Embed Size (px)

Citation preview

IRS Forms W-9, W-8,

W-2, 1099-Misc: How

to Comply, Oh My!©2018 Region One Education Service Center

Agenda• Obtaining Vendor Information• TIN Matching• What is Form 1099?• Overview of 1099 Reporting Requirements/Who is

Required to File• Definitions/Applicability/Distribution• Detailed Requirements for Form 1099-Misc• Q&A• Resources ©2018 Region One Education Service Center

Obtaining Vendor

Information

©2018 Region One Education Service Center

OBTAINING VENDOR INFORMATION

» Form W-9- Provide to every vendor- Used to obtain an identifying number of a vendor- Identifies the type of business➢ Sole proprietor➢ LLC➢ Corporation➢ Partnership➢ Trust/Estate

©2018 Region One Education Service Center

Form W-9

©2018 Region One Education Service Center

FORM W-9» Provides the identifying number for the vendor

- Sole proprietor use Social Security Number (SSN)- Corporations, partnerships and estates use Employer

Identification Number (EIN)- LLC – Name must match with SSN or EIN

➢ A LLC can be treated as a sole proprietor, partnership or corporation➢ DO NOT assume that LLC in the business name means that you do

not have to file a Form 1099

» Certifies that the Taxpayer Identification Number (TIN) is correct

» Taxpayer certifies that they are not subject to backup withholding or exempt

©2018 Region One Education Service Center

FORM W-9 (cont.)» The IRS site states:➢ If the district does not obtain an SSN or EIN before the

district pays the contractor, the district must withhold income tax from the payment, generally referred to as backup withholding

➢ Backup withholding rules require that twenty-four percent (24%) of the payment be withheld, and reported on Form 945, Annual Return of Withheld Federal Income Tax

➢ https://www.irs.gov/forms-pubs/form-945-annual-return-of-withheld-federal-income-tax

©2018 Region One Education Service Center

FORM W-9 (cont.)» When is it necessary for a Vendor to complete a NEW W-9➢ New Vendor➢ Name Change (example: doing business as)➢ Staff and Students receiving payments other than

reimbursements➢ Business Entity Change – such as sole owner to

corporation, sole owner to partnership, partnership to corporation, etc.

©2018 Region One Education Service Center

TIN MATCHING PROGRAMS

» Allows payers or authorized agents who submit forms 1099-INT, DIV, PATR, OID, MISC and B the capability of submitting an online Taxpayer Identification Number (TIN) and name combination to be matched against IRS records

» Allows verification of W-9’s using vendor’s TIN» TIN can be either Employer Identification Number (EIN)

or a Social Security Number (SSN)

©2018 Region One Education Service Center

TIN MATCHING PROGRAMS (cont.)

» IRS site available 24 hours per day, 7 days per week» Access IRS TIN matching by visiting e-services at

www.irs.gov/individuals/e-services-registration- Registration is required for this service

» Contact e-services- 866-255-0654- 6:30 a.m. to 6 p.m. CST, Monday – Friday

©2018 Region One Education Service Center

IRS TIN MATCHING SITE

©2018 Region One Education Service Center

-Once registered, access the TIN Matching site at:https://www.irs.gov/tax-professionals/e-services-online-tools-for-tax-professionals

©2018 Region One Education Service Center

-Login with Username

©2018 Region One Education Service Center

-Provide Password

-The Site Image and Site Phrase are part of the

registration process

©2018 Region One Education Service Center

-Enter security code from text message

-Phone number provided during registration process

©2018 Region One Education Service Center

-Select Organization

-Set up during registration process

©2018 Region One Education Service Center

-Accept Terms of Agreement

©2018 Region One Education Service Center

-Choose an Interactive Session or Bulk Session

-Typically use Interactive

©2018 Region One Education Service Center

-Choose TIN type from dropdown – either EIN or SSN

-Enter the 9-digit number and the Business Name exactly as it

appears on IRS documents

-Add

©2018 Region One Education Service Center

-Verify the entry and Submit

-The Result Code will dictate whether the number matches

-Save screen as proof of verification

©2018 Region One Education Service Center

TIN MATCHING PROGRAMS (cont.)

» For verifying SSN’s- District can verify up to five (5) SSN’s by calling

the Social Security Administration (SSA)- Verify up to fifty (50) by writing to the SSA- See SSA website for more information

www.ssa.gov/employer

©2018 Region One Education Service Center

Form W-8https://apps.irs.gov/app/picklist/list/formsInstructions.html?value=w-8&criteria=formNumber

©2018 Region One Education Service Center

Form W-8» Used by non-resident aliens who do work and/or make income in

the U.S. or foreign business entities who make income in the U.S.

» Non-resident aliens are charged 30 percent on funds received by US companies.

» Anyone working for a U.S. company but living in a foreign country that has entered into an income tax treaty with the United States: Australia, Armenia, the Netherlands, Canada and Mexico.

» Corporations that perform business in the United States but have no actual presence in the country

©2018 Region One Education Service Center

W-8BEN» Used primarily by entities and individuals to claim foreign

status or treaty benefits to establish that the Payee is not a US entity.

» Is there a US reporting TAX ID Number? If yes, then is part II completed claiming Treaty benefits? If so, then payment is tax exempt if income is covered by an article in the Treaty.

» All fields in line 10 must be completed to claim exemption on royalty payments. If there is no Tax ID number, then payment

is subject to 30% withholding.©2018 Region One Education Service Center

W-8BEN-E» Used by beneficiary owners (businesses only) that claim to be

tax residents outside of the United States.

» Foreign persons are subject to U.S. tax at a 30% rate on income they receive from U.S. sources that consists of: Interest (including certain original issue discount (OID)); Dividends; Rents; Royalties; Premiums; Annuities; Compensation for, or in expectation of, services performed; Substitute payments in a securities lending transaction; or Other fixed or determinable annual or periodical

gains, profits, or income.

©2018 Region One Education Service Center

W-8ECI» Used primarily by the payee or beneficial owner indicating that the income that

is listed on the form is effectively connected with the conduct of a trade or business within the United States. (The foreign parent company / organization has a location inside the US from which product is sent or services performed and that location does not have a separate US Tax ID number.)

» If there is a US tax reporting number, the payment is subject to 30% tax withholding unless there is a services income listed on line 9.⋄ In that case, payment is exempt from withholding. If there is not a services

income listed on line 9 then we are required to obtain from the entity a different type of W-8 form.

» If there is no US tax reporting number, then payment is subject to 30% withholding.

©2018 Region One Education Service Center

W-8EXP» Used primarily by the following entities to claim exemption from

tax withholding: Foreign governments, foreign tax exempt organizations, foreign private foundations, government of a US possession, or foreign central bank of issue. ⋄ These entities must be claiming exemption under IRS Code

115(2) 501© 89s, 895 94 1443(b). Otherwise they need to file a W-8BEN or W-ECI.

» Payment for form, W-8EXP, is usually exempt from withholding.

©2018 Region One Education Service Center

W-8IMY» Used primarily by an intermediary, a withholding foreign

partnership, a withholding foreign trust or a flow through entity.

» Copies of appropriate withholding certificates, documentary evidence, and withholding statements must be attached to the W-8IMY.

» Payment for form, W-8IMY, is usually exempt from withholding.

©2018 Region One Education Service Center

Entities Flowchart

Form W-2https://www.irs.gov/pub/irs-pdf/iw2w3.pdf

©2018 Region One Education Service Center

Form W-2» Used by employer to report wage and salary information for

employees.

» Shows the amount of taxes withheld from a paycheck that is used to file Federal tax.

» IRS requires employers to report wage and salary information for employees and other taxes withheld from paycheck by January 31.

» Amounts withheld are remitted to the IRS.

©2018 Region One Education Service Center

Form W-2

©2018 Region One Education Service Center

What is Form 1099?

©2018 Region One Education Service Center

» 1099 – A Acquisition or Abandonment of Secured Property

» 1099 – B Proceeds from Broker and Barter Exchange Transactions

» 1099 – C Cancellation of Debt» 1099 – CAP Changes in Corporate

Control and Capital Structure» 1099 – DIV Dividends and Distributions» 1099 – G Certain Government Payments» 1099 – INT Interest Income» 1099 – K Payment Card and Third Party

Network Transactions» 1099 – LTC Long-Term Care and

Accelerated Death Benefits

TYPES OF FORM 1099

» 1099 – MISC Miscellaneous Income» 1099 – OID Original Issue Discount» 1099 – PATR Taxable Distributions Received

From Cooperatives» 1099 – Q Payments from Qualified Education

Programs» 1099 – QA Distribution from ABLE Accounts» 1099 – R Distributions from Pensions,

Annuities, Retirement or Profit-Sharing Plans, etc.

» 1099 – S Proceeds from Real Estate Transactions

» 1099 – SA Distributions from an HSA, Archer MSA, or Medicare Advantage MSA

©2018 Region One Education Service Center

WHAT IS FORM 1099-MISC?» Type of tax form» Typically they are given to independent contractors, also known

as "freelancers“, as a record of the income they received» The income earned will be noted, but there will not be any

deductions for Federal income taxes, nor will any deferred compensation, social security, or medical deductions be taken

» The 1099 recipient is not an employee of the district» The district is obligated only to tender the income to the

contractor sans any deductions» Those who receive 1099 income come from a wide spectrum

and are generally compensated on a "per job" basis and are not treated as employees

©2018 Region One Education Service Center

Overview

©2018 Region One Education Service Center

OVERVIEW

» 1099-MISC reporting provides two important functions- Notifies the IRS of payments made to vendors- Provides notice to the vendor of annual payments and

record of information submitted to the IRS

©2018 Region One Education Service Center

OVERVIEW (cont.)

©2018 Region One Education Service Center

OVERVIEW (cont.)

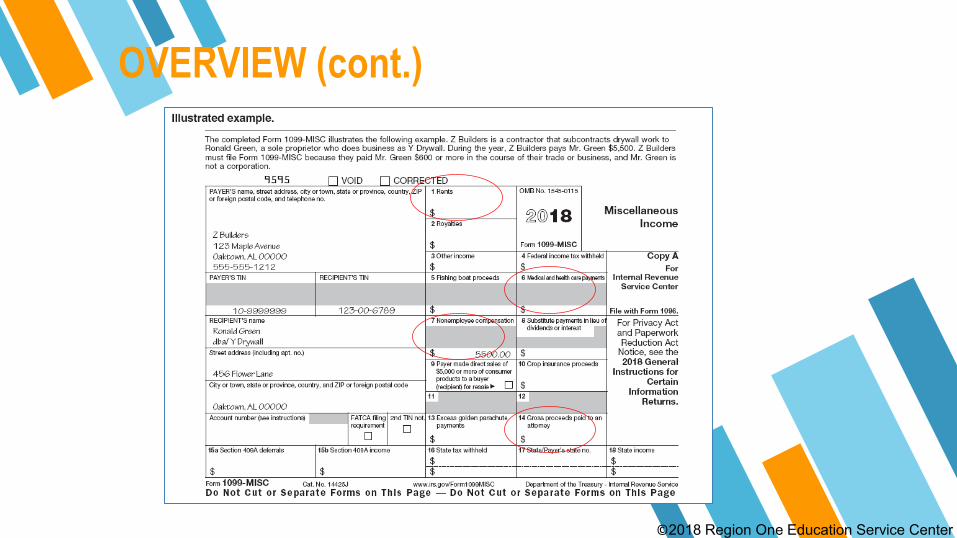

» Any entity conducting a trade or business is required to file Form 1099-MISC for each person to whom you have paid during the year:

at least $600 in: • Rents (Box 1);• services performed by someone who is not your employee (Box 7);• prizes and awards (Boxes 3 and 7);• other income payments (Box 3);• medical and health care payments (Box 6);• crop insurance proceeds (Box 10);• cash payments for fish (or other aquatic life) you purchase from anyone engaged in the trade or

business of catching fish (Box 7);• generally, the cash paid from a notional principal contract to an individual, partnership, or estate;• payments to an attorney (Box 7 or Box 14); or• any fishing boat proceeds,

©2018 Region One Education Service Center

OVERVIEW (cont.)

» Who receives a 1099-MISC?- Individuals- Partnerships- Nonprofit organizations- Estates- Trusts- Medical and attorney sole proprietors/corporations

» Reportable payments to corporations. The following payments made to corporations generally must be reported on Form 1099-MISC:- Medical and health care payments reported in box 6.- Fish purchases for cash reported in box 7.- Attorneys' fees reported in box 7.- Gross proceeds paid to an attorney reported in box 14.

©2018 Region One Education Service Center

OVERVIEW (cont.)

» Payments for which a Form 1099-MISC is not required- Generally, payments to a corporation (including a limited

liability company (LLC) that is treated as a C or S corporation). However, refer to Reportable payments to corporations.

©2018 Region One Education Service Center

NON-REPORTABLE PAYMENTS» Do not issue 1099’s for:

- Payments to employees (e.g., fringe benefits, travel reimbursements, etc.)- Products- Worker’s compensation- Storage- Utilities- Payments to governmental agencies- Corporations (Unless they are Medical or Attorney Fees) - Scholarships (Unless they are paid for teaching research or other service

condition for receiving the grant/scholarship are considered wages and must be reported on Form W-2)

©2018 Region One Education Service Center

OVERVIEW - COMPLIANCE

» An internal policy allows district to comply with IRS regulations concerning issuance and accuracy of annual tax statements to vendors- Facilitates IRS reporting requirements

➢ Certain types of payments made to vendors must be reported to the IRS

➢ Having a signed W-9 on file allows districts to report the correct combination of Tax Identification Number (TIN) and name, thus avoiding IRS penalties

- Evidence of validity is documented➢ Having a signed W-9 on file is considered evidence that the payee

is a valid individual or business➢ Avoids inappropriate payments to fraudulent entities

©2018 Region One Education Service Center

OVERVIEW COMPLIANCE (cont.)

» A district, on an annual basis, must issue 1099 tax statements to all eligible vendors regarding the income they received

» The district must electronically transmit a file to the IRS with accurate data pertaining to those vendors including Name, Address, Tax Identification Number and Gross Income

©2018 Region One Education Service Center

EXAMPLES OF REPORTABLE PAYMENTS

➢ Rentso Office spaceo Parking spaceo Equipment

➢ Non-employee compensation (services)o Advertisingo Custodial/maintenanceo Professional feeso Appraiserso Consultants/Honorariumso Awards

©2018 Region One Education Service Center

Definitions

Applicability

Distribution

©2018 Region One Education Service Center

DEFINITIONS

» Vendor- A vendor for this purpose is every entity, business or

person that have a vendor record in your Accounts Payable system

» Vendor Maintenance- The electronic means of storing changes to the

vendor information who supplies goods/services» Eligible Vendor

- A vendor that is required to receive a 1099 Form due to the type of payment received

©2018 Region One Education Service Center

APPLICABILITY» Best Practice – Set up a policy/procedure that allows for review of vendor data

during the set up process and a periodic review process for vendors that have been on the system for some time.

» This policy applies to all staff that deal with vendors» WHO SHOULD KNOW THIS POLICY➢ Staff that create/review vendor set up➢ Business Office staff with Purchasing and Accounts Payable responsibility ➢ Senior Financial or Business Officers➢ Campus/Department Administrators➢ Program Directors➢ Faculty

©2018 Region One Education Service Center

DISTRIBUTION

» If reporting Non-employee compensation payments (box 7) the due date to the recipient is on or before January 31

» Form 1099’s are due to the IRS by January 31

» Who must file electronically. If you are required to file 250 or more information returns during the year, you must file electronically.

©2018 Region One Education Service Center

DISTRIBUTION

» The IRS address for filing information returns electronically is https://fire.irs.gov/

⋄ Refer to IRS Publication 1220 for general instructions and to set up an account.

⋄ Electronic Filing - you are required to establish an account on the FIRE System before transmitting files electronically. For more information on creating a User ID, password, PIN, secret phrase, and connecting to the FIRE System

⋄ Submission must comply with specified file Format

⋄ Assistance Needed – Contact the IRS at 866-455-7435

©2018 Region One Education Service Center

DISTRIBUTION - CORRECTIONS

» If an information return was successfully processed by the IRS and you identify an error with the file after the IRS accepted the file and it is in "Good, Released" status, you need to file a corrected return. Do not file the original file again as this may result in duplicate reporting. File only the returns that require corrections. Do not code information returns omitted from the original file as corrections. If you omitted an information return, it should be filed as an original return. The standard correction process will not resolve duplicate reporting. All fields of the corrected return must be complete.

©2018 Region One Education Service Center

DISTRIBUTION - CORRECTIONS

» Treasury Regulation 301.6011-2 requires filers who are required to file 250 or more information returns for any calendar year to file the returns electronically. The 250 or more requirement applies separately for each type of form filed and separately for original and corrected returns. Example: If a payer has 100 Forms 1099-A to correct, the returns can be filed on paper because they fall under the 250 threshold. However, if the payer has 300 Forms 1099-B to correct, the forms must be filed electronically.

» The filer or transmitter must furnish corrected statements to recipients as soon as possible. If a filer or transmitter discovers errors that affect a large number of recipients, contact the IRS at 866-455-7438 (toll-free). Send corrected returns to the IRS and notify the recipients.

©2018 Region One Education Service Center

Detailed Requirements for

Form 1099-Misc

©2018 Region One Education Service Center

FORM 1099-MISC Box 1 – Rents

» Enter amounts of $600 or more for all types of rents, such as the following:➢ Real estate rentals paid for office space, however, you do

not have to report these payments on Form 1099-MISC if you paid them to a real estate agent

➢ Machine rentals – if the machine rental is part of a contract that includes both the use of the machine and the operator, prorate the rental between the rent of the machine (box 1) and the operator’s charge (box 7)

➢ Land rentals (parking lots, etc.)©2018 Region One Education Service Center

FORM 1099-MISC Box 2 – Royalties

» Enter gross royalty payments (or similar amounts) of $10 or more

» Report royalties from oil, gas, or other mineral properties before reduction for severance and other taxes that may have been withheld and paid

» Surface royalties should be reported in box 1

©2018 Region One Education Service Center

FORM 1099-MISC Box 3 – Other Income» Enter other income of $600 or more required to be reported on Form 1099-MISC

that is not reportable in one of the other boxes on the form» Deceased employee's wages - If you made the payment after the year of death,

do not report it on Form W-2, Report the payment on Form 1099-MISC box 3.» Also enter into box 3 prizes and awards that are not for services performed – do

not include prizes and awards paid to your employees; report these on Form W-2» Prizes and awards for services performed by nonemployees, such as an award for

the top commission salesperson should be reported in box 7» Report in box 3 all punitive damages, any damage for nonphysical injuries or

sickness, and any other taxable damages – report all compensatory damages for nonphysical injuries or sickness, such as employment discrimination or defamation

©2018 Region One Education Service Center

FORM 1099-MISC Box 4 – FIT Withheld

» Enter backup withholding, e.g. persons who have not furnished their TIN’s to you are subject to withholding (24% effective December 2017) on payments required to be reported in boxes 1, 2, 3, 5, 6, 7, 8, 10, and 14, with exceptions

©2018 Region One Education Service Center

FORM 1099-MISC Box 6 – Medical and

Health Care Payments» Enter payments of $600 or more made in the course of business to each

physician or other supplier or provider of medical or health care services» Include payments made by medical and health care insurers under health,

accident, and sickness insurance programs» If the payment is made to a corporation, list the corporation as the recipient

rather than the individual providing the service – reporting is not required for payments to pharmacies for prescription drugs

» The exemption from issuing Form 1099-MISC to corporation does not apply to payments for medical or health care services provided by corporations, including professional corporations

» The exemption does apply to payments made to a tax-exempt hospital or extended care facility owned and operated by the United States, a state, the District of Columbia, or any other of their political subdivisions, agencies, or instrumentalities

©2018 Region One Education Service Center

FORM 1099-MISC Box 7 –

Nonemployee Compensation» Enter nonemployee compensation of $600 or more – include fees, commissions,

prizes and awards for services performed as a nonemployee, other forms of compensation for services performed for your district by an individual who is not your employee, and fish purchases for cash

» What is nonemployee compensation? If the following conditions are met, you must generally report a payment as nonemployee compensation:➢ Payment to someone who is not your employee➢ Payment for services in the course of your trade or business (including

governments)➢ Payment to an individual, partnership, estate, or, in some cases, a

corporation➢ Payments to the payee of at least $600 during the year

©2018 Region One Education Service Center

FORM 1099-MISC Box 7 –

Nonemployee Compensation (cont.)» Some examples of payments to be reported in box 7:➢ Professional service fees, such as fees to attorneys (including corporations,

accountants, architects, contractors, engineers, etc.➢ Payment for services, including payment for parts or materials used to

perform the services if supplying the parts or materials was incidental to providing the service

➢ A fee paid to a nonemployee, including an independent contractor, or travel reimbursement for which the nonemployee did not account to the payer, if the fee and reimbursement total at least $600

➢ Payments to nonemployee entertainers for services➢ Exchanges of services between individuals in the course of their trade or

business

©2018 Region One Education Service Center

FORM 1099-MISC Box 7 –

Nonemployee Compensation (cont.)» IRS 20 Factor Test: Independent Contractor or Employee

⋄ worker classification pamphlet - irs.gov

©2018 Region One Education Service Center

FORM 1099-MISC Box 14 – Gross

Proceeds Paid to an Attorney

» Payments made to an attorney in the course of your trade or business in connection with legal services, for example, as in a settlement agreement are reportable in box 14

» These rules apply whether or not the legal services are provided to the payer and whether or not the attorney is the exclusive payee

» General legal fees are reported in box 7

©2018 Region One Education Service Center

FORM 1099-MISC Boxes 5, 8, 10, and 13

» Payments made by a local government that would require entries to these boxes would be an exception and normally not seen

©2018 Region One Education Service Center

WHY FILE FORM 1099-MISC?

» The Internal Revenue Service shares some tips on filing Forms 1099-MISC, Miscellaneous Income, to avoid costly penalties

https://www.tax.gov/Governments/Employers/WhyFileForm1099-MISC

Quick References

»1099-MISC Instructions – https://www.irs.gov/forms-pubs/about-form-1099misc

»TIN Matching – https://www.irs.gov/tax-professionals/e-services-online-tools-for-tax-

professionals

»Publication 1220 – https://www.irs.gov/forms-pubs-search?search=1220

»IRS FIRE – https://fire.irs.gov/

»IRS 20 Factor Test: Independent Contractor or Employee -www.irs.gov/pub/irs-utl/x-26-07.pdf

©2018 Region One Education Service Center

Resources

» IRS Webinar Portal:⋄https://www.irsvideos.gov/Governments/Employers

» IRS Contact:⋄Steve Obrien

Phone: 512-339-5508Email: [email protected]

Q&A

©2018 Region One Education Service Center

Contacts

Lori A. [email protected]

Amanda [email protected]

Marc David [email protected]

Hector [email protected]

©2018 Region One Education Service Center