011. Including M&FG, 2008=105.1, 2009=100.7, 2010=102.4, 2011=106.4 Sources: A.M. Best, ISO.

95.7

99.3100.8

108.2

101.0

92.6

100.898.4

100.1

107.5

115.8

90

100

110

120

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011*

Best Combined

Ratio Since 1949 (87.6)

As Recently as 2001, Insurers Paid Out

Nearly $1.16 for Every $1 in Earned

Premiums

Relatively Low CAT Losses, Reserve Releases

Cyclical Deterioration

Heavy Use of Reinsurance Lowered Net

Losses

Relatively Low CAT Losses, Reserve Releases

Avg. CAT Losses,

More Reserve Releases

Higher CAT

Losses, Shrinking Reserve

Releases, Toll of Soft

Market

Underwriting Gain (Loss)1975–2011E*

* Includes mortgage and financial guaranty insurers in all yearsSources: A.M. Best, ISO; Insurance Information Institute.

Large Underwriting Losses Are NOT Sustainable in Current Investment Environment

-$55

-$45

-$35

-$25

-$15

-$5

$5

$15

$25

$35

75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 1011*

Cumulative underwriting deficit from 1975 through

2011 is $479B

($ Billions) Underwriting losses in

2011 totaled $36.5B, the

largest since 2001

109.4110.2

118.8

109.5

112.5

110.2

107.6

104.1

109.7 110.2

102.5

105.4

91.2

94.8

101.299.5

101.0

107.5

102.0102.0

111.1112.3

122.3

90

95

100

105

110

115

120

125

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09

10

11

P

12

F

Co

mm

erc

ial L

ine

s C

om

bin

ed

Ra

tio

*2007-2012 figures exclude mortgage and financial guaranty segments.Source: A.M. Best; Insurance Information Institute

Commercial Lines Combined Ratio, 1990-2012F*

Commercial lines underwriting

performance in 2011 was the worst since 2002

74

75

2

(2)

(8)

(3)

(7)(10) (10)

(4)

(0)

11

24

15

119

(5)

(9)

(14)

(10) (11)(7)

(5)(2)

-$20

-$15

-$10

-$5

$0

$5

$10

$15

$20

$25

$309

2

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09

10

11

E

12

F

13

F

Pri

or

Yr.

Re

se

rve

Re

lea

se

($

B)

-6

-4

-2

0

2

4

6

8 Imp

ac

t on

Co

mb

ine

d R

atio

(Po

ints

)

Prior Yr. ReserveDevelopment ($B)

Impact onCombined Ratio(Points)

P/C Reserve Development, 1992–2013F

Reserve Releases Remained Strong in 2010 But Tapered Off in 2011. Releases Are Expected to

Further Diminish in 2012 and 2103Note: 2005 reserve development excludes a $6 billion loss portfolio transfer between American Re and Munich Re. Including this transaction, total prior year adverse development in 2005 was $7 billion. The data from 2000 and subsequent years excludes development from financial guaranty and mortgage insurance. Sources: Barclays Capital; A.M. Best.

Prior year reserve releases totaled $8.8

billion in the first half of 2010, up from

$7.1 billion in the first half of 2009

2. SURPLUS/CAPITAL/CAPACITY

76

Have Large Global Losses Reduced Capacity in the Industry, Setting

the Stage for a Market Turn?

76

77

Policyholder Surplus, 2006:Q4–2011:Q4

Sources: ISO, A.M .Best.

($ Billions)

$487.1$496.6

$512.8$521.8

$478.5

$455.6

$437.1

$463.0

$490.8

$511.5

$540.7$530.5

$544.8

$559.2 $559.1

$538.6

$550.3

$564.7

$505.0$515.6$517.9

$420

$440

$460

$480

$500

$520

$540

$560

$580

06:Q4 07:Q1 07:Q2 07:Q3 07:Q4 08:Q1 08:Q2 08:Q3 08:Q4 09:Q1 09:Q2 09:Q3 09:Q4 10:Q1 10:Q2 10:Q3 10:Q4 11:Q1 11:Q2 11:Q3 11:Q4

2007:Q3Previous Surplus Peak

Quarterly Surplus Changes Since 2011:Q1 Peak

11:Q2: -$5.6B (-1.0%)11:Q3: -$26.1B (-4.6%)11:Q4: -$14.3B (-2.5%)

Surplus as of 12/31/11 was down 2.5% below its all

time record high of $564.7B set as of 3/31/11. A new record high in 2012 is

possible.

*Includes $22.5B of paid-in capital from a holding company parent for one insurer’s investment in a non-insurance business in early 2010.

The Industry now has $1 of surplus for every $0.80 of NPW, close to the strongest claims-

paying status in its history.

78

3. REINSURANCE MARKET CONDITIONS

Record Global Catastrophes Activity is

Pressuring Pricing

78

79

Reinsurer Share of Recent Significant Market Losses

Source: Insurance Information Institute from reinsurance share percentages provided in RAA, ABIR and CEA press release, Jan. 13, 2011.

Billions of 2011 Dollars

$0$5

$10$15$20$25$30$35$40

JapanEarthquake/

Tsunami (Mar2011)

New Zealand Earthquake (Feb

2011)

Thailand Floods(Aug - Nov 2011)

Chile Earthquake(Feb. 2010)

AustraliaCyclone/ Floods(Jan-Feb 2011)

Reinsurer SharePrimary Insurer Share

40% Reinsurance share of total insured loss

Reinsurers Paid a High Proportion of Insured Losses Arising from Major Catastrophic Events Around the World in Recent Years

$0.4$4.0

$22.5$9.5

$15.0

$3.5

$37.5

$13.0

$6.0

$10.0

$7.9

$8.3

$2.2$2.8

$5.0

73%60%

95%44%

79

Source: Guy Carpenter, GC Capital Ideas.com, February 28, 2012.

Historical Capital Levels of Guy Carpenter Reinsurance Composite, 1998—3Q11

80

Most excess reinsurance capacity was

removed from the market in 2011, but

there does not appear to be a

shortage, leading to modest increases in

2012 reinsurance renewals except in areas hit hard by

CATs.

81

Global Property Catastrophe Rate on Line Index, 1990—2012 (as of Jan. 1)

15%

-3%

-13%

-8%

-20% -18% -1

1%

3%

14%

-11%

-6%

-9%

-16%

10%

-12%

-3%

8%

14%

76%

68%

25%

20%

0%

115

141

230

200184

147

123

152

255

233

195

235

184

199

133111

105

237

100

154

173

145

190

-40%

-20%

0%

20%

40%

60%

80%

100%

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

Ye

ar

Ov

er

Ye

ar

% C

ha

ng

e in

RO

L

0

50

100

150

200

250

300

Cu

mu

lativ

e R

ate

on

Lin

e (1

99

0=

10

0)

Year Over Year % Change

Cumulative Rate on Line Index

Sources: Guy Carpenter; Insurance Information Institute.

Property-Cat reinsurance pricing is up about 8% as of 1/1/12—modest relative

to the level CAT losses

4. RENEWED PRICING DISCIPLINE

82

Is There Evidence of a Broad and Sustained Shift in Pricing?

82

83

-5%

0%

5%

10%

15%

20%

25%

71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11*

Premium Growth Is Up Modestly: More in 2012?

(Percent)1975-78 1984-87 2000-03

Shaded areas denote “hard market” periodsSources: A.M. Best (historical and forecast), ISO, Insurance Information Institute.

Net Written Premiums Fell 0.7% in 2007 (First Decline

Since 1943) by 2.0% in 2008, and 4.2% in 2009, the First 3-Year Decline Since 1930-33.

NWP was up 0.9% in 2010

2011 growth

was +3.3%

85

Average Commercial Rate Change,All Lines, (1Q:2004–4Q:2011)

-3.2

%-5

.9%

-7.0

%-9

.4%

-9.7

% -8.2

%-4

.6% -2

.7%

-3.0

%-5

.3%

-9.6

%-1

1.3

%-1

1.8

%-1

3.3

%-1

2.0

%-1

3.5

%-1

2.9

% -11

.0%

-6.4

% -5.1

%-4

.9%

-5.8

%-5

.6%

-5.3

%-6

.4% -5.2

%-5

.4%

-2.9

%

2.8

%

-0.1

% 0.9

%

-0.1

%

-16%

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

1Q

04

2Q

04

3Q

04

4Q

04

1Q

05

2Q

05

3Q

05

4Q

05

1Q

06

2Q

06

3Q

06

4Q

06

1Q

07

2Q

07

3Q

07

4Q

07

1Q

08

2Q

08

3Q

08

4Q

08

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

Source: Council of Insurance Agents & Brokers (1Q04-4Q11); Insurance Information Institute

KRW Effect

Pricing as of Q3:2011 was positive for the first time

since 2003. Slightly stronger gains in Q4.

(Percent)

Q2 2011 marked the 30th consecutive quarter of price

declines

86

Change in Commercial Rate Renewals, by Account Size: 1999:Q4 to 2011:Q4

Source: Council of Insurance Agents and Brokers; Barclay’s Capital; Insurance Information Institute.

Percentage Change (%)

KRW Effect: No Lasting Impact

Pricing turned positive (+0.9%) in Q3:2011, the first increase in

nearly 8 years; Q4:2011 renewals were up 2.8%

Pricing Turned Negative in Early

2004 and Remained that

way for 7 ½ years

Peak = 2001:Q4 +28.5%

Trough = 2007:Q3 -13.6%

87

Cumulative Qtrly. Commercial Rate Changes, by Account Size: 1999:Q4 to 2011:Q4

1999:Q4 = 100

Source: Council of Insurance Agents and Brokers; Barclay’s Capital; Insurance Information Institute.

Despite Q4:2011 gain of 2.8%, pricing today is

where is was in late 2000 (pre-9/11)

Upward pricing pressure is small for large accounts, 1.8% in

Q4:2011, vs. 3.1% for small accounts and

3.5% for medium accounts

88

Change in Commercial Rate Renewals, by Line: 2011:Q4

Source: Council of Insurance Agents and Brokers; Insurance Information Institute.

Major Commercial Lines Renewed Uniformly Upward in Q4:2011 for Only the Second Time Since 2003; Property Lines

& Workers Comp Leading the Way

Percentage Change (%)

2.7% 3.0%

5.7%

7.5%

0.8%

2.0% 2.0% 2.1% 2.2% 2.3%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

Su

rety

EP

L

Co

mm

l Au

to

D&

O

Ge

ne

ral

Lia

bili

ty

Um

bre

lla

Co

nst

ruct

ion

Bu

s.In

terr

up

tion

Co

mm

erc

ial

Pro

pe

rty

Wo

rke

rsC

om

p

Property lines are showing larger increases than

casualty lines, with the exception of workers

compensation

INVESTMENTS: THE NEW REALITY

89

How Much of a Threat Are Persistently Low Interest Rates for (Re)Insurers?

89

Property/Casualty Insurance Industry Investment Income: 2000–2013F1

$38.9$37.1 $36.7

$38.7

$54.6

$51.2

$47.1 $47.6$49.0

$45.5$46.4

$39.6

$49.5

$52.3

$30

$40

$50

$60

00 01 02 03 04 05 06 07 08 09 10 11 12F 13F

Investment Income in 2011 Was Surprisingly Strong, Though Investment Income Is Likely to Weaken in 2012 Due to Persistently Low Interest Rates

1 Investment gains consist primarily of interest and stock dividends.*2012F-201F based on Conning projections.Sources: ISO; Conning Research & Consulting; Insurance Information Institute.

($ Billions)

Investment earnings in 2011 were 10.3% below

their 2007 pre-crisis peak

Property/Casualty Insurance Industry Investment Gain: 1994–2011:Q41

$35.4

$42.8$47.2

$52.3

$44.4

$36.0

$45.3$48.9

$59.4$55.7

$64.0

$31.7

$39.2

$53.4$56.2$58.0

$51.9$56.9

$0

$10

$20

$30

$40

$50

$60

$70

94 95 96 97 98 99 00 01 02 03 04 05* 06 07 08 09 10 11

Investment Gains in 2011 Were Surprisingly Robust. Investment Gains Recovered Significantly in 2011 Due to Realized Investment Gains; The

Financial Crisis Caused Investment Gains to Fall by 50% in 2008

1 Investment gains consist primarily of interest, stock dividends and realized capital gains and losses.* 2005 figure includes special one-time dividend of $3.2B.Sources: ISO; Insurance Information Institute.

($ Billions)

Investment gains in 2011 were $2.8B above 2010 levels—a surprise given falling rates

and flat stock markets

93

P/C Insurer Net Realized Capital Gains/Losses, 1990-2011

Sources: A.M. Best, ISO, Insurance Information Institute.

$2.8

8

$4.8

1 $9.8

9

$9.8

2

$10.

81 $18.

02

$13.

02

$16.

21

$6.6

3

-$1.

21

$6.6

1

$9.1

3

$9.7

0

$3.5

2 $8.9

2

-$7.

90

$5.6

9

$7.1

9

-$19

.81

$9.2

4

$6.0

0

$1.6

6

-$25

-$20

-$15

-$10

-$5

$0

$5

$10

$15

$20

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11

Insurers Posted Net Realized Capital Gains in 2010 and 2011 After Following Two Years of Realized Losses During the Financial Crisis. Realized Capital

Losses Were the Primary Cause of 2008/2009’s Large Drop in Profits and ROE

($ Billions) $27.0B positive swing since 2008

94

U.S. 10-Year Treasury Note Yields:A Long Downward Trend, 1990–2012*

*Monthly, through March 2012. Note: Recessions indicated by gray shaded columns.Sources: Federal Reserve Bank at http://www.federalreserve.gov/releases/h15/data/Monthly/H15_TCMNOM_Y10.txt National Bureau of Economic Research (recession dates); Insurance Information Institutes.

1%

2%

3%

4%

5%

6%

7%

8%

9%

'90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12

Yields on 10-Year U.S. Treasury Notes have been essentially

below 5% for nearly a decade.

Since roughly 80% of P/C bond/cash investments are in 10-year or shorter durations, most P/C insurer portfolios will have low-yielding bonds for years to come.

Yields on 10-Year U.S. Treasury Notes have

been essentially below 4% since January 2008.

94

3-Month Interest Rates forMajor Global Economies, 2008-2013F

0.7

%

0.3

% 0.7

%

2.0

% 2.5

%

1.4

%1.8

%

0.6

%

2.1

%

1.3

%

1.0

%

0.2

%

0.9

%

0.2

% 0.7

%

2.9

%

0.9

%

0.2

%

1.1

%

0.2

%

0.8

%

4.9

%

1.1

%

0.1

%

0.9

%

0.2

%

0.9

%

5.1

%

0.9

%

0.1

%

1.2

%

0.3

%

1.1

%

5.1

%

1.2

%

0.2

%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Euro Area Japan UK China Netherlands US

20082009201020112012F2013F

Source: Blue Chip Economic Indicators, Apr. 2012 edition.

Interest rates remain generally low in much of the

world, depressing insurer investment earnings. Central banks in many

countries, including the US, are intentionally holding

rates low.

97

-1.8

%

-1.8

%

-2.0

%

-3.6

%

-3.3

%

-3.3

%

-3.7

%

-4.3

%

-5.2

%

-5.7

%

-7.3%

-1.9

%

-2.1

%

-3.1

%

-8%-7%-6%-5%-4%-3%-2%-1%0%

Perso

nal L

ines

Pvt Pass

Aut

o

Pers P

rop

Comm

ercia

l

Comm

l Auto

Credit

Comm

Pro

p

Comm

Cas

Fidelity

/Sure

ty

Warra

nty

Surplu

s Line

s

Med

Mal

WC

Reinsu

rance

**

Lower Investment Earnings Place a Greater Burden on Underwriting and Pricing Discipline

*Based on 2008 Invested Assets and Earned Premiums**US domestic reinsurance onlySource: A.M. Best; Insurance Information Institute.

Reduction in Combined Ratio Necessary to Offset 1% Decline in Investment Yield to Maintain Constant ROE, by Line*

97

www.iii.org

Thank you for your timeand your attention!

Twitter: twitter.com/bob_hartwigDownload at www.iii.org/presentations

Insurance Information Institute Online:

98