Embed Size (px)

Citation preview

1

Tata Chemicals Limited

LeaderFocused

ProgressiveEstablished

Inorganic Chemicals

Fertilizers

2

•The Tata Group

3

The Tata Group

Engineering25%

Materials21%

Energy9%

Services10%

Comm & info systems

23%

Chemicals5%

Consumer products

7%

Figures in %Segmental distribution - sales

4

Financial insight

1,497

2,707

805

10,774

11,206

8,986

10,524

USD million –

FY 2003

Net forex earnings

Exports

PAT

Sales

Total income

Gross Block

Value of assetsCapital market perspective

• 31 Tata companies listed on

various stock exchanges

• Accounts for approx 3.5% of

the total market capitalization

of all listed companies in India

• Over 2.1 million shareholders

5

•Tata Chemicals

6

Business portfolio

Urea37%

Cement7%Salt

14%

Soda ash34%

Others8%

Figures in %Sales distribution

7

Perspective - Key businesses

Soda Ash

One of the largest single site soda ash producer globallyPlant capacity: 875,000 MTLargest market share in IndiaMultiple product variants addressing diverse markets

Salt

Urea

Pioneer in branded salt market in IndiaLargest salt brand in IndiaHigh brand equity and premium perception

Most energy efficient manufacturing facility in IndiaPlant capacity: 864,000 MTLeading presence in high demand centersClose association with target consumer

8

•Business perspective

9

Sector dynamics

20051987

2396 2501

16841835 1877

2140

51 43 158 99

190518181730

2371

0

500

1000

1500

2000

2500

3000

FY '00 FY '01 FY '02 FY '03

in '0

00

M

Demand Domestic capacity Domestic production Imports

• Demand presently short of supply, average capacity utilization of Indian industry: 81%

• Glass is the fastest growing customer segment

• Threat of increasing import volumes, with custom duties expected to be reduced in line with

WTO recommendations making efficiencies key

10

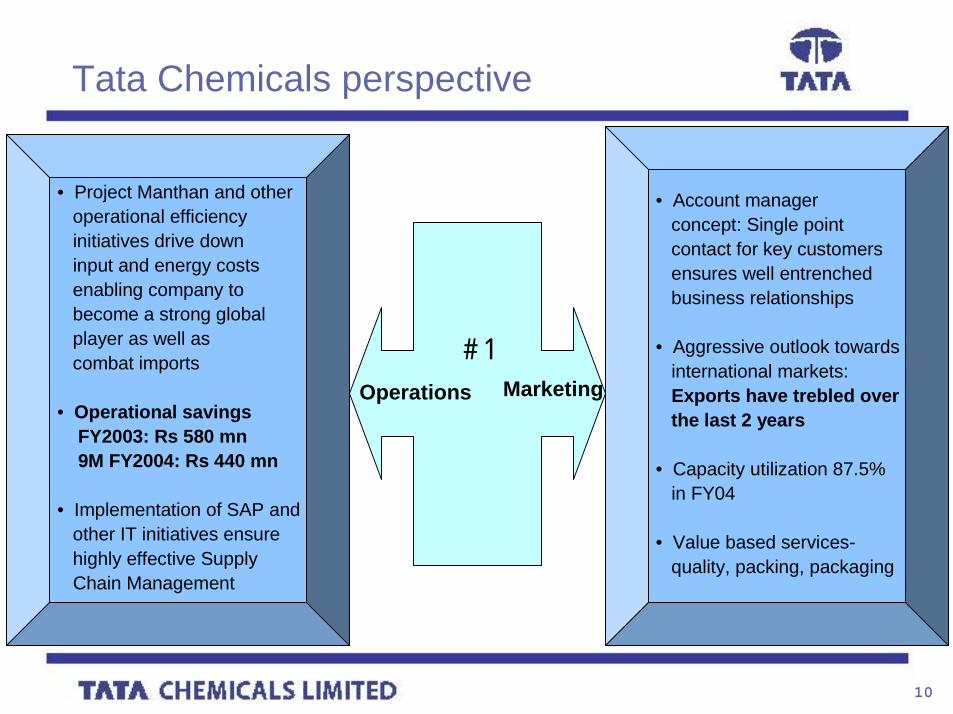

Tata Chemicals perspective

• Account manager concept: Single pointcontact for key customersensures well entrenched business relationships

• Aggressive outlook towardsinternational markets: Exports have trebled over the last 2 years

• Capacity utilization 87.5% in FY04

• Value based services-quality, packing, packaging

MarketingOperations

• Project Manthan and otheroperational efficiency initiatives drive downinput and energy costsenabling company to become a strong global player as well as combat imports

• Operational savingsFY2003: Rs 580 mn9M FY2004: Rs 440 mn

• Implementation of SAP andother IT initiatives ensurehighly effective SupplyChain Management

# 1

11

•Salt

12

The Indian Salt industry

Anapoorna23%

Tata Salt39%

Other28%

Nirma6%

Dandi4%

Branded iodised

27%

Loose unbranded

73%

• Total demand for edible salt in India: 5.46 million tonnes, Demand for branded edible salt: 0.7

mil tonnes

• Education and awareness gradually altering consumption patterns towards iodized salt

• National brands growing at 7%

November 2003

13

Tata Chemicals perspective

Contributed Rs 3.5million towards social & community programme

Reorganizedset-up from 1national to 29

distributors and 24 CFAs – increases

penetration

Revamped marketingteam, specialized skillsbrand mgt, marketing, promotion, etc

Samundar ‘crystal salt’ expands presence in

segment

# 1

Highlights

• Tata Salt ranked No. 6

in the Brand Equity

survey of India’s most

trusted brands

• Ranked No. 1 in the

Food Additives segment

• Ranked 18th in A C Nielsen

Global Brand Equity Index

• Marketshare greater than

the combined share of

next three national branded

players

14

•Fertiliser

15

The Indian fertiliser sector

• Third largest producer and consumer of fertiliser in the world

• Dominated by PSUs and Co operatives

• Installed capacity of approximately 20 million MT

• Highly complex industry with plants using a wide variety of feedstock, varying capacity, technology and vintage

• Consumption patterns presently heavily skewed towards nitrogenous fertilisers. NPK ratio of 7:2:1 as against an average of 5:2:3 internationally

• Urea constitutes 85% of nitrogenous fertiliser consumption and 58% of total consumption

• Sector emerging from being highly protected to a more liberalized and efficiency encouraging environment

16

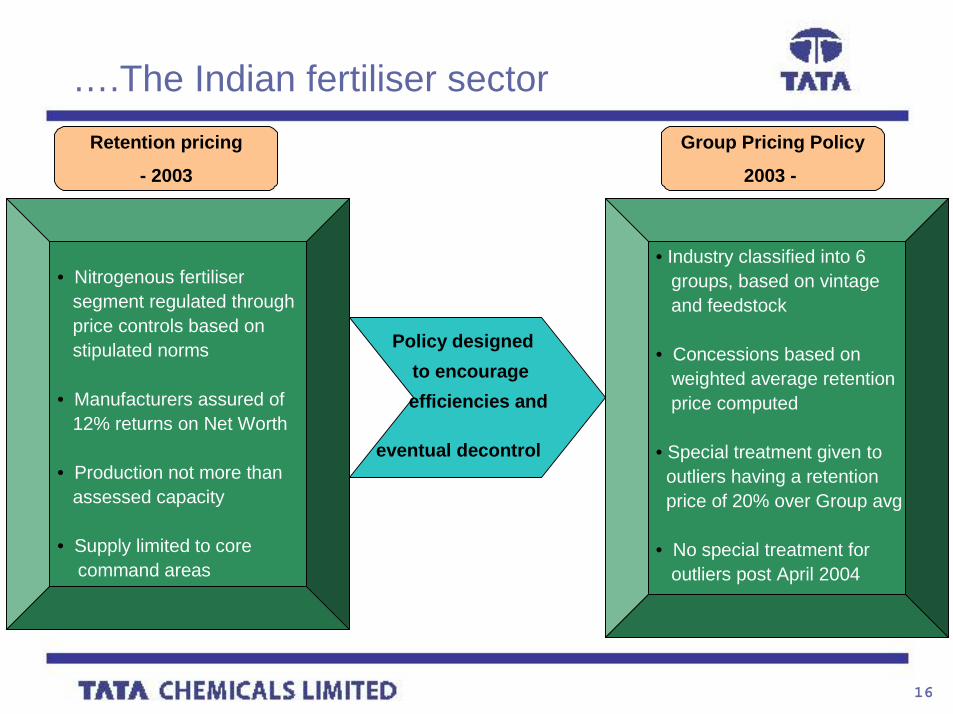

….The Indian fertiliser sector

• Nitrogenous fertiliser segment regulated through price controls based on stipulated norms

• Manufacturers assured of 12% returns on Net Worth

• Production not more than assessed capacity

• Supply limited to corecommand areas

• Industry classified into 6groups, based on vintageand feedstock

• Concessions based on weighted average retentionprice computed

• Special treatment given to outliers having a retention price of 20% over Group avg

• No special treatment for outliers post April 2004

Policy designedto encourageefficiencies and

eventual decontrol

Retention pricing

- 2003

Group Pricing Policy

2003 -

17

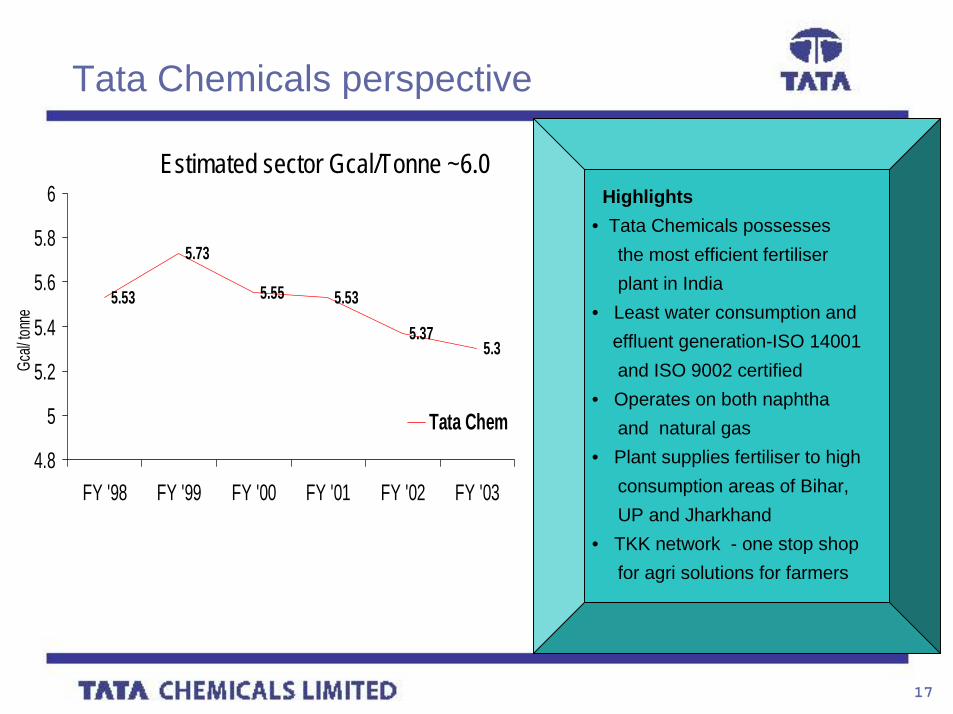

Tata Chemicals perspective

5.53

5.73

5.55 5.53

5.375.3

4.8

5

5.2

5.4

5.6

5.8

6

FY '98 FY '99 FY '00 FY '01 FY '02 FY '03

Gcal/

tonn

e

Tata Chem

Estimated sector Gcal/Tonne ~6.0Highlights

• Tata Chemicals possessesthe most efficient fertiliserplant in India

• Least water consumption andeffluent generation-ISO 14001and ISO 9002 certified

• Operates on both naphthaand natural gas

• Plant supplies fertiliser to highconsumption areas of Bihar,UP and Jharkhand

• TKK network - one stop shopfor agri solutions for farmers

18

9M FY 2003-04 Financial Results January 2004

•Financials

19

RatiosQ3 2003 FY2003 FY2002

CURRENT RATIO 3.56:1 3.23:1 2.63:1

DEBTORS TURNOVER RATIO 7.62:1 6.16:1 3.68:1

CREDITORS TURNOVER RATIO 5.84:1 10.7:1 10.27:1

INVENTORY TURNOVER RATIO 5.3:1 6.4:1 4.52:!

OPERATING PROFIT MARGIN (operating income considered not incl of cost of goods sold) 27.5% 25.5% 26.2%

NET PROFIT RATIO 13.5% 11.5% 8.4%

INTEREST SERVICE COVERAGE RATIO 9.39:1 3.9:1 4.16:1

RETURN ON CAPITAL EMPLOYED (Operation 12.2% 12.0% 13.1%

RETURN ON Net worth 10.3% 12.0% 8.2%

DEBT/EQUITY RATIO 0.27 0.50 0.68

ASSETS COVERAGE RATIO 4.11 2.88 2.35

20

9M FY 2003-04 Financial Results January 2004

•9M FY 2003-04 Results

21

Revenue performance

1258011816

4000

6000

8000

10000

12000

14000

9M FY2003 9M FY2004

Rs.

mn

4672

4375

2000

3000

4000

5000

Q3 FY2003 Q3FY2004

Rs.

mn

6% 7%

9M FY 2004 Q3 FY 2004

22

Profit from operations

9M FY 2004 Q3 FY 20043651

3379

2929

0

1000

2000

3000

4000

9M FY2003 9M FY2004

Rs

mn

0

10

20

30

40

50

%EBITDA Margin

11491167

27 25

0

300

600

900

1200

1500

Q3 FY2003 Q3 FY2004

Rs

mn

0

7

14

21

28

35

%

EBITDA Margin

Marginal decline in profit from operations in Q3 FY2004 attributable mainly to • Withdrawal of sales tax benefit on soda ash • implementation of Group Pricing Policy (The Group Pricing Policy is however

expected to have a positive influence on Tata Chemicals in the long term)

23

PAT

38% 6%

9M FY 2004 Q3 FY 20041880

1365

7.56

10.41

0

500

1000

1500

2000

9M FY2003 9M FY2004

Rs

mn

0

3

6

9

12

%PAT EPS

590555

3.073.26

0

150

300

450

600

Q3 FY2003 Q3 FY2004

Rs

mn

0

1

2

3

4

5

%

PAT EPS

24

Financial Management

9270

61704910

0.54

0.51

0.29

0

2000

4000

6000

8000

10000

12000

31-Dec-02 30-Sep-03 31-Dec-03

Rs

mn

0.0

0.2

0.4

0.6

0.8

1.0

%

Debt Debt-equity ratio

Close to 50% debt reduction between Dec 2002 and Dec 2003

25

…Financial Management

8.510

20

8.5

10.1

8.4

0

5

10

15

20

25

Q3 FY03 Q2 FY04 Q3 FY04

Rs

mn

0

3

6

9

12

%

Interest Cost of borrowing

Over 50% decline in interest costs YOY

26

9M FY 2003-04 Financial Results January 2004

•Perspective of proposed merger

•with Hind Lever Chemicals

27

Hind Lever Chemicals Limited

Leader in its chosen product segments

Chemicals

Fertilizers

Largest STPP player with a nation-wide customer base and significant market

share

Well entrenched distribution network in

key consumption markets

World-class integrated manufacturing facility,

with high asset productivity and strong

safety/environment management systems

Pioneer in ‘branding’ –comprehensive range

of products under ‘Paras’ brand, high customer loyalty

28

Overview

• Both companies possess natural operating synergies across their key operating activities in the chemicals and agri inputs sectors

• The merger ratio has been defined at 2.5:1 by independent financial advisors (2.5 shares of TCL for every 1 share of HLCL)

• The transaction will enable the development of a superioroperating model and business profile by strengthening the Company’s position in its defined areas

29

Growth outlook

• Capacity enhancement• Inorganic growth opportunitiesFertiliser

• Exploring international markets• Enhancing relationships with key customers,

strengthening global and domestic competitive positionInorganic

chemicals

Soda Ash

Food additives• Reach out to all market segments• Expand offerings e.g. cooking soda

Continuous enhancement of financial & operational efficiencies