Embed Size (px)

Citation preview

September 2010

“UNUSUALLY UNCERTAIN”

Patrick O’Toole, CGA, CFAVice-President, CIBC Global Asset Management

2 2

CIBC Global Asset Management

History: Our firm has focused on the active management of assets since 1972. We are committed to our clients, which helps explain why many have been with us for more than 30 years.

Depth: Clients with more than 250 mandates have chosen CIBC Global Asset Management Inc. as their investment partner, with $58 billion in assets managed on their behalf.

Strength: CIBC Global Asset Management has the dedication of 136 employees, including 54 investment professionals. We also benefit from the resources, reliability, and stability of CIBC.

Assets Under Management ($BN) at Dec. 31, 2009

Bonds$28

Money Market$12

Stocks$18

3 3

MESSAGE

CREDIT CRISIS FALLOUT WILL LAST 5+ YEARS– YEAR 2 HAS PASSED

ECONOMIES STILL NEED LIFE SUPPORT– SECULAR HEADWINDS ARE FORMIDABLE

CENTRAL BANKS WILL MOVE SLOWLY TO RAISE RATES– THIS IS NOT A TYPICAL POSTWAR RECESSION/RECOVERY

4 4

Economy – National Bureau of Economic Research Indicators

Source: Datastream and CIBC Global Asset Management Inc.

Both industrial production and manufacturing suffered a record fall during this recession.

At this pace, they’ll take several more years to achieve prior heights.

Unfortunately, recent indicators point to them topping out.

U.S. Manufacturing & Trade Sales

Current vs. Average Expansions

The Good

100

102

104

106

108

110

112

114

JUN 07 DEC 07 JUN 08 DEC 08 JUN 09 DEC 09 JUN 10 DEC 10

Current Expansion of Manufacturing & Trade SalesAverage Expansions

U.S. Manufacturing & Trade Sales Expansion vs. Average Expansions

Source: Datastream & CIBC Global Asset Management Inc. Calculations

Assuming recession ended in June 2009 (=100)

U.S. Industrial Production

Current vs. Average Expansions

100

104

108

112

116

JUN 07 DEC 07 JUN 08 DEC 08 JUN 09 DEC 09 JUN 10 DEC 10

Current Expansion of Industrial ProductionAverage Expansions

U.S. Industrial Production Expansion vs. Average Expansions

Source: Datastream & CIBC Global Asset Management Inc. Calculations

Assuming recession ended in June 2009 (=100)

5 5

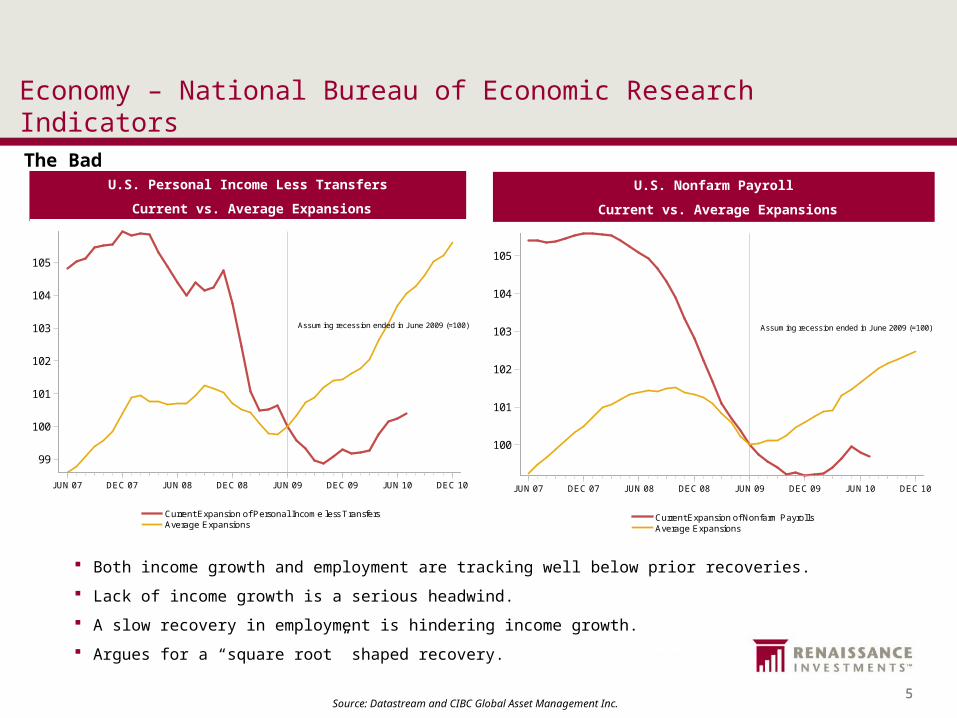

The Bad

Source: Datastream and CIBC Global Asset Management Inc.

Both income growth and employment are tracking well below prior recoveries.

Lack of income growth is a serious headwind.

A slow recovery in employment is hindering income growth.

Argues for a “square root” shaped recovery.

U.S. Personal Income Less Transfers

Current vs. Average Expansions

99

100

101

102

103

104

105

JUN 07 DEC 07 JUN 08 DEC 08 JUN 09 DEC 09 JUN 10 DEC 10

Current Expansion of Personal Income less TransfersAverage Expansions

U.S. Personal Income less Transfers Expansion vs. Average Expansions

Source: Datastream & CIBC Global Asset Management Inc. Calculations

Assuming recession ended in June 2009 (=100)

U.S. Nonfarm Payroll

Current vs. Average Expansions

100

101

102

103

104

105

JUN 07 DEC 07 JUN 08 DEC 08 JUN 09 DEC 09 JUN 10 DEC 10

Current Expansion of Nonfarm PayrollsAverage Expansions

U.S. Nonfarm Payroll Expansion vs. Average Expansions

Source: Datastream & CIBC Global Asset Management Inc. Calculations

Assuming recession ended in June 2009 (=100)

Economy – National Bureau of Economic Research Indicators

6 6

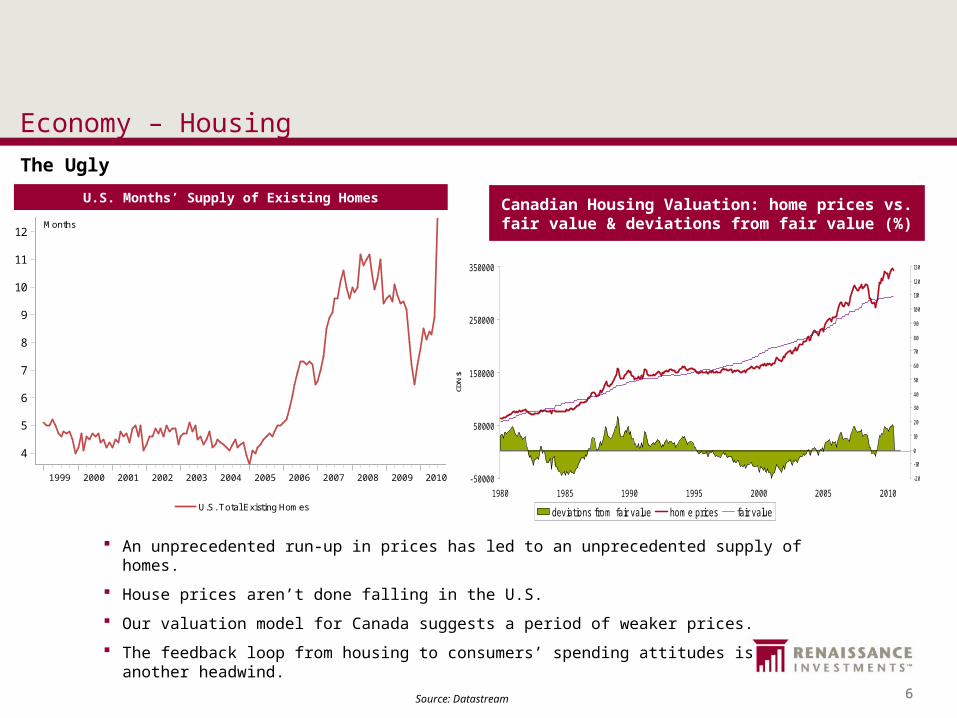

Economy – Housing

Source: Datastream

An unprecedented run-up in prices has led to an unprecedented supply of homes.

House prices aren’t done falling in the U.S.

Our valuation model for Canada suggests a period of weaker prices.

The feedback loop from housing to consumers’ spending attitudes is another headwind.

U.S. Months’ Supply of Existing Homes

The Ugly

4

5

6

7

8

9

10

11

12

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

U.S. Total Existing Homes

U.S. Months' Supply of Existing Homes

Source: Datastream

Months

- 50000

50000

150000

250000

350000

1980 1985 1990 1995 2000 2005 2010

CDN

$

-20

-10

0

10

20

30

40

50

60

70

80

90

100

110

120

130

deviations from fair value home prices fair value

Canadian Housing Valuation: home prices vs. fair value & deviations from fair value (%)

7 7

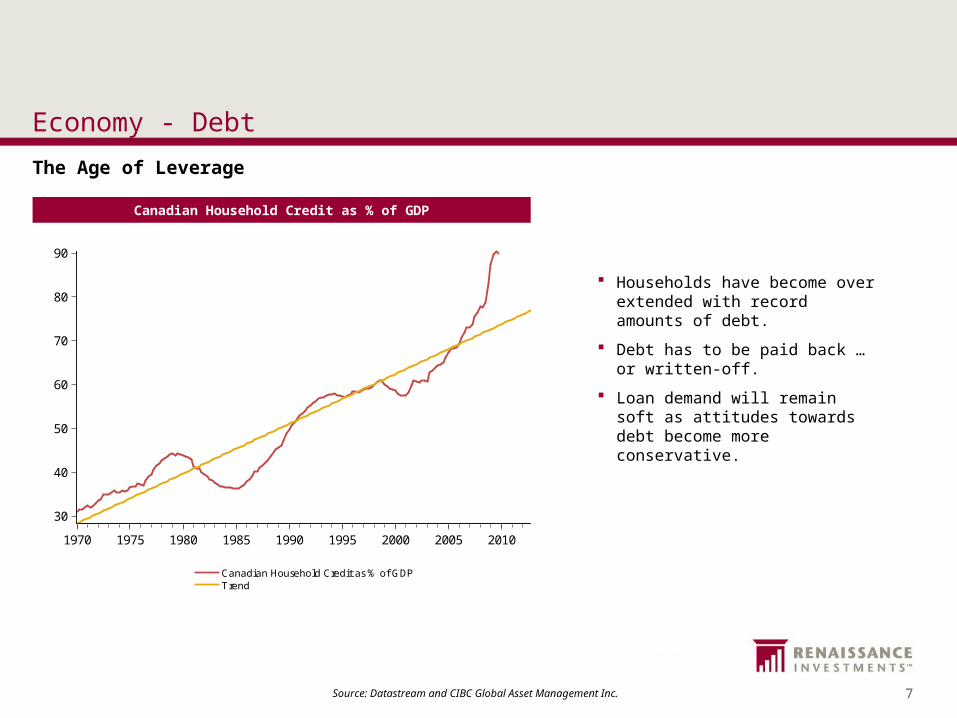

Economy - Debt

Source: Datastream and CIBC Global Asset Management Inc.

Households have become over extended with record amounts of debt.

Debt has to be paid back … or written-off.

Loan demand will remain soft as attitudes towards debt become more conservative.

The Age of Leverage

30

40

50

60

70

80

90

1970 1975 1980 1985 1990 1995 2000 2005 2010

Canadian Household Credit as % of GDPTrend

Canadian Household Credit as % of GDP

Source: Datastream & CIBC Global Asset Management Inc. Calculations

Canadian Household Credit as % of GDP

8 8

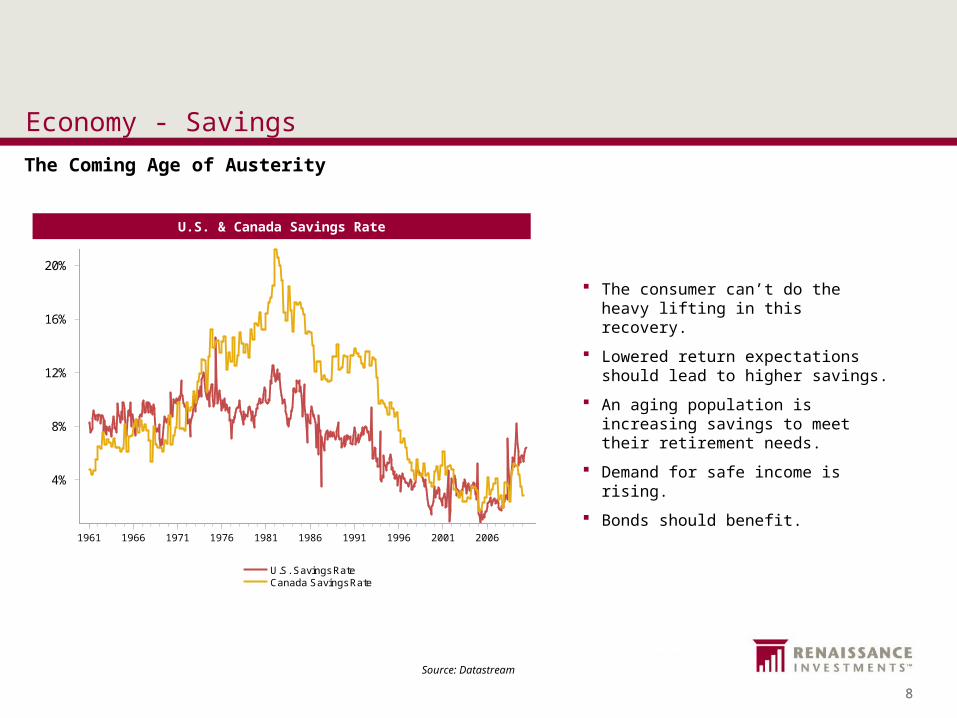

Economy - Savings

Source: Datastream

The consumer can’t do the heavy lifting in this recovery.

Lowered return expectations should lead to higher savings.

An aging population is increasing savings to meet their retirement needs.

Demand for safe income is rising.

Bonds should benefit.

U.S. & Canada Savings Rate

The Coming Age of Austerity

4%

8%

12%

16%

20%

1961 1966 1971 1976 1981 1986 1991 1996 2001 2006

U.S. Savings RateCanada Savings Rate

U.S. & Canada Savings Rate

Source: Datastream

9 9

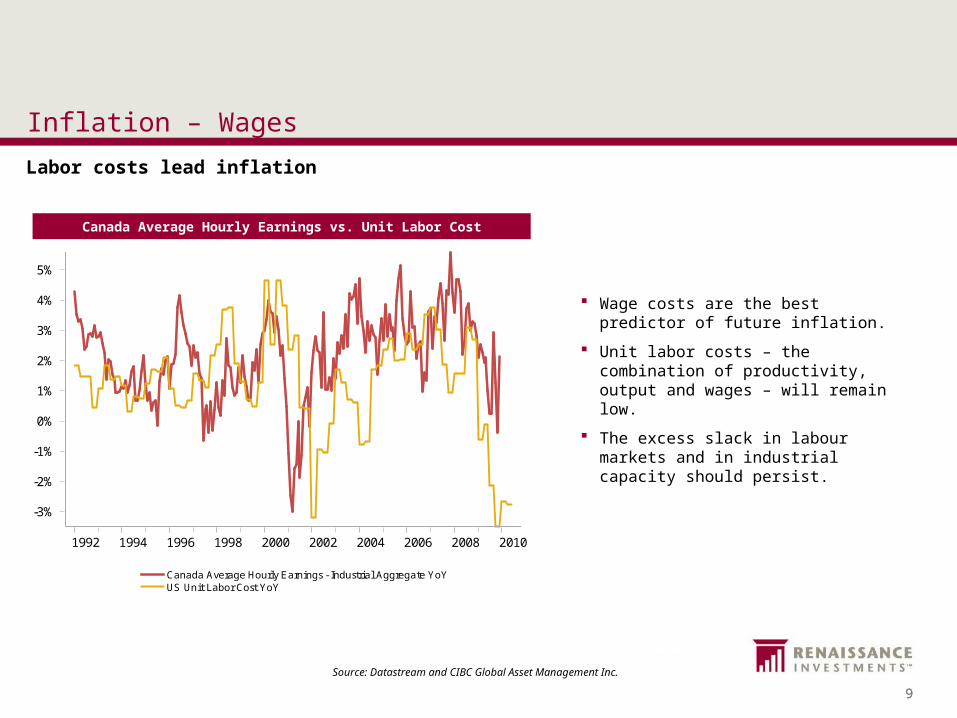

Inflation – Wages

Source: Datastream and CIBC Global Asset Management Inc.

Wage costs are the best predictor of future inflation.

Unit labor costs – the combination of productivity, output and wages – will remain low.

The excess slack in labour markets and in industrial capacity should persist.

Canada Average Hourly Earnings vs. Unit Labor Cost

Labor costs lead inflation

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Canada Average Hourly Earnings - Industrial Aggregate YoYUS Unit Labor Cost YoY

Canada Average Hourly Earnings vs U.S. Unit Labor Cost

Source: Datastream & CIBC Global Asset Management Inc. Calculations

10 10

Inflation - CPI

Source: Datastream and CIBC Global Asset Management Inc.

Inflation remains low in deleveraging periods.

Commodity prices are a small component of inflation.

A strong Canadian dollar is a restraining force on prices.

Low and stable inflation is expected.

CPI – Total (Year-To-Year Changes)

Inflation has remained stable for years

0%

2%

4%

6%

8%

10%

12%

14%

60 65 70 75 80 85 90 95 00 05 10

U.S. CPI Total YoYCanadian CPI Total YoY

CPI - Total (Year-to-Year Changes)

Source: Datastream & CIBC Global Asset M anag ement Inc. Calculations

11 11

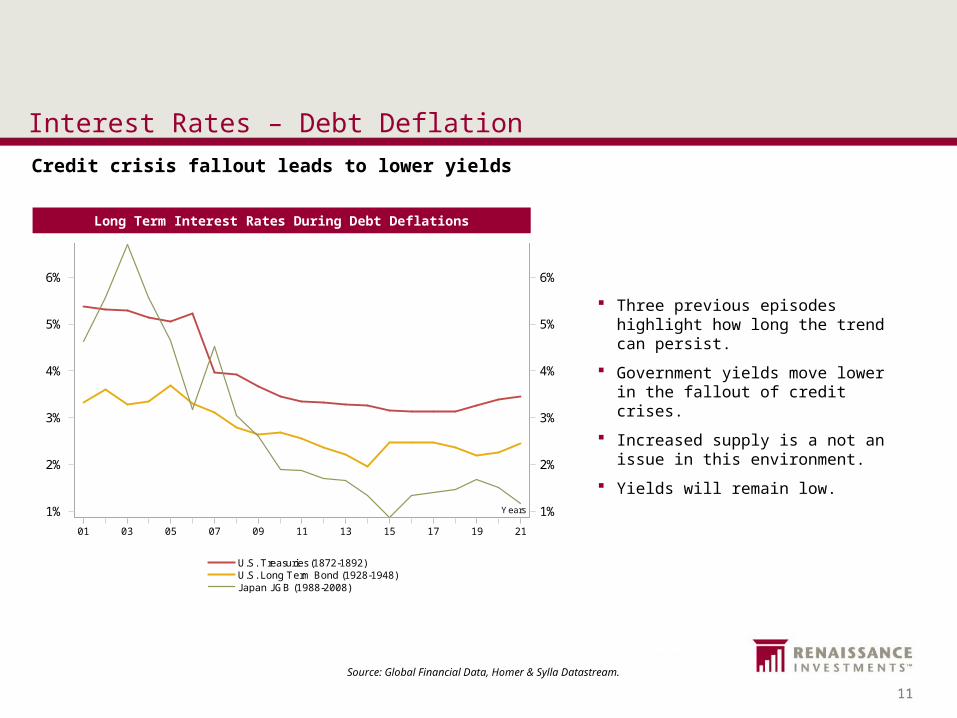

Interest Rates – Debt Deflation

Source: Global Financial Data, Homer & Sylla Datastream.

Three previous episodes highlight how long the trend can persist.

Government yields move lower in the fallout of credit crises.

Increased supply is a not an issue in this environment.

Yields will remain low.

Long Term Interest Rates During Debt Deflations

1%

2%

3%

4%

5%

6%

1%

2%

3%

4%

5%

6%

01 03 05 07 09 11 13 15 17 19 21

U.S. Treasuries (1872-1892)U.S. Long Term Bond (1928-1948)Japan JGB (1988-2008)

Long Term Interest Rates during Debt Deflations

Source: Global Financial Data, Homer & Sylla, Datastream

Y ears

Credit crisis fallout leads to lower yields

12 12

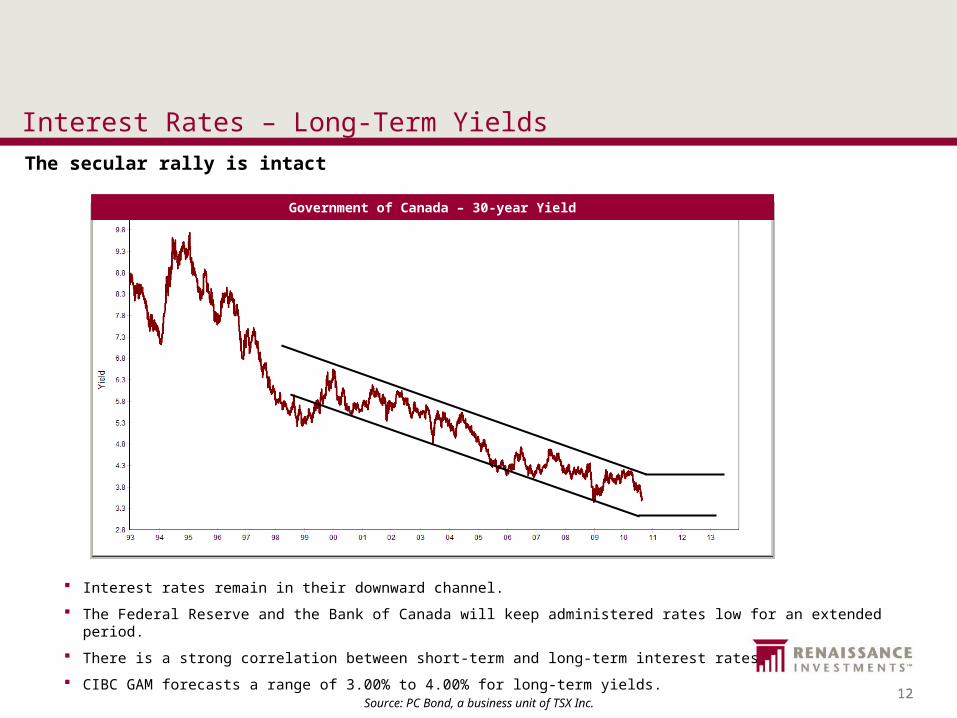

Interest Rates – Long-Term YieldsThe secular rally is intact

Government of Canada – 30-year Yield

Interest rates remain in their downward channel.

The Federal Reserve and the Bank of Canada will keep administered rates low for an extended period.

There is a strong correlation between short-term and long-term interest rates.

CIBC GAM forecasts a range of 3.00% to 4.00% for long-term yields.

Source: PC Bond, a business unit of TSX Inc.

13 13

Yield Curve - 30yr less 2yr

Interest Rates – Yield CurveA steep curve cures bankers’ ills

An extended period of low short-term rates relieves pressure on rising bond yields.

Current “steepness” is needed as financial institutions repair their balance sheets.

Source: PC Bond, a business unit of TSX Inc.

14 14

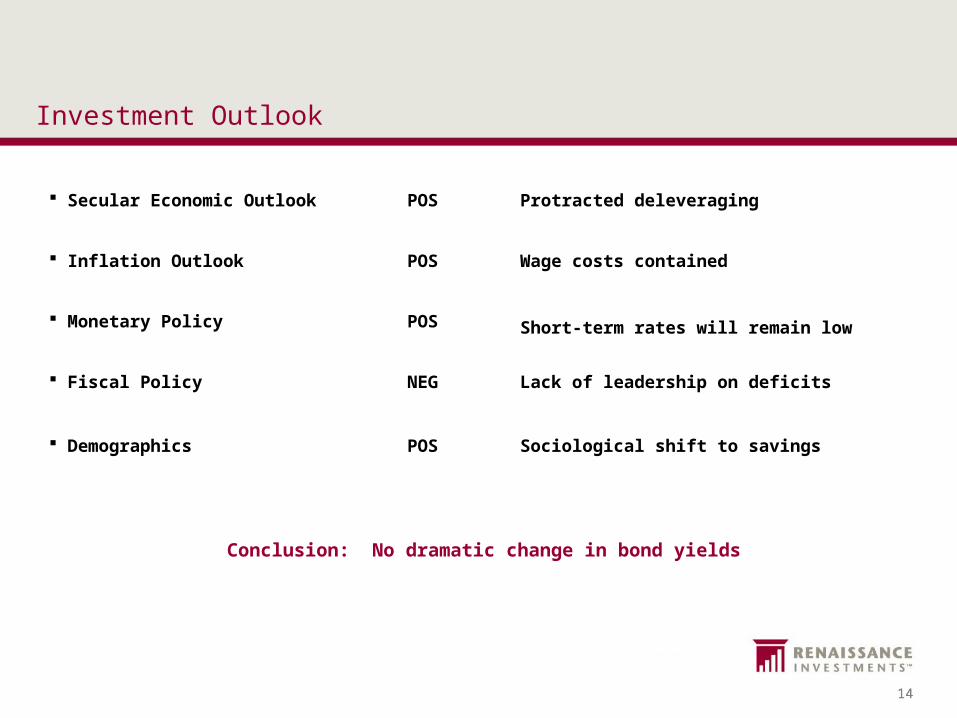

Investment Outlook

Conclusion: No dramatic change in bond yields

Secular Economic Outlook POS Protracted deleveraging

Inflation Outlook POS Wage costs contained

Monetary Policy POS Short-term rates will remain low

Fiscal Policy NEG Lack of leadership on deficits

Demographics POS Sociological shift to savings

15 15

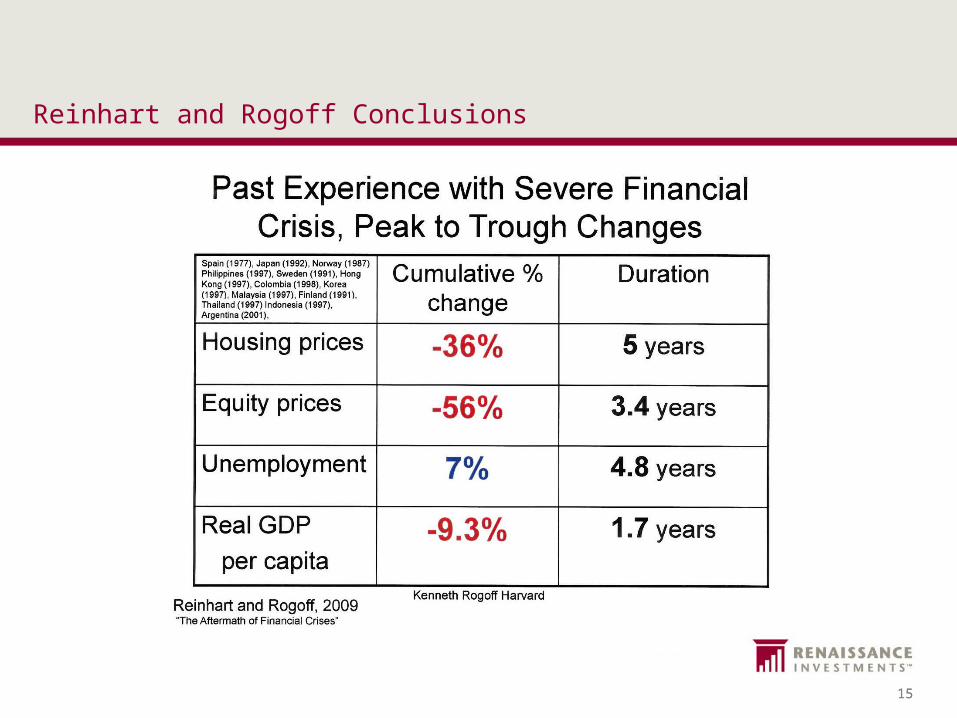

Reinhart and Rogoff Conclusions

16 16

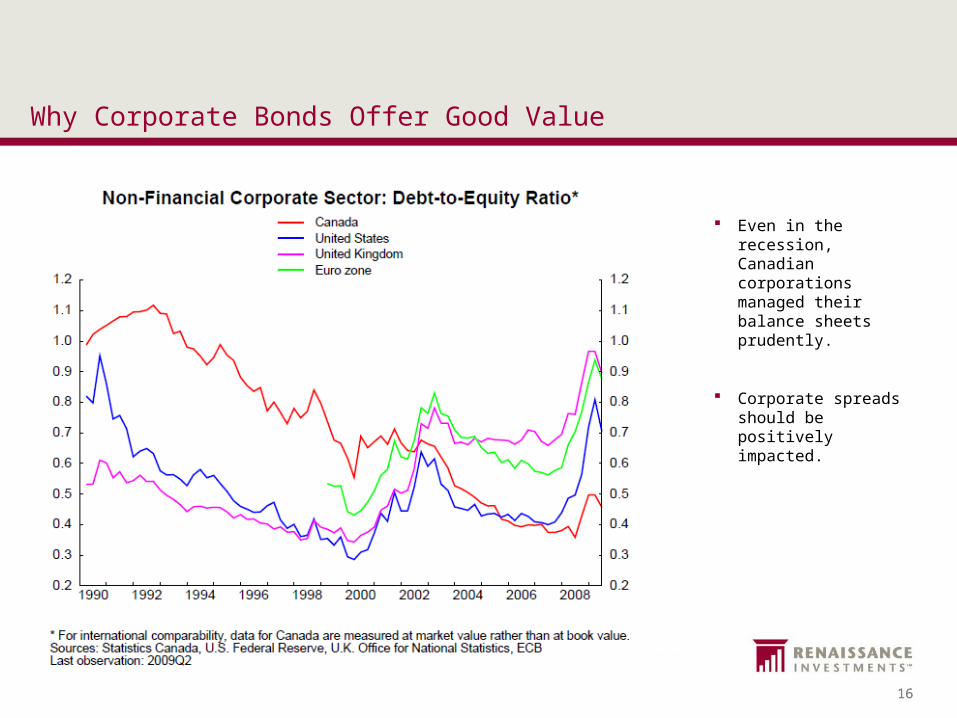

Even in the recession, Canadian corporations managed their balance sheets prudently.

Corporate spreads should be positively impacted.

Why Corporate Bonds Offer Good Value

17 17

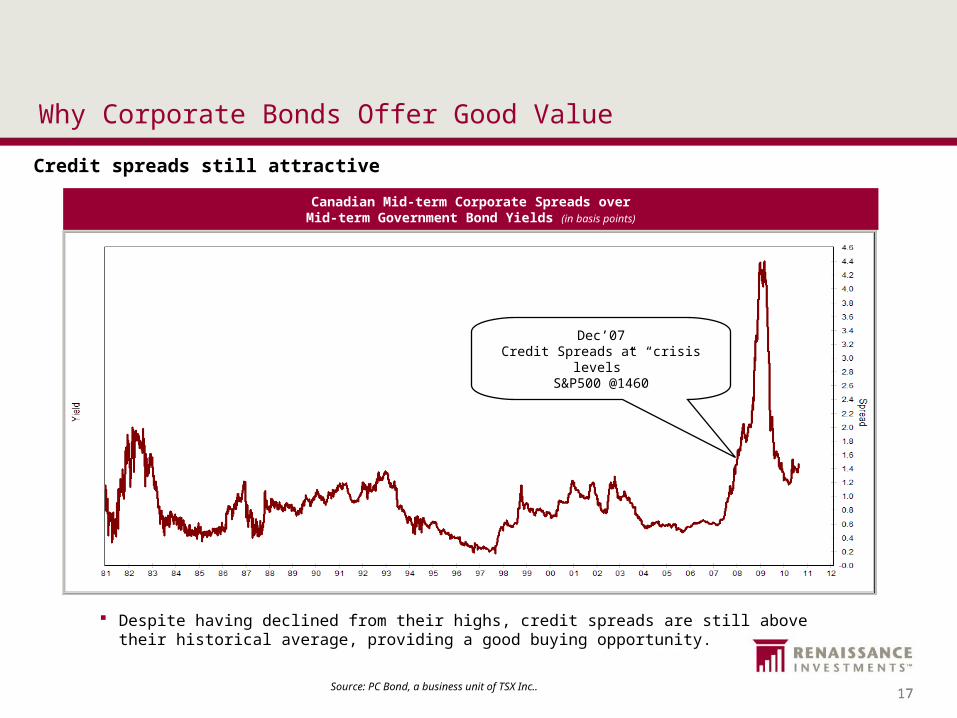

Why Corporate Bonds Offer Good Value

Dec’07Credit Spreads at “crisis levels”

S&P500 @1460

Canadian Mid-term Corporate Spreads overMid-term Government Bond Yields (in basis points)

Source: PC Bond, a business unit of TSX Inc..

Despite having declined from their highs, credit spreads are still above their historical average, providing a good buying opportunity.

Credit spreads still attractive

18 18

0

300

600

900

1,200

1,500

1,800

2,100

J ul-95 J ul-96 J ul-97 J ul-98 J ul-99 J ul-00 J ul-01 J ul-02 J ul-03 J ul-04 J ul-05 J ul-06 J ul-07 J ul-08 J ul-09 J ul-10

Year

Sp

read

+648

+906

Dot-Com

+958

9/11 & Enron

+995

Wcom/Tyco/Actg/Mgmt

+312

Beginning of Sub-Prime Mortgage Crisis

+1094

US Bank Bailout

Plan

+817

RussianCrisis

Bear Stearns Bailout

US Auto Bailout Plan

+1985

+780

Gov’t Liquidity HY Inflows

Why Corporate Bonds Offer Good Value

US High Yield Spread

Source: BAC-Merrill Lynch

High yield spreads also attractive

Spreads have spiked to new highs at each major crisis, but have consistently returned to historical averages afterwards.

High-yield bonds remain attractive, and we have added new issues.

Selection is key. We do rigorous credit research on each issuer.

19 19

Why Corporate Bonds Offer Good Value

0%

4%

8%

12%

16%

20%

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10

Cumulative Excess Returns

Cumulative Excess Returns of DEX Corporates vs DEX Canada Universe

Source: Datastream & CIBC Global Asset Management Inc. Calculations

Cumulative Excess Returns of DEX Corporatesvs. DEX Canada Universe

Over the long-run, corporate bonds have beat the DEX Canada Universe

Source: PC Bond, a business unit of TSX Inc..

20 20

Renaissance Corporate Bond Capital Yield Fund

A tax efficient way to gain exposure to corporate bonds

Who should invest?– Clients seeking tax efficient monthly distributions– Clients looking for Corporate Bond exposure– Clients looking to diversify their fixed income holdings

Product specifications– Manager: CGAM (Patrick O’Toole – Jeff Waldman)– Target 3% distribution

Benchmark Range

DEX Corporate Bond Universe Index (Investment Grade) 80%

BAC-ML US High Yield Cash Pay Index (100% hedged) 14%

10%-30%

BAC-ML Canadian High Yield index (100% hedged) 6%

21 21

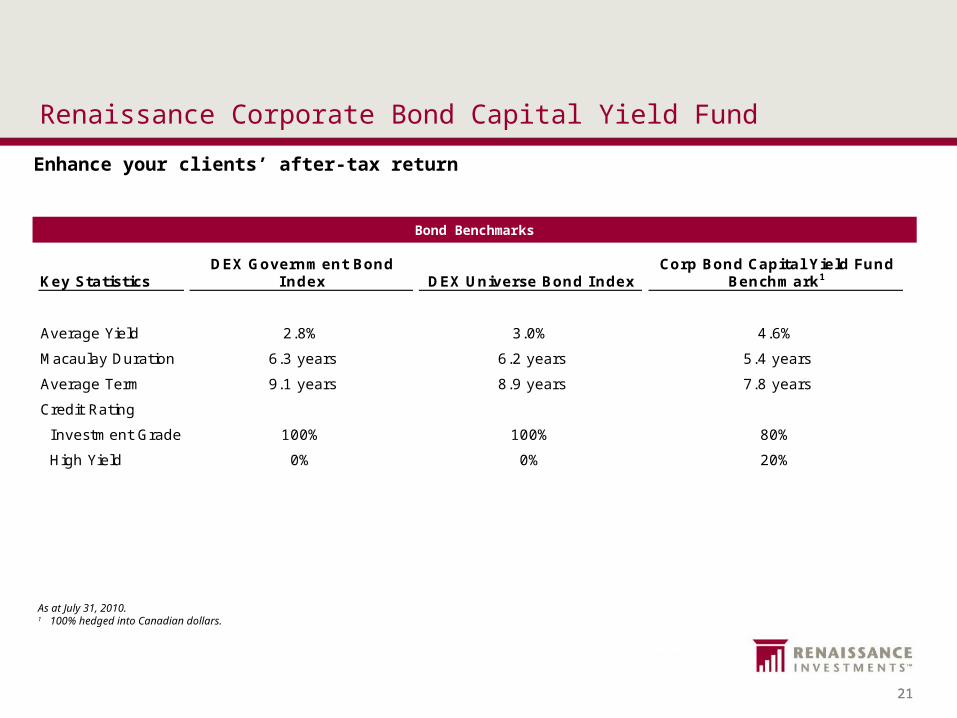

Renaissance Corporate Bond Capital Yield Fund

Bond Benchmarks

As at July 31, 2010.1 100% hedged into Canadian dollars.

Key Statistics DEX Government Bond

Index DEX Universe Bond Index Corp Bond Capital Yield Fund

Benchmark1

Average Yield 2.8% 3.0% 4.6%

Macaulay Duration 6.3 years 6.2 years 5.4 years

Average Term 9.1 years 8.9 years 7.8 years

Credit Rating

Investment Grade 100% 100% 80%

High Yield 0% 0% 20%

Enhance your clients’ after-tax return

22 22

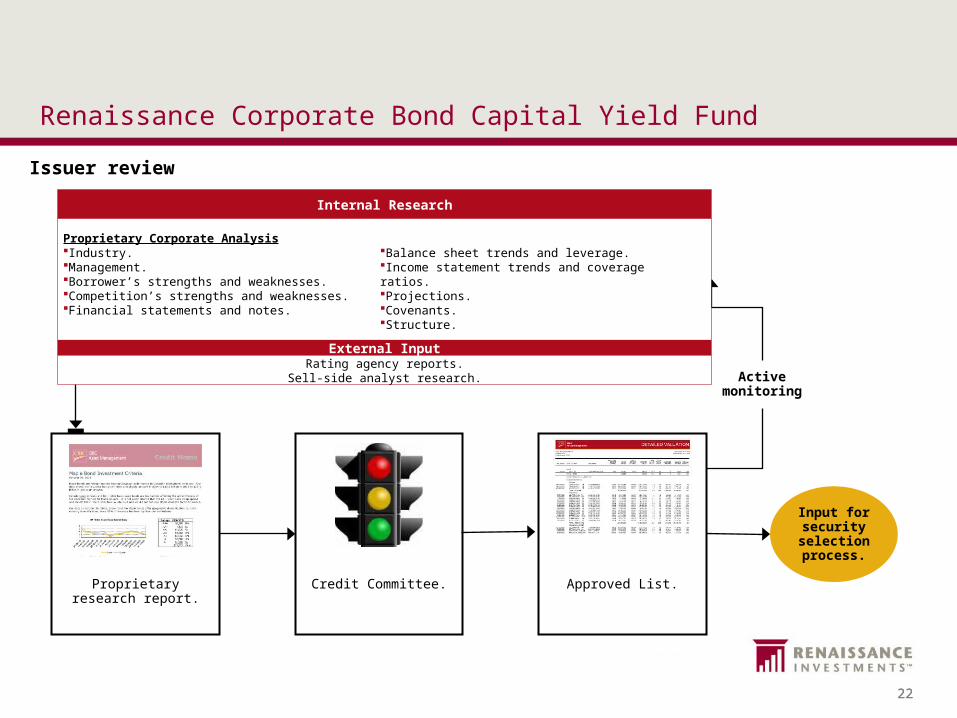

Active monitoring

Proprietary research report.

Input for security selection process.

Credit Committee. Approved List.

Renaissance Corporate Bond Capital Yield Fund

Issuer review

Internal Research

External InputRating agency reports.

Sell-side analyst research.

Proprietary Corporate AnalysisIndustry.Management.Borrower’s strengths and weaknesses.Competition’s strengths and weaknesses.Financial statements and notes.

Balance sheet trends and leverage.Income statement trends and coverage ratios.Projections.Covenants.Structure.

23 23

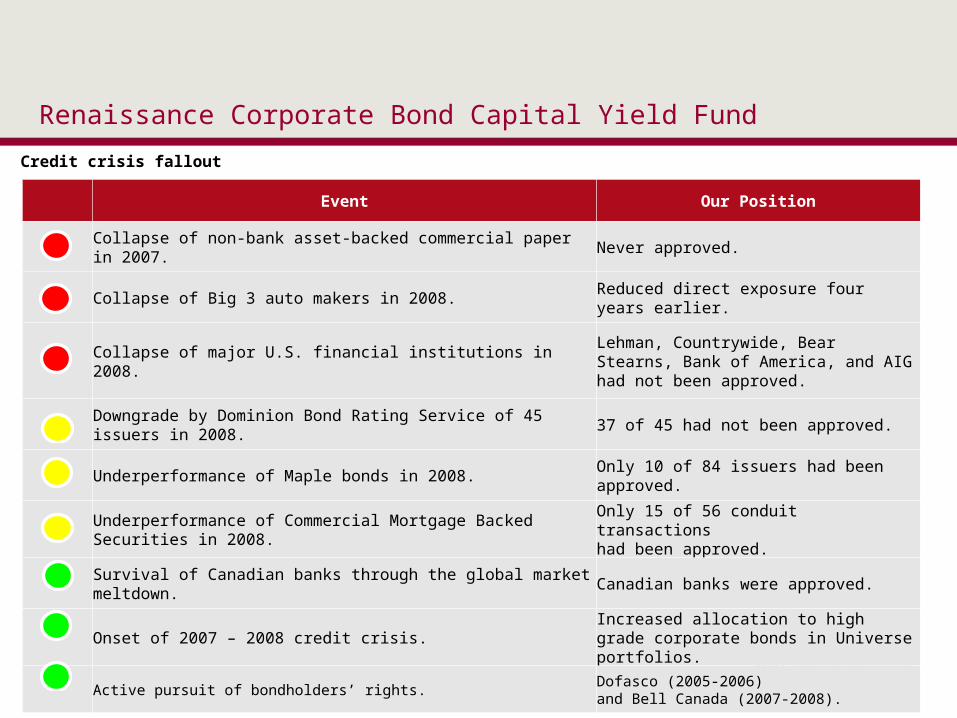

Renaissance Corporate Bond Capital Yield Fund

Credit crisis fallout

Event Our Position

Collapse of non-bank asset-backed commercial paper in 2007. Never approved.

Collapse of Big 3 auto makers in 2008.Reduced direct exposure four years earlier.

Collapse of major U.S. financial institutions in 2008.Lehman, Countrywide, Bear Stearns, Bank of America, and AIG had not been approved.

Downgrade by Dominion Bond Rating Service of 45 issuers in 2008.

37 of 45 had not been approved.

Underperformance of Maple bonds in 2008.Only 10 of 84 issuers had been approved.

Underperformance of Commercial Mortgage Backed Securities in 2008.

Only 15 of 56 conduit transactionshad been approved.

Survival of Canadian banks through the global market meltdown.

Canadian banks were approved.

Onset of 2007 – 2008 credit crisis.Increased allocation to high grade corporate bonds in Universe portfolios.

Active pursuit of bondholders’ rights.Dofasco (2005-2006)and Bell Canada (2007-2008).

24 24

Renaissance Corporate Bond Capital Yield Fund

Renaissance Corporate Bond Capital Yield Fund 4.3%

Benchmark 4.6%

Credit Mix - % Weight vs. Benchmark

-4

3

-1

7

-1

-14

10

-20 -15 -10 -5 0 5 10 15

CCC

B

BB

BBB

A

AA

AAA

Industry Mix - % Weight vs. Benchmark

5

1

-10

8

-2

-3

-3

4

-15 -10 -5 0 5 10

Sec'n

R/E

Infra

I nd'l

Fin'l

Energy

Comm'ns

Cash

As at July 31, 2010.Source: PC Bond, a business unit of TSX Inc. and CIBC Global Asset Management Inc.

25 25

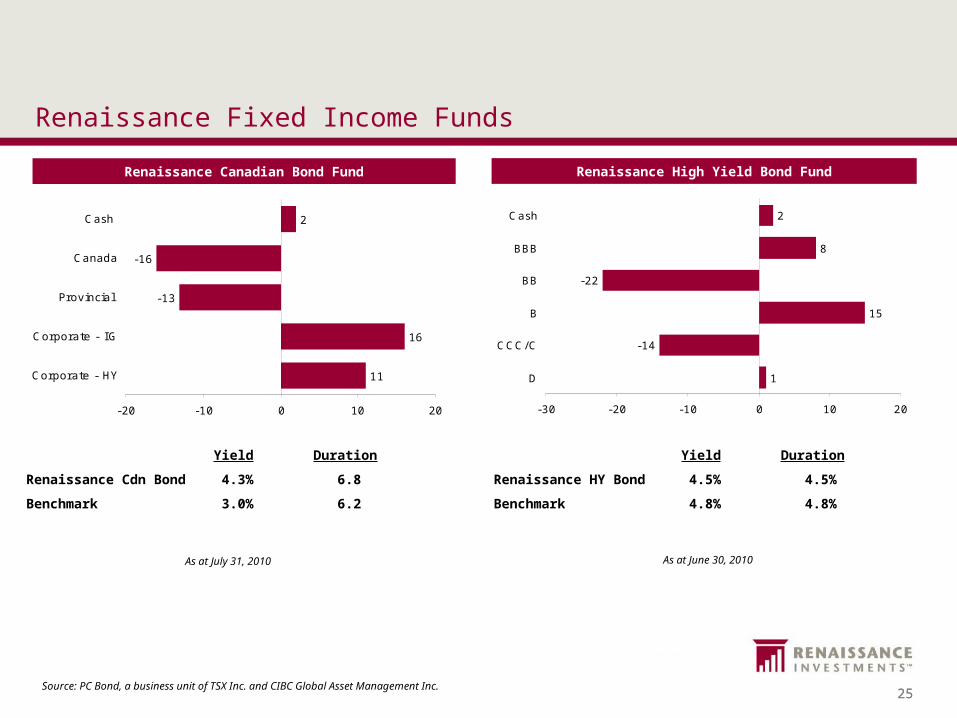

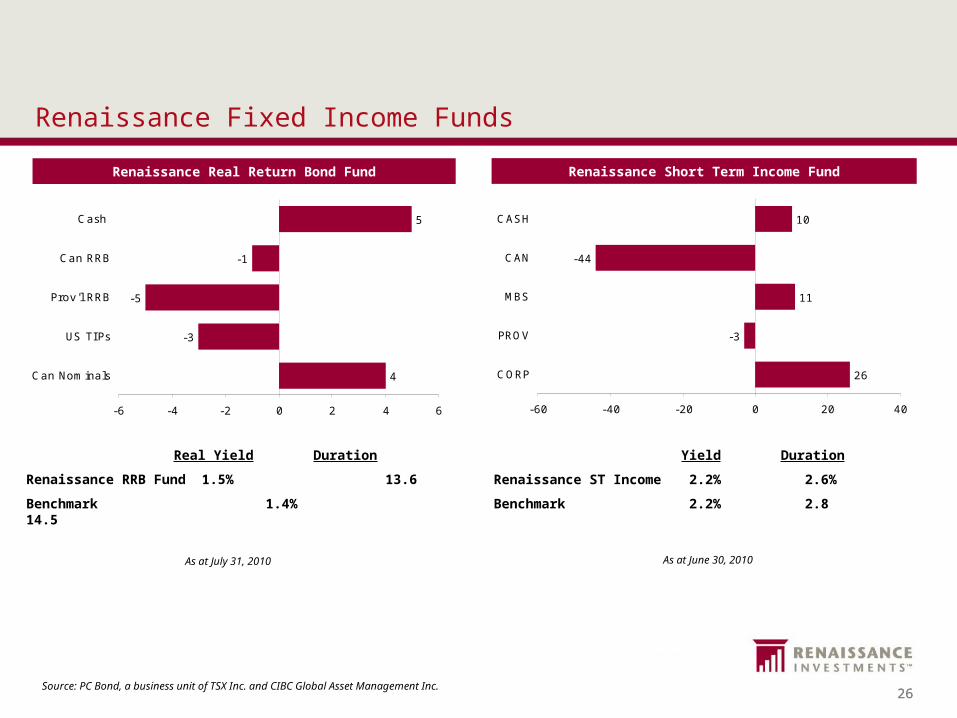

Renaissance Fixed Income Funds

Yield Duration

Renaissance Cdn Bond 4.3% 6.8

Benchmark 3.0% 6.2

Renaissance Canadian Bond Fund

11

16

-13

-16

2

-20 -10 0 10 20

Corporate - HY

Corporate - I G

Provincial

Canada

Cash

Renaissance High Yield Bond Fund

1

-14

15

-22

8

2

-30 -20 -10 0 10 20

D

CCC/C

B

BB

BBB

Cash

Yield Duration

Renaissance HY Bond 4.5% 4.5%

Benchmark 4.8% 4.8%

As at July 31, 2010 As at June 30, 2010

Source: PC Bond, a business unit of TSX Inc. and CIBC Global Asset Management Inc.

26 26

Real Yield Duration

Renaissance RRB Fund 1.5% 13.6

Benchmark 1.4% 14.5

Renaissance Real Return Bond Fund

4

-3

-5

-1

5

-6 -4 -2 0 2 4 6

Can Nominals

US TI Ps

Prov'l RRB

Can RRB

Cash

Renaissance Short Term Income Fund

26

-3

11

-44

10

-60 -40 -20 0 20 40

CORP

PROV

MBS

CAN

CASH

Yield Duration

Renaissance ST Income 2.2% 2.6%

Benchmark 2.2% 2.8

Renaissance Fixed Income Funds

As at July 31, 2010 As at June 30, 2010

Source: PC Bond, a business unit of TSX Inc. and CIBC Global Asset Management Inc.

27 27

Conclusion

The deleveraging process will continue for years, hurting growth

Inflation is not a problem

The low interest rate environment continues

Corporate bonds are still attractive

Diversify Your Fixed Income Portfolio

28 28

Thank You

© 2010 CIBC Global Asset Management Inc. operates under the name of CIBC Asset Management in Canada and is a member of the CIBC Group of Companies. CIBC Asset Management is a Registered Trade-mark of CIBC / CIBC Global Asset Management Inc. licensee.

The user agrees that TSX Inc. and the parties from whom TSX Inc. obtains data do not have any liability for the accuracy or completeness of the data provided or for delays, interruptions or omissions therein or the results to be obtained through the use of this data. The user further agrees that neither TSX Inc. nor the parties from whom it obtains data make any representation, warranty or condition, either express or implied, as to the results to be obtained from the use of the data, or as to the merchantable quality or fitness of the data for a particular purpose.

PC-Bond, a business unit of TSX Inc. Copyright © TSX Inc. All rights reserved. The information contained herein may not be redistributed, sold or modified or used to create any derivative work without the prior written consent of TSX Inc.

APT® is a software solution that provides enhanced analytics, research, models and proprietary data to empower investment professionals to make strategic investment decisions.

This material was prepared for investment professionals only and is not for public distribution. It is for informational purposes only and is not intended to convey investment, legal, or tax advice. All information in this document is as of June 30, 2010 unless otherwise indicated, and is subject to change. The views expressed by the team(s) throughout this document may differ from the views of other teams within CIBC Global Asset Management Inc.The material and/or its contents may not be reproduced without the express written consent of CIBC Asset Management. ™ CIBC Asset Management is a registered trademark of Canadian Imperial Bank of Commerce. ™Renaissance Investments and "invest well. live better." are registered trademarks of CIBC Asset Management Inc.

29 29

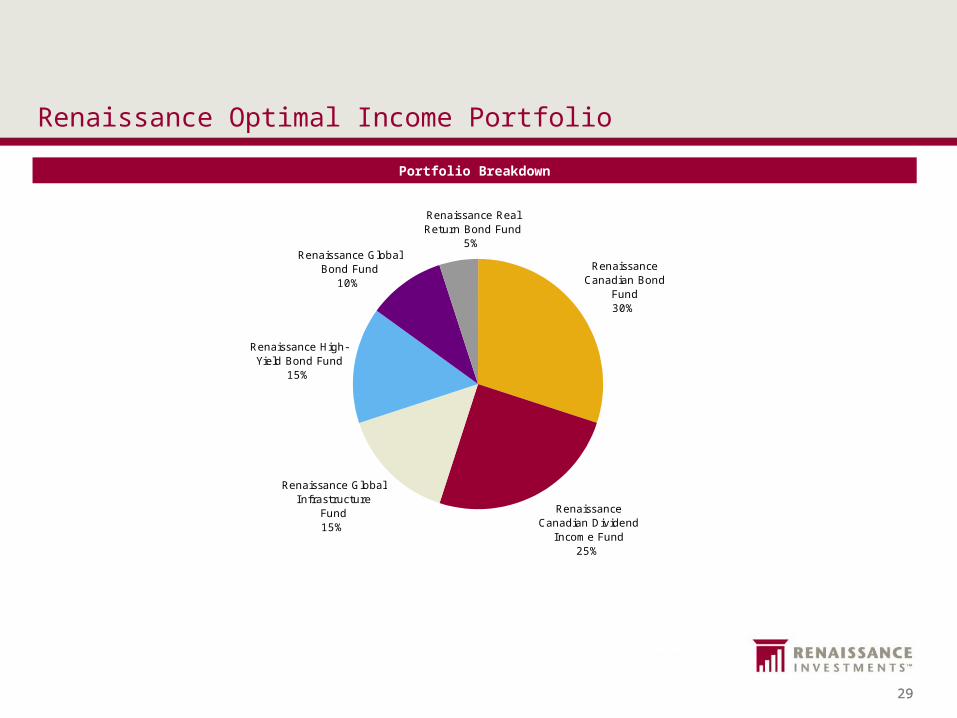

Renaissance Optimal Income Portfolio

Portfolio Breakdown

Renaissance Canadian Bond

Fund30%

Renaissance Canadian Dividend

Income Fund25%

Renaissance Global Infrastructure

Fund15%

Renaissance High-Yield Bond Fund

15%

Renaissance Real Return Bond Fund

5%Renaissance Global

Bond Fund10%

30 30

Renaissance Optimal Income Portfolio

“Making the fixed income part of your book work for you again”

** Annualized as at February 28, 2010.

31 31

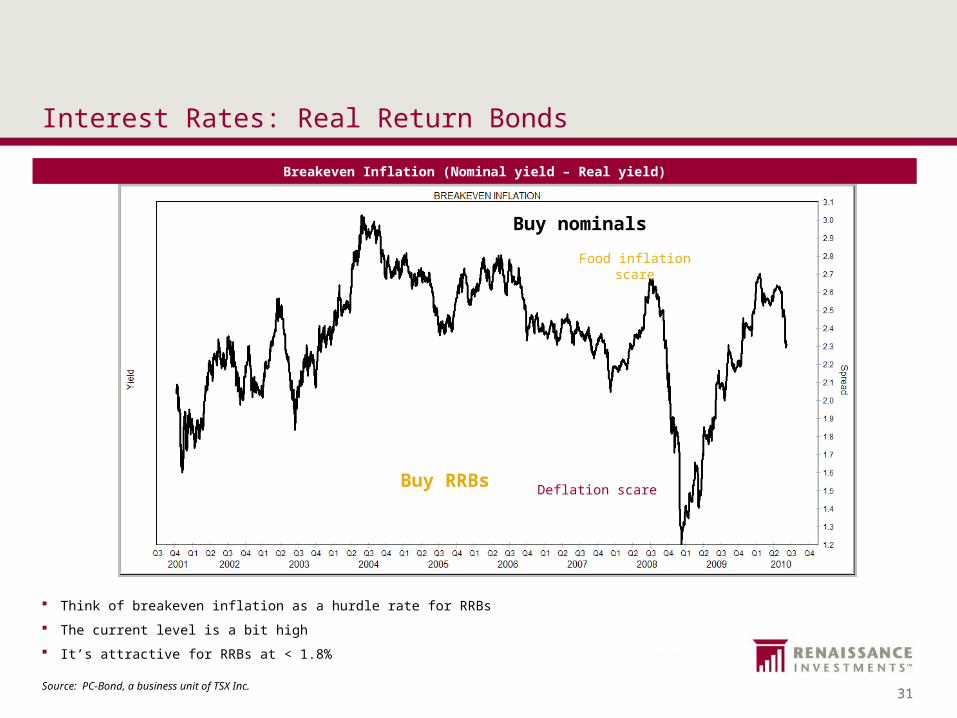

Think of breakeven inflation as a hurdle rate for RRBs

The current level is a bit high

It’s attractive for RRBs at < 1.8%

Food inflation scare

Deflation scare

Buy nominals

Buy RRBs

Interest Rates: Real Return Bonds

Source: PC-Bond, a business unit of TSX Inc.

Breakeven Inflation (Nominal yield – Real yield)

32 32

Questions &

Answers