Embed Size (px)

Citation preview

Termination Rate Debate Dr. Christoph Stork

Tuesday, 21 August 12

Termination = MonopolyMonopolies require price regulation Termination rates at cost of efficient operator

Provide incentive to invest in new technologies to reduce costsPromote competition and economic efficiencyPromote universal service through low retail prices

Tuesday, 21 August 12

Dominant operators will argue that if MTRs are lowered

Retail prices will increaseThere will be less subscribersOperators will invest lessHowever, the opposite is the case - Increased competition leads to:

lower retail pricesmore subscribers and operators have to invest more to stay competitive

Tuesday, 21 August 12

Waterbed Effects

Tuesday, 21 August 12

Readers Newspaper Advertisers

Two sided market Interdependent prices No cost causationNewspapers: lower price per newspaper = more readers= higher advertising revenue per page

Tuesday, 21 August 12

Two-sided market would predict

MTR OFF-Net

Fixed

Down

Up

On-net

Up

Up Less Subscribers

Tuesday, 21 August 12

Argument 1Wholesale Price: contractually fixedRetail Prices: Many prices varying product by product and change frequently

MTR On-NetPeak

On-Net Off Peak

On-Net Off Off Peak

OFF-Net

Peak

OFF-Net Off Peak

OFF-Net Off Off Peak

Fixed Peak

Fixed Off Peak

Fixed Off Off PeakOn-Net

SMS

OFF-Net SMS

Product 2

Product 1

Introduction of new cheaper products do not lead to MTR increases

Tuesday, 21 August 12

Argument 2Termination rates are mostly symmetrical ... contradicts the two-sided market argument

If Asymmetry then smaller has higher MTRMTR cannot be increased because of higher market share (newspaper example)

Operator 1

Operator 2

Tuesday, 21 August 12

p=x+a Off-Net Price

Operator 1Revenue=p*qMTR x

q=f(p) subject to price elasticity of

subscribers of operator 2Quantity of call

terminated

Argument 3Operators can only set their own retail prices but not those of other operators...Cannot control q and p

Operator 2

Tuesday, 21 August 12

High MTR = subsidisation within the sector

No funds from outside the sectorWhy should subscribers of one network subsidise subscribers from other networks?Why should one operator be given a subsidy to role out network infrastructure at the expense of another operators?

Tuesday, 21 August 12

Two-sided market & Waterbed Effect

Fail to predict market outcomes correctly Cannot be empirically observed following termination rate cutsRetail and wholesale prices are not interdependent

Tuesday, 21 August 12

0

1000

2000

3000

4000

0 5 10 15 20 25Cost

of O

ECD

bas

ket i

n US

cen

ts

Mobile Termination Rates 2009 in US cents

OECD countries (TMG2010)

Tuesday, 21 August 12

0

125

250

375

500

0 5 10 15 20 25

Min

utes

of u

se

Mobile Termination Rates 2009 in US cents

OECD countries (TMG2010)

Tuesday, 21 August 12

Pro Waterbed EffectsWaterbed effect is masked by other developments such as increased competition and decreasing unit costs Questionable evidence from panel data studies:

1) Constructing data sets with enough data points is impossible2) Omitted variables may render models invalid3) Retail prices used for modelling only prices of dominant operators

Tuesday, 21 August 12

No of operators

sequence of market entry

market shares

user profiles

lock-ins and club effects

technologies

price elasticity

income elasticity

business models used by

operatorsBrand loyalty

past regulatory

interventions

substitute technologies

regulatory strategies

communication laws and policies and many other social and economic factors

Mobile penetration rates and mobile retail prices in a country depend on many factors

Tuesday, 21 August 12

GhanaTanzania

KenyaNigeria

Ethiopia*Rwanda

BeninBotswana

TunisiaNamibiaSenegalUgandaZambia

Côte d’IvoireMozambiqueSouth Africa

CameroonBurkina Faso 11.04

8.59

7.64

7.45

7

6.57

6.33

6.12

5.06

5.06

5.04

4.92

3.74

3.74

3.63

3.35

2.93

2.29 GhanaTanzania

KenyaNigeria

Ethiopia*Rwanda

BeninBotswana

TunisiaNamibiaSenegalUgandaZambia

Côte d’IvoireMozambiqueSouth Africa

CameroonBurkina Faso 12.54

9.3

7.64

7.45

8.15

6.6

6.95

6.12

8.96

5.06

5.04

7.5

6.87

3.74

7.76

5.93

7.26

3.04

Cheapest operator Dominant operatorGhana

TanzaniaKenya

NigeriaEthiopia*

RwandaBenin

BotswanaTunisia

NamibiaSenegalUgandaZambia

Côte d’IvoireMozambiqueSouth Africa

CameroonBurkina Faso 12.54

9.3

10.36

8.32

9.54

8.18

7.04

7.52

8.96

5.36

6.66

8.81

6.87

3.74

7.76

5.93

7.26

3.15

Most expensive operator

Cheapest Prepaid product in country in US$Feb 2010

Tuesday, 21 August 12

Alternative 1: Panel data model based on operators not countries

Incorporate all operators of a countryIncrease the data available by a factor of 3 or 4allows to include significant explanatory variables such as market share and year of market entry The waterbed effect is a hypothesis about the pricing strategies of operators and as such need to be tested at the operator level

Tuesday, 21 August 12

Alternative 2: Case StudiesA less econometrically sophisticated but more plausible: Did Vodafone UK increase its retail prices after any MTR reduction in the UK? And how did the smaller operators or the net-interconnect-payers react?

Tuesday, 21 August 12

Case Study Kenya

Tuesday, 21 August 12

MTR US cents

Mar 2007 Mar 2009 July 2011 July 2013

1.201.401.752.70

5.376.40

7.60

Tuesday, 21 August 12

Retail Prices

Jan-10 Sep-10 Jan-11

1.962.24

0

1.901.91

4.12

1.142.09

6.15

2.46

6.70

7.75Safaricom* Airtel Orange Yu

Tuesday, 21 August 12

Safaricom’s key performance indicators for financial years ending in March

2007 2008 2009 2010

Revenue billion KES 47.45 61.37 70.48 83.96

Subscribers in million 6.10 10.23 13.36 15.79

EBITDA Margin 51.7% 45.9% 39.6% 43.6%After-tax profit in billion KES

12 13.85 10.54 15.15Dividend paid in billion KES

3 2 4 8

Tuesday, 21 August 12

Termination rate reduction In Kenya

9.5% more subscribers in last quarter or 2010 quarterRetail prices dropped by 60%Opposite effect to the waterbed effect!

Tuesday, 21 August 12

Case Study Namibia

Tuesday, 21 August 12

In 2009 MTC stated that if termination rates are reduced to cost it’s

EBITDA margin would drop to 36.8%Would investment less and not be able to fund WACSPay less dividends to Government

Tuesday, 21 August 12

Termination Rates US cents

Jan 2009 July 2009 Jan 2010 July 2010 Jan 2011

4.105.50

6.808.20

9.00

4.105.50

6.808.20

14.40

MTRFTR

Tuesday, 21 August 12

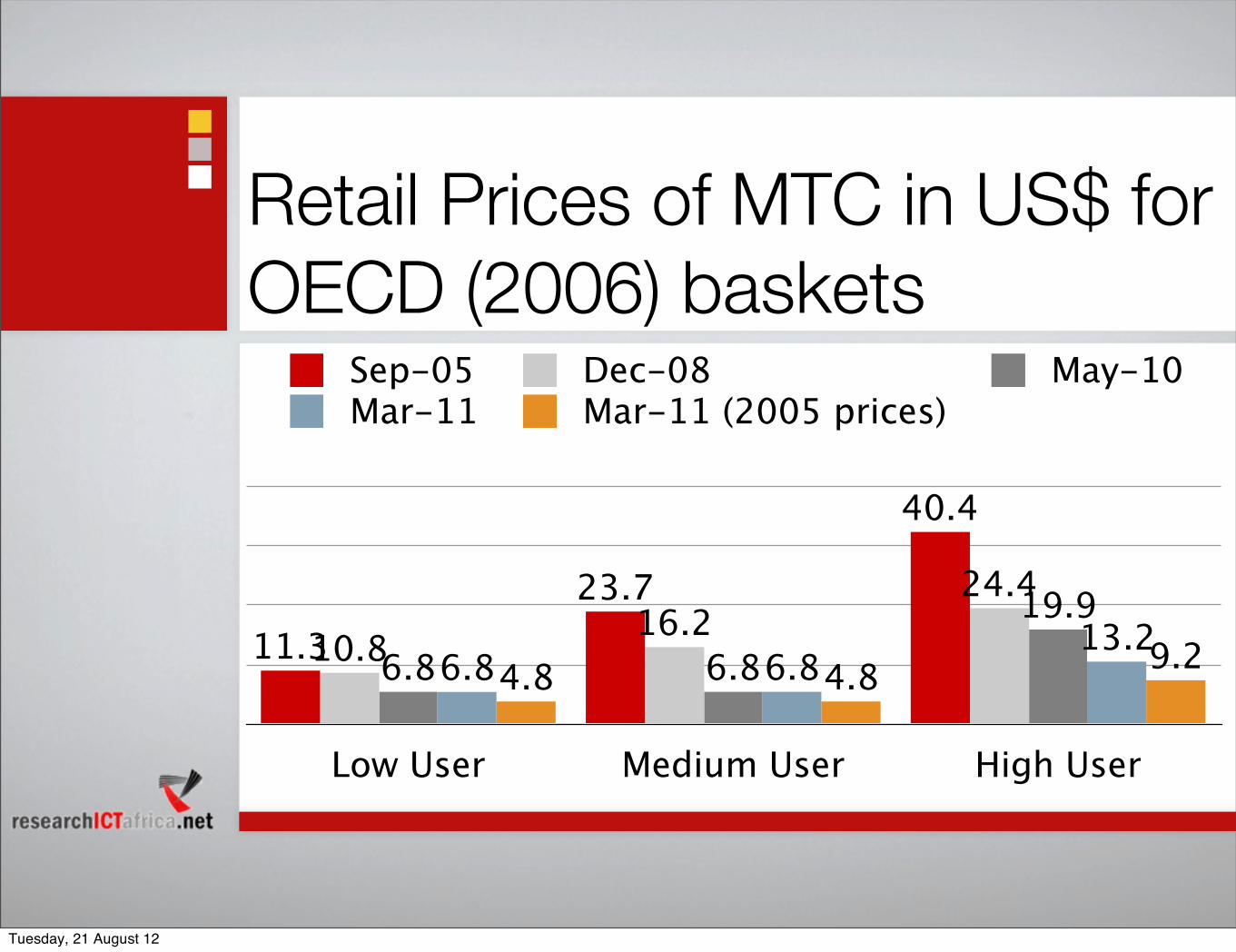

Retail Prices of MTC in US$ for OECD (2006) baskets

Low User Medium User High User

9.24.84.813.2

6.86.819.9

6.86.8

24.416.2

10.8

40.4

23.711.3

Sep-05 Dec-08 May-10Mar-11 Mar-11 (2005 prices)

Tuesday, 21 August 12

MTC key performance indicators

2005 2006 2007 2008 2009 2010

Subscribers in million 0.40 0.56 0.74 1.00 1.28 1.53

EBITDA Margin 61% 60.2% 52.2% 50.9% 53.8% 55.8%After-tax profit millionUS$

39.90 45.94 46.27 48.53 52.79 54.10Dividend paid in million US$

14.99 10.90 33.38 30.11 50.41 52.26Capital Expenditure in million US$ 35.4 55.9

Tax payments in million US$

19.96 23.35 24.11 24.62 27.10 25.5

Tuesday, 21 August 12

Case Study MTN

Nigeria, South Africa, Botswana

Tuesday, 21 August 12

Tuesday, 21 August 12

InterconnectLarge reduction in MTR in Nigeria and RSA

• MTR changes in Nigeria and RSA

• RSA peak rate dropped from ZAR 1.25 to

Large reduction in MTR in Nigeria and RSA

Group interconnect(ZAR bn)

p ppZAR 0.89

• Nigeria peak rate dropped from 11.4 Naira to 8.2 Naira

2009 19.5

Cost Revenue

-14.1• Interconnect revenue decreased 13%

• RSA revenue decreased 10%

• Nigeria revenue decreased 25% in local currency5 4 Margin % currency

• Net interconnect margin increased from 28% to 32%

• Higher on net traffic offset some of the

5.4 Margin %

28%

• Higher on-net traffic offset some of the interconnect rate decline

• RSA prepaid on-net improved 7pts to 61%

• Nigeria total on-net increased by 4pts to 83%

2010 17.0-11.5

• Nigeria total on net increased by 4pts to 83%

5.5 Margin %

32%32%

Tuesday, 21 August 12

High User OECD usage baskets in US$

MTN South Africa Mascom MTN Nigeria

36.544.4

68.4

36.544.4

68.457.9

44.4

68.460.7

46.6

68.4

US c

ents

Feb 2010 Jan 2011 Feb 2011 Mar 2011

Tuesday, 21 August 12

ConclusionNo Waterbed Effect in Namibia, Kenya, Botswana, South Africa or NigeriaTwo-sided market argument can clearly be rejectedRetail prices decrease after termination rate cutsOperators pursue different pricing strategiesCost based termination rates lead to more competition:

more subscribersmore trafficmore investmentbigger pie of revenues to share among operators

Tuesday, 21 August 12

More recent evidence

Tuesday, 21 August 12

Vodacom - Impact of mobile termination rates in South Africa

FY 2011 ending March 2011

FY2012 ending March 2012

Difference

Interconnection Revenue 6,755 6,062 -693

Interconnection Expenditure 5,682 4,923 -759

Net Interconnect Profit 1,073 1,139 66

Tuesday, 21 August 12

Telkom Fixed-line operating revenues and expenses in ZAR million (Telkom 2011, Telkom 2012)

Telkom Fixed-line operating revenues and expenses in ZAR million (Telkom 2011, Telkom 2012)

Telkom Fixed-line operating revenues and expenses in ZAR million (Telkom 2011, Telkom 2012)

Telkom Fixed-line operating revenues and expenses in ZAR million (Telkom 2011, Telkom 2012)

FY 2011 ending March 2011

FY2012 ending March 2012

Interconnection Revenues

Total Revenues 1,679 1,757

Interconnection Revenues

Mobile Domestic 498 375Interconnection Revenues Mobile International 186 630Interconnection Revenues

Fixed 328 262

Interconnection Revenues

International 667 490

Interconnection Expenses

Total Expenditure 5,193 4,839

Interconnection Expenses

Mobile network operators 3,704 3,218Interconnection Expenses Fixed 404 306Interconnection Expenses

International network operators 792 1,029

Interconnection Loss TotalInterconnection Loss Total -3,514 -3,082Interconnection Loss Mobile onlyInterconnection Loss Mobile only -3,206 -2,843Tuesday, 21 August 12

MTNMTN South Africa is a net-receiverNet profit (revenues - expenses) from call termination decreased from ZAR 1,481 million in 2010 to ZAR 1,182 million in 2011 However MTN is still a net-receiverhttp://www.mtn.com/Investors/Financials/Documents/booklet.pdf, accessed 19 June 2012

Tuesday, 21 August 12

Table 6 Mobile Termination glide PathTable 6 Mobile Termination glide PathTable 6 Mobile Termination glide PathProduct Peak Off Peak

March 2011 73c 65cMarch 2012 56c 52cMarch 2013 40c 40cSource: Government Gazette No. 33698, 29 October 2010. Call Termination RegulationsSource: Government Gazette No. 33698, 29 October 2010. Call Termination RegulationsSource: Government Gazette No. 33698, 29 October 2010. Call Termination Regulations

Tuesday, 21 August 12

January 2012 OECD Low User Basket costs in USD (FX= average 2010)January 2012 OECD Low User Basket costs in USD (FX= average 2010)January 2012 OECD Low User Basket costs in USD (FX= average 2010)January 2012 OECD Low User Basket costs in USD (FX= average 2010)January 2012 OECD Low User Basket costs in USD (FX= average 2010)January 2012 OECD Low User Basket costs in USD (FX= average 2010)

Country Name Cheapest product from Dominant OperatorCheapest product from Dominant Operator Cheapest product in countryCheapest product in country % cheaper than dominant Country Name Rank US$ Rank US$ % cheaper than dominant

Mauritius 1 2.39 5 2.39 Dominant is cheapestEthiopia 2 2.61 7 2.61 naNamibia 3 2.74 8 2.74 Dominant is cheapestKenya 4 2.85 1 1.90 33.4%Egypt 5 2.91 9 2.91 Dominant is cheapestSudan 6 3.53 6 2.46 30.5%Ghana 7 3.87 11 3.28 15.1%Libya 8 3.90 14 3.90 Dominant is cheapestRwanda 9 4.28 3 2.16 49.4%Guinea 10 4.62 2 1.93 58.1%Sierra Leone 11 5.04 13 3.88 23.1%Uganda 12 5.51 10 2.94 46.6%Congo Brazaville 13 5.63 17 5.63 Dominant is cheapestTanzania 14 5.82 12 3.75 35.7%Algeria 15 6.21 4 2.28 63.3%Tunisia 16 7.24 18 6.46 10.9%Senegal 17 8.11 24 8.11 Dominant is cheapestBotswana 18 8.16 20 7.66 6.0%Sao Tome &Principe 19 8.21 25 8.21 Dominant is cheapestNigeria 20 8.40 16 5.22 37.8%Madagascar 21 8.45 27 8.45 Dominant is cheapestMali 22 8.78 29 8.78 Dominant is cheapestBurkina Faso 23 8.88 28 8.53 4.0%Benin 24 9.10 22 7.92 13.0%Mozambique 25 10.00 33 10.00 Dominant is cheapestChad 26 10.14 34 10.14 Dominant is cheapestD.R. Congo 27 10.37 19 7.62 26.5%Côte d’Ivoire 28 10.41 36 10.41 Dominant is cheapestCameroon 29 10.44 35 10.28 1.5%South Africa 30 11.07 32 9.83 11.2%Togo 31 11.18 38 11.18 Dominant is cheapestZambia 32 12.05 26 8.22 31.8%Niger 33 12.30 31 9.77 20.6%Central African Republic 34 12.33 39 12.33 Dominant is cheapestAngola 35 12.50 41 12.50 Dominant is cheapestSwaziland 36 12.87 44 12.87 naMalawi 37 13.01 45 13.01 Dominant is cheapestZimbabwe 38 13.48 43 12.67 6.0%Morocco 39 13.56 42 12.53 7.6%Gabon 40 16.11 30 9.09 43.5%Lesotho 41 16.51 40 12.43 24.7%Cape Verde 42 18.15 46 18.15 Dominant is cheapestGambia 43 na 15 4.33 naMauritania 44 na 21 7.77 naLiberia 45 na 23 8.09 naSeychelles 46 na 37 11.04 naSource: Research ICT Africa Mobile Pricing Report 2012Source: Research ICT Africa Mobile Pricing Report 2012Source: Research ICT Africa Mobile Pricing Report 2012Source: Research ICT Africa Mobile Pricing Report 2012Source: Research ICT Africa Mobile Pricing Report 2012Source: Research ICT Africa Mobile Pricing Report 2012

Tuesday, 21 August 12

January 2012 May 2012

27

32

24

30

Cheapest prepaid product from Dominant OperatorCheapest prepaid product in country

Tuesday, 21 August 12

40

55

70

85

100

Jan 11 Mar 11 May 11 Jul 11 Sept 11 Nov 11 Jan 12 Mar 12 May 12

8ta Cell C MTN South AfricaVodacom South Africa Virgin Mobile

Tuesday, 21 August 12

On-net / Off-net differentialOn-net / Off-net differentialOn-net / Off-net differentialOn-net / Off-net differentialOn-net / Off-net differentialOperator Product Jan-12 May 2012 Price Change

8taPrepaid Voice 0 0 0.00

Cell C

99 for real NA 0.00 NA

Cell CEasychat 99c 0.51 0.51 0.00

Cell CEasychat allday 0 0 0.00Cell CEasychat per second 0 0 0.00

Cell C

Easychat standard 0 0 0.00

MTN

Call Per Second 0.17 0.17 0.00

MTNCall Per Second Peak 0.00 0.00 0.00

MTNMuziq 0.50 0.50 0.00MTNOne Rate 0 0 0.00

MTN

Zone 0.35 0.35 0.00Virgin MobilePrepay 0.74 0.74 0.00

Vodacom

Freedom 99 NA 0.00 NA

Vodacom

4U Prepaid 0.18 0.18 0.00

VodacomBig Bonus Voucher 0.26 0.26 0.00

VodacomPrepaid All Day per minute 0 0 0.00VodacomPrepaid All Day per second 0.10 0.10 0.00

Vodacom

Vodacom 4 less 0.29 0.29 0.00

Vodacom

Day saver 0.33 0.33 0.00

Tuesday, 21 August 12