Embed Size (px)

Citation preview

Tariff petition before the

Hon’ble Uttarakhand

Electricity Regulatory

Commission

True Up for FY2014-15

Annual Performance Review

FY 2015-16

&

Multi-Year Tariff for FY2016-

17, FY2017-18, FY2018-19

for

Khatima Hydro Power Project

(3X 13.8 MW)

November 2015

By UJVN Limited

Dehradun

Tariff petition before the Hon’ble Uttarakhand Electricity Regulatory Commission

2

AFFIDAVIT

BEFORE THE HON’BLE UTTARAKHAND ELECTRICITY REGULATORY

COMMISSION, DEHRADUN, UTTARAKHAND.

FILING

NO.CASE

NO.

In the matter of:Filing of Petition for true up for the financial year 2014-15, APR

for FY 2015 and for determination of Hydro Generation Tariff

for the financial years from 2016-17 to FY 2018-19 for Khatima

hydro power station of UJVN Ltd. under Section 62 and 86 of the

Electricity Act, 2003 read with the relevant regulations and

guidelines of the Commission

AND

In the matter of: UJVN Ltd., a Company incorporated under the provisions of the

Companies Act, 1956 and having its registered office at

UJJWAL, Maharani Bagh, GMS Road, Dehra Dun – Petitioner.

Tariff petition before the Hon’ble Uttarakhand Electricity Regulatory Commission

3

Tariff petition before the Hon’ble Uttarakhand Electricity Regulatory Commission

4

1. Specific Legal Provisions under which the Petition is

being filed

1) UJVN Ltd. under Section 62 and 86 of the Electricity Act, 2003 read with

(a) Regulation 10 of the Uttarakhand Electricity Regulatory Commission (Terms and

Conditions for Determination of Multi Year Tariff) Regulations, 2015

(b) Regulation 1(3) and 13 of the Uttarakhand Electricity Regulatory Commission (Terms

and Conditions for Determination of tariff) Regulations,2011

is filing this Tariff Petition before the Hon’ble Commission for approval of tariffs for the

financial years from 2016-17 to 2018-19, Annual Performance Review for the financial years

2015-16 and true up for the financial years from 2014-15.

2. Limitation of the case

2) Since an application for tariff determination by any generating company has to be filed

before the Hon’ble Commission before 30th November of every year therefore, the present

petition is not barred by limitation under Regulation of Uttarakhand Electricity Regulatory

Commission Conduct of Business Regulation 2014.

3. Facts of the case

1) The Petitioner, UJVN Ltd.is a company incorporated under the provisions of the Companies

Act, 1956, having its registered office at UJJWAL, Maharani Bagh, GMS Road, Dehradun;

2) It is submitted that Government of Uttaranchal (GoU) vide order dated November 5,

2001 transferred all hydropower assets of Uttar Pradesh Jal Vidyut Nigam Limited

(UPJVNL) located in the State of Uttarakhand to UJVNL with effect from November 09,

2001. In compliance to the said order, administrative and financial control of all hydro

power plants of UPJVNL in operation or under construction was taken over by UJVNL with

effect from November 09, 2001. GOU order also defines the basis of division of assets and

liabilities between UPJVNL and UJVNL and is self-explanatory;

3) Though administrative and financial control was transferred to UJVNL on November 09,

2001, UJVNL initiated discussions with UPJVNL for formulation of transfer scheme as per

the said GOU order on mutually agreed terms.

4) Government of Uttarakhand (GoU) has notified the provisional transfer scheme vide its

notification no. 70/AS (E)/I/2008-04 (3)/22/08 dated 07/03/08.

5) The Hon’ble Uttarakhand Electricity Regulatory Commission issued the following tariff

regulations for hydro generating stations in the State of Uttarakhand, applicable for plants

Tariff petition before the Hon’ble Uttarakhand Electricity Regulatory Commission

5

of capacity more than 25 MW.

a. Uttarakhand Electricity Regulatory Commission (Terms and Conditions for

Determination of Hydro Generation Tariff) Regulations, 2004 (hereinafter referred to as

the “Tariff Regulations 2004”) issued on 14th May 2004. In accordance to the notification

dated November 29, 2011, the Tariff Regulations 2004 were valid up to the date April 30,

2012.

b. Uttarakhand Electricity Regulatory Commission (Terms and Conditions for Determination

of Tariff) Regulations, 2011 (hereinafter referred to as the “Tariff Regulations 2011”)

issued on 19th December 2011. These regulations were applicable from April 1, 2013 to

March 31, 2016.

c. Uttarakhand Electricity Regulatory Commission (Terms and Conditions for

Determination of Multi Year Tariff) Regulations, 2015 (hereinafter referred to as the

“Tariff Regulations 2015”) issued on September 10, 2015. These regulations are applicable

from April 1, 2016 onwards.

6) It is submitted that in development of these petitions, UJVNL has been guided by principles

that are inherent in the Tariff Orders of the Commission dated 12/07/06, 14/03/07,

18/03/08, 21/10/09, 05/04/10, 10/05/11, 04/04/2012, 06/05/2013, 03/09/2013,

10/04/2014 and 11/04/15 to the extent the same are acceptable to the Petitioner.

Facts of the case

Contents

AFFIDAVIT 2

1. Specific Legal Provisions under which the Petition is being filed 4

2. Limitation of the case 4

3. Facts of the case 4

List of Annexures 8

1. Chapter1: Truing Up of FY2014-15 and Annual PerformanceReview of FY2015-16 9

1.1. Norms of Operation 9

1.2. Capital Cost 10

1.3. Additional Capitalisation 11

1.4. Debt Equity Ratio 13

1.5. Return on Equity Ratio 13

1.6. Depreciation 14

1.7. Interest on loan capital 15

1.8. 15

1.9. O&M expenses 16

1.10. Interest on working capital 18

1.11. Non-Tariff Income 19

1.12. Design Energy 20

1.13. Truing up on account of controllable factors for FY2014-15 20

1.14. Truing up on account of NAPAF for FY2014-15 21

1.15. Impact of truing up for FY2014-15 22

1.16. Income Tax 22

1.17. Claim of UPCL relating to electricity charges of the electricity consumed by employees of UJVN Limited 23

2. Tariff determination for FY2016-17, FY2017-18 and FY2018-19 24

2.1. Norms of Operation 24

2.2. Additional Capitalisation 25

2.3. Return on Equity 26

2.4. Depreciation 26

2.5. Interest on Loan Capital 28

2.6. O&M Expenses 29

2.7. Interest on working capital 31

2.8. Non-Tariff Income 32

2.9. Total Fixed Charges 33

2.10. Design Energy 33

2.11. Capacity charges and Energy Charge rate 33

2.12. Income Tax 34

2.13. Water Tax 34

Facts of the case

3. Status of Directives in Tariff Order Dated 4 April 2012 35

3.1. Action taken by UJVNL on directives 35

4. Cause of Action 37

5. Ground of Relief 38

Not Applicable 38

6. Details of Remedies Exhausted 39

7. Matter Not Previously Filed or Pending With any Court 40

8. Relief sought 41

8.1. Relief Sought from the Hon’ble Commission 41

9. Interim Order, if any, prayed for 43

10. Details of Index 44

11. Particulars of the Fee remitted 45

12. List of Enclosures 46

13. HYDRO FORMATS Error! Bookmark not defined.

List of Annexure

List of Annexure

S.No. Annexure Details Page No.

1 Annexure-1 Technical Report of HEP 67

2 Annexure-2 Audited Accounts for 2014-15 74

3 Annexure-3 Allocation of Additional

Capitalisation 2014-15

110

4 Annexure-4 Calculation Sheet of Interest Rate for

normative loan

111

5 Annexure-5 Plant Wise Balance sheet 113

6 Annexure-6 Recruitment Plan 141

7 Annexure-7 SBI PLR Rate 142

8 Annexure-8 Excess provision for Non-Tariff

Income

143

9 Annexure-9 UPCL/UJVNL Letter 5906/ 8116 144

10 Annexure-10 Copy of Water Tax Order 151

11 Annexure-11 Calculation of Water Tax Impact 155

Chapter1: Truing Up of FY2014-15 and Annual Performance Review of FY2015-16

1. Chapter1: Truing Up of FY2014-15 and Annual Performance

Review of FY2015-16

1.1. Norms of Operation

The norms specified by the Hon’ble Commission as applicable for the Khatima power station are as

follows:

1.1.1. Normative Plant Availability Factor (NAPAF)

a. Based on the norms for run of the river stations, the NAPAF for the station has been

considered at 47% for the FY 2014-15and FY 2015-16 respectively in the Order dated

03/09/2013 passed by this Hon’ble Commission.

b. Khatima Hydro Power Station could not achieve the normative plant availability factor

determined by the Hon’ble Commission for the FY 2014-15 due to forced closure of the Power

Station since 31-8-2014 due to breaching of Power Channel, which was beyond the control of

Petitioner. The actual PAFM achieved was 15.36 % for FY 2014-15 as against approved

NAPAF of 47% for FY2014-15.The petitioner therefore requests before the Hon’ble

Commission that provision passed in tariff order dated 03.09.2013 may further be

allowed as per revised schedule of RMU and revise the NAPAF of Khatima Power

Station for FY 2014-15 as 23.04 %

c. The copy of Annual Report on Technical Performance of Khatima HEP highlighting the

calculation and justification is annexed here and marked as Annexure –1.

d. The petitioner also requests before the Hon’ble Commission that provision passed in

tariff order dated 03.09.2013 may further be allowed as per revised schedule of RMU for

FY 2015-16.

1.1.2. Auxiliary Energy Consumption including Transformation Losses

a. The Petitioner has claimed transformation losses and auxiliary consumption as detailed in

Table 1 below at the normative levels specified by the Hon’ble Commission through the

regulations and in its earlier tariff order.

b. It is respectfully submitted that in accordance to the abovementioned claim, Auxiliary

Consumption and Transformation Losses have been computed as per the norms prescribed

under Regulation 51(2) of Regulation of 2011 and enumerated below:

Table 1 Auxiliary Consumption and Transformation Losses

Station Particulars Norm Quantum (MU)

Type of Station

a) Surface Yes

b) Underground No

Type of excitation

a) Rotating exciters on generator Yes

Chapter1: Truing Up of FY2014-15 and Annual Performance Review of FY2015-16

Station Particulars Norm Quantum (MU)

b) Static excitation No

Auxiliary Consumption including

Transformation losses

(As % of Total Generation)

0.7% 1.36

1.2. Capital Cost

1.2.1. Petitioner has already informed along with detailed explanation to the Hon’ble Commission

in the previous tariff petitions for various financial years (from FY 2007 to FY 2015) that

there has been limited transfer of historical data from UPJVNL to UJVNL. Despite the

Petitioner’s repeated follow-up, complete technical details are yet to be received. Certain

essential documents such as the Detailed Project Reports, CEA clearances or Project

Completion Reports have also not been provided. UJVNL is therefore not in a position to

provide details regarding the break-up of original cost of fixed assets and those approved by

a competent authority on COD.

1.2.2. Transfer Scheme between UPJVNL & UJVNL is still not finalized. This matter has also been

appraised to GoU from time to time. GoU had notified the value of GFA for the purpose of

RoE provisionally by notification dated 7/03/08. Further, the Hon’ble Commission has

considered the amount of Rs. 2.21 Crore for additional capitalization on the date of

commissioning of MB-I HEP. The value of the Gross Fixed Assets (GFA) for nine large

hydro projects (LHPs), notified by the GoU and considered by the Hon’ble Commission in its

Tariff Order dated April 4, 2012 is tabulated below:

Table 2 Opening GFA as on January 2000 (Rs. Crore)

Plant Amount (Rs. Crore)

Dhakrani 12.40

Dhalipur 20.37

Chibro 87.89

Khodri 73.97

Kulhal 17.51

Ramganga 50.02

Chilla 124.89

ManeriBhali-I 111.93

Khatima 7.19

Total 506.17

Chapter1: Truing Up of FY2014-15 and Annual Performance Review of FY2015-16

1.2.3. It is respectfully submitted that in view of the facts stated above the value of opening GFA of

Rs. 506.17 Crores determined by the Hon’ble Commission for 9 LHPs which are transferred

to UJVNL by UPJVNL may also be considered for the purpose of this Tariff Order, pending

finalization and notification of the Transfer Scheme.

1.2.4. Accordingly, the value of opening GFA, as on January 2000, transferred to UJVNL for Khatima

Power House amounting to Rs. 87.89 Crores may be considered by Hon’ble Commission

pending finalisation and notification of the Transfer Scheme.

1.3. Additional Capitalisation

1.3.1. Hon’ble Commission, during Truing Up exercise, in its Tariff Order dated April 11, 2015 has

already approved Additional Capitalisation for Kulhal HEP till FY 2013-14 based on audited

annual accounts. The approved figures are as under:

Table 3 Additional Capitalisation as per tariff order dated April 11, 2015 (Rs. Crore)

Financial Year FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

Additional

capitalization

0.01 0.03 0.10 0.11 0.08 0.05 0.33 0.73 0.21 0.07 0.02 0.01 0.03

1.3.2. The above additional capitalisationup to the FY 2013-14 for Khatima HEP has already been

approved by the Hon’ble Commission in its tariff order dated April 11,2015

1.3.3. The Petitioner, as per observations of the Hon’ble Commission, is maintaining proper asset

books of various components of Additional Capitalisation. The breakup of components of

Additional Capitalisation presented in the above table is as under:

Table 4Components of Additional Capitalisation till FY 2014-15 (Rs. Crore)

Financial

Year

FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

Land 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Building 0.00 0.00 0.04 0.01 0.00 0.00 0.06 0.00 0.01 0.00 0.00 0.00 0.00

Major Civil

Works

0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Plant & Machinery

0.00 0.00 0.00 0.01 0.00 0.01 0.24 0.62 0.16 0.02 0.00 0.00 0.01

Vehicles 0.01 0.00 0.01 0.07 0.02 0.01 0.00 0.00 0.01 0.01 0.00 0.00 0.00

Furniture &

Fixture

0.00 0.00 0.01 0.00 0.01 0.01 0.01 0.02 0.01 0.02 0.00 0.00 0.01

Office

Equipment

0.00 0.02 0.03 0.01 0.04 0.03 0.02 0.09 0.03 0.02 0.02 0.00 0.01

Total 0.01 0.03 0.10 0.11 0.08 0.05 0.33 0.73 0.21 0.07 0.02 0.01 0.03

Chapter1: Truing Up of FY2014-15 and Annual Performance Review of FY2015-16

1.3.4. It is respectfully submitted that in order to ensure efficiency and safety as well as ensuring

continuous operation of the plants the additional capitalization was required to be incurred

which may kindly be considered and allowed by the Hon’ble commission. Kind attention is

invited to Regulation 24(2) of the Tariff Regulations 2011 explicitly permit additional

works/service, which may become necessary for efficient and successful operation of the

plant.

„24(2) In case of hydro generating stations, any additional expenditure which has become

necessary on account of damage caused by natural calamities (but not due to flooding of

power house attributable to the negligence of the generating company), including due to

geological surprises, after adjusting for proceeds from any insurance scheme, and expenditure

incurred due to any additional work which has become necessary for successful and efficient

plant operation;‟

1.3.5. It is now respectfully submitted that the actual additional capitalisation in the true-up year

FY2014-15 and the projected additional capitalisation for APR year FY2015-16 for Khatima

Power House is as follows:

Table 5 Additional Capitalisation

Financial Year FY2014-15

(actual)

FY2015-16

(RE)

Land 0.00 0.00

Building -0.04 0.00

Major Civil Works -1.56 0.00

Plant & Machinery 42.16 35.86

Vehicles 0.00 0.00

Furniture & Fixture 0.00 0.08

Office Equipment 0.01 0.04

Total 40.58 35.99

1.3.6. Details of additional capitalisation for the FY 2014-15 are based on Audited Annual accounts

for the FY 2014-15 of the Corporation. A Copy of the Audited Annual Accounts for the FY

2014-15 is annexed here and marked as Annexure – 2

1.3.7. It is further respectfully submitted that the accounts had been maintained centrally for the

various HEPs. In certain instances one - to - one correlation of the accounting divisions is

possible with individual stations. However, for others, some form of apportionment is

necessary for allocating certain expenses that are incurred by accounting units that serves

more than one station.

1.3.8. The additional capital expenses incurred by such accounting divisions serving more than one

station have been allocated as detailed below:-

Head Office/ CSPPO: The 85% of the additional capitals expenses have been

allocated to the 9 LHPs, 10% of the additional capitals expenses have been allocated

to MB-II and the remaining 5% to SHPs. Further the allocation among the

LHPs/SHPs is done on the basis of installed capacity of each LHP/SHP.

Chapter1: Truing Up of FY2014-15 and Annual Performance Review of FY2015-16

Additional Capitalization of DDD Dakpathar: The additional capitals expenses

have been allocated between Chibro, Khodri, Dhakrani, Dhalipur and Kulhalin the

ratio of their respective installed capacity.

General Manager Office/ DGM Civil Dhalipur: allocated on Chilla, Ramganga,

Khatima, Chibro, Khodri, Dhakrani, Dhalipur, Kulhal LHPs and Pathri, Mohdpur

and Galogi SHP which are within the control of the concerned GM/ DGM which

further has been allocated to each LHP/SHP in the ratio of their installed capacity.

A copy of allocation sheet of additional capitalization for the FY2014-15 is annexed here and

marked as Annexure-3.

1.3.9. The Petitioner respectfully prays that the additional capital expenditure incurred/ accrued

for FY 2014-15 as detailed above in Table 5 may kindly be approved.

1.4. Debt Equity Ratio

1.4.1. In accordance with the Regulation 26 (2) of Tariff Regulations 2011, normative debt-equity

ratio of 70:30 has been considered for True-up of FY2014-15. This normative debt-equity

ratio has been considered on GFA as on January 2000 and additional capitalisation incurred

till respective financial year.

1.5. Return on Equity Ratio

1.5.1. It is respectfully submitted that petitioner has computed return on equity on opening equity for

each financial year as considered by the Hon’ble Commission in its earlier tariff orders.

1.5.2. In accordance with Opening GFA of Rs. 7.19 crores as on January 2000, equity amount has

been calculated as in FY 2000. Further, after taking into account normative equity

percentage of 30% on additional capitalization and opening GFA as approved by the

Hon’ble Commission till 2013-14, the opening equity for FY2014-15 is calculated as Rs.

2.69 Crores. Based on the Additional Capitalisation occurred in FY2014-15 as explained in

the section 1.2 the equity base is increasing at a rate of 30% of additional capitalisation in

each year from FY 2008-09 onwards. In accordance with Tariff Regulations 2011, 15.50%

post tax Return on Equity has been adopted for Khatima HEP. The resultant returns are as

follows:

Table 6 Return on Equity for True Up Years (Rs. Crores)

Year 2014-15

(Actual) 2015-16 (RE)

Opening Equity 2.69 14.86

Addition 12.17 10.80

Closing Equity 14.87 25.66

Average Equity 8.78 20.26

RoE rate 15.50% 15.50%

RoE 1.36 3.14

Chapter1: Truing Up of FY2014-15 and Annual Performance Review of FY2015-16

1.5.3. It is respectfully prayed that the Return on Equity proposed in accordance as per table

6for FY2014-15 may kindly be considered and allowed by the Hon’ble Commission.

1.6. Depreciation

1.6.1. In the Tariff Order dated April 4, 2012, Hon’ble Commission directed the Petitioner to claim

the depreciation on additional capitalisation from the next Tariff filing in accordance with the

rates specified under the Regulations for different class of assets instead of claiming it at

2.66%.

1.6.2. It is submitted that the depreciation on Additional Capitalisation from FY 2001-02 onwards has

been computed based on the rates specified under the Tariff Regulations 2004 and Tariff

Regulations 2011 as applicable for relevant year.

1.6.3. As per regulation 29 (6) of the Tariff Regulations 2011, the depreciation for first 12 years of

plant operation after CoD are calculated by depreciating the difference between the

cumulative depreciation recovered so far and the depreciation as per the rates specified in the

regulation.

‟29 (6) In case of the existing projects, the balance depreciable value as on 01.04.2013 shall

be worked out by deducting the cumulative depreciation as admitted by the Commission upto

31.03.2013, from the gross depreciable value of the assets. The difference between the

cumulative depreciation recovered and the depreciation so arrived at by applying the

depreciation rates as specified in these Regulations corresponding to 12 years shall be spread

over the remaining period upto 12 years. The remaining depreciable value as on 31st March

of the year closing after a period of 12 years from the date of commercial operation shall be

spread over the balance life.‟

1.6.4. The following rates have been considered for the purpose of calculating depreciation:

On Opening GFA – No Depreciation is claimed since 90% depreciation has already been

recovered.

On Additional Capitalisation from FY 2001-02 to FY 2014-15 onwards: Rates of

depreciation are as under:

Table 7 Rates of Depreciation (Tariff Regulation 2011)

Component Rates

Land 0.00%

Building 3.34%

Major Civil works 5.28%

Plant & Machinery 5.28%

Vehicles 9.50%

Furniture & Fixture 6.33%

Office Equipment 6.33%

Chapter1: Truing Up of FY2014-15 and Annual Performance Review of FY2015-16

Table 8 Depreciation for FY2014-15 on additional capitalisation (Rs. crore)

Component FY2014-15 (actual) FY2015-16 (RE)

Land 0.00 0.00

Building 0.01 0.00

Major Civil works 0.00 -0.08

Plant & Machinery 0.07 2.30

Vehicles 0.00 0.00

Furniture & Fixture 0.01 0.01

Office Equipment 0.03 0.02

Total 0.11 2.25

Total including Dep. On

Opening GFA

- -

Total 0.11 2.25

1.6.5. It is respectfully prayed that the depreciation proposed in accordance with above table for

the FY2014-15may kindly be considered and allowed by the Hon’ble Commission.

1.7. Interest on loan capital

1.7.1. It is respectfully submitted that in accordance with the earlier tariff orders of the Hon’ble

Commission, for the purpose of calculation of interest on loan, normative debt been

considered as 70% of additional capitalisation only.

1.7.2. The interest on normative loan has been calculated as under:

Table 9 Interest on Loan Capital for truing up (Rs. Crore)

1.8. FY2014-15 (actual) FY2015-16 (RE)

Opening Debt 0.54 29.06

Addition 28.40 25.19

Repayment 0.11 2.25

Closing Debt 28.84 52.00

Average Debt 14.69 40.53

Rate of Interest (%) 12.25% 12.25%

Interest on Loan 1.80 4.97

Chapter1: Truing Up of FY2014-15 and Annual Performance Review of FY2015-16

1.8.1. Rate of interest for normative loans forKhatima HEP is assumed to be same as weighted

average rate of all the loans forKhatimaHEPfor year 2014-15. A copy of working sheet of

calculation of interest rate along with details of Loans is annexed here and marked as

Annexure-4.

1.8.2. It is respectfully prayed that the Interest on Loan proposed in accordance with table 9 for

the FY2014-15 may kindly be considered and allowed by the Hon’ble Commission.

1.9. O&M expenses

1.9.1. In accordance to the Regulation 31(1) of Regulations 2011 regarding Operation and

Maintenance (O&M) expenses

Operation and Maintenance or O&M expenses‟ shall comprise of expenses incurred on

manpower, repair & maintenance (R&M) and administrative and general expenses, including

insurance expenses.

1.9.2. The O&M expenses approved by the commission for FY2014-15, actuals for FY2014-15 and

the projections for FY2015-16 have been computed as under:

Table 10Actual O&M expenses for truing up years (in Rs. Crore)

Components/F

Y

2014-15

(Approved)

2014-15

(Actual)

2015-16 (RE)

Employee

Expenses

8.53 9.88 11.76

R&M Expenses 2.76 2.90 3.35

A&G Expenses 0.53 1.24 1.30

O&M Expenses 11.82 14.01 16.41

1.9.3. It is respectfully submitted that O & M expenses for the FY2014-15 have been considered as

per the audited accounts. The components of total O&M expenses have been considered as

per plant wise balance sheet prepared by the petitioner as per the Hon’ble Commission

directive in the section 5.5.2 of the tariff order dated April 10,2014. The plant wise balance

sheet is annexed here and marked as Annexure-5

1.9.4. In accordance with Regulation 15 of UERC Tariff Regulations 2011, the sharing of gains and

losses on account of controllable factors for the financial year FY2014-15 is to be done as

follows:

(1) The approved aggregate gain to the applicant on account of controllable factors shall

be dealt with in the following manner:

(a) 20% of such gain shall be passed on as rebate in tariffs over such period as may be

specified in the Order of the Commission

(b) The balance amount of gain may be utilized at the discretion of the Applicant

Chapter1: Truing Up of FY2014-15 and Annual Performance Review of FY2015-16

(2) The approved aggregate loss to the applicant on account of controllable factors shall

be dealt with in the following manner:

(a) 25% of the amount of such loss shall be allowed by the Commission to be

recovered through tariffs over such period as may be specified in the Order of the

Commission under;

(b) The balance amount of loss shall be absorbed by the Applicant

The claimed O&M expenses for the FY 2014-15 has been derived as per the regulation 15

of Tariff Regulations 2011 and has been tabulated below:

Table 11 Sharing of gains and losses of O&M expenses for FY 2014-15

Expense Unit

Approved as

per tariff

order dated

10.04.2015

Actual as

per audited

accounts

Gain or loss on

account of

controllable

factors

Utility’s

Share of

Gain/loss

Claimed

for true-

up as per

regulation

Employee

Cost

Rs.

Crore 8.53 9.88 (1.35) 0.34 8.87

R&M Cost Rs.

Crore 2.76 2.90 (0.14) 0.04 2.80

A&G Cost Rs.

Crore 0.53 1.24 (0.71) 0.18 0.71

Total Rs.

Crore 11.82 14.01 (2.19) 0.55 12.37

1.9.5. It may be noted that the petitioner has considered employee expense as controllable factor as

per Section 12(6) of UERC Tariff Regulations 2011. However, the petitioner respectfully

prays to the Hon’ble Commission that employee expense is beyond the control of, and could

not be mitigated by the petitioner, hence may kindly allowed to be treated as an uncontrollable

factor.

1.9.6. The O&M Expenses for 2015-16 have been projected in accordance with the Regulation 48

(2d). For the purpose of calculation of O&M, FY 2014-15 has been considered as the base

year.

1.9.7. The CPI Inflation and WPI Inflation used for the escalation of Employee Cost and R&M,

A&G cost respectively is as follows:

Table 12CPI and WPI Inflation

Years CPI Inflation WPI Inflation

FY 2012-13 10.44% 7.35%

FY 2013-14 9.68% 5.98%

FY 2014-15 6.29% 2.00%

Average Inflation 8.80% 5.11%

Chapter1: Truing Up of FY2014-15 and Annual Performance Review of FY2015-16

1.9.8. The K factor has been computed by dividing average R&M for last three years (FY 2012-13 to

FY 2014-15) by average of last three years opening GFA (FY 2012-13 to FY 2014-15)

1.9.9. The Growth Factor for the nth year (Gn) has been calculated on the basis of the recruitment plan

of the petitioner. The recruitment plan of the petitioner has been annexed here as Annexure 8.

Accordingly the Growth Factor is tabulated below:

Table 13Growth Factor (Gn)

Year Growth Factor (Gn)

FY 2015-16 9.45%

1.9.10. It is respectfully prayed that the Operation and Maintenance Expenses proposed in

accordance with Table 10for the FY 2014-15 may kindly be considered and allowed by

the Hon’ble Commission.

1.10. Interest on working capital

1.10.1. In accordance with the norms established under Tariff Regulations 2011, the components of

working capital are as follows:

O&M expense at one month of projected expenses

Maintenance spares @15% of operation and maintenance expenses

Receivables at two months of annual fixed charge

1.10.2. In accordance to the Regulation 34(1)(c) of Regulations 2011, which provides the norms for

the calculation of rate of interest on working capital for the Hydro Generating Stations, the

computation shall be on the basis of following factors:

“Rate of interest on working capital shall be on normative basis and shall be equal to the State

Bank Advance Rate (SBAR) of State Bank of India as on the date on which the application for

determination of tariff is made.”

1.10.3. Hon’ble Commission, in the previous Tariff Orders dated21/10/09, 05/04/10, 10/05/11,

04/04/2012, 06/05/2013, 10/04/2014 and 11/04/15, pursuant to the request of the Petitioner,

while estimating the interest on working capital, had considered the prevailing PLR, so as

to effectively capture the existing market conditions. Accordingly, in the present Tariff

Petition also, the Petitioner has considered prevailing SBI PLR as on April 1st of

respective financial year (copy enclosed in Annexure-7). The details of working capital

and interest thereon for are given hereunder:

Chapter1: Truing Up of FY2014-15 and Annual Performance Review of FY2015-16

Table 14 Interest on Working Capital for Truing Up (Rs. Crore)

1.10.4.

Components 2014-15 (actual) 2015-16 (RE)

1 month O&M

expense

1.17 1.37

15% spares 2.10 2.46

2 month receivables 2.51 4.43

Total Working Capital 5.78 8.26

Rate of interest (%) 14.75% 14.75%

Interest on Working

Capital

0.85 1.22

1.10.5. It is respectfully prayed that the Interest on Working Capitalproposed in

accordance with above table for the FY 2014-15 may kindly be considered and

allowed by the Hon’ble Commission.

1.11. Non-Tariff Income

1.11.1. In accordance to the Regulation 47 of Regulations 2011 the Non-Tariff Income for any

Generating Station is to be considered as:

“The amount of non-tariff income relating to the Generation Business as approved by the

Commission shall be deducted from the Annual Fixed Charges in determining the Net

Annual Fixed Charges of the Generation Company.

Provided that the Generation Company shall submit full details of its forecast of nontariff

income to the Commission in such form as may be stipulated by the Commission from time

to time.”

1.11.2. The Non-Tariff income for the FY 2014-15 as claimed for true up of tariff is based on

audited accounts along with adjustments on account of excess provision for liabilities

written back. The detailed sheet showing calculation of adjustments on account of excess

provision is annexed here and marked as Annexure 8

1.11.3. The Non-Tariff income for the revised estimates for FY 2015-16 is based on the average

of actual Non-Tariff income for the previous two financial years FY 2013-14 and FY

2014-15

1.11.4. The non-tariff income earned by the Petitioner has been deducted from the Annual Fixed

Charges to arrive at net Annual Fixed Charges.

Chapter1: Truing Up of FY2014-15 and Annual Performance Review of FY2015-16

Table 15Non Tariff Income for truing up (in Rs. Core)

Unit Approved figures

for FY2014-15

Actual figures for

FY2014-15

FY2015-16 (RE)

Non Tariff

Income

Rs. Crore 0.35 1.42 1.40

1.12. Design Energy

1.12.1. It is respectfully submitted that in the previous Tariff Orders, Commission had determined the

Design Energy and saleable energy of 194.05 MU and192.69 MU respectively for the

Khatima HEP in its earlier orders. The petitioner has adopted the aforesaid design energy and

saleable energy for Khatima HEP

1.13. Truing up on account of controllable factors for FY2014-15

1.13.1. The gross and net Annual Fixed Charges for Khatima power plant for the truing up years

is provided in the table below:

Table 16 Approved and Actual Annual Fixed Charges for FY2014-15

Components/FY Approved figures

for FY2014-15

Actual figures

for FY2014-15

Interest on Loan 0.03 1.80

RoE 0.42 1.36

Depreciation 0.25 0.11

O&M Expenses 11.82 12.37

Interest on Working

Capital

0.72 0.85

Less: Non-Tariff Income 0.35 1.42

Net Annual Fixed

Charge

12.89 15.07

Gain or loss to utility

(2.18)

Chapter1: Truing Up of FY2014-15 and Annual Performance Review of FY2015-16

1.13.2. Therefore it is respectfully submitted that the Hon’ble Commission may kindly consider

and allow the aforesaid Annual Fixed Charges which has been computed strictly in

accordance to the Tariff Regulation of 2011.

1.13.3. It is respectfully prayed to the Hon’ble Commission that the difference between

approvedactual AFC of FY2014-15 along with its carrying cost may kindly be approved

1.14. Truing up on account of NAPAF for FY2014-15

1.14.1. The capacity charge approved by the Commission is based on the approved design energy

calculated using NAPAF. The actual capacity charge collected is based on the actual

generation units for the respective year. The gain or loss to the utility on account of this

difference between the approved capacity charge and the actual capacity charge would be

recovered or paid back in accordance with Regulation 15 of UERC Tariff Regulations

2011.

(1) The approved aggregate gain to the applicant on account of controllable factors shall

be dealt with in the following manner:

(a) 20% of such gain shall be passed on as rebate in tariffs over such period as may be

specified in the Order of the Commission

(b) The balance amount of gain may be utilized at the discretion of the Applicant

(2) The approved aggregate loss to the applicant on account of controllable factors shall

be dealt with in the following manner:

(a) 25% of the amount of such loss shall be allowed by the Commission to be

recovered through tariffs over such period as may be specified in the Order of the

Commission under;

(b) The balance amount of loss shall be absorbed by the Applicant

1.14.2. The Capacity Charge approved by the Commission for FY2014-15 in the tariff order

dated April 10, 2014, the actual Capacity Charge recovered for FY2014-15 and the

sharing of gain or loss is as under:

Table 17 Approved and actual capacity charge collected for FY2014-15

Amount (in Rs. Crore)

Approved Capacity Charge6.45

Actual Capacity Charge recovered1.91

Gain or (Loss) to utility(4.54)

Utility's share 1.13

Chapter1: Truing Up of FY2014-15 and Annual Performance Review of FY2015-16

1.14.3. It is respectfully submitted that in case of Khatima HEP the gain along with

carrying cost for FY 2014-15 and for FY 2015-16, may kindly be approved as per

the above table.

1.15. Impact of truing up for FY2014-15

1.15.1. As presented in section 1.11 and 1.12 of this petition, the gain or loss to the utility would

be added or subtracted from the annual fixed charge of the first year of next control

period. Carrying cost on the gain or loss is calculated using the SBI PLR rate of 14.05%

as follows:

Table 18 Impact of truing-up for 2014-15

2015 2016

Opening Gain or Loss of AFC - 3.56

Addition during the year on

account of controllable factors

2.18 -

Addition during the year on

account of NAPAF

1.13 -

Closing Gain or Loss of AFC 3.32 3.56

Carrying Cost 0.24 0.53

Total Closing Gain or Loss of

AFC

3.56 4.09

1.15.2. It is respectfully submitted that in case of Khatima HEP this gain along with the

carrying cost for FY 2014-15 and 2015-16, may kindly be approved.

1.16. Income Tax

It is respectfully submitted that as per Regulation 35 of Tariff Regulations,2011:

“Income Tax, if any, on the income stream of the regulated business of Generating Companies,

Transmission Licensees, Distribution Licensees and SLDC shall be reimbursed to the Generating

Companies, Transmission Licensees, Distribution Licensees and SLDC as per actual income tax paid,

based on the documentary evidence submitted at the time of truing up of each year of the Control

Period, subject to the prudence check.”

In view of the above, it is respectfully submitted that income tax on actual basis may kindly be

allowed to be recovered from the beneficiaries

Chapter1: Truing Up of FY2014-15 and Annual Performance Review of FY2015-16

1.17. Claim of UPCL relating to electricity charges of the electricity

consumed by employees of UJVN Limited

1.17.1. Working Employees of UJVN Ltd, those residing outside the power station colonies of

UJVN Ltd and pensioners/family pensioners residing in the state of Uttarakhand, are

availing electricity facility from the mains of UPCL since November 2001.

In regard to supply of electricity to the employees/pensioners/family pensioners of UJVN

, UPCL has raised a bill of Rs 62.25 Crores vide letter no 8116 dated 21/09/2015 for the

period starting from November 2001 to March 2015. However UJVN Ltd does not agree

with the methodology adopted by UPCL regarding determination no of

employees/pensioners/family pensioners, average consumption per month per consumer,

and rate of per unit consumption. In this regard Petitioner has asked for clarification from

UPCL vide letter no 5906 dated 09/10/2015. The letters dated 21.09.2015 and dated

09.10.2015 are placed at Annexure- 10

Here, it is pertinent to inform that the Hon’ble commission in its order dated 27.04.2015

In the matter of dispute between UJVN Ltd and Uttarakhand Power Corporation relating

to payment has ordered as below:

“3. The claim of the Respondent relating to electricity charges of the electricity consumed

by Petitioner‟s employees, as and when these are firmed up and accepted by the

Petitioner be posed to the Commission and then the Commission will set mechanism for

their recovery/adjustment out of ongoing monthly installment decided above”

Moreover, UPCL has made suo-moto adjustment of Rs.30.125 Crore for above electricity

bill in the three monthly installments till Nov 2015 against the true up amount provided to

UJVN Ltd in tariff order 2015-16. It is noteworthy that the facility of electricity supply to

the employees/pensioners/family pensioners was provided by the erstwhile Uttar Pradesh

Electricity Board (UPSEB). After unbundling of UPSEB the facility has been continued

by UJVN Ltd.

1.17.2. In view of all above, the Petitioner humbly prays the Hon’ble Commission to direct

UPCL to adhere to the earlier directive of Hon’ble Commission as mentioned above

and not to adjust the above amount unilaterally.

Tariff determination for FY2016-17, FY2017-18 and FY2018-19

2. Tariff determination for FY2016-17, FY2017-18 and FY2018-

19

2.1. Norms of Operation

The norms specified by the Hon’ble Commission as applicable for the Khatima power station are as

follows:

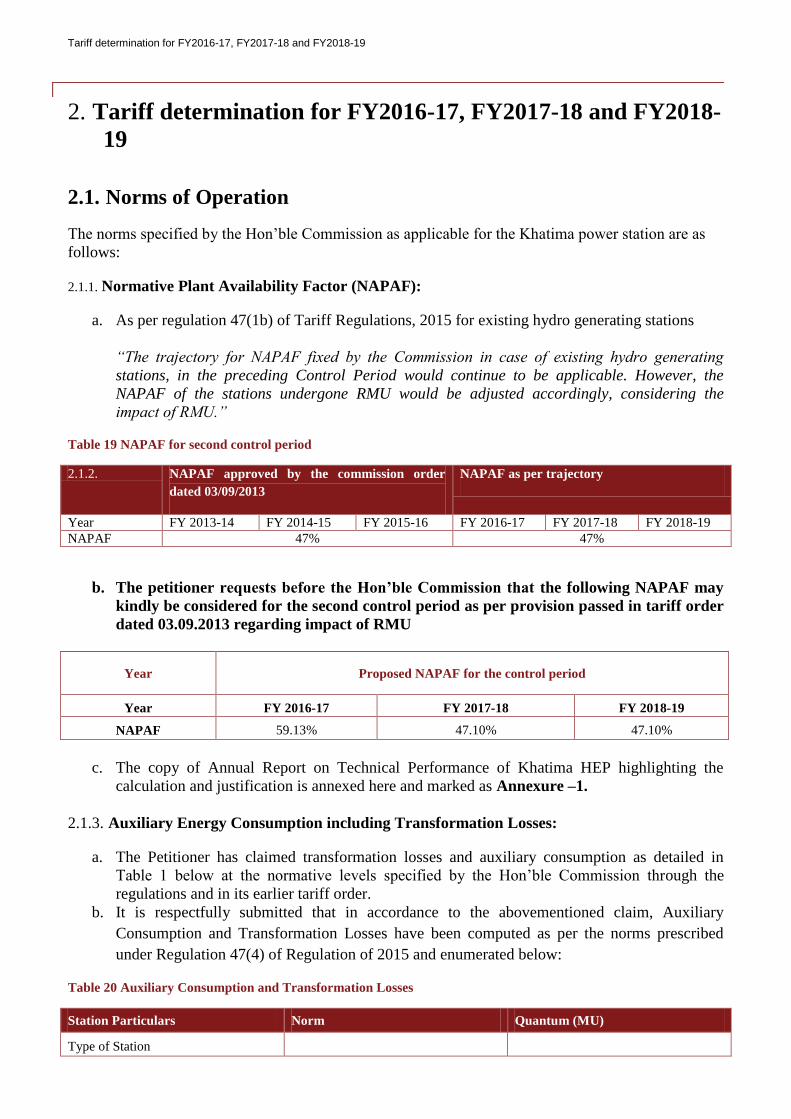

2.1.1. Normative Plant Availability Factor (NAPAF):

a. As per regulation 47(1b) of Tariff Regulations, 2015 for existing hydro generating stations

“The trajectory for NAPAF fixed by the Commission in case of existing hydro generating

stations, in the preceding Control Period would continue to be applicable. However, the

NAPAF of the stations undergone RMU would be adjusted accordingly, considering the

impact of RMU.”

Table 19 NAPAF for second control period

2.1.2. NAPAF approved by the commission order

dated 03/09/2013

NAPAF as per trajectory

Year FY 2013-14 FY 2014-15 FY 2015-16 FY 2016-17 FY 2017-18 FY 2018-19

NAPAF 47% 47%

b. The petitioner requests before the Hon’ble Commission that the following NAPAF may

kindly be considered for the second control period as per provision passed in tariff order

dated 03.09.2013 regarding impact of RMU

Year Proposed NAPAF for the control period

Year FY 2016-17 FY 2017-18 FY 2018-19

NAPAF 59.13% 47.10% 47.10%

c. The copy of Annual Report on Technical Performance of Khatima HEP highlighting the

calculation and justification is annexed here and marked as Annexure –1.

2.1.3. Auxiliary Energy Consumption including Transformation Losses:

a. The Petitioner has claimed transformation losses and auxiliary consumption as detailed in

Table 1 below at the normative levels specified by the Hon’ble Commission through the

regulations and in its earlier tariff order.

b. It is respectfully submitted that in accordance to the abovementioned claim, Auxiliary

Consumption and Transformation Losses have been computed as per the norms prescribed

under Regulation 47(4) of Regulation of 2015 and enumerated below:

Table 20 Auxiliary Consumption and Transformation Losses

Station Particulars Norm Quantum (MU)

Type of Station

Tariff determination for FY2016-17, FY2017-18 and FY2018-19

Station Particulars Norm Quantum (MU)

a) Surface Yes

b) Underground No

Type of excitation

a) Rotating exciters on generator Yes

b) Static excitation No

Auxiliary Consumption including

Transformation losses

(As % of Total Generation)

0.7% 1.36

2.2. Additional Capitalisation

2.2.1. It is pertinent to note here that in order to ensure efficiency, safety and continuous

operation of the plants, the proposed additional capitalization has to be incurred. It is also

to be noted that the additional capital expenditure incurred thereto was in accordance to

Regulation 22 (2e) of the UERC (Terms and Conditions of determination of Multi Year

Tariff) Regulations, 2015.

„22 (2e) Any additional capital expenditure which has become necessary for efficient

operation of generating station or transmission system as the case may be. The claim

shall be substantiated with the technical justification duly supported by the documentary

evidence like test results carried out by an independent agency in case of deterioration of

assets, report of an independent agency in case of damage caused by natural calamities,

obsolescence of technology, up-gradation of capacity for the technical reason such as

increase in fault level‟

2.2.2. The projections of the additional capitalisation for FY2016-17, FY2017-18 and FY2018-

19 for Khatima HEP are as detailed below:

Table 21Additional Capitalisation for the Control Period

Financial Year FY2016-17 FY2017-18 FY2018-19

Land 0.00 0.00 0.00

Building 0.30 0.30 0.15

Major Civil Works 0.00 0.00 0.00

Plant & Machinery 50.20 12.15 0.15

Vehicles 0.01 0.01 0.01

Furniture & Fixture 0.01 0.01 0.01

Office Equipment 0.03 0.03 0.00

Total 50.54 12.49 0.32

Tariff determination for FY2016-17, FY2017-18 and FY2018-19

2.2.3. The details of the major works as part of additional capitalization for Khatima HEP has

been detailed in the Business Plan submitted along with this petition.

2.2.4. Therefore it is respectfully prayed that the Additional Capitalizationfor FY 2016-17

to 2018-18 as proposed in the above table 21 may kindly be allowed by the Hon’ble

Commission.

2.3. Return on Equity

2.3.1. For proposed tariff from FY 2016-17 to FY 2018-19, Section 26(2) of Tariff Regulations 2015

have been considered for calculating RoE. Section 26(2) is reproduced as under:

“Return on equity shall be computed on at the base rate of 15.5% for thermal generating

stations, transmission licensee, SLDC and run of the river hydro generating station and at the

base rate of 16.50% for the storage type hydro generating stations and run of river generating

station with pondage and distribution licensee on a post-tax basis.”

2.3.2. It is respectfully submitted that the return on equity computed by the petitioner for Khatima HEP

is in accordance with the aforesaid regulation.

Table 22 Calculation of RoE for FY2016-17 to FY2018-19

Year 2016-17 2017-18 2018-19

Opening Equity 25.66 40.82 44.57

Net Addition 15.16 3.75 0.10

Closing Equity 40.82 44.57 44.67

Average Equity 33.24 42.70 44.62

RoE Rate 15.50% 15.50% 15.50%

RoE 5.15 6.62 6.92

2.3.3. It is respectfully prayed that the Return on Equity proposed in accordance with

above table for the FY2016-17, FY2017-18 and FY2018-19 may kindly be considered

and allowed by the Hon’ble Commission.

2.4. Depreciation

2.4.1. Relevant provisions pertaining to depreciation under Regulation 28 of Tariff Regulation

2015 are reproduced as under –

“The value base for the purpose of depreciation shall be the capital cost of the asset

admitted by the Commission.

(1) Provided that no depreciation shall be allowed on assets funded through Consumer

Contribution and Capital Subsidies/Grants.

(2) The salvage value of the asset shall be considered as 10% and depreciation shall be

allowed up to maximum of 90% of the capital cost of the asset.

Tariff determination for FY2016-17, FY2017-18 and FY2018-19

…….

(4) Depreciation shall be calculated annually based on Straight Line Method and at rates

specified in Appendix - II to these Regulations.

Provided that, the remaining depreciable value as on 31st March of the year closing after

a period of 12 years from the date of commercial operation shall be spread over the

balance useful life of the assets.

(5) In case of the existing projects, the balance depreciable value as on 01.04.2016 shall

be worked out by deducting the cumulative depreciation as admitted by the Commission

upto 31.03.2016, from the gross depreciable value of the assets. The difference between

the cumulative depreciation recovered and the depreciation so arrived at by applying the

depreciation rates as specified in these Regulations corresponding to 12 years shall be

spread over the remaining period upto 12 years. The remaining depreciable value as on

31st March of the year closing after a period of 12 years from the date of commercial

operation shall be spread over the balance life.”

2.4.2. In accordance with above provisions and rates provided in Tariff Regulations 2015,

depreciation has been calculated based on rates tabulated as under:

Table 23 Rates of Depreciation as per Tariff Regulations 2015

Component Rates – First 12 years Rates – Balance Life

Land 0.00% 0.00%

Building 3.34% 2.61%

Major Civil Works 5.28% 2.61%

Plant & Machinery 5.28% 1.59%

Vehicles 9.50% 0.00%

Furniture & fixture 6.33% 1.05%

Office Equipment 6.33% 1.05%

2.4.3. Tariff regulations 2015 are applicable from 1st April 2016 onwards. Hence till FY2015-16,

Tariff Regulations 2011 are applicable. Tariff regulations 2011 in turn are applicable

from 1st April 2013. Hence, till FY 2012-13, Petitioner has calculated depreciation based

on Tariff Regulations 2004.

2.4.4. Hence % of depreciation on Additional Capitalisation from FY 2013-14 onwards needs to

be reconciled with the % of depreciation for the 12 years as per Tariff Regulations 2011

and Tariff regulations 2004.

Table 24 Proposed Depreciation % for FY2016-17 to FY2018-19

Component 2016-17 2017-18 2018-19

Land (Ownership) 3.34% 3.34% 3.34%

Tariff determination for FY2016-17, FY2017-18 and FY2018-19

Component 2016-17 2017-18 2018-19

Building 5.28% 5.28% 5.28%

Major Civil Works 5.28% 5.28% 5.28%

Plant & Machinery 9.50% 9.50% 9.50%

Vehicles 6.33% 6.33% 6.33%

Furniture & fixture 6.33% 6.33% 6.33%

Office Equipment 3.34% 3.34% 3.34%

Table 25Proposed depreciation on additional capitalization from FY2016-17 to FY2018-19 (in Rs. Crore)

Component 2016-17 2017-18 2018-19

Land (Ownership) 0.00 0.00 0.00

Building 0.00 0.01 0.02

Major Civil Works -0.08 -0.08 -0.08

Plant & Machinery 4.19 6.84 7.48

Vehicles 0.00 0.00 0.00

Furniture & fixture 0.01 0.01 0.01

Office Equipment 0.02 0.02 0.02

Total 4.15 6.81 7.46

Table 26 Proposed depreciation on GFA from FY2016-17 to FY2018-19 (in Rs. Crore)

Component 2016-17 2017-18 2018-19

GFA 0 0 0

2.4.5. It is respectfully prayed that the depreciation proposed in accordance with above

table for the FY 2016-17, FY 2017-18 and FY 2018-19 may kindly be considered and

allowed by the Hon’ble Commission.

2.5. Interest on Loan Capital

2.5.1. It is submitted that in terms of the directives of the Hon’ble Commission, interest on

normative debt has been considered on the value equivalent to 70% of additional

capitalisation only.

2.5.2. Rate of interest for normative loans for Khatima HEP is assumed to be same as weighted

average rate of loans for all loans for Khatima HEP for year 2014-15. A copy of working

sheet of calculation of interest rate along with details of loans is annexed here and marked as

Annexure-4.

Accordingly, the interest on normative debt has been calculated as under:

Tariff determination for FY2016-17, FY2017-18 and FY2018-19

Table 27 Interest on Loan for FY 2016-17, 2017-18 and 2018-19

2016-17 2017-18 2018-19

Opening Balance 52.00 83.24 85.17

Addition 35.38 8.75 0.22

Repayment 4.15 6.81 7.46

Closing Balance 83.24 85.17 77.94

Average Debt 67.62 84.20 81.56

Rate of Interest 12.25% 12.25% 12.25%

Interest on Loan 8.28 10.32 9.99

2.5.3. It is respectfully submitted that the Hon’ble Commission may kindly consider and

allow the aforesaid interest on Normative Loan.

2.6. O&M Expenses

2.6.1. In accordance with Regulation 3(55) of Tariff Regulations 2015 –

“ „Operation and maintenance expenses‟ or „O&M expenses‟ means the expenditure

incurred on operation and maintenance of the Company or of a particular project and

includes the expenditure on manpower, repairs, spares, consumables, insurance and

overheads but excludes fuel expenses and water charges;”

2.6.2. In accordance with Regulation 48(2d) of Tariff Regulations 2015, for Generating Stations in

operation for more than five years in Base Year -

„Post determination of base O&M Expenses for the base year, i.e. FY 2014-15, the O&M

expenses for the nth year and also for the year immediately preceding the Control Period,

i.e. 2015-16 shall be approved based on the formula given below:-

O&Mn = R&Mn + EMPn + A&Gn

Where –

O&Mn – Operation and Maintenance expenses for the nth year;

EMPn – Employee Costs for the nth year;

R&Mn – Repair and Maintenance Costs for the nth year;

A&Gn – Administrative and General Costs for the nth year;

The above components shall be computed in the manner specified below:

EMPn = (EMPn-1) x (1+Gn) x (1+CPIinflation)

R&Mn = K x (GFA n-1 ) x (1+WPIinflation) and

A&Gn = (A&Gn-1) x (1+WPIinflation)+ Provision

Where -

EMPn-1 – Employee Costs for the (n-1)th year;

A&G n-1 – Administrative and General Costs for the (n-1)th year;

Tariff determination for FY2016-17, FY2017-18 and FY2018-19

Provision: Cost for initiatives or other one-time expenses as proposed by the

Generating Company and approved by the Commission after prudence check.‟

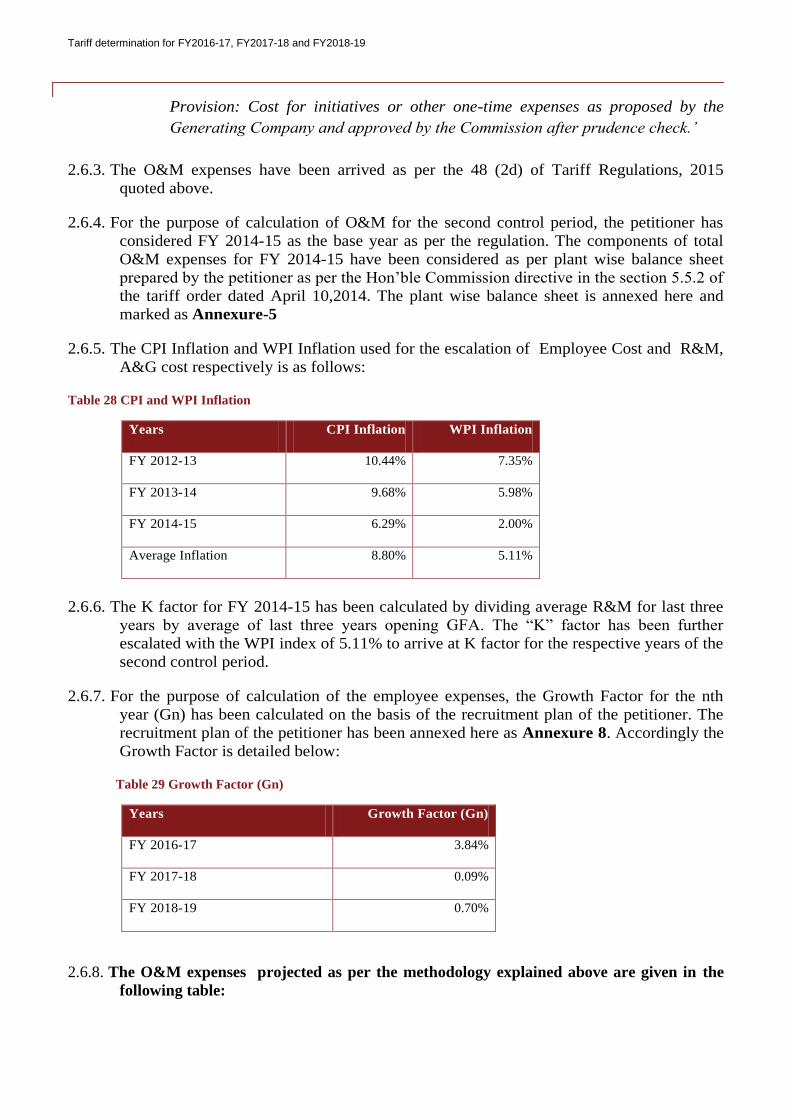

2.6.3. The O&M expenses have been arrived as per the 48 (2d) of Tariff Regulations, 2015

quoted above.

2.6.4. For the purpose of calculation of O&M for the second control period, the petitioner has

considered FY 2014-15 as the base year as per the regulation. The components of total

O&M expenses for FY 2014-15 have been considered as per plant wise balance sheet

prepared by the petitioner as per the Hon’ble Commission directive in the section 5.5.2 of

the tariff order dated April 10,2014. The plant wise balance sheet is annexed here and

marked as Annexure-5

2.6.5. The CPI Inflation and WPI Inflation used for the escalation of Employee Cost and R&M,

A&G cost respectively is as follows:

Table 28 CPI and WPI Inflation

Years CPI Inflation WPI Inflation

FY 2012-13 10.44% 7.35%

FY 2013-14 9.68% 5.98%

FY 2014-15 6.29% 2.00%

Average Inflation 8.80% 5.11%

2.6.6. The K factor for FY 2014-15 has been calculated by dividing average R&M for last three

years by average of last three years opening GFA. The “K” factor has been further

escalated with the WPI index of 5.11% to arrive at K factor for the respective years of the

second control period.

2.6.7. For the purpose of calculation of the employee expenses, the Growth Factor for the nth

year (Gn) has been calculated on the basis of the recruitment plan of the petitioner. The

recruitment plan of the petitioner has been annexed here as Annexure 8. Accordingly the

Growth Factor is detailed below:

Table 29 Growth Factor (Gn)

Years Growth Factor (Gn)

FY 2016-17 3.84%

FY 2017-18 0.09%

FY 2018-19 0.70%

2.6.8. The O&M expenses projected as per the methodology explained above are given in the

following table:

Tariff determination for FY2016-17, FY2017-18 and FY2018-19

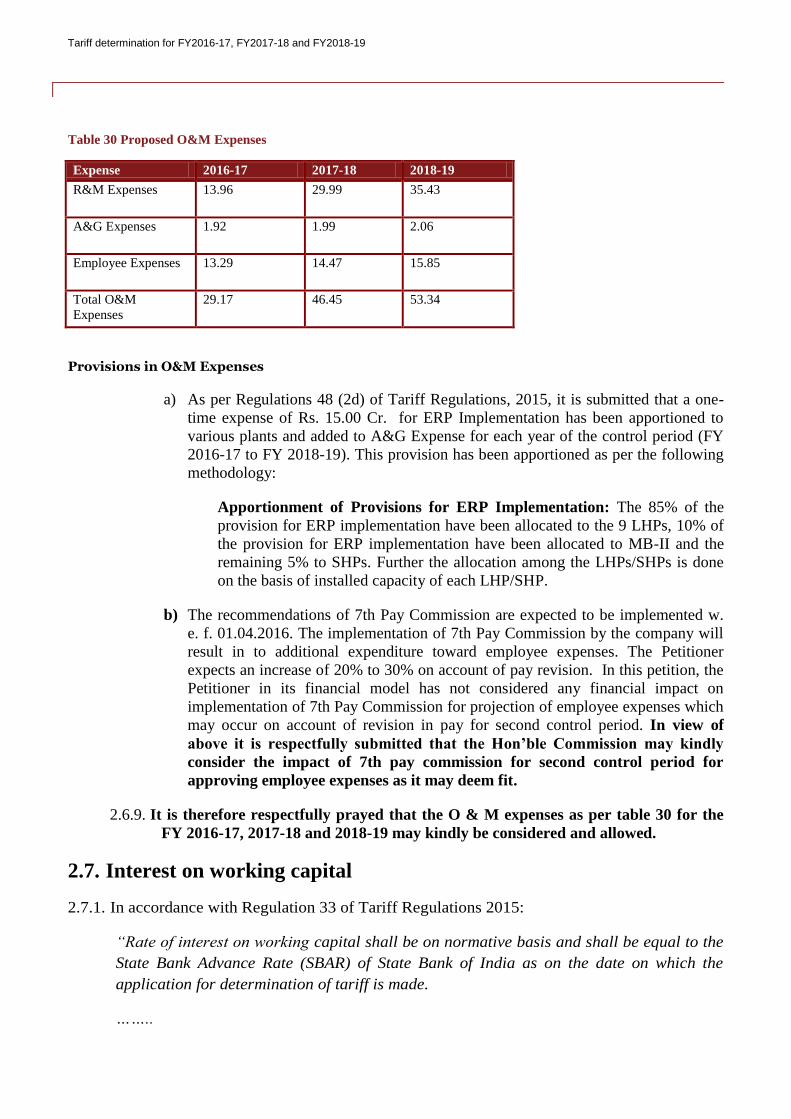

Table 30 Proposed O&M Expenses

Expense 2016-17 2017-18 2018-19

R&M Expenses 13.96 29.99 35.43

A&G Expenses 1.92 1.99 2.06

Employee Expenses 13.29 14.47 15.85

Total O&M

Expenses

29.17 46.45 53.34

Provisions in O&M Expenses

a) As per Regulations 48 (2d) of Tariff Regulations, 2015, it is submitted that a one-

time expense of Rs. 15.00 Cr. for ERP Implementation has been apportioned to

various plants and added to A&G Expense for each year of the control period (FY

2016-17 to FY 2018-19). This provision has been apportioned as per the following

methodology:

Apportionment of Provisions for ERP Implementation: The 85% of the

provision for ERP implementation have been allocated to the 9 LHPs, 10% of

the provision for ERP implementation have been allocated to MB-II and the

remaining 5% to SHPs. Further the allocation among the LHPs/SHPs is done

on the basis of installed capacity of each LHP/SHP.

b) The recommendations of 7th Pay Commission are expected to be implemented w.

e. f. 01.04.2016. The implementation of 7th Pay Commission by the company will

result in to additional expenditure toward employee expenses. The Petitioner

expects an increase of 20% to 30% on account of pay revision. In this petition, the

Petitioner in its financial model has not considered any financial impact on

implementation of 7th Pay Commission for projection of employee expenses which

may occur on account of revision in pay for second control period. In view of

above it is respectfully submitted that the Hon’ble Commission may kindly

consider the impact of 7th pay commission for second control period for

approving employee expenses as it may deem fit.

2.6.9. It is therefore respectfully prayed that the O & M expenses as per table 30 for the

FY 2016-17, 2017-18 and 2018-19 may kindly be considered and allowed.

2.7. Interest on working capital

2.7.1. In accordance with Regulation 33 of Tariff Regulations 2015:

“Rate of interest on working capital shall be on normative basis and shall be equal to the

State Bank Advance Rate (SBAR) of State Bank of India as on the date on which the

application for determination of tariff is made.

……..

Tariff determination for FY2016-17, FY2017-18 and FY2018-19

In case of hydro power generating stations and transmission system and SLDC, the

working capital shall cover:

(i) Operation and maintenance expenses for one month

(ii) Maintenance spares @ 15% of operation and maintenance expenses

(iii) Receivables equivalent to two months of the annual fixed charges”

2.7.2. The Petitioner has considered prevailing SBI PLR as on October 1, 2015 in accordance

with regulations for the second control period (copy enclosed in Annexure-12)

Table 31 Interest on Working Capital for FY2016-17 to 2018-19

2016-17 2017-18 2018-19

One month O&M

expenses

2.43 3.87 4.45

Maintenance Spares -

15% of O&M

Expenses

4.38 6.97 8.00

2 months receivables 7.90 12.00 13.32

Total Working

Capital

14.71 22.84 25.77

Rate of Interest 14.05% 14.05% 14.05%

Interest on Working

Capital

2.07 3.21 3.62

2.7.3. It is therefore respectfully prayed that Interest on Working Capital for the FY 2016-

17, 2017-18 and 2018-19 respectively may kindly be considered and allowed as per

the above table.

2.8. Non-Tariff Income

2.8.1. In accordance to the Regulation 46 of Tariff Regulations 2015 the Non-Tariff Income for

any Generating Station is to be considered as:

“The amount of non-tariff income relating to the Generation Business as approved by the

Commission shall be deducted from the Annual Fixed Charges in determining the Net Annual

Fixed Charges of the Generating Company.

Provided that the Generation Company shall submit full details of its forecast of non tariff

income to the Commission in such form as may be stipulated by the Commission from time

to time.”

Tariff determination for FY2016-17, FY2017-18 and FY2018-19

2.8.2. The Non-Tariff income for the three financial years of control period viz. FY 2016-17,

2017-18 and 2018-19 is taken as average of actual Non-Tariff income for the financial

years FY 2013-14 and FY 2014-15.

Table 32 Non -Tariff Income for truing up (in Rs. Core)

Unit FY2016-17 FY 2017-18 FY 2018-19

Non-Tariff Income Rs. Crore 1.40 1.40 1.40

2.9. Total Fixed Charges

2.9.1. The gross and net Annual Fixed Charges for each of the tariff years for the second control

period is provided in the table below:

Table 33 Proposed Fixed Charges for FY2016-17 to 2018-19

Component 2016-17 2017-18 2018-19

Interest on Loan Capital 8.28 10.32 9.99

RoE 5.15 6.62 6.92

Depreciation 4.15 6.81 7.46

O&M Expenses 29.17 46.45 53.34

Interest on Working Capital 2.07 3.21 3.62

Less: Non Tariff Income 1.40 1.40 1.40

Total AFC (Rs. Crore)

47.42 72.01 79.93

2.9.2. In accordance with above table it is respectfully prayed to the Hon’ble Commission to

kindly consider and allow the Annual Fixed Charges for the FY2016-17, 2017-18

and 2018-19 respectively as per the above table.

2.10. Design Energy

2.10.1. It is respectfully submitted that in the previous Tariff Orders, Commission had determined the

Design Energy and saleable energy of 194.05MU and 192.69 MUrespectively for the Khatima

HEP in its earlier orders. The petitioner has adopted the aforesaid design energy and saleable

energy for Khatima HEP.

2.11. Capacity charges and Energy Charge rate

2.11.1. In accordance with the Tariff Regulations 2015, the Energy Charges and Capacity Charges are

calculated as under:

Tariff determination for FY2016-17, FY2017-18 and FY2018-19

Table 34 Capacity Charges and Energy Charge Rate

2016-17 2017-18 2018-19

Gross Design Energy 194.05 194.05 194.05

Auxiliary

Consumption&

Transformation Loss

0.70% 0.70% 0.70%

Net Primary Energy 192.69 192.69 192.69

Energy Charge 1.23 1.87 2.07

Capacity Charge 1.23 1.87 2.07

2.11.2. It is therefore respectfully prayed to the Hon’ble Commission that capacity charges

and energy chargesfor FY2016-17, 2017-18 and 2018-19 respectively may kindly be

considered and allowed as per the above table.

2.12. Income Tax

It is respectfully submitted that as per Regulation 34 of Tariff Regulations, 2015:

Income Tax, if any, on the income stream of the regulated business of Generating Companies,

Transmission Licensees, Distribution Licensees and SLDC shall be reimbursed to the Generating

Companies, Transmission Licensees, Distribution Licensees and SLDC as per actual income tax paid,

based on the documentary evidence submitted at the time of truing up of each year of the Control

Period, subject to the prudence check.

In view of the above, it is respectfully submitted that income tax on actual basis may kindly be

allowed to be recovered from the beneficiaries

2.13. Water Tax

As per the Government of Uttarakhand Order No. 2883/II-2015/01(50)/2011 dated 07 November 2015

(copy enclosed in Annexure 10), a water tax is to be paid by the generating company to the

Government of Uttarakhand along with the existing royalty and cess. The tentative calculation of the

impact of water tax on UJVN Limited has been enclosed in the Annexure11and UJVN may kindly be

allowed by the Hon’ble Commission to recover the same from the beneficiaries UPCL and HPSEB.

Status of Directives in Tariff Order Dated 4 April 2012

3. Status of Directives in Tariff Order Dated 4 April 2012

3.1. Action taken by UJVNL on directives

S. No. Directives Form of

Submiss

ion

Timelines Action to be Taken by

the Petitioner

1 Performance Improvement Measures (5.1.1):

The Commission hereby directs the Petitioner to

implement the recommendations contained in the

Report specifically with regard to manpower

deployment & rationalization and reduction in

planned maintenance days.

Report

Implemented the

recommendations

contained in the Report

specifically with regard to

manpower deployment &

rationalization and

reduction in planned

maintenance days.

2 Depreciation (5.1.2): N.A. N.A. Complied with the

directives of the Hon’ble

Commission.

3 Return on Equity (5.1.3):

The Commission again directs UJVN Ltd. that

till the time transfer scheme is finalised it should

continue to submit the updated quarterly

progress report to the Commission.

Report Quarterly

Progress

Report

Quarterly Progress Report

for the 1st& 2nd quarter

submitted vide letter dated

04.08.2015 & 23.11.2015

to the Hon’ble

Commission.

4 Utilisation of Expenses approved by the

Commission (5.2.1):

The Commission again directs UJVN Ltd. to

submit annual budget for future financial years

by 30th of April of the respective financial year.

Annual

Budget

By 30th April

of every

Financial

Year

Annual Budget for the FY

2015-16 submitted vide

letter dated 29.04.2015.

5 Colony Consumption (5.2.2) :

The Commission hereby directs the Petitioner to

install the meters for all un-metered connections

in its colonies by June 30, 2015 and submit

compliance report by July 31, 2015.

Complia

nce

Report

By July 31,

2015

Reports submitted vide

letter dated 29.07.2015 to

the Hon’ble Commission.

6 Income from electricity distribution to

Sundry Consumers (5.2.3):

The Commission further directs the Petitioner to

submit a quarterly status of the progress till the

entire handing over of distribution business is

completed.

Status

Report

Quarterly

Progress

Report

Quarterly Progress Report

for the 1st& 2nd quarter

submitted vide letters

dated 10.08.2015 &

05.10.2015 to the Hon’ble

Commission.

7 Design Energy (5.4.1):

The Commission in this regard directs the

Petitioner to pursue the above matter with

appropriate authorities to arrange the DPRs for

each of its hydro generating stations and submit

the quarterly progress report to the Commission.

Status

Report

Quarterly

Progress

Report

8 Segregation of Accounts (5.4.2):

N.A. N.A. Complied with the

directives of Hon’ble

Commission.

9 Viability/Status of RMU works (5.5):

The Commission further directs the Petitioner to

submit the report on comparison of its RMU

costs with RMU costs of other Hydel generating

stations by June 30, 2015.

Complia

nce

Report

By June 30,

2015

Status Report submitted

vide letter dated

03.07.2015 to the Hon’ble

Commission.

Status of Directives in Tariff Order Dated 4 April 2012

S. No. Directives Form of

Submiss

ion

Timelines Action to be Taken by

the Petitioner

10 Status of upcoming projects (5.5.1) :

“The Commission directs the Petitioner to

submit quarterly progress report of status of all

its upcoming projects at regular intervals”.

Report Quarterly

Progress

Report

Quarterly Progress Report

for the 1st& 2nd quarter

submitted vide letter dated

04.08.2015 & 23.11.2015

to the Hon’ble

Commission.

11 Details of Additional Capitalization for MB-II

(5.6.1):

The Commission, therefore, directs UJVN Ltd.

to submit the year wise details of actual

additional capitalisation carried out by it till FY

2014-15 for MB-II LHP alongwith the

justification of the same within 3 months of the

date of Order.

Complia

nce

Report

By July 10,

2015

Details submitted vide

letter dated 29.07.2015 to

the Hon’ble Commission.

Cause of Action

4. Cause of Action

The cause of action for the present petition arises on the basis of compliance of the UERC(Terms

and Conditions for Determination of Tariff) Regulations 2011 and UERC (Terms and Conditions

for Determination of Tariff) Regulations 2015

Ground of Relief

5. Ground of Relief

Not Applicable

Details of Remedies Exhausted

6. Details of Remedies Exhausted

Not Applicable

Matter Not Previously Filed or Pending With any Court

7. Matter Not Previously Filed or Pending With any Court

The petitioner (s) further declares that it has not previously filed any petition or writ petition or

suit regarding the matter in respect of which this petition has been made, before the Commission,

or any other court or any other authority, nor any such writ petition or suit is pending before any

of them.

Relief sought

8. Relief sought

8.1. Relief Sought from the Hon’ble Commission

8.1.1. In view of the facts mentioned above, the Petitioner respectfully prays for the relief as

stated below:

8.1.2. The Petitioner respectfully requests that the orders of the Hon’ble Commission may

adequately consider the positions expounded in the present petition for approval of

Annual Fixed Charges for FY2016-17, FY2017-18 and FY2018-19 and true up for the

FY2014-15 based on audited account. This Petition incorporates substantially improved

information as compared to the earlier tariff petition. However the Petitioner is making

continuous efforts to refine the information system further which has started generating

results. The same may be suitably considered for the orders of the Hon’ble Commission.

8.1.3. The financial projections have been developed based on the Petitioner’s assessment, trend

available and estimates available. There could be differences between the projections and

the actual performance of the Petitioner. The Hon’ble Commission may condone the

same. The Petitioner also requests the Hon’ble Commission to allow to make revisions to

the Petition and submit additional relevant information that may emerge or become

available subsequent to this filing.

8.1.4. The petitioner respectfully requests that the Hon’ble Commission may consider and allow

the recovery of Income Tax and Water Tax from the beneficiaries in its order.

8.1.5. In view of the foregoing, the Petitioner respectfully prays that the Hon'ble Commission

may:

Accept and approve the accompanying projected financial information of the

Petitioner for determination of generation tariff for the FY2016-17, FY2017-18 and

FY2018-19 and true up for the FY2014-15 prepared in accordance with Tariff

Regulations established by the Hon’ble Commission and directives of the Hon’ble

Commission contained in the earlier tariff orders.

Grant suitable opportunity to the Petitioner within a reasonable time frame to file

additional material information that may be subsequently available;

Grant the waivers prayed with respect to such filing requirements as the Petitioner is

unable to comply with at this stage of filing;

Treat the filing as complete in view of substantial compliance and also the specific

humble requests for waivers with justification placed on record;

Condone any inadvertent omissions/ errors/ shortcomings and permit the Petitioner to

add/ change/ modify/ alter this filing and make further submissions as may be

required at a future date;

Consider and approve the Petitioner’s application including all requested regulatory

treatments in the filing;

Relief sought

Consider the submissions of Petitioner that could be at variance with the orders and

regulations of the Hon’ble Commission, but are nevertheless fully justified from a

practical viewpoint;

Pass such orders as the Hon’ble Commission may deem fit and proper keeping in

mind the facts and circumstances of the case.

Interim Order, if any, prayed for

9. Interim Order, if any, prayed for

Not Applicable

Details of Index

10. Details of Index

The list of enclosures is detailed below:

Particulars of the Fee remitted

11. Particulars of the Fee remitted

The details of the fee remitted are as follows:

Bank Draft No – 872486

Amount-10,00,000/-

In favour of - Uttarakhand Electricity Regulatory Commission

Drawn at - PNB, Yamuna Colony

Dated -26.11.2015

List of Enclosures

12. List of Enclosures

47

VERIFICATION

I, Lalit Mohan Verma S/o Late Sh. S. L. Verma, aged 57 years, working as Director (Finance), UJVN Ltd.,

residing at Gali No. 2, House No. 3, Vasant Vihar Enclave, Dehradun-248006 do hereby verify that the

contents of the Paragraph Nos. 1 to 12 of the accompanying Petition are true and correct to my personal

knowledge and based on the perusal of official records, information received and the legal advice which I

believe to be true.

(Signature of Petitioner)