Embed Size (px)

DESCRIPTION

Stock Options and Trading Strategies. Finance (Derivative Securities) 312 Tuesday, 12 September 2006 Readings: Chapters 9 & 10. Notation. c : European call option price p :European put option price S 0 :Stock price today K :Strike price T :Life of option - PowerPoint PPT Presentation

Citation preview

Stock Options and Stock Options and Trading StrategiesTrading Strategies

Finance (Derivative Securities) 312

Tuesday, 12 September 2006

Readings: Chapters 9 & 10

NotationNotation c : European call option price p : European put option price S0: Stock price today K : Strike price T : Life of option : Volatility of stock price C : American Call option price P : American Put option price ST: Stock price at option maturity D : Present value of dividends during option’s life r : Risk-free rate for maturity T with cont comp

Factors Influencing Factors Influencing ValueValue

c p C PVariable

S0

KTrD

+ + –+

? ? + ++ + + ++ – + –

–– – +

– + – +

Upper and Lower BoundsUpper and Lower Bounds

Call Options• Stock price is upper bound for both American

and European

Put Options• Exercise price is upper bound for both

American and European (PV of K)

Upper and Lower BoundsUpper and Lower Bounds

Suppose that

c = 3 S0 = 20

T = 1 r = 10%

K = 18 D = 0

Is there an arbitrage opportunity?

Upper and Lower BoundsUpper and Lower Bounds

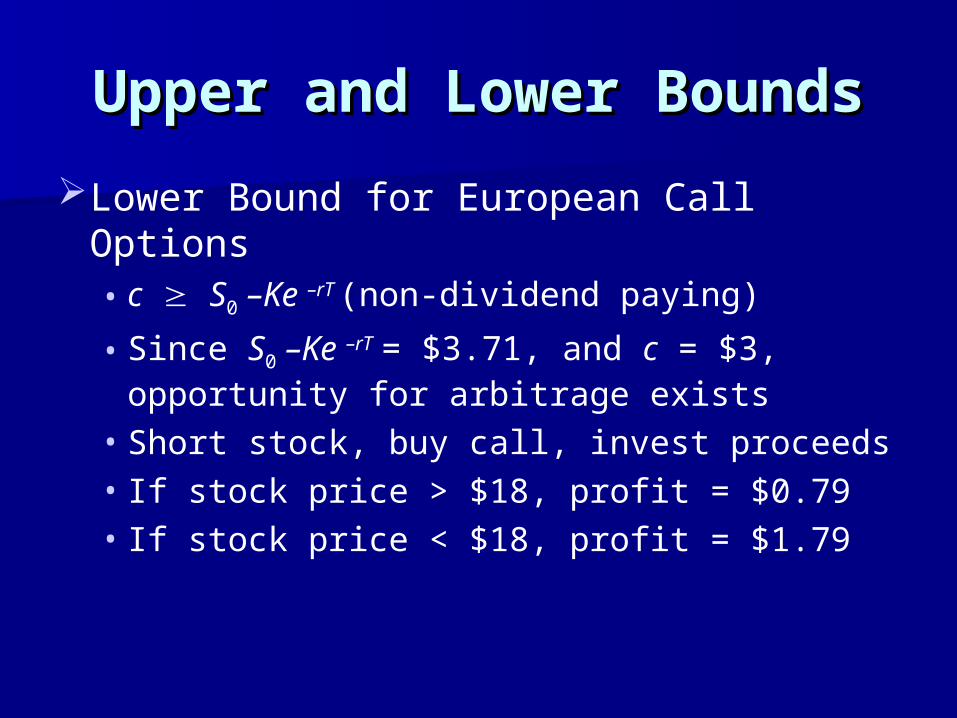

Lower Bound for European Call Options • c S0 –Ke –rT (non-dividend paying)

• Since S0 –Ke –rT = $3.71, and c = $3, opportunity for arbitrage exists

• Short stock, buy call, invest proceeds• If stock price > $18, profit = $0.79• If stock price < $18, profit = $1.79

Upper and Lower BoundsUpper and Lower Bounds

Suppose that

p = 1 S0 = 37

T = 0.5 r = 5%

K = 40 D = 0

Is there an arbitrage opportunity?

Upper and Lower BoundsUpper and Lower Bounds

Lower Bound for European Put Options • p Ke–rT – S0

(non-dividend paying)• Since Ke–rT – S0 = $2.01, and p = $1,

opportunity for arbitrage exists• Borrow p + S0 , buy stock, repay loan• If stock price < $40, profit = $1.04• If stock price > $40, profit = $3.04

Put-Call ParityPut-Call Parity

Consider strategy I:

Buy a share, and buy a put option

ST ≤ K ST > K

Buy Stock ST ST

Buy Put K – ST 0

Total K ST

Put-Call ParityPut-Call Parity

Consider strategy II:

Buy a call option, and borrow Ke–rT

ST ≤ K ST > K

Buy Call 0 ST – K

Invest Ke–rT K K

Total K ST

Put-Call ParityPut-Call Parity

If two portfolios provide the same return, they must cost the same to set up, otherwise an opportunity for arbitrage exists

p + S0 = c + Ke–rT

American OptionsAmerican Options

Early exercise of calls (non-dividend paying)• Insurance• Time value

Early exercise of puts (non-dividend paying)• Insurance worth forgoing

Effect of DividendsEffect of Dividends

Consider strategy I:

Buy a put, a share, and borrow D + Ke–rT

ST ≤ K ST > K

Buy Share ST ST

Buy Put K – ST 0

Borrow D+Ke-rT –K –K

Total 0 ST – K

Effect of DividendsEffect of Dividends

Consider strategy II:

Buy a call

ST ≤ K ST > K

Buy Call 0 ST – K

Total 0 ST – K

p + S0 = c + D + Ke–rT

Bull Spread using CallsBull Spread using Calls

K1 K2

Profit

ST

Bull Spread using PutsBull Spread using Puts

K1 K2

Profit

ST

Bear Spread using CallsBear Spread using Calls

K1 K2

Profit

ST

Bear Spread using PutsBear Spread using Puts

K1 K2

Profit

ST

Calendar Spread using Calendar Spread using CallsCalls

Profit

ST

K

Calendar Spread using Calendar Spread using PutsPuts

Profit

ST

K

Protective PutProtective Put

Buy stock, worth $50Buy put option, exercise price $53,

premium $5Used when the investor is worried the

stock price will fallPut option provides insurance against loss

on the stock

Protective PutProtective Put

At expiry:

ST Payoff (Stock + Put) Profit 45 -5 + 8 = 3 3 - 5 = -2

50 0 + 3 = 3 3 - 5 = -255 5 + 0 = 5 5 - 5 = 060 10 + 0 = 10 10 - 5 = 565 15 + 0 = 15 15 - 5 = 1070 20 + 0 = 20 20 - 5 = 15

Protective PutProtective PutProfit

0ST-2

-50

48Stock

Put Option

Protective Put

Breakeven point

-5

48 50 53 55

Covered CallCovered Call

Buy stock, worth $50Write call option, exercise price $60,

premium $5Used to boost income with premiums

collected, and locks in a selling price (though potential capital gains are forfeited)

Covered CallCovered Call

At expiry:

ST Payoff Profit 30 -20 -15 40 -10 -5 50 0 5 60 10 15 70 10 15 80 10 15

Covered CallCovered CallProfit

0 ST

5

-50

45 50 60 65

Stock

Call Option

Covered Call 15

-45

Breakeven point

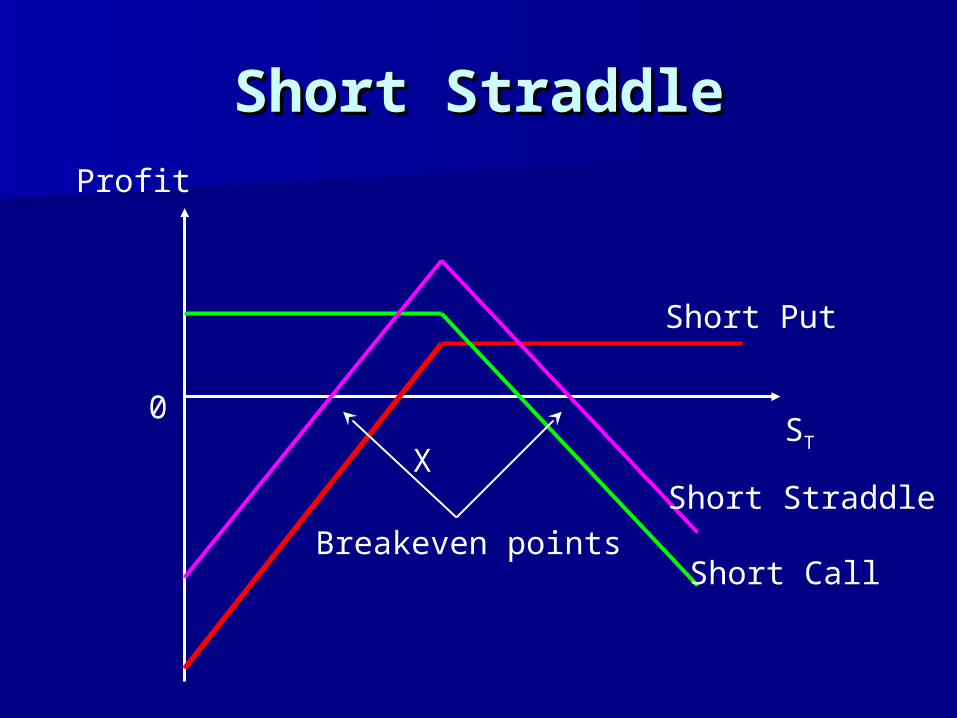

StraddlesStraddles

Buy call and put with same exercise priceUsed when share price is expected to

move, but direction uncertainFor short straddle, sell call and put

Long StraddleLong StraddleProfit

0 ST

Long Call

Long Put

Long Straddle

X

Breakeven points

Short StraddleShort StraddleProfit

0ST

Short Call

Short Put

Short Straddle

X

Breakeven points

StranglesStrangles

Buy out-of-the-money call and put, where XC > XP

Similar to straddle, but price needs to move by greater amount in order to breakeven

Costs less than straddleFor short strangle, sell call and put

Long StrangleLong StrangleProfit

0 ST

Long Call

Long Put

LongStrangle

XP XC

Breakeven points

Short StrangleShort StrangleProfit

0

ST

Long Call

Short Put

Short Strangle

XP XC

Breakeven points

Strips and StrapsStrips and Straps

Strip is a bearish straddleBuy 2 puts and 1 call with same X

Strap is a bullish straddleBuy 1 put and 2 calls with same X

StripStripProfit

0 ST

Long Put x 2

Long Call

Strip

X

Breakeven points

StrapStrapProfit

0 ST

Long Call x 2

Long Put

Strap

X

Breakeven points

Butterfly SpreadButterfly Spread

Buy put option with relatively low exercise price (X1)

Buy call option with a relatively high exercise price (X3)

Sell a put option and a call option with an exercise price between X1 and X3 (X2)

Butterfly SpreadButterfly SpreadProfit

0 ST

Long Call X3

Short Call X2

X1 X3

X2

Long Put X1

Short Put X2

Butterfly

Breakeven points