Embed Size (px)

Citation preview

Deutsche Bank Markets Research

Japan

Synthetic Equity & Index Strategy

Japan Indices

Date 15 May 2014

Land of the Rising Equity Allocation

A closer look at new indices adopted by GPIF

________________________________________________________________________________________________________________

Deutsche Bank Securities Inc.

Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1.MCI (P) 148/04/2014.

Contributors

Shan Lan

Strategist (+852) 22036716 [email protected]

Will Stephens

Strategist (+852) 22036719 [email protected]

Major asset allocation changes in Japanese pension funds are in sight Japan is the second largest country in the world in terms of pension fund assets, following the US. Major Japanese pension funds including GPIF (Government Pension Investment Fund) are facing mounting pressure to boost returns as pension payouts for the world’s oldest population swell and Prime Minister Shinzo Abe and the Bank of Japan seek to spur price gains. GPIF plans to complete its new five-yearly plan by June of this year. Based on the recommendations from the various committee members made public, significant changes in asset allocation are expected, including increasing allocation to equity by reducing the bond weighting in the portfolio.

Pension fund allocations may provide a catalyst after weakness YTD We estimate there could be significant new money injected into the domestic equity market, ranging from $50 bn to over $100 bn. We believe this has the potential to provide positive support for Japan’s equity market, following a disappointing start to the year.

New domestic benchmarks: more diversified and spotlight on smart beta GPIF recently announced that it will adjust some of its current equity allocation partially out of traditional passive (Topix) and active investments towards smart beta allocations (S&P GIVI Japan, Nomura Rafi and MSCI Japan Small Cap) and additional indices for passive investments including the recently introduced Nikkei 400. Globally, 2013 saw the rise of smart beta indices which bridge the gap between active and passive index management styles. We see the adoption of smart beta and increased focus on shareholder returns as a significant long-term positive for the Japanese equity markets.

Nikkei 400 – shareholder return a positive, but still quite similar profile to Topix The Nikkei 400 and its focus on shareholder returns have garnered significant attention. We believe it will be a much easier index for investors to replicate relative to the Topix, and should provide a simple transition, given its similar return profile and high correlation (99.8%) to the Topix. The upcoming introduction of futures should spur further acceptance of the Nikkei 400. We find that the impact of the increased focus on ROE in the Nikkei 400 is partially offset by its backward looking mechanism, market cap weighting and high level of diversification, resulting in it having very similar performance and fundamental characteristics to other broad indices such as the Topix and MSCI Japan. That said, we believe the Nikkei 400 and the increasingly proactive approach of Japanese pension funds should act as longer-term catalysts for renewed focus on motivating corporate Japan to deliver shareholder returns.

15 May 2014

Japan Indices

Page 2 Deutsche Bank Securities Inc.

Table Of Contents

Potential Asset Allocation Changes in Japanese Pension Funds .. 3 Major asset allocation changes are in sight ....................................................................... 3 New Domestic Equity Benchmarks: more diversified and spotlight on smart beta .......... 7 New asset allocation could potentially inject over $100 bn to domestic equity market ... 8 Equity allocations may act as a positive catalyst ............................................................. 10 Recent trends in Smart Beta investments. ....................................................................... 13

Benchmark Comparison .............................................................. 15 A glimpse at the new benchmarks .................................................................................. 15 Cross-index Performance ................................................................................................. 19

A Closer Look .............................................................................. 23 Nikkei 400 ......................................................................................................................... 23 Russell Nomura Prime ...................................................................................................... 26 S&P GIVI Japan ................................................................................................................ 29 RAFI .................................................................................................................................. 31 Topix ................................................................................................................................. 34 MSCI Japan ...................................................................................................................... 36 MSCI Japan Small Cap ..................................................................................................... 38

Listed Products tracking these indices ........................................ 41 List of ETFs tracking these indices ................................................................................... 42

15 May 2014

Japan Indices

Deutsche Bank Securities Inc. Page 3

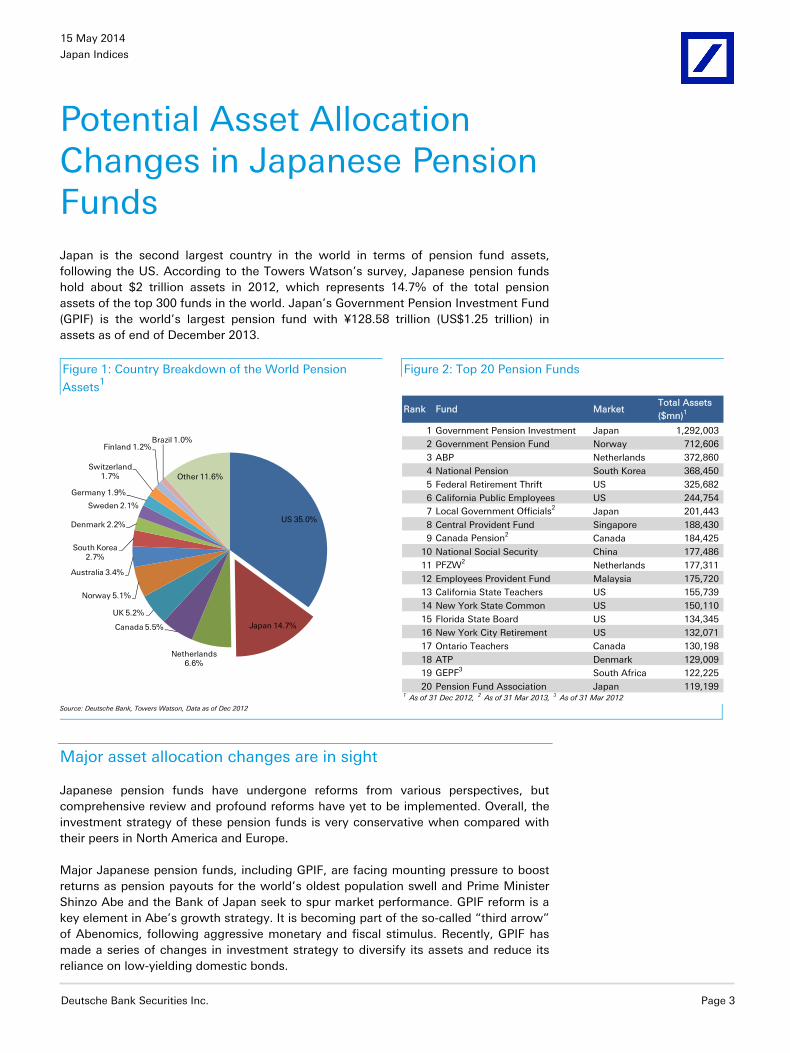

Potential Asset Allocation Changes in Japanese Pension Funds Japan is the second largest country in the world in terms of pension fund assets, following the US. According to the Towers Watson’s survey, Japanese pension funds hold about $2 trillion assets in 2012, which represents 14.7% of the total pension assets of the top 300 funds in the world. Japan’s Government Pension Investment Fund (GPIF) is the world’s largest pension fund with ¥128.58 trillion (US$1.25 trillion) in assets as of end of December 2013.

Figure 1: Country Breakdown of the World Pension

Assets1

Figure 2: Top 20 Pension Funds

US 35.0%

Japan 14.7%

Netherlands 6.6%

Canada 5.5%

UK 5.2%

Norway 5.1%

Australia 3.4%

South Korea 2.7%

Denmark 2.2%

Sweden 2.1%

Germany 1.9%

Switzerland 1.7%

Finland 1.2%Brazil 1.0%

Other 11.6%

Rank Fund MarketTotal Assets ($mn)1

1 Government Pension Investment Japan 1,292,003

2 Government Pension Fund Norway 712,606

3 ABP Netherlands 372,860

4 National Pension South Korea 368,450

5 Federal Retirement Thrift US 325,682

6 California Public Employees US 244,754

7 Local Government Officials2 Japan 201,443

8 Central Provident Fund Singapore 188,430

9 Canada Pension2 Canada 184,425

10 National Social Security China 177,486

11 PFZW2 Netherlands 177,311

12 Employees Provident Fund Malaysia 175,720

13 California State Teachers US 155,739

14 New York State Common US 150,110

15 Florida State Board US 134,345

16 New York City Retirement US 132,071

17 Ontario Teachers Canada 130,198

18 ATP Denmark 129,009

19 GEPF3 South Africa 122,225

20 Pension Fund Association Japan 119,199 1 As of 31 Dec 2012, 2 As of 31 Mar 2013, 3 As of 31 Mar 2012

Source: Deutsche Bank, Towers Watson, Data as of Dec 2012

Major asset allocation changes are in sight

Japanese pension funds have undergone reforms from various perspectives, but comprehensive review and profound reforms have yet to be implemented. Overall, the investment strategy of these pension funds is very conservative when compared with their peers in North America and Europe.

Major Japanese pension funds, including GPIF, are facing mounting pressure to boost returns as pension payouts for the world’s oldest population swell and Prime Minister Shinzo Abe and the Bank of Japan seek to spur market performance. GPIF reform is a key element in Abe’s growth strategy. It is becoming part of the so-called “third arrow” of Abenomics, following aggressive monetary and fiscal stimulus. Recently, GPIF has made a series of changes in investment strategy to diversify its assets and reduce its reliance on low-yielding domestic bonds.

15 May 2014

Japan Indices

Page 4 Deutsche Bank Securities Inc.

Figure 3: 2007-2012 Annualized Growth of Assets of Top 20 Funds (Split by fund

domicile – in local currency)

-1.2%

0.9%

2.4%

6.5%

7.8%

11.0%

11.1%

11.4%

12.5%

14.4%

16.5%

-2.0% 1.0% 4.0% 7.0% 10.0% 13.0% 16.0%

Japan

U.S.

Canada

Netherlands

South Africa

Singapore

Denmark

Malaysia

South Korea

Norway

China

Source: Deutsche Bank, Towers Watson

Figure 4: Asset Allocation Comparison (Average of Top 20 Funds vs GPIF)

0%

10%

20%

30%

40%

50%

60%

70%

Equities Bonds Alternatives & Cash

GPIF

Top 20 funds - Weighted Avg

Top 20 funds - Simple Avg

Source: Deutsche Bank, Towers Watson, data as of 2012, GPIF, data as of Dec 2013

Last year, a reform panel (The Panel for Sophisticating the Management of Public/Quasi-public Funds) was established under the minister in charge of economic revitalization pursuant to the “Japan revitalization strategy” which was formulated as part of Abe’s growth strategy (the third arrow”). This 7-member panel, led by Takatoshi Ito, the dean of the graduate school of Public Policy at Tokyo University, recommended a number of changes in its final report published in November 20131.

1 “Final Report”, Panel for Sophisticating the Management of Public/Quasi-public Funds, November 2013

15 May 2014

Japan Indices

Deutsche Bank Securities Inc. Page 5

Highlights include:

Wage / price inflation linkage: Since benefits paid out from some funds are linked to nominal wage growth rate and inflation rates, it is reasonable to set investment return targets as specific rates above the nominal wage growth rate or inflation rates.

Reduce bond weighting: Present investment portfolios of public and quasi-public funds that invest heavily in domestic bonds need to be revised to improve returns and hold down interest rate risks.

Increase exposure to alternatives: Under a long-term outlook on benefits and contributions in pension finance, GPIF and the like should diversify investments by investing in new types of assets (including real estate investment trusts, real estate, infrastructure, venture capital, private equity and commodities).

Increase active management: Currently, the ratio of active investments is generally low. GPIF, for example, has only about 20 percent of its domestic equity in actively managed portfolios. Consideration should be made to increase the ratio of active investments, depending on the size and characteristics of each fund.

- Less reliance on the Topix: As a benchmark for passive investments in stocks, many funds track the Topix index. Funds should consider improvements including tolerating some deviation from the index or using other indexes that enable more efficient investment.

Risk management and governance: The panel also recommended implementing new risk management measures and a better governance structure over the medium term. It also recommended reestablishing the fund as new type of legal entity.

In the same report, the reform panel outlined a roadmap for the reform of GPIF and addressed the improvements to be made across three timelines: 1) immediately, 2) in approximately one year, and 3) after legal revision has been completed.

Issues to be addressed immediately include

Revise investments within the current policy asset mix (flexible investment using the permissible range of deviation, reviewing active investment)

Consider investment return targets and degree of risk tolerance

Consider the use of new benchmarks in passive investments

Issues to be addressed in about one year include:

Decide on a new policy asset mix based on the results of the reexamination of pension finance

Invest in new types of assets (mainly in liquid assets and assets that can be evaluated without difficulty)

Establish “baby” funds for more flexible deployment of capital

Since the release of this report, the GPIF has taken actions dealing with the above mentioned issues that need to be addressed immediately. The domestic bond allocation has decreased from 58% to 55.2%, and the domestic stock allocation increased about 1%, from 16.2% to 17.2%. The international stock allocation has increased from 13.5% to 15.2%. As of Dec. 31, GPIF had 65.8% of its assets in domestic bonds and 10.6% in offshore debt. The total equity allocation is about 32.4%

15 May 2014

Japan Indices

Page 6 Deutsche Bank Securities Inc.

with international stocks representing 15% of the total assets. Please see Figure 5 below for a more detailed overview of their asset allocation.

Takatoshi Ito, head of the reform panel, said in an interview in February 2 that GPIF should put 50% its assets in stocks and increase its yearly return goal to 5 percent. Members of the advisory group also recommended adding new assets such as real-estate trusts, infrastructure and private-equity investments and commodities.

It is reported that GPIF said on Feb. 28 that it will put as much as $2.7 billion in infrastructure investments over the next five years, in partnership with Development Bank of Japan Inc. and Ontario Municipal Employees Retirement System 3.

Another important committee that has significant influence over GPIF’s asset allocation and operations is the Investment Advisory Committee (IAC), appointed by the Ministry of Health, Labour, and Welfare (“MHLW”). It monitors the implementation of GPIF’s polices and advises the president. On April 22, the MHLW announced a reshuffle of the investment committee. Keio University professor Yasuhiro Yonezawa will be the head of the committee, and three members from the above mentioned advisory group, who spearheaded changes in the fund’s strategy to achieve higher return, will also join the committee. The committee members will be reduced to 8, and only two of the 10 previous members will stay on the committee. The new committee will play a leading role in setting GPIF’s new investment allocation expected to be released in June.

There is also a 21-member government appointed advisory group including 6 IAC members, helping the MHLW conduct a 5-yearly review of GPIF’s basic portfolio. This year is the final year of the most recent 5-year mid-term plan. Major changes in asset allocation are expected with the introduction of the new mid-term plan. The transition will not happen in one day and we expect its impact should be gradual and last for some time. The new recommendations on the asset allocation are likely to be formalized by June, while the implementation is likely to begin immediately after the announcement.

2 “Japan’s GPIF Should Own $600 Billion of Stocks”, Anna Kitanaka and Shigeki Nozawa, Bloomberg news, 17-Feb-2014. 3 “GPIF Shakes Up Committee with Three Abe Panel Members”, Anna Kitanaka and Shigeki Nozawa, Bloomberg news, 22-Apr-2014.

15 May 2014

Japan Indices

Deutsche Bank Securities Inc. Page 7

Figure 5: Current Asset Allocation in GPIF’s Portfolio as of December 2013

Asset CategoryCurrent Target

Alloance Range (+/-)

Upper Bound

Lower Bound

Current Allocation

Market Value (Y billion)

Domestic Bonds 60% 8% 68% 52% 55.22% 71,003 International Bonds 11% 5% 16% 6% 10.60% 13,636 Total Bond 71% 65.8% 84,639

Domestic Stocks 12% 6% 18% 6% 17.22% 22,147 International Stocks 12% 5% 17% 7% 15.18% 19,522 Total Stock 24% 32.4% 41,669

Short-term Assets 5% 5% 5% 1.77% 2,271

Total 100.0% 100.0% 128,579

55.22%

10.60%

17.22%

15.18%

1.77%

Domestic Bonds

International Bonds

Domestic Stocks

International Stocks

Short-term Assets

Source: Deutsche Bank, GPIF

New Domestic Equity Benchmarks: more diversified and spotlight on smart beta

In April, GPIF altered its domestic stock strategy, and awarded 14 active mandates and 10 passive mandates for its Japanese equities allocations, eight of which had existing mandates from the fund 4. The fund will introduce a performance-based fee structure for active managers. GPIF is also planning active investments in a wider range of foreign bonds. These announced changes are quite consistent with the recommendations from the reform panel, in our view. Highlights of the main changes include:

For Passive investments, in addition to Topix, select three new indices: Nikkei 400, MSCI Japan, and Russell Nomura Prime.

For Active investment, in addition to the traditional active management, allocate some assets to Smart Beta active management, targeting to effectively capture mid- to long-term excess returns through indexing strategy. This represents the first time GPIF will employ the idea of smart beta.

4 “GPIF’s Selection of Domestic Equity Investment Managers and Revision of Manager Structure”, GPIF, 4-Apr-2014.

15 May 2014

Japan Indices

Page 8 Deutsche Bank Securities Inc.

For traditional active management, GPIF has selectively chosen managers from a wide range of investment strategies including strategies such as increasing shareholder value via engagement with company management.

Figure 6: Revision of Manager Structure for Domestic Equity Investment

TOPIX

Passive Investments (TOPIX)

JPX-Nikkei 400

MSCI Japan

Russell Nomura Prime

Smart Beta Active Management

Traditional Active Management

Traditional Active Management

Current New (Potential)

Pas

sive

In

vest

men

tsA

ctiv

e In

vest

men

ts

- MSCI Japan Small- Nomura RAFI Ref- S&P GIVI

Ind

exin

gS

trat

egy

Source: Deutsche Bank, GPIF

New asset allocation could potentially inject over $100 bn to domestic equity market

GPIF plans to complete its new five-yearly plan by June of this year. Based on the recommendations from the various committee members made public, we have analyzed three potential scenarios on GPIF’s new allocations. The purpose of this analysis is not to predict exactly what the new allocation will be, but rather to gauge the magnitude of the potential impact of the upcoming changes.

Scenario 1 assumes a more aggressive move to riskier assets (the allocation to equity will increase from the current 33% to 50%, while bond allocation will decrease from the current 65.8% to 40%). Scenario 3 reflects a more conservative change (Equity weight to increase from 33% to 40%, while bond weight to decrease to 57%). Scenario 2 is in between Scenario 1 and Scenario 3. In addition, we also assume the allocation to other assets including Real Estate and Private Equity to gradually increase from 1% to 5%. Again we are not trying to predict GPIF’s new allocation, but rather to analyze the impact if GPIF shifts assets between asset classes. As we do not expect the reshuffle of GPIF’s asset allocation to be a one-time event, our Scenario 1 can be viewed as a relatively longer-term asset allocation target, while Scenario 3 is more likely to reflect potential near-term changes. We estimate there could be significant new money injected to the domestic equity market ranging from $50 bn to over $100 bn.

The downside is obviously felt in the bond market if GPIF’s exposure to stocks comes at the expense of buying Japanese government bonds. Some have speculated that the Bank of Japan, already a big JGB buyer, may act to fill the void to prevent a precipitous market selloff.

The full impact of this major shift in GPIF’s asset allocation could potentially be much larger as other public and private pension funds and life insurers follow suit. As discussed above, Japan has the second largest base of pension assets in the world.

15 May 2014

Japan Indices

Deutsche Bank Securities Inc. Page 9

Besides GPIF, Japan has two other pension funds in the top 20 in the world (Figure 2). In addition, it is reported by Asia Asset Management 5 that Japanese mega trust banks, including Sumitomo Mitsui Trust Bank, Mitsubishi UFJ Trust and Banking, Mizuho Trust and Banking, and Resona Bank, will allocate more investment to equities, while reducing government bond holdings, in order to generate higher returns for clients. Corporate pensions make up approximately half of these accounts, equivalent in aggregate to 36 trillion yen (US$352.27 billion). For fiscal year 2014, which began on April 1, asset allocation for combined domestic and overseas equities has been raised to 58%, an increase of four percentage points. The allocation for foreign stocks will mirror that of local shares, at 29% of holdings.

Figure 7: Potential Asset Allocation Change in GPIF’s

Portfolio | Scenario 1 |

Figure 8: Estimated Flows | Scenario 1 |

35.00%

5.00%26.58%

23.42%

5.00%5.00%

Potential weights

Domestic Bonds International BondsDomestic Stocks International StocksShort-term Assets Other assets (incl. Infra & Real Estate)

55.22%

10.60%

17.22%

15.18%

1.77%

Current weights

(45,000) (30,000) (15,000) - 15,000 30,000

Bonds

Stocks

Short-term Assets

Other assets (incl. Infra & Real Estate)

Potential Flows (¥ billion)

Ass

et C

lass

Domestic International Overall

Source: Deutsche Bank, GPIF

Figure 9: Potential Asset Allocation Change in GPIF’s

Portfolio | Scenario 2 |

Figure 10: Estimated Flows | Scenario 2 |

43.00%

6.00%

23.92%

21.08%

3.00% 3.00%

Potential weights

Domestic Bonds International BondsDomestic Stocks International StocksShort-term Assets Other assets (incl. Infra & Real Estate)

55.22%

10.60%

17.22%

15.18%

1.77%

55.22%

10.60%

17.22%

15.18%

1.77%

Current weights

55.22%

10.60%

17.22%

15.18%

1.77%

Current weights

(30,000) (15,000) - 15,000 30,000

Bonds

Stocks

Short-term Assets

Other assets (incl. Infra & Real Estate)

Potential Flows (¥ billion)

Ass

et C

lass

Domestic International Overall

Source: Deutsche Bank, GPIF

5 “Japan’s mega trust banks up equities allocation”, Asia Asset Management, 29-Apr-2014

15 May 2014

Japan Indices

Page 10 Deutsche Bank Securities Inc.

Figure 11: Potential Asset Allocation Change in GPIF’s

Portfolio | Scenario 3 |

Figure 12: Estimated Flows | Scenario 3 |

49.00%

8.00%

21.26%

18.74%

2.00% 1.00%

Potential weights

Domestic Bonds International BondsDomestic Stocks International StocksShort-term Assets Other assets (incl. Infra & Real Estate)

55.22%

10.60%

17.22%

15.18%

1.77%

Current weights

(30,000) (15,000) - 15,000 30,000

Bonds

Stocks

Short-term Assets

Other assets (incl. Infra & Real Estate)

Potential Flows (¥ billion)

Ass

et C

lass

Domestic International Overall

Source: Deutsche Bank, GPIF

Equity allocations may act as a positive catalyst

These potential shifts could provide significant support for the market going forward. Japan’s markets have been under pressure year-to-date with the Nikkei 225 and Topix down 11.6% and 9.2% respectively. The Japanese benchmark indices are the worst performing global indices on the year. Concerns around Abenomics’ efficacy, disappointment with the lack of additional measures by the BOJ, the slowdown in Yen weakness and profit taking have weighed on the market in 2014. More recently, increased concerns surrounding the hike in the consumption tax have pressured the Nikkei, resulting in the index re-testing the key 14,000 level.

Figure 13: Nikkei Performance Relative to S&P 500 and MSCI World in JPY Terms

0%

10%

20%

30%

40%

50%

60%

70%

Dec

-12

Jan-

13

Feb-

13

Mar

-13

Mar

-13

Apr

-13

May

-13

May

-13

Jun-

13

Jul-1

3

Jul-1

3

Aug

-13

Sep

-13

Sep

-13

Oct

-13

Nov

-13

Dec

-13

Dec

-13

Jan-

14

Feb-

14

Feb-

14

Mar

-14

Apr

-14

Apr

-14

Nor

mal

ized

Ret

urns

(%)

S&P 500 (JPY Terms) MSCI World (JPY Terms) Topix JPX Nikkei 400

Source: Deutsche Bank, Bloomberg Finance LP

We have previously highlighted the potential risks to Japan’s equity markets through this period (“Sell in May? Positioning for Japan’s consumption tax hike”, 26 Mar 14). We feel there can be continued weakness over the immediate term, but believe that any weakness presents a compelling buying opportunity. Deutsche Bank remains positive on the medium- to longer-term outlook for Japan, based on our strong US Dollar thesis and the gains from reform.

15 May 2014

Japan Indices

Deutsche Bank Securities Inc. Page 11

Figure 14: Value Traded on the Tokyo Stock Exchange – last 10 years

-

10,000

20,000

30,000

40,000

50,000

60,000

Dec

-04

Jun-

05

Dec

-05

Jun-

06

Dec

-06

Jun-

07

Dec

-07

Jun-

08

Dec

-08

Jun-

09

Dec

-09

Jun-

10

Dec

-10

Jun-

11

Dec

-11

Jun-

12

Dec

-12

Jun-

13

Dec

-13

Val

ue T

rade

d (U

S$ m

n)

TSE1/TSE2 Daily Value Traded

Source: Deutsche Bank, Bloomberg Finance LP

The timing of this current weak patch is happening at the same time as GPIF’s potential re-allocation in favor of additional domestic equity exposure. We believe that a positive announcement on GPIF’s investment plans could provide a positive catalyst for the markets. While the exact potential buying impact remains uncertain, we believe it should be positive for sentiment, which has been waning in recent months.

The high end of our domestic flow estimate is approximately US$ 100bn. The TSE has seen average daily turnover of approximately US$ 21bn in 2014. While the timing and exact size of any GPIF additional allocation remains uncertain, we believe it should be positive from a flow perspective as well, especially for constituents of the newly proposed benchmarks, such as the Nikkei 400.

Figure 15: Rolling 3m Nikkei / USDJPY correlation – Last 5 years

-20%

0%

20%

40%

60%

80%

100%

Sep

-08

Dec

-08

Mar

-09

Jun-

09

Sep

-09

Dec

-09

Mar

-10

Jun-

10

Sep

-10

Dec

-10

Mar

-11

Jun-

11

Sep

-11

Dec

-11

Mar

-12

Jun-

12

Sep

-12

Dec

-12

Mar

-13

Jun-

13

Sep

-13

Dec

-13

Mar

-14Rol

ling

3m C

orre

latio

n (%

)

2009 2010 2011 2012 2013 2014 Avg-36.4% Avg-42.4%Avg-17.8% Avg-32.3% Avg-56.9% Avg-46.8%

Source: Deutsche Bank, Bloomberg Finance LP

In addition to providing a general boost in sentiment, the GPIF re-allocation may benefit the following thematic ideas. Currently there is significant uncertainty around the timing and size of any reallocation. These strategies would be more effective if the timing and the size of the allocation are known. Potential themes include:

Least liquid stocks. While a US$100bn additional allocation should be readily absorbed by the market given Japan’s $20bn+ daily turnover levels, not all stocks will be impacted equally. Given that the exact split and timing of the upcoming changes remain uncertain, one strategy would be to look at the least liquid stocks in Nikkei 400 and other indices which are receiving allocations as

15 May 2014

Japan Indices

Page 12 Deutsche Bank Securities Inc.

an interesting way to play pension re-allocation in Japan. Please see section “A closer look” later in the report for the highest flow impacted names for the Nikkei 400 and other indices.

Overlap vs unique constituents. We expect a significant amount of the allocation will go towards the Nikkei 400 and other new indices adopted by GPIF, and we see the indices gaining in significance over time. One strategy would be to look at stocks which are in more than one index. The estimated inflows should be summed up, so we would expect more significant flows than that from any single index. Please see Figure 18 for a comparison of the membership across all indices we discussed in this report. Figure 16 shows the top 20 illiquid stocks that are constituents in all the indices being adopted by GPIF except MSCI Japan small cap. On the other hand, if GPIF reallocates assets from one index to another, for example, moving assets from tracking Topix to tracking Nikkei 400, then those unique constituents in Nikkei 400 but not in Topix would receive more inflows. While these are interesting ideas, we have concerns about the relatively limited liquidity, high concentration in JASDAQ names, and the uncertainty around timing and sizing of any reallocation.

Inclusion/exclusion and reweights. The Nikkei 400 and other new indices adopted by GPIF will conduct annual or semi-annual rebalances this year. Looking for potential inclusion/exclusion or even re-weight names, such as those for Nikkei 400 driven by the 3-year ROE calculation may be an interesting trade. Rebalance dynamics for the Nikkei, Topix and MSCI Japan are somewhat well understood by the market at this point, but with the Nikkei 400 being a new index, and S&P GIVI and RAFI as less known indices, some interesting trading opportunities may develop surrounding their rebalances.

Figure 16: Top 20 Illiquid Stocks with overlap in all the indices*

Ticker NameFlow $

mm

Flow shares

mm Days

9042 JP Equity HANKYU HANSHIN HOLDINGS INC 178.22 32.53 19.46

9041 JP Equity KINTETSU CORP 167.62 47.73 14.36

8377 JP Equity HOKUHOKU FINANCIAL GROUP INC 66.45 34.48 14.27

8334 JP Equity GUNMA BANK LTD/THE 60.87 11.46 14.21

9364 JP Equity KAMIGUMI CO LTD 57.77 6.06 14.07

8369 JP Equity BANK OF KYOTO LTD/THE 77.27 9.49 14.01

9001 JP Equity TOBU RAILWAY CO LTD 135.02 27.60 13.50

9008 JP Equity KEIO CORP 96.87 13.70 12.93

9007 JP Equity ODAKYU ELECTRIC RAILWAY CO LTD 134.24 15.30 12.59

8333 JP Equity JOYO BANK LTD/THE 88.70 18.24 11.96

4581 JP Equity TAISHO PHARMACEUTICAL HOLDINGS CO LTD 87.75 1.19 11.74

9022 JP Equity CENTRAL JAPAN RAILWAY CO 540.46 4.41 11.65

9005 JP Equity TOKYU CORP 181.77 28.90 11.56

4088 JP Equity AIR WATER INC 59.53 4.24 11.46

8418 JP Equity YAMAGUCHI FINANCIAL GROUP INC 55.75 6.05 11.09

3382 JP Equity SEVEN & I HOLDINGS CO LTD 795.41 20.17 10.97

2897 JP Equity NISSIN FOODS HOLDINGS CO LTD 97.53 2.04 10.11

7309 JP Equity SHIMANO INC 201.46 2.02 9.96

8766 JP Equity TOKIO MARINE HOLDINGS INC 563.23 19.12 9.95

9020 JP Equity EAST JAPAN RAILWAY CO 668.36 9.17 9.72

*Except MSCI Japan Small Cap and Nikkei 225 Source: Deutsche Bank, Bloomberg Finance LP. N.B. based on AUM assumptions outlined in the “A closer look” section

15 May 2014

Japan Indices

Deutsche Bank Securities Inc. Page 13

Recent trends in Smart Beta investments6.

The past few years have witnessed the rise of alternative or smart beta indices which are bridging the gap between active and passive index management styles. We see the recent adoption of GPIF to include smart beta benchmarks as part of this global trend.

Smart beta lacks a precise definition and generally includes any rules-based strategy for equity market exposure that uses a scheme other than the market capitalization of the broad market to determine the index constituents and/or the weightings. These strategies offer alternative beta exposures based upon fundamental factors, technical factors, style factors, different weighting schemes, or any combination thereof. A strategy as simple as an Equal-Weight index is considered smart beta. One of the key attractions of this developing suite of indices is the cost efficiency compared to the management fees of active funds. Cynics may state that “smart beta” is sometimes just used as a clever marketing term; however we believe that if used wisely, these products are a valuable tool in portfolio construction.

Smart beta strategies saw massive growth in 2013 as investors sought higher risk-adjusted returns through lower-cost, index products. Around 25% of the ETF inflows in 2013 went to alternative beta products. In a recent survey of institutional investors by Cogent research, over half (53%) of managers intend to increase their allocations to smart beta products in the future.7 We expect this interest in smart beta products to continue to be a significant theme in 2014.

Figure 17: The Growth of Smart Beta ETFs Globally

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

US

$ m

illio

ns

Daily Cumulative Cash Flows

Source: Deutsche Bank, Bloomberg Finance LP, Reuters Data as of 30 April 2014 Smart-Beta ETFs is assumed as all non-market-cap and price based index ETFs

Traditionally investors have used market capitalization indices for relatively low-cost passive exposure to equity markets and paid managers to implement active strategies. Smart beta attempts to blend the best of both worlds by offering rules-based products intended to exploit systematic biases or inefficiencies in the market. Most importantly, these smart beta products are offered at a lower cost than actively managed strategies. Many investors use smart beta strategies packaged in an ETF wrapper, but smart beta strategies can also be traded as index swaps.

6 “Synthesizing Equity in 2014”, Pam Finelli, et. al., 17-Dec-2013 7 “Institutions Favor Smart Beta ETFs”, CME Group, 11-Dec-2013

15 May 2014

Japan Indices

Page 14 Deutsche Bank Securities Inc.

While market capitalization-weighted indices are well-diversified and liquid, their implicit bias towards large-cap stocks is sometimes considered less attractive. Market capitalization, a function of price, implicitly over-weights stocks that have been rising and under-weights stocks that have underperformed and may be undervalued. Numerous studies have shown alternative beta strategies have outperformed the market historically over long periods of time. The small-cap and value premiums are classic examples of this. While smart beta strategies have historically outperformed market capitalization strategies on a risk-adjusted basis, this is not always the case over shorter time horizons.

Critics of smart beta in fact argue that these strategies are just cleverly marketed ways of taking active positions on small-cap and value. According to James Montier of GMO, "when [smart beta] strategies are corrected for their exposure to 'value' and 'small,' they exhibit no statistically significant outperformance compared to the cap weighted benchmark." Montier continues to note that now is a particularly inconvenient time to use smart beta as "both value and small have very unattractive expected returns in the U.S. on our data."8

8 “No Silver Bullets in investing (just old snake oil in new bottles).” White Paper. GMO. December 2013.

15 May 2014

Japan Indices

Deutsche Bank Securities Inc. Page 15

Benchmark Comparison

A glimpse at the new benchmarks

The following table provides information on the constituent overlap across all the major indices. Broad indices, such as the Topix and the Russell Nomura Prime, have the most overlap with the remaining indices. With its focus on small caps, the MSCI Japan Small Cap Index has the least overlap with other indices as others don’t have specific small cap focus. Additionally, having a relatively small universe, the Nikkei 225 constituents also have lower overlap. The distinct eligibility criterion for some of the indices has resulted in a number of unique constituents to those particular indices which are not part of any other index. These are the S&P GIVI (19), MSCI Japan Small Cap (18) and Russell Nomura Prime (2). Topix also has 558 unique constituents which is a result of its very broad coverage.

Figure 18: Constituents overlap

Constituents OverlapNikkei 400

MSCI Japan

RN Prime S&P GIVIFTSE RAFI Japan

MSCI JP SC

TopixNikkei 225

Unique constituents

Nikkei 400 400 245 398 291 204 149 388 152 0

MSCI Japan 245 320 314 225 240 0 312 175 0

RN Prime 398 314 999 714 267 650 958 225 2

S&P GIVI 291 225 714 1007 174 615 917 128 19

FTSE RAFI Japan 204 240 267 174 267 26 267 175 0

MSCI JP SC 149 0 650 615 26 875 780 50 18

Topix 388 312 958 917 267 780 1797 225 558

Nikkei 225 152 175 225 128 175 50 225 225 0

Unique constituents 0 0 2 19 0 18 558 0 597

Source: urwqeDeutsche Bank, Bloomberg Finance LP

As we expect the Nikkei 400 is likely to become one of the more followed indices in Japan, we looked to conduct a detailed comparison of it relative to the three other major indices in Japan, the Nikkei 225, the Topix and MSCI Japan. In Figure 19, we summarize many of the key differences between the four indices. We highlight differences in index weight concentration, sector exposure and market cap profile. We also look at the potential ease of trading the new index by assessing how easy it should be to replicate as a cash portfolio, the overall liquidity profile of the index and how difficult it should be to trade the “tail” of the index. We also assess the various futures, options and total return swap options available for each index.

15 May 2014

Japan Indices

Page 16 Deutsche Bank Securities Inc.

Figure 19: Japan Major Index comparison Nikkei 400 Nikkei 225 Topix MSCI Japan

Constituents 400 225 1797 320

Rebalance Annual (Aug)

Annual (Oct) Annual (Oct) Semi-Annual (May/Nov)

Quarterly (Feb/Aug)

Concentration Top 5, 10 and 20 constituents account for 8.1, 15.2 and 27.8%

of the index. Top name is SoftBank at 1.91% of the index

Top 5, 10 and 20 constituents account for 25.4, 33.8 and

46.6% of the index. Top name is Fast Retailing at 8.7% of the

index

Top 5, 10 and 20 constituents account for 13.0, 19.5 and

28.8% of the index. Top name is Toyota at 4.7% of the index.

Overall very diverse given highest number of constituents.

Top 5, 10 and 20 constituents account for 15.6, 22.9 and

33.5% of the index. Top name is Toyota at 5.9% of the index

Sector Exposure Most diversified sector exposure of any of the major

indices (lowest standard deviation). Largest weighting to

Industrials, followed by Consumer Discretionary and

Financials. Underweight Cons Disc and overweight Indust

relative to other indices

Most concentrated sector exposure of the major indices (highest standard deviation of

exposure). Overweight Telecoms , IT, healthcare and Consumer Discretionary. Very underweight Financials (-11%

relative to other major indices).

Very diversified. Largest exposure to Financials, Cons Disc and Industrials. Lowest

sector exposure is to Energy. Overweight Cons Disc (by 2.7%) and underweight Industrials (by 1.9%) relative to the Nikkei 400.

Very diversified. Largest exposure to Consumer

Discretionary, Financials and Industrials. Largest exposure to Financials of any major index at

20%. Underweight Industrials and Consumer Staples relative

to other indices.

Index-Weighted Average Market Cap (US$ mn)

24,555 26,276 28,879 34,126

Market Cap Profile 65.5% and 29.9% of the index weight is from large cap and

mid-cap stocks. Small caps account for 4.6% by index

weight and 32% by number. Index-weighted average market

cap of US$ 24.5 bn

65.2% and 30.6% of the index weight is form large cap and

mid-cap stocks. Small caps account for 4.3% by index

weight and 19.6% by number. Index-weighted average market

cap of US$ 26.2 bn

Largest small-cap bias. 58.8% and 27.2% of the index weight is from large cap and mid-cap stocks. Small and micro caps

account for 14% by index weight and 80.5% by number.

Index-weighted average market cap of US$ 28.9 bn

Most significant large-cap bias. 69.1% and 30.2% of the index

weight is from large cap and mid-cap stocks. Small caps

account for only 0.6% by index weight and 3.8% by number.

Index-weighted average market cap of US$ 34.1 bn

Index-Weighted Average ADV (US$ mn)

111.5 163.4 124.0 147.2

Liquidity The Nikkei 400 has a mixed liquidity profile. It has the

lowest overall index weighted average liquidity, but the "tail"

of the index has superior liquidity to the Topix, though

lower than the Nikkei 225 and the MSCI Japan

The Nikkei 225 has the best liquidity profile of the four

indices, due the fact that it has the least number of stocks and

is top-heavy in very liquid stocks

The Topix has the worst liquidity profile given the large

number of stocks and significant exposure to small-

caps. Its overall average ADV is superior to the Nikkei 400, but

the tail of the Topix is very illiquid, with the last 5% of the

index having an average ADV of US$ 1.5mn per day

MSCI Japan has a very good liquidity profile given its bias

towards larger cap stocks and very low exposure to small-

caps.

Replication Should be relatively easy to replicate, especially relative to

the Topix. Though the liquidity of the last 1% of stocks is not great when compared to the Nikkei 225 and MSCI Japan

Very easy to replicate, though large weightings in Fast

Retailing and Softbank create basis risk for loose

benchmarking. Even the tail of the index is very liquid with

average ADV of US$ 42mn for the last 1% of the index

Very difficult to replicate given "long tail" of illiquid small and

micro-caps

Should be relatively easy to replicate, especially relative to

the Topix

Futures No. Expected to be launched in November

Yes. Extremely liquid. The main Nikkei 225 first contract (NK1)

trades US$ 10bn+ per day. Total futures first contracts on

the Nikkei trade US$ 22bn+ including minis, SGX and CME.

Yes. Not as liquid as the Nikkei, but trades ~US$ 6.9bn per day.

Relatively high open interest

Futures are available on Eurex but have limited liquidity.

Liquidity can be sourced by dealers

Options No. It has been reported by Risk magazine that a few OTC trades

have gone through

Liquid listed market and extremely liquid OTC market

Relatively liquid listed and OTC market, though significantly smaller than the Nikkei 225

N/A

Swaps Liquidity is still nascent Active - often used for hedging option books

Active - often used by local institutions

Active - popular among global investors

Source: Deutsche Bank, Bloomberg Finance LP. N.B. Large cap is defined as having full market cap of greater than US$10bn, followed by mid-cap greater than US$ 2bn, small-cap at greater than US$ 300mn and micro cap less than US$ 300mn.

15 May 2014

Japan Indices

Deutsche Bank Securities Inc. Page 17

JPX Nikkei 400: Benefits of the Topix without the Tail? As highlighted in the previous table, one of the consistent issues with the Topix is its high number of constituents and the fact that the “tail” consists of a large number of relatively illiquid small caps. This can be seen below in the stark difference between the distribution of large-, mid-, and small-caps contribution to index weighting and the total number of constituents across the four major indices. The Nikkei 400, while having a similar correlation profile and slightly superior long-term returns, should be easier to replicate and implement than the Topix. When futures contracts are introduced, which is expected to be in November, it should also be easier to hedge.

Figure 20: Stock Size Distribution – Index Weight Figure 21: Stock Size Distribution – No. of Constituents

0%

20%

40%

60%

80%

100%

NKY 400 NKY TPX MXJPMicro Cap Small Cap Mid Cap Large Cap

0%

20%

40%

60%

80%

100%

NKY 400 NKY TPX MXJP

Micro Cap Small Cap Mid Cap Large Cap

Source: Deutsche Bank, Bloomberg Finance LP. N.B. Large cap is defined as having full market cap of greater than US$10bn, followed by mid-cap greater than US$ 2bn, small-cap at greater than US$ 300mn and micro cap less than US$ 300mn

Source: Deutsche Bank, Bloomberg Finance LP. N.B. Large cap is defined as having full market cap of greater than US$10bn, followed by mid-cap greater than US$ 2bn, small-cap at greater than US$ 300mn and micro cap less than US$ 300mn

While the overall index-weighted liquidity profile of the Nikkei 400 is slightly less than the Topix with overall average index weighted ADV of US$ 111.5mn vs. US$ 124.0mn for the Topix, it should be easier to implement given the smaller tail impact. The overall ADV profile of the 4 major indices is shown in Figure 22. Fully replicating the Topix is much more difficult as the liquidity of the tail is much lower. Looking at the stocks which make up the 95% - 99% bucket of the Topix’ index weight, there are 576 stocks to trade, representing the 713th through 1,289th constituent of the index. The weighted average daily turnover of these stocks is US$ 1.7mn. Looking at the last 1% of the Topix, stocks 1,290 through 1,797, the weighted average stock has an ADV of US$ 0.656mn. This can be seen below in Figure 23.

The Nikkei 400 has weighted average ADV of US$ 8.4mn for the 95 – 99% bucket and US$ 3.6mn for the last 1% of the index. The Nikkei 225 and MSCI Japan show even higher liquidity in their tails, a function of their smaller number of constituents.

Figure 22: Index Average ADV Profile - Cumulative Figure 23: Index Avg ADV Profile –Weighting Buckets

64

128

256

512

1024

2048

0% 20% 40% 60% 80% 100%

Wei

ghte

d A

DV

(US

$ m

n, L

og)

Cumulative Index Weight (%)

JPX Nikkei 400 Nikkei 225 Topix MSCI Japan

0.5

2

8

32

128

512

0- 20% 20-40% 40-60% 60-80% 80-90% 90-95% 95-99% 99-100%W

eigh

ted

AD

V (U

S$m

n, L

og )

Index Weighting BucketsJPX Nikkei 400 Nikkei 225 Topix MSCI Japan

Source: Deutsche Bank, Bloomberg Finance LP. Represents the cumulative average liquidity profile of the index as you move from the largest constituents (LHS) to the smallest (RHS)

Source: Deutsche Bank, Bloomberg Finance LP. Represents the weighted average liquidity of the index at various weighting buckets. For example 99 – 100% represents the weighted liquidity of the last 1% of the index.

15 May 2014

Japan Indices

Page 18 Deutsche Bank Securities Inc.

Valuation Summary Figure 24 shows a valuation summary of the major traditional and smart beta indices in Japan. On a trailing basis, the Nikkei 400 looks relatively more attractive relative to peers, with lower P/E, in-line P/B and higher ROE. That said, the Nikkei 400 looks in-line with other major indices on a forward looking basis based on Bloomberg consensus data. On 1-year forward data (“FY1”), the index still has slightly above average ROE at 8.7% vs. 8.6% average. The index’s forward Price to Book ratio though is higher than average, at 1.2x versus an average of 1.1x. A similar trend can be seen in the 2-year forward (“FY2”) data. Similarly, the Nikkei 400’s trailing P/E of 14.0 is more attractive than the group average of 14.3, but the index is more expensive on a FY1 basis at 13.5x vs. 13.3x.

Figure 24: Japan Major Index Comparison Name P/E (TTM) P/E FY1 P/E FY2 P/B (TTM) P/B (FY1) P/B (FY2) ROE

(TTM)ROE (FY1) ROE (FY2) EV/EBITD

A (TTM) EV/EBITD

A (FY1)EV/EBITD

A (FY2)

JPX Nikkei Index 400 14.0 13.6 12.4 1.3 1.2 1.1 9.5 8.7 8.8 9.0 8.8 8.2

Nikkei 225 18.6 16.2 14.6 1.5 1.4 1.3 8.4 9.5 9.8 8.9 8.3 7.8

Topix Index 13.8 13.2 11.9 1.2 1.1 1.1 9.0 8.6 8.7 9.1 8.6 8.0

Topix Core 30 Idx 11.6 11.9 10.8 1.2 1.1 1.0 10.7 8.5 8.6 9.6 9.6 8.9

Topix 500 Index 13.6 13.2 11.9 1.2 1.1 1.1 9.2 8.6 8.7 9.2 8.7 8.1

Msci Japan 13.5 13.0 11.7 1.2 1.1 1.1 9.4 8.7 8.8 9.5 9.0 8.4

Msci Japan Small Cap 14.8 13.2 11.9 1.0 1.0 0.9 6.9 7.5 8.1 8.6 7.9 7.3

FTSE RAFI Japan 12.1 12.1 10.7 1.0 1.0 0.9 8.9 8.3 8.5 8.4 8.0 7.4

Average 14.0 13.3 12.0 1.2 1.1 1.1 9.0 8.5 8.7 9.0 8.6 8.0

Div Yld (TTM)

Div Yld (FY1)

Div Yld (FY2)

5-Year Change

3-Year Change

2-Year Change

1-Year Change

YTD Change

3m Change

1m Change

JPX Nikkei Index 400 1.9 2.1 2.2 39.5 42.2 55.9 -3.4 -8.5 0.5 4.4

Nikkei 225 1.7 1.8 1.9 58.4 49.3 60.5 -2.4 -11.6 0.6 3.6

Topix Index 2.0 2.0 2.2 37.2 40.9 56.4 -3.9 -9.1 -0.1 4.4

Topix Core 30 Idx 2.4 2.5 2.8 22.2 36.8 57.4 -5.5 -11.2 -1.1 5.1

Topix 500 Index 2.0 2.1 2.3 34.9 39.5 56.5 -3.9 -9.4 -0.1 4.5

Msci Japan 2.0 2.2 2.4 35.4 38.6 56.0 -4.5 -9.9 -0.6 4.1

Msci Japan Small Cap 2.0 1.9 2.1 45.6 16.8 21.0 -3.3 -5.0 -0.7 2.5

FTSE RAFI Japan 2.2 2.3 2.5 35.3 37.5 58.5 -3.7 -9.2 -0.3 4.6

S&P Givi Japan Jpy 47.4 47.1 57.9 -2.5 -7.1 0.8 4.0

Russell Nomura Prime 37.6 40.3 56.0 -3.7 -9.1 -0.1 4.5

Average 2.0 2.1 2.3 38.6 37.7 52.8 -3.8 -9.2 -0.2 4.2 Source: Deutsche Bank, Bloomberg Finance LP. N.B. Fundamental data was unavailable for Russell Nomura Prime and S&P GIVI indices.

Trailing vs. Forward ROE Metrics This differential is trailing versus forward metrics is likely due the Nikkei 400’s selection methodology which uses 3-year trailing ROE as an input. While it would be difficult to use a forward ROE methodology due to constant changes in consensus estimates, we do highlight that this opens up the index to being in situations such as the above, where the Nikkei 400 marginal ROE advantage may not be “worth” the additional valuation costs. This analysis assumes that consensus estimate data is correct, which of course it may not be.

Nikkei 400 Forward ROE vs. P/B The relative additional P/B premium of the above indices is charted relative to ROE in Figure 25 below. We added simple regression lines to give an indication of where the ROE vs. P/B trade-off curve is currently priced based on Bloomberg consensus estimates.

15 May 2014

Japan Indices

Deutsche Bank Securities Inc. Page 19

While a relatively small sample set, based on the universe above, the Nikkei 400 could be considered slightly expensive relative to other major benchmarks at this point in time.

Figure 25: Major Japan Indices – Forward ROE vs. Forward P/B

JPNK400

JPNK400

8.0

8.5

9.0

9.5

10.0

1.0 1.1 1.2 1.3 1.4 1.5

Forw

ard

ROE

(%)

Forward P/BSeries1 Series2 Linear (Series1) Linear (Series2)

Source: Deutsche Bank, Bloomberg Finance LP. N.B. ROE and P/B data was unavailable for Russell Nomura Prime and S&P GIVI indices.

While the ROE calculation may be backward looking, the increased focus on ROE and shareholder returns in general is likely to be positive for the market overall. If the Nikkei 400 develops further cachet, companies may be incentivized to improve returns in order to seek entry, which should be positive. The increased focus of major domestic investors, such as GPIF and other pension funds, should also pressure corporate Japan to look to improve returns.

Cross-index Performance

From a performance perspective, the Nikkei 400 has very similar performance to other broad-based market-capitalization weighted indices in Japan, such as the Topix and the Russell / Nomura Prime index. Over the last 3-years, the Nikkei 400 has seen price return of 42.2%, relatively in line with the Topix and Prime indices at 40.9% and 40.3%. On a 1-year basis, the Nikkei 400 has returned -3.4% vs. the Topix and Prime at -3.9% and -3.7%, respectively.

Figure 26: Traditional Benchmark Performance – 1 year Figure 27: Smart Beta Benchmark Performance – 1 year

-15%-10%-5%0%5%

10%15%20%

May

-13

Jun-

13

Jul-1

3

Aug

-13

Sep

-13

Oct

-13

Nov

-13

Dec

-13

Jan-

14

Feb-

14

Mar

-14

Apr

-14

May

-14

Nor

mal

ized

Ret

urn

(%)

R/N Prime TPX NKYMSCI Japan JPNK400

-15%-10%-5%0%5%

10%15%20%

May

-13

Jun-

13

Jul-1

3

Aug

-13

Sep

-13

Oct

-13

Nov

-13

Dec

-13

Jan-

14

Feb-

14

Mar

-14

Apr

-14

May

-14

Nor

mal

ized

Ret

urn

(%)

S&P GIVI RAFIMSCI Japan Small JPNK400

Source: Deutsche Bank, Bloomberg Finance LP, Nikkei Source: Deutsche Bank, Bloomberg Finance LP, Nikkei

15 May 2014

Japan Indices

Page 20 Deutsche Bank Securities Inc.

On a longer term basis, the Nikkei 400 has shown better relative price performance returning 39.5% on a 5-year basis versus the Topix and Prime with 37.2% and 37.6% price return. Our pro-forma Nikkei 400 data goes back to September 2006 and has declined -20.4% relative to -25.7% and -25.5% for the Topix and Russell / Nomura Prime indices, respectively.

Figure 28: Traditional Benchmark Performance – 2006 to

Current

Figure 29: Smart Beta Benchmark Performance – 2006 to

Current

-60%

-40%

-20%

0%

20%

Sep

-06

Mar

-07

Sep

-07

Mar

-08

Sep

-08

Mar

-09

Sep

-09

Mar

-10

Sep

-10

Mar

-11

Sep

-11

Mar

-12

Sep

-12

Mar

-13

Sep

-13

Mar

-14

Nor

mal

ized

Ret

urn

(%)

R/N Prime TPX NKYMSCI Japan JPNK400

-60%

-40%

-20%

0%

20%

Sep

-06

Mar

-07

Sep

-07

Mar

-08

Sep

-08

Mar

-09

Sep

-09

Mar

-10

Sep

-10

Mar

-11

Sep

-11

Mar

-12

Sep

-12

Mar

-13

Sep

-13

Mar

-14

Nor

mal

ized

Ret

urn

(%)

S&P GIVI RAFIMSCI Japan Small JPNK400

Source: Deutsche Bank, Bloomberg Finance LP, Nikkei Source: Deutsche Bank, Bloomberg Finance LP, Nikkei

Note that the above data primarily represents a period when the Nikkei 400 did not exist. As it becomes more widely accepted, its performance may diverge going forward. Also, if an increased focus on ROE begins to take hold in Japan, we may also see additional divergence in the index’s performance. This “ROE halo” impact may be tempered though by the backward looking nature of the index’s calculation methodology as we described earlier.

Performance has been more differentiated relative to other indices such as the Nikkei 225, likely due to its price weighting methodology and some of the previously highlighted smart beta indices, such as the RAFI and the GIVI.

Figure 30: Correlation to Nikkei 400 - Traditional

Benchmarks

Figure 31: Correlation to Nikkei 400 – Smart Beta

Benchmarks

90.0%

92.0%

94.0%

96.0%

98.0%

100.0%

Dec

-06

May

-07

Oct

-07

Mar

-08

Aug

-08

Jan-

09Ju

n-09

Nov

-09

Apr

-10

Sep

-10

Feb-

11Ju

l-11

Dec

-11

May

-12

Oct

-12

Mar

-13

Aug

-13

Jan-

14

3-m

onth

Cor

rela

tion

(%)

JPNK400 & TPX JPNK400 & R/N Prime JPNK400 & MSCI Jp JPNK400 & NKY

50%

60%

70%

80%

90%

100%

90%

92%

94%

96%

98%

100%

Sep

-06

Apr

-07

Nov

-07

Jun-

08Ja

n-09

Au g

-09

Mar

-10

Oct

-10

Ma y

-11

Dec

-11

Jul-1

2Fe

b-13

Sep

-13

Apr

-143-

mon

th C

orre

latio

n (%

)

JPNK400 & S&P GIVIJPNK400 & RAFIJPNK400 & MSCI Jp Small (RHS)

Source: Deutsche Bank, Bloomberg Finance LP, Nikkei Source: Deutsche Bank, Bloomberg Finance LP, Nikkei

In line with the similar performance profile, the Nikkei 400 has been very highly correlated with other traditional benchmark indices in Japan. Since September 2006, the Nikkei 400’s rolling 3-month correlation with the Topix, MSCI Japan and Russell

15 May 2014

Japan Indices

Deutsche Bank Securities Inc. Page 21

Nomura Prime indices has never been below 99%. The correlation has been lower with the Nikkei 225 and other non-traditional indices as can be seen above.

Figure 32: Nikkei 400 less Topix – Daily Return Differentials

-1.0%

-0.5%

0.0%

0.5%

1.0%

Sep

-06

Jan-

07

Ma y

-07

Sep

-07

Jan-

08

May

-08

Sep

-08

Jan-

09

May

-09

Sep

-09

Jan-

10M

ay-1

0

Sep

-10

Jan-

11

Ma y

-11

Sep

-11

Jan-

12

May

-12

Sep

-12

Jan-

13

Ma y

-13

Sep

-13

Jan-

14

Diff

eren

ce in

Dai

ly R

etur

ns (%

)

Daily Change Difference - JPNK400 less TPX Average = 0.004%

Source: Deutsche Bank, Bloomberg Finance LP, Nikkei

The performance similarity with the Topix can be seen in Figure 32 above, which charts the daily performance differential in the Nikkei 400 versus the Topix since September 2006. The average daily performance difference over that period is 0.004%, or 4/10 of a basis point. The largest divergence occurred following the Tohoku earthquake in March 2011 with a 67bps outperformance of the Nikkei 400 relative to the Topix.

Figure 33: Relative Correlation vs. USDJPY – Traditional

Benchmarks

Figure 34: Relative Correlation vs. USDJPY – Smart Beta

Benchmarks

-60%

-10%

40%

90%

Dec

-06

May

-07

Oct

-07

Mar

-08

Aug-

08Ja

n-09

Jun-

09N

ov-0

9A

pr-1

0Se

p-10

Feb-

11Ju

l-11

Dec

-11

May

-12

Oct

-12

Mar

-13

Aug

-13

Jan-

143-m

onth

Cor

rela

tion

(%)

TPX / JPY R/N Prime / JPYMSCI Jp / JPY JPNKY400 / JPY NKY / JPY

-60%-40%-20%

0%20%40%60%80%

Dec

-06

May

-07

Oct

-07

Mar

-08

Au g

-08

Jan-

09Ju

n-09

Nov

-09

Apr

-10

Sep

-10

Feb-

11Ju

l-11

Dec

-11

Ma y

-12

Oct

-12

Mar

-13

Aug

-13

Jan-

143-m

onth

Cor

rela

tion

(%)

S&P GIVI / JPY RAFI / JPYMSCI Jp Small / JPY JPNKY400 / JPY

Source: Deutsche Bank, Bloomberg Finance LP, Nikkei Source: Deutsche Bank, Bloomberg Finance LP, Nikkei

Figures 33 and 34, above, show the various Japanese benchmark’s correlation with USDJPY. All of the indices have a similar relationship to the Yen, with the exception of the MSCI Small Cap index.

15 May 2014

Japan Indices

Page 22 Deutsche Bank Securities Inc.

Figure 35: Rolling 3m Tracking Error vs. Nikkei 400 –

Traditional Benchmarks

Figure 36: Rolling 3m Tracking Error vs. Nikkei 400 –

Smart Beta Benchmarks

0%2%4%6%8%

10%12%14%16%

Sep

-06

Mar

-07

Sep

-07

Mar

-08

Sep

-08

Mar

-09

Sep

-09

Mar

-10

Sep

-10

Mar

-11

Sep

-11

Mar

-12

Sep

-12

Mar

-13

Sep

-13

Mar

-14Rol

ling

3-m

onth

Tra

ckin

g Er

ror (

%)

NKY R/N Prime MSCI Japan TPX

0%5%

10%15%20%25%30%35%

Dec

-06

Jun-

07D

ec-0

7Ju

n-08

Dec

-08

Jun-

09D

ec-0

9Ju

n-10

Dec

-10

Jun-

11D

ec-1

1Ju

n-12

Dec

-12

Jun-

13D

ec-1

3Rol

ling

3-m

onth

Tra

ckin

g Er

ror (

%)

S&P GIVI RAFI MSCI Japan Small

Source: Deutsche Bank, Bloomberg Finance LP, Nikkei Source: Deutsche Bank, Bloomberg Finance LP, Nikkei

Given the similar performance and correlation profiles, the large market-cap weighted indices show very small tracking error relative to Nikkei 400.This can be seen above in Figure 35.

Figure 37: Rolling 3m Realized Volatility – Traditional

Benchmarks

Figure 38: Rolling 3m Realized Volatility – Smart Beta

Benchmarks

0%10%20%30%40%50%60%70%80%

Sep-

06M

ar-0

7Se

p-07

Mar

-08

Sep-

08M

ar-0

9Se

p-09

Mar

-10

Sep-

10M

ar-1

1Se

p-11

Mar

-12

Sep-

12M

ar-1

3Se

p-13

Mar

-14

Rea

lized

Vol

atili

ty (%

)

R/N Prime TPX NKYMSCI Japan JPNK400

0%10%20%30%40%50%60%70%80%

Sep-

06M

ar-0

7Se

p-07

Mar

-08

Sep-

08M

ar-0

9Se

p-09

Mar

-10

Sep-

10M

ar-1

1Se

p-11

Mar

-12

Sep-

12M

ar-1

3Se

p-13

Mar

-14

Rea

lized

Vol

atili

ty (%

)

S&P GIVI RAFIMSCI Japan Small JPNK400

Source: Deutsche Bank, Bloomberg Finance LP, Nikkei Source: Deutsche Bank, Bloomberg Finance LP, Nikkei

The volatility profile of the traditional benchmarks is relatively similar. The Nikkei 225 has shown an average premium of 2 volatility points over the Nikkei 400 throughout the period. The Topix has shown an average 0.2% volatility premium, in line with its high correlation to the Nikkei 400.

Increasing adoption of Nikkei 400 may impact its dynamic with other indices As we have previously highlighted, the Nikkei 400 has very similar characteristics to the Topix and the Russell / Nomura Prime, and to a lesser extent, MSCI Japan. It may diverge going forward as it begins to become a more widely accepted index. This would especially be the case if ROE takes on a more important role in the Japanese market.

15 May 2014

Japan Indices

Deutsche Bank Securities Inc. Page 23

A Closer Look

Nikkei 400

JPX-Nikkei 400 is designed to encourage investment in stocks with high return on equity, which is a measure of how well companies use shareholders’ money to generate income. This new index aims to promote the quality, corporate governance and capital efficiency of Japanese companies using the power of the market. GPIF and other major pension funds have recently chosen this index as benchmark. Although they have not announced the size of their portfolio yet, we expect that it will be in the billions of dollars. In addition, there are now more than 20 funds (ETFs and Open-ended Funds) in Japan tracking the index, despite it only having launched in January 2014. It has attracted close to ¥87 billion (US$850 million) in inflows so far. The bulk of the flows has come from the three exchange-traded funds (ETFs) that Nomura Asset Management, Nikko Asset Management and Mitsubishi UFJ Asset Management set up to track the new index. The three ETFs garnered a combined ¥50 billion (US$490 million) in assets as of end of April. Osaka Exchange, Inc. (OSE) also announced that it will introduce futures based on JPX-Nikkei 400 by the end of November 2014.

Figure 39: Cumulative Inflows to ETFs Tracking Nikkei 400

-

100

200

300

400

500

600

US

$ m

illio

n

Nikkei Index 400 ETFs - Daily Cum. Flows

Source: Deutsche Bank, Bloomberg Finance LP

All these will put pressure on Japanese firms which don’t have a high ROE scores to perform better, otherwise they won’t be members of this important benchmark. Generally speaking, Japanese companies perform poorly on ROE metrics when compared with those in other countries in the region or in the US (9.49 for Nikkei 400, and 8.95 for Topix, vs. 15.08 for S&P 500, and 12.83 for MSCI Asia ex Japan). Japanese companies tend to hold on to less-profitable businesses and maintain large capital bases without investing for growth or distributing cash to investors. Some Japanese companies may start to change in response to this new index, however, the process may take a long time as relatively strong labor protection in the close-knit business society of Japan makes it very difficult to layoff workers and unload underperforming assets.

15 May 2014

Japan Indices

Page 24 Deutsche Bank Securities Inc.

Highlights of index methodology Eligible universe: Stocks listed in TSE (1st Section, 2nd section, Mothers, JASDAQ)

Excluding issues listed less than 3 yrs, Liabilities > assets, during any of the past 3 fiscal years, operating deficit, or overall deficit in all of the past 3 fiscal years, to be Delisted, etc.

Constituent selection/Index Calculation

1. The top 1000 issues will be selected: from those eligible based on trading value in the past 3 years and market cap on the base date for selection.

2. Scoring based on Quantitative Indicators: 1st: 1000 points – 1000th: 1 point. Then, overall score is determined by aggregating those ranking scores with the following weights. : 3 year average ROE (40%), 3-year cumulative operating profit (40%), market cap (20%).

3. Scoring based on Qualitative Indicators: the score is determined so that at most around 10 constituents are different from those chosen with only quantitative score above. Scores based on appointment of Independent Outside Directors (at least 2), Adoption or Scheduled Adoption of IFRS (pure IFRS), Disclosure of English Earnings Information via TDnet (Company Announcements Distribution Service in English).

4. Determination of Constituents: the 400 issues will be selected in descending order of high scores as constituents.

5. Each stock in the index is weighted by its free float market cap.

Sector weight comparison We also compare the sector/industry weights of the Nikkei 400 and Topix. The Nikkei 400 has a bias towards Capital Goods, but is underweight in Automobile & Components and Banks. The Nikkei 400 uses a sector classification system consisting of 6 sectors and 36 industries, which is different from Topix who uses Topix 17 series. They both are different from the GICS sector classification. To make the comparison consistent for all indices we analyze the sector weights based on GICS industry group.

15 May 2014

Japan Indices

Deutsche Bank Securities Inc. Page 25

Figure 40: Industry Group Weights: Nikkei 400 vs. Topix

1.9%

-2.3

%

0.5%

-1.5

%

0.1% 0.

6%

0.6% 1.

0%

0.9%

0.1%

-0.7

%

0.3% 0.

6%

-0.2

%

-0.2

%

-0.1

%

0.3%

0.3%

-1.0

%

0.1%

-0.5

%

-0.1

%

-0.6

%

-0.2

%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

0.0%

3.0%

6.0%

9.0%

12.0%

15.0%

18.0%

Ind

ust

ry G

rou

p W

eig

hts

Nikkei 400TOPIXOver/under weight - rhs

Source: Deutsche Bank, Bloomberg Finance LP, Nikkei, Topix

Illiquid stocks and stocks with largest index weight As GPIF has not released their new asset allocation, we don’t know exactly how much it will allocate to each index. Based on Scenario One discussed above, and assuming that 50% of the additional allocation to passive will be into the Nikkei 400, then the inflow would be close to US$20bn. GPIF is likely to implement this change gradually over a certain period of time. To get a sense of the potential impact, we estimate the most impacted names in the index by total value to trade and days to trade, assuming US$15 bn new money to invest in the index. If the actual inflow is US$5bn, then the impact will be just one third of the numbers in the tables below.

Figure 41: Top 20 Most Illiquid Stocks

Ticker Name% Index Weight Flow $mm

Flow shares

mm Days

3167 JP Equity TOKAI Holdings Corp 0.015% 2.20 0.64 7.26

9031 JP Equity Nishi-Nippon Railroad Co Ltd 0.058% 8.75 2.28 6.37

8012 JP Equity Nagase & Co Ltd 0.060% 9.03 0.74 6.10

9045 JP Equity Keihan Electric Railway Co Ltd 0.102% 15.28 3.71 5.94

9042 JP Equity Hankyu Hanshin Holdings Inc 0.323% 48.51 8.86 5.30

8544 JP Equity Keiyo Bank Ltd/The 0.042% 6.29 1.43 5.14

8600 JP Equity TOMONY Holdings Inc 0.028% 4.24 1.00 5.10

9003 JP Equity Sotetsu Holdings Inc 0.072% 10.77 3.02 5.09

9948 JP Equity Arcs Co Ltd 0.040% 5.93 0.30 5.01

8051 JP Equity Yamazen Corp 0.022% 3.23 0.50 4.76

8356 JP Equity Juroku Bank Ltd/The 0.051% 7.60 2.18 4.63

2782 JP Equity Seria Co Ltd 0.041% 6.08 0.16 4.61

8385 JP Equity Iyo Bank Ltd/The 0.111% 16.70 1.86 4.57

7458 JP Equity Daiichikosho Co Ltd 0.055% 8.26 0.29 4.42

4045 JP Equity Toagosei Co Ltd 0.045% 6.79 1.62 4.39

3098 JP Equity Cocokara fine Inc 0.026% 3.84 0.14 4.13

8359 JP Equity Hachijuni Bank Ltd/The 0.117% 17.48 3.20 4.09

7451 JP Equity Mitsubishi Shokuhin Co Ltd 0.021% 3.20 0.14 4.04

9041 JP Equity Kintetsu Corp 0.311% 46.64 13.28 4.00

1417 JP Equity Mirait Holdings Corp 0.025% 3.69 0.42 3.92

Source: Deutsche Bank, Bloomberg Finance LP., Nikkei, Note: Assuming US$15bn of inflows

15 May 2014

Japan Indices

Page 26 Deutsche Bank Securities Inc.

Figure 42: Top 20 Largest Weights

Ticker Name% Index Weight Flow $mm

Flow shares

mm Days

9984 JP Equity SoftBank Corp 1.909% 286.37 3.86 0.26

6954 JP Equity FANUC Corp 1.766% 264.94 1.47 1.39

6501 JP Equity Hitachi Ltd 1.502% 225.33 31.69 1.62

9432 JP Equity Nippon Telegraph & Telephone Corp 1.476% 221.47 4.00 1.99

4502 JP Equity Takeda Pharmaceutical Co Ltd 1.471% 220.66 4.92 1.50

9433 JP Equity KDDI Corp 1.435% 215.20 4.04 1.38

7203 JP Equity Toyota Motor Corp 1.433% 214.94 3.98 0.49

3382 JP Equity Seven & I Holdings Co Ltd 1.432% 214.82 5.45 2.96

7267 JP Equity Honda Motor Co Ltd 1.405% 210.81 6.38 1.04

8411 JP Equity Mizuho Financial Group Inc 1.399% 209.86 107.28 1.45

2914 JP Equity Japan Tobacco Inc 1.372% 205.76 6.27 1.49

7751 JP Equity Canon Inc 1.332% 199.86 6.36 1.62

8316 JP Equity Sumitomo Mitsui Financial Group Inc 1.273% 190.98 4.84 0.60

8306 JP Equity Mitsubishi UFJ Financial Group Inc 1.273% 190.89 36.01 0.60

8802 JP Equity Mitsubishi Estate Co Ltd 1.259% 188.79 8.34 1.60

8058 JP Equity Mitsubishi Corp 1.211% 181.71 10.16 2.08

8801 JP Equity Mitsui Fudosan Co Ltd 1.210% 181.43 6.14 1.57

4503 JP Equity Astellas Pharma Inc 1.180% 177.00 15.92 2.16

9020 JP Equity East Japan Railway Co 1.180% 176.98 2.43 2.58

9437 JP Equity NTT DOCOMO Inc 1.135% 170.26 10.73 1.66

Source: Deutsche Bank, Bloomberg Finance LP, Nikkei Note: Assuming US$15bn of inflows

Russell Nomura Prime

Russell and Nomura Securities Co., Ltd. produce a family of Japan equity indexes, including the Prime index. The indexes are value weighted and include only common stocks domiciled in Japan. All indexes are subsets of the Russell/Nomura Total Market™ Index, which represents 98% of the investable Japan equity market.

Highlights of index methodology Eligible universe: The Prime index consists of the largest 1,000 securities by available market capitalization in the Russell/Nomura Total Market Index (TMI) containing the top 98% (approximately 1,400 stocks) of the available market capitalization in the Japanese market. Stocks under supervision (examination) and stocks under supervision (confirmation), REITs and Foreign stocks listed in Japan are excluded from the universe for TMI.

Constituent selection/Index Calculation

1. Negative list (exclusion of low liquidity stocks): Stocks ranked 2,001st or lower in terms of average monthly trading value in the year to the regular reconfiguration date of record are excluded.

2. Banding method (900–1,100 rule): Stocks ranked 900 or higher by float-adjusted market capitalization are included in the index, regardless of whether or not they were included in the index prior to the reconfiguration. Stocks ranked 901 to 1,100 are included in the index only if they were

15 May 2014

Japan Indices

Deutsche Bank Securities Inc. Page 27

included in the index prior to the reconfiguration, until 1,000 stocks have been selected. If 1,000 stocks have not been selected after going through the 1,100 stocks in this way, stocks ranked between 901 and 1,100 that were not included in the index prior to the reconfiguration are selected until a total of 1,000 stocks has been selected.

3. Each stock in the index is weighted by its free float market cap.

Sector weight comparison Among all the analyzed indices in this section, Russell Nomura Prime industry group weights are closest with that of Topix. The maximum overweight and underweight percentage across all the industry group are just 0.4% and 0.6% respectively. Again, as Russell and Topix use different sector classification system, to make the comparison consistent for all indices, we analyze the sector weights based on GICS industry group.

Figure 43: Industry Group Weights: Russell Nomura Prime vs. Topix

-0.1

%

-0.6

%

0.1%

0.4%

-0.1

%

0.2%

0.0%

0.3%

-0.3

%

0.0%

-0.2

%

0.1%

0.0%

0.2%

0.1%

0.0%

-0.1

% 0.1%

0.0% 0.

0%

-0.1

%

0.1%

0.0% 0.

1%

-0.8%

-0.6%

-0.4%

-0.2%

0.0%

0.2%

0.4%

0.6%

0.0%

3.0%

6.0%

9.0%

12.0%

15.0%

18.0%

Ind

ust

ry G

rou

p W

eig

hts

Russell Nomura Prime

TOPIX

Over/under weight - rhs

Source: Deutsche Bank, Bloomberg Finance LP, Russell, Topix

Illiquid stocks and stocks with largest index weight As explained above, we don’t know exactly how much GPIF will allocate to each index. Based on Scenario One discussed above, and assuming that 25% of the additional allocation to passive will be into the Nikkei 400, then the inflow would be close to US$10bn. GPIF is likely to implement this change gradually over a certain period of time. To get a sense of the potential impact, we estimate the most impacted names in the index by total value to trade and days to trade, assuming US$5 bn new money to invest in the index. If the actual inflow is US$2bn, then the impact will be just 40% of the numbers in the tables below.

15 May 2014

Japan Indices

Page 28 Deutsche Bank Securities Inc.

Figure 44: Top 20 Most Illiquid Stocks

Ticker Name% Index Weight

Flow $ mm

Flow shares

mm Days

9708 JP Equity IMPERIAL HOTEL,LTD. 0.009% 0.47 0.02 3.95

7914 JP Equity KYODO PRINTING CO.,LTD. 0.006% 0.32 0.12 2.78

8173 JP Equity JOSHIN DENKI CO.,LTD. 0.009% 0.47 0.06 2.74

8066 JP Equity MITANI CORPORATION 0.012% 0.60 0.03 2.69

3201 JP Equity THE JAPAN WOOL TEXTILE CO.,LTD. 0.014% 0.70 0.09 2.43

4958 JP Equity T.HASEGAWA CO.,LTD. 0.011% 0.57 0.04 2.36

8536 JP Equity THE HIGASHI-NIPPON BANK,LIMITED 0.011% 0.54 0.21 2.32

8342 JP Equity THE AOMORI BANK,LTD. 0.016% 0.82 0.30 2.28

8529 JP Equity THE DAISAN BANK,LTD. 0.008% 0.39 0.23 2.25

8395 JP Equity THE BANK OF SAGA LTD. 0.008% 0.39 0.19 2.22