Embed Size (px)

Citation preview

www.harriswilliams.com

Member FINRA/SIPC

Transportation & Logistics Automotive Aftermarket Sector Update

January 2013

1 of 8

Transportation & Logistics

Automotive Aftermarket Sector Update January 2013

Welcome to the first issue of the Harris Williams & Co. Transportation & Logistics (T&L) Automotive Aftermarket Sector Update. We hope to use this forum to keep you (investors, senior managers, entrepreneurs, and others focused on the auto aftermarket) up to speed on what we are seeing in our sector, apprised of industry news and events, and connected to the auto aftermarket companies that we are fortunate to work with everyday.

We hope to bring you transcripts of relevant discussions we have with senior industry professionals, like this month’s discussion with Michael Klein, Chief Executive Officer of IDQ. We also want to keep you apprised of the transactions we are executing in the various sub-sectors, including suppliers, distributors, retailers, and service providers.

We hope you enjoy reviewing this newsletter, and please email us your thoughts and opinions. We want to ensure that this newsletter is informative and helpful as you continue to focus on the automotive aftermarket space.

Regards,

Frank F. Mountcastle, III Managing Director

[email protected] +1 (804) 915-0124

Jason D. Bass Managing Director

[email protected] +1 (804) 915-0132

Joseph H. Conner, III Director

[email protected] +1 (804) 915-0151

Richmond P: +1 (804) 648-0072 F: +1 (804) 648-0073

Boston P: +1 (617) 482-7501 F: +1 (617) 482-7503

Cleveland P: +1 (216) 222-9870 F: +1 (216) 222-0158

London P: +44 203 170 8838 F: +44 207 681 1907

Minneapolis P: +1 (612) 359-2700 F: +1 (612) 359-2701

Philadelphia P: +1 (267) 675-5900 F: +1 (267) 675-5901

San Francisco P: +1 (415) 288-4260 F: +1 (415) 288-4269

Greetings from the HW&Co.

Transportation & Logistics Team

Contacts

2 of 8

Transportation & Logistics

Automotive Aftermarket Sector Update January 2013

Bio: Michael Klein is the President and Chief Executive Officer of IDQ, manufacturer and distributor of “Do it Yourself” aftermarket products. Mr. Klein formerly served as Chief Executive Officer of Murray’s Discount Auto Stores, a 100+ store chain based in Belleville, Michigan and now part of O’Reilly Automotive. Prior to joining Murray’s Discount Auto Stores, Mr. Klein was a Certified Public Accountant and Certified Financial Planner with the Michigan accounting firm of Gordon & Company. Mr. Klein graduated (with High Distinction) in 1979 from Wayne State University in Detroit and holds a B.S. degree in Business Administration.

_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ __

HW&Co.: Key trends in the automotive aftermarket, including a growing light vehicle car population and increasing average age of light vehicles, continues to provide support for the growth of aftermarket products and services. How are these overall macro trends impacting IDQ? The broader industry? What opportunities will these macro trends create in the market going forward? Michael Klein (MK): A sluggish economy has convinced more consumers to seek cost-saving DIY (“Do it Yourself”) solutions. This has benefited nearly every major retailer (see the recent stock performance of O’Reilly Automotive and AutoZone for example) and suppliers to those retailers. While the light vehicle car population is growing, the key variable for all of us is the increasing age of the fleet, which is resulting in the need for increased maintenance and repair, including the recharging of air conditioning systems. HW&Co.: In recent years, the aftermarket has seen a shift in the growth of the DIY and “Do-It-For-Me” (DIFM) market segments. Do you see changes in either market with a continuing recovery in the economy? What types of industry players should be best positioned to take advantage of any changes in the market? MK: While OE sales have risen a bit over the last few years, I think the growth in the DIY channel will be permanent for many categories, including the aftermarket. Consumers need to save money and have learned that there are ample opportunities to save by servicing and repairing their own vehicles. Leading retailers such as O'Reilly, AutoZone, and Advance Auto are in the best position to service those consumer needs given their breadth of inventory and near-national footprints. HW&Co.: Given continued economic uncertainty, what indicators are you focused on for signs of growth or weakness in the economy? What impact, if any, will this have on investment decisions at IDQ? What are you hearing from your CEO peer group regarding future investment? MK: We look closely at miles driven and the price of gasoline, as these seem to be some of the bellwethers for the industry - though by far the biggest factor for us is extremes in weather (especially when you are selling air conditioning products!). I think most suppliers continue to be cautiously optimistic about the long-term growth prospects of the aftermarket, and the smart ones are investing alongside their retail partners. At IDQ, we are investing heavily in the aftermarket and are positioning ourselves to benefit from ongoing industry growth, alongside our retail partners. As an example, we recently launched an entirely new brand of products under the AC PRO name after an exhaustive 3-year study and investment. This new brand has been extremely well received by both retailers and consumers alike. HW&Co.: What strategies are you implementing at IDQ to become more valuable to your customers?

Aftermarket Talk with Michael Klein,

Chief Executive Officer, IDQ

3 of 8

Transportation & Logistics

Automotive Aftermarket Sector Update January 2013

MK: IDQ has always been about providing solutions for both consumers and retail partners, and we continue to drive valued innovation in the category. We have embarked on a nationwide marketing campaign for our AC PRO line to heighten consumer awareness about air conditioning recharge products (many consumers don't realize they can restore their cold air in 10 minutes with our product and save themselves hundreds of dollars). We have also strengthened our "back office" support for the category by launching social media platforms, increasing our category management tools (which our overworked customers love since it shifts these responsibilities from them to us), and providing valuable regulatory support and awareness (for example, this year we led the successful effort in Wisconsin to repeal a 1993 ban on DIY use of air conditioning products). HW&Co.: What are you seeing in terms of the M&A environment within the aftermarket? What do you think are the key drivers of a successful M&A strategy? MK: There has been less M&A activity than I would have anticipated over the last several months. On the public company side, many of our retail partners are experiencing strong growth in their stock prices, driving high potential valuations. On the private company side, I expect M&A volume to rebound over the coming months. I think one of the key drivers for prospective purchasers is to have a long-term perspective and begin building relationships with potential partners early. As the CEO of a leading aftermarket business, I understand the importance of having a true partnership with an equity sponsor. On the supplier side of the industry, I expect further consolidation and anticipate increased efficiency and customer service in the category as a result. HW&Co.: Given the attractive dynamics in the industry, clients regularly ask us for best practices in identifying attractive aftermarket investment opportunities. What words of advice would you give to those seeking investment opportunities in the sector? MK: Do your homework - talk to our trade association to learn about industry trends and outlook, talk to retail customers to really learn what is on their minds, spend time in retail stores, and watch what consumers are buying. The aftermarket is not an incredibly complex industry, but it does require a lot of "belt and suspenders" research. While I encourage your clients to use their resources for due diligence, don't rely on a third party "expert" to do the hard work of truly understanding the industry. HW&Co.: Here is a question that we could only ask of a true Detroit guy: Will the World Series sweep get the Tigers fired up for next season or crush morale heading into next year? MK: No one is more resilient than a Detroiter - we have suffered through over 55 years of the Lions! With the Tigers, we were a victim of circumstance this year - the six day layoff waiting for the Giants to finish their playoff killed us! Next year, we will be very hungry, and having Torii Hunter and Victor Martinez to support Miguel Cabrera will undoubtedly lead to future World Series success (though I personally wish they would wrap up the Series in late September/early October so I am not freezing at the ball park)!

Aftermarket Talk (continued)

4 of 8

Transportation & Logistics

Automotive Aftermarket Sector Update January 2013

Date Announced Acquirer Target Sector Target Description12/19/2012 Advance Auto Parts BWP Distributors Distributors and

RetailersBWP Distributors, Inc. supplies, markets, and distributes automobile parts and products.

12/17/2012 O'Reilly Automotive VIP, Inc. Auto Parts Distributors and Retailers

VIP, Inc., Auto Parts Related Assets comprises automotive parts sales and distribution business.

12/11/2012 Monro Muffler Brake Ken Towery's Auto Care Dealerships and Service Providers

Towery's Auto Care distributes and sells tires and operates car care centers under the Tire King name.

12/4/2012 Robert Bosch SPX Service Solutions Suppliers SPX Service Solutions distributes measurement products, thermal equipment and services.

12/3/2012 Auto Air Export Global Parts Distributors Distributors and Retailers

Global Parts supplies automotive aftermarket air conditioning parts and radiators.

12/3/2012 Management Affinia Brake Business Suppliers Affinia's brake business supplies, distributes, and retails brake products.

12/3/2012 Fisher Auto Parts Brownlee Distributing Distributors and Retailers

Brownlee Distributing distributes brake products, chemicals, engine parts, and other auto parts.

11/30/2012 Leonard Green & Partners CCC Information Services Dealerships and Service Providers

CCC Information Services Group provides software to auto body collision repair companies.

11/29/2012 Monomoy Capital Holley Performance Products Suppliers Holley manufactures fuel systems for street performance and drag race vehicles.

11/27/2012 Service King Paint and Body Wade Auto Body Dealerships and Service Providers

Wade Auto Body provides auto collision repairs services in Texas.

11/19/2012 1-800 Radiator Four Seasons Radiator Distributors and Retailers

Four Seasons Radiator supplies parts for automotive and industrial uses.

11/1/2012 Technical Chemical Blue Magic Suppliers Blue Magic develops, manufactures, and sells specialty chemical products for the aftermarket.

10/17/2012 Zep Industries Ecolab Vehicle Care Suppliers Ecolab's Vehicle Care division supplies car, truck, and fleet wash operators with cleaning products.

10/9/2012 TPG Capital Fleetpride Distributors and Retailers

Fleetpride supplies heavy-duty truck and trailer replacement parts.

9/7/2012 Sun Capital Partners Heartland Automotive Services

Dealerships and Service Providers

Heartland is a franchisee of quick lube retail service stores for automotive needs.

U.S. Auto Industry has its best year since 2007: The Detroit Free Press reports that the U.S. auto industry experienced a successful 2012, with major producers reporting large sales increases. Companies posted December sales of 1.36 million cars and trucks, up 10% over last year. Sales gains occurred despite a sluggish economy and as the industry continues to cut sales incentives, which fell 5.1% for the year.

Despite disconnect in recent years, miles driven outlook has been overlooked as a barometer of the aftermarket’s growth potential: The AASA’s special report on forecasting aftermarket growth warns that significant growth in the aftermarket industry will need to be driven by increases in miles traveled, despite the aftermarket’s resilience as miles driven has stagnated in recent years. The EIA expects significant growth through 2035, but at a slower rate than the pre-recession period. This potential future tailwind is not being captured in many analyst expectations and could fuel aftermarket growth over the long term.

Spike in lease terminations and softening of used car prices to affect 2013 car sales: Business Wire reports that the latest Edmunds report on 2013 auto sales shows 500,000 more lease terminations than 2012, which will bolster sales despite uncertain economic trends. Edmunds senior analysts predict four percent growth in car sales for 2013 to 15 million new vehicles. Other factors affecting car sales include used car prices softening $200-300 per vehicle from 2012 prices.

How innovation is shifting the role of OEM and aftermarket parts suppliers: Booz & Co. reports in its new 2013 Automotive Industry Perspective that suppliers are playing increasingly important roles in R&D historically reserved for OEMs. As renewed focus is placed on serving significant demand for technological innovation for a variety of automotive applications, OEMs are cutting back on R&D costs, shouldering them on suppliers. Suppliers will need agility in evaluating innovation opportunities in order to continue to thrive.

What We’re

Reading

Recent M&A Transactions

5 of 8

Transportation & Logistics

Automotive Aftermarket Sector Update January 2013

Source: Capital IQ

Source: Capital IQ

Source: Capital IQ

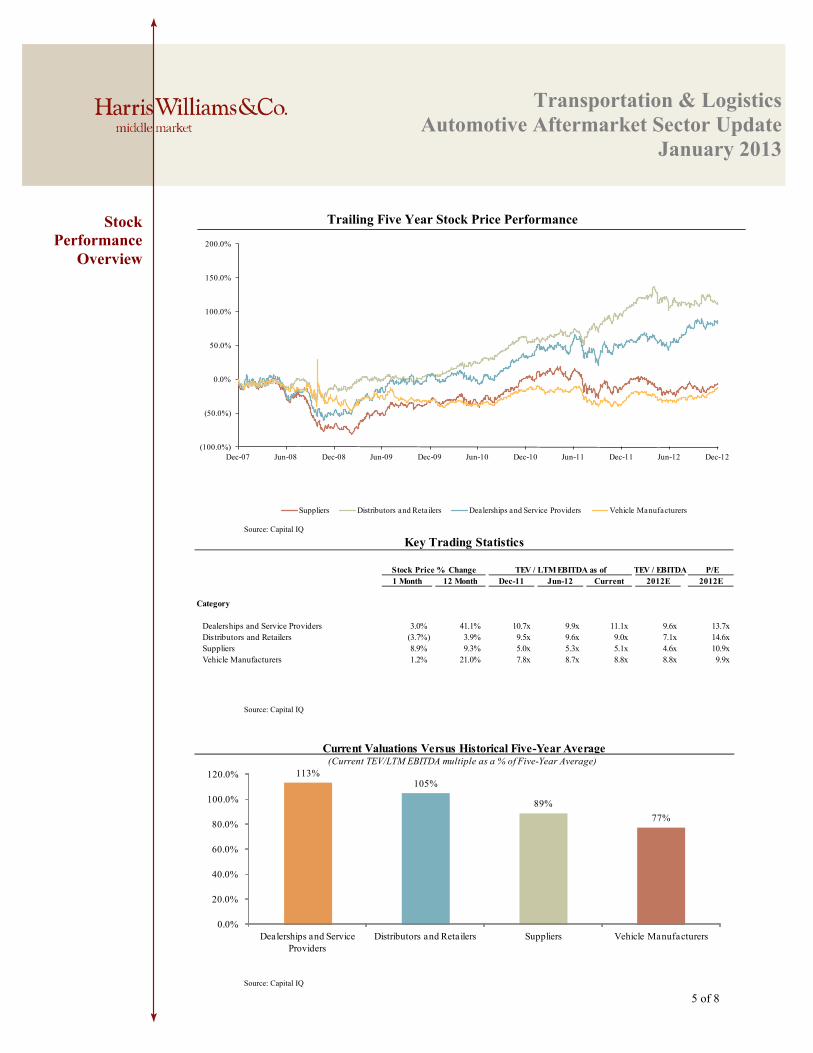

Trailing Five Year Stock Price Performance

Stock Performance

Overview

(100.0%)

(50.0%)

0.0%

50.0%

100.0%

150.0%

200.0%

Dec-07 Jun-08 Dec-08 Jun-09 Dec-09 Jun-10 Dec-10 Jun-11 Dec-11 Jun-12 Dec-12

Suppliers Distributors and Retailers Dealerships and Service Providers Vehicle Manufacturers

Key Trading Statistics

Stock Price % Change TEV / EBITDA P/E 1 Month 12 Month Dec-11 Jun-12 Current 2012E 2012E

Category

Dealerships and Service Providers 3.0% 41.1% 10.7x 9.9x 11.1x 9.6x 13.7xDistributors and Retailers (3.7%) 3.9% 9.5x 9.6x 9.0x 7.1x 14.6xSuppliers 8.9% 9.3% 5.0x 5.3x 5.1x 4.6x 10.9xVehicle Manufacturers 1.2% 21.0% 7.8x 8.7x 8.8x 8.8x 9.9x

TEV / LTM EBITDA as of

Current Valuations Versus Historical Five-Year Average(Current TEV/LTM EBITDA multiple as a % of Five-Year Average)

113%105%

89%77%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

Dealerships and Service Providers

Distributors and Retailers Suppliers Vehicle Manufacturers

6 of 8

Transportation & Logistics

Automotive Aftermarket Sector Update January 2013

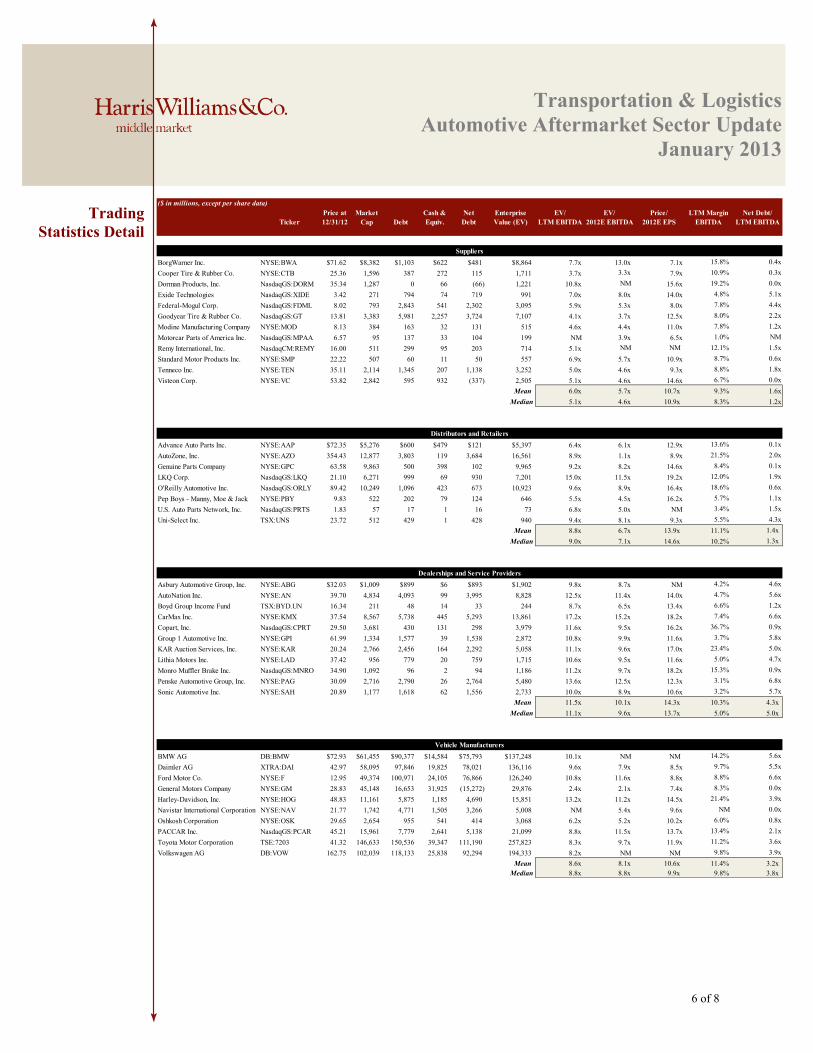

Trading Statistics Detail

($ in millions, except per share data)Price at Market Cash & Net Enterprise EV/ EV/ Price/ LTM Margin Net Debt/

Ticker 12/31/12 Cap Debt Equiv. Debt Value (EV) LTM EBITDA 2012E EBITDA 2012E EPS EBITDA LTM EBITDA

SuppliersBorgWarner Inc. NYSE:BWA $71.62 $8,382 $1,103 $622 $481 $8,864 7.7x 13.0x 7.1x 15.8% 0.4xCooper Tire & Rubber Co. NYSE:CTB 25.36 1,596 387 272 115 1,711 3.7x 3.3x 7.9x 10.9% 0.3xDorman Products, Inc. NasdaqGS:DORM 35.34 1,287 0 66 (66) 1,221 10.8x NM 15.6x 19.2% 0.0xExide Technologies NasdaqGS:XIDE 3.42 271 794 74 719 991 7.0x 8.0x 14.0x 4.8% 5.1xFederal-Mogul Corp. NasdaqGS:FDML 8.02 793 2,843 541 2,302 3,095 5.9x 5.3x 8.0x 7.8% 4.4xGoodyear Tire & Rubber Co. NasdaqGS:GT 13.81 3,383 5,981 2,257 3,724 7,107 4.1x 3.7x 12.5x 8.0% 2.2xModine Manufacturing Company NYSE:MOD 8.13 384 163 32 131 515 4.6x 4.4x 11.0x 7.8% 1.2xMotorcar Parts of America Inc. NasdaqGS:MPAA 6.57 95 137 33 104 199 NM 3.9x 6.5x 1.0% NMRemy International, Inc. NasdaqCM:REMY 16.00 511 299 95 203 714 5.1x NM NM 12.1% 1.5xStandard Motor Products Inc. NYSE:SMP 22.22 507 60 11 50 557 6.9x 5.7x 10.9x 8.7% 0.6xTenneco Inc. NYSE:TEN 35.11 2,114 1,345 207 1,138 3,252 5.0x 4.6x 9.3x 8.8% 1.8xVisteon Corp. NYSE:VC 53.82 2,842 595 932 (337) 2,505 5.1x 4.6x 14.6x 6.7% 0.0x

Mean 6.0x 5.7x 10.7x 9.3% 1.6xMedian 5.1x 4.6x 10.9x 8.3% 1.2x

Distributors and RetailersAdvance Auto Parts Inc. NYSE:AAP $72.35 $5,276 $600 $479 $121 $5,397 6.4x 6.1x 12.9x 13.6% 0.1xAutoZone, Inc. NYSE:AZO 354.43 12,877 3,803 119 3,684 16,561 8.9x 1.1x 8.9x 21.5% 2.0xGenuine Parts Company NYSE:GPC 63.58 9,863 500 398 102 9,965 9.2x 8.2x 14.6x 8.4% 0.1xLKQ Corp. NasdaqGS:LKQ 21.10 6,271 999 69 930 7,201 15.0x 11.5x 19.2x 12.0% 1.9xO'Reilly Automotive Inc. NasdaqGS:ORLY 89.42 10,249 1,096 423 673 10,923 9.6x 8.9x 16.4x 18.6% 0.6xPep Boys - Manny, Moe & Jack NYSE:PBY 9.83 522 202 79 124 646 5.5x 4.5x 16.2x 5.7% 1.1xU.S. Auto Parts Network, Inc. NasdaqGS:PRTS 1.83 57 17 1 16 73 6.8x 5.0x NM 3.4% 1.5xUni-Select Inc. TSX:UNS 23.72 512 429 1 428 940 9.4x 8.1x 9.3x 5.5% 4.3x

Mean 8.8x 6.7x 13.9x 11.1% 1.4xMedian 9.0x 7.1x 14.6x 10.2% 1.3x

Dealerships and Service ProvidersAsbury Automotive Group, Inc. NYSE:ABG $32.03 $1,009 $899 $6 $893 $1,902 9.8x 8.7x NM 4.2% 4.6xAutoNation Inc. NYSE:AN 39.70 4,834 4,093 99 3,995 8,828 12.5x 11.4x 14.0x 4.7% 5.6xBoyd Group Income Fund TSX:BYD.UN 16.34 211 48 14 33 244 8.7x 6.5x 13.4x 6.6% 1.2xCarMax Inc. NYSE:KMX 37.54 8,567 5,738 445 5,293 13,861 17.2x 15.2x 18.2x 7.4% 6.6xCopart, Inc. NasdaqGS:CPRT 29.50 3,681 430 131 298 3,979 11.6x 9.5x 16.2x 36.7% 0.9xGroup 1 Automotive Inc. NYSE:GPI 61.99 1,334 1,577 39 1,538 2,872 10.8x 9.9x 11.6x 3.7% 5.8xKAR Auction Services, Inc. NYSE:KAR 20.24 2,766 2,456 164 2,292 5,058 11.1x 9.6x 17.0x 23.4% 5.0xLithia Motors Inc. NYSE:LAD 37.42 956 779 20 759 1,715 10.6x 9.5x 11.6x 5.0% 4.7xMonro Muffler Brake Inc. NasdaqGS:MNRO 34.90 1,092 96 2 94 1,186 11.2x 9.7x 18.2x 15.3% 0.9xPenske Automotive Group, Inc. NYSE:PAG 30.09 2,716 2,790 26 2,764 5,480 13.6x 12.5x 12.3x 3.1% 6.8xSonic Automotive Inc. NYSE:SAH 20.89 1,177 1,618 62 1,556 2,733 10.0x 8.9x 10.6x 3.2% 5.7x

Mean 11.5x 10.1x 14.3x 10.3% 4.3xMedian 11.1x 9.6x 13.7x 5.0% 5.0x

Vehicle ManufacturersBMW AG DB:BMW $72.93 $61,455 $90,377 $14,584 $75,793 $137,248 10.1x NM NM 14.2% 5.6xDaimler AG XTRA:DAI 42.97 58,095 97,846 19,825 78,021 136,116 9.6x 7.9x 8.5x 9.7% 5.5xFord Motor Co. NYSE:F 12.95 49,374 100,971 24,105 76,866 126,240 10.8x 11.6x 8.8x 8.8% 6.6xGeneral Motors Company NYSE:GM 28.83 45,148 16,653 31,925 (15,272) 29,876 2.4x 2.1x 7.4x 8.3% 0.0xHarley-Davidson, Inc. NYSE:HOG 48.83 11,161 5,875 1,185 4,690 15,851 13.2x 11.2x 14.5x 21.4% 3.9xNavistar International Corporation NYSE:NAV 21.77 1,742 4,771 1,505 3,266 5,008 NM 5.4x 9.6x NM 0.0xOshkosh Corporation NYSE:OSK 29.65 2,654 955 541 414 3,068 6.2x 5.2x 10.2x 6.0% 0.8xPACCAR Inc. NasdaqGS:PCAR 45.21 15,961 7,779 2,641 5,138 21,099 8.8x 11.5x 13.7x 13.4% 2.1xToyota Motor Corporation TSE:7203 41.32 146,633 150,536 39,347 111,190 257,823 8.3x 9.7x 11.9x 11.2% 3.6xVolkswagen AG DB:VOW 162.75 102,039 118,133 25,838 92,294 194,333 8.2x NM NM 9.8% 3.9x

Mean 8.6x 8.1x 10.6x 11.4% 3.2xMedian 8.8x 8.8x 9.9x 9.8% 3.8x

7 of 8

Transportation & Logistics

Automotive Aftermarket Sector Update January 2013

Companies above represent select experience of Harris Williams & Co. professionals.

Our Professionals have deep expertise across the spectrum of Transportation & Logistics sectors.

Third-Party Logistics

Surface Transportation

Rail

Aviation

Marine

Transportation Equipment

Automotive

a portfolio company of

has been acquired by

a portfolio company of

has been acquired by

a portfolio company of

has been acquired by

a portfolio company of

has been acquired by

portfolio companies of

have completed a merger with

a portfolio company of

Recent HW&Co. Tombstones

8 of 8

Transportation & Logistics

Automotive Aftermarket Sector Update January 2013

Harris Williams & Co.’s Transportation & Logistics Group has industry-leading experience in a broad range of attractive niches, including automotive and heavy duty vehicles aftermarket, third party logistics, surface transportation, airport and aviation services, marine transportation, transportation equipment, and transportation infrastructure. Our middle market leadership and sell-side execution excellence deliver unmatched results for our clients. For more information, contact one of our professionals.

Sources:

• Capital IQ • Thomson Financial • S&P • Reuters

Harris Williams & Co. (www.harriswilliams.com) is a preeminent middle market investment bank focused on the advisory needs of clients worldwide. The firm has deep industry knowledge, global transaction expertise, and an unwavering commitment to excellence. Harris Williams & Co. provides sell-side and acquisition advisory, restructuring advisory, board advisory, private placements, and capital markets advisory services. Investment banking services are provided by Harris Williams LLC, a registered broker-dealer and member of FINRA and SIPC, and Harris Williams & Co. Ltd, which is authorised and regulated by the Financial Services Authority (FRN #540892). Harris Williams & Co. is a trade name under which Harris Williams LLC and Harris Williams & Co. Ltd conduct business. THIS REPORT MAY CONTAIN REFERENCES TO REGISTERED TRADEMARKS, SERVICE MARKS AND COPYRIGHTS OWNED BY THIRD-PARTY INFORMATION PROVIDERS. NONE OF THE THIRD-PARTY INFORMATION PROVIDERS IS ENDORSING THE OFFERING OF, AND SHALL NOT IN ANY WAY BE DEEMED AN ISSUER OR UNDERWRITER OF, THE SECURITIES, FINANCIAL INSTRUMENTS OR OTHER INVESTMENTS DISCUSSED IN THIS REPORT, AND SHALL NOT HAVE ANY LIABILITY OR RESPONSIBILITY FOR ANY STATEMENTS MADE IN THE REPORT OR FOR ANY FINANCIAL STATEMENTS, FINANCIAL PROJECTIONS OR OTHER FINANCIAL INFORMATION CONTAINED OR ATTACHED AS AN EXHIBIT TO THE REPORT. FOR MORE INFfaORMATION ABOUT THE MATERIALS PROVIDED BY SUCH THIRD PARTIES, PLEASE CONTACT US AT THE ABOVE ADDRESSES OR NUMBER. The information and views contained in this report were prepared by Harris Williams & Co. (“Harris Williams”). It is not a research report, as such term is defined by applicable law and regulations, and is provided for informational purposes only. It is not to be construed as an offer to buy or sell or a solicitation of an offer to buy or sell any financial instruments or to participate in any particular trading strategy. The information contained herein is believed by Harris Williams to be reliable but Harris Williams makes no representation as to the accuracy or completeness of such information. Harris Williams and/or its affiliates may be market makers or specialists in, act as advisers or lenders to, have positions in and effect transactions in securities of companies mentioned herein and also may provide, may have provided, or may seek to provide investment banking services for those companies. In addition, Harris Williams and/or its affiliates or their respective officers, directors and employees may hold long or short positions in the securities, options thereon or other related financial products of companies discussed herein. Opinions, estimates and projections in this report constitute Harris Williams’ judgment and are subject to change without notice. The financial instruments discussed in this report may not be suitable for all investors and investors must make their own investment decisions using their own independent advisors as they believe necessary and based upon their specific financial situations and investment objectives. Also, past performance is not necessarily indicative of future results. No part of this material may be copied or duplicated in any form or by any means, or redistributed, without Harris Williams’ prior written consent. Copyright© 2013 Harris Williams & Co., all rights reserved

Frank Mountcastle Managing Director [email protected] +1 804-915-0124

Jason Bass Managing Director [email protected] +1 804-915-0132

Joseph Conner Director [email protected] +1 804-915-0151

Jershon Jones Vice President [email protected] +1 804-932-1356

Jeff Burkett Vice President [email protected] +1 804-932-1334

Contact Us