Embed Size (px)

Citation preview

SELECTIVE PRE-AUDIT SELECTIVE PRE-AUDIT ON GOVERNMENT ON GOVERNMENT TRANSACTIONSTRANSACTIONS

Brief BackgroundBrief Background

• traditionally, government auditing is on a pre-audit system

• General McArthur issued General Order No. 72 ON 23 May 1900 prescribing that “civilian officials’ estimates for funds needed (cash advances) shall be coursed thru the department heads and forwarded through the Auditor to the Military Governor for approval. Military officials charged with disbursing funds shall forward their estimates to division headquarters, to the Auditor, thence to the Military Governor for approval

Brief BackgroundBrief Background

• On 23 February 1901, the US President issued an unnumbered executive order which stated among others that the warrants to be issued by the Military Governor were to be countersigned by the Auditor. When peace and order reigned in the Philippine Islands, the civil government ushered and the Office of the Auditor was converted into a Bureau of Insular Auditor. Countersigning of warrants still remained. Even during the reign of Governor Generals and the change of the Bureau of Insular Auditor to the Bureau of Audits, and during the Commonwealth regime, the system of countersigning of warrants by the Auditor prevailed.

Brief BackgroundBrief Background

• The shortcomings of the pre-audit system was then felt by the government authorities. In the early 1953, then Acting Auditor General Pedro M. Jimenez lifted pre-audit of expenditures in national agencies not exceeding P200 (raised to P500 in 1955), to “reduce to the minimum the delay in the payment of claims” . When Gimenez became a full pledged Auditor General, pre-audit in all government owned and controlled corporations as well as national government agencies (except for a few transactions), was lifted. Ironically, two years later, Gimenez restored pre-audit in the Department of Public Highways and one month from that date, restored the pre-audit of all government corporate expenditures. The restoration of pre-audit in national government agencies followed six months later, “to countervail expenditures that tend to dry cash in the treasury and those leading to uneconomical operations”.

Brief BackgroundBrief Background

• Again in 1967 then Auditor General Ismael Mathay Sr. , took exploratory steps towards the lifting of pre-audit (disbursements not exceeding P5,000 was exempted from pre-audit). However, full pre-audit was still in effect through the Auditor’s inspection activities. The biggest attempt in the lifting of pre-audit was in 1976 when then Chairman Francisco Tantuico, Jr. issued COA Circular 76-26 and its subsequent amendments partially lifting pre-audit towards the full implementation of post-audit. Pre-audit was totally lifted in 1996.

Legal BasisLegal BasisSection 2(1) of Article IX D of the 1987 Constitution of the Section 2(1) of Article IX D of the 1987 Constitution of the Philippines which states that:Philippines which states that:

“The Commission on Audit shall have the power, authority, and duty to examine, audit, and settle all accounts pertaining to the revenue and receipts of, and expenditures or uses of funds and property, owned or held in trust by, or pertaining to, the Government or any of its subdivisions, agencies, or instrumentalities, including government-owned or controlled corporations with original charters, and on a post-audit basis: (a) constitutional bodies, commissions and offices that have been granted fiscal autonomy under this Constitution (b) autonomous state college and universities; (c) other government-owned or controlled corporations and their subsidiaries; and (d) such non-governmental entities receiving subsidy or equity, directly or indirectly, from or through the government, which are required by law or the granting institution to submit such audit as a condition of subsidy or equity. However, where the internal control systems of the audited agencies is inadequate, the Commission may adopt such measures, including temporary or special pre- audit, as are necessary and appropriate to correct the deficiencies. x x x x x x x

• The Commission shall have exclusive authority, subject to the limitations in this Article, to define the scope of its audit and examination, establish the techniques and methods required therefore, x x x x x x

Legal BasisLegal BasisSection 2(2) of Article IX D of the 1987 Constitution of the Section 2(2) of Article IX D of the 1987 Constitution of the Philippines which states that:Philippines which states that:

MINUTES OF THE PROCEEDINGS OF MINUTES OF THE PROCEEDINGS OF THE CONSTITUTIONAL CONVENTIONTHE CONSTITUTIONAL CONVENTION

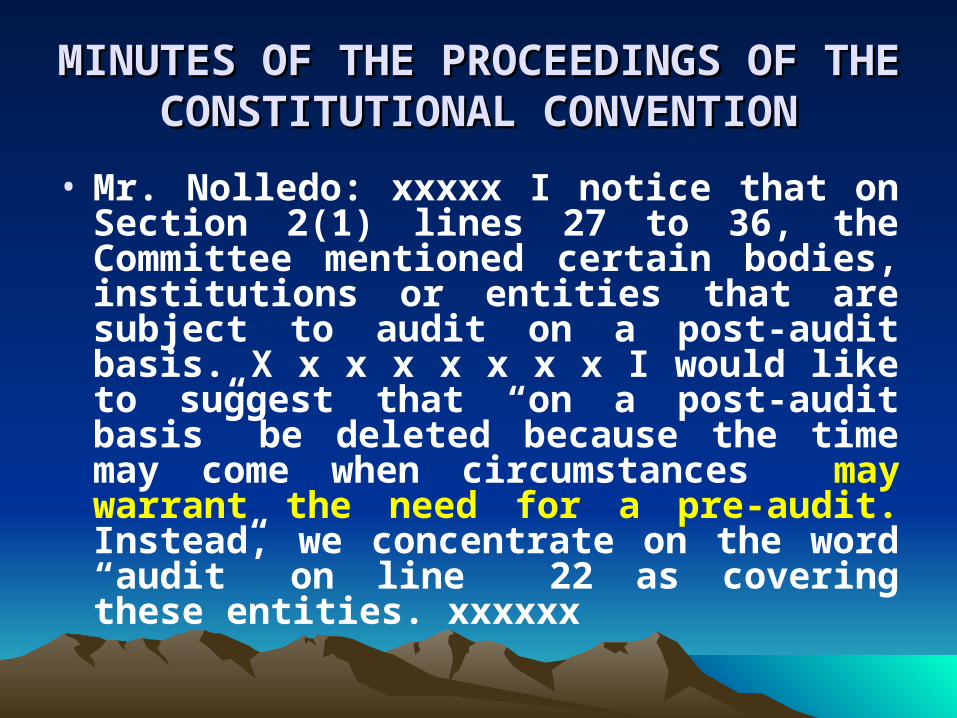

• Mr. Nolledo: xxxxx I notice that on Section 2(1) lines 27 to 36, the Committee mentioned certain bodies, institutions or entities that are subject to audit on a post-audit basis. X x x x x x x x I would like to suggest that “on a post-audit basis” be deleted because the time may come when circumstances may warrant the need for a pre-audit. Instead, we concentrate on the word “audit” on line 22 as covering these entities. xxxxxx

MINUTES OF THE PROCEEDINGS MINUTES OF THE PROCEEDINGS OF THE CONSTITUTIONAL OF THE CONSTITUTIONAL

CONVENTIONCONVENTION

• Mr. Monsod: Maybe we should explain why the Committee made an exception on these institutions and made them on a post-audit basis, because normally COA Audit is both on a pre-audit and post-audit basis. This decision was really very difficult on the part of the Committee, for it involved discussions, as well as a very lengthy testimony by the Commission on Audit. There are certain companies or institutions within the government itself which by the nature of their functions would be hampered by pre-audit procedures. The question now is: Would limiting the COA to post-audit procedures not allow abuses on the part of these institutions?

MINUTES OF THE PROCEEDINGS MINUTES OF THE PROCEEDINGS OF THE CONSTITUTIONAL OF THE CONSTITUTIONAL

CONVENTIONCONVENTION (CONTINUATION- Mr. Monsod)• As a matter of fact, if we look at the performance of COA at this

time, perhaps over 80-90 per cent of the anomalies unearthed were on a post-audit basis. The reason there were so many anomalies during the Marcos year’s is not the absence of a pre-audit or a post-audit function. As a matter of fact, there was a pre-audit function, but it was a whole system to defraud and misspend that was put in place that prevented COA from the exercise of its normal function. Under normal circumstances, a post-audit is a very effective tool and deterrent, but we must balance it against the normal operations of corporations that must necessarily involve huge amounts of money on a day-to-day basis.

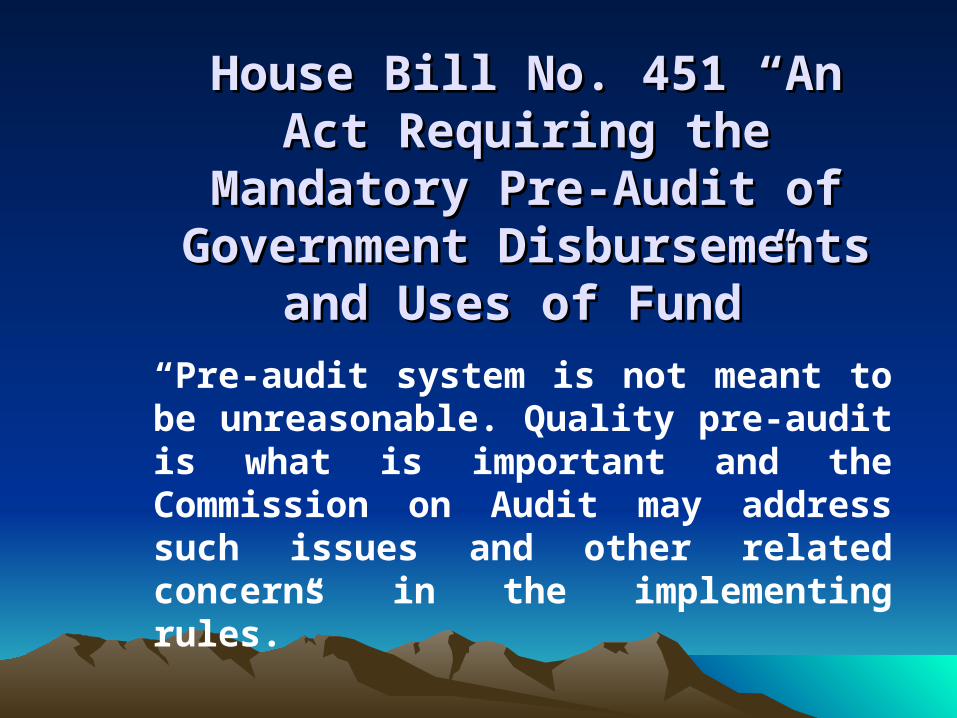

House Bill No. 451 “An Act House Bill No. 451 “An Act Requiring the Mandatory Pre-Requiring the Mandatory Pre-

Audit of Government Audit of Government Disbursements and Uses of Disbursements and Uses of

Fund”Fund”

“Pre-audit system is not meant to be unreasonable. Quality pre-audit is what is important and the Commission on Audit may address such issues and other related concerns in the implementing rules.”

House Bill No. 451…House Bill No. 451…

The argument that this pre-audit scheme will The argument that this pre-audit scheme will result in further delays, establishing another result in further delays, establishing another unnecessary level of review, that may unnecessary level of review, that may unduly prejudice implementation of urgent unduly prejudice implementation of urgent government projects and transactions must government projects and transactions must now yield to the higher interest to protect now yield to the higher interest to protect and conserve government resources and and conserve government resources and minimize losses from illegal expenditures in minimize losses from illegal expenditures in these hard times.these hard times.

RATIONALERATIONALE

• Rising incidents of illegal, irregular, wasteful and anomalous disbursements of huge amounts of public funds

• Marked inadequacies in internal controls as exemplified by anomalies uncovered or reported after assessment of risk-prone areas in government operations

WHY SELECTIVE PRE-AUDIT?

• not all government agencies are subject to pre-audit

• not all transactions of the government are subject to pre-audit - only 10 transactions are initially identified

DEFINITION AND GENERAL SCOPE DEFINITION AND GENERAL SCOPE OF PRE-AUDIT OF PRE-AUDIT

Pre-audit is the examination of documents supporting a transaction or series of transactions before these are paid for and recorded.

DEFINITIONDEFINITION…continued…continued

Pre-audit operates to-

- determine that the proposed expenditure is in compliance with appropriation law and other specific statutory authority and regulations

- assure that sufficient funds are available

- initially determine that the transaction is not illegal irregular, extravagant, excessive, unconscionable or unnecessary

- determine that the transaction is approved by proper authority and supported by authentic underlying evidences

INITIAL DETERMINATIONINITIAL DETERMINATION

As used in the circular “initially determine” emphasize that-

• Determination of the auditor is not yet final and could be modified in post-audit

- In cases of technical matters, the auditor may possess some degree of competency in determining the reasonableness of price but still needs the assistance of a technical expert.

INITIAL DETERMINATIONINITIAL DETERMINATION…… (continued)(continued)

The final determination contemplated above shall be understood only for purposes of the pre-audit or post-audit at the level of the auditor.

PRE-AUDIT VS. POST-AUDIT

• Pre-audit is a review before a transaction is paid for or recorded. Post-audit refers to review after the transaction is recorded or consummated.

• Pre-audit is an upfront auditing procedure undertaken on the documents supporting a transaction prior to its payment or recording.

COVERAGECOVERAGE

Agencies

- national government agencies, local government units and GOCCs with original charter

Exception: national high schools, GOCCs audited on an engagement basis and barangays

COVERAGE…COVERAGE… continued continuedTransactions - cash advances - payments of salaries and terminal leave benefits - payments for infrastructure projects - payments for road right-of-way - procurement of capital assets, goods and services - payments thru ADA (suspended under COA Circular No.

2009- 005 dated September 15, 2009)

- releases of funds to NGOs/Pos (suspended under COA Circular No. 2009-007 dated September 25,

2009) - transfer of funds between government agencies - disbursements from trust funds of LGUs - disposal of real property and unserviceable

property

SPECIFIC SCOPE OF PRE-AUDIT SPECIFIC SCOPE OF PRE-AUDIT Cash advances

- all cash advances including those for foreign travel funded out of local funds

Exceptions: cash advances for payroll fund, intelligence funds, petty cash funds, revolving funds and local travel expenses

SPECIFIC SCOPESPECIFIC SCOPE… … continuedcontinued

Payment of salaries and terminal leavebenefits

- payment of first salary after appointment by

transfer or reinstatement and last payment of

salary prior to transfer

- all payments of terminal leave benefits

SPECIFIC SCOPESPECIFIC SCOPE… … continuedcontinued

Infrastructure projects - Only the advance payments to contractors and the

first and last progress billings are subject to pre-audit

- First progress billing covers first collection on work accomplishment

- Pre-audit of last progress billing must consider all previous payments

SPECIFIC SCOPESPECIFIC SCOPE… … continuedcontinued

Variation orders

• all first payments under variation orders related to contracts within the monetary threshold are subject to pre-audit

• First payment and last progress billing under variation orders which bring a contract within the monetary threshold are subject to pre-audit

SPECIFIC SCOPESPECIFIC SCOPE… … continuedcontinued

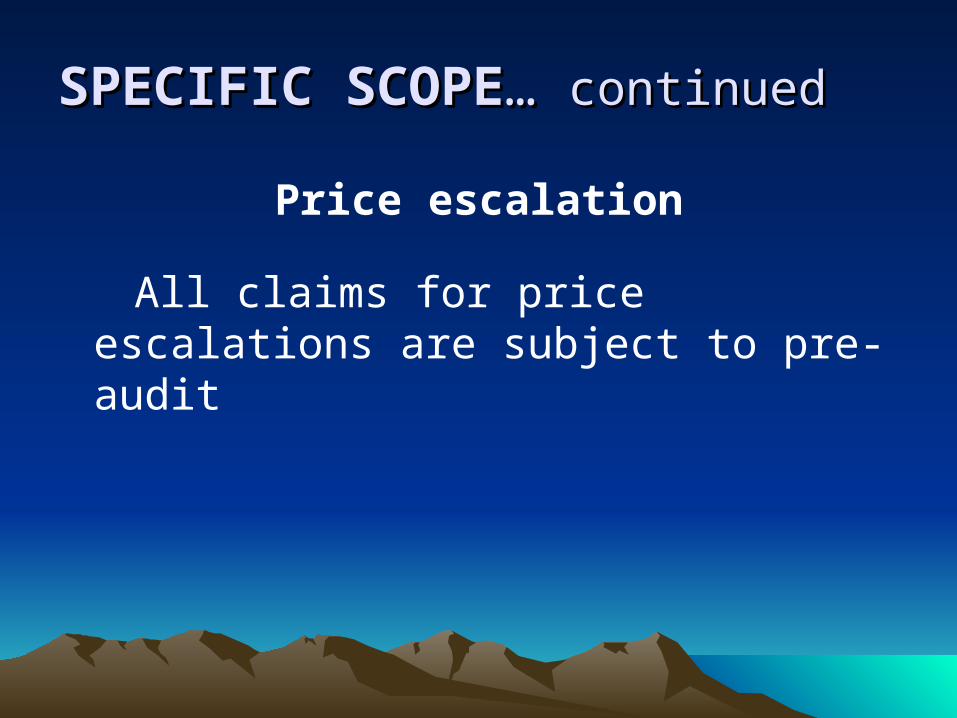

Price escalation

All claims for price escalations are subject to pre-audit

SPECIFIC SCOPESPECIFIC SCOPE… … continuedcontinued

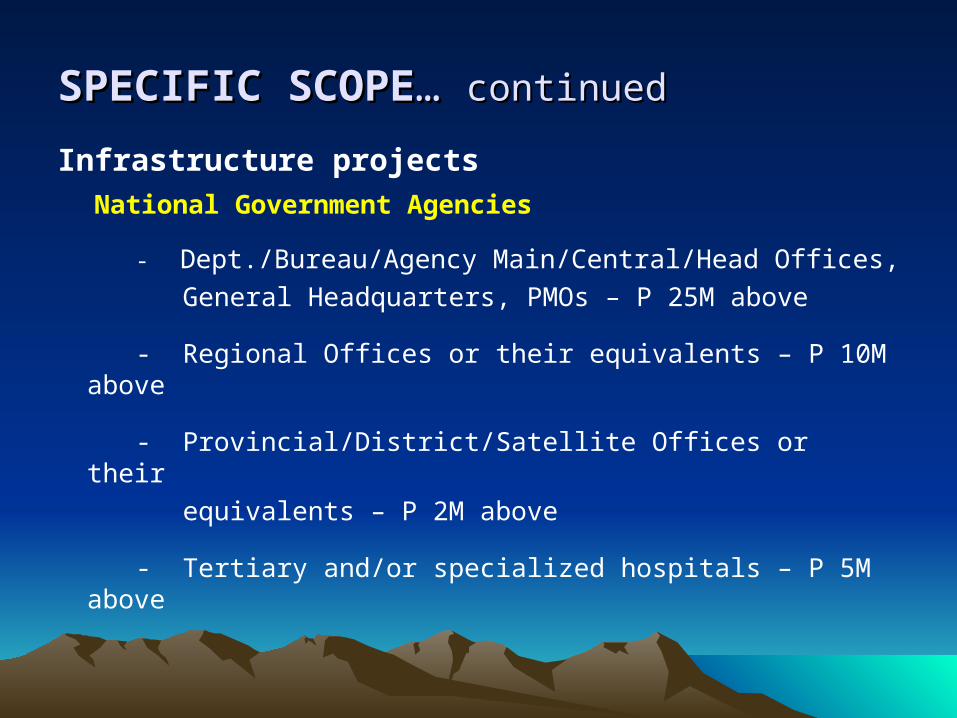

Infrastructure projects National Government Agencies

- Dept./Bureau/Agency Main/Central/Head Offices, General Headquarters, PMOs – P 25M above

- Regional Offices or their equivalents – P 10M above

- Provincial/District/Satellite Offices or their equivalents – P 2M above

- Tertiary and/or specialized hospitals – P 5M above

SPECIFIC SCOPESPECIFIC SCOPE… … continuedcontinued

Local Government Units - Cities within MM, other highly urbanized cities, first class provinces – P 5M above

- Provinces/cities below first class – P 3M above

- Municipalities – P 1M above

GOCCs - Head Offices, PMOs – P 25M above

- Regional/Provincial Branches/Field Offices – P 10M above

- Tertiary and/or specialized hospitals – P5M above

SPECIFIC SCOPESPECIFIC SCOPE… … continuedcontinued

Payments for road right-of-way

• All claims for road right-of-way to be pre-audited based on its compliance with the requirements of RA No. 8974 and its implementing rules and regulations

SPECIFIC SCOPESPECIFIC SCOPE… … continuedcontinued

Procurement of capital assets, goods and services

- capital assets (land and building)

- supplies, materials, general support services (rentals,

janitorial, security, solid waste management) labor - procurement of construction materials for projects implemented by administration

only first payment for general support services is subject to pre-audit

SPECIFIC SCOPE… continuedSPECIFIC SCOPE… continued

Procurement of Goods… continued Procurements subject to pre-audit: - at least P 2M for NGAs, GOCCs, cities within MM, other highly

urbanized cities and first class provinces

- at least P 1M for provinces/cities below first class

- at least P500,000 for municipalities

Exception: - Procurement between government agencies

- Procurement of goods and services to address the effects

and impacts of natural calamities or emergencies during

its existence shall be exempt from pre-audit (as amended under COA Circular No. 2009-007 dated Sept. 25, 2007)

SPECIFIC SCOPESPECIFIC SCOPE… … continuedcontinued

Transfer of funds between and among government agencies

- all transfers of funds either thru funding check or bank transfer between and among bank accounts of agencies or between different bank accounts of the same government agency.

SPECIFIC SCOPESPECIFIC SCOPE… … continuedcontinued

Exceptions:

- Routinary fund transfers between government banks

- Transfers of funds to address an emergency or existing calamity

- Releases of NCAs and NTAs

SPECIFIC SCOPESPECIFIC SCOPE… … continuedcontinued

Disbursements from trust funds of LGUs “Disbursement of trust funds of local government

units covered by pre-audit shall include only trust funds received from national government agencies and government –owned and controlled corporations intended to implement specific projects which could be either as infrastructure project or procurement. Thus, the thresholds established in items 4.3.2 ( infrastructure projects) and 4.5.3 (procurement of goods and services) of the Circular shall govern” ( as amended under COA Circular No. 2009-007 dated September 25, 2009)

SPECIFIC SCOPESPECIFIC SCOPE… … continuedcontinued Disposal of real property, unserviceable property

and those no longer needed

- Include only those undertaken through negotiated sale for NGAs/GOCCs and private sales for LGUs

Real property - at least P1 million for NGAs and GOCCs - regardless of amount for LGUs Unserviceable property/those no longer needed - at least P500,000 for NGAs/GOCCs - acquisition/transfer cost of at least P50,000 for provinces/cities and P25,000 for municipalities/barangays

SPECIFIC SCOPESPECIFIC SCOPE… … continuedcontinued

Acquired assets of GFIs – at least

P50M

Exception: Disposal to previous owners in the exercise of the right of redemption

DUTIES AND RESPONSIBILITIES OF DUTIES AND RESPONSIBILITIES OF AGENCY OFFICIALSAGENCY OFFICIALS• no transactions are paid without evidence of the

pre-audit action

• all disbursement vouchers, advices/instructions, MOAs, MOUs, contracts, purchase/letter orders, loan agreements, bond flotation/certificates of indebtedness, appraisal reports and their supporting documents are submitted

• disbursement vouchers for infrastructure projects are accompanied by duly accomplished relevant checklist for technical review

DUTIESDUTIES… … (continued)(continued)

• copies of delivery documents are furnished to the auditor within 24 hours after acceptance of deliveries

• the agency’s Annual Procurement Plan and its amendments are submitted within the first quarter

• a separate logbook of transactions subject to and submitted for pre-audit is maintained.

EVIDENCE OF AUDIT ACTIONEVIDENCE OF AUDIT ACTION

• Pre-audit action is evidenced by a pre-audit stamp impressed upon the face of the disbursement voucher and its supporting documents with the following statement:

Pre-audited pursuant to COA Circular No. 2009-002 dated May 18, 2009

EVIDENCE OF AUDITEVIDENCE OF AUDIT……continuedcontinued

• In case of deficiencies or defects, the disbursement voucher and its supporting documents should be returned to the head of the agency within 24 hours from such determination informing him of the action taken and indicating the reasons therein

• Credit Notice for cash advances

APPEALAPPEAL

• Adverse action of the auditor may be appealed to the Cluster/Regional Director

• Decision of the Cluster/Regional Director shall not be subject to appeal to higher authorities

• Agency may pursue the proposed transaction notwithstanding the adverse action of the auditor or director.

APPEAL APPEAL … … (continued)(continued)

• Appeal is permitted as an extraordinary remedy to afford the aggrieved party another opportunity to ventilate its cause.

• Appeal is limited to the Cluster/Regional Director because the proposed transaction is not yet consummated and the CP does not act on hypothetical issues.

PENAL PROVISIONSPENAL PROVISIONS

• Non-liquidation of cash advances subjects the accountable officer to liability under Sec. 128 in relation to Sec. 89 of PD 1445 and/or other applicable laws and administrative regulations.

• Non-submission of transaction for pre-audit before consummation is a ground for initiating administrative disciplinary action in accordance with Section 127 of PD 1445 and Section 55, Title I-B, Book V of EO No. 292, without prejudice to disallowance, if warranted

OVERSIGHT COMMITTEEOVERSIGHT COMMITTEE

• The Assistant Commissioners’ Group

• Authority and responsibility

- recommend to CP the inclusion/exclusion of transactions subject to pre-audit

- develop mechanism for evaluating progress of agencies

in enhancing/improving their internal control

- develop mechanism/process by which agencies may

be exempted from pre-audit using the risk-calibrated

agency audit framework

![[GOVERNMENT OF GRENADA – AUDIT DEPARTMENT]](https://img.dokumen.tips/doc/110x75/586a20d31a28abc92d8bc2fa/government-of-grenada-audit-department.jpg)