Embed Size (px)

Citation preview

Seeing Optical with ClarityAn Overview of Broadband Economics

Steven GlapaVP of Marketing & Product Management

Digital City Expo, January 23, 2008

PROPRIETARY & CONFIDENTIAL 2

The Cobbler’s Children

Source: OECD, April 2007

1

3

5

7

9

11

13

15

17

19

21

23

25

61.0

45.6

21.7

18.2

17.6

8.8

8.1

7.6

7.5

7.4

7.3

6.2

6.0

6.0

4.8

4.6

4.2

3.1

2.6

2.3

2.3

2.2

1.7

1.6

1.2

Japan

Korea

Finland

Sweden

France

Netherlands

Portugal

Canada

Poland

Norway

Austria

Belgium

Iceland

Germany

United StatesDenmark

Italy

Luxembourg

United Kingdom

Switzerland

New Zealand

Ireland

Australia

Czech Republic

Spain

Top 25 Average: 10.4

2001

2007

2002

2003

2004

2005

2006

0.51 subscribers/HH

Korea, with0.9 subs/HH

Average Broadband Subscriber’s Data Rate, MbpsUS Broadband Penetration Rank

PROPRIETARY & CONFIDENTIAL 3

It’s a big country, part one

1

10

100Mbps

0 2,000 4,000 6,000 8,000 10,000 pops/km²

KoreaJapan

Australia

UKNewZealand

United States

CanadaWestern Europe (Average)

R² = 0.57

Average Broadband Data Rate v. Urban Population Density

Source: OECD, April 2007; Demographia.

Cities over 500k pops

PROPRIETARY & CONFIDENTIAL 4

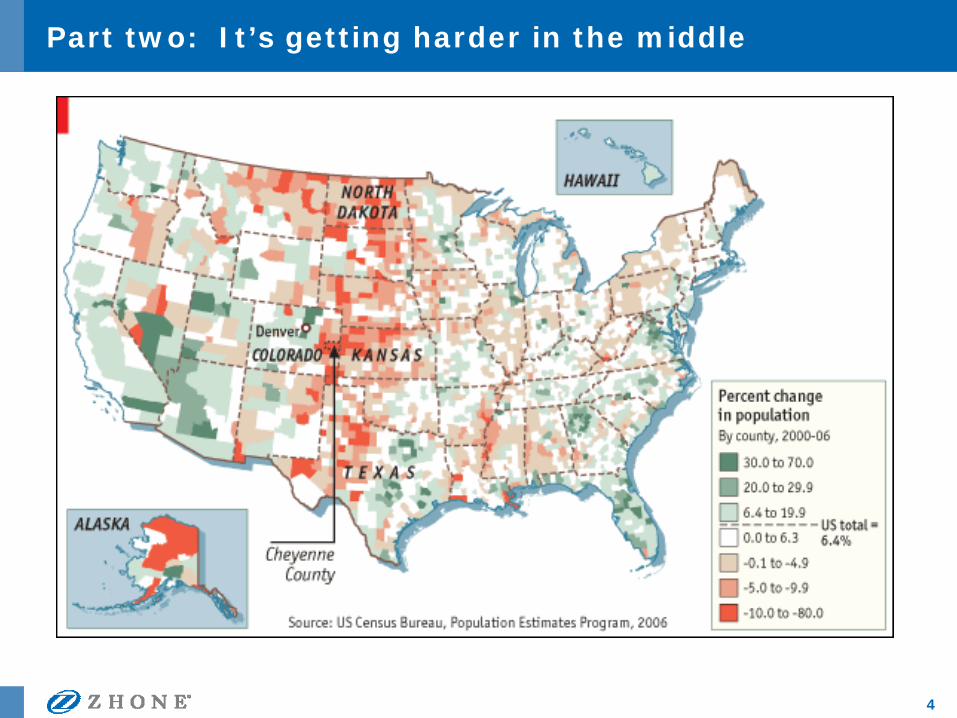

Part two: It’s getting harder in the middle

PROPRIETARY & CONFIDENTIAL 5

Part three: Partial solutions

9 million homes and businesses passed today

3 million more each year through 2010

That’s 20%.

Source: Verizon.

Clarity

“Access” (a.k.a. the last mile)can be confusing

Some contributions to reduce confusion

• Demand and the future

• Wireline technology

• Wireless technology

Another time: Content, IPTV, VoIP, backbone, ISP partnerships for full or wholesale operator model

PROPRIETARY & CONFIDENTIAL 7

Zhone — Access for a Converging World

Founded in 1999 ZHNE on NASDAQ since 2003

$175m annual revenues, 50% outside US

EFM, GPON, Wireless,xDSL, Active Ethernet

CO and Customer Prem

Silicon Valley R&D for innovation and responsiveness

Made in USA for quality(Florida manufacturing)

450 employees Sales & support offices worldwide

Strategic focus on integrated multi-service access solutions

PROPRIETARY & CONFIDENTIAL 8

600 Customers and Counting

USA

Global Customer Base: NLECs, IOCs, CLECs, PTTs & MSOs

Canada

Europe

Asia

Middle East &Africa

Caribbean &Latin America

PROPRIETARY & CONFIDENTIAL 9

Confusion about realistic solutions is all too easy

site acquisition/installation cost1x site cost per antennasite op & maint costsite wired backhaul recurring costbase station cost / sectormodem costs (desktop, laptop, handset)indoor antenna + cable costoutdoor antenna + cable costoutdoor antenna installation costNOC initial setupNOC cost per data subscriber unit of capacityNOC cost per line of VoIP capacitybackbone connectivity per subtech support (wholesale, retail)NOC opex, all elseretail opex, all else (mbx, web space, etc.)subscriber acquisition expenseservice wholesale price by categorywholesaler share of subscriber modem expensesubscriber churncorporate overheadnetwork amortization periodspectrum unit costspectrum depreciation period

usage per average subscriber in busy hour by service segment and year, over timeaggregate consumption as function of busy-hour usageretail ARPU by segment, over timesubscriber device price (paid by subscriber), over timesubscriber adoptionmodem type mix over time

baseline hardware link budgetadjustments for technologyservice definition (data rate, cell edge coverage target)sector antenna incremental gain over omnismart antenna gainslaptop built-in antenna gainlaptop adjustment for cell-edge data ratedesktop built-in antenna gaindesktop + window-mount antenna gaindesktop + prof’l-install antenna gainwall losscomposite fading marginranges by configuration and morphologyisolated cell spectral efficiencyinterference-limited cell spectral efficiency

sectors/cellspectrum availablespectrum re-use configuration (intra- and inter-cell)antennas/sectorspectrum operating pointcapacity reserveplanned coverage for fixed service over timeplanned coverage for mobile service over timebackhaul approach

geographic sizepop densitypops / HH ratioresidential broadband penetrationtotal candidate SMEs in marketPC penetrationlaptop share of PC installed basemobile phone penetrationmorphology mix

Financial and Operating ParametersCustomer Behavior by Segment

Link Budgets, Capacity and RangeDeploymentMarket

PROPRIETARY & CONFIDENTIAL 10

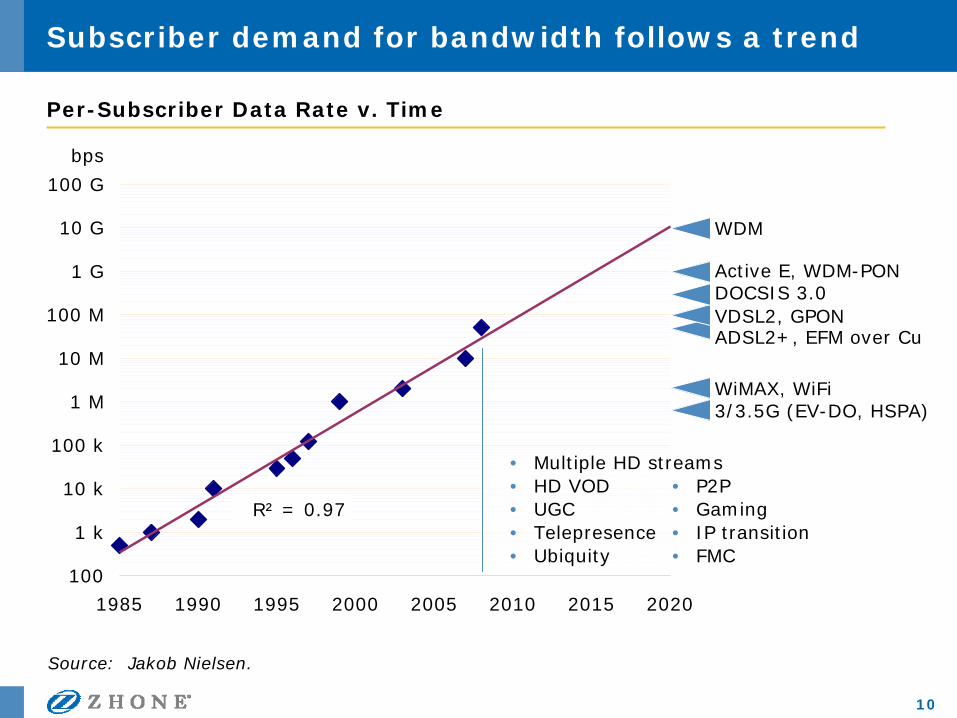

Subscriber demand for bandwidth follows a trend

Source: Jakob Nielsen.

1985 1990 1995 2000 2005 2010 2015 2020

100

1 k

10 k

100 k

1 M

10 M

100 M

1 G

10 G

100 G

bps

R² = 0.97

3/3.5G (EV-DO, HSPA)WiMAX, WiFi

ADSL2+, EFM over CuVDSL2, GPON

WDM

DOCSIS 3.0Active E, WDM-PON

Per-Subscriber Data Rate v. Time

• Multiple HD streams• HD VOD• UGC• Telepresence• Ubiquity

• P2P• Gaming• IP transition• FMC

PROPRIETARY & CONFIDENTIAL 11

ARPU v. bandwidth: Pipe economics are critical

cellular voice

wireline voice

satellite data

cellular data

wired broadband

on-demand HD

satellite TV

digital cable TV

10¢ $11¢0.1¢0.01¢

Willingness to Pay per Unit of Capacity Consumed

US$/MB

Sources: US commercial network offers circa January, 2008; Zhone analysis.

Clarity

“Access” can be confusing

Some contributions to help

• Demand and the future

• Wireline technology

• Wireless technology

PROPRIETARY & CONFIDENTIAL 13

The current copper crop

Rate/Reach for Current Cu-based Broadband Access Technologies

25

50

75

100

125

150

175

200 Mbps

Sources: DSL Forum; Zhone testing.

VDSL22 bonded pairs

VDSL2

ADSL2+ (2 pr)

EFM (8 pr)ADSL2+

EFM (1 pr)

0 1.0 2.0 miles0.5 1.5

PROPRIETARY & CONFIDENTIAL 14

Adding fiber

Rate/Reach for Fiber-based Broadband Access Technologies

Sources: DSL Forum; Zhone testing.

0 2

100

200VDSL22 bonded pairs

VDSL2

ADSL2+ (2 pr)EFM (8 pr)ADSL2+EFM (1 pr)

1,000 Mbps

300

400

500

600

700

800

900

60 miles4 6 8

GPON (2.5 G split 32 ways)

Active Ethernet (Dedicated fiber)

PROPRIETARY & CONFIDENTIAL 15

Four fiber access scenarios to assess

PROPRIETARY & CONFIDENTIAL 16

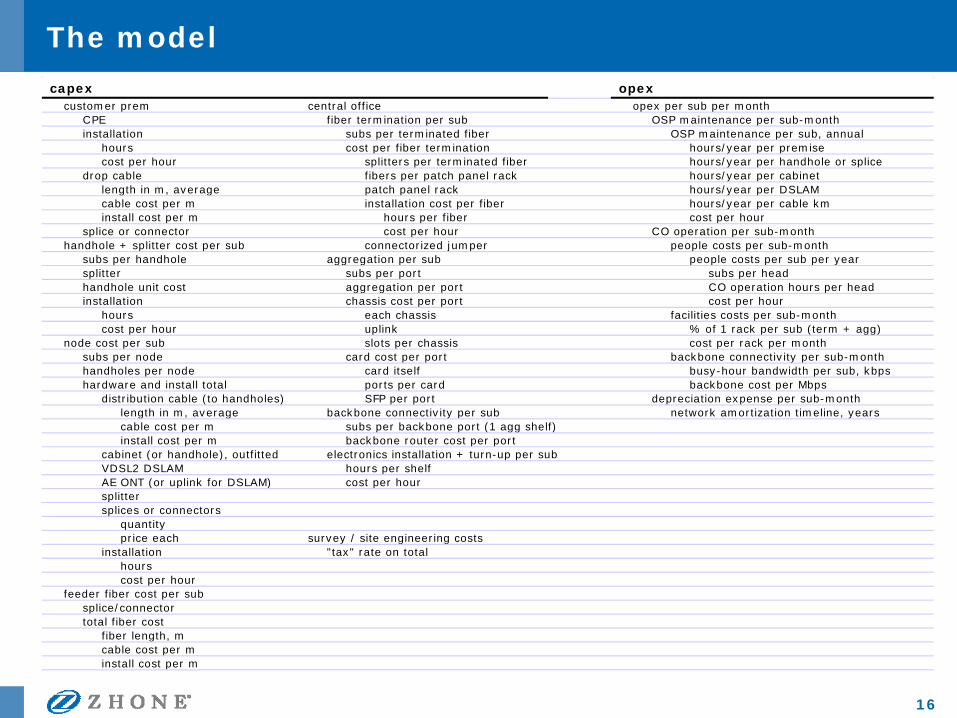

The model

capex opexcustomer prem central office opex per sub per month

CPE fiber termination per sub OSP maintenance per sub-monthinstallation subs per terminated fiber OSP maintenance per sub, annual

hours cost per fiber termination hours/year per premisecost per hour splitters per terminated fiber hours/year per handhole or splice

drop cable fibers per patch panel rack hours/year per cabinetlength in m, average patch panel rack hours/year per DSLAMcable cost per m installation cost per fiber hours/year per cable kminstall cost per m hours per fiber cost per hour

splice or connector cost per hour CO operation per sub-monthhandhole + splitter cost per sub connectorized jumper people costs per sub-month

subs per handhole aggregation per sub people costs per sub per yearsplitter subs per port subs per headhandhole unit cost aggregation per port CO operation hours per headinstallation chassis cost per port cost per hour

hours each chassis facilities costs per sub-monthcost per hour uplink % of 1 rack per sub (term + agg)

node cost per sub slots per chassis cost per rack per monthsubs per node card cost per port backbone connectivity per sub-monthhandholes per node card itself busy-hour bandwidth per sub, kbpshardware and install total ports per card backbone cost per Mbps

distribution cable (to handholes) SFP per port depreciation expense per sub-monthlength in m, average backbone connectivity per sub network amortization timeline, yearscable cost per m subs per backbone port (1 agg shelf)install cost per m backbone router cost per port

cabinet (or handhole), outfitted electronics installation + turn-up per subVDSL2 DSLAM hours per shelfAE ONT (or uplink for DSLAM) cost per hoursplittersplices or connectors

quantityprice each survey / site engineering costs

installation "tax" rate on totalhourscost per hour

feeder fiber cost per subsplice/connectortotal fiber cost

fiber length, mcable cost per minstall cost per m

PROPRIETARY & CONFIDENTIAL 17

FTTx Cost Comparison

27

651

327

233

143

1,121

1,798

2,593

1,798

1,776

AE FTTN +VDSL2

ActiveEthernetFTTP

WDM-PON,CO Split*

GPON,CO Split

GPON,Field Split

9.87

18.20

20.40

15.47

14.34

CO OSP

Capex per Subscriber, $ Opex per Subscriber-Month, $

1,150

2,450

2,920

2,030

1,920Total:

Depreciation

Total:

CO OpsOSP Maint.

*Rough estimates!Sources: various industry/customer benchmarks; Zhone analysis.

PROPRIETARY & CONFIDENTIAL 18

FTTx Costs v. Data Rate

AE FTTN +VDSL2

ActiveEthernetFTTP

WDM-PON,CO Split*

GPON,CO Split

GPON,Field Split

Capex per Subscriber, $/Mbps Opex per Subscriber-Month, $/Mbps

*Rough estimates!Sources: various industry/customer benchmarks; Zhone analysis.

14

2

9

26

25

0.12

0.02

0.07

0.20

0.18

PROPRIETARY & CONFIDENTIAL 19

The right wireline access

It all depends...

• Investment time horizon

• Service definition

• Customer segment needs

• Asset initial conditions

Choosing

• Equipment flexibility, versatility for network evolution and heterogeneity

• Do the math, with some good help

Clarity

“Access” can be confusing

Some contributions to help

• Demand and the future

• Wireline technology

• Wireless technology

PROPRIETARY & CONFIDENTIAL 21

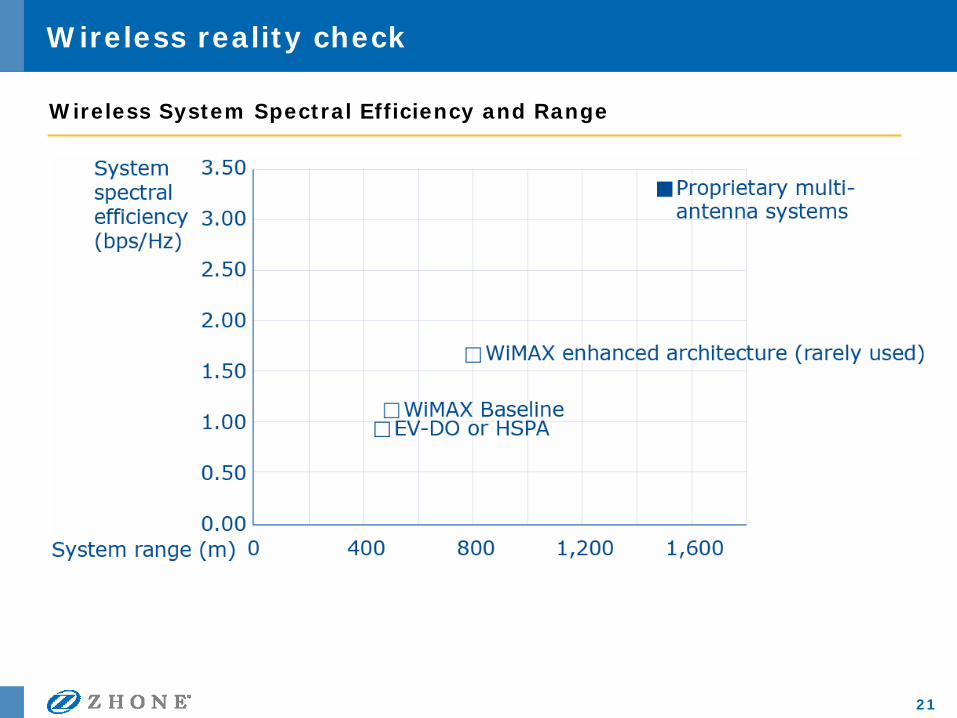

Wireless reality check

Wireless System Spectral Efficiency and Range

PROPRIETARY & CONFIDENTIAL 22

It pays to inspect capacity claims carefully

>50%Measure with a subscriber device antenna configuration and/or power consumption impractical for operator’s business model

2xHighlight underlying chip or symbol rates that sound good but have a loose connection to user data bit rates

30–40%Measure with only one user active in the sector

30–40%Include ‘system bits’ and airlink overhead

very largeAllow marketing to improvise, since no hardware needsto back up the claim yet

20–30%Discuss lab measurements that cannot be replicated infield conditions

30–40%Measure with subscriber device at zero base station range

30–40%Count only higher-efficiency downlink, not aggregatethroughput

20%Exclude guard bands within the allocation

From there, an enterprising vendor can...

2xExclude one half of an FDD (paired) allocation

2–4xMeasure a single sector in isolation

The starting point: a figure relevant to operator economics, i.e. field-proven aggregate net user throughput per sector in a multi-cell, fully-loaded (interference-limited) network

Lies, Damned Lies, and Spectral Efficiency

Overstatement Seen in Practice

PROPRIETARY & CONFIDENTIAL 23

Spectrum is a big challenge in the US

0

5

10

15

500

1,0001,5002,0002,5003,0003,5004,0004,5005,000

0

5

10

15

20

25

30

Cell radius, km(left axis)

Benchmark wireless network cost, US$k per km²

(right axis)

Operating frequency,

MHz

Most attractive frequencies already in use for mobile voice, public safety, paging, etc.

RuralRange

SuburbanUrban

Weighted average cost

Wireless network range and coverage cost as a function of operating frequency

PROPRIETARY & CONFIDENTIAL 24

An interesting tool for municipal applications

0 20 40 60 $80k

ZhoneWi-Fi

MobileWiMAX(802.16e)

0 500 $1,000 0 20 40 60 $80k

Capex per Site Capex per Mbps Capex per km²

PROPRIETARY & CONFIDENTIAL 25

Public IP Network

City Gov’tIP Network

HeadEnd

IP Digital Video Recorder

Wide-area Wi-Fi Applications

100% remotely powered high definition cameras & Wi-Fi Access Points

Fully isolated Public and City Government networks

Secure Video Server location (Telco Central Office)

Centralized battery backup

Indoor repeater unit

PROPRIETARY & CONFIDENTIAL 26

Zhone-enabled Video Surveillance

• CCTV resolution is 640 x 480, using analog cameras

• Pan-Tilt-Zoom cameras enable close-up shots, but operator must adjust PTZ in real time to capture the targeted field of view

• In this city, the same CCTV staff that are used to actively monitor in-building cameras (in the courthouse, city buildings, etc.) are also monitoring the external surveillance cameras

PROPRIETARY & CONFIDENTIAL 27

In Sum

Access technology holds great promise for economic development and service innovation

There are many choices, best made carefully

The better solutions provide flexibility, support evolution

We and our partners are here to help

Thank YouFor more info, come see us in booth 36/37