Embed Size (px)

Citation preview

EQUITY RESEARCH

UNITED STATES OF AMERICA HEALTHCARE - Medical Equipment & Supplies

MEDTRONICCOMPANY UPDATE: Prospects for 2004

BUYBUY

PAGE 1ANN RIFE COX ENDOWMENT FUND

|COXSMUSM

SCHOOL

OF BUSINESS

That’s a lot of Solid Heart Beats. April 8, 2004

COMPANY PROFILE

Medtronic is one of the largest medical technology

company that manufacturers implantable biomedical

devices, with sales to over 120 countries. The

Company treats chronic diseases by primarily offering

products, which include bradycardia pacing, tachy-

arrhythmia management, heart failure, atrial fi brillation,

coronary vascular disease, endovascular disease,

peripheral vascular disease, heart valve replacement,

extra-corporeal cardiac support, minimally invasive

cardiac surgery, malignant and non-malignant pain,

diabetes, urological disorders, gastroenterological

ailments, movement disorders, spinal surgery,

neurosurgery, neurodegenerative disorders and

ear, nose and throat (ENT) surgery. Medtronic

operates in fi ve business segments: Cardiac Rhythm

Management (CRM); Neurological and Diabetes;

Spinal, Ear, Nose and Throat, and Surgical Navigation

Technologies (SNT); Vascular, and Cardiac Surgery.

Cardiac Rhythm Management products (bradycardia

& tachycardia) accounted for 47.4% of 2002 sales;

Neurological, Spinal, and Diabetes, 35.3%; Vascular

products (stents), 10.1%; and Cardiac Surgery (heart

values, perfusion systems), 7.2%.SOURCE: Valueline and Reuters.com

INVESTMENT THESIS

Healthy, diverse revenue base with a strong balance sheet. Although Medtronic is trading

at a premium, their diverse business combinations and rich cash fl ow offers management an

opportunity to augment internal growth with further acquisitions and stock repurchases.

Favorable demographics and trends will drive growth in the market. Irrespective

of company size and product, Medtronic’s overall customer base seems to be expanding

domestically and overseas as changing demographics and rising standards of living will

demand a steady stream of new and improved medical products.

Market consensus expects growth expectations for 2004 and 2005 to be around 15%.

After with net income falling in 2001 and 2002 – due to increased acquisitions and competition

from drug-eluting stents (DES), Medtronic’s businesses have strengthen and stabilized with

diversifi ed product lines. The Company’s bare metal stents seems to be performing well

in Europe and is again penetrating the DES (medical devices that improve coronary artery

disease) market. Meanwhile, the important CRM business will perservere positively, given

both a recent sharp increase in reimbursement for Medicare and a strong product pipeline.

Research & Development (R&D) expenditures have continued to pay off. Medtronic

recently launched two FDA-approved heart devices designed to treat irregular heart beats and

abnormalities. The Food and Drug Administration (FDA) also approved their CD Horizon

Legacy 5.5 spinal system. Further, the FDA approved the Guardian continuous glucose

monitoring system. Also, Medtronic’s Physio-Control division announced a partnership

with Walgreens to sell automated external defi brillators online. Medtronic further received

Japanese approval for their Sprinter Semi-Compliant Rapid Exchange Balloon Dilatation

Catheter. Additionally, Medtronic is continuing SCD-HeFT research, the largest implantable

cardioverter defi brillators (ICD) trial to date, for benefi ts of ICDs in a broad group of patients

at risk of sudden cardiac arrest. Results of this Medtronic-National Institute of Health co-

sponsored trial will emerge near the end of fi scal year 2004. Recently, Medtronic received

FDA-approval to begin its Endeavor III clinical study – a randomized trial study evaluating

the safety and effi cacy of Medtronic’s Endeavor DES.

DES represents an opportunity for further growth for Medtronic in 2004-2006. Drug-

coated stents constitute the next, biggest development in stent technology and promise to

double the size of $2.5 billion sector. Data from Endeavor I and II DES showed positive

results, and their DES program remains on track to obtain European approval in late 2004,

US approval in late 2005, and Japanese approval in late 2006. If expectations fall through,

Medtronic will be the third market entrant in the US DES market after Boston’s Scientifi c’s

recent Taxus DES FDA-approval. According to Merrill Lynch Research, Medtronic could

potentially capture US DES revenues of $360-plus million and 10% of the market share.

Benjamin Q. Luong Email: [email protected]

Kanaiya Kapadia Email: [email protected]

Miranda Peters Email: [email protected]

Ryan Wannemacher Email: [email protected]

FINANCIAL STATISTICS

Price: $48.90 (as of April 8, 2004)

Symbol | Exchange: MDT | NYSE

52-Week Range: $42.90-$52-92

Market Capitalization: $59.169 billion

Shares Outstanding: 1,210 billion

Relative Price-to-Earnings (P/E): 1.10

Trailing P/E: 31.96 (Stock) vs. 30.85 (Industry)

Forward P/E: 25.70 (Stock) vs. 22.50 (Industry)

Current PEG Ratio: 1.8 (Stock) vs. 1.51 (Industry)

Forward PEG Ratio: 1.6 (Stock) vs. 1.25 (Industry)

Return on Assets (ROA): 18.1%

Return on Equity (ROE): 19.3%

Annual Dividend: 0.30

Dividend Yield: 0.59%

Price Target: $59.39

Financial History

SOURCE: Company

Reports

MDT | PAGE 2SOUTHERN METHODIST UNIVERSITY

ANN RIFE COX ENDOWMENT FUNDSMU : COX SCHOOL OF BUSINESS

BUSINESS MODEL

The Medical Equipment and Supplies Industry develops,

manufactures and markets products used to improve patient

health. These include commodity-type items such as kits, trays,

gloves, gowns, syringes, and other disposable medical supplies.

Medical device products provide a steady cash fl ow for companies

and usually some of their revenues are budgeted for Research &

Development (R&D). Important value-added products include

infusion and related intravenous supplies and equipment,

diagnostic and laboratory products, wound-management

supplies, orthopedic, reconstructive implants, spinal devices,

surgical devices, cardiac products, and diagnostic equipment.

The Industry’s most profi table groups are those involved with

innovative high-technology products, such as implantable

and external cardiac defi brillators, orthopedic devices, and

sophisticated diagnostic imaging systems. New products will be

the engine of growth in the market because they have a very high

growth potential. Currently, the Standard & Poor’s (S&P) Health

Care Equipment Index gained 8.4% compared to a 1.1% gain from

the consolidated S&P Health Care Index.

Business Segments

Generally, markets for certain products, such as cardiac and

orthopedic devices are dominated by a small number of players,

including Medtronic, Guidant Corporation, and Boston Scientifi c.

Currently, the industry is intensifying into new market prospects,

such as orthobiologics, deep brain stimulation, drug-coated

coronary stents, congestive heart failure treatment, and robotic

surgery. The United States (US) will particularly benefi t

cardiovascular products, such as pacemaker, defi brillators, and

angioplasty catheters, which are used mostly on elderly patients.

Also, this Industry represents several, developed business

segments that Medical Device manufacturers can derive their

revenues from: Cardiology, Diagnostic Imaging, Orthopedics,

In-vitro Diagnostics, Peripheral Vascular Disease, and other (see

Chart A).

Cardiology: In 2002, worldwide medical device sales accounted

for approximately 6.9%. Cardiac Rhythm Management (CRM)

represented 44% of the cardiology market. Other products such as

coronary stents took 17%; angioplasty, angiographic catheters and

other interventional devices accounted for 13%; products used

in bypass procedures, heart values and other surgical items took

15%; vascular grafts and other vascular products contributed 5%,

and the rest, 6%. According to the American Heart Association’s

Heart and Stroke Statistical Update 2002, since 1999, 62 million

Americans had some form of cardiovascular disease (CVD) and

accounted for 40.1% of all deaths that year. Since 1900, CVD

has been the Number One killer in the US every year, except

1918. Global CVD market is expected to expand by 13% to 14%

annually through 2007 (see Chart C).

Diagnostic Imaging: This particular segment has been steady,

measuring in the range between $4.5 billion to $5.0 billion. As

of to date, diagnostic imaging product sales still come from

conventional x-ray equipment, ultrasound imaging, magnetic

resonance imaging, radiation therapy, nuclear medicine, and

computed tomography.

Orthopedics: These products are used to repair or replace parts of

the human skeletal system. Generally, they have been achieving

a compound annual growth rate of 7 to 9%, generating global

orthopedic industry generated sales of about $13 billion. US,

Europe, Asia, and other markets have contributed sales of 63%,

19%, 13%, and 5%, respectively. An area growing faster than 20%

annually, is the $2.4 billion spine market. Over 10,000 spinal cord

injuries occur each year in the US and nearly 50% of which are

related to motor vehicle accidents. Additionally, in the US, there

are 1.1 million spinal procedures each year.

In-vitro Diagnostics: This segment represents a worldwide

market worth of about $23 billion, accounting for an estimated

12% of total industry sales. In-vitro diagnostics involve tests

performed on blood, urine, and other body fl uids and tissues to

detect pathological conditions. For overseas markets, especially

in development nations, a stronger growth in this segment is

expected.

Peripheral Vascular Disease (PVD): This newly-interested

segment focus on non-coronary diseases of the vascular system,

including the brain. For instance, the most prevalent diagnosis

is a stroke. PVD affects about one in 20 persons over the age

of 50 or about eight million people in the US. PVD is attractive

to medical device manufacturers because they can extend their

patient treatment capacity to both arterial and venous diseases and

aneurysms (localized swellings in arteries). Guidant, Medtronic,

and Boston Scientifi c have become leading innovators in this

segment market.

Specifi cally, Medtronic’s diverse core businesses focus in

Cardiology, Orthopedics, Peripheral Vascular Disease, and

Neurology areas (see Chart E).

CHART A : Projected US Sales for 2005

SOURCE: Standard & Poor’s

MDT | PAGE 3SOUTHERN METHODIST UNIVERSITY

ANN RIFE COX ENDOWMENT FUNDSMU : COX SCHOOL OF BUSINESS

OVERALL MARKET PERSPECTIVE

Market Size

The worldwide medical device business represented a global

market of about $190 billion in 2002 — an increase of about 10%

from $172 billion in 2001. According to Standard & Poor’s, US

medical device manufacturers continue to generate about 40% of

their unit sales in foreign markets, regardless of the pricing benefi ts

accruing from a weakened US dollar relative to both the Euro and

the Yen. During 2002, about $85 billion, or 45%, of industry sales

were generated overseas.

Industry Outlook

Industry outlook remains favorable and positive. According

to Standard & Poor’s, worldwide market growth for medical

supplies and devices is expected to be around 12% as of mid-

2003. While rising healthcare cost seems to be the focus around

the world, the aging population, the availability of new and better

medical treatments, and the global demand for healthcare products

and services continues to be strong worldwide, particularly in

developing markets. U.S. companies are benefi ting from sales of

new technology devices by forcing a premium on unit pricing in

comparison to older products. Aided by price and volume increases

and favorable foreign exchange fl uctuations, Standard & Poor’s

expect industrywide sales growth will approximate 15% growth in

2004. Interventional cardiology and cardiac rhythm management,

spinal surgery and orthopedic joint replacements will be among

the products that will contribute to that growth. Earnings will be

expected to grow approximately 18% to 20% in 2004. Expansion

in gross margins due to a higher proportion of sales from new

products, stable R&D outlays, reduced interest costs, and positive

tax rate implications will drive this performance measure.

Recently, the Centers for Medicare & Medicaid Services proposed

new rates for implantable cardioverter defi brillators (ICDs)

which will increase Medicare reimbursements by 3.9%. This

guideline as well as few other legislations, such as Medicare RX

($400 billion budget allocated for the elderly) is expected to

increase the number of people receiving ICDs by about 65,000

per year. An increase in Medicare reimbursements is seen as a

positive factor.

Drug-coated (or -eluting) coronary stents have become the

center of the attention. The fi rst product line approval by the

FDA was given to Johnson & Johnson (J&J) for their Cypher stent.

This drug device is intended to help reduce restenosis (reblockage)

of a treated coronary artery. Coronary stents are fl exible metal

tubes that are inserted into diseased coronary arteries after an

angioplasty procedure — a catheter with a small balloon at the

end is inserted into a blocked artery. Once the infl ating balloon

clears the blockage, the balloon catheter is removed and the stent,

which acts as a platform to keep the artery open, is inserted.

While the procedure can effectively restore blood fl ow to the

heart and often eliminates the need for invasive coronary artery

bypass graft (CABG) surgery, vessel reclosure or restenosis at

the site of the stent may occur. This negative after-effect can be

treated by coating the stent with drugs. Recently, medical device

companies have demonstrated that drug-coated coronary stents can

signifi cantly reduce restenosis. The drugs used to coat coronary

stents are anticancer compounds that inhibit cell proliferation and

dynamically allows for release of the drug over a period of time.

So far, J&J has been unable to meet all of the demand coming

from physicians and their patients for their Cypher product,

which leaves ample room for competitors to penetrate the market.

Coronary stents presently account for industrywide sales of $2.5

billion or about 19% of the interventional cardiology market. As

other companies gain FDA approval for their drug coated stent,

the global stent market will reach $4.5 billion by the end of 2004

(see Chart B).

Increases in Mergers & Acquisitions. A number of smaller

acquisitions are taking place run by some of the largest players,

who seek to fi ll their product lines with niche acquisitions. These

deals will provide great opportunity for them to capitalize on the

recent increases in stock prices and historically low levels of

interest rates.

Continued aging population = more patient population.

Medicare constituents at the age of 65 and older may more than

double in the coming decades, from 37 million today to 70 million

in 2030 and 82 million in 2050. Although the elderly represents

slightly less than 13% of the total US population, they contribute

an estimated 40% of total healthcare expenditures. Also, an aging

bundle of baby boomers will provide further stimulus for industry

wide demand. Baby boomers currently represent 23% of the US

population. According to the World Health Organization, the

global over-65 age population is projected to rise from 390 million

in 1997 to 800 million people by 2025. However, an expected 24

million deaths per year will increase in the years ahead mostly

because many people have unhealthy lifestyles, such as smoking,

obesity, poor diet, or lack of exercise.

CHART B : Drug-Eluting Stent (DES) Market

SOURCE: Standard & Poor’s

MDT | PAGE 4SOUTHERN METHODIST UNIVERSITY

ANN RIFE COX ENDOWMENT FUNDSMU : COX SCHOOL OF BUSINESS

Outpatient procedures heightens equipment sales. Inpatient

procedures are shifting towards the less expensive outpatient

settings. Nearly 75% of all surgical procedures will be performed

on an outpatient basis because new medical device technology

has helped fuel this trend. With the aid of new medical products,

surgeons now perform a one-day surgical procedure for conditions

that once required expensive inpatient surgery, lengthy and

expensive hospital stays, and weeks of recuperation.

Managed care enterprises = Biggest customer. Managed Care

enterprises have developed infl uential, bargaining power within

medical markets. Managers of health maintenance organizations

(HMOs), preferred provider organizations (PPOs), large hospital

consortiums, government agencies, and other large managed

care buyers have made more purchasing decisions. For instance,

60% of all medical device purchases in the United States are

made by managed care buyers, and this percentage is projected

to rise to over 80% by 2005, according to the Advanced Medical

Technology Association.

Increased Internet-based sales usage. In order to combat

competitive pricing pressures on gross margins, many medical

device manufacturers have resorted to the Internet to close this

offset by boosting shipment volumes.

PRODUCTS AND SERVICES (see Chart D and G)

Medtronic operates in fi ve key business units developing products

in Cardiac Rhythm Management (CRM), Cardiac Surgery,

Vascular, Neurological and Diabetes, and Spinal, ENT and SNT.

Medtronic CRM develops products that restore and regulate a

patient’s heart rhythm, as well as improve the heart’s pumping

function. The business markets implantable pacemakers,

defi brillators, cardiac ablation catheters, monitoring and diagnostic

CHART D : Medtronic Product Pipeline

CHART C : Cardiovasuclar IndustrySOURCE: Standard & Poor’s

SOURCE: Company Reports & Website

MDT | PAGE 5SOUTHERN METHODIST UNIVERSITY

ANN RIFE COX ENDOWMENT FUNDSMU : COX SCHOOL OF BUSINESS

devices and cardiac resynchronization devices, including the fi rst

implantable device for the treatment of heart failure. In addition,

the business markets automated external defi brillators (AEDs)

- which are increasingly being placed in public places, such as

businesses, airports, shopping centers and even homes - and

the industry’s fi rst Internet-based network to enable physicians

to remotely monitor their patients who have cardiac devices.

Medtronic Cardiac Surgery develops products that are

used in both arrested and beating heart bypass surgery.

The business also markets the industry’s broadest line

of heart valve products for both replacement and repair,

plus autotransfusion equipment and disposable devices

for handling and monitoring blood during major surgery.

Medtronic Vascular develops products and therapies that treat a

wide range of vascular diseases and conditions. These products

include coronary, peripheral and neurovascular stents, stent graft

systems for diseases and conditions throughout the aorta, and distal

protection systems. The business is also moving forward with the

development of a drug-eluting stent to prevent restenosis. Medtronic

Vascular also markets a full line of balloon angioplasty catheters,

guide catheters, guidewires, diagnostic catheters and accessories.

Medtronic Neurological and Diabetes offers therapies for

movement disorders, chronic pain and diabetes. It also offers

diagnostics and therapeutics for urological and gastrointestinal

conditions, including incontinence, benign prostatic hyperplasia

(BPH)/enlarged prostate and gastroesophageal refl ux disease

(GERD). Products include infusion and neurostimulation systems,

as well as shunts and powered surgical tools for cranial surgery.

Medtronic Spinal, ENT and SNT develops and manufactures

products that treat a variety of disorders of the cranium

and spine, including traumatically induced conditions,

deformities and tumors. It also develops image-guided

surgical navigation systems (SNT) and a wide range of

products for use in ENT (ear, nose and throat) procedures.

COMPETITION

Three main competitors fight for this market: Guidant Corporation,

St. Jude Medical, and Boston Scientific Corporation (see Chart D,

E, F and Exhibit 1). Medtronic ranks 1st among others due to their

diverse product segments and sales, capturing much of CRM.

Guidant Corporation (GDT)

The Company develops, manufactures and markets implantable

defi brillator systems, implantable pacemaker systems, coronary

stent systems, angioplasty systems and cardiac surgery systems.

Guidant’s lifesaving medical technologies are designed to improve

life-threatening cardiac and vascular disease. Its primary medical

devices treat the heart, managing its rhythms, clearing its arteries

and permitting less-invasive surgeries. Guidant has principal

operations in the United States, Europe and Asia. Guidant recently

won FDA approval for their new cardiac devices and ICD.

SOURCE: Yahoo!.com

CHART E : Competitve factors - Product Line SalesSOURCE: Standard & Poor’s

CHART D : Competitve factors - Geographic Sales

MDT | PAGE 6SOUTHERN METHODIST UNIVERSITY

ANN RIFE COX ENDOWMENT FUNDSMU : COX SCHOOL OF BUSINESS

St. Jude Medical, Inc. (STJ)

Together with its subsidiaries, STJ develops, manufactures and

distributes cardiovascular medical devices for the global cardiac

rhythm management (CRM), cardiac surgery (CS) and cardiology

and vascular access (C/VA) therapy areas. The Company’s

principal CRM products are bradycardia pacemaker systems

(pacemakers), tachycardia implantable cardioverter defi brillator

systems and electrophysiology catheters. Its principal CS

products are mechanical and tissue heart valves, and valve repair

products. C/VA products offered include vascular closure devices,

angiography catheters, guidewires and hemostasis introducers.

The principal geographic markets for St. Jude Medical’s products

are the United States, Europe and Japan. The Company also sells

its products in Canada, Latin America, Australia, New Zealand and

the Asia-Pacifi c region.SOURCE: Yahoo!.com

Boston Scientific Corporation (BSX)

A worldwide developer, manufacturer and marketer of medical

devices whose products are used in a range of interventional

medical specialties, including interventional cardiology, peripheral

interventions, neurovascular intervention, electrophysiology,

vascular surgery, endoscopy, oncology, urology and gynecology.

The Company’s products are offered for sale by two dedicated

business groups, Cardiovascular and Endosurgery. The

Cardiovascular organization focuses on products and technologies

for use in interventional cardiology, peripheral interventions,

vascular surgery, electrophysiology and neurovascular

procedures. The Endosurgery organization focuses on products

and technologies for use in oncology, endoscopy, urology and

gynecology procedures. During 2003, approximately 72% of

the Company’s net sales were derived from the Cardiovascular

business and approximately 28% from the Endosurgery business.

Boston Scientifi c recently won FDA approval for their Taxus DES

and launched their Sentinol self-expanding Nitinol Biliary Stent

System. Boston recently acquired Precision Vascular for new

projects in interventional cardiology, oncology, and endoscopy.

SOURCE: Yahoo!.com

RISK ANALYSIS

According to S&P, widening government budget defi cits both

in the US and abroad may result in industrywide pricing

pressure. Thus, longer-term growth in healthcare spending may

slide steeply.

Foreign markets are stressed out. Europe: France and

Germany account for nearly 50% of the continent’s medical device

sales. Due to increased budget defi cits, these two countries have

focused on lowering healthcare expenditure levels. Japan: At

about $24 billion annually, Japan is the largest global market for

medical technologies. US manufacturers exports about $2 billion

to Japan each year. According to the S&P, Japan represents about

10% of industry sales by US manufacturers in 2002. However,

trends indicated this has fallen in recent years. China: In order to

combat these political policies, US medical device manufactures

have resorted to the Chinese market — an area of potential

growth. According to the US Department of Commerce, US

medical device exports to China doubled to $227 million from

1997 to 2002. Regardless, Medtronic’s foreign operations could

be negatively impacted by changes in foreign policy changes on a

political, social and economic level.

Additionally, foreign governments frequently impose

reimbursement limits. In effect, government spending will be

controlled and their citizens will be able to obtain medical products

and services at a low cost. Executive decisions regarding limiting

or eliminating reimbursement for Medtronic products may have a

materially adverse affect on their net earnings.

Increased Market Risk. Due to the global nature of their

operations, Medtronic is also susceptible to foreign currency

exchange rate fl uctuations. However, the primary currencies are

hedged towards the Euro and the Japanese Yen so that earnings

and cash fl ow volatility will be minimized. In 2002, foreign

translations were favorable in sales and product growth.

Increased regulatory requirements from Food and Drug

Administration (FDA) and other comparable foreign agencies.

There has been an increase in the amount of testing, such as side-

effects testing, and documentation required for FDA clearance of

new drugs and devices, which consequently increases new product

introductions expenses. Future FDA approval or non-approval

of medical devices could adversely impact Medtronic’s fi nancial

condition and market position.

Increased Legal Implications. While companies must navigate

FDA requirements prior to commercializing their products,

intellectual property lawsuits, such as patent infringements, are an

important risk element, along with potential product recalls. Many

suits, involving Guidant, J&J, Boston Scientifi c, Arterial Vascular

Engineering, and Medtronic still have ongoing battles with each

other with fi nal rulings still pending. Medtronic also operates

in an industry vulnerable to product liability claims brought by

individuals or class groups seeking monetary relief.

CHART F : Competitive Factors Matrix*

*Ratings based on three factors on a scale from 1 to 5: CRM Sales, COGS-to-

Sales, and Patents. Medtronic (blue), Guidant (purple), St. Jude (yellow), Boston

Scientifi c (baby blue).

MDT | PAGE 7SOUTHERN METHODIST UNIVERSITY

ANN RIFE COX ENDOWMENT FUNDSMU : COX SCHOOL OF BUSINESS

CUSTOMERS

Medtronic’s revenue base includes a diverse mixture of customers

from around the world. The Company supply medical device

products for health care facilities, such as managed care

enterprises and hospitals; physicians and profi t and non-profi t

organizations in the fi eld of cardiology, cardiovascular surgery,

electrophysiology, endrocrinology, ENT surgery, gastroenterology,

guided surgery (SNT), neurology, neurosurgery, oncology, pain

management, spinal surgery, urology/urogynecology, vascular

and many other medical fi elds; and patients with diseases,

such as Abdominal Aortic Aneurysm (AAA), Bladder Control

Problems, Benign Prostatic Hyperplasia (enlarged prostate),

Cancer, Diabetes, Digestive Problems, Heartburn (GERD), Heart

Conditions, Hydrocephalus, Ménière’s Disease, Pain, Parkinson’s

Disease, Seizures and Fainting, Severe Spasticity, Shaking/Tremor,

Sinusitis, Spinal Disorders, Unexplained Fainting and many other

chronic diseases.

DUE DILIGENCE

Medisend is a non-profi t organization based in Dallas and recycles

the medical surplus (surgical, diagnostic, and therapeutic medical

supplies and equipment) of wealthy countries. According to

Medisend, more than $6 billion worth of medical surplus is

generated in the US. Medisend gathers these medical surplus and

distributes them to more than 71 countries. In their biomedical

equipment storage area, Medisend carries numerous working

equipment that have been replaced by newer technology.

Medisend receives requests from these 71 developing countries

for their older generation biomedical equipment because there

is a shortage and a lack of government funds to purchase new

equipment. However, with only a small amount of equipment

left in stock, Medisend can supply those countries with limited

capability. Thus, Medisend suggested that overall demand for new

or old equipment and supplies will accelerate in the future.

PAST ACQUISITIONS

Medtronic slid downwards during 2001 and 2002 due to

increased acquisitions, but has now stabilized and strengthen

their diversifi ed product lines for future growth. For instance, the

Company acquired Spinal Dynamic Corporation for development

of an artifi cial disc designed to maintain mobility of the cervical

spine. The artifi cial disc is currently marketed in Europe and will

hit the US markets by 2007. During the second quarter of 2002,

the Company completed acquisitions in Minimed (world leader

in developing medical systems for treating diabetes) and Medical

Research Group (developer of implantable pumps and sensors for

treating diabetes) for a total purchase price of $3.807 billion. In the

third quarter of fi scal year 2002, Medtronic acquired Endonetics

(developer of technologies for the diagnosis and treatment of

gastroesophageal refl ux disease or GERD) for $67.2 million. In

the fourth quarter of fi scal year 2002, the Company also acquired

VidaMed, Inc. (developer of non-surgical treatment products for

benign prostatic hyperplasia or BPH) for $328.6 million.

MANAGEMENT & OWNERSHIPSource: Dun & Bradstreet and Yahoo!.com

CEO & CHAIRMAN: ARTHUR D COLLINS JR (1948)

Graduated Miami University of Ohio. Graduated Wharton School,

MS in business administration. 1978-1992 Abbott Laboratories,

various management positions, lastly Corporate Vice President.

Jun 1992-present: Medtronic, Inc.

CHIEF FINANCIAL OFFICER: ROBERT L RYAN (1943)

Prior to 1982 several management positions at Citibank and

McKinsey & Company. 1982-1993 Union Texas Petroleum Corp,

treasurer, 1983 Controller, 1984 Vice President Finance and Chief

Financial Offi cer.

Apr. 1993-present Medtronic, Inc, Senior Vice President and

Chief Financial Offi cer

GENERAL COUNSEL DAVID J SCOTT

He came to Medtronic from United Distillers & Vintners (UDV)

in London, England, where he has served as general counsel since

1997. Prior to that, he served as Senior Vice President and General

Counsel for London-based International Distillers & Vintners

(IDV). He graduated from Cornell Law School in 1978 and started

his professional career as a trial lawyer in upstate New York.

SENIOR EXECUTIVE STEPHEN MAHLE

He has been Senior Vice President and President, Cardiac

Rhythm Management, since January 1998. Prior to that, he was

president, Brady Pacing, from May 1995 to December 1997 and

vice president and general manager, Brady Pacing, from January

1990 to May 1995. Mr. Mahle has been with the company for 28

years and served in various general management positions prior

to 1990.

SENIOR EXECUTIVE ROBERT M GUEZURAGA

He has been Senior Vice President and President, Cardiac Surgery,

since August 1999, and served as Vice President and General

Manager of Medtronic Physio-Control International, Inc., from

September 1998 to August 1999. Mr. Guezuraga joined the

company after its acquisition of Physio-Control International, Inc.

in September 1998, where he had served as president and chief

operating offi cer since August 1994. Prior to that, Mr. Guezuraga

served as president and CEO of Positron Corporation from 1987

to 1994 and held various management positions within General

Electric Corporation, including GE’s Medical Systems division.

Breakdown of Major Holders

% of Shares held by All Insider and 5% Owners: 1%

% of Shares held by Institutional & Mutual Fund Owners: 70%

% of Float held by Institutional & Mutual Fund Owners: 70%

Number of Institutions Holding Shares: 10

MDT | PAGE 8SOUTHERN METHODIST UNIVERSITY

ANN RIFE COX ENDOWMENT FUNDSMU : COX SCHOOL OF BUSINESS

FUNDAMENTAL ANALYSIS (see Exhibit 1)

Sales and Net Income (see Chart G)

Medtronic ranks 1st

in sales and net income among our

choice of comparable companies. Net income was driven by

growth in Medtronic’s Cardiac Rhythm Management (CRM) and

Spinal, Ear, Nose, and Throat (ENT), and Surgical Navigation

Technology (SNT) operating segments. CRM net sales increased

23% because of new product introductions, continued strong

growth in existing products, growth in the emerging heart failure

market, and the acceleration in growth of the tachyarrhythmia

market. Therefore, Medtronic achieved a 47% increase in net

sales of implantable defi brillators and a 10% increase in net sales

of pacing systems. Spinal, ENT, and SNT net sales increased 32%

because of continued strong growth in existing products, growth

in the spinal market, continued acceptance of their INFUSE Bone

Graft product for spinal fusion and their rapidly growing family of

MAST (Minimally Access Spine Technologies) products.

Earnings per Share (EPS) Medtronic seems to be the underperformer in EPS each

year, but still exhibits EPS growth appreciation each year. We

believe Medtronic’s different fi scal year-end date among others

accounts for this discrepancy or offset as there may be cyclical

factors not incorporated into EPS estimates.

Balance Sheet Medtronic has a large cash amount of $1,190.3 billion,

which allows them to potential pursue opportunities to capitalize

on new investments. Total debt, common equity, assets, receiv-

ables, and inventory are high across the board.

Stock Data

Medtronic’s current stock price is relatively low among

the comparable companies. Medtronic also possess higher than

aggregate common shares, market capitalizations and enterprise

value.

Financial Ratios Medtronic exhibited a high Last Fiscal Year (LFY) EBIT-

DA margins of 30.6% against other comparable companies. Yet,

Medtronic and Guidant also hold LFY gross margins of approxi-

mately 75%. Medtronic maintains relatively well-above averaged

and better Return on Equity (ROE) of 19.3%, shy under St. Jude

Medical’s ROE of 20.9%. Return on Assets (ROA) in terms of

measuring profi tability for Medtronic is also well-above average

at 18.1%. Current ratio is also very low at 1.11, indicating that

Medtronic is less liquid than others.

Growth Historical 3-year revenue growth rate for Medtronic

looks attractive at 15.18% while St. Jude has a history of 17.91%

growth. Medtronic’s year-over-year (YOY) EPS growth and pro-

jected growth in EPS with the next fi ve years is relatively moder-

ate at around 16%. However, Morningstar.com determined the

latest quarter YOY EPS growth rate to be 56.0%. Also, Medtronic

offers a Dividend Yield of 0.59%.

Risk Debt does not seem to be a critical risk factor for Medtron-

ic. Standard and Poor’s Rating Group and Moody’s Investors Ser-

vice issued Medtronic a strong long-term debt ratings of AA- and

A1, respectively, and strong short-term debt ratings of A-1+ and

P-1, respectively. Current ratings have remained unchanged and

rank Medtronic in the top 10% of all U.S. companies.

Relative Valuation Medtronic’s Current Fiscal Year (CFY) Price-to-Earn-

ings (P/E) is fairly high at 30.0 while Next Fiscal Year (NFY) P/E

also remains high at 25.7. Because the P/E ratios are somewhat

high, the market seems to be more willing to pay for each dollar of

annual earnings. However, Medtronic’s TTM P/E ratio of 31.96

is lower than its main competitors whereas Boston Scientifi c,

Guidant and St. Jude Medical have P/E ratios of 78.52, 51.9, and

40.49, respectively. Also, Relative P/E is high at 1.10, but below

St. Jude Medical’s 1.24. Additionally, Medtronic’s current P/E-to-

Growth (PEG) ratio is high at 1.8 when compared to the Industry’s

1.51 PEG ratio. NFY PEG also remains high at 1.6 for Medtronic.

TTM PEG ratio of 1.68 from Medtronic lies between Boston Sci-

entifi c’s and St. Jude Medical’s PEG numbers. In sum, Medtronic

demonstrates an overall easing combination of comparative, valu-

ation measures.

DFCF MODEL ASSUMPTIONS (see Exhibit 2)

We made several assumptions that will serve as inputs into our

DFCF model for simplicity purposes.

Capital Expenditures-to-Depreciation ratio Using Medtronic’s 2003 fi nancial fi gures, we arrived at

a ratio of 0.93 and gradually grew to 1.50 for purposes of grow-

ing capital expenditures and expectations that the Company will

pursue investments throughout forecasted years. The decrease

in capital expenditures from 2003 to 2004 results from a sharp

decrease in Long-term Net Assets from 2003 to 2004 as working

capital dramatically increased in 2003.

Revenue growth % Historically, Medtronic has achieved around 15% rev-

enue growth each year. We have conservatively determined that

Medtronic will implicitly grow at an average of 12.8% throughout

forecasted years, although market consensus predict 15%. For

years 2004 and 2005, we project revenue to grow at 11%. In the

years 2006 to 2009, we expect Medtronic to recognize at least

12% revenue growth based on new product releases. Gradually,

revenue growth will drop 100 basis points and will eventually

reach 12% towards the terminal year. We also expect Medtronic

to receive large synergies from their entrance in the DES market

during years 2005 to 2009. By 2010 and beyond, Medtronic may

pursue expansion plans and in effect, may reduce revenue growth.

MDT | PAGE 9SOUTHERN METHODIST UNIVERSITY

ANN RIFE COX ENDOWMENT FUNDSMU : COX SCHOOL OF BUSINESS

Our revenue assumptions are based on the following reasons: our

investment thesis outlined at the beginning, increased competi-

tion that could detract revenues from Medtronic, increased price

pressure from foreign markets and competition, strong product

demand, and solid business segments. We also believe Medtronic

will be able to sustain 12% revenue growth terminally for these

following reasons in addition to continuing, favorable demograph-

ics.

Cost of Goods Sold (COGS) and Selling, General, and

Administrative (SGA) Effi ciencies We assumed COGS growth effi ciencies to range from

11.6% to 11.7% growth each year — in-line with about 24% of

revenues produced each year (see Exhibit 2 - Key Percentages).

We also assume SGA growth effi ciencies to slowly decline from

11.5% to 11.3% (in-line with about 31% of revenues produced

each year) towards terminal year as Medtronic attempts to estab-

lish signifi cant quality measures. However, we projected 11.5%

SGA growth in the terminal year for perpetuity.

Depreciation-to-Assets Using Medtronics’ 2003 fi nancial fi gures, we arrived at

4.3% (also see Exhibit 2 - Key Percentages) and assumed this per-

centage remained constant for purposes of growing depreciation

throughout forecasted years.

Debt Interest Rate % Using interest expense by long-term and short-term debt,

we determined the debt interest rate to be 8.3% and assumed this

percentage remained constant for purposes of growing interest

expense throughout forecasted years.

Tax rate Medtronic has benefi ted from their tax strategies that

allowed them to use a tax rate below the standard. Therefore, we

used a fair tax rate of 31.7% for 2003 and kept this fi gure constant

throughout forecasted years.

Working Capital Growth

Working capital dramatically increased from 2002 to

2003. According to Company reports, the increase in working

capital primarily relates to the reclassifi cation of $1,973.8 million

of contingent convertible debentures from current liabilities to

long-term liabilities in the second quarter of fi scal year 2003. In

April 26, 2002, Medtronic’s working capital, current ratio, and net

cash position were negatively impacted by the $4,057.6 million

of cash paid in fi scal year 2002 for acquisitions. From 2004 and

beyond, we normalized working capital and long-term net assets

by growing working capital at fl exible growth rates. We assumed

working capital to slowly grow at 8% by 2007 after assuming

Medtronic achieves 12% revenue growth from their DES and

other product releases in 2006.

Debt Growth We assumed a 10% growth in debt for the next three years

as Medtronic utilizes new capital for R&D expenses for furthering

completion of product trials and then moderately grew their debt

to 15% by 2006.

Key Percentages for 2003 Percentages for each line item indicate as percentage of

revenue except for Depreciation, which is a ratio between current

year’s Depreciation and previous year’s Long-term net assets.

These percentages were used to forecast most line items in fore-

casted years (see Exhibit 2).

Beta We regressed the beta equity of the fi rm using Medtronic

and S&P returns of the last ten years to arrive at 0.964 (see Exhibit

3).

Weighted Average Cost of Capital (WACC) With our inputs and class consensus of a risk-free rate of

2.7% and a Market Premium of 6%, we calculated the WACC to

be 8.48% for the levered fi rm (see Exhibit 3).

Terminal Growth % We used 4% as a terminal growth input to determine the

intrinsic value of the company (see Exhibit 4).

FINAL VALUATION & CONCLUSION

Based on our assumptions, we have determined that Medtronic

is undervalued on a Discounted Free Cash Flow (DFCF) basis.

We feel that Medtronic has the capability and the capacity to

pursue and achieve much growth in the industry. We also feel

Medtronic’s diverse business segments will attract a large portion

of the overall customer base, capturing signifi cant revenues, and

thus, justifi es the premium price. If Medtronic performs better

than expected 15% revenue growth over our forecasted 13% in the

coming years, Medtronic will undoubtedly be an attractive stock

in comparison to other competitors and be in a strong position.

Further, we believe favorably that Medtronic will be able to obtain

FDA-and-abroad approval as well as penetrate the DES market

as a top-line competitor. In conclusion, we view these factors,

including favorable investment highlights, positive qualitative

and quantitative analysis, modest fundamentals, and strong

management structure constitute Medtronic an attractive buy.

MDT | PAGE 10SOUTHERN METHODIST UNIVERSITY

ANN RIFE COX ENDOWMENT FUNDSMU : COX SCHOOL OF BUSINESS

EXHIBIT 1 : Comparable Company Analysis

Rex

Th

om

pso

n P

/E A

ggre

gate

Rati

o (

Th

om

pso

n P

EA

R)

The

Thom

pso

n P

EA

R m

ethod i

s det

erm

ined

usi

ng t

he

rati

o o

f th

e su

m o

f th

e al

l co

mpar

able

s’

mar

ket

cap

ital

izat

ion by t

he

sum

of

the

each

com

par

able

s’ c

om

mon s

har

es t

imes

thei

r E

PS

.

MDT | PAGE 11SOUTHERN METHODIST UNIVERSITY

ANN RIFE COX ENDOWMENT FUNDSMU : COX SCHOOL OF BUSINESS

EX

HIB

IT 2

: P

roje

cted

Fin

anci

als

MDT | PAGE 12SOUTHERN METHODIST UNIVERSITY

ANN RIFE COX ENDOWMENT FUNDSMU : COX SCHOOL OF BUSINESS

EX

HIB

IT 2

: P

roje

cted

Fin

anci

als

(conti

nued

)

MDT | PAGE 13SOUTHERN METHODIST UNIVERSITY

ANN RIFE COX ENDOWMENT FUNDSMU : COX SCHOOL OF BUSINESS

EXHIBIT 3 : Risk and Required Return

CHART G : Net Sales by operating segmentsSOURCE: Company Reports

MDT | PAGE 14SOUTHERN METHODIST UNIVERSITY

ANN RIFE COX ENDOWMENT FUNDSMU : COX SCHOOL OF BUSINESS

EX

HIB

IT 4

: S

ensi

tivit

y A

nal

ysi

s

MDT | PAGE 15SOUTHERN METHODIST UNIVERSITY

ANN RIFE COX ENDOWMENT FUNDSMU : COX SCHOOL OF BUSINESS

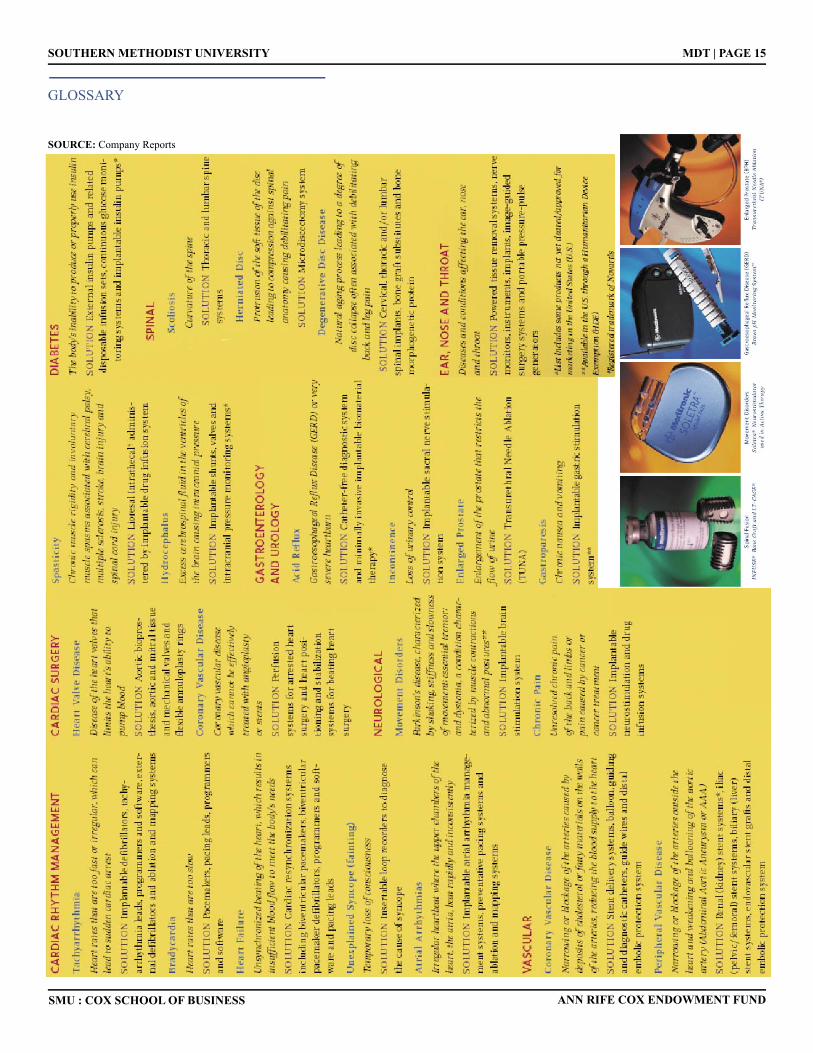

GLOSSARY

SOURCE: Company Reports