Embed Size (px)

Citation preview

Spill Over Covid-19 and Indices around the Globe

Dwi Pramaya Bhakti and Hidajat Sofyan Widjadja

Both are lecturer of Perbanas ABFI Jakarta

Abstract

The impact of Covid-19 has had implications for all aspects of life, especially in the economic

sector. Measurement of the impact of the pandemic has been carried out by all countries in the

world without exception. The different patterns of the impact of Covid-19 on the economic cycle

in each country are different depending on the initial impact until it reaches its peak. For example,

China has experienced the peak of Covid-19 in early 2020. Italy and several European countries

in April and May 2020. The United States including Indonesia in November and December 2020.

Finally, India has only experienced the peak of Covid-19 in May 2021. This is also what has caused

economic policy makers in various countries to apply different patterns. Indonesia as a country

with a very open economy has implemented major social restrictions in various cities throughout

Indonesia, especially those related to other countries. This research will use a combination of

cross-section and time series data which will then be processed by panel data. The data used is

the number of confirmed Covid-19 countries between March 2020 and May 2021. This timing is

based on the pattern of Covid-19 influence that has spread throughout the world An important

finding from this study is that the covid-19 variable greatly influences the stock price index in the

USA, INDONESIA and KSA during the study period. But for the long term, the variables Gold and

Crude oil will again be the main determinants of the global index.

Keywords: COVID-19, Vector Autoregressive (VAR), Indonesian Stock Market and World

Indices

JEL Classification: C22, G11, G15, C32

Introduction

The impact of Covid-19 has had implications for all aspects of life, especially in the

economic sector. Measurement of the impact of the pandemic has been carried out by all countries

in the world without exception. The impact of COVID-19 on all countries has caused a slowdown

in economic growth in almost all of the world. The different patterns of the pandemic from one

country to another cause the handling to be different. if China has been free from the covid-19

pandemic, it is precisely when almost all countries in the world are struggling to fight the pandemic

in early March 2020. Europe, in this case Italy, followed by France, Germany and the UK, have

fought against the pandemic in April to July of the same year. followed by the United States, which

struggled against the pandemic in November and December 2020. Indonesia was among the worst

hit in mid-March 2020, but the peak of the pandemic was only seen in November and December

in 2020.

Research on the impact of Covid-19 on economic performance is very massive in the

scientific world, both the branch of economics itself and its derivatives as well as a wider

dimension. During 2020 and currently entering the second half of 2021, research on the impact of

covid-19 is still being carried out considering the impact and spectrum of this pandemic is very

broad in the dimensions of human life in the modern era. This pandemic has a greater impact on

the economy and other dimensions than previous pandemics such as the Spanish Flu in the early

20th century and the pandemic in the late 20th and early 21st centuries.

This study will reveal in detail the types and impacts of research from several researchers

which will be explained in the next section, namely the study of literature. Furthermore, the author

will try to do a hypothesis on this research. The next section is a brief discussion of the research

methodology. Next is to discuss the regression results and analyze them. The final part is

conclusion and discussion.

Literature Study

The COVID-19 pandemic proved to be a true black swan (Thaleb, NN, 2007); completely

unexpected, it may be remembered as one of the most significant, widespread events affecting the

global financial markets, economies, and all of humanity. Its rapid spread has also demonstrated

the dark side of globalisation and how intense may be a global spillover effect between

countries.(Zeremba, and all 2020). The outbreak itself, as well as the ensuing spiral of containment

and closure policies, led to an unprecedented economic and financial downturn not witnessed for

decades since the Great Depression, which is believed to be very different from any previous

downswings (Bernanke, 2020; Reinhart, 2020), and far worse than the Global Financial Crisis

(Fund, 2020).

Wang and Enilov (2020) use panel Granger non-causality tests to investigate the impact of

COVID-19 cases on stock market returns in the G7 countries. For Canada, France, Germany, Italy,

and the US, the causality runs from COVID-19 cases to stock market returns, while mixed results

obtain for the UK, and no relationship is documented for Japan.

Nader Alber (2020) attempts to investigate the effects of Coronavirus spread on stock

markets using panel data analysis, on daily basis over the period from March 1, 2020 until

September 30, 2020. Coronavirus spread has been measured by daily cases and daily deaths per

million of population, while stock return is measured by Δ in sectoral indices. This has been

conducted after dividing the research period into 6 months from March to September and has been

applied on 17 sectors in the Egyptian Exchange.

Beirne, Renzhi, Sugandi, and Volz (2020) empirically examines the reaction of global

financial markets across 38 economies to the COVID-19 outbreak, with a special focus on the

dynamics of capital flow across 14 emerging market economies. Using daily data over the period

4 January 2010 to 30 April 2020 and controlling for a host of domestic and global macroeconomic

and financial factors, we use a fixed effects panel approach and a structural VAR framework to

show that emerging markets have been more heavily affected than advanced economies.

What determines a country’s financial immunity to a global pandemic? To answer this

question, Zeremba and All (2020) investigated the behavior of 67 equity markets around the world

during the COVID-19 outbreak in 2020. They consider a multidimensional data set that includes

factors from finance, economic, demographics, technological development, healthcare,

governance, culture and law.

Ramelli and Wagner (2020) discuss the impact of US firms’ trade and financial policies on

US stock prices during the COVID-19 pandemic. They make the point that investors retreated

from the stocks of US firms that were highly exposed to the People’s Republic of China (PRC), in

line with the traditional response of markets to increase in times of uncertainty. As the virus spread

to Europe and the US, investors became more concerned about the financial conditions of firms

located in these areas, particularly those with high debt and/or low liquidity, with negative

repercussion for stock prices/

Baker et al. (2020) find that the impact of COVID-19 on US stock market volatility is much

greater than that of previous pandemics that occurred since the year 1900, in particular due to the

economic ramifications of containment policies.

Maroua & Slim (2020) aim to examine the effect of COVID-19 pandemic on stock market

in KSA applying an Autoregressive Distributed Lag (ARDL) cointegration approach. More

especially, it analyzes the relationship between the natural logarithm of trading volume of Tadawul

All shares index (TASI) and the natural logarithm of daily COVID-19 confirmed cases in both the

short-run and the long-run. The bounds test for cointegration is carried out for daily series over the

period from March 02, 2020 until May 20, 2020.Toda-Yamamoto causality test is implemented

between variables. The results indicate that there is a negative impact of COVID-19 on stock

market only in the long-run. Causality test reveals a unidirectional causality from COVID-19

prevalence’s measure to stock market. Robustness check seems to be conclusive.

Thakur (2020) attempts to investigate the movement of US stock market during the COVID

19 pandemic. The paper has used time series analysis using Vector Autoregression (VAR) model

using data from Jan 23, 2020 to June 19, 2020. The finding suggests that Standard and Poor Index

which has been used as reference for capital market has shown negative causality with increase in

number of new cases at global level.

Alber & Saleh (2020) attempts to investigate the effects of 2020 Covid-19 world-wide

spread on stock markets of GCC countries. Findings show that there are significant differences

among stock market indices during the research period. Besides, stock market returns seem to be

sensitive to Coronavirus new deaths. Moreover, this has been confirmed for March without any

evidence about these effects during April and May 2020. Moreover, Smales (2020) addresses the

investor attention and the response of US Stock sectors to the COVID-19 crisis from Dec., 31,

2019 to May, 31, 2020. This has been conducted using the S&P500 Composite Index and

considering returns on the 11 sectors within the Global Industry Classification Standard (GICS).

Gormsen and Koijen (2020) use data from the aggregate stock market and dividend futures

to quantify how investors’ expectations about economic growth evolve across horizons in response

to the coronavirus outbreak and subsequent policy responses in both US and EU until June 2020.

Dividend futures, which are claims to dividends on the aggregate stock market in a particular year,

can be used to directly compute a lower bound on growth expectations across maturities or to

estimate expected growth using a forecasting model.

Methodology

Methodology of VAR in Matrix

Furthermore, Granger causality test between the variables studied in the vector error

correction framework (VECM). Before carrying out this stage, the stages in the Granger causality

test are to perform a stationary test and co-integration between the observed variables. The ADF

test (The Augmented Dickey-Fuller) has been used to study stationary variables in time-series data

from studies to find the order of integration between variables. The ADF test has been carried out

by estimating the regression as follows. (Bhakti, D.P, 2018)

ΔYt= α0 + α1 Yt-1 + Σ γj ΔYt-j + εt

The ADF test is based on the Zero Hypothesis, where H0: Yt is not 1 (0). If the ASF statistic

is less than the critical value, then the null hypothesis is rejected, otherwise if the ADF value

exceeds the critical value, then H0 is accepted. If the variable to be tested is stationary at that level,

the variable is said to be integrated with zero order. I(0). If the variable is at a non-stationary level,

then an ADF test is performed and a first difference test is performed on the variables used for the

unit root test. The variable is said to be co-integrated in the 1st Order, I (1), that is, if it has a

stationary variable completeness.

The next stage is to test Johansen's co-integration test which has been applied to examine

whether long-term equilibrium occurs between variables. Johansen's approach to the co-

integration test is based on 2 statistical tests. First, looking for statistical tests, second looking for

the maximum Eigen value in statistical tests. The search for statistical tests can be specified as

follows:

τ trace = -T Σ log (1-λi),

Where λ is the largest Eigen value in the matrix Π, and T is the number of observations.

In the search test, Hypothesis Zero is the number of different co-integrating vectors (s) less than

or equal to the number of co-integrating relationships (r). The maximum Eigen value test studies

the null hypothesis whose value is equal to r or the integration relationship to the alternative

relationship r+1 with statistical tests.

λ max = -T log (1- λ r+1 ). Where λ r+1 is (r+1) of the largest root Eigen value. In the

search test, the null hypothesis, r = 0 is tested against the alternative r+1 of the co-integrating

vector. At the end, Granger Causality Test has been used to determine whether a time series is

useful in predicting other variables, so as to find directions and relationships between variables in

the study. Co-integration between two stationary variables has been tested by Johansen Trace and

maximum Eigen value test.

In the Granger causality test, the vector in the endogenous variable is divided into 2 sub-

vectors, Y1t and Y2t with dimensions K1 and K2 separately, so, K = K1 + K2. The sub vector Y1t

is said to be Granger-causal to Y2t if it contains important information to predict the next set of

variables. To test this property, the VAR ratings that follow the no-exogenous variable form of the

model can be considered.

A0Yt = At Yt-1 + ……+Ap+1 Y t-p-1 + B0Xt+……. +BqXt-q+ C* D*t + ut

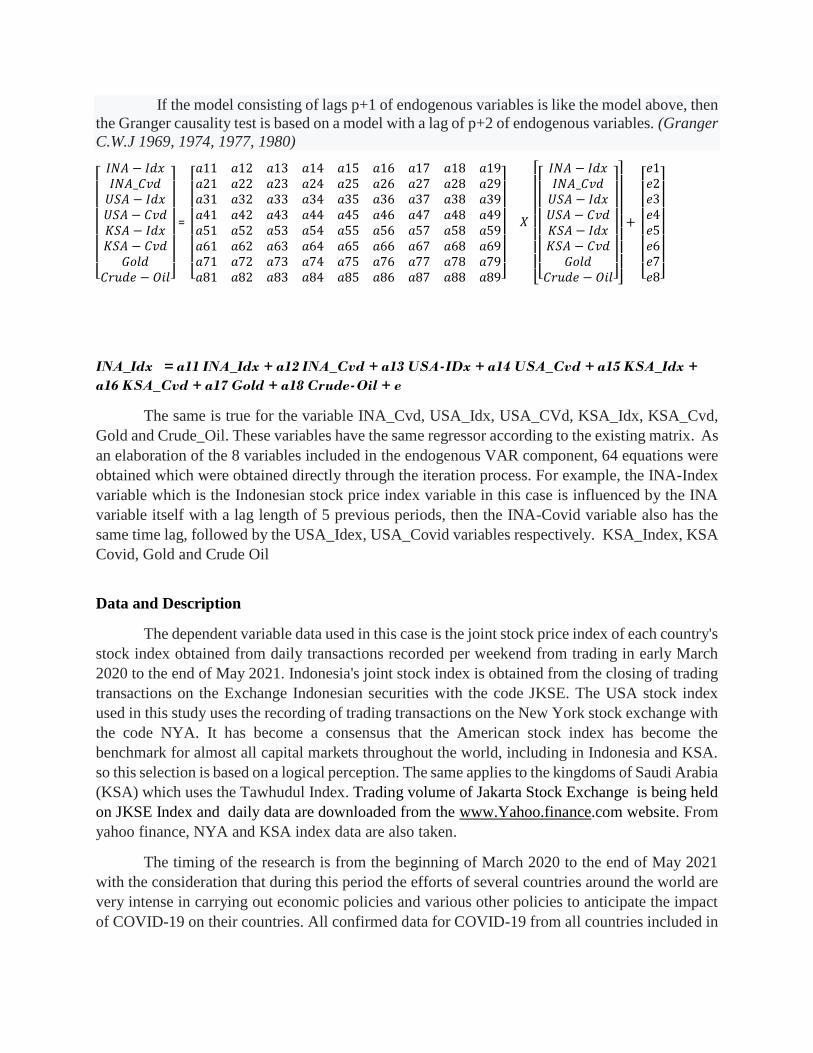

If the model consisting of lags p+1 of endogenous variables is like the model above, then

the Granger causality test is based on a model with a lag of p+2 of endogenous variables. (Granger

C.W.J 1969, 1974, 1977, 1980)

[

𝐼𝑁𝐴 − 𝐼𝑑𝑥𝐼𝑁𝐴_𝐶𝑣𝑑𝑈𝑆𝐴 − 𝐼𝑑𝑥𝑈𝑆𝐴 − 𝐶𝑣𝑑𝐾𝑆𝐴 − 𝐼𝑑𝑥𝐾𝑆𝐴 − 𝐶𝑣𝑑

𝐺𝑜𝑙𝑑𝐶𝑟𝑢𝑑𝑒 − 𝑂𝑖𝑙]

=

[ 𝑎11 𝑎12 𝑎13 𝑎14 𝑎15 𝑎16 𝑎17 𝑎18 𝑎19𝑎21 𝑎22 𝑎23 𝑎24 𝑎25 𝑎26 𝑎27 𝑎28 𝑎29𝑎31 𝑎32 𝑎33 𝑎34 𝑎35 𝑎36 𝑎37 𝑎38 𝑎39𝑎41 𝑎42 𝑎43 𝑎44 𝑎45 𝑎46 𝑎47 𝑎48 𝑎49𝑎51 𝑎52 𝑎53 𝑎54 𝑎55 𝑎56 𝑎57 𝑎58 𝑎59𝑎61 𝑎62 𝑎63 𝑎64 𝑎65 𝑎66 𝑎67 𝑎68 𝑎69𝑎71 𝑎72 𝑎73 𝑎74 𝑎75 𝑎76 𝑎77 𝑎78 𝑎79𝑎81 𝑎82 𝑎83 𝑎84 𝑎85 𝑎86 𝑎87 𝑎88 𝑎89]

𝑋

[

[

𝐼𝑁𝐴 − 𝐼𝑑𝑥𝐼𝑁𝐴_𝐶𝑣𝑑𝑈𝑆𝐴 − 𝐼𝑑𝑥𝑈𝑆𝐴 − 𝐶𝑣𝑑𝐾𝑆𝐴 − 𝐼𝑑𝑥𝐾𝑆𝐴 − 𝐶𝑣𝑑

𝐺𝑜𝑙𝑑𝐶𝑟𝑢𝑑𝑒 − 𝑂𝑖𝑙]

]

+

[ 𝑒1𝑒2𝑒3𝑒4𝑒5𝑒6𝑒7𝑒8]

INA_Idx = a11 INA_Idx + a12 INA_Cvd + a13 USA-IDx + a14 USA_Cvd + a15 KSA_Idx +

a16 KSA_Cvd + a17 Gold + a18 Crude-Oil + e

The same is true for the variable INA_Cvd, USA_Idx, USA_CVd, KSA_Idx, KSA_Cvd,

Gold and Crude_Oil. These variables have the same regressor according to the existing matrix. As

an elaboration of the 8 variables included in the endogenous VAR component, 64 equations were

obtained which were obtained directly through the iteration process. For example, the INA-Index

variable which is the Indonesian stock price index variable in this case is influenced by the INA

variable itself with a lag length of 5 previous periods, then the INA-Covid variable also has the

same time lag, followed by the USA_Idex, USA_Covid variables respectively. KSA_Index, KSA

Covid, Gold and Crude Oil

Data and Description

The dependent variable data used in this case is the joint stock price index of each country's

stock index obtained from daily transactions recorded per weekend from trading in early March

2020 to the end of May 2021. Indonesia's joint stock index is obtained from the closing of trading

transactions on the Exchange Indonesian securities with the code JKSE. The USA stock index

used in this study uses the recording of trading transactions on the New York stock exchange with

the code NYA. It has become a consensus that the American stock index has become the

benchmark for almost all capital markets throughout the world, including in Indonesia and KSA.

so this selection is based on a logical perception. The same applies to the kingdoms of Saudi Arabia

(KSA) which uses the Tawhudul Index. Trading volume of Jakarta Stock Exchange is being held

on JKSE Index and daily data are downloaded from the www.Yahoo.finance.com website. From

yahoo finance, NYA and KSA index data are also taken.

The timing of the research is from the beginning of March 2020 to the end of May 2021

with the consideration that during this period the efforts of several countries around the world are

very intense in carrying out economic policies and various other policies to anticipate the impact

of COVID-19 on their countries. All confirmed data for COVID-19 from all countries included in

this study were obtained from the Johns Hopkins University Covid-19 center which is also

affiliated with data at the World Health Organization (WHO).

EMPIRICAL RESULTS

Statistic descriptive

INA_INDEX USA_INDEX KSA_INDEX GOLD

Mean 5436.439 13509.29 29.89918 1806.864

Median 5304.500 13185.50 29.95451 1816.500

Maximum 6373.000 16708.00 39.24000 2010.000

Minimum 4195.000 9133.000 21.44511 1484.000

Std. Dev. 613.4961 1903.841 4.420635 105.3921

Skewness -0.016308 -0.056555 0.268885 -0.595139

Kurtosis 1.664482 2.082330 2.373219 3.458156

Jarque-Bera 4.907847 2.351007 1.875641 4.473335

Probability 0.085956 0.308664 0.391480 0.106814

Sum 358805.0 891613.0 1973.346 119253.0

Sum Sq. Dev. 24464538 2.36E+08 1270.231 721987.8

Observations 66 66 66 66

INA_COVID USA_COVID KSA_COVID CRUDE_OIL

Mean 27518.41 499232.8 6824.788 44.96045

Median 27069.50 367336.5 3422.000 41.28500

Maximum 90052.00 1753319. 28957.00 69.23000

Minimum 2.000000 20.00000 1.000000 16.94000

Std. Dev. 22450.18 435877.2 7242.887 13.52552

Skewness 0.789016 1.360235 1.565598 -0.035969

Kurtosis 3.161975 3.748660 4.690845 2.274784

Jarque-Bera 6.920155 21.89399 34.82420 1.460561

Probability 0.031427 0.000018 0.000000 0.481774

Sum 1816215. 32949366 450436.0 2967.390

Sum Sq. Dev. 3.28E+10 1.23E+13 3.41E+09 11891.08

Observations 66 66 66 66

Prior to examining the results from panel structural VAR, it is useful to consider the

trajectory of global financial markets and capital flows in the aftermath of the COVID-19 outbreak

It can be seen that government bond yields initially declined globally given rising uncertainty

amidst a bleak economic outlook, suggesting that investors considered sovereign bonds as safe

haven assets at the time. On Black Monday (9 March 2020), financial markets panicked over the

worsening of the COVID-19 pandemic and the concomitant oil price war between Saudi Arabia

and the Russian Federation. Stock markets tanked, while bond yields spiked. In compiling the

VAR structure, steps were made by Christopher Sim and Granger, who were pioneers in compiling

VAR in the mid-1980s. The consistency of these two economists in economics and the

methodology they work with, has led them both to get the prestigious Nobel Prize. The stages of

VAR can be seen in Appendixes 1 to 4.

Vector Autoregression Estimates

Date: 06/10/21 Time: 22:39

Sample (adjusted): 3/16/2020 5/31/2021

Included observations: 64 after adjustments

Standard errors in ( ) & t-statistics in [ ] INA_INDEX USA_INDEX KSA_INDEX GOLD INA_INDEX(-1) 0.499199 0.104049 -0.001156 0.043568

(0.21437) (0.60231) (0.00107) (0.06065)

[ 2.32863] [ 0.17275] [-1.07646] [ 0.71832]

INA_INDEX(-2) -0.234701 -0.274442 -0.000527 -0.071435

(0.20826) (0.58513) (0.00104) (0.05892)

[-1.12696] [-0.46903] [-0.50492] [-1.21237]

INA_COVID(-1) -0.003486 -0.000386 3.26E-05 7.71E-05

(0.00428) (0.01204) (2.1E-05) (0.00121)

[-0.81357] [-0.03208] [ 1.51825] [ 0.06361]

INA_COVID(-2) 0.007967 0.011293 -2.38E-05 -0.000114

(0.00386) (0.01083) (1.9E-05) (0.00109)

[ 2.06624] [ 1.04239] [-1.23209] [-0.10480]

USA_INDEX(-1) 0.003634 0.222617 0.000655 -0.063778

(0.08401) (0.23604) (0.00042) (0.02377)

[ 0.04325] [ 0.94311] [ 1.55770] [-2.68319]

USA_INDEX(-2) 0.106049 0.271562 0.000470 0.027997

(0.08472) (0.23802) (0.00042) (0.02397)

[ 1.25182] [ 1.14092] [ 1.10756] [ 1.16810]

USA_COVID(-1) 0.000559 0.000536 1.33E-06 2.56E-05

(0.00022) (0.00061) (1.1E-06) (6.1E-05)

[ 2.58084] [ 0.87980] [ 1.22527] [ 0.41719]

USA_COVID(-2) -0.000248 -0.000238 -1.79E-06 1.65E-05

(0.00024) (0.00069) (1.2E-06) (6.9E-05)

[-1.01395] [-0.34630] [-1.46277] [ 0.23832]

KSA_INDEX(-1) 70.75988 357.9212 0.893512 13.07208

(35.7918) (100.562) (0.17923) (10.1264)

[ 1.97698] [ 3.55922] [ 4.98538] [ 1.29089]

KSA_INDEX(-2) -92.46659 -178.1962 -0.363054 4.435994

(39.0206) (109.634) (0.19539) (11.0399)

[-2.36968] [-1.62538] [-1.85805] [ 0.40181]

KSA_COVID(-1) 0.004216 0.003958 1.22E-05 -0.005911

(0.00982) (0.02758) (4.9E-05) (0.00278)

[ 0.42947] [ 0.14351] [ 0.24866] [-2.12829]

KSA_COVID(-2) -0.005008 0.004896 -4.61E-05 0.007304

(0.01041) (0.02925) (5.2E-05) (0.00295)

[-0.48105] [ 0.16738] [-0.88483] [ 2.47958]

GOLD(-1) 0.692224 1.628000 0.004816 0.775988

(0.47027) (1.32130) (0.00235) (0.13305)

[ 1.47196] [ 1.23212] [ 2.04518] [ 5.83218]

GOLD(-2) -0.841024 -1.879444 -0.004773 -0.025049

(0.45646) (1.28247) (0.00229) (0.12914)

[-1.84251] [-1.46549] [-2.08812] [-0.19396]

CRUDE_OIL(-1) 0.485628 -3.758131 0.021290 -0.393287

(10.5720) (29.7035) (0.05294) (2.99110)

[ 0.04594] [-0.12652] [ 0.40216] [-0.13149]

CRUDE_OIL(-2) 12.53310 7.881672 0.036947 0.918412

(9.56798) (26.8825) (0.04791) (2.70703)

[ 1.30990] [ 0.29319] [ 0.77116] [ 0.33927]

C 2578.881 2209.152 5.705730 517.2791

(865.151) (2430.76) (4.33222) (244.773)

[ 2.98084] [ 0.90883] [ 1.31705] [ 2.11330] R-squared 0.962769 0.968692 0.980995 0.883041

Adj. R-squared 0.950094 0.958034 0.974525 0.843225

Sum sq. resids 900179.9 7106046. 22.57182 72056.49

S.E. equation 138.3935 388.8348 0.693002 39.15504

F-statistic 75.96099 90.88821 151.6240 22.17808

Log likelihood -396.4590 -462.5744 -57.46228 -315.6544

Akaike AIC 12.92059 14.98670 2.326946 10.39545

Schwarz SC 13.49405 15.56015 2.900400 10.96890

Mean dependent 5443.719 13568.89 30.09108 1813.531

S.D. dependent 619.4978 1898.085 4.341850 98.88922 Determinant resid covariance (dof adj.)

Determinant resid covariance

Log likelihood

-3299.192

Akaike information criterion 107.3

497

Schwarz criterion 111.9

374

Number of coefficients 136

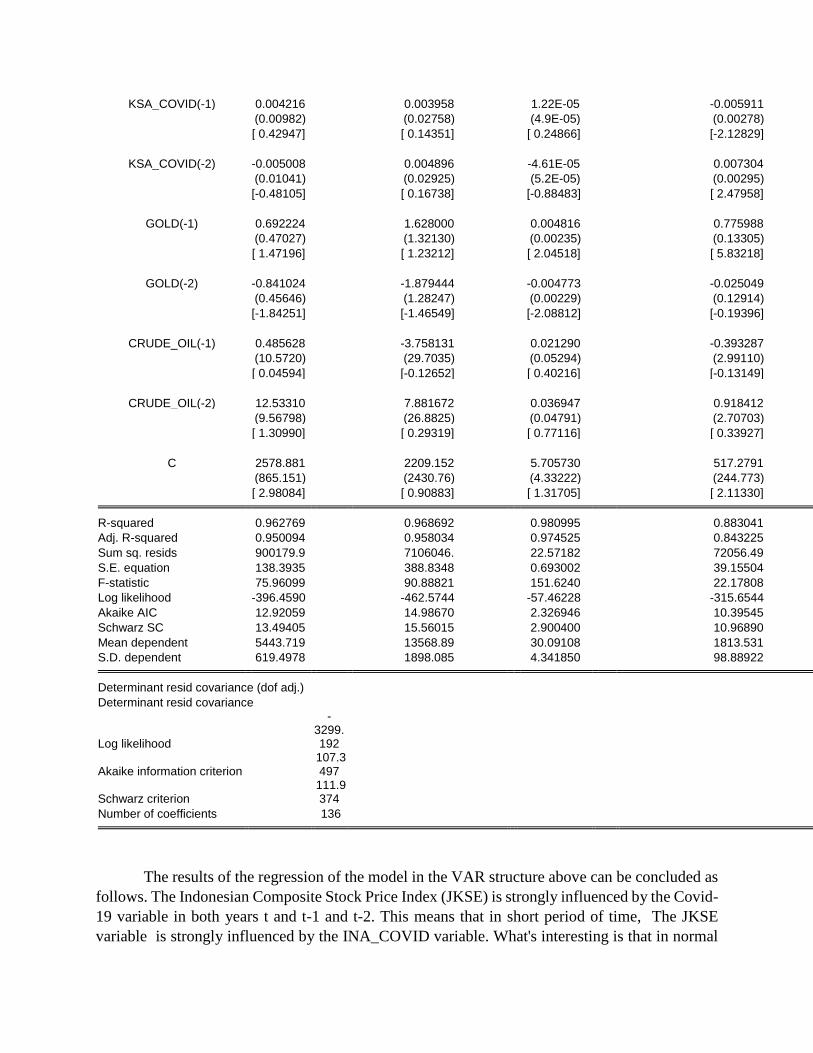

The results of the regression of the model in the VAR structure above can be concluded as

follows. The Indonesian Composite Stock Price Index (JKSE) is strongly influenced by the Covid-

19 variable in both years t and t-1 and t-2. This means that in short period of time, The JKSE

variable is strongly influenced by the INA_COVID variable. What's interesting is that in normal

situations, usually JKSE or INA_INDEX is strongly influenced by the performance of the New

York Stock Exchange, which in this case is a pooling of top US companies that are members of

the Fortune 500. In the period of this study the USA_INDEX variable can be said to be significant

if the t test enlarged to 10%. This means that the NYSE does not have a strong influence on the

JKSE with a 5% probability test. The same thing also happened to the variable Gold and Crude

Oil. Both did not significantly affect the JKSE and NYSE indexes. In normal situations, Gold and

Crude Oil indicators are usually very significant in influencing both the INA_Index and

USA_Index variables. For the KSA index, the results of the regression in the VAR structure are

still strongly influenced by the USA index more than other variables. This is understandable

considering the strong inter-relationship between US and KSA interests in terms of investment and

other matters.

4,400

4,800

5,200

5,600

6,000

6,400

I II III IV I II

2020 2021

INA_INDEX_F

20

24

28

32

36

40

I II III IV I II

2020 2021

KSA_INDEX_F

9,000

10,000

11,000

12,000

13,000

14,000

15,000

16,000

17,000

I II III IV I II

2020 2021

USA_INDEX_F

Forecast Evaluation

Date: 06/10/21 Time: 22:44

Sample: 3/02/2020 5/31/2021

Included observations: 66

Variable Inc. obs. RMSE MAE MAPE Theil CRUDE_OIL 66 4.405371 3.374577 8.014188 0.046013

GOLD 66 84.76001 70.61182 3.829458 0.023231

INA_COVID 66 14754.25 10447.45 53.14936 0.217533

INA_INDEX 66 274.1048 224.0758 4.044083 0.024977

KSA_COVID 66 5043.723 3930.315 58.68300 0.283428

KSA_INDEX 66 1.344173 1.004067 3.159258 0.021795

USA_COVID 66 405750.4 299846.3 88.54880 0.343269

USA_INDEX 66 451.0506 336.0296 2.522196 0.016297 RMSE: Root Mean Square Error

MAE: Mean Absolute Error

MAPE: Mean Absolute Percentage Error

Theil: Theil inequality coefficient

Figure 1 shows the dynamics of expected Index growth expectations in the Indonesia, US

and KSA respectively. Growth expectations did not respond much to Country lockdown such in

Italy, Germany, UK and France. For Example, the lockdown in Italy, is followed by growth

expectations start to deteriorate). The travel restrictions on visitors to the US from the EU leads to

a sharp deterioration of growth expectations. This is occurs once again following the declaration

of the national emergency and the subsequent actions by the Federal Reserve on March 15.

Following the US fiscal stimulus program, GDP growth has stabilized somewhat in the US but

continued to deteriorate in the EU. By June 8, expected dividend growth over the next year is down

by 9% for the S&P 500 index and 14% for the Euro Stoxx 50 index. The estimate of GDP growth

over the next year is down by 2.0% in the US and 3.1% in the EU. As a word of caution, we

emphasize that these estimates are based on a forecasting model estimated using historical data. In

these unprecedented times, there is a risk that the historical relation between growth and asset

prices changes, meaning these estimates come with uncertainty. Nevertheless, in discussing what

asset markets may tell about investors’ growth expectations, we argue that dividend futures should

play a central role. (Gormsen and Koijen, 2020)

The policies carried out by Indonesia in the midst of the COVID-19 pandemic were met

with pros and cons, considering that the sectors affected by the pandemic actually rose on autopilot.

The government's policies that are felt to be directly related to the lower class are not clearly

visible. Once again, Indonesia has a unique social character and can be a role model for the world.

The nature of the community that works together is the mainstay of the community to get out of

the crisis turmoil due to the pandemic. We can see that during the pandemic, people provide food

assistance to low-income people, such as online motorcycle taxis, scavengers and other poor

people. This is what makes Indonesia resistant to the COVID-19 pandemic whose impact is very

massive and is felt by almost all elements of society.

Conclusion and Discussion

Looking at the structure of the equations compiled in the VAR model, it can be concluded

that both the Indonesia Composite Stock Index (JKSE) and the NYSE are strongly influenced by

Covid-19 data, in the form of confirmed COVID-19 patients. Surprisingly, the indicators of world

oil and world gold prices which have so far greatly influenced both the NYSE and JKSE, in the

period of this research, from March 1, 2020 to May 31, 2021, do not have a significant influence

on the two indices above.

The theoretical implication that can be drawn from the regression results above is that it

is true that Covid-19 is the main determining indicator in the pandemic era, especially in the

research period (March 2020 to May 2021). Once again, the opinion of many economists who call

Covid-19 a black swan phenomenon is understandable, considering that no one can predict when

it will occur and how long it will last. But one thing that can be learned is that, when the worst

condition occurs, the prediction of the long run will get better. This is what is happening at this

time, where conditions that were not previously thought have occurred, other things that are

remarkable or beyond human reasoning can happen.

.

The managerial implication of this research is very important for monetary and financial

policy makers both in the US and Indonesia, namely the momentum of providing fiscal stimulus

to the poor. cash transfer is the best way to deal with the pandemic that affects the middle to lower

economy. on the other hand, the covid-19 pandemic for financial investors, especially the capital

market, can be used as a honeymoon event in stock trading. how not, the very deep fall of stock

exchange trading is always followed by a rebound in either the short or medium term. In the midst

of the Covid-19 pandemic, many investors actually gained very large gains when collecting stocks

that fell at the beginning of the pandemic.

Referrences

Alber, N. (2020 ). “The Effect of Coronavirus Spread on Stock Markets: The Case of the Worst 6

Countries,” Available at: http://ssrn.com/abstract=3578080

Alber, N. & Saleh, A. (2020). “The Impact of Covid-19 Spread on Stock Markets: The Case of the

GCC Countries," International Business Research 13 (11)

Beirne, J, Renzhi N, Sugandi E, and Volz Ulrich, “Financial Market and Capital Flow Dynamics

During The Covid-19 Pandemic“ ADBI Working Paper Series

Eom, T.H. and Rubenstein, R. 2006. Do state-funded property tax exemptions increase local

government inefficiency? An analysis of New York State’s STAR Program, Public Budgeting &

Finance, 26(1): 66–87

Eom, T.H , Lee S.H , and Hua Xu , “Introduction to Panel Data Analysis: Concepts and Practices”

, Hanyang University of China

Gujarati, D.N. 2003. Basic Econometrics, 4th ed., New York: McGraw Hill.

Wooldridge, J.M. 2006. Introductory Econometrics: A Modern Approach, 3rd ed., Mason, Ohio:

Thomson South-Wester

Granger, C. W. J. (1969). Investigating Causal Relations by Econometric Models and Cross-

Spectral Methods. Econometrica, 37, 424-38.

Granger, C. W. J. and Newbold, P. (1974). "Spurious regressions in econometrics". Journal of

Econometrics 2 (2): 111–120

Granger, C. W. J. and Newbold, P. (1977). Forecasting Economic Time Series. Academic Press

Granger C.W.J. (1980) “Testing for Causality - A Personal Viewpoint”, Journal of Economic

Dynamics and Control, 2, 329-52

Heckman, J.J. 2000. Casual parameters and policy analysis in economics: A twentieth century

retrospective, The Quarterly Journal of Economics, 115(1): 45–97.

Heckman, J.J. 2001. Micro data, heterogeneity and the evaluation of public policy: Nobel lecture,

Journal of Political Economy, 109(4): 673–748

Lucas, R. 1976. The Phillips curve and labor market, in Carnegie-Rochester Conference Series on

Public Policy, K. Brunner and A.H. Meltzer (Eds.), North-Holland Publishing Company.

Maddala, G.S. 2001. Introduction to Econometrics, 3rd ed., New York: John Wiley & Sons

Ramelli, Stefano and Alexander F. Wagner. 2020. Feverish Stock Price Reactions to COVID-19.

Swiss Finance Institute Research Paper Series No. 20-12. Zurich: Swiss Finance Institute

Sims, C.A (1982), “Policy Analysis with Econometric Models”, Brooking Papers on Economic

Activity, 107-64

Zaremba Adam, Kizysc R , Tzouvanasd P, Aharone David Y , and Demir E, “The Quest for

Multidimensional Financial Immunity to the COVID-19 Pandemic: Evidence from International

Stock Markets”, SSRN.com

Thakur, S. (2020). “Effect of COVID-19 on Capital Market with Reference to S&P 500,”

Available at: SSRN 3640871

Alber, N, Refaat (2020) The Effects of Covid-19 Spread on the Egyptian Exchange Sectors:

Winners and Losers across Time : http://ssrn.com/abstract=3741179

Gormsen, N.J and Koijen, R.S.J, “Coronavirus: Impact on Stock Prices and Growth Expectation”

Working Paper 27387 http://www.nber.org/papers/w27387, NBER Working Paper Series

National Bureau of Economic Research 1050 Massachusetts Avenue Cambridge, MA 02138 June

2020

Appendix 1. Computing Unit Root

Null Hypothesis: INA_INDEX has a unit root

Exogenous: Constant

Lag Length: 0 (Automatic - based on SIC, maxlag=10) t-Statistic Prob.* Augmented Dickey-Fuller test statistic -0.925908 0.7739

Test critical values: 1% level -3.534868

5% level -2.906923

10% level -2.591006 *MacKinnon (1996) one-sided p-values.

Augmented Dickey-Fuller Test Equation

Dependent Variable: D(INA_INDEX)

Method: Least Squares

Date: 06/11/21 Time: 07:20

Sample (adjusted): 3/09/2020 5/31/2021

Included observations: 65 after adjustments Variable Coefficient Std. Error t-Statistic Prob. INA_INDEX(-1) -0.033471 0.036150 -0.925908 0.3580

C 190.3485 197.4051 0.964253 0.3386 R-squared 0.013425 Mean dependent var 8.707692

Adjusted R-squared -0.002235 S.D. dependent var 177.1323

S.E. of regression 177.3301 Akaike info criterion 13.22419

Sum squared resid 1981097. Schwarz criterion 13.29109

Log likelihood -427.7862 Hannan-Quinn criter. 13.25059

F-statistic 0.857305 Durbin-Watson stat 1.529181

Prob(F-statistic) 0.358027

Appendix 2. Computing Stationary

Null Hypothesis: D(INA_INDEX) has a unit root

Exogenous: Constant

Lag Length: 0 (Automatic - based on SIC, maxlag=10) t-Statistic Prob.* Augmented Dickey-Fuller test statistic -7.636764 0.0000

Test critical values: 1% level -3.536587

5% level -2.907660

10% level -2.591396

*MacKinnon (1996) one-sided p-values.

Augmented Dickey-Fuller Test Equation

Dependent Variable: D(INA_INDEX,2)

Method: Least Squares

Date: 06/11/21 Time: 07:21

Sample (adjusted): 3/16/2020 5/31/2021

Included observations: 64 after adjustments Variable Coefficient Std. Error t-Statistic Prob. D(INA_INDEX(-1)) -0.879147 0.115120 -7.636764 0.0000

C 17.41721 20.17856 0.863154 0.3914 R-squared 0.484708 Mean dependent var 12.60938

Adjusted R-squared 0.476397 S.D. dependent var 222.9809

S.E. of regression 161.3499 Akaike info criterion 13.03578

Sum squared resid 1614096. Schwarz criterion 13.10324

Log likelihood -415.1449 Hannan-Quinn criter. 13.06236

F-statistic 58.32017 Durbin-Watson stat 2.141562

Prob(F-statistic) 0.000000

Appendix 3 Computing AR Root Graph

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

-1.5 -1.0 -0.5 0.0 0.5 1.0 1.5

Inverse Roots of AR Characteristic Polynomial

Appendix 4. Granger Causality Test

VEC Granger Causality/Block Exogeneity Wald Tests

Date: 06/11/21 Time: 11:30

Sample: 3/02/2020 5/31/2021

Included observations: 60

Dependent variable: D(INA_INDEX,2) Excluded Chi-sq df Prob. D(INA_COVID,2) 14.05388 4 0.0071

D(USA_INDEX,2) 5.561590 4 0.2344

D(USA_COVID,2) 24.12999 4 0.0001

D(KSA_INDEX,2) 10.41048 4 0.0341

D(KSA_COVID,2) 0.806225 4 0.9376

D(GOLD) 16.06977 4 0.0029

D(CRUDE_OIL) 3.980824 4 0.4086 All 77.51796 28 0.0000

Dependent variable: D(INA_COVID,2) Excluded Chi-sq df Prob. D(INA_INDEX,2) 5.857322 4 0.2101

D(USA_INDEX,2) 3.480870 4 0.4808

D(USA_COVID,2) 8.592531 4 0.0721

D(KSA_INDEX,2) 2.529026 4 0.6394

D(KSA_COVID,2) 0.336255 4 0.9874

D(GOLD) 1.343464 4 0.8540

D(CRUDE_OIL) 2.861125 4 0.5813 All 35.24525 28 0.1628

Dependent variable: D(USA_INDEX,2) Excluded Chi-sq df Prob. D(INA_INDEX,2) 8.612173 4 0.0716

D(INA_COVID,2) 7.019992 4 0.1348

D(USA_COVID,2) 6.206789 4 0.1842

D(KSA_INDEX,2) 2.120195 4 0.7137

D(KSA_COVID,2) 1.964788 4 0.7422

D(GOLD) 5.678326 4 0.2245

D(CRUDE_OIL) 5.380007 4 0.2505 All 30.44673 28 0.3422

Dependent variable: D(USA_COVID,2) Excluded Chi-sq df Prob. D(INA_INDEX,2) 5.140453 4 0.2732

D(INA_COVID,2) 14.80365 4 0.0051

D(USA_INDEX,2) 7.101568 4 0.1306

D(KSA_INDEX,2) 1.381230 4 0.8475

D(KSA_COVID,2) 1.795747 4 0.7733

D(GOLD) 5.238392 4 0.2637

D(CRUDE_OIL) 0.759088 4 0.9438 All 37.70108 28 0.1042

Dependent variable: D(KSA_INDEX,2) Excluded Chi-sq df Prob. D(INA_INDEX,2) 6.665887 4 0.1546

D(INA_COVID,2) 10.65305 4 0.0308

D(USA_INDEX,2) 6.232408 4 0.1825

D(USA_COVID,2) 1.567931 4 0.8145

D(KSA_COVID,2) 0.919798 4 0.9217

D(GOLD) 3.953907 4 0.4123

D(CRUDE_OIL) 1.116784 4 0.8916 All 23.45882 28 0.7098

Dependent variable: D(KSA_COVID,2) Excluded Chi-sq df Prob. D(INA_INDEX,2) 11.44653 4 0.0220

D(INA_COVID,2) 4.468796 4 0.3463

D(USA_INDEX,2) 12.56446 4 0.0136

D(USA_COVID,2) 2.850433 4 0.5832

D(KSA_INDEX,2) 5.056394 4 0.2816

D(GOLD) 4.549962 4 0.3367

D(CRUDE_OIL) 4.563563 4 0.3351 All 35.32102 28 0.1607

Dependent variable: D(GOLD) Excluded Chi-sq df Prob. D(INA_INDEX,2) 1.892150 4 0.7556

D(INA_COVID,2) 4.439357 4 0.3498

D(USA_INDEX,2) 1.228818 4 0.8733

D(USA_COVID,2) 1.907682 4 0.7527

D(KSA_INDEX,2) 4.113663 4 0.3908

D(KSA_COVID,2) 3.365413 4 0.4986

D(CRUDE_OIL) 3.791164 4 0.4350 All 35.84425 28 0.1466

Dependent variable: D(CRUDE_OIL) Excluded Chi-sq df Prob.

D(INA_INDEX,2) 8.989068 4 0.0614

D(INA_COVID,2) 10.57935 4 0.0317

D(USA_INDEX,2) 12.48598 4 0.0141

D(USA_COVID,2) 14.00376 4 0.0073

D(KSA_INDEX,2) 13.66354 4 0.0085

D(KSA_COVID,2) 6.680530 4 0.1538

D(GOLD) 6.741651 4 0.1502 All 46.51023 28 0.0154

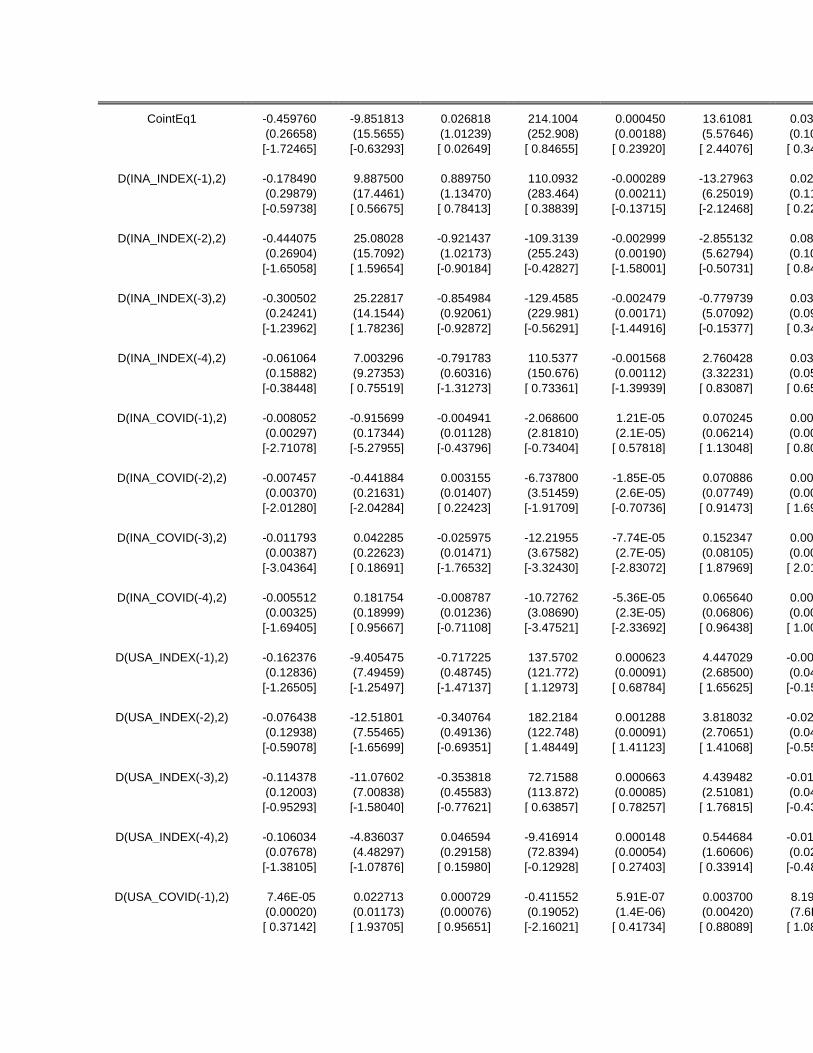

Appendix 5 Computing Vector Error Correction Estimates

Vector Error Correction Estimates

Date: 06/11/21 Time: 07:42

Sample (adjusted): 4/13/2020 5/31/2021

Included observations: 60 after adjustments

Standard errors in ( ) & t-statistics in [ ] Cointegrating Eq: CointEq1 D(INA_INDEX(-1)) 1.000000

D(INA_COVID(-1)) -0.004278

(0.00275)

[-1.55516]

D(USA_INDEX(-1)) -0.411914

(0.07452)

[-5.52773]

D(USA_COVID(-1)) -0.000570

(9.5E-05)

[-5.99133]

D(KSA_INDEX(-1)) 128.2346

(28.6396)

[ 4.47753]

D(KSA_COVID(-1)) -0.044520

(0.00602)

[-7.39269]

GOLD(-1) -0.185750

(0.10814)

[-1.71765]

CRUDE_OIL(-1) -0.330587

(0.35746)

[-0.92482]

C 358.4305

Error Correction: D(INA_INDEX,2

) D(INA_COVID,2

) D(USA_INDEX,

2) D(USA_COVID,

2) D(KSA_INDEX,

2) D(KSA_COVID,

2) D(GOLD)

CointEq1 -0.459760 -9.851813 0.026818 214.1004 0.000450 13.61081 0.035190

(0.26658) (15.5655) (1.01239) (252.908) (0.00188) (5.57646) (0.10056)

[-1.72465] [-0.63293] [ 0.02649] [ 0.84655] [ 0.23920] [ 2.44076] [ 0.34994]

D(INA_INDEX(-1),2) -0.178490 9.887500 0.889750 110.0932 -0.000289 -13.27963 0.024876

(0.29879) (17.4461) (1.13470) (283.464) (0.00211) (6.25019) (0.11271)

[-0.59738] [ 0.56675] [ 0.78413] [ 0.38839] [-0.13715] [-2.12468] [ 0.22071]

D(INA_INDEX(-2),2) -0.444075 25.08028 -0.921437 -109.3139 -0.002999 -2.855132 0.085968

(0.26904) (15.7092) (1.02173) (255.243) (0.00190) (5.62794) (0.10149)

[-1.65058] [ 1.59654] [-0.90184] [-0.42827] [-1.58001] [-0.50731] [ 0.84708]

D(INA_INDEX(-3),2) -0.300502 25.22817 -0.854984 -129.4585 -0.002479 -0.779739 0.031254

(0.24241) (14.1544) (0.92061) (229.981) (0.00171) (5.07092) (0.09144)

[-1.23962] [ 1.78236] [-0.92872] [-0.56291] [-1.44916] [-0.15377] [ 0.34179]

D(INA_INDEX(-4),2) -0.061064 7.003296 -0.791783 110.5377 -0.001568 2.760428 0.039147

(0.15882) (9.27353) (0.60316) (150.676) (0.00112) (3.32231) (0.05991)

[-0.38448] [ 0.75519] [-1.31273] [ 0.73361] [-1.39939] [ 0.83087] [ 0.65342]

D(INA_COVID(-1),2) -0.008052 -0.915699 -0.004941 -2.068600 1.21E-05 0.070245 0.000906

(0.00297) (0.17344) (0.01128) (2.81810) (2.1E-05) (0.06214) (0.00112)

[-2.71078] [-5.27955] [-0.43796] [-0.73404] [ 0.57818] [ 1.13048] [ 0.80855]

D(INA_COVID(-2),2) -0.007457 -0.441884 0.003155 -6.737800 -1.85E-05 0.070886 0.002370

(0.00370) (0.21631) (0.01407) (3.51459) (2.6E-05) (0.07749) (0.00140)

[-2.01280] [-2.04284] [ 0.22423] [-1.91709] [-0.70736] [ 0.91473] [ 1.69591]

D(INA_COVID(-3),2) -0.011793 0.042285 -0.025975 -12.21955 -7.74E-05 0.152347 0.002952

(0.00387) (0.22623) (0.01471) (3.67582) (2.7E-05) (0.08105) (0.00146)

[-3.04364] [ 0.18691] [-1.76532] [-3.32430] [-2.83072] [ 1.87969] [ 2.01956]

D(INA_COVID(-4),2) -0.005512 0.181754 -0.008787 -10.72762 -5.36E-05 0.065640 0.001237

(0.00325) (0.18999) (0.01236) (3.08690) (2.3E-05) (0.06806) (0.00123)

[-1.69405] [ 0.95667] [-0.71108] [-3.47521] [-2.33692] [ 0.96438] [ 1.00815]

D(USA_INDEX(-1),2) -0.162376 -9.405475 -0.717225 137.5702 0.000623 4.447029 -0.007633

(0.12836) (7.49459) (0.48745) (121.772) (0.00091) (2.68500) (0.04842)

[-1.26505] [-1.25497] [-1.47137] [ 1.12973] [ 0.68784] [ 1.65625] [-0.15765]

D(USA_INDEX(-2),2) -0.076438 -12.51801 -0.340764 182.2184 0.001288 3.818032 -0.027043

(0.12938) (7.55465) (0.49136) (122.748) (0.00091) (2.70651) (0.04881)

[-0.59078] [-1.65699] [-0.69351] [ 1.48449] [ 1.41123] [ 1.41068] [-0.55409]

D(USA_INDEX(-3),2) -0.114378 -11.07602 -0.353818 72.71588 0.000663 4.439482 -0.019855

(0.12003) (7.00838) (0.45583) (113.872) (0.00085) (2.51081) (0.04528)

[-0.95293] [-1.58040] [-0.77621] [ 0.63857] [ 0.78257] [ 1.76815] [-0.43852]

D(USA_INDEX(-4),2) -0.106034 -4.836037 0.046594 -9.416914 0.000148 0.544684 -0.014174

(0.07678) (4.48297) (0.29158) (72.8394) (0.00054) (1.60606) (0.02896)

[-1.38105] [-1.07876] [ 0.15980] [-0.12928] [ 0.27403] [ 0.33914] [-0.48940]

D(USA_COVID(-1),2) 7.46E-05 0.022713 0.000729 -0.411552 5.91E-07 0.003700 8.19E-05

(0.00020) (0.01173) (0.00076) (0.19052) (1.4E-06) (0.00420) (7.6E-05)

[ 0.37142] [ 1.93705] [ 0.95651] [-2.16021] [ 0.41734] [ 0.88089] [ 1.08082]

D(USA_COVID(-2),2) -0.000162 0.021072 0.000471 -0.439413 8.92E-07 0.001078 5.07E-05

(0.00022) (0.01279) (0.00083) (0.20781) (1.5E-06) (0.00458) (8.3E-05)

[-0.74142] [ 1.64757] [ 0.56581] [-2.11453] [ 0.57687] [ 0.23533] [ 0.61398]

D(USA_COVID(-3),2) 0.000182 0.017195 0.001598 0.241994 2.00E-06 -0.002558 1.00E-05

(0.00025) (0.01433) (0.00093) (0.23276) (1.7E-06) (0.00513) (9.3E-05)

[ 0.74208] [ 1.20034] [ 1.71486] [ 1.03968] [ 1.15458] [-0.49833] [ 0.10841]

D(USA_COVID(-4),2) 0.000660 0.027094 0.001489 0.381120 1.10E-06 -0.000395 -9.29E-06

(0.00020) (0.01139) (0.00074) (0.18509) (1.4E-06) (0.00408) (7.4E-05)

[ 3.38399] [ 2.37853] [ 2.00930] [ 2.05916] [ 0.80241] [-0.09687] [-0.12623]

D(KSA_INDEX(-1),2) 70.90091 6014.759 -106.3397 -63433.40 -1.049828 -2312.722 -30.32159

(69.2756) (4044.96) (263.086) (65722.5) (0.48878) (1449.14) (26.1319)

[ 1.02346] [ 1.48698] [-0.40420] [-0.96517] [-2.14787] [-1.59593] [-1.16033]

D(KSA_INDEX(-2),2) 81.84985 6122.056 -132.3758 -47703.89 -1.013504 -2750.904 -26.85711

(71.9551) (4201.41) (273.262) (68264.5) (0.50768) (1505.19) (27.1426)

[ 1.13751] [ 1.45714] [-0.48443] [-0.69881] [-1.99634] [-1.82762] [-0.98948]

D(KSA_INDEX(-3),2) 0.863698 4702.259 -215.9304 -49367.92 -0.803860 -2155.685 -34.89441

(65.9110) (3848.50) (250.309) (62530.5) (0.46504) (1378.75) (24.8627)

[ 0.01310] [ 1.22184] [-0.86266] [-0.78950] [-1.72859] [-1.56350] [-1.40348]

D(KSA_INDEX(-4),2) 40.88320 3006.763 -47.70380 -35343.86 -0.116606 -874.0523 -7.532492

(44.3510) (2589.62) (168.431) (42076.2) (0.31292) (927.753) (16.7299)

[ 0.92181] [ 1.16108] [-0.28323] [-0.84000] [-0.37264] [-0.94212] [-0.45024]

D(KSA_COVID(-1),2) -0.008108 -0.055797 -0.007146 12.30112 4.50E-05 0.010780 -0.004402

(0.01144) (0.66825) (0.04346) (10.8578) (8.1E-05) (0.23941) (0.00432)

[-0.70848] [-0.08350] [-0.16441] [ 1.13293] [ 0.55759] [ 0.04503] [-1.01964]

D(KSA_COVID(-2),2) -0.007541 -0.198028 0.006653 12.10061 5.83E-05 -0.212137 -0.005592

(0.01117) (0.65237) (0.04243) (10.5997) (7.9E-05) (0.23372) (0.00421)

[-0.67492] [-0.30355] [ 0.15680] [ 1.14160] [ 0.73911] [-0.90767] [-1.32673]

D(KSA_COVID(-3),2) -0.007737 -0.055877 -0.014282 5.863222 2.83E-05 0.176189 -0.006227

(0.00913) (0.53281) (0.03465) (8.65710) (6.4E-05) (0.19088) (0.00344)

[-0.84786] [-0.10487] [-0.41213] [ 0.67727] [ 0.43999] [ 0.92302] [-1.80912]

D(KSA_COVID(-4),2) -0.004684 0.059535 0.028093 6.360987 4.85E-05 -0.047921 -0.002927

(0.00797) (0.46533) (0.03027) (7.56077) (5.6E-05) (0.16671) (0.00301)

[-0.58773] [ 0.12794] [ 0.92821] [ 0.84131] [ 0.86175] [-0.28745] [-0.97371]

D(GOLD(-1)) 0.634102 17.61648 0.644470 388.0502 0.001387 -8.371264 -0.163895

(0.46392) (27.0882) (1.76183) (440.130) (0.00327) (9.70456) (0.17500)

[ 1.36682] [ 0.65034] [ 0.36579] [ 0.88167] [ 0.42367] [-0.86261] [-0.93655]

D(GOLD(-2)) -0.948509 21.91701 -1.267944 -556.3714 0.000368 -3.446925 0.066093

(0.39390) (22.9998) (1.49592) (373.702) (0.00278) (8.23987) (0.14859)

[-2.40796] [ 0.95292] [-0.84760] [-1.48881] [ 0.13233] [-0.41832] [ 0.44481]

D(GOLD(-3)) 1.039519 4.167195 3.730438 380.2367 0.005910 -4.226477 -0.044800

(0.48602) (28.3785) (1.84575) (461.094) (0.00343) (10.1668) (0.18334)

[ 2.13883] [ 0.14684] [ 2.02109] [ 0.82464] [ 1.72345] [-0.41571] [-0.24436]

D(GOLD(-4)) 0.760407 3.716705 -1.129962 -448.8828 -0.002304 17.43608 0.148333

(0.45752) (26.7143) (1.73752) (434.055) (0.00323) (9.57062) (0.17258)

[ 1.66202] [ 0.13913] [-0.65033] [-1.03416] [-0.71379] [ 1.82183] [ 0.85948]

D(CRUDE_OIL(-1)) -5.187147 -378.1723 -14.41469 5681.778 0.068346 348.1718 -0.262931

(11.9125) (695.562) (45.2398) (11301.5) (0.08405) (249.191) (4.49359)

[-0.43544] [-0.54369] [-0.31863] [ 0.50275] [ 0.81317] [ 1.39721] [-0.05851]

D(CRUDE_OIL(-2)) 7.827794 -645.0067 55.97923 -2764.454 0.025979 -70.73245 1.653109

(9.51398) (555.515) (36.1310) (9026.01) (0.06713) (199.017) (3.58883)

[ 0.82277] [-1.16110] [ 1.54934] [-0.30628] [ 0.38702] [-0.35541] [ 0.46063]

D(CRUDE_OIL(-3)) 9.743638 336.5220 20.71735 -874.1859 0.027793 -75.85999 3.427928

(7.45507) (435.296) (28.3119) (7072.70) (0.05260) (155.948) (2.81218)

[ 1.30698] [ 0.77309] [ 0.73175] [-0.12360] [ 0.52839] [-0.48644] [ 1.21896]

D(CRUDE_OIL(-4)) -4.953048 364.6796 -29.34248 -3938.372 -0.032274 -210.9002 -4.126178

(7.36298) (429.919) (27.9622) (6985.33) (0.05195) (154.022) (2.77744)

[-0.67270] [ 0.84825] [-1.04936] [-0.56381] [-0.62126] [-1.36929] [-1.48561]

C -4.416970 467.1706 -37.51750 -1237.626 -0.086136 -180.8658 1.910721

(19.7031) (1150.45) (74.8259) (18692.5) (0.13902) (412.158) (7.43233)

[-0.22418] [ 0.40608] [-0.50140] [-0.06621] [-0.61962] [-0.43883] [ 0.25708] R-squared 0.867120 0.735784 0.779988 0.748854 0.705761 0.707113 0.607680

Adj. R-squared 0.698464 0.400433 0.500742 0.430092 0.332303 0.335371 0.109736

Sum sq. resids 254772.8 8.69E+08 3674418. 2.29E+11 12.68271 1.11E+08 36252.21

S.E. equation 98.98967 5779.937 375.9306 93912.50 0.698424 2070.708 37.34054

F-statistic 5.141351 2.194071 2.793192 2.349254 1.889803 1.902162 1.220377

Log likelihood -335.7498 -579.7778 -415.8131 -747.0560 -38.51317 -518.1876 -277.2536

Akaike AIC 12.32499 20.45926 14.99377 26.03520 2.417106 18.40625 10.37512

Schwarz SC 13.51179 21.64605 16.18057 27.22200 3.603901 19.59305 11.56192

Mean dependent 3.166667 54.61667 -18.40000 -1446.400 0.020978 0.216667 2.566667

S.D. dependent 180.2686 7464.560 532.0409 124400.1 0.854732 2539.973 39.57502 Determinant resid covariance (dof adj.) 8.55E+34

Determinant resid covariance 1.06E+32

Log likelihood -2893.406

Akaike information criterion 105.7802

Schwarz criterion 115.5538

Number of coefficients 280

Appendix 6 Computing Variance Decomposition Response of D(INA_INDE

X):

Period D(INA_INDEX) D(INA_COVID

) D(USA_INDE

X) D(USA_COVI

D) D(KSA_INDEX

) D(KSA_COVI

D) GOLD CRUDE_OIL 1 98.98967 0.000000 0.000000 0.000000 0.000000 0.000000 0.000000 0.000000

2 49.45153 -26.30335 -7.810547 30.20432 1.532832 19.09187 26.30534 -3.501568

3 27.72653 -22.03783 35.58754 -16.77782 -0.286402 17.82375 -33.17091 11.02614

4 4.457314 -53.07925 -8.991869 -2.998671 -12.19831 11.41768 27.16427 7.516554

5 -4.359242 -7.071244 -32.80648 46.64739 -17.98768 1.486360 22.63976 0.119222

6 70.84426 -19.79412 -4.268301 -13.09778 -21.33004 11.64507 7.911950 -3.473559

7 31.48940 -4.984444 16.86227 3.831054 -16.77485 19.30294 -20.27434 -1.783494

8 16.83715 -18.31931 -17.98915 17.10362 -17.54224 9.086136 -3.466365 2.474385

9 18.51897 -7.896582 -25.87376 32.07039 -13.28068 25.59127 16.73677 2.591561

10 38.60658 6.311310 6.223579 21.49672 -4.555450 14.58229 26.14716 -2.038612 Response of

D(INA_COVID):

Period D(INA_INDEX) D(INA_COVID

) D(USA_INDE

X) D(USA_COVI

D) D(KSA_INDEX

) D(KSA_COVI

D) GOLD CRUDE_OIL 1 -1800.185 5492.450 0.000000 0.000000 0.000000 0.000000 0.000000 0.000000

2 -314.9097 1504.280 -931.4226 2729.391 1568.605 456.2125 721.3783 -260.7251

3 301.0283 2764.171 -1407.822 983.0111 -307.5509 251.5137 952.4648 52.32383

4 530.5834 1458.357 -981.2296 2050.128 206.6670 475.9949 999.1415 -122.4837

5 -543.4798 1112.584 -1026.559 3028.070 353.0645 399.7043 624.3685 198.8450

6 700.9566 -474.3921 -1776.845 -255.1029 -606.5822 -75.13076 363.8520 166.4615

7 -995.5395 1500.129 -619.5294 2074.459 334.6182 -377.5088 1031.759 -215.4095

8 -150.7427 166.9968 -1384.725 1620.233 -309.9686 72.79468 337.3816 73.93642

9 495.0050 1541.154 -886.5811 468.0150 -632.0882 179.5857 124.9503 -199.4616

10 -795.8729 1650.629 -187.4129 1148.269 252.7977 -393.9166 863.4495 -63.01491 Response of

D(USA_INDEX):

Period D(INA_INDEX) D(INA_COVID

) D(USA_INDE

X) D(USA_COVI

D) D(KSA_INDEX

) D(KSA_COVI

D) GOLD CRUDE_OIL 1 192.7350 -32.94661 321.0787 0.000000 0.000000 0.000000 0.000000 0.000000

2 107.0264 -42.42410 0.565089 66.50213 -65.20298 -25.48855 23.81349 -10.03048

3 -27.05895 -33.03215 145.3217 15.50883 13.59436 50.17921 -25.02795 32.19051

4 -24.27254 -160.1361 29.29039 42.64645 -18.59153 -23.53614 90.05184 22.61676

5 34.28563 1.897322 60.68001 67.50617 -75.09873 0.015135 -26.97027 -12.25588

6 163.9966 -90.66125 113.5400 17.75650 -7.958789 -14.52302 -21.66167 -0.666976

7 53.62550 -77.20970 113.3626 -13.21992 -65.79428 22.09275 -50.38934 5.027681

8 43.28242 -81.42569 107.4141 15.76213 -20.01635 -1.346498 -38.65736 -2.342825

9 -13.60274 -25.14228 80.49715 60.24792 -19.00572 21.89540 8.629999 20.27523

10 98.55721 -37.84344 98.07431 25.62058 -10.05321 -10.81655 13.80352 -4.694000 Response of

D(USA_COVID):

Period D(INA_INDEX) D(INA_COVID

) D(USA_INDE

X) D(USA_COVI

D) D(KSA_INDEX

) D(KSA_COVI

D) GOLD CRUDE_OIL 1 -13247.33 6493.065 -30729.66 87507.69 0.000000 0.000000 0.000000 0.000000

2 29035.92 -16723.67 -9365.844 35626.79 -7806.145 8316.195 12382.62 3902.023

3 33464.99 -46366.84 -2507.139 24188.62 -11328.53 2561.553 -10264.20 -2929.425

4 -1813.474 -61976.66 -17668.61 38099.77 -11878.68 -6039.852 -17279.18 4976.808

5 4552.917 -61649.89 -36570.74 34057.02 -21427.56 -889.5595 -16452.23 6138.958

6 21928.65 -26701.73 15141.14 13065.53 -5598.889 -10164.13 -1644.348 -6476.774

7 27817.76 -44396.26 14490.55 2362.657 -7086.285 -10357.85 -40867.07 -2347.748

8 9062.370 -35836.35 -8638.397 16209.67 -11707.99 -4617.110 -23157.44 1022.841

9 -3761.824 -24829.33 -12546.37 31197.67 -7402.053 -7132.994 937.8663 1429.655

10 25918.44 -20981.37 12832.90 16263.13 9425.271 -6697.770 -12977.35 -3333.181 Response of

D(KSA_INDEX):

Period D(INA_INDEX) D(INA_COVID

) D(USA_INDE

X) D(USA_COVI

D) D(KSA_INDEX

) D(KSA_COVI

D) GOLD CRUDE_OIL 1 0.281789 0.056669 0.490094 0.020713 0.405659 0.000000 0.000000 0.000000

2 0.077588 0.049452 0.215845 -0.014467 0.092388 0.088350 0.044277 0.047426

3 -0.034482 -0.158274 0.190025 0.079499 0.047237 0.061873 0.051132 0.007861

4 -0.015790 -0.316208 0.036310 -0.042207 0.007655 -0.059933 0.081779 0.047544

5 0.055573 -0.051818 0.154436 -0.081893 0.135331 -0.016775 -0.046564 0.008864

6 0.102191 0.105821 0.332646 -0.018542 0.173363 -0.003739 -0.047831 -0.002989

7 0.122266 -0.130702 0.242377 -0.093753 0.063010 0.034490 -0.082854 -0.007862

8 0.046812 -0.061023 0.228823 -0.073734 0.099213 0.000682 -0.012812 0.010641

9 -0.062438 -0.019006 0.169543 0.037862 0.147960 0.036776 0.077342 0.044535

10 0.092538 0.048595 0.217004 0.004205 0.155851 0.020281 -0.008169 0.005995 Response of

D(KSA_COVID):

Period D(INA_INDEX) D(INA_COVID

) D(USA_INDE

X) D(USA_COVI

D) D(KSA_INDEX

) D(KSA_COVI

D) GOLD CRUDE_OIL 1 284.0102 506.0426 -509.0173 3.403477 435.3719 1871.478 0.000000 0.000000

2 -129.6248 248.7495 -282.8506 -527.4750 403.1001 987.8968 -410.1415 238.9979

3 536.2512 216.2720 -422.2190 -617.0190 118.1008 76.02689 -227.7351 -38.77020

4 967.2674 637.8612 50.24104 -420.0015 385.6363 786.5755 -342.6636 -171.8151

5 562.3763 324.8364 -450.4118 -328.6220 562.6251 581.4962 114.5603 -57.08032

6 -94.26371 158.1385 -91.06531 -535.3461 294.0960 400.3598 244.2974 157.0076

7 201.9416 329.5722 -318.4534 -311.6277 155.8784 229.4554 577.2904 -36.02595

8 358.6103 344.3594 -717.8319 -339.9889 281.8765 190.6121 244.2707 -48.97138

9 431.4028 108.4291 -369.0477 -614.5994 597.4611 109.1571 247.0663 40.01470

10 107.0561 341.6766 -104.5241 -409.0156 265.5916 398.7213 288.7982 12.51206 Response of

GOLD:

Period D(INA_INDEX) D(INA_COVID

) D(USA_INDE

X) D(USA_COVI

D) D(KSA_INDEX

) D(KSA_COVI

D) GOLD CRUDE_OIL 1 -6.880423 -2.025249 1.570559 -3.433652 -3.569057 -1.189939 36.25553 0.000000

2 -15.17248 -0.864247 -17.68436 2.164605 -16.36305 -12.33084 30.08840 -0.190938

3 -12.50082 3.361784 -20.63454 5.522425 -14.13253 -17.34234 36.75998 -1.571686

4 -17.87360 8.479488 -22.44995 6.313248 -13.51194 -16.49757 35.42208 -0.025988

5 -11.50962 10.59700 -19.76127 13.06505 -8.868854 -16.00353 40.44525 -4.185692

6 -17.34681 4.623280 -20.04849 17.39614 -14.99784 -9.041405 39.09682 0.757155

7 -17.35592 2.015135 -26.35093 19.56757 -20.05556 -9.214221 44.72077 -0.367309

8 -17.98187 0.539104 -27.19908 17.50041 -21.32294 -9.952269 39.48172 -0.079386

9 -16.27042 0.140588 -27.78502 15.58374 -17.31977 -10.15637 36.02909 -0.746684

10 -17.18108 4.785824 -27.51197 19.37826 -19.94298 -7.738204 34.57244 -0.926749 Response of

CRUDE_OIL:

Period D(INA_INDEX) D(INA_COVID

) D(USA_INDE

X) D(USA_COVI

D) D(KSA_INDEX

) D(KSA_COVI

D) GOLD CRUDE_OIL 1 -0.003423 -0.069564 1.355635 -0.579736 1.216564 0.632315 -0.043574 0.695424

2 -0.082267 0.346242 1.109252 -0.569795 1.467462 0.791907 0.451243 0.550311

3 -0.438123 0.111353 1.488298 -0.613299 1.525466 1.149203 -0.355909 0.587892

4 -0.682408 -0.527378 1.355642 -0.803465 1.212519 1.481709 -0.211446 0.743303

5 -0.936840 -0.094421 1.021693 -0.408996 0.712121 1.783625 -0.248000 0.617014

6 -0.576236 0.594782 1.407108 -0.596963 0.851556 1.941100 -0.579708 0.531730

7 -0.508072 0.795619 1.388974 -0.739981 0.889946 2.185281 -1.060009 0.570517

8 -0.619070 1.168904 1.008854 -0.188434 0.859018 2.193433 -0.768706 0.473176

9 -0.478098 1.112726 0.750393 0.300039 0.820421 2.384724 -0.546148 0.499383

10 -0.050046 0.953757 0.936771 0.202156 0.904377 2.353287 -0.458290 0.498852 Cholesky Ordering: D(INA_INDEX) D(INA_COVID) D(USA_INDEX) D(USA_COVID) D(KSA_INDEX) D(KSA_COVID)

GOLD

CRUDE_OIL