Embed Size (px)

Citation preview

State Form 1099-MISC Tax Reporting

Mary Kallewaard Cokala Tax Information Reporting Solutions, LLC

www.cokala.com October 7, 2016

Agenda

• January 31 Federal filing date for 1099-MISC NEC states move filing date to Jan. 31

• Other current issues in state 1099 compliance

• Nexus: Where must you file?

• Withholding: Where must you withhold state income tax from payments?

• File direct to state or use IRS combined filing?

January 31 filing due date

• Federal Forms 1099-MISC for 2016 that report an amount in box 7 (“NEC”) have a new due date for filing to the IRS: January 31, 2017

• Some states have changed to a January 31 due date for 1099-MISC NEC filing or for all 1099 filing to the state

January 31 state filing due date

• Alabama

– If the 1099 reports Alabama income tax withheld

• California

– For 1099-MISC NEC reported in box 7

• Delaware

– Announced the regulatory change is in progress

January 31 state filing due date • District of Columbia

– If the 1099 reports DC income tax withheld

• Georgia – If 1099-MISC NEC and Georgia income tax withheld

• Idaho – If 1099s report Idaho income tax withholding and are filed along

with W-2 forms (legislation may make further changes)

• Iowa – TOTAL CHANGE: Reinstated 1099 reporting, gave it January 31

due date

January 31 state filing due date

• Kentucky – But 1099s are filed only if they report KY tax withheld

• Louisiana – But Jan. 31 may apply only to returns reporting

Louisiana tax withheld (seeking clarification)

• Massachusetts – Jan. 31 due date for M-945 that reconciles MA tax

withheld, but 1099s appear to still be due Feb. 28

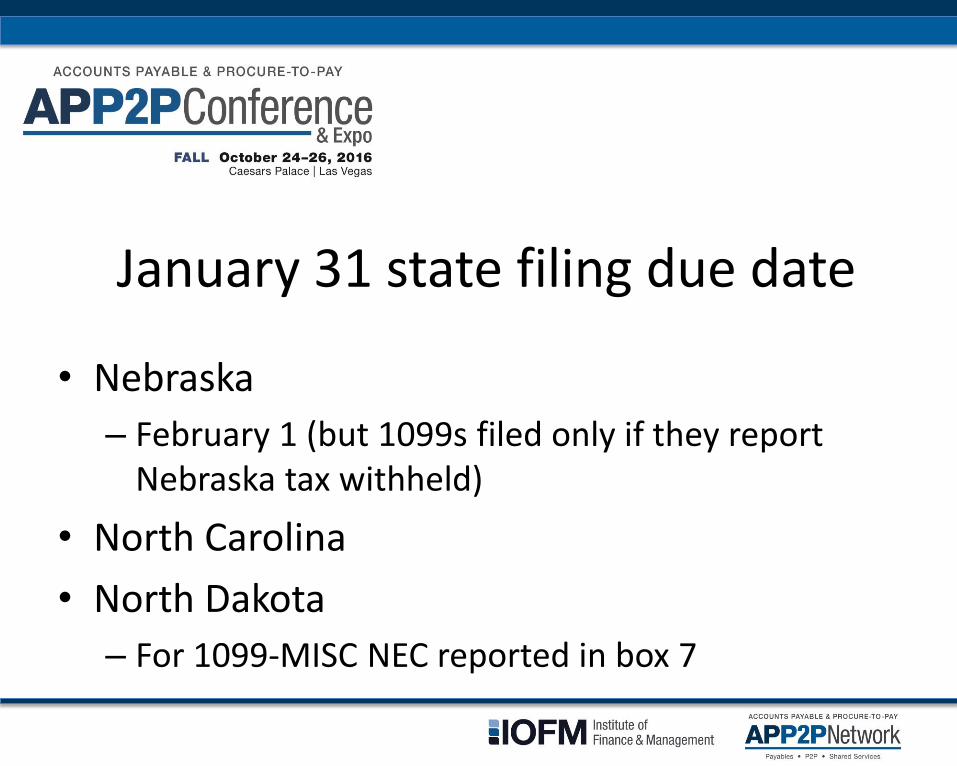

January 31 state filing due date

• Nebraska

– February 1 (but 1099s filed only if they report Nebraska tax withheld)

• North Carolina

• North Dakota

– For 1099-MISC NEC reported in box 7

January 31 state filing due date

• Ohio – For 1099-MISC NEC reported in box 7, but 1099-MISC

returns required only if they report Ohio tax withheld

• Oregon – State tax agency has indicated likely to change to Jan. 31

for forms that report Oregon tax withheld

• Pennsylvania – For 1099-MISC NEC reported in box 7, but awaiting

clarification of possible Jan. 31 due date for all 1099-MISC

January 31 state filing due date

• South Carolina – But 1099-MISC forms filed only if they report South

Carolina income tax withheld

• Vermont

• Virginia – But 1099-MISC forms filed only if they report Virginia

income tax withheld

January 31 state filing due date

• Wisconsin

– Jan. 31 for 1099-MISC forms that report Wisconsin income tax withheld; Feb. 28 for others

• Check state websites to monitor for additional states that may follow the lead of Congress and impose the January 31 filing due date

Top issues in state 1099 filing

• States need information earlier, to check against income tax returns

• States share information with IRS – Regardless of whether you asked IRS to forward data

• State audits and information requests

• Audits of others (individuals or entities) lead state tax examiners to your organization

Nexus: Where must you file?

• Nexus to report 1099s is a complex issue

– Where do you have business locations?

– Where do you operate and serve customers?

– Where do you have employees working?

– Which states are the source of Form 1099-MISC reportable income you are paying?

State tax withholding requirements

• State backup withholding: Piggybacked on federal backup withholding for missing or incorrect taxpayer ID number

• State withholding on specific types of non-wage income

State tax withholding requirements • State backup withholding where federal BWH applies:

– California: 7% – Colorado: 4.63% – Georgia: 6% (on reportable fees for services) – Iowa: 5% – Maine: 5% – Minnesota: 9.85% (if an entertainment entity or an individual

fails to furnish tax ID number) – South Carolina: 7% – Vermont: 24% of federal 28% (6.72% of payment)

State income tax withholding on specific types of payments

• California: 7% on certain payments to nonresidents • Colorado: 4.63% if tax ID number is an ITIN • Connecticut: 6.99% on certain entertainers and athletes • Kansas: 4.5% on management and consulting fees paid to a non-

resident of Kansas • Massachusetts: At wage withholding rates, on payments to

performers (individuals or entities) • Minnesota: 2% on entertainers not Minnesota residents (individuals

or entities), $600 threshold or $1,000 threshold for public speakers

State income tax withholding on specific types of payments

• Missouri: 2% on payments to entertainers not Missouri residents (individuals or entities), $300 threshold

• Nebraska: Tax calculated from Nebraska tax agency publication, withheld from certain nonresident individuals and entities providing personal services in Nebraska

• North Carolina: 4% if the tax ID number furnished by an independent contractor is an ITIN; 4% on payments to non-NC resident performers, entertainers, public speakers, athletes (individuals or certain entities), $1,500 annual threshold

• South Carolina: 7% if the tax ID number furnished is an ITIN (unless an IRS Form 8233 claim of withholding exemption is in effect for the year)

• Wisconsin: 6% on payments to entertainers not Wisconsin residents (individuals or entities), $7,000 annual threshold, surety bond may avoid withholding

State income tax withholding on specific types of payments

• Construction contractors – Many states have withholding requirements if contactor is

not resident in the state – May be provision for contractor to furnish surety bond to

the state to avoid withholding

• Oil and gas / mineral royalties, production payments, severance – Colorado, Kansas, Montana, New Mexico, North Dakota,

Oklahoma, Pennsylvania, Utah

No 1099-MISC filing • No 1099-MISC filing to state because state does not have income

tax: – Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee

(taxes only interest and dividends), Texas, Washington, Wyoming

• No 1099-MISC filing to state (though state has income tax): – Illinois, Iowa, Maryland, New York IOWA has reinstated 1099 filing – Arizona (by default because no 1099 filing if no tax withheld, and state

has no provision for withholding from 1099-MISC reportable payments)

– Indiana (for nearly all payers because no 1099 filing if no tax withheld, and withholding on 1099-MISC reportable payments is limited to members of sports race teams)

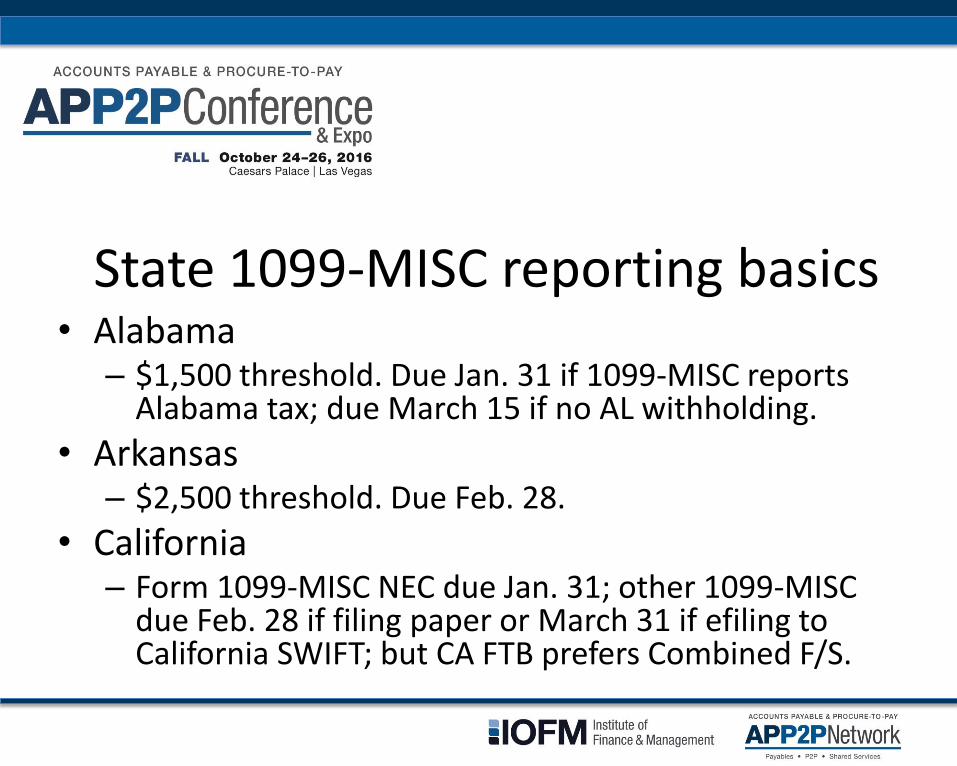

State 1099-MISC reporting basics • Alabama

– $1,500 threshold. Due Jan. 31 if 1099-MISC reports Alabama tax; due March 15 if no AL withholding.

• Arkansas – $2,500 threshold. Due Feb. 28.

• California – Form 1099-MISC NEC due Jan. 31; other 1099-MISC

due Feb. 28 if filing paper or March 31 if efiling to California SWIFT; but CA FTB prefers Combined F/S.

State 1099-MISC reporting basics • Colorado

– Due Feb. 28 if filing paper (up to 249); due March 31 if filing electronically.

• Connecticut – Due March 31. Electronic filing required.

• Delaware – Agency has said anticipate change to Jan. 31 due date for 1099-MISC

NEC; otherwise due Feb. 28 if filing paper; due March 31 if filing electronically.

• District of Columbia – Due Jan. 31; report only if the 1099-MISC reports DC income tax

withholding.

State 1099-MISC reporting basics • Georgia

– Form 1099-MISC NEC due Jan. 31; otherwise due Feb. 28; but report only if withholding GA tax.

• Hawaii – Due Feb. 28.

• Idaho – If withholding reported on 1099-MISC and filed along with

W-2s, due Jan. 31 and filed electronically. Otherwise 1099-MISC due Feb. 28 (but legislature might enact Jan. 31 due date).

State 1099-MISC Reporting Basics

• Iowa – Has reinstating 1099 reporting – Due Jan. 31 – All electronic filing – Optional for 2016 due in 2017, but mandatory for 2017 due in

2018 and penalties have been reinstated for failure to file

• Kansas – Due Feb. 28.

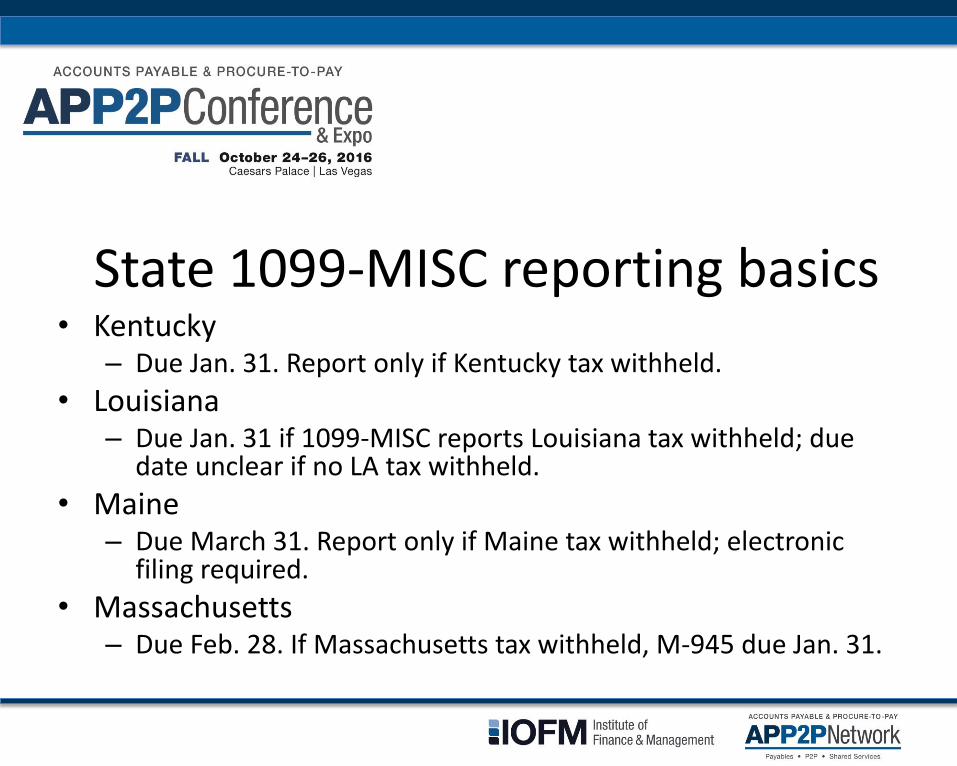

State 1099-MISC reporting basics • Kentucky

– Due Jan. 31. Report only if Kentucky tax withheld.

• Louisiana – Due Jan. 31 if 1099-MISC reports Louisiana tax withheld; due

date unclear if no LA tax withheld.

• Maine – Due March 31. Report only if Maine tax withheld; electronic

filing required.

• Massachusetts – Due Feb. 28. If Massachusetts tax withheld, M-945 due Jan. 31.

State 1099-MISC reporting basics

• Michigan – Due Feb. 28. Reporting to cities also required.

• Minnesota – Due Feb. 28.

• Mississippi – Due Feb. 28 if filing paper (fewer than 25 forms); due March 31

if filing electronically.

• Missouri – $1,200 threshold. Due Feb. 28.

State 1099-MISC reporting basics • Montana

– Due Feb. 28.

• Nebraska – Due Feb. 1. Report only if 1099-MISC reports Nebraska tax

withheld.

• New Jersey – Due Feb. 15 (but considered timely up to Feb. 28).

• New Mexico – Due Feb. 28. Report 1099-MISC only if New Mexico tax

withheld; except for oil and gas payments which require filing.

State 1099-MISC reporting basics • North Carolina

– Due Jan. 31. Electronic filing required.

• North Dakota – 1099-MISC NEC due Jan. 31; other 1099-MISC due Feb. 28 if

they report ND withholding or if filing non-withholding forms on paper (fewer than 250 forms) or due March 31 if no withholding and filing electronically

• Ohio – 1099-MISC NEC due Jan. 31; other 1099-MISC due Feb. 28 if

filing on paper (fewer than 250 forms) or due March 31 if filing electronically.

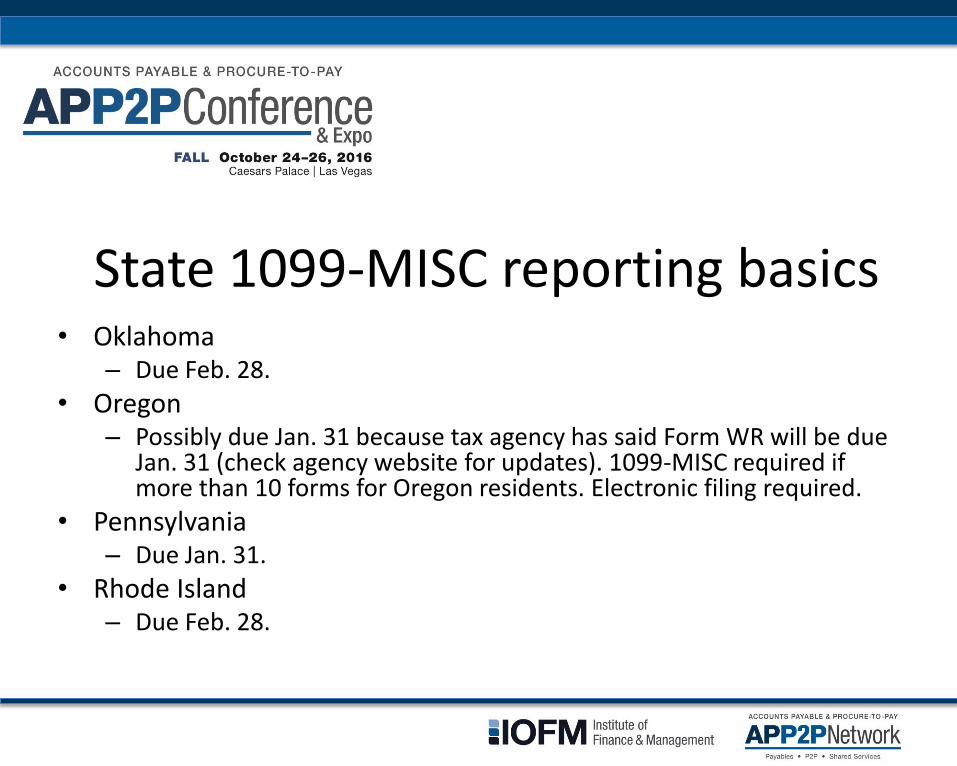

State 1099-MISC reporting basics • Oklahoma

– Due Feb. 28.

• Oregon – Possibly due Jan. 31 because tax agency has said Form WR will be due

Jan. 31 (check agency website for updates). 1099-MISC required if more than 10 forms for Oregon residents. Electronic filing required.

• Pennsylvania – Due Jan. 31.

• Rhode Island – Due Feb. 28.

State 1099-MISC reporting basics • South Carolina

– Due Jan. 31. Electronic filing required if 250 or more forms.

• Utah – Report only if Utah tax withheld, and Utah withholding does not

apply to 1099-MISC generally (only to mineral production payments; see Form TC-675R due Feb. 28 if filing paper, March 31 if filing electronically)

• Vermont – Due Jan. 31 if 1099-MISC reports Vermont tax withheld; unclear

whether 1099-MISC not reporting withholding will be due Jan. 31 or Feb. 28.

State 1099-MISC reporting basics

• Virginia – Due Jan. 31. Report if 1099-MISC shows Virginia tax

withheld. Electronic filing required.

• West Virginia – Due Feb. 28. Electronic filing required if 1099-MISC reports

WV tax withheld or if 50 or more forms.

• Wisconsin – Due Jan. 31 if reporting Wisconsin tax withheld; due Feb.

28 if no Wisconsin tax withheld.

Combined Federal/State Filing

• IRS will extract 1099 data from your IRS electronic file, for states you specify, and send the data to state tax agencies

• Not all states participate – And in addition, if 1099s report state income tax withheld,

most participating states require those 1099s to be filed directly to state tax agency

• Available only for these forms: – 1099-MISC, -B, -DIV, -G, -INT, -K, -OID, -PATR, -R, -5498

Combined Federal/State Filing State Code State Code State Code Alabama 01 Kansas 20 Nebraska 31 Arizona 04 Louisiana 22 New Jersey 34 Arkansas 05 Maine 23 New Mexico 35 California 06 Maryland 24 North Carolina 37 Colorado 07 Massachusetts 25 North Dakota 38 Connecticut 08 Michigan 26 Ohio 39 Delaware 10 * Minnesota 27 South Carolina 45 Georgia 13 Mississippi 28 Vermont 50 Hawaii 15 Missouri 29 Virginia 51 Idaho 16 Montana 30 Wisconsin 55 Indiana 18 * Delaware publication (Aug. 2016) says CF/SF no longer allowed for 1099-MISC

IRS electronic file, “A” Record

• In the “A” Record (information about payer)

– Field position 6

– Enter numeral 1 in this position if you want your IRS electronic file used for Combined Federal/State Filing

– If the Payer “A” Record is coded for CF/SF, there also must be coding in the Payee “B” Records and the State Totals “K” Records.

IRS electronic file, “B” Records

• Each “B” record is the 1099 data for a payee

• All reportable data for each payee, including

– Field positions 488-489: Payee State

– Enter two alpha characters that are the valid U.S. Postal Service state abbreviation for the payee’s address

IRS electronic file, “K” Record • If you want to use Combined Federal/State Reporting,

create a “K” record for each state

• Each “K” record reports totals for that state: – Total number of payees reported for the state

– Total amounts reported, by 1099 form type

– Total amount of state income tax withheld (optional)

• Insert one or more “K” records (one for each state) into your file after the “C” record and before the “F” record

Extensions of filing date

• States do not automatically honor extended filing due dates you may have obtained from the IRS

• Check state publications and websites to find out whether the state grants filing extensions and how to request an extension

States may change rules at any time

• No two states are alike in their 1099-MISC filing requirements

• All states with filing requirements have penalties for failure to file

• Check state websites because state legislatures and tax agencies may change rules, due dates, forms or publications at any time – Including close to calendar year end and sometimes after

January 1 of the filing year

![Preparing your 1099-MISC for printing and mailing · Clear Printed flag - [Tools\Clear Print Indicators] 07_Print_and_Mail_in_Account_Ability Page 14 OFM Training: IRS 1099-MISC Reporting](https://img.dokumen.tips/doc/110x75/5f989ccbf1bba20ff35dfc28/preparing-your-1099-misc-for-printing-and-mailing-clear-printed-flag-toolsclear.jpg)