Embed Size (px)

Citation preview

2

Sales first quarter 2002: SEK 12,487 m. (12,405) Earnings before interest and taxes, EBIT: SEK 770 m. (952)

Scania GroupScania Group

3

Operating income (EBIT) SEK 770 m. (952)EBIT margin for Scania products 6.6%Lower truck deliveries (-16%)Higher bus deliveries (+9%)Positive trend in service sales and customer financePositive currency rate effectsCost-cutting and adjustment programmes in both European and Latin American operations continue

Operating income (EBIT) SEK 770 m. (952)EBIT margin for Scania products 6.6%Lower truck deliveries (-16%)Higher bus deliveries (+9%)Positive trend in service sales and customer financePositive currency rate effectsCost-cutting and adjustment programmes in both European and Latin American operations continue

Scania highlights Scania highlights First quarter 2002First quarter 2002

4

First quarter 2002 and outlookFirst quarter 2002 and outlook

Central andeastern Europe

Improved order bookings

Latin America

Uncertainty

Rest of the world

Low volume

Western Europe

Market bottoming out????

Stronger order bookings

AsiaStronger order bookings

5

SEK m.

0

300

600

900

1,200

1,500

1,800

2,100

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

Quarterly EBIT and EBIT marginQuarterly EBIT and EBIT marginScania GroupScania Group

6.3%

8.6%9.1%

11.2%9.0%

1998 1999

11.6%

629

1,010851

1,1021,2401,263

1,139

11.6%

1,403

9.2%

1,105

2000

1,051

7.9%

901

8.3%13.3%

2,027

7.7%

952

2001

650

4.7%

402

3.4%

463

3.1%

2002

11.4% 770

6.2%

6

SEK m.

0

300

600

900

1,200

1,500

1,800

2,100

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

Quarterly EBIT and EBIT marginQuarterly EBIT and EBIT marginScania productsScania products

6.6%

9.2%9.8%

12.0%9.7%

12.8%

1998 1999

12.4%568

938789

1,0471,178 1,192

1,086

12.5%

1,336

10.1%

1,049

2000

984

8.6%

872

9.4%13.9%

1,904

943

8.5%

2001

597

4.9%384

3.7%

432

3.2%

2002

724

6.6%

7

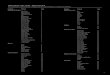

1,5001,7001,9002,1002,3002,5002,7002,9003,1003,3003,5003,7003,900

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Scania order bookings Scania order bookings -- truckstrucksWestern EuropeWestern Europe

Units

2000

20012002

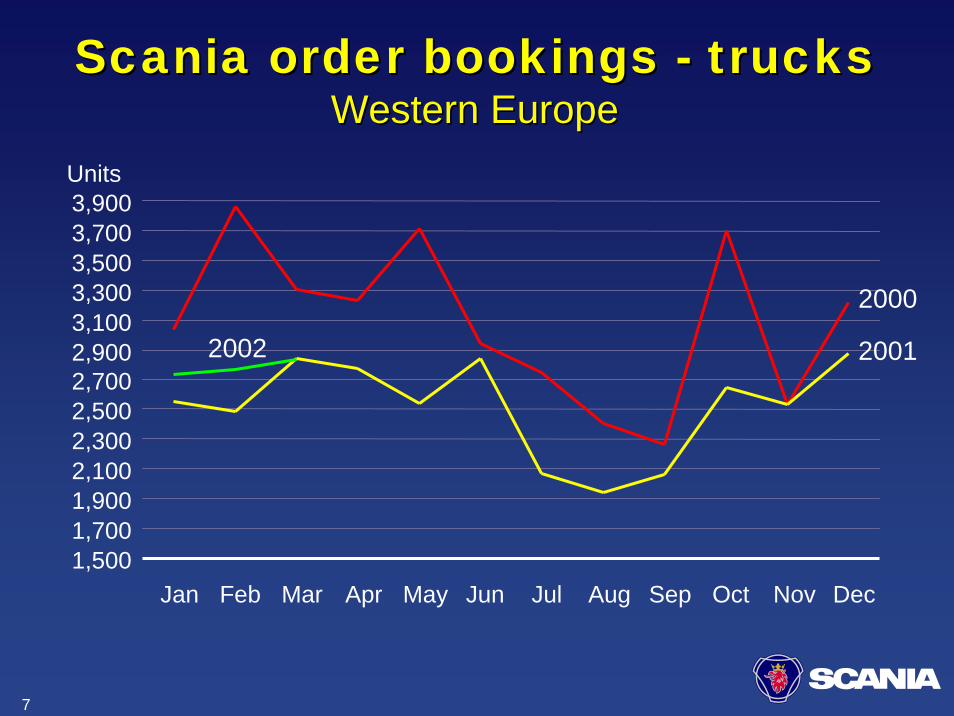

8

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

Q1 Q2 Q3 Q4

Scania order bookings Scania order bookings -- truckstrucksWestern EuropeWestern Europe

Units

200020012002

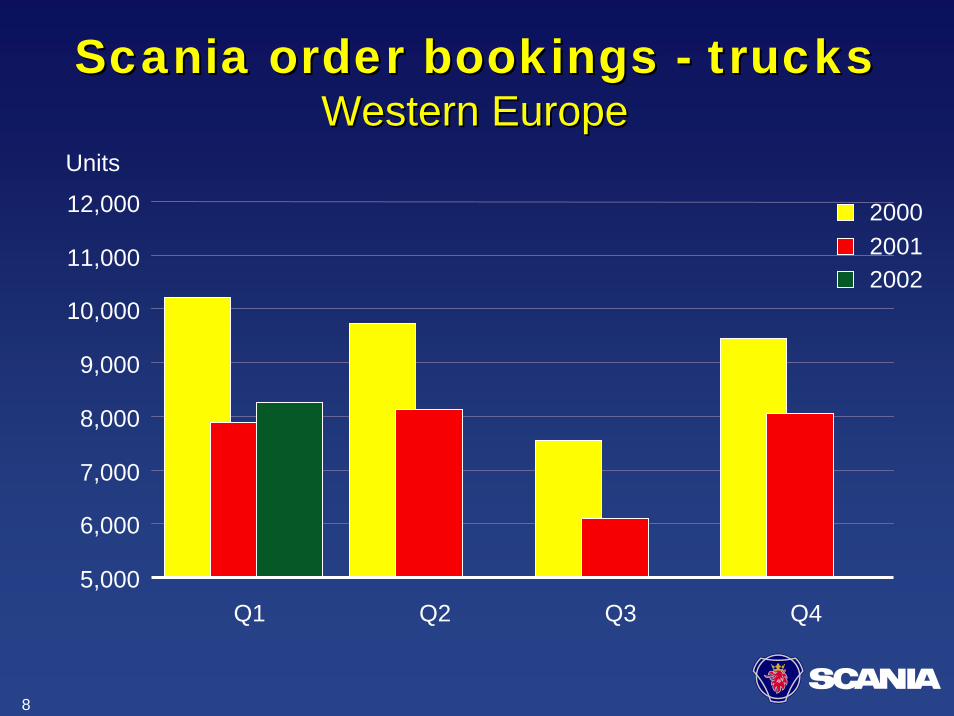

9

01,0002,0003,0004,0005,0006,0007,0008,0009,000

10,00011,00012,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q11998 1999 2000 2001 2002

Scania truck deliveries Scania truck deliveries Western EuropeWestern Europe

Units

10

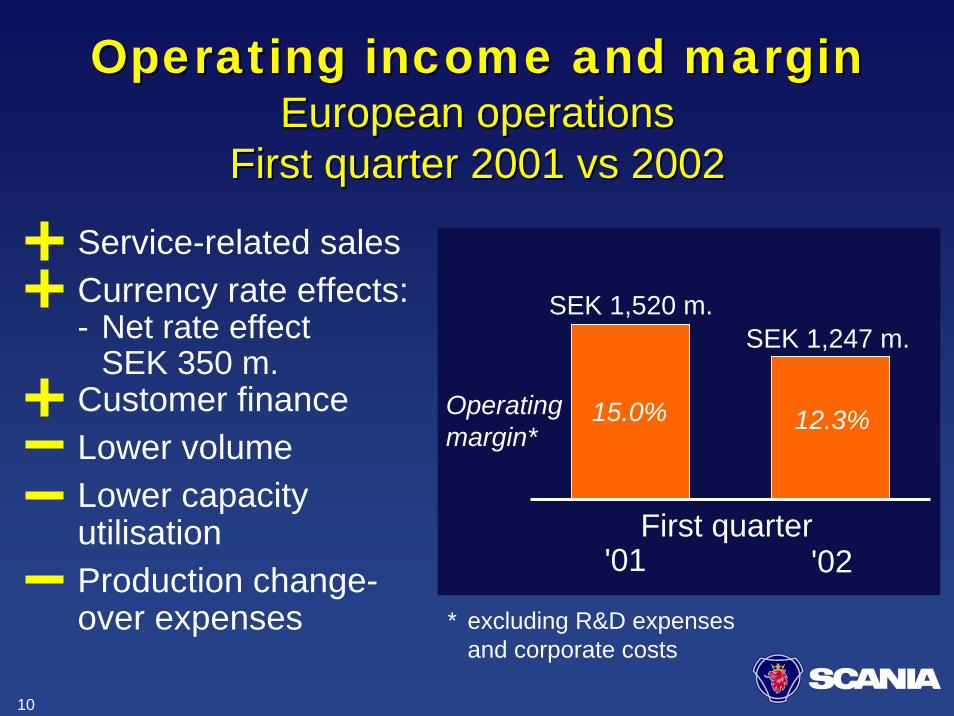

Service-related sales Currency rate effects:- Net rate effect

SEK 350 m.Customer financeLower volumeLower capacityutilisationProduction change-over expenses

Operating income and marginOperating income and marginEuropean operationsEuropean operations

First quarter 2001 vs 2002First quarter 2001 vs 2002

SEK 1,520 m.SEK 1,247 m.

Operating margin*

15.0% 12.3%

'01 '02First quarter

* excluding R&D expenses and corporate costs

11

Mercedes 18.2 19.0

Scania 14.3 14.7

RVI 13.6 14.0

DAF 11.7 13.6

Volvo 15.4 13.2

MAN 13.9 12.2

Iveco 9.7 10.6

CompetitionCompetitionWestern EuropeWestern Europe

Jan-Feb '01 Jan-Feb '02Make Market share Market share Trend

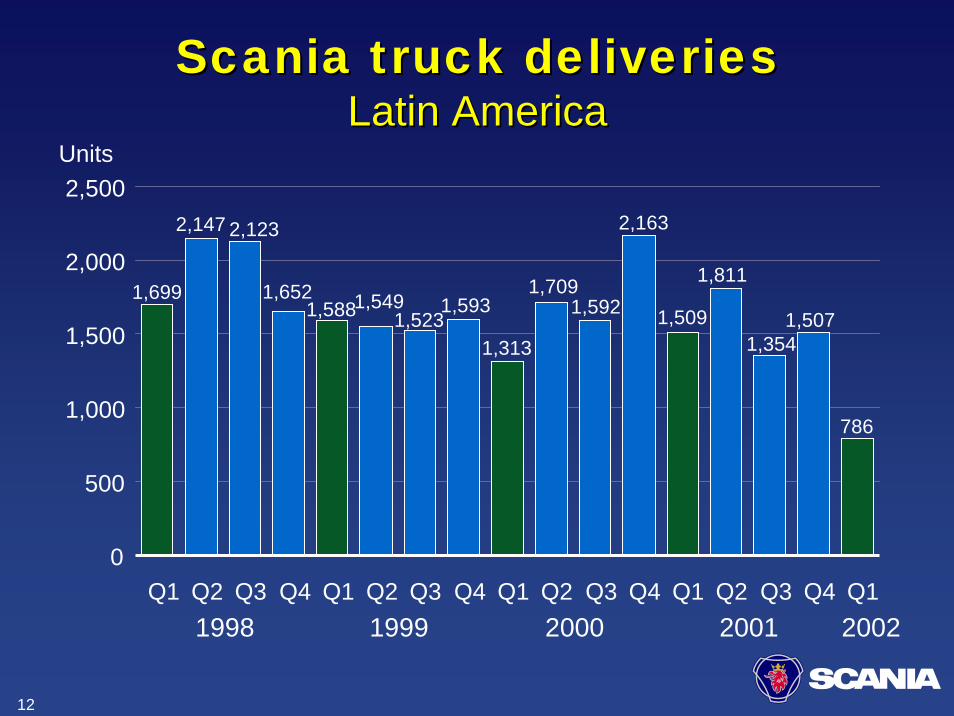

12

0

500

1,000

1,500

2,000

2,500

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

Units

Scania truck deliveriesScania truck deliveriesLatin AmericaLatin America

1998 1999

1,699

2,147 2,123

1,6521,5881,549

1,5231,593

1,313

2000

1,7091,592

2,163

1,509

2001

1,811

1,3541,507

2002

786

13

Operating incomeOperating incomeLatin American operationsLatin American operationsFirst quarter 2001 vs 2002First quarter 2001 vs 2002

SEK -36 m. SEK -58 m.

Increased pricesCost savingsVolume

'01 '02First quarter

14

Mercedes 26.9 28.3

Volvo 22.9 22.4

Scania 29.1 17.6

Volkswagen 7.5 12.8

Iveco 5.2 8.9

Ford 7.4 8.3

International 1.1 1.7

CompetitionCompetitionBrazilBrazil

Jan-Mar '01 Jan-Mar '02Make Market share Market share Trend

15

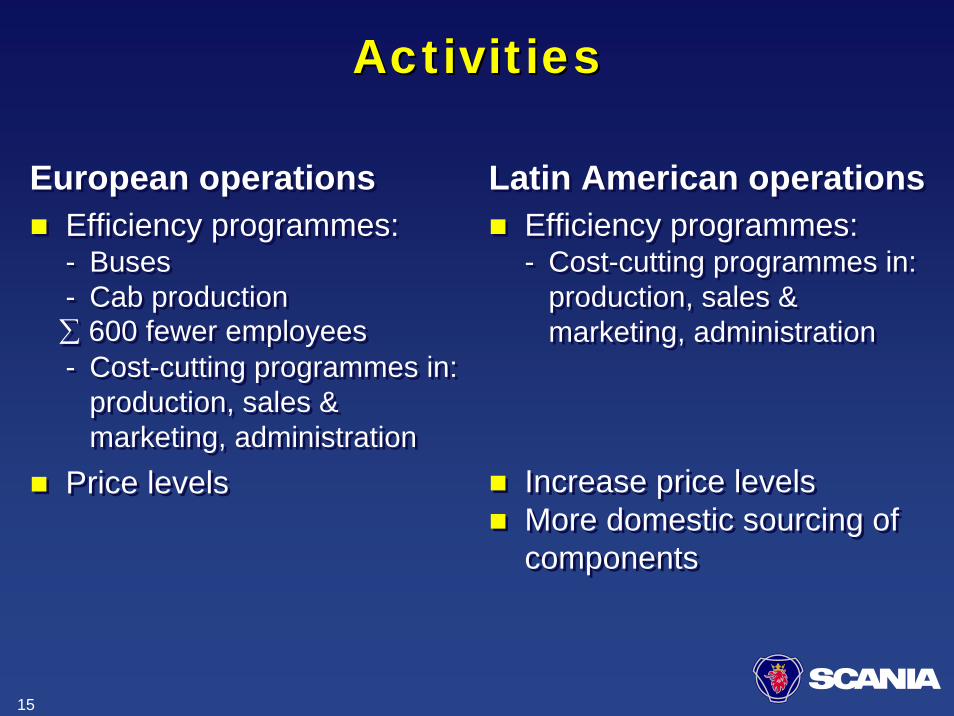

ActivitiesActivities

European operationsEfficiency programmes:- Buses - Cab production

- Cost-cutting programmes in:production, sales &marketing, administration

Price levels

European operationsEfficiency programmes:- Buses - Cab production

- Cost-cutting programmes in:production, sales &marketing, administration

Price levels

Latin American operationsLatin American operations

∑ 600 fewer employees∑ 600 fewer employees

Efficiency programmes:- Cost-cutting programmes in:

production, sales &marketing, administration

Increase price levels More domestic sourcing of components

Efficiency programmes:- Cost-cutting programmes in:

production, sales &marketing, administration

Increase price levels More domestic sourcing of components

16

Operating income (EBIT) SEK 770 m. (952)EBIT margin for Scania products 6.6%Lower truck deliveries (-16%)Higher bus deliveries (+9%)Positive trend in service sales and customer financePositive currency rate effectsCost-cutting and adjustment programmes in both European and Latin American operations continue

Operating income (EBIT) SEK 770 m. (952)EBIT margin for Scania products 6.6%Lower truck deliveries (-16%)Higher bus deliveries (+9%)Positive trend in service sales and customer financePositive currency rate effectsCost-cutting and adjustment programmes in both European and Latin American operations continue

Summing up Summing up First quarter 2002First quarter 2002

17

Svenska Svenska Volkswagen AB and Volkswagen AB and Din Din Bil Sverige Bil Sverige ABAB

Both sold to Volkswagen AGImporting/distributing VW, Audi, Seat, Skoda and Porsche to SwedenCars – consumer productsTrucks – investment productsSvenska Volkswagen divested for SEK 870 m. and Din Bil for SEK 450 m.Scania’s profit approximately SEK 550 m.

Both sold to Volkswagen AGImporting/distributing VW, Audi, Seat, Skoda and Porsche to SwedenCars – consumer productsTrucks – investment productsSvenska Volkswagen divested for SEK 870 m. and Din Bil for SEK 450 m.Scania’s profit approximately SEK 550 m.

18

Scania and Hino form business alliance

Scania and Hino Scania and Hino form business allianceform business alliance

Leverage Scania’s and Hino’s complementary market presence and product ranges

Pilot introduction of Scania tractor units in Japan

Evaluation of potential use of Hino 7/8-litre engines in Scania vehicles

Exchange of know-how regarding emission control technology

Leverage Scania’s and Hino’s complementary market presence and product ranges

Pilot introduction of Scania tractor units in Japan

Evaluation of potential use of Hino 7/8-litre engines in Scania vehicles

Exchange of know-how regarding emission control technology

19

Concentration of– cab body welding (1996): from Meppel to Oskarshamn– 6-cylinder engine production (1999): from Zwolle to Södertälje– axle production (1999-2000): from Zwolle to Falun– 8-cylinder engine production (2001): from Zwolle to Södertälje– cab production (2002): from Meppel to Oskarshamn– development, production development and production of bus

chassis: from Katrineholm to Södertälje– development, production development and production of bus

bodies: in Katrineholm– side-member process (2003): from Zwolle and Södertälje to

Luleå

Concentration of– cab body welding (1996): from Meppel to Oskarshamn– 6-cylinder engine production (1999): from Zwolle to Södertälje– axle production (1999-2000): from Zwolle to Falun– 8-cylinder engine production (2001): from Zwolle to Södertälje– cab production (2002): from Meppel to Oskarshamn– development, production development and production of bus

chassis: from Katrineholm to Södertälje– development, production development and production of bus

bodies: in Katrineholm– side-member process (2003): from Zwolle and Södertälje to

Luleå

StructureStructureEuropean production system

For Demanding PeopleFor Demanding PeopleFor Demanding People