Embed Size (px)

Citation preview

Tax Evasionthrough

Shares

How to catch them !

Prashant Kumar ThakurIncome Tax Officer

Author

Prashant Kumar Thakur

Udita, Flat 50203i, 1050/1 Survey Park

Santoshpur, Kolkata-700075

Email: [email protected]

Mob: 9831096533

Ist Edition, : 2008

2nd Edition : 31/12/2011

Note :

The views expressed in this book are solely of the author .Income Tax Department has

nothing to do with the content of this book.

All rights reserved.

Dedication

One man, other than the author, responsible for this book is Sri R .S. Upadhyay, CIT(Training). A chance meeting with him flared up the desire to pen the book.

One woman behind successful completion of this book-Alka, my better half.

One couple without whom this book was impossible-my parents!

Five officers who played

silent role in my learning and training - Sri Samir Mukhopadhya, CIT –thanks

for his great mentorship, Sri B.B.Mohanty, CIT– learned from him fast deci-

sion and smooth management style, Sri A.K. Bala, CIT- inculcated from him

his simple, open and firm approach, Sri J.R. Singh, CIT-for his friendly and

fatherly teachings and Sri R.N.Bhatacharya-Addl. CIT-(retired)-who taught

me how to be a good boss. Thanks to all of them.

Preface to Second Edition

Overwhelming response from officers and professionals ,spread across the coun-try to the first edition is the reason for this updated second edition .

So what is new in the second edition? Almost entirely the topics are rewritten with fair amount of sprinkling of case laws and circulars issued by authorities. A few topics have been deleted . Newly added topics relate to tax evasion practice through Futures & Option trades” and use of mergers for tax evasion .

Readers should note that case laws referred under various topics are not neces-sarily in favour of income tax department. Many are in favour of tax payers. The purpose to include all relevant case laws, whether favourable to department or not , is to broaden the idea of readers on a provision of law.

I hope the book will serve its purpose .

Suggestion, criticism & comments are welcome at [email protected]

Kolkata-31/12//2011 Prashant Kumar Thakur

Preface to First Edition

Some of the questions bothering me from the time I joined the department

“Why do we refer the books written by “outsiders” only-who have their

own reasons to give a perspective in the larger interest of their readers-the

assessees? Why is there absolute dearth of books written by officers for the

officers of the department ?”.

While the books writen by “outsiders” definitely enhance knowledge on Income

Tax Act, such books can not teach-how to enquire or investigate a case. This

can be taught by an officer only, who has rich experience of investigation,

enquiry and assessments. Not getting in-house experts on income tax is a

big irony because, we are supposed to study the I T Act for more than thirty

years, but still junior officers are compelled to search for guidance on income

tax from books written by “outsiders”. I am quite hopeful that other officers

of the department will also share their expertise like the one great effort

of past- a five volume compilation named “Techniques of Investigation for

Assessment”. That is a superb guide book

For the last fourteen years, I am in search of a guide book on shares’ related

cases. I could not find any. So, I pen this book. Suggestion, criticism, comments

& case studies which will be incorporated in future editions are welcome at

Kolkata-11/3/2008 Prashant Kumar Thakur

Part-I

Evasion Practices 1. Bogus Purchase Of Shares to Reduce Business Profit. 2

2. Unquoted Shares & Tax Evasion 14

3. Evasion Through Reverse Conversion Of Shares? 27

4. Speculation Loss And Tax Evasion? 37

1. Mix Speculation Loss With Trading Income.

2. Claiming Speculation Loss As Hedge Loss

5. How To Detect Closing Stock Undervaluation? 47

6. How To Detect If Short Term Is Claimed

As Long Term Gain? 50

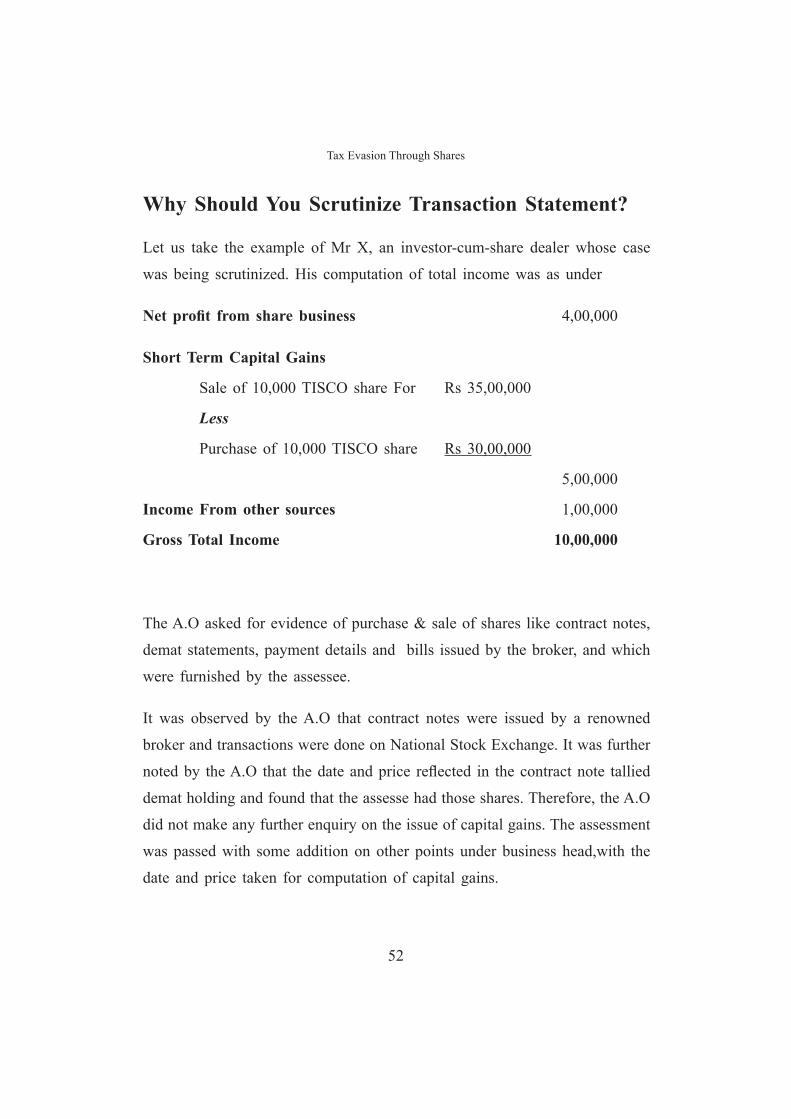

7. Why Should You Scrutinize Transactions Statement? 52

8. How Family and Private Companies Are

Used For Evasion? 55

9. Use of Mergers for Tax Evasion 61

10. How To Decide If Share Transaction Is Business Or

Investment Activity? 70

11. Why Should You Scrutinize Transactions

Of Last Seven Days ? 84

12. How To Handle Cases Of Evasion Through Penny Stocks? 86

1. When Bogus LTCG On Penny Stock Created Legally.

2. When Bogus LTCG On Penny Stock Created By

Using False Documents.

12. Tax Evasion through Futures & Option Trades 102

13. Tax Evasion by Changing Client Codes 107

Part II

Don’t Forget These Points

1. Why Should You Keep An Eye On Warrant? 113

2. How Preference Share Creates Capital Gains? 118

3. Can Scrutiny Of Security Deposit Bring Tax? 123

4. Why Knowledge Of SCRA Is Important For Share Cases? 125

5. How To Easily Apply Explanation To Section 73? 134

6. ESOP, Phantom Stock Option & A flash back on FBT ! 142

Part IIIBack To Basics

1. What Are The Procedure For Share Transactions In Dematerialized Form? 153 2. How Internet Can Bring You Information You Always Wanted For ? 155 3. Important Circulars/Instructions Issued By CBDT 156 1. Period of holding in case of dematerialized shares. 2. Determination of the ‘date of transfer’ and holding period for the purpose of capital gains. 3. Distinction between shares held as stock-in-trade and shares held as investment 4. What is the meaning of ‘hedging’ with respect to

Explanation to section 73 ? 4. Important Circulars Issued By SEBI. 169 1. Transfer of shares from pool account to clients account. 2. Time duration for transfer of funds and securities from member to client. 3. What is the definition of ‘negotiated deal’ ? 4. Circular regulating negotiated deal. 5. Circular regulating broker-client relationship. 6. MAPIN abolished 7. NSE Circular on Penalty for Client Code Modification 5. Certain Important Judgments You Must Refer To 183 1. What are the views of different courts on the issue “business or investment income” 2. Are illegal expense or losses allowable? 3. Is surplus on “sale as going concern” taxable as capital gains? 4. Are bonus shares or rights to shares capital asset? 5. Does exchange of shares fall within the meaning of transfer? 6. Does reduction of share capital give rise to capital gains? 8. Whether trading in units and govt. securities fall within the ambit

of the word “commodity” as given in section 43(5) of the IT Act? 9. Whether the sale of warrants received against debentures held as

stock-in-trade give rise to taxable revenue receipt? 6. What Is A Contract Note? 187 7. Why Is Demat Transaction Statement Important For Share Investigation? 189 9. What Is A Private Limited Company And What Are Its Privileges? 19110. What does “Beneficial Owner” mean in context of share ownership ? 192 11. What Are Derivatives? 19312. Books Maintained By The Broker & Stock Exchanges? 196 13. The Addresses of Different Stock Exchanges? 197 14. Address of Six Regional Directors (RD) under Ministry Of Corporate Affairs 202 15. Terms Every Assessing Officer Must Know 203

1

Evasive Practices

Part 1 of the book is devoted to evasive techniques of tax avoidance

used by some unscrupulous share dealers. This part of the book

consists of 11 topics. Each topic has been discussed at length

and an endeavour to give step wise guidance has been made. The

views of higher judicial fora as well as circulars of CBDT & SEBI,

wherever needed, have been incorporated.

Bogus Purchase Of Shares to Reduce Business ProfitBogus purchase of shares means showing share purchase without actually

purchasing shares. Since the actual purchase is not made, there can be no

question of sale of such shares. Therefore, those shares are carried to closing

stocks. One of the most popular methods of valuation of closing stock-cost

or market price, whichever is lower1, is then followed by the assessee. The

devaluation in share price i.e difference between purchase price of shares

and the closing price of same shares , is used to adjust the profit of other

business carried by the assessee.

Let us take an example to understand this technique. Mr X is a share dealer

and during FY 2009-10, he found that he had earned profit of Rs 60 lakhs.

However, he wanted to file return for Rs 5 lakhs. Therefore, his problem was

to reduce 55 lakhs of income. Finally when his profit and loss account was

prepared, it showed profit of Rs 5 lakhs only. He prepared profit and loss

account as under :

Profit & Loss Account Of Mr X

Opening Stock Rs. 22,00,000 Sale Rs.2,47,10,000

Purchase Rs. 2,60,00,000 Closing stock Rs.60,00,000

Interest Rs. 12,00,000

Other expense 8,00,000

Net Profit 5,10,000

3,07,10,000 3,07,10,0001 Chainrup Sampatram v. CIT [1953] 24 ITR 481 (SC), A.L.A. Firm v. CIT [1991] 189 ITR 285 (SC

2

The problem of Mr X–the tax evader was solved without giving even a small

hint as far as his P & L account was concerned.

Can you detect such cases?

Two reasons why such cases can be detected with a little work are :

First is that he woke up very late to evade tax. This casual approach brings

him face to face with two genuine problems. After 31st March, he can neither

show any acceptance of delivery of shares nor can he make any payments by

cheques. Therefore, purchase is shown on credit side and he is also without

any evidence of delivery.

Second reason is that share trade in India is fully computerized and requires

involvement of third parties like stock exchange or depository participants or

banks. These third parties can be helpful in gathering evidences to prove the

wrongs perpetrated by the tax evaders.

Steps to Catch Them !

Therefore, one can detect such tax evasion cases by following steps :

1. Ask for certain details in a particular format.2. Analyse the details.3. Enquire & collect evidences.4. Dealing with different scenarios.

5. Summing up & assessments

First two steps are required to identify such cases, third step is necessary for

collecting evidence and the last two to counter alibis of assessee and finalise

the findings.

3

4

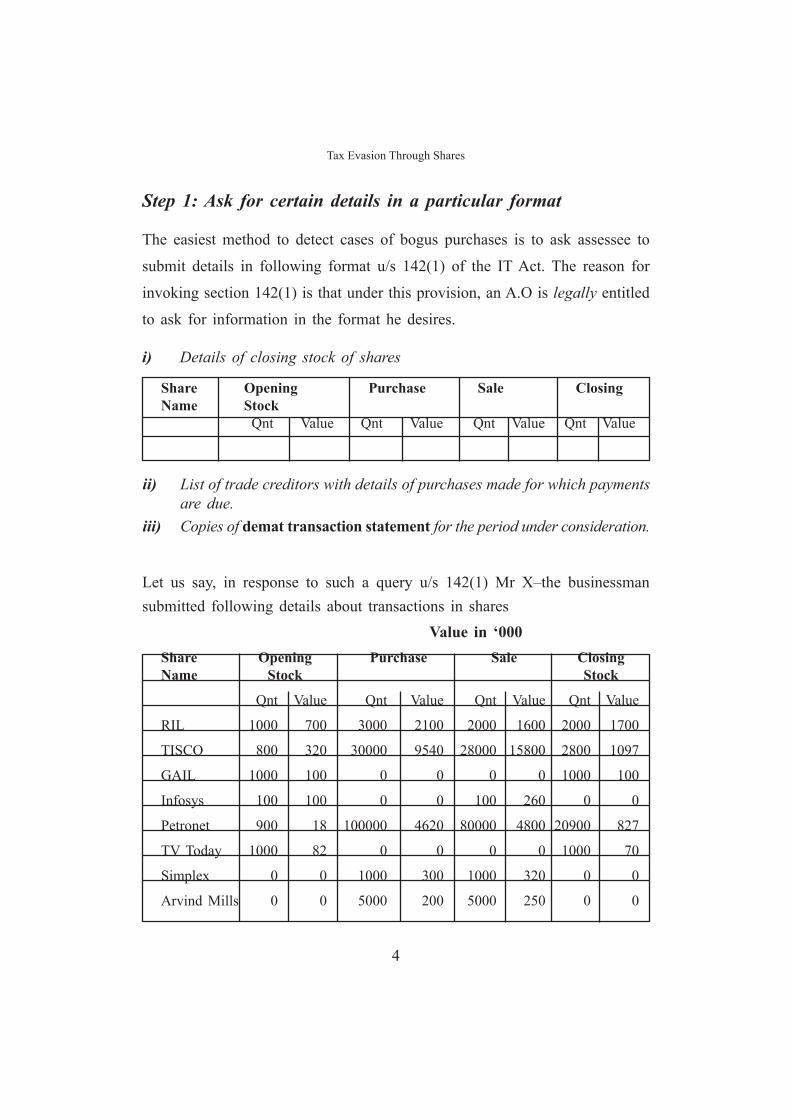

Tax Evasion Through Shares

Let us say, in response to such a query u/s 142(1) Mr X–the businessman submitted following details about transactions in shares Value in ‘000

Share Opening Purchase Sale Closing Name Stock Stock

Qnt Value Qnt Value Qnt Value Qnt Value

RIL 1000 700 3000 2100 2000 1600 2000 1700

TISCO 800 320 30000 9540 28000 15800 2800 1097

GAIL 1000 100 0 0 0 0 1000 100

Infosys 100 100 0 0 100 260 0 0

Petronet 900 18 100000 4620 80000 4800 20900 827

TV Today 1000 82 0 0 0 0 1000 70

Simplex 0 0 1000 300 1000 320 0 0

Arvind Mills 0 0 5000 200 5000 250 0 0

Step 1: Ask for certain details in a particular format

The easiest method to detect cases of bogus purchases is to ask assessee to

submit details in following format u/s 142(1) of the IT Act. The reason for

invoking section 142(1) is that under this provision, an A.O is legally entitled

to ask for information in the format he desires.

i) Details of closing stock of shares

Share Opening Purchase Sale Closing Name Stock Qnt Value Qnt Value Qnt Value Qnt Value

ii) List of trade creditors with details of purchases made for which payments are due.

iii) Copies of demat transaction statement for the period under consideration.

5

Bogus Purchase Of Shares to Reduce Business Profit

Ballarpur 10000 380 0 0 10000 480 0 0

Mukta Arts 5000 500 0 0 5000 300

SmkayConsultant 0 0 10000 1200 0 0 10000 110

Zircon 0 0 12000 1840 0 0 12000 103

Shyam Tele 1000 100 2000 110 0 0 3000 300

Biocon 5 350 1000 500 1005 1200 0 0

Guest Financial 0 0 20000 2000 0 0 20000 240

Rel Petro 1000 50 20000 1250 0 0 21000 1050

Step 2 : Analyse the details

(i). Concentrate on big purchases

Segregate data related to all big purchases of shares which have not

been sold or only a very small percentage of total purchase is sold.

For example, in the aforesaid chart, shares which have been purchased

during the year and not sold are :

Values in Thousands(‘000)

Share Opening Stock Purchase Sale Closing Name Stock

Qnt Value Qnt Value Qnt Val Qnt Value

Mukta Arts 5000 500 0 0 5000 300

Smkay Consultant 0 0 10000 1200 0 0 10000 110

Zircon 0 0 12000 1840 0 0 12000 103

Guest Financial 0 0 20000 2000 0 0 20000 240

Rel Petro 1000 50 20000 1250 0 0 210000 1050

6

Tax Evasion Through Shares

(ii) : Try to find out answers of following questions

1. Are these shares listed on NSE, BSE or regional stock exchanges? [Refer to Part III for more on listing of shares]

2. Are these shares well known?

3. Whether diminutions in the value of these shares as on the last day of the year are very high?

4. Are these shares purchased on credit?

A share listed on regional stock exchange on which there is very high diminution in value and if such share is purchased on credit, it is most likely to be a bogus share purchase.

The aforesaid chart shows that out of five shares, two of them are well known, i.e., Mukta Arts and Reliance Petro and both are listed companies. Even the closing stocks value of those two shares have reduced only marginally. Therefore, both these shares have to be left out of scrutiny angle. Rest of the three shares have to be taken up for further enquiry & investigation because it is apparent that total devaluation on account of these three shares totals to Rs 45,87,000.

Value in Thousands (‘000)Share Opening Purchase Sale Closing Deva- Stock Stock lua- tion

Qnt Val Qnt Val Qnt Val Qnt Val

Smkay Consultant 0 0 10000 1200 0 0 10000 110 1090

Zircon 0 0 12000 1840 0 0 12000 103 1737

Guest Financial 0 0 20000 2000 0 0 20000 240 1760

5040 453 4587

7

Once you filter out the shares fit enough for deep investigation, concentrate all

your efforts to find out answers to the genuineness of purchase of those shares

Step 3: Steps to enquire into & collect evidences

Enquiry and collection of evidences involve following steps

i. Analyse demat transaction statement.

ii. Write a letter to the stock exchange

iii. Send a letter to the broker

iv. Have peep into broker’s demat account

v. Examine books of account of the Broker.

i. Analyse demat transaction statement.

Demat transaction statement is like a passbook of shares. (Read more about

demat transaction statement in Part III of the book). If the assessee has done

any mischief, he will not submit the transaction statement and will always pray

for more time. Therefore , in the very first notice u/s 142(1), you must ask for

demat account number and name with address of the depository participant

(DP) with whom he maintains demat account. The details furnished can be

utilised at this stage. If you know the DP address, send a letter u/s 133(6)

and ask for transaction statement related to the assessee for financial year.

Peruse the transaction statement of the assessee to find if the shares were credited

in his account, three or four days after the date of purchase (i.e ,transaction

date) shown in the contract note. If you do not find entry of shares on the

date or even in any month of the relevant financial year, then this is the 1st

evidence on record that no transaction in those shares had taken place. Now,

your work has increased manifold

Bogus Purchase Of Shares to Reduce Business Profit

8

Tax Evasion Through Shares

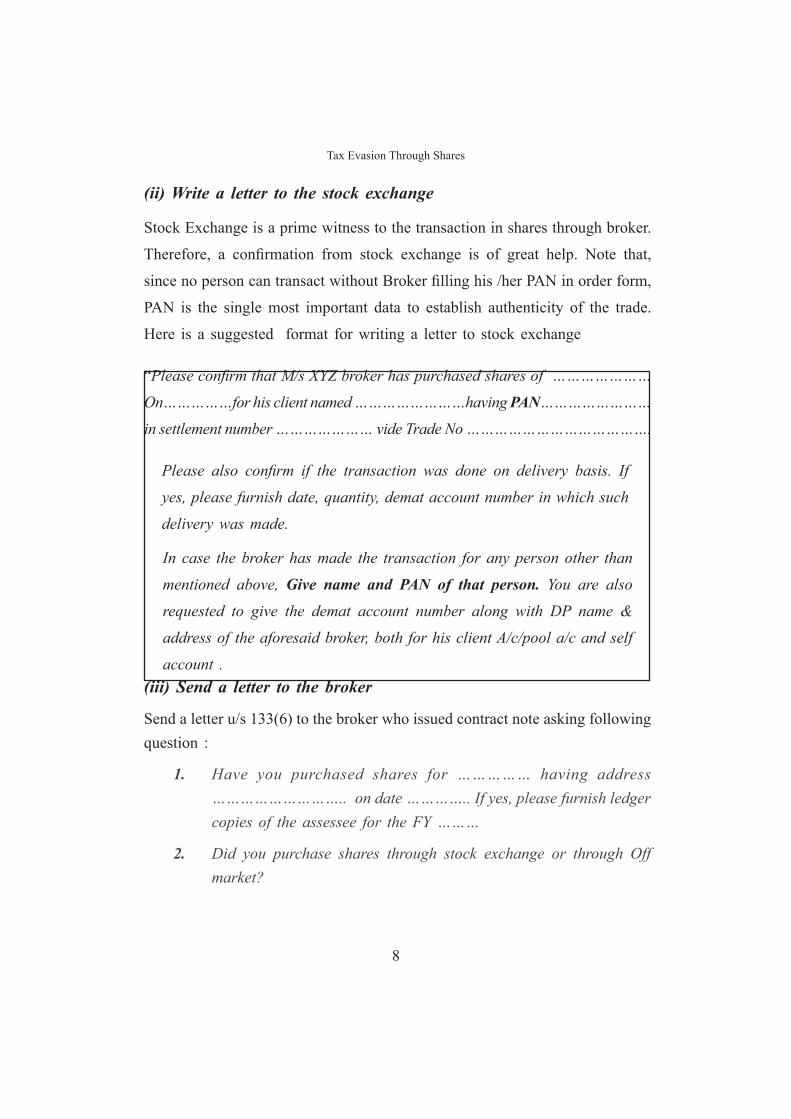

(ii) Write a letter to the stock exchange

Stock Exchange is a prime witness to the transaction in shares through broker.

Therefore, a confirmation from stock exchange is of great help. Note that,

since no person can transact without Broker filling his /her PAN in order form,

PAN is the single most important data to establish authenticity of the trade.

Here is a suggested format for writing a letter to stock exchange

“Please confirm that M/s XYZ broker has purchased shares of …………………

On……………for his client named ……………………having PAN……………………

in settlement number ………………… vide Trade No ………………………………….

Please also confirm if the transaction was done on delivery basis. If

yes, please furnish date, quantity, demat account number in which such

delivery was made.

In case the broker has made the transaction for any person other than

mentioned above, Give name and PAN of that person. You are also

requested to give the demat account number along with DP name &

address of the aforesaid broker, both for his client A/c/pool a/c and self

account .(iii) Send a letter to the broker

Send a letter u/s 133(6) to the broker who issued contract note asking following question :

1. Have you purchased shares for …………… having address ……………………….. on date ………….. If yes, please furnish ledger copies of the assessee for the FY ………

2. Did you purchase shares through stock exchange or through Off market?

9

3. If shares have been purchased from any person other than stock exchange, give name, address, details of payment, the date of delivery taken in your accounts.

4. When did deliver of shares to assessee and in which demat account?

5. Enclose your Demat Transaction Statement for period under consideration.

In all probabilities, if the broker has done some mischief, he will not answer the notice u/s 133(6) or he may shirk from answering In that case, issue him notice u/s 131 of the I T Act and ask questions given above including documents required for investigation.

(iv) Have peep into broker’s demat account

1. Write a letter u/s 133(6) to the depository of the broker for the demat transaction statements of the broker-personal as well as pool account,related to the impugned shares for the relevant financial year.

2. Peruse the demat transaction statement of the broker.If you do not find any incoming shares or any credit in brokers account on that day or even within few days after the date, an additional evidence will be on record that no purchase was made by the broker even off-market.1

3. Also note the balance of shares being shown in broker’s demat accounts in impugned share. If you do not find any balance before the date on which the assessee claimed to have transaction, this finding would be very useful against the broker’s alibi that the transaction was executed off-market.

1 Read SEBI Circular MRD/DoP/SE/DEP/Cir-3/2004 dt 24.08.2004

Bogus Purchase Of Shares to Reduce Business Profit

10

Tax Evasion Through Shares

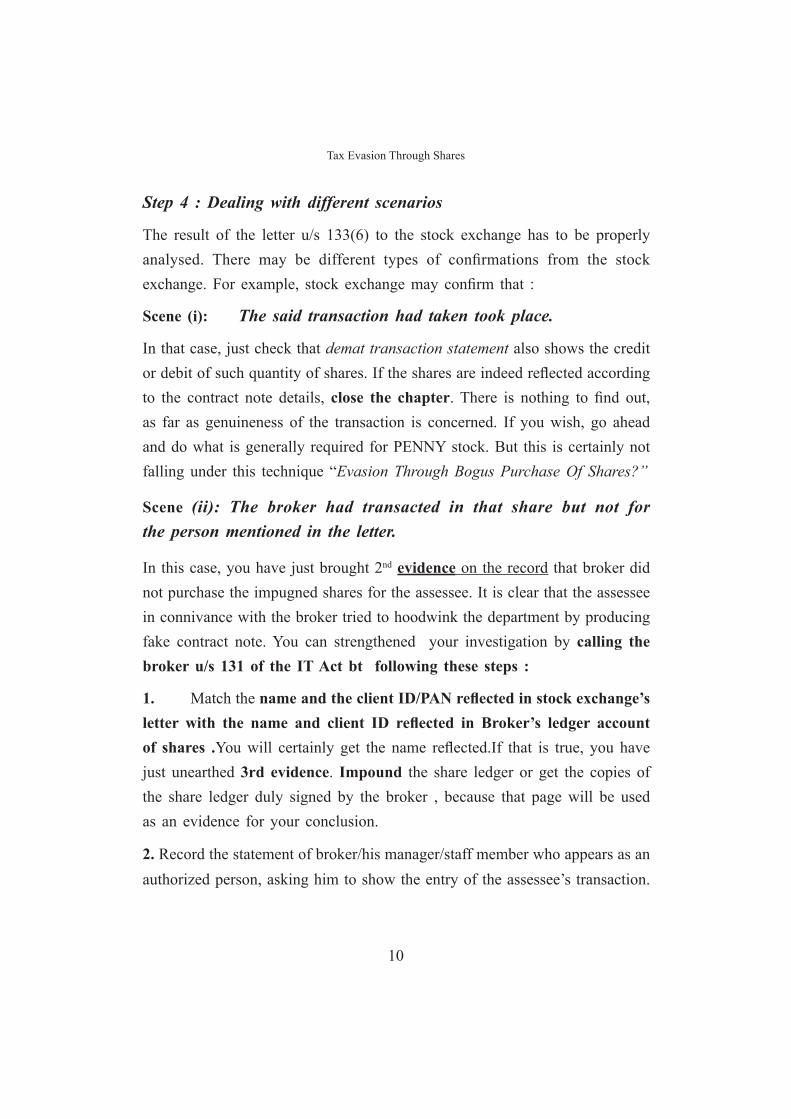

Step 4 : Dealing with different scenarios

The result of the letter u/s 133(6) to the stock exchange has to be properly analysed. There may be different types of confirmations from the stock exchange. For example, stock exchange may confirm that :

Scene (i): The said transaction had taken took place.

In that case, just check that demat transaction statement also shows the credit or debit of such quantity of shares. If the shares are indeed reflected according to the contract note details, close the chapter. There is nothing to find out, as far as genuineness of the transaction is concerned. If you wish, go ahead and do what is generally required for PENNY stock. But this is certainly not falling under this technique “Evasion Through Bogus Purchase Of Shares?”

Scene (ii): The broker had transacted in that share but not for the person mentioned in the letter.

In this case, you have just brought 2nd evidence on the record that broker did not purchase the impugned shares for the assessee. It is clear that the assessee in connivance with the broker tried to hoodwink the department by producing fake contract note. You can strengthened your investigation by calling the broker u/s 131 of the IT Act bt following these steps :

1. Match the name and the client ID/PAN reflected in stock exchange’s letter with the name and client ID reflected in Broker’s ledger account of shares .You will certainly get the name reflected.If that is true, you have just unearthed 3rd evidence. Impound the share ledger or get the copies of the share ledger duly signed by the broker , because that page will be used as an evidence for your conclusion.

2. Record the statement of broker/his manager/staff member who appears as an authorized person, asking him to show the entry of the assessee’s transaction.

11

Evasion Through Bogus Purchase Of Shares.

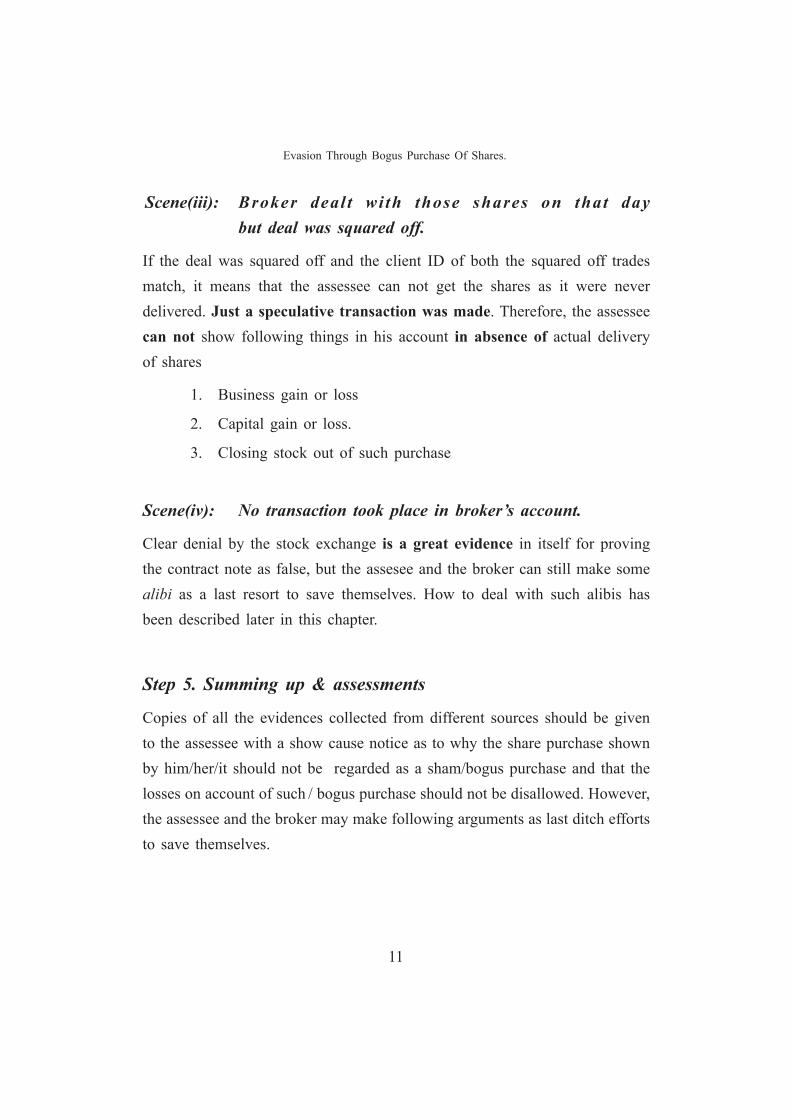

Scene(iii): Broker deal t wi th those shares on that day but deal was squared off.

If the deal was squared off and the client ID of both the squared off trades match, it means that the assessee can not get the shares as it were never delivered. Just a speculative transaction was made. Therefore, the assessee can not show following things in his account in absence of actual delivery of shares

1. Business gain or loss

2. Capital gain or loss.

3. Closing stock out of such purchase

Scene(iv): No transaction took place in broker’s account.

Clear denial by the stock exchange is a great evidence in itself for proving the contract note as false, but the assesee and the broker can still make some alibi as a last resort to save themselves. How to deal with such alibis has been described later in this chapter.

Step 5. Summing up & assessments

Copies of all the evidences collected from different sources should be given to the assessee with a show cause notice as to why the share purchase shown by him/her/it should not be regarded as a sham/bogus purchase and that the losses on account of such / bogus purchase should not be disallowed. However, the assessee and the broker may make following arguments as last ditch efforts to save themselves.

12

Tax Evasion Through Shares

How to counter last ditch efforts of evaders who may argue as follows:

The shares are not reflected in his demat transaction statement because he(the assessee) did not take the delivery from the broker and kept the shares with the broker only, so that whenever he wanted to sell, he would just tell his broker to sell and order will be executed.

He does not know what broker has done. He purchased shares from the broker and he is not responsible for any misdeed of broker.

Similarly, broker may say “the stock exchange has not confirmed the transaction because he had made “off market” deal which was not routed through stock exchange.”

There is no reason for accepting the arguments of the assessee or the broker on following grounds :

1. There are clear evidences on record that authenticity of the contract note is not proved.

2. Burden of proof1 of purchase is on the assessee. No proof was produced by the assessee or the broker to show that there was actual purchase.

3. Even broker’s demat account on examination does not show that he had purchased the impugned shares. It is also to be noted that there was no balance of shares in his pool account before transaction dates.

4. The broker could not show from which party he made the off market purchase and when those shares were delivered to him.

5. The broker is supposed to transfer the shares from pool account to his client within two days under SEBI’s rule. Why did he not do so? 2

1 CIT v. Calcutta Agency Ltd. [1951] 19 ITR 191 (SC)/2 SEBI circular on transfer of share by broker to its client MRD/DoP/SE/Dep/Cir-30/2004 (go to Back to Basics)

13

6. The assessee could not convince the extraordinary need for authorization

to the broker to keep the shares on behalf of him.

7. The broker could not say under what law he acted as “caretaker of the

share” ,if any.

8. Even the payment was not made by the assessee for the purchase and the

delivery was also not made. Therefore, there was no purchase and sale at

all.

Case Laws Reference

Bogus Capital gains : Assistant Commissioner Of Income ... vs Smt. Ranjit Kaur

on 11 August, 2005. 99 TTJ 568

Burden of proof : Lakshimaratan Cotton Mills Co. Ltd. v. CIT [1969] 73 ITR 634 (SC)/ , Dalmia Jain & Co. Ltd. v. CIT [1958] 33 ITR 294 (Pat.)/Dey’s Medical

Stores Mfg. (P.) Ltd. v. CIT [1986]

–End–

Bogus Purchase Of Shares to Reduce Business Profit

14

Tax Evasion Through Shares

Unquoted Shares & Tax Evasion Common ways of routing back the black money (earned profits on which no

tax is paid) in business are :

1. Unsecured loan receipt

2. Using the concealed income for purchase and showing purchase on

credits, i.e ,creating fictitious creditors,

3. Gifts from someone

4. Investment in immovable properties and undervaluing it.

5. Earning tax exempt income like agricultural income, etc

However, this chapter deals with two methods ,both involve shares of private

limited companies for converting black money into white

Readers may note that after amendment in section 56(2) of the I T Act

effective from 1st October 2009 , practice of conversion of black money into

white by using the two methods described below has almost died down .

Method 1: Create your own private limited company

Say, a contractor Mr X has two crores of unaccounted money which he wants

to convert in white without giving a single penny as tax. He converts these

two crores of black money easily into tax exempt money in the following

five steps:

1. He creates a private limited company ABC P Ltd having authorsied

capital of Rs 20 lakhs. He along with his wife invests Rs 10 lakhs

as capital required to set up a company.

2. Let us say the authorsied and issued share capitals are as follows

Authorised 2,00,000 shares of Rs 10

15

Issued 1,00,000 shares of Rs 10 face value

Initial subscriber: Mr X 50000 shares

Mrs X 50000 shares

3. The assessee, Mr X wants to convert Rs 2 Crore in FY 2008-09. Therefore, he will issue 1,00,000 shares of the company ABC Pvt Ltd , to others for Rs 200 at a premium of Rs 190 per shares.

4. Nobody will subscribe to the shares of ABC P Ltd at such high premium in the absence of any substantial business or future prospect. Mr X contacts a broker specialized in arranging fake subscribers to such premium issues. The broker manages many investment companies. He gets the cheque for Rs 2 Crore issued from five or six of these investment companies. The broker gets cash equivalent of cheques and the commission from Mr X.

5. When the money arrives in ABC Ltd’s bank account, Mr X immediately transfers the application money to his other companies or concerns. The balance sheet of the company ,after the shares are issued and subscribed by those companies may be as under:

Capital 20, 00,000 Investments 40, 00,000

Reserve 1,90,00,000 Loans &Advances 1,70,00,000

2, 10,00,000 2,10,00,000

[the aforesaid balance sheet is simplified for clarity purpose]

6. The return for the Asst Yr 2009-10 is filed and there is chance that this return may not be scrutinized. Even if it is scrutinized, if the A.O is not alert, he may not investigate the origin of capital .

Unquoted Shares & tax Evasion

16

Tax Evasion Through Shares

company. The merged subscribed capital actually helps in masking the money which has been routed through different companies.

7. In FY 2008-09 or to be on safer side, in FY 2009-10, Mr X and Mrs Y will purchase back 1,00,000 shares issued at premium of Rs 190 for a mere Rs 15 per share. So, they will issue cheques for Rs 15 lakhs to those share holders and purchase all the shares.

8. The effect would be that investment companies will claim capital loss which may be adjusted with other capital gains. Mr X receives back Rs 1,90,00,000 in form of capital of the company by paying Rs 15 lakhs by cheque. How clever !

9. The company’s balance sheet does not reflect any purchase or sale by individual shareholders ; as such these transactions go unnoticed.

10. An illustration of the method is given below

For this, he uses his company wherein

there are 1,00,000 of shares left

to be issued.

Mr X wantsto convert Rs

2 Crore ofblack money.

This way, Xgets backwhite moneyof Rs 2 Cr ascapital by using cash.

After one ortwo years, X

buys backsame share for

Rs 15

X pays Rs2 crore cash +

fees, Brokerarranges cheques for Rs. 2 Crore issued by 3 or 4

companies.

He issuesshares for Rs200. A brokerarranges share

subscibers

17

Method 2: Buy a private limited company

This method is , in fact , a business proposition for a bunch of people who have specialised in creation of companies and believe in perseverance and luck. Simply put, the process of creating a company is as under:

1. A company is created with a small capital and with very big amount of share premium.

2. All those share application moneys are used to buy investments in private limited companies , which are also created by same person for the same purpose. For example, their balance sheet will show as under

Capital

Shares Issued 20000 Rs 2,00,000

Reserve Premium Rs 2,00,00,000

Assets

Investment in shares Rs 2,00,00,000

(The list of investments may be in 10-20 private limited companies created in the same way

Each company holds investments the other companies )

3. Now , let us say, someone wants to convert black money into white. He will approach the person who is controlling these companies, who will transfer the 20000 shares on very low price. Say Rs 2,00,000 in this case. That person will pay , say Rs 2,00,000 by cheque ,as a price for shares to be transferred and commission /fee for buying such company , say 5 % of total capital ( Rs2.2 Crore) in cash.

Unquoted Shares & tax Evasion

18

Tax Evasion Through Shares

4. After the company is bought, the new controlling person will start selling the shares shown as investment , usually on same price on which it was bought . The purpose is simple. Bring cheque for equivalent cash . The person who created those companies , has the responsibility to buy those shares.

Now the new company is flush with real money which was black money of the unscrupulous person. He uses that money for whatever purpose he wants it to be.

How to catch such an evasion?

The modus operandi of the persons who indulge in creating such companies and selling them to prospective tax evaders is that they disperse all these companies in different wards , so that no one A.O will have grip over them. Their operations are also covered in different years , so linking of each case is also difficult. In author’s opinion ,Investigation wing is more suitable for such enquiry and getting the whole chain of links exposed in this “black to white operation” on the ground of better resources of intelligence, lack of burden of time limited work ,wide area of operation and unlimited power into things to enquire into things. All these help in investigation of source of application money, in examining the intention of the parties involved and in piercing the layers of funds movement are required.

Anyway, however hard that task may be, it is not beyond the capabilities and abilities of the A.O. In fact, in many cases, one can catch the culprits at the first stage itself , when money in the form of application amount is received by the tax evader company.

19

Steps involved for achievement of success by the A.O for investigating and assessing such cases are :

1. Identify the cases.

2. Examine application money

3. Go deep into layers of fund movements.

4. Collect evidences.

5. Record statements under oath.

Step1 : Identify the cases :

A company’s annual report contains balance sheet and P & L accounts for two years. Get hold of the earlier two years balance sheets and P & L accounts and compare the share capital of the company with respect to its activities. If you find that :

i) The company is not very profitable

ii) It is not carrying any major business

iii) It is earning some interest and dividend only.

iv) Most of its funds are used for giving loans and advances.

If such a company suddenly issues shares at a very high premium and also

gets subscriptions for such issue, then you have just got the perfect case

for questioning the receipt of the capital.

Let us take an example, a typical case where capital of the company for fours years is compared and can be as under :

Capital 2003-04 2004-05 2005-06 2006-07

Authorsied (Nos) 2,00,000 2,00,000 2,00,000 2,00,000

Authorised capital (Val) (Rs.) 20,00,000 20,00,000 20,00,000 20,00,000

Issued & Subscribed (Nos) (Rs.) 100000 100000 100000 2,00,000

Unquoted Shares & tax Evasion

20

Tax Evasion Through Shares

Issued & Subscribed (Value) (Rs.) 10,00,000 10,00,000 10,00,000 20,00,000

Net Profit (Rs.) (24000) 100000 110000 85000

Reserve(Premium) (Rs.) 0 0 0 1,90,00,000

One can see from the aforesaid chart that the net profit earned by the company is very dismal. Even then such a company is able to get the capital at a very high premium. The natural question would be “Why will anybody be interested in such a company?”

Step 2: Examine application money. Call for details of all the shareholders who subscribed to the “premium

issue” and work on each subscriber as if you have got a case to verify the unsecured loan from such shareholdes. The analogy between an unexplained loan and unexplained application money for subscribing to shares is perfect, because in both cases money is first credited to the books of the receiver ,i.e , the assessee. Therefore, try to find out the truth about application money on three legally settled parameters :

1. Identity of the person subscribing to the shares

2. Creditworthiness of the subscribers

3. Genuineness of the transaction

Step 3: Go deep into the layers

Generally most of share applicants in such cases will be companies. Their

identity may not be suspect as it is easily verifiable these days. The modus

operandi of the Operators (the person who are in business of creating capital

companies ) is to bring subscription by depositing cash and issuing cheques. But

21

the cash is not deposited in the bank account of the subscribing company. The

deposit of cash is generally made in different companies’ or persons’ accounts

and from those accounts, cheques are issued to the subscribing companies. The

subscribing company, once money reaches to its account, issues cheques to

the share issuing company. The operator of such schemes makes it sure that

the money passes through more than one layer. That is why, when you check

the bank account of subscribing company, you will invariably find that the

company has also received the money from somebody else and issued cheque

either on the same day or after a few days to the share issuing company.

Let us take an example. Say, we are investigating into subscription of shares

worth Rs 25 lakhs issued by a company, named ABC P Ltd . Let us say

LMN P Ltd has subscribed to the shares by paying a cheque for Rs 25 lakh.

In that case, you may find fund movements as given below :

ABC P Ltd received Rs 25 Lakhs of share application money from LMN P Ltd.

LMN P Ltd says that it received Rs 25 Lakhs from XYZ P Ltd as advance.

Bank account of XYZ P Ltd. shows deposit of three cheques from three persons/companies totalling to Rs 25 Lakhs just before the date of issuing cheques

Bank account of these three persons shows deposits of cash equivalent to the amounts deposited

1st Layer

2nd Layer

3rd Layer

ÔÔ

Ô

Unquoted Shares & tax Evasion

22

Tax Evasion Through Shares

The A.O will have to go at least up to the 3rd layer, only then the real picture will emerge. This is the reason that I stated in the beginning that to break the chain, investigation wing is most suitable. The A.O has to go deep up to the third layer where one will find that the there is no explanation for such cash deposit. The scrutiny up to such level will certainly be helpful in bringing out the real story.

Step 4: Collecting evidences

While going deep into the layers of fund movements, one should get following data :

1. Shareholders list of those companies ,e.g, LMN P Ltd and XYZ P Ltd.

(You may even find that there are common shareholders)

2. Capital, Loans, and Advances. (You may find that these companies have also issued the shares at

premium and advanced loans or used the money to purchase shares of other private limited companies) 3. Addresses of all those companies.

(You may find that all addresses are same or within same city)

4. Name of auditors of these companies. (It may just happen that auditors are also found to be same)

5. Place where they are being assessed. (It is likely that they are being assessed at the same station)

6. Net profits (All these companies have only income from other sources and

very small profits)

23

7. Business these companies are carrying on. (Generally these are investment companies)

8. Investments in different companies. (The investment by these companies is generally in related companies

which they sell after a year or two.)

Step 5 : Banks are the real places for investigation

The modus operandi of the people is such that the name of the game is getting a cheque for cash. The cash is certainly deposited somewhere down the chain. Therefore, investigation is a matter of time devotion with the bank managers. That is the reason I stated, that compared to an A.O , investigation department which has wide powers of enquiry , is much more suitable for such an enquiry.

In fact , the greatest tool in the hands of the investigation department , now is the information collected by Financial Intelligence Units who monitor funds transfer through banking channel in real time basis.

Step 6 : Recording of statements u/s 131

Deep enquiry will certainly bring out instances of cash deposits at certain layers. In that case it is very important that the person in whose account such cash deposits have been made are examined in details. Apart from the questions based on the facts and circumstances which come on the record at the time of an enquiry, following questions ought to be asked to everybody whose involvement in chain circulation of subscription amount comes on record.

1. What is the source of cash deposit?

2. Why did he pay the cheque to the company immediately after depositing cash?

Unquoted Shares & tax Evasion

24

Tax Evasion Through Shares

3. What is the relationship between company/person in whose account cash has been deposited and the company to which the loan was

issued? 4. Who received the cheque of application money

and how the delivery of that cheque was made?

5. Who are the auditors of the company?

6. If it was loan, how come the company or the person came to know

about the need of the loan by that person?

7. What were the net profits of the company for the last three years?

8. What is the ratio of total loans taken and given by the company?

Most important decision of the Supreme Court on the issue of addition of money shown as share application moneyWhen an A.O is successful in getting to the bottom of the chain and finding

cash deposits somewhere down the chain , should he add the share capital

amount in the hands of the assessee whose case he was scrutinizing or

unexplained amount should be added in the hands of person in whose bank

account cash got deposited.

In other words, let us say the A.O is investigating into the case of ABC P

Ltd in which Rs 2 Crore share application was received from two companies,

FGH Pvt Ltd and TQL P Ltd. On further investigation , he found that cash

was deposited in two individuals accounts - X and Y- who transferred the

amount by cheque to two companies ZYZ and WTU P Ltd , who transferred

the money as share application to FGH & TQL who , in turn , transferred

money as share application to ABC P Ltd , whose case was being investigated .

The question is in whose hand the unexplained cash deposits should be

added . In ABC Pvt ltd or in hands of individual Mr X or Mr Y in whose

25

account cash was deposited or XYZ P ltd or WTU Pvt ltd who were the

first recipients of the unexplained cash deposits in individual account.

Fortunately, the controversy regarding the point of addition of unexplained

cash which travelled to different accounts , has been settled by Hon’ble

Supreme Court while dismissing the Special Leave Petition of the Income Tax

Department. Perhaps , it is one of the tiniest order from the Apex Court which

clearly spells out the point where those unexplained cash deposits should be

added. Since it is very small order , full order is given below

Supreme Court of India

CIT vs Lovely Exports (P) Ltd.

Special Leave to Appeal No. 11993 of 2007

S.H. Kapadia and B. Sudershan Reddy, JJ

11 January 2008

V. Shekhar with Chinmoy Pradip Sharma and B.V. Balaram Das for the Petitioner

ORDER

By The Court :

Delay condoned.

2. Can the amount of share money be regarded as undisclosed income under

s. 68 of IT Act, 1961 ? We find no merit in this Special Leave Petition for

the simple reason that if the share application money is received by the

assessee company from alleged bogus shareholders, whose names are

given to the AO, then the Department is free to proceed to reopen their

individual assessments in accordance with law. Hence, we find no infirmity

with the impugned judgment.

3. Subject to the above, Special Leave Petition is dismissed

Unquoted Shares & tax Evasion

26

Tax Evasion Through Shares

In author’s opinion, the law is now settled that addition u/s 68 of the I T Act can be done in the hands of person in whose account money is deposited provided he files return of income and is very much identifiable ; else addition should be done in hands of the first beneficiary company/person who is identifiable and files return of income with the department.

Therefore, in the aforesaid example ,addition u/s 68 of the I T Act in the hand of ABC Pvt Ltd will not sustain judicial scrutiny when finding is that XYZ or WTU Pvt Ltd were the first beneficiary companies which received money out of cash deposits .

Case law reference

CIT v. Divine Leasing & Finance Ltd. (2008) 216 CTR (SC) 195Bharti Syntex Ltd. vs DCIT 125 TTJ 484Midas Golden Distilleries (P) Ltd. vs CIT 137 TTJ 82CIT vs GP International Ltd ; 229 CTR 86CIT vs Oasis Hospitalities (P) Ltd. 238 CTR 402

–End–

27

Evasion Through Reverse Conversion Of Shares?The reverse conversion means that the stock-in-trade is being converted into investments to claim the benefit of lower or nil tax on capital gains.

Let us start with an example. Mr. X is a share dealer who has prepared his computation of total income, P & L account and balance sheet for FY 2008-09 (Asst Yr 2009-10 ) as under :

Computation of total income

Net Profit As per P & L A/c 1,82,00,000Less Capital gains 1,80,00,000A) Business Income 2,00,000B) Income from Capital GainsSale of BEML on 1/1/2009 2,00,00,000Lesscost of share purchased on 1/9/2005 20,00,000Long term capital gains(exempt) 1,80,00,000C) Income from other sources 1,00,000 Gross Total Income 3,00,000LessFixed deposit for 5 years(u/s 80C) 1,00,000Total Income 2,00,000

The Profit & Loss account of Mr X was as follows Opening stock 75,00,000 Sale 3,15,00,000Purchase 2,87,00,000 Closing Stock 62,00,000Expenses 13,00,000 Capital Gains 1,80,00,000Net Profit 1,82,00,000

28

Tax Evasion Through Shares

Balance Sheet of Mr X was drawn as follows

Capital 45,00,000 Investment 1,20,00,000

Net Profit 1,82,00,000 Stock-in-trade 62,00,000

Sundry Creditors 20,00,000 Bank Balance 56,00,000

Debtors 1,00,000

2,47,00,000 2,48,00,000

When the case was selected for scrutiny, the A.O asked for the evidence of purchase

and sale of shares on which capital gains were claimed. It was found that the shares

were transacted through the National Stock Exchange. The assessee also furnished

payment evidence regarding the sale. The A.O test checked the computation, tallied

purchase and sale quantity, value and date with the contract note submitted by the

assessee and was satisfied with the claim of the assessee. Therefore, the A.O did

not press on the capital gains issue and passed the assessment order without further

scrutinising the case.

Was there something more to be seen?

The case related to FY 2008-09. When his return for FY 2007-08 was perused, the balance sheet enclosed with the return was as follows :

Balance Sheet for FY 2007-08

Capital 42,50,000 Investment 12,00,000

Add Net Profit 2,50,000 Stock-in-trade 95,00,000

Sundry Creditors 70,00,000 Bank Balance 5,00,000

Debtors 3,00,000

1,15,00,000 1,15,00,000

29

A careful scrutiny of the balance sheet for FY 2007-08 shows that closing stock-in-trade was Rs 95,00,000 whereas the opening stock in FY 2008-09 was shown at Rs 75,00,000. This is certainly a discrepancy because closing stock of a year is opening stock of the next year. Enquiry revealed that the decrease in the value of the closing stocks of shares was on account of shifting the shares of BEML from stock-in-trade to investment account. The assessee had done this window dressing of his balance sheet with an ultimate objective that the gain of Rs 1.82 Crore should be shown as long term capital gain to evade tax.

The aforesaid example was a simplistic one regarding the reverse conversion of stock-in-trade. You may come across even more innovative scheme of reverse conversion.

Evasion Through Reverse Conversion Of Shares?

Why such craze for reverse conversion?In the past, businessmen used to convert the investment into stock-in-trade for simple reason that in case of long-term capital gain, the rate of tax was fixed at 20% but there was limitation for charging expense against such capital gains. The I .T. Act allow very specific types of expenses as cost of acquisition of capital asset whereas in case shares are treated as stock-in-trade, one has the infinite possibilities to charge every kind of expense against income from sale of shares. One of the favourite claims of expense is interest on unsecured loan. These unsecured loans in many cases, are unaccounted moneys, routed back to the assessee’s business as unsecured loans. Thus,the double benefit using black money as well as claiming interest on it for reduction of tax liabilities could be availed if the shares were stock-in-trade.

However, the time has changed now. Two major factors which have encouraged unscrupulous persons to adopt reverse conversion of stock tactics for tax evasion are:

1. The phenomenal rise of the stock market.

2. The provision of nil tax on long term gains and 15 % tax on short

30

Tax Evasion Through Shares

term gains.

Let us understand the reason for such reverse conversion with the help of stock price chart of BEML, a public sector company listed on NSE and BSE is given below :

1745.90

1572.55

1399.20

1225.85

1052.50

879.15

705.80

532.45

359.10

185.75

12.40

Price : 1026.55 14.11.2006

BEML

29.03.1995 16.09.1997 10.01.2000 03.05.2002 13.08.204 29.12.2006Left click and drag mouse to select range, release to zoom in. Right click to zoom out.

In 1995, the shares of BEML were quoting at Rs 185 which touched Rs 12.50 during FY 1999-00 and towards the end of FY 2005-06 went up to Rs 1514. So somebody who purchased 1 lakh shares of BEML for Rs 185 as stock-in-trade in 1995 had incurred huge losses in next five years because of the drop in price of shares of BEML. However, the loss in value was utilized to reduce other profits as the stock-in-trade is valued at market or cost whichever is lower.As the scenario completely changed towards the end of FY 2005-06 ,if he sells the shares , let us say, on 28/02/2006 when the price reached Rs 1514, he earns huge profits and also pay staggering amount of tax as computed below :

Sale Value 1514 x 1,00,000 shares = 15,14,00,000Less Cost of the shares Rs 185* x 1, 00,000= 1,85,00,000Gain reflected in P & L account = Rs 13,29,00,000Tax @ 30 % = 3,98,70,000

(* For simplicity, price as on 1.4.05 is taken at Rs 185)

Compare it with the situation that if he would have kept shares as investment,

31

tax would have been nil, as the rate of tax in case of long-term gains on shares is nil. The situation like this has created a desire among the tax evaders to adopt innovative approach to evade tax.

The arguments of assessee & implication.The pet replies of the assessee in cases of reverse conversion of stock-in-trade into investment will be as follows :

1. There is no bar under the I.T.Act for such conversion ;

2. The shares were held for quite some time and

3. He was free to change the nature of holding ,i.e, he was free to treat his holding as an investment with the logic that the shares which had been converted into investment were those which had been held for a longer period.

To understand how to counter the aforesaid arguments, find the facts and then draft the assessment order, we have to understand first of all why the conversion of investment into stock-in-trade was brought within the meaning of transfer in relation to capital asset.

The provision regarding conversion of investment into stock-in-trade was not in existence until 1/4/1985. Sub-section 2 to section 45 was inserted with effect from 1/4/1985 in following words

“(2) Notwithstanding anything contained in sub-section (1), the profits or gains arising from the transfer by way of conversion by the owner of a capital asset into, or its treatment by him as stock-in-trade of a business carried on by him shall be chargeable to income-tax as his income of the previous year in which such stock-in-trade is sold or otherwise transferred by him and, for the purposes of section 48, the fair market value of the asset on the date of such conversion or treatment shall be deemed to be the full value of the consideration received or accruing as a result of the transfer of the capital asset.”

Evasion Through Reverse Conversion Of Shares?

32

Tax Evasion Through Shares

This amendment was brought by Finance Act 1984 to nullify the effect of judgment of Supreme Court in case of CIT vs Shirinbai K Kooka [1962] 46 ITR 86. The brief facts of the case was

:“The assessee is a Parsi lady who held by way of investment a large

number of shares of different companies. These shares were purchased before

the end of and after 1939-40 at a cost price which was much less than

their market value on April 1, 1945. Her dividend income was assessed to

income-tax for several years prior to April 1, 1945 ; but in the assessment

year 1946-47, the relevant accounting year being financial year 1945-46,

the Income-tax Officer found that the assessee had converted her shares

into her stock-in-trade and carried on a trading activity, viz., a business in

shares. Her income for the assessment year 1946-47 was therefore computed

on the basis of the profits which she made by the sale of her shares as

a trading activity, the profits being calculated on the difference between

the ruling market price at the beginning of the account year and the sale

proceeds. For the assessment year 1947-48, the relevant accounting year

being the financial year 1946-47, it was found by the Income-tax Officer

that the sale proceeds of the shares which the assessee had sold amounted

to Rs. 5,49,487.

The assessee then appealed to the Appellate Assistant Commissioner who

enhanced the income of the assessee by a sum of Rs. 2,91,307 including a

capital gain of Rs. 37,590. The Tribunal agreed with the view of the income

tax officer. On being approached by assesse for a reference to High Court,

the Tribunal framed the question of law in the following terms :

“Whether, the assessee’s assessable profit on the sale of shares is

the difference between the sale price and the cost price, or the

difference between the sale price and the market price prevailing

33

on April 1, 1945?” The aforesaid question of law was then referred to the High Court of Bombay under section 66(1) of the Indian Income-tax Act, 1922 (XI of 1922). The High Court answered the question in favour of the assessee and held that the assessee’s assessable profit on the sale of shares was the difference between the sale price and the market price prevailing on April 1, 1945. The Supreme Court upheld decision of High Court and dismissed petition of department.

To overcome effect of such judgment sub-section 2 was inserted in section 45 of the I T Act. Further, section 2(47) which defines ‘transfer’, was also amended to include such conversion. The subsection (iv) of section 2(47) thus states :

2(47) “transfer”, in relation to a capital asset, includes,- (iv) in a case where the asset is converted by the owner thereof into, or is treated by him as, stock-in-trade of a business carried on by him, such conversion or treatment; or

Similar situation has now arrived. The assessee finds fruit in converting the stock-in-trade into investment, because that is more beneficial to him. The department can not allow reverse conversion, if the sole reason for resorting to such conversion by the assessee is to evade tax. So, A.O has to

i. Detect such cases,

ii. Bring out the facts associated with such conversion,and

iii. Then disallow the conversion and assess the gain under “business head”

Evasion Through Reverse Conversion Of Shares?

34

Tax Evasion Through Shares

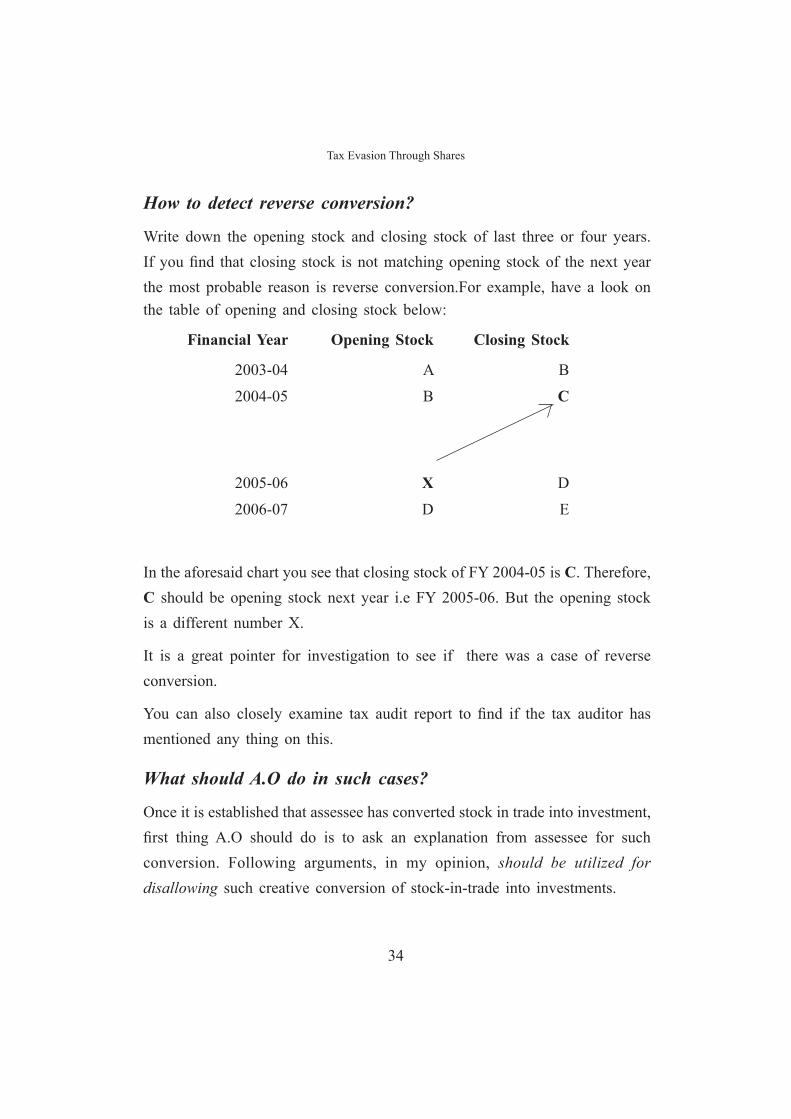

How to detect reverse conversion?

Write down the opening stock and closing stock of last three or four years. If you find that closing stock is not matching opening stock of the next year the most probable reason is reverse conversion.For example, have a look on the table of opening and closing stock below:

Financial Year Opening Stock Closing Stock

2003-04 A B

2004-05 B C

2005-06 X D

2006-07 D E

In the aforesaid chart you see that closing stock of FY 2004-05 is C. Therefore, C should be opening stock next year i.e FY 2005-06. But the opening stock is a different number X.

It is a great pointer for investigation to see if there was a case of reverse conversion.

You can also closely examine tax audit report to find if the tax auditor has mentioned any thing on this.

What should A.O do in such cases?

Once it is established that assessee has converted stock in trade into investment, first thing A.O should do is to ask an explanation from assessee for such conversion. Following arguments, in my opinion, should be utilized for disallowing such creative conversion of stock-in-trade into investments.

35

i) The intention of the assessee is mala fide in the sense that there is no

cogent reason for such conversion other than saving on tax.

ii) In the past, the loss on account of devaluation of closing stock-in-trade was always adjusted with the income as the valuation is done as per market value or cost whichever is lower. Now suddenly, assessee has changed its method of accounting from the stock-

in-trade into investment, the loss of revenue on account of such

conversion can not be sustained on account of clever accounting.

iii) Stock-in-trade is not a capital asset. Simply changing the

nomenclature can not change the character of the asset. The shares

which were carried in accounts book for so long as stock-in-trade

can not be rechristened as investment simply because one day,

one changes its treatment.

iv) Such conversion is against the regularly followed method of

accounting and u/s 145(3) the A.O is empowered to make the

account in the manner provided in section 144 of the I T Act.

How to determine period of holding in case of converted asset ?The issue of determining the period of holding will certainly arise to determine

whether the converted asset is short term or long term. The problem comes

when the stock-in-trade which is being held for say 6 years and converted

to investment and after one year , say it is sold. The question arises from

which date the period of holding should be counted. Let us take an example:

Mr X bought certain private limited companies shares on 01/06/2003 and

was showing it as stock-in-trade. On 01/04/2006 , he convert the shares as

Evasion Through Reverse Conversion Of Shares?

36

Tax Evasion Through Shares

investment in his balance sheet. Let us say , he sells the shares on 01/10/2010.

When he computes capital gains, he takes indexation from the date of original

buy i.e 01/06/2003 (FY 2003-04) . Is he correct?

In author opinion, which is based on settled case laws, the date on which a

stock in tade is converted is the date on which that capital asset has taken birth.

So the age of the asset should be counted from that date. In the example stated

above, the indexation should be from 01/04/2006 and not from 01/06/2003

ITAT, Delhi in case of Splendor Construction (P) Ltd v. ITO (2009) 20

DTR (Del) (Trib) 282 a similar issue came up before the tribunal. The

assessee converted stock in trade into investment in April 2002 and was sold

subsequently in December 2002. The stock-in-trade -lands- were acquired

during the financial year 1998-99. The assessee claimed the capital gain as long

term on the reasoning that it was owned by it for more than 36 months. The

tribunal held that the period of holding as stock in trade is to be ignored

and only the period for which the asset was held as capital asset will be

determinative of the capital gain as to whether short term or long term.

In the case of Commissioner of Income-tax Vs. Santosh L. Chowgule

[1998] 234 ITR 0787 , Bombay High Court held that it is only “the life of

the converted asset which should be considered in reckoning whether it is a

short-term or long term capital asset.

Further Case Law Reference !• ACIT vs Bright Star Investment Pvt. Ltd. on 2/7/2008 (Assessee Favour )

• CIT Vs. Chunilal Khushaldas [1974] 093 ITR 0369(Guj)

• Manecklal Premchand (Decd.) Vs. CIT [1990] 186 ITR 0554(Bom)

–End–

37

Speculation Loss And Tax Evasion!

A share trader does not distinguish between speculation loss and business loss. For him both are trades-one with delivery and the other without delivery. When he prepares his business P & L account, he finds the actual profit or loss.

For example a trader earning Rs 10 lakh in delivery based trade and incurring speculation loss of Rs 10 lakh, in practical sense, earned nothing. However, Income Tax Act treats speculation loss differently. Section 73 of Act provides that speculation loss can be adjusted only with the speculation gain. So when the computation of total income as per I.T. Act is done, he finds that he will have to pay tax with interest on Rs 10 lakh of business income and speculation loss of Rs 10 lakh has to be carried forward.

Thus, he starts devising ways to save himself from financial burden which he feels is purely out of technical reasons. Add to this is the fact that method of evasion of tax in such situation is very easy to implement. He does not have to make any fake documents but a simple twist to computation of total income in a particular manner can save him tax.

Following two methods are being adopted by the share dealers.

I. Mix Speculation Loss With Trading Income.

II. Claiming Speculation Loss As Hedge Loss

The first method is very crude method of evading tax whereas the second method is sophisticated.

Mix Speculation Loss With Trading Income.

Let us start with an example. Following are the P & L account and computation of total income of Mr X for FY 2008-09 (Asst Yr 2009-10).

38

Tax Evasion Through Shares

Opening 1,39,60,000 Sale 8,40,00,000

Purchase 7,56,00,000 Closing stock 1,20,33,000

Speculation Loss 6,00,000

Expense 34,37,000

Net Profit 20,36,000

Computation of total income of Mr X

Income from business 24,00,000

Add Income from other sources 2,50,000

Gross Total Income 26,50,000

Deduction u/s 80 C 1,00,000

Total Income 25,50,000

Perusal of P & L account shows that speculation loss of Rs 6,00,000 has been

treated by the assessee as business loss since he has not added it to his total

income. The A.O passed the assessment order adding the speculation loss

and allowed it to be carried forward.

Are we satisfied with the disallowance of the speculation loss debited in P &

L account in this case? If you go deeper in the case, you may just find that

the assessee has actually adjusted very large speculation loss. The explicit

speculation loss shown in the P & L account was a kind of bait to A.O by the

shrewd tax evader to entangle him on somewhere else so that actual misdeed

remains hidden.

39

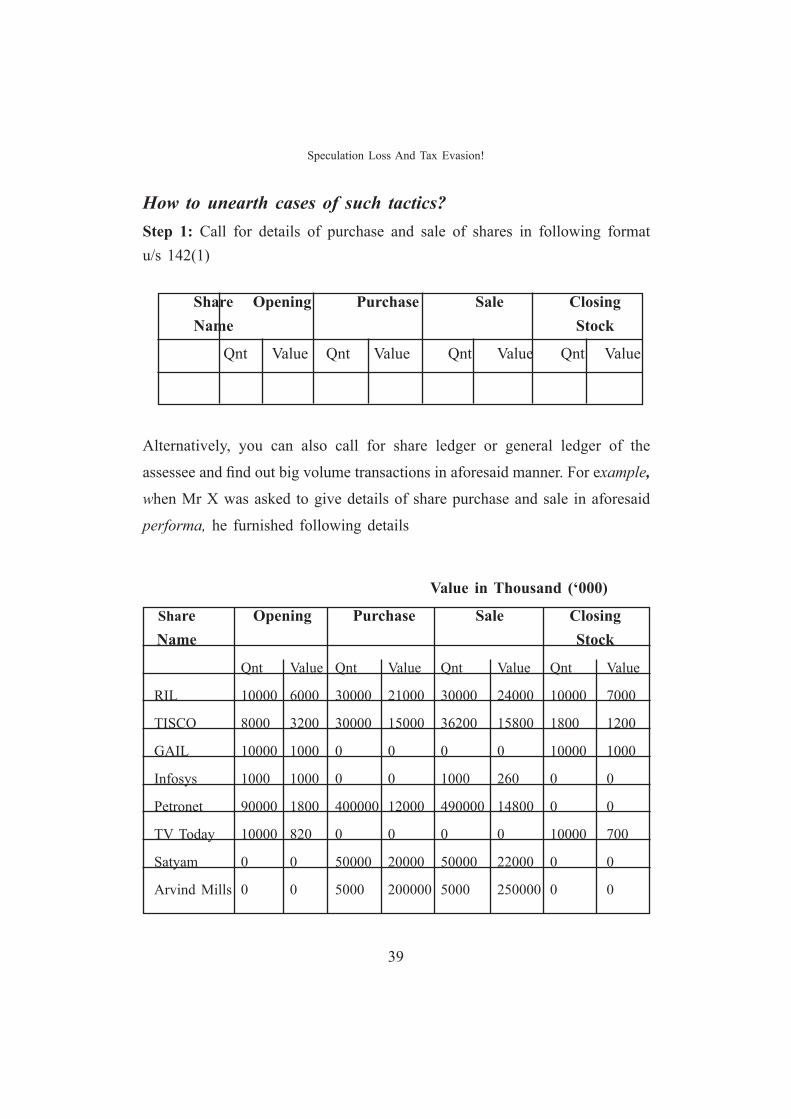

How to unearth cases of such tactics?Step 1: Call for details of purchase and sale of shares in following format u/s 142(1)

Share Opening Purchase Sale Closing Name Stock

Qnt Value Qnt Value Qnt Value Qnt Value

Alternatively, you can also call for share ledger or general ledger of the

assessee and find out big volume transactions in aforesaid manner. For example,

when Mr X was asked to give details of share purchase and sale in aforesaid

performa, he furnished following details

Value in Thousand (‘000)

Share Opening Purchase Sale Closing Name Stock

Qnt Value Qnt Value Qnt Value Qnt Value

RIL 10000 6000 30000 21000 30000 24000 10000 7000

TISCO 8000 3200 30000 15000 36200 15800 1800 1200

GAIL 10000 1000 0 0 0 0 10000 1000

Infosys 1000 1000 0 0 1000 260 0 0

Petronet 90000 1800 400000 12000 490000 14800 0 0

TV Today 10000 820 0 0 0 0 10000 700

Satyam 0 0 50000 20000 50000 22000 0 0

Arvind Mills 0 0 5000 200000 5000 250000 0 0

Speculation Loss And Tax Evasion!

40

Tax Evasion Through Shares

Ballarpur 10000 380 0 0 10000 480 0 0

Mukta Arts 0 5000 500 0 0 5000 300

TELCO 0 0 10000 1200 0 0 10000 1100

Maruti 0 0 12000 1840 0 0 12000 1730

M & M 1000 100 2000 110 0 0 3000 100

Biocon 1000 350 1000 500 2000 1200 0 0

MRF 0 0 20000 2000 0 0 20000 1800

Rel Petro 1000 50000 20000 1250 0 0 21000 1050

Step 2: Segregate those shares in which despite very high volume of transactions (i.e highest purchase & sale value wise), the gain is not very high.

If you analyse the aforesaid table, you can see that higher volume of purchase & sale are in following cases

Share Opening Purchase Sale Closing Name Stock

Qnt Value Qnt Value Qnt Value Qnt Value

RIL 10000 6000 30000 21000 30000 24000 10000 7000

TISCO 8000 3200 30000 15000 36200 15800 1800 1200

Petronet 90000 1800 400000 12000 490000 14800 0 0

Satyam 0 0 50000 2000 50000 22000 0 0

Step 3: Ask for the demat transaction statement from the assessee of these

four shares. Alternatively, you can also fetch yourself the demat transaction

statement from the depository participant of the assessee by invoking provision

u/s 133(6).

41

Step 4 : Compare the total numbers of shares incoming (credited) with the numbers of shares shown as purchased by the assessee in response notice u/s 142(1). If numbers match, there is no speculation.

However, if the number of purchase shown in the details of purchase furnished by the assessee is more than numbers shown in demat transaction statement, there is every possibility that speculative transaction are mixed with the delivery based transactions.

In the aforesaid example, when the transaction statements of RIL and TISCO were tallied with the figures shown in details filed by the assessee, the numbers credited in the transaction statement were less by 8000 and 9000 respectively. Further, shares of Satyam were not reflected in transaction statement at all.

Step 5 : Ask the assessee to produce the contract notes related to purchase and sale of those shares of the company in which you have found out mismatch in numbers. If assessee has done what you caught, assessee will either fail to produce or will furnish fake contract note.

When the relevant contract notes were perused, it was found that extra numbers of shares of RIL, TISCO and Satyam reflected in the details furnished by the assessee were actually of speculation. The contract notes related to those transactions clearly showed that trade was squared off and had resulted in losses as under:—

RIL 7, 60,000

TISCO 8, 00,000

Satyam 20,00,000

Total speculative loss adjustment 35, 60,000

Thus the assessee had mixed non-delivery based trades(speculative) with delivery based trades, so that speculative losses get adjusted with delivery based trade. That way it hides !

Speculation Loss And Tax Evasion!

42

Tax Evasion Through Shares

How to find out the sign of speculation from contract note?1. In case, speculative transactions are performed by a broker on behalf

of assessee, the transactions are, in most cases, squared off same day. Therefore, in all probability, you will find in the same contract note both the debit and credit entries of all details of share transactions.

2. Another way is to ask details of share transactions from the brokers of the assessee. Two separate details should be asked – one for share transaction where delivery was made and one for share transactions without delivery.

3. Write to the stock exchange for confirmation of the trade and ask specifically whether the shares were purchased on delivery basis.

4. Ask the assessee to explain why so many numbers of shares are not reflected in demat transaction statement.

Shortcut to catch the quantum of speculation business!In the very beginning, you must ask for details of all the brokers with whom the assessee had an account. This trick is easier to implement if number of brokers are not many. Send letter u/s 133(6) to all those brokers asking following details about assessee

1. Easiest way to know is ask for Form 10DB which is for declaration of STT deducted at source. Code 3 of the Form 10 DB related to day trading i.e sale of shares without taking delivery (speculative).

2. Details of shares which were purchased on delivery and sold on delivery.

3. To give statement of accounts of all those transaction for which no delivery was made. i.e. assessee squared off dealings through him.

4. Ask for payment details.

The details sent by the brokers should be tallied with the details procured from the assessee and any mismatch should be identified & enquired into.

43

Claiming Speculation Loss as Hedge Loss

This method is quite sophisticated as the assessee tries to evade tax under the garb of innocence that his case falls under exceptional circumstances which allows speculation loss to be treated as business loss. Let us go by an example.

The P & L account of assessee, say Mr X is as under

Opening 1,39,60,000 Sale 8,40,00,000

Purchase 7,06,00,000 Closing stock 1,20,33,000

Speculation Loss 60,00,000

Expense 34,37,000

Net Profit 20,36,000

The computation of income of Mr X shows that the assessee has adjusted the

speculation loss of Rs 60 lakhs as business loss. At the time of scrutiny, the

A.O asked him why speculation should not be added back to his income as

the speculation loss can not be adjusted with the business income.

The assessee replied very shrewdly as under

“Sir,

With due respect to you, I would like to bring in your attention that the said

speculation loss of Rs 60 lakhs were actually business loss in terms of section

43(5) (b) which says

“Speculative transaction” means a transaction in which a contract

for the purchase or sale of any commodity, including stocks and

shares, is periodically or ultimately settled otherwise than by the

actual delivery or transfer of the commodity or scrips :

Speculation Loss And Tax Evasion!

44

Tax Evasion Through Shares

Provided that for the purposes of this clause-

(a) ……………………….

(b) a contract in respect of stocks and shares entered into by a dealer or investor therein to guard against loss in his holdings of stocks and shares through price fluctuations; or

©……..

shall not be deemed to be a speculative transaction;

The speculation loss of Rs 60 lakhs was incurred in course of speculation of shares of MRF to guard against my holding of shares of MRF which you can see from closing stock of shares.”

The A.O. however did not agree with the reply of the assessee. He disallowed the speculation loss to be adjusted as business loss.

What was the actual trick?

Assessee brought following facts on record in support of his claim –

There is speculation loss of Rs. 60,00,000,

The speculation loss was incurred on the shares of MRF.

There was holding in shares of MRF in assessee’s stock in trade.

However, most important fact is not on the record–i.e. whether the speculation was really for minimizing the risk of investment in MRF shares. In the instant case, the A.O found that

The date of speculation was 1/5/2010.

There were no shares of MRF before 1/5/2010.

The shares of MRF shown in stock in trade were purchased on 1/9/2009.

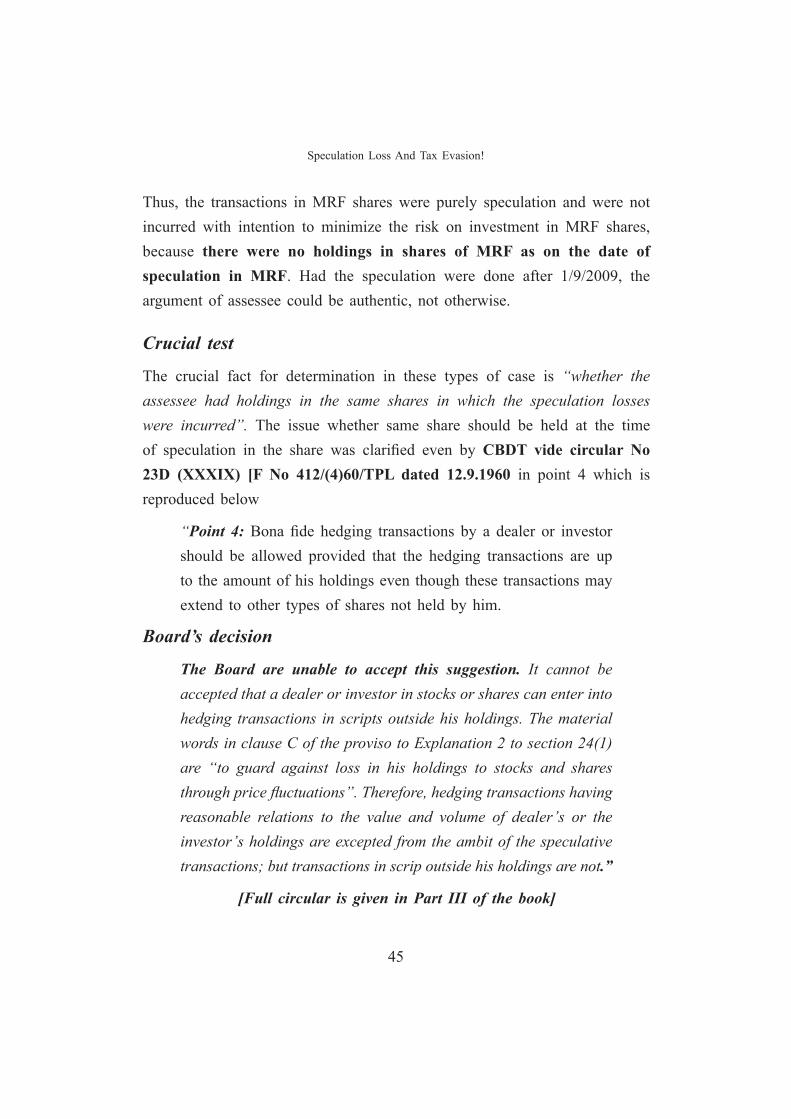

45

Thus, the transactions in MRF shares were purely speculation and were not incurred with intention to minimize the risk on investment in MRF shares, because there were no holdings in shares of MRF as on the date of speculation in MRF. Had the speculation were done after 1/9/2009, the argument of assessee could be authentic, not otherwise.

Crucial test

The crucial fact for determination in these types of case is “whether the assessee had holdings in the same shares in which the speculation losses were incurred”. The issue whether same share should be held at the time of speculation in the share was clarified even by CBDT vide circular No 23D (XXXIX) [F No 412/(4)60/TPL dated 12.9.1960 in point 4 which is reproduced below

“Point 4: Bona fide hedging transactions by a dealer or investor should be allowed provided that the hedging transactions are up to the amount of his holdings even though these transactions may extend to other types of shares not held by him.

Board’s decision

The Board are unable to accept this suggestion. It cannot be accepted that a dealer or investor in stocks or shares can enter into hedging transactions in scripts outside his holdings. The material words in clause C of the proviso to Explanation 2 to section 24(1) are “to guard against loss in his holdings to stocks and shares through price fluctuations”. Therefore, hedging transactions having reasonable relations to the value and volume of dealer’s or the investor’s holdings are excepted from the ambit of the speculative transactions; but transactions in scrip outside his holdings are not.”

[Full circular is given in Part III of the book]

Speculation Loss And Tax Evasion!

46

Tax Evasion Through Shares

Lessons learnt !

If assessee claims that a speculation transaction is actually business transaction

within the meaning of section 43(5)(b) of the I T Act, following steps must

be taken to confirm if the speculation falls within the exception provided u/s

43(5)(b) of the I T Act.

1. Note the names of share and respective dates of speculation

transactions.

2. It must be confirmed if the assessee possessed those company’s shares

on the date when he made speculation transaction resulting in

loss.

3. It should also be noted that if the numbers of shares held by assessee

as on the date (s) of speculation is very small in comparison to

speculative transactions done, such speculation transaction should

also not be considered covered u/s 43(5) read with CBDT’s circular.

Case Law Reference

1. ACIT vs Dinesh K Mehta [ITAT Mumbai] 2010 39 SOT 488- [Revenue Favor ]

2. CIT v. Hotz Hotel Pvt. Ltd. [2003] 128 Taxman 160 (Delhi)

3. Davenport & Co. P. Ltd. V/s. CIT reported in 100 ITR 715 (S.C.)

4. CIT v. Joseph John [1968] 67 ITR 74 (SC)

–End–

47

How To Detect Closing Stock Undervaluation ?The closing stock under valuation is a very common trick to reduce the profit. This method is applied in all kinds of business. But in case of shares, it can be applied very easily on account of sheer number of closing stock items. In many cases one may find the numbers of closing stock of shares as many as 400 or even 600 shares. If the A.O is not vigilant to check the market price of closing stock, tax evaders can quite easily reduce taxable profits without much effort.

Method of valuation

The accounting standard AS 2 issued by ICAI is prescribed for valuation of inventory but AS-2 is not valid for valuation of stock-in-trade in relation to shares, debentures and other financial instruments. Therefore no accounting standard is prescribed for valuation of closing stock of shares. Three common methods for valuation of closing stock are :

1. At cost

2. At lower of cost or market value ;

3. At average cost

The time tested and legally settled method is “cost or market value whichever is lower”. This method is beneficial to traders as the notional loss in valuation of stock-in-trade with respect to cost is allowed to be adjusted with the current years’ profits. As such, it is most accepted method of valuation of closing stock-in-trade. That the diminution in the value of closing stock is allowed under this method, also make it a tool to evade tax. If you refer the chapter “Evasion Through Bogus Purchase Of Shares”, the tax evasion is possible because of this method. This chapter, however, is not on the merits or demerits of method of valuation, but on the subject of undervaluation trick adopted by some unscrupulous share traders.

48

Tax Evasion Through Shares

Let us take an example. The P & L account of Mr X, a share dealer, for FY 2009-10 was as follows :

Opening 1,39,60,000 Sale 8,40,00,000

Purchase 7,56,00,000 Closing stock 1,20,33,000

Speculation Loss 6,00,000

Expense 34,37,000

Net Profit 24,36,000

Details of closing stock as on 31/3/2009

Share Name Opening Qnt Value RIL 10000 4100000TISCO 8000 3200000GAIL 10000 1000000 Infosys 1000 1000000 Petronet LNG 90000 1800000 TV Today 10000 82000 Satyam 0 0 Arvind Mills 0 0 Ballarpur 10000 351000 Mukta Arts 0 TELCO 0 0 Maruti 0 0 M & M 1000 100000 Biocon 1000 350000 MRF 0 0 Rel Petro 1000 50000 12033000

49

This is only an example, that’s why, the list of closing stock is kept very small.

Let us say, in the aforesaid case, the average purchase cost of RIL shares is Rs 500. However the valuation of closing stock has been done at average price of Rs 410 per share. It means that if assessee is following “cost or market price whichever lower” method, Rs 410 should be the market price as on last date when the stock exchange was open. If you took the trouble to confirm with the rate on NSE or BSE, it might be found that rate was actually 480. What it means that assessee, reduced its income by Rs 7 Lakhs.

This is very crude method for the tax evasion, but A.Os should be vigilant to get the confirmation of the closing rate on major stock exchange concerned and verify valuation done by assessee.

How to check the closing stock price?

There are two ways to confirm the stock rate :

1. By consulting certain books which publishes closing rates of stocks.

2. Visit the internet sites of NSE, BSE or CSE or any regional stock exchange. Website addresses are given in Part III of the book.

And check the price on the last day of the year which may not necessarily be 31st March but last day means the last day stock exchange was open. One can verify the price of the share on a particular day by visiting web site of the stock exchange.

[Read how internet helps you in investigation of share cases in Part III of the book.]

Which Stock Exchange’s Price?

In author’s opinion the stock exchange from which such transaction was done, should be taken for valuation of the closing market rate.

–End–

How To Detect Closing Stock Undervaluation ?

50

Tax Evasion Through Shares

How To Detect If Short Term Is Claimed As Long Term Gain?

This method is the easiest to implement. Shares held for 12 months are short term capital asset and for one day more, shares become long term capital asset. Long term gains on shares sold through stock exchanges are exempt u/s 10(38) and short term gains on shares chargeable to STT are taxed @10% (15% proposed by Budget 2008). Therefore, an unscrupulous investor tries to disguise a short term as long term gains for the stupendous tax savings