Embed Size (px)

DESCRIPTION

This report provides a new detailed quantitative assessment of the consequences of climate change on economic growth through to 2060 and beyond. It focuses on how climate change affects different drivers of growth, including labour productivity and capital supply, in different sectors across the world. The sectoral and regional analysis shows that while the impacts of climate change spread across all sectors and all regions, the largest negative consequences are projected to be found in the health and agricultural sectors, with damages especially strong in Africa and Asia.

Citation preview

The Economic Consequences of

Climate ChangePOLICY HIGHLIGHTS

CIRCLEFurther degradation of the environment and natural capital can compromise prospects for future economic growth and human

well-being. The OECD Environmental Outlook to 2050: Consequences of Inaction (OECD, 2012) projected significant consequences

of climate change, biodiversity loss, water scarcity and health impacts of pollution by 2050, unless more ambitious policies are

implemented. The Environmental Outlook, however, presented a one-way analysis of the impacts of socioeconomic developments

on the environment. Specifically, it took no account of the feedbacks from environmental challenges and resource scarcity to the

economy. This report, The Economic Consequences of Climate Change seeks to address this gap through a detailed economic

modelling framework that links climate change impacts to specific aspects of regional economic activity, such as labour

productivity, the supply of production factors such as capital, and changes in the structure of demand. This detailed global analysis,

which covers a wide range of impact categories including agriculture, coastal zones, some extreme events, health and energy

and tourism demand, is used to assess the economic consequences of climate change until 2060, and is complemented by more

stylised integrated assessment modelling of post-2060 economic impacts.

CIRCLEFurther degradation of the environment and natural capital can compromise prospects for future economic growth and human

well-being. The OECD Environmental Outlook to 2050: Consequences of Inaction (OECD, 2012) projected significant consequences

of climate change, biodiversity loss, water scarcity and health impacts of pollution by 2050, unless more ambitious policies are

implemented. The Environmental Outlook, however, presented a one-way analysis of the impacts of socioeconomic developments

on the environment. Specifically, it took no account of the feedbacks from environmental challenges and resource scarcity to the

economy. This report, The Economic Consequences of Climate Change seeks to address this gap through a detailed economic

modelling framework that links climate change impacts to specific aspects of regional economic activity, such as labour

productivity, the supply of production factors such as capital, and changes in the structure of demand. This detailed global analysis,

which covers a wide range of impact categories including agriculture, coastal zones, some extreme events, health and energy

and tourism demand, is used to assess the economic consequences of climate change until 2060, and is complemented by more

stylised integrated assessment modelling of post-2060 economic impacts.

OECD POLICY HIGHLIGHTS The Economic Consequences of Climate Change - 1

THE ECONOMIC CONSEQUENCES OF CLIMATE CHANGE

Main messages

• In almost all regions, market consequences from climate change are projected to be negative, and there are significant non-market impacts and downside risks of tipping points and very severe impacts.

• The macroeconomic costs from selected market impacts alone amount to 1.0 to 3.3% of annual Gross Domestic Product (GDP) by 2060 and 2 to 10% by the end of the century in the absence of new policies. This is driven by a continued build-up of greenhouse gas concentrations, which are projected to lead to a global average temperature increase of 1.6-2.6°C by 2060 and 2.5-5.5°C by the end of the century in absence of new policies.

• Of the impacts modelled in the analysis, changes in crop yields and in labour productivity are projected to affect the economy most strongly, causing losses to annual global GDP in 2060 of 0.8% and 0.9%, respectively, and several percent in the most vulnerable regions.

• Net economic consequences are projected to be negative in 23 of the 25 regions modelled in the analysis. They are especially large in Africa and Asia, where the regional economies are vulnerable to a range of different climate impacts, such as heat stress and crop yield losses. Macroeconomic costs in most countries in these regions by 2060 are projected to be between 1.5% and 6.5% of GDP. In countries in higher latitudes, i.e. Canada and Russia, the net economic benefits are projected to outweigh the negative impacts, at least in the coming decades.

• Climate impacts affect all sectors in the economy through important indirect effects on the rest of the economy, not least through the relocation of labour and capital, and represent a systemic risk to the global economy.

• The macroeconomic consequences of climate change are fundamentally non-linear: they increase more than proportionately with temperatures. Uncertainties in the economic and climate system imply a risk that macroeconomic costs from market impacts alone run into the double digits well before the end of the century.

• Once greenhouse gases are emitted, they will have unavoidable and enduring effects on the climate and economy for a century or more, thereby permanently locking the world into higher impacts and stronger downside risks. Together, this implies a strong call for ambitious policy action both on mitigation and on adaptation.

• Ambitious adaptation and mitigation policies can reduce the future costs of climate change, but – perhaps more importantly – also limit the downside risks associated with high impacts and crucial tipping points. However, if only adaptation policies are adopted, total climate change costs are substantially higher than when only mitigation policies are adopted. In an optimal mix that minimises the total costs of climate change, there will be some costs from mitigation action, some costs associated with adaptation policies, and some costs from remaining market impacts.

• The benefits of adaptation policies, from a reduction in the selected market impacts alone, may amount to more than 1 percentage point of GDP by the end of the century, as the stylised analysis shows. It also highlights that if barriers to adaptation are strong, the costs of climate change can even double.

• Early and ambitious mitigation action (aimed at minimising total climate costs) can help economies avoid half of the macroeconomic consequences by 2060 and could reduce projected reductions of global GDP from 2-10% to 1-3% by the end of the century. It can also reduce the risk of triggering the worst negative long-term consequences of climate change. Less ambitious mitigation policies in the first decades will have lower short-term costs, but lead to higher long-term risks. Despite the potential of mitigation to limit emissions, significant impacts from climate change are projected to persist in vulnerable regions, such as in most countries in Africa and Asia.

• Mitigation policies will reduce the negative impacts of climate change on all economic sectors, yet the costs of these policies will not be borne by all sectors proportionally to their expected benefits. Just like the market impacts included in the modelling analysis, the mitigation policy leads to a shift in the structure of the economy towards more services.

POLICY H

IGH

LIGH

TS

1As successive assessment reports by the

Intergovernmental Panel on Climate Change (IPCC)

have shown, it is clear that climate change is occurring

and that further emissions of greenhouse gases will

amplify the consequences of climate change on both

socioeconomic and natural systems. The current

knowledge base for the impacts of climate change is only

sufficient to model a subset of these potential impacts

and capture some of the relevant uncertainties.

The Economic Consequences of Climate Change provides

a detailed global quantitative assessment of the

economic consequences of climate change. Most

existing studies of climate impacts have a stylised,

aggregated representation of the economy. This report

uses a multi-sector, multi-region modelling approach

to assess how a range of climate change impacts affect

the global economy. The report covers impacts on

agriculture, coastal zones, some extreme events, health

and energy and tourism demand. This report is not a

prediction of what will happen, nor a synthesis of the full

consequences of climate change. It sheds light, however,

on how these impacts affect the composition of GDP over

time and how sectoral consequences spill over to other

sectors and regions.

Trying to understand what climate change may mean for

the future of our societies is daunting. While a certain

amount of climate change is already locked-in, the range

of possible outcomes over the course of this century

and beyond is very wide. It can therefore reasonably be

asked what value a modelling analysis of the economic

consequences of climate change at a global level can

offer policy makers. After all, a combination of the

uncertainties and the necessary simplifications of a

model representation of the global economy will likely

dominate any aggregate result. But that is to miss the

point of the exercise. It is the direction of these changes

Why a modelling assessment of the economic consequences of climate change?

2 - OECD POLICY HIGHLIGHTS The Economic Consequences of Climate Change

and the interactions in the economic system that they

induce rather than their aggregate magnitude that is

most illuminating.

Besides projected market impacts, policymakers need to

take into account the large downside risks and long-

term effects of climate change when designing policies

to mitigate emissions of greenhouse gases and adapt

to the impacts of climate change. The reason is that

emission reductions lead to a stream of future benefits

and reduced risks, while adaptation reduces the adverse

consequences of climate impacts that are already

underway and helps societies proactively prepare for

the future. Therefore, the calculation of the benefits of

policy action should be based on the full stream of future

avoided impacts, and not simply follow the time profile of

market impacts as they emerge.

When policymakers assess the costs and benefits of

mitigation action, they need to think of including a ‘risk

premium’ to reflect the risks of crossing irreversible

tipping points, and to avoid the downside risks of more

severe impacts. Mitigation not only reduces the expected

level of climate impacts, but it also considerably reduces

uncertainties about the magnitude of the impacts and

downside risks. Finally, there are important co-benefits

from most policy actions that can be reaped immediately

and locally, such as air quality benefits. Policy makers

need to take these into account when determining the

appropriate policy efforts.

The magnitude and distributional consequences of both

market impacts and policy action are uncertain but

this study provides insights on long-run trends and the

mechanisms that link climate change impacts and global

economic activity. These will be valuable in informing

attempts to manage the significant and accumulating risk

of serious climatic disruption.

OECD POLICY HIGHLIGHTS The Economic Consequences of Climate Change - 3

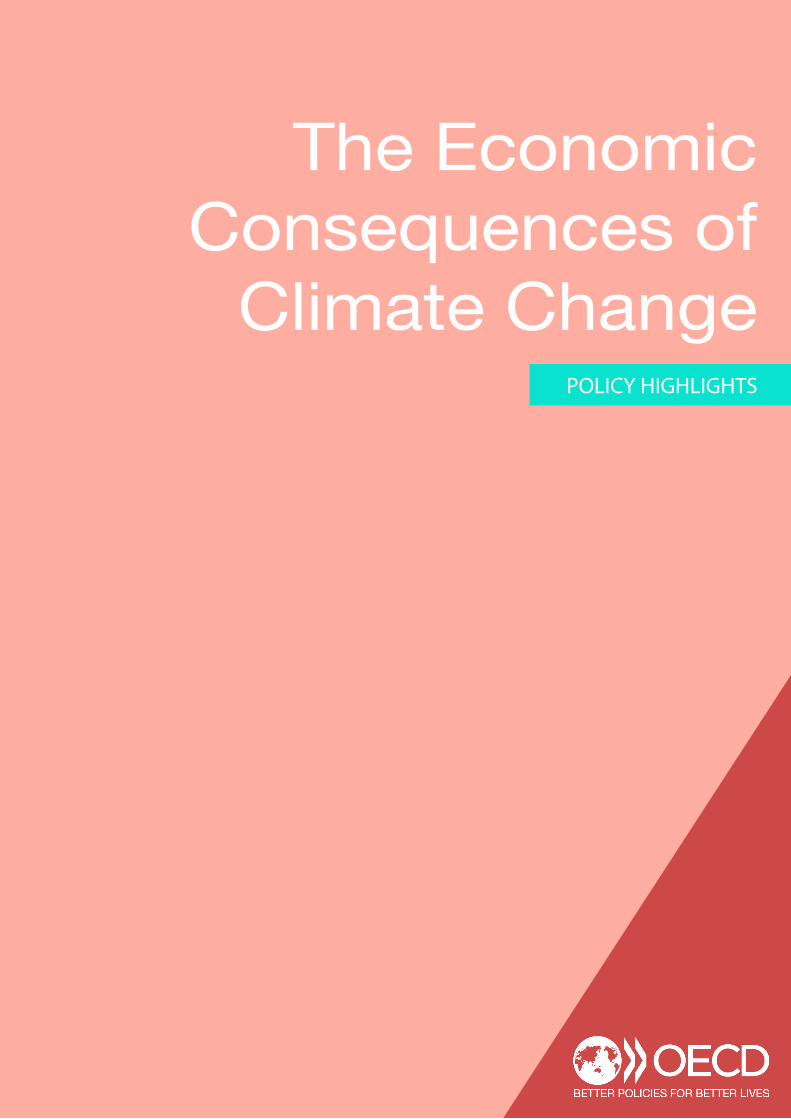

2Modelling the economic consequences of climate change

POLICY H

IGH

LIGH

TSThe modelling analysis in The Economic Consequences of

Climate Change is based on an assessment of climate

impacts from the literature, and specifies the effects

of the selected set of climate change impacts on the

drivers of economic growth, such as the productivity

and supply of specific production factors, as well as

changes in consumer demand induced by climate

change. The production function approach allows for a

detailed assessment of a subset of the direct and indirect

consequences of climate change for the economy for a

selected number of climate change impacts (see Table).

Other major impacts of climate change are investigated

outside the modelling framework.

Detailed assessments of these specific impacts are fed

into the OECD’s global dynamic computable general

equilibrium (CGE) model ENV-Linkages to assess the

implications for different economic activities until

2060 (see Figure). By using a multi-region, multi-sector

dynamic CGE model, the assessment can link different

impacts directly to specific drivers of economic growth,

including labour productivity, capital stocks and land

supply, as well as assess the indirect effects these impacts

have on the rest of the economy (other sectors and final

demand), and on the economies of other countries. The

detailed numerical assessment using ENV-Linkages is

complemented with a more stylised assessment of the

long-run implications (beyond 2060) using the AD-DICE

integrated assessment model. All impact assessments are

based on the Representative Concentration Pathway (RCP)

8.5 or the A1B emissions scenario as used by the IPCC.

Figure 1. Linking economic and climate change models

Economic model

Projects sectoral and regionaleconomic activity, and projects

corresponding emissions pathway

Impact models

Links climate change indicatorsto (sectoral) biophysical climate

impacts

Assessment of economicconsequences

Link biophysical impacts to changes in economic variables to be fed back ino the

economic model

Climate model

Links emissions pathway to temperature change and other climate change

indicators

4 - OECD POLICY HIGHLIGHTS The Economic Consequences of Climate Change OECD POLICY HIGHLIGHTS The Economic Consequences of Climate Change - 5

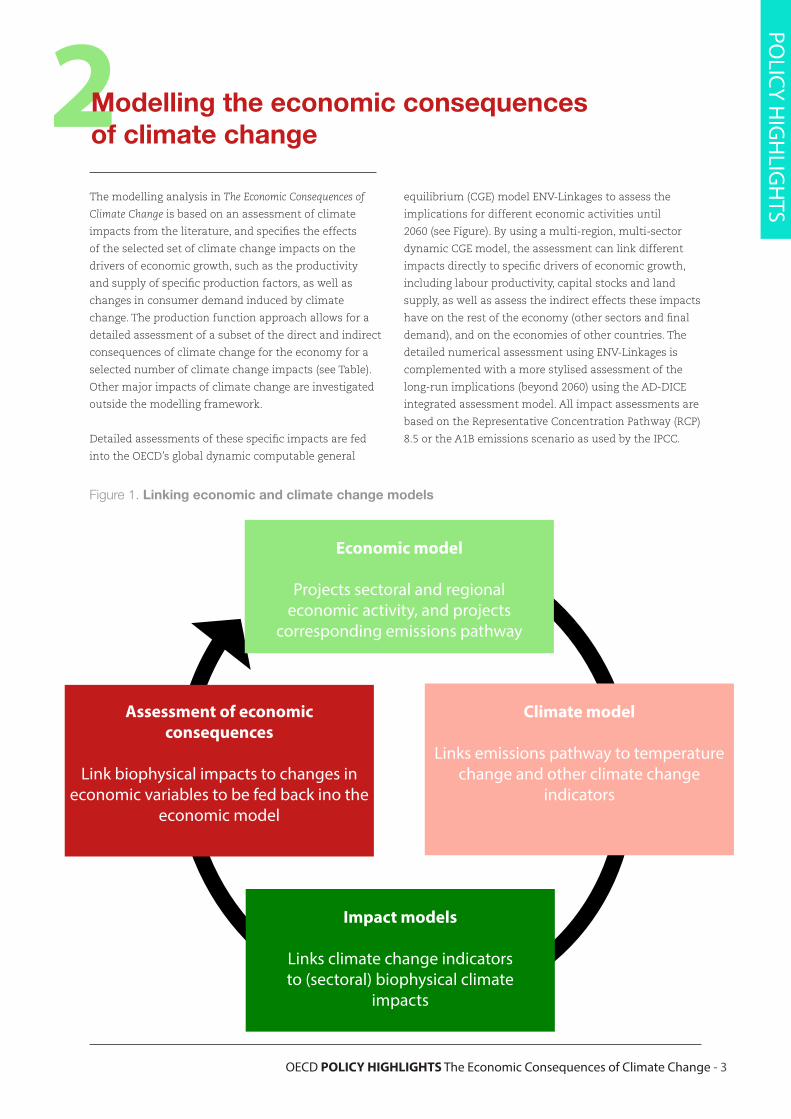

Table 1. Quality of the coverage of the sectors in the adaptation literature

Note: “Modelled” implies that the impact is captured (at least partially) in the main modelling framework; “stand-alone” refers to a quantitative assessment outside the main modelling framework, and “qualitatively” implies only a qualitative assessment was possible in this report.

AGRICULTURE Changes in crop yields (incl. land productivity and water stress)Livestock mortality and morbidity from heat and cold exposureChanges in pasture- and rangeland productivity Changes in aquaculture productivityChanges in fisheries catches

modelled

qualitatively

stand-alonequalitativelymodelled

COASTAL ZONES Loss of land and capital from sea level riseNon-market impacts in coastal zones

modelledqualitatively

EXTREME EVENTS Mortality, land and capital impacts from hurricanesMortality, land and capital impacts from floods

modelledstand-alone

HEALTH Mortality from heat exposure (incl. heatwaves)Morbidity from heat and cold exposure (incl. heatwaves)Mortality and morbidity from infectious diseases, cardiovascular and respiratory diseases

stand-alonemodelledmodelled

ENERGY DEMAND Changes in energy demand for cooling and heating modelled

TOURISM DEMAND Changes in tourism flows and services modelled

ECOSYSTEMS Loss of ecosystems and biodiversityChanges in forest plantation yields

stand-alonequalitatively

WATER STRESS Changes in energy supplyChanges in availability of drinking water to end users (incl. households)

qualitativelyqualitatively

HUMAN SECURITY Civil conflictHuman migration

qualitativelyqualitatively

TIPPING POINTS Large scale disruptive events stand-alone

Managing risks over time is at the heart of all climate

policy setting. Despite the many uncertainties, it is still

valuable to assess both the direct and indirect economic

consequences from the selected climate change impacts

listed above. The OECD ENV-Linkages model simulations

suggest that negative consequences on GDP are projected

to gradually increase over time and rise faster than global

economic activity. If no further climate change action is

undertaken, the combined negative effect of the selected

4 - OECD POLICY HIGHLIGHTS The Economic Consequences of Climate Change OECD POLICY HIGHLIGHTS The Economic Consequences of Climate Change - 5

impacts on global annual GDP is projected to rise over time to

likely levels of 1.0% to 3.3% by 2060, with a central projection

of 2%. This range reflects uncertainty in the equilibrium

climate sensitivity (ECS) – a measure indicating how sensitive

the earth’s climate reacts to a doubling of atmospheric CO2 –

using a likely range of 1.5°C to 4.5°C. Assuming a wider range

of 1°C to 6°C in the ECS, global GDP losses could amount to

0.6% to 4.4% in 2060.

3Projecting the economic consequences of climate change

POLICY H

IGH

LIGH

TS

Source: ENV-Linkages model.

As temperatures continue to rise to a projected 4°C above

pre-industrial levels by 2100 (with a likely uncertainty

range of 2.5°C to 5.5°C), AD-DICE projections suggest that

GDP may be reduced by between 2% and 10% by the end

of the century relative to the no climate change baseline

scenario (likely ECS range). As experimental projections

with the AD-DICE model show, continuing to emit

greenhouse gas emissions as usual until 2060 will commit

the world to macroeconomic costs in a range of 1% to 6%

of global GDP by the end of the century even if emissions fall

to zero in 2060. However, assessments of impacts for higher

temperature increases are much less robust; they could even

lead to global macroeconomic costs of 12% by 2100 when non-

linearities in the economic consequences to climate change

are strong (as shown by using the Weitzman damage function,

which assumes that large temperature increases lead to much

more dramatic reductions in GDP by including a higher power

term in the damage function).

-7%

-6%

-5%

-4%

-3%

-2%

-1%

0%

2010 2020 2030 2040 2050 2060 uncertainty ranges in 2060due to uncertainty in ECS

South & South-East Asia

OECD Pacific

Rest of Europe & Asia

OECD Europe

Latin America

OECD America

World

Sub-Saharan Africa

Middle East & North Africa

Figure 2. Global and regional changes in GDP from selected climate change impacts, central projection (Percentage change in regional GDP)

6 - OECD POLICY HIGHLIGHTS The Economic Consequences of Climate Change OECD POLICY HIGHLIGHTS The Economic Consequences of Climate Change - 7

The range of projections does not capture the

considerable uncertainties and risks from climate

change that could potentially lead to much more

severe consequences (especially in the long-run), or

result in smaller economic consequences than in the

central projection. Some major uncertainties stem from

assumptions on economic growth, demographics, ECS,

projections of regional climate, and the valuation of

climate change impacts. Large downside risks of climate

change are associated with uncertainty about the response of

the climate system to temperature increases beyond 2°C, the

impact of climate change on economic growth, irreversible

tipping points, and the non-market impacts of climate change.

Taking only one of these sources of uncertainties, the ECS, into

consideration already yields wide uncertainty ranges, although

in almost all regions the sign of the net effects on GDP is not in

doubt.

Source: AD-DICE model.

Figure 3. Changes in global GDP from selected climate change impacts in the very long run (Percentage change w.r.t. no climate change baseline)

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2010 2020 2030 2040 2050 2060 2070 2080 2090 2100

Likely uncertainty range - central projection until 2100 Likely uncertainty range - central projection until 2060Central projection until 2100 Central projection until 2060 (committed by 2060)Weitzman damage function

6 - OECD POLICY HIGHLIGHTS The Economic Consequences of Climate Change OECD POLICY HIGHLIGHTS The Economic Consequences of Climate Change - 7

4Regional variation in economic consequences of climate change

POLICY H

IGH

LIGH

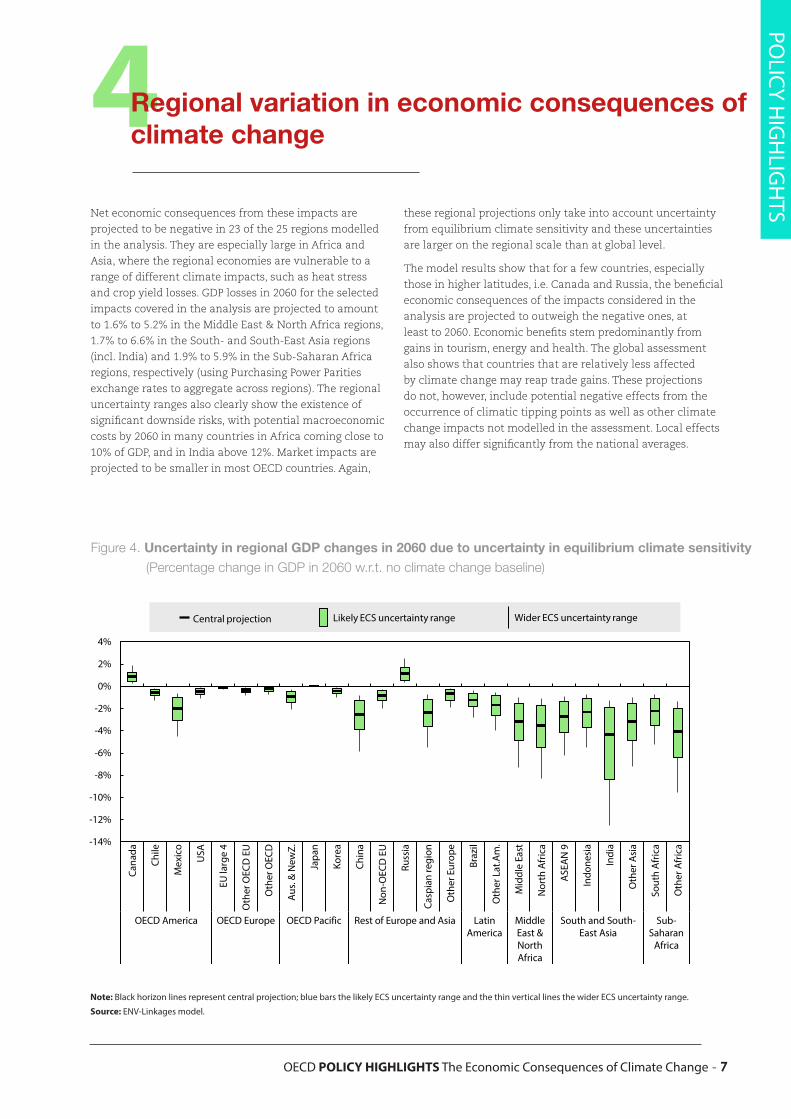

TSNet economic consequences from these impacts are

projected to be negative in 23 of the 25 regions modelled

in the analysis. They are especially large in Africa and

Asia, where the regional economies are vulnerable to a

range of different climate impacts, such as heat stress

and crop yield losses. GDP losses in 2060 for the selected

impacts covered in the analysis are projected to amount

to 1.6% to 5.2% in the Middle East & North Africa regions,

1.7% to 6.6% in the South- and South-East Asia regions

(incl. India) and 1.9% to 5.9% in the Sub-Saharan Africa

regions, respectively (using Purchasing Power Parities

exchange rates to aggregate across regions). The regional

uncertainty ranges also clearly show the existence of

significant downside risks, with potential macroeconomic

costs by 2060 in many countries in Africa coming close to

10% of GDP, and in India above 12%. Market impacts are

projected to be smaller in most OECD countries. Again,

these regional projections only take into account uncertainty

from equilibrium climate sensitivity and these uncertainties

are larger on the regional scale than at global level.

The model results show that for a few countries, especially

those in higher latitudes, i.e. Canada and Russia, the beneficial

economic consequences of the impacts considered in the

analysis are projected to outweigh the negative ones, at

least to 2060. Economic benefits stem predominantly from

gains in tourism, energy and health. The global assessment

also shows that countries that are relatively less affected

by climate change may reap trade gains. These projections

do not, however, include potential negative effects from the

occurrence of climatic tipping points as well as other climate

change impacts not modelled in the assessment. Local effects

may also differ significantly from the national averages.

Note: Black horizon lines represent central projection; blue bars the likely ECS uncertainty range and the thin vertical lines the wider ECS uncertainty range.

Source: ENV-Linkages model.

Figure 4. Uncertainty in regional GDP changes in 2060 due to uncertainty in equilibrium climate sensitivity (Percentage change in GDP in 2060 w.r.t. no climate change baseline)

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

Cana

da

Chile

Mex

ico

USA

EU la

rge

4

Oth

er O

ECD

EU

Oth

er O

ECD

Aus

. & N

ewZ.

Japa

n

Kore

a

Chin

a

Non

-OEC

D E

U

Russ

ia

Casp

ian

regi

on

Oth

er E

urop

e

Braz

il

Oth

er L

at.A

m.

Mid

dle

East

Nor

th A

fric

a

ASE

AN

9

Indo

nesi

a

Indi

a

Oth

er A

sia

Sout

h A

fric

a

Oth

er A

fric

a

OECD America OECD Europe OECD Pacific Rest of Europe and Asia LatinAmerica

MiddleEast &NorthAfrica

South and South-East Asia

Sub-Saharan

Africa

Central projection Likely ECS uncertainty range Wider ECS uncertainty range

OECD POLICY HIGHLIGHTS The Economic Consequences of Climate Change - 9

5Sectoral variation in the economic consequences of climate change

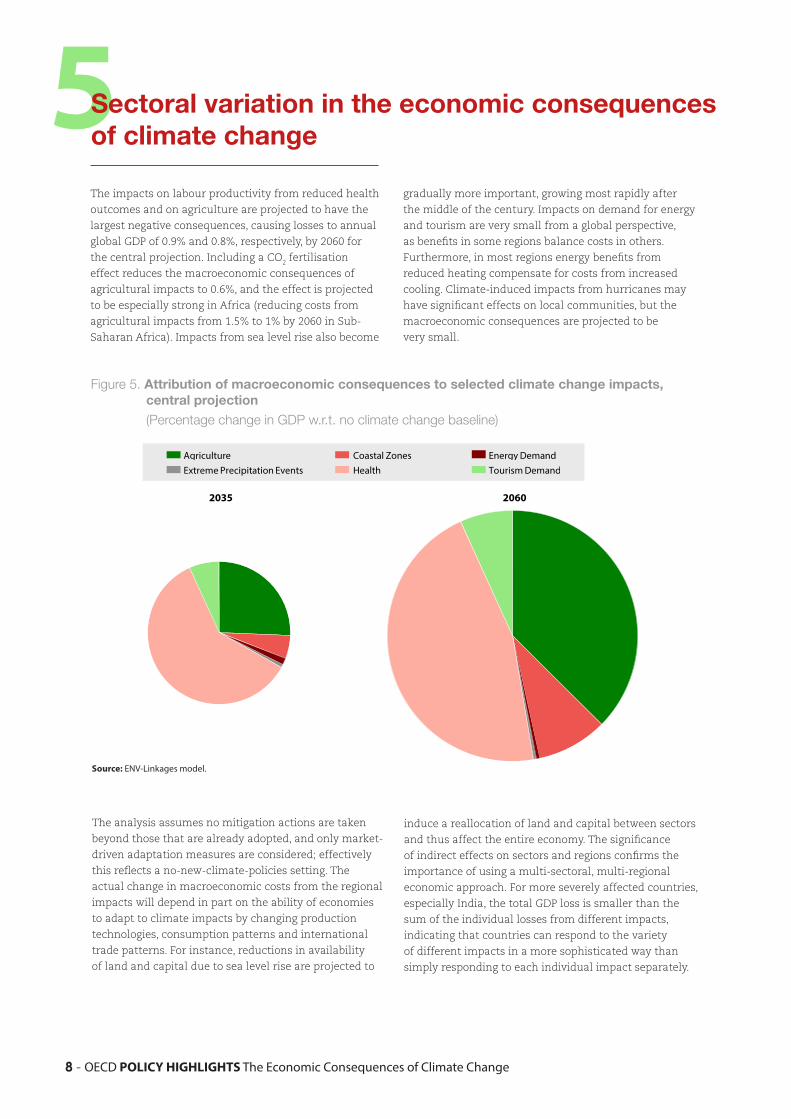

The impacts on labour productivity from reduced health

outcomes and on agriculture are projected to have the

largest negative consequences, causing losses to annual

global GDP of 0.9% and 0.8%, respectively, by 2060 for

the central projection. Including a CO2 fertilisation

effect reduces the macroeconomic consequences of

agricultural impacts to 0.6%, and the effect is projected

to be especially strong in Africa (reducing costs from

agricultural impacts from 1.5% to 1% by 2060 in Sub-

Saharan Africa). Impacts from sea level rise also become

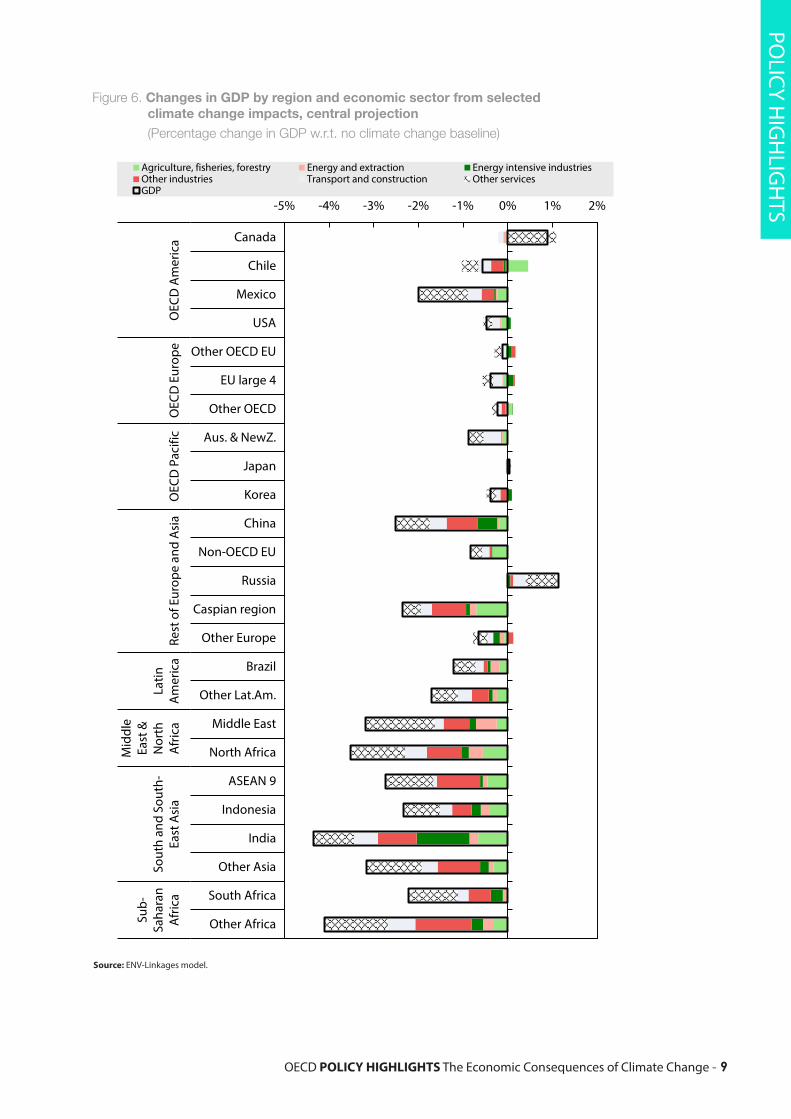

The analysis assumes no mitigation actions are taken

beyond those that are already adopted, and only market-

driven adaptation measures are considered; effectively

this reflects a no-new-climate-policies setting. The

actual change in macroeconomic costs from the regional

impacts will depend in part on the ability of economies

to adapt to climate impacts by changing production

technologies, consumption patterns and international

trade patterns. For instance, reductions in availability

of land and capital due to sea level rise are projected to

induce a reallocation of land and capital between sectors

and thus affect the entire economy. The significance

of indirect effects on sectors and regions confirms the

importance of using a multi-sectoral, multi-regional

economic approach. For more severely affected countries,

especially India, the total GDP loss is smaller than the

sum of the individual losses from different impacts,

indicating that countries can respond to the variety

of different impacts in a more sophisticated way than

simply responding to each individual impact separately.

8 - OECD POLICY HIGHLIGHTS The Economic Consequences of Climate Change

Source: ENV-Linkages model.

Figure 5. Attribution of macroeconomic consequences to selected climate change impacts, central projection (Percentage change in GDP w.r.t. no climate change baseline)

gradually more important, growing most rapidly after

the middle of the century. Impacts on demand for energy

and tourism are very small from a global perspective,

as benefits in some regions balance costs in others.

Furthermore, in most regions energy benefits from

reduced heating compensate for costs from increased

cooling. Climate-induced impacts from hurricanes may

have significant effects on local communities, but the

macroeconomic consequences are projected to be

very small.

Coastal ZonesExtreme Precipitation Events

Energy DemandTourism DemandHealth

Agriculture

2035 2060

OECD POLICY HIGHLIGHTS The Economic Consequences of Climate Change - 9

POLICY H

IGH

LIGH

TS

8 - OECD POLICY HIGHLIGHTS The Economic Consequences of Climate Change

Source: ENV-Linkages model.

Figure 6. Changes in GDP by region and economic sector from selected climate change impacts, central projection (Percentage change in GDP w.r.t. no climate change baseline)

-5% -4% -3% -2% -1% 0% 1% 2%

Canada

Chile

Mexico

USA

Other OECD EU

EU large 4

Other OECD

Aus. & NewZ.

Japan

Korea

China

Non-OECD EU

Russia

Caspian region

Other Europe

Brazil

Other Lat.Am.

Middle East

North Africa

ASEAN 9

Indonesia

India

Other Asia

South Africa

Other Africa

OEC

D A

mer

ica

OEC

D E

urop

eO

ECD

Pac

ific

Rest

of E

urop

e an

d A

sia

Latin

Am

eric

a

Mid

dle

East

&N

orth

Afr

ica

Sout

h an

d So

uth-

East

Asi

a

Sub-

Saha

ran

Afr

ica

Agriculture, fisheries, forestry Energy and extraction Energy intensive industriesOther industries Transport and construction Other servicesGDP

OECD POLICY HIGHLIGHTS The Economic Consequences of Climate Change - 1110 - OECD POLICY HIGHLIGHTS The Economic Consequences of Climate Change

6From macroeconomic consequences to the full costs of inaction

The modelling approach in The Economic Consequences

of Climate Change includes as many market impacts

as possible, but can only provide a partial picture of

the consequences of climate change, as it cannot take

into account non-market aspects of well-being (e.g.

premature deaths) or impacts for which the available

data are insufficient. The modelling analysis is therefore

complemented by stand-alone quantitative information

specifically calculated for this report for some of the

impacts which could not be incorporated.

• Urban flood impacts are highly uncertain, in

part because they rely on projections of regional

and local precipitation, as well as behavioural

responses. Moreover, only potential costs in absence

of adaptation efforts could be assessed. The two

countries that have by far the largest projected

potential urban flood costs are India and China. For

OECD countries, the climate-induced potential urban

flood costs are projected to be much smaller (see

Figure).

• The regions with the highest number of premature

fatalities from heat stress are the ones with high

population (like China and India) or where aging

increases the size of the vulnerable population at

risk (such as the EU and the US). In new calculations

by the Japanese National Institute for Environmental

Studies (NIES), the global death toll from heat

stress is projected to increase from less than 150

thousand people annually in the current climate,

to more than a million by the 2050s and close to 3

million by 2080s. The associated welfare costs in

OECD countries are projected to be highest in North

American and EU countries.

• For loss of ecosystem services, a Willingness-to-

Pay approach is used to quantify the associated

economic costs, although this cannot be used

as a proxy for the effect of loss of biodiversity or

specific ecosystem services on different sectors in

the economy. For the CIRCLE baseline, by 2060, this

approach yields a value of around 1% of GDP for

most high income countries.

• The modelling analysis does not fully include

uncertain but high-impact large-scale singular

events in the climate system, such as a shut-down of

the Gulf Stream or collapse of the West Antarctic ice

sheet. While the temperature thresholds associated

with the triggering of such events remain uncertain,

in general terms their likelihood increases with

more severe climatic changes, and they are expected

to have severe permanent effects on the economy.

If the risks of such events are – in a rudimentary

way – included in the stylised analysis by adopting

a damage function that projects much more

rapidly rising economic consequences for higher

temperatures, then the consequences for the level of

GDP could reach double digits well before the end of

the century.

The report also qualitatively discusses a number of

important climate impacts that could not be quantified,

including impacts on reduced winter mortality from

extreme cold, local disruptions of infrastructure from

extreme weather events, changes in water stress and

impacts on human security (specifically migration and

conflict). Although for some of these effects, and for

particular regions, the consequences may be positive, the

existing evidence collated by the Intergovernmental Panel

on Climate Change (IPCC) and others points to significant

further downside risks for negative consequences.

On balance, the costs of inaction presented here are

therefore likely to underestimate the full costs of climate

change impacts.

OECD POLICY HIGHLIGHTS The Economic Consequences of Climate Change - 1110 - OECD POLICY HIGHLIGHTS The Economic Consequences of Climate Change

7Avoided impacts from policy action

The economic consequences of climate change, as

outlined in detail in the report, with losses in gross

domestic product (GDP) for almost all regions and

numerous important other consequences, imply a

strong call for policy action. By implementing ambitious

mitigation policies to reduce the emission sources of

climate change, and adaptation policies to best deal with

the remaining consequences, the worst impacts may be

avoided, and the economic consequences from climate

change substantially reduced. The benefits of adaptation

policies, from a reduction in the selected impacts alone,

may amount to more than 1 percentage point of GDP

by the end of the century, as the stylised analysis with

AD-DICE shows. It also highlights that if barriers to

adaptation are strong, and firms and households are not

able to adapt at all, the costs of climate change can even

double.

Source: OECD calculations based on Winsemius and Ward (2015).

Figure 7. Climate change costs from urban floods by 2080 (Billions of USD, 2005 PPP exchange rates)

POLICY H

IGH

LIGH

TS

below - 1 from -1 to 0 from 0 to 1 from 10 to 100 above 100

OECD POLICY HIGHLIGHTS The Economic Consequences of Climate Change - 1312 - OECD POLICY HIGHLIGHTS The Economic Consequences of Climate Change

Source: AD-DICE model.

Figure 8. Components of climate change costs from selected climate change impacts for different adaptation and mitigation scenarios (Percentage of no climate change baseline GDP level)

Early and ambitious mitigation action (aimed at

minimising total climate costs, which limits temperature

change to 2.5°C, according to the AD-DICE projections)

can help economies avoid half of the GDP consequences

by 2060 (i.e. reduce them to 1% of annual GDP; excluding

the economic effects of the mitigation policy itself). It

can also reduce the risk of triggering the worst long-term

consequences of climate change. Despite the potential

of mitigation to limit impacts, however, significant

costs from climate change are projected to persist in

vulnerable regions, such as in most countries in Africa

and Asia.

Mitigation not only reduces the expected level of climate

costs, but ambitious mitigation action also considerably

reduces the risks of large economic costs (the likely

uncertainty range reduces from 2-10% to 1-3% by

2100 for the selected climate impacts, according to the

simulations). Furthermore, less ambitious mitigation

policies in the first decades will have lower short-term

costs, but lead to higher long-term risks (in quantitative

terms, this result is heavily influenced by the choice

of discount rate). But mitigation will not remove all

impacts, so there is still a need for adaptation. However,

if only adaptation policies are adopted, the economic

consequences are substantially larger than when only

mitigation policies are adopted. In the optimal mix, there

will be some costs from mitigation action, some costs

associated with adaptation policies, and some remaining

impacts.

Mitigation policies will reduce the negative impacts

of climate change on all economic sectors, yet the

costs of these policies will not be borne by all sectors

proportionally to their expected benefits. The detailed

CGE model analysis is used to shed further light on

this, again with a horizon to 2060. Agriculture, for

example, despite its relatively small size, will experience

substantial direct and indirect impacts from climate

change; its high emissions could imply substantial

costs from stringent economy-wide mitigation policies.

For energy production and the industrial sectors the

climate impacts are smaller than the potential effects

from stringent economy-wide mitigation policies.

Renewable power generation can substantially increase

production activities if an ambitious mitigation policy

is implemented, but on balance the negative effects

on fossil fuel producers outweigh those on renewables.

Services are projected to benefit from the mitigation

policy as they are relatively clean, but they are negatively

affected by climate impacts. However, given the large size

of services compared to the other sectors, the relative

share of the services sectors in total GDP can increase,

i.e. they are relatively less affected than other sectors.

Thus, both climate impacts and the mitigation policy lead

to a shift in the structure of the economy towards more

services. However, as mitigation policies reduce climate

impacts, the projected gains in the services sector may

be smaller than when mitigation policies are investigated

without consideration of the benefits of policy action.

0%

2%

4%

6%

8%

10%

12%

2050 2100 2050 2100 2050 2100 2050 2100 2050 2100 2050 2100

No mitigation Optimalmitigation

No mitigation Optimalmitigation

No mitigation Optimalmitigation

Full adaptation Flow adaptation No adaptation

Adaptation costs Mitigation costs Residual damages

OECD POLICY HIGHLIGHTS The Economic Consequences of Climate Change - 1312 - OECD POLICY HIGHLIGHTS The Economic Consequences of Climate Change

Note: Mitigation policy aimed at minimising total climate costs (limiting temperature change to 2.5°C).Source: ENV-Linkages model.

Figure 9. Regional changes in GDP from selected climate change impacts with and without mitigation policy (Percentage change in GDP in 2060 w.r.t. no climate change baseline)

8Improving the knowledge base for better climate policies

Despite the detailed modelling frameworks used and

careful calibration of sectoral and regional economic

activity, The Economic Consequences of Climate Change

presents just one projection of a possible scenario for

the economic implications of climate change until

2060. The aggregate results do not represent the total

social costs of climate change. It is not a prediction of

what will happen, nor a synthesis of the full literature

on climate change. Other models and other scenarios

would give quantitatively different results. More robust

insights would be gathered from a broader analysis, using

multiple scenarios and multiple models. This would,

however, represent a substantial additional research

effort. Additional research efforts are also needed to

reduce the major knowledge gaps on the economic

consequences of climate change, not least concerning the

regional economic consequences of triggering important

tipping points, which could potentially have effects on

the economy that are an order of magnitude higher

than those included in the modelling analysis here.

Furthermore, a robust methodology is needed to include

non-market impacts and co-benefits of policy action

into the evaluation. The value of the analysis provided in

this report is therefore more in terms of identifying the

direction and relative magnitude of the different effects

that have been modelled rather than precise numerical

projections. The report aims to give insights on how

ignoring climate change may be detrimental to economic

growth, affect the structures of economies around the

world, and on how adaptation and mitigation policies

may reduce these risks.

-4.0%

-3.5%

-3.0%

-2.5%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

OECDAmerica

OECDEurope

OECDPacific

Rest ofEurope &

Asia

LatinAmerica

Middle East& NorthAfrica

South &South-East

Asia

Sub-Saharan

Africa

Avoided impacts Change in GDP after mitigation

CONTACT

Rob Dellink, Co-ordinator Modelling and Outlooks, [email protected]

Elisa Lanzi, Policy Analyst, [email protected]

PHOTO CREDITS

©Adrian Scottow, 2010

©iStock.com/TimArbaev

©iStock.com/ 3alexd

©Topten22photo | Dreamstime.com

©dreamstime_m_8855290 rt

FOR FURTHER INFORMATION

OECD (2015), The Economic Consequences of Climate Change, OECD Publishing, Paris,

http://dx.doi.org/10.1787/9789264235410-en.

OECD (2012), OECD Environmental Outlook to 2050: The Consequences of Inaction,

OECD Publishing, Paris, http://dx.doi.org/10.1787/9789264122246-en.

THE ECONOMIC CONSEQUENCES OF CLIMATE CHANGE ON THE WEB

www.oecd.org/environment/circle.htm

www.oecd.org/environment/modelling.htm