Embed Size (px)

Citation preview

Supply

Chapter 5

Goals & Objectives

1. Supply Curve & Price2. Changes to supply.3. Theory of Production.4. 3 Stages of Production.5. 4 Measures of Cost.6. Identify 2 key measures of revenue.

7. Business Decisions & Gov’t

Supply

• Amount of a product offered for sale at all possible prices that could prevail in the market.

• Law of Supply: principle that suppliers will normally offer more for sale at higher prices rather than lower prices.

Supply & Price

Change in Supply

• 1. Cost of Inputs: Labor wages (minimum wage increases?), gasoline prices, capital goods prices, property taxes, business taxes, gov’t regulations

• 2. Productivity: Commission, Sales, Piece-work, fringe benefits, 401K, profit sharing.

Minimum Wage Requirements are Input Costs

Change in Supply

• 3. Technology: Robotics, Computers, Smart Cars, Smart phones, Wireless

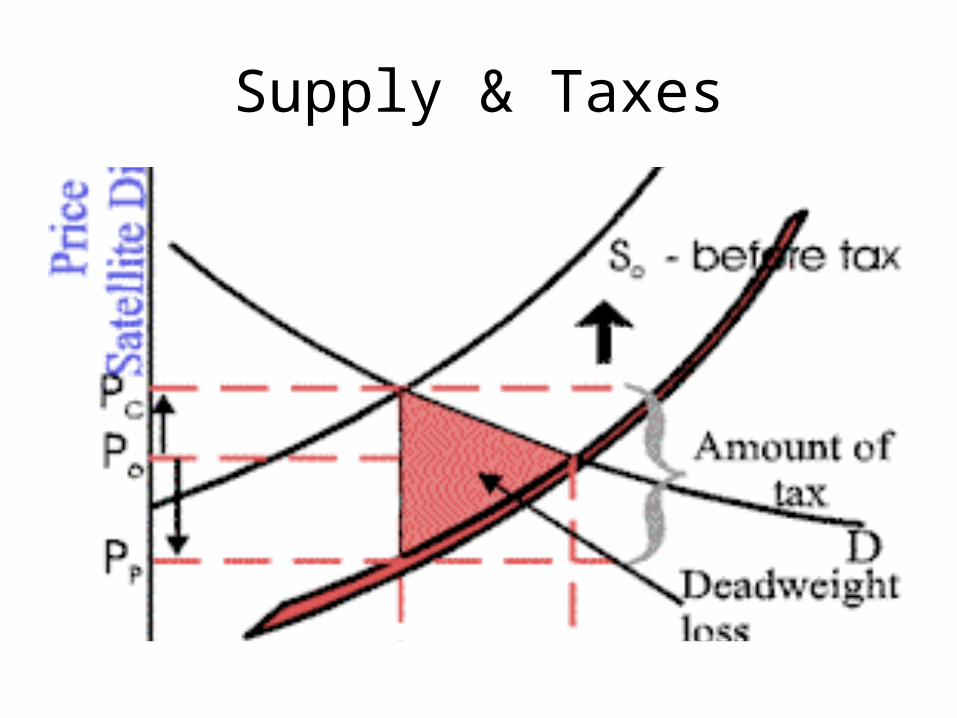

• 4. Taxes and Subsidies: High taxes lowers profit margins which lowers production and raises consumer prices.– Subsidies: designed to protect producers profits. Short

Run: lowers consumer prices– Long Run: Reduces competition and raises prices without

continued subsidies.

Supply & Taxes

Change in Supply

• 5. Expectations: Futures/Options.– Gasoline prices… Investors expect oil prices to rise due to gov’t

regulations, investors buy more oil stock, causes the price of oil to rise which causes gasoline prices to rise, investors make dividends.

– Hurricane & Gas Prices: Hurricane shuts down supply of oil which causes a shortage of gasoline which causes increased gasoline prices. (JIT theory)

• 6. Government Regulations: Global Warming Scheme; shuts down pipeline & drilling on public lands which causes artificial oil shortages & high gasoline prices.

Regulations & Supply

Change in Supply

• 7. Number of Sellers:– Increased number of sellers/producers/competing

business will cause an increase in production and lower consumer prices.

– Decrease number of sellers/producers/competing business will cause a decrease in production and higher consumer prices.

– Cost-Push Inflation: government licensing requirements, increased taxation & regulations decrease the number of producers & high prices.

Community Reinvestment Act

Fannie Mae & Freddie MacFederal Requirement for Banks to issue

loans to borrowers with no credit history or poor credit history.

Trade Off: Increased default rate for banks. Increased foreclosures and higher collateralized debt obligations, fewer profits.

Opportunity Costs: Less money to lend to qualified borrowers & higher interest rates.

Sub-Prime Loans & Inflation

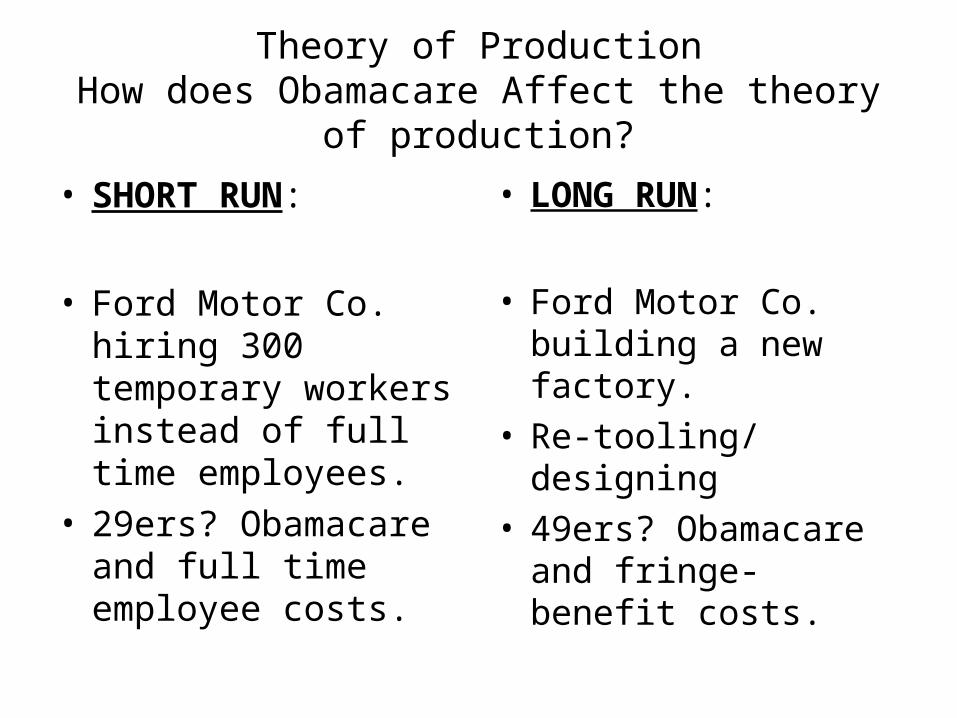

Theory of ProductionHow does Obamacare Affect the theory of production?

• SHORT RUN:

• Ford Motor Co. hiring 300 temporary workers instead of full time employees.

• 29ers? Obamacare and full time employee costs.

• LONG RUN:

• Ford Motor Co. building a new factory.

• Re-tooling/designing• 49ers? Obamacare and

fringe-benefit costs.

29ers & Obamacare

49ers & Obamacare

3 Stages of Production

1. Increasing returns: More workers equals increased productivity. Greater supply equals greater profits. (6 employees)

2. Diminishing returns: Workers at marginal production rates creates increased costs and break-even profits. (10 employees)

3. Negative returns: Too many workers at marginal production rates creates costs exceeding profits. (11 employees)

Measures of CostMeasures of Cost

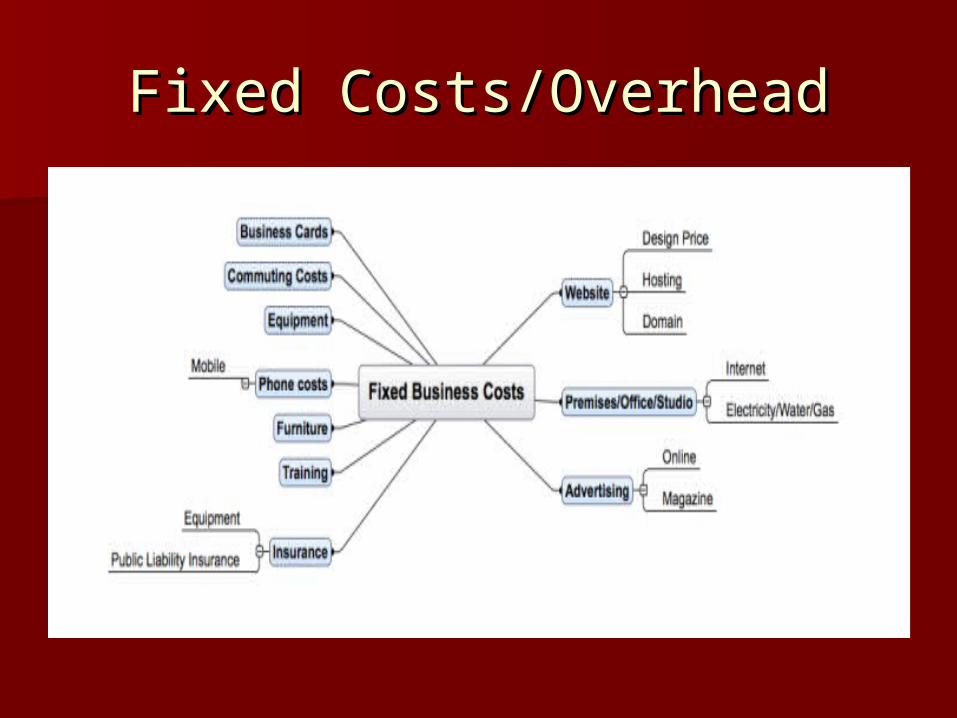

1.1. Fixed CostsFixed Costs: Land, Leases, : Land, Leases, Mortgages, Capital Goods Costs, Mortgages, Capital Goods Costs, Utility Costs, Property Taxes, Sales Utility Costs, Property Taxes, Sales Taxes, Income Taxes, License Fees, Taxes, Income Taxes, License Fees, Insurance Costs, Employee BenefitsInsurance Costs, Employee Benefits

2.2. OverheadOverhead: Sum total of all fixed : Sum total of all fixed costs.costs.

Fixed Costs/OverheadFixed Costs/Overhead

Measures of Cost

• 3. Variable Costs: Labor and Resource Costs

• 4. Total Costs: Sum Total of Fixed and Variable Costs.

• 5. Marginal costs: producing more than needed. (JIT Theory)

E-COMMERCEE-COMMERCE

Avoids advertising Costs, Taxes and Avoids advertising Costs, Taxes and RegulationsRegulations

Internet is the last unregulated commerce Internet is the last unregulated commerce market. market.

State and Local Governments demand federal State and Local Governments demand federal interstate commerce regulation.interstate commerce regulation. Why? Who Benefits from regulation?Why? Who Benefits from regulation? Who loses from regulation and taxation?Who loses from regulation and taxation?

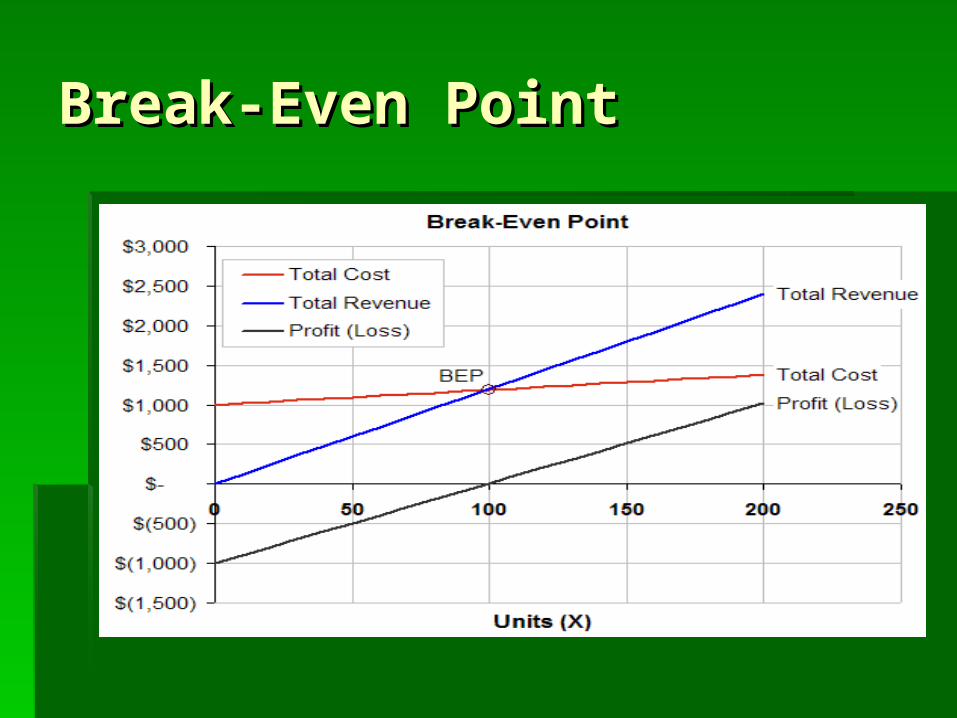

Measures of RevenueMeasures of Revenue

Break-even pointBreak-even point: :

1.1. Total CostsTotal Costs: Variable + Fixed + Marginal: Variable + Fixed + Marginal

2.2. Subtracted By: Subtracted By:

3.3. Total RevenueTotal Revenue: Total output multiplied by units sold.: Total output multiplied by units sold.

4.4. Break-Even Point: Break-Even Point: Total revenue needed to pay for total Total revenue needed to pay for total business costs.business costs.

5.5. Marginal Revenue: Marginal Revenue: Additional output past break-even Additional output past break-even point.point.

Break-Even PointBreak-Even Point