Embed Size (px)

Citation preview

Revision 3 – 23-May-2014 Prepared for – Mornington Peninsula Shire Council – ABN: N/A

Mornington Peninsula Shire Council 23-May-2014

Southern Peninsula AquaticReport to Council June 2014

Attachment 1

Davis Langdon, an AECOM company Southern Peninsula Aquatic

Revision 3 – 23-May-2014 Prepared for – Mornington Peninsula Shire Council – ABN: N/A

Southern Peninsula Aquatic Report to Council June 2014

Client: Mornington Peninsula Shire Council ABN: N/A

Prepared by Davis Langdon Australia Pty LtdLevel 45, 80 Collins Street, Melbourne VIC 3000, Australia T +61 3 9933 8800 F +61 3 9933 8801 www.davislangdon.com ABN 40 008 657 289

23-May-2014

Job No.: 60318327

Davis Langdon in Australia and New Zealand is certified to the latest version of ISO9001, ISO14001, AS/NZS4801 and OHSAS18001.

© Davis Langdon Australia Pty Ltd (Davis Langdon). All rights reserved.

Davis Langdon has prepared this document for the sole use of the Client and for a specific purpose, each as expressly stated in the document. No other party should rely on this document without the prior written consent of Davis Langdon. Davis Langdon undertakes no duty, nor accepts any responsibility, to any third party who may rely upon or use this document. This document has been prepared based on the Client’s description of its requirements and Davis Langdon’s experience, having regard to assumptions that Davis Langdon can reasonably be expected to make in accordance with sound professional principles. Davis Langdon may also have relied upon information provided by the Client and other third parties to prepare this document, some of which may not have been verified. Subject to the above conditions, this document may be transmitted, reproduced or disseminated only in its entirety.

Attachment 1

Davis Langdon, an AECOM company Southern Peninsula Aquatic

Revision 3 – 23-May-2014 Prepared for – Mornington Peninsula Shire Council – ABN: N/A

Quality Information Document Southern Peninsula Aquatic

Ref 60318327

Date 23-May-2014

Prepared by Mark Hayden

Reviewed by Peter Southwell

Revision History

Revision RevisionDate Details

Authorised

Name/Position Signature

1 28.04.14 Draft Mark Hayden

2 09.05.14 Final Peter Southwell

3 23.05.14 Updated for 10 June Meeting

Mark Hayden

Attachment 1

Davis Langdon, an AECOM company Southern Peninsula Aquatic

Revision 3 – 23-May-2014 Prepared for – Mornington Peninsula Shire Council – ABN: N/A

Table of Contents 1.0 Purpose 22.0 Design Competition Brief Overview 13.0 Design and Business Case Enhancements 3

3.1 Waterplay / Waterslides 33.2 Gymnasium 43.3 Kitchen / Café 43.4 Outdoor Viewing Deck 5

4.0 Rosebud Memorial Hall 65.0 Financial Considerations 86.0 Way Forward 9

Appendix ASPA Waterslides Review and Business Plan A

Appendix BSPA Component Review B

Attachment 1

Davis Langdon, an AECOM company Southern Peninsula Aquatic

Revision 3 – 23-May-2014 Prepared for – Mornington Peninsula Shire Council – ABN: N/A

1.0 Purpose Mornington Peninsula Shire Council has engaged Davis Langdon as external Project and Cost Manager to the Southern Peninsula Aquatic (SPA) project.

The process of engaging a Principal Consultant to provide all design related consultancy services has commenced in accordance with the Procurement Management Plan and the following two stage tender process:

Stage 1 Tender – Expressions of Interest

Expressions of Interest for Principal Design Consultant Services were sought and submissions from 15 organisations were received on 04 April 2014. Following the evaluation of submissions by an Evaluation Panel, a short list of four highly capable architectural firms (Cox Architecture, Peddle Thorp, Suters Architects and Williams Ross) was finalized to participate in the second stage design competition.

Stage 2 Tender – Design Competition

The second stage of the agreed tender process will seek design submissions from the shortlisted organisations in response to Council’s project brief. As part of the second stage tender, shortlisted organisations will also be required to provide proposals in relation to fixed consultancy fees on the basis of the brief.

The purpose of this report is to seek Council’s endorsement of the design competition brief for the Southern Peninsula Aquatic project that provides for a wide degree of design innovation and excellence.

Attachment 1

Davis Langdon, an AECOM company Southern Peninsula Aquatic

Revision 3 – 23-May-2014 Prepared for – Mornington Peninsula Shire Council – ABN: N/A

1

2.0 Design Competition Brief Overview The design competition brief is a comprehensive document developed by Davis Langdon with input from the Project Steering Committee and Council’s Business Planning Consultant, SGL Group. The brief provides for a high degree of design flexibility and innovation by describing Council’s project requirements, but without being prescriptive regarding how those requirements are achieved. In addition, the invitation to the shortlisted organisations specifically invites tenderers to propose innovative approaches and design solutions within the contexts of functionality and value-for-money.

The brief outlines Council’s requirements for SPA under key headings as summarised below:

1. Introduction

Purpose and ownership of the brief

2. Project Purpose

Council’s project vision, key objectives and success criteria

3. Appraisal

Background information on the Shire, the Council and the project

Summary of the feasibility studies completed, key business case assumptions and service requirements

Summary of Council’s strategy for development in Rosebud, including the Urban Design Framework

Summary of the State Government’s planning position and available Town Planning approval processes

Schedule of reference documents (copies of which are also provided to tenderers)

4. Definition

The site extent and overview of any key opportunities and constraints, including the existing Memorial Hall

The precinct masterplan extent, including key locations of interest

An outline scope of works based on the endorsed functional area schedule contained within the SGL Feasibility Study (Business Case)

Council’s key functional requirements under various headings including:

o Safety

o Sustainable design

o Finishes and material selection

o Building services

o Building structure

o Civil infrastructure, parking and landscaping

o Utilities and site services

Requirements for Statutory approvals and compliance with Standards

5. Precedent

Summary of precedent projects which should be referred to in developing the design, including positive and negative examples

6. Design

Processes for managing and ensuring design quality

Process for design approvals

7. Program

Attachment 1

Davis Langdon, an AECOM company Southern Peninsula Aquatic

Revision 3 – 23-May-2014 Prepared for – Mornington Peninsula Shire Council – ABN: N/A

2

Key project milestones

8. Cost

Summary of Council’s project budget and any exclusions

Requirements for input into grant funding applications

9. Management

Council’s project Governance Structure

10. People

Summary of the project team, including Council departments and external consultants

11. Communications

Summary of Council’s communications strategy

12. Procurement

Summary of Council’s intended procurement strategy

13. Risk

Summary of the project risk management strategy

Attachment 1

Davis Langdon, an AECOM company Southern Peninsula Aquatic

Revision 3 – 23-May-2014 Prepared for – Mornington Peninsula Shire Council – ABN: N/A

3

3.0 Design and Business Case Enhancements Davis Langdon has been involved with and responsible for a large number of successful community aquatic and recreation projects, and strongly endorses Council’s vision and objectives for SPA.

Davis Langdon has completed a detailed review of all project documentation (including the SGL Feasibility Studies and proposed component area schedule). Drawing on its experience with other similar projects, Davis Langdon believes that there are certain trends in contemporary aquatic centre design and operational models that are relevant to and should be considered for the SPA project, subject to these being supported by a business case. Those potential enhancements are outlined below.

3.1 Waterplay / Waterslides Through our recent project experience and observation of current aquatic centre trends we have noted that the inclusion of aquaplay (and in particular waterslides) is now considered as a ‘must have’ by many Councils for their aquatics projects.

To maximise the value of this significant additional investment, we have noted that these installations are most successful when they are accessible year-round internally from within the pool hall, although the waterslides themselves can be located external to the building. Whilst aquaplay features consist of generally low height water spray equipment suitable for younger ages, waterslides provide activity for the teenage and youth market which otherwise can be difficult to cater for. Aquaplay and waterslide features are generally highly used and may become a year round draw card for aquatics facilities, often leading to extended stays (and spends) by patrons.

In particular we have noted Council’s stated aims to engage with youth through appropriate facilities and resources, and we believe these aims would be delivered on SPA by including an enhanced waterplay/waterslide component. Whilst we note that the current brief includes an allowance for a splash pad likely suitable for ages up to 7 years it may be worth considering enhancing the internal waterplay offer to include play equipment suitable for ages up to 10-12 years, with Waterslides providing play activity for ages 10-12 and above.

In summary the benefits of waterslides are:

Provide aquaplay activity for the youth / teenage and family markets

Can provide year round activity if accessible from within pool hall

Can act as a significant drawcard promoting increased and extended visitation

Can provide the most visually striking external feature with forms that are instantly recognisable and iconic

Meet current community expectations and contemporary design features that drive successful aquatic facilities

In summary the benefits of additional waterplay are:

Provides aquaplay activity for the younger market and families

Can provide year round activity if accessible from within pool hall

Can act as a significant drawcard promoting increased and extended visitation

Can provide a high activity internal/external attraction with vibrant colours and movement

Meet current community expectations and contemporary design features that drive successful aquatic facilities

SGL Group has been requested to consider whether the Business Case would support the addition of Waterslides and this report is included as Appendix A. In summary SGL note that the addition of Waterslides could offer significant benefits, and could be consistent with current trends for Local Government aquatic centres. The SGL Business Case review anticipates that the addition of Waterslides to the scope of SPA could drive increased attendance and deliver an additional operating surplus of $125,000 by year 3 rising to a $190,000 surplus by year 10.

On the basis of above Davis Langdon recommends that Council consider the addition of Waterslides and an increased internal waterplay allowance as an enhancement to the current SPA component brief.

Attachment 1

Davis Langdon, an AECOM company Southern Peninsula Aquatic

Revision 3 – 23-May-2014 Prepared for – Mornington Peninsula Shire Council – ABN: N/A

4

It should also be noted that it may not be possible for Council to add Waterslides to the SPA site at a later date if not planned for as part of the SPA project given the restricted foreshore site and need to make adequate allowances for spatial planning as well as plant and other services infrastructure. If Council determines that it is unable to currently fund the addition of Waterslides but may wish to add this facility at a later date, then Davis Langdon would recommend that the Waterslides be fully designed now as part of the SPA project and tendered as an option or second stage to the main construction contract.

3.2 Gymnasium The recent trend towards Council aquatic centres becoming significantly larger has been primarily driven by the addition of dry fitness spaces. This follows and supports the general growth in private and community health and fitness programs and increased awareness of the benefits of healthy lifestyles. It also responds to our aging population and the resultant expansion of community involvement in health, fitness and rehabilitation programs for the elderly.

Dry facilities including gymnasiums and program rooms attract a strong membership base, and can therefore offset the high operating costs of co-located aquatic facilities associated. In our experience, dry fitness demand is continuing to rise and many recently completed facilities are already planning gymnasium expansions due to demand exceeding Business Case projections, including Geelong Leisurelink after only 12 months of operation. At Ringwood Aquanation, Maroondah City Council has determined that the gymnasium’s 300 sqm mezzanine future expansion zone should be built now as part of the current construction project due to the expected high demand for gymnasium area from the local community.

Whilst we endorse the decision the project team took to expand SPA’s gymnasium floor area from 500 sqm to 700 sqm, we also believe it would be prudent to consider whether the Business Case would support a further expansion to 1000 sqm either as part of a future expansion provision, or as part of the current SPA project.

SGL Group has been requested to consider whether the Business Case would support the potential expansion of the gymnasium from 700 sqm to 1000 sqm and their response is included as Appendix B. In summary whilst SGL confirms that the Business Case does not currently support the increase in gymnasium floor area, they also support Davis Langdon’s observation that demand in other recently completed facilities has outstripped projections, and recommend that a future expansion zone of 300 sqm be catered for now as part of the SPA project.

On the basis of above Davis Langdon recommends that Council consider the addition of 300 sqm future gymnasium expansion zone as an enhancement to the current SPA component brief.

3.3 Kitchen / Café Our experience is that scale, service offering and positioning of cafés need to be carefully considered within aquatic centres to maximise their potential for efficient staffing and positive financial return. Increasingly the fitout of café areas is moving towards an upmarket feel and away from the traditional aquatic centre kiosk to meet community expectations. It is also important that cafes have the ability to serve to wet and dry areas, and this can present design and operational challenges in layout and heating/cooling systems.

Given the high services and fitout cost of kitchen areas, Davis Langdon believes that there may also be an opportunity for efficiencies to be achieved if the Memorial Hall kitchen is co-located adjacent to the SPA café/kitchen. This would be on the basis that the kitchen serving the Memorial Hall could continue to be operated independently by Hall users, as well as potentially by the SPA café/kitchen operator. The practicalities of this option would need to be further developed in consultation with users and operators.

SGL Group has been requested to consider whether the Business Case would support an increase to the kitchen / café and their response is included as Appendix B. In summary whilst SGL does not believe the current SPA brief supports an increased café offer, they also note that there may be opportunities to review co-location of Memorial Hall kitchen services if the Memorial Hall is to be demolished.

On this basis Davis Langdon recommends that the Principal Consultant be given the freedom to explore the practicalities and benefits of co-locating the SPA and Memorial Hall kitchens as part of their design competition responses, but that the current café / kitchen area provisions are not expanded.

Attachment 1

Davis Langdon, an AECOM company Southern Peninsula Aquatic

Revision 3 – 23-May-2014 Prepared for – Mornington Peninsula Shire Council – ABN: N/A

5

3.4 Outdoor Viewing Deck Davis Langdon note the significant potential for views of the Bay to be provided from the upper level of SPA, given that Bay views at ground level are obscured by foreshore sand dunes and vegetation. This could be achieved with the provision of a relatively inexpensive outdoor viewing deck at level 1 which is accessible by SPA users and the public including café patrons. Davis Langdon recommends that this provision be included in the current SPA component brief.

Attachment 1

Davis Langdon, an AECOM company Southern Peninsula Aquatic

Revision 3 – 23-May-2014 Prepared for – Mornington Peninsula Shire Council – ABN: N/A

6

4.0 Rosebud Memorial Hall The existing Memorial Hall currently occupies a corner of the foreshore site and was constructed in 1958. It has no specific strategic significance as a hall except for its capacity, being one of the largest halls in the Shire.

The Hall is used for a mixture of regular community activities and one off events. It is one of the Shire’s largest venues with a capacity in excess of 200 patrons. The main uses are amateur theatre, exercise / dance classes and bingo. The Memorial Hall comprises a large hall, a small hall, commercial standard kitchen, stage, green rooms, office and public toilets.

Davis Langdon has identified a number of potentially significant issues regarding integration of the existing Memorial Hall into the proposed new SPA facilities:

1. The Hall would require a major refurbishment to bring its finishes up to an acceptable quality, to upgrade and/or provide new building services to meet current code requirements, to provide improvements to meet fire protection and disabled accessibility regulations, to address any building fabric and/or structural issues and to deal with the removal of any hazardous materials that may be present.

2. The Hall finished floor level is 2.02m AHD which is below flood level. If the Hall is to be retained and integrated a level transition zone will need to be incorporated between it and the new facilities, and dispensation from current regulations may be required to allow this level to remain.

3. The Hall’s current location places it in a poor position in the context of the proposed new SPA facilities. It occupies the south eastern corner of the site which would otherwise be the primary entry point for SPA as it relates directly to Point Nepean Road and the Rosebud Commercial District within the Urban Design Framework. With the Hall retained in its current location the new SPA entry would be ‘tucked away’ between it and the bay trail bike path, and would result in a somewhat compromised entry and loss of potential flexibility.

4. Due to the limited available site footprint the new SPA facilities will occupy two levels. This may be present challenges with regards to integration of the single story Hall both aesthetically and functionally.

5. The increased demand on the site as a result of SPA will likely call for additional parking capacity on the foreshore as part of the development. Ideally the existing parking to the east of the Hall would be expanded to provide parking at one location, however this is not possible with the Hall retained at its current location

6. Aesthetically the architectural merit of the Hall is questionable and its appearance is dated. It may look out of place next to the new modern SPA facilities and difficult to successfully integrate it with SPA architecturally.

Taking these considerations into account, there may be an opportunity for Council to consider demolition of the existing Memorial Hall, with the Hall’s functions to be fully retained with the provision of new floor area at the lower level of the SPA project. This could enable:

The creation of a bold new site entry and identity for the new facilities with excellent visibility to Point Nepean Road and the Rosebud Commercial District;

The creation of a centralised, efficient and more attractive parking zone and new entry forecourt;

A more efficient overall site layout which maximises the development potential of the site;

Building forms and appearance to become properly integrated;

Enhanced functionality and service provision for Hall users, with new facilities which meet current codes, standards and performance requirements, and minimise the need for ongoing maintenance;

Efficiencies to be achieved with opportunities for:

o New flexible multiuse spaces which could be divisible with operable walls and therefore improve utilisation,

o Co-located service areas and shared amenities such as a large entry foyer and public toilets.

o Consolidation of Council services currently housed in or associated with the Hall, including booking, management, security, cleaning, maintenance and out-of-hours use.

Attachment 1

Davis Langdon, an AECOM company Southern Peninsula Aquatic

Revision 3 – 23-May-2014 Prepared for – Mornington Peninsula Shire Council – ABN: N/A

7

o Consolidation of current Hall external storage areas

Davis Langdon has met with current Hall users who were supportive of a new Hall option and proposed new floor area allocations and functions have been provisionally agreed.

Davis Langdon estimates that the cost of major refurbishment of the Hall is expected to be up in the order of $2M, depending on the scope and extent of integration. The cost of equivalent new facilities is expected to be in the order $3M (all excluding GST), subject to floor area and quality of fitout.

SGL Group have been requested to consider the potential benefits of demolishing the Memorial Hall and providing new facilities and their response is including as Appendix B. In summary SGL note benefits which are consistent with the comments provided by Davis Langdon above.

On the basis of the above considerations, Davis Langdon recommends that Council consider design responses from shortlisted tenderers which include demolition and replacement of the existing Memorial Hall with the current Hall functions to be retained and where possible enhanced.

Attachment 1

Davis Langdon, an AECOM company Southern Peninsula Aquatic

Revision 3 – 23-May-2014 Prepared for – Mornington Peninsula Shire Council – ABN: N/A

8

5.0 Financial Considerations Should Council adopt the project enhancements recommended within this report, the estimated additional capital costs for the SPA project would be as summarised below. Option 1 assumes retention and integration of the Memorial Hall following a major refurbishment, Option 2 assumes new Hall floor area with functions retained.

Item Description Option 1 Option 2

1 Memorial Hall major refurbishment $2,000,000 $0

2 New Hall facilities $0 $3,000,000

3 Waterslides (x 2), including additional floor area, plant and services

$3,000,000 $3,000,000

4 Additional internal waterplay $200,000 $200,000

SUB-TOTAL (Ex GST) $5,200,000 $6,200,000

Attachment 1

Davis Langdon, an AECOM company Southern Peninsula Aquatic

Revision 3 – 23-May-2014 Prepared for – Mornington Peninsula Shire Council – ABN: N/A

9

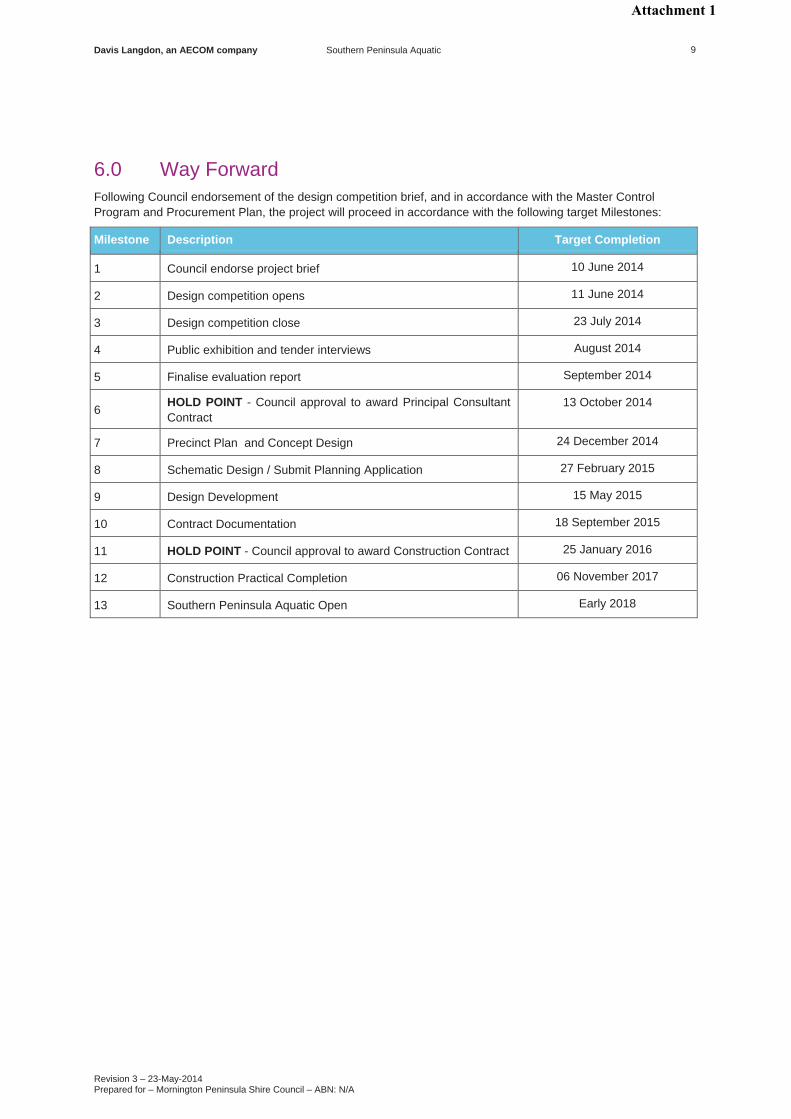

6.0 Way Forward Following Council endorsement of the design competition brief, and in accordance with the Master Control Program and Procurement Plan, the project will proceed in accordance with the following target Milestones:

Milestone Description Target Completion

1 Council endorse project brief 10 June 2014

2 Design competition opens 11 June 2014

3 Design competition close 23 July 2014

4 Public exhibition and tender interviews August 2014

5 Finalise evaluation report September 2014

6 HOLD POINT - Council approval to award Principal Consultant Contract

13 October 2014

7 Precinct Plan and Concept Design 24 December 2014

8 Schematic Design / Submit Planning Application 27 February 2015

9 Design Development 15 May 2015

10 Contract Documentation 18 September 2015

11 HOLD POINT - Council approval to award Construction Contract 25 January 2016

12 Construction Practical Completion 06 November 2017

13 Southern Peninsula Aquatic Open Early 2018

Attachment 1

Davis Langdon, an AECOM company Southern Peninsula Aquatic

Revision 3 – 23-May-2014 Prepared for – Mornington Peninsula Shire Council – ABN: N/A

Appendix A

SPA Waterslides Review and Business Plan

Attachment 1

Prepared by SGL Consulting Group Australia Pty Ltd

www.sglgroup.net

SPA Centre Waterslide Review and Business Plan May 2014

Attachment 1

SPA Centre Waterslide Review and Business Plan .docx (VIC 21.2014) - 5 May 2014 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

SGL Consulting Group Australia Pty Ltd Adelaide 2a Mellor St West Beach SA 5024 Phone: +61 (08) 8235 0925 Fax: +61 (08) 8353 1067 Email: [email protected] Brisbane PO Box 713 Mount Gravatt Queensland 4122 Mobile: +61 (0) 416 235 235 Email: [email protected] Melbourne Level 6, 60 Albert Road South Melbourne VIC 3205 Phone: +61 (03) 9698 7300 Fax: +61 (03) 9698 7301 Email: [email protected] Perth 19 Clayton Street East Fremantle WA 6158 Phone: +61 (0) 8 9319-8991 Mobile: +61 (0) 407 901 636 Email: [email protected] Sydney 1/273 Alfred St Nth North Sydney NSW 2060 Mobile: +61 (04) 17 536 198 Email: [email protected]

SGL also has offices in: • Auckland • Christchurch • Wellington

Attachment 1

SPA Centre Waterslide Review and Business Plan .docx (VIC 21.2014) - 5 May 2014 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

Table of Contents Executive Summary

1 SPA Centre Waterslides ...................................................................................... 11.1 Introduction ................................................................................................................ 11.2 Waterslide and Water Play Development Trends ................................................... 1

1.2.1 Early Waterslide Development ............................................................................... 11.2.2 Multiple Slides Off One Tower and Covered In Flumes ......................................... 21.2.3 The Waterpark Water Slide Phase ........................................................................ 21.2.4 Splash Pads and Water Play Equipment ............................................................... 21.2.5 The Adventure Water Slide Ride Phase ................................................................ 3

1.3 Example of Water Slide Ride Development at Council Aquatic Facilities ............ 31.4 Current Waterslide Product Review ......................................................................... 7

1.4.1 Body Ride Water Slides ....................................................................................... 101.5 Recommended Waterslides for SPA Rosebud ..................................................... 10

1.5.1 Body Ride Water Slides Component Brief and Cost Allowance .......................... 10

2 Waterslide Business and Cost Benefit Analysis ............................................ 122.1 Introduction .............................................................................................................. 122.2 Proposed Operating Model and Business Results ............................................... 12

2.2.1 Projected Option One Waterslide Revenue ......................................................... 122.2.2 Projected Option Two Waterslide Revenue ......................................................... 132.2.3 Waterslide Charging Option Comparisons ........................................................... 132.2.4 Waterslide Operational Expenditure Review ....................................................... 132.2.4.1 Waterslide Operational Expenditure Projections .............................................. 142.2.5 Projected Waterslide Operating Budget Year 3 ................................................... 142.2.6 Projected Waterslide Operating Budget Year 1 to 10 .......................................... 15

2.3 Projected Waterslide Capital Repayment Cost ..................................................... 152.3.1 Projected Waterslide Option One 10 Year Loan Repayment .............................. 172.3.2 Projected Waterslide Option Two 15 Year Loan Repayment .............................. 172.3.3 Projected Waterslide Option Three 20 Year Loan Repayment ............................ 182.3.4 Projected Waterslide Options Loan Repayment Comparisons at Year 10 .......... 18

2.4 Summary of Key Business and Loan Findings ..................................................... 18

Directory of Tables TABLE 1. SPA CENTRE WATERSLIDE 10-YEAR OPERATING PROJECTIONS .............................. IITABLE 2 PROJECTED LOAN OPTION COMPARISON NET ANNUAL RESULT ............................... IIITABLE 1.1 SAMPLE OF INDOOR AQUATIC WATERSLIDE/WATER PLAY AREAS .......................... 3TABLE 1.2 SPA CENTRE WATERSLIDE COMPONENT LIST AND INDICATIVE COST ................. 11TABLE 2.1 WATERSLIDE COMPONENT LIST AND INDICATIVE COST ......................................... 12TABLE 2.2 OPTION ONE CHARGE WATERSLIDE REVENUE PROJECTIONS .............................. 13TABLE 2.3 OPTION TWO CHARGE WATERSLIDE REVENUE PROJECTIONS .............................. 13TABLE 2.4 WATERSLIDE 10-YEAR OPERATING PROJECTIONS .................................................. 15TABLE 2.5 WATERSLIDE OPTION ONE 10-YEAR LOAN SCHEDULE ............................................ 16TABLE 2.6 WATERSLIDE OPTION TWO 15-YEAR LOAN SCHEDULE ........................................... 16TABLE 2.7 WATERSLIDE OPTION THREE 20-YEAR LOAN SCHEDULE ........................................ 16TABLE 2.8 WATERSLIDE OPTION ONE 10-YEAR LOAN TERM REPAYMENT COMPARISON .... 17TABLE 2.9 WATERSLIDE 15-YEAR LOAN TERM REPAYMENT COMPARISON ............................ 17TABLE 2.10 SPA CENTRE WATERSLIDE 20-YEAR LOAN TERM REPAYMENT COMPARISON .. 18TABLE 2.11 PROJECTED LOAN OPTION COMPARISON NET ANNUAL RESULT......................... 18

Attachment 1

SPA Centre Waterslide Review and Business Plan .docx (VIC 21.2014) - 5 May 2014 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

EXECUTIVE SUMMARY 1. INTRODUCTION This report has been developed as an addendum to the SPA Centre Base Case 10 Year Financial to test the viability of adding waterslides to the facility component mix at the proposed SPA Centre Rosebud. The business projections and cost benefit analysis are based on the projected user visits listed in the November 2013 SPA Centre Base Case 10 Year Financial Model. 2. WATERSLIDE DEVELOPMENT TRENDS In the past five years waterslides have become a high use feature of successful aquatic leisure centres. These facilities especially attract children, youth and families and have been attributed to attracting more regular use by these key user markets. In particular waterslides have been attributed to attracting back youth to aquatic facilities due to the adventure water challenge slides provide. Importantly they provide safe adventure water that can be designed with covered flumes and warm water to be used all year round. The report reviews the history of waterslide development and indicates that most centres built in the past five years in Victoria have waterslide components as base facilities. 3. RECOMMENDED SPA CENTRE WATERSLIDES The first SPA Centre Feasibility Study did not recommend waterslides as a key component as back in 2005 these features were only just starting to be added to indoor aquatic and leisure centres. As indicated in the past 5 years such facilities have been proven to be very successful in attracting more children, youth and families to these facilities if waterslides are provided. Recognising the projected facility being planned as a district facility with 80,000 plus population user catchment and the potential high use by campers, holiday makers and day visitors to Rosebud we recommend that waterslides be added to the base facility component brief and these:

• Include as a first stage a tower and two body slide flumes (one for body slides and one for body slides and inflatable slides).

• Ensure the tower and pool hall crash down zone has capacity to add a further two slides at a future date (future proof expanded business opportunity).

A capital cost allowance of $3 million should be used as a guide for product selection and installation based on current facility development trends and facility component scope. 4. PROPOSED OPERATING MODEL AND BUSINESS PROJECTIONS The current operating modes for waterslides include two different charging model options being:

• Option One: Direct hourly charge model

• Option two: peak hour charge model for all users at peak time.

The financial review completed in section 2.2 indicates both options are likely to raise between $318,850 (option 2) and $322,000 (option 1) in annual revenue so we have used the upper level as the revenue guide for financial modeling. The projected waterslide 10 year operating projections are:

Table 1. SPA Centre Waterslide 10-Year Operating Projections

Category Year 1 $

Year 2 $

Year 3 $

Year 4 $

Year 5 $

Year 6 $

Year 7 $

Year 8 $

Year 9 $

Year 10 $

Total 10 Years

$ Revenue 302,970 312,340 322,000 334,880 348,275 362,206 376,694 391,762 407,433 423,730 3,582,291 Expenditure 187,273 192,075 197,000 201,925 206,973 212,147 217,451 222,887 228,460 234,171 2,100,363 Surplus/(Loss) 115,697 120,265 125,000 132,955 141,302 150,059 159,243 168,875 178,973 189,559 1,481,928 Note: Assume CPI increase 2.5% plus visit growth/fee increases 1.5%

Attachment 1

SPA Centre Waterslide Review and Business Plan .docx (VIC 21.2014) - 5 May 2014 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

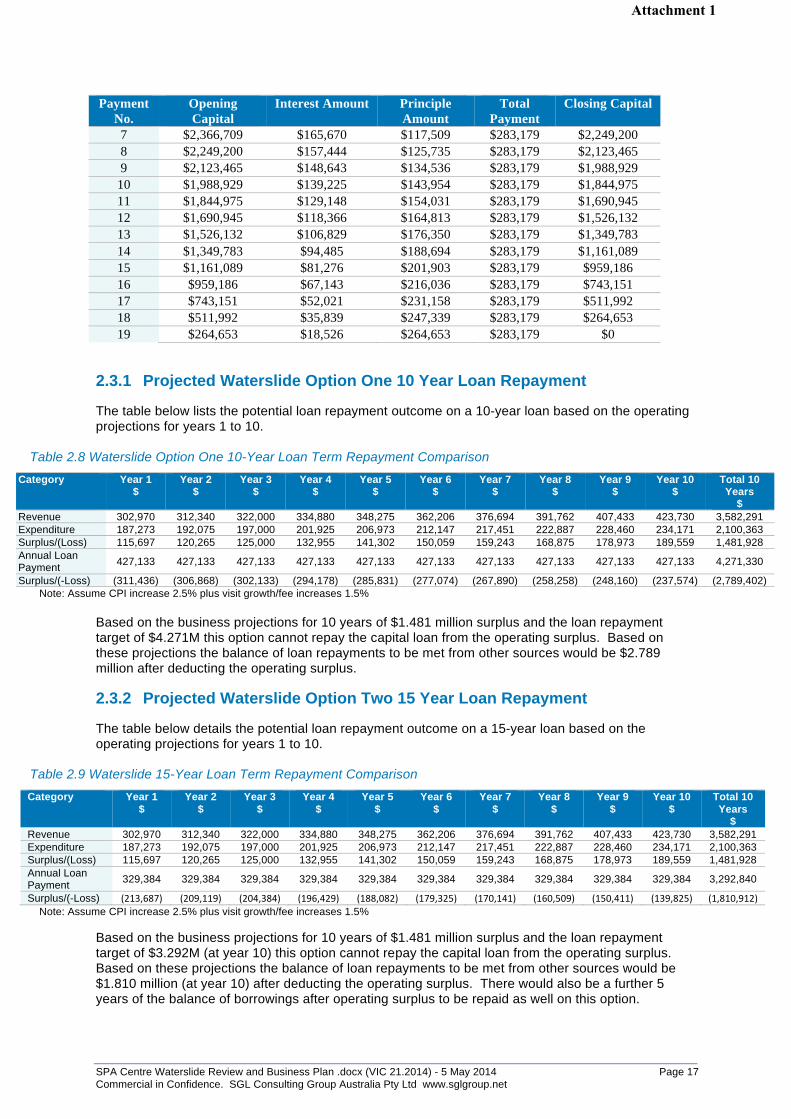

Based on the business projections the 10-year business case would see waterslide annual operating surpluses range from $115,697 in year one increasing to $189,559 by year 10. This would see a combined operating surplus of $1.481M over 10 years that could be used to assist with repaying loans to help fund the annual capital loan repayments. 5. WATERSLIDE CAPTIAL REPAYMENT REVIEW The net operating surplus/(loss) for the first 10 years of waterslide operations is predicted at a combined operating surplus of $1.481 million. Based on capital loan term options of 10 years, 15 years or 20 years term the following business result is projected by year 10, if all funds were borrowed for each of the loan terms.

Table 2 Projected Loan Option Comparison Net Annual Result

Category Year 1 $

Year 2 $

Year 3 $

Year 4 $

Year 5 $

Year 6 $

Year 7 $

Year 8 $

Year 9 $

Year 10 $

Total 10 Years

$ Option One 10 Year Loan Surplus/(Loss)

(311,436) (306,868) (302,133) (294,178) (285,831) (277,074) (267,890) (258,258) (248,160) (237,574) (2,789,402)

Option Two 15 Year Loan Surplus/(Loss)

Option Three 20 Year Loan Surplus/(Loss)

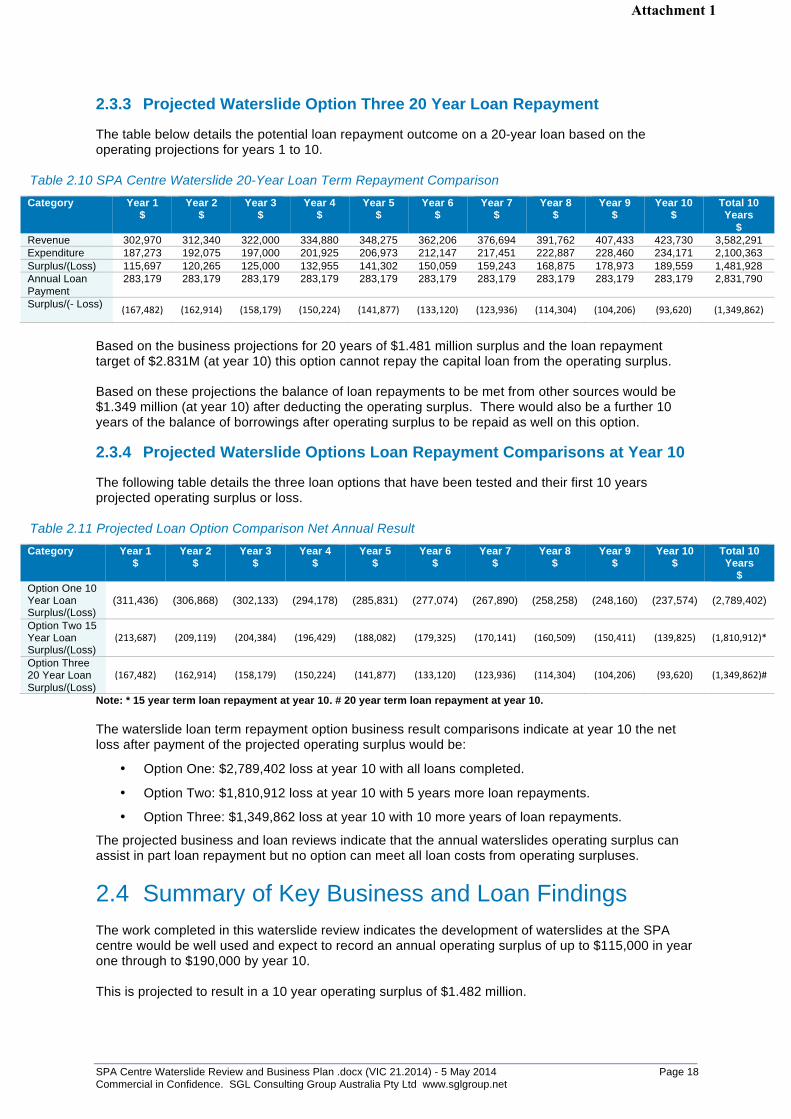

Note: * 15 year term loan repayment at year 10. # 20 year term loan repayment at year 10. If Council was to borrow the funds for waterslide development estimated to cost $3M then the waterslide projected annual operating surplus of $1.482 million could be used to part repay annual loan repayments. Based on the respective business projections and variable loan repayments the three loan options see at the 10 year mark a combined operating deficit after loan repayments of:

• Option One: $2,789,402 loss at year 10 with all loans completed.

• Option Two: $1,810,912 loss at year 10 with 5 years more loan repayments.

• Option Three: $1,349,862 loss at year 10 with 10 more years of loan repayments.

The projected business and loan review results indicate that the annual waterslides operating surplus can assist in part loan repayment but no one option can meet all loan costs from operating surpluses. 6. RECOMMENDED DEVELOPMENT The popularity of waterslides and their ability to attract high use is now well established in the aquatic leisure industry. There is a range of options for waterslide development with a large array of slides to choose from at varying capital cost. SGL recommend development of an enclosed tower and initially two body slides at the SPA Centre at an estimated capital cost of $3 million (final budget to be based on slide development chosen). It is also recommended that the tower and pool hall building be future proof designed to ensure further slides can be added to the tower in the future. Based on industry user trends and recognized charging systems SGL has completed detailed business planning for the waterslides. This review projects an annual operating surplus of $115,000 in year one to up to $190,000 by year 10 for the proposed SPA Centre waterslides. These results indicate over the 10-year review period that the waterslides could generate a combined 10-year operating surplus of $1,481,928.

Attachment 1

SPA Centre Waterslide Review and Business Plan .docx (VIC 21.2014) - 5 May 2014 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

If the $3 million capital cost was borrowed the operating surplus could be used to assist with part funding loan repayments but alternative funding would also be needed to meet the full capital cost. SGL believe that the development of waterslides at the SPA Centre would be a significant user attractor for children, youth and families and should be added to the component brief subject to Council funding capacity or seeking alternative funding support for such facilities.

Attachment 1

SPA Centre Waterslide Review and Business Plan .docx (VIC 21.2014) - 5 May 2014 Page 1 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

1.1 Introduction This report has been developed as an addendum to the SPA Centre Base Case 10 Year Financial to test the viability of adding waterslides to the facility component mix at the proposed SPA Centre Rosebud. The report has been developed in two sections being:

• Section One: Overview of waterslide development trends and viability.

• Section Two: Spa Centre recommended waterslide development and business projections and cost benefit analysis.

The business projections and cost benefit analysis are based on the projected user visits listed in the November 2013 SPA Centre financial model.

1.2 Waterslide and Water Play Development Trends The aquatics Industry has gone through a number of development phases and product and facility development trends with waterslides and water play equipment since the first facilities were developed around the 1970s and 1980s. The first stages started with a range of commercial developers building stand-alone waterslides and then some Councils installing waterslides and some limited play equipment. This section lists details on these facility development trends and identifies options for various facility types and associated costs and user attraction

1.2.1 Early Waterslide Development

The first waterslides were usually developed as open-air outdoor single slides made for individual body slide riders. The slide was either entered from a tower or from a raised in-ground mound. The rider was aided in their ride by running water down the slide, which was pumped to the top of the slide and propelled by gravity to a plunge pool below. Most slides in these days dropped into a large plunge pool at the bottom of the slide. The early slide designs saw the rider exit the slide above the waterline and drop into the plunge pool. Over the years with more knowledge of potential rider injury by the 1980s most slide plunge pools had the slide protruding into the water so the rider was slowed by the back flow of water as it fell from the slide into the plunge pool. In the 1970s and 1980s across Australia there was a significant development of single waterslides at a large number of local council aquatic centres. The majority of these slides were developed as outdoor and open flumed so their use was impacted by cold or wet weather conditions. The industry also saw a number of commercial operators develop water slides at privately owned sites (where there were no public swimming pools) particularly around country tourist towns.

1 SPA Centre Waterslides

Attachment 1

SPA Centre Waterslide Review and Business Plan .docx (VIC 21.2014) - 5 May 2014 Page 2 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

Due to the high numbers of people being attracted to this new thrill ride many commercial operators did financially very well out of such developments and this continued through to mid 1990s.

1.2.2 Multiple Slides Off One Tower and Covered In Flumes

The next stage of waterslide industry development saw the option to develop multiple slide rides of different size, height, speed and skill off the one tower. As new slide configurations and associated speed and adventure became important to users the covered flume was introduced to allow riders to move around the slide at high speed. This also protected the rider from cold and wet conditions and a number of operators added heated water into the slide flume to enable people to ride the slides longer. The covered in flume also allowed manufacturers to develop slides at much higher and greater change of angles, creating greater speed and constant change in direction. The covered in flumes also allowed development of thrill rides such as “The black hole” as well as introducing lighting and sound effects.

By the late 1980s many single slide operations had ceased, as users became bored with the one slide configuration. Many commercial operators sold out of their business or sold slides to Councils and community Aquatic Centres, as the aged infrastructure needed replacing or updating.

1.2.3 The Waterpark Water Slide Phase

The need to keep people amused for longer time whilst visiting aquatic facilities lead to the evolution of the small to medium size waterpark or theme leisure water area. In the 1980s there was a significant increase of new facilities (particularly in the USA and Europe where there were large populations to be attracted to such facilities). Some aquatic centres also started to add leisure water as part of their traditional swimming pool areas and this also saw the development of the first indoor waterslides in Melbourne and Sydney. Australia for example due to its broad population spread only saw limited development of Waterparks. Wet n Wild at the Gold Coast and Water Theme Parks in Perth and Adelaide (long summers and hot weather) were developed in the 1980s. There were also smaller waterparks developed along the east coast at many holiday destinations. In the 1980s a range of theme parks such Sea World (Gold Coast), Wonderland (Sydney) and Dream World (Gold Coast) added waterpark components to traditionally dry parks to attract people to stay longer in their parks. In late 2013 Australia’s second major outdoor water park Wet and Wild Sydney was developed by the Village Roadshow Corporation on community land in Western Sydney. This park has attracted over 600,000 visits in 3 months with more than 100,000 people taking out 12-month park memberships.

1.2.4 Splash Pads and Water Play Equipment

In the late 1980s and 1990s there was significant demand to take static water areas into a more water playground theme. This saw a number of wave pools built as part of multi-purpose leisure centres as well as the introduction of multi use areas such as:

• Rapid Rivers

• Waterslides

• Water play equipment

• Food and beverage services pool side

Most facilities developed in the 1990s saw designers build free form pools and then add somewhat ad hoc basic play equipment and sprays.

Attachment 1

SPA Centre Waterslide Review and Business Plan .docx (VIC 21.2014) - 5 May 2014 Page 3 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

This approach has now been superseded by play and water splash parks that maximise play and fun and then add water zones appropriate to the size and scale of development and user.

1.2.5 The Adventure Water Slide Ride Phase

In the 1980s and 1990s there was a major increase in different ranges of waterslide products and design. The open and closed individual rider slides were improved for speed and thrill experience. Over time, a number of new products were also developed with more efficient and different size rider flumes that allowed different ride experiences such as:

• Inflatables,

• Multi-person tubes and

• Multi-person rafts.

To enable higher speeds to run these rides tower height was increased from the standard 8 to 10 metres to 12 metres and some even went up to 15 metres high. The waterslide flumes were also increased in diameter from 800 mm (individual rider width) to 1200 mm for inflatables and 1320 mm for multi-person inflatables and rafts. The extra width and height in the slides allowed designers to introduce high speed and high-banked radius turns therefore increasing variation in waterslide rides and experiences.

In the 1990s and through the 2000s these changes lead to truly a diverse mix of thrill and adventure rides where people can ride together in rafts and inflatables. Today many derivatives of the original waterslide concept have evolved to now include:

• Whirlpool Tubs: Riders in rafts/inflatables can go from slides to swirling whirlpools and then back into slides.

• Wave/Flow Riders: Riders can use small surfboards to ride a shallow wave and then be shot out into a slide to a lazy river.

• Speed slides: Multiple steep slides side by side that allow riders to race each other.

• Adventure Rides: Specialist rides such as

Master Blaster: Rollercoaster inflatable ride that uses water and conveyor belts to speed participants up and down a wet rollercoaster.

Tornado: Inflatable ride that sees multi-person inflatable drop 90 degrees into a closed waterslide and then come out into a large cylinder that shoots riders around 240 degrees and then out to a plunge pool.

Speed Bowl: Individual and inflatable waterslide that sees riders emerge from a waterslide into a large speed bowl. Riders slide around the bowl and eventually drop through a central hole to a plunge pool.

Cyclone Racer: Covered in multi flume that twists around each other and allow riders to race each other through 240 degrees use of the flume (in a black hole so riders do not know where they are).

With the advent of now more than 1,000 waterparks throughout the world there are new ride products being developed all the time. As parks compete against each other for business there is ongoing retrofitting of rides and slides happening every major aquatic season.

1.3 Example of Water Slide Ride Development at Council Aquatic Facilities

Table 1.1 on the next page provides information on a range of aquatic leisure facilities with waterslides developed over the past 2 to 6 years.

Attachment 1

SPA Centre Waterslide Review and Business Plan .docx (VIC 21.2014) - 5 May 2014 Page 4 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

Table 1.1 Sample of Indoor Aquatic Waterslide/Water Play Areas

Facility/Location Facility Features Geelong LeisureLink Waurn Ponds Geelong Vic Australia

Built 3 years ago the $31M replacement aquatic facility has been well received. Key features include: • Has now in-excess of 900,000 annual visits and more than 10,000 members across

health and fitness, LTS and multi-visit passes. • Gym – state-of-the-art gym with extensive floor space and a wide range of cardio and

strength equipment. • Group exercise rooms – three areas that house Les Mills, freestyle, cycle and mind-body

classes. • Wellness centre – home to Corio Bay Health Group. • Café – featuring a large seated area overlooking water areas. • Change rooms – separate wet and dry areas plus family and unisex accessible rooms. • Main pool - an 8-lane 50m pool with ramp access which can be divided into two 25m

pools. • Program pool – multi use warm water pool with ramp access. • Learners’ pool – designed for Learn to swim classes and recreation. • Toddlers’ pool • Spa and sauna The attached indoor waterpark (tension membrane fabric) includes: • Cannon Ball Slide – a high-energy tube ride with an exhilarating drop, giant bowl spins

and an exciting transition into the slide pool. • The Black Hole – a fully enclosed slide that shoots you into a spiral of pitch black tubes

where you twist, turn and drop until the final splashdown. • Adventure Playground – includes slides, water cannons, spinning water wheel and a large

overhead tipping bucket allowing kids to splash, climb and be entertained for hours. • Splash Pad - featuring fountains and water spray equipment where children can play

safely on rubber mat flooring in zero depth water. The centre is now recording a much higher spend per visit ($6 to $7) due to the new waterslides and water play areas plus major health club. Management indicates these facilities have also contributed to major increases in food and beverage sales and retail sales as people are staying at the centre longer.

Casey RACE – Cranbourne Vic Aust.

Developed and owned by the City of Casey the Casey RACE incorporates: • Indoor $40M centre open 3 years • Indoor 51.5m pool with moveable boom • Separate warm water pool and learn to swim pools • Large spa and sauna area • 900mm² gym and 500m² dray activities rooms • $9M indoor leisure area that includes water slides, water play equipment and integrated

leisure pools • School change and group entry • Well located café and retail services. • Crèche and youth room The centre services a population of 60,000 people and attracted 580,000 visits in year 1 and 750,000 visits in year 2. Peak price charge covers use of all waterslide and water play features and this is set at an extra fee on normal entry charges of $1.00 for children and $1.50 for adults per visit. Centre peak times are set at 4 pm to 9 pm weekdays and all day Saturday and Sunday and public holidays. The extra charge guarantees that all waterslides and water play features are always available to use at no extra cost (except for the peak surcharge). All casual users of the facilities at peak time pay this extra charge. Management estimates 75% of casual paying customers visit the centre in peak times and this saw an estimated return of $350,000 to $400,000 in year one in extra revenue using the two time zone entry fee. They now estimate this fee raises more than $500,000 in entry fees a year.

Attachment 1

SPA Centre Waterslide Review and Business Plan .docx (VIC 21.2014) - 5 May 2014 Page 5 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

Facility/Location Facility Features

Glen Eira Sports and Aquatic Centre is located in East Bentleigh, Victoria, Australia GESAC is one of the two latest major indoor aquatic leisure facilities built at a cost of $45m in Melbourne and includes indoor and outdoor aquatic facilities plus indoor health and fitness and indoor sport court facilities. The centre has been open 2 years and has achieved more than 10,000 members and most programs are at capacity. The centre was developed at an outdoor pool site (East Bentleigh Swimming Pool) and already has had to add extra car parking and service areas due to high use. A feature of the centre is its leisure water with water play zone, interactive water jets and slides and indoor warm water program pools. They charge for these in peak use times using the extra charge model and estimate to raise between $500,000 and $600,000 annually from this activity area

WaterMarc – Greensborough Vic Australia

WaterMarc is the latest community aquatic leisure centre built in Melbourne at a capital cost of $45M and is part of a regional shopping centre redevelopment in Greensborough in the City of Banyule. It is positioned as the Northern Metropolitan Regional Aquatic Leisure Centre and has a mix of competition, recreation, leisure, health and fitness, wellness and social facilities. Annual attendances are estimated at around 1M visits year one and this is increasing. The centre has very good examples of well designed warm water program pools, health and fitness centre, wellness and indoor adventure water play and water slides The centre is well serviced by underground car parking and lifts. It also presents a very good example of self-service food and beverage areas linked to wet/dry lounges. They charge an hourly fee for use of the waterslides being $6 for unlimited rides and estimate annual waterslide revenue at $320,000 year 1 and $360,000 year 2.

Attachment 1

SPA Centre Waterslide Review and Business Plan .docx (VIC 21.2014) - 5 May 2014 Page 6 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

Facility/Location Facility Features Caroline Bay Trust Aoraki Aquatic Leisure Centre Timaru

Caroline Bay Trust Aoraki Centre is an indoor heated aquatic centre in Timaru featuring: • Main Pool, 25m x 25m - 1.4m to 3.4m deep, 27.8°C (10 lanes). • Program Pool, 17m x 12m - 1.2m x 1.8m deep, 32°C. Variable depth pool. Includes

wheelchair access and hydrotherapy area. • Leisure Pool with Splash Deck and Beach Access, 32°C. • Toddlers Pool, 33°C. • Outdoor 50m Pool (8 lanes). Seasonal pool closed in winter. • Chillax Area - Steam, Sauna and Spa, 38°C. • Children’s Water Playground with waterslides, water jets and buckets. • Rapid River • Bombing Tower (3m high) - subject to pool space availability • Springboard (1m high) - subject to pool space availability • Hoist and ramp access to some pools • Private family change rooms and disabled change facilities • Large modern change rooms • Lift access to gym The centre attracted 400,000 visits in year 1. They charge per rider by the hour and estimate waterslide revenue at around $250,000.

Todd Energy Aquatic Centre – New Plymouth North Island New Zealand

The Todd Energy Aquatic Centre is an indoor and outdoor swimming pool and complex centrally located in New Plymouth adjacent to the Coastal Walkway, The centre was redeveloped and now includes the following indoor water areas: • Main pool: Wave machine, water features, eight lanes, tarzan rope and inflatable toys.

Temperature 28 degrees. Depth 0.0 - 2.1m, length 25m. • Spa pool: Temperature 37 degrees. • Tots pool: Bubbles feature and slide. Temperature 32 degrees. Depth 0.3-0.5m • Hydroslides: Two slides (one turboslide and one family slide). Entry and exit is

within the indoor complex being. o Turbo slide: Users must be over eight years of age and be 120

centimetres or taller and not weigh more than 105 kilograms. o Family slide: Children five to seven must ride with a caregiver over the

age of 16. Children over the age of eight can ride the family slide unaccompanied.

• Outdoor main pool: Seven lanes. Length 50m. Depth 1.1–1.4m. Open Labour Weekend until mid April.

• Outdoor learners pool: Depth 0.8m. • Outdoor tots pool: Depth 0.3m. • Dive pool: Depth 3.9m. Two diving boards 1m and 3m high.

The centre attracts around 600,000 annual visits and they charge waterslide use by the hour and estimate annual income at around $300,000.

Attachment 1

SPA Centre Waterslide Review and Business Plan .docx (VIC 21.2014) - 5 May 2014 Page 7 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

A review of the a range of latest built facilities indicates they all have significant leisure water features and their business results clearly shows that the inclusion of waterslides and water play facilities are working well and directly contributing to:

• Increased visitations with larger numbers of people attending with families and friends. • Keep people at the centres longer due to the entertainment and social facilities offered. • Increasing numbers of people purchasing food and beverage and retail services, as they are

staying longer and looking to use such offers. • Allowing higher entry fees to be charged. • Increasing the annual fees per visit from those seen at a traditional aquatic leisure centre. • Generating more revenue to help fund the increased operating costs of adding water play and

waterslides to such facilities. • Allowing facilities to market themselves to a broader interest market (children and families)

than just the health and fitness and lap swimming user markets.

1.4 Current Waterslide Product Review There are now a number of waterslide manufacturers worldwide and a very broad range of waterslide products available to choose from. They range from:

• Standard body slides for one rider

• Inflatable slides for one rider

• Larger flume slides for 2 to 4 riders using inflatables.

The larger flume rides take more riders per slide using inflatables and are more of a stand alone feature adventure ride whilst the traditional one person body slide is less of a major feature but can usually take more riders per hour. Examples of major adventure rides (what the industry calls signature rides) currently on the market include:

• The Master Blaster: Gravity defying ride using jetted water an inner tubes and can be customised for sites and budgets.

• Boomerango: Inner tube ride with vertical drops and high speed action. Requires modification to provide shelter for all year use.

• The Anaconda: Tube/raft ride for 3/4/6 users with enclosed dark ride. • Aqualoop: Trap door entry fast body ride slide reaching speeds of up to 60 kilometres per

hour and 2.5g. • Aquadrop: Multiple slides without the loop and two slides so riders can complete against

each other. • Superbowl: Inner tube ride starting in a waterslide and then entering a bowl and then splash

down to a flume exit. • Spacebowl: Single person body slide ride similar to the super bowl. This ride is what is at

LeisureLink, Casey RACE etc. • Large Enclosed Body Slides: Custom fitted water slides that can deliver a range of

experiences and can be sized for body slide or inner tubes.

Some examples of what some of these types of waterslides look like from a range of different manufacturers are listed in the following photos on the next two pages.

Attachment 1

SPA Centre Waterslide Review and Business Plan .docx (VIC 21.2014) - 5 May 2014 Page 8 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

Attachment 1

SPA Centre Waterslide Review and Business Plan .docx (VIC 21.2014) - 5 May 2014 Page 9 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

These slides are expensive and range from $1M to $2M plus the tower. They are usually better suited to regional or major aquatic leisure centres that attract more than 800,000 annual visits. They do require staffing to control riders especially at the top of the tower where riders have to enter the holding area and get into/onto inflatables. Pool staff need to assist with ensuring all riders are set to enter the slide and that the slide is clear from the last riders before sending the next group off.

Attachment 1

SPA Centre Waterslide Review and Business Plan .docx (VIC 21.2014) - 5 May 2014 Page 10 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

These larger rides also may have a pool exit due to the large inflatable and this means more staffing is needed at the ride exit to clear the water before the next riders are released at the top of the slide. This process of loading and unloading riders from inflatables does have an impact on number of riders per hour. Due to this process the total rider capacity per hour for larger adventure riders is usually less than single body slide rides where people can enter and clear the slides faster. Subject to the waterslide ride chosen rider capacity per hour can range from 200 to 400 riders per hour. This can impact on rider value as well as slow loading rides may see large numbers of people having to queue for these types of rides.

1.4.1 Body Ride Water Slides

Traditionally body ride waterslides are the most common waterslides as they have fast throughput of riders and can take up a smaller development footprint and can use exit flumes at concourse level to quickly clear the slide for the next rider. Again subject to the height of entry to the slide and length of slide hourly through put can much more than that of adventure or signature rides and can range from 400 to 600 riders per hour. Industry trends indicate that it is essential that a number of body slides be developed off one tower to ensure ride options and keep people interested with different ride experiences. These slides work best at sub-regional, district or local facilities with lower user numbers and the key to success is ensuring that multiple rides are offered to ensure high throughput and variety of ride experience. Subject to ride type chosen these slides also require less staffing to control riders and this can impact on the operational viability of such rides at lower throughput centres. Most waterslides require staff at the entry point to control when riders enter the slide but when using exit flumes staff at the bottom of the slide can be minimal.

1.5 Recommended Waterslides for SPA Rosebud The Spa Centre Rosebud has been planned as a district facility catering for users in the main catchment zone from Portsea in the south to Safety Beach in the north. Feasibility business modeling indicates the centre has been planned to attract between 430,000 and 510,000 annual visits. The site has some unknowns that are expected to positively increase the predicted user catchment at distinct times, as it is also well located to attract (over summer vacation periods and weekends) the large number of holiday campers and day visitors, that come to the Southern Peninsula area. The provision of waterslides at the SPA Centre would therefore be seen as a catalyst to attracting greater annual family and children and youth visits than projected. In our industry experience we feel the centre user throughput would best be serviced by a range of lower cost, higher use body slides rather than developing a higher cost major adventure or signature ride and body slides at this site. Regional locations such as Frankston (2 major signature water slide rides) and Greensborough (2 major signature waterslide rides) have invested more than $4M in major rides as they have been developed for 1 million plus visits and therefore can justify such large capital investment whilst also having higher usage and income to cover the large staffing cost to supervise and control such rides.

1.5.1 Body Ride Water Slides Component Brief and Cost Allowance

Based on these trends and suitability factors it is recommended that the following waterslide component brief be further considered. Please note the projected business model and cost benefit analysis of this facility component is listed in section two of this report.

Attachment 1

SPA Centre Waterslide Review and Business Plan .docx (VIC 21.2014) - 5 May 2014 Page 11 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

Table 1.2 SPA Centre Waterslide Component List and Indicative Cost

Component Details Indicative Capital Cost Allowance Covered in Waterslide Tower

• Covered in access tower built off side of pool hall with doorway access to main pool hall.

• Main waterslide exit platform set at 12.5m high with capacity for up to 4 slides to exit from this platform.

• Cover height 15m to top of tower. • Can be a propriety item supplied by

waterslide manufacturer or designed in association with them

• Allow $600,000 for tower and connection of services etc.

Two Body Slide Fully Enclosed Flumes (Slide 1 800mm for body sliding and slide 2 1322mm to allow for inflatable ride option plus body slide).

• Flume one to be a 800mm wide flume tube fully enclosed water slide 150m-length 11approx.

• Flume two to be an 1322mm flume tube fully enclosed waterslide 150m length 11approx.

• Allow $500,000 for flume one. • Allow $600,000 for flume two. • Total Cost $1,100,000

Allow for Future More Waterslides to be Developed off Tower

• Allow for future weight of up to two more waterslides exiting from the 12.5m platform

• Covered in tower capital cost

Extra Pool Hall Concourse • Allow for clear waterslide flume exit zone at pool concourse level.

• Area allowance is 15m x 15m = 225m2

• Allow for glass low-level structure to cover over pool concourse area where flumes exit.

• 225m2 x $2,500m2 = $562,500 Plant and Equipment • Waterslide plant and equipment • Allow $300,000 Fees and Contingency • Allow for fees 10% and contingency of

say 7% (as it is already a designed propriety item).

• Total indicative capital cost $2,562,500

• 17% fees and contingency = $435,625

• Total indicative project cost is $2,998,125 say $3 million

The pictures below highlight the type of enclosed flume and tower proposed for the SPA Centre.

Enclosed Body Slide Flumes Located Outside and Off Tower

Options for Slide Entry at Top of Tower Platform for Single or Double Start

Attachment 1

SPA Centre Waterslide Review and Business Plan .docx (VIC 21.2014) - 5 May 2014 Page 12 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

2.1 Introduction Waterslides were not included in the original SPA Centre project component brief when it was originally developed back in 2005, as at that time they were relatively new to Local Government community aquatic facilities. Over the past 5 years such facilities have become very popular and are now being included in most new facilities. In particular these facilities are attracting back youth and families to community aquatic facilities as they add new entertainment, adventure and thrill activities. Section one of this report summaries the history of development of waterslides at such facilities and recommends multiple body ride slides that have capacity of one slide to be able to take multiple people inflatable rides. The estimated capital allowance for the proposed waterslides has been set at $3 million. This section looks at the projected business impact of the proposed new facility components and then considers the cost benefit analysis of this extra facility feature based on capital funding from loans and repayment being met from operating profits.

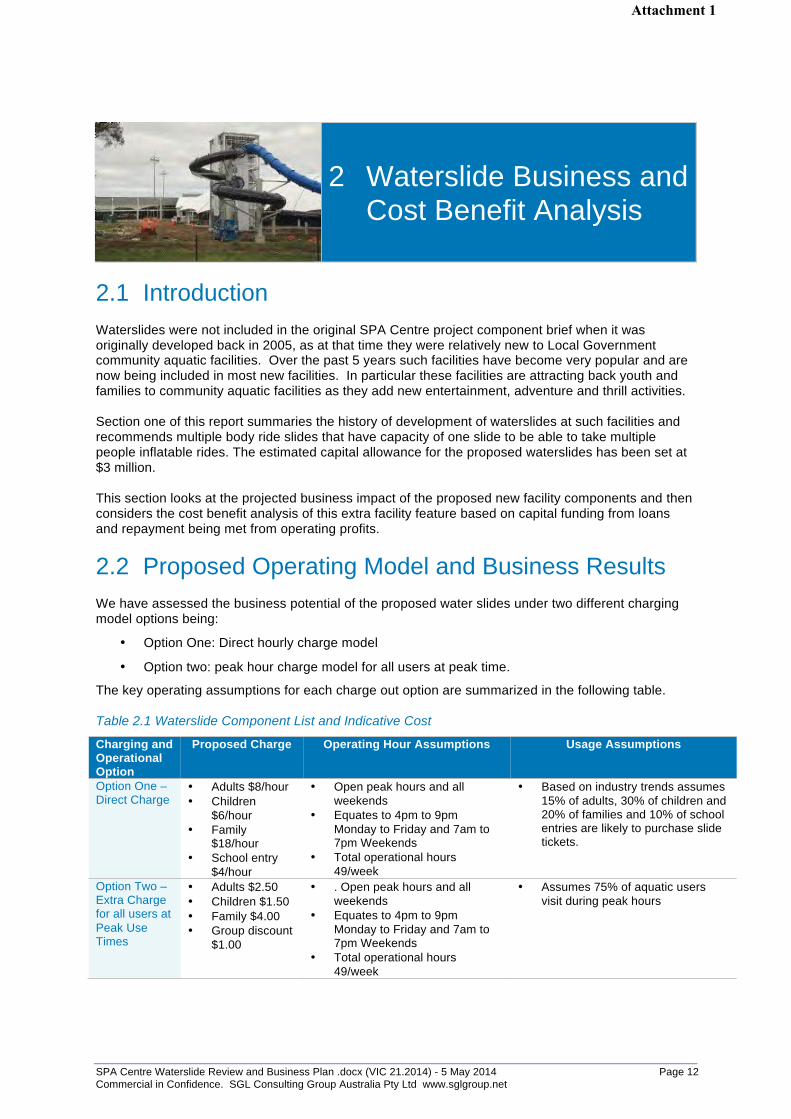

2.2 Proposed Operating Model and Business Results We have assessed the business potential of the proposed water slides under two different charging model options being:

• Option One: Direct hourly charge model

• Option two: peak hour charge model for all users at peak time.

The key operating assumptions for each charge out option are summarized in the following table. Table 2.1 Waterslide Component List and Indicative Cost

Charging and Operational Option

Proposed Charge Operating Hour Assumptions Usage Assumptions

Option One – Direct Charge

• Adults $8/hour • Children

$6/hour • Family

$18/hour • School entry

$4/hour

• Open peak hours and all weekends

• Equates to 4pm to 9pm Monday to Friday and 7am to 7pm Weekends

• Total operational hours 49/week

• Based on industry trends assumes 15% of adults, 30% of children and 20% of families and 10% of school entries are likely to purchase slide tickets.

Option Two – Extra Charge for all users at Peak Use Times

• Adults $2.50 • Children $1.50 • Family $4.00 • Group discount

$1.00

• . Open peak hours and all weekends

• Equates to 4pm to 9pm Monday to Friday and 7am to 7pm Weekends

• Total operational hours 49/week

• Assumes 75% of aquatic users visit during peak hours

2 Waterslide Business and Cost Benefit Analysis

Attachment 1

SPA Centre Waterslide Review and Business Plan .docx (VIC 21.2014) - 5 May 2014 Page 13 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

2.2.1 Projected Option One Waterslide Revenue

The following table details the potential waterslide revenue based on the option one charging model and using year three (consolidated business use year) usage projections. Table 2.2 Option One Charge Waterslide Revenue Projections

Entry Category

Proposed Charge

Total Annual

Projected Visits Year 3

Assumed % of Visits Who will

Purchase Waterslide

Tickets

Number of Visits Purchasing

Waterslide Tickets

Projected Annual Waterslide Revenue

Year 3

Adults $8/hour 85,945 15% of adult 12,900 $103,200 Child $6/hour 63,811 30% of children 19,200 $115,200 Family $18/hour 28,000 20% of families 5,600 $100,800 School Entry

$4/hour 5,200 10% school entries

520 $2,800

Projected Annual Waterslide Revenue

$322,000

Based on the business assumptions and industry trends the option one charge model would be likely to raise $322,000 in waterslide revenue in year 3.

2.2.2 Projected Option Two Waterslide Revenue

The following table details the potential waterslide revenue based on the option two charging model and using year three (consolidated business use year) usage projections. Table 2.3 Option Two Charge Waterslide Revenue Projections

Entry Category

Proposed Extra Entry

Charge

Total Annual Projected

Visits Year 3

Assumed % of Visits Who Will

Visit at Peak Hour Times

Number of Visits Paying Peak Hour

Extra Entry Fee

Projected Annual Waterslide Revenue

Year 3 Adults $2.50 85,945 75% 63,700 $159,250 Child $1.50 63,811 75% 47,900 $71,850 Family $4.00 28,000 75% 21,000 $84,000 Groups $1.00 5,000 75% 3,750 $3,750 Projected Annual Waterslide Revenue

$318,850

Based on the business assumptions and industry trends the option two charging model would be likely to raise $318,850 in waterslide revenue in year 3.

2.2.3 Waterslide Charging Option Comparisons

The waterslide revenue for each option has been projected to be:

• Option One – Direct Charge: $322,000/year 3

• Option Two – Peak Hour Use Charge: $318,850/year 3

As can be concluded from the review based on all modeling assumption for the two different models annual waterslide revenue has been projected at between $318,000 and $322,000 so we have used $322,000 as the base revenue target for cost benefit analysis. If Council decides to go ahead with the waterslides then it can complete more detailed reviews of either charging model and does not have to adopt one at the moment due to them returning similar revenue projections.

Attachment 1

SPA Centre Waterslide Review and Business Plan .docx (VIC 21.2014) - 5 May 2014 Page 14 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

2.2.4 Waterslide Operational Expenditure Review

This section looks at the main operational costs to operate the waterslides. It covers staff supervision, energy costs, maintenance allowances and cost of user armbands (option one only). 1. Staffing Costs Both charging options indicate the likely operational hours for each option are 49 hours per week. Based on say using 50 hours per week and two staff employed at all times to supervise this area during operational hours the annual staff cost to operate the waterslides would be:

• 100 staff hours/week x $30.50/hour (includes wage rate of $25/hour and on-cost of $5.50 at 22.6% of wage rate) = $3,050/week.

• Waterslide weekly salaries of $3,050/week x 52 weeks = $158,600.

• Total annual waterslide salary costs say $160,000 year.

Please note we have assumed that any cleaning down of this area would be done by staff at low use times and have not allocated a specific cleaning cost to the activity area. 2. Energy Costs Waterslides are low users of energy with main service requirements being power to operate water pumps to slides when they are operational. The slides normally use existing filtered water from the pools (subject to final design and where plant room is located). Based on other similar centres we have estimated energy costs at:

• 50 hours operational time per week x $10/hour = $520/week

• $520/week x 52 weeks = $27,040/year

• Total annual waterslide energy costs say $27,000/year

3. Maintenance Allowances If propriety company waterslides are purchased then they will have 10 years warranty on parts and labour for main items. Reviews of similar complexes indicate the slides have minimal maintenance requirements so we have allowed for $10,000/year for any maintenance works. 4. Armbands for Option One Charge System If Council decides to use the option one charging system then there will be need to purchase arm bands for hourly users so pool attendants can control who has paid and not paid. These cost around $0.20/band but most centres get them at no cost as they negotiate for sponsors logos to be on the armband. We therefore have not made an allowance for these items in the waterslide operating budget.

2.2.4.1 Waterslide Operational Expenditure Projections

Based on the operational expenditure allowances in the previous section the annual operational costs to operate the waterslides for 50 hours a week is estimated to be:

• Annual salary costs $160,000/year

• Annual energy costs $27,000/year

• Annual Maintenance Costs $10,000

• Estimated Annual Waterslide Operating Costs $197,000

Attachment 1

SPA Centre Waterslide Review and Business Plan .docx (VIC 21.2014) - 5 May 2014 Page 15 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

2.2.5 Projected Waterslide Operating Budget Year 3

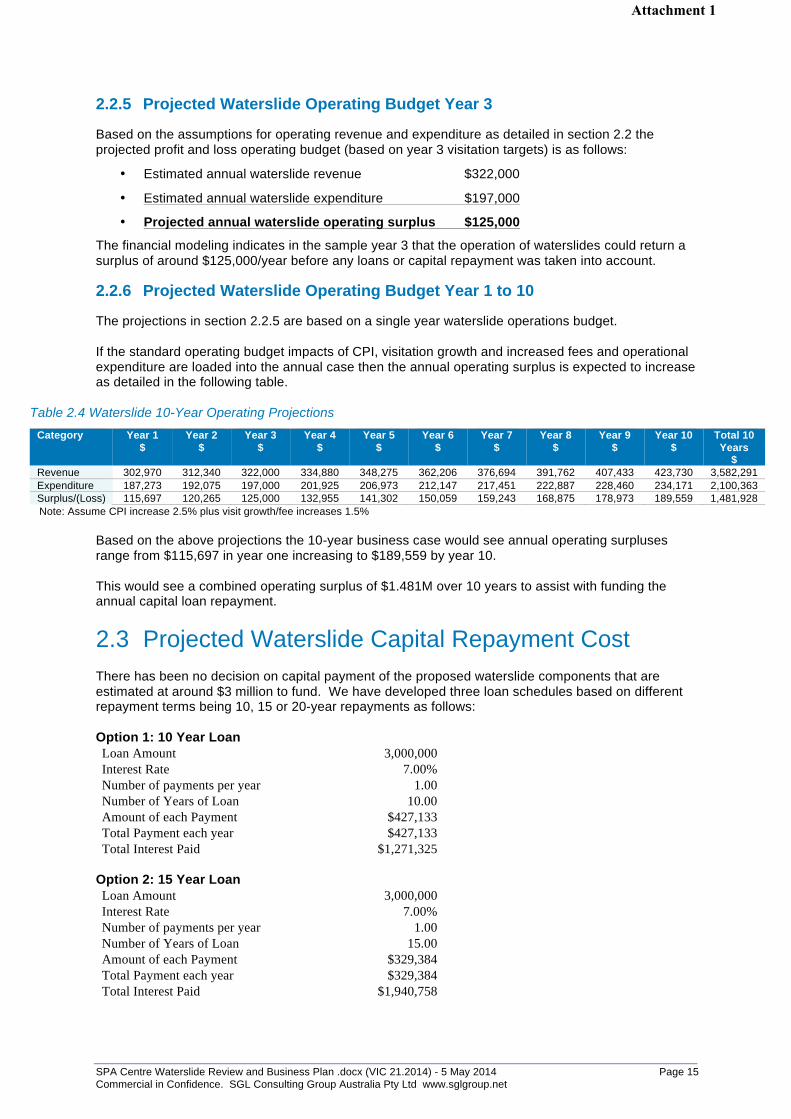

Based on the assumptions for operating revenue and expenditure as detailed in section 2.2 the projected profit and loss operating budget (based on year 3 visitation targets) is as follows:

• Estimated annual waterslide revenue $322,000

• Estimated annual waterslide expenditure $197,000

• Projected annual waterslide operating surplus $125,000

The financial modeling indicates in the sample year 3 that the operation of waterslides could return a surplus of around $125,000/year before any loans or capital repayment was taken into account.

2.2.6 Projected Waterslide Operating Budget Year 1 to 10

The projections in section 2.2.5 are based on a single year waterslide operations budget. If the standard operating budget impacts of CPI, visitation growth and increased fees and operational expenditure are loaded into the annual case then the annual operating surplus is expected to increase as detailed in the following table.

Table 2.4 Waterslide 10-Year Operating Projections

Category Year 1 $

Year 2 $

Year 3 $

Year 4 $

Year 5 $

Year 6 $

Year 7 $

Year 8 $

Year 9 $

Year 10 $

Total 10 Years

$ Revenue 302,970 312,340 322,000 334,880 348,275 362,206 376,694 391,762 407,433 423,730 3,582,291 Expenditure 187,273 192,075 197,000 201,925 206,973 212,147 217,451 222,887 228,460 234,171 2,100,363 Surplus/(Loss) 115,697 120,265 125,000 132,955 141,302 150,059 159,243 168,875 178,973 189,559 1,481,928 Note: Assume CPI increase 2.5% plus visit growth/fee increases 1.5%

Based on the above projections the 10-year business case would see annual operating surpluses range from $115,697 in year one increasing to $189,559 by year 10. This would see a combined operating surplus of $1.481M over 10 years to assist with funding the annual capital loan repayment.

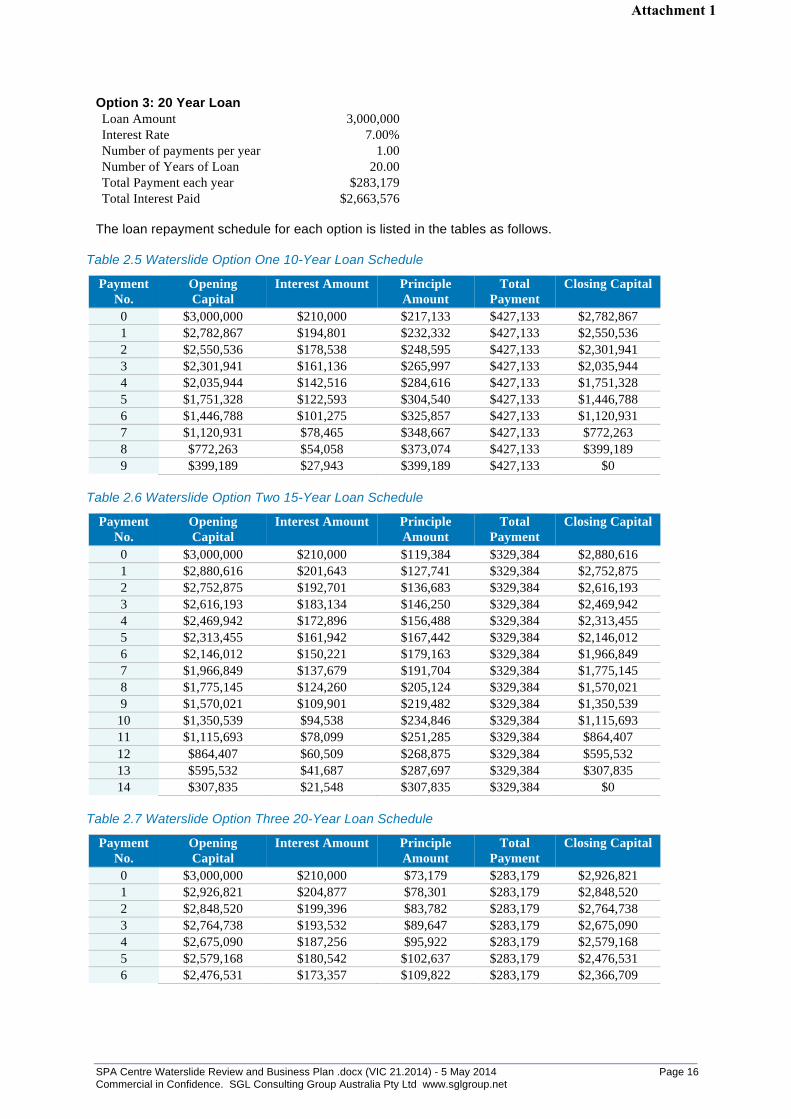

2.3 Projected Waterslide Capital Repayment Cost There has been no decision on capital payment of the proposed waterslide components that are estimated at around $3 million to fund. We have developed three loan schedules based on different repayment terms being 10, 15 or 20-year repayments as follows: Option 1: 10 Year Loan Loan Amount 3,000,000 Interest Rate 7.00% Number of payments per year 1.00 Number of Years of Loan 10.00 Amount of each Payment $427,133 Total Payment each year $427,133 Total Interest Paid $1,271,325

Option 2: 15 Year Loan Loan Amount 3,000,000 Interest Rate 7.00% Number of payments per year 1.00 Number of Years of Loan 15.00 Amount of each Payment $329,384 Total Payment each year $329,384 Total Interest Paid $1,940,758

Attachment 1

SPA Centre Waterslide Review and Business Plan .docx (VIC 21.2014) - 5 May 2014 Page 16 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

Option 3: 20 Year Loan Loan Amount 3,000,000 Interest Rate 7.00% Number of payments per year 1.00 Number of Years of Loan 20.00 Total Payment each year $283,179 Total Interest Paid $2,663,576

The loan repayment schedule for each option is listed in the tables as follows.

Table 2.5 Waterslide Option One 10-Year Loan Schedule

Payment No.

Opening Capital

Interest Amount Principle Amount

Total Payment

Closing Capital

0 $3,000,000 $210,000 $217,133 $427,133 $2,782,867 1 $2,782,867 $194,801 $232,332 $427,133 $2,550,536 2 $2,550,536 $178,538 $248,595 $427,133 $2,301,941 3 $2,301,941 $161,136 $265,997 $427,133 $2,035,944 4 $2,035,944 $142,516 $284,616 $427,133 $1,751,328 5 $1,751,328 $122,593 $304,540 $427,133 $1,446,788 6 $1,446,788 $101,275 $325,857 $427,133 $1,120,931 7 $1,120,931 $78,465 $348,667 $427,133 $772,263 8 $772,263 $54,058 $373,074 $427,133 $399,189 9 $399,189 $27,943 $399,189 $427,133 $0