Embed Size (px)

Citation preview

Structured Finance

www.indiaratings.co.in 8 March 2013

Auto Loans

STFCL CV Trust Dec 12 - I New Issue

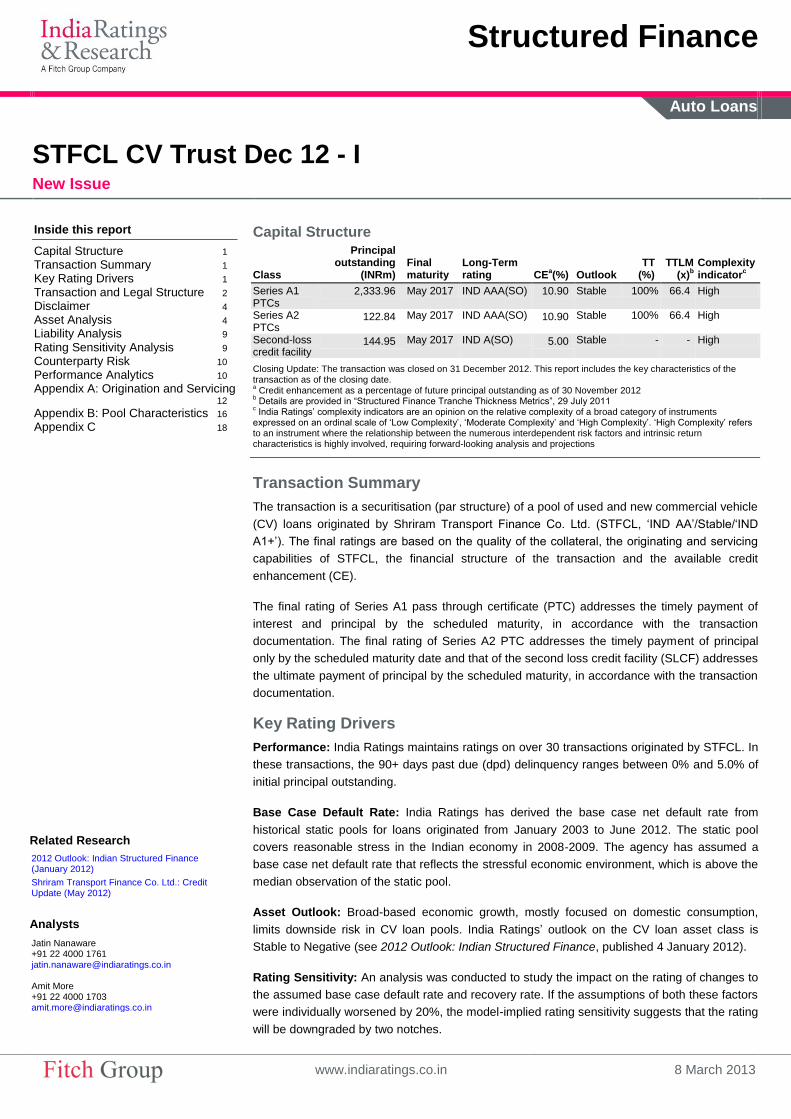

Capital Structure

Class

Principal outstanding

(INRm) Final maturity

Long-Term rating CE

a(%) Outlook

TT (%)

TTLM (x)

b Complexity indicator

c

Series A1 PTCs

2,333.96 May 2017 IND AAA(SO) 10.90 Stable 100% 66.4 High

Series A2 PTCs

122.84 May 2017 IND AAA(SO) 10.90 Stable 100% 66.4 High

Second-loss credit facility

144.95 May 2017 IND A(SO) 5.00 Stable - - High

Closing Update: The transaction was closed on 31 December 2012. This report includes the key characteristics of the transaction as of the closing date. a Credit enhancement as a percentage of future principal outstanding as of 30 November 2012

b Details are provided in “Structured Finance Tranche Thickness Metrics”, 29 July 2011

c India Ratings‟ complexity indicators are an opinion on the relative complexity of a broad category of instruments

expressed on an ordinal scale of „Low Complexity‟, „Moderate Complexity‟ and „High Complexity‟. „High Complexity‟ refers to an instrument where the relationship between the numerous interdependent risk factors and intrinsic return characteristics is highly involved, requiring forward-looking analysis and projections

Transaction Summary

The transaction is a securitisation (par structure) of a pool of used and new commercial vehicle

(CV) loans originated by Shriram Transport Finance Co. Ltd. (STFCL, „IND AA‟/Stable/„IND

A1+‟). The final ratings are based on the quality of the collateral, the originating and servicing

capabilities of STFCL, the financial structure of the transaction and the available credit

enhancement (CE).

The final rating of Series A1 pass through certificate (PTC) addresses the timely payment of

interest and principal by the scheduled maturity, in accordance with the transaction

documentation. The final rating of Series A2 PTC addresses the timely payment of principal

only by the scheduled maturity date and that of the second loss credit facility (SLCF) addresses

the ultimate payment of principal by the scheduled maturity, in accordance with the transaction

documentation.

Key Rating Drivers

Performance: India Ratings maintains ratings on over 30 transactions originated by STFCL. In

these transactions, the 90+ days past due (dpd) delinquency ranges between 0% and 5.0% of

initial principal outstanding.

Base Case Default Rate: India Ratings has derived the base case net default rate from

historical static pools for loans originated from January 2003 to June 2012. The static pool

covers reasonable stress in the Indian economy in 2008-2009. The agency has assumed a

base case net default rate that reflects the stressful economic environment, which is above the

median observation of the static pool.

Asset Outlook: Broad-based economic growth, mostly focused on domestic consumption,

limits downside risk in CV loan pools. India Ratings‟ outlook on the CV loan asset class is

Stable to Negative (see 2012 Outlook: Indian Structured Finance, published 4 January 2012).

Rating Sensitivity: An analysis was conducted to study the impact on the rating of changes to

the assumed base case default rate and recovery rate. If the assumptions of both these factors

were individually worsened by 20%, the model-implied rating sensitivity suggests that the rating

will be downgraded by two notches.

Inside this report

Capital Structure 1

Transaction Summary 1

Key Rating Drivers 1

Transaction and Legal Structure 2

Disclaimer 4

Asset Analysis 4

Liability Analysis 9

Rating Sensitivity Analysis 9

Counterparty Risk 10

Performance Analytics 10

Appendix A: Origination and Servicing 12

Appendix B: Pool Characteristics 16

Appendix C 18

Related Research

2012 Outlook: Indian Structured Finance (January 2012)

Shriram Transport Finance Co. Ltd.: Credit Update (May 2012)

Analysts

Jatin Nanaware +91 22 4000 1761 [email protected] Amit More +91 22 4000 1703 [email protected]

Structured Finance

STFCL CV Trust Dec 12 - I

March 2013 2

Data Adequacy, Criteria Application and Model

STFCL has provided India Ratings with a set of data which includes key data fields used in the

agency‟s analysis of CV loan pools. STFCL also provided the agency with loan-by-loan data for

the current pool. The static pool data provided belonged to 10 vintages from 2001 to 2012 and

contained aggregated default rates by origination month, up to June 2012. Dynamic data

exhibiting delinquency rates by parameters such as geography, loan-to-value (LTV) ratio and

internal rate of return (IRR) was also made available.

The methodology used to rate the transaction is based on India Ratings‟ India ABS Criteria

Report, Rating Criteria for Indian Asset Backed Securitisations and Structured Finance Rating

Criteria, both published 12 September 2012 (see Applicable Criteria).

India Ratings‟ analysis used two models - the simulation model and the cash flow model. The

former was used to estimate gross default from net default rates. The cash flow model was

used to test whether the stressed asset cash flows as well as the CE provided in the

transaction were able to cover timely interest and principal payments for Series A1 PTCs,

timely payment of principal for Series A2 and the ultimate payment of principal to the second

loss credit facility.

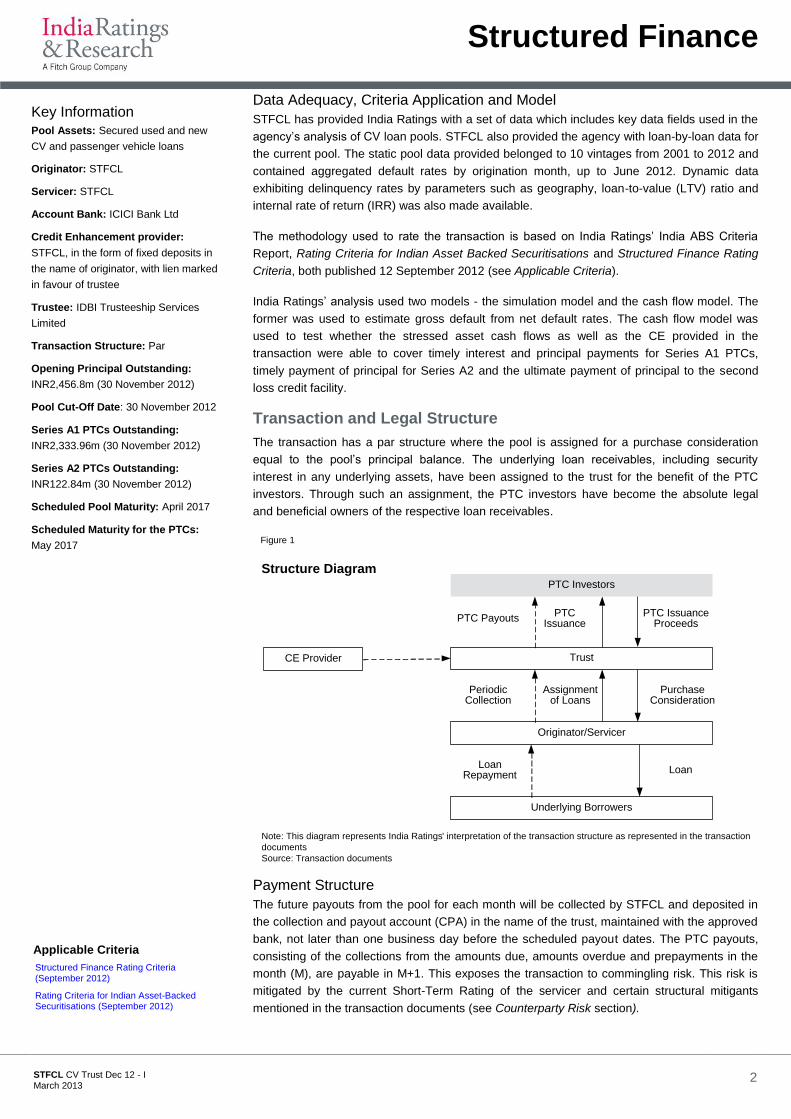

Transaction and Legal Structure

The transaction has a par structure where the pool is assigned for a purchase consideration

equal to the pool‟s principal balance. The underlying loan receivables, including security

interest in any underlying assets, have been assigned to the trust for the benefit of the PTC

investors. Through such an assignment, the PTC investors have become the absolute legal

and beneficial owners of the respective loan receivables.

Figure 1

Structure Diagram

Note: This diagram represents India Ratings' interpretation of the transaction structure as represented in the transaction

documents

Source: Transaction documents

PTC Investors

PTC PayoutsPTC Issuance

ProceedsPTC

Issuance

Trust

Periodic Collection

Assignment of Loans

Purchase Consideration

Originator/Servicer

Loan Repayment

Loan

Underlying Borrowers

CE Provider

Payment Structure

The future payouts from the pool for each month will be collected by STFCL and deposited in

the collection and payout account (CPA) in the name of the trust, maintained with the approved

bank, not later than one business day before the scheduled payout dates. The PTC payouts,

consisting of the collections from the amounts due, amounts overdue and prepayments in the

month (M), are payable in M+1. This exposes the transaction to commingling risk. This risk is

mitigated by the current Short-Term Rating of the servicer and certain structural mitigants

mentioned in the transaction documents (see Counterparty Risk section).

Key Information

Pool Assets: Secured used and new

CV and passenger vehicle loans

Originator: STFCL

Servicer: STFCL

Account Bank: ICICI Bank Ltd

Credit Enhancement provider:

STFCL, in the form of fixed deposits in

the name of originator, with lien marked

in favour of trustee

Trustee: IDBI Trusteeship Services

Limited

Transaction Structure: Par

Opening Principal Outstanding:

INR2,456.8m (30 November 2012)

Pool Cut-Off Date: 30 November 2012

Series A1 PTCs Outstanding:

INR2,333.96m (30 November 2012)

Series A2 PTCs Outstanding:

INR122.84m (30 November 2012)

Scheduled Pool Maturity: April 2017

Scheduled Maturity for the PTCs:

May 2017

Applicable Criteria

Structured Finance Rating Criteria (September 2012)

Rating Criteria for Indian Asset-Backed Securitisations (September 2012)

Structured Finance

STFCL CV Trust Dec 12 - I

March 2013 3

Priority of Payments

On the payout date, the payments will be made from the available distribution amount in the

following order of priority:

Figure 2 Summary of Payments Waterfall

1 Statutory or regulatory dues payable by assignee 2 Overdue interest payouts to Series A1 3 Overdue principal payouts to Series A1 and Series A2 PTC investor 4 Scheduled interest payouts to Series A1 PTC investor 5 Scheduled principal payouts to Series A1 and Series A2 PTC investor 6 Replenishment of SLCF to the extent of utilisation 7 Replenishment of FLCF to the extent of utilisation 8 Interest Payouts to Series A2

Source: Transaction documents

Credit Enhancement

The transaction benefits from CE in the following forms:

Any future collections against the opening overdues as of 30 November 2012 would be

available to make good any future shortfalls and form a part of CE.

The internal CE in the form of excess interest spread (EIS), which, according to the

schedule, is 9.39% of total pool principal outstanding (POS). This arises as a spread

between underlying pool IRR and scheduled coupon to be paid to PTC investors.

The external CE of 10.90% of total POS will be made available to cover shortfalls on

account of default (90+dpd loans), temporary delinquencies (0-90 dpd loans) and pool

prepayments. The CE is divided into a first loss credit facility (FLCF) of 5.0% of total POS

and SLCF of 5.90% of total POS. The external CE is provided by the originator in the form

of fixed deposits held with an account bank.

Clean-Up Call Option

The originator/seller has a clean-up call option to repurchase fully performing residual loan

assets at par if, in aggregate, they form less than 10% of the original securitised pool balance.

This option will be applicable only to the performing assets at the sole discretion of the seller.

Legal Analysis

India Ratings reviewed the final transaction documentation to understand whether the terms

and structure of the transaction conformed to information previously received.

The key documents related to the transaction include the following:

The trust deed

The assignment agreement

The collection and servicing agency agreement

the first loss facility agreement

the second loss facility agreement

the power of attorney

The legal opinion provided by the transaction counsel opines on the following key issues:

Enforceability of documents: The transaction documents have been duly authorised,

executed and delivered and constitute legal, valid and binding obligations of the parties

thereto and are enforceable against each of them in accordance with their terms.

Adherence to the Reserve Bank of India (RBI) guidelines and true sale: The transaction

complies with the RBI Guidelines on Securitisation of Standard Assets dated 1 February

2006, 7 May 2012 and 21 August 2012. The assignment of the assets by the seller to the

Structured Finance

STFCL CV Trust Dec 12 - I

March 2013 4

trustee by way of the deed of assignment satisfies the test of a true sale as set out under

the securitisation guidelines.

Bankruptcy remoteness of assets: The assets purchased by the trustee are held by it in

trust for the benefit of the PTC holders and therefore would not form a part of the

originator‟s assets in the event of liquidation or winding up of the originator.

Bankruptcy remoteness of CE (FD) from the seller: The CE will be provided as fixed

deposits in a bank, rated at least „IND A‟/Stable by India Ratings, in the name of the

originator, to be held in trust for the benefit of trustee with a lien marked in favour of

trustee. The CE to be thus provided is bankruptcy remote from the originator. (see

Counterparty Risks section).

Valid constitution of the trust: The trust is validly constituted under the trust deed and will

be recognised as a duly constituted trust in accordance with the provisions of the Indian

Trusts Act, 1882.

Adherence to minimum retention requirement (MRR): The transaction adheres with the

MRR requirement as per the RBI‟s Securitisation Guidelines of 2012.

Disclaimer

For the avoidance of doubt, India Ratings relies, in its credit analysis, on legal and/or tax

opinions provided by transaction counsel. As India Ratings has always made clear, India

Ratings does not provide legal and/or tax advice or confirm that the legal and/or tax opinions or

any other transaction documents or any transaction structures are sufficient for any purpose.

The agency draws your attention to the disclaimer at the foot of this report, which makes it clear

that this report does not constitute legal, tax and/or structuring advice from India Ratings, and

should not be used or interpreted as legal, tax and/or structuring advice from India Ratings.

Should readers of this report need legal, tax and/or structuring advice, they are urged to

contact relevant advisers in the relevant jurisdictions.

Asset Analysis

India Ratings‟ asset analysis of the pool is based on a four-step process.

Step 1. An originator and servicer review

Step 2. Analysis of asset characteristics of the pool

Step 3. Base case assumptions are derived for three key performance variables: defaults,

recoveries and prepayments (based on historical data as well as the economic

environment and asset class outlook)

Step 4. Stressed scenarios are applied for the rating level

Originator/Servicer

India Ratings conducted a complete review of the originator/servicer of this transaction, and

such a review will typically be conducted at regular intervals. India Ratings‟ originator/servicer

review included an assessment of the origination and credit appraisal processes, the credit

underwriting process, collection and recovery processes, operational and financial stability, and

the soundness of its internal control procedures.

India Ratings has conducted the latest on-site operational review in October 2012 at Mumbai.

The agency is of the opinion that STFCL‟s origination and servicing capabilities are of an

acceptable standard. For the detailed originator and servicer review, refer to Appendix A.

The strengths and weaknesses of servicing and origination functions of STFCL are as follows:

Strengths

Increase in the number of field officers in tune with the rise in disbursement volumes in

recent years.

Structured Finance

STFCL CV Trust Dec 12 - I

March 2013 5

Officers who source the loans are also in charge of collections and a part of their salary is

linked to the collections.

Along with relationship-based credit appraisal, a thorough review of the underlying obligor

and the vehicle is conducted. STFCL maintains a valuation of around 700 products, which

is updated frequently.

Weaknesses and Mitigating Factors

The resolution of delinquent accounts is mainly focused on persuasion rather than that of

repossession. This may not be very effective in the current scenario where the earning

capacity of the obligor will be under pressure owing to a slowdown in the economy. This

weakness is mitigated by the fact that STFCL always has the option to repossess the asset

to recover the loan amount,

If the levels of originations increase beyond a certain limit, STFCL may find it difficult to

replicate the cash collection model in future. In the past, the management has proactively

increased the number of back-office personnel to address the increased level of workflow.

It is probable that if workflow increases in future, the management will take a similar action.

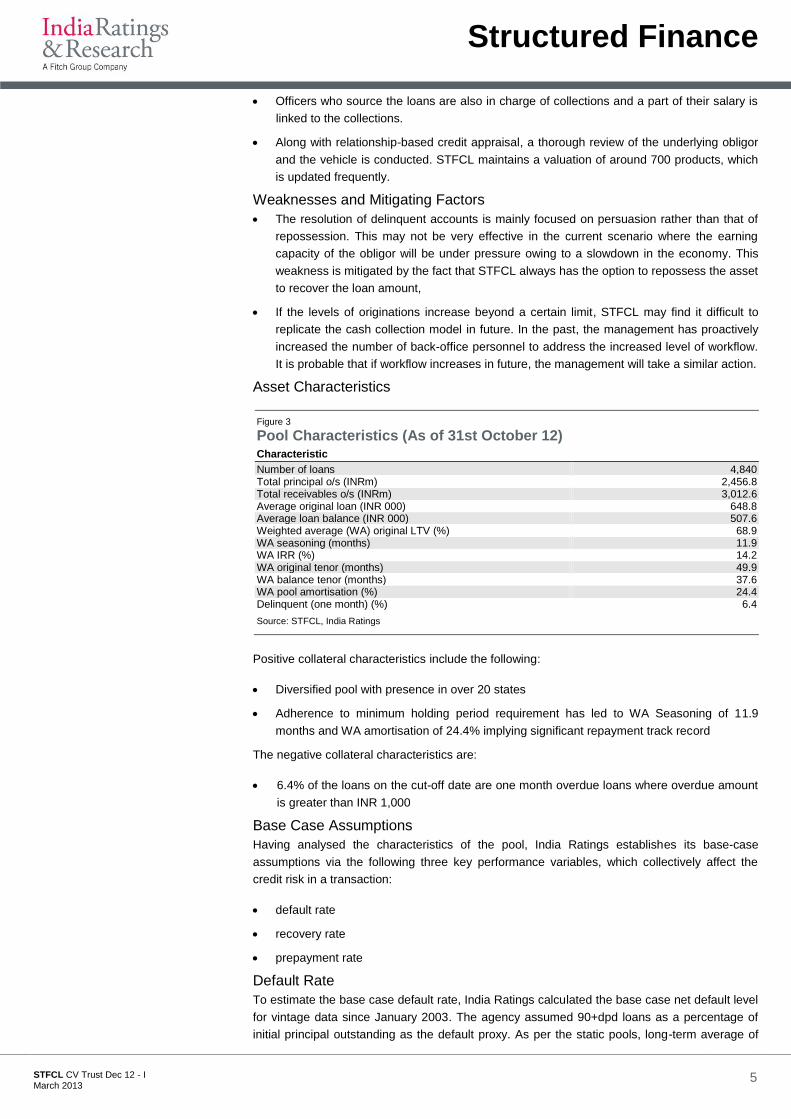

Asset Characteristics

Figure 3 Pool Characteristics (As of 31st October 12) Characteristic

Number of loans 4,840 Total principal o/s (INRm) 2,456.8 Total receivables o/s (INRm) 3,012.6 Average original loan (INR 000) 648.8 Average loan balance (INR 000) 507.6 Weighted average (WA) original LTV (%) 68.9 WA seasoning (months) 11.9 WA IRR (%) 14.2 WA original tenor (months) 49.9 WA balance tenor (months) 37.6 WA pool amortisation (%) 24.4 Delinquent (one month) (%) 6.4

Source: STFCL, India Ratings

Positive collateral characteristics include the following:

Diversified pool with presence in over 20 states

Adherence to minimum holding period requirement has led to WA Seasoning of 11.9

months and WA amortisation of 24.4% implying significant repayment track record

The negative collateral characteristics are:

6.4% of the loans on the cut-off date are one month overdue loans where overdue amount

is greater than INR 1,000

Base Case Assumptions

Having analysed the characteristics of the pool, India Ratings establishes its base-case

assumptions via the following three key performance variables, which collectively affect the

credit risk in a transaction:

default rate

recovery rate

prepayment rate

Default Rate

To estimate the base case default rate, India Ratings calculated the base case net default level

for vintage data since January 2003. The agency assumed 90+dpd loans as a percentage of

initial principal outstanding as the default proxy. As per the static pools, long-term average of

Structured Finance

STFCL CV Trust Dec 12 - I

March 2013 6

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

90+dpd

Loan Origination Month

(%)

New CV - Peak 90+dpd Trend (Origination 2003-2012)

Source: STFCL

0.0

2.0

4.0

6.0

8.0

10.0

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 55 58

(Months Since Origination)

WA 90+dpd (%) - New CV Static Pool

2003 2004 2005 2006 2007 2008 2009 2010 2011(%)

Source: STFCL

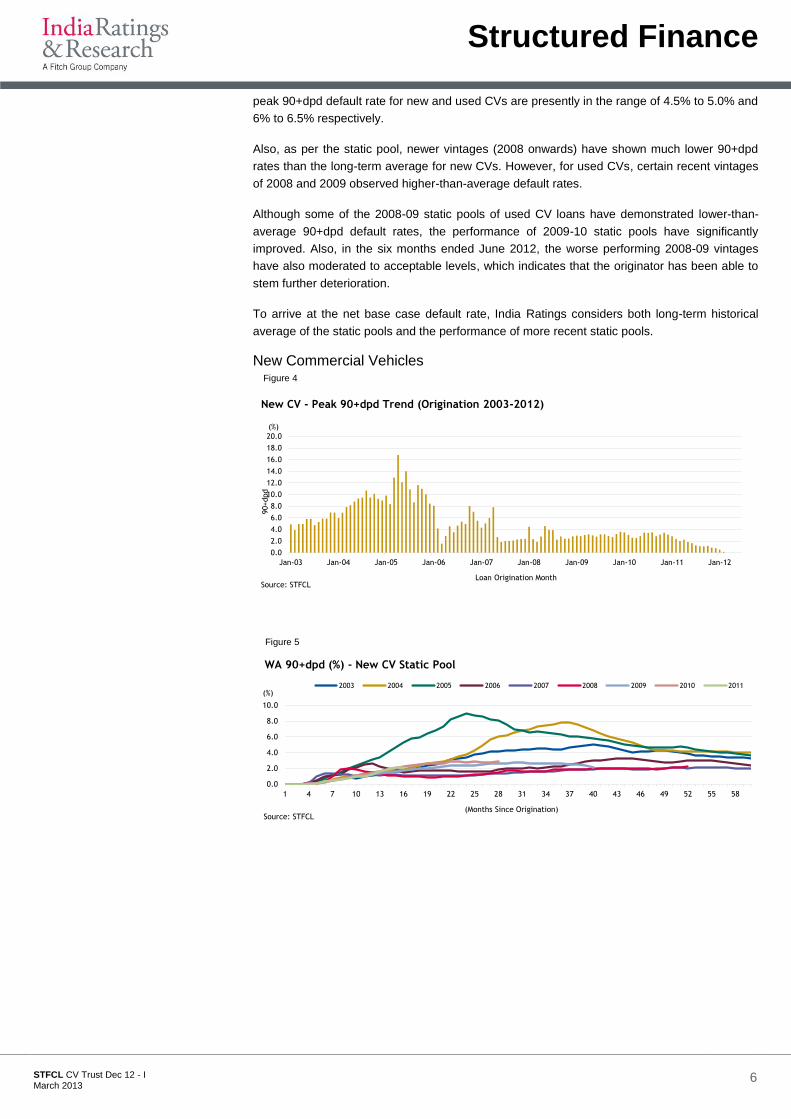

peak 90+dpd default rate for new and used CVs are presently in the range of 4.5% to 5.0% and

6% to 6.5% respectively.

Also, as per the static pool, newer vintages (2008 onwards) have shown much lower 90+dpd

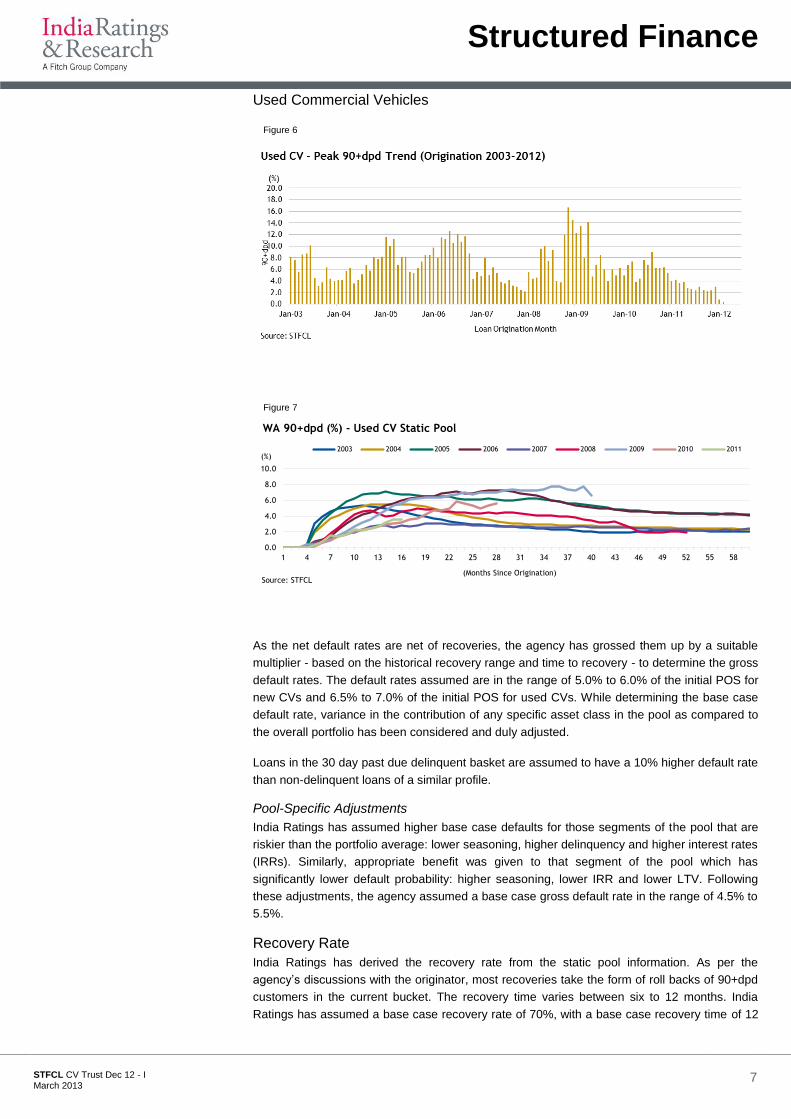

rates than the long-term average for new CVs. However, for used CVs, certain recent vintages

of 2008 and 2009 observed higher-than-average default rates.

Although some of the 2008-09 static pools of used CV loans have demonstrated lower-than-

average 90+dpd default rates, the performance of 2009-10 static pools have significantly

improved. Also, in the six months ended June 2012, the worse performing 2008-09 vintages

have also moderated to acceptable levels, which indicates that the originator has been able to

stem further deterioration.

To arrive at the net base case default rate, India Ratings considers both long-term historical

average of the static pools and the performance of more recent static pools.

New Commercial Vehicles Figure 4

Figure 5

Structured Finance

STFCL CV Trust Dec 12 - I

March 2013 7

0.0

2.0

4.0

6.0

8.0

10.0

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 55 58

(Months Since Origination)

WA 90+dpd (%) - Used CV Static Pool

2003 2004 2005 2006 2007 2008 2009 2010 2011(%)

Source: STFCL

Used Commercial Vehicles Figure 6

Figure 7

As the net default rates are net of recoveries, the agency has grossed them up by a suitable

multiplier - based on the historical recovery range and time to recovery - to determine the gross

default rates. The default rates assumed are in the range of 5.0% to 6.0% of the initial POS for

new CVs and 6.5% to 7.0% of the initial POS for used CVs. While determining the base case

default rate, variance in the contribution of any specific asset class in the pool as compared to

the overall portfolio has been considered and duly adjusted.

Loans in the 30 day past due delinquent basket are assumed to have a 10% higher default rate

than non-delinquent loans of a similar profile.

Pool-Specific Adjustments

India Ratings has assumed higher base case defaults for those segments of the pool that are

riskier than the portfolio average: lower seasoning, higher delinquency and higher interest rates

(IRRs). Similarly, appropriate benefit was given to that segment of the pool which has

significantly lower default probability: higher seasoning, lower IRR and lower LTV. Following

these adjustments, the agency assumed a base case gross default rate in the range of 4.5% to

5.5%.

Recovery Rate

India Ratings has derived the recovery rate from the static pool information. As per the

agency‟s discussions with the originator, most recoveries take the form of roll backs of 90+dpd

customers in the current bucket. The recovery time varies between six to 12 months. India

Ratings has assumed a base case recovery rate of 70%, with a base case recovery time of 12

Structured Finance

STFCL CV Trust Dec 12 - I

March 2013 8

months.

Prepayment Rate

As per the agency‟s experience in this asset class, prepayments have historically been low and

the monthly prepayment rate ranges from 0.1% to 1.0%. As per the data shared by the

originator, the monthly prepayment rate increases with seasoning. The agency also believes

that, due to low competition in CV financing, the economic slowdown, and high prepayment

penalties, it may be more difficult for obligors to refinance their loans. However, given the

availability of excess interest spread (EIS) in the transaction, India Ratings has assumed a

prepayment rate above the average prepayment rate observed to stress the EIS. The agency

has assumed a base case monthly prepayment rate of 0.25% in the first year since issuance

which increases thereafter.

Yield Compression

The agency reviewed the yield distribution of the assets in the securitised pool and assumed

that 40% of borrowers with the highest interest rate loans will either prepay or default. The

percentage reduction in the pool yield is then deducted from the month-on-month weighted-

average pool yield and applied to the interest collections in India Ratings‟ cash flow model.

Liquidity Risk

India Ratings observed the peak 0–90 day delinquencies for all static pools to determine the

liquidity shortfall the originator may face in case of a temporary delinquency, i.e., less than

90dpd.

Stress Scenarios

After developing base case assumptions for gross defaults, recoveries and prepayment rates,

India Ratings stressed these variables for the rating level.

Gross Default Rate Stresses

A stress multiple in the range of 4.0 to 5.5 is applied to the base case default rate in this

transaction. This range of stress multiple is commensurate with a „IND AAA(SO)‟ stress level

for Indian ABS ratings. The stress multiples have been benchmarked against historical peak

default data of Indian structured finance transactions.

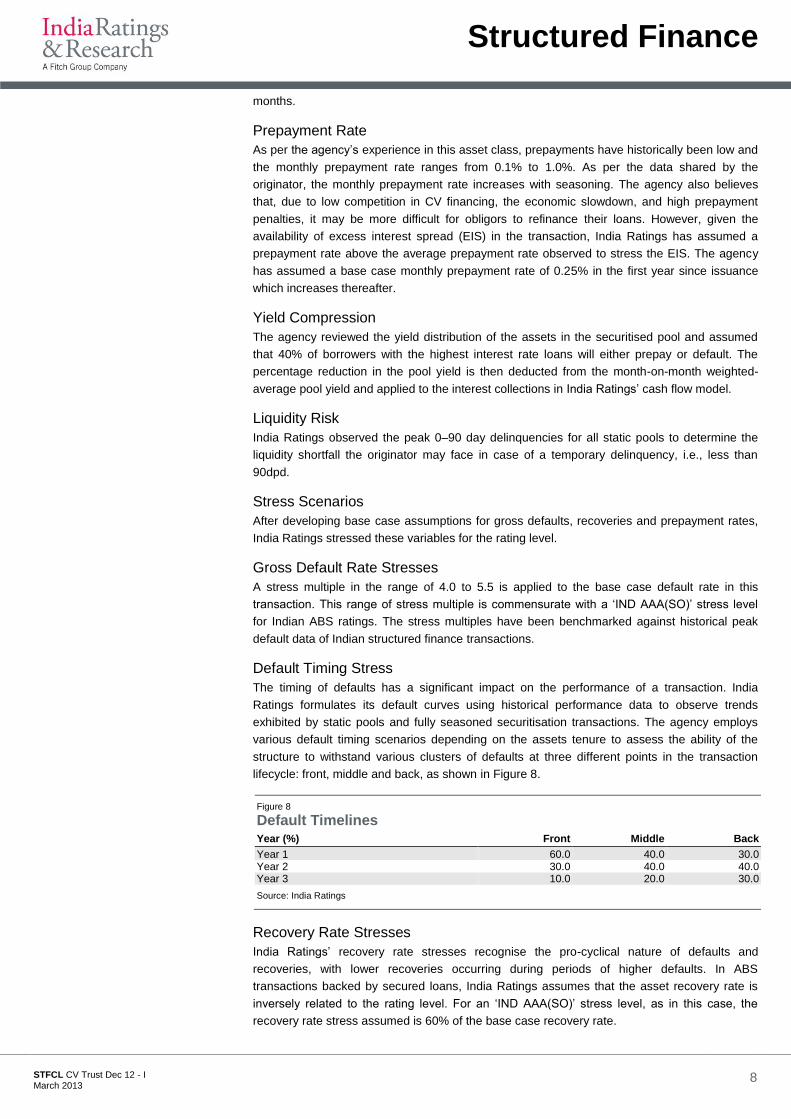

Default Timing Stress

The timing of defaults has a significant impact on the performance of a transaction. India

Ratings formulates its default curves using historical performance data to observe trends

exhibited by static pools and fully seasoned securitisation transactions. The agency employs

various default timing scenarios depending on the assets tenure to assess the ability of the

structure to withstand various clusters of defaults at three different points in the transaction

lifecycle: front, middle and back, as shown in Figure 8.

Figure 8 Default Timelines Year (%) Front Middle Back

Year 1 60.0 40.0 30.0 Year 2 30.0 40.0 40.0 Year 3 10.0 20.0 30.0

Source: India Ratings

Recovery Rate Stresses

India Ratings‟ recovery rate stresses recognise the pro-cyclical nature of defaults and

recoveries, with lower recoveries occurring during periods of higher defaults. In ABS

transactions backed by secured loans, India Ratings assumes that the asset recovery rate is

inversely related to the rating level. For an „IND AAA(SO)‟ stress level, as in this case, the

recovery rate stress assumed is 60% of the base case recovery rate.

Structured Finance

STFCL CV Trust Dec 12 - I

March 2013 9

Liability Analysis

India Ratings uses its cash flow model to test whether the stressed asset cash flows, as well as

the CE and excess interest spread provided in the transaction, are able to cover the following:

The timely interest and principal payments to Series A1

The timely principal payments to Series A2

The ultimate principal payments on the rated SLCF

Cash Flow Modelling

India Ratings‟ cash flow model considers two sides of the transaction: the assets and the

liabilities.

Key assumptions for the asset side of the cash flow model are the base case defaults, timing of

defaults, recoveries, pool yield and prepayments. These assumptions are subject to rating-

specific stresses within the cash flow model.

Stressed asset cash flows are then applied to the liability side of the cash flow model, based on

the priority of payments/waterfall set out in the transaction documentation.

In summary, the stressed asset cash flows are applied to the specified liability waterfall. The

shortfall in each period is calculated to determine whether the CE provided in the transaction

exceeds India Ratings‟ break-even CE amount.

Rating Sensitivity Analysis

This section provides an insight into the model-implied sensitivities of the transaction when

base case assumptions, with respect to one or more variables, are changed, while holding

others equal. The results below should only be considered as one of the many potential

outcomes, given that the transaction is dynamically exposed to multiple risk factors.

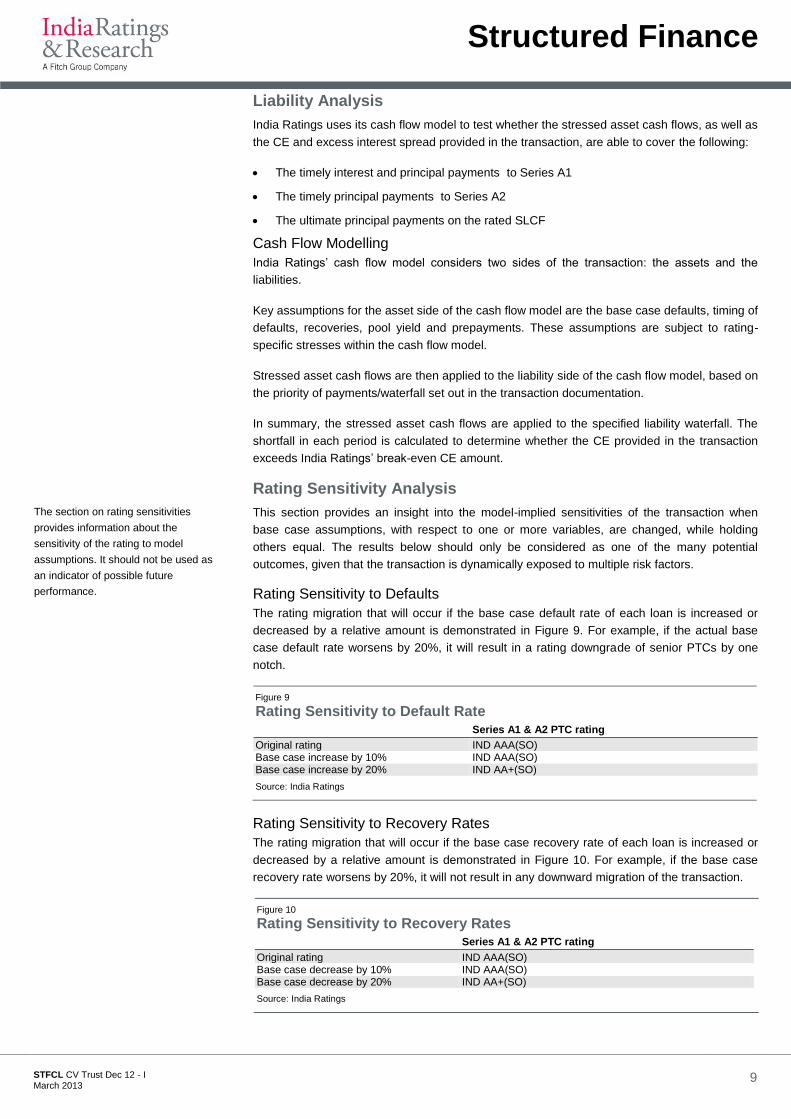

Rating Sensitivity to Defaults

The rating migration that will occur if the base case default rate of each loan is increased or

decreased by a relative amount is demonstrated in Figure 9. For example, if the actual base

case default rate worsens by 20%, it will result in a rating downgrade of senior PTCs by one

notch.

Figure 9 Rating Sensitivity to Default Rate Series A1 & A2 PTC rating

Original rating IND AAA(SO) Base case increase by 10% IND AAA(SO) Base case increase by 20% IND AA+(SO)

Source: India Ratings

Rating Sensitivity to Recovery Rates

The rating migration that will occur if the base case recovery rate of each loan is increased or

decreased by a relative amount is demonstrated in Figure 10. For example, if the base case

recovery rate worsens by 20%, it will not result in any downward migration of the transaction.

Figure 10 Rating Sensitivity to Recovery Rates Series A1 & A2 PTC rating

Original rating IND AAA(SO) Base case decrease by 10% IND AAA(SO) Base case decrease by 20% IND AA+(SO)

Source: India Ratings

The section on rating sensitivities

provides information about the

sensitivity of the rating to model

assumptions. It should not be used as

an indicator of possible future

performance.

Structured Finance

STFCL CV Trust Dec 12 - I

March 2013 10

Rating Sensitivity to Shifts in Multiple Factors

Figure 11 summarises the rating sensitivity attributed to stressing default rate and recovery rate

assumptions concurrently.

Figure 11 Rating Sensitivity to Multiple Factors (Default Rate and Recovery Rate)

Default rate

Recovery rate Base case Base case + 10% Base case + 20%

Base case IND AAA(SO) IND AAA(SO) IND AA+(SO) Base case – 10% IND AAA(SO) IND AA+(SO) IND AA(SO) Base case – 20% IND AA+(SO) IND AA(SO) IND AA(SO)

Source: India Ratings

Counterparty Risk

Credit Enhancement Provider

The CE is maintained as fixed deposits in the account bank in the name of the CE provider

(STFCL) and with lien marked to the trustee. The counterparty risk is mitigated by a rating

trigger incorporated in the transaction documents. If the CE provider is downgraded below „IND

A‟/„IND A1‟ publicly or privately by India Ratings, the fixed deposit accounts will be transferred

in the name of the trustee within 30 calendar days.

Servicer

The agency recognises the importance of the servicing counterparty role fulfilled by STFCL

(„IND AA‟/„IND A1+‟) in the performance of the underlying loan portfolio.

The transaction documents contain a servicer replacement event, where, if the servicer‟s rating

falls below „IND A1‟ or „IND A‟, the trustee will have an option to replace the existing servicer

with a new servicer within 30 calendar days.

Since the collections from the borrowers remain with the servicer for one month, the transaction

is exposed to commingling risk. The transaction documents contain a rating trigger to mitigate

this commingling risk. As per this trigger, if the servicer‟s rating falls below „IND A1‟ or „IND A‟,

the collections from borrowers are to be deposited in the Collection and Payout Account on a

daily basis.

The transaction document also contains a second trigger, whereby if the servicer is

downgraded below „IND A2‟ and „IND BBB‟, and if requested by the investor, the servicer will

perform either of the following two actions:

Inform the obligors to make all payments due under the loan agreements to the assignee

directly

Post collateral for one month exposure to cover commingling risk

Account Bank

The originator has provided the CE to be in the form of fixed deposits with account bank (the

designated bank) in the name of the originator, with lien marked to the trustee. If the

designated bank is downgraded below „IND A‟/„IND A1‟, publicly or privately, by India Ratings,

the seller will ensure that the CE is placed with another bank whose rating is equivalent to or

higher than „IND A‟ within 30 calendar days.

Performance Analytics

India Ratings initiates surveillance only once final ratings have been assigned to a transaction.

The agency has a dedicated team of analysts who monitor and review Indian ABS transactions

rated by India Ratings. Clear and timely reporting is essential to assess the performance of a

transaction and form an accurate credit view.

Structured Finance

STFCL CV Trust Dec 12 - I

March 2013 11

India Ratings expects the report from the servicer to provide the following information with

respect to collections from the pool contracts during the previous month:

Billed amount to the borrowers

Actual collections from borrowers towards this billed amount during the month

The amount and number of contracts of prepayments/advance payments from the

borrowers

Ageing analysis of overdues

Debits from and credits to the cash collateral account and credits to the CPA

Actual payments made to the series A1 and Series A2 PTCs

Any prepayments from borrowers or foreclosures (number of contracts and amounts

obtained thereto)

Revised cash flow schedule

Contract details

Structured Finance

STFCL CV Trust Dec 12 - I

March 2013 12

Appendix A: Origination and Servicing

Originator Profile

STFCL is the flagship non-banking finance company of the Shriram group, and is one of the

largest financiers of CVs in India with more than 525 branches and few franchisees (63% of

which are in western and southern India). The Shriram group has diversified interests,

spreading across financial services industries which include consumer and commercial finance,

financial product distribution, „chit‟ funds (pooled saving schemes among individuals) and life

insurance. The group also promotes and manages several companies in industrial and

manufacturing sectors.

Over the years, STFCL has built up strong disbursement and collection skills in the „small

operator segment of the business. The small operator segment comprises non-fleet operators

who own no more than five vehicles and source their business from fleet operators. STFCL‟s

business focuses on creating knowledge of each type of asset ranging from light commercial

vehicles to heavy commercial vehicles and tippers and also building close relationships with

truckers to enhance business. The gross NPA has been in the range of 1.6%-2.3% and is less

than auto finance companies that are also auto/CV manufacturers. In the used CV segment,

STFCL has a market share of over 20%.

STFCL‟s mainstay business segment is used CVs. With a strong operating history and a limited

number of players in the market, STFCL dominates used CV financing with virtually no

competition. However, in the new vehicle financing business, it is constrained by a lot of

competition from private banks and manufacturing finance companies. In the financing

segment, customers look for a quicker turnaround; hence the opportunity cost attached for

financing companies is high but most rely on the loyalty of customers and expect repeat

business. The used CV segment of five to 15 year-old vehicles is primarily dominated by

STFCL as few financing options are available in the market. However, in the one to seven-

year-old segment, more financing options are available, making the market more competitive.

As pointed out by STFCL, customers who have financed old CVs gradually progress to finance

new CVs.

Origination

STFCL has classified the geographical regions in the following manner: north, east, west, south

and central. STFCL, based on its 30 years of experience, has demarcated regions that have

traditionally higher credit risk for each asset class, to keep defaults in check. In addition to the

branches, the company follows the franchise model where it has a profit sharing and first loss

default guarantee (FLDG) arrangement with the franchisee operator. There are around 500

franchisees spread across India. These franchisees originate on behalf of STFCL by not only

financing other asset classes, such as autos and three wheelers, but also helping STFCL to

penetrate into new customer bases.

STFCL‟s customer base comprises small road transport operators (SRTOs) who have few

supporting documents or sufficient proof of income since they operate in an unorganised

sector. In such a situation, it is imperative to maintain close relationships with customers.

STFCL‟s field executives/product executives are not only responsible for origination but also for

collections for cases referred by them. Each of the field executives/product executives

manages a specific product and handles around 150 accounts. With increasing origination

volumes, the executive count was scaled up to close to 15,000 in September 2012 from 4,952

in FY07. The field executives frequently visit the trucking clusters (which are catchment areas

for contacting truckers) and those locations where the load tendering happens.

The company‟s origination practices therefore primarily focus on the customer profile, the

territory of operation and the product it is financing.

Credit Appraisal

The company‟s credit appraisal process has two components: fixed policy and variable policy.

Structured Finance

STFCL CV Trust Dec 12 - I

March 2013 13

The fixed policy applies to all retail loan advances and the variable policy applies to each asset

class (based on the characteristics of the asset class and the expertise STFCL has built in

evaluating such asset class).

Each branch is managed by a credit executive who reports to the credit manager at the

strategic business unit (SBU) level. The product executive sources the business, collects all the

required information as per the company procedure, and forwards the credit application to the

credit executive. In case of any waivers from the prescribed credit policy, the product executive

must seek exemptions from the product manager or above. The company has a credit template

for each asset that it finances, which is suitably modified by the credit risk team regularly based

on updated information.

Credit approval is only given following an applicant‟s interview with the branch manager, and

the sanction period is normally two to three days.

Since the company concentrates on lending to SRTOs, branches are instructed to keep the

total exposure to a single operator to less than INR2.5m. The company follows the policy of not

financing over five vehicles to the same borrower at any point in time. Bulk financing of this kind

involve the decision of the SBU head. Any deviation from the norm is analysed and corrective

action is taken by the SBU head during regular visits to the branches. Each branch manages

around 1,000-1,200 agreements with a team of five to six field officers. If the number of

advances crosses the threshold, a new centre is established to cater the increased demand.

Credit Underwriting

The process starts with the product executive sourcing a loan applicant. The product executive

is an expert in one asset class and therefore has a good understanding of the application and

end-use of the product. For each used vehicle, the product executive prepares a dossier which

includes the following documents and information:

1. Insurance policy of the used vehicle

2. Travel permit of the vehicle

3. Tax challan of the vehicle

4. B-extract of the vehicle: The B-extract gives the complete details of the vehicle such as its

past owners, the date of registration and its permit, and its status on tax payments. If the

vehicle has been involved in any violation of the laws, the B-extract is withheld by the

Regional Transport Office.

5. A physical verification report of the vehicle, which includes the health of its engine,

gearbox, chassis and tyres along with a photograph

6. Viability chart, which is a projection of the cash flows that would be generated by the

applicant given the contracts he/she has with other fleet operators, the route that he/she

normally operates and the freight rates applicable for such routes

7. Valuation of the vehicle: The company maintains valuations for 700 different models.

These are updated on a quarterly basis based on new information regarding model

performance, new model launches and other business environment variables.

A physical inspection of the vehicle is carried out by a trained field officer and product

executive. The finance is primarily based on the condition of the vehicle and its model type. In

certain specific cases, a valuation report is also sought. The average LTV for the old CV

portfolio is in the range of 60-70% while for new CVs, it is around 90%. For new vehicles,

STFCL only finances the chassis and not the full body.

The details are then sent to the credit executive. The credit executive makes reference checks

on the applicant from the circle of traders he/she normally does business with and also from the

place of residence of the applicant.

Structured Finance

STFCL CV Trust Dec 12 - I

March 2013 14

The group„s policy is to provide cheaper financing to customers who have a clean track record

with the company, or those applicants who are guaranteed by an existing customer of the

company (who has a clean track record). In case the customer is new and/or the guarantor is

not an existing customer of the company, the financing is costlier or the loan advanced is lower

as a percentage of the asset value.

If the documents are found to be in order, the applicant is invited for an interview with the

branch manager. The final approval is given by the branch manager only after a face-to-face

meeting with the applicant.

The company gains comfort from the fact it has in-depth information about the region and

cluster of operation.

The loan granted by STFCL has twofold protection; one is by way of a full charge on the

vehicle of the borrower and the other is by way of a guarantee provided by existing STFCL

customers (people who have already taken a loan from STFCL) for the new borrower. In case

of default by the new borrower, STFCL also has a full charge on the guarantor‟s vehicle.

The tenor of new CV loans is generally around four to five years, while that of the old CV loans

is for around three to four years. Typically, the loan ticket size for old CVs ranges from

INR50,000 to INR500,000, whereas for new CVs, the loan ticket size ranges from INR500,000

to INR1,500,000. For the first year, the depreciation for popular models is around 20%, while

for less popular models it is approximated at 30%. For subsequent years, depreciation is

assumed to be 10% for both kinds of vehicles.

Servicing and Collection

The servicing function at STFCL is highly dependent on the close relationship with each

customer. At the time of origination, a payment schedule is furnished to the borrower. The

company sends periodic statements to customers for payment receipt confirmation. While

making site visits to the trucking clusters, the field executives make themselves aware of the

general business environment, the freight rates and the specific customers who may be facing

difficulties in sourcing business, or those whose vehicles may have broken down or been

impounded by the law enforcement authorities. The servicing at STFCL is active in that the

collections team does not always have to depend on a missed payment before they initiate

action.

Loan collection is conducted in essentially two ways: cash and cheques. The collections are

either conducted by field executives on their trips to the clusters or made when customers visit

the branch to pay their monthly instalments branch to pay their monthly instalments. The

compensation structure for the field executives is based on three components: fixed salary,

sales generated and collection performance. One field executive at STFCL is typically given the

responsibility of tracking the collections for around 150 contracts. In case the field executive is

not able to collect dues from a delinquent customer, it is the responsibility of the other officers

at the branch along with the branch manager, to make collections. In case of late payment,

STFCL charges penal interest.

STFCL repossesses vehicles only as the last resort and prefers to bring the customer to the

negotiating table. The overall strategy is to let the vehicle run with the original owner as, in

STFCL‟s view, this improves the probability of the loan getting repaid.

Investor Accounting/Custodial Account Management

The monthly reports are subject to three layers of verification within STFCL. The first layer

check is performed by the accounts team, the second layer check by the finance team and the

third layer check is performed by the internal audit function.

Data Surveillance

Surveillance at STFCL keeps track of 90+ dpd loans in the first year. This is a primary

Structured Finance

STFCL CV Trust Dec 12 - I

March 2013 15

parameter that is studied every month to understand the quality of origination and servicing of

the loans on a continual basis. STFCL also monitors its information as regards the performance

of each asset class to update the valuation for each asset class it is financing.

Information Management

STFCL developed a FoxPro-based information management system in the 1990s, wherein

information was collected at individual collection points and aggregated, with a lag. Critical data

points related to client background and history were not part of this system, which continued to

operate until 2006.

Thereafter, STFCL developed an in-house web-based ERP application called UNO that runs

on Microsoft SQL 2008 and .Net 4.0. UNO is designed, developed and managed by Shriram

Value Services and Take Solutions.

The data centre primary site is in Chennai and the secondary disaster recovery site is in

Mumbai. The data at the Chennai Data Centre is replicated to Mumbai Disaster Recovery

Centre on an online basis. The data is also replicated to the Mumbai head-office for data back-

up.

Recruitment and Training

Field officers are recruited locally and are trained for six months before they are given field

responsibility. Their performance is reviewed periodically.

Marketing and Future Strategy

The company does not actively advertise through television or other popular media. Most of the

clients are SRTOs and STFCL intends to build its clientele through a referral marketing

strategy, wherein an existing client, with a strong track record, guarantees the new client. The

product type by asset class, make and model type is well diversified.

Structured Finance

STFCL CV Trust Dec 12 - I

March 2013 16

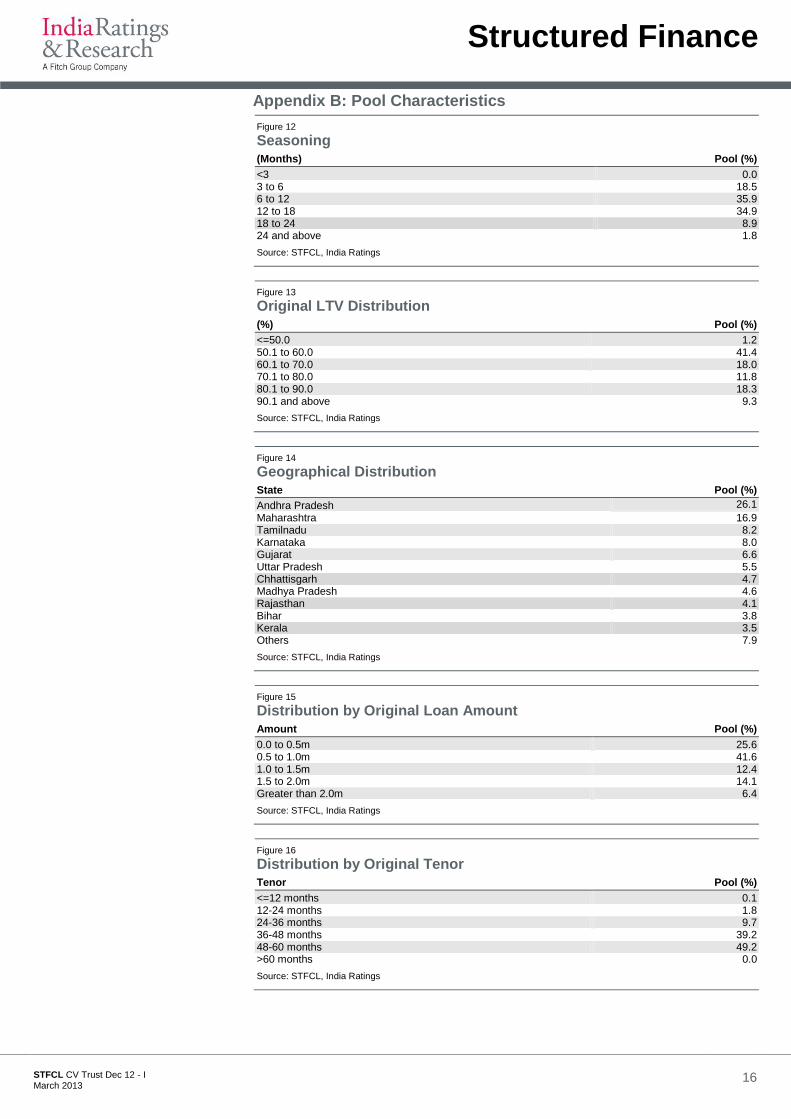

Appendix B: Pool Characteristics

Figure 12 Seasoning (Months) Pool (%)

<3 0.0 3 to 6 18.5 6 to 12 35.9 12 to 18 34.9 18 to 24 8.9 24 and above 1.8

Source: STFCL, India Ratings

Figure 13 Original LTV Distribution

(%) Pool (%)

<=50.0 1.2 50.1 to 60.0 41.4 60.1 to 70.0 18.0 70.1 to 80.0 11.8 80.1 to 90.0 18.3 90.1 and above 9.3

Source: STFCL, India Ratings

Figure 14 Geographical Distribution State Pool (%)

Andhra Pradesh 26.1

Maharashtra 16.9 Tamilnadu 8.2 Karnataka 8.0 Gujarat 6.6 Uttar Pradesh 5.5 Chhattisgarh 4.7 Madhya Pradesh 4.6 Rajasthan 4.1 Bihar 3.8 Kerala 3.5 Others 7.9

Source: STFCL, India Ratings

Figure 15

Distribution by Original Loan Amount Amount Pool (%)

0.0 to 0.5m 25.6 0.5 to 1.0m 41.6 1.0 to 1.5m 12.4 1.5 to 2.0m 14.1 Greater than 2.0m 6.4

Source: STFCL, India Ratings

Figure 16

Distribution by Original Tenor Tenor Pool (%)

<=12 months 0.1 12-24 months 1.8 24-36 months 9.7 36-48 months 39.2 48-60 months 49.2 >60 months 0.0

Source: STFCL, India Ratings

Structured Finance

STFCL CV Trust Dec 12 - I

March 2013 17

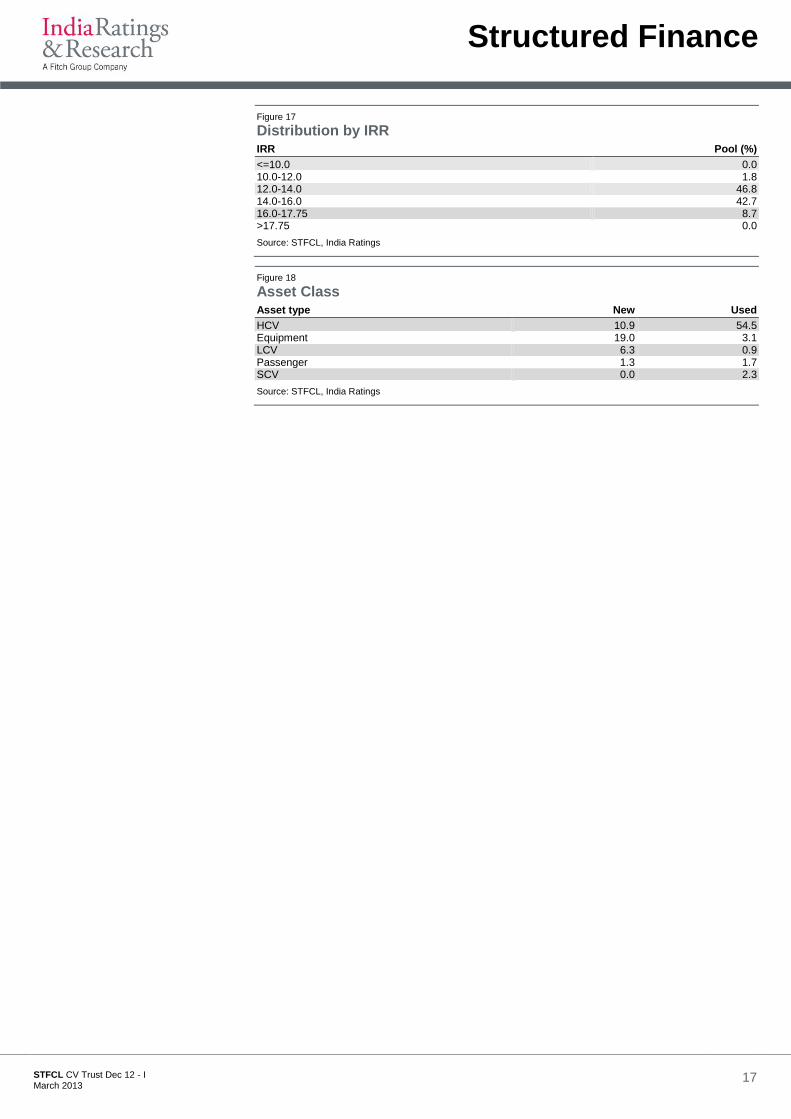

Figure 17

Distribution by IRR IRR Pool (%)

<=10.0 0.0 10.0-12.0 1.8 12.0-14.0 46.8 14.0-16.0 42.7 16.0-17.75 8.7 >17.75 0.0

Source: STFCL, India Ratings

Figure 18 Asset Class Asset type New Used

HCV 10.9 54.5 Equipment 19.0 3.1 LCV 6.3 0.9 Passenger 1.3 1.7 SCV 0.0 2.3

Source: STFCL, India Ratings

Structured Finance

STFCL CV Trust Dec 12 - I

March 2013 18

Appendix C

Figure 19 Deal Comparison

Transaction name STFCL DA

March 2012 - 02 STFCL CV Trust

Nov 12 - II Small Operators

Trust 2013 STFCL CV Trust

Dec 12 - I

Asset class (%) New CV: 9.3;

Used CV: 21.7; New tractor:11.1;

Used tractor:54.4;

New pssgr:2.0; Used pssgr:1.5

New CV: 18.7%; Used CV: 75.5%; New Pssgr:1.2%; Used Pssgr:4.6%

New CV: 18.2%; Used CV: 75.5%; New Pssgr:3.7%; Used Pssgr:2.7%

New CV: 36.2%

Used CV: 60.8%

New Pssgr: 1.3%

Used Pssgr: 1.7%

WA original LTV (%) 64.0 62.7 65.4 68.9 WA original tenor (months)

37.3 51.9 50.2 49.9

WA seasoning (months) 4.0 14.0 12.4 11.9 Pool amortised (%) 8.7 28.5 25.6 24.4 WA IRR (%) 26.2 14.1 14.7 14.2 Loans delinquent (%) 18.0 8.9 7.8 6.4 Transaction structure Par Par Par Par CE (% POS) 12.50 10.85 10.50 10.90

pssgr: Passenger vehicle Source: India Ratings

Structured Finance

STFCL CV Trust Dec 12 - I

March 2013 19

ALL CREDIT RATINGS ASSIGNED BY INDIA RATINGS ARE SUBJECT TO CERTAIN LIMITATIONS AND DISCLAIMERS. PLEASE READ THESE LIMITATIONS AND DISCLAIMERS BY FOLLOWING THIS LINK: HTTP://WWW.INDIARATINGS.CO.IN/UNDERSTANDINGCREDITRATINGS.JSP IN ADDITION, RATING DEFINITIONS AND THE TERMS OF USE OF SUCH RATINGS ARE AVAILABLE ON THE AGENCY'S PUBLIC WEBSITE WWW.INDIARATINGS.CO.IN. PUBLISHED RATINGS, CRITERIA, AND METHODOLOGIES ARE AVAILABLE FROM THIS SITE AT ALL TIMES. INDIA RATINGS‟ CODE OF CONDUCT, CONFIDENTIALITY, CONFLICTS OF INTEREST, AFFILIATE FIREWALL, COMPLIANCE, AND OTHER RELEVANT POLICIES AND PROCEDURES ARE ALSO AVAILABLE FROM THE CODE OF CONDUCT SECTION OF THIS SITE.

Copyright © 2012 by Fitch, Inc., Fitch Ratings Ltd. and its subsidiaries. One State Street Plaza, NY, NY 10004.Telephone: 1-800-753-4824, (212) 908-0500. Fax: (212) 480-4435. Reproduction or retransmission in whole or in part is prohibited except by permission. All rights reserved. In issuing and maintaining its ratings, India Ratings & Research (India Ratings) relies on factual information it receives from issuers and underwriters and from other sources India Ratings believes to be credible. India Ratings conducts a reasonable investigation of the factual information relied upon by it in accordance with its ratings methodology, and obtains reasonable verification of that information from independent sources, to the extent such sources are available for a given security or in a given jurisdiction. The manner of India Ratings factual investigation and the scope of the third-party verification it obtains will vary depending on the nature of the rated security and its issuer, the requirements and practices in the jurisdiction in which the rated security is offered and sold and/or the issuer is located, the availability and nature of relevant public information, access to the management of the issuer and its advisers, the availability of pre-existing third-party verifications such as audit reports, agreed-upon procedures letters, appraisals, actuarial reports, engineering reports, legal opinions and other reports provided by third parties, the availability of independent and competent third-party verification sources with respect to the particular security or in the particular jurisdiction of the issuer, and a variety of other factors. Users of India Ratings‟ ratings should understand that neither an enhanced factual investigation nor any third-party verification can ensure that all of the information India Ratings relies on in connection with a rating will be accurate and complete. Ultimately, the issuer and its advisers are responsible for the accuracy of the information they provide to India Ratings and to the market in offering documents and other reports. In issuing its ratings India Ratings must rely on the work of experts, including independent auditors with respect to financial statements and attorneys with respect to legal and tax matters. Further, ratings are inherently forward-looking and embody assumptions and predictions about future events that by their nature cannot be verified as facts. As a result, despite any verification of current facts, ratings can be affected by future events or conditions that were not anticipated at the time a rating was issued or affirmed.

The information in this report is provided "as is" without any representation or warranty of any kind. A rating provided by India Ratings is an opinion as to the creditworthiness of a security. This opinion is based on established criteria and methodologies that India Ratings is continuously evaluating and updating. Therefore, ratings are the collective work product of India Ratings and no individual, or group of individuals, is solely responsible for a rating. The rating does not address the risk of loss due to risks other than credit risk, unless such risk is specifically mentioned. India Ratings is not engaged in the offer or sale of any security. All India Ratings reports have shared authorship. Individuals identified in a India Ratings report were involved in, but are not solely responsible for, the opinions stated therein. The individuals are named for contact purposes only. A report providing a rating by India Ratings is neither a prospectus nor a substitute for the information assembled, verified and presented to investors by the issuer and its agents in connection with the sale of the securities. Ratings may be changed or withdrawn at any time for any reason in the sole discretion of India Ratings. India Ratings does not provide investment advice of any sort. Ratings are not a recommendation to buy, sell, or hold any security. Ratings do not comment on the adequacy of market price, the suitability of any security for a particular investor, or the tax-exempt nature or taxability of payments made in respect to any security. India Ratings receives fees from issuers, insurers, guarantors, other obligors, and underwriters for rating securities. The assignment, publication, or dissemination of a rating by India Ratings shall not constitute a consent by India Ratings to use its name as an expert in connection with any registration statement filed under the United States securities laws, the Financial Services and Markets Act of 2000 of The United Kingdom, or the securities laws of any particular jurisdiction including India. Due to the relative efficiency of electronic publishing and distribution, India Ratings research may be available to electronic subscribers up to three days earlier than to print subscribers.

The ratings above were solicited by, or on behalf of, the issuer, and therefore, India Ratings has been compensated for the provision of the ratings.