Embed Size (px)

Citation preview

P A C I F I C

Royalty financingHelp your business grow without sacrificing capital

Royalty financing from Anglo Pacific is an overlooked alternative for small to mid cap mining companies to raise funds. This leaflet explains why royalty financing can be considered as an advantageous alternative to debt or equity.

Is royalty financing right for your company?A company demonstrating some of the following characteristics might be a suitable candidate for royalty financing through Anglo Pacific:

• Market capitalisation which does not reflect the true potential value of the project – management should avoid unnecessary dilution of equity and earnings.

• Low forecast cost of production/good operating margin.

• Operates in a stable legal jurisdiction.

• Long (10 years plus) expected production life – not always established in terms of proven reserves but with reasonable expectation from interpretation of geology and level of drilling/operations.

• Multi-project company where financing at the parent company level would dilute its other projects.

A possible example: A company with 80 million shares outstanding at $1 per share looking to raise $16 million towards the cost of a 120,000 ozs p.a. production facility starting up in two years time. The company either issues 20 million shares at 80 cents or grants a 3% royalty. Forecast revenues of $120 million with an EBIT margin of 30%.

Equity

Revenue $120m

NSR 0% $0m

Costs $84m

EBIT $36m

Shares o/s 100 million

Dilution

EPS 20%

Equity 20%

Royalty

Revenue $120m

NSR 3% $3.6m

Costs $84m

EBIT $32.4m

Shares o/s 80 million

Dilution

EPS 10%

Equity nil

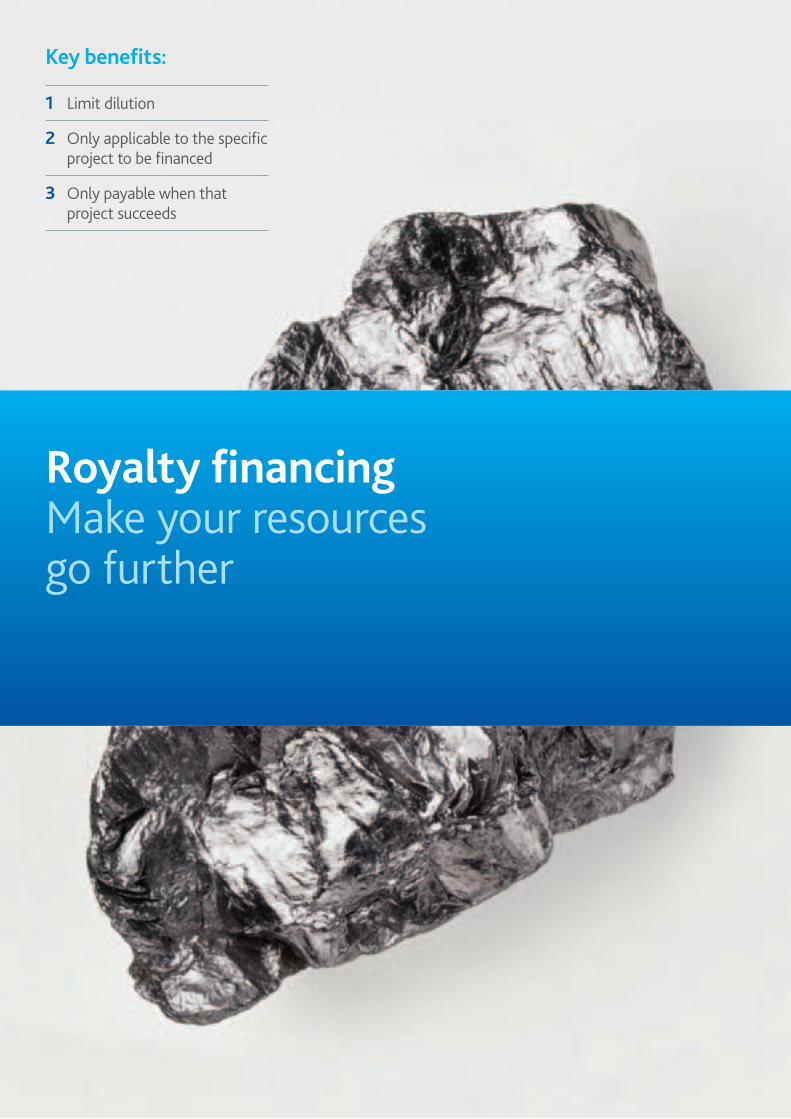

Royalty financingMake your resources go further

Key benefits:

1 Limit dilution

2 Only applicable to the specific project to be financed

3 Only payable when that project succeeds

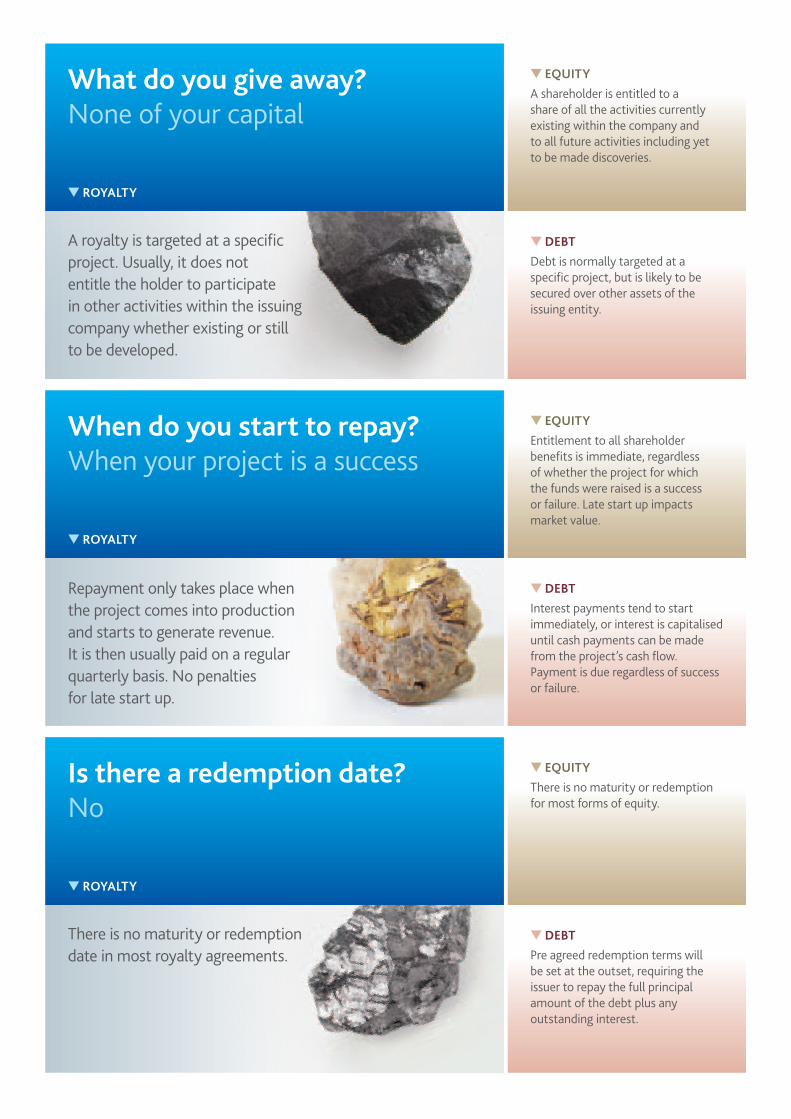

▼ EQUITYEntitlement to all shareholder benefits is immediate, regardless of whether the project for which the funds were raised is a success or failure. Late start up impacts market value.

▼ DEBTInterest payments tend to start immediately, or interest is capitalised until cash payments can be made from the project’s cash flow. Payment is due regardless of success or failure.

When do you start to repay?When your project is a success

▼ ROYALTY

▼ EQUITYThere is no maturity or redemption for most forms of equity.

▼ DEBTPre agreed redemption terms will be set at the outset, requiring the issuer to repay the full principal amount of the debt plus any outstanding interest.

Is there a redemption date?No

▼ ROYALTY

▼ EQUITYA shareholder is entitled to a share of all the activities currently existing within the company and to all future activities including yet to be made discoveries.

▼ DEBTDebt is normally targeted at a specific project, but is likely to be secured over other assets of the issuing entity.

What do you give away?None of your capital

▼ ROYALTY

Repayment only takes place when the project comes into production and starts to generate revenue. It is then usually paid on a regular quarterly basis. No penalties for late start up.

There is no maturity or redemption date in most royalty agreements.

A royalty is targeted at a specific project. Usually, it does not entitle the holder to participate in other activities within the issuing company whether existing or still to be developed.

Ongoing liability?▼ ROYALTY In most cases the issuer has

a contractual obligation to make regular payments according to the terms of the royalty agreement as long as the project is in operation.

▼ EQUITY The commitments are as laid down by applicable company law.

▼ DEBT Various restrictions are frequently imposed by the debt provider, such as covenants to protect the loan and restrict use of cash flow until loan repayments have been made.

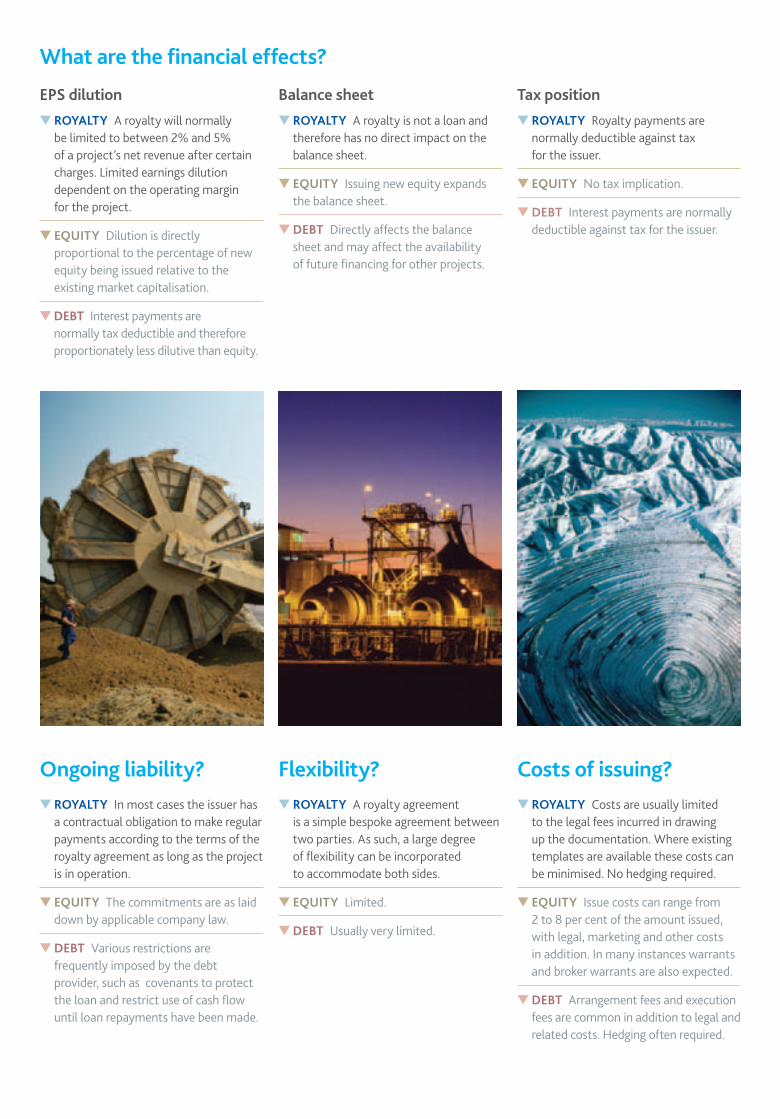

Flexibility?▼ ROYALTY A royalty agreement

is a simple bespoke agreement between two parties. As such, a large degree of flexibility can be incorporated to accommodate both sides.

▼ EQUITY Limited.

▼ DEBT Usually very limited.

Costs of issuing?▼ ROYALTY Costs are usually limited

to the legal fees incurred in drawing up the documentation. Where existing templates are available these costs can be minimised. No hedging required.

▼ EQUITY Issue costs can range from 2 to 8 per cent of the amount issued, with legal, marketing and other costs in addition. In many instances warrants and broker warrants are also expected.

▼ DEBT Arrangement fees and execution fees are common in addition to legal and related costs. Hedging often required.

EPS dilution

▼ ROYALTY A royalty will normally be limited to between 2% and 5% of a project’s net revenue after certain charges. Limited earnings dilution dependent on the operating margin for the project.

▼ EQUITY Dilution is directly proportional to the percentage of new equity being issued relative to the existing market capitalisation.

▼ DEBT Interest payments are normally tax deductible and therefore proportionately less dilutive than equity.

Balance sheet

▼ ROYALTY A royalty is not a loan and therefore has no direct impact on the balance sheet.

▼ EQUITY Issuing new equity expands the balance sheet.

▼ DEBT Directly affects the balance sheet and may affect the availability of future financing for other projects.

Tax position

▼ ROYALTY Royalty payments are normally deductible against tax for the issuer.

▼ EQUITY No tax implication.

▼ DEBT Interest payments are normally deductible against tax for the issuer.

What are the financial effects?

P A C I F I C

Contact usCall Chris Orchard on +44 (0) 20 7318 6360Visit www.anglopacificgroup.com

Anglo Pacific Group PLC17 Hill Street, London W1J 5NZ, United Kingdom

Important NoticeThis document has been provided for general information purposes only, is current only as of its date, is intended for your use only and does not constitute an offer or commitment, a solicitation of an offer or commitment, or any advice or recommendation, to enter into or conclude a transaction with or involving, Anglo Pacific Group PLC (Anglo Pacific). Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. The information herein may not be applicable or suitable to the specific investment objectives, financial situation or particular needs of recipients and should not be used in substitution for the exercise of independent judgment. The information set forth herein has been obtained from or based upon sources believed by Anglo Pacific to be reliable, but Anglo Pacific, its directors, employees, agents and representatives do not represent or warrant its accuracy or completeness. Any recipient interested in engaging in a transaction with or involving Anglo Pacific should conduct its own investigation and analysis and consult with its own professional advisers as to the risks involved in engaging in any such transaction. To the maximum extent permitted by law, Anglo Pacific, its directors, employees, agents and representatives do not accept any liability arising from inaccuracies and/or mistakes and/or from decisions and/or actions taken or not taken by any party based on this document. This document may not be reproduced, either in part or in full, without the written approval of Anglo Pacific. © 2010, Anglo Pacific Group PLC. Q3 2010