8/14/2019 Stock Market Developments

1/2

Stock Market Developments

The stock markets of the world were at a time of indecision when

we last wrote a weekago. That indecision, spurred on principally by

the decision of the government of the

USA to re-separate the functions of commercial and investment

banking has become, at

least for the moment, a world bear market.

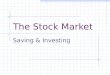

Figure 1.

Stock Markets in 2010

90.0%92.0%

94.0%

96.0%

98.0%

100.0%

102.0%

104.0%

12/3

1/200

9

1/2/20

10

1/4/20

10

1/6/20

10

1/8/20

10

1/10/2010

1/12/2010

1/14/2010

1/16/2010

1/18/2010

1/20

/2010

1/22

/2010

1/24

/2010

1/26

/2010

DJI FTSE CAC 40 HSI Iboves a S&P

Figure 1, above shows the performance of six stock markets,

based upon a comparative

analysis of their respective equity indices from the beginning

of 2010. The indices chosen

are the Dow Jones Industrial Average (DJI), and the Standard and

Poors 500 (S&P

500) of the USA, the Financial Times and London Stock Exchange

100 Index (FTSE100) of the United Kingdom, The Cotation Assistee en

Continu 40 (CAC 40) of

France, China`s Hang Seng Index (HSI), and Brazil`s Indice da

Bolsa de Valores de

Sao Paulo (Ibovespa). 100% represents the index for each market

at close of businesson the last day of trading of 2009.

We have become accustomed to seeing the IBovespa index being

among the two bestperformers between October 2008, and December,

2009. Indeed, we have been surprised

at the Ibovespa`s resilience given the Brazilian Government`s

successful attempts to

discourage foreign investors from investing in the equity and

fixed income marketsthanks to a flat tax at the moment of

investment of 2%. However, in looking at the stock

market performance in through January 26th, we see a new picture

emerging.

The two worst performing indices are those of the emerging

markets represented, Brazil

and China. The HSI of China had been the front runner since the

crisis for a long time,but due to an increase in Yuan interest

rates in November 2009, that market became

essentially static. The Brazilian market, as measured by the

Ibovespa continued its climbthroughout December, reaching over

70.000 points on eight consecutive business days.

The new story, however is one of the HSI falling 8.1% in 2010,

while the Bovespa has

fallen 4.5%. Meanwhile, the performances of the stock markets in

the more developedcountries have fallen by: CAC 40, 3.3%, FTSE,

2.5%; the Dow Jones, 2.2%, and the S&P

2.1%.

8/14/2019 Stock Market Developments

2/2

What is going on?

First, there is a general lack of consensus, not so much about

whether the world`s

economic situation will continue to improve, but how quickly.

Secondly there are serious

concerns about the amount of liquidity in the world. There was

an enormous amount ofartificial liquidity created by the various

Central Banks to aid with the crisis, and that will

slowly be withdrawn through 2010. There is also the investor

liquidity that was in the

market throughout 2009, but which has been absorbed through the

acquisition of evermore expensive assets. Thirdly, investors have

seen markets rise rapidly over the last

year, and have come to the conclusion that the markets upward

mobility is limited, and

thus they are withdrawing to other assets and other markets.

Also, investors in Brazilian stocks are becoming clearer about

the effects of the crisis on

the Brazilian economy. While the story continues to be good

there is more concern about

Brazilian Governmental indebtedness, and a bet that in an

election year that indebtedness

will not be closely controlled. Also, of concern is the

indebtedness of Brazilianconsumers which is growing a lot faster

than income, and finally, the parlous state of the

trade balance which will probably only get worse, save a

significant realignment of theReal/ US Dollar exchange rates.