Embed Size (px)

Citation preview

1

September 2012

Corporate Presentation

Corporate Presentation

Q1 2013

2

Disclaimer

This presentation is incomplete without reference to, and should be viewed solely in conjunction with the oral briefing which accompanies it. This presentation does not constitute an offer to sell

or a solicitation of an offer to subscribe for or purchase any interest in any company and may not be relied upon by you. This document is not intended to, nor will it, form the basis of any

agreement in respect of any contract.

The content of this presentation has not been approved by an authorised person within the meaning of the Financial Services and Markets Act 2000 (“FSMA”).

Reliance on the information contained in this presentation for the purposes of engaging in any investment activity may expose the investor to a significant risk of losing all of the property or

assets invested. Any person who is in any doubt about the investment to which this presentation relates should consult a person duly authorised for the purposes of FSMA who specialises in the

acquisition of shares and other securities. The information in this presentation is subject to updating, revision and amendment. The information in this presentation, which includes certain

information drawn from public sources does not purport to be comprehensive and has not been independently verified. This presentation does not constitute or form part of any offer or invitation

to sell, or any solicitation of any offer to purchase or subscribe for or otherwise acquire, any securities in San Leon Energy plc (the “Company”) in any jurisdiction or any other body corporation or

an invitation or an inducement to engage in investment activity under section 21 of the Financial Services and Markets Act 2000, nor shall it or any part of it form the basis of or be relied on in

connection with any contract therefore. This presentation does not constitute an invitation to effect any transaction with the Company or to make use of any services provided by the Company.

No reliance may be placed for any purpose whatsoever on the information contained in this presentation or any assumptions made as to its completeness. No representation or warranty, express

or implied, is given by the Company, any of its subsidiaries or any of its advisers, directors, officers, employees or agents, as to the accuracy, reliability or completeness of the information or

opinions contained in this presentation or in any revision of the presentation or of any other written or oral information made or to be made available to any interested party or its advisers and,

save in the case of fraud, no responsibility or liability is accepted (and all such liability is hereby excluded for any such information or opinions). No liability is accepted by any of them for any

such information or opinions (which should not be relied upon) and no responsibility is accepted for any errors, misstatements in or omissions from this presentation or for any loss howsoever

arising, directly or indirectly, from any use of this presentation or its contents. The information and opinions contained in this presentation are provided as at the date of this presentation and are

subject to change without notice.

In the United Kingdom, this presentation is only being distributed to persons who are reasonably believed to be persons who fall within Articles 19 (1) and 19 (5) (investment professionals) or 49

(2) (High net worth Companies etc.) of The Financial Services and Markets Act 2000 (Financial Promotions) Order 2005 (“Financial Promotion Order”) or to other persons to whom this

presentation may otherwise be lawfully distributed. Persons who do not fall within any of these definitions should return this presentation immediately to the Company and in any event, must not

act or rely upon the information contained in this presentation.

The securities referred to herein have not been, and will not be, registered under the US Securities Act of 1933, as amended (the “Securities Act”) and may not be offered

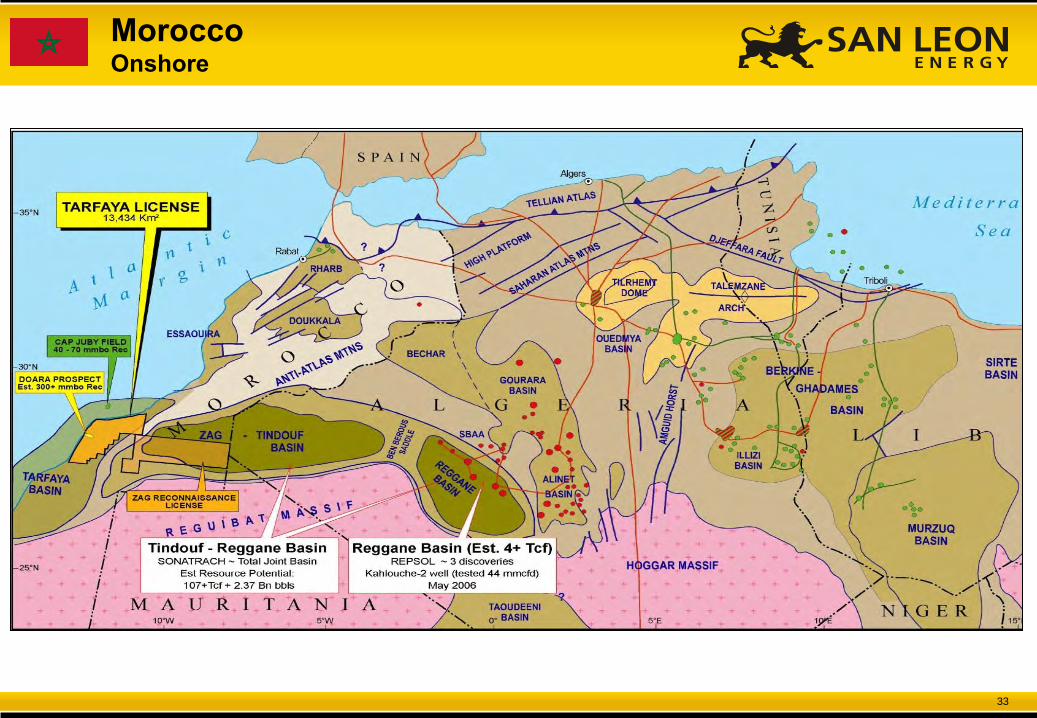

or sold in or into the United States except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act or unless

registered under the Securities Act. There will be no public offering of the securities in the United States.

By listening to this presentation, each person is deemed to confirm, warrant and represent that they fall under one of the Articles set out above. The content of this

presentation is confidential and is reproduced solely for your information and may note be reproduced, transmitted or further distributed to any other person or published,

in whole or in part, for any purpose.

No recipient of the information in this presentation should deal in or arrange any dealing in or otherwise base any behaviour (including any action or inaction) in relation to any securities to which

this document relates (including behaviour referred to in section 118(6) of the Financial Services and Markets Act 2000) which would or might constitute market abuse (as defined in section 118

of the Financial Services and Markets Act 2000). The information in this presentation may constitute price sensitive information and recipients should be aware of the relevant obligations and

restrictions under Part V of the Criminal Justice Act 1993. Any financial projection and other statements of anticipated future performance that are included in this presentation or otherwise

furnished are for illustrative purposes only and are based on assumption by the Company’s management that are subject to significant risks and uncertainties and may prove to be incomplete or

inaccurate. Actual results achieved may vary from the projections and the variations may be material. Variations in the assumptions underlying the projections may also significantly affect

projected results. This presentation has not been examined, reviewed or compiled by the Company’s independent certified accountants. No representation or warranty of any kind is made with

respect to the accuracy or completeness of the financial projections or other forward-looking statements, any assumptions underling them, the future operations or the amount of any future

income or loss. By attending the presentation, or reading or accepting this document you agree to be bound by the foregoing limitations.

3

San Leon Energy Plc

Page

1. San Leon Energy Plc Overview 4

2. High Impact Exploration 11

3. Near Term Production 44

4. European Shale Play 57

4

Key Data AIM Symbol: SLE US ADR Symbol: GLGYY Share price (21/2/13): 7.5p Market Cap (21/2/13): £140 million Shares Outstanding: 1,882 million 52 week price range: 7.29p – 13.00p 3 month avg. Volume: 5.1 million Directors ownership: 6.54%

Board of Directors Oisín Fanning Executive Chairman Paul Sullivan Managing Director John Buggenhagen Exploration Director Raymond King Non-Exec & Co. Sec. Jeremy Boak Non-Executive Director Con Casey Non-Executive Director John Conlin Non-Executive Director Daniel Martin Non-Executive Director John Matthews Non-Executive Director Piotr Rozwadowski Non-Executive Director

Significant Shareholders (1)

Toscafund Asset Management LLP 13.99% Quantum Partners LP 11.48% Blackrock Investment Mgmt Ltd 6.67%(2)

Kulczyk Investments S.A 4.70% Oisín Fanning (Executive Chairman) 3.23% Paul Sullivan (Managing Director) 3.18% Phil Thompson 3.02% Cheyne Capital Management (UK) LLP 1.92% Lord Sainsbury 1.52% Macquarie Bank Ltd 1.45% 55 North Capital Partners Ltd 1.08% 12 Month Share Price Performance

San Leon Energy Plc Key Information

(1) As at 21 February 2013 (2) Includes 0.09% CFD’s

5

• Independent E&P company listed on AIM with market cap of £140mm (€162mm) (1)

• Extensive and balanced portfolio of conventional and unconventional (shale/tight) assets across Europe and North Africa

• Diverse Prospect Inventory: develop a portfolio of prospects from low risk, short term, low cost exploration through to huge upside company maker plays

• Extensive land base: ~ 17.8 million net acres across 84 licences in 10 countries

• Experienced management and in-house technical team with local and regional expertise applying proven technology to underexplored acreage

• Secured material attractive acreage position through acquisition and organic growth:

• Gold Point Energy Corp. (Poland) - 2009

• Island Oil and Gas (Albania, Morocco, Ireland) - 2010

• Realm Energy International Corp. (Poland, Spain, France) - 2011

• Aurelian Oil and Gas Plc (Poland, Romania, Slovakia) - 2013

• Significant upside through carried exploration wells in Poland and Morocco

• NovaSeis: Established cableless land based seismic crew to increase control and reduce costs

• PGS seismic facility: Enabled offshore 3D seismic programmes in Ireland and Albania to de-risk assets

San Leon Energy Plc (SLE.L)

(1) As at 21 February 2013

6

Novaseis Vibration Trucks

Carboniferous Shale /

Tight Gas

Siciny-2

Baltic Basin Shale Gas,

Lewino 1G2

Baltic Basin Shale Gas

Szymkowo-1 Main Dolomite Oil, 2012

San Leon Energy Plc

NovaSeis Poland

NovaSeis Morocco

7

Albania 1 Licence 1.0 Million Net Acres

San Leon assets Poland 42 Licences 4.8 Million Net Acres

Germany 1 Licence 15.6 Thousand Net Acres

Spain 2 Licences 8 Under Application 2.2 Million Net Acres

Morocco 5 Licences 6.0 million Net Acres

France 10 Under Application 2.4 Million Net Acres

Ireland 8 Licences 0.6 million Net Acres

Romania 1 Licence 0.1 Million Net Acres

Bulgaria 1 Licence 0.1 Million Net Acres

Slovakia 3 Licences 0.3 Million Net Acres

Italy 2 Licences 0.2 Million Net Acres

San Leon Energy Plc Major European / North African Presence

84 Licences covering 28.5 Million Gross Acres / 17.8 Million Net Acres

8

Durresi Block, Albania Alban Prospect 3.2 Tcf/145 MMboe recoverable Drill Ready Offshore Conventional Gas/Condensate Target Farm-out in Process

SW Carboniferous, Poland Tight Gas and Shale Play 61 Tcf potential net recoverable resource Morocco Offshore

Foum Draa / Sidi Moussa 2 Bln bbls & 1 Tcf gas recoverable Farm-out complete Cairn $60mm well carry planned 2013/14 Genel $50mm well carry planned 2014

North Porcupine, Ireland Benbaun Prospect 180 MMbbl Recoverable Drill Ready Offshore Conventional Oil Target Farm-out in Process

Resources are based upon internal review and represent mid case gross best estimates unless otherwise stated

San Leon Energy Plc High Impact Exploration

Baltic Basin, Poland Paleozoic Shale Gas Play 1.5 million acres held with estimated 129 Tcf Prospective Resources in Baltic Basin Pilot 45,000 acre development estimated with 1Tcf recoverable

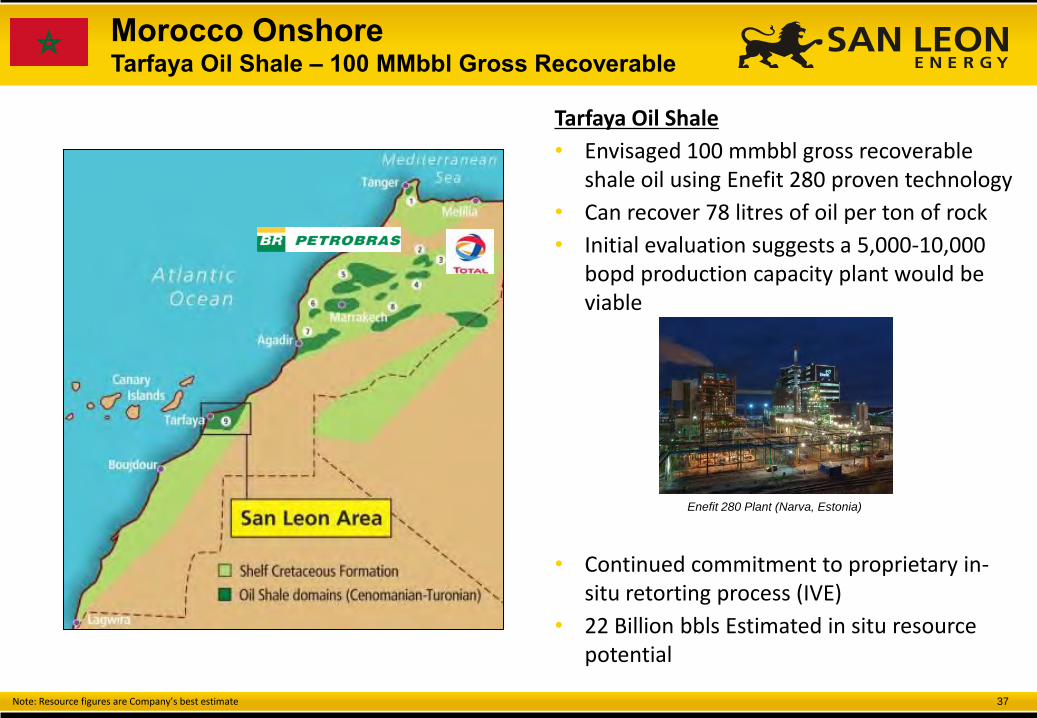

Morocco Onshore Tarfaya Oil Shale 100 MMbbl recoverable Unconventional (Utilises proven Enefit technology)

Targeting >5 Bln bbls and >100 Tcf resources across numerous High Impact

plays

Barryroe, Ireland 280 MMbbl Recoverable Conventional Oil Discovery 4.5% Net Profit Interest Zero future capital exposure

Morocco Onshore Tarfaya Casa Mar Lead 55 MMboe Recoverable Drillable Conventional Oil Target Morocco Onshore Zag Prospect 3.7 Tcf + 55 MMbbl Recoverable Conventional Oil & Gas Target

Morocco Onshore Zag Shale Gas Play 10+ Tcf Recoverable Unconventional resource

Main Dolomite Resource Oil Play, Poland Bln+ bbls potential net recoverable resource

9 All resources numbers are management best estimate Mid Case gross recoverable resources . Costs are gross estimates to prove the play. First production assumes success from current plans

San Leon Energy Plc Poland: Near Term Production Opportunities

Silvia Prospect Block 106 (50% Equity) 4.75 mmbbl and 18 bcf 12 bcf Czarne discovery close by First production 2014 ~3,700m exploration well + test

Rawicz (100% Equity) 12.8 bcf First production 2013 Exploration well + test

Siekierki Tight Gas Field Poznan East (90% Equity) Commercialisation of 3 existing wells 12 bcf SLE detailed Engineering review in progress Potential 422bcf contingent resources

Kowale Anticline Trend Karpaty West (60% Equity) 220 bcf Low cost shallow wells 3 Exploration wells First production 2014

Niebieszczany-1 Bieszczady (25% Equity) 0.6 mmbbl and 12.7 bcf Re-frac and test of Nieb-1

Rogity-1 Braniewo (40% Equity) 5.5 mmbbl Mid Case recoverable First production 2014 Vertical Frac

Czasław -1 Nowa Sol (100% Equity) 0.5 mmbbl Acidisation of existing well First production 2014

Putna Brodina, Romania (50% Equity) 24 mmbbl or 86 bcf Exploration well 2013/14

Siciny-2 Gora (100% Equity) Up to 225 bcf Frac existing well 2013 First production from successful frac

Net Recoverable Resource

Near-Term Commercialisation of existing wells

3 MMbbl and 240 Bcf

New Exploration 8 MMbbl and 555 Bcf

POLAND

10

Siekierki Finalise Apex Engineering review prior to decision on

early commercialisation

San Leon Energy Plc Potential 18 Month Forward Plan

2013 - 2014

Czasław, Nowa Sol Acidisation of existing well

Silvia, Block 106 Drill Vertical Exploration Well

Niebieszczany-1 Re-frac of existing Well & tie in

Karpaty West Drill 3 shallow vertical Expl

Wells

Rawicz Drill Vertical Exploration Well

Rogity-1 Frac & Test existing well

North Porcupine, Ireland Farm-out of licence prior to

drilling

Putna, Brodina 3D Seismic / Exploration Well

Siciny-2, Gora DFIT & Frac of existing well

Zag, Morocco Conventional gas prospect +

shale gas

Tarfaya, Morocco Casa Mar prospect + oil shale

studies

Durresi, Albania Farm-out of licence with

carried drilling programme

Sidi Moussa, Morocco Genel $50mm carry on

offshore well 2014

Foum Draa, Morocco Cairn $60mm carry on offshore well 2013/14

Gdansk West Frac and test Cambrian oil

potential in existing well

Early Production Potential

High Impact Potential

Medium Term Potential

11

San Leon Energy Plc

Page

1. San Leon Energy Plc Overview 4

2. High Impact Exploration 11

Poland – Baltic Basin Shale Play

Permian Basin Tight Gas / Shale Play

Poland – Permian Basin – Main Dolomite Conventional Oil Play

Albania Offshore

Morocco Offshore and Onshore

Ireland Offshore

3. Near Term Production 44

4. European Shale Play 57

12

2. Permian Basin Permian Main Dolomite Oil Play Permian Rotliegendes Gas Play Carboniferous Unconventional Gas Play

1. Baltic Basin Paleozoic shale gas/condensate play

Poland Diverse Portfolio Across Many Plays

3. Carpathians Deep Fold Belt Oil/Gas Play Shallow Foredeep Oil/Gas Play

Carpathians

Carpathian Foredeep

Baltic Syneclise (basin) 42 Licences across 4.8 million Net Acres (7.0m Gross)

13

• Access to gas, condensate and oil plays in Paleozoic shales; known hydrocarbon-rich source rocks

• Brittle shales and carbonates favourable for fracking

• High potential in Lower Silurian, Ordovician, and Cambrian

• High liquids potential in Eastern part of basin

• Relatively simple tectonic setting with a complex stratigraphic model

• 129 Tcf of recoverable gas is estimated Baltic Basin area (1)

• Other majors exploring the Baltic Basin

– Conoco Phillips; ENI; Marathon; Nexen; BNK

Poland – Baltic Basin Paleozoic Shale Plays

(1) US EIA World Shale Gas Resources Report 2011

Ordovician and Silurian Gas/Condensate Potential

Ordovician and Silurian Overpressured Gas

Potential Silurian Oil Potential

Baltic Basin Acreage

14

Poland – Baltic Basin 129TCF Paleozoic Shale Play

Material Acreage Position: • 1.4 million gross acres (5,658 km2) • 0.9 million net acres (3,520 km2)

Basin wide Diversity:

• SLE is the only company in the Baltic with such a diverse geologic acreage position – gas, liquids, shallow, deep

Partnerships:

• Talisman Energy, Hutton Energy and LNG Energy

Talisman Energy farm-in:

• 3 wells drilled in 2011/12

• First 1,000+ metres horizontal and multi-stage frac planned in 2013

• Option for 3 additional wells

Huge upside potential in shale gas valuations: • US development shale gas acreage has traded for up to $38,000 per acre • Polish exploration shale gas acreage trading at $30- $500 /acre

15

Poland – Baltic Basin Acreage Valuations

10

100

1000

10000

$/A

cre Baltic licences proven with modern wells

Expected Value Per Acre Post Planned Work Programme

Petronas/Montney $6,000/acre

Exxon/Duvernay $4,500/acre

Statoil/Australia $15/acre

Initial Exploration in Basin. 1 – 20 vertical wells

Vertical/Horizontal wells with Frac and Flow Test 2 – 5 wells within Concession

Pilot Production/Production 30+ horizontal wells

Statoil/Bakken $11,500/acre

Shell/Marcellus $4,700/acre

Total/Australia $37/acre

5000

No wells

500

30000

Sasol/Talisman $38,000/acre

Total/Utica $15,000/acre

50 Baltic licences without modern wells

5

16

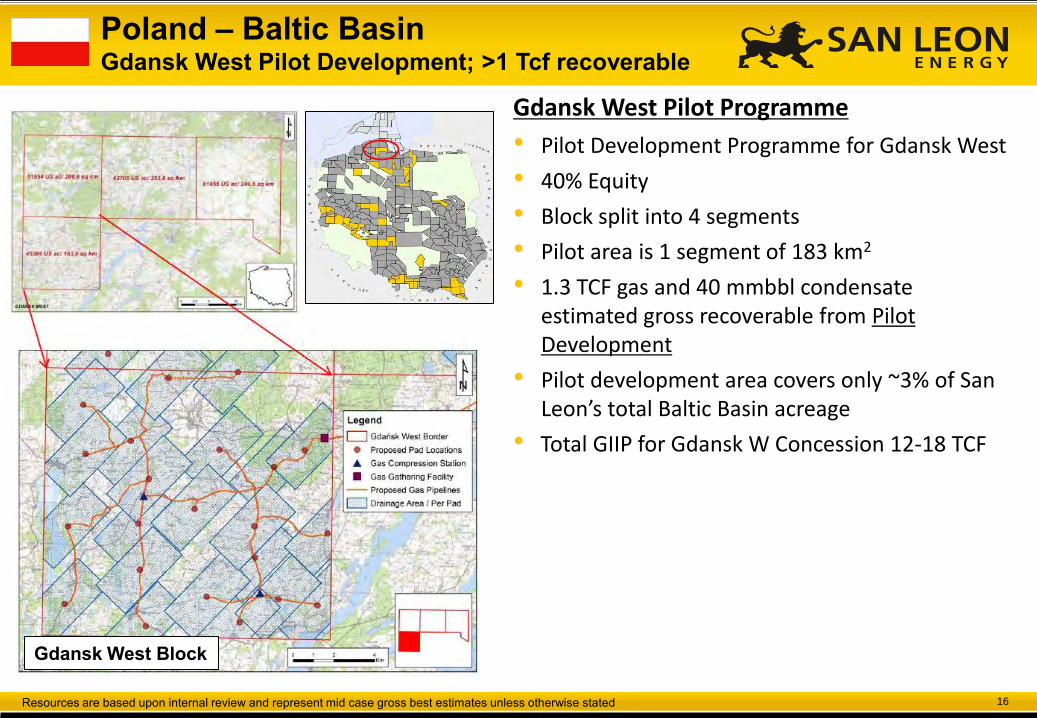

Gdansk West Pilot Programme

• Pilot Development Programme for Gdansk West

• 40% Equity

• Block split into 4 segments

• Pilot area is 1 segment of 183 km2

• 1.3 TCF gas and 40 mmbbl condensate estimated gross recoverable from Pilot Development

• Pilot development area covers only ~3% of San Leon’s total Baltic Basin acreage

• Total GIIP for Gdansk W Concession 12-18 TCF

Poland – Baltic Basin Gdansk West Pilot Development; >1 Tcf recoverable

Gdansk West Block

Resources are based upon internal review and represent mid case gross best estimates unless otherwise stated

17

San Leon Energy Plc

Page

1. San Leon Energy Plc Overview 4

2. High Impact Exploration 11

Poland – Baltic Basin Shale Play

Permian Basin Tight Gas / Shale Play

Poland – Permian Basin – Main Dolomite Conventional Oil Play

Albania Offshore

Morocco Offshore and Onshore

Ireland Offshore

3. Near Term Production 44

4. European Shale Play 57

18

• Prolific onshore European hydrocarbon province

• 3 main target formations:

– Permian Main Dolomite of the Zechstein

– Conventional oil – Low cost/Low risk prospects

– Tight oil – Huge upside potential

– Permian Rotliegendes Sandstone

– Conventional – Low cost/Low risk prospects

– Tight gas – Huge upside potential

– Carboniferous Unconventional

– Shale

– Tight gas sand

Poland – Permian Basin Summary of Plays

• > 100 mmbbl oil in Main Dolomite

• > 7 TCF gas discovered in Rotliegendes

• Thick, unexplored Carboniferous source rock section

• San Leon Energy with dominant acreage position in southern part of basin (Fore-Sudetic Monocline)

19

• San Leon pioneering gas play in West Poland

• Carboniferous shales have sourced all Rotliegendes gas in Permian Basin

• Siciny-2 well drilled in 2012 providing rare core and extensive Carboniferous data

Poland – SW Carboniferous 61 TCF Risked Net Recoverable Tight Gas & Shale Play

• >10,000 km2 unexplored in Permian Basin under lease

• Siciny-2 suggests >200 Bcf/Section(1) GIIP in Tight Sand

• Upside of 70 Bcf/Section GIIP in Shale

• May extend across 13 San Leon licences

• This yields a risked 61 Tcf net recoverable resource

(1) A section is one square mile

20

Siciny-2

Poland – SW Carboniferous Basin Siciny-2, Gora Block – Carboniferous Gas Play

Forward Plan for Siciny-2 (225 Bcf)

• DFIT and Frac of Siciny 2 – 2013

• 40% Chance of Commercial Success of which

• 10% chance that 2 Bcf can be recovered flowing at 500 mscf/d

• 90% chance to drill a new 5,500m horizontal well

• Leading to a 225 Bcf development plan

• 49 well development

Forward Plan for Carboniferous Gas Play (~61 Tcf Net Risked Recoverable)

• Interpret recently acquired 3D seismic on Rawicz & Siciny

• Drill 3 additional appraisal wells in 2014 (Gora, Rawicz and Wschowa)

• Evaluation of development options

– Horizontal drilling; Frac design; Facilities and pipeline design

• Acquire 2D seismic in 2013 (Olesnica, Wielun, Praszka and Prusice)

• Drill Exploration wells in 2014 resulting 2D

• Evaluate possibility of Carboniferous exploration licences (Nowa Sol, 243/Laski & Cybinka/Torzym)

21

San Leon Energy Plc

Page

1. San Leon Energy Plc Overview 4

2. High Impact Exploration 11

Poland – Baltic Basin Shale Play

Permian Basin Tight Gas / Shale Play

Poland – Permian Basin – Main Dolomite Conventional Oil Play

Albania Offshore

Morocco Offshore and Onshore

Ireland Offshore

3. Near Term Production 44

4. European Shale Play 57

22

• Billion+ bbl potential in Main Dolomite tight oil play

• Mississippi Lime / Bakken Analogue

• SLE controls more than 6,000 km2 of Main Dolomite platform and lagoon deposits within oil generating window.

• Low porosity intervals aided by highly fractured zones with high permeability

• Main Dolomite reservoir is self-sourcing

• Seismic processing may be used to detect sweet spots (high k)

• Industry-standard methodologies may be used to optimise productivity

– Underbalanced drilling

– Horizontal drilling

– Acidizing

– Fracking

Oil in fractured Main Dolomite in Sosna 1 core

Poland – Main Dolomite > Billion Bbl Risked Recoverable Tight Oil Play

23

• Play with proven production requires modern completion and stimulation practices to exploit properly

• Tight oil play in Main Dolomite platform/lagoon facies

• Potentially 4 Billion Barrels net risked across SLE licences

• Significant drilling in 1970’s. All wells have oil shows (oil in core, oil to surface in DST, smell of oil in drilling mud)

• 4 fields put on production in 1970’s

– Low production rates

– Minimal stimulation

– Non-optimal drilling and completion

• Remaining reserves in old oil fields.

• 20+ structures identified in 2011 3D seismic

– Folded Main Dolomite has higher likelihood of being fractured

• Lelechow and Czaslaw drilled in 2012

– Testing to optimize stimulation techniques

• Wells designed for horizontal sidetracks

• Prove completion and stimulation concept in Nowa Sol, then further drilling in other SLE licences

Poland – Main Dolomite Nowa Sol Project : > Billion bbl Tight Oil Play

Open Fractures

24

San Leon Energy Plc

Page

1. San Leon Energy Plc Overview 4

2. High Impact Exploration 11

Poland – Baltic Basin Shale Play

Permian Basin Tight Gas / Shale Play

Poland – Permian Basin – Main Dolomite Conventional Oil Play

Albania Offshore

Morocco Offshore and Onshore

Ireland Offshore

3. Near Term Production 44

4. European Shale Play 57

25

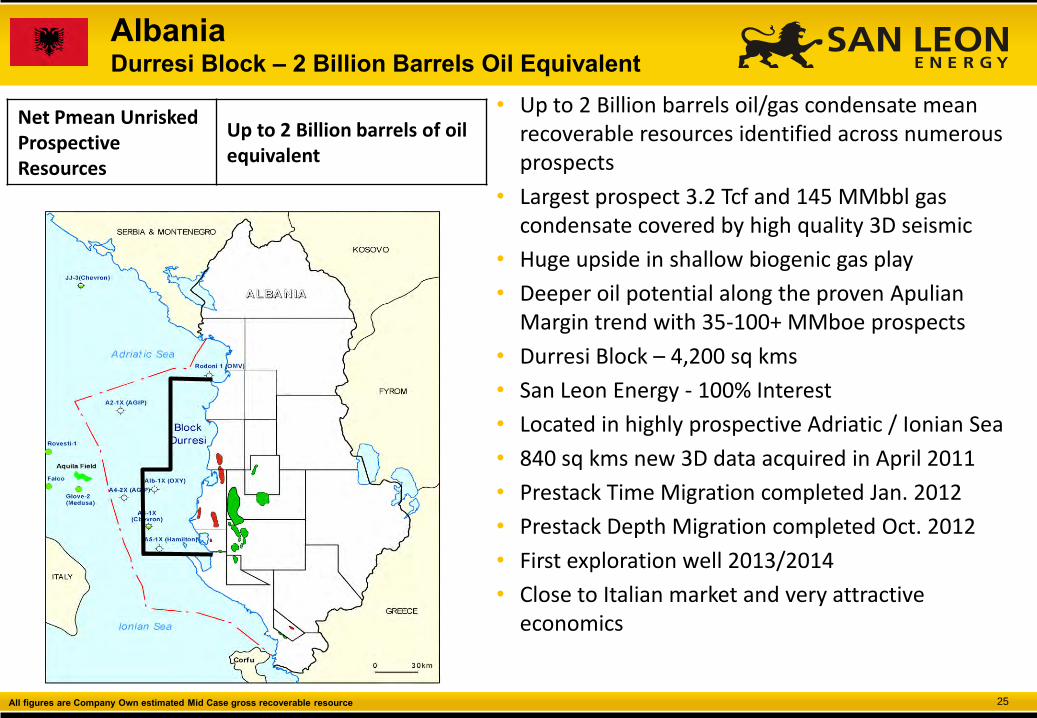

• Up to 2 Billion barrels oil/gas condensate mean recoverable resources identified across numerous prospects

• Largest prospect 3.2 Tcf and 145 MMbbl gas condensate covered by high quality 3D seismic

• Huge upside in shallow biogenic gas play

• Deeper oil potential along the proven Apulian Margin trend with 35-100+ MMboe prospects

• Durresi Block – 4,200 sq kms

• San Leon Energy - 100% Interest

• Located in highly prospective Adriatic / Ionian Sea

• 840 sq kms new 3D data acquired in April 2011

• Prestack Time Migration completed Jan. 2012

• Prestack Depth Migration completed Oct. 2012

• First exploration well 2013/2014

• Close to Italian market and very attractive economics

Albania Durresi Block – 2 Billion Barrels Oil Equivalent

Net Pmean Unrisked Prospective Resources

Up to 2 Billion barrels of oil equivalent

All figures are Company Own estimated Mid Case gross recoverable resource

26

Three Working Petroleum Systems

1. Ionian zone – good to excellent quality source rocks of type I/II are present in the Upper Triassic, Lower Jurassic and Lower Cretaceous

2. Peri Adriatic Depression (PAD) – Tortonian to Pliocene terrigenous section is of poor type III source rock for gas while the Aquitanian/Burdigalian is slightly better.

3. Biogenic gas system – Due to fast rate of sedimentation and low geothermal gradient, the biogenic gas generation zone is thick (surface to 3500m) and key parameters are very similar to Po Basin, where 14 TCF of recoverable biogenic gas has been proven. On the Durresi Block, the A4-1X well found a 50 BCF biogenic gas accumulation. To the west of the Duressi Block, the Falco Field has proven 200 BCF of recoverable biogenic gas.

Four Proven Play Types 1. Miocene sandstones charged from the underlying Mesozoic section (Kucova, Patosi and Marinza oil fields, onshore Albania)

2. Cretaceous-Eocene age fractured carbonate reservoirs charged from the Mesozoic section (Rovesti, Aquila, Giove - offshore Italy; and Visoka, Gorishti-Koculi, Ballshi-Hekal, Finiq-Krane, Cakran-Mollaj, Amonica and Delvina oil fields -onshore Albania)

3. Miocene sandstones charged from Tertiary source rocks (Divjaka, Frakulla, Ballaj, Povelca, Panaja and Durresi - onshore Albania gas fields)

4. Biogenic gas accumulations in the post-evaporitic sequence, Po Valley analogue (Falco, Divjaka - onshore Albania], A4-1X – offshore Albania)

Albania Durresi – Highly Prospective Offshore Block

27

Alban Complex (Equity 100%)

• 3.2 Tcf and 145 MMbbl gas condensate mean case recoverable resources

• Alban Core and Alban East prospects

• Mature prospect covered by excellent quality 3D seismic

• 150m water depth with reservoir at approx 2,500 metres

• Currently seeking farm-in partner to carry in 1-2 offshore wells

• First exploration well 2013/2014;

• Development plan for subsea tie-back to terminal either Brindisi in Italy or Vlore in Albania

Albania Alban Complex – 3.2 Tcf prospect on Durresi Block

• Multiple prospects with up to 2 billion barrels of oil equivalent

Alban Core Alban

East

All figures are Company Own estimated Mid Case gross recoverable resource

28

Fault block `A`

Fault block `B`

A3-1X GR 5 Km 5 Km

N-S fullstack seismic profile through on the Alban structure

Alban Centre Prospect

Alban East Prospect

Alban Centre Prospect • In the crest of the Alban structure.

• Contains two likely to be separated fault blocks with very strong seismic indications

• Pmean recoverable reserves: 2.3 Tcf of thermogenic gas + 108 MMbbls of condensate

• Chance of success: 36%

• Depth interval: 1400 - 2400m

Alban East Prospect • On the east of the Alban folded structure • Pmean recoverable reserves: 0.9 Tcf of

thermogenic gas + 37 MMbbls of condensate

• Chance of success: 34% • Depth interval: 2400 - 3400m

Albania Alban Complex Prospects

29

N S

Planned wells A3-1X

Durresi 3D Far stack arbitrary line

A3-1X GR (1200m – 2250m)

Note abrupt termination of amplitude at fault

Also there is a significant velocity anomaly below the prospect!

Albania Alban Centre Prospect

30

San Leon Energy Plc

Page

1. San Leon Energy Plc Overview 4

2. High Impact Exploration 11

Poland – Baltic Basin Shale Play

Permian Basin Tight Gas / Shale Play

Poland – Permian Basin – Main Dolomite Conventional Oil Play

Albania Offshore

Morocco Offshore and Onshore

Ireland Offshore

3. Near Term Production 44

4. European Shale Play 57

31

Morocco Offshore Foum Draa / Sidi Moussa 2 Bln bbls & 1 Tcf gas Farm-out complete Cairn $60mm well carry planned 2013/14 Genel $50mm well carry planned 2014

Morocco Onshore Tarfaya Oil Shale 100 MMbbl recoverable Unconventional (Utilises proven Enefit technology Assuming 10,000 bpd facility) Upside of 500 MMbbl using larger facility

Morocco Onshore Tarfaya Casa Mar Lead 55 MMboe Gross Recoverable Drillable Conventional Oil Target

Morocco Onshore Zag Prospect 3.7 Tcf + 55 MMbbl Gross Recoverable Conventional Oil & Gas Target

Morocco Onshore Zag Shale Gas Play 10+ Tcf Recoverable Unconventional resource

Morocco Large and Diverse Plays; Excellent Fiscal Terms

Excellent fiscal terms: 30% corporate tax - after a 10 year production holiday Onshore & <200m water depth 10% royalty on oil production (first 300,000 tons of production exempt) 5% royalty on gas production (first 300 million cubic meters exempt) Offshore & >200m water depth 7% royalty on oil production (first 500,000 tons of production exempt) 3.55% royalty on gas production (first 500 million cubic meters exempt)

32

Foum Draa

• SLE retains 14.17% working interest

• $60MM well carry from Cairn Energy

• $20MM Bank guarantee paid

• 1st Exploration well 2013/2014

• 3,800 km2 3D acquired in 2002 by Shell

Sidi Moussa

• SLE retains 8.5% working interest

• $50MM well carry from Genel Energy

• $17MM Bank guarantee paid

• 1st Exploration well 2013/2014

• 1,460 km2 3D acquired in 2000

• Over 7,000 km 2D acquired from 1983-

1999

Total Unrisked Prospective Resources

Oil (MMbbl) Gas (Bcf)

P10 6,105 3,145

P50 2,139 1,009

P90 752 303

** NSAI Dec. 31, 2011 Resource Estimate

Morocco Offshore 2 Billion bbls Oil + 1 Tcf Gas on Block

De-risking through Farm-Outs

33

Morocco Onshore

34

(From Craig, et al, 2006)

Morocco Onshore: Silurian Shale Gas Potential

35

CASA MAR Prospect

13,434 km2

CASA MAR Prospect

Morocco Onshore Tarfaya Casa Mar Prospect – 55 MMbbl

Note: Resource figures are Company’s best estimate

36

Morocco Onshore Tarfaya Casa Mar Prospect

San Leon WI • 52.5% (Operator)

Resources • 55MMbbl Net P50 Unrisked

Prospective Resources

Overview

• Acquired 600 km 2D seismic

• Very favourable fiscal terms

• 1.9 million acres (7,700 km2)

• Large syn-rift structures (Triassic)

• Proven Tertiary play in southern part of license area

Casa Mar Prospect

• Oolitic shoal play with huge potential (Casa Mar Prospect, right)

• Structure trap ~55 MMbbl

• Strat trap upside >1 Bln bbl

• Jurassic source rock

Note: Resource figures are Company’s best estimate

W E

• Prograding shoal is under up to 300 km2 closure (mean case 66 km2) • Conservative resource estimate is 40 MMBO recoverable • Casa Mar SL-1 well planned for Q1 2014

Casa Mar drillable prospect targeting 55 mmbbl conventional

Oil

Oolitic formations are known for very high permeability/productivity

37

Morocco Onshore Tarfaya Oil Shale – 100 MMbbl Gross Recoverable

Note: Resource figures are Company’s best estimate

Tarfaya Oil Shale

• Envisaged 100 mmbbl gross recoverable shale oil using Enefit 280 proven technology

• Can recover 78 litres of oil per ton of rock

• Initial evaluation suggests a 5,000-10,000 bopd production capacity plant would be viable

• Continued commitment to proprietary in-situ retorting process (IVE)

• 22 Billion bbls Estimated in situ resource potential

Enefit 280 Plant (Narva, Estonia)

38

Morocco Onshore Tarfaya Oil Shale

Pre-feasibility 12 months

• Re-examine rock mechanics and kerogen characteristics

• Work with EOT(1) to establish yield and operating parameters

• 10 ton bulk sample testing in German plant

•Work with contractors on mining and construction plans

• Establish detailed costing for mining construction and equipment cost

• Finalise capital program • Formalise JV partnerships

• Work with ONHYM to crystallise commercial licence terms for shale oil exploitation

Licence application

Project execution 36 months from licence award

• Finalise equity and suppliers

• Order mining equipment

• Earth works for plant site

• Order long lead time items

• Fine tune plant design

• Finalise debt arrangement

• Commence construction

• Prepare haulage, storage and pit

• Strip overburden in preferred mine site

• Commission plant

Fiscal terms finalisation

(1) EOT – Enefit Outotec Technology

39

San Leon • 52.5% (Operator)

Resources • 14+ TCF Net P50 Unrisked

Prospective Resources

Overview

• 3.7 Tcf onshore conventional gas play at moderate depth

• 5.4 million acres (21,807 km2)

• Proven hydrocarbon system

• World-class Silurian source rock

• Structural closures in Cambrian through Devonian (500 BCF)

• Large gas discoveries to the east of the Licence and gas discovery to the south of Licence

• Repsol Discovery of 800 BCF in Algeria

• 190 sq km Devonian Reef imaged on 2D seismic (3.7 TCF)

• Unconventional Shale Gas Play (using SLE’s Polish shale gas experience)

Completed

Activity

• Merged basin-wide aeromagnetic survey

• Acquired 1,675 km 2D seismic in 2011 (NovaSeis acquisition)

Note: Resource figures are Company’s best estimate

Silurian Shale Play NW

Devonian Reef Play

Reef Play has >5 TCF recoverable in gas case (>700 MMBO in oil case)!

Proposed well (3700m) will test Devonian Reef (3.7 TCF potential) and Cambrian fractured carbonate

Morocco Onshore Zag – 3.7 Tcf Conventional Gas Prospect + Shale Gas

40

San Leon Energy Plc

Page

1. San Leon Energy Plc Overview 4

2. High Impact Exploration 11

Poland – Baltic Basin Shale Play

Permian Basin Tight Gas / Shale Play

Poland – Permian Basin – Main Dolomite Conventional Oil Play

Albania Offshore

Morocco Offshore and Onshore

Ireland Offshore

3. Near Term Production 44

4. European Shale Play 57

41

Corrib Gas Field GIIP 1 TCF Triassic

27/4-1 Oil Discovery Middle Jurassic

Connemara Oil Field 150 MMBO Upper Jurassic

Spanish Point Gas Condensate Discovery 1.4 TCF and 160 MMstb Upper Jurassic

Burren Oil Discovery Lower Cretaceous

Celtic Sea Barryroe Oil Field Seven Heads Gas Field Old Head of Kinsale Schull

Rockall/Erris Margin Dooish and West Dooish Gas Condensate Discovery Triassic/Permian

Rockall

Slyne

North Porcupine

South Porcupine

Ireland: Licences

San Leon Licences

• 8 licences

• 1,333 MMboe prospective resources (Company est.)

• ~1 million acres

• 4 Offshore Atlantic Margin Licences

• All operated; 2,880 km2 area

• 4 Offshore Celtic Basin Licences

• Seven Heads Producing Gas Field (12.5% interest)

• Barryroe Oil Discovery – 4.5% Net Profit Interest

• Old Head of Kinsale

• Schull

Ireland – Key Facts

• Atlantic Margin – only 42 Exploration Wells

• Significant oil prospects

• Huge remaining potential

• Excellent Fiscal Regime

• Political stability

• Exxon drilling Q2 2013

Source: Hannon Westwood

42

Ireland: Atlantic Margin North Porcupine Licence 1/04

B Prospect

C1 Prospect

H Prospect

Connemara Field

J1 Lead

J2 & J3 Leads

7 km

11 km

18 km

FPSO Location

• New 3D survey revealed new, hitherto unrecognised, ‘B’ prospect at (2200m SS) in proven oil play directly analogous to UK Buzzard field

• Low risk 4-way dip closure with huge stratigraphic upside (21km2); Play elements proven at Connemara

• Pmean recoverable reserves 180 MMbbl, GCoS 33%

• P10 470 MMbbl

• Potential to tie in further fields and prospects identified on Licence, including discovered Connemara Field

• San Leon Energy (Operator) 74%*; Supernova (Bluewater) 20%; Valhalla Oil & Gas 6%

Development Plan

• 400m water depth; 2500m reservoir depth

• 14 production well development (Mid Case); 7 water injection wells

• Subsurface facilities with FPSO

*Subject to Regulatory approval

43

4.5% Net Profit Interest in Barryroe

field

P50 NPV10 = $88 MM*

(1) February 2011 RPS Energy Report for Landsdowne Oil & Gas plc adjusted to Providence Resources (Operator) recent announcements (2) Calculated from Seymour Pierce research report Oct 2012

Ireland: Celtic Sea Barryroe Field 4.5% NPI

San Leon holds 4.5% Net Profit Interest on Barryroe Oil Field; No further capital exposure

Operator currently further evaluating field:

• Assigned P50 STOIIP(1) of 1.8 bln bbls of oil across 4 horizons (P10 – 2.8 Bln bbls)

• Assigned 280 MMbbl P50 recoverable resource (1) from two horizons

• P50 NPV10 = $88 million net to SLE (2)

• 430 API – premium light quality oil

• Updated Operator CPR expected Q1 2013

Oil Recovery Recoverable NPV /

STOIIP Factor Reserves boe NPV

mmbbl % mmbbl $/boe $mm

Basil Wealden 756 31% 234 7.0 1,641

Middle Wealden 287 16% 46 7.0 321

Lower Wealden 416 0% - 7.0 -

Purbeckian 362 0% - 7.0 -

Total 1,821 280 1,962

4.5% NPI 88

(2) (1) (1) (1)

44

San Leon Energy Plc

Page 1. San Leon Energy Plc Overview 4

2. High Impact Exploration 11

3. Near Term Production & Other Assets 44

Silvia, Block 106 - Permian Main Dolomite, Conventional Oil Play

Czasław, Nowa Sol – Permian Main Dolomite Tight Oil Play

Rawicz - Permian Rotliegendes, Conventional Gas Play

Siekierki, Poznan East - Permian Rotliegendes, Tight Sandstone

Rogity-1, Braniewo - Baltic Basin

Kowale Trend, Karpaty West – Carpathians

Niebieszczany-1, Bieszczady - Carpathian Krosno Play

Putna, Brodina - Romanian Carpathians

4. European Shale Play 57

45 All resources numbers are management best estimate Mid Case gross recoverable resources . Costs are gross estimates to prove the play. First production assumes success from current plans

San Leon Energy Plc Poland: Near Term Production Opportunities

Silvia Prospect Block 106 (50% Equity) 4.75 mmbbl and 18 bcf 12 bcf Czarne discovery close by First production 2014 ~3,700m exploration well + test

Rawicz (100% Equity) 12.8 bcf First production 2013 Exploration well + test

Siekierki Tight Gas Field Poznan East (90% Equity) Commercialisation of 3 existing wells 12 bcf SLE detailed Engineering review in progress Potential 422bcf contingent resources

Kowale Anticline Trend Karpaty West (60% Equity) 220 bcf Low cost shallow wells 3 Exploration wells First production 2014

Niebieszczany-1 Bieszczady (25% Equity) 0.6 mmbbl and 12.7 bcf Re-frac and test of Nieb-1

Rogity-1 Braniewo (40% Equity) 5.5 mmbbl Mid Case recoverable First production 2014 Vertical Frac

Czaslaw-1 Nowa Sol (100% Equity) 0.5 mmbbl Acidisation of existing well First production 2014

Putna Brodina, Romania (50% Equity) 24 mmbbl or 86 bcf Exploration well 2013/14

Siciny-2 Gora (100% Equity) Up to 225 bcf Frac existing well 2013 First production from successful frac

Net Recoverable Resource

Near-Term Commercialisation of existing wells

3 MMbbl and 240 Bcf

New Exploration 8 MMbbl and 555 Bcf

POLAND

46

• First-mover advantage – San Leon has secured the largest acreage position in Poland after the state company PGNiG

• 42 licences covering 4.8 million net acres

• Partnerships – Important strategic partnerships with PGNiG, Talisman Energy, Hutton Energy, Celtique Energy and LNG Energy

• Diverse portfolio – Baltic Basin Paleozoic shale gas; Carboniferous tight/shale gas; and Permian conventional oil and gas

• Import dependency – High Russian dependency and strong demand to offset imports and dependence on coal

• Strong economics – High oil and gas prices linked to oil prices coupled with low royalty and tax regime

• Politics – Stable political environment

• Infrastructure – Good infrastructure close to onshore assets

• Underexplored – Central Europe is historically underexplored due to history and size of FSU reserves

Poland Attractive Economics and Political Regime

47

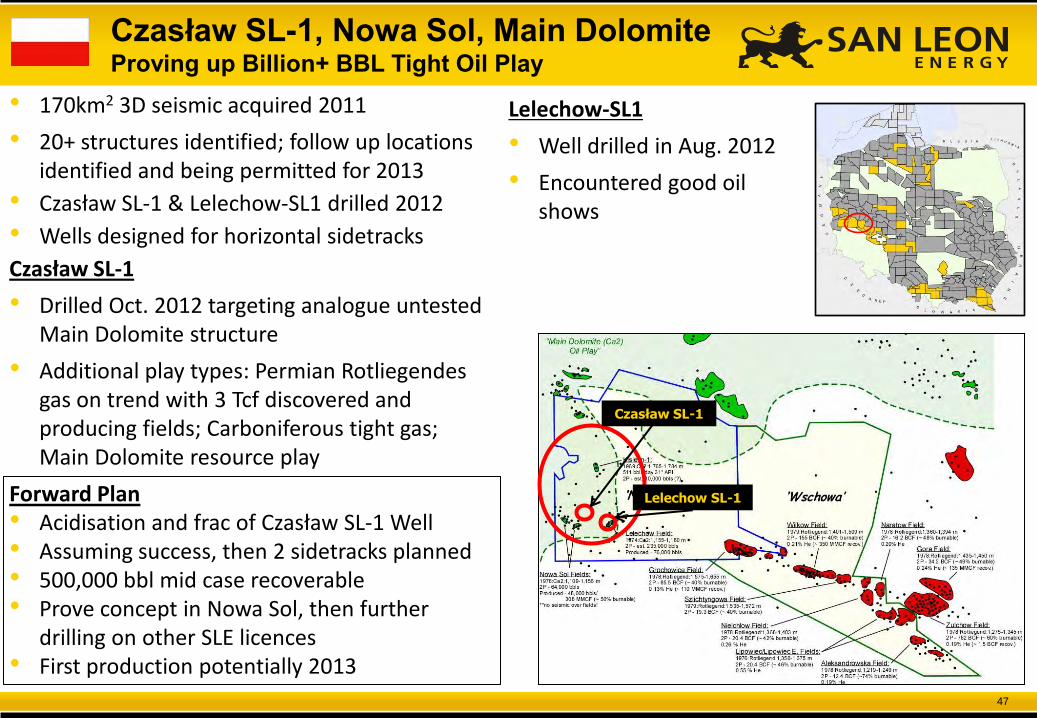

Czasław SL-1, Nowa Sol, Main Dolomite Proving up Billion+ BBL Tight Oil Play

• 170km2 3D seismic acquired 2011

• 20+ structures identified; follow up locations identified and being permitted for 2013

• Czasław SL-1 & Lelechow-SL1 drilled 2012

• Wells designed for horizontal sidetracks

Czasław SL-1

• Drilled Oct. 2012 targeting analogue untested Main Dolomite structure

• Additional play types: Permian Rotliegendes gas on trend with 3 Tcf discovered and producing fields; Carboniferous tight gas; Main Dolomite resource play

Forward Plan • Acidisation and frac of Czasław SL-1 Well • Assuming success, then 2 sidetracks planned • 500,000 bbl mid case recoverable • Prove concept in Nowa Sol, then further

drilling on other SLE licences • First production potentially 2013

Lelechow SL-1

Czasław SL-1

Lelechow-SL1

• Well drilled in Aug. 2012

• Encountered good oil shows

48

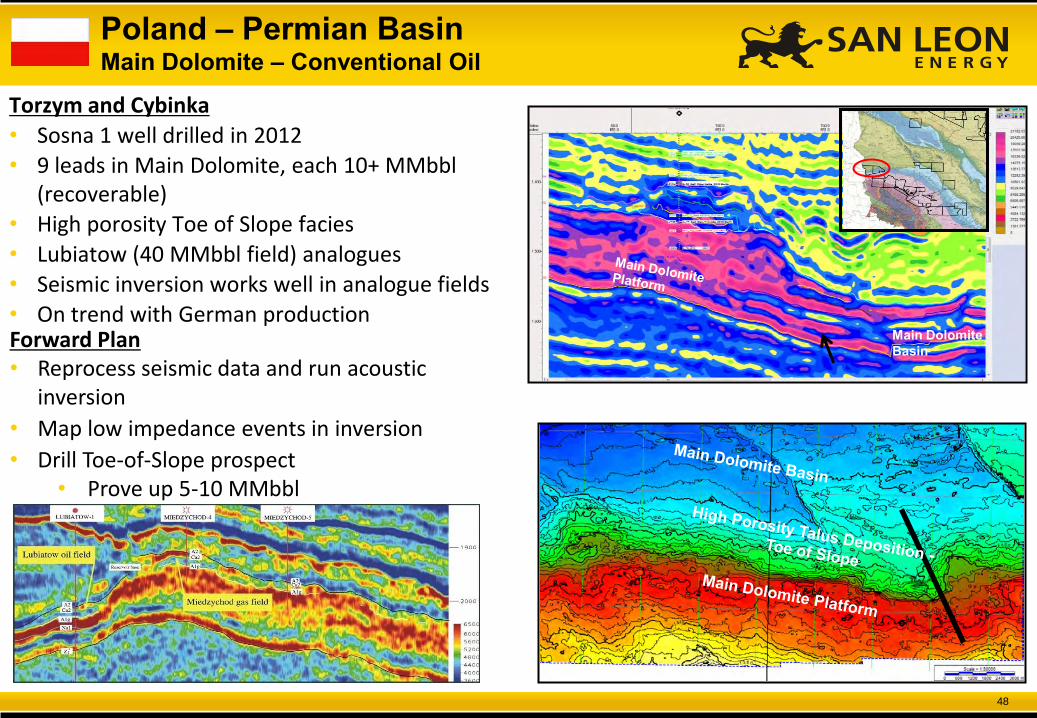

Torzym and Cybinka

• Sosna 1 well drilled in 2012

• 9 leads in Main Dolomite, each 10+ MMbbl (recoverable)

• High porosity Toe of Slope facies

• Lubiatow (40 MMbbl field) analogues

• Seismic inversion works well in analogue fields

• On trend with German production

High Porosity Talus Deposition? - Toe of Slope

Main Dolomite Basin Forward Plan

• Reprocess seismic data and run acoustic inversion

• Map low impedance events in inversion

• Drill Toe-of-Slope prospect • Prove up 5-10 MMbbl

Poland – Permian Basin Main Dolomite – Conventional Oil

49

Laski

• Main Dolomite Atoll complex

• Thick, reef facies on structural high

• 120 MMbbl structure (in place)

• High porosity reef facies

• Bronsko analogue (520 bcf)

Forward Plan

• Shoot 3D seismic data over Atoll – 2013

• Process and invert 3D survey, map prospect

• Drill exploration well 2014

Poland – Permian Basin Main Dolomite – Conventional Oil

50

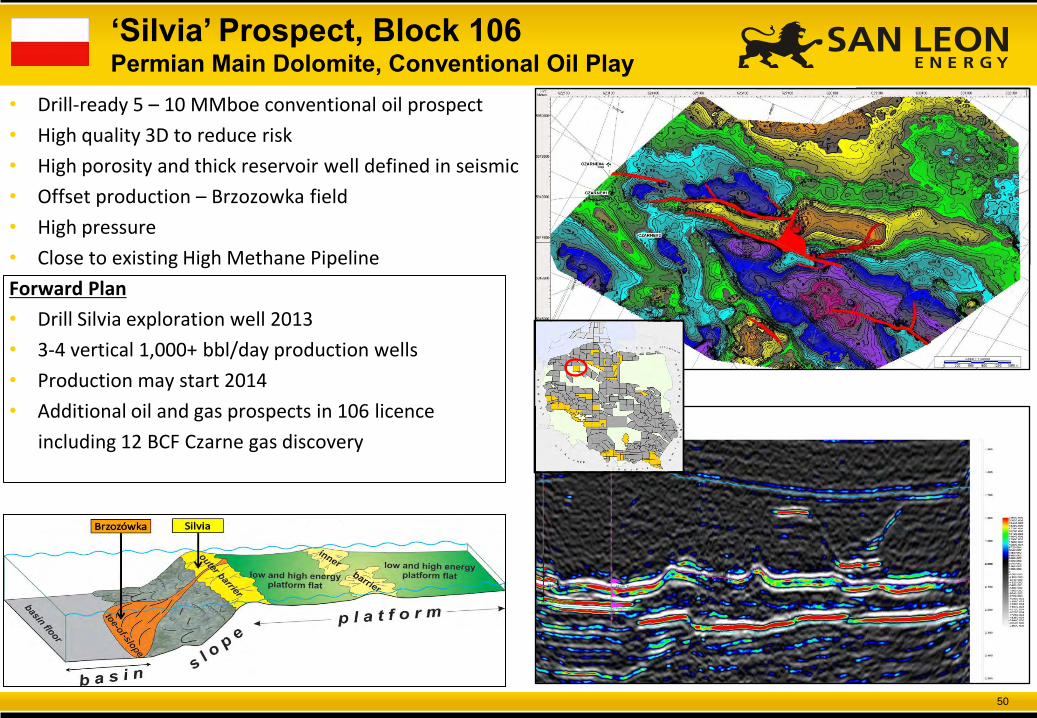

‘Silvia’ Prospect, Block 106 Permian Main Dolomite, Conventional Oil Play

• Drill-ready 5 – 10 MMboe conventional oil prospect

• High quality 3D to reduce risk

• High porosity and thick reservoir well defined in seismic

• Offset production – Brzozowka field

• High pressure

• Close to existing High Methane Pipeline

Forward Plan

• Drill Silvia exploration well 2013

• 3-4 vertical 1,000+ bbl/day production wells

• Production may start 2014

• Additional oil and gas prospects in 106 licence

including 12 BCF Czarne gas discovery

51

Rawicz Permian Rotliegendes, Conventional Gas Plays

• 7+ Tcf conventional gas discovered in Rotliegendes in Polish Permian Basin

• Permian under-explored, little modern 3D data

• San Leon has concessions covering unproduced discoveries:

– Rawicz discovery (~10 Bcf), Rawicz Licence; Czarne discovery (12 Bcf), Block 106 Licence; Dobrzen discovery (9 Bcf), Prusice Licence

• Additional Rotliegendes fields will be imaged in new 3D seismic

– Zuchlow Lead (Gora Licence); Izbice Lead (Gora Licence); Mallorca Lead (Gora/Wschowa Licence); Block 106 Leads

Forward Plan for Rawicz

• Drill Rawicz appraisal well 2013

– anticipate first production 2014

– 12.8 Bcf gross mid case recoverable resource

– Close to existing gas infrastructure

– Additional development wells to follow in 2014 and 2015

• Continue seismic interpretation of Siciny 3D and other Permian Basin 3D’s - further develop Rotliegendes prospects

52 (1) Resources and NPV10 taken from RPS CPR (May 2012)

Siekierki Gas Field, Poznan East Permian Rotliegendes, Tight Sandstone

• Drilling:

• Trzek-1 vertical (2007); (flowed 2.5 mmscf/d)

• Trzek-2 MFHW (2011); (flowed 3.0 mmscf/d)

• Trzek-3 MFHW (2011); (flowed 3.2 mmscf/d)

• NPV10 €383 million gross (1)

Krzesinki-1 Gas Discovery (2011)

• GIIP: 5-20 Bcf GIIP (1)

• 3 bcf Recoverable Resource (Co. est)

• Requires frac of existing well then potential tie in to local industry

Siekierki Gas Field

• Contingent Resources: 422 Bcf 2C Gross Contingent Resources (1)

• GIIP: 2 TCF Mid Case GIIP (1)

• Current Plan: APEX undertaking an independent review of Siekierki to determine the next steps in the commercialisation of the ~9 bcf gas from existing wells and future long term development of the 422 bcf recoverable resource from the field

• Seismic: 420 km2 3D seismic and 500 km 2D seismic since 2007

53

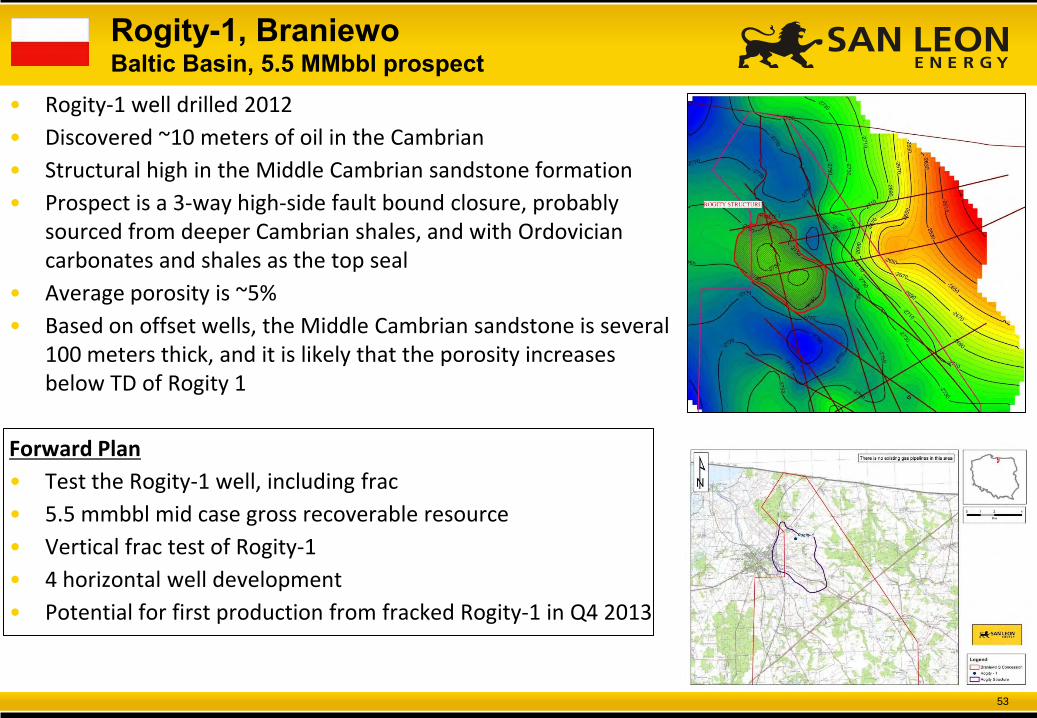

Rogity-1, Braniewo Baltic Basin, 5.5 MMbbl prospect

• Rogity-1 well drilled 2012

• Discovered ~10 meters of oil in the Cambrian

• Structural high in the Middle Cambrian sandstone formation

• Prospect is a 3-way high-side fault bound closure, probably sourced from deeper Cambrian shales, and with Ordovician carbonates and shales as the top seal

• Average porosity is ~5%

• Based on offset wells, the Middle Cambrian sandstone is several 100 meters thick, and it is likely that the porosity increases below TD of Rogity 1

Forward Plan

• Test the Rogity-1 well, including frac

• 5.5 mmbbl mid case gross recoverable resource

• Vertical frac test of Rogity-1

• 4 horizontal well development

• Potential for first production from fracked Rogity-1 in Q4 2013

54

Kowale Trend, Karpaty West Carpathians

San Leon WI • 60% (Operator); PGNiG (40%)

Resources • 220 BCF Net P50 Unrisked Prospective

Resources

Overview

• Four licences 587,000 acres (2,349 km2)

• Working hydrocarbon system with production on licenses

• On trend with numerous fields in Czech Republic, to the west

• Close to existing infrastructure

• Multiple play types with opportunities for multi-target wells

• 52 leads identified on modern 2D seismic

• Relatively shallow target depths

Completed

Activity

• Acquired new 2D seismic

• Reprocessed legacy seismic

Example of a shallow gas amplitude anomaly which will be a likely candidate for upcoming

drilling campaign

Forward Plan

• High-grading of leads into drillable prospects

• Multi-well shallow drilling program planned for late 2013 (truck-mounted rig with low cost shallow wells)

• Possible 3D in 2014

Kowale Anticline Trend

• 220 Bcf Mid Case Prospective Resources

• Low cost drilling

• High recovery >50%

• Close to existing infrastructure

55

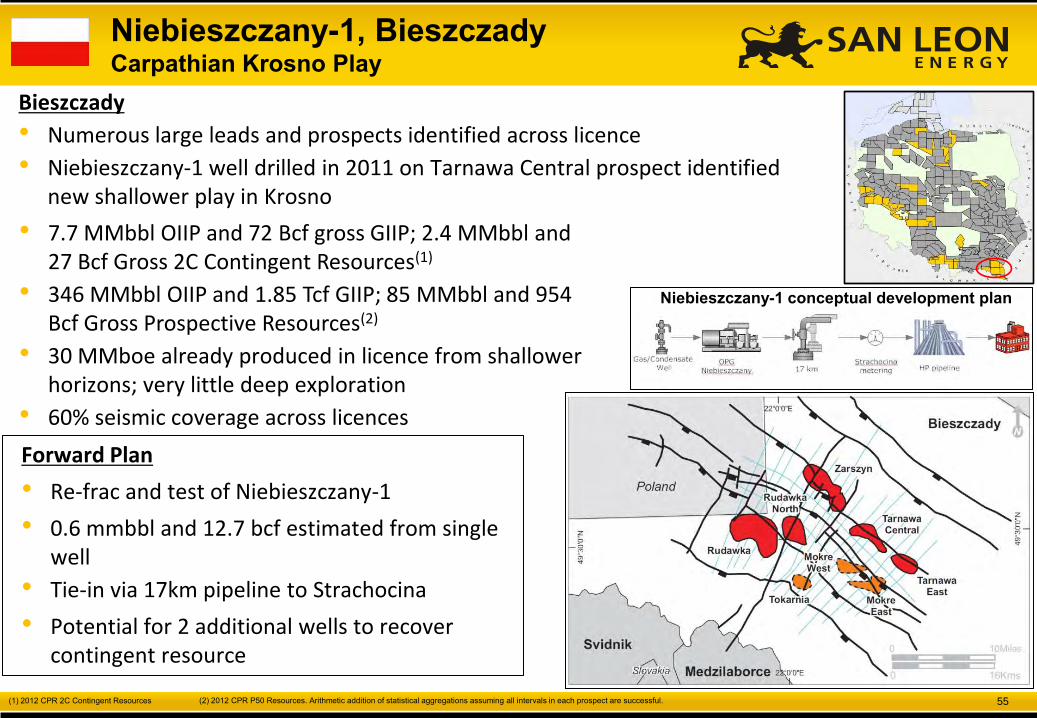

Niebieszczany-1, Bieszczady Carpathian Krosno Play

Bieszczady

• Numerous large leads and prospects identified across licence

• Niebieszczany-1 well drilled in 2011 on Tarnawa Central prospect identified new shallower play in Krosno

• 7.7 MMbbl OIIP and 72 Bcf gross GIIP; 2.4 MMbbl and 27 Bcf Gross 2C Contingent Resources(1)

• 346 MMbbl OIIP and 1.85 Tcf GIIP; 85 MMbbl and 954 Bcf Gross Prospective Resources(2)

• 30 MMboe already produced in licence from shallower horizons; very little deep exploration

• 60% seismic coverage across licences

Forward Plan

• Re-frac and test of Niebieszczany-1

• 0.6 mmbbl and 12.7 bcf estimated from single well

• Tie-in via 17km pipeline to Strachocina

• Potential for 2 additional wells to recover contingent resource

Niebieszczany-1 conceptual development plan

(2) 2012 CPR P50 Resources. Arithmetic addition of statistical aggregations assuming all intervals in each prospect are successful. (1) 2012 CPR 2C Contingent Resources

56

Putna, Brodina Romanian Carpathians

San Leon WI • 50% (Operator); Romgaz (50%)

Resources • 39 MMbbl (net for Putna Prospect) Net P50 Unrisked

Prospective Resources

Overview

• One licence 356,000 acres (1,449 km2)

• Working hydrocarbon system with significant fields on trend

• Best analogue is Lopushna field ~35km to the north (Ukraine) – 47 MMbbl recoverable

• Additional play types include biogenic gas (proven AVO targets)

• 3D will be acquired to de-risk and optimize location for the Putna Prospect, as well as identify other prospects

Completed

Activity

• Acquired new 2D seismic; Reprocessed legacy seismic

• Acquired Magneto-telluric (MT) survey

Planned

Activity

• Acquire ~150 sq km 3D seismic

• Drill Putna Prospect Q1/Q2 2014

Forward Plan

• 150 km2 seismic

• 4,000m Putna Well

• 24 MMbbl oil or 86 bcf gas prospect (50/50)*

* Company Estimated Mid Case Gross Unrisked Recoverable Resource

57

San Leon Energy Plc

Page

1. San Leon Energy Plc Overview 4

2. High Impact Exploration 11

3. Near Term Production 44

4. European Shale Play 57

58

• Several TCF shale gas potential

• Under-explored – Less than 500 exploration wells drilled.

• Active petroleum systems proven.

• Rich source rocks proven in wells and out-crop

• San Leon focus on unconventional resources in Northern Spain

• 2 licences granted

• 8 licences pending

• ~2 Million acres in total

• Excellent fiscal terms

• Current national debate on fracking

• Significant activity in Spain – Repsol

– Shesa

– BNK

– Union Fenosa

– Heyco

– Petroleum Oil and Gas

Spain Unconventional Resources

Geminis 118,463 Cantabrian

Libra 93,365 Cantabrian

Cronos 239,596 Almazon

Aquiles 252,927 Zaragoza

Pegaso 254,232 Pamploma-Jaca

Quimera 249,655 Pamploma-Jaca

Perseo 253,913 Solsona

Prometeo 254,566 Solsona

Atlas 255,349 Solsona

Hellios 256,032 Solsona

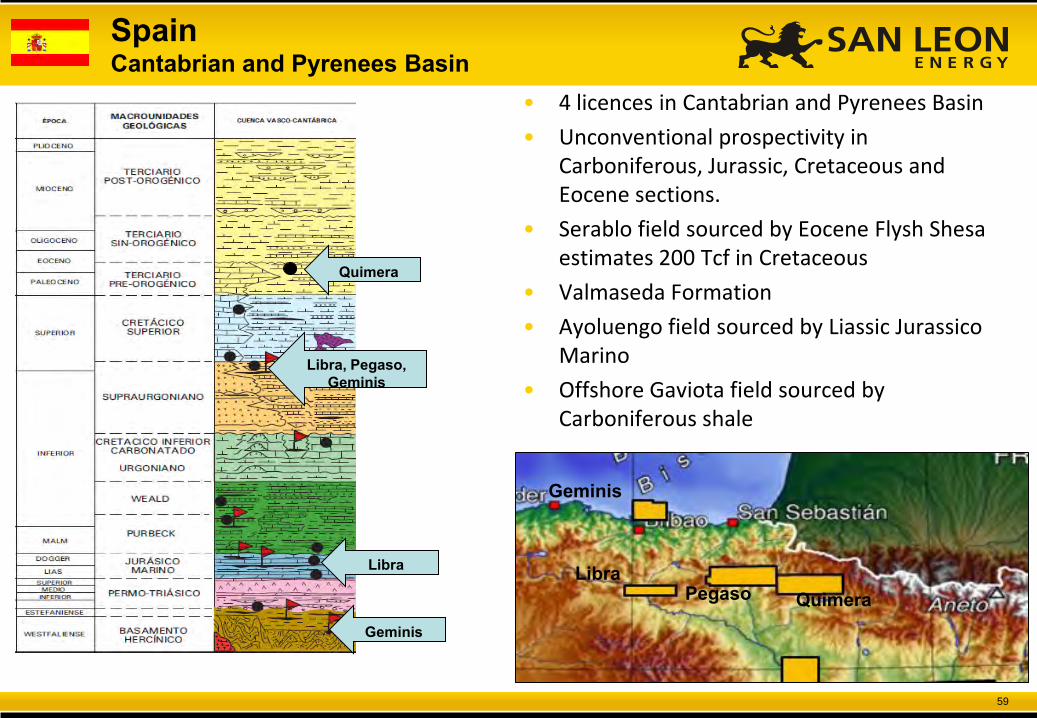

59

• 4 licences in Cantabrian and Pyrenees Basin

• Unconventional prospectivity in Carboniferous, Jurassic, Cretaceous and Eocene sections.

• Serablo field sourced by Eocene Flysh Shesa estimates 200 Tcf in Cretaceous

• Valmaseda Formation

• Ayoluengo field sourced by Liassic Jurassico Marino

• Offshore Gaviota field sourced by Carboniferous shale

Libra

Geminis

Pegaso Quimera

Quimera

Libra, Pegaso, Geminis

Libra

Geminis

Spain Cantabrian and Pyrenees Basin

60

• Shesa estimates 200 Tcf in Valmaseda Fm.

• Tested >30 mmcfd in 1960’s - without stimulation

• Valmaseda Fm. comprised of thick alternating shale sand sequences

• Black Flysch is thick, deep marine, high TOC shale.

• SLE holds > 200,000 acres in Libra and Geminis

Libra

Libra

Geminis

Pegaso Quimera

Spain Cantabrian and Pyrenees Basin

61

• 6 licences in Ebro Basin and sub-basins

• More than 1.5 million acres

• Paleozoic section is main target

• Organic rich shales in Carboniferous, Silurian and Ordovician

• Analogous to shale gas plays in Poland and Germany

• ShaleLog analysis on key wells

• 200 meter Silurian organic shale logged in Ballobar (Prometeo licence)

• 150 meters Paleozoic organic shale logged in Caspe (Helios licence)

• Organic shales well documented in outcrop in nearby mountains

Aquiles

Prometeo Perseo

Atlas Helios

Cronos

Caspe 1 Ballobar 1

Spain Ebro Basin

62

Paris Basin Cross section 4 - Potential Shale Targets

• Prospective > 100 MMboe

• Age: Upper Liassic (Toarcian)

• Kerogen: Type II

• Oil content: 60 kg of HC/ton

• TOC : 1 to 12% (Average 6%)

• Ro: <1.3 % (Oil window)

• Thickness : 10 to 70 m

France: Paris Basin – Licences Under Application

Upper organic shale member

Ba

se

To

arc

ian

T

op

Do

me

ria

n

Lo

we

r D

om

eri

an

Sch

ist

Ca

rto

n

Ba

nc d

e R

oc

Lower organic shale member

Middle Member

Application KM2

Date

Meaux 825 19/11/2009

Meaux (extension) 16 21/02/2011

Dicy 636 21/06/2010

Champcenest 52 15/03/2010

Montmort-Lucy 952 11/12/2009

Phithiviers 1,407 15/03/2010

Courpalay 118 19/11/2009

Sezanne 870 11/12/2009

Sens 775 11/12/2009

Samois S/Seine 370 25/05/2010

Blyes 3,283 20/04/2010

Sens-Est (Extension) 68 In Process

Rouffy 96 In ProcessWilliston Basin Paris Basin

Paris Basin vs. Bakken Shale

Applications Pending

W E

Paris Basin Cross Section

63

• NovaSeis was established in 2011 by San Leon Energy to acquire its onshore seismic data at significantly reduced costs with the flexibility to optimize acquisition parameters in difficult data areas while reducing the surface footprint.

• The Crew has recently completed the acquisition of more than 2,280 km of 2D seismic across SLE’s Tarfaya and Zag Licenses in Morocco; 100 km 2D Poland and 220 km2 3D in Poland with plans for more than 500 km2 3D and 1,500 km 2D in Poland.

NovaSeis

The Crew is equipped with:

• Cableless OYO Geospace Seismic Recorder (GSR) system

• 4,200 GSR/battery units – full 2D and 3D capability

• 5 Sercel NOMAD 65 vibrators sources (65,000 lbs)

• Full surveying capabilities

• In-field processing QC with Vista software

GSR Unit with Battery and Geophone string attached

64

Siekierki Finalise Apex Engineering review prior to decision on

early commercialisation

San Leon Energy Plc Potential 18 Month Forward Plan

2013 - 2014

Czasław, Nowa Sol Acidisation of existing well

Silvia, Block 106 Drill Vertical Exploration Well

Niebieszczany-1 Refrac of existing Well & tie in

Karpaty West Drill 3 shallow vertical Expl

Wells

Rawicz Drill Vertical Exploration Well

Rogity-1 Frac & Test existing well

North Porcupine, Ireland Farm-out of licence prior to

drilling

Putna, Brodina 3D Seismic / Exploration Well

Siciny-2, Gora DFIT & Frac of existing well

Zag, Morocco Conventional gas prospect +

shale gas

Tarfaya, Morocco Casa Mar prospect + oil shale

studies

Durresi, Albania Farm-out of licence with

carried drilling programme

Sidi Moussa, Morocco Genel $50mm carry on

offshore well 2014

Foum Draa, Morocco Cairn $60mm carry on offshore well 2013/14

Gdansk West Frac and test Cambrian oil

potential in existing well

Early Production Potential

High Impact Potential

Medium Term Potential

65

Oisín Fanning Executive Chairman [email protected]

Paul Sullivan Managing Director [email protected]

John Buggenhagen Exploration Director [email protected]

Ireland

3300 Lake Drive

Citywest Business Camp

Dublin 24

Ireland

+353 1 291 6292

London

43 Grosvenor Street

London, W1K 3HL

United Kingdom

+44 20 3617 3913

Warsaw

Mokotowska 1

Zebra Tower

00-640, Warsaw

Poland

+48 22 379 97 00

Nominated Advisor Broker Joint Broker Joint Broker

Westhouse Securities Ltd 1 Angel Court London EC2Y 7HJ

Macquarie Capital Advisers Ropemaker Place 28 Ropemaker Street London EC2Y 9HD

Fox-Davies Capital Ltd. 1 Tudor Street London EC2Y 0AH

FirstEnergy Capital 85 London Wall London EC2M 7AD

Contact Information