Embed Size (px)

Citation preview

Sustainable Market Share Index™

Research on 2015-2020 IRI Purchasing Data Reveals Sustainability Drives Growth, Survives the PandemicRandi Kronthal-SaccoTensie WhelanUpdated: July 16, 2020

Sustainable Market Share Index™: Executive Summary

We reviewed consumer purchasing of sustainability-marketed products in 36 CPG categories comprising ~40% of the total CPG market* ($). Our findings are:

• Sustainability-marketed products delivered 54.7% of CPG market growth (2015-2019) despite representing only 16.1% share of the category($) in 2019, up +2.4 ppts vs. 2015 (Pgs. 5,6 ). Sustainability-marketed products grew 7.1x faster than products not marketed as sustainable (Pg. 7).

• Sustainabilty marketed products continue to grow despite the COVID-19 pandemic (Pgs. 10-13).

• The market share of sustainability-marketed products aligns along a continuum based on perceived category functionality or efficacy (Pg. 15). Even in categories with low shares, shares of sustainability-marketed products increased.

• Sustainability-marketed branded products enjoy a significant price premium of 39.5%** vs. their conventionally-marketed branded counterparts, with a widening premium of +5.3 pts vs. 2014 (Pgs. 17-20).

• Per capita, the top 5 states for purchases of sustainability-marketed products are NH, ME, MA,VT and CT (Pg. 22).

• Upper income, millennials, college-educated and urban consumers are more likely to buy sustainability-marketed products. In addition, Middle Income, Baby Boomers and Gen Xers contribute a significant percent of sustainable sales (Pgs. 24-27).

*Excluding alcohol and tobacco. **Weighted by $ Sustainable Sales of categories examined

2

Sustainable Market Share Index™: Research QuestionsConsumer packaged goods (CPG) companies are responding to changing generational expectations, including for more sustainable product offerings, yet understanding of sustainable purchasing trends is limited.

The NYU Stern Center for Sustainable Business partnered with IRI, who provided the data pro bono, to assess the following:

1. Have purchases of sustainable products increased over time?

2. Have sustainable purchases been impacted by COVID-19?

3. Are there specific product categories for which the purchases of more sustainable product options out- or under-perform less sustainable alternatives?

4. What is the impact of price on purchases of sustainable products?

5. Are there geographical differences in sustainable purchasing?

6. What is the demographic profile of the sustainable purchaser?

3

Note: This study represents an updated and significantly expanded review of consumer purchasing first presented in March 2019.

Sustainable Market Share Index™: Research Question 1

Research Question 1:

Have purchases of sustainable products increased over time?

Research Result:

Not only are sustainability-marketed products growing but they also are contributing to a disproportionate share of the CPG category growth.

4

Ann

ual $

Sha

re o

f Sus

tain

abili

ty-

Mar

kete

d Pr

oduc

ts

13.7%

16.1%

0%

5%

10%

15%

20%

25%

2015 2019

Sustainable Market Share Index™: Sustainable Market Share

Across all categories studied, sustainability-marketed products account for 16.1%* share of market ($) in 2019, up from 13.7%* in 2015.

* Shares updated due to CSB & IRI re-categorizations; based on 36 categories examined

5

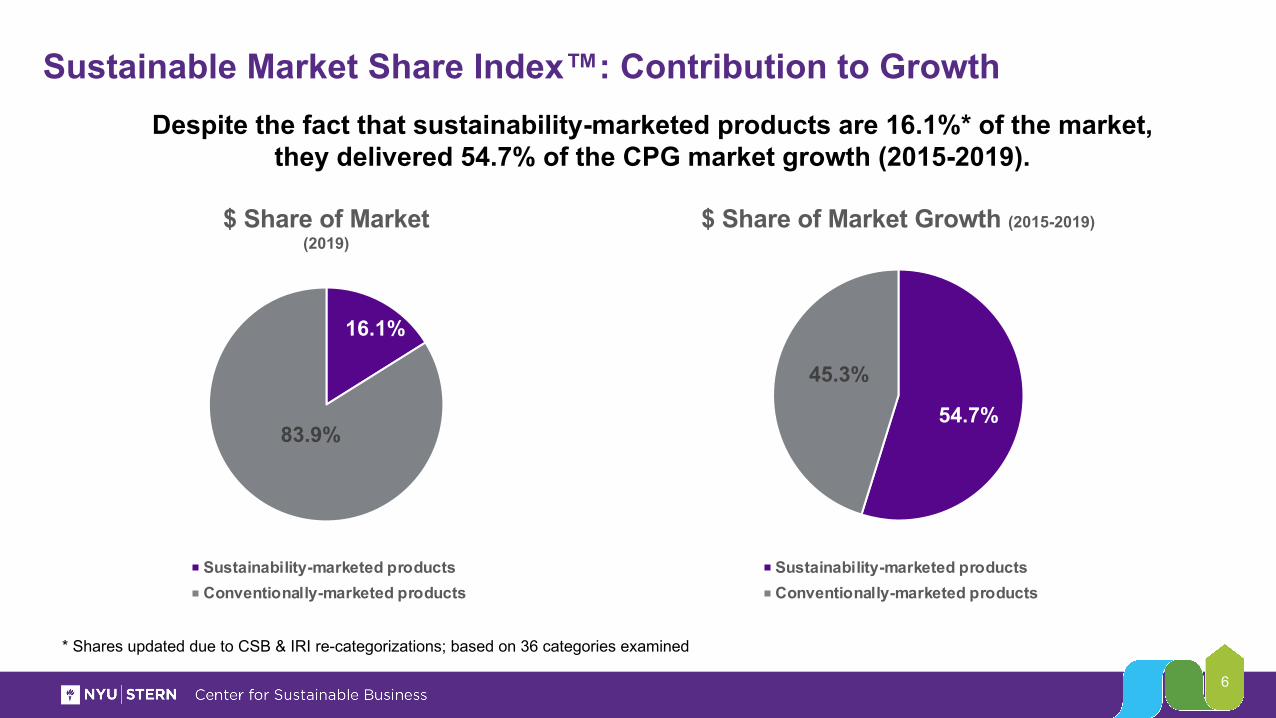

Sustainable Market Share Index™: Contribution to GrowthDespite the fact that sustainability-marketed products are 16.1%* of the market,

they delivered 54.7% of the CPG market growth (2015-2019).

46.9%54.7%

45.3%

$ Share of Market Growth (2015-2019)

Sustainability-marketed productsConventionally-marketed products

16.1%

83.9%

$ Share of Market(2019)

Sustainability-marketed productsConventionally-marketed products

* Shares updated due to CSB & IRI re-categorizations; based on 36 categories examined

6

Sustainable Market Share Index™: Growth RateSustainability-marketed products grew 7.1x faster than conventionally-

marketed products, and 3.8x faster than the CPG market.

46.9%

Note: Based on 36 categories examined

7

100

105

110

115

120

125

130

2015 2016 2017 2018 2019

Sustainablility-marketed products Category Conventionally-marketed products

Total Market 4-YR CAGR:1.56%

Conventionally-marketed 4-YR CAGR:0.83%

Sustainability-marketed4-YR CAGR:5.86%

Inde

x (B

ase

Year

201

5=

100)

Sustainable Market Share Index™: Category PerformanceIn ~90% of individual product categories, the growth of sustainability-marketed

products outpaced the growth of their respective categories.

-30.00%

-10.00%

10.00%

30.00%

50.00%

70.00%

90.00%

110.00%

130.00%

150.00%

Sanita

ry Nap

kins

Laun

dry Care

Floor C

leane

rs

Deodoran

t

Diapers

Soap

Facia l T

issue

Carbonate

d Bev

erages

Skin C

areSou

p

Cookies

Dish D

eterg

ent

Toothp

aste

Pet Tre

ats

Fresh B

read &

Roll

s

Vitamins

Dinner E

ntrees

-FZ

Cereal

Natural C

heese

Weig

ht Con

trol

Bottled

Juice

s

Laun

dry Dete

rgent

Crack

ers

Sal ty S

nack

s

Food and

Tras

h Bag

s

Coffee

Chocola

te Can

dy

Energy

Drin

ks

Pet Fo

odYog

urt

Househ

old C

leane

rMilk

Paper

Towels

Toilet

Tissue

Cups an

d Plates

Paper

Napkin

s

Sustainability-marketed products

Category

% C

hang

e in

Sal

es (2

015-

19)

** * * *

*Note: Actual sales growth for sustainability-marketed products in these categories from 2015-19 were 1019%, 901%, 545%, 449%, 280%, 197% and 160%, respectively

* *

* Paper towels, cups and plates, toilet tissue and paper napkins lost share to private label. Because we did not have visibility into private label to ascertain if there were claims regarding sustainability, we had to assume they were not marketed as sustainable. So, in fact, if private labels were making claims of sustainability (as we have observed they do on shelf), these categories may not have seen share decline of sustainability-marketed products.

8

Sustainable Market Share Index™: Research Question 2

Research Question 2:

Have sustainable purchases been impacted by COVID-19?

Research Result:

• Purchases of sustainability marketed products continue to grow in the face of the pandemic.

9

Sustainable Market Share Index™: 2020 Dollar Sales

10

Both sustainability-marketed and total category sales grew significantly and similarly the week ending March 15th

80.00

100.00

120.00

140.00

160.00

180.00

Week E

nd 01

-05-20

Week E

nd 01

-12-20

Week E

nd 01

-19-20

Week E

nd 01

-26-20

Week E

nd 02

-02-20

Week E

nd 02

-09-20

Week E

nd 02

-16-20

Week E

nd 02

-23-20

Week E

nd 03

-01-20

Week E

nd 03

-08-20

Week E

nd 03

-15-20

Week E

nd 03

-22-20

Week E

nd 03

-29-20

Week E

nd 04

-05-20

Week E

nd 04

-12-20

Week E

nd 04

-19-20

Week E

nd 04

-26-20

Week E

nd 05

-03-20

Week E

nd 05

-10-20

Week E

nd 05

-17-20

Week E

nd 05

-24-20

Week E

nd 05

-31-20

Week E

nd 06

-07-20

Week E

nd 06

-14-20

Inde

x vs

Wee

k of

1-0

5-20

*Sustainability-Marketed Products and Total Category $ Index

Category $ Sustainability-Marketed Products $* Index vs 100

Sustainable Market Share Index™: Sustainable Shares: COVID-19Shares of sustainability-marketed products grew significantly the week of March 15th and have continued to maintain share through

mid-June

16.13%

16.39% 16.87% 17.38%

19.32%

16.81%

16.86%

16.87%

16.53% 16.94%

16.94%

16.64%

16.40%

16.37%

16.18%

10.00%

12.00%

14.00%

16.00%

18.00%

20.00%

22.00%

24.00%

Year End2019

8 WeeksEnd 2-23-

20

WeekEnd 03-

01

WeekEnd 03-

08

WeekEnd 03-

15

WeekEnd 03-

22

WeekEnd 03-

29

WeekEnd 04-

05

WeekEnd 04-

12

WeekEnd 04-

19

WeekEnd 04-

26

WeekEnd 05-

03

WeekEnd 05-

10

WeekEnd 05-

17

4 WeeksEnd 6-14

Sustainability-Marketed Product Share

11

-1.00

-0.50

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

Cer

eal

Deo

dora

nt

Coo

kies

San

itary

Nap

Sou

p

Cra

cker

s

Dia

pers

Floo

r C

lean

ers

Laun

dry

Car

e

Food

& T

rsh

Bg

Pet

Tre

ats

Ene

rgy

Drin

ks

Toot

hpas

te

Laun

dry

Det

Car

b B

ev

Vita

min

s

Din

Ent

rees

Sal

ty S

nack

s

Cup

s an

d Pl

ates

Pet

Foo

d

Dis

h D

eter

gent

Bot

tled

Juic

es

Cho

cola

te

Yog

urt

Nat

ural

Che

ese

Hou

se C

lean

er

Fres

h B

read

Faci

al T

issu

e

Milk

Ski

n C

are

Pap

er N

ap

Soa

p

Toile

t Tis

sue

Wei

ght C

ontro

l

Cof

fee

Pap

er T

owel

s

Sustainable Market Share Index™: March 15 share performancePaper goods, skincare and food items drove the

greatest week to week share increases (week ending March 15 vs prior week).

12

Shar

e ch

ange

wee

k en

ding

Mar

ch 1

5 vs

. prio

r per

iod

Sustainable Market Share Index™: YTD Sustainable Market ShareSustainability-marketed products now account for 16.8% YTD, +.6pts vs. 2019

Ann

ual $

Sha

re o

f Sus

tain

abili

ty-

Mar

kete

d Pr

oduc

ts

13.66%*

16.13%*16.77%**

0%

5%

10%

15%

20%

25%

2015 2019 2020 YTD**

* Shares updated due to CSB & IRI re-categorizations** January-June 15th, 2020

13

Sustainable Market Share Index™: Research Question 3

Research Question 3:

Are there specific product categories where the purchases of more sustainable product options out or underperform less sustainable alternatives?

Research Result:

• Yes. Categories that demand high functionality (e.g., detergent) do not have a large percentage of sustainable purchases, but nevertheless experienced share growth.

• Conversely, categories with low functionality demands (e.g., dairy) have higher category consumption.

14

Sustainable Market Share Index™: Shares of Sustainable Products

0%

10%

20%

30%

40%

50%

60%

70%

80%

Food an

d Trash

Bags

Carbonate

d Bev

erages

Energy D

rinks

Pet Foo

d

Pet Treats

Laund

ry Detergen

t

Laund

ry Care

Chocolate C

andy

Toothpa

ste

Sanita

ry Nap

kins

Cookies

Diapers

Paper

Napkin

s

Cups and

Plates

Deodora

nt

Househo

ld Clean

er

Dish D

etergent

Dinner Entr

ees -

FZ

Vitamins

Salty S

nack

s

Paper

Towels

Weight Contr

ol

Soup

Floor Clean

ers

Fresh Bread

& Rolls

Cracke

rs

Cereal

Skin C

are

Natural C

heese

Coffee

Soap

Bottled J

uices Milk

Facial T

issue

Yogurt

Toilet T

issue

2019

Sus

tain

abilit

y-M

arke

ted

Prod

ucts

$ S

hare

of C

ateg

ory >20% Share

Toilet TissueYogurtFacial TissueMilkBottled JuiceSoapCoffeeNatural CheeseSkin Care

5%- 20% ShareCerealCrackersFresh BreadFloor CleanerSoupWeight ControlPaper TowelsSalty SnacksVitaminsFrozen DinnerDish DetergentHousehold CleanerDeodorantCups and PlatesPaper Napkins

<5% ShareDiapersCookiesSanitary NapkinsToothpasteChocolateLaundry CareLaundry DetergentPet TreatsPet FoodEnergy DrinksCarbonated BevTrash Bags

15

Sustainable Market Share Index™: Research Question 4

Research Question 4:

What is the impact of price on purchases of sustainable products*?

Research Result:

• Despite significant price premiums, sustainability-marketed products grew far faster than the conventionally branded players and had lower price sensitivity in 2/3rds of the categories examined.

Analysis conducted was among branded players and excluded store brand/private label; based on 36 categories examined

16

34.21%39.46%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2014 2018

Sust

aina

bilit

y-M

arke

ted

Prod

ucts

’ Pric

e Pr

emiu

m

vs. C

onve

ntio

nally

-Mar

kete

d Pr

oduc

ts

+ 5.3pts

Sustainable Market Share Index™: Price PremiumSustainability-marketed products enjoyed a sizeable price premium at

39%* over conventionally-marketed products, and increased +5.3 pts since 2014

*Weighted by $ Sustainable Sales of categories examined; analysis excluded store brand/private label

17

-58%

-33%-27%

-19%

-5%

3% 3%14% 18% 20% 21% 22% 22% 23%

28% 29% 32% 32% 35%42% 46% 47% 49% 50% 50%

56%

74%80%

100%

112% 114%123%

134% 135%

165%

-75%

-50%

-25%

0%

25%

50%

75%

100%

125%

150%

175%

Paper Napki

ns

Skincar

e

Paper Towels

Vitamins

Dish Dete

rgent

Laundry Dete

rgent

Energy D

rinks

Facial Ti

ssues

Salty Snack

sMilk

Household

Cleaner

Natural

Cheese

Deodorant

Foods and Tras

h Bags

Diapers

Weight C

ontrol

Floor C

leaners

SoapCere

alSoup

Yogurt

Cups & Plate

s

Fresh B

read &

Rolls

Chocolate

Toothpast

e

Crackers

Sanitary N

apkins

Bottled Ju

ices

Coffee

Dinner E

ntrees

Cookies

Pet Treats

Pet Food

Laundry Care

Carbonated

Beverages

2018

Sus

tain

abilit

y-M

arke

ted

Prod

ucts

’ Pric

e Pr

emiu

m/D

isco

unt

Sustainable Market Share Index™: Price Premium by CategoryPrice premiums ranged from 3% to over 150%. Only a few categories

had a price discount vs. conventionally-marketed products.

18

21.37%

2.95%

0%

5%

10%

15%

20%

25%

$ Sa

les

% G

row

th (E

x-Pr

ivat

e La

bel)

2014

-201

8

Sustainability-Marketed Products Conventionally-Marketed Products

Sustainable Market Share Index™: Growth of Sustainable Branded PlayersAmong branded players, sustainability-marketed products grew over 7x faster than conventionally-marketed products, indicating consumers’ willingness to

pay higher prices.

7X

19

Sustainable Market Share Index™: Price SensitivitySustainability-marketed products had lower price sensitivity in most categories studied: Food categories had the greatest price leverage.

-3

-2

-1

0

1

2

3

4

5

6

Diapers

Dinner

Entree

s

Cereal

Pet Foo

d

Dish D

eterge

nt

Pet Trea

ts

Yogurt

Fresh B

read a

nd R

olls

Natural

Che

ese

House

hold

Cleane

r

Carbon

ated B

evera

ges

Energy

Drin

ks

Weight C

ontro

l

Cookie

s

Crackers

Choco

late

Coffee

Salty S

nack

s

Bottled

Juice

s

Floor C

leane

rs

Sanita

ry Nap

kins

Soup

Milk

Deodo

rant

Soap

Paper

Towels

Facial

Tiss

ues

Vitamins

Skinca

re

Laun

dry C

are

Food T

rash B

ags

Cups &

Plates

Paper

Napkin

s

Toothp

aste

Laun

dry D

eterge

nt

Toilet

Tissu

e

Diff

eren

ce in

Ela

stic

ity b

etw

een

Sust

aina

bilit

y-M

arke

ted

and

Con

vent

iona

lly-M

arke

ted

Prod

ucts

Price sensitivity is the % change in volume due to a 1% change in price.

Less Sensitive to Price More Sensitive to Price

20

Sustainable Market Share Index™: Research Question 5

Research Question 5:

Are there geographical differences in sustainable purchasing?

Research Result:

• Yes. The top 5 states in terms of per capita* basis spending of sustainability-marketed products are New Hampshire, Maine, Massachusetts, Vermont, and Connecticut; the bottom five are Mississippi, Utah, Texas, Alabama and Kentucky

• Measured by state-wide purchases, however, California, Florida, Texas, New York, and Pennsylvania top the ranking in terms of total sustainable dollars spent due to the size of the states.

*STI: PopStats; based on 36 categories examined

21

Sustainable Market Share Index™: Geography

22

Sustainable Market Share Index™: Research Question 6

Research Question 6:

What is the demographic profile of the sustainable purchaser*?

Research Result:

• Millennials, upper income, college-educated and more urban cohorts are more likely to buy sustainability-marketed products.

• Baby Boomers, Gen Xers, upper and middle income, college educated and urban cohorts account for the bulk of the sustainable dollars spent.

Analysis conducted using IRI HH panel data; based on 35 categories examined23

The younger the household, the more likely they were to buy sustainability-marketed products. However, most sustainability-marketed product purchases came from Gen X

and Boomers.

Total CPG Sustainable Sales

Composition

Millennials 25%

Generation X 32%

Boomers 33%

Seniors & Retirees 10%

Sustainable Market Share Index™: Generational Cohorts

Chart read as: Millennials purchased a significantly higher percent (>1.2x) of their Carbonated Beverage purchases on sustainability-marketed products, than did Average HHs.

Index 120+Index 80-120Index <80

24

The higher the education, the more likely they were to buy sustainability-marketed products. Most of the sustainability-marketed product sales came from College graduates

or those with some college education.

* 7% had no female present

Total CPG Sustainable Sales

Composition*

Post Graduate

School17%

Graduated College 33%

Some College 25%

Graduated High School 16%

Some High School or

Less2%

Sustainable Market Share Index™: Household Education

Chart read as: Female HH who attended Post Graduate School purchased a significantly higher percent (>1.2x) of their Carbonated Beverage purchases on sustainability-marketed products, than did Average HHs.

Index 120+Index 80-120

Index <80

25

The higher the household income, the more likely they were to buy sustainability-marketed products. Upper/middle income made up the highest percent of sustainability-

marketed product dollars spent.

Total CPG Sustainable Sales

Composition

Upper 38%

Middle 39%

Lower 22%

Sustainable Market Share Index™: Income Tiers

Chart read as: Upper Income Households purchased a significantly higher percent (>1.2x) of their Carbonated Beverage purchases on sustainability-marketed products, than did Average HHs.

Index 120+Index 80-120

Index <80

26

The more urban the residence, the more likely the purchases of sustainability-marketed products. County A accounted for just under half of the total CPG

sustainability-marketed dollars spent.

Total CPG Sustainable Sales

Composition

Coun

ty A

44%

Coun

ty B

30%

Coun

ty C

/D

26%

Sustainable Market Share Index™: Urbanicity

Chart read as: County A purchased a significantly higher percent (>1.2x) of their Carbonated Beverage purchases on sustainability-marketed products, than did Average HH’s.

Index 120+

Index 80-120Index <80

27

Additional Research Planned

Early 2021, the NYU Stern Center for Sustainable Business will release:• The full year impact of COVID-19 on sustainability-marketed product purchases.• The impact of a narrowing price gap between sustainability-marketed products and

conventionally-marketed products on volumes as well as a detailed analysis of price elasticity.

28

About the NYU Stern Center for Sustainable BusinessThe NYU Stern Center for Sustainable Business was founded on the principle that sustainable business is good business; delivering better financial results while protecting the planet and its people. We aim to help current and future business leaders embrace proactive and innovative mainstreaming of sustainability, resulting in competitive advantage and resiliency for their companies as well as a positive impact for society.

Randi Kronthal-Sacco is a Senior Scholar, Marketing and Corporate Outreach for the NYU Stern Center for Sustainable Business. Ms. Kronthal-Sacco was a senior executive at Johnson & Johnson and is a Stern alumna.

Tensie Whelan is a Clinical Professor at NYU Stern and Founding Director of the NYU Stern Center for Sustainable Business.

Please contact [email protected] or [email protected] with any comments or questions.

29

AcknowledgmentsThe NYU Stern Center for Sustainable Business would like to thank the IRI organization for the generous donation of its data.

A special thank you to IRI’s Larry Levin, Executive V.P., Market and Shopper Intelligence. We also are grateful for the support of Jeanne Livelsberger, Executive Vice President and co-Leader of IRI’s Market and Shopper Intelligence Center of Excellence, and Sheila Noojibail, Vice President and leader of IRI’s Shopper Intelligence Platform.

We would like to acknowledge the research support of NYU Interns Dorea Novaez, Alexandra Walstad, Samuel Wallace, Ethan Ou, Jessica Tou, Patrick Wu, and Anirudh Dave as well as market research consultants Elena Kanner and Biren Shah.

30

Appendix

MethodologyData

• IRI Point of Sale and HH panel data in all measured channels in U.S. excluding alcohol and tobacco

Selection Criteria

• 36 categories examined held the largest dollar volume; in a few cases, smaller categories were included to ensure fair representation of all major CPG segments

• 73,293 products reviewed; products with 0.00 dollar share of category were not considered unless identified as organic.

• Due to lack of visibility into private label product claims, private label was not included as sustainability-marketed, with the exception of organic private label in the food categories.

Sustainability-Marketed Products Determination

• Identified all skus for each category marketed as sustainable with on-package communication, e.g. 3rd party certification (e.g. USDA Organic), containing organic ingredients, no phosphates, no phthalates, etc.

• Sustainability determination focused on the product itself, not the recyclability of the package.

• A very conservative approach was adopted. For example, the following was not considered sustainable:• Natural with no other sustainable identification• Recyclable packaging

Other Assumptions/Information

• Products that were deemed sustainability-marketed in 2018 were considered sustainability-marketed in 2015. This likely depressed the growth numbers.

• We made no attempt to assess if products marketed as sustainable were, in fact, sustainable. Instead, we focused on whether the marketing of a product as sustainable would drive purchase.

All estimates and analysis in this paper based on Information Resources Inc., data are by the authors and not by Information Resources, Inc.

32