Embed Size (px)

Citation preview

Sec. 8.2 – 8.3Sec. 8.2 – 8.3

Exchange RiskExchange Risk

What is a Short Position?What is a Short Position?

Liabilities > assetsLiabilities > assets

If you are borrowing Yen to buy $ If you are borrowing Yen to buy $ denominated assets? Are you denominated assets? Are you short or long?short or long?

Who is long?Who is long?

Who is long on $? Who is short?Who is long on $? Who is short?

What Happens if the Yen falls?What Happens if the Yen falls?

QuickTime™ and aTIFF (Uncompressed) decompressor

are needed to see this picture.

DefinitionDefinition

Foreign Exchange Risk = Foreign Exchange Risk = Variability in the value of an exposure that is Variability in the value of an exposure that is caused by uncertainty about exchange rate caused by uncertainty about exchange rate changes.changes.

RiskRisk

Risk is a function of 2 variablesRisk is a function of 2 variables Volatility of exchange ratesVolatility of exchange rates

Degree of exposureDegree of exposure

Degree of RiskDegree of Risk Low = rate fixed, low exposureLow = rate fixed, low exposure

High = rate volatile, high exposureHigh = rate volatile, high exposure

ConsequencesConsequences

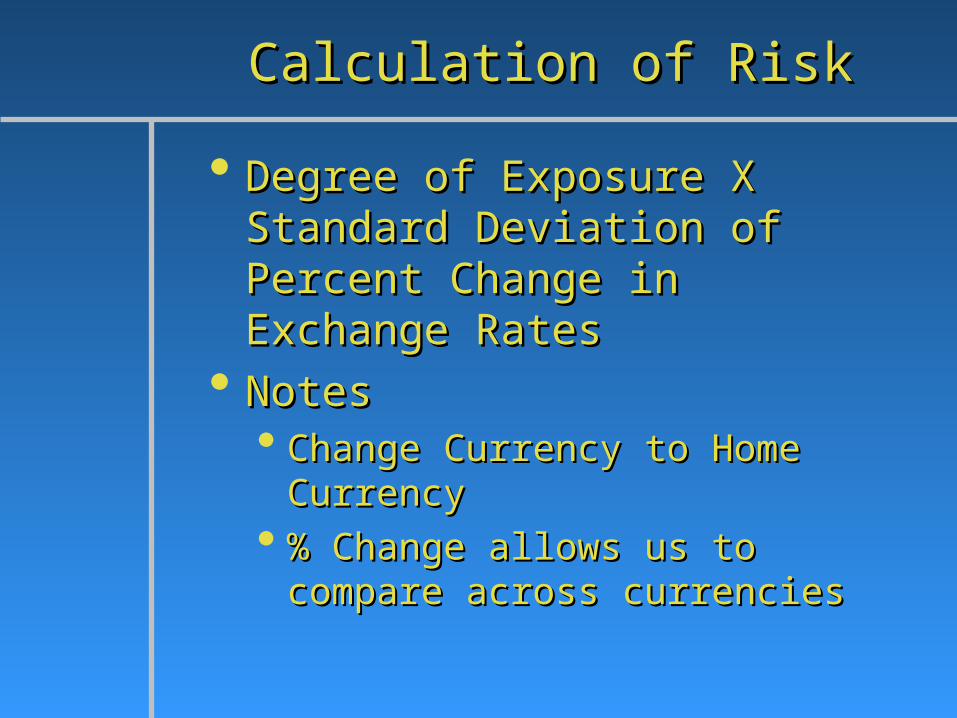

Calculation of RiskCalculation of Risk

Degree of Exposure X Standard Degree of Exposure X Standard Deviation of Percent Change in Deviation of Percent Change in Exchange RatesExchange Rates

NotesNotes Change Currency to Home CurrencyChange Currency to Home Currency

% Change allows us to compare % Change allows us to compare across currenciesacross currencies

ExampleExample

Example:Example: John has 200 Euros in receivables John has 200 Euros in receivables

due in 6 months. Forward Exchange due in 6 months. Forward Exchange rate is 1.50$/Euro. Standard rate is 1.50$/Euro. Standard Deviation of Percent Change is10%. Deviation of Percent Change is10%. What is the Exchange Risk?What is the Exchange Risk? Step 1 – Convert Exposure to home Step 1 – Convert Exposure to home

currency:currency:1.50$/Euro X 200 Euro = $3001.50$/Euro X 200 Euro = $300

Example cont. Example cont.

Step 2 – Multiply Exposure by SD of % Step 2 – Multiply Exposure by SD of % Change:Change:$300 X 10% = $30$300 X 10% = $30

Probabilities:Probabilities: One SD, 68% probability the receivables will One SD, 68% probability the receivables will

be worth between $270 - $330be worth between $270 - $330

Two SD, 95% probability the receivables will Two SD, 95% probability the receivables will be worth between $240 - $360be worth between $240 - $360

Three SD, 99.7% probability the receivables Three SD, 99.7% probability the receivables will be worth between $210 - $390will be worth between $210 - $390

Example cont.Example cont.

$60 $70 $80 $90 $100 $110 $120 $130 $140

Value at RiskValue at Risk

The most we can lose over some The most we can lose over some period, given normal market period, given normal market conditionsconditions

Usually 99% confidence levelUsually 99% confidence level

Example 2Example 2

Manny is expecting to receive 400 Manny is expecting to receive 400 UK Pounds in UK Pounds in 1 month1 month. Forward . Forward exchange rate is 2.00$/Pound. exchange rate is 2.00$/Pound. Using Table 8-1, What will be the Using Table 8-1, What will be the exchange risk?exchange risk? 2.00 $/Pound X 400 Pound = $8002.00 $/Pound X 400 Pound = $800 Monthly Un-annualized SD = 2.66Monthly Un-annualized SD = 2.66 SD = 800 X 2.66% = $21,28SD = 800 X 2.66% = $21,28 68% Probability Manny will receive 68% Probability Manny will receive

between $778.72 and $821.28between $778.72 and $821.28

Ex Risk with Multiple CurrenciesEx Risk with Multiple Currencies

More Currencies = more complexMore Currencies = more complex

Exposures and risks cannot simply Exposures and risks cannot simply be added togetherbe added together

Must Consider correlation of Must Consider correlation of movements in relation to home movements in relation to home currencycurrency

CalculationCalculation

Risk = Sum of exchange Variances + Risk = Sum of exchange Variances + Sum of Covariance of particular Sum of Covariance of particular currenciescurrencies

Example: Example: Variance of annual percentage changes in Variance of annual percentage changes in

$/Yen is 600 percentage points, and $/Yen is 600 percentage points, and Variance of $/DM is 500 percentage points. Variance of $/DM is 500 percentage points. From Table 8-2, correlation is 0.624 and the From Table 8-2, correlation is 0.624 and the covariance is 346.5. What is the exchange covariance is 346.5. What is the exchange risk associated with $100 of Yen and $100 risk associated with $100 of Yen and $100 of DM?of DM?

Calculations cont.Calculations cont.

100^2Var(Ry) + 100^2Var(Rdm) + 100^2Var(Ry) + 100^2Var(Rdm) + 2(100^2)Cov(Ry,Rdm)2(100^2)Cov(Ry,Rdm)

Var = 100^2(600+500+2(346.5)) = 100^2*1793Var = 100^2(600+500+2(346.5)) = 100^2*1793

SD = Square Root of 100^2*1793 = 4234 SD = Square Root of 100^2*1793 = 4234 cents or $42.34cents or $42.34

Review Problem 2Review Problem 2

Suppose Sweta has $100 worth of Suppose Sweta has $100 worth of accounts payable in C$ and $100 worth accounts payable in C$ and $100 worth of accounts payable in A$, both due in of accounts payable in A$, both due in 90 days, and want to know the SD of 90 days, and want to know the SD of the portfolio of payables.the portfolio of payables.

She knows that the 90 day $/C$ % She knows that the 90 day $/C$ % change is 8, the $/A$ % change is 20, change is 8, the $/A$ % change is 20, and the correlation between the two and the correlation between the two is .35is .35

What is SD of her portfolio?What is SD of her portfolio?

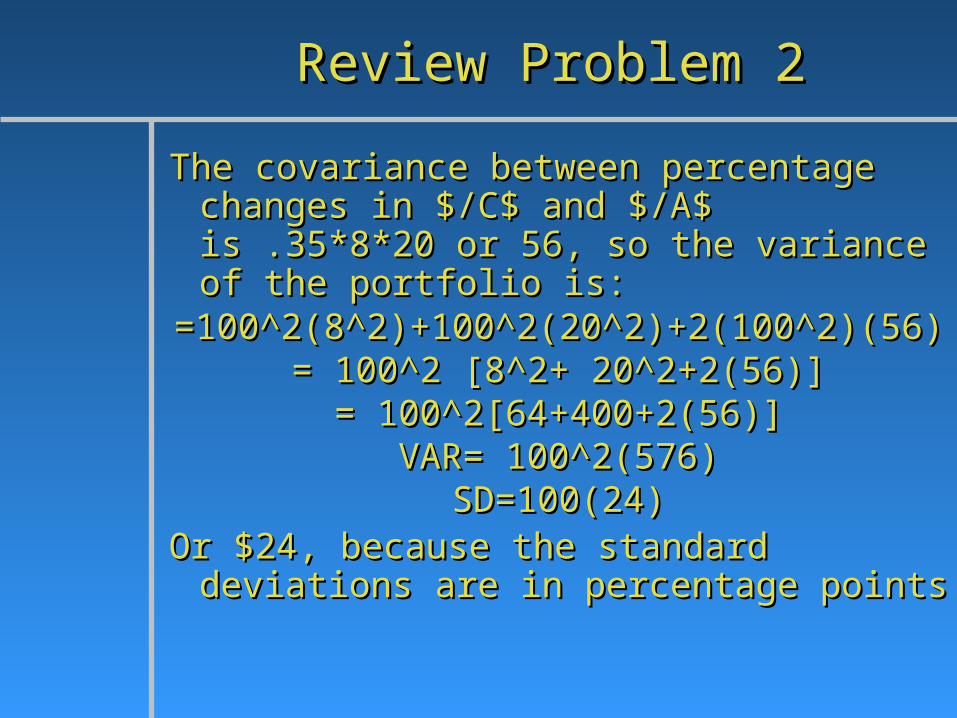

Review Problem 2Review Problem 2

The covariance between percentage The covariance between percentage changes in $/C$ and $/A$ is .35*8*20 or changes in $/C$ and $/A$ is .35*8*20 or 56, so the variance of the portfolio is:56, so the variance of the portfolio is:

=100^2(8^2)+100^2(20^2)+2(100^2)(56)=100^2(8^2)+100^2(20^2)+2(100^2)(56)= 100^2 [8^2+ 20^2+2(56)]= 100^2 [8^2+ 20^2+2(56)]

= 100^2[64+400+2(56)]= 100^2[64+400+2(56)]VAR= 100^2(576)VAR= 100^2(576)

SD=100(24)SD=100(24)Or $24, because the standard deviations Or $24, because the standard deviations

are in percentage pointsare in percentage points

Delta hedgingDelta hedging

The process in finance of setting or The process in finance of setting or keeping the delta of a portfolio of keeping the delta of a portfolio of financial instruments zero, or as close financial instruments zero, or as close to zero as possible - where delta is the to zero as possible - where delta is the sensitivitysensitivity of the value of a derivative to of the value of a derivative to changes in the price of its underlying changes in the price of its underlying instrument. instrument.

This is achieved by entering into positions This is achieved by entering into positions with offsetting positive and negative with offsetting positive and negative deltas such that these balance out to deltas such that these balance out to bring the net delta to zero bring the net delta to zero

Mathematically Mathematically

Delta is the partial derivative of the Delta is the partial derivative of the instrument or portfolio's fair value with instrument or portfolio's fair value with respect to the price of the underlying respect to the price of the underlying security , and indicates sensitivity to the security , and indicates sensitivity to the price of the underlying. Therefore, if a price of the underlying. Therefore, if a position is delta neutral (or, position is delta neutral (or, instantaneously delta-hedged) its instantaneously delta-hedged) its instantaneous change in value, for an instantaneous change in value, for an infinitesimal change in the value of the infinitesimal change in the value of the underlying, will be zero underlying, will be zero

Any Questions?Any Questions?