Embed Size (px)

Citation preview

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 1/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 1

SUMMER TRAINING REPORT

on

PORTFOLIO MANAGEMENT AND

INVESTMENT TRENDS

Submitted in partial fulfilment of the requirements of the two year

Post Graduate Programme (PGP).

Submitted by:

KESHARPU SEKHAR

Roll No: PG20095518

Batch : 2009-2011

IILM Institute for Higher Education

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 2/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 2

DECLARATION FORM

Ihereby declare that the Project work entitled, PORTFOLIO MANAGEMENT AND

INVESTMENT TRENDS submitted by me for the partial fulfillment of the Post Graduate

Program (PGP) to IILM Institute for Higher Education, is my own original work and has not

been submitted earlier either to IILM or to any other Institution for the fulfilment of the

requirement for any course of study. I also declare that no chapter of this manuscript in whole or

in part is lifted and incorporated in this report from any earlier / other work done by me or others.

Place : GURGAON

Date :10/07/2010

Signature of Student:

Name of Student: KESHARPU SEKHAR

Address : FL-17, NEELANCHAL NAGAR

BERHAMPUR

OR ISSA

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 3/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 3

ACKNOWLEDGEMENT

I wish to express my gratitude to Sharekhan¶s management for giving us anopportunity to be a part of their esteem organization and enhance our knowledge

by granting permission to do our Summer Internship Program under their kindguidance.

I am grateful to Mr. Arvind Kumar (Asst. Sales Manager), our guide, for hisinvaluable guidance and cooperation during the course of the program. He

provided us with his assistance and support whenever needed that has been

instrumental in completion of this program.

I am also sincerely thankful to my faculty guide, Mr.Harsh Vardhan who was of immense help and took up all my queries and suggested me his invaluablesuggestions. His guidance and encouragement has showed the path of fulfillmentto my project.

I want to give my special thanks to all members of IILM, for providing me anopportunity to work on this project with this great organization.

At last I would like to thank all the respondents who I met in the preparation and

who gave their valuable time to provide me with all required information.

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 4/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 4

Executive Summary

This report contains the different investment strategies taken by the

investors (mainly small investors) and the trends of investment in different

investment instruments. Project focused on findings of risk tolerance of

investors and the time horizon they want to remain invested in the market.

The project extended to find out the instrument in which different investors

are now investing.

To understand the trend of the investor I have gone through a field

survey, based on investment strategy questionnaire. The result of the survey

depicts a clear picture of current investment trend in Indian market. The

analysis shows that the age groups of 18-30 years are more adaptable tothe high risk where as the age group of 41-50 are the safe players. Annual

income and the disposable income also played a major role in the

investment strategies in the investor¶s mind. Results reveal that most

investor¶s first priority to invest is the ³Tax Savings´.

The project continues with the Portfolio Management. Its starts by

defining portfolio management in detail. The portfolio management study

has been done on different investment instrument like Savings bank A/c,

ULIP (Unit Linked Insurance Policy), Mutual Funds, Stocks and other

different private Banks and AMC¶s. In the end a hypothetical portfolio is

created.

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 5/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 5

Table of content

Sl. No. Particulars Page no.

1) Industry Study 6

2) Company Profile 12

y Management team 16y Products and Services 16y Competitors 18y SWOT Analysis 19y Training Process 21

3) Project 24

y Introduction 24y Study of Financial Products 31y Field Survey 50y Objective 51y Investment Trend Analysis 52y Recommendations 73y Portfolio Management 76y Creating Portfolio 78

4) Annexure 85

5) References 87

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 6/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 6

Industry Study:Indian Stock Markets are one of the oldest in Asia. Its history dates back to nearly200 years ago. The earliest records of security dealings in India are meager andobscure. The East India Company was the dominant institution in those days and

business in its loan securities used to be transacted towards the close of the

eighteenth century.

By 1830's business on corporate stocks and shares in Bank and Cotton presses took place in Bombay. Though the trading list was broader in 1839, there were only half a dozen brokers recognized by banks and merchants during 1840 and 1850.The 1850's witnessed a rapid development of commercial enterprise and brokerage

business attracted many men into the field and by 1860 the number of brokers

increased into 60.

In 1860-61 the American Civil War broke out and cotton supply from UnitedStates of Europe was stopped; thus, the 'Share Mania' in India begun. The number of brokers increased to about 200 to 250. However, at the end of the AmericanCivil War, in 1865, a disastrous slump began (for example, Bank of Bombay Share

which had touched Rs 2850 could only be sold at Rs. 87).

In 1887, they formally established in Bombay, the "Native Share and Stock

Brokers' Association" (which is alternatively known as "The Stock Exchange"). In1895, the Stock Exchange acquired a premise in the same street and it wasinaugurated in 1899. Thus, the Stock Exchange at Bombay was consolidated.

Thus in the same way, gradually with the passage of time number of exchanges

were increased and at currently it reached to the figure of 24 stock exchanges.

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 7/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 7

TRANSACTION CYCLE:

A person holding assets (Securities/Funds), either to meet his liquidity needs or to

reshuffle his holdings in response to changes in his perception about risk and return

of the assets, decides to buy or sell the securities. He selects a broker and instructs

him to place buy/sell order on an exchange. The order is converted to a trade as

soon as it finds a matching sell/buy order. At the end of the trade cycle, the trades

are netted to determine the obligations of the trading member¶s securities/funds as

per settlement cycle. Buyer/seller delivers funds/ securities and receives

securities/funds and acquires ownership of the securities.

A securities transaction cycle is presented above. Just because of this Transaction

cycle, the whole business of Securities and Stock Broking has emerged. And as an

Placing Order

Settlement of

trades

Decision totrade

Trade

Execution

Clearing of

Trades

Funds or

Securities Transaction

Cycle

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 8/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 8

extension of stock broking, the business of Online Stock broking/ Online Trading/

E-Broking has emerged.

HISTORY OF ONLINE TRADING:

Online stock trading is very old concept for big institutions who tradethru private networks owned by Reuter's "Instinet" and a system called"Posit" since 1969. But it becomes internet based for lay men only in late 90s.

Funny, that actually idea was first time used by a company making Beer called "WIT beer" to help its shareholders trade its shares. That¶s how "WIT

Capital" was born which is considered pioneer of this concept. It was mademainstream and household name by a offshoot of Charles Schwab & Co called

eSchwab which is used by millions of people in USA.L

ot of NR I

's i know playin US stock market even when they come to India for holidays via websiteof eSchwabe.

There are other serious players like E*trade, DATEK online etc. All thiscompanies ask you to start account with US $5000 and you can buy and sellstock using these funds. They also issue you a check book which you can useto make payments from this account. Or use their ATM card to withdraw cashfrom your stock trading account.

Today practically every big name brokerage firm offers online stock tradingas it reduces their costs. Earlier they had army of brokers on phone withclients executing trade, which is done by computers accepting orders fromclients directly. This firm now offers human access to high net worth accounts, andto rest at charge per trade.

E- Broking - A small beginning:

You have some money to dabble with. Trading shares on BSE/NSE has always been your dream. When will you ever find the time? And besides, the hassle of finding a broker is not easy. Realizing there is untapped market of investors whowant to be able to execute their own trades when it suits them, brokers have taken

their trading rooms to the Internet. Known as online brokers, they allow you to buyand sell shares via Internet.

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 9/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 9

There are 2 types of online trading service: discount brokers and full service

online broker. Discount online brokers allow you to trade via Internet at reducedrates. Some provide quality research, other don¶t. Full service online brokerage islinked to existing brokerages. These brokers allow their clients to place onlineorders with the option of talking/ chatting to brokers if advice is needed. Brokeragerates here are higher. 5Paisa.com, ICICIDirect.com, IndiaBulls.com,

Sharekhan.com, Geojit securities.com, HDFCsec.com, Tatatdw.com,Kotakstreet.com are some of the online broking sites in India. With Net trading insecurities and rapid consolidation between multiple stock exchanges, theinternational securities marketplace is fast becoming a "global village" through thecreation of a universal virtual equity market.

Compared to the Western countries, online trading is still in its infancy in India.

With trading turnover at around Rs. 10 crores per day from online tradingcompared to a combined gross turnover of around Rs. 9000-10,000 crores handled

by the BSE and NSE together, online trading has a long way to go.

INTERNET TRADING IN INDIA:

In the past, investors had no option but to contact their broker to get real time

access to market data. The Net brings data to the investor on line and net brokingenables him to trade on a click. Now information has become easily accessible to

both retail as well as big investors.

The development of broking in India can be categorized in 3 phases:1. Stock brokers offering on their sites features such as live portfolio manager, livequotes, market research and news to attract more investors.2. Brokers offering on line broking and relationship management by providing andoffering analysis and information to investors during broking and non- brokinghours based on their profile and needs, that is, customized services.3. Brokers (now e- brokers) will offer value management or services such as initial

public offerings on line, asset allocation, portfolio management, financial planning,tax planning, insurance services and enable the investors to take better and well-

considered decisions.

Market Size: Growth of Online Brokerage market:

In five years of its existence in India, online broking has grown to account for atenth of the total trading volumes. If the numbers are considered for only the retailsegments, the growth is starker. Almost half of the Rs 5,000 crore-6,000 crore

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 10/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 10

daily market volumes on the NSE are accounted for by non-retail entities such asforeign institutional investors, domestic institutions, mutual funds and arbitragetraders. Institutions aren't online customers anyway. Of the rest of the retailsegment, current estimates suggest that online broking's reach is close to 30 per cent.

As of September this year, there were 11.7 lakhs Internet trading accounts

registered with the NSE, of which roughly 9.5 lakhs are unique users. It's still asmall proportion of the estimated 3 crore Internet users in the country. As moresurfers take to trading online, analysts expect their number to keep doubling everyyear until 30-40 per cent of India's overall trades are done online, as is the case insome mature Internet markets like South Korea's.

The Internet's effect here has more to do with the bandwidth it has created for both

brokers and clients. Banga, director of India bulls offers an example. "Traders fromAjmer use our online platform. It would otherwise have been prohibitively loss-making to open a branch there." Thanks to the new channel, volumes are growingfaster in the non-metros, where transparency is low in offline trading. "Thesecustomers were made to pay higher charges by small brokers, since they weren'taware of the market rates," says Vikash Shankar of Sharekhan.com.That is one of

the reasons why more than 60 per cent of Sharekhan¶s online trading turnover comes from non-metros.

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 11/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 11

Company Profile

Sharekhan Ltd. is one of the leading retail stock broking house of SSK I Groupwhich is running successfully since 1922 in the country. It is the retail broking armof the Mumbai- based SSK I Group, which has over eight decades of experience inthe stock broking business. Sharekhan offers its customers a wide range of equityrelated services including trade execution on BSE, NSE, Derivatives, depositoryservices, online trading, investment advice etc. The firm¶s online trading andinvestment site - www.sharekhan.com ± was launched on Feb 8, 2000. The sitegives access to superior content and transaction facility to retail customers acrossthe country. Known for its jargon-free, investor friendly language and high qualityresearch, the site has a registered base of over one lakh customers. The content-richand research oriented portal has stood out among its contemporaries because of itssteadfast dedication to offering customers best-of - breed technology and superior market information. The objective has been to let customers make informed

decisions and to simplify the process of investing in stocks.

On April 17, 2002 Sharekhan launched Speed Trade, a net- based executableapplication that emulates the broker terminals along with host of other informationrelevant to the Day Traders. This was for the first time that a netbased tradingstation of this caliber was offered to the traders. In the last six months Speed Tradehas become a de facto standard for the Day Trading community over the net.

Sharekhan¶s ground network includes over 331 centers in 137 cities in India which provide a host of trading related services.

Sharekhan has always believed in investing in technology to build its business. Thecompany has used some of the best-known names in the IT industry, like Sun

Microsystems, Oracle, Microsoft, Cambridge Technologies, Nexgenix, Vignette,Verisign Financial Technologies India Ltd, Spider Software Pvt Ltd. To build itstrading engine and content.

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 12/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 12

The Morakhiya family holds a majority stake in the company. HSBC, Intel &Carlyle are the other investors. With a legacy of more than 80 years in the stock markets, the SSK I group ventured into institutional broking and corporate finance18 years ago. Presently SSK I is one of the leading players in institutional brokingand corporate finance activities. SSK I holds a sizeable portion of the market ineach of these segments. SSK I¶s institutional broking arm accounts for 7% of themarket for Foreign Institutional portfolio investment and 5% of all Domestic

Institutional portfolio investment in the country. It has 60 institutional clientsspread over India, Far East, UK and US. Foreign Institutional Investors generateabout 65% of the organization¶s revenue, with a daily turnover of over US$ 2million. The Corporate Finance section has a list of very prestigious clients and hasmany µfirsts¶ to its credit, in terms of the size of deal, sector tapped etc. The grouphas placed over US$ 1 billion in private equity deals. Some of the clients includeBPL Cellular Holding, Gujarat Pipavav, Essar, Hutchison, Planetasia, and

Shopper¶s Stop.

PROFILE OF THE COMPANY :

Name of the company : Sharekhan ltd.

Year of Establishment : 1925

Headquarter : ShareKhan SSK I

A-206 Phoenix HousePhoenix Mills Compound

Lower ParelMumbai - Maharashtra, I NDIA- 400013

Nature of Business : Service Provider

Services : Depository Services, Online Services andTechnical Research.

Number of Employees : Over 3500

Website : www.sharekhan.com

Slogan : Your Guide to The Financial Jungle.

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 13/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 13

ACHIEVEMENTS OF SHAREKHAN:

Rated among the top 20 wired companies along with Reliance, HUJl, Infosys, etc by µBusiness Today¶, January 2004 edition.

Awarded µTop Domestic Brokerage House¶ four times by Euro money andAsia money.

Pioneers of online trading in India amongst the top 3 online trading websitesfrom India. Most preferred financial destination amongst online brokingcustomers.

Winners of ³Best Financial Website´ award.

India¶s most preferred brokers within 5 years. ³Awaaz customers Award 2005´.

Vision :

To be the best retail brokering Brand in the retail business of stock market.

Mission :

To educate and empower the individual investor to make better investmentdecisions through quality advice and superior service.

Sharekhan is infact-

Among the top 3 branded retail service providers

No. 1 player in online business

Largest network of branded broking outlets in the country serving morethan 7,00,000 clients.

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 14/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 14

Get everything you need at a Sharekhan outlet!

All you have to do is walk into any of our 640 share shops across 280 cities in

India to get a host of trading related services - our friendly customer service staff

will also help you with any accouts related queries you may have.

A Sharekhan outlet offers the following services:

Online BSE and NSE executions (through BOLT & NEAT terminals)

Free access to investment advice from Sharekhan's Research team

Sharekhan ValueLine (a monthly publication with reviews of recommendations,

stocks to watch out for etc) Daily research reports and market review (High Noon & Eagle Eye)

Pre-market Report (Morning Cuppa)

Daily trading calls based on Technical Analysis

Cool trading products (Daring Derivatives and Market Strategy)

Personalised Advice

Live Market Information

Depository Services: Demat & Remat Transactions

Derivatives Trading (Futures and Options)

Commodities Trading IPOs & Mutual Funds Distribution

Internet-based Online Trading: SpeedTrade

SHAREKHAN LIMITED¶S MANAGEMENT TEAM:

Mr. Dinesh Murikya :Owner of the company

Mr. Tarun Shah :Chief Executive Officer (CEO) of the company

Mr. Shankar Vailaya : Director (Operations) of the company

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 15/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 15

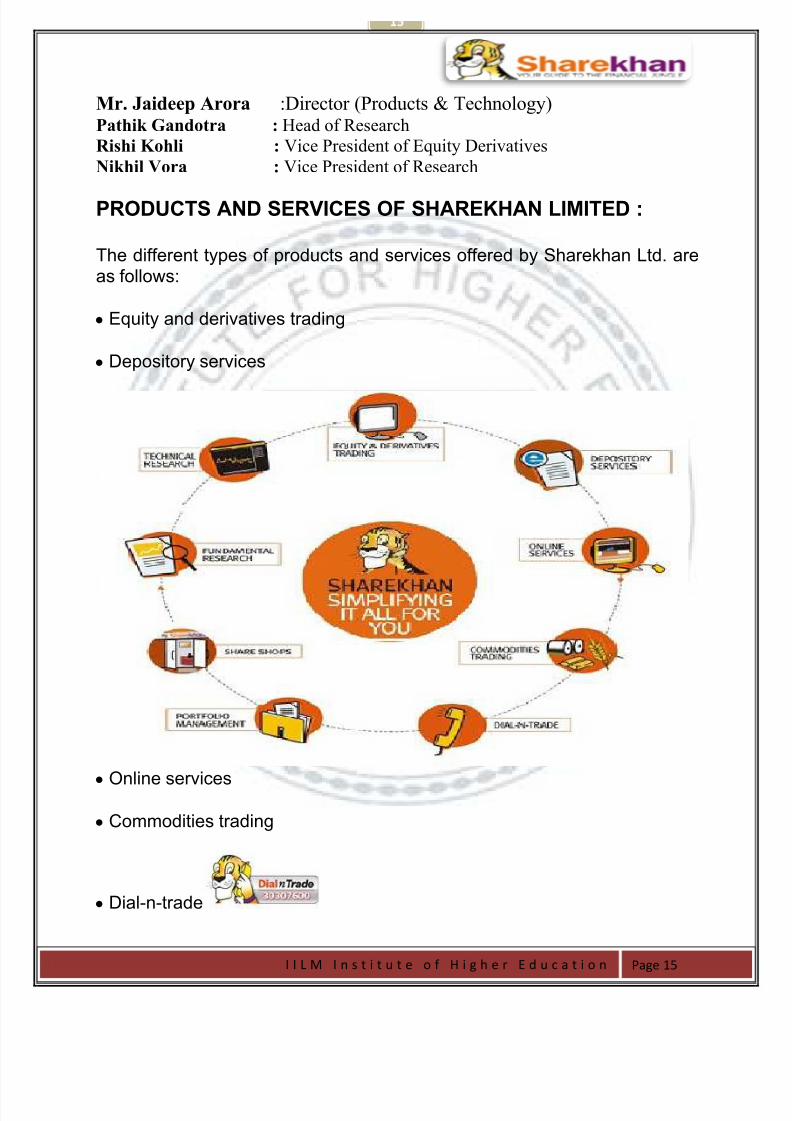

Mr. Jaideep Arora :Director (Products & Technology) Pathik Gandotra : Head of ResearchRishi Kohli : Vice President of Equity DerivativesNikhil Vora : Vice President of Research

PRODUCTS AND SERVICES OF SHAREKHAN LIMITED :

The different types of products and services offered by Sharekhan Ltd. areas follows:

yEquity and derivatives trading

yDepository services

y

Online services

yCommodities trading

yDial-n-trade

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 16/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 16

yPortfolio management

yShare shops

yFundamental research

yTechnical research

FINANCIAL PRODUCTS AVAILABLE AT SHAREKHAN:

SHAREKHAN

EQUITY

CASH

MARGIN

BTST

SPOT

DERIVATIVES

FUTURES

OPTIONS

MUTUALFUNDS

PURCHASES

REDEMPTION

SIP & SWP

SWITCHIN/OUT

TRANSFER IN

IPOs BONDS

GOI BONDSSHAREKHAN

BONDS

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 17/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 17

COMPETITORS:

SWOT ANALYSIS:

Strengths:

y It is a pioneer in online trading with a turn over of Rs.400crores and

more than 800 peoples working in the organization.

y

SSKI the parent company of Share Khan has more than eight decades of trust and credibility in the Indian stock market. In the Asian Money

Brokers poll SSKI won the Indias best broking house for 2004 award.

y Share Khan provides multi-channel access to all its customers through a

strong online presence with www.sharekhan.com, 250 share shops in

130 cities and a call-center based Dial-n-Trade facility

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 18/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 18

y Share Khan has dedicated research teams for fundamental and technical

research. Which constantly track the pulse of the market and provide

timely investment advice free of cost to its clients which has a strike rate

of 70-80%.

Weakness:

y Localized presence due to insufficient investments for country wide

expansion.

y Lack of awareness among customers because of non-aggressive

promotional strategies (print media, newspapers, etc).

y Lesser emphasis on customer retention.

y Focuses more on HNIs than retail investors which results in meager

market-share as compared to close competitors.

Opportunities:

y With the booming capital market it can successfully launch new services

and raise its clients base.

y It can easily tap the retail investors with small saving through promotional

channels like print media, electronic media, etc.

y As interest on fixed deposits with post office and banks are all time low,

more and more small investors are entering into stock market.

y Abolition of long term capital gain tax on shares and reduction in short

term capital gain is making stock market as hot destination for investment

among small investors.

y Increasing usage of internet through broadband connectivity may boost a

whole new breed of investors for trading in securities.

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 19/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 19

Threats:

y Aggressive promotional strategies by close competitors may hamper Share

Khans acceptance by new clients.

y Lack of sufficient branch-offices for speedy delivery of services.

y Other players are providing margin funds to investors on easy terms where

as there is no such facility in share khan.

y More and more players are venturing into this domain which can further

reduce the earnings of Share Khan.

TRAINING PROCESS:

Student¶s work profile(role and responsibilities) :

I worked there with SHAREKHAN LTD. with a profile of Customer Acquisitionand Revenue Generation. This profile offerered me to understand the need of customer and provide them the best deal possible with maximization of the profit,

both for the company as well as for the customer.

So for fulfillment of the targets one needs to:

y Capitalize on the old and loyal clientage which can be building slowly by

advising people in the best possible way.

y Generating new leads through various activities.

Generation of leads :

Since I was new in the field so I had to start from scratch and generate new

leads to sustain in the market.

Cold calling is one of the trusted ways of getting to the customers without meetingthem. Although the rate of conversion remained very less, for cold calling thequality and accent remains a very important criterion. This activity gave me mixed

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 20/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 20

result. I often got success and generated many leads through it but it also landedme in awkward position where the customer were in different mood and made ushear words for which a marketer should be always prepared to hear. Corporatecalls always remained more difficult to crack with respect to retail sector.Thecorporate were the most difficult and most temping to get the business from. Ittook me one one day to crack Hi-tech Gears.

At SHAREKHAN I was provided with detailed training regarding share market,how it operates and also how to trade via its online portal and also through itsapplication software i.e Trade Tiger. Information regarding equities trading,derivatives trading and commodities trading was also provided.

After the third week my performance also improved and I was able to get close tothe targets, though it looked difficult to achieve in the beginning. To get awareness

of the every product I attended diversified calls. This helped me to implementcross selling to get better results.

LIMITATIONS of Cold Calling:

Voice and accent plays a major role.

The right time to call a customer cannot be decided, as the customer may in

a different mood at the time of calling.

Time consuming

Less success rate

Description of live experience :

I was supposed to use the database provided by the company to make cold calls or

by directly meeting people to get new leads.

While making cold calls, we need to have:

Good Communication Skills (Voice quality is clear and articulate)

Persistent and able to bounce back from rejection

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 21/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 21

Good organizational skills.

Ability to project a telephone personality (Enthusiasm, friendliness)

Flexibility: can adapt to different types of clients and new situations.

Using a good database is very essential.

³Eighty percent of our business comes from 20 percent of our customers" is afrequent statement at any sales convention. There's hardly a sales executive who isnot aware of the 80/20 rule´.

While talking to customers, I analyze their needs. Whether they want to go for

investment purpose or insurance or both. Suggest them the plan that best suitsthem. If they agree to it then either we send across the agents to close the deal or close it themselves.

Problems faced while selling products:

Past experience, word of mouth.

People do not want security products.

Lack of knowledge and less awareness about demat account.

People risk appetite is very low, so they are afraid of mutual fund as well.

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 22/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 22

PROJECT :

Introduction:

Indian economy and Investment Sectorial growth:

India economy is developing at a fast rate and every sector of Indiaeconomy is showing a positive growth. The growth development product in

India in the year 2006-07 is 9.2%. The rate of robust growth of in industrial

development is 10.6%. µThe Economists¶ have also observed high growth in

manufacturing sector and telecommunication sectors. The Infrastructure

sector is also showing impressive growth in the year 2006-07. The

secondary sectors as also shown upward growth, the BSE and NSE sensex

has closed at high marks of 21000 and 7000 respectively. In this way all

these sectors have contributed to overall growth of Indian economy.

Behind China, India is the second fastest growing economy. According

to a survey by Goldman Sachs, India will become the 3rd largest economy

by 2035. This is measured in $US. If we use PPP (purchasing power parity)

which takes into account local purchasing power, India already has the 3rd

largest economy.

The economy has been growing at an average growth rate of 8.8 per

cent in the last four fiscal years (2003-04 to 2006-07), with the 2006-07

growth rate of 9.6 per cent being the highest in the last 18 years.

Significantly, the industrial and service sectors have been contributing amajor part of this growth, suggesting the structural transformation

underway in the Indian economy.

Within the investment sector the real estate is raising sky high due to

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 23/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 23

Strong Economic Growth: The world¶s fourth largest economy, growing at

over 8% the last two years and forecast to grow at over 7% over the next

five; Growth measures supported across the political spectrum; a boom in

the services sector with a strong revival of industry; powerful internal

consumption and demand.

The Rise of the Middle-Class: 300 million and growing with higher

disposable incomes and even higher aspirations; educated, professional

workforce driving urbanization beyond the traditional metro cities.

.

Before I start I have to explain what investment is and why people

want to invest? It is very important for me to understand how people plan

before investing. These things are discussed below:

INVESTMENTS

nvestment = Cost Of Capital, like buying securities or other monetary or

paper (financial) assets in the money markets or capital markets, liquid real

assets, such as gold, real estate, or collectibles. Types of financial

investments include shares, other equity investment, and bonds. These financial

assets are then expected to provide income or positive future cash flows, and mayincrease or decrease in value giving the investor capital gains or losses.

People usually invest when they have good amount of ideal money to

spend. The main objective is to save money for future uncertainties, capital

appreciation, more income and most of all tax savings.

Investing is not guesswork or prediction. It takes more than just a

µtip¶; it needs training to plan, instinct to pick and sheer intellect to make it

work for the investor. Human nature is fickle, his wants keep changing.

An investment can be described as perfect if it satisfies all the needs of

all investors. So, the starting point in searching for the perfect investment

would be to examine investor needs. If all those needs are met by the

investment, then that investment can be termed the perfect investment.

I

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 24/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 24

Most investors and advisors spend a great deal of time understanding the

merits of the thousands of investments available in India. Little time,

however, is spent understanding the needs of the investor and ensuring that

the most appropriate investments are selected for him.

Why people invest?

Investors do invest in different instrument to simplify their lifestyle and to

make certain goals in future life. Most investors invest for the long term to

fulfill the inflation and for the capital appreciation. By and large the investors

have typical requirement to fill, and those are:-

y Capital preservation: - The chance of losing some capital has been a

primary need. This is perhaps the strongest need among investors in

India, who have suffered regularly due to failures of the financial

system.

y Wealth generation: - This is largely a factor of investment

performance, including both short-term performance of an investment

and long-term performance of a portfolio. Wealth accumulation is the

ultimate measure of the success of an investment decision.

y Life Cover:- Many investors look for investments that offer good

return with adequate life cover to manage the situations in case of any

eventualities. Recent days investors do invest in the endowment

policies and ULIPs.

y Tax savings: Legitimate reduction in the amount of tax payable is an

important part of the Indian psyche. Every rupee saved in taxes goes

towards wealth accumulation.

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 25/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 25

y Income: This refers to money distributed at intervals by an

investment, which are usually used by the investor for meeting regular

expenses. Mostly daily traders invest for income.

y Future Uncertainty: - No one has seen the future so every person

personally save money for any contingencies. People invest in short

term for this. There must be an easy cash withdraw for the

contingencies.

y Ease of withdrawal: This refers to the ability to invest long term but

withdraw funds when desired. This is strongly linked to a sense of

ownership. It is normally triggered by a need to spend capital, change

investments or cater to changes in other needs.

y Beat inflation: - inflation is a major player in the economy. It

reduced the valuation of rupee. Investors do in vest to maintain the

buying capacity of them.

y Retirement planning: - most of the service person do invest to get

return after the vesting period, for that the investment such a manner

that the returns comes at the time of retirement.

Investment Planning

Investors need to identify the financial goals throughout life or for the

next 10 to 15 years depending upon the time horizon selected by the

investor, and prioritizing them. Investment Planning is important because it

helps in deriving the maximum benefit from the investments.

Success as an investor depends upon his investment in right

instrument in right time and for the right period. This, in turn, depends on

the requirements, needs and goals. For most investors, however, the three

prime criteria of evaluating any investment option are liquidity, safety and

level of return.

Investment Planning also helps to decide upon the right investment

strategy. Besides individual requirement, investment strategy would

also depend upon age, personal circumstances and risk appetite.

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 26/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 26

Investment Planning also helps in striking a balance between risk and

returns. By prudent planning, it is possible to arrive at an optimal mix

of risk and returns, which suits particular needs and requirements.

Investment means putting the ideal money to work to earn more

money. Done wisely, it can help you meet financial goals. Investing

even a small amount can produce considerable rewards over the long-

term, especially if you do it regularly. But one needs to decide about

how much he / she wants to invest and where.

Options before investment

Investors choose wisely before investing which solely depends on the

present market conditions, future prospect of the instrument, the

return offered by the company and the season to invest in that

particular instrument. For example, a good investment for a long-term

life insurance plan may not be a good investment for higher education

expenses. In most cases, the right investment is a balance of three

things: Liquidity, Risk tolerance and Return.

Liquidity ± How easily an investment can be converted to cash, since

part of invested money must be available to cover financial

emergencies.

Risk tolerance - The biggest risk is the risk of losing the money thathas been invested, but the main thing is to how much investor can

cover up and sustain with that. Another equally important risk is that

investments may not provide enough growth or income to offset the

impact of inflation, which could lead to a gradual increase in the cost

of living. There are additional risks as well (like decline in economic

growth). But the biggest risk of all is not investing at all.

Return - Investments are made for the purpose of generating returns.

Safe investments often promise a specific, though limited return.

Those that involve more risk offer the opportunity to make - or lose - a

lot of money.

The Investment Process

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 27/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 27

Investors like to invest through the instinct and want to gain

profit from the market by investing. However, while financial

institutions are undoubtedly a part of the process of investing. As

investors, it is not surprising that we focus so much of our energy and

efforts on investment philosophies and strategies, and so little on theinvestment process. It is far more interesting to read about how Peter

Lynch picks stocks and what makes Warren Buffett a valuable investor,

than it is to talk about the steps involved in creating a portfolio or in

executing trades. Though it does not get sufficient attention,

understanding the investment process is critical for every investor for

several reasons:

1. Investment planning centrally depends upon the portfolio of theinvestor; as a result the primary step of the investment process is to

make a portfolio. By emphasizing the sequence, it provides for an

orderly way in which an investor can create his or her own portfolio or

a portfolio for someone else.

2. The investment process provides a structure that allows investors to

see the source of different investment strategies and philosophies. By

so doing, it allows investors to take the hundreds of strategies thatthey see described in the common press and in investment newsletters

and to trace them to their common roots.

3. The investment process emphasizes the different components that are

needed for an investment strategy but strategies that look good on

paper never work for those who use them.

STEPS INVOLVED IN INVESTMENT PLANNING

Investment is not only prediction it has its own reasons behind every up and

down in the market. So it is has its own theory to move in particular

directions. To get in to the market investors must go through the following

process.

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 28/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 28

Analysis and profiling of the instrument: - The first step is

performing a Need Analysis check. The requirements and expectations

of the investor should be met by the instrument. During the profiling

investor should consider their age, their profession, the number of

dependents, and their income. By doing this check, the risk profile of the investor should be designed.

Evaluating the alternatives: - The next step would be revaluating

the needs. Other investment instruments and options should be

analyzed. The risk-return profile of investment products is evaluated in

this step. Every investment product varies according to its return

potential and riskiness. Investment products giving a high rate of

return are generally risky and volatile. The products giving a lowerrate of return usually are less risky.

Analyse the Profile: - The next step would be analyse the risk-return

profile of the investor on to the investment portfolio. The investment

instruments are matched with the risk-return profile of the investor. All

the investment alternatives that offer expected rate of return are

evaluate for consideration.

Preparing an Optimum Portfolio: - Then according to the risk

appetite and return pattern an optimum portfolio is designed for the

investor. The basket of investment instrument selected in the previous

step are given due weightage and appropriate amount of money is

invested in each of the investment avenue so as to get maximum

return with minimum possible risk.

Consistent Monitoring: - Finally a continuous watch on the portfoliois extremely important. Fundamental analysis of the investment

products done in the previous stages would only help in selecting the

right product but the right time of entry or exit from a particular

stream is evaluated by doing a technical analysis. For this professional

portfolio management is a must.

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 29/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 29

STUDY OF FINANCIAL PRODUCTS

Investment options in India

Savings Bank Account (SB A/c)

Saving Bank account (SB account) is meant to promote the habit of saving

among the people. It also facilitates safekeeping of money. In this schemefund is allowed to be withdrawn whenever required, without any condition.

Hence a savings account is a safe, convenient and affordable way to save

money. Banks generally put some restrictions on the total number of

withdrawals permitted during specific time periods. Banks also stipulate

certain minimum balance to be maintained in savings accounts. Normally a

higher minimum balance is stipulated in cheque operated accounts as

compared to non-cheque operated accounts.

Features:The minimum amount to open an account in a nationalized bank is Rs 500. If

cheque books are also issued, the minimum balance of Rs 1000 has to be

maintained. However in some private or foreign bank the minimum balance

is Rs 5,000 or more and can be up Rs. 10,000. One cheque book is issued to

a customer at a time.

Analysis and profiling of

the instrument

Evaluating the

alternatives

Analyse the

Profile

Preparing an

Optimum Portfolio

Consistent Monitoring Investment

planning

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 30/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 30

A Savings account can be opened either individually or jointly with another

individual. In a joint account only the sign of one account holder is needed

to write a cheque. But at the time of closing an account, the sign of the both

the account holders are needed.

Certain non-profit welfare organizations are also permitted to open Savings

bank accounts with banks.

Return

Interest @ 3.5 % p.a. with effect from 1/3/2003.

The amount of interest will be calculated for each calendar month on the

lowest balance in credit of any account between the close of the tenth day

and the last day of each month. In Savings Bank account, bank follows the

simple interest method. The rate of interest may change from time to timeaccording to the rules of Reserve Bank of India.

One can withdraw his/her money by submitting a cheque in the bank and

details of the account, i.e. the Money deposited, withdrawn along with the

dates and the balance, is recorded in a passbook.

y Advantages

It's much safer to keep your money at a bank than to keep a large

amount of cash in your home.y Bank deposits are fairly safe because banks are subject to control of

the Reserve Bank of India with regard to several policy and operational

parameters, many of the banks also give internet banking facility

through with one do the transactions like withdrawals, deposits,

statement of account etc.

y Banks provide Auto-Mated Teller machine(ATM) for 24 hours cash

withdrawn, some banks also have 24 hours open branches in very few

selected cities.

Mutual fund in India

A mutual fund is nothing more than a collection of stocks and/or bonds. Youcan think of a mutual fund as a company that brings together a group of people and invests their money in stocks, bonds, and other securities. Eachinvestor owns shares, which represent a portion of the holdings of the fund.

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 31/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 31

You can make money from a mutual fund in three ways:

1) Income is earned from dividends on stocks and internet on bonds. A fundpays out nearly all of the income it receives over the year to fund owners inthe form of a distribution.

2) If the fund sells securities that have increased in price, the fund has acapital gain. Most funds also pass on these gains to investors in adistribution.3) If fund holdings increase in price but are not sold by the fund manager,the fund's shares increase in price. You can then sell your mutual fundshares for a profit.

Funds will also usually give you a choice either to receive a check fordistributions or to reinvest the earnings and get more shares.

Advantages of Mutual Funds:

Professional Management - The primary advantage of funds (at leasttheoretically) is the professional management of your money. Investors

purchase funds because they do not have the time or the expertise tomanage their own portfolios. A mutual fund is a relatively inexpensive wayfor a small investor to get a full-time manager to make and monitorinvestments.

Diversification - By owning shares in a mutual fund instead of owningindividual stocks or bonds, your risk is spread out. The idea behinddiversification is to invest in a large number of assets so that a loss in any

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 32/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 32

particular investment is minimized by gains in others. In other words, themore stocks and bonds you own, the less any one of them can hurt you(think about Enron). Large mutual funds typically own hundreds of differentstocks in many different industries. It wouldn't be possible for an investor tobuild this kind of a portfolio with a small amount of money.

Economies of Scale- Because a mutual fund buys and sells large amounts of securities at a time, its transaction costs are lower than what an individualwould pay for securities transactions.

Liquidity- Just like an individual stock, a mutual fund allows you to requestthat your shares be converted into cash at any time.

Simplicity - Buying a mutual fund is easy! Pretty well any bank has its ownline of mutual funds, and the minimum investment is small. Most companiesalso have automatic purchase plans whereby as little as $100 can beinvested on a monthly basis.

Disadvantages of Mutual Funds:

Professional Management - Did you notice how we qualified the advantageof professional management with the word "theoretically"? Many investorsdebate whether or not the so-called professionals are any better than you orI at picking stocks. Management is by no means infallible, and, even if the

fund loses money, the manager still takes his/her cut. We'll talk about this indetail in a later section.

Costs - Mutual funds don't exist solely to make your life easier - all fundsare in it for a profit. The mutual fund industry is masterful at burying costsunder layers of jargon. These costs are so complicated that in this tutorialwe have devoted an entire section to the subject.

Dilution - It's possible to have too much diversification. Because fundshave small holdings in so many different companies, high returns from a few

investments often don't make much difference on the overall return. Dilutionis also the result of a successful fund getting too big. When money poursinto funds that have had strong success, the manager often has troublefinding a good investment for all the new money.

Taxes - When making decisions about your money, fund managers don't

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 33/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 33

consider your personal tax situation. For example, when a fund managersells a security, a capital-gains tax is triggered, which affects how profitablethe individual is from the sale. It might have been more advantageous forthe individual to defer the capital gains liability.

No matter what type of investor you are, there is bound to be a mutual fundthat fits your style. According to the last count there are more than 10,000mutual funds in North America! That means there are more mutual fundsthan stocks.

It's important to understand that each mutual fund has different risks andrewards. In general, the higher the potential return, the higher the risk of loss. Although some funds are less risky than others, all funds have somelevel of risk - it's never possible to diversify away all risk. This is a fact for allinvestments.Each fund has a predetermined investment objective that tailors the fund'sassets, regions of investments and investment strategies. At thefundamental level, there are three varieties of mutual funds:1) Equity funds (stocks)2) Fixed income funds (bonds)3) Money market funds.

All mutual funds are variations of these three asset classes. For example,while equity funds that invest in fast-growing companies are known asgrowth funds, equity funds that invest only in companies of the same sectoror region are known as specialty funds.

Let's go over the many different flavors of funds. We'll start with the safestand then work through to the more risky.

Money Market Funds:The money market consists of short-term debt instruments, mostly Treasurybills. This is a safe place to park your money. You won't get great returns,but you won't have to worry about losing your principal. A typical return istwice the amount you would earn in a regular checking/savings account and

a little less than the average certificate of deposit (CD).

Bond/Income Funds:Income funds are named appropriately: their purpose is to provide currentincome on a steady basis. When referring to mutual funds, the terms "fixed-income," "bond," and "income" are synonymous. These terms denote fundsthat invest primarily in government and corporate debt. While fund holdingsmay appreciate in value, the primary objective of these funds is to provide a

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 34/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 34

steady cash flow to investors. As such, the audience for these funds consistsof conservative investors and retirees.

Bond funds are likely to pay higher returns than certificates of deposit andmoney market investments, but bond funds aren't without risk. Because

there are many different types of bonds, bond funds can vary dramaticallydepending on where they invest. For example, a fund specializing in high-yield junk bonds is much more risky than a fund that invests in governmentsecurities. Furthermore, nearly all bond funds are subject to interest raterisk, which means that if rates go up the value of the fund goes down.

Balanced Funds:

The objective of these funds is to provide a balanced mixture of safety,income and capital appreciation. The strategy of balanced funds is to investin a combination of fixed income and equities. A typical balanced fund mighthave a weighting of 60% equity and 40% fixed income. The weighting mightalso be restricted to a specified maximum or minimum for each asset class.

A similar type of fund is known as an asset allocation fund. Objectives aresimilar to those of a balanced fund, but these kinds of funds typically do nothave to hold a specified percentage of any asset class. The portfoliomanager is therefore given freedom to switch the ratio of asset classes asthe economy moves through the business cycle.

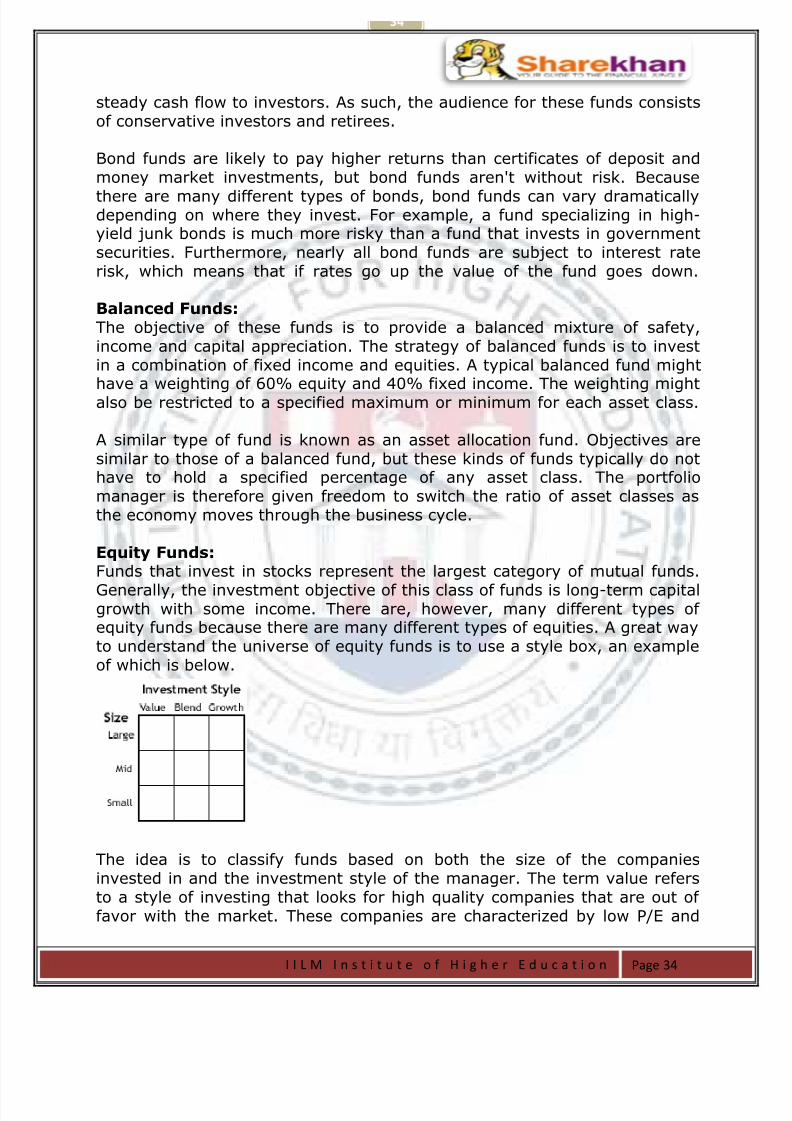

Equity Funds:Funds that invest in stocks represent the largest category of mutual funds.

Generally, the investment objective of this class of funds is long-term capitalgrowth with some income. There are, however, many different types of equity funds because there are many different types of equities. A great wayto understand the universe of equity funds is to use a style box, an exampleof which is below.

The idea is to classify funds based on both the size of the companiesinvested in and the investment style of the manager. The term value refersto a style of investing that looks for high quality companies that are out of favor with the market. These companies are characterized by low P/E and

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 35/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 35

price-to-book ratios and high dividend yields. The opposite of value isgrowth, which refers to companies that have had (and are expected tocontinue to have) strong growth in earnings, sales and cash flow. Acompromise between value and growth is blend, which simply refers tocompanies that are neither value nor growth stocks and are classified as

being somewhere in the middle.

For example, a mutual fund that invests in large-cap companies that are instrong financial shape but have recently seen their share prices fall would beplaced in the upper left quadrant of the style box (large and value). Theopposite of this would be a fund that invests in startup technologycompanies with excellent growth prospects. Such a mutual fund would residein the bottom right quadrant (small and growth).

Global/International Funds: An international fund (or foreign fund) invests only outside your homecountry. Global funds invest anywhere around the world, including yourhome country.

It's tough to classify these funds as either riskier or safer than domesticinvestments. They do tend to be more volatile and have unique countryand/or political risks. But, on the flip side, they can, as part of a well-balanced portfolio, actually reduce risk by increasing diversification.Although the world's economies are becoming more inter-related, it is likelythat another economy somewhere is outperforming the economy of your

home country.

Specialty Funds:

This classification of mutual funds is more of an all-encompassing categorythat consists of funds that have proved to be popular but don't necessarilybelong to the categories we've described so far. This type of mutual fundforgoes broad diversification to concentrate on a certain segment of theeconomy.

Sector funds are targeted at specific sectors of the economy such as

financial, technology, health, etc. Sector funds are extremely volatile. Thereis a greater possibility of big gains, but you have to accept that your sectormay tank.

Regional funds make it easier to focus on a specific area of the world. Thismay mean focusing on a region (say Latin America) or an individual country(for example, only Brazil). An advantage of these funds is that they make iteasier to buy stock in foreign countries, which is otherwise difficult and

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 36/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 36

expensive. Just like for sector funds, you have to accept the high risk of loss,which occurs if the region goes into a bad recession.

Socially-responsible funds (or ethical funds) invest only in companies thatmeet the criteria of certain guidelines or beliefs. Most socially responsible

funds don't invest in industries such as tobacco, alcoholic beverages,weapons or nuclear power. The idea is to get a competitive performancewhile still maintaining a healthy conscience.

Index Funds:

The last but certainly not the least important are index funds. This type of mutual fund replicates the performance of a broad market index such as theS&P 500 or Dow Jones Industrial Average (DJIA). An investor in an indexfund figures that most managers can't beat the market. An index fundmerely replicates the market return and benefits investors in the form of lowfees.

Costs are the biggest problem with mutual funds. These costs eat into yourreturn, and they are the main reason why the majority of funds end up withsub-par performance.

What's even more disturbing is the way the fund industry hides coststhrough a layer of financial complexity and jargon. Some critics of theindustry say that mutual fund companies get away with the fees they chargeonly because the average investor does not understand what he/she ispaying for.

Fees can be broken down into twocategories:1. On-going yearly fees to keep you invested in the fund.2. Transaction fees paid when you buy or sell shares in a fund (loads).

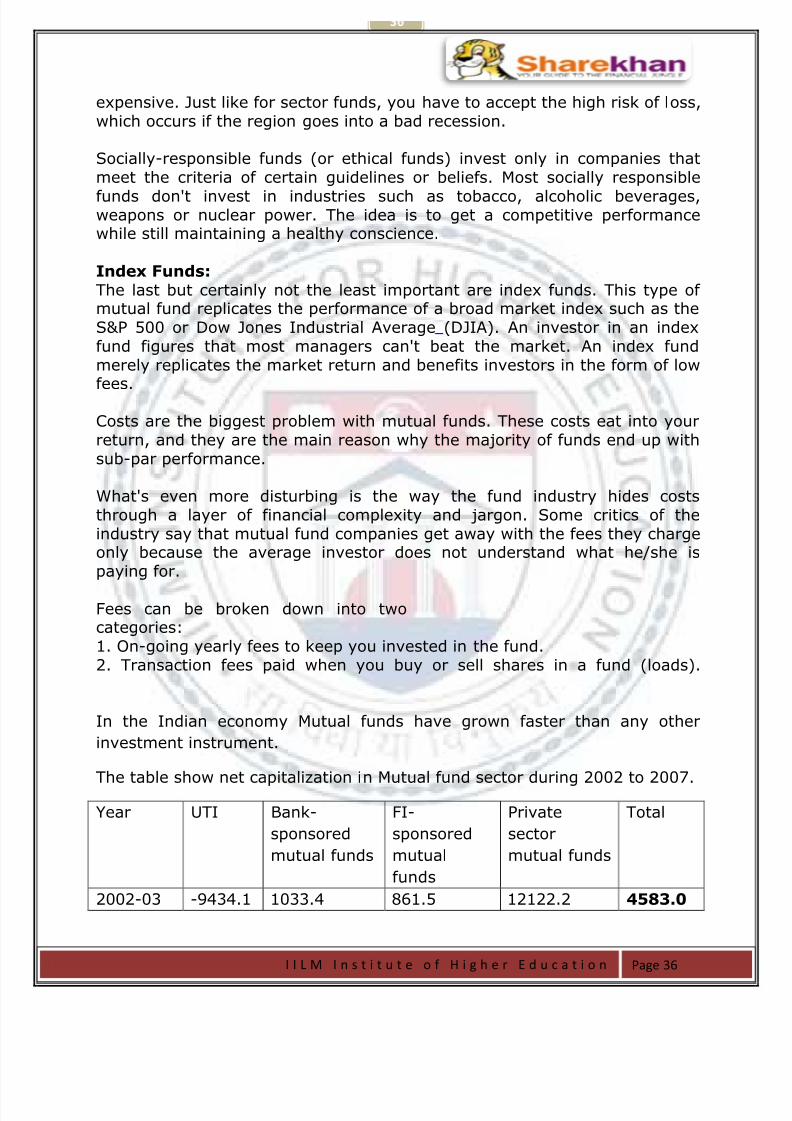

In the Indian economy Mutual funds have grown faster than any other

investment instrument.

The table show net capitalization in Mutual fund sector during 2002 to 2007.

Year UTI Bank-

sponsored

mutual funds

FI-

sponsored

mutual

funds

Private

sector

mutual funds

Total

2002-03 -9434.1 1033.4 861.5 12122.2 4583.0

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 37/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 37

2003-04 1049.9 4526.2 786.8 41509.8 47872.7

2004-05 -2467.2 706.5 -3383.5 7933.1 2788.9

2005-06 3423.8 5364.9 2111.9 41581 52481.6

2006-07 7326.1 3032.0 4226.1 76687 91271.2

NET RESOURCES MOBILISED BY MUTUAL FUNDS 2002 to 2007

FEW TERMS IN MUTUAL FUNDS

NAV: -mutual fund's price per share or exchange-traded fund's (ETF) per-

share value. In both cases, the per-share rupee amount of the fund is

derived by dividing the total value of all the securities in its portfolio, less

any liabilities, by the number of fund shares outstanding.

In terms of corporate valuations, the value of assets less liabilities equals

net asset value (NAV), or "book value".

In the context of mutual funds, NAV per share is computed once a day based

on the closing market prices of the securities in the fund's portfolio. All

mutual fund¶s buy and sell orders are processed at the NAV of the trade

date. However, investors must wait until the following day to get the trade

price.

Mutual funds pay out virtually all of their income and capital gains. As a

result, changes in NAV are not the best gauge of mutual fund performance,

which is best measured by annual total return.

Because ETFs and closed-end funds trade like stocks, their shares trade at

market value, which can be a dollar value above (trading at a premium) or

below (trading at a discount) NAV.

SALE PRICE: - when an investor wants to disinvest from the investment

he/she sell the unit(s) of the stock of the shares of mutual fund. The sell

results the loss or gain of the capital. The tax law provides special rules for

determining how much gain or loss you have, and in what categories, when

you sell mutual fund shares. Tax is one of the main concerns during the sell.

(Total asset value ±liabilities) /no. of units= Net asset value

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 38/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 38

The tax gain or loss from mutual fund sales is calculated by comparing your

tax basis in the shares sold to the sales proceeds net of any transaction

costs. In general, the tax-planning objective is to maximize the basis in the

shares being sold to minimize the gain, or maximize the loss.

TYPES OF MUTUAL FUND SCHEMES

y By Structure

o Open - Ended Schemes

o Close - Ended Schemes

o Interval Schemes

y By Investment Objective

o Growth Schemes

o Income Schemes

o Balanced Schemes

o Money Market Schemes

y Other Schemes

o Tax Saving Schemes

o Special Schemes

Index Schemes

Sector Specific Schemes

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 39/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 39

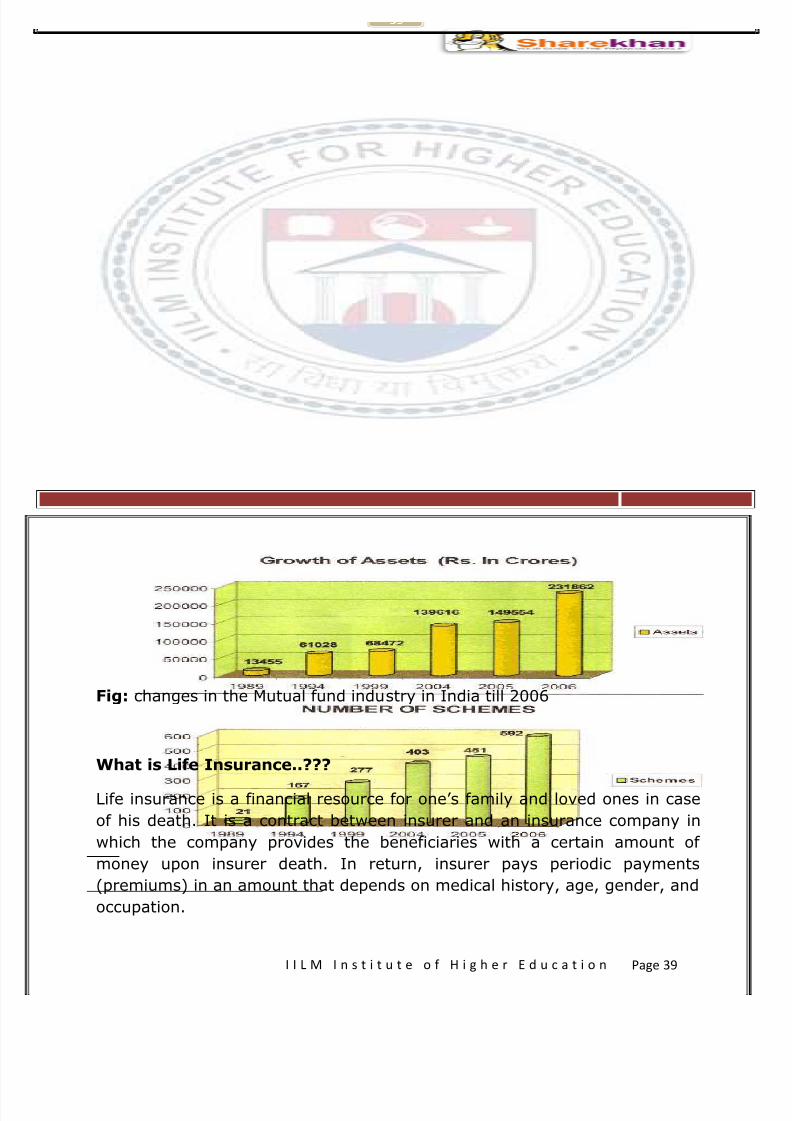

Fig: changes in the Mutual fund industry in India till 2006

What is Life Insurance..???

Life insurance is a financial resource for one¶s family and loved ones in case

of his death. It is a contract between insurer and an insurance company in

which the company provides the beneficiaries with a certain amount of

money upon insurer death. In return, insurer pays periodic payments

(premiums) in an amount that depends on medical history, age, gender, and

occupation.

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 40/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 40

Background1

Though the history of insurance dates back to 1818 with the establishment

of the Oriental Life Insurance company in Calcutta, and then when LIC was

established in the year 1956. For private life insurance sector in particular

things started taking shape after the recommendation of Malhotra committee

which put forward a proposal for the establishment of the regulatory body

and also encouraged to set up unit linked insurance pension plan. It was

after his recommendation that IRDA (Insurance regulatory and development

authority) was established in April 2000. After that in the year 2001 the

sector was finally opened for the private players and foreign private. They

are allowed to have 26% share in Indian company. The real innovation

happened in this time only, when Life insurance companies introduced ULIPs

with greater flexibilities. After making a magnificent entry and becoming the

most popular life insured product.

The other decision taken simultaneously to provide the supporting systems

to the insurance sector and in particular the life insurance companies was

the launch of the IRDA¶s online service for issue and renewal of licenses to

agents.

Due to IRDA the transparency and rules and regulations are still here in the

insurance market.

1 (insurance chronicle, Icfai publications & current scenario by jawahar)

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 41/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 41

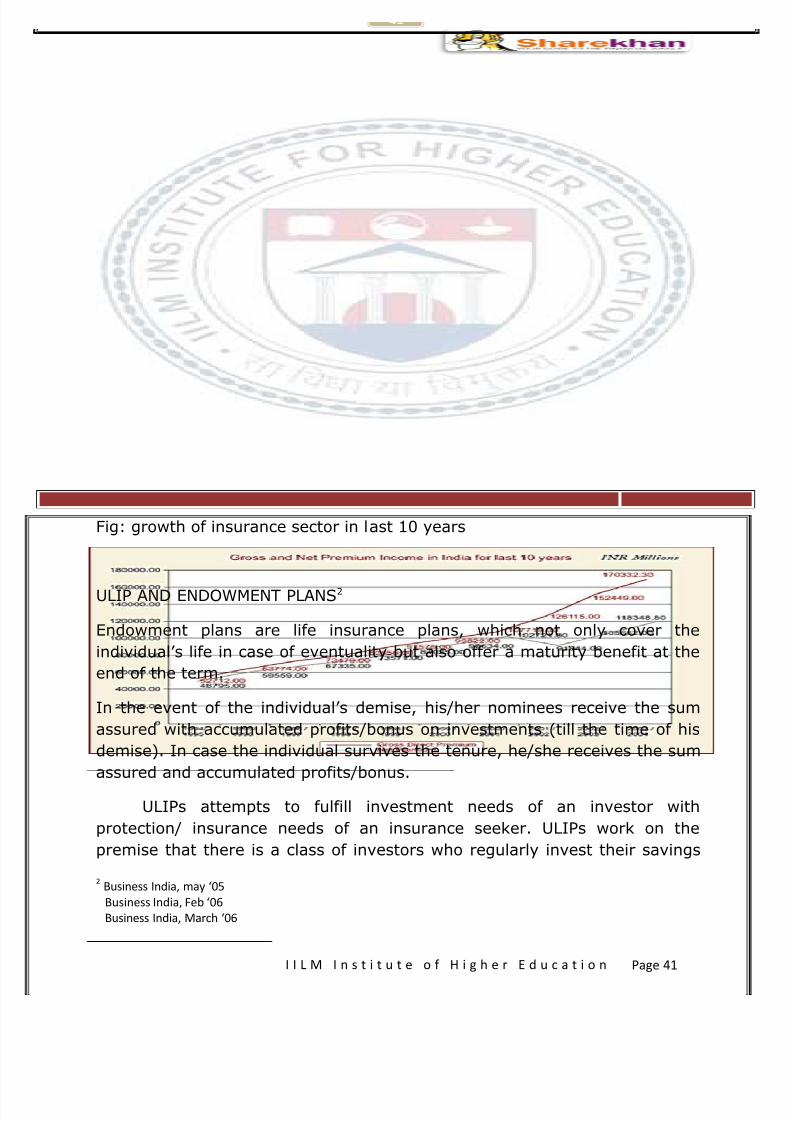

Fig: growth of insurance sector in last 10 years

ULIP AND ENDOWMENT PLANS2

Endowment plans are life insurance plans, which not only cover the

individual¶s life in case of eventuality but also offer a maturity benefit at the

end of the term.

In the event of the individual¶s demise, his/her nominees receive the sum

assured with accumulated profits/bonus on investments (till the time of his

demise). In case the individual survives the tenure, he/she receives the sum

assured and accumulated profits/bonus.

ULIPs attempts to fulfill investment needs of an investor with

protection/ insurance needs of an insurance seeker. ULIPs work on the

premise that there is a class of investors who regularly invest their savings

2Business India, may 05

Business India, Feb 06

Business India, March 06

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 42/85

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 43/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 43

3. The maturity benefit is not typically a fixed amount and the maturity

period can be advanced or extended.

4. Investments can be made in gilt funds, balanced funds, money market

funds, growth funds or bonds.

5. The policyholder can switch between schemes, for instance, balanced to

debt or gilt to equity, etc.

6. The maturity benefit is the net asset value of the units.

7. The costs in ULIP are higher because there is a life insurance component

in it as well, in addition to the investment component.

8. Insurance companies have the discretion to decide on their investment

portfolios.

9. They are simple, clear, and easy to understand.

10. Being transparent the policyholder gets the entire episode on the

performance of his fund.

11. Lead to an efficient utilization of capital.

12. ULIP products are exempted from tax and they provide life insurance.

13. Provides capital appreciation.

14. Investor gets an option to choose among debt, balanced and equity

funds.

ULIPs vs. Mutual Funds

Unit Linked Insurance Policies (ULIPs) as an investment avenue are closest

to mutual funds in terms of their structure and functioning. As is the case

with mutual funds, investors in ULIPs is allotted units by the insurance

company and a net asset value (NAV) is declared for the same on a daily

basis.

Similarly ULIP investors have the option of investing across various schemes

similar to the ones found in the mutual funds domain, i.e. diversified equity

funds, balanced funds and debt funds to name a few.

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 44/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 44

Mutual fund investors have the option of either making lump sum

investments or investing using the systematic investment plan (SIP) route

which entails commitments over longer time horizons. The minimum

investment amounts are laid out by the fund house.

ULIP investors also have the choice of investing in a lump sum (single

premium) or using the conventional route, i.e. making premium payments

on an annual, half-yearly, quarterly or monthly basis. In ULIPs, determining

the premium paid is often the starting point for the investment activity.

ULIPs Mutual Funds

Investment

amounts

Determined by the

investor and can be

modified as well

Minimum investment

amounts are determined

by the fund house

Expenses

No upper limits,

expenses

determined by the

insurance company

Upper limits for

expenses chargeable to

investors have been set

by the regulator

Portfolio

disclosure Not mandatory*

Quarterly disclosures are

mandatory

Modifying

asset

allocation

Generally permitted

for free or at a

nominal cost

Entry/exit loads have to

be borne by the investor

Tax benefits

Section 80C

benefits are

available on allULIP investments

Section 80C benefits are

available only on

investments in tax-saving funds

MAJOR DIFFERENCES IN ULIPs AND MUTUAL FUNDs

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 45/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 45

If a mutual fund investor in a diversified equity fund wishes to shift his

corpus into a debt from the same fund house, he could have to bear an exit

load and/or entry load.

On the other hand most insurance companies permit their ULIP inventors to

shift investments across various plans/asset classes either at a nominal or

no cost (usually, a couple of switches are allowed free of charge every year

and a cost has to be borne for additional switches).

With these comparable there are certain factors where in these two differ.

Mutual funds are essentially short to medium term products. The liquidity

that these products offer is valuable for investors. ULIPs, in contrast, are

positioned as long-term products and going ahead, there will be separate

playing fields for ULIPS and MFs, with the product differentiation between

them becoming more pronounced. ULIPs do not seek to replace mutualfunds, they offer protection against the risk of dying too early, and also help

people save for retirement. Insurance has to be an integral part of one's

wealth management portfolio. Further, exposure of Indian households to

capital markets is limited.

ULIPs and mutual funds are, therefore, not likely to cannibalize each other in

the long run. The primary objective of an insurance product is protection.

The whole reason why it has evolved as a savings plan in the minds of

certain people is because there is a significant savings component attached

to it; however, it is still not the primary purpose of the plan. Second, there

are various kinds of insurance products; the element of protection in each

varies. In certain plans the level of protection is low and the savings

component high, but that is a choice to the customer.

While ULIPs as an investment avenue is closest to mutual funds in terms of

their functioning and structure, the first and foremost purpose of insurance

is and will always be 'protection'. The value that it provides cannot be

downplayed or underestimated. As an instrument of protection, insurance

provides benefits that no investment can offer. It is important for an investorto understand his financial goals and horizon of investment in order to make

an informed investment decision. The decision to invest in either a mutual

fund or a ULIP should depend on the time period of investment, individual

financial goals as well as risk taking appetite, and it¶s about time the

industry and customer realise it.

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 46/85

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 47/85

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 48/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 48

Bills - Debts securities maturing in less than one year.

Notes - Debt securities maturing in one to ten years.

Bonds - Debt securities maturing in more than ten years.

Marketable securities from the Indian government± known collectively as

Treasuries and are as Treasury bonds, Treasury notes and Treasury bills.

Municipal Bonds ± Municipal bonds, known as ³munis´, are the next

progression in term of risk. The major advantage in munis is that the returns

are free from State/central tax. Local government some time makes their

debt non-taxable for residents, thus making some municipal bonds

completely tax free. Because of the tax-savings yield in munis is lower than

the taxable bonds.

Corporate bonds ± A company can issue bonds just as it can issue stock.

Generally, a short term corporate bond is less than five years; intermediate

is five to twelve years, and long term is over 12 years.

Corporate bonds are characterized by higher yields because there is a higher

risk of a company defaulting than a government. The company¶s credit

quality is most important: the higher the credit quality, lower the interest

rate the investor receives.

Bondholders are not owners of the corporation. But if the company gets infinancial trouble and needs to dissolve, bondholders must be paid off in full

before stockholders get anything.

Zero coupon Bonds: - This is a type of bond that make no coupon

payments but instead is issued at a considerable discount to par value. For

example, let us say, a zero coupon bond with a Rs. 1,000 par value and 10

years to maturity is trading at Rs. 600; then investor would be paying

Rs.600 today that will worth Rs. 1,000 after 10 years.

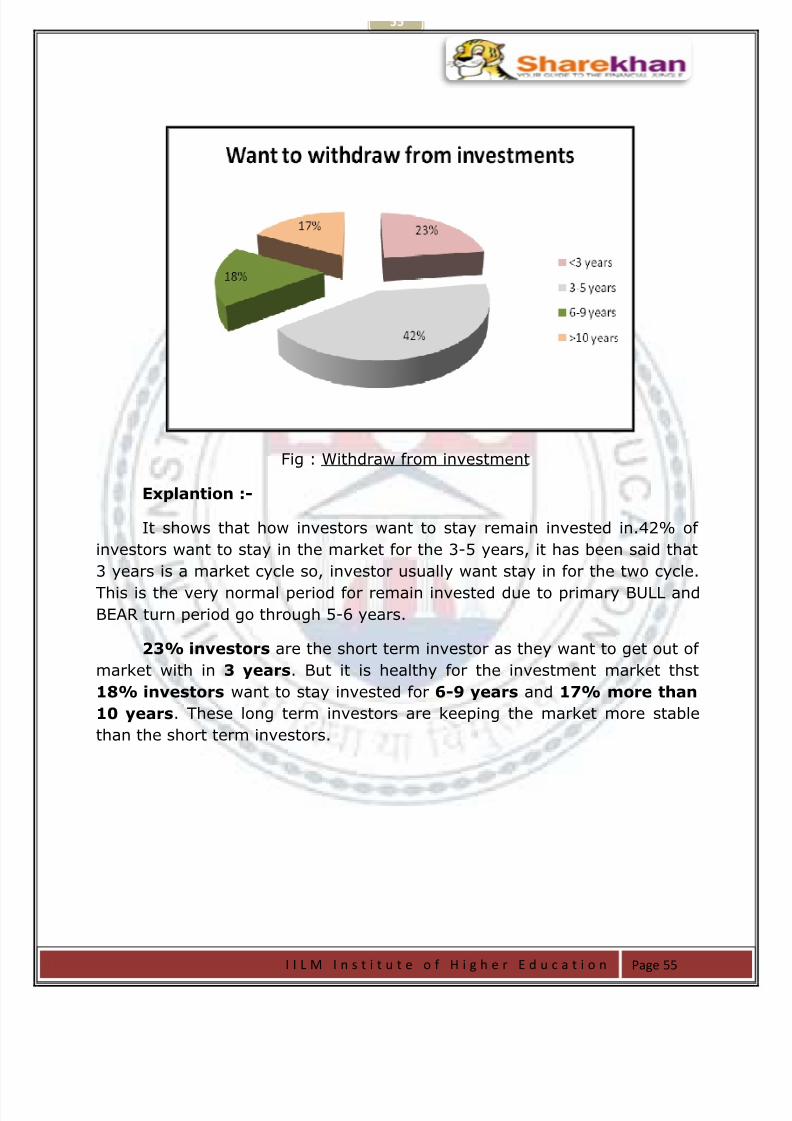

FIELD SURVEY

The field survey was based on the investment strategies taken by the small

investors and the instrument they prefer to invest. To fulfill the particular I

8/8/2019 SHEKHAR-Portfolio Management and Investment Trends

http://slidepdf.com/reader/full/shekhar-portfolio-management-and-investment-trends 49/85

I I L M I n s t i t u t e o f H i g h e r E d u c a t i o n Page 49

have done field survey in about 160 people in the NCR. The entire summer

internship is surrounded by this investment strategy and making portfolio.

The entire project is designed like this: -

Formation of questionnaire depending upon the investor mindset and the need.

I put strong emphasis on the questionnaire that respondent

must fill the questionnaire. For that I restrict my questions to

six. Thus it becomes short and time saving.

After gathering the entire data I analyzed it using MS Excel.

Objective of the Project: