Embed Size (px)

Citation preview

September 20, 2010

China: Portfolio Strategy

Social housing – A new growth focus

Social housing progress picking up noticeably Social housing is clearly a key new focal point in the Chinese govt’s

social welfare and investment agenda. Slow build progress and low

completion rates in the past were due to insufficient pressure from the

top, and lack of local govt economic incentive. We expect a noticeable

pick-up in pace as the central govt escalates political pressure and

introduces a stream of supportive policies to jump start investment.

We should see more progress in economic housing for sale (rather

than low-cost rentals) and in tier one/two cities. MOHURD announced

on Sept 19 that ‘10E’s 5.8m targeted units will all begin construction by

end-Sept, and 60%+ of targeted units will finish construction by yr-end.

Likely to help cushion investment demand risksThe market is concerned that commodity property tightening may

reduce GFA/investment and hurt the upstream suppliers. Our analysis

shows: (a) residential housing is only half of property GFA and other

segments are not exposed to the same policies; (b) social housing could

offset a good portion of potential commodity property slowdown. For

example, if commodity housing growth is 10pp slower in 2010E, GFA

impact could be offset by 20pp higher social housing completion rate.

Positive for upstream; low impact on property Building materials, steel, construction services and machinery are sectors

with social housing exposure (we are overweight machinery and building

materials). We do not expect social housing to seriously affect commodity

property developers, due to minimal overlap in product/target audience.

Buy-rated stocks with social housing exposure include Anhui Conch (H)

and Angang (H). Our new China policy momentum basket GSCNPLCY

also includes social housing beneficiaries.

Social housing targets, if met, may equal 30%-50% of commodity housing GFA

Source: MOHURD, Goldman Sachs Research estimates.

This is a redacted version of our original

“Social housing – A new growth focus”

report published September 20, 2010. For a

copy of the complete report please contact

your Goldman Sachs sales representative.

Helen Zhu

+852-2978-0048 [email protected] Goldman Sachs (Asia) L.L.C.

Timothy Moe, CFA

+852-2978-1328 [email protected] Goldman Sachs (Asia) L.L.C.

Christopher Eoyang

+81(3)6437-9888 [email protected] Goldman Sachs Japan Co., Ltd.

Ben Bei

+852-2978-1220 [email protected] Goldman Sachs (Asia) L.L.C.

The Goldman Sachs Group, Inc. does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification, see the end of the text. Other important disclosures follow the Reg AC certification, or go to www.gs.com/research/hedge.html. Analysts employed by non-US affiliates are not registered/qualified as research analysts with FINRA in the U.S. This report is intended for distribution to GS institutional clients only.

The Goldman Sachs Group, Inc. Goldman Sachs Global Economics, Commodities and Strategy Research

Units (mn)

Avg Floor

Space

(sqm/unit)

Floor

Space

(sqm,mn

Low Rental Housing 1.8 50 90 Economic Housing 1.2 60 72 Shantytown Renovation 2.8 70 196 Total 5.8 358 Low Rental Housing 1.5 50 74 Economic Housing 1.0 60 60 Shantytown Renovation 2.3 70 162 Total 4.8 296

2010

Social housing category

2011&12 (yearly)

September 20, 2010 China: Portfolio Strategy

Goldman Sachs Global Economics, Commodities and Strategy Research 2

Table of contents

Social housing has had a slow start historically 2

Social housing is divided into three major models 2

Poor completion progress historically due to lack of emphasis and motivation 3

Costs are significant without full funding; margins are thin 6

More emphasis will lead to policy support and concrete progress 6

Central government focus has dramatically picked up, as a way to address potential social problems and

to support growth 6

Increased focus has already been met with results 7

We believe more policies will be introduced to encourage faster social housing build 8

More immediate progress expected in first tier cities and in economic housing/capped price housing 8

We expect improving social housing build to partly offset risks of commodity housing slowdown 9

Our base case shows still teens yoy growth in GFA completion 9

Concerns over commodity housing drag on GFA growth may be overdone 10

Positive for cement, steel, construction services and machinery; low impact on property 12

Upstream industries are key beneficiaries 12

We believe cannibalization impact on commodity housing property developers will be very limited 15

Social housing is represented in our new China Policy Momentum basket 16

Appendix: Additional data 17

Social housing has had a slow start historically

Social housing is divided into three major models

China’s need for affordable housing has become increasingly evident in the past few

quarters, as commodity residential property prices reached new highs. By late 2009,

commodity property prices had become a focal point of social discontent and symbol of

the widening wealth gap. The concept of social housing has been around for years, but the

focus on widespread investment has only gained prominence in the recent past.

The exhibit below illustrates different types of social housing available in China. The

blue highlighted types are the officially defined social housing products. Of these, official

build targets do not yet explicitly include public rental housing, a new product type starting

off a low base. Capped price housing (in gray) is not classified as social housing but is a

similar type of product to economic housing.

September 20, 2010 China: Portfolio Strategy

Goldman Sachs Global Economics, Commodities and Strategy Research 3

Exhibit 1: Social housing differs by ownership and target segment

Note: Detailed policies may differ at the local government level.

Source: GS Global ECS Research.

Different products cater to different needs groups. All involve land provided by the

government and property for use at below market prices. Differences lie in the ownership

structure (own or rent) and degree of price discount (slightly or dramatically below market).

For example, economic housing (ASPs could be 50% or more below market) may cater to

an even lower affordability group than capped price housing (ASPs 20%-30% below

market). Similarly, low rental housing may be only a few hundred Rmb in rent while public

rental housing may be closer to the high triple digits.

Poor completion progress historically due to lack of emphasis and

motivation

Unfortunately, available data on the social housing market is extremely scarce. NBS

reports yearly economic housing GFA completed but lacks data on low-cost rental housing.

Clean, apples-to-apples data on the entire social housing market in terms of past GFA

completion or total investment is not available.

We do know that economic housing completion rates have historically been small.

The exhibit below shows completion for economic housing (and as a proportion of

commodity residential housing) – the ratio is low double digits to even single digits during

certain periods. While this data does not represent the low-cost rentals, we believe

completion rates for such are even smaller (for reasons we will discuss later in this report).

Low rental housing Economic Housing Shanty-town renovation Public rental housing Capped price housing

How does it work?

Government constructs

housing for low income

families at deeply

discounted rents

Government or developer

constructs housing and

sell to med to low income

class at a discounted,

capped price

Government renovates/ reconstructs

shanty-town area. The original

residents are compensated by new/

renovated flats for free or at a very

cheap price

Government constructs housing for

mid income families at discounted

rents, but higher than low rental

housing

Government or developer constructs

housing and sell to mid income

class at discounted price, but higher

than econ housing price

Ownership? Government Purchaser Original residents/purchaser Government Purchaser

Land injection needed?Y Y N Similar to low rental housing model Similar to economic housing model

Construction cost needed?Y

Borne by govt or

developerY Similar to low rental housing model Similar to economic housing model

Proceeds from saleN To government/developer

Y (for additional units after

compensating original residents)Similar to low rental housing model Similar to economic housing model

Pros

Most affordable, more

flexibility to adjust

occupancy and rentals

over time

Less hassle in managing

properties than rentals;

developer may bear most

of construction working

capital expenses

Similar to economic housing model Similar to low rental housing model Similar to economic housing model

Cons

Requires the most

upfront govt financial

burden in land injection

and construction cost -

no immediate cash

inflow of size

Ownership belongs to

buyer, less flexible to

meet longer-term or

lowest end user needs.

Often requires 'bundling'

of social and commodity

housing in one area to

ensure construction

progress.

Similar to economic housing model Similar to low rental housing model Similar to economic housing model

September 20, 2010 China: Portfolio Strategy

Goldman Sachs Global Economics, Commodities and Strategy Research 4

Exhibit 2: Economic housing completion rate historically has been low vs. commodity

housing Property developers’ economic housing completion rate has been poor

Note: Data based on NBS statistics on property developers.

Source: NBS, CEIC, GS Global ECS Research.

Local governments had insufficient motivation to fund such projects historically. The

exhibits below are a back-of-the-envelope analysis of social housing costs per year, based

on the central government’s published units completion targets.

Exhibit 3: 2010-12E social housing target is for 15.4m

units

Exhibit 4: Social housing land opportunity cost should be

in line with nationwide land sale price

Source: Ministry of Land and Resources (MLR), Ministry of Finance (MoF), CEIC, GS Global ECS Research.

Source: Ministry of Housing and Urban Development (MOHURD), MLR, CEIC, GS Global ECS Research.

0%

5%

10%

15%

20%

25%

30%

0

100

200

300

400

500

600

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

sqm mn Floor space completed-Commodity housing

Floor space completed-Economic housing

Economic housing as % of total residential

Units (mn)

Total target for 2010-2012 15.4 Plan for 2010 5.8 Target for 2011 and 2012 each 4.8

2011-12 Social housing target

Housing land sale proceeds (Rmb, mn) 1,339,180 Housing land sold (sqm, mn) 765 Housing land sale price (Rmb/sqm) 1,751

2009 Land sale price

September 20, 2010 China: Portfolio Strategy

Goldman Sachs Global Economics, Commodities and Strategy Research 5

Exhibit 5: Social housing direct construction costs and land opportunity costs are significant Construction costs are only part of the equation

Note: Assume % allocation for each category of social housing in 2011-12 will be same as 2010; 2011-12E target is 2010-12E target minus 2010, divided evenly between the two years. *In calculating land opportunity cost, we use half of the shantytown renovation land required to calculate cost, assuming half the land is needed to house existing inhabitants and the other half is available for redevelopment/redeployment.

Source: MOHURD, MLR, MoF, CEIC, Goldman Sachs Research.

The two key cost components are:

1. Construction cost: We derive this by multiplying target units completed by the

different size per type of unit, then assume Rmb 1,500-2,000 per square meter

construction cost. Our discussions with developers and housing construction

companies suggest that the construction cost range is around Rmb1,500 for second

and third tier cities and slightly higher for first tier cities (raw material prices are not

dramatically different but labor costs do vary). We believe that some more bullish

estimates of as low as Rmb1,000 per square meter construction cost are unrealistic.

2. Land opportunity cost: Land cost is an opportunity cost – the local government does

not need to buy the land, but is giving up potential land sale proceeds that the land

could otherwise generate.

Land price per sq meter in line with national average: We assume nationwide

average land sale price in 2009 (it is not reasonable to assume land cost much

lower than nationwide average because although social housing is sometimes on

the outskirts of towns, this is not always the case, and demand/construction is likely

to be centered in the cities where commodity property price is most out of reach).

We estimate that about 65% of the land price is sufficient to meet relocation

expenses (necessary for economic housing and low-cost rentals), while the other

35% is profit margin for the local government. For shantytown renovation, we

assume half of the land has opportunity cost as the other half will be reallocated

back to the original inhabitants post social housing construction.

Plot ratio of 1.5x: We have assumed 1.5x plot ratio for social housing. This might

seem counterintuitive, since many lower-end commodity residential properties

have even higher plot ratios at 2+. However, because low rises tend to be much

cheaper and faster to construct on a per GFA basis (lower demands on

sophistication/strength of foundation, frame, elevator systems, etc.), most social

housing projects so far have been low rise (up to six stories, no elevator). We note

that plot ratios may rise going forward, as we think it does not make sense to penny

pinch on construction cost when the land needs for lower plot ratios are likely to

imply higher land opportunity cost, which most likely more than offsets any

construction cost savings.

Units (mn)

Avg Floor

Space

(sqm/unit)

Total Floor

Space

(sqm,mn)

Avg

constructio

n cost

(Rmb/sqm)

Total

constructi

on cost

(Rmb, bn)

Plot ratio

assumed

Land

required

(sqm, mn)

Land cost

(Rmb/sqm)

Total land

cost

(Rmb, bn)

Total cost

(Rmb, bn)

Low Rental Housing 1.8 50 90 1,500 135 1.5 60 1,751 105 240 Economic Housing 1.2 60 72 2,000 144 1.5 48 1,751 84 228 Shantytown Renovation 2.8 70 196 1,500 294 1.5 131 1,751 114 408 Total 5.8 358 573 239 304 877 Low Rental Housing 1.5 50 74 1,500 112 1.5 50 1,751 87 199 Economic Housing 1.0 60 60 2,000 119 1.5 40 1,751 70 189 Shantytown Renovation 2.3 70 162 1,500 243 1.5 108 1,751 95 338 Total 4.8 296 474 198 251 725

2010

Social housing category

2011&12 (yearly)

September 20, 2010 China: Portfolio Strategy

Goldman Sachs Global Economics, Commodities and Strategy Research 6

Costs are significant without full funding; margins are thin

Central government funding only meets a fraction of the cost. The budget allocated by

the central government for social housing this year (Rmb63 bn) can meet only 11% of

construction cost and 7% of total cost (including land opportunity cost) if this year’s 5.8mn

units target were to be completed. And this does not include the 1.2mn units targeted for

rural reconstruction or other types of new products like public rental housing or capped

price housing (these new products are still small scale and related targets are not yet

explicit). The intention is that local governments bear the brunt of the expenses.

Local governments lack economic motivation to pursue social housing. Although local

governments could fund social housing with bank lending or fiscal revenue, officials lack

motivation to do so because:

1. social housing projects are either extremely low return or negative return, and are (in

many cases) unable to become self-funding even over time;

2. target KPIs from the central government tended to be tied to economic growth, so loan

quotas were prioritized towards higher economic return projects.

Even the social housing projects that did get the green light were met with low

enthusiasm from the supply chain. Commodity housing developers are unenthusiastic

about participating, because social housing margins are designed to be very thin (single

digit vs. 30%+ for commodity housing). The bulk of construction thus far has been borne by

state-owned enterprises under the local governments’ oversight.

More emphasis will lead to policy support and concrete progress

Central government focus has dramatically picked up, as a way to

address potential social problems and to support growth

We show in the exhibit below the potential funding sources to meet social housing

construction costs this year. Although we have not included land opportunity cost in the

shortfall calculation, it is important to note that land injections are also a detractor from the

government budget, as it directly sacrifices commodity property land sale proceeds.

Key sources of cash funds for construction include the central government grant, a

required 10% of local government land sale profit for the year (as per MOHURD rules),

and proceeds from the sale of economic housing (we assume quick sales of the

economic housing given demand vastly exceeds supply). Other funding sources include

housing provident fund (HPF) interest or possible additional proceeds from sale/rental of

commercial shops and surrounding facilities, but these are not likely to be significant.

September 20, 2010 China: Portfolio Strategy

Goldman Sachs Global Economics, Commodities and Strategy Research 7

Exhibit 6: Social housing funding gap is not insignificant

Source: MOHURD, MoF, GS Global ECS Research.

Creative types of financing have also started to materialize, such as REIT structures and

build-transfer models with construction partners (which lightens the upfront funding need

for the local government). We expect their maturation and development to further rectify

the funding shortfall issues.

The central government has also directed HPF resources to be allocated to social

housing construction loans.

Up to 50% of HPF surplus: MOHURD, MoF, NDRC, PBOC and CBRC issued a joint

document titled ‘Regarding utilizing HPF funding to support social housing construction

pilot projects’, declaring that local governments can tap up to 50% of HPF surplus (HPF

balance net of necessary withdrawals) as long-term borrowing for social housing

construction. Loan duration is limited to three years for economic housing and shantytown

renovation, and five years for cheap rentals. As of end-2008, the potential 50% of HPF

surplus available equalled around Rmb160 bn. Tapping into this fund will be a gradual

process as only approved pilot cities and projects can participate.

Pilot cities identified: In early August 2010, MOHURD announced that 28 pilot cities

building 133 social housing projects would start to tap this fund. Total funding from HPF

available to these projects for borrowing is Rmb49 bn in this first batch.

Increased focus has already been met with results

MOHURD announced on Sept 19 that:

– By end August, 75% of economic housing/low rental housing targets for 2010E has

commenced construction, equivalent to 2.2m units; while 65% of shantytown

renovation target units have commenced construction, equivalent to 1.9m units.

– Progress on the above construction will be monitored and it is expected that at least

60% of 2010E targeted units will complete construction before year-end.

– MOHURD and relevant agencies will continue to monitor progress and ensure that all

of 2010E social housing targeted units begin construction by end Sept.

– Year-to-August social housing investment has reached Rmb 470bn (GS comment: it is

unclear whether this refers to construction cost only or also land relocation expenses

or other costs).

Rmb (bn) GS comment

Central government budget 63 Previously announced

Local government 344

10% Land sale profit 40 Assume conservatively that land sales proceeds fall by -20% yoy

and profit margin is approx 35% as per our property team

Sale of econ/renovated housing 291 Assume 0% margin over construction cost to govt for econ housing

& half of renovation housing is sold, other half is returned to original residents

Housing provident fund interest 13 Assume 1% interest income from fund balance per year

Total funding 407

Construction cost need 573 Excludes land opportunity costs from local government land sales profit

Relocation cost 123 Assume 65% of total land cost of low rental housing and economic housing

Funding gap 289% shortfall 50%

Social Housing funding

September 20, 2010 China: Portfolio Strategy

Goldman Sachs Global Economics, Commodities and Strategy Research 8

– Furthermore, relevant agencies are in the process of drafting the ‘2010-12 social

housing project construction plan’ which will be unveiled in time.

We believe more policies will be introduced to encourage faster

social housing build

Repeated speeches from the highest level leaders emphasize the importance of social

housing as one of the key priorities for 2010 and beyond. Not only does social housing help

to alleviate quality of life issues for low- to middle-class Chinese, we believe the

policymakers also intend for social housing to help sustain investment as its commodity

property tightening measures have already slowed developers’ pace of new project starts,

as the ASP outlook is increasingly murky. We believe that as macro policy is gradually

loosened in the coming quarters, social housing will be one key niche area to see

meaningful support.

Possible further forms of policy assistance that may be considered over time (some of

which we believe may be adopted in the upcoming ‘2010-12 social housing project

construction plan’) include:

More dedicated land supply required from the local governments, and greater

supervision in meeting targets

Exhibit 7: Land supply for social housing is intended to be >30% of total for 2010E, higher than historical actual Only 21% of full-year social housing land supply was spent in 1H10

Source: MLR, CEIC, GS Global ECS Research.

Tying social housing completion targets to local government officials’ KPIs

Bundling social housing obligations with land sales to commodity developers (a piece

of land won requires a fraction to be developed into economic housing – developers end

up bidding lower for the land but are forced to construct social housing and to bear

construction cost)

Linking future land auction qualifications more explicitly with commodity property

developers’ social housing

Greater funding resource allocation from the central government

Preferential policies from banks and other funding sources towards social housing

More immediate progress expected in first tier cities and in

economic housing/capped price housing

The development of social housing across China remains a long and winding road, in our

view. Deep-rooted issues cannot be resolved in a short time. More central government

policies or not, we are not so optimistic to assume that targeted completion rates are

within our sights near-term.

1H10/FY10Land Supply

(Hectare)

Low rental

housing

Economic

housing

Shanty-town

renovation

Med/Small

Size

% Social

housing

completion

%

2009 (Actual) 76,461 3,000 18.3%

2010 (Plan) 184,749 7,051 17,402 36,606 80,431 33.0%

1H10 (Actual) 56,108 1,513 4,433 6,596 29,535 22.4% 21%

Total

residential

housing

10,958

Social housing

September 20, 2010 China: Portfolio Strategy

Goldman Sachs Global Economics, Commodities and Strategy Research 9

2010E may reach only 60% completion rate, considering dismal completion rates in 1H10

and the need to severely back-load investment in 2H10. Nonetheless, given the latest

MOHURD announcement and high conviction in meeting this figure, we believe 60%

should be achievable.

But we expect improvements thereafter, as gradual policy implementation and

structural fixes to accelerate the pace of development. We believe completion rates can

show increases yoy to 80%+ by 2011-12E. This could even prove conservative, considering

that MOHURD and relevant agencies are requiring that all of the 2010E’s 5.8m units

commence construction by end Sept.

We expect economic housing in first and second tier cities to report the most progress

near-term, because:

Economic housing is sold after construction for an immediate cash flow

turnaround – even if the margin is very low, at least the construction cash expenses

can be recouped quickly.

Economic housing is easier to ‘bundle’ with commodity housing development, as

mentioned earlier, because it does not require as much operating / management

commitment as low rental housing, and typically is geared towards middle-income

customers that may fit in better with the commodity pricing inhabitants/buyers.

Tier one and two cities may see faster progress, as they face much greater demand for

social housing vs. lower-tier cities where prices have not moved as much, and because

their governments tend to have more funding resources/flexibility.

We expect improving social housing build to partly offset risks of

commodity housing slowdown

Our base case shows still teens yoy growth in GFA completion

To what extent would a potential slowdown in commodity residential housing GFA

completion put total property investment at risk? We have done the sensitivity analysis in

the below to try to answer this question. We acknowledge that due to aforementioned

incomplete historical data, as well as significant uncertainties on regulatory oversight and

execution, that there could be meaningful deviations from our estimates.

1. We assume 10% floor space completion growth for non-residential (commercial

mostly) and for residential housing other than commodity and social housing (i.e.

dorms, etc). This looks reasonable to us vs. the 1H10A trend and also is roughly in the

middle of the historical ranges. Our property team estimates that total GFA growth for

commercial and residential property should reach 20% per year for 2010-12E, based on

an average of 2.3 follow-on years (between 2000 and 2009) to complete GFA under

construction. So we feel 10% is sufficiently conservative.

September 20, 2010 China: Portfolio Strategy

Goldman Sachs Global Economics, Commodities and Strategy Research 10

Exhibit 8: National floor space completed has been growing at double digits for most

years

Source: NBS, CEIC, GS Global ECS Research.

Exhibit 9: Social housing assumptions on floor space GFA completion

Note: 1) Assume residential housing built by developers is commodity housing in 2009. 2) 2009 social housing floor space is calculated by proportion of land supply comparing to 2010 target

Source: MOHURD, MLR, NBS, CEIC, GS Global ECS Research.

2. We assume 20% commodity residential housing growth per annum as per our

property team’s estimate. We note that this is the area where government is tightening

policy and thus is the more controversial area of investment that the market is

concerned about.

3. We assume conservatively a 60% social housing completion rate for 2010E

ramping up to 80% for 2011-12E. What level is actually reached will depend largely

upon some of the supportive policies discussed earlier and oversight on

implementation/execution.

Assuming the above, we estimate yearly GFA growth in the teens for 2010-12E.

Concerns over commodity housing drag on GFA growth may be

overdone

We feel that the risk of a possible slowdown in commodity housing investment dragging

down overall GFA growth /investment into single digit or even negative territory are

overdone.

Historically commodity residential housing is only about half the total China GFA,

with the other half belonging to areas not subject to the policy tightening.

Social housing targets are equivalent to 30%-50% of the commodity housing GFA

by our estimate, so the potential contribution is quite significant. If completion rates

are reasonable, it could be enough to buffer some degree of potential miss on

commodity residential housing.

sqm mn

Floor space

completed-

Total yoy %

Floor space

completed-

Residential yoy %

Floor space

completed-

Non-

residential yoy %

2005 1,103 14% 611 10% 492 19%

2006 1,121 2% 594 -3% 527 7%

2007 1,270 13% 661 11% 609 16%

2008 1,281 1% 658 0% 623 2%

2009 1,574 23% 789 20% 785 26%

2010(1-7) 527 10% 290 10% 237 10%

Residential housing

Assumed

growth rate

Commod

housing-

Base caseBase case

growth rate

Social

housing

target

Base case

completion

%

Social

housing-

Base case

Other

residential

housingAssumed

growth rate yoy %

2009 785 596 82 111 1,574 5%

2010E 864 10% 716 20% 358 60% 215 122 10% 1,916 22% 11%

2011E 950 10% 859 20% 296 80% 237 134 10% 2,180 14% 11%

2012E 1,045 10% 1,030 20% 296 80% 237 147 10% 2,460 13% 10%

Non-residential

Floor space

completed (sqm

mn)

Social

housing %

of total

Total floor

space-

Base case

September 20, 2010 China: Portfolio Strategy

Goldman Sachs Global Economics, Commodities and Strategy Research 11

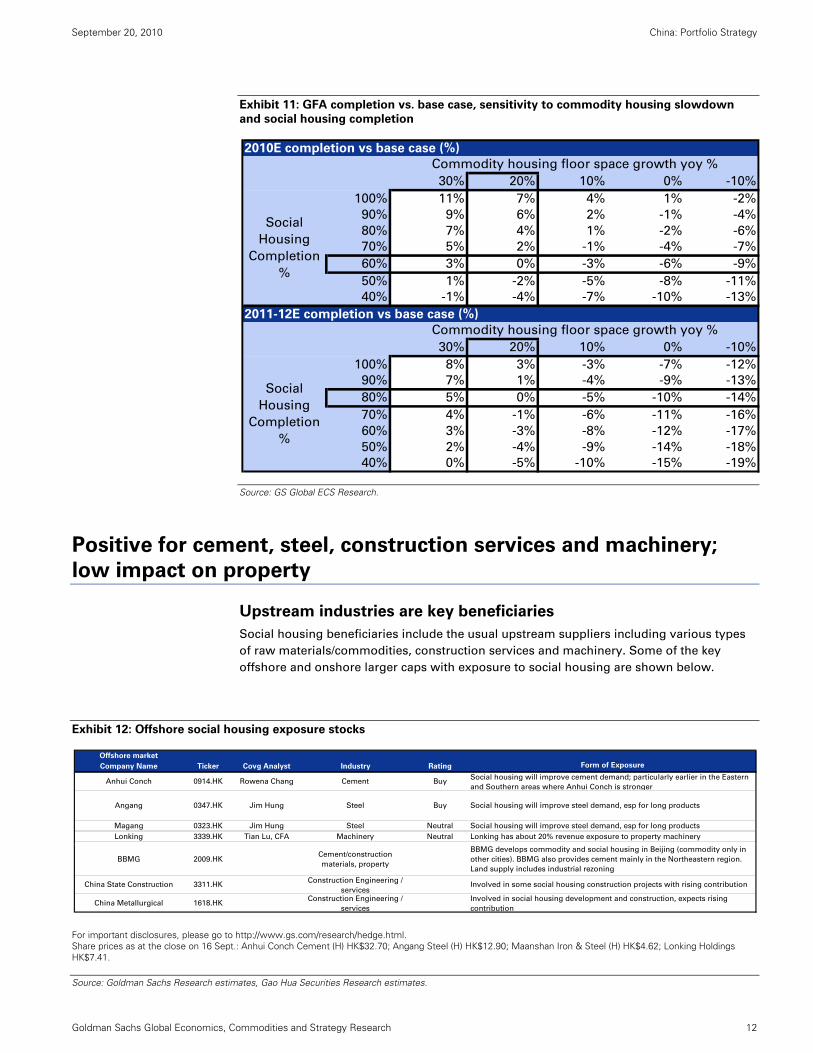

The exhibits below show the implied total GFA growth rates across different assumptions

for yearly commodity residential GFA completion growth vs. various social housing target

completion assumptions.

We also show the GFA completion rate vs our base case scenario described above. Even if

commodity housing were to grind to a halt in 2010E with zero growth (very unlikely in our

view given the construction schedule already underway), missing our estimates by 20pp

growth, total impact to GFA completion base case would be negligible, if social housing

completion could reach 80%.

Exhibit 10: GFA growth sensitivity to commodity housing slowdown and social housing

completion

Source: GS Global ECS Research.

2010E GFA growth yoy %

Commodity housing floor space growth yoy %

30% 20% 10% 0% -10%

100% 35% 31% 27% 23% 19%

90% 32% 29% 25% 21% 17%

80% 30% 26% 22% 19% 15%

70% 28% 24% 20% 16% 13%

60% 26% 22% 18% 14% 10%

50% 23% 19% 16% 12% 8%

40% 21% 17% 13% 10% 6%

2011-12E GFA growth yoy % avg

Commodity housing floor space growth yoy %

30% 20% 10% 0% -10%

100% 19% 15% 11% 7% 4%

90% 18% 14% 10% 7% 3%

80% 17% 13% 9% 6% 2%

70% 17% 13% 9% 5% 2%

60% 16% 12% 8% 4% 1%

50% 15% 11% 7% 4% 0%

40% 15% 11% 7% 3% -1%

Social

Housing

Completion

%

Social

Housing

Completion

%

September 20, 2010 China: Portfolio Strategy

Goldman Sachs Global Economics, Commodities and Strategy Research 12

Exhibit 11: GFA completion vs. base case, sensitivity to commodity housing slowdown

and social housing completion

Source: GS Global ECS Research.

Positive for cement, steel, construction services and machinery;

low impact on property

Upstream industries are key beneficiaries

Social housing beneficiaries include the usual upstream suppliers including various types

of raw materials/commodities, construction services and machinery. Some of the key

offshore and onshore larger caps with exposure to social housing are shown below.

Exhibit 12: Offshore social housing exposure stocks

For important disclosures, please go to http://www.gs.com/research/hedge.html. Share prices as at the close on 16 Sept.: Anhui Conch Cement (H) HK$32.70; Angang Steel (H) HK$12.90; Maanshan Iron & Steel (H) HK$4.62; Lonking Holdings HK$7.41.

Source: Goldman Sachs Research estimates, Gao Hua Securities Research estimates.

2010E completion vs base case (%)

Commodity housing floor space growth yoy %

30% 20% 10% 0% -10%

100% 11% 7% 4% 1% -2%

90% 9% 6% 2% -1% -4%

80% 7% 4% 1% -2% -6%

70% 5% 2% -1% -4% -7%

60% 3% 0% -3% -6% -9%

50% 1% -2% -5% -8% -11%

40% -1% -4% -7% -10% -13%

2011-12E completion vs base case (%)

Commodity housing floor space growth yoy %

30% 20% 10% 0% -10%

100% 8% 3% -3% -7% -12%

90% 7% 1% -4% -9% -13%

80% 5% 0% -5% -10% -14%

70% 4% -1% -6% -11% -16%

60% 3% -3% -8% -12% -17%

50% 2% -4% -9% -14% -18%

40% 0% -5% -10% -15% -19%

Social

Housing

Completion

%

Social

Housing

Completion

%

Offshore market

Company Name Ticker Covg Analyst Industry Rating Form of Exposure

Anhui Conch 0914.HK Rowena Chang Cement BuySocial housing will improve cement demand; particularly earlier in the Eastern

and Southern areas where Anhui Conch is stronger

Angang 0347.HK Jim Hung Steel Buy Social housing will improve steel demand, esp for long products

Magang 0323.HK Jim Hung Steel Neutral Social housing will improve steel demand, esp for long products

Lonking 3339.HK Tian Lu, CFA Machinery Neutral Lonking has about 20% revenue exposure to property machinery

BBMG 2009.HKCement/construction

materials, property

BBMG develops commodity and social housing in Beijing (commodity only in

other cities). BBMG also provides cement mainly in the Northeastern region.

Land supply includes industrial rezoning

China State Construction 3311.HKConstruction Engineering /

servicesInvolved in some social housing construction projects with rising contribution

China Metallurgical 1618.HKConstruction Engineering /

services

Involved in social housing development and construction, expects rising

contribution

September 20, 2010 China: Portfolio Strategy

Goldman Sachs Global Economics, Commodities and Strategy Research 13

It is challenging to quantify exact earnings implications by stock, as each company has

may have only a portion of their revenues exposed to property or social housing in

particular. We do expect that the proportion of social housing exposure for the above

names will increase over time.

Exhibit 13: Cement and machinery have more property revenue exposure than steel

Source: Goldman Sachs Research estimates, Gao Hua Securities Research estimates.

Commodities & machinery companies can benefit more immediately from social housing

Our commodities and machinery analysts have performed broader industry sensitivity

analyses on their sectoral demand for various levels of social housing completion rates, as

shown below:

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Steel Cement Sany Heavy Lonking Guangxi Liugong

Property Infrastructure Others

September 20, 2010 China: Portfolio Strategy

Goldman Sachs Global Economics, Commodities and Strategy Research 14

Exhibit 14: Cement supply/demand could swing favorably if social housing completion rates are higher

Source: Goldman Sachs Research estimates, Gao Hua Securities Research estimates.

Exhibit 15: Steel supply/demand is slightly less sensitive due to less property exposure

Source: Goldman Sachs Research estimates, Gao Hua Securities Research estimates.

For example, our cement analyst Rowena Chang forecasts 2010E cement oversupply of 7m

tons (assuming 50% social housing completion) would become 7m of undersupply if

completion rate could reach 70%. A swing in the supply/demand situation could have

numerous impacts on industry dynamics due to higher sales volumes as well as likely

higher ASP.

20% 30% 40% 50% 60% 70% 80%

2010E Floor Space Completed

(mn sqm)72 107 143 179 215 251 286

2010E Cement Consumption from

Social Housing

(mn tonnes)

14 21 29 36 43 50 57

Implied 2010E oversupply condition

(mn tonnes)29 22 14 7 0 -7 -14

20% 30% 40% 50% 60% 70% 80%

2011E Floor Space Completed

(mn sqm)59 89 118 148 178 207 237

2011E Cement Consumption from

Social Housing

(mn tonnes)

12 18 24 30 36 41 47

Implied 2011E oversupply condition

(mn tonnes)20 14 8 2 -4 -10 -16

2010E Social Housing Completion Ratio

2011E Social Housing Completion Ratio

20% 30% 40% 50% 60% 70% 80%

2010E Floor Space Completed

(mn sqm)72 107 143 179 215 251 286

2010E Steel Consumption from Social

Housing

(mn tonnes)

7 11 14 18 21 25 29

Implied 2010E oversupply condition (mn

tonnes)30 26 23 19 15 12 8

20% 30% 40% 50% 60% 70% 80%

2011E Floor Space Completed

(mn sqm)59 89 118 148 178 207 237

2011E Steel Consumption from Social

Housing

(mn tonnes)

6 9 12 15 18 21 24

Implied 2011E oversupply condition (mn

tonnes)20 17 14 11 8 5 3

2010E Social Housing Completion Ratio

2011E Social Housing Completion Ratio

September 20, 2010 China: Portfolio Strategy

Goldman Sachs Global Economics, Commodities and Strategy Research 15

Construction services companies show selective interest, but are keener to diversify into even higher-margin businesses

Companies like CCCC, CRG and CRC are actively looking for diversification avenues, as in

the medium- to longer-term, capex demand from areas like railroads may decline past their

peak periods. However, interest in social housing is selective as some are keener to move

into higher-margin businesses like property development instead. We forecast a less

immediate impact on this sub-set of companies. As the exhibit below shows, only China

Metallurgical Corp is currently involved actively in social housing.

Exhibit 16: Construction services and engineering companies generally have less exposure to date

Source: Goldman Sachs Research estimates, Gao Hua Securities Research estimates.

We believe cannibalization impact on commodity housing property

developers will be very limited

We believe the inevitable pick-up in social housing is unlikely to meaningfully affect

commodity housing developers because:

1. Product overlap should be small: Social housing sizes are on the small side and

should not overlap much with the same addressable market as commodity housing.

The insufficient supply vs. hypothetical demand and lack of clarity in who can qualify

and when means that buyers who may be able to borderline afford a commodity

property are unlikely to indefinitely delay purchase plans to wait for the social housing

allocation. In addition, the longer-term targets more skewed towards rentals rather

than economic housing, which further reduces overlap issues.

2. Ownership conditions are different: The government will impose strict rules on

transfer of economic housing, which will limit demand strictly to self-use, whereas

commodity housing demand will also include investment, rental, and speculation.

3. Product bundling requirements will be reflected in land bid prices: Most of the

property developers are uninterested in building social housing due to unattractive

margins/returns. Going forward, land bids could have a rising ‘bundling’ aspect

whereby a portion of land must be developed for social housing – this is already

starting to take place in some locations. This may not necessarily meaningfully erode

returns for commodity housing developers because they will take the construction

expenses and working capital needs into their returns calculation, and accordingly

lower their land bid prices as well.

According to our conversations with a number of developers, both SOE and private, only

Vanke showed clear interest in building social housing, as Chairman Wang Shi said in post-

results briefings that this is Vanke’s responsibility, it is a large and growing market, and

participation will be positive for company image and branding to various constituency

groups.

Company Name Ticker Main BusinessExposure to Property

Development?

Exposure to Property

Construction? Current Participation in Social Housing?

China State Construction 3311.HKBuilding Construction, International Engineering

Contracting, Real estateHK and overseas Mainly in HK and overseas

One social housing related project is a build-

transfer project in Tianjin that they recently won

the bid for.

CRCC 1186.HK Railload Construction Services close to 10% of revenue Single digit Slight exposure (one project only)

CCCC 1800.HK Infrastructure Construction Services

None at listco for now, but may

have exposure when property

assets are transferred from the

parent after the recent merger

with China National Real Estate

Development Group

Not meaningful No

CRG 0390.HKRailload Construction Services and Construction

Contractingclose to 10% of revenue Single digit No

MCC 1618.HKNatural Resources Exploitation Businesses,

Engineering and ConstructionSingle digit about 15% of total revenue Yes. Act as both developer and constructor

September 20, 2010 China: Portfolio Strategy

Goldman Sachs Global Economics, Commodities and Strategy Research 16

Social housing is represented in our new China Policy Momentum

basket

We have recently introduced GS Policy Momentum basket ticker GSCNPLCY1, which

includes exposure to a variety of focused investment themes, including social housing (as

well as rural/Western/Central development, consumption, etc.). Magang, Lonking and

Anhui Conch are three of the social housing beneficiaries that are included in the basket.

For more details on the basket, please see our report entitled Asia Pacific: Portfolio

Strategy: Selected slices for an undulating upturn, published September 17.

1 Note: The ability to trade this basket will depend upon market conditions, including liquidity and

borrow constraints at the time of trade.

September 20, 2010 China: Portfolio Strategy

Goldman Sachs Global Economics, Commodities and Strategy Research 17

Appendix: Additional data

Exhibit 17: Bottom-up targets for 2010E social housing construction new starts, by province

* Newly started units are yearly averages from 2-3 year announced targets.

Source: Various media reports, MOHURD.

Provinces/Regions # of units (New start) # of units (Completion)

Beijing 136,000 46,000

Tianjin 85,000 NA

Hebei 31,800 NA

Shanxi 200,000 NA

Inner Mongolia 350,000 275,000

Jilin 436,000 NA

Heilongjiang 234,000 NA

Shanghai 150,000 NA

Jiangsu* 186,000 NA

Zhejiang 50,000 NA

Anhui 160,000 70,000

Fujian 70,000 60,000

Jiangxi 130,000 NA

Shandong* 152,000 NA

Henan 160,000 NA

Hubei* 220,000 NA

Hainan 100,000 NA

Hunan 230,000 NA

Guangdong* 169,000 84,000

Chongqing* 200,000 NA

Sichuan 199,300 NA

Guizhou 100,000 NA

Yunnan* 200,000 NA

Shaanxi* 100,000 NA

Gansu* 67,000 NA

Qinghai* 60,000 NA

Ningxia 35,000 NA

Xinjiang 80,000 NA

Total 4,291,100

Target for Social Housing Constructions (Provincial, 2010)

September 20, 2010 China: Portfolio Strategy

Goldman Sachs Global Economics, Commodities and Strategy Research 18

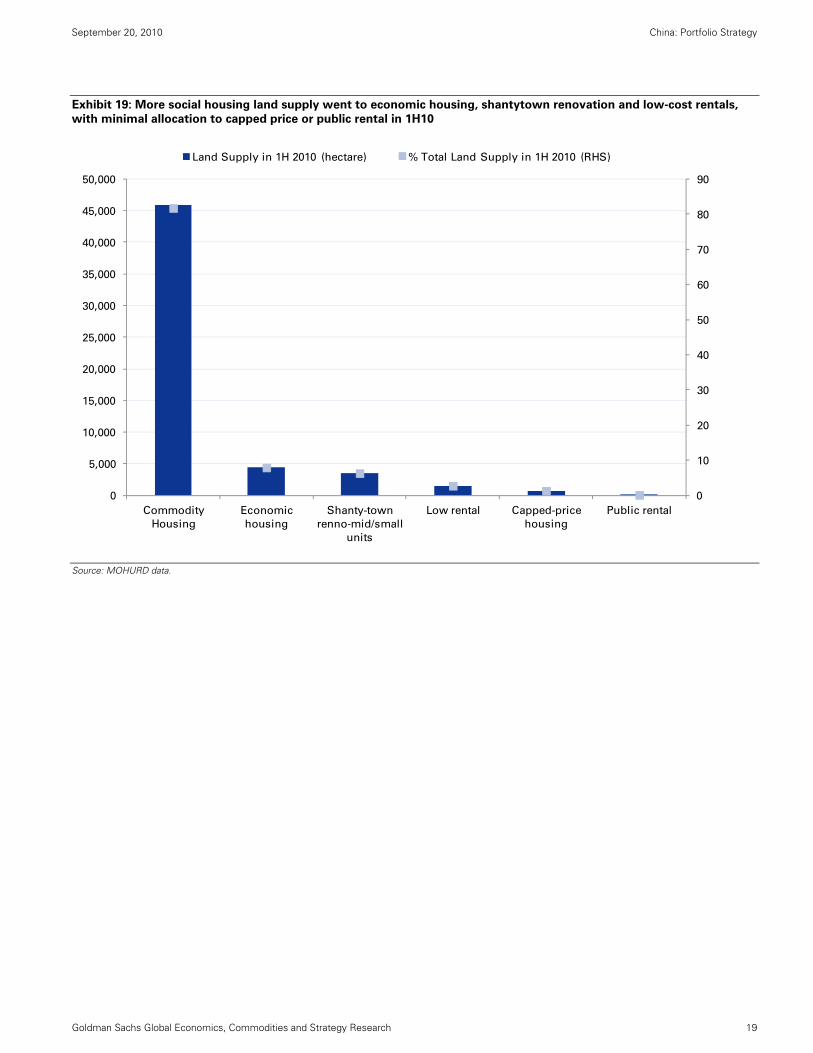

Exhibit 18: Social housing is targeted to comprise 30% of 2010E land supply, but has only reached 17% in 1H10

Source: MOHURD data.

Provinces and Regions

Planned Land

Supply in 2010

(Hectare)

Actual Land

Supply in 1H

10 (Hectare)

1H10 as % of 2010

planned supply

Land

Supply for

Social

Housing in

Social

housing %

of 1H10

land supply

Beijing 2,500 1,450 58% 99 7%

Tianjin 1,740 1,568 90% 192 12%

Hebei 9,779 2,398 25% 329 14%

Shanxi 4,730 484 10% 115 24%

Inner Mongolia 10,489 2,513 24% 483 19%

Liaoning 12,708 3,906 31% 126 3%

Jilin 5,565 1,219 22% 238 20%

Heilongjiang 8,753 2,557 29% 524 20%

Shanghai 1,100 321 29% 235 73%

Jiangsu 13,010 6,615 51% 1,304 20%

Zhejiang 8,240 2,736 33% 547 20%

Anhui 10,674 2,238 21% 430 19%

Fujian 4,234 812 19% 84 10%

Jiangxi 4,391 1,538 35% 246 16%

Shandong 18,165 6,357 35% 652 10%

Henan 7,372 2,692 37% 845 31%

Hubei 5,548 1,665 30% 152 9%

Hunan 3,180 1,491 47% 197 13%

Guangdong 7,504 1,830 24% 121 7%

Guangxi 5,002 924 18% 151 16%

Hainan 1,564 336 21% 103 31%

Chongqing 6,449 1,191 18% 208 17%

Sichuan 8,160 2,711 33% 469 17%

Guizhou 4,544 1,639 36% 396 24%

Yunnan 4,970 1,392 28% 51 4%

Tibet 270 42 16% 16 39%

Shaanxi 3,466 1,022 29% 244 24%

Gansu 2,420 499 21% 127 25%

Qinghai 835 161 19% 114 71%

Ningxia 1,787 644 36% 234 36%

Xinjiang 4,822 989 21% 332 34%

Xinjiang Legion 1,427 167 12% 108 64%

Total 185,399 56,108 30% 9,472 17%

September 20, 2010 China: Portfolio Strategy

Goldman Sachs Global Economics, Commodities and Strategy Research 19

Exhibit 19: More social housing land supply went to economic housing, shantytown renovation and low-cost rentals,

with minimal allocation to capped price or public rental in 1H10

Source: MOHURD data.

0

10

20

30

40

50

60

70

80

90

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

Commodity

Housing

Economic

housing

Shanty-town

renno-mid/small

units

Low rental Capped-price

housing

Public rental

Land Supply in 1H 2010 (hectare) % Total Land Supply in 1H 2010 (RHS)

September 20, 2010 China: Portfolio Strategy

Goldman Sachs Global Economics, Commodities and Strategy Research 20

Reg AC

We, Helen Zhu, Timothy Moe, CFA, Christopher Eoyang and Ben Bei, hereby certify that all of the views expressed in this report accurately reflect our

personal views about the subject company or companies and its or their securities. We also certify that no part of our compensation was, is or will be,

directly or indirectly, related to the specific recommendations or views expressed in this report.

Investment Profile

The Goldman Sachs Investment Profile provides investment context for a security by comparing key attributes of that security to its peer group and

market. The four key attributes depicted are: growth, returns, multiple and volatility. Growth, returns and multiple are indexed based on composites

of several methodologies to determine the stocks percentile ranking within the region's coverage universe.

The precise calculation of each metric may vary depending on the fiscal year, industry and region but the standard approach is as follows:

Growth is a composite of next year's estimate over current year's estimate, e.g. EPS, EBITDA, Revenue. Return is a year one prospective aggregate

of various return on capital measures, e.g. CROCI, ROACE, and ROE. Multiple is a composite of one-year forward valuation ratios, e.g. P/E, dividend

yield, EV/FCF, EV/EBITDA, EV/DACF, Price/Book. Volatility is measured as trailing twelve-month volatility adjusted for dividends.

Quantum

Quantum is Goldman Sachs' proprietary database providing access to detailed financial statement histories, forecasts and ratios. It can be used for

in-depth analysis of a single company, or to make comparisons between companies in different sectors and markets.

Disclosures

Coverage group(s) of stocks by primary analyst(s)

Compendium report: please see disclosures at http://www.gs.com/research/hedge.html. Disclosures applicable to the companies included in this

compendium can be found in the latest relevant published research.

Option Specific Disclosures

Price target methodology: Please refer to the analyst’s previously published research for methodology and risks associated with equity price

targets.

Pricing Disclosure: Option prices and volatility levels in this note are indicative only, and are based on our estimates of recent mid-market levels.

All prices and levels exclude transaction costs unless otherwise stated.

Buying Options - Investors who buy call (put) options risk loss of the entire premium paid if the underlying security finishes below (above) the

strike price at expiration. Investors who buy call or put spreads also risk a maximum loss of the premium paid. The maximum gain on a long call or

put spread is the difference between the strike prices, less the premium paid.

Selling Options - Investors who sell calls on securities they do not own risk unlimited loss of the security price less the strike price. Investors who

sell covered calls (sell calls while owning the underlying security) risk having to deliver the underlying security or pay the difference between the

security price and the strike price, depending on whether the option is settled by physical delivery or cash-settled. Investors who sell puts risk loss of

the strike price less the premium received for selling the put. Investors who sell put or call spreads risk a maximum loss of the difference between

the strikes less the premium received, while their maximum gain is the premium received.

For options settled by physical delivery, the above risks assume the options buyer or seller, buys or sells the resulting securities at the

settlement price on expiry.

Company-specific regulatory disclosures

Compendium report: please see disclosures at http://www.gs.com/research/hedge.html. Disclosures applicable to the companies included in this

compendium can be found in the latest relevant published research.

Distribution of ratings/investment banking relationships

Goldman Sachs Investment Research global coverage universe

Rating Distribution Investment Banking Relationships

Buy Hold Sell Buy Hold Sell

Global 31% 53% 16% 47% 44% 34%

September 20, 2010 China: Portfolio Strategy

Goldman Sachs Global Economics, Commodities and Strategy Research 21

As of July 1, 2010, Goldman Sachs Global Investment Research had investment ratings on 2,814 equity securities. Goldman Sachs assigns stocks as

Buys and Sells on various regional Investment Lists; stocks not so assigned are deemed Neutral. Such assignments equate to Buy, Hold and Sell for

the purposes of the above disclosure required by NASD/NYSE rules. See 'Ratings, Coverage groups and views and related definitions' below.

Price target and rating history chart(s)

Compendium report: please see disclosures at http://www.gs.com/research/hedge.html. Disclosures applicable to the companies included in this

compendium can be found in the latest relevant published research.

Regulatory disclosures

Disclosures required by United States laws and regulations

See company-specific regulatory disclosures above for any of the following disclosures required as to companies referred to in this report: manager

or co-manager in a pending transaction; 1% or other ownership; compensation for certain services; types of client relationships; managed/co-

managed public offerings in prior periods; directorships; for equity securities, market making and/or specialist role. Goldman Sachs usually makes a

market in fixed income securities of issuers discussed in this report and usually deals as a principal in these securities.

The following are additional required disclosures: Ownership and material conflicts of interest: Goldman Sachs policy prohibits its analysts,

professionals reporting to analysts and members of their households from owning securities of any company in the analyst's area of coverage.

Analyst compensation: Analysts are paid in part based on the profitability of Goldman Sachs, which includes investment banking revenues. Analyst as officer or director: Goldman Sachs policy prohibits its analysts, persons reporting to analysts or members of their households from serving as an

officer, director, advisory board member or employee of any company in the analyst's area of coverage. Non-U.S. Analysts: Non-U.S. analysts may

not be associated persons of Goldman Sachs & Co. and therefore may not be subject to NASD Rule 2711/NYSE Rules 472 restrictions on

communications with subject company, public appearances and trading securities held by the analysts.

Distribution of ratings: See the distribution of ratings disclosure above. Price chart: See the price chart, with changes of ratings and price targets in

prior periods, above, or, if electronic format or if with respect to multiple companies which are the subject of this report, on the Goldman Sachs

website at http://www.gs.com/research/hedge.html.

Additional disclosures required under the laws and regulations of jurisdictions other than the United States

The following disclosures are those required by the jurisdiction indicated, except to the extent already made above pursuant to United States laws

and regulations. Australia: This research, and any access to it, is intended only for "wholesale clients" within the meaning of the Australian

Corporations Act. Canada: Goldman Sachs & Co. has approved of, and agreed to take responsibility for, this research in Canada if and to the extent it

relates to equity securities of Canadian issuers. Analysts may conduct site visits but are prohibited from accepting payment or reimbursement by the

company of travel expenses for such visits. Hong Kong: Further information on the securities of covered companies referred to in this research may

be obtained on request from Goldman Sachs (Asia) L.L.C. India: Further information on the subject company or companies referred to in this

research may be obtained from Goldman Sachs (India) Securities Private Limited; Japan: See below. Korea: Further information on the subject

company or companies referred to in this research may be obtained from Goldman Sachs (Asia) L.L.C., Seoul Branch. Russia: Research reports

distributed in the Russian Federation are not advertising as defined in the Russian legislation, but are information and analysis not having product

promotion as their main purpose and do not provide appraisal within the meaning of the Russian legislation on appraisal activity. Singapore: Further

information on the covered companies referred to in this research may be obtained from Goldman Sachs (Singapore) Pte. (Company Number:

198602165W). Taiwan: This material is for reference only and must not be reprinted without permission. Investors should carefully consider their

own investment risk. Investment results are the responsibility of the individual investor. United Kingdom: Persons who would be categorized as

retail clients in the United Kingdom, as such term is defined in the rules of the Financial Services Authority, should read this research in conjunction

with prior Goldman Sachs research on the covered companies referred to herein and should refer to the risk warnings that have been sent to them by

Goldman Sachs International. A copy of these risks warnings, and a glossary of certain financial terms used in this report, are available from

Goldman Sachs International on request.

European Union: Disclosure information in relation to Article 4 (1) (d) and Article 6 (2) of the European Commission Directive 2003/126/EC is available

at http://www.gs.com/client_services/global_investment_research/europeanpolicy.html which states the European Policy for Managing Conflicts of

Interest in Connection with Investment Research.

Japan: Goldman Sachs Japan Co., Ltd. is a Financial Instrument Dealer under the Financial Instrument and Exchange Law, registered with the Kanto

Financial Bureau (Registration No. 69), and is a member of Japan Securities Dealers Association (JSDA) and Financial Futures Association of Japan

(FFAJ). Sales and purchase of equities are subject to commission pre-determined with clients plus consumption tax. See company-specific

disclosures as to any applicable disclosures required by Japanese stock exchanges, the Japanese Securities Dealers Association or the Japanese

Securities Finance Company.

Ratings, coverage groups and views and related definitions

Buy (B), Neutral (N), Sell (S) -Analysts recommend stocks as Buys or Sells for inclusion on various regional Investment Lists. Being assigned a Buy

or Sell on an Investment List is determined by a stock's return potential relative to its coverage group as described below. Any stock not assigned as

a Buy or a Sell on an Investment List is deemed Neutral. Each regional Investment Review Committee manages various regional Investment Lists to a

global guideline of 25%-35% of stocks as Buy and 10%-15% of stocks as Sell; however, the distribution of Buys and Sells in any particular coverage

group may vary as determined by the regional Investment Review Committee. Regional Conviction Buy and Sell lists represent investment

recommendations focused on either the size of the potential return or the likelihood of the realization of the return.

Return potential represents the price differential between the current share price and the price target expected during the time horizon associated

with the price target. Price targets are required for all covered stocks. The return potential, price target and associated time horizon are stated in each

report adding or reiterating an Investment List membership.

Coverage groups and views: A list of all stocks in each coverage group is available by primary analyst, stock and coverage group at

http://www.gs.com/research/hedge.html. The analyst assigns one of the following coverage views which represents the analyst's investment outlook

on the coverage group relative to the group's historical fundamentals and/or valuation. Attractive (A). The investment outlook over the following 12

months is favorable relative to the coverage group's historical fundamentals and/or valuation. Neutral (N). The investment outlook over the following

12 months is neutral relative to the coverage group's historical fundamentals and/or valuation. Cautious (C). The investment outlook over the

following 12 months is unfavorable relative to the coverage group's historical fundamentals and/or valuation.

September 20, 2010 China: Portfolio Strategy

Goldman Sachs Global Economics, Commodities and Strategy Research 22

Not Rated (NR). The investment rating and target price have been removed pursuant to Goldman Sachs policy when Goldman Sachs is acting in an

advisory capacity in a merger or strategic transaction involving this company and in certain other circumstances. Rating Suspended (RS). Goldman

Sachs Research has suspended the investment rating and price target for this stock, because there is not a sufficient fundamental basis for

determining, or there are legal, regulatory or policy constraints around publishing, an investment rating or target. The previous investment rating and

price target, if any, are no longer in effect for this stock and should not be relied upon. Coverage Suspended (CS). Goldman Sachs has suspended

coverage of this company. Not Covered (NC). Goldman Sachs does not cover this company. Not Available or Not Applicable (NA). The information

is not available for display or is not applicable. Not Meaningful (NM). The information is not meaningful and is therefore excluded.

Global product; distributing entities

The Global Investment Research Division of Goldman Sachs produces and distributes research products for clients of Goldman Sachs, and pursuant

to certain contractual arrangements, on a global basis. Analysts based in Goldman Sachs offices around the world produce equity research on

industries and companies, and research on macroeconomics, currencies, commodities and portfolio strategy. This research is disseminated in

Australia by Goldman Sachs & Partners Australia Pty Ltd (ABN 21 006 797 897) on behalf of Goldman Sachs; in Canada by Goldman Sachs & Co.

regarding Canadian equities and by Goldman Sachs & Co. (all other research); in Hong Kong by Goldman Sachs (Asia) L.L.C.; in India by Goldman

Sachs (India) Securities Private Ltd.; in Japan by Goldman Sachs Japan Co., Ltd.; in the Republic of Korea by Goldman Sachs (Asia) L.L.C., Seoul

Branch; in New Zealand by Goldman Sachs & Partners New Zealand Limited on behalf of Goldman Sachs; in Russia by OOO Goldman Sachs; in

Singapore by Goldman Sachs (Singapore) Pte. (Company Number: 198602165W); and in the United States of America by Goldman Sachs & Co.

Goldman Sachs International has approved this research in connection with its distribution in the United Kingdom and European Union.

European Union: Goldman Sachs International, authorized and regulated by the Financial Services Authority, has approved this research in

connection with its distribution in the European Union and United Kingdom; Goldman Sachs & Co. oHG, regulated by the Bundesanstalt für

Finanzdienstleistungsaufsicht, may also distribute research in Germany.

General disclosures

This research is for our clients only. Other than disclosures relating to Goldman Sachs, this research is based on current public information that we

consider reliable, but we do not represent it is accurate or complete, and it should not be relied on as such. We seek to update our research as

appropriate, but various regulations may prevent us from doing so. Other than certain industry reports published on a periodic basis, the large

majority of reports are published at irregular intervals as appropriate in the analyst's judgment.

Goldman Sachs conducts a global full-service, integrated investment banking, investment management, and brokerage business. We have

investment banking and other business relationships with a substantial percentage of the companies covered by our Global Investment Research

Division. Goldman Sachs & Co., the United States broker dealer, is a member of SIPC (http://www.sipc.org).

Our salespeople, traders, and other professionals may provide oral or written market commentary or trading strategies to our clients and our

proprietary trading desks that reflect opinions that are contrary to the opinions expressed in this research. Our asset management area, our

proprietary trading desks and investing businesses may make investment decisions that are inconsistent with the recommendations or views

expressed in this research.

We and our affiliates, officers, directors, and employees, excluding equity and credit analysts, will from time to time have long or short positions in,

act as principal in, and buy or sell, the securities or derivatives, if any, referred to in this research.

This research is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be

illegal. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of

individual clients. Clients should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, if

appropriate, seek professional advice, including tax advice. The price and value of investments referred to in this research and the income from them

may fluctuate. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur.

Fluctuations in exchange rates could have adverse effects on the value or price of, or income derived from, certain investments.

Certain transactions, including those involving futures, options, and other derivatives, give rise to substantial risk and are not suitable for all investors.

Investors should review current options disclosure documents which are available from Goldman Sachs sales representatives or at

http://www.theocc.com/publications/risks/riskchap1.jsp. Transactions cost may be significant in option strategies calling for multiple purchase and

sales of options such as spreads. Supporting documentation will be supplied upon request.

All research reports are disseminated and available to all clients simultaneously through electronic publication to our internal client websites. Not all

research content is redistributed to our clients or available to third-party aggregators, nor is Goldman Sachs responsible for the redistribution of our

research by third party aggregators. For all research available on a particular stock, please contact your sales representative or go to

http://360.gs.com.

Disclosure information is also available at http://www.gs.com/research/hedge.html or from Research Compliance, 200 West Street, New York, NY

10282.

Copyright 2010 The Goldman Sachs Group, Inc.

No part of this material may be (i) copied, photocopied or duplicated in any form by any means or (ii) redistributed without the prior written consent of The Goldman Sachs Group, Inc.