Embed Size (px)

Citation preview

STRATEGIC HOUSING MARKET

ASSESSMENT UPDATE

MOLE VALLEY DISTRICT COUNCIL

Cobweb Consulting

Final report

December 2020

CONTENTS

Executive summary 1

Chapter 1 Introduction 6

Chapter 2 Policy context 8

Chapter 3 Housing needs assessment 19

Chapter 4 Affordable housing needs 38

Chapter 5 Housing requirements of specific groups 62

Appendix 1 Mole Valley and the Gatwick Diamond 107

1

EXECUTIVE SUMMARY

Housing needs assessment

• Applying the current standard housing need assessment methodology leads to a housing need

of 453 dwellings per annum in Mole Valley.

• We also ran two alternative scenarios. Alternative Scenario 1 uses the approach set out in NPPG

standard methodology, apart from using the latest ONS 2018-based household projections. This

produces an estimate of housing need of 194 dwellings per annum.

• Alternative Scenario 2 applies the government’s standard national methodology as set out in its

August 2020 consultation. This produces an estimate of 563 dwellings per annum.

• Many local authorities in the South East region experience large increases in assessed need

under this proposed new algorithm. There has been considerable concern about this, and it is

likely that a decisions to ‘rebalance’ the regional approach will emerge. The Council should

monitor this to ensure it uses the most up to date methodology.

• NPPF and NPPG require that local authorities should use the standardised need assessment

methodology, drawing on MHCLG’s 2014-based household projections, to calculate the level of

housing need in their areas unless there are exceptional circumstances. No exceptional

circumstances have been identified in Mole Valley.

• The recommended breakdown of new private sector market dwellings by size is 25% one-

bedroomed units, 45% two-bedroomed units, 20% three-bedroomed units, and 10% four-

bedroomed units. It is also recommended that 25% of new completions should be in the form

of flats and apartments.

• The assessment of need figure is an important consideration in local planning, but a range of

other matters, including the requirement for affordable housing and the availability of sites for

housing will need to be considered by the Council in arriving at a decision about the target level

of new housing provision to be included in its local plan.

Affordable housing needs requirement

• The need for affordable housing differs from overall new housing need. The latter is an

assessment of the amount of additional housing stock required to cater for future household

growth, using the Government’s formula. The affordable housing requirement estimates the

total amount of affordable housing required, which could be met in a variety of ways in addition

to building more homes (for example, by the reletting of existing affordable homes when

tenants leave).

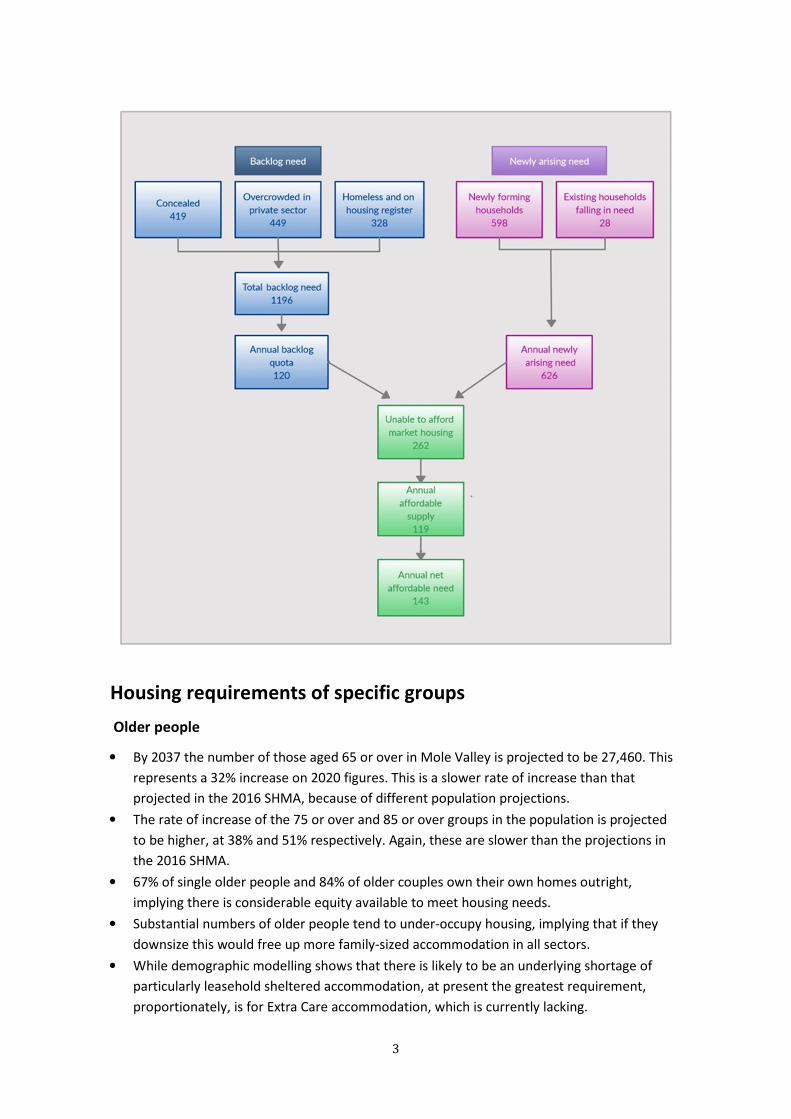

• Backlog housing need is need which exists at the start of the period for which a plan is being

prepared. It was assessed to be 1,196 households. It was assumed that backlog housing need

would be met over a ten-year period, leading to an annual quota of backlog need of 120

households.

2

• There are two additional sources of affordable housing need. The largest source is newly

forming households (598 per annum). The other is existing households not currently in need but

falling into need in the future (28 per annum).

• These three sources of need add up to an overall total of annual need of 746 households,

before taking account of the ability of these households to afford market housing.

• An estimated 262 households per annum could not afford to pay the market entry threshold

cost and therefore needed affordable housing.

• Other affordable housing thresholds were also examined. The lowest cost threshold was based

on current actual average rent levels in the social rented sector. 68 households per annum

could not afford these rents (the estimates of incomes include housing benefits) suggesting that

the housing benefit system is not helping all households to fully meet their housing costs, and

that some low income households will need to spend a higher proportion of their income on

housing than assumed.

• 52 households could afford a social rent, and a rent up to 59% of the lower quartile private rent.

They would therefore require social rented housing at or slightly above current social rent

levels.

• The next threshold was set at 60% of the lower quartile market rent, which approximates to

Affordable Rents. 87 households could afford a rent at 60-79% of the lower quartile market

rent.

• This leaves another 55 households who could afford 80-99% of the market threshold rent,

which is comparable to the costs of Shared Ownership.

• As a further indicator, housing thresholds were identified for new building dwellings by number

of bedrooms and the ability of households to purchase at these levels under the proposed First

Home mechanism was examined. 202 households could buy a first home each year, most of

whom required one or two bedroomed units. Those able to afford a larger unit would probably

have an income above the eligibility level for the scheme.

• These numbers should not be treated as exact, because a household near any one of the

thresholds might shift its demand by devoting more of its income towards housing.

• The annual supply of affordable housing units is estimated at 119 units, and deducting this

from gross need of 262 provides a net annual requirement for affordable housing of 143 units

per annum.

• There is an apparent small surplus of one-bedroomed units. Setting this aside, 50% of

affordable units should be two-bedroomed, 35% three bedroomed and 15% four-bedroomed.

• The Council’s Affordable Housing Strategy 2020-2025 indicates that there is an over-supply of

unpopular older persons’ accommodation (which is not let as supported housing) in the housing

association stock which would account for the surplus.

• The chart below summarises the process of calculating affordable need and the numbers in

need.

3

Housing requirements of specific groups

Older people

• By 2037 the number of those aged 65 or over in Mole Valley is projected to be 27,460. This

represents a 32% increase on 2020 figures. This is a slower rate of increase than that

projected in the 2016 SHMA, because of different population projections.

• The rate of increase of the 75 or over and 85 or over groups in the population is projected

to be higher, at 38% and 51% respectively. Again, these are slower than the projections in

the 2016 SHMA.

• 67% of single older people and 84% of older couples own their own homes outright,

implying there is considerable equity available to meet housing needs.

• Substantial numbers of older people tend to under-occupy housing, implying that if they

downsize this would free up more family-sized accommodation in all sectors.

• While demographic modelling shows that there is likely to be an underlying shortage of

particularly leasehold sheltered accommodation, at present the greatest requirement,

proportionately, is for Extra Care accommodation, which is currently lacking.

4

• There is a case for the authority considering facilitating more Park Homes, as a relatively

affordable option for older people.

• Looking ahead to 2040 there will need to be an additional 436 units of rented sheltered

accommodation and 1,369 leased or market rent sheltered units

• There will be a need for 384 units of Extra Care accommodation between 2020 and 2040,

73% of which should be leasehold and 27% rented.

Households with disabled members including wheelchair users

• A steady increase in the number of older people with mobility disabilities is forecast

between now and 2040 (a 42% increase), but a minor decrease is projected for working-age

people.

• Demographic modelling suggests that 174 households have an unmet need for wheelchair

accessible accommodation. Others will have accessible housing needs that may not require

full-wheelchair accessible standards.

• There is some mismatch between the numbers needing social/affordable wheelchair

accessible stock, and the allocations to that stock when it becomes available.

• We suggest further work is undertaken to look more deeply into the economic

circumstances of those potential 174 requiring such accommodation, to determine how

many or what proportion could access market products.

• But in the interim it is clear that more effective use of the social housing wheelchair

assets that come into availability be made, by ensuring they are let to those that require

wheelchair accessible accommodation.

Students

• There are over 3,700 students resident in the district during term time, including older

school students.

• 81% live with their parents. Around 14 % live in the private rented sector.

• There are currently no Higher Education establishments based in Mole Valley, though there

are a number in surrounding authorities, and London colleges and universities are easily

accessible by rail

• There are currently no plans to build any purpose-built student accommodation in the

district.

• The district is a ‘net exporter’ of students – that is, the number of residents that leave the

authority for elsewhere during term time is greater than the numbers that come in.

• In view of the above there does not seem to be a strong case for purpose-built student

accommodation to be prioritised against other demands.

Private rented sector (PRS)

• The PRS has expanded in Mole Valley by 80% between the last two Censuses and is now

likely to be providing homes for 26% of households

• Private renters, including those with children, tended to live in smaller properties than

owners, and to be more overcrowded.

• Although private renters are more economically active than average, they are slightly

more likely to be in lower-paid and less responsible jobs than average.

5

• Rents have increased by between 15% and 25% since 2011 (depending on bedsize); there

are signs that the increase rate is slowing.

• Assuming up to a third of household incomes could go on housing costs, 40% of renters

cannot afford a median rent two bedroom home.

• The number of PRS tenancies let to those claiming Housing Benefit has reduced sharply,

by 41%, since 2013; if it is becoming less of an option for those on lower incomes, this

must be of concern to the authority, particularly given the high proportion of households

with dependent children that rely upon it.

• In spite of the reduction in claims, new claimants represent 50% of net annual affordable

housing need.

• Loss of a PRS tenancy accounted for 26% of initial assessments under the Homelessness

Reduction Act 2017 in 2018-19

• To date the authority has not had to use the PRS as a source of temporary

accommodation to a great extent.

• Looking to the future, it seems likely that landlords will continue to exit the Housing

Benefit / Universal Credit sub-sector and ‘upmarket’ their offers, to the detriment of

those on lower incomes. There must be concern about access for those on the lower

end of the income spectrum, and the knock on effects on homelessness services if this

scenario arises. The authority may wish to take measure to engage with landlords

offering homes at the lower end of the price spectrum, to assist them remain in this

market

Those wishing to build their own homes

• As of September 2020, 125 individuals had registered as interested in self or custom

build under the monitoring arrangements set up under the Self-Build and Custom

Housing Building Act. However, currently only 85 of these is eligible.

• The Act expects an authority to make provision in certain circumstances for suitable

serviced plots to meet demand as evidenced by the register. Regulations in force from

2016 give authorities the option to divide the register, based on eligibility tests, including

local connection and financial viability. Only those that can pass the eligibility tests would

be entitled to district support.

• Of the 85, 34 are eligible under Part 1 of the register – that is, they have established

some form of local connection with Mole Valley and demonstrated ability to finance their

schemes.

• Of the 34, 80% currently live in the area, 50% work there, and nearly 40% have family

connections. The majority have substantial assets or access to mortgages

• There is no data available yet to indicate whether demand for self-build in Mole Valley is

relatively high or low; but in the context of other priorities for scarce land resources,

including the 564 households on the housing register, and the annual deficit of 143

affordable homes, we suggest that there is little evidence that self-build should be

prioritised above other demands.

6

Chapter 1

Introduction

Background

1.1 In August 2020 Cobweb Consulting were commissioned by Mole Valley District Council to

undertake an update of the Mole Valley section of the 2016 Strategic Housing Market Assessment

that had been produced for the Housing Market Area covering Kingston on Thames and North East

Surrey.

1.2 The commission is in the context of the authority preparing a new Local Plan and updating its

evidence base to support this.

1.3 As a supplement to this commission we were also asked to produce an update report of the

housing market linkages between Mole Valley and the Gatwick Diamond. This appears as

Appendix 1 to the main report.

1.4 Since the last SHMA, there have been significant changes to the National Planning Policy

Framework (NPPF) and National Planning Practice Guidance. The key element is a new standard

method for assessing future housing requirements. The standard method itself has undergone

several iterations.

1.5 Most of the material in the 2016 study is still relevant; this commission is an update rather

than a full SHMA. This update focusses on the assessment of housing needs, affordable housing

requirements, and housing requirements for specific groups.

1.6 All the data we use is the most up to date available at the date of writing. However, readers

should be aware that some data sets, especially the 2011 Census, will be less than contemporary.

Where possible we have tried to use more up to date data, for example using the English Housing

Survey to update information on concealed households and the proportion of Private Rented

Sector homes

Methodology

1.7 The methodology adopted was primarily a desk-based analysis of secondary data from

standard sources, as well as analysis of administrative data held by Mole Valley. To give this data

context, a series of interviews with representatives and stakeholders in different parts of the

housing market were held to validate and inform the conclusions of this report .

7

Report structure

1.8 The rest of this report is structured as follows:

• Chapter 2 The policy context

• Chapter 3 Housing needs assessment

• Chapter 4 Affordable housing needs

• Chapter 5 The housing requirements of specific groups.

• Appendix 1 Mole Valley and the Gatwick Diamond

Acknowledgements and authorship

1.9 We would like to thank our project client, Natalie Blaken of Nupremis Cambridge Ltd. Among

the many staff at Mole Valley who have helped, we would particularly thank Andy Barber, Planning

Policy Officer and Jane Smith and Duncan Clarke, Planning Policy Managers. From the housing

and environmental health teams we would like to thank Alison Wilks, Del Smith, Dina

Bouwmeester, Kirsty Jones, and Lisa Shepherd. Additionally, we would thank the stakeholders from

different sectors of Mole Valley’s housing market for their input.

1.10 This report was researched and written by Danny Friedman, Ros Grimes and Philip Leather, of

Cobweb Consulting.

8

Chapter 2

The policy context

Key messages

• National Planning Policy Framework (NPPF) requires local authorities to base their planning

policies on a local housing needs assessment, calculated using a standardised national

methodology, together with an assessment of affordable housing need.

• The methodology was changed in February 2019 to include a requirement to use the 2014-

based ONS household projections as the starting point for the standardised national

methodology.

• The government is now consulting on a further set of changes which will change the housing

methodology calculation formula and permit the use of up to date household projections.

• National Planning Practice Guidance (NPPG) no longer refers to an objective assessment of

need (OAN) or to the preparation of a strategic housing market assessment.

• The standardised national methodology for identifying housing need is not mandatory but

must be followed unless there are exceptional circumstances which suggest an alternative

approach.

• Constraints on provision such as land availability or infrastructure should not be considered

when estimating need, although they are of course relevant in developing policies.

• Total housing need should be broken down by age group, type of household, size of

household, tenure, and any special requirements (such as needs for people with disabilities

or wheelchair users).

• A separate and detailed approach to assessing the need for affordable housing is also set out

in NPPG. This has not changed substantially from previous guidance. NPPG requires the

provision of appropriate housing for older people and people with disabilities including

specialist and supported housing.

• The government is in the process of introducing a new affordable housing product known as

First Homes which will provide a discount on a dwelling purchased in the private market by

certain priority groups. The details of this scheme are still being finalised but in August 2020

the government proposed a pilot scheme of 1,500 dwellings nationally.

• At time of writing, two unprecedented areas of uncertainty surround the UK housing

market, the economy and society more widely. The first is the impact of leaving the

European Union and the second is the COVID-19 pandemic. The scope of report does not

take account of either of these uncertainties and it would be premature to do so. However,

it will be important to monitor evidence on their impact as it emerges in coming years and to

take this into account in planning policies for housing.

9

Introduction

2.1 This chapter highlights the key aspects of planning policy and guidance which this Strategic

Housing Market Assessment (SHMA) Update for Mole Valley has considered.

2.2 The National Planning Policy Framework (NPPF), originally published in 2012, sets out the

government’s principles and policies relating to planning. After remaining unchanged since its initial

publication, the NPPF was revised after consultation in July 2018, and revised again in February

2019. In August 2020 the Government published a White Paper, Planning for the future1, which sets

out further proposals for wide-ranging changes to the planning system including the process of local

plan preparation. During August and September 2020 the government held a consultation on

changes to planning policy and regulations in four areas:

• changes to the standard method for assessing local housing need.

• Transitional arrangements for First Homes sold at a discount to market price for first time

buyers including key workers.

• temporarily lifting the small sites threshold below which developers do not need to

contribute to affordable housing.

• extending the current Permission in Principle to major development.

National Planning Policy Framework (2012)

2.3 The first NPPF published in 2012, introduced a presumption in favour of sustainable

development as the underlying feature of planning policy, and set out an intention on the part of the

government to secure a significant increase in the supply of housing through the planning system.

2.4 The NPPF and planning practice guidance formally required in each area, local planning

authorities to prepare a Strategic Housing Market Assessment (SHMA). The purpose of an SHMA was

to develop a clear understanding of housing needs in an area, with neighbouring planning

authorities working together where Housing Market Areas (HMAs) crossed their boundaries. The

SHMA was required to provide a full assessment of the need for both market housing and affordable

housing, which would provide the basis for local plan policies relating to future housing supply and

to the proportion of affordable housing in new developments.

2.5 The 2016 SHMA was required to include an objective assessment of housing need (OAN)

based on robust evidence. SHMAs were required to be thorough but proportionate, and to build

where possible on secondary information sources rather than primary surveys.

2.6 NPPG was updated at intervals, but few changes were made to the guidance on housing need.

However, there was considerable volume of additional practice on Examination in Public of Local

Plans; Appeals against the refusal of individual planning applications; and the development of

Neighbourhood Plans. In addition, a body of case law emerged where applicants, local authorities or

the Secretary of State sought clarification through the Courts of the definition of OAN, and the

process of its calculation. As a result, by 2017, the assessment of the OAN within a SHMA had

become a complex and time-consuming process.

1 See MHCLG (2020) Planning for the future, White Paper August 2020, at www.gov.uk/mhclg.

10

NPPF 2018, 2019 and 2020 Changes to the Planning System consultation

2.7 The increasing concern at the cost of preparation and the extended timetable for public

examination of planning policies setting out future housing requirements led the government to

make revisions to the NPPF with the aim of reducing the complexity of the process of calculating

OAN. The new NPPF, published in July 2018, included the requirement for local authorities to use a

standard methodology for the assessment of housing need. The detail of the standard methodology

was set out in an amended version of NPPG in September 2018.

2.8 In the same month, the Office of National Statistics (ONS) published a new set of official

household projections, based on population projections using 2016 rather than 2014 as the base

year. The updated projections showed a significant reduction in the projected annual average level

of household growth in many areas across the country. The government’s objective at this time is to

achieve 300,000 new homes per year. To ensure that the planning system provided the framework

for that delivery, the government made further changes to NPPF and NPPG in 2019 to require local

authorities to continue to use the 2014-based household projections (rather than the updated 2016

projections) in assessing housing need unless there were strong reasons for not doing so.

2.9 In June 2020, ONS published a set of 2018-based household projections, using its most up to

date population forecasts. These confirmed the reduction in household numbers identified in the

previous 2016-based projections, and at national level showed a further reduction, making the 2014-

based projections which NPPG specifies are to be used in local planning even more divergent from

current trends. As a result, the government is proposing to revise its standard methodology for

assessing housing need. The new proposals published in August 2020, in ‘Changes to the Current

Planning System’, and subject to a consultation which ended on 1 October 2020, indicate the

baseline demographic need assessment which forms Step 1 of the standard methodology should use

the latest official projections, unless a percentage increase above existing local housing stock levels

results in a higher figure. At present Step 2 of the standard methodology adjusts the baseline

demographic need by a factor based on the extent to which the ratio of the median housing sale

price to median earnings for people in employment exceeds a value of 4.0. The proposed new

method retains this but adds to it a further factor which takes account of the change in this

affordability ratio over the last ten years. Currently, the housing need assessment produced by the

standard methodology is also capped to impose a limit on the extent of change in assessed need

from the level enshrined in previous local plans, but the new proposals eliminate this capping stage.

National Planning Practice Guidance

2.10 The current NPPF sets the requirement for planning authorities to prepare assessments of

housing need. NPPG provides the detail on how to carry these out:

• Firstly, an assessment of housing need, based on the standard methodology set out in the

PPG, unless there are clear reasons for adopting an alternative (NPPF para 60 and NPPG

Housing and economic needs assessment2 para 001 Reference ID: 2a-001-20190220); and

2 All subsequent references to paragraphs from PPG relate to the Housing and economic needs assessment

section of the guidance so the title of the section is omitted in these references. The guidance is published

online and is subject to continuous amendment. Paragraph references are correct at 14-07-2019.

11

• Secondly, an assessment of the current number of households and projected number of

households who lack their own housing and who cannot afford to meet their housing needs in

the market (NPPF paras 61-64 and NPPG guidance paras 018 Reference ID: 2a-018-20190220

to 024 Reference ID: 2a-024-20190220).

2.11 The current steps to derive the minimum annual local housing need are set out in Paragraph:

004 Reference ID: 2a-004-20190220 of NPPG. Step 1 is to derive the annual average number of net

additional households expected to form over a ten-year period starting at the current year from the

relevant official projections. In Step 2, this figure is adjusted using a formula based on the level of

affordability of housing in each area. In Step 3, the resulting figure is assessed to see whether it may

be subject to capping.

2.12 The guidance indicates that the standard assessment should be made at the start of the plan-

making process and that it should be revised when appropriate. The Office for National Statistics

(ONS) usually publishes revised affordability data annually and updates of household projections

every two years.

2.13 The guidance stresses that the standard assessment is an estimate of the minimum level of

need in an area, and it refers to circumstances when there may be a higher level of need (Paragraph:

010 Reference ID: 2a-010-20190220), for example:

• when economic growth strategies are in place requiring additional housing to support them

• where strategic infrastructure improvements, especially to transport infrastructure, are

planned which provide the opportunity for higher growth or require higher growth to make

them viable

• or where one authority has agreed to take on unmet need from other areas.

Housing Needs of Different Groups and Housing for Older People and People with

Disabilities

2.14 The guidance on the needs of certain groups of households has been expanded beyond that in

the previous version. The guidance now notes that the need for housing for particular groups of

people may exceed, or be proportionally high in relation to, the overall housing need figure

calculated using the standard method. This is because the needs of particular groups are calculated

for the whole population of an area , rather than from the smaller number of new households

calculated by the standard housing needs method. Hence, when producing policies to address the

need of specific groups, authorities will need to consider how the needs of individual groups can be

addressed within the constraint of the overall new housing need established. The need for particular

sizes, types and tenures of homes as well as the housing needs of particular groups should also be

considered separately from overall need (Paragraph: 017 Reference ID: 2a-017-20190220).

Affordable housing

2.15 The guidance on the need for affordable housing (PPG guidance paras 018 Reference ID: 2a-

018-20190220 to 024 Reference ID: 2a-024-20190220) has remained largely unchanged. This need

should be calculated firstly by estimating the backlog of need from people who currently occupy

12

unsuitable housing (or who cannot form separate households) together with need arising from

newly forming households in the future. Secondly, the proportion of these households who are

unable to afford market housing and who require affordable housing is calculated. The current and

future supply of affordable housing is then deducted from this requirement to produce an estimate

of net affordable need. Affordable housing need may be disaggregated into categories based on the

different types of affordable housing available, such as social or affordable rented housing,

intermediate housing or First Homes. At present, housing provided by the private rented sector is

not included.

2.16 Mole Valley Council has published an Affordable Housing Strategy 2020-25 which includes a

detailed analysis of the need for affordable housing, the supply, and policies to address affordable

need which is referred to extensively in Chapter 4. The Strategy’s overall ambition is to continue to

deliver new affordable homes and increase delivery by the council. Firstly, to increase the delivery of

affordable homes that are of sustainable construction, energy efficient and where possible have

social rents; and secondly in the longer term, with the right conditions, become a developer and

potentially a landlord of affordable/council housing.

2.17 The Strategy provides a range of actions to achieve these aims that includes maintaining the

critical partnership with housing association partners and developers and looking at alternative

methods of delivery, including the Council building new affordable homes. It also seeks to prioritise

the mitigation of climate change in the construction process and development of affordable homes

for social rent and for those with support needs, especially older people whose needs in later life

could be met by extra care housing. Opportunities through the Council’s regeneration activities,

working with parish councils and rural communities and community led groups to deliver affordable

homes are also highlighted. The Strategy will be annually reviewed, and progress reported to the

Council’s Scrutiny Committee.

Implications

2.18 The objective of this study is to produce estimates of future housing need. The current NPPF

clearly requires that these should be based on the standard methodology, unless exceptional

circumstances apply. This study complies with this requirement, providing a full explanation of the

components of the estimate and the sources used. However, we have also undertaken two

additional scenarios. Firstly, a detailed assessment of housing need using the most recent 2018-

based ONS household projections, and secondly an analysis using the new standard assessment

methodology proposed by the government in Changes to the Current Planning System, August 2020.

Consultation on these proposals is now complete but at the time of writing the government has not

announced how it intends to proceed.

National housing policy context

2.19 Government housing policy in the period since 2013 has been set in the wider context of

continuing restrictions on public expenditure driven by ‘austerity’. Interventions have focused on

methods of influencing demand and supply in the private market, rather than on direct social sector

provision. Wider reforms, seeking to reduce or contain public expenditure on the welfare benefits

system have also had, or in future will have, major impacts on housing.

13

2.20 The recovery in house prices and market transactions in the housing market after the global

financial crisis in 2008 was encouraged by a gradual easing of mortgage lending terms such as

deposit requirements and loan to income ratios. Government interventions also sought to support

the market, notably through the Help to Buy scheme, which has to date received over £10 billion of

government equity loan funding. Many commentators argue that the Help to Buy scheme has simply

stimulated price increases in the new build sector rather than increased supply. An independent

evaluation of Help to Buy for MCHLG reported limited levels of additionality in both demand and

supply. Comments in the press and from some professional bodies have been far more critical3 .

2.21 On the supply side, the emphasis of government policy has been on changes to the planning

system which the government believes will boost supply. These include measures to secure the

allocation of more land for housing and the granting of more planning permissions in areas of higher

demand. These measures include the requirement to have a 5 year land supply; the Housing Delivery

Test, the national housing need assessment methodology; and changes to the Town and Country

Planning (General Permitted Development) Order to allow certain offices to be converted into

residential units without planning consent.

2.22 The White Paper, Fixing Our Broken Housing Market published in February 2017 made the

issue of increasing the overall supply of new housing a key objective of government policy, and its

proposals to secure higher allocations of land, higher levels of planning permissions for housing, and

higher levels of build out from these permissions represented a significant step up in the scale and

range of interventions. The White Paper also included proposals for expanding the private rented

sector by attracting more institutional providers or investors. However, changes to the taxation

arrangements for private landlords are argued by some to be likely to reduce future growth in the

private rented sector, and to change the structure of the sector. The White Paper also included

proposals to make renting fairer for tenants.

The social rented sector

2.23 The social rented sector has experienced increasing challenges over the period since 2013.

Welfare reforms have sought to reduce or contain the costs to government of housing benefit

payments to social rented tenants, and to reduce levels of under-occupation in the sector. Support

for Right to Buy has also continued to reduce the social rented stock. At the same time grant or loan

finance for new development has remained generally restricted, and increasingly targeted on areas

where affordability ratios suggest that need is highest.

2.24 The Rent Standard4 governs the rents which Private Regulated Providers of Social Housing

(PRPSH) can charge their tenants. Social housing rents are based on a rent formula based on the

3 Ministry of Housing, Communities and Local Government (2018) Evaluation of the Help to Buy Equity Loan

Scheme 2017, Christine Whitehead, Peter Williams, Ipsos MORI and the London School of Economics. A report

by Morgan Stanley, The help to buy premium – and its unintended consequences, is also widely cited in press

and other commentary.

and Wilcox S and Williams P (2018) Dreams and Reality: Government finance, taxation and the private housing

market, London, Chartered Institute of Housing. 4 See Policy Statement on rents for social housing, MHCLG, Feb 2019

14

relative value of each property, relative local income levels, and the size of the property. A

requirement to reduce rents over a four-year period was introduced in 2016. From 2020 onwards,

further limitations apply to social rents. These changes have provided a way to contain housing

benefit costs, but they have posed potential future challenges to the viability of some organisations

in the sector, or to their ability to develop new housing, leading to mergers and restructuring. The

net result has been a more or less static number of social rented dwellings nationally, which in the

context of overall housing growth has led to a declining overall share. Proposals for changes to the

funding of supported housing also led to uncertainties which adversely affected development, and

some of these remain a concern for the longer term.

2.25 In 2011, the government also enabled PRPSHs to charge affordable rents which may be set at

up to 80% of local market rents inclusive of service charges). Landlords can only let new properties

at an affordable rent when they meet certain conditions. Existing vacant properties can also be

converted from social rent to affordable rent in certain circumstances. Regulations specify how an

affordable rent is to be determined and place a limit on annual increases. Since 2015 social landlords

may also charge a full market rent where a tenant household has an income of £60,000 per annum

or more and separate regulations apply to such tenants.

2.26 Following the tragedy at Grenfell Tower in 2017, the government issued A New Deal for Social

Housing, in August 2018. The Green Paper set out a series of objectives and proposals and sought

comments on reforms to social rented housing to achieve these objectives, including:

• ensuring homes are safe and decent,

• effective measures to deal with complaints and disputes

• measures to empower residents and to strengthening the Regulator,

• the tackling of stigma associated with the sector, and celebrating thriving communities

• expanding affordable housing supply with social rented homes as a springboard to home

ownership.

2.27 Shortly before leaving office the then-Prime Minister Theresa May announced that an action

plan to implement the Green Paper recommendations would be published in September 2019. No

plan has been published by the time of writing, and none of the recommendations have been

implemented. Instead, a Housing White Paper has been promised. The Secretary of State for

Housing Communities and Local Government announced in August 2020 that that work on the

White Paper has been ‘paused’ because of the pandemic5..

2.28 However, a certain amount of background work and consultation has been undertaken in the

intervening period, which will be built on when the White Paper emerges. This includes:

• Safety: implementing the Hackitt Review recommendations, which would improve building

safety standards, and testing various types of cladding, adding sprinklers and alarm systems

to existing buildings. A review of the 2006 Decent Homes Standard is also recommended.

• Complaints: Consulting on improving and streamlining the process of making complaints by

tenants, with standardised stages, and possible strengthening of the Housing Ombudsman

5 https://www.insidehousing.co.uk/news/news/social-housing-white-paper-work-paused-during-pandemic-

says-jenrick-67845

15

role.

• Empowering residents: measures suggested include landlord performance league tables,

rewarding (via the Affordable Housing Programme) good landlord performance, linking Key

Performance Indicators to regulatory judgements for housing associations, giving greater

choice to tenants through enhanced stock transfer and tenant management initiatives, and

additional tenant training and involvement in contractor selection. And strengthening the

powers of the Social Housing Regulator.

• Addressing stigma: apart from tenant consultation on this issue, there is little concrete

discussion at the moment. The final report of the Building Better, Building Beautiful

Commission, published in January 2020 highlighted the impact of high-quality design in

addressing stigma6.

• Boosting the supply of social housing and supporting home ownership: the most concrete

step taken here was to relax the barriers to local authorities building homes, through

withdrawal of the borrowing cap and more strategic investment by Homes England.

However, there are concerns that the commitment to social housing is undermined by the

proposals in the White Paper ‘Planning for the Future, published in August 20207 to scrap

Section 106 agreements, which have been the biggest sole contributor to affordable housing

development in recent years. There are also proposals to make shared ownership staircasing

possible in smaller steps.

2.27 It should be emphasised that with the exception of the few measures noted above, none of

the aspirations of the Green Paper have been realised to date. The legacy of Grenfell Tower

continues to dominate housing policy and practice, as landlords, tenants and freeholders face up to

the implications of and costs associated with non-compliance with fire safety standards, security,

and panel replacement.

Homelessness and rough sleeping

2.28 Concerns over homelessness have continued to feature in the media and in government

policy , with a recent increased emphasis arising from the rapid growth of rough sleeping in many

areas, argued by some commentators to be a result of longer-term welfare reforms. In August 2018

the government published a Rough Sleeping Strategy seeking to halve the incidence of rough

sleeping by 2022 and end it by 2027. In December 2018 this was followed by a delivery plan. Mole

Valley has benefitted from to a share of the £131,440 allocated to four East Surrey authorities under

the initiative.8 Further funding (£144,000) has been made available to the Council by MHCLG from

the Next Steps Programme in 2020/21 to continue to support, in the long term, rough sleepers

assisted by the ‘Everyone Initiative’ that commenced in March 2020 in response to the pandemic .

2.29 In 2018 the Homelessness Reduction Act 2017 placed new duties on local authorities (and

referral agencies) to help prevent homelessness and ‘relieve’ homelessness if it does occur. These

duties apply to all those in need, regardless of status, whether intentional or if they have a local

connection. They cover, for example, rough sleepers and younger single people. The measures do

6 https://www.gov.uk/government/publications/living-with-beauty-report-of-the-building-better-building-

beautiful-commission 7 https://www.gov.uk/government/consultations/planning-for-the-future 8 https://www.gov.uk/government/publications/rough-sleeping-initiative-2020-to-2021-funding-allocations

16

not go as far as placing a full rehousing duty for these applicants on the authority – that remains

within the criteria set by the 1996 Housing Act. However, it does require authorities to thoroughly

assess all applicants and provide a personalised response. Mole Valley will be publishing a new

Homelessness Strategy and Rough Sleeping Strategy 2020-2025 that at the time of writing is in draft

form. It will replace the previous Homelessness Strategy 2015-2020, which describes the problems

of homelessness and rough sleeping in the district in detail and sets out policies and initiatives to

address them.

Leaving the European Union

2.30 Any discussion of policy context needs to have regard to leaving the European Union and its

impact on housing markets. The House of Commons Library original briefing paper9 suggested

caution when looking at market changes since the vote to leave the European Union, citing global

political uncertainty and the broader UK economy as other significant factors. Nonetheless, it noted

that though initial fears of a major drop in consumer confidence and house prices were not realised,

there were concerns about the longer term, after exit from the European Union, and beyond.

2.31 Looking ahead, the longer-term housing market impact of leaving the European Union will

be intrinsically tied into the economic as well as the political impact. The variables here are

substantial: the relationship between the pound and the Euro and the cost of building materials;

changes to interest rates affecting mortgages; the ability of London to retain its international

financial role which will undoubtedly impact on areas outside but close to Greater London; the

results of single or bilateral market trade negotiations; and the wider impact of migration policy

including access to construction workers.

COVID-19 and housing markets

2.32 It is impossible, of course, to ignore the shock of the COVID-19 virus pandemic on housing

markets, policy and practice. Savills have summarised the broad-brush impact on housing markets as

follows:

In general, we can expect the pandemic to affect the housing market in a number of ways:

• General uncertainty will weigh on consumer sentiment;

• Restrictions on people’s ability to go about their day-to-day business will impede normal

estate agency, mortgage and conveyancing processes10

• Stock market falls will make people feel less secure about their personal financial situation;

and

• A negative impact on earnings, employment and wealth generation11.

2.33 There are several steps that the government and housing providers are taking or have taken

to ameliorate the situation as far as possible. These include:

9 Brexit: implications for the housing market and construction, Briefing Paper 07666, House of Commons

Library October 2016 10 At the time of writing, some restrictions on these processes have been lifted and a degree of normality has

returned to the housing market transaction process, subject to local lockdown measures. 11 https://www.savills.co.uk/research_articles/229130/298265-0/coronavirus-and-the-uk-housing-market

17

• A buffer period before private and social landlords can begin to take possession action.

• A mortgage payment ‘holiday’ for homeowners and Buy to Let landlords

• Guidance on delaying or slowing house-moves.

• The removal of Stamp Duty on the purchase of dwellings of under £500,000 until the end of

March 2021.

• The Government has written to local authorities in England asking them to house all people

sleeping rough, and those in hostels and night shelters and invested in the Next Steps

Programme.

• Furlough payment arrangements and the introduction of Self-Employed income support to

protect earnings to some extent.

• Additional personal support at a regional level, depending on the tier of lockdown

implemented

2.34 A range of estimates of the economic and housing impact of COVID-19 have now been

published and others will follow as evidence of these changes emerges12. A substantial increase in

unemployment is widely accepted as likely. Within some parts of the housing market, prices are

reported to be rising as households seek to relocate into larger dwellings or dwellings with a garden,

and to move from urban areas to suburban and more rural locations with lower housing densities,

but rising unemployment may impact on these aspirations. Mole Valley Council officers report that

there is evidence of increased levels of downsizing by older people as a result of the temporary

removal of Stamp Duty, which may increase the supply of larger units for families who are able to

afford them. A local housing association reported a dramatic increase in interest in Shared

Ownership when the first lockdown was lifted, as those trapped in ‘cooped up’ arrangements

sought alternatives. But a conclusive analysis of the impact of COVID-19 on housing markets is

impossible at this stage. This is a matter which the Council will need to monitor carefully.

First Homes

2.35 In February 2020 the government published a consultation paper on First Homes: getting

you on the ladder13. This reiterated the impact of existing measures such as Help to Buy, Right to

Buy, stamp duty relief, and the provision of support to the construction of affordable rented homes

and shared ownership homes. However, it set out a new scheme to secure First Homes on new

housing developments, which would be sold at a discount of 30% of market value, to priority groups

including key workers and serving members of the armed forces. Resales of First Homes would be

restricted to a price set at 70% of the market value at the time of sale so as to pass the discount on

to others in housing need.

2.36 In August 2020 the government published further details of the First Homes scheme taking

account of responses to the comments received. The scheme will commence with a pilot of 1,500

12 For example, https://www.pwc.co.uk/premium/covid-19/uk-economic-update-covid-19.pdf,

https://www.research.ox.ac.uk/Article/2020-04-07-the-economic-impact-of-covid-19 13 See MHCLG (2020) First Homes: getting you on the ladder, consultation in the design and delivery of First Homes.

18

First Homes. 30% will be the minimum discount, but local planning authorities will be able to require

that developers increase this to 40% or 50% if there is evidence that 30% is not enough to make

homes affordable to those in priority groups, and provided that this level of discount is viable. There

will be a price cap on First Homes of £250,000 across England outside London, making the maximum

First Home price £357,000. An assessment of the current new build sector across Mole Valley carried

out by the Council suggests that this rules out three and four bedroomed homes completely, but as

the scheme is targeted on first-time buyers this may not exclude many households. Studio and one-

and two-bedroom units should be eligible in areas such as Leatherhead and Dorking where prices

are lower and where there is an established market for them. An assessment of the affordability of

First Homes is included in Chapter 4 but this needs to be monitored carefully in the future as

experience with the new product develops.

19

Chapter 3

Housing Need Assessment

Key messages

• This chapter provides an assessment of the level of housing need in Mole Valley using the

standard national methodology, together with an assessment of how need will change as a

result of proposed changes to this methodology. It also considers other matters relevant to the

assessment of housing need.

• Applying the current standard housing need assessment methodology leads to a housing need

of 453 dwellings per annum in Mole Valley.

• Alternative Scenario 1 uses the approach set out in NPPG standard methodology, apart from

using the latest ONS 2018-based household projections. This produces an estimate of housing

need of 194 dwellings per annum.

• Alternative Scenario 2 applies the government’s proposed new standard national methodology

as set out in its August 2020 consultation. This produces an estimate of 563 dwellings per

annum.

• Many local authorities in the South East region experience large increases in assessed need

under this proposed new algorithm. It is likely that a decision on this proposal will emerge

during the period of preparation of the local plan so the Council should monitor this to ensure

it uses the most up to date methodology.

• NPPF and NPPG require that local authorities should use the standardised need assessment

methodology, drawing on MHCLG’s 2014-based household projections, to calculate the level of

housing need in their areas unless there are exceptional circumstances. No exceptional

circumstances have been identified in Mole Valley.

• The recommended breakdown of new private sector market dwellings by size is 25% one-

bedroomed units, 45% two-bedroomed units, 20% three-bedroomed units, and 10% four-

bedroomed units. It is also recommended that 25% of new completions should be in the form

of flats and apartments.

• The assessment of need figure is an important consideration in local planning, but a range of

other matters, including the requirement for affordable housing and the availability of sites for

housing will need to be considered by the Council in arriving at a decision about the target

level of new housing provision to be included in its local plan.

Introduction

3.1 As Chapter 2 described, the approach which governments have required local authorities to

take in assessing housing need have been subject to many recent amendments. The frequency of

these changes after a long period of stability introduces an element of uncertainty into estimates of

housing need. In this section we firstly set out the estimated housing need in Mole Valley using the

standard national methodology set out in the NPPF issued in 2019 and in subsequent NPPG. At the

time of writing this remains the official approach. The chapter also addresses the impact of new

2018-based household projections issued in 2020 by the Office of National Statistics (ONS) and

presents a scenario which applies these projections to the existing standard methodology. However,

20

the government has also issued (in July 2020) proposals for a new standard methodology for

calculating housing need. These may be amended after consultation (although previous

consultations have not tended to result in significant amendments) but their implications for housing

need in Mole Valley are also set out in this section. We consider that having this range of estimates

available will provide the Council with the best advice on how to proceed in setting future targets for

housing provision in the area.

The 2019 Standard Assessment of Need

3.2 The approach to be followed is set out in NPPG published in February 2019. Step 1 is to ‘set

the baseline using national household growth projections, for the area of the local authority’. The

calculation is required to start at the current year (2020) and to estimate annual average household

growth over the next ten years. At the time of writing, NPPG specifies that local authorities should

use the 2014-based household projections published by the MHCLG, unless exceptional

circumstances apply. Table 3.1 below shows the calculation, with the baseline of annual growth set

out in the final column. Table 3.1 also shows the same calculation using the 2016- and 2018-based

household projections subsequently published by the Office of National Statistics.

Table 3.1 Step 1 Household projections and annual average growth

2020 households 2030 households Annual Average Growth

MHCLG 2014-based 38,183 41,417 323.4

ONS 2016-based 37,571 39,862 229.1

ONS 2018-based 37,207 38,584 137.7

Sources: ONS, 2016-based household projections; ONS, 2016-based household projections; MHCLG 2014-based household projections.

3.3 Projected annual average household growth in Mole Valley has fallen from over 300 in the

2014-based projections to only 138 in the most up-to-date set of projections. This is accounted for

by both differences in the underlying population projections on which they are based; and by

differences in the assumptions made about the propensity of the population to form separate

households, which is determined through a series of estimated household formation rates. The

2014-based household projections produced by MHCLG take as their starting point ONS mid-year

estimates up to 2013 and the ONS 2014-based population projections. The most recent 2018-based

ONS projections take mid-year estimates up to 2019 and the ONS 2018-based population

projections.3.4 Step 2 of the current standard assessment of need requires the calculation of a

median workplace earnings-based affordability ratio, which is then used to calculate an adjustment

factor. This is applied to the average annual projected household growth figure calculated in Step 1

to produce a minimum annual housing need estimate.

3.5 NPPG specifies that the most recent median workplace-based affordability ratio, published

by the Office for National Statistics at local authority level, should be used. Data for 2019, published

in March 2020, is the most recent available14. The 2018 ratio is 13.55, a reduction from the 2018

peak of 14.57 and the lowest ratio since 2015. This compares to a ratio of 12.43 for Surrey as a

whole, 10.12 for the South East region, and 7.70 for England and Wales.

14 The data may be found at

https://www.ons.gov.uk/peoplepopulationandcommunity/housing/datasets/ratioofhousepricetoworkplaceba

sedearningslowerquartileandmedian, Table 5c.

21

The formula for calculating the adjustment factor is:

Adjustment factor = ( Local affordability ratio - 4

) x 0.25 + 1 4

3.6 The first stage in calculating the adjustment factor is to subtract 4.0 from the workplace-

based affordability ratio, leading to a figure of 9.55. In stage 2 this is divided by 4, giving a result of

2.3875. The third stage is to multiply this by 0.25, giving a result of 0.596875. The fourth and final

stage is to add 1.0 to this result to give a final adjustment factor of 1.596875.

3.7 If applied to baseline household growth, the adjustment factor gives a minimum annual

household need of 516 dwellings per annum (rounded to the nearest whole dwelling), based on the

MHCLG 2014-based household projections.

The 2019 Standard Assessment of Need: Step 3

3.8 Step 3 of the standard method is to apply capping to the minimum annual household need

figures calculated in Step 2. In Mole Valley, the capped figure is the higher of (a) 140% of the figure

calculated in Step 1, namely 323 x 1.4 = 453; or (b) the figure set out in the most recent adopted

local plan, which is 188 dwellings per annum15. The capped estimate of need is therefore 453

dwellings per annum.

3.9 This assessment follows the approach currently set out in NPPF and in more detail in PPG

and is summarised below:

Households at 2020 (MHCLG 2014-based projection) 38,183

Households at 2030 (MHCLG 2014-based projection) 41,417

Net Household Growth 3,234 over 10 years

Local affordability ratio (March 2020) 13.55

Adjustment Factor (NPPG formula calculation) 1.596875

Uncapped housing requirement (NPPG formula) 516 units pa

Capped (40%) housing requirement 453 units pa

Regulation 18 Draft plan requirement 449 units pa

SHMA OAN 2016 391 units pa

Alternative Scenario 1: Assessment of need using 2018-based household

projections

3.10 At the end of June 2020 ONS produced new household projections based on their 2018 sub-

national population projections. This section shows the result of substituting these more up-to-date

projections into the standard national methodology for assessing housing need. As Table 3.1 above

showed, the 2018-based household projections show annual average household growth from 2020-

30 of 137.7 households per annum. Application of the adjustment factor derived from the 2019

15 Mole Valley Core Strategy, 2009-2026 at https://www.molevalley.gov.uk/home/building-planning/local-

plans/adopted-planning-policy-documents

22

median house price to workplace-based earnings ratio (1.596875) gives minimum annual household

need of 220 dwellings per annum (rounded to the nearest whole dwelling). Application of the cap to

the figure derived by using the 2018-based household projections as the basis for the calculation in

Step 1 gives 138 x 1.4 = 193, which is higher than the figure in the most recent adopted local plan.

The capped estimate of need using the 2018-based household projections is thus 193 dwellings

per annum:

Households at 2020 (ONS 2018-based projection) 37,207

Households at 2030 (ONS 2018-based projection) 38,584

Net Household Growth 1,377 over 10 years

Local affordability ratio (March 2020) 13.55

Adjustment Factor (NPPF formula calculation) 1.596875

Uncapped housing requirement (NPPG formula) 220 units pa

Capped (40%) housing requirement 193 units pa

3.11 Official population projections are based on assumptions about births, deaths and migration.

Revisions in these assumptions lead to differences between projections over time. More recent

projections are more accurate than older ones as they use more recent data on trends, but all

projections become less reliable over the longer term as the assumptions which they make about

future demographic trends may not be fulfilled. The most recent ONS population projections (the

2018-based projections) generally suggest lower population growth in both the short and the longer

term than the previous (2014-based and 2016-based) ONS population projections (Table 3.2). For

2039, the last year covered by all three sets of projections, the population of Mole Valley was

projected to be 99,100 in the 2014-based projections. The 2018-based projections now estimate the

population in the same year to be only 87,725, or over 11,000 fewer. The reductions are apparent

from the start of the new projections in 2018 and they steadily increase year on year. The reduction

in projected population between the two sets of projections occurs due to assumptions that there

will be an increase in the level of natural decline in the population (mainly as a result of fewer

births), and a decline in projected net inward migration. It is assumed that fewer people will be

leaving the district to move elsewhere in the UK or abroad.

3.12 As well as publishing projections of recent and future population, ONS produces estimates

(referred to as mid-year estimates or MYEs) of the population in recent past years. These are more

accurate than the projections, as they are based on recorded trends rather than projected trends.

Taking the year 2014, the mid-year estimate of the population of Mole Valley was some 2,000

persons higher than the ONS-2014 based population projection had assumed. This difference was

subsequently reversed so that by 2019, the mid-year estimate of population was 1,000 lower than

the 2014-based projection because in practice, the population of Mole Valley has been more or less

static at about 87,000 since 2015. It is only projected to increase by 980 persons or 1% in the twenty-

five years from 2018 to 2043. This low growth means that household projections based on pre-2018

population data are likely to substantially over-estimate household growth going forward, unless

there is a divergence from recent trends.

23

Table 3.2 Comparison of population estimates and projections

2014 2016 2018 2019 2029 2039

Mid-Year estimates 86,900 87,300 87,300 87,200 NA NA

ONS 2014-based SNPP 86,200 86,900 87,800 88,300 94,000 99,100

ONS 2016-based SNPP NA 87,300 87,600 87,900 90,900 93,700

ONS 2018-based SNPP NA NA 87,253 87,112 87,103 87,725

Sources: ONS 2014, 2016 and 2018-based sub-national population projections; ONS mid-year population estimates, via NOMIS

3.13 Additionally, the differences between the series of household projections can be explained

by the assumptions made about household formation rates. Household projections apply a range of

estimated household formation rates to the population to calculate the number of households

which will be formed from that population. The 2018-based projections, for example, have

formation rates for 16 age groups, broken down by gender, and by year – a total of 800 rates, which

may also be further broken down by marital status and household type. Household formation rates

for the 2014-based MHCLG household projections were derived from data from the 1971, 1981,

1991, 2001 and 2011 Censuses, supplemented by Labour Force Survey (LFS) data. The 2018-based

ONS household projections were derived from the 2001 and 2011 Censuses only. Table 3.3 below

compares some of the rates used in the 2014 and 2018 based official projections. It shows that there

have been very substantial reductions in household formation rates for men in most age groups,

offset to some degree by increases in household formation for female age groups.

24

Table 3.3 Comparison of household formation rates in Mole Valley

2018-based 2014-based

Percentage Point

Difference

2019 2039 2019 2039 2019 2039

Male 20-24 15% 10% 14% 12% 1 -2

25-29 34% 26% 45% 41% -11 -15

30-34 56% 45% 75% 68% -19 -23

35-39 69% 59% 88% 87% -19 -28

40-44 76% 67% 94% 95% -19 -28

45-49 79% 73% 95% 95% -16 -22

50-54 80% 76% 95% 94% -14 -18

55-59 80% 76% 97% 97% -18 -21

60-64 77% 73% 97% 96% -20 -23

65-69 74% 67% 98% 98% -24 -31

70-74 84% 92% 99% 99% -16 -8

75-79 88% 96% 99% 99% -11 -3

80-84 92% 98% 99% 100% -8 -1

Female 20-24 12% 12% 8% 9% 4 3

25-29 22% 25% 16% 18% 7 6

30-34 29% 34% 18% 21% 11 13

35-39 30% 35% 16% 17% 14 18

40-44 33% 39% 18% 20% 15 19

45-49 37% 45% 19% 18% 18 27

50-54 43% 52% 22% 23% 21 30

55-59 44% 52% 25% 27% 19 26

60-64 41% 41% 24% 24% 17 17

65-69 36% 22% 28% 28% 8 -5

70-74 40% 25% 33% 39% 7 -13

75-79 51% 36% 42% 44% 9 -7

80-84 68% 64% 56% 53% 12 11

Source: MHCLG, 2014-based household projections and ONS, 2016-based household projections

3.14 A key issue in assessing housing need relates to the cause of the decline in household

formation rates, or putting it another way, the higher projected average household size. Is this a

result of changing household preferences, such as sharing by groups of unrelated individuals, or the

result of increasing affordability problems? Or is it simply a lack of supply, making it harder for

individuals wishing to live on their own or to afford to do so? The latter explanation might be termed

suppressed household formation.

3.15 Defining, measuring and tackling suppressed household formation raises many difficulties.

Affordability is inevitably a constraint on household formation in any housing market – the question

is at what stage do affordability problems become problematic, and lead to overcrowding, or levels

of dwelling occupancy which cause other problems?

25

3.16 These are complex issues. In its 2017 White Paper Fixing our broken housing market, the

government decided that it wished to increase supply with the aim of improving affordability, and

through this to permit more households to form. It did so by introducing a national supply target

above that which would be derived from household projections alone.

3.17 This is a pragmatic policy response which recognised the difficulty of precise calculations of

suppressed household formation, but which determined and set a definitive target.

3.18 In that sense the government’s current requirement that local planning authorities should

set aside the most up to date projections and use outdated projections is unnecessary, as it relies on

both inaccurate population projections and household formation trends which are out of date. The

latest consultation abandons this approach and returns to the use of the most up-to-date

projections, but at the same time increases the factor to be applied to the demographic base

projections.

Alternative Scenario 2 Proposed new standard methodology

3.19 In August 2020 the government published a paper16 setting out proposed changes to the

standard national methodology for the assessment of housing need. Consultation on these

proposals remains open at the time of writing and closes on 1st October 2020.

3.20 Step 1 in the proposed new approach is entitled Setting the baseline –providing stability and

certainty by incorporating a blend of household projections and stock. It proposes that the baseline

for the revised standard method should be whichever is the higher of (a) 0.5% of the existing

housing stock in each local authority, or (b) the latest projected average annual household growth

over a 10-year period. The Government considers that the target of 0.5% of the existing stock in an

area provides a reasonable baseline target for annual additions. It also takes the view that

household projections have a role in topping up this baseline where the latest projected average

annual growth is higher than 0.5% of the existing stock.

3.21 The consultation specifies the data source to be used for an estimate of the size of the

dwelling stock as MHCLG Live Table 12517. The most recently published data relates to 2019 and

shows that the total stock in Mole Valley is 38,772, of which 0.5% is 193.86 dwellings. The household

projections element of the baseline must use the latest ONS national household growth projections

for the local authority area18. The latest 2018-based ONS household projections set out in Table 3.1

above showed annual average household growth of 137.7, a lower figure than 0.5% of the dwelling

stock. Accordingly, the proposed new method would produce a baseline for Mole Valley of 194

dwellings per annum (rounded to the nearest whole dwelling).

3.22 Step 2 of the new proposed approach is entitled Adjusting for market signals – maintaining

price signals using the current affordability ratio and the change in affordability over the last 10

years. The government proposes that the standard method will include two adjustments to the

baseline, using the median house price to workplace-based median earnings ratio to produce a

16 See MHCLG (2020) Changes to the current planning system: Consultation on changes to planning policy and

regulations, August 2020, pp 11-18. 17See https://www.gov.uk/government/collections/dwelling-stock-including-vacants (Table 125) 18 The calculation is required to use the principal projection set out in Table 406 of the projections.

26

factor to apply to the baseline in Step 1. Stage 1 in Step 2 follows the present approach, using this

ratio for the most recent year for which data is available. The formula to adjust the ratio using 2019

data would give an adjustment factor of 0.596875.

3.23 In Stage 2 of Step 2 the government proposes to make a further adjustment to take account

of the extent of change in the affordability ratio over time. The affordability ratio for each local

authority ten years before the most recent available ratio will be subtracted from that ratio. The

difference will be multiplied by 0.25 and added to the figure from Step 2 Stage 1 to give a final

factor. For Mole Valley, the 2019 ratio was 13.55. The ratio in 2009 was 8.33 and the difference

between these ratios is 5.22. Multiplying this by 0.25 gives an addition of 1.305. Adding this to the

factor from Step 2 Stage 1 gives an adjustment factor of 1.901875. Finally, the new approach

proposes a further addition of 1.0 to this factor, making a final adjustment factor of 2.901875.

Authorities where affordability has worsened over the last ten years will have their estimated need

increased as a result of this additional factor, whilst those where affordability has improved will

experience a reduction in need.

3.24 The final part of the calculation (equivalent to Step 3 in the existing standard methodology)

is to apply this factor to the baseline figure from Step 1. For Mole Valley this indicates an overall

assessment of 193.8644 * 2.901875 = 563 dwellings (rounded to the nearest whole dwelling). The

government proposes that this figure should not be subject to capping as under the present method.

The result of this new proposal is to increase the standard assessment for Mole Valley by 110

dwellings per annum or 24.3%. When aggregated across all local authorities in England, the

proposed new methodology produces an estimate of 337,250 dwellings. The stages in this

calculation are summarised below:

Households at 2020 (ONS 2018-based projection) 37,207

Households at 2030 (ONS 2018-based projection) 38,584

Net Household Growth 1,377 over 10 years

Local affordability ratio (March 2020) 13.55

Adjustment factor 1 – affordability ratio 1.596875

Adjustment factor 2 – change in affordability 1.305000

Combined adjustment factor 2.901875

Housing requirement 563 units pa

Regulation 18 Draft plan requirement 449 units pa

SHMA OAN 2016 391 units pa

3.25 The proposed new standard methodology on its own would lead to an annual addition to

the dwelling stock in Mole Valley of almost 1.5%. Compounded over a twenty-year period this would

result in a 30% increase in the dwelling stock in the district, and over thirty years a more than 50%

increase. The scale of growth implied by the standard methodology is therefore transformational. It

exceeds the level of household growth projected on current trends over the 2020-2040 period, 7%,

by a very wide margin.

27

Housing and economic growth

3.26 In 2018, Mole Valley Council published an Economic Prosperity Strategy19. It set out a

considerable number of economic strengths in the district, including the high productivity level of its

economy, the high proportions of knowledge based workers with creative and entrepreneurial

talent, the low level of unemployment at that time, the attractive environment, good links to

London, and proximity to both Gatwick and Heathrow airports. It noted that Mole Valley plays an

important role in the Gatwick Diamond area which in turn plays a significant role in the economy of

the South East region. The relationship between Mole Valley and the Gatwick Diamond is discussed

in detail in Appendix 1. There were also some threats to be addressed in the strategy including a

highly constrained built environment, a shortage of commercial and industrial premises, an ageing

population, and significantly a shortage of affordable housing/accommodation. The strategy

highlighted the need to strike a balance between protecting the natural environment (which was an

important factor making the area attractive to businesses and workers), and the need to support the

economy and meet affordable housing requirements.

3.27 The economic strategy does not set employment growth targets, so it is impractical to assess

the specific housing requirement arising from its proposals. However, the scale of additional housing

provision identified by the current standard national housing need assessment methodology and the

currently-proposed revised methodology are both significantly greater than the underlying trend in

demographic household growth. Demographic growth averages 137 dwellings per annum over the

2020-2030 period, the current standard assessment identifies a need of 453 dwellings per annum,

and the proposed new approach set out in the Government’s consultation identifies a need of 563

dwellings. These levels of need clearly provide a very wide margin of housing provision above the

basic demographic need and should be adequate to support economic growth.

Market signals

3.28 In the past, NPPG relating to housing need estimation required local authorities to consider

the need for an uplift to housing need to take account of market signals. These were indicators such

as house prices or affordability ratios which could show that the demand for housing was higher

than that indicated by demographic trends. Guidance did not suggest any specific uplift or relate the

degree of uplift to any specific indicators. Over time, as a result of the accumulation of evidence at

Local Plan enquiries and from other sources, Planning Inspectors tended to identify an uplift of 20%

as justified when severe affordability problems were identified in an area. Such rates were applied in

some (but not all) areas of the South East and East of England and in London where affordability

problems were worst. Subsequently, through its standardised need assessment methodology, the

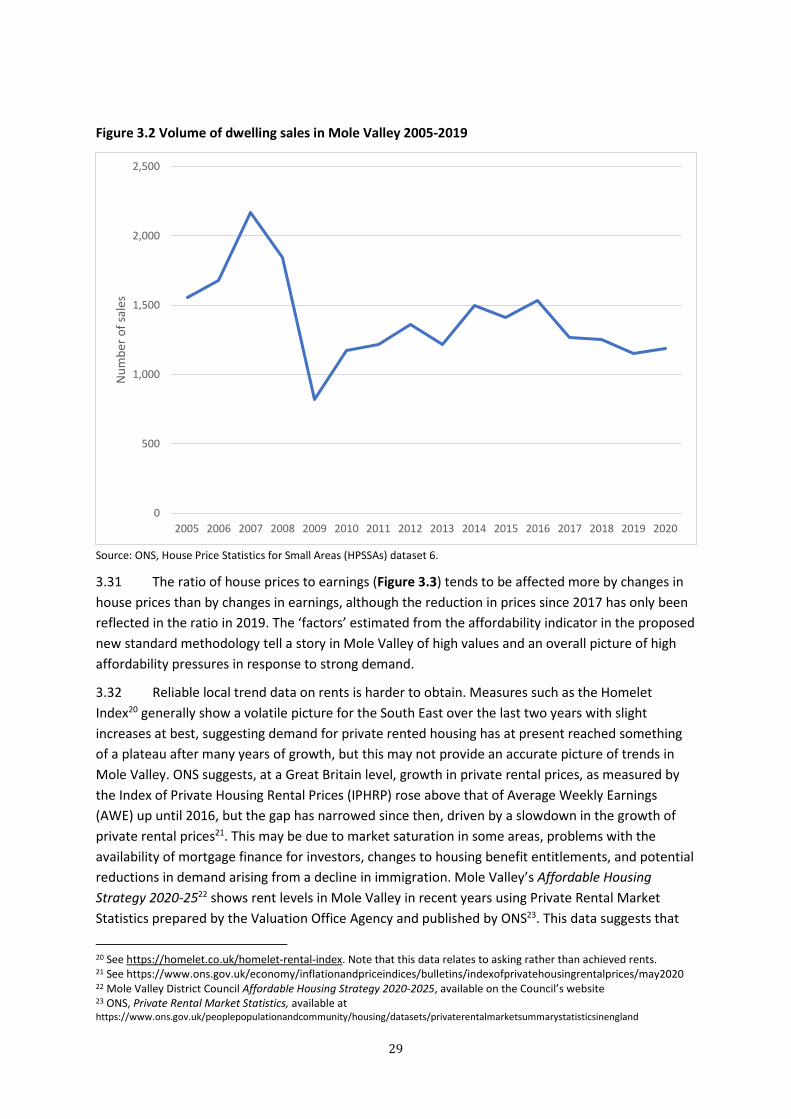

government defined a ‘factor’ which it required local authorities to apply to basic demographic