Embed Size (px)

Citation preview

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 1/38

Akanksha Bijalwan (16018)

Parthsarthi Gupta (16025)

Nikita (16030)

BFIA 3

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 2/38

Companies = Orchards

Smart apple farmers routinely saw off dead and weakened branches to

keep their trees healthy.

Every year, they also cut back a number of vigorous limbs - those that are

blocking light from the rest of the tree or otherwise hampering its growth.

And, as the growing season progresses, they pick and discard some

perfectly good apples, ensuring that the remaining fruit gets the energy

needed to reach its full size and ripeness.

Only through such careful, systematic priming does an orchard produce its

highest possible yield.

- Dranikoff, Koller and Schneider (2002)

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 3/38

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 4/38

Combinations

Many a times, spin off is used as a precursor of equity carve

outs.

(15-20% of the shares in the spun off company are offered in

the primary market to generate some cash inflow)

Split off is sometimes also applied as a second step after an

equity carve out, but has also been used independently to

take a private subsidiary public.

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 5/38

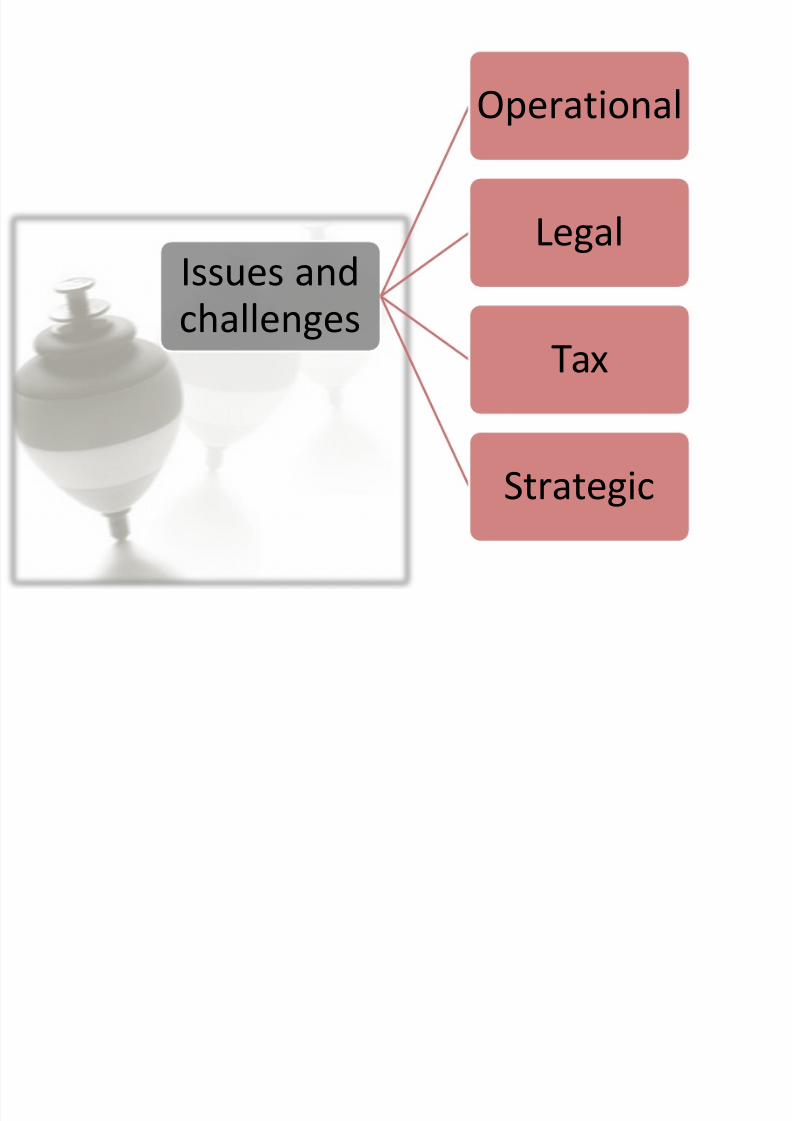

Issues andchallenges

Operational

Legal

Tax

Strategic

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 6/38

OPERATIONAL ISSUES

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 7/38

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 8/38

Example : Tyco International

• In 2007, Tyco International split into : Covidien, Tyco

Electronics, and the original Tyco International.

•

Shortly after the spin-off, then-CFO Chris Coughlin :“…the health care business, Covidien, had made significant

strides in attracting new talent that would probably not have

been attracted to the old Tyco.”

In a health care company with a clearly defined strategy,

employees and prospective employees could see themselves

advancing professionally while remaining in health care and

playing a significant role in the business.

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 9/38

The challenge

• Coughlin : “The most challenging part was to get the

management teams in place and transferring the technical

knowledge from some of the corporate functions that resided

at the Tyco headquarters to the two new businesses.”

• So they set up a formal mechanism to manage the whole

transition process and held reviews every month with each

function.

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 10/38

LEGAL ISSUES

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 11/38

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 12/38

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 13/38

Demerger is essentially a scheme of arrangement

under Section 391 to 394 of the Companies Act,

1956 requiring approval by:

• Majority of shareholders holding shares representing

three-fourths value in meeting convened for the purpose;

and

• Sanction of High Court.

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 14/38

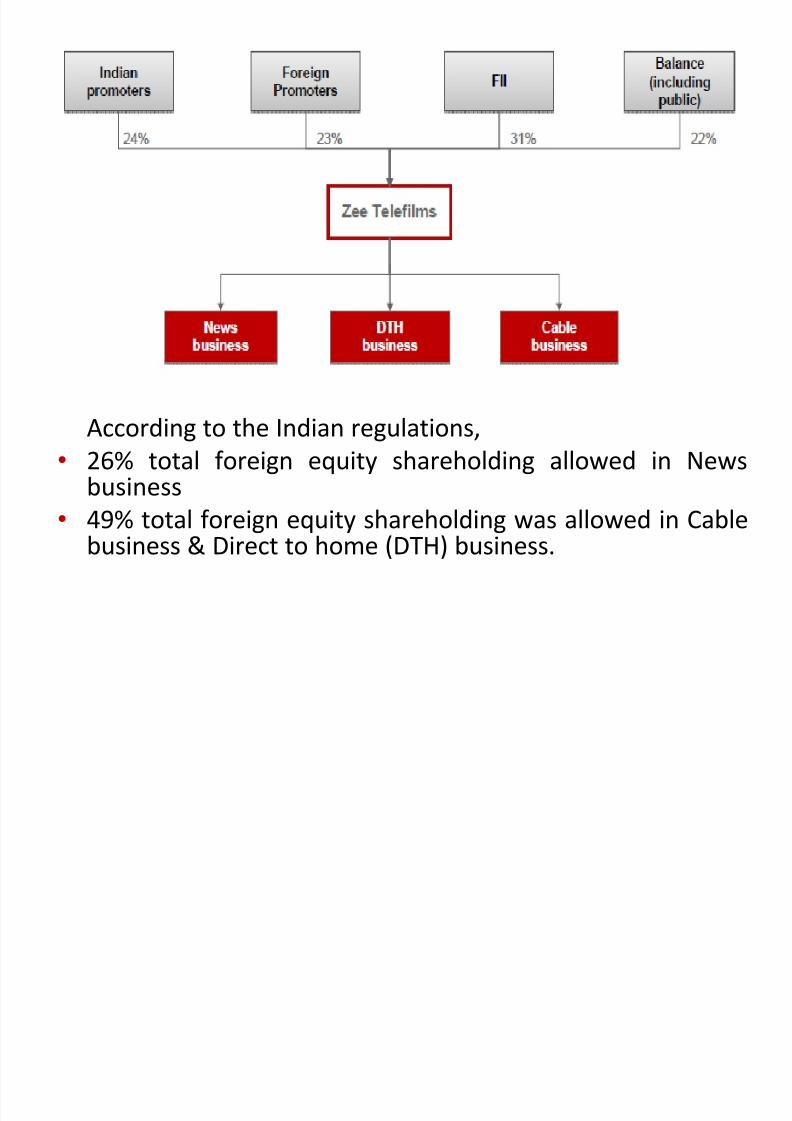

Case study

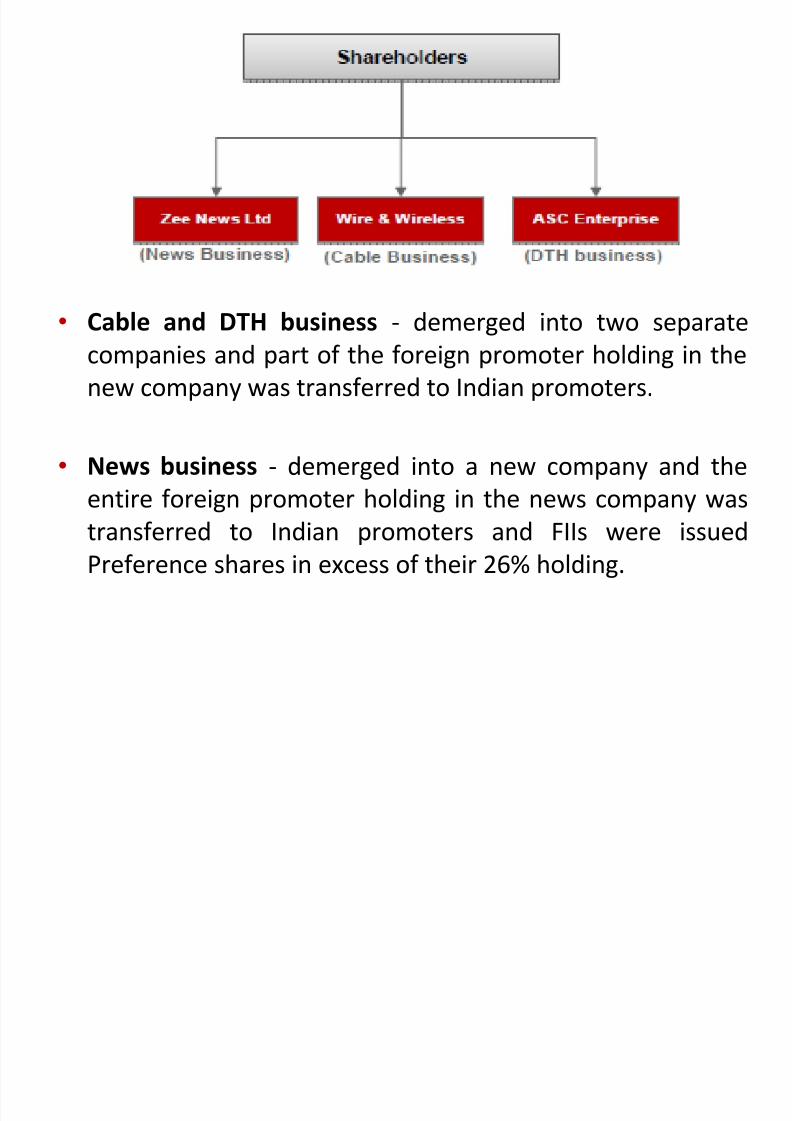

• Demerged Company: Zee Telefilms

• Resulting Companies: Zee News Limited, Wire and Wireless

India Limited & ASC enterprise

• Effective Date: 22nd November 2006

• Reason for demerger: Non compliance with the Indianregulations.

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 15/38

According to the Indian regulations,

• 26% total foreign equity shareholding allowed in Newsbusiness

• 49% total foreign equity shareholding was allowed in Cable

business & Direct to home (DTH) business.

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 16/38

• Cable and DTH business - demerged into two separate

companies and part of the foreign promoter holding in the

new company was transferred to Indian promoters.

• News business - demerged into a new company and the

entire foreign promoter holding in the news company was

transferred to Indian promoters and FIIs were issued

Preference shares in excess of their 26% holding.

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 17/38

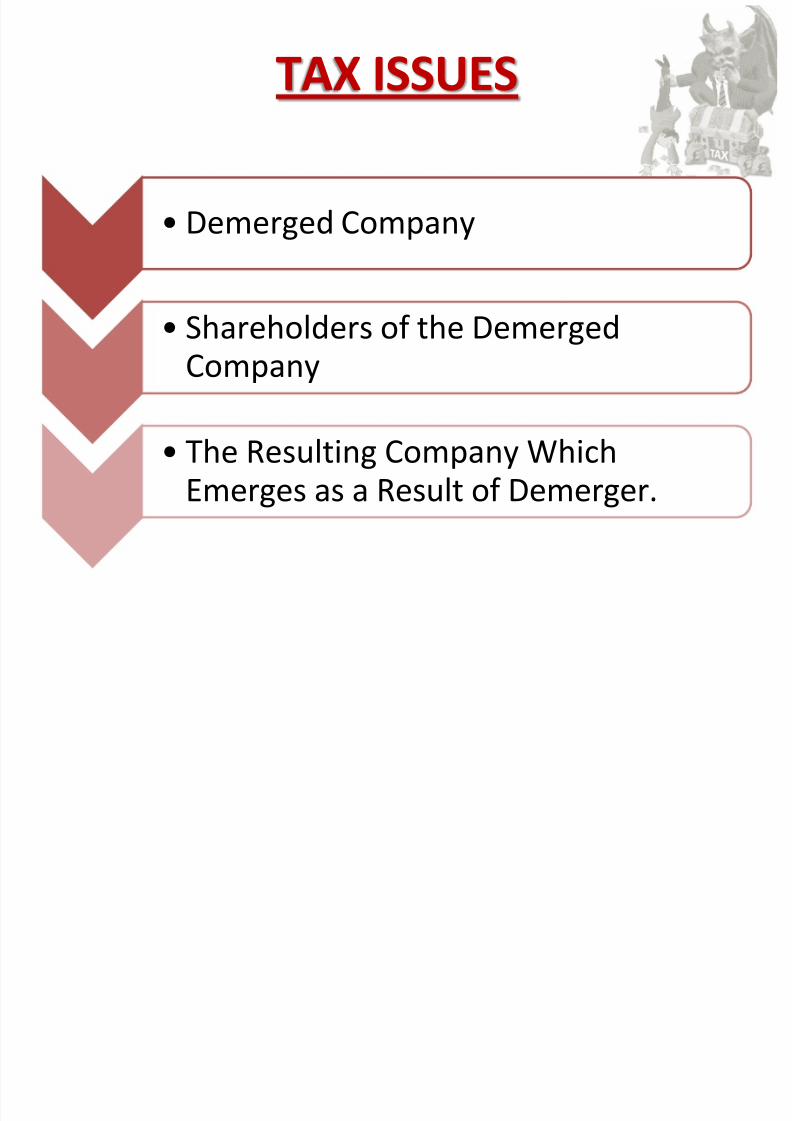

TAX ISSUES

• Demerged Company

• Shareholders of the DemergedCompany

• The Resulting Company WhichEmerges as a Result of Demerger.

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 18/38

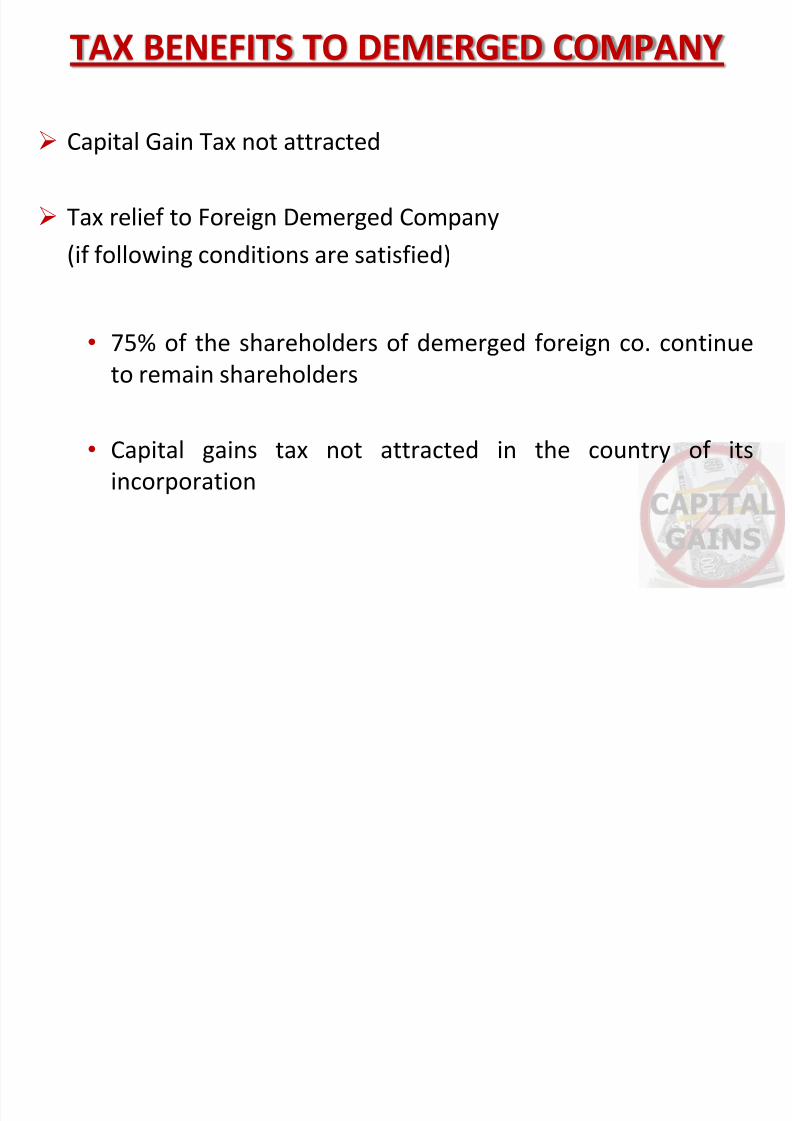

TAX BENEFITS TO DEMERGED COMPANY

Capital Gain Tax not attracted

Tax relief to Foreign Demerged Company

(if following conditions are satisfied)

• 75% of the shareholders of demerged foreign co. continue

to remain shareholders

• Capital gains tax not attracted in the country of its

incorporation

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 19/38

TAX BENEFITS TO RESULTING COMPANY

Amortisation of expenditure in case of amalgamation

or demerger

Depreciation as apportioned

The accumulated losses and unabsorbed

depreciation

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 20/38

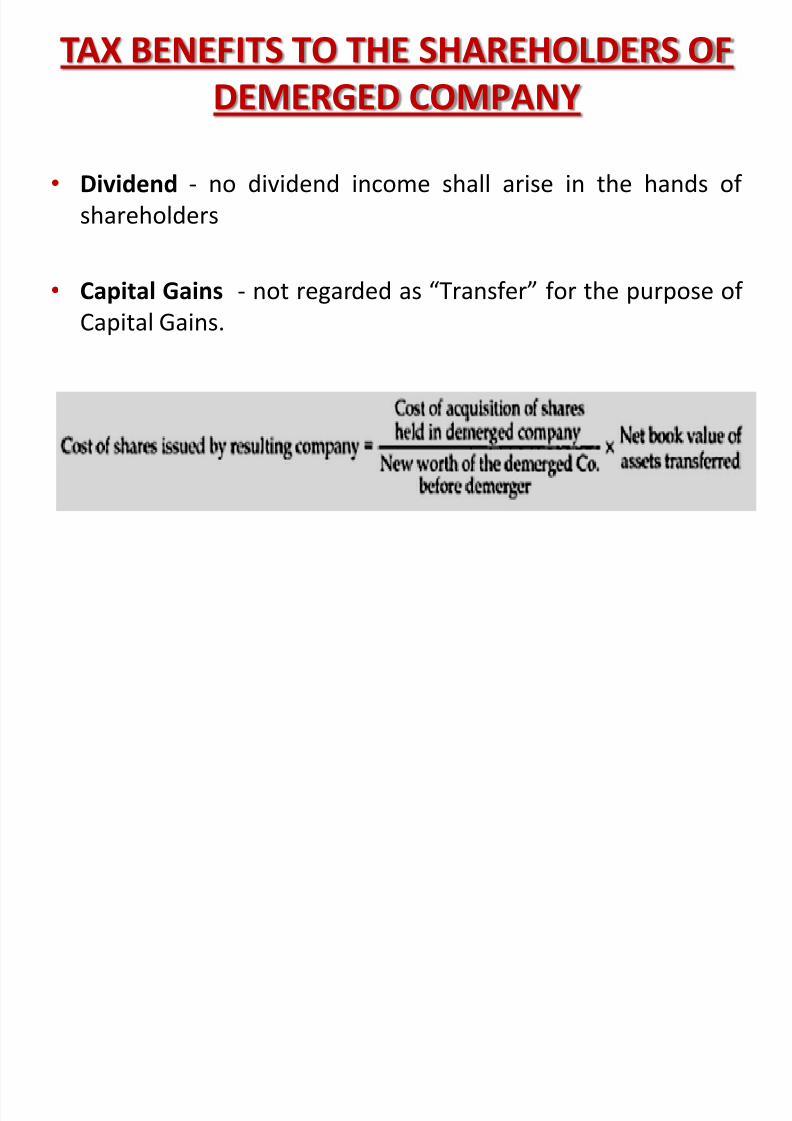

TAX BENEFITS TO THE SHAREHOLDERS OF

DEMERGED COMPANY

• Dividend - no dividend income shall arise in the hands of

shareholders

• Capital Gains - not regarded as “Transfer” for the purpose of

Capital Gains.

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 21/38

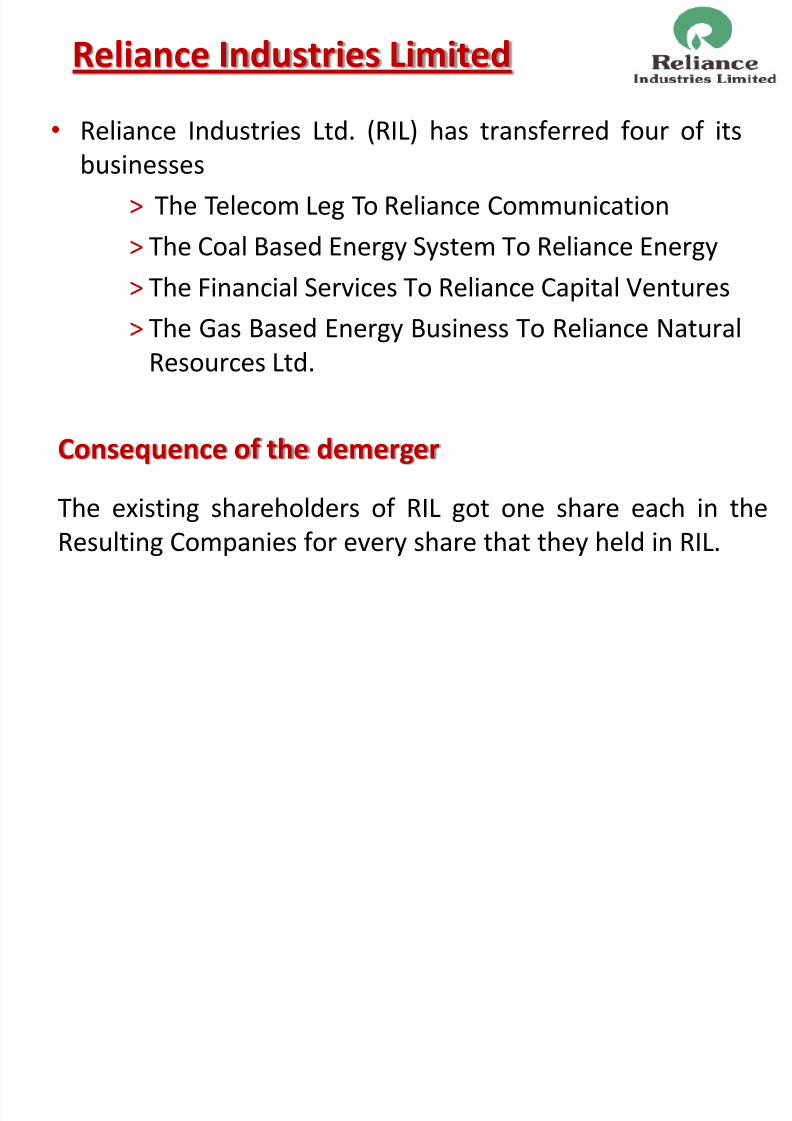

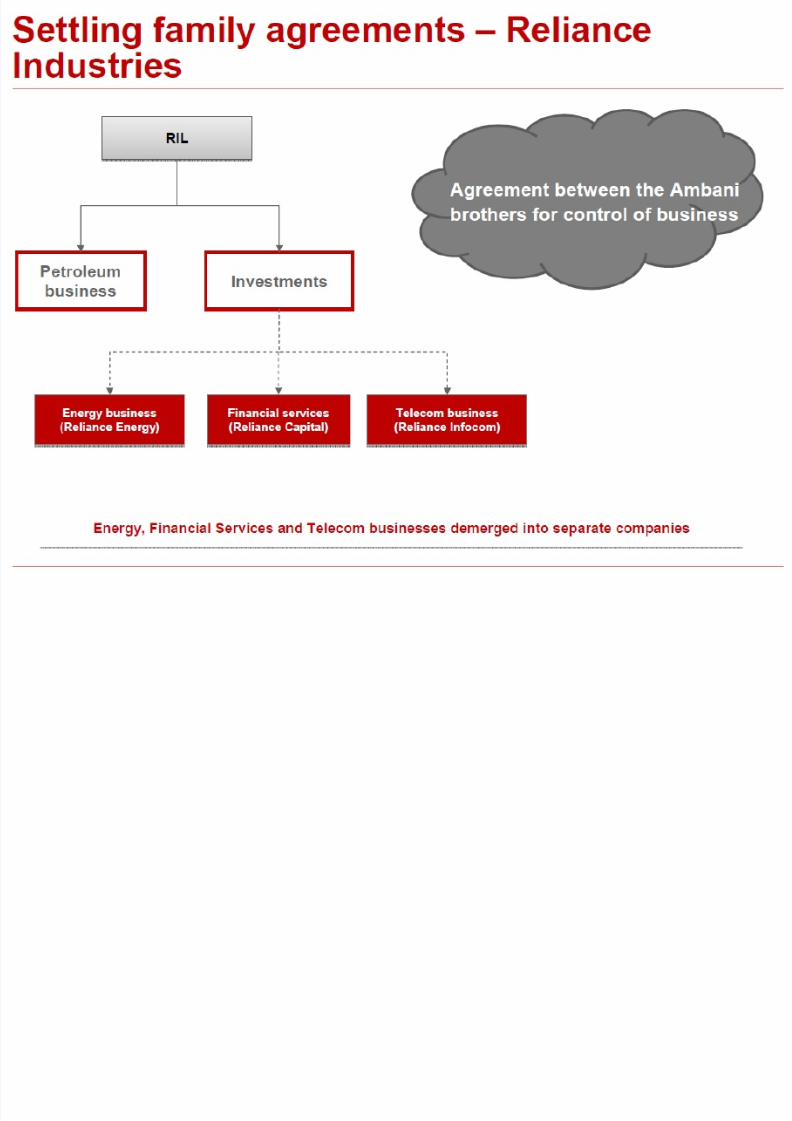

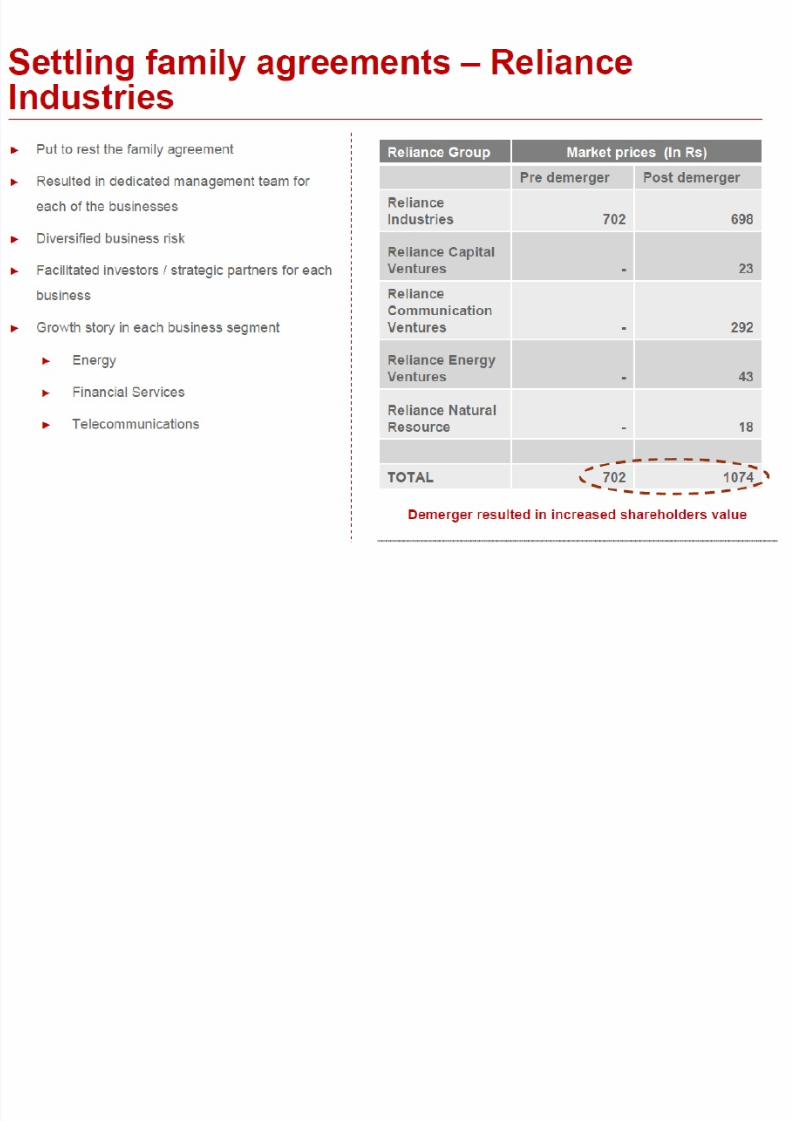

Reliance Industries Limited

•

Reliance Industries Ltd. (RIL) has transferred four of itsbusinesses

> The Telecom Leg To Reliance Communication

> The Coal Based Energy System To Reliance Energy

> The Financial Services To Reliance Capital Ventures

> The Gas Based Energy Business To Reliance Natural

Resources Ltd.

Consequence of the demerger

The existing shareholders of RIL got one share each in the

Resulting Companies for every share that they held in RIL.

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 22/38

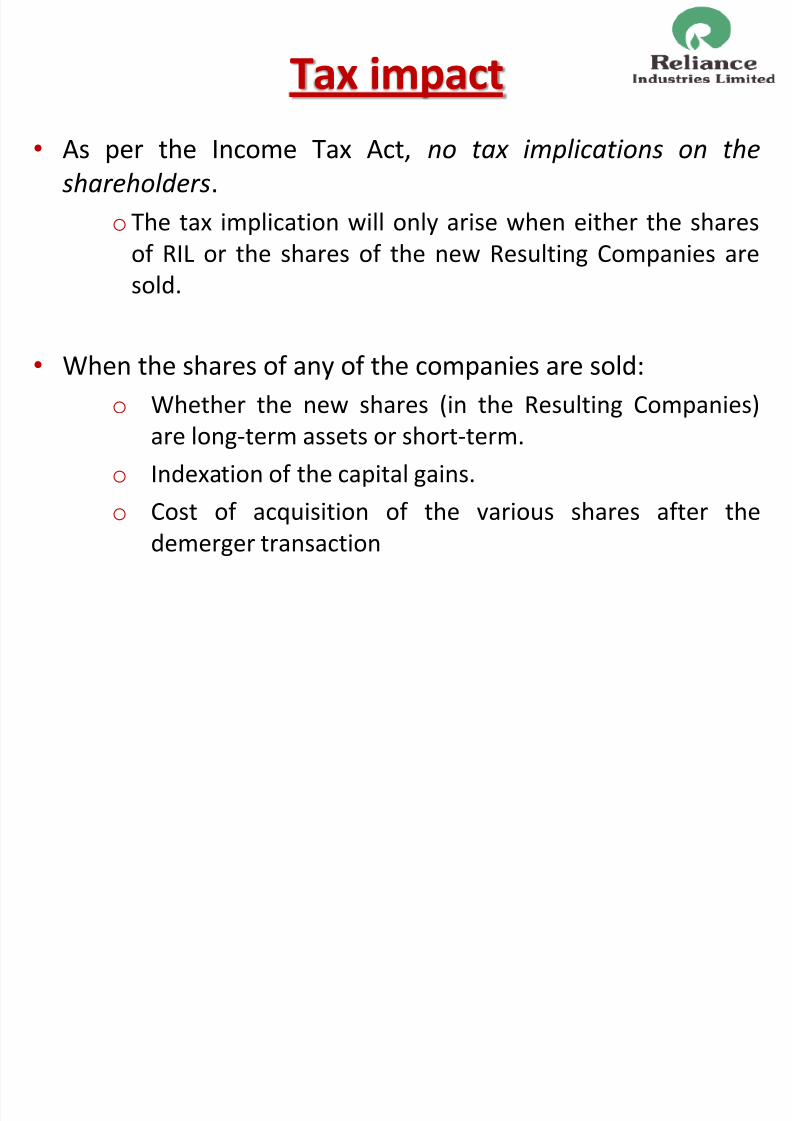

Tax impact

• As per the Income Tax Act, no tax implications on the

shareholders.

oThe tax implication will only arise when either the shares

of RIL or the shares of the new Resulting Companies are

sold.

• When the shares of any of the companies are sold:

o

Whether the new shares (in the Resulting Companies)are long-term assets or short-term.

o Indexation of the capital gains.

o Cost of acquisition of the various shares after the

demerger transaction

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 23/38

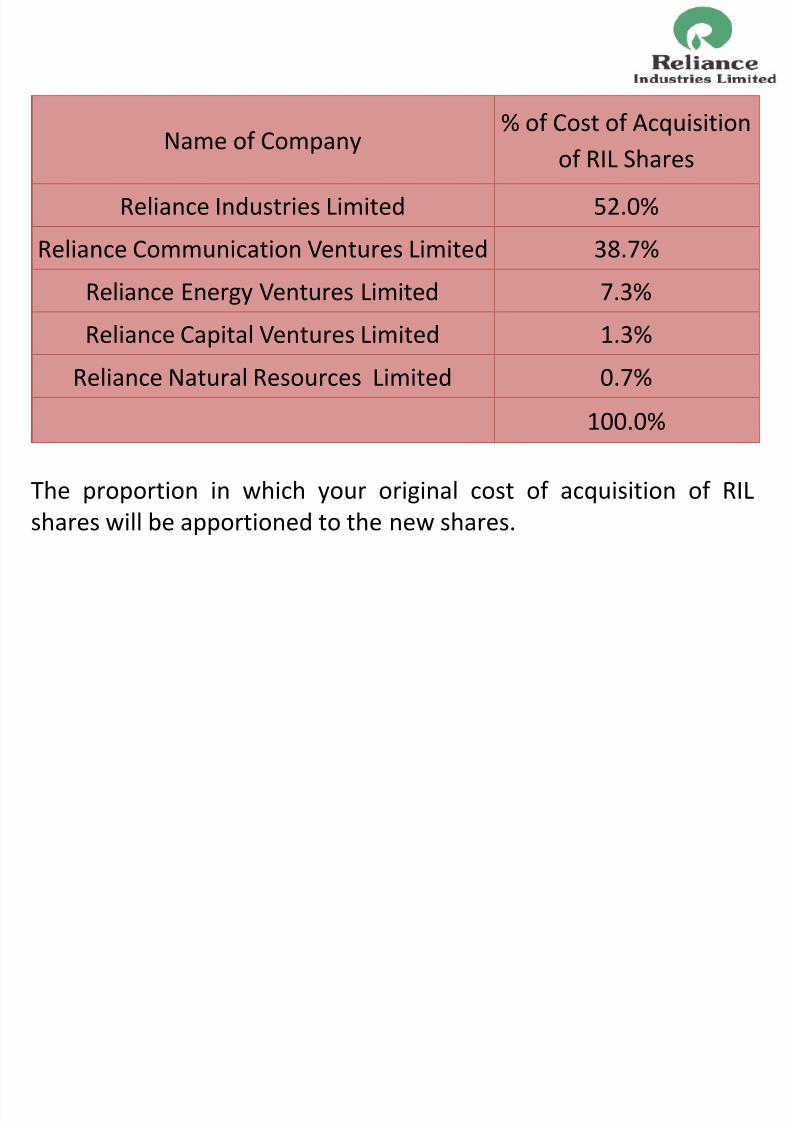

The proportion in which your original cost of acquisition of RIL

shares will be apportioned to the new shares.

Name of Company% of Cost of Acquisition

of RIL Shares

Reliance Industries Limited 52.0%

Reliance Communication Ventures Limited 38.7%

Reliance Energy Ventures Limited 7.3%

Reliance Capital Ventures Limited 1.3%

Reliance Natural Resources Limited 0.7%

100.0%

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 24/38

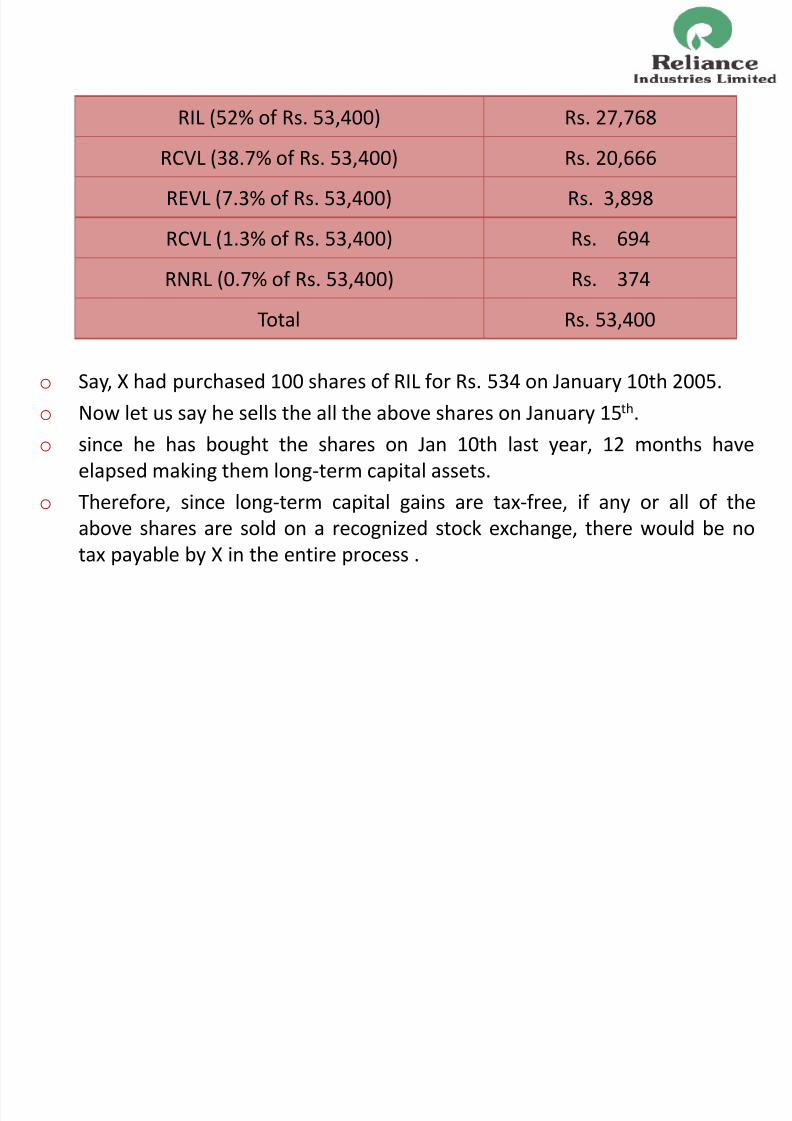

RIL (52% of Rs. 53,400) Rs. 27,768

RCVL (38.7% of Rs. 53,400) Rs. 20,666

REVL (7.3% of Rs. 53,400) Rs. 3,898

RCVL (1.3% of Rs. 53,400) Rs. 694

RNRL (0.7% of Rs. 53,400) Rs. 374

Total Rs. 53,400

o Say, X had purchased 100 shares of RIL for Rs. 534 on January 10th 2005.

o Now let us say he sells the all the above shares on January 15th

.o since he has bought the shares on Jan 10th last year, 12 months have

elapsed making them long-term capital assets.

o Therefore, since long-term capital gains are tax-free, if any or all of the

above shares are sold on a recognized stock exchange, there would be no

tax payable by X in the entire process .

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 25/38

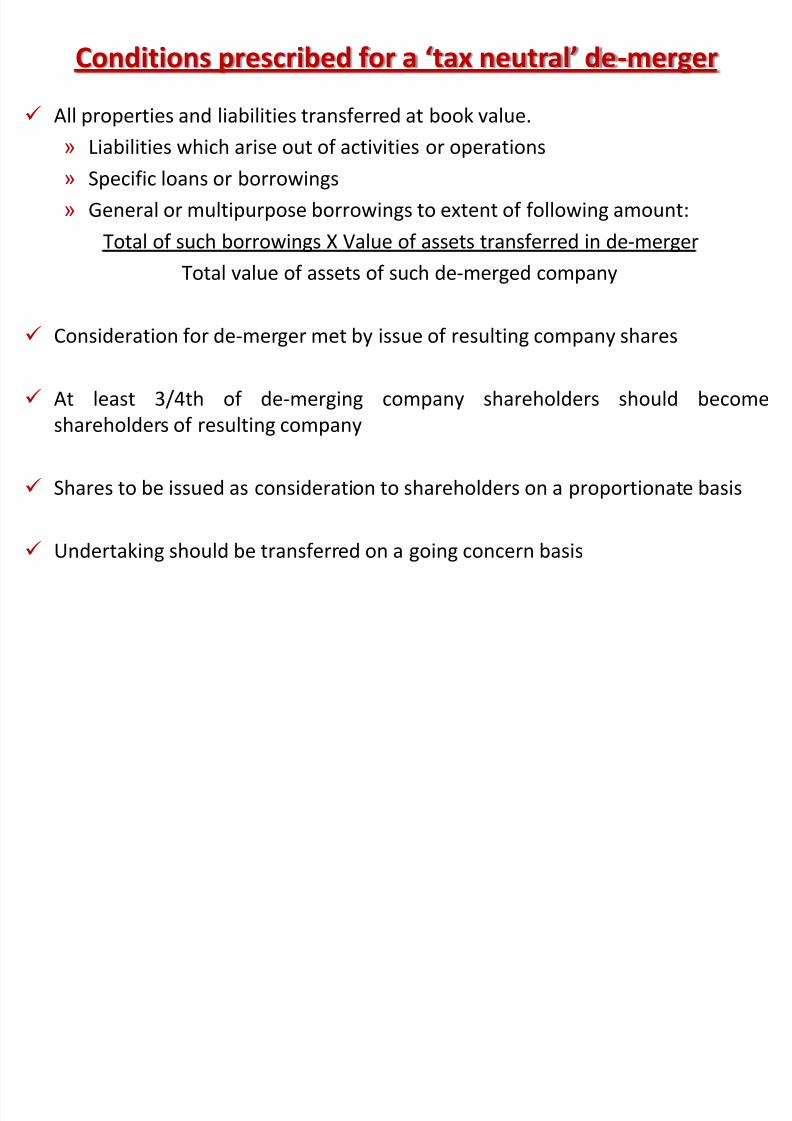

Conditions prescribed for a ‘tax neutral’ de-merger

All properties and liabilities transferred at book value.

» Liabilities which arise out of activities or operations

» Specific loans or borrowings

» General or multipurpose borrowings to extent of following amount:

Total of such borrowings X Value of assets transferred in de-merger

Total value of assets of such de-merged company

Consideration for de-merger met by issue of resulting company shares

At least 3/4th of de-merging company shareholders should become

shareholders of resulting company

Shares to be issued as consideration to shareholders on a proportionate basis

Undertaking should be transferred on a going concern basis

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 26/38

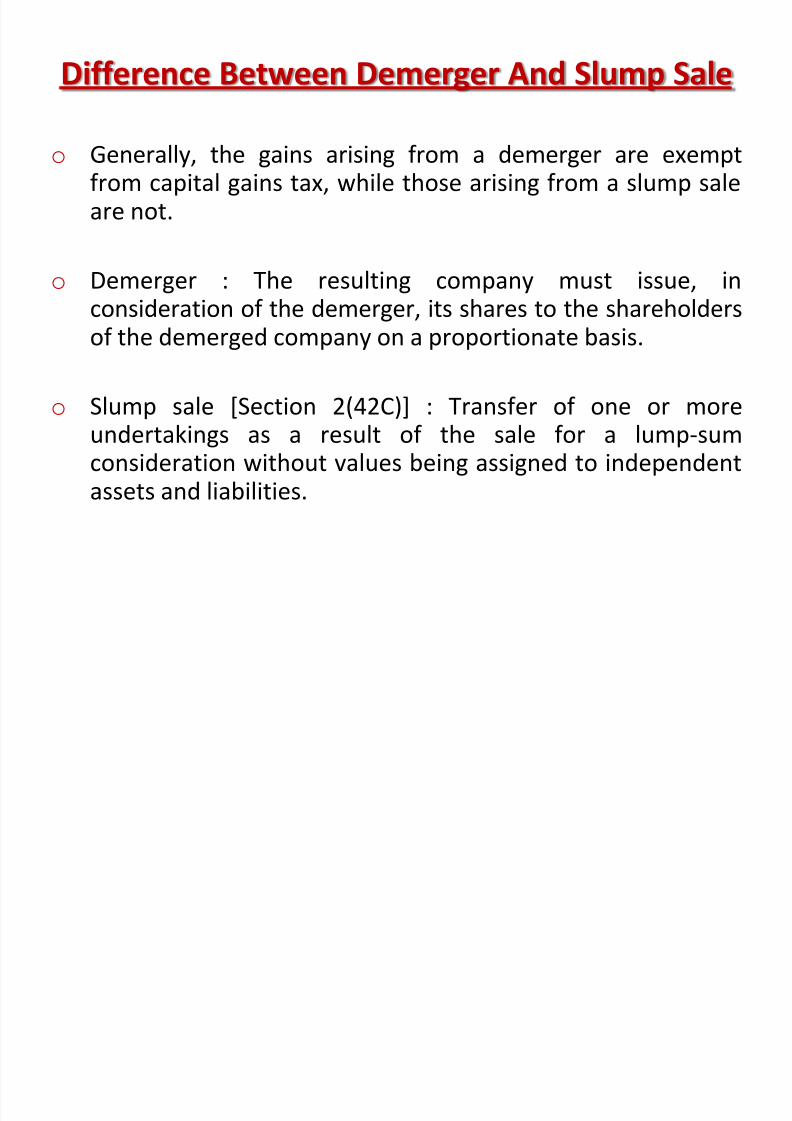

Difference Between Demerger And Slump Sale

o Generally, the gains arising from a demerger are exemptfrom capital gains tax, while those arising from a slump saleare not.

o Demerger : The resulting company must issue, inconsideration of the demerger, its shares to the shareholdersof the demerged company on a proportionate basis.

o

Slump sale [Section 2(42C)] : Transfer of one or moreundertakings as a result of the sale for a lump-sumconsideration without values being assigned to independentassets and liabilities.

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 27/38

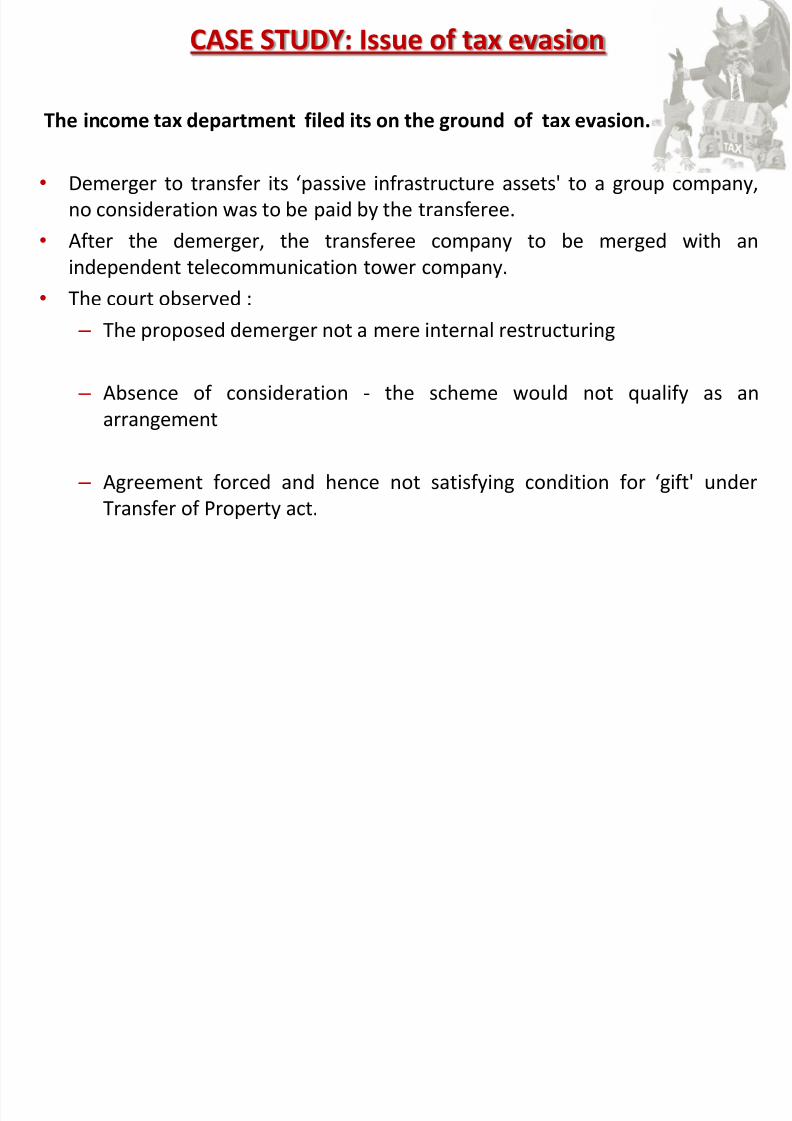

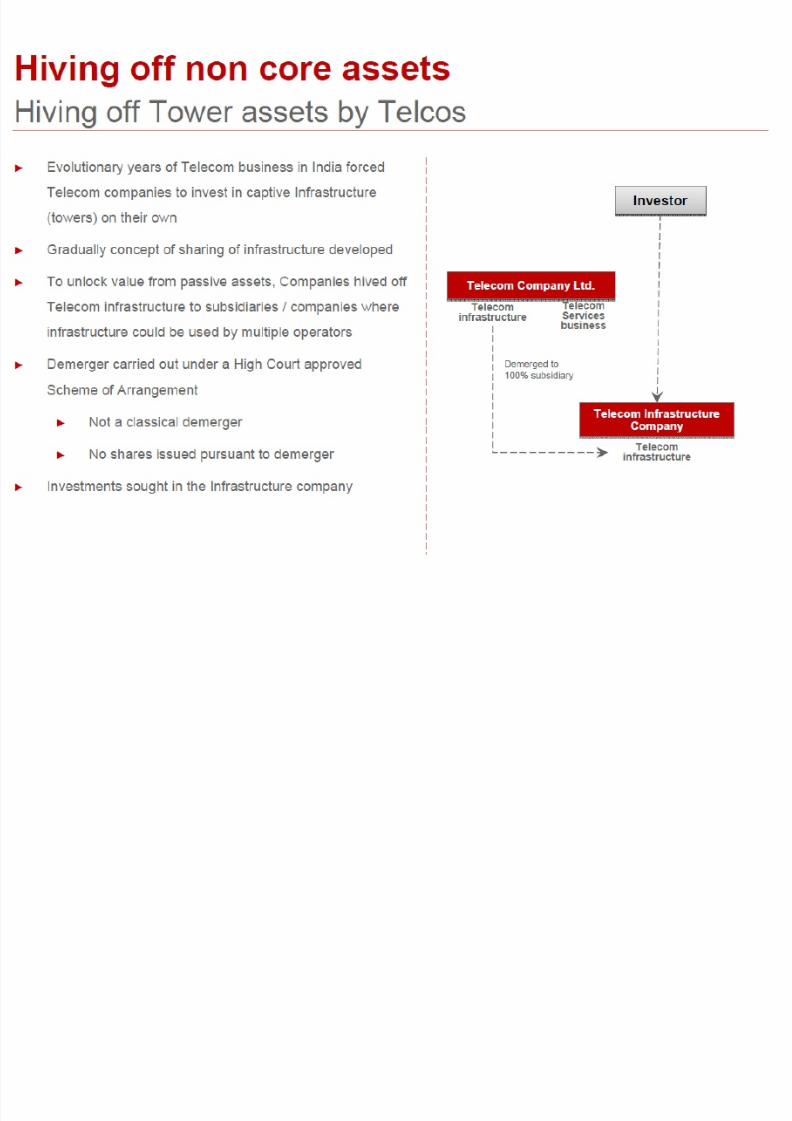

CASE STUDY: Issue of tax evasion

The income tax department filed its on the ground of tax evasion.

• Demerger to transfer its ‘passive infrastructure assets' to a group company,

no consideration was to be paid by the transferee.

• After the demerger, the transferee company to be merged with an

independent telecommunication tower company.

• The court observed :

– The proposed demerger not a mere internal restructuring

– Absence of consideration - the scheme would not qualify as an

arrangement

– Agreement forced and hence not satisfying condition for ‘gift' under

Transfer of Property act.

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 28/38

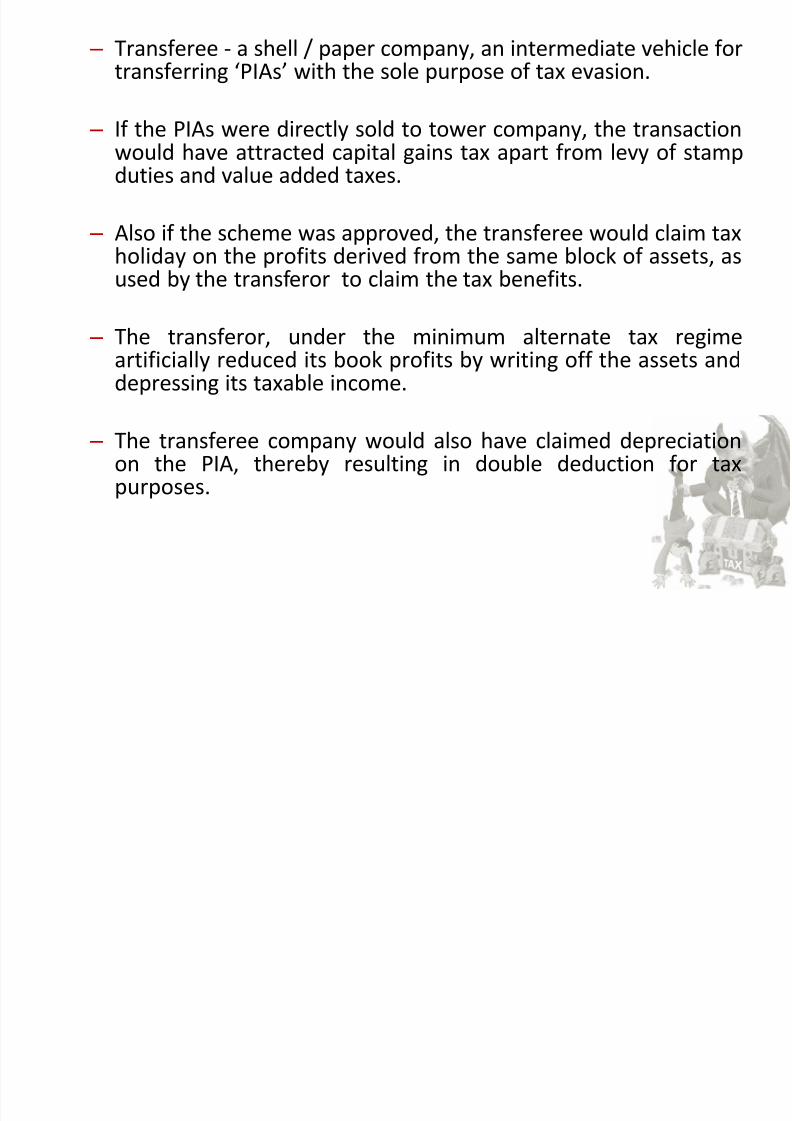

– Transferee - a shell / paper company, an intermediate vehicle fortransferring ‘PIAs’ with the sole purpose of tax evasion.

– If the PIAs were directly sold to tower company, the transactionwould have attracted capital gains tax apart from levy of stampduties and value added taxes.

– Also if the scheme was approved, the transferee would claim taxholiday on the profits derived from the same block of assets, as

used by the transferor to claim the tax benefits.

– The transferor, under the minimum alternate tax regimeartificially reduced its book profits by writing off the assets anddepressing its taxable income.

– The transferee company would also have claimed depreciationon the PIA, thereby resulting in double deduction for taxpurposes.

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 29/38

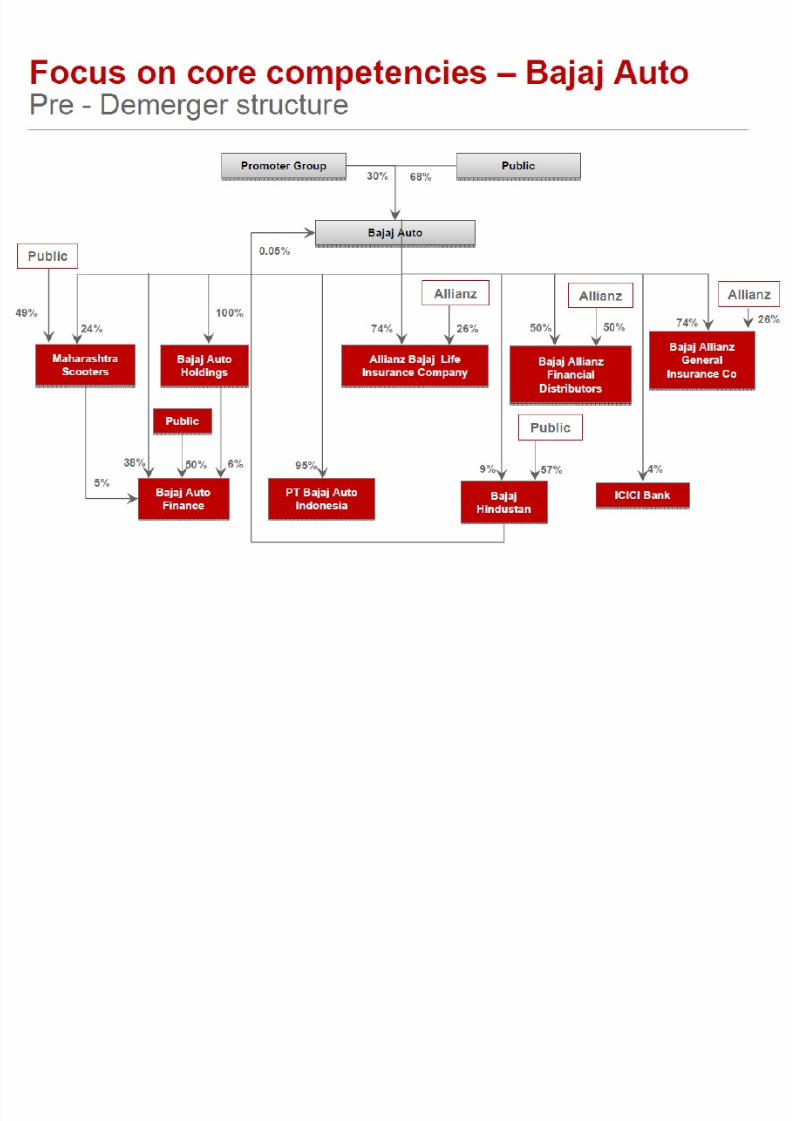

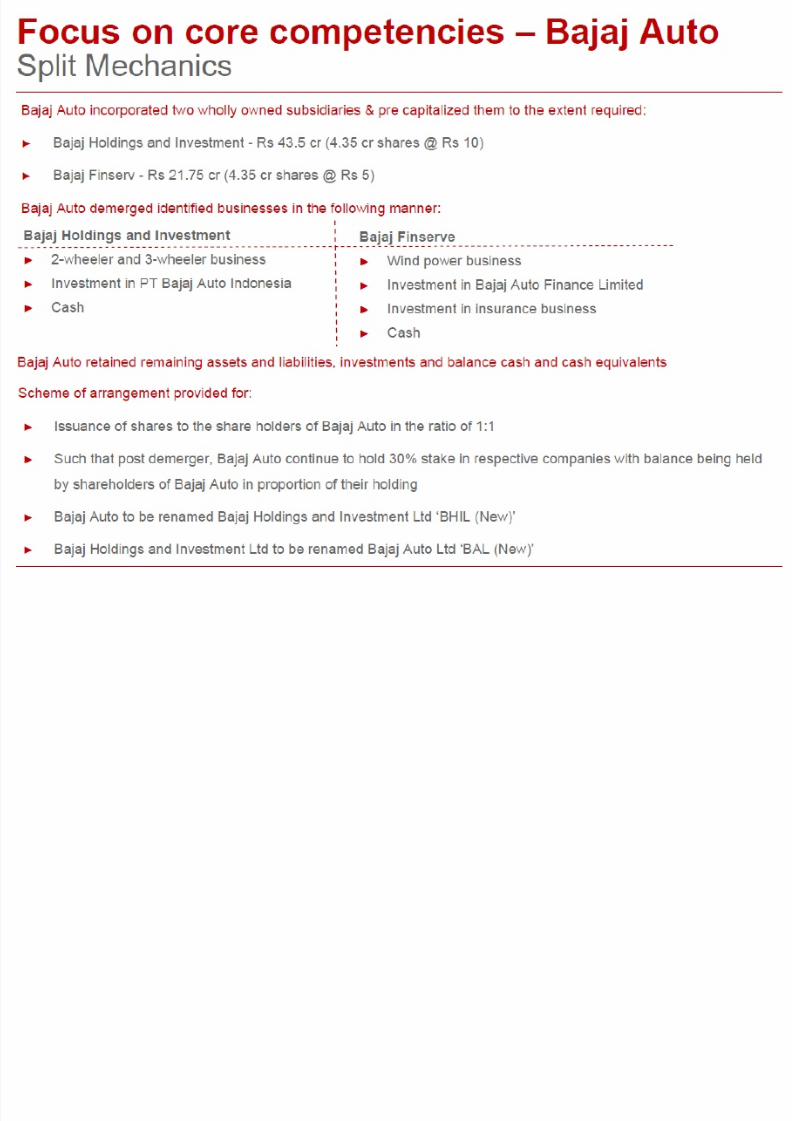

STRATEGIC ISSUES

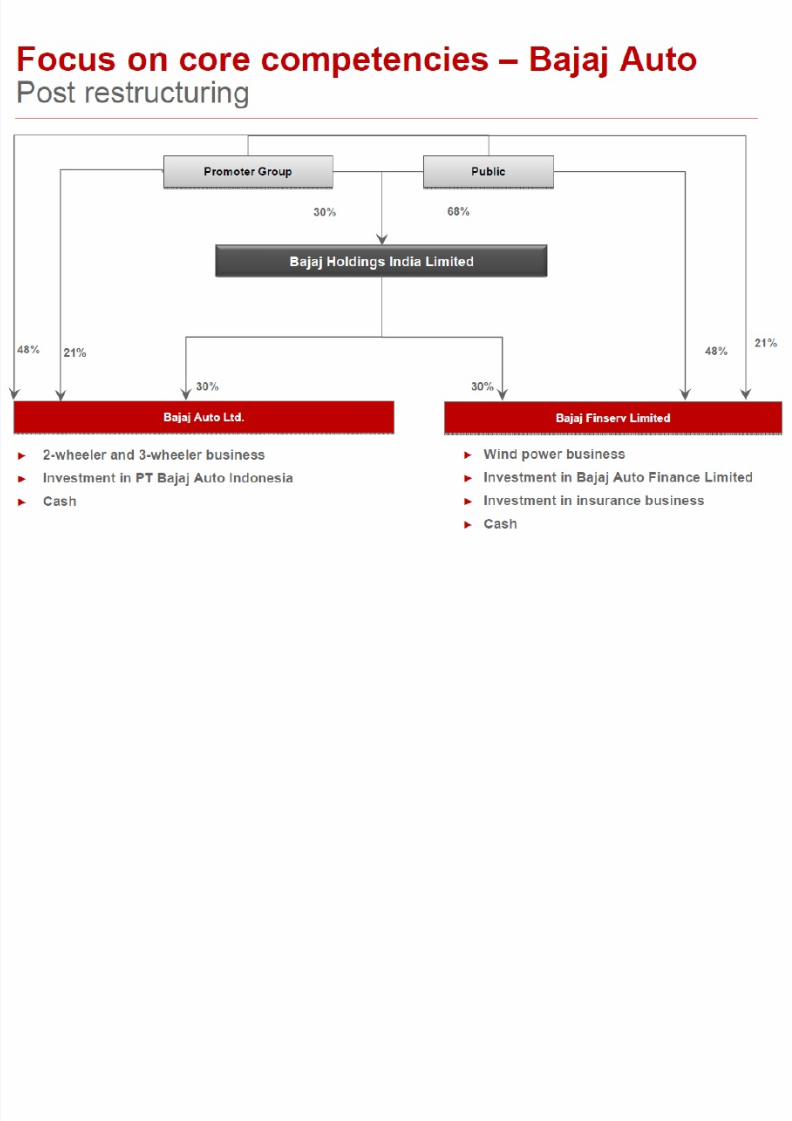

FOCUSSING ON CORE COMPETENCIES/ RECAPITALISATION• Bajaj Auto

UNLOCKING SHAREHOLDER VALUE• The Reliance Demerger

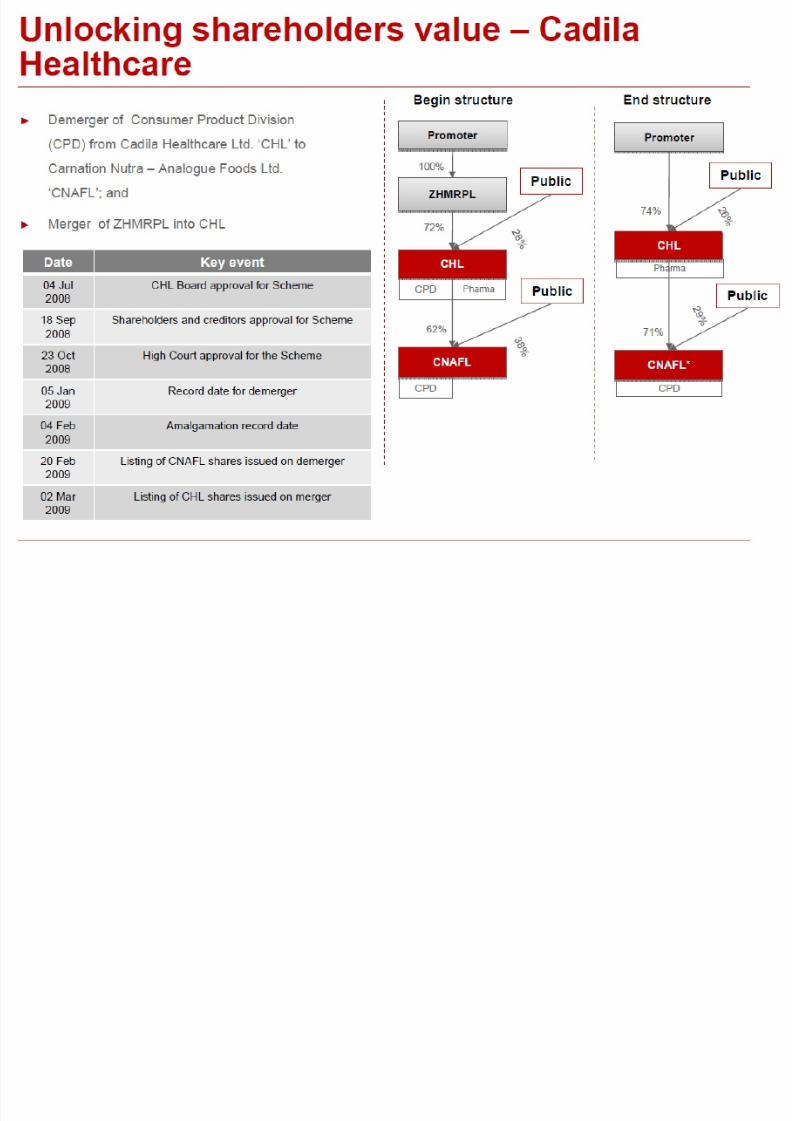

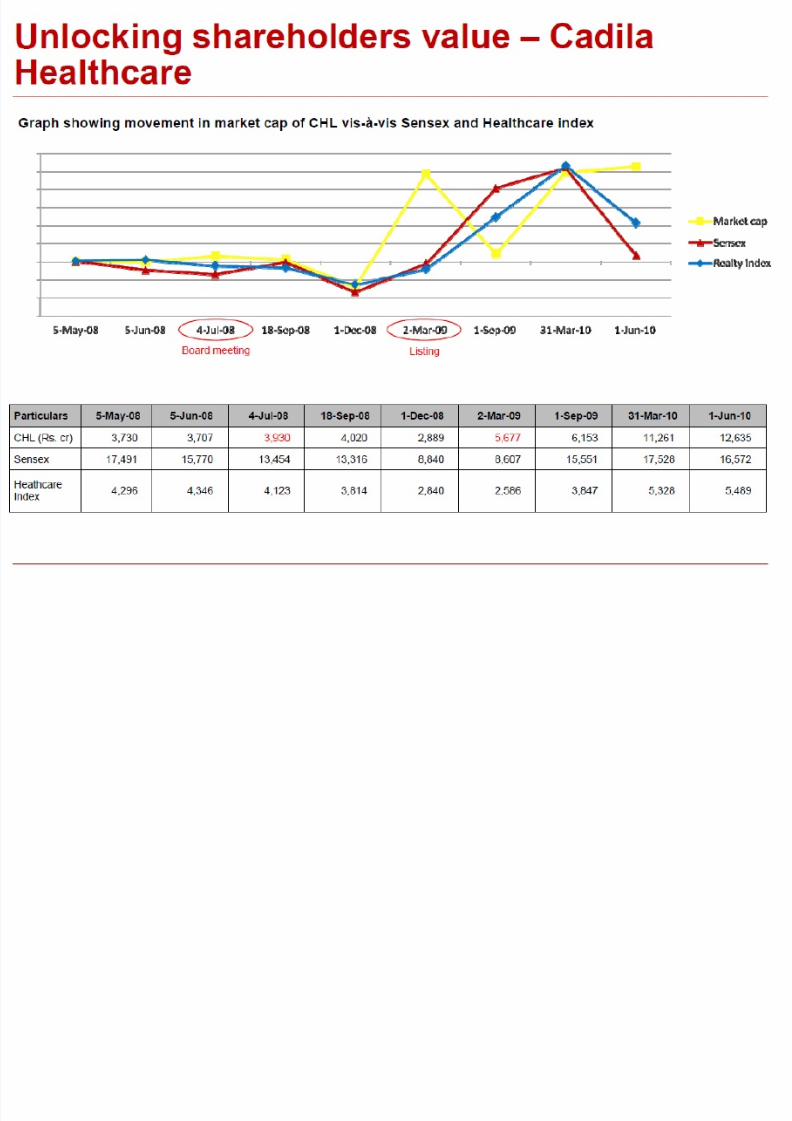

• Cadila Healthcare

• Eveready Industries

• GE Shipping

HIVING OFF NON-CORE ASSETS

• Telecom Companies

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 30/38

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 31/38

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 32/38

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 33/38

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 34/38

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 35/38

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 36/38

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 37/38

8/13/2019 Spinoff Final (1)

http://slidepdf.com/reader/full/spinoff-final-1 38/38