Embed Size (px)

Citation preview

THE ADVISOR’S GUIDE TO

MEDICARE AND MEDICAID (2017 EDITION)

Researched and Written by: Edward J. Barrett

CFP, ChFC, CLU, CEBS, RPA, CRPS, CRPC

2

DISCLAIMER

This course is designed as an educational program for financial professionals. EJB Financial Press is not engaged in rendering legal or other professional advice and the reader should consult legal counsel as appropriate. We try to provide you with the most accurate and useful information possible. However, one thing is certain and that is change. The content of this publication may be affected by changes in law and in industry practice, and as a result, information contained in this publication may become outdated. This material should in no way be used as a source of authority on legal and/or tax matters. Laws and regulations cited in this publication have been edited and summarized for the sake of clarity. Names used in this publication are fictional and have no relationship to any person living or dead.

EJB Financial Press, Inc. 7137 Congress St.

New Port Richey, FL 34653 (800) 345-5669

www.EJBfinpress.com

This book is manufactured in the United States of America

© 2017 EJB Financial Press Inc., Printed in U.S.A. All rights reserved

3

ABOUT THE AUTHOR Edward J. Barrett CFP®, ChFC®, CLU, CEBS®, RPA, CRPC®, CRPS®, began his career in the financial and insurance services back in 1978 with IDS Financial Services, becoming a leading financial advisor and top district sales manager in Boston, Massachusetts. In 1986, Mr. Barrett joined Merrill Lynch in Boston as an estate and business-planning specialist working with over 400 financial advisors and their clients throughout the New England region. In 1992, after leaving Merrill Lynch and moving to Florida, Mr. Barrett founded The Barrett Companies Inc. and Broker Educational Sales & Training Inc., Wealth Preservation Planning Associates and The Life Settlement Advisory Group Inc. Mr. Barrett was a qualifying member of the Million Dollar Round Table, Qualifying Member Court of the Table® and Top of the Table® producer. He holds the Certified Financial Planner designation CFP®, Chartered Financial Consultant (ChFC), Chartered Life Underwriter (CLU), Certified Employee Benefit Specialist (CEBS), Retirement Planning Associate (RPA), Chartered Retirement Planning Counselor (CRPC) and the Chartered Retirement Plans Specialist (CRPS) professional designations. EJB Financial Press EJB Financial Press, Inc. (www.ejbfinpress.com) was founded in 2004, by Mr. Barrett to provide advanced educational and training manuals approved for correspondence continuing education credits for insurance agents, financial advisors, accountants and attorneys throughout the country. Broker Educational Sales & Training Inc. Broker Educational Sales & Training Inc. (BEST) is a nationally approved provider of continuing education and advanced training programs to the mutual fund, insurance, financial services industry and an approved sponsor of CPE courses with the National Association of State Boards of Accountancy and Quality Assurance Service (QAS). For more information visit our website at selfstudyce.brokered.net or call us at 800-345-5669.

4

This page left blank intentionally

5

TABLE OF CONTENTS ABOUT THE AUTHOR ......................................................................................... 3 SECTION ONE MEDICARE ............................................................................ 13 CHAPTER 1 INTRODUCTION TO MEDICARE .............................................. 15 Overview ........................................................................................................................... 15 Learning Objectives .......................................................................................................... 15 History of Medicare .......................................................................................................... 15 Medicare Administration .................................................................................................. 17 Medicare Parts .................................................................................................................. 17

Original Medicare: Part A and Part B ...................................................................... 17 Medicare Part C ........................................................................................................ 18 Medicare Part D ........................................................................................................ 18

Medicare Eligibility .......................................................................................................... 18 Applying for Medicare Benefits ............................................................................... 19 Choosing Medicare Coverage ................................................................................... 19 Number of People Enrolled in Medicare .................................................................. 20

Medicare Financing .......................................................................................................... 21 Medicare Trust Funds ....................................................................................................... 21

The Hospital Insurance (HI) Trust Fund ................................................................... 22 The Supplementary Medical Insurance (SMI) Trust Fund ....................................... 22 Trust Fund Board of Trustees ................................................................................... 22

Medicare Spending ........................................................................................................... 22 Recent Trends in Medicare Spending ....................................................................... 24 Future Trends in Medicare Spending ........................................................................ 24

Medicare Gaps and Out-of-Pocket Costs .......................................................................... 25 The 2017 Trustees Report on Medicare ............................................................................ 26

Short-Range Results.................................................................................................. 26 Long-Range Results .................................................................................................. 27 Conclusion ................................................................................................................ 27

Medicare and the Affordable Care Act (ACA) of 2010 ................................................... 28 Medicare SGR Update ...................................................................................................... 28 Chapter 1 Review Questions ............................................................................................ 30 CHAPTER 2 MEDICARE PART A ................................................................. 31 Overview ........................................................................................................................... 31 Learning Objectives .......................................................................................................... 31 Who Is Eligible For Part A (HI) ....................................................................................... 31

Special Eligibility Rules for Persons with End-Stage Renal Disease ....................... 32 Special Rules for Government Employees ............................................................... 32

Part A Premium................................................................................................................. 33 State Medicare Savings Program .............................................................................. 33

Part A Financing ............................................................................................................... 34 HI Trust Fund .................................................................................................................... 34 Part A Covered Services ................................................................................................... 36

Costs for Part A Services .......................................................................................... 38 Part A Enrollment Periods ........................................................................................ 38

6

Part A Late Enrollment Fee ...................................................................................... 40 Chapter 2 Review Questions ............................................................................................ 41 CHAPTER 3 MEDICARE PART B .................................................................. 43 Overview ........................................................................................................................... 43 Learning Objectives .......................................................................................................... 43 Part B Eligibility ............................................................................................................... 43

Part B Financing ....................................................................................................... 44 SMI Trust Fund ......................................................................................................... 44

Standard Part B Premium.................................................................................................. 45 Income-Related Monthly Adjusted Amount (IRMAA) ............................................ 46 Hold Harmless Provision .......................................................................................... 47 The “Doc Fix” ........................................................................................................... 47

Part B Deductibles and Coinsurance Amounts ................................................................. 49 Part B Types of Services Covered .................................................................................... 49

Types of Common Services Covered ....................................................................... 50 Types of Preventive Services Covered ..................................................................... 53 Type of Services Not Covered .................................................................................. 54

Part B Enrollment Periods ................................................................................................ 54 Automatic Enrollment Period (AEP) ........................................................................ 54 Initial Enrollment Period........................................................................................... 55 General Enrollment Period ....................................................................................... 55 Special Enrollment Period (SEP) .............................................................................. 55 Part B Late Enrollment Fees ..................................................................................... 56 Chapter 3 Review Questions .................................................................................... 57

CHAPTER 4 MEDICARE ADVANTAGE PLANS (PART C) .......................... 59 Overview ........................................................................................................................... 59 Learning Objectives .......................................................................................................... 59 History of MA Plans ......................................................................................................... 59

The Balanced Budget Act of 1997 ............................................................................ 60 Medicare and the Medicare Modernization Act of 2003 .......................................... 60

Medicare Advantage Benefits ........................................................................................... 62 MA Enrollment ................................................................................................................. 62 Types of MA Plans ........................................................................................................... 63

Health Maintenance Organizations (HMO) Plans .................................................... 64 Preferred Provider Organization (PPO) Plans .......................................................... 65 Private Fee-for-Service Plans (PFFS) ....................................................................... 66 Special Needs (SNP) Plans ....................................................................................... 67 Medical Savings Accounts ........................................................................................ 69

Payments to Medicare Private Plans ................................................................................. 70 MA Premiums ................................................................................................................... 71

Average Premium Trend ........................................................................................... 71 Zero Premium Plans .................................................................................................. 72 Premium Variation Across States ............................................................................. 72

Cost Sharing ...................................................................................................................... 73 Out-of- Pocket Limits ............................................................................................... 73

Part D Cost Sharing .......................................................................................................... 74 Part D Deductibles .................................................................................................... 74

7

Prescription Drug And Supplemental Benefits ................................................................. 74 Choosing a MA Plan ......................................................................................................... 75

MA Plan Star Quality Ratings .................................................................................. 75 MA Enrollment Periods .................................................................................................... 76 MA Plans and the ACA .................................................................................................... 80 Chapter 4 Review Questions ............................................................................................ 81 CHAPTER 5 MEDICARE PART D ................................................................. 83 Overview ........................................................................................................................... 83 Learning Objectives .......................................................................................................... 83 History of Part D ............................................................................................................... 83 Part D Administration ....................................................................................................... 85

Part D Spending and Financing ................................................................................ 85 Part D SMI Trust Fund ............................................................................................. 85 Part D SMI Trust Fund ............................................................................................. 85

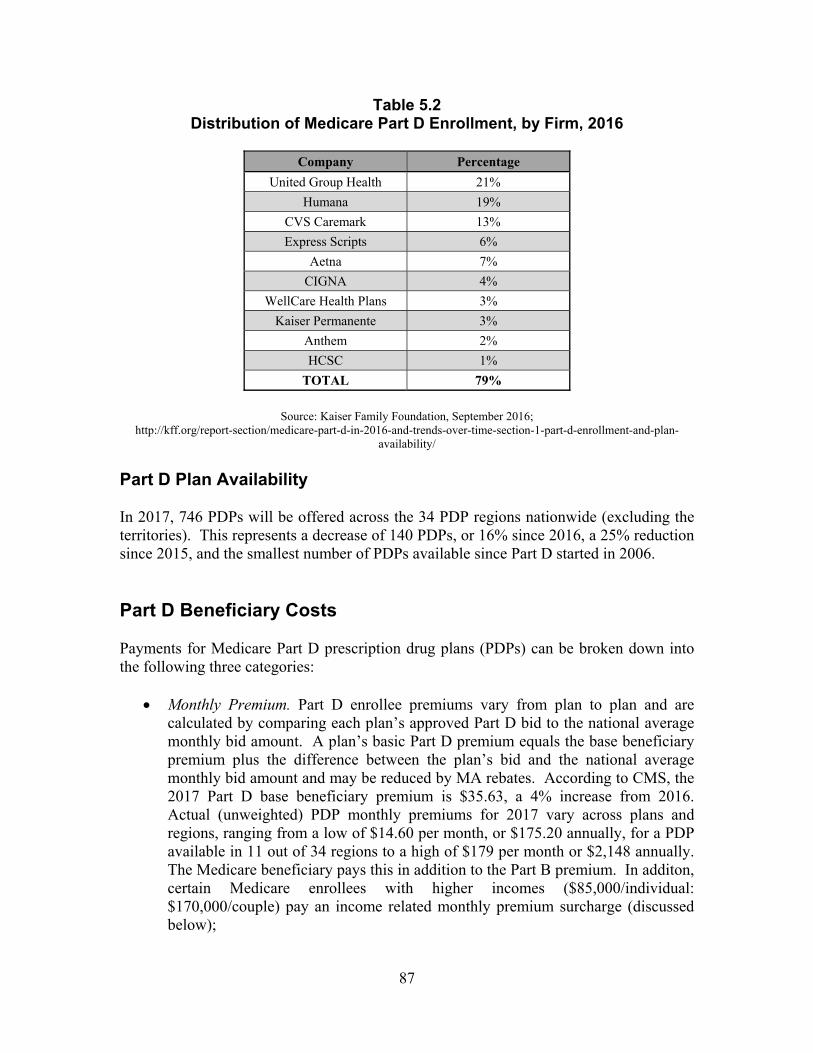

Types of Medicare Part D Plans ....................................................................................... 86 Part D Market Concentration ............................................................................................ 86

Part D Plan Availability ............................................................................................ 87 Part D Beneficiary Costs ................................................................................................... 87 Part D IRMAA Premiums ................................................................................................. 88

The “Doc Fix” ........................................................................................................... 89 The Standard (Model) Drug Benefit Parameters ...................................................... 90

Part D Drug Formularies and Tiers ................................................................................... 91 Part D Excluded Drugs ............................................................................................. 93

Part D Drug Pharmacies.................................................................................................... 94 Part D Enrollment ............................................................................................................. 94 Medicare Plan Finder ........................................................................................................ 98 Extra Help Program .......................................................................................................... 98

Background ............................................................................................................... 99 Eligibility Criteria ..................................................................................................... 99 Income Limits ......................................................................................................... 100 Household Size ....................................................................................................... 101 Resource Limits ...................................................................................................... 101 2017 LIS Subsidy Benchmark Premium Amounts ................................................. 102

Chapter 5 Review Questions .......................................................................................... 104 CHAPTER 6 MEDICARE SUPPLEMENTAL INSURANCE POLICIES ....... 105 Overview ......................................................................................................................... 105 Learning Objectives ........................................................................................................ 105 Background ..................................................................................................................... 105 Medigap Legislation ....................................................................................................... 106 Trends in Medigap Coverage .......................................................................................... 108

Companies Offering Coverage ............................................................................... 109 Consumer Satisfaction with Medigap Policies ....................................................... 112

Standard Medigap Plans ................................................................................................. 113 Basic Benefits ......................................................................................................... 114 Medigap Plan A ...................................................................................................... 115 Medigap Plan B ....................................................................................................... 115 Medigap Plan C ....................................................................................................... 116

8

Medigap Plan D ...................................................................................................... 117 Medigap Plan E ....................................................................................................... 117 Medigap Plan F ....................................................................................................... 118 Medigap Plan G ...................................................................................................... 119 Medigap Plan H ...................................................................................................... 120 Medigap Plan I ........................................................................................................ 120 Medigap Plan J ........................................................................................................ 121 Medigap Plan K ...................................................................................................... 121 Medigap Plan L ....................................................................................................... 122 Medigap Plan M ...................................................................................................... 123 Medigap Plan N ...................................................................................................... 123

Medigap Premiums ......................................................................................................... 124 Issue Age ................................................................................................................. 124 Attained Age ........................................................................................................... 125 Community Age Rated ........................................................................................... 125

Medigap Premium Rates ................................................................................................. 126 Choosing a Medigap Policy ............................................................................................ 126 Medigap Enrollment Dates ............................................................................................. 127

Open Enrollment ..................................................................................................... 128 Guaranteed Issue ..................................................................................................... 128

Regulation of Medigap Policies ...................................................................................... 129 Role of the NAIC .................................................................................................... 129 State Regulation ...................................................................................................... 130

Medigap Policies and the ACA ....................................................................................... 130 Chapter 6 Review Questions .......................................................................................... 132 CHAPTER 7 OPTIONS FOR REFORMING MEDICARE ............................. 133 Overview ......................................................................................................................... 133 Learning Objectives ........................................................................................................ 133 Background ..................................................................................................................... 134 Raise the Medicare Eligibility Age ................................................................................. 134

Argument in Favor .................................................................................................. 135 Argument Against ................................................................................................... 135

Raise Medicare Premiums for Higher-Income Beneficiaries ......................................... 135 Argument in Favor .................................................................................................. 135 Argument Against ................................................................................................... 136

Generate New Revenue by Increasing the Payroll Tax Rate .......................................... 136 Argument in Favor .................................................................................................. 137 Argument Against ................................................................................................... 137

Increase Supplemental Plan Costs and Reduce Coverage .............................................. 137 Argument in Favor .................................................................................................. 138 Argument Against ................................................................................................... 139

Impose Cost-sharing for the First 20 days of a Stay in a SNF ........................................ 139 Argument in Favor .................................................................................................. 140 Argument Against ................................................................................................... 140

Require Drug Companies to Give Rebates or Discounts to Medicare ............................ 140 Argument in Favor .................................................................................................. 141 Argument Against ................................................................................................... 141

9

Medicare Outlook ........................................................................................................... 142 Payments to Health Care Providers ................................................................................ 143 Payments to Medicare Advantage Plans ......................................................................... 144 Medicare Benefit Improvements ..................................................................................... 144 Revenues to the Medicare Trust Funds ........................................................................... 145 Medicare Part B and Part D Premiums for Higher-Income Beneficiaries ...................... 145 Payment and Delivery System Reforms and New Quality Incentives ........................... 146 Independent Payment Advisory Board ........................................................................... 146 Chapter 7 Review Questions .......................................................................................... 149 SECTION TWO MEDICAID ............................................................................. 151 CHAPTER 8 INTRODUCTION TO MEDICAID .............................................. 153 Overview ......................................................................................................................... 153 Learning Objectives ........................................................................................................ 153 Background ..................................................................................................................... 153

State Participation Requirements ............................................................................ 154 Medicaid Financing ........................................................................................................ 155 Medicaid Enrollment and Total Spending ...................................................................... 156

Enrollment and Total Spending .............................................................................. 157 State Medicaid Spending ........................................................................................ 157 Looking Ahead........................................................................................................ 157

Medical Costs Covered by Medicaid .............................................................................. 158 Services Covered in Every State ............................................................................. 158 Optional Services .................................................................................................... 159

Eligibility for Medicaid................................................................................................... 159 General Requirements ............................................................................................. 161

Requirements for Coverage ............................................................................................ 161 Care Must Be Prescribed by Doctor ....................................................................... 161 Provider Must Be Participating In Medicaid .......................................................... 162 Treatment Must Be Medically Necessary ............................................................... 162

Medicaid Coverage Groups ............................................................................................ 162 Category Needy .............................................................................................................. 163

SSI Based Standards ............................................................................................... 163 Section 209(b) States .............................................................................................. 164 Medicaid Eligibility Rules for Married Spouses .................................................... 165

Treatment of Assets ........................................................................................................ 166 The Community Spouse Resource Allowance (CSRA) ......................................... 166

The Assessment .............................................................................................................. 167 Treatment of Income ....................................................................................................... 168

The Minimum Monthly Maintenance Needs Allowance ........................................ 169 The Revised Community Spouse Resource Allowance .......................................... 169

Reconciling the Revised CSRA and the CSMIA ............................................................ 170 Medically Needy Program .............................................................................................. 171

Medicaid Needy Eligibility ..................................................................................... 171 Spend-Down ........................................................................................................... 172 Income Eligibility ................................................................................................... 173 Budget Period.......................................................................................................... 174 Pay-In Spend-down ................................................................................................. 175

10

Costs of Medicaid Coverage ........................................................................................... 175 No Payments to Medical Providers......................................................................... 176 Fees to States for Medicaid Services ...................................................................... 176 Enrollment Fee ........................................................................................................ 176 Monthly Premium ................................................................................................... 176 Co-Payments ........................................................................................................... 176

The Deficit Reduction Act (DRA) of 2005 ..................................................................... 177 The Look-Back Period [Section 6011] ................................................................... 177 The Penalty Period Start Date [Section 6011(b)] ................................................... 178 When Period of Ineligibility Starts and the Penalty ............................................... 178 Imposing Partial Months of Ineligibility [Section 6016(a)] ................................... 179 Hardship Waivers [Section 6011(d)(e)] .................................................................. 179 Codifying “Income First” Methodology for Protecting Community Spouse ......... 180 Home Equity Limits (Section 6014) ....................................................................... 181 Disclosure and Treatment of Annuities (Section 6012) .......................................... 181 State Long-Term Care Partnerships (Section 6021) ............................................... 182 Continuing Care Retirement Communities (Section 6015) .................................... 182 Promissory Note, Loan, or Mortgage ..................................................................... 182 Life Estate ............................................................................................................... 182

Medicaid Expansion and the ACA ................................................................................. 183 States Participating/Not Participating in the Medicaid Expansion ......................... 184 Who Pays For Medicaid Expansion? ...................................................................... 186 Additional Provisions Affecting Medicaid Expansion ........................................... 186

Future of Medicaid .......................................................................................................... 187 Chapter 8 Review Questions .......................................................................................... 188 CHAPTER 9 MEDICAID PLANNING ........................................................... 189 Overview ......................................................................................................................... 189 Learning Objectives ........................................................................................................ 189 The Ethics of Medicaid Planning .................................................................................... 189 Transferring Assets to Qualify for Medicaid .................................................................. 191

Permitted Transfers ................................................................................................. 193 Medicaid Planning and Trusts ........................................................................................ 193

Revocable Trusts ..................................................................................................... 194 Irrevocable Trust ..................................................................................................... 194 Special Needs Trusts ............................................................................................... 195 Qualified Income (‘Miller”) Trusts ......................................................................... 197 Testamentary Trusts ................................................................................................ 199

Medicaid Planning and Annuities ................................................................................... 199 How Purchasing an Annuity Depletes Assets ......................................................... 199 Single Premium Immediate Annuity ...................................................................... 200 Why Annuities Don’t Violate Medicaid Rules ....................................................... 200 Annuity Requirements to Avoid Medicaid Penalties.............................................. 201 Recent Court Cases ................................................................................................. 201

Medicaid Planning and IRAs .......................................................................................... 205 IRA in Payout Status ............................................................................................... 206 Use of an Annuity in an IRA .................................................................................. 206

Medicaid and Promissory Notes ..................................................................................... 207

11

How It Works .......................................................................................................... 208 Medicaid Estate Recovery Program (MERP) ................................................................. 209

Status of Estate Recovery Program ......................................................................... 210 Use of Liens ............................................................................................................ 210

Role of the Children ........................................................................................................ 211 Filial Responsibilities Laws ............................................................................................ 211

Generally Not Enforced .......................................................................................... 212 Chapter 9 Review Questions .......................................................................................... 213 CHAPTER REVIEW ANSWERS ..................................................................... 215 CONFIDENTIAL FEEDBACK FORM ............................................................... 217

12

This page left blank intentionally

13

SECTION ONE

MEDICARE

14

This page left blank intentionally

15

CHAPTER 1 INTRODUCTION TO MEDICARE Overview Medicare is a federal insurance program that pays covered health care services of qualified beneficiaries. While commonly known as Medicare, it was established in 1965 under Title XVIII - Health Insurance for the Aged and Disabled within the Social Security Act as a federal entitlement program. As part of the Social Security Amendments signed into law by President Lyndon B. Johnson in 1965, the Medicare legislation established a health insurance program for aged persons that would complement the retirement, survivors, and disability insurance benefits created under Title II of the Social Security Act. This chapter will examine the background of the federal health insurance program: Medicare. We will examine the differences between Traditional Medicare and Medicare Advantage (Part C), the financing and rules for eligibility. At the end of the chapter, we will examine the finances of the two Medicare Trust Funds (HI and SMI) and review the short-range and long-range conclusions of the 2017 Medicare Trustees Report. Learning Objectives Upon completion of this chapter, you will be able to:

Relate the history and the administration of the Medicare program; Identify the various Parts of Medicare: Part A, Part B, Part C, and Part D; Distinguish the differences in coverage between Traditional Medicare and

Medicare Advantage (Part C); Explain the financing and spending budgets of Medicare; Outline the Medicare gaps and out-of-pocket costs for the beneficiaries; and Describe the financial outlook of the Medicare program.

History of Medicare Medicare was established in 1965 as a federal insurance program to provide what the private insurance market did not: adequate, affordable health insurance for America elderly population regardless of income or health status. Prior to Medicare only half of the population age 65 and older had health insurance. Even among those 65 and older

16

who were insured, premiums and other out-of-pocket costs were close to three times what younger people paid, even though the elderly had on average only half as much income. Since 1965, the Medicare program has undergone considerable change. Most recently, the Patient Protection and Affordable Care Act (ACA) of 2010 (ACA, P.L. 111-148 as amended), made numerous changes to the Medicare program. It is important to remember, that the Medicare program is an entitlement program, which means that it is required to pay for covered services provided to enrollees so long as specific criteria are met. Currently, Medicare is the nation’s largest health insurance program, accounts for one in five health care dollars, and currently accounts for 15 percent of the federal budget—a figure that is expected to reach 17.5 percent by 2027. According to the 2017 Annual Report of the Boards of Trustees of the Federal Hospital Insruance and Federal Supplementary Medical Insurance Trust Funds, in 2016 Medicare covered 56.8 million people: 47.8 million aged 65 and older, and 9.0 million disabled (see Table 1.1).

Table 1.1 Medicare Enrollment (1996-2016)

Year Total Persons Aged Persons Disabled

1996 19.1 19.1 --

1970 20.4 20.4 --

1975 24.9 22.7 2.2

1980 28.4 25.5 3.0

1985 31.1 28.1 2.9

1990 34.3 31.0 3.3

1995 37.6 33.2 4.4

2000 39.7 34.3 5.4

2005 42.6 35.8 6.8

2010 47.7 39.6 8.1

2011 48.9 40.5 8.4

2012 50.9 42.2 8.6

2013 52.3 43.5 8.8

2014 53.8 44.9 8.9

2015 55.3 46.3 9.0

2016 56.8 47.8 9.0

Notes: Represents those enrolled in HI (Part A) and/or SMI (Part B and Part D). Data for 1966-1995 are as of July. Numbers may

not add to totals because rounding. Based on 2016 Trustees Report. Source: CMS, Office of the Actuary; http://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-

Reports/ReportsTrustFunds/Downloads/TR2017.pdf

17

Medicare Administration The Department of Health and Human Services (DHHS) has the overall responsibility for administration of the Medicare program. Within the Department of Health and Human Services (DHHS), responsibility for administering Medicare rests with the Centers for Medicare & Medicaid Services (CMS), whose central office is in Baltimore, Maryland. The Social Security Administration (SSA) offices assists, however, by initially determining an individual’s Medicare entitlement; by withholding Part B premiums from the Social Security benefit checks of most beneficiaries; by providing general information about the program, and by maintaining Medicare data on the master beneficiary record, which is the Social Security Administration’s primary record of beneficiaries. The Medicare Prescription Drug, Improvement, and Modernization Act (MMA) requires Social Security Administration (SSA) to undertake a number of additional Medicare-related responsibilities, including making low-income subsidy determinations under Part D; notifying individuals of the availability of Part D subsidies, withholding Part D premiums from monthly Social Security cash benefits for those beneficiaries who request such an arrangement; and, for 2007 and later, making determinations as to the amount of the individual’s Part B premium if the income-related monthly adjustment applies. The Internal Revenue Service (IRS) in the Department of the Treasury collects the Part A payroll taxes from workers and their employers. IRS data, in the form of income tax returns; plays a role in determining which Part D enrollees are eligible for low-income subsidies (and to what degree); and, for 2007 and later, which Part B enrollees are subject to the income-related monthly adjustment amount (IRMAA) in their premiums (and to what degree). Medicare Parts Medicare originally consisted of two parts:

Hospital Insurance (HI), also known as Part A; and Supplementary Medical Insurance (SMI), which in the past was also known

simply as Part B. Original Medicare: Part A and Part B Original Medicare is made up of both Part A and Part B. Part A helps pay for inpatient hospital, home health, skilled nursing facility, and hospice care. Part A is provided free of premiums to most eligible people; certain otherwise ineligible people may voluntarily pay a monthly premium for coverage (see Chapter 2 for a full discussion of Part A). Part B helps pay for physician, outpatient hospital, home health, and other services. To be covered by Part B, all eligible beneficiaries must pay a monthly premium (see Chapter 3 for a full discussion of Part B).

18

Medicare Part C A third part of Medicare, sometimes known as Part C, is the Medicare Advantage program, which was established as the Medicare+ Choice program by the Balanced Budget Act (BBA) of 1997 (Law 105-33) and subsequently renamed and modified by the Medicare Prescription Drug, Improvement, and Modernization Act (MMA) of 2003 (Public Law 108-173). The Medicare Advantage program expands beneficiary options for participation in private-sector health care plans (see Chapter 4 for a full discussion of Part C). Medicare Part D The Medicare Prescription Drug, Improvement, and Modernization Act (MMA) of 2003 also established a fourth part of Medicare, known as Part D, to help pay for prescription drugs not otherwise covered by Original Medicare (Part A and/or Part B). Part D initially provided access to prescription drug discount cards, on a voluntary basis and at limited cost, to all enrollees (except those entitled to Medicaid drug coverage) and, for low-income beneficiaries, transitional limited financial assistance for purchasing prescription drugs and a subsidized enrollment fee for the discount cards. This temporary plan began in mid-2004 and phased out during 2006. In 2006 and later, Part D provides subsidized access to prescription drug insurance coverage on a voluntary basis, upon payment of premium, for all beneficiaries, with premium and cost-sharing subsidies for low-income enrollees (see Chapter 5 for a full discussion of Part D). Note: Part D activities are handled within the SMI Trust Fund, but in an account separate from Part B. It should thus be noted that the traditional treatment of “SMI” and “Part B” as synonymous is no longer accurate, since SMI now consists of both Parts B and D. The purpose of the two separate accounts within the SMI Trust Fund is to ensure that funds from one part are not used to finance the other. Medicare Eligibility As was discussed above, when first implemented in 1966, Medicare covered most persons age 65 or over. In 1973, the following groups also became eligible for Medicare benefits:

Persons entitled to Social Security or Railroad Retirement disability cash benefits for at least 24 months;

Most persons with end-stage renal disease (ESRD); and Certain otherwise non-covered aged persons who elect to pay a premium for

Medicare coverage. Beginning in July 2001, persons with Amyotrophic Lateral Sclerosis (Lou Gehrig’s disease) are allowed to waive the 24-month waiting period.

19

Applying for Medicare Benefits Medicare benefits become available at the beginning of the beneficiaries birth month upon reaching their 65th birthday. This is true even if the beneficiary is still working. If they are eligible, they will receive their Medicare card (red, white and blue) in the mail 3 months before their 65th birthday. Medicare benefits are also available after an individual has been receiving Social Security disability benefits for two years (receive their Medicare card on their 25th month of disability) or has end-stage renal disease (ESRD) requiring renal dialysis or a kidney transplant. If a beneficiary doesn’t want Part B, he/she must follow the instructions that come with the card, and send the card back. If the beneficiary keeps the card, he/she keeps Part B and will be required to pay the Part B premiums (discussed below). Note: The best and official source of answers to many Medicare questions can be found in the “Medicare and You 2017” booklet. To download a copy visit https://www.medicare.gov/pubs/pdf/10050-Medicare-and-You.pdf Choosing Medicare Coverage There are two main choices an individual, who qualifies for Medicare, can choose to receive Medicare coverage. They are:

Original Medicare (Medicare Part A and Part B); or Medicare Advantage Plan (Part C).

Here are the following steps a Medicare beneficiary must take to choose his or her Medicare program. In the following chapters, the words “beneficiary, they, their(s), he/she, and patient, etc.”, means the “person enrolling for coverage”. Step 1: Decide as beneficiary which option of coverage:

A. Original Medicare:

o Part A (HI); and o Part B (MI);

Or B. Part C: Medicare Advantage Plan (like and HMO or PPO):

o Combines Part A, Part B and usually Part D.

Step 2: Decide if the beneficiary needs drug coverage (Part D): o Medicare Prescription Drug Plan; or o Medicare Advantage with Drug Plan (MA-PD).

Step 3: Decide if beneficiary needs to add supplemental coverage to their Original Medicare. Note: If beneficiary joins a Medicare Advantage Plan, they will not need (and can’t be sold) a Medicare Supplement policy (also known as Medigap).

20

Number of People Enrolled in Medicare As was discussed above, 55.3 million people (or approximately one out of every six individuals) received care financed through one or more parts of Medicare, in 2015. While 84 percent of Medicare enrollees are 65 and older, 16 percent are under 65 and disabled. Almost 32 percent of these beneficiaries have chosen to enroll in Part C private health plans that contract with Medicare to provide Part A and Part B health services. Table 1.2 displays the projected average monthly enrollment during fiscal year 2015. According to CMS’ Office of the Actuary, it projects that 99 percent of total persons (beneficiaries) participate in Part A, 92 percent participate in Part B and 75 percent participate in Part D.

Table 1.2 Medicare Enrollmements FY 2016

HI or Part A

SMI

Part B Part D Total All persons 56.88 50.7 41.8 55.3 Aged persons 47.88 42.5 34.8 46.3 Disabled persons 9.0 8.2 7.0 9.0

NOTES: Projected average monthly enrollment during fiscal year62016. Aged/disabled split of Part D enrollment not

available. Based on 2017 Trustees Report. Numbers may not add to totals because of rounding. Source: CMS, Office of the Actuary;

http://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/ReportsTrustFunds/Downloads/TR2017.pdf

CMS’ Office of the Actuary projects that the total number of people enrolled in the Medicare program will increase to 81 million in 2030 (see Table 1.3). The rate of increase in Medicare enrollment will accelerate until 2030 as more members of the baby-boom generation has become eligible.

Table 1.3 Enrollment in Medicare Program is Projected

to Grow Rapidly in the next 20 Years

20.1 28.0 33.7 39.348.0

63.780.6 87.2 90.3 96.1 103.2

110.5

0

50

100

150

1970 1980 1990 2000 2011 2020 2030 2040 2050 2060 2070 2080

Note: Enrollment numbers are based on Part A enrollment only. Beneficiaries enrolled in Part B are not included.

Source: CMS Office of the Actuary, 2014

21

Medicare Financing Under current law, the government draws from several sources of revenue to finance Medicare (see figure 1.4). All revenue collected is deposited into the Medicare Trust funds.

Figure 1.4 Sources of Medicare Revenue, 2016

Note: Data are for the calendar year. Source: 2017 Annual Report of the Boards of Trustees of the Federal Hospital Insurance and Federal

Supplementary Medical Insurance Trust Funds, Table II.B1. https://www.ssa.gov/policy/docs/statcomps/supplement/2016/supplement16.pd

Medicare Trust Funds Medicare’s financial operations are accounted for through two trust funds maintained by the Department of Treasury. They are:

The Hospital Insurance (HI) Trust Fund for Part A; and The Supplementary Medicare Insurance (SMI) Trust Fund for Parts B and D.

Note: For beneficiaries enrolled in the Medicare Advantage (Part C), payments are made on their behalf in appropriate portions from the HI and SMI Trust Funds.

22

The Hospital Insurance (HI) Trust Fund The HI Trust Fund, into which Medicare payroll taxes and other dedicated revenue are credited, pays for inpatient hospital stays and other benefits provided under Medicare Part A. Total HI payroll tax income in calendar year 2016 amounted to $241.1 billion—an increase of 6.0 percent over the amount of $227.4 billion for the precediung 12-month period. This increase in tax income resulted primarily from increases in the number of workers and in their average earnings. The payroll tax accounted for 87 percent of total revenue collected in the HI Trust Fund. The Supplementary Medical Insurance (SMI) Trust Fund The SMI Trust Fund is used to pay for physician visits and other Medicare Part B services as well as the Medicare Part D prescription drug benefit. The SMI Trust Fund is financed primarily through monthly Part B and Part D premiums paid by beneficiaries and general revenue. In 2016, general revenue ($272.3 billion) accounted for 74 percent of the SMI Trust Fund revenue and 42 percent of all Medicare revenue ($644.4 billion), while total beneficiary premiums made up 30.2 percent of the SMI Trust Fund revenue and 13 percent of Medicare revenue overall. Trust Fund Board of Trustees A Board of Trustees, composed of two appointed members of the public and four members who serve by virtue of their positions in the Federal government, oversees the financial operations of the HI and SMI Trust Funds. The Secretary of the Treasury is the managing trustee. The Board of Trustees reports to Congress on the financial and actuarial status of the Medicare trust funds on or about the first day of April each year. State agencies (usually State Health Departments under agreements with CMS) identify, survey, and inspect provider and supplier facilities and institutions wishing to participate in the Medicare program. In consultation with CMS, these agencies then certify the facilities that are qualified. The Centers for Medicare and Medicaid Services (CMS) is also responsible for establishing the reimbursement rate of all covered services. Medicare Spending Medicare spending was 15 percent of total federal spending in 2016, and is projected to rise to 17.5 percent by 2027 (see Figure 1.5).

23

Figure 1.5

Note: All amounts are for federal fiscal year 2016. Consists of mandatory Medicare spending minus income from premiums and other offsetting receipts.

²Includes spending on other mandatory outlays minus income from offsetting receipts. Source: Congressional Budget Office, An Update to the Budget and Economic Outlook, 2017 to 2027 (June 2017).

Kaiser Family Foundation: The Fcts on Medicare Spending, July 2017 http://www.kff.org/medicare/issue-brief/the-facts-on-medicare-spending-and-financing/

In 2016, Medicare benefit payments totaled $675 billion, up from $375 billion in 2006. The distribution of Medicare benefit payments has changed in significant ways over the past ten years (see Figure 1.6).

Figure 1.6

Note: *Consists of Medicare benefit spending on hospice, durable medical equipment, Part B drugs, outpatient dialysis,

ambulance, lab services, and other Part B services.

Source: Congressional Budget Office, June 2017 Medicare Baseline. Kaiser Family Foundation: The Fcts on Medicare Spending, July 2017

http://www.kff.org/medicare/issue-brief/the-facts-on-medicare-spending-and-financing/

24

Most notably, the share of total spending on hospital inpatient services declined by one-third between 2006 and 2016, from 32 percent to 21 percent, while payments to Medicare Advantage (private health plans which cover all Part A and Part B benefits) doubled, from 15 percent to 30 percent, as private plan enrollment has grown steadily since 2006. Thirty percent of benefit spedning ws for Medicare Advantage plans; in 2017, 33 percent of Medicare beneficiaries are enrolled in Medicare Advantage plans, up from 16 percent in 2006. Over these years, spending on outpatient prescription drugs (Part D) increased from 9 percent of total benefit payments to 14 percent in 2016, according to the Kaiser Family Foundation. Recent Trends in Medicare Spending Medicare spending is growing for many of the same reasons health care spending in the private sector is growing—higher prices for providers, intensity of services and new medical technology. In the last five years, total and per capita Medicare spending have grown more slowly than in the previous decade. Annual growth in total Medicare spending averaged 4.4% between 2010 and 2016, compared to 9.0% between 2000 and 2010, based on data from the Office of the Actuary, National Health Statistics Group (OACT), despite growth in the number of beneficiaries and increases in health care costs over these years (see Figure 1.7). Spending per capita was lower than total program spending in both time periods; per capita spending growth averaged just 1.3% between 2010 and 2016, compared to 7.4% between 2000 and 2010.

Figure 1.7

Source: Kaiser Family Foundation: The Fcts on Medicare Spending, July 2017

http://www.kff.org/medicare/issue-brief/the-facts-on-medicare-spending-and-financing/

Future Trends in Medicare Spending The Congressional Budget Office (CBO) projects that mandatory spending for net Medicare outlays (that is, Medicare spending minus income from premiums and other offsetting receipts) are projected to increase from $591 billion in 2016 to $1,075 trillion in 2026 (see Figure 1.8). Between 2016 and 2026, Medicare’s share of the budget is projected to increase from 15.2% to 16.8%, while Medicare spending as a share of the gross domestic product (GDP) is projected to increase from 3.2% to 3.9%. CBO’s short-

25

term estimates, however, do not take into account the spending effects of changes to Medicare’s physician payment system brought about by the Medicare Access and CHIP Reauthorization Act of 2015 (MACRA), a new law to repeal and replace Medicare’s Sustainable Growth Rate (SGR) formula. These effects are incorporated, however, in the most recent Medicare spending projections from OACT. Over the next decade, OACT projects that total Medicare spending will increase from $695 billion in 2016 to $1.2 trillion in 2026.

Figure 1.8

Note: All amounts are for federal fiscal years; amounts are in billions and consist of mandatory Medicare spending minus income from premiums an other offsetting receipts.

Source: Congressional Budget Office, Updated Budget Projections: 2016 to 2026 (March 2016); March 2016 Medicare Baseline.

Medicare Gaps and Out-of-Pocket Costs Medicare provides protection against the costs of many health care services, but has relatively high deductibles and cost-sharing requirements, no limit on out-of-pocket spending, and (until 2020) a coverage gap (“donut hole”) in the prescription drug benefit. Moreover, Medicare does not pay for many services needed by elderly and disabled beneficiaries, such as long-term care, vision, hearing-aides or dental services. In a report released by the Kaiser Foundation, “How Much Is Enough? Out-of-pocket Spending among Medicare Beneficiaries: A Chartbook,”(July 2014), their key finding is that in 2010 Medicare beneficiaries spent $4,734 out of their own pockets for health care spending, on average, including premiums for Medicare and other types of supplemental insurance and costs incurred for medical and long-term care services.

Premiums for Medicare and supplemental insurance accounted for 42 percent ($1,989) of average total out-of-pocket spending among beneficiaries in traditional Medicare in 2010; and

Of the remaining 58 percent ($2,744) of average total out-of-pocket spending on services, long-term facility costs are the largest component (accounting for 18 percent of total out-of-pocket spending), followed by medical providers/supplies

26

(14%), prescription drugs (11%), and dental care (6%). Neither long-term care services and supports nor dental services are covered by Medicare.

According to a recent report by the Kaiser Family Foundation, “The Facts on Medicare Spending and Financing”, www.kff.org ,Medicare pays for only 51% of the average healthcare costs for an American senior, and they have estimated that a Medicare beneficiary with an AGI of $85,000 ($170,000 if married filing jointly) will spend on average $8,000 each year on routine medical expenses in retirement. The 2017 Trustees Report on Medicare The Social Security Act requires that the Board, among other duties, report annually to the Congress on the financial and actuarial status of the HI and SMI Trust Funds. The 2017 report is the 52nd that the Board has submitted. Short-Range Results The estimated depletion date for the HI trust fund is 2029, one year later than in last year’s report. As in past years, the Trustees have determined that the fund is not adequately financed over the next 10 years. HI expenditures are projected to be lower than last year’s estimates, mostly due to lower inpatient hospital utilization assumptions and lower-than-expected spending in 2016. In 2016, HI income exceeded expenditures by $5.4 billion. The Trustees project modest surpluses to continue in 2017 through 2022, with a return to deficits thereafter until the trust fund becomes depleted in 2029. The assets were $199.1 billion at the beginning of 2017, representing about 67 percent of expenditures during the year, which is below the Trustees’ minimum recommended level of 100 percent. The HI trust fund has not met the Trustees’ formal test of short-range financial adequacy since 2003 (as discussed in section III.B). Growth in HI expenditures has averaged 2.1 percent annually over the last 5 years, compared with non-interest income growth of 5.9 percent. Over the next 5 years, projected annual growth rates for expenditures and non-interest income are 5.7 percent and 5.8 percent, respectively. The SMI trust fund is expected to be adequately financed over the next 10 years and beyond because premium income and general revenue income for Parts B and D are reset each year to cover expected costs and ensure a reserve for Part B contingencies. A hold-harmless provision in the law restricted Part B premium increases for most beneficiaries in 2017 to an average increase of about $4.00 per month. However, for the 30 percent of beneficiaries to whom the provision does not apply, the 2017 Part B monthly premium rate increased substantially from $121.80 to $134.00. (See sections II.F and III.C for further details.) Part B and Part D costs have averaged annual growth of 5.4 percent and 8.3 percent, respectively, over the last 5 years, as compared to growth of 3.7 percent for GDP. Under current law, the Trustees project an average annual Part B growth rate of 7.8 percent over the next 5 years; for Part D, the estimated average annual increase in expenditures for these 5 years is 6.4 percent. The projected average annual rate of growth for the U.S. economy is 5.2 percent during this period, significantly slower than for Part B and Part D. A finding of excess general revenue Medicare funding

27

(defined as a determination that occurs when the difference between Medicare’s total outlays and its dedicated financing sources6 exceeds 45 percent of outlays) is projected for fiscal year 2023. Therefore, the Trustees are issuing a determination of projected excess general revenue Medicare funding in this report. Such determinations were previously made in each of the 2006 through 2013 reports. Long-Range Results For the 75-year projection period, the HI actuarial deficit has decreased to 0.64 percent of taxable payroll from 0.73 percent of taxable payroll in last year’s report. (Under the illustrative alternative projections, the HI actuarial deficit would be 1.76 percent of taxable payroll, compared to 1.85 percent in last year’s report.) The 0.09 percent of payroll decrease in the actuarial deficit was primarily due to lower spending in 2016 and lower projected utilization of inpatient hospital services than were previously estimated. Part B outlays were 1.6 percent of GDP in 2016, and the Board projects that they will grow to about 2.6 percent by 2091 under current law. The long-range projections as a percent of GDP are slightly higher than those in last year’s report. (Part B costs in 2091 would be 4.2 percent under the illustrative alternative scenario.) The Board estimates that Part D outlays will increase from 0.5 percent of GDP in 2016 to about 1.2 percent by 2091. These long-range outlay projections, as a percent of GDP, are slightly lower than those shown in last year’s report. Transfers from the general fund finance about three-quarters of SMI costs and are central to the automatic financial balance of the fund’s two accounts. Such transfers represent a large and growing requirement for the Federal budget. SMI general revenues currently equal 1.7 percent of GDP and would increase to an estimated 2.7 percent in 2091. Conclusion Total Medicare expenditures were $679 billion in 2016. The Board projects that expenditures will increase in future years at a faster pace than either aggregate workers’ earnings or the economy overall and that, as a percentage of GDP, they will increase from 3.6 percent in 2016 to 5.9 percent by 2091 (based on the Trustees’ intermediate set of assumptions). If the reduced price increases for physicians and other health services under Medicare are not sustained and do not take full effect in the long range as in the illustrative alternative projection, then Medicare spending would instead represent roughly 9.0 percent of GDP in 2091. Growth under any of these scenarios, if realized, would substantially increase the strain on the nation’s workers, the economy, Medicare beneficiaries, and the Federal budget. The Trustees project that HI tax income and other dedicated revenues will fall short of HI expenditures in most future years. The HI trust fund does not meet either the Trustees’ test of short-range financial adequacy or their test of long-range close actuarial balance. The Part B and Part D accounts in the SMI trust fund are expected to be adequately financed because premium income and general revenue income are reset each year to cover expected costs. Such financing, however, would have to increase faster than the economy to cover expected expenditure growth. The financial projections in this report indicate a need for substantial steps to address Medicare’s remaining financial challenges. Consideration of further reforms should occur

28

in the near future. The sooner solutions are enacted, the more flexible and gradual they can be. Moreover, the early introduction of reforms increases the time available for affected individuals and organizations—including health care providers, beneficiaries, and taxpayers—to adjust their expectations and behavior. The Trustees recommend that Congress and the executive branch work closely together with a sense of urgency to address the depletion of the HI trust fund and the projected growth in HI (Part A) and SMI (Parts B and D) expenditures. Medicare and the Affordable Care Act (ACA) of 2010 As mentioned above in the 2016 Medicare Trustees report, the “Affordable Care Act” or ACA contains roughly 165 provisions affecting the Medicare program including enhanced benefits (free prevention services and phasing out the Part D coverage gap); spending reductions affecting plans and providers; delivery system reforms, premium increases for higher-income beneficiaries; and a payroll tax on earnings for higher-income people. In addition, the law authorizes a new Independent Payment Advisory Board tasked with constraining the growth in Medicare spending over time. In fact, the 2017 Medicare Trustees Report shows that passing health care reform legislation was important in extending the solvency of the Medicare trust funds. Medicare’s costs are projected to be substantially lower due to savings in the ACA. However, the report also points out the need to further reform our health care system so that Medicare’s costs, which will grow due to the retirement of the baby boom generation and the increase in health spending per beneficiary, are affordable for both the federal government and individuals. Medicare SGR Update Congress has been debating the shortcoming of the SGR policy for more than a decade. Each year for the past decade, the SGR has perpetuated a vicious cycle that has threatened dramatic payment cuts to physicians and endangered access to care for seniors. Over the same time, the SGR has also forced a series of extremely expensive short-term Congressional patches to be passed -16 patches in all costing American taxpayers $154 billion. And what has Congress obtained for $154 billion? Some would say: perpetuation of a bad policy and the obligation to spend more money on future patches. Since 2003, Congress has invested more in legislative patches than the most recent CBO estimated cost of $117 billion to simply repeal the SGR altogether. The cost of each short-term patch has grown significantly over time. In the last three years alone, the cost of stopping the looming cut grew from $14.9 billion in 2011 to $25.2 billion in 2013. Previously, short-term legislative patches have grown the problem by increasing an SGR proposed payment cut from 5 percent in 2007 to 24 percent for 2014. At the same time, it has been reported that there is an enormous and widening gap between what Medicare

29

pays and the actual cost of caring for seniors. Since 2001, the cost of care has risen by 25 percent while physician payments have risen less than 4 percent. Today, average Medicare practice expense payments cover only 54 percent of physicians’ direct costs. Many are calling on Congress to take action. President Barrack Obama had signed into law the bipartisan bill H.R. 2, the “Medicare Access and CHIP Reauthorization Act of 2015,”also referred to as the “Doc Fix” bill, which permanently repeals the flowed Sustainable Growth Rate (SGR) formula and replaces it with a stable Medicare payment system that rewards physicians for providing high-quality, high-value health care. Without this new law, physicians would have faced a 21.2 percent decrease in Medicare payment rates taking effect on April 1, 2015. The new law ends the cycle of annual short-term fixes, which have occurred 17 times since 2001. The law fully repeals the SGR formula and replaces it with a gradual evolution to a new value-based physician payment system. Initially, physicians will see modest annual updates to the existing fee-for-service system coupled with increasing opportunity to earn pay-for-performance bonuses and to participate in APMs involving performance goals and shared risk. The law supports this transition with various studies, evaluations and system requirements to guide the development of the new value-based payment approach. The big question: How is this going to be paid for? One way will be the elimination of Medigap first-dollar coverage: Beginning in 2020, new Medigap plans sold will limit coverage to costs above the amount of the Part B deductible ($183 in 2017). In addition, beginning in 2018, the income-related premium adjustment for Parts B and D will increase the percentage that Medicare beneficiaries with modified adjusted gross income (MAGI) between $133,501 and $160,000 ($267,001-$320,000 for a couple) will pay from 50 percent to 65 percent. Beneficiaries that earn $160,001 and above ($320,001 and above for a couple) will pay 80 percent. Starting in 2020, this policy will update the threshold for inflation based on where beneficiaries were in 2019.

30

Chapter 1 Review Questions

1. Medicare was established in 1965 under what Title of the Social Security Act? ( ) A. Title X ( ) B. Title XVIII ( ) C. Title XXIII ( ) D. Title XXX 2. Which of the following Trust Funds is used to pay expenses for Part A? ( ) A. The Hospital Insurance (HI) Trust Fund ( ) B. The Supplementary Medical Insurance (SMI) Trust Fund ( ) C. The Disability Insurance (DI) Trust Fund ( ) D. The Old-age Survivor Insurance (OASI) Trust Fund 3. True or False. The Department of Health and Human Services (DHHS) has the

overall responsibility for administration of the Medicare program.

( ) A. True ( ) B. False 4. What is the estimated asset depletion date for the HI trust fund? ( ) A. 2016 ( ) B. 2024 ( ) C. 2025 ( ) D. 2028 5. Which of the following Acts enacted by congress repeals the flowed Sustainable

Growth Rate (SGR) formula and replaces it with a stable Medicare payment system that rewards physicians for providing high-quality, high-value health care?

( ) A. The Bipartisan Budget Act of 2015 ( ) B. The Deficit Reduction Act of 2005 ( ) C. The Medicare Access and CHIP Reauthorization Act of 2015 ( ) D. The Medicare Modernization Act of 2003

31

CHAPTER 2 MEDICARE PART A Overview Medicare Part A is referred to as Hospital Insurance (HI) and covers most of the cost of inpatient care in hospitals (such as critical access hospitals, inpatient rehabilitation facilities and long-term care hospitals) and several other services. This chapter will review Medicare Part A, its eligibility requirements; services provided; how it is financed; its various out-of-pocket costs (such as premiums, deductibles and copays); and the enrollment periods. Learning Objectives Upon completion of this chapter, you will be able to:

Determine eligibility for Part A; Explain the financing of Part A; Outline Part A covered services and costs; and Observe Part A enrollment periods and late fees.

Who Is Eligible For Part A (HI) All persons age 65 and over who are entitled to monthly Social Security benefits (or would be entitled to benefits except that an application for benefits has not been filed), or monthly benefits under Railroad Retirement programs (whether retired or not), are eligible for benefits. Persons age 65 and over can receive Medicare benefits even if they continue to work. Enrollment in the program while working will not affect the amount of any future Social Security benefits. A dependent or survivor of a person entitled to HI benefits, or a dependent of a person under age 65 who is entitled to retirement or disability benefits, is also eligible for HI (Part A) benefits if the dependent or survivor is at least 65 years old. For example, a woman age 65 or over who is entitled to a spousal or widow’s Social Security benefit is eligible for benefits under Hospital Insurance.

32

A Social Security disability beneficiary is covered under Medicare after entitlement to disability benefits for 24 months or more. Those covered include disabled workers at any age, disabled widows and widowers age 50 or over, beneficiaries age 18 or older who receive benefits because of disability beginning before age 22 and disabled qualified railroad retirement annuitants. Medicare coverage is automatic. No application is required. A person who becomes re-entitled to disability benefits within five years after the end of a previous period of entitlement (within seven years in the case of disabled widows or widowers and disabled children) is automatically eligible for Medicare coverage without the need to wait another 24 months. However, if the previous period of disability ends on or after March 1, 1988 and the current impairment is the same as or directly related to the impairment in the previous period of disability, he/she is covered without again needing to meet the 24-month waiting period requirement. However, and further, if the previous period of disability ends on or after March 1, 1988, he/she is covered without again needing to meet the 24-month waiting period requirement, if the current impairment is the same as (or directly related to) that in the previous period of disability. Coverage will continue for 24 months after an individual is no longer entitled to receive disability payments because he/she has returned to work, provided he/she was considered disabled on or after December 10, 1980, and the disabling condition continues. Special Eligibility Rules for Persons with End-Stage Renal Disease Part A coverage is also provided to insured workers (and their dependents) with end-stage renal diseases (ESRD) who require renal dialysis or a kidney transplant even if they are working. Coverage can begin the first day of the third month after the month dialysis treatments begins. Special Rules for Government Employees Federal employees who were not covered under Social Security (temporary workers have been covered since 1951) began paying the Hospital Insurance (HI) portion of Social Security tax in 1983. Those covered under Social Security, such as virtually all hired after 1983, pay the HI tax as well as the Social Security Old-Age, Survivors, and Disability Insurance (OASDI) tax. A transitional provision provides credit for retroactive quarters of coverage for federal employees who were employed before 1983 and also on January 1, 1983. State and local government employees hired after March 31, 1986, are covered under Medicare coverage and tax provisions. A person who was performing substantial and regular service for a state or local government before April 1, 1986, is covered provided he/she was a bona fide employee on March 31, 1986, and the employment relationship was not entered into in order to meet the requirements for exemption from coverage.

33