Embed Size (px)

Citation preview

1

© Sembcorp Industries 2012

Vital PartnersEssential Solutions

Sembcorp PUB Public Private Partnership

© Sembcorp Industries 2012

An Introduction To Sembcorp

2

© Sembcorp Industries 2012

100%

Temasek Holdings 49.5%*

Public Shareholders 50.5%

Sembcorp Utilities

Provides energy, water, and onsite services to customers including companies in energy intensive industry clusters as petrochemical and chemical hubs. The Utilities segment also provides solid waste management services

Sembcorp Development

Owns, develops, markets and manages urban developments comprising industrial parks as well as business, commercial and residential space in Vietnam, China and Indonesia

Sembcorp MarineMarket cap** S$10.4 bn

Offers a full spectrum of integrated marine and offshore engineering solutions from ship repair, shipbuilding, ship conversion, rig building & repair to offshore engineering & construction including topsides fabrication

100% 60.6%*

Public Shareholders39.4%

Market cap** S$10.2 bn

* Direct and indirect holdings as at September 30, 2012. The percentage is calculated based on the number of issued shares excluding shares held as treasury shares** Market cap for Sembcorp Industries and Sembcorp Marine as September 30, 2012

Group Structure

3

© Sembcorp Industries 2012

Sustainable Earnings

Net Profit before EI 5-year (2006-2011)CAGR: 16%

8.18.6

9.9 9.68.8 9.0

5.1

FY06 FY07 FY08 FY09 FY10 FY11 1H12

793

1,031

683

809

526 507

FY06 FY07 FY08 FY09 FY10 FY11 1H12

Net Profit = Net profit attributable to shareholders of the CompanyEI = Exceptional itemsCAGR = Compounded annual growth rate

Turnover 5-year (2006-2011)CAGR: 2%

367

4

(S$bn) 06 07 08 09 10 11 1H12

Turnover 8.1 8.6 9.9 9.6 8.8 9.0 5.1

(S$m) 06 07 08 09 10 11 1H12

Net profit before EI 381 557 534 683 761 809 367

EI 650 (31) (27) - 32 - -

3

© Sembcorp Industries 2012

Growing Energy Needs

Global Water Scarcity

Global Urbanisation

Increasing Environmental Awareness

GLOBAL TRENDS OUR BUSINESSES

Energy Marine

Water Urban Development

5

Positioned for the Future

© Sembcorp Industries 2012 6

Our Global Footprint

Global Operations across 16 Countries in Six Continents

Well-Positioned in Fast-Growing Emerging Markets

4

© Sembcorp Industries 2012

Utilities

+ Energy+ Water+ Solid Waste Management

© Sembcorp Industries 2012

Utilities Global Footprint

CHILEAntofagasta

Santiago

PANAMALake Gatun

The CaribbeanAntigua

SOUTH AFRICABallito

Mbombela

(Nelspruit)

UKTeesside

Bournemouth

PHILIPPINESSubic Bay

INDONESIABatam

Talang Kelapa

Nanjing

Zhangjiagang

Qidong

Tianjin

Qinzhou

FushunUAEFujairah

OMANSalalah

VIETNAMBa Ria-

Vung Tau

Shenyang

Xinmin

Qitaihe

Yanjiao

Fuzhou

Yancheng

Zhumadian

AUSTRALIA

SINGAPOREJurong Island

Changi

INDIAAndhra

Pradesh

Energy

WaterOn-site Logistics

Solid Waste Management (multiple locations)

Entrenched Position in Growing Markets

8

Shanghai

Hulunbeier

Huanghua

Yangcheng

8

CHINA

5

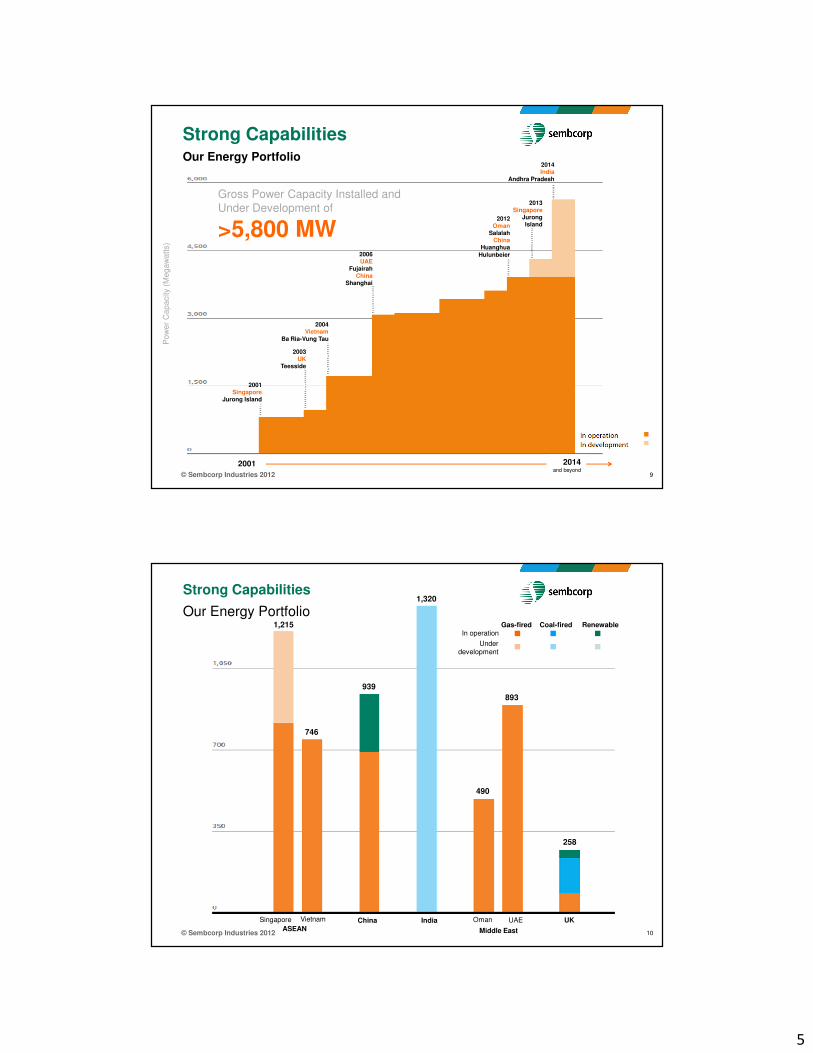

© Sembcorp Industries 2012 9

Strong CapabilitiesOur Energy Portfolio

2001 2014 and beyond

2001Singapore

Jurong Island

2003UK

Teesside

2004Vietnam

Ba Ria-Vung Tau

2006UAE

FujairahChina

Shanghai

2014India

Andhra Pradesh

Gross Power Capacity Installed and Under Development of

>5,800 MW

Po

we

r C

ap

acity (

Me

ga

wa

tts)

2012Oman

SalalahChina

HuanghuaHulunbeier

2013Singapore

JurongIsland

© Sembcorp Industries 2012

Strong Capabilities

Our Energy Portfolio

ASEAN Middle East

China India UK

10

Singapore Vietnam Oman UAE

Gas-fired Coal-fired RenewableIn operation

Under development

258

893

490

1,320

1,215

939

746

6

© Sembcorp Industries 2012

Growing Renewable Energy Capabilities

Fuel Type Facilities Steam capacity

Powercapacity

BiomassSembcorp Biomass Power Station (UK)

COD: 2007

35 MW

Energy- from-Waste (EfW)

Sembcorp Woodchip Boiler Plant

Phase 1 (Singapore) COD: 2011

20 tph 4 MW (equivalent MW)

Sembcorp Woodchip Boiler Plant

Phase 2 (Singapore) COD: 2013

40 tph 9 MW(equivalent MW)

Energy from Waste Boilers

(Singapore) COD: 2014

140 tph 31 MW(equivalent MW)

Wind

China Wind Power Assets(China)

Acquisition completed in Sep 2012

248 MW

Total 327 MW

11

Targeting a high-efficiency portfolio of thermal and renewable energy assets,

with a growing component of low carbon capacity

From 39 MW to

327MWof renewable energy capabilities

≈5% of power and steam portfolio from renewables

© Sembcorp Industries 2012

Sembcorp’s Energy-from-Waste Value Chain

Growing Renewable Energy Capabilities

12

Tph: tonnes per hour

7

© Sembcorp Industries 2012

A Water Player With A Difference

Winner of 2011 Global Water Intelligence (GWI) Global Water Awards “Water Company of the Year”

Strong Capabilities

Complete range of water products Closed loop approach minimises discharge

Total water & wastewater treatment

solutions for industrial & municipal

sectors:

� Wastewater treatment

� Reclaimed water

� Desalinated water

� Potable water

� Water for industrial use including

demineralised water, industrial water,

raw water, chilled water, cooling

water, seawater cooling and firewater

13

© Sembcorp Industries 2012

1997SingaporeJurong Island

2009Singapore

ChangiChina

Tianjin

2003UK

Teesside

2008China

Shenyang

2005China

NanjingShanghai

ChinaXinminQitaiheYanjiaoFuzhou

YanchengZhumadian

IndonesiaBatamTalangKelapa

PhilippinesSubic Bay

2010South Africa

BallitoMbombela(Nelspruit)

UKBournemouth

ChileAntofagasta

Santiago

PanamaLake Gatun

The CaribbeanAntigua

1997

Developer, Owner and Operator of Water and Wastewater Treatment Facilities with

>7,000,000 m3/day

Wate

r &

waste

wate

r tr

eatm

ent cap

acity

(m3/d

ay)

2006UAE

FujairahChina

Zhangjiagang

14

Strong CapabilitiesOur Water Portfolio

2011China

Qinzhou

2015UAEFujairah

2015 and beyond

2013Singapore

JurongIslandChina

QidongFushun9,000,000

7,000,000

5,000,000

3,000,000

1,000,000

In operation

Under development

2012Oman

SalalahSingapore

JurongIsland

8

© Sembcorp Industries 2012UKMiddle East & Africa The Americas

Serving a Population of Over

5 million Worldwide

In Operation

Municipal

Industrial

InDevelopment

15

Singapore Indonesia Philippines Oman UAE South Africa Chile Panama The Caribbean

ASEANChina

69,00069,000

69,000

69,0004,005,480

69,0001,500,000

69,0001,200,000

69,000900,000

69,000600,000

69,000300,000

69,0000

69,000295,200

69,00092,250

69,0001,327,280

69,000591,800

69,000220,850

69,000444,000

69,000205,624

69,00076,00069,00017,000

Strong CapabilitiesOur Water Portfolio

© Sembcorp Industries 2012

Multi-Customer Business Model

Leveraging Capabilities In Energy And Water

Bundled Offer Approach

Industrial Site Customers

On-site Logistics and Services �Service corridor�Chemical storage and terminalling�Asset protection�Hazardous waste incineration�Industrial gases

Energy�Power generation and retail�Process steam production and supply

�Natural gas import, supply and retail

Water�Wastewater treatment�Reclaimed water�Desalinated water�Potable Water�Water for industrial use, including demineralised water, industrial water, raw water, chilled water, cooling water, seawater cooling and firewater

16

9

© Sembcorp Industries 2012

Wilton International, UK

� 770 ha world class manufacturing site

� Sembcorp owns the site and provides energy, water and on-site logistics and services

� Operational since 1949

� Total project cost: £296 million (US$529 million)

Jurong Island, Singapore

� 3,200 ha world class chemical hub in Singapore

� Sembcorp provides energy, water and on-site logistics and services to over 40 multinationals

� Operational since 1997

� Total project cost: S$2.5 billion (US$1.6 billion)

17

Leveraging Capabilities In Energy And Water

Sembcorp facilities Service corridor (under development)

Existing Service Corridor

© Sembcorp Industries 2012

Solid Waste Management

Capabilities include:

� Collection and treatment of municipal, industrial & commercial, construction & demolition and bio-hazardous waste

� Recycling, resource recovery & composting

� Waste-derived fuel including woodchip production

>1.9 millionhouseholds and establishments served

>3.1 milliontonnes of waste collected per year

>430,000tonnes of recyclables collected per year

>13,000medical customers served

Focused on energy from waste to enhance competitiveness of businesses across the Group

18

10

© Sembcorp Industries 2012

Marine

© Sembcorp Industries 2012

Global Network Of Strategically Located Shipyards

A Global Hub

CHINA(Through COSCO shipyards with

2,045,000 dwt total dock capacity) Dalian, Guangdong, Lianyungang,Nantong, Qidong, Shanghai,Zhoushan

INDONESIA� PT SMOE Indonesia (69 ha)� PT Karimun Sembawang Shipyard (31 ha)

SINGAPORE� Jurong Shipyard (1,100,000 dwt, 68 ha)� Sembawang Shipyard (775,000 dwt, 86 ha)� SMOE* (25 ha)� PPL Shipyard (20 ha)� Jurong SML (62,500 dwt, 12 ha)� New Yard Facility** (3,075,000 dwt, 206 ha)

USA� Sembcorp-Sabine Shipyard (90 ha)

Brazil� Estaleiro Jurong Aracruz (82.5 ha)

dwt: deadweight tonnes; ha: hectares* SMOE’s facilities are located on the same plot of land

as Sembawang Shipyard

India� Sembmarine Kakinada (31 acres)

20

11

© Sembcorp Industries 2012

Growing And Expanding Our Business

|1963-1969| |1970-1975| |1976-1994| |1995-2000| |2001-2005| |2006-2012|

Ship repair (1963)

Shipbuilding (1970)

Ship conversion and offshore (1976)

Offshore engineering (1995)

Rig building (2001)

Offshore production fixed & floating facilities (2006)

21|2012 & beyond|

Drillships (2012)

© Sembcorp Industries 2012

Urban Development

12

© Sembcorp Industries 2012

Our Regional Presence

China

� Wuxi-Singapore Industrial Park

� Sino-Singapore Nanjing Eco Hi-tech Island

� Singapore-Sichuan Hi-tech Innovation Park

� China-Singapore Suzhou Industrial Park*

Indonesia

� Gallant Venture (listed on SGX)

– Batamindo Industrial Park

– Bintan Industrial Estate

� Kendal Regency Industrial Park

� Karimun Marine & Industrial Complex*

Vietnam

�Vietnam Singapore Industrial Park (VSIP)

�VSIP Binh Duong Integrated Township & Industrial Park

�VSIP Bac Ninh Integrated Township & Industrial Park

�VSIP Hai Phong Integrated Township & Industrial Park

�VSIP Quang Ngai Integrated Township & Industrial Park

*Projects not managed by SCD

23

© Sembcorp Industries 2012 24

Sharpen Competitive EdgeBusiness Model

1990 2007 Future potential

Valu

e C

reation

Industrial Park Model

Utilities

Facilities Management

Urban Development Model

Utilities

Facilities Management

Land Developer• Industrial land sales

Real Estate Developer• Ready-built factories (RBF)• Built-to-suit factories

Land Developer• Industrial land sales• Commercial & Residential land

sales

Real Estate Developer• Ready-built factories (RBF)• Built-to-suit factories• Commercial & Residential

- Within the Parks- Around the Parks

13

© Sembcorp Industries 2012

Why PPP?

© Sembcorp Industries 2012

� Strategic Fit

� Complement our global total water

solutions footprint

� Showcase our leadership in operational

and integrated water solution provider

expertise

Why PPP?

� Opportunity for future collaborations across entire supply chain to reap technology and

optimization benefits

� Diversity in different business models in different sectors increases Sembcorp Group

experience and provides opportunities for continuous improvements through sharing via

our global best practices network

� Enhances international and global organizational skills within the Group

14

© Sembcorp Industries 2012

Sembcorp PUB PPP Commercial Structure

© Sembcorp Industries 2012

Contracts Structure

Sembcorp NEWaterSembcorp NEWater

EPC contract with

Sembcorp Utilities

Power supply

Contract with

Sembcorp Power

Water Supply Agreement with PUB

O&M Contract

with Sembcorp

Industries

Turnkey project

• Notice to Proceed: Feb 2008

• Initial Completion: 31 Jul 09 (15 MiGD)

• Final Completion: 31 May 10 (50 MiGD)

O&M services contract

• Sembcorp Industries

• O&M of NEWater plant (25 years)

• Sembcorp NEWater wholesales NEWater to

PUB for Island wide distribution and sales.

• PUB Changi WRP provides feedwater to

Sembcorp NEWater

• Applicable tariff will be paid by PUB based

on actual NEWater quantity supplied

• Technical requirements specified in Water

Supply Agreement

Power supply contract

• Sembcorp Power

• 25 years supplies from final

completion

15

© Sembcorp Industries 2012

Facilities Description

© Sembcorp Industries 2012

Production of NEWater

16

© Sembcorp Industries 2012

Equalization Tank32,000 m3

Effluent Transfer Pumps

CWRP

Liquid

Treatment

Module 1

300µm MF Feed Auto-strainers

MF Feed Pumps

Sodium HypochloriteAmmonium Sulfate*

Micro Filtration13,000 m3/h, 93% recovery(7 trains x 8 blocks x 120

modules)ReverseOsmosis

Feed Tanks

RO Feed Pumps

8” RO 9,500 m3/h, 80% recovery

(10 trains x 135+63 vessels x 7 elements)

RO Anti-scalantSodium Bisulfite

Low-Pressure UV(6 units x 30 lamps)

NEWater Storage Tanks(5 x 17,100 m3)

So

diu

m H

yd

roxid

eS

od

ium

Hyp

och

lorite

NEWater Pumps3,150 m3/h @ 72m

each

Sodium HypochloriteSulfuric Acid*

* Dosed when necessary

Ø900 mm to Bedok NF

NIP Ø2,200 mm to Mandai Hill Service

Reservoir

Qu

ality

An

aly

zers

Flo

wm

ete

rs

PUB

Sembcorp

Process Flow DiagramProcess Flow DiagramProcess Flow DiagramProcess Flow Diagram

© Sembcorp Industries 2012

Plant Layout - Architecture

32

17

© Sembcorp Industries 2012

Plant Layout

33

NEWater Process Area

MF / RO / UV

NEWater Storage Area

Equilization Tank

MF Feedwater Pumping

NEWater Pumping Station & Valve Vault

© Sembcorp Industries 2012

Feedwater Tank Inlet

34

Feedwater Source: ~300K M3/D

Secondary treated effluent from

PUB Changi Water Reclamation Plant

18

© Sembcorp Industries 2012

Equalization and Diversion Tanks L85m x W32m x H11m – 32K M3

35

© Sembcorp Industries 2012

Micro Filtration Feed Pump System~ 4K M3/H, 450KW, Variable Speed Drive

36

19

© Sembcorp Industries 2012

Auto Strainer SystemAmiad 20” Dia, 300 microns

37

© Sembcorp Industries 2012

Micro Filtration TrainsSiemens Memcor, 7 trains x 8 Blocks x 120 modules13K M3/H, 93% Recovery

38

20

© Sembcorp Industries 2012

Reverse Osmosis TrainsToray, 9.5K M3/H, 80% recovery10 trains x 135 vessels x 7 elements

39

© Sembcorp Industries 2012

Ultra-violet Disinfecting System6 units

40

21

© Sembcorp Industries 2012

NEWater Storage TanksDia 40M x H14.3M, 5 x 17K M3

41

© Sembcorp Industries 2012

NEWater Pumping Station5 x ~3K M3/H

42

22

© Sembcorp Industries 2012

Process Plant Area

43

Clean in Place Facilities

Chemical Dosing Facilities

UV / RO / MFProcess Units

© Sembcorp Industries 2012

PPP Critical Success Factors

23

© Sembcorp Industries 2012

PPP – Critical Success Factors

45

• Long term contract with outputs defined

• Clear sharing and allocation of risks

• Performance based payment mechanism

• Rewards and costs sharing for continuous improvements

• Services Delivery Management not construction nor goods supply contract management

• Proactive and transparent plant information monitoring and sharing – collaboration attitude

• Relationship = Partnership (mentality must be actively cultivated with Senior Management sponsorship)

© Sembcorp Industries 2012

Examples on Critical Success Factors

24

© Sembcorp Industries 2012

Some Examples of CSFs

47

� Long term contract with output defined� Sembcorp will provide innovative,

essential and cost effective solutions (see our tag line)

� Clear sharing and allocation of risks� Each party assumes risks they are in

best position to manage

� Rewards and costs sharing� Sembcorp will optimize but some

technology needs piloting

� Services Delivery Management� Feedwater quality wide fluctuation

task force� Proactive and open communication

can be a very effective low costs solution too

© Sembcorp Industries 2012

Some Examples of CSFs

48

� Relationship management

� Proactively seek to improve on relationship

� Assign the right people (flexible mentality)

� Senior Management sponsorship (commit the resources)

� Take the opportunity to Celebrate every success regardless of size

� Proactively champion plant performance continuous improvements (seek common goals)

25

© Sembcorp Industries 2012

Moving On – Next 20 Years

© Sembcorp Industries 2012

Relationship Management is Key

50

• PPP is interdependent and long term in nature

• Step – in rights is good on paper and is lose – lose

• Build up partnership based on common ground – mutual benefits• Flexibility• Behaviors to support mutual respect and understanding• Transparent and open communications• Seek common goals

Coming together is a beginning; keeping together is progress;working together is success.

- Henry Ford