Embed Size (px)

Citation preview

Scotia INNOVA Portfolios® 2013Simplified ProspectusNovember 8, 2013

Scotia INNOVA Income Portfolio (Series A and Series T units)

Scotia INNOVA Balanced Income Portfolio (Series A and Series T units)

Scotia INNOVA Balanced Growth Portfolio (Series A and Series T units)

Scotia INNOVA Growth Portfolio (Series A units)

Scotia INNOVA Maximum Growth Portfolio (Series A units)

No securities regulatory authority has expressed an opinion about theseunits. It is an offence to claim otherwise.

The Portfolios and the units they offer under this simplified prospectus arenot registered with the U.S. Securities and Exchange Commission. Units ofthe Portfolios may be offered and sold in the United States only in relianceon exemptions from registration.

Table of contentsIntroduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iFund specific information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1Scotia INNOVA Income Portfolio . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4Scotia INNOVA Balanced Income Portfolio . . . . . . . . . . . . . . . . . . . . . 6Scotia INNOVA Balanced Growth Portfolio . . . . . . . . . . . . . . . . . . . . 8Scotia INNOVA Growth Portfolio . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10Scotia INNOVA Maximum Growth Portfolio . . . . . . . . . . . . . . . . . . . 12

What is a mutual fund and what are the risks ofinvesting in a mutual fund? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Organization and management of the Scotia INNOVAPortfolios . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Purchases, switches and redemptions . . . . . . . . . . . . . . . . . . . . . 21Optional services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24Fees and expenses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25Impact of sales charges . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26Dealer compensation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26Income tax considerations for investors . . . . . . . . . . . . . . . . . . . 27What are your legal rights? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

Introduction

In this document, portfolio or Portfolio means a mutual fund thatis offered for sale under this simplified prospectus; Manager, we,us, and our refer to 1832 Asset Management L.P. (formerly ScotiaAsset Management L.P.); Scotiabank includes The Bank of NovaScotia (Scotiabank) and its affiliates, including The Bank ofNova Scotia Trust Company (Scotiatrust), 1832 Asset Manage-ment L.P., Scotia Securities Inc. and Scotia Capital Inc.(including ScotiaMcLeod® and Scotia iTRADE®, each a divisionof Scotia Capital Inc.); ScotiaFunds refers to all of our mutualfunds and the series thereof which are offered under separatesimplified prospectuses under the ScotiaFunds® brand andincludes the Scotia mutual funds offered under this simplifiedprospectus; Tax Act means the Income Tax Act (Canada); andunderlying fund refers to a mutual fund (either a ScotiaFund orother mutual fund) in which a fund invests.

This simplified prospectus contains selected important informationto help you make an informed investment decision about thePortfolios and to understand your rights as an investor. It’s dividedinto two parts. The first part, from pages 1to 13 contains specificinformation about each of the Portfolios offered for sale under thissimplified prospectus. The second part, from pages 14 to 28 con-tains general information that applies to all of the Portfoliosoffered for sale under this simplified prospectus and the risks ofinvesting in mutual funds generally, as well as the names of thefirms responsible for the management of the Portfolios.

Additional information about the Portfolios is available in theirannual information form, their most recently filed Fund Facts,their most recently filed annual and interim financial statementsand their most recently filed annual and interim managementreports of fund performance. These documents are incorporatedby reference into this simplified prospectus. That means theylegally form part of this simplified prospectus just as if they wereprinted in it.

You can get a copy of the Portfolios’ annual information form,their most recently filed Fund Facts, financial statements andmanagement reports of fund performance at no charge by calling1-800-268-9269 (416-750-3863 in Toronto) for English, or1-800-387-5004 for French, or by asking your mutual fund repre-sentative.

These documents and other information about the Portfolios arealso available at www.scotiafunds.com.

i

Fund specific information

The portfolios offered under this simplified prospectus are part ofthe ScotiaFunds family of funds. ScotiaFunds offer a number ofseries of units. The portfolios offer one or more of Series A andSeries T units.

The Scotia INNOVA Portfolios are a family of 5 mutual funds pro-viding investors with professionally managed solutions designedto suit their investment profile. Each of the Scotia INNOVAPortfolios may invest in a mix of other mutual funds, each ofwhich follow a different investment objective and strategy. In thealternative, in addition to investing in mutual funds a Portfoliomay also choose to obtain exposure to a particular investmentstrategy by investing directly in equity securities and fixedincome securities. Each Portfolio will follow a strategic assetallocation investment strategy.

All of the Scotia INNOVA Portfolios offered for sale under thissimplified prospectus offer Series A units and some of the ScotiaINNOVA Portfolios also offer Series T units. Series A units andSeries T units are available to all investors. Series T units areintended for investors seeking stable monthly distributions.Monthly distributions on Series T units of a Portfolio may consistof net income, net realized capital gains and/or a return of capi-tal. Any net income and net realized capital gains in excess of themonthly distributions will be distributed annually at the end ofeach year. You’ll find more information about the different Seriesof units under the heading About the Series A and Series T units.

The Scotia INNOVA Portfolios give you:

• strategic asset allocation

• market capitalization diversification

• geographic diversification

• portfolio advisor style diversification

• ongoing oversight of the asset mix, fund selection andindividual security selection

• ongoing portfolio rebalancing to ensure that the appropriatelong-term asset mix is maintained.

The selection of investments for the Scotia INNOVA Portfolios issubject to a multi-step investment process. Prior to including anunderlying fund in, or removing an underlying fund from, theScotia INNOVA Portfolios, we conduct a thorough review ofappropriate underlying funds and determine if the Portfolio willinvest in an underlying fund or if the Portfolio will invest directlyin the securities held by an underlying fund.

When determining whether to include a particular underlyingfund or investment, we consider the asset mix of each of the

Scotia INNOVA Portfolios which are designed for different typesof investors with unique risk/reward profiles.

Each Scotia INNOVA Portfolio is diversified by asset class, capital-ization, geography and investment style. We monitor the under-lying funds in which the Portfolios invest regularly and considerthe underlying funds’ quantitative and qualitative attributes, andthe diversification benefits that they bring to each of the ScotiaINNOVA Portfolios. When deciding to invest in an underlyingfund, we may consider a variety of criteria, including manage-ment style, investment performance and consistency, risk attrib-utes and the quality of the fund’s manager or portfolio advisor.

About the Portfolio descriptions

On the following pages, you’ll find detailed descriptions of each ofthe Portfolios to help you make your investment decisions. Here’swhat each section of the Portfolio descriptions tells you:

Portfolio details

This section gives you some basic information about each Portfo-lio, such as its start date and its eligibility for registered plans,including Registered Retirement Savings Plans (“RRSPs”), Regis-tered Retirement Income Funds (“RRIFs”), Registered EducationSavings Plans (“RESPs”), Registered Disability Savings Plans(“RDSPs”), Life Income Funds (“LIFs”), Locked-in RetirementIncome Funds (“LRIFs”), Locked-in Retirement Savings Plans(“LRSPs”), Prescribed Retirement Income Funds (“PRIFs”) andTax-Free Savings Accounts (“TFSAs”).

All of the Portfolios offered under this simplified prospectus are,or are expected to be, qualified investments under the Tax Act forregistered plans. In certain cases, we may restrict purchases ofunits of certain Portfolios by certain registered plans.

What does the portfolio invest in?

This section tells you the Portfolio’s fundamental investmentobjectives and the strategies it uses in trying to achieve thoseobjectives. Any change to the fundamental investment objectivesmust be approved by a majority of votes cast at a meeting of unit-holders called for that purpose.

About derivatives

Derivatives are investments that derive their value from the priceof another investment or from anticipated movements in interestrates, currency exchange rates or market indexes. Derivatives areusually contracts with another party to buy or sell an asset at a

1

later time and at a set price. Examples of derivatives are options,forward contracts, futures contracts and swaps.

• Options generally give holders the right, but not the obligation,to buy or sell an asset, such as a security or currency, at a setprice and a set time. Option holders normally pay the otherparty a cash payment, called a premium, for agreeing to givethem the option.

• Forward contracts are agreements to buy or sell an asset, suchas a security or currency, at a set price and a set time. Theparties have to complete the deal, or sometimes make orreceive a cash payment, even if the price has changed by thetime the deal closes. Forward contracts are generally nottraded on organized exchanges and are not subject to stand-ardized terms and conditions.

• Futures contracts, like a forward contract, are agreements tobuy or sell an asset, such as a security or currency, at a setprice and a set time. The parties have to complete the deal, orsometimes make or receive a cash payment, even if the pricehas changed by the time the deal closes. Futures contracts arenormally traded on a registered futures exchange. Theexchange usually specifies certain standardized terms andconditions.

• Swaps are agreements between two or more parties toexchange principal amounts or payments based on returns ondifferent investments. Swaps are not traded on organizedexchanges and are not subject to standardized terms and con-ditions.

A Portfolio can use derivatives as long as it uses them in a waythat’s consistent with the Portfolio’s investment objectives andwith Canadian securities regulations. All of the Portfolios may usederivatives to hedge their investments against losses fromchanges in currency exchange rates, interest rates and stockmarket prices. Some of the Portfolios may also use derivatives togain exposure to financial markets or to invest indirectly in secu-rities or other assets. This can be less expensive than buyingsecurities or assets directly.

When a portfolio uses derivatives for purposes other than hedg-ing, it holds enough cash or money market instruments to fullycover its positions, as required by securities regulations.

Investing in other mutual funds

Some of the portfolios may, from time to time, invest some or allof their assets in other mutual funds (“underlying funds”) thatare managed by us or one of our affiliates or associates, includingother ScotiaFunds, or by third party investment managers. Whendeciding to invest in other mutual funds, the portfolio advisormay consider a variety of criteria, including management style,investment performance and consistency, risk attributes and thequality of the underlying fund’s manager or portfolio advisor.

Portfolios that engage in repurchase and reverserepurchase transactions

The Portfolios may enter into repurchase or reverse repurchaseagreements to generate additional income from securities held ina Portfolio. When a mutual fund agrees to sell a security at oneprice and buy it back on a specified later date (usually at a lowerprice), it is entering into a repurchase transaction. When amutual fund agrees to buy a security at one price and sell it backon a specified later date (usually at a higher price), it is enteringinto a reverse repurchase transaction. For a description of thestrategies the Portfolios use to minimize the risks associated withthese transactions, see the discussion under Repurchase andreverse repurchase transaction risk.

Portfolios that lend their securities

The Portfolios may enter into securities lending transactions togenerate additional income from securities held in the Portfolio.A mutual fund may lend securities held in its portfolio to quali-fied borrowers who provide adequate collateral. For a descriptionof the strategies the Portfolios use to minimize the risks asso-ciated with these transactions, see the discussion under Secu-rities lending risk.

Funds that engage in short selling

Mutual funds may be permitted to engage in a limited amount ofshort selling under securities regulations. A “short sale” is wherea fund borrows securities from a lender which are then sold inthe open market (or “sold short”). At a later date, the samenumber of securities are repurchased by the fund and returned tothe lender. In the interim, the proceeds from the first sale aredeposited with the lender and the mutual fund pays interest tothe lender. If the value of the securities declines between thetime that the fund borrows the securities and the time itrepurchases and returns the securities, the fund makes a profitfor the difference (less any interest the fund is required to pay tothe lender). In this way, the mutual fund has more opportunitiesfor gains when markets are generally volatile or declining.

What are the risks of investing in the portfolio?

This section tells you the risks of investing in the Portfolio. You’llfind a description of each risk in Specific risks of mutual funds.

Investment risk classification methodology

A risk classification rating is assigned to each Portfolio to provideyou with information to help you determine whether the Portfoliois appropriate for you. Each Portfolio is assigned a risk rating inone of the following categories: low, low to medium, medium,medium to high or high.

2

The investment risk rating for each Portfolio is reviewed at leastannually as well as if there is a material change in a fund’sinvestment objective or investment strategies.

The methodology used to determine the risk ratings of the Portfo-lio for purposes of disclosure in this simplified prospectus isbased on a combination of the qualitative aspects of the method-ology recommended by the Fund Risk Classification Task Force ofthe Investment Fund Institute of Canada and the Manager’squantitative analysis of a Portfolio’s historic volatility. TheManager takes into account other qualitative factors in makingits final determination of each Portfolio’s risk rating. In partic-ular, the standard deviation of each Portfolio is reviewed. Stan-dard deviation is a common statistic used to measure thevolatility of an investment. Portfolios with higher standard devia-tions are generally classified as being more risky. Qualitativefactors taken into account include key investment policy guide-lines which may include but are not limited to regional, sectoraland market capitalization restrictions as well as asset allocationpolicies.

The Manager recognizes that other types of risk, both measurableand non-measurable, may exist and that historical performancemay not be indicative of future returns and a fund’s historic vola-tility may not be indicative of its future volatility.

The methodology that the Manager uses to identify the invest-ment risk level of the Portfolios is available on request at no costby contacting us toll free at 1-800-268-9269 (416-750-3863 inToronto) for English or 1-800-387-5004 for French or by email [email protected] or by writing to us at the address onthe back cover of this simplified prospectus.

Who should invest in this portfolio?

This section can help you decide if the Portfolio might be suitablefor your investment portfolio. It’s meant as a general guide only.For advice about your investment portfolio, you should consultyour mutual fund representative. If you don’t have a mutual fundrepresentative, you can speak with one of our representatives atany Scotiabank branch or by calling a Scotia Securities Inc.office.

Distribution policy

This tells you when the Portfolio usually distributes any netincome and capital gains, and where applicable, returns of capi-tal, to unitholders. The Portfolios may also make distributions atother times.

Distributions on units held in registered plans and non-registeredaccounts are reinvested in additional units of the Portfolio,unless you tell your mutual fund representative that you want toreceive cash distributions. For information about how dis-tributions are taxed, see Income tax considerations for investors.

Portfolio expenses indirectly borne by investors

This is an example of how much a Portfolio might pay inexpenses. It is intended to help you compare the cost of investingin a Portfolio with the cost of investing in other mutual funds.Each Portfolio pays it owns expenses, but they affect you becausethey reduce the Portfolio’s returns.

The table shows how much the Portfolio would pay in expenseson a $1,000 investment with a 5% annual return. The informationin the tables assumes that the Portfolio’s management expenseratio (MER) was the same throughout each period shown as itwas during its last completed financial year. You’ll find moreinformation about fees and expenses in Fees and expenses.

3

SC

OT

IAIN

NO

VA

INC

OM

EP

OR

TF

OL

IO

Scotia INNOVA Income PortfolioFund details

Fund type Canadian fixed income balanced fund

Start date Series A units: January 19, 2009Series T units: January 11, 2010

Type of securities Series A units and Series T units of amutual fund trust

Eligible forregistered plans?

Yes

Portfolio advisor The Manager Toronto, Ontario

Sub-Advisor Aurion Capital Management Inc.Toronto, Ontario

What does the fund invest in?

Investment objectives

The Portfolio’s objective is to achieve a balance of currentincome and long term capital appreciation, with a significantbias towards income. It invests primarily in a diversified mixof mutual funds, and/or equity securities and/or fixed incomesecurities located anywhere in the world.

Any change to the fundamental investment objectives mustbe approved by a majority of votes cast at a meeting of unit-holders for that purpose.

Investment strategies

The Portfolio is an asset allocation fund that allocates yourinvestment between two asset classes: fixed income andequities.

The table below outlines the target weighting for each assetclass in which the Portfolio invests.

Asset ClassTarget

Weighting

Fixed Income 75%

Equities 25%

The underlying funds, equity securities and fixed incomesecurities in which the Portfolio invests may change fromtime to time, but in general we will keep the target weightingfor each asset class no more than 10% above or below theamounts set out above. You’ll find more information oninvesting in underlying funds in Investing in other mutualfunds. Although up to 100% of the Portfolio’s assets may beinvested in underlying funds, once the Portfolio reaches asufficient size, the portfolio advisor and/or the sub-advisormay determine that it is more efficient to invest the Portfoliodirectly in securities in one or more asset classes.

The portfolio advisor and/or the sub-advisor may usederivatives such as options, futures, forward contracts andswaps to hedge against losses from changes in stock prices,commodity prices, market indexes or currency exchangerates and to gain exposure to financial markets. It will onlyuse derivatives as permitted by securities regulations.

The portfolio can invest up to 40% of its assets in foreignsecurities.

The portfolio and an underlying fund managed by us mayalso engage in short selling on the conditions permitted byCanadian securities rules. In determining whether securitiesof a particular issuer should be sold short, the portfolio advi-sor utilizes the same analysis that is described above fordeciding whether to purchase the securities. Where theanalysis generally produces a favourable outlook, the issueris a candidate for purchase. Where the analysis produces anunfavourable outlook, the issuer is a candidate for a shortsale. For a more detailed description of short selling and thelimits within which the underlying fund may engage in shortselling, please refer to What are the risks? – Short sellingrisk.

What are the risks of investing in the fund?

To the extent that the Portfolio invests in underlying funds,it indirectly has the same risks as the underlying funds itholds. The Portfolio takes on the risks of an underlying fundin proportion to its investment in that fund. To the extent itinvests directly in equity and fixed income securities, thePortfolio will have the risks associated with investingdirectly in such equity and fixed income securities.

The risks applicable to the Portfolio include:

• asset-backed and mortgage-backed securities risk

• commodity risk

• credit risk

• currency risk

• derivatives risk

• emerging markets risk

• equity risk

• foreign investment risk

• fund-of-funds risk

• income trust risk

• interest rate risk

4

• issuer-specific risk

• liquidity risk

• repurchase and reverse repurchase transaction risk

• securities lending risk

• series risk

• short selling risk

• small company risk

• U.S. withholding tax risk.

You’ll find details about each of these risks under What is amutual fund and what are the risks of investing in amutual fund?

During the 12 months preceding October 11, 2013, up to30.0% of the net assets of the portfolio were invested in Sco-tia Canadian Income Fund Series I, up to 17.1% of the netassets of the portfolio were invested in Scotia Private Short-Mid Government Bond Pool Series I, and up to 11.0% of thenet assets of the portfolio were invested in Scotia PrivateCanadian Corporate Bond Pool Series I.

Who should invest in this fund?

This Portfolio may be suitable for you if:

• you want a balanced holding with a significant biastowards income, which is diversified by asset class,investment style, geography and market capitalization

• you can accept low to medium risk

• you’re investing for the medium to long term.

Please see Investment Risk Classification Methodology for adescription of how we determined the classification of thisPortfolio’s risk level.

Distribution policy

For Series A units, the Portfolio distributes any net incomeand net realized capital gains by the end of December ofeach calendar year.

Investors holding Series T units will receive stable monthlydistributions consisting of net income, net realized capitalgains and/or, a return of capital. The dollar amount of yourmonthly distribution is reset at the beginning of each calen-dar year. The distribution amount will be a factor of thepayout rate for Series T units (which is expected to remainat or about 3%), of the average daily net asset value per unitof the Series T units during the previous calendar year, and

the number of Series T units of the Portfolio you own at thetime of the distribution.

The payout rate for Series T units of the Portfolio may beadjusted in the future, if we determine that conditionsrequire an adjustment of distributions or that payment of adistribution would have a negative effect on the investors inthe Portfolio. Distributions by this Portfolio are not guaran-teed to occur on a specific date and neither we nor the Port-folio is responsible for any fees or charges incurred by youbecause the Portfolio did not effect a distribution on aparticular day.

Investors should not confuse the cash flow distribution withthe portfolio’s rate of return or yield.

The payout rate on Series T units of the Portfolio may begreater than the return on the Portfolio’s investments. Aportion of the distribution for Series T units is expected toconsist of a return of capital, which is not taxable in the yearreceived. Please see Income Tax Considerations for Invest-ors for more details.

The Portfolio will distribute any excess net income and netrealized capital gains annually in December.

Distributions on units held in registered plans andnon-registered accounts are reinvested in additional units ofthe Portfolio, unless you tell your dealer that you want toreceive cash distributions.

Fund expenses indirectly borne by investors

This example shows the Portfolio’s expenses on a $1,000investment with a 5% annual return.

Fees and expensespayable over 1 year 3 years 5 years 10 years

Series A units $ 18.76 59.13 103.65 235.93

Series T units $ 18.76 59.13 103.65 235.93S

CO

TIA

INN

OV

AIN

CO

ME

PO

RT

FO

LIO

5

SC

OT

IAIN

NO

VA

BA

LA

NC

ED

INC

OM

EP

OR

TF

OL

IO

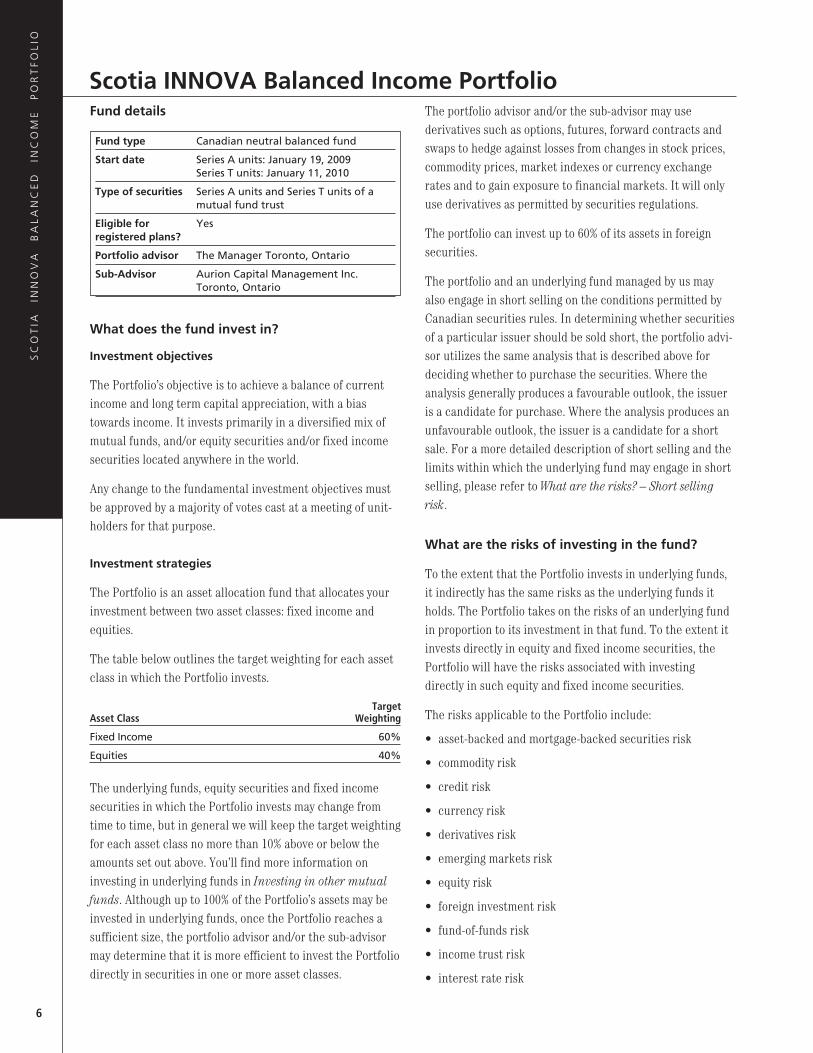

Scotia INNOVA Balanced Income PortfolioFund details

Fund type Canadian neutral balanced fund

Start date Series A units: January 19, 2009Series T units: January 11, 2010

Type of securities Series A units and Series T units of amutual fund trust

Eligible forregistered plans?

Yes

Portfolio advisor The Manager Toronto, Ontario

Sub-Advisor Aurion Capital Management Inc.Toronto, Ontario

What does the fund invest in?

Investment objectives

The Portfolio’s objective is to achieve a balance of currentincome and long term capital appreciation, with a biastowards income. It invests primarily in a diversified mix ofmutual funds, and/or equity securities and/or fixed incomesecurities located anywhere in the world.

Any change to the fundamental investment objectives mustbe approved by a majority of votes cast at a meeting of unit-holders for that purpose.

Investment strategies

The Portfolio is an asset allocation fund that allocates yourinvestment between two asset classes: fixed income andequities.

The table below outlines the target weighting for each assetclass in which the Portfolio invests.

Asset ClassTarget

Weighting

Fixed Income 60%

Equities 40%

The underlying funds, equity securities and fixed incomesecurities in which the Portfolio invests may change fromtime to time, but in general we will keep the target weightingfor each asset class no more than 10% above or below theamounts set out above. You’ll find more information oninvesting in underlying funds in Investing in other mutualfunds. Although up to 100% of the Portfolio’s assets may beinvested in underlying funds, once the Portfolio reaches asufficient size, the portfolio advisor and/or the sub-advisormay determine that it is more efficient to invest the Portfoliodirectly in securities in one or more asset classes.

The portfolio advisor and/or the sub-advisor may usederivatives such as options, futures, forward contracts andswaps to hedge against losses from changes in stock prices,commodity prices, market indexes or currency exchangerates and to gain exposure to financial markets. It will onlyuse derivatives as permitted by securities regulations.

The portfolio can invest up to 60% of its assets in foreignsecurities.

The portfolio and an underlying fund managed by us mayalso engage in short selling on the conditions permitted byCanadian securities rules. In determining whether securitiesof a particular issuer should be sold short, the portfolio advi-sor utilizes the same analysis that is described above fordeciding whether to purchase the securities. Where theanalysis generally produces a favourable outlook, the issueris a candidate for purchase. Where the analysis produces anunfavourable outlook, the issuer is a candidate for a shortsale. For a more detailed description of short selling and thelimits within which the underlying fund may engage in shortselling, please refer to What are the risks? – Short sellingrisk.

What are the risks of investing in the fund?

To the extent that the Portfolio invests in underlying funds,it indirectly has the same risks as the underlying funds itholds. The Portfolio takes on the risks of an underlying fundin proportion to its investment in that fund. To the extent itinvests directly in equity and fixed income securities, thePortfolio will have the risks associated with investingdirectly in such equity and fixed income securities.

The risks applicable to the Portfolio include:

• asset-backed and mortgage-backed securities risk

• commodity risk

• credit risk

• currency risk

• derivatives risk

• emerging markets risk

• equity risk

• foreign investment risk

• fund-of-funds risk

• income trust risk

• interest rate risk

6

• issuer-specific risk

• liquidity risk

• repurchase and reverse repurchase transaction risk

• securities lending risk

• series risk

• short selling risk

• small company risk

• U.S. withholding tax risk.

You’ll find details about each of these risks under What is amutual fund and what are the risks of investing in amutual fund?

During the 12 months preceding October 11, 2013, up to29.9% of the net assets of the portfolio were invested in Sco-tia Canadian Income Fund Series I, and up to 10.4% of thenet assets of the portfolio were invested in Scotia CanadianDividend Fund Series I.

Who should invest in this fund?

This Portfolio may be suitable for you if:

• you want a balanced holding with a bias towards income,which is diversified by asset class, investment style, geog-raphy and market capitalization

• you can accept low to medium risk

• you’re investing for the medium to long term.

Please see Investment Risk Classification Methodology for adescription of how we determined the classification of thisPortfolio’s risk level.

Distribution policy

For Series A units, the Portfolio distributes any net incomeand net realized capital gains by the end of December ofeach calendar year.

Investors holding Series T units will receive stable monthlydistributions consisting of net income, net realized capitalgains and/or, a return of capital. The dollar amount of yourmonthly distribution is reset at the beginning of each calen-dar year. The distribution amount will be a factor of thepayout rate for Series T units (which is expected to remainat or about 4%), of the average daily net asset value per unitof the Series T units during the previous calendar year, andthe number of Series T units of the Portfolio you own at thetime of the distribution.

The payout rate for Series T units of the Portfolio may beadjusted in the future, if we determine that conditionsrequire an adjustment of distributions or that payment of adistribution would have a negative effect on the investors inthe Portfolio. Distributions by this Portfolio are not guaran-teed to occur on a specific date and neither we nor the Port-folio is responsible for any fees or charges incurred by youbecause the Portfolio did not effect a distribution on aparticular day.

Investors should not confuse the cash flow distribution withthe portfolio’s rate of return or yield.

The payout rate on Series T units of the Portfolio may begreater than the return on the Portfolio’s investments. Aportion of the distribution for Series T units is expected toconsist of a return of capital, which is not taxable in the yearreceived. Please see Income Tax Considerations for Investorsfor more details.

The Portfolio will distribute any excess net income and netrealized capital gains annually in December.

Distributions on units held in registered plans andnon-registered accounts are reinvested in additional units ofthe Portfolio, unless you tell your dealer that you want toreceive cash distributions.

Fund expenses indirectly borne by investors

This example shows the Portfolio’s expenses on a $1,000investment with a 5% annual return

Fees and expensespayable over 1 year 3 years 5 years 10 years

Series A units $ 19.68 62.04 108.74 247.53

Series T units $ 19.68 62.04 108.74 247.53

SC

OT

IAIN

NO

VA

BA

LA

NC

ED

INC

OM

EP

OR

TF

OL

IO

7

SC

OT

IAIN

NO

VA

BA

LA

NC

ED

GR

OW

TH

PO

RT

FO

LIO

Scotia INNOVA Balanced Growth PortfolioFund details

Fund type Global neutral balanced fund

Start date Series A units: January 19, 2009Series T units: January 11, 2010

Type of securities Series A units and Series T units of amutual fund trust

Eligible forregistered plans?

Yes

Portfolio advisor The Manager Toronto, Ontario

What does the fund invest in?

Investment objectives

The Portfolio’s objective is to achieve a balance of currentincome and long term capital appreciation, with a biastowards capital appreciation. It invests primarily in adiversified mix of mutual funds, and/or equity securities and/or fixed income securities located anywhere in the world.

Any change to the fundamental investment objectives mustbe approved by a majority of votes cast at a meeting of unit-holders for that purpose.

Investment strategies

The Portfolio is an asset allocation fund that allocates yourinvestment between two asset classes: fixed income andequities.

The table below outlines the target weighting for each assetclass in which the Portfolio invests.

Asset ClassTarget

Weighting

Fixed Income 40%

Equities 60%

The underlying funds, equity securities and fixed incomesecurities in which the Portfolio invests may change fromtime to time, but in general we will keep the target weightingfor each asset class no more than 10% above or below theamounts set out above. You’ll find more information oninvesting in underlying funds in Investing in other mutualfunds. Although up to 100% of the Portfolio’s assets may beinvested in underlying funds, once the Portfolio reaches asufficient size, the portfolio advisor may determine that it ismore efficient to invest the Portfolio directly in securities inone or more asset classes.

The portfolio advisor may use derivatives such as options,futures, forward contracts and swaps to hedge against lossesfrom changes in stock prices, commodity prices, marketindexes or currency exchange rates and to gain exposure tofinancial markets. It will only use derivatives as permitted bysecurities regulations.

The portfolio can invest up to 80% of its assets in foreignsecurities.

The portfolio and an underlying fund managed by us mayalso engage in short selling on the conditions permitted byCanadian securities rules. In determining whether securitiesof a particular issuer should be sold short, the portfolio advi-sor utilizes the same analysis that is described above fordeciding whether to purchase the securities. Where theanalysis generally produces a favourable outlook, the issueris a candidate for purchase. Where the analysis produces anunfavourable outlook, the issuer is a candidate for a shortsale. For a more detailed description of short selling and thelimits within which the underlying fund may engage in shortselling, please refer to What are the risks? – Short sellingrisk.

What are the risks of investing in the fund?

To the extent that the Portfolio invests in underlying funds,it indirectly has the same risks as the underlying funds itholds. The Portfolio takes on the risks of an underlying fundin proportion to its investment in that fund. To the extent itinvests directly in equity and fixed income securities, thePortfolio will have the risks associated with investingdirectly in such equity and fixed income securities.

The risks applicable to the Portfolio include:

• asset-backed and mortgage-backed securities risk

• commodity risk

• credit risk

• currency risk

• derivatives risk

• emerging markets risk

• equity risk

• foreign investment risk

• fund-of-funds risk

• income trust risk

8

• interest rate risk

• issuer-specific risk

• liquidity risk

• repurchase and reverse repurchase transaction risk

• securities lending risk

• series risk

• short selling risk

• small company risk

• U.S. withholding tax risk.

You’ll find details about each of these risks under What is amutual fund and what are the risks of investing in a mutualfund?

During the 12 months preceding October 11, 2013, up to27.0% of the net assets of the portfolio were invested in Sco-tia Canadian Income Fund Series I, up to 12.4% of the netassets of the portfolio were invested in Scotia CanadianDividend Fund Series I, and up to 11.7% of the net assets ofthe portfolio were invested in Scotia Private InternationalEquity Pool Series I.

Who should invest in this fund?

This Portfolio may be suitable for you if:

• you want a balanced holding with a bias towards equity,which is diversified by asset class, investment style, geog-raphy and market capitalization

• you can accept medium risk

• you’re investing for the medium to long term.

Please see Investment Risk Classification Methodology for adescription of how we determined the classification of thisPortfolio’s risk level.

Distribution policy

For Series A units, the Portfolio distributes any net incomeand net realized capital gains by the end of December ofeach calendar year.

Investors holding Series T units will receive stable monthlydistributions consisting of net income, net realized capitalgains and/or, a return of capital. The dollar amount of yourmonthly distribution is reset at the beginning of each calen-dar year. The distribution amount will be a factor of thepayout rate for Series T units (which is expected to remainat or about 5%), of the average daily net asset value per unit

of the Series T units during the previous calendar year, andthe number of Series T units of the Portfolio you own at thetime of the distribution.

The payout rate for Series T units of the Portfolio may beadjusted in the future, if we determine that conditionsrequire an adjustment of distributions or that payment of adistribution would have a negative effect on the investors inthe Portfolio. Distributions by this Portfolio are not guaran-teed to occur on a specific date and neither we nor the Port-folio is responsible for any fees or charges incurred by youbecause the Portfolio did not effect a distribution on aparticular day.

Investors should not confuse the cash flow distribution withthe portfolio’s rate of return or yield.

The payout rate on Series T units of the Portfolio may begreater than the return on the Portfolio’s investments. Aportion of the distribution for Series T units is expected toconsist of a return of capital, which is not taxable in the yearreceived. Please see Income Tax Considerations for Investorsfor more details.

The Portfolio will distribute any excess net income and netrealized capital gains annually in December.

Distributions on units held in registered plans andnon-registered accounts are reinvested in additional units ofthe Portfolio, unless you tell your dealer that you want toreceive cash distributions.

Fund expenses indirectly borne by investors

This example shows the Portfolio’s expenses on a $1,000investment with a 5% annual return.

Fees and expensespayable over 1 year 3 years 5 years 10 years

Series A units $ 21.12 66.57 116.67 265.58

Series T units $ 21.22 66.89 117.24 266.87S

CO

TIA

INN

OV

AB

AL

AN

CE

DG

RO

WT

HP

OR

TF

OL

IO

9

SC

OT

IAIN

NO

VA

GR

OW

TH

PO

RT

FO

LIO

Scotia INNOVA Growth PortfolioFund details

Fund type Global equity balanced fund

Start date Series A units: January 19, 2009

Type of securities Series A units of a mutual fund trust

Eligible forregistered plans?

Yes

Portfolio advisor The Manager Toronto, Ontario

What does the fund invest in?

Investment objectives

The Portfolio’s objective is to achieve a balance of long termcapital appreciation and current income, with a significantbias towards capital appreciation. It invests primarily in adiversified mix of mutual funds, and/or equity securities and/or fixed income securities located anywhere in the world.

Any change to the fundamental investment objectives mustbe approved by a majority of votes cast at a meeting of unit-holders for that purpose.

Investment strategies

The Portfolio is an asset allocation fund that allocates yourinvestment between two asset classes: fixed income andequities.

The table below outlines the target weighting for each assetclass in which the Portfolio invests.

Asset ClassTarget

Weighting

Fixed Income 25%

Equities 75%

The underlying funds, equity securities and fixed incomesecurities in which the Portfolio invests may change fromtime to time, but in general we will keep the target weightingfor each asset class no more than 10% above or below theamounts set out above. You’ll find more information oninvesting in underlying funds in Investing in other mutualfunds. Although up to 100% of the Portfolio’s assets may beinvested in underlying funds, once the Portfolio reaches asufficient size the portfolio advisor may determine that it ismore efficient to invest the Portfolio directly in securities inone or more asset classes.

The portfolio advisor may use derivatives such as options,futures, forward contracts and swaps to hedge against lossesfrom changes in stock prices, commodity prices, market

indexes or currency exchange rates and to gain exposure tofinancial markets. It will only use derivatives as permitted bysecurities regulations.

The portfolio can invest up to 100% of its assets in foreignsecurities.

The portfolio and an underlying fund managed by us mayalso engage in short selling on the conditions permitted byCanadian securities rules. In determining whether securitiesof a particular issuer should be sold short, the portfolio advi-sor utilizes the same analysis that is described above fordeciding whether to purchase the securities. Where theanalysis generally produces a favourable outlook, the issueris a candidate for purchase. Where the analysis produces anunfavourable outlook, the issuer is a candidate for a shortsale. For a more detailed description of short selling and thelimits within which the underlying fund may engage in shortselling, please refer to What are the risks? – Short sellingrisk.

What are the risks of investing in the fund?

To the extent that the Portfolio invests in underlying funds,it indirectly has the same risks as the underlying funds itholds. The Portfolio takes on the risks of an underlying fundin proportion to its investment in that fund. To the extent itinvests directly in equity and fixed income securities, thePortfolio will have the risks associated with investingdirectly in such equity and fixed income securities.

The risks applicable to the Portfolio include:

• asset-backed and mortgage-backed securities risk

• commodity risk

• credit risk

• currency risk

• derivatives risk

• emerging markets risk

• equity risk

• foreign investment risk

• fund-of-funds risk

• income trust risk

• interest rate risk

• issuer-specific risk

• liquidity risk

• repurchase and reverse repurchase transaction risk

10

• securities lending risk.

• short selling risk

• small company risk

• U.S. withholding tax risk.

You’ll find details about each of these risks under What is amutual fund and what are the risks of investing in a mutualfund?

During the 12 months preceding October 11, 2013, up to15.0% of the net assets of the portfolio were invested in Sco-tia Canadian Income Fund Series I, up to 14.2% of the netassets of the portfolio were invested in Scotia Private Inter-national Equity Pool Series I, and up to 12.2% of the netassets of the portfolio were invested in Scotia CanadianDividend Fund Series I.

Who should invest in this fund?

This Portfolio may be suitable for you if:

• you want a balanced holding with a significant biastowards equity, which is diversified by asset class, invest-ment style, geography and market capitalization

• you can accept medium risk

• you’re investing for the long term.

Please see Investment Risk Classification Methodology for adescription of how we determined the classification of thisPortfolio’s risk level.

Distribution policy

The Portfolio distributes any net income and net realizedcapital gains by the end of December of each calendar year.

Distributions on units held in registered plans andnon-registered accounts are reinvested in additional units ofthe Portfolio, unless you tell your dealer that you want toreceive cash distributions.

Fund expenses indirectly borne by investors

This example shows the Portfolio’s expenses on a $1,000investment with a 5% annual return.

Fees and expensespayable over 1 year 3 years 5 years 10 years

Series A units $ 22.24 70.12 122.90 279.77

SC

OT

IAIN

NO

VA

GR

OW

TH

PO

RT

FO

LIO

11

SC

OT

IAIN

NO

VA

MA

XIM

UM

GR

OW

TH

PO

RT

FO

LIO

Scotia INNOVA Maximum Growth PortfolioFund details

Fund type Global equity fund

Start date Series A units: January 19, 2009

Type of securities Series A units of a mutual fund trust

Eligible forregistered plans?

Yes

Portfolio advisor The Manager Toronto, Ontario

What does the fund invest in?

Investment objectives

The Portfolio’s objective is long term capital appreciation. Itinvests primarily in a diversified mix of mutual funds and/orequity securities located anywhere in the world.

Any change to the fundamental investment objectives mustbe approved by a majority of votes cast at a meeting of unit-holders for that purpose.

Investment strategies

The Portfolio is an asset allocation fund that allocates yourinvestment amongst various equities.

The table below outlines the target weighting for each assetclass in which the Portfolio invests.

Asset ClassTarget

Weighting

Equities 100%

The underlying funds, and equity securities in which thePortfolio invests may change from time to time, but in gen-eral we will keep the target weighting between Canadian andForeign equities no more than 10% above or below theamounts set out above. You’ll find more information oninvesting in underlying funds in Investing in other mutualfunds. Although up to 100% of the Portfolio’s assets may beinvested in underlying funds, once the Portfolio reaches asufficient size, the portfolio advisor may determine that it ismore efficient to invest the Portfolio directly in securities inone or more asset classes.

The portfolio advisor may use derivatives such as options,futures, forward contracts and swaps to hedge against lossesfrom changes in stock prices, commodity prices, marketindexes or currency exchange rates and to gain exposure tofinancial markets. It will only use derivatives as permitted bysecurities regulations.

The portfolio can invest up to 100% of its assets in foreignsecurities.

The portfolio and an underlying fund managed by us mayalso engage in short selling on the conditions permitted byCanadian securities rules. In determining whether securitiesof a particular issuer should be sold short, the portfolio advi-sor utilizes the same analysis that is described above fordeciding whether to purchase the securities. Where theanalysis generally produces a favourable outlook, the issueris a candidate for purchase. Where the analysis produces anunfavourable outlook, the issuer is a candidate for a shortsale. For a more detailed description of short selling and thelimits within which the underlying fund may engage in shortselling, please refer to What are the risks? – Short sellingrisk.

What are the risks of investing in the fund?

To the extent that the Portfolio invests in underlying funds,it indirectly has the same risks as the underlying funds itholds. The Portfolio takes on the risks of an underlying fundin proportion to its investment in that fund. To the extent itinvests directly in equity securities, the Portfolio will havethe risks associated with investing directly in such equitysecurities.

The risks applicable to the Portfolio include:

• asset-backed and mortgage-backed securities risk

• commodity risk

• currency risk

• derivatives risk

• emerging markets risk

• equity risk

• foreign investment risk

• fund-of-funds risk

• income trust risk

• interest rate risk

• issuer-specific risk

• liquidity risk

• repurchase and reverse repurchase transaction risk

• securities lending risk

• short selling risk

• small company risk

• U.S. withholding tax risk.12

You’ll find details about each of these risks under What is amutual fund and what are the risks of investing in a mutualfund?

During the 12 months preceding October 11, 2013, up to18.6% of the net assets of the portfolio were invested in Sco-tia Private International Equity Pool Series I, up to 15.7% ofthe net assets of the portfolio were invested in Scotia Cana-dian Dividend Fund Series I up to 12.7% of the net assets ofthe portfolio were invested in Scotia Private Canadian SmallCap Pool Series I, and up to 11.0% of the net assets of theportfolio were invested in Scotia Private Canadian GrowthPool Series I.

Who should invest in this fund?

This Portfolio may be suitable for you if:

• you want an all equity holding, which is diversified byinvestment style, geography and market capitalization

• you can accept medium to high risk

• you’re investing for the long term.

Please see Investment Risk Classification Methodology for adescription of how we determined the classification of thisPortfolio’s risk level.

Distribution policy

The Portfolio distributes any net income and net realizedcapital gains by the end of December of each calendar year.

Distributions on units held in registered plans andnon-registered accounts are reinvested in additional units ofthe Portfolio, unless you tell your dealer that you want toreceive cash distributions.

Fund expenses indirectly borne by investors

This example shows the Portfolio’s expenses on a $1,000investment with a 5% annual return.

Fees and expensespayable over 1 year 3 years 5 years 10 years

Series A units $ 23.58 74.32 130.27 296.53

SC

OT

IAIN

NO

VA

MA

XIM

UM

GR

OW

TH

PO

RT

FO

LIO

13

What is a mutual fund and what are the risks of investing in a

mutual fund?For many Canadians, mutual funds represent a simple and afford-able way to meet their financial goals. But what exactly is amutual fund, why invest in them, and what are the risks?

What is a mutual fund?

A mutual fund is an investment that pools your money with themoney of many other people. Professional portfolio advisors usethat money to buy securities that they believe will help achievethe fund’s investment objectives. These securities could includestocks, bonds, mortgages, money market instruments, or acombination of these.

When you invest in a mutual fund, you receive units of the fund.Each unit represents a proportionate share of all of the mutualfund’s assets. All of the investors in a mutual fund share in thefund’s income, gains and losses. Investors also pay their share ofthe fund’s expenses.

Why invest in mutual funds?

Mutual funds offer investors three key benefits: professionalmoney management, diversification and accessibility.

• Professional money management. Professional portfolio advi-sors have the expertise to make the investment decisions. Theyalso have access to up-to-the-minute information on trends inthe financial markets, and in-depth data and research onpotential investments.

• Diversification. Because your money is pooled with that ofother investors, a mutual fund offers diversification into manysecurities that may not have otherwise been available toindividual investors.

• Accessibility. Mutual funds have low investment minimums,making them accessible to nearly everyone.

No guarantees

While mutual funds have many benefits, it’s important toremember that an investment in a mutual fund isn’t guaranteed.Unlike bank accounts or guaranteed investment certificates(GICs), mutual fund units aren’t covered by the Canada DepositInsurance Corporation (CDIC) or any other government depositinsurer, and your investment in the fund is not guaranteed byScotiabank.

Under exceptional circumstances, a mutual fund may suspendyour right to sell your units. See Suspending your right to buy,switch and sell units for details.

What are the risks?

While everyone wants to make money when they invest, you couldlose money, too. This is known as risk. Like other investments,mutual funds involve some level of risk. The value of a fund’ssecurities can change from day to day for many reasons, includingchanges in the economy, interest rates, and market and companynews. That means the value of mutual fund units can vary. Whenyou sell your units in a fund, you could receive less money thanyou invested.

The amount of risk depends on the fund’s investment objectivesand the types of securities it invests in. A general rule of investingis that the higher the risk, the higher the potential for gains aswell as losses. Cash equivalent funds usually offer the least riskbecause they invest in highly liquid, short-term investments suchas treasury bills. Their potential returns are tied to short-terminterest rates. Income funds invest in bonds and other fixedincome investments. These funds typically have higher long-termreturns than cash equivalent funds, but they carry more riskbecause their prices can change when interest rates change.Equity funds expose investors to the highest level of risk becausethey invest in equity securities, such as common shares, whoseprices can rise and fall significantly in a short period of time.

Managing risk

While risk is an important factor to consider when you’re choos-ing a mutual fund, you should also think about your investmentgoals and when you’ll need your money. For example, if you’resaving for a large purchase in the next year or so, you might con-sider investing in a fund with low risk. If you want your retire-ment savings to grow over the next 20 years, you can probablyafford to put more of your money in equity funds.

A carefully chosen mix of investments can help reduce risk as youmeet your investment goals. Your mutual fund representative canhelp you build a portfolio that’s suited to your goals and riskcomfort level.

If your investment goals or tolerance for risk changes, remember,you can and should change your investments to match your newsituation.

Specific risks of mutual funds

The value of the investments a mutual fund holds can change fora number of reasons. You’ll find the specific risks of investing ineach of the Scotia INNOVA Portfolios in the individual funddescriptions starting on page 4. This section tells you more about

14

each risk. To the extent that a fund invests in underlying funds, ithas the same risks as its underlying funds. Accordingly, anyreference to a fund in this section is intended to also refer to anyunderlying funds that a fund may invest in.

Asset-backed and mortgage-backed securities risk

Asset-backed securities are debt obligations that are backed bypools of consumer or business loans. Mortgage-backed securitiesare debt obligations backed by pools of mortgages on commercialor residential real estate. To the extent that a fund invests inthese securities, it will be sensitive to asset-backed andmortgage-backed securities risk. If there are changes in themarket perception of the issuers of these types of securities, or inthe creditworthiness of the parties involved, then the value of thesecurities may be affected. In the use of mortgage-backed secu-rities, there is also a risk that there may be a drop in the interestrates charged on mortgages, a mortgagor may default on itsobligations under a mortgage or there may be a drop in the valueof the property secured by the mortgage.

Commodity risk

Some funds may invest directly or indirectly in gold or in compa-nies engaged in the energy or natural resource industries. Themarket value of such a mutual fund’s investments may beaffected by adverse movements in commodity prices. Whencommodity prices decline, this generally has a negative impact onthe earnings of companies whose business is based in commod-ities, such as oil and gas.

Credit risk

A fixed income security, such as a bond, is a promise to pay inter-est and repay the principal on the maturity date. There’s always arisk that the issuer will fail to honour that promise. This is calledcredit risk. To the extent that a fund invests in fixed incomesecurities, it will be sensitive to credit risk. Credit risk is lowestamong issuers that have a high credit rating from a credit ratingagency. It’s highest among issuers that have a low credit rating orno credit rating. Issuers with a low credit rating usually offerhigher interest rates to make up for the higher risk. The bonds ofissuers with poor credit ratings generally have yields that arehigher than bonds of issuers with superior credit ratings. Bondsof issuers that have poor credit ratings tend to be more volatile asthere is a greater likelihood of bankruptcy or default. Credit rat-ings may change over time. Please see Foreign investment risk inthe case of investments in foreign government debt.

Currency risk

When a mutual fund buys an investment that’s denominated in aforeign currency, changes in the exchange rate between that

currency and the Canadian dollar will affect the value of thefund.

Derivatives risk

To the extent that a fund uses derivatives, it will be sensitive toderivatives risk. Derivatives can be useful for hedging againstlosses, gaining exposure to financial markets and making indirectinvestments, but they involve certain risks:

• Hedging with derivatives may not achieve the intended result.Hedging instruments rely on historical or anticipated correla-tions to predict the impact of certain events, which may or maynot occur. If they occur, they may not have the predictedeffect.

• It’s difficult to hedge against trends that the market hasalready anticipated.

• Costs relating to entering and maintaining derivatives con-tracts may reduce the returns of a fund.

• A currency hedge will reduce the benefits of gains if thehedged currency increases in value.

• Currency hedging can be difficult in smaller emerging growthcountries because of the limited size of those markets.

• Currency hedging provides no protection against changes inthe value of the underlying securities.

• There’s no guarantee that a liquid exchange or market forderivatives will exist. This could prevent a fund closing out itspositions to realize gains or limit losses. At worst, a fund mightface losses from having to exercise underlying futures contracts.

• The prices of derivatives can be distorted if trading in theirunderlying stocks is halted. Trading in the derivative might beinterrupted if trading is halted in a large number of the under-lying stocks. This would make it difficult for a fund to close outits positions.

• The counterparty in a derivatives contract might not be able tomeet its obligations. When using derivatives, a mutual fundrelies on the ability of the counterparty to the transaction toperform its obligations. In the event that a counterparty fails tocomplete its obligations, the mutual fund may bear the risk ofloss of the amount expected to be received under options,forward contracts or other transactions in the event of thedefault or bankruptcy of a counterparty.

• Derivatives trading on foreign markets may take longer and bemore difficult to complete. Foreign derivatives are subject tothe foreign investment risks described below. Please see for-eign investment risk.

• Investment dealers and futures brokers may hold a fund’sassets on deposit as collateral in a derivative contract. As aresult, someone other than the fund’s custodian is responsiblefor the safekeeping of that part of the fund’s assets.

15

• The regulation of derivatives is a rapidly changing area of lawand is subject to modification by government and judicialaction. The effect of any future regulatory changes may make itmore difficult, or impossible, for a fund to use certainderivatives.

Emerging markets risk

The Portfolios and some underlying funds may invest in foreigncompanies or governments (other than the U.S.) which may belocated in, or operate, in developing countries. Companies inthese markets may have limited product lines, markets orresources, making it difficult to measure the value of the com-pany. Political instability, possible corruption, as well as lowerstandards of business regulation increase the risk of fraud andother legal issues. In addition to foreign investment riskdescribed below, these mutual funds may be exposed to greatervolatility as a result of such issues.

Equity risk

Funds that invest in equities, such as common shares, areaffected by changes in the general economy and financial mar-kets, as well as by the success or failure of the companies thatissued the securities. When stock markets rise, the value ofequity securities tends to rise. When stock markets fall, the valueof equity securities tends to fall. Convertible securities may alsobe subject to interest rate risk.

Foreign investment risk

Investments issued by foreign companies or governments otherthan the U.S. can be riskier than investments in Canada and theU.S. Foreign countries can be affected by political, social, legal ordiplomatic developments, including the imposition of currencyand exchange controls. Some foreign markets can be less liquid,are less regulated, and are subject to different reporting practicesand disclosure requirements than issuers in North Americanmarkets. It may be more difficult to enforce a fund’s legal rightsin jurisdictions outside of Canada. In general, securities issued inmore developed markets, such as Western Europe, have lowerforeign investment risk. Securities issued in emerging or develop-ing markets, such as Southeast Asia or Latin America, have sig-nificant foreign investment risk and are exposed to the emergingmarkets risks described above.

Fund-of-funds risk

If a mutual fund invests in an underlying fund, the risks asso-ciated with investing in that mutual fund include the risks asso-ciated with the securities in which the underlying fund invests,along with the other risks of the underlying fund. Accordingly, amutual fund takes on the risk of an underlying fund and its

respective securities in proportion to its investment in that under-lying fund. If an underlying fund suspends redemptions, the fundthat invests in the underlying fund may be unable to value part ofits portfolio and may be unable to process redemption orders.

Interest rate risk

Mutual funds that invest in fixed income securities, such asbonds, mortgages and money market instruments, are sensitive tochanges in interest rates. In general, when interest rates are ris-ing, the value of these investments tends to fall. When rates arefalling, fixed income securities tend to increase in value. Fixedincome securities with longer terms to maturity are generallymore sensitive to changes in interest rates. Certain types of fixedincome securities permit issuers to repay principal before thesecurity’s maturity date. There is a risk that an issuer willexercise this prepayment right after interest rates have fallen andthe funds that hold these fixed income securities will receivepayments of principal before the expected maturity date of thesecurity and may need to reinvest these proceeds in securitiesthat have lower interest rates.

Issuer-specific risk

The market value of an individual issuer’s securities can be morevolatile than the market as a whole. As a result, if a single issuer’ssecurities represent a significant portion of the market value of afund’s assets, changes in the market value of that issuer’s secu-rities may cause greater fluctuation in the fund’s unit value thanwould normally be the case. A less-diversified fund may also suf-fer from reduced liquidity if a significant portion of its assets isinvested in any one issuer. In particular, the fund may not be ableto easily liquidate its position in the issuers as required to fundredemption requests.

Generally, mutual funds are not permitted to invest more than 10percent of their assets in any one issuer. This restriction does notapply to investments in debt securities issued or guaranteed bythe Canadian or U.S. government, securities issued by a clearingcorporation, securities issued by mutual funds that are subject tothe requirements of National Instrument 81-102 – Mutual Fundsand National Instrument 81-101- Mutual Fund Prospectus Dis-closure, or index participation units issued by a mutual fund.

Liquidity risk

Liquidity is a measure of how quickly an investment can be soldfor cash at a fair market price. If a fund can’t sell an investmentquickly, it may lose money or make a lower profit, especially if ithas to meet a large number of redemption requests. In general,investments in smaller companies, smaller markets or certainsectors of the economy tend to be less liquid than other types ofinvestments. The less liquid an investment, the more its valuetends to fluctuate.

16

Repurchase and reverse repurchase transaction risk

The Portfolios and some underlying funds may enter intorepurchase or reverse repurchase agreements to generate addi-tional income. When a mutual fund agrees to sell a security atone price and buy it back on a specified later date from the sameparty with the expectation of a profit, it is entering into arepurchase agreement. When a mutual fund agrees to buy a secu-rity at one price and sell it back on a specified later date to thesame party with the expectation of a profit, it is entering into areverse repurchase agreement. Mutual funds engaging inrepurchase and reverse repurchase transactions are exposed tothe risk that the other party to the transaction may becomeinsolvent and unable to complete the transaction. In those cir-cumstances, there is a risk that the value of the securities boughtmay drop or the value of the securities sold may rise between thetime the other party becomes insolvent and the time the fundrecovers its investment. Mutual funds that engage in these trans-actions reduce this risk by holding, as collateral, enough of theother party’s cash or securities to cover that party’s repurchase orreverse repurchase obligations. To limit the risks associated withrepurchase and reverse repurchase transactions, the collateralheld in respect of the repurchase or reverse repurchase obliga-tions must be marked to market on each business day and be fullycollateralized at all times with acceptable collateral which has avalue at least equal to 102% of the securities sold or cash paid forthe securities by the mutual fund. Prior to entering into arepurchase agreement, a mutual fund must ensure that theaggregate value of the securities of a mutual fund that have beensold pursuant to repurchase transactions, together with anysecurities loaned, does not exceed 50% of its total asset value atthe time that the mutual fund enters into the transaction.

Securities lending risk

The Portfolios and some underlying funds may enter into secu-rities lending transactions to generate additional income fromsecurities held in a mutual fund’s portfolio. A mutual fund maylend securities held in its portfolio to qualified borrowers whoprovide adequate collateral. In lending its securities, a mutualfund is exposed to the risk that the borrower may not be able tosatisfy its obligations under the securities lending agreement andthe lending mutual fund is forced to take possession of thecollateral held. Losses could result if the collateral held by themutual fund is insufficient, at the time the remedy is exercised,to replace the securities borrowed. Mutual funds must receivecollateral worth no less than 102% of the value of the loanedsecurities and borrowers must adjust that collateral daily toensure this level is maintained. Prior to entering into a securitieslending agreement, a mutual fund must ensure that the aggregatevalue of the securities loaned together with those that have beensold pursuant to repurchase transactions, does not exceed 50% ofits total asset value.

Series risk

Some Portfolios and some underlying funds may offer two or moreseries of units of the same fund. Although the value of each seriesis calculated separately, there’s a risk that the expenses orliabilities of one series of units may affect the value of the otherseries. If one series is unable to cover its liabilities, the otherseries are legally responsible for covering the difference. Webelieve that this risk is very low.

Short selling risk

Certain mutual funds may engage in a limited amount of shortselling. A “short sale” is where a mutual fund borrows securitiesfrom a lender which are then sold in the open market (or “soldshort”). At a later date, the same number of securities arerepurchased by the mutual fund and returned to the lender. Inthe interim, the proceeds from the first sale are deposited withthe lender and the mutual fund pays interest to the lender. If thevalue of the securities declines between the time that the mutualfund borrows the securities and the time it repurchases andreturns the securities, the mutual fund makes a profit for thedifference (less any interest the mutual fund is required to pay tothe lender). Short selling involves certain risks. There is noassurance that securities will decline in value during the periodof the short sale sufficient to offset the interest paid by themutual fund and make a profit for the mutual fund, and secu-rities sold short may instead appreciate in value. The mutualfund also may experience difficulties repurchasing and returningthe borrowed securities if a liquid market for the securities doesnot exist. The lender from whom the mutual fund has borrowedsecurities may go bankrupt and the mutual fund may lose thecollateral it has deposited with the lender. Each mutual fund thatengages in short selling will adhere to controls and limits that areintended to offset these risks by short selling only securities oflarger issuers for which a liquid market is expected to be main-tained and by limiting the amount of exposure for short sales. Themutual funds also will deposit collateral only with lenders thatmeet certain criteria for creditworthiness and only up to certainlimits.

Small company risk

The prices of shares issued by smaller companies tend to fluc-tuate more than those of larger corporations. Smaller companiesmay not have established markets for their products and may nothave solid financing. These companies generally issue fewershares, which increases their liquidity risk.

U.S. withholding tax risk

Generally, the Foreign Account Tax Compliance provisions of theU.S. Hiring Incentives to Restore Employment Act of 2010 (or

17

“FATCA”) impose a 30% withholding tax on “withholdable pay-ments” made to a mutual fund, unless the mutual fund entersinto a FATCA agreement with the U.S. Internal Revenue Service(the “IRS”) (or is subject to an IGA as described below) to com-ply with certain information reporting and other requirements.Compliance with FATCA will require a mutual fund to requestand obtain certain information from its investors and (whereapplicable) their beneficial owners (including informationregarding their identity, residency and citizenship) and to dis-close such information and documentation to the IRS.

Withholdable payments include (i) certain U.S. source income(such as interest, dividends and other passive income) and(ii) gross proceeds from the sale or disposition of property thatcan produce U.S. source interest or dividends. The withholdingtax applies to withholdable payments made on or after July 1,2014 (or January 1, 2017 in the case of gross proceeds). The 30%withholding tax may also apply to any “foreign passthru pay-ments” paid by a mutual fund to certain investors on or afterJanuary 1, 2017. The scope of foreign passthru payments will bedetermined under the U.S. Treasury regulations that have yet tobe issued. Moreover, the foregoing rules and requirements may bemodified by an intergovernmental agreement between Canadaand the U.S. (the “Canada-U.S. IGA”), future U.S. Treasury regu-lations, or other guidance. Under the Canada-U.S. IGA, it isanticipated that a mutual fund will not have to enter into anindividual agreement with the IRS but will have to comply withthe terms of the Canada-U.S. IGA including registration require-ments with the IRS and requirements to identify, and report cer-tain information on accounts held by U.S. persons owning,directly or indirectly, an interest in the mutual fund, or report onaccounts held by certain other persons or entities. Because theCanada-U.S. IGA has not yet been finalized, it is not possible todetermine presently (i) whether the mutual fund will be able tocomply and (ii) what impact, if any, the Canada-U.S. IGA willhave on its investors. If a mutual fund is unable to comply withthese requirements, the imposition of the 30% U.S. withholdingtax may affect the net asset value of the mutual fund and mayresult in reduced investment returns to investors. It is possiblethat the administrative costs arising from compliance withFATCA and/or the Canada-U.S. IGA and future guidance may alsocause an increase in the operating expenses of the mutual funds.

18

Organization and management of the Scotia INNOVA Portfolios

Manager

1832 Asset Management L.P.Scotia Plaza52nd Floor40 King Street WestToronto, Ontario M5H 1H1

As manager, we are responsible for the overall business and operation of the Portfolios. This includes:

• arranging for portfolio advisory services providing or arranging for administrative services.

1832 Asset Management L.P. is a wholly-owned subsidiary by The Bank of Nova Scotia.

Effective September 30, 2013, Scotia Asset Management L.P. changed its name to 1832 Asset Management L.P.

Trustee

1832 Asset Management L.P.Toronto, Ontario

As trustee, we control and have authority over each Portfolio’s investments in trust for unitholders under the termsdescribed in the master declaration of trust.

Principal distributor

Scotia Securities Inc.Toronto, Ontario

As principal distributor, Scotia Securities Inc. markets and sells units of the Portfolios where they qualify for sale inCanada. We or Scotia Securities Inc. may hire participating dealers to assist in the sale of units of the Portfolios.

Scotia Securities Inc. is a wholly-owned subsidiary of Scotiabank, which is the parent company of 1832 AssetManagement L.P.

Custodian

The Bank of Nova ScotiaToronto, Ontario

The custodian holds the investments of the Portfolios and keeps them safe to ensure that they are used only for thebenefit of investors.

The Bank of Nova Scotia is the parent company of 1832 Asset Management L.P.

Registrar

1832 Asset Management L.P.Toronto, Ontario

As registrar, we make arrangements to keep a record of all unitholders of the Portfolios, process orders and issue tax slipsto unitholders.

Auditor

PricewaterhouseCoopers LLPToronto, Ontario

The auditor is an independent firm of chartered accountants. The firm audits the annual financial statements of the fundsand provides an opinion as to whether they are fairly presented in accordance with Canadian generally acceptedaccounting principles.

Portfolio advisor The portfolio advisor provides investment advice and makes the investment decisions for the Portfolios.

1832 Asset Management L.P.Toronto, Ontario

1832 Asset Management L.P. is wholly owned by The Bank of Nova Scotia.

Portfolio Sub-advisor We have authority to retain portfolio sub-advisors. The sub-advisor provides investment advice and makes investmentdecisions for certain Portfolios. You’ll find the Portfolios for which the sub-advisor acts in the fund descriptions startingon page 4.

Aurion CapitalManagement Inc.

Toronto, Ontario

60% of Aurion Capital Management Inc. is owned by DundeeWealth Inc., a wholly owned subsidiary of Scotiabank.

Independent ReviewCommittee