Embed Size (px)

Citation preview

RISK MANAGEMENT IN TWO NIGERIAN BANKS

BY

OKOYE IFEOMA

PG/M.SC/06/45978

BEING A RESEARCH DISSERTATION PRESENTED IN PARTIAL

FULFILLMENT OF THE REQUIREMENTS FOR THE AWARD OF MASTERS OF

SCIENCE (M.SC) DEGREE IN BANKING AND FINANCE

DEPARTMENT OF BANKING AND FINANCE

FACULTY OF BUSINESS ADMINISTRATION

UNIVERSITY OF NIGERIA

ENUGU CAMPUS

SUPERVISOR: DR. B. E. CHIKELEZE

SEPTEMBER, 2010.

APPROVAL

This dissertation has been approved for the department of Banking and Finance, faculty of

Business Administration, University of Nigeria, Enugu Campus by

__________________________________ ________________

DR. B. E. CHIKELEZE Date

_______________________________ ____________

DR. J.U.J. ONWUMERE Date

CERTIFICATION

I, Okoye Ifeoma, a post graduate student of the department of Banking and Finance with

Registration Number PG/MSc/45978, has satisfactorily completed the requirements of

research work for the masters‟ degree in Finance.

This work embodied in this dissertation is original and has not to the best of my knowledge,

been submitted in part or in full for any other diploma or degree of this or any other

university.

__________________________________ ________________

Okoye, Ifeoma Date

(Student)

DEDICATION

This work is dedicated to God Almighty, who made this work a reality. I also dedicate this

research work to my husband and my sons.

ACKNOWLEDGEMENT

My gratitude goes to my supervisor, Dr. B. E. Chikeleze for his commitment in this work.

My appreciation also goes to Dr. J. U. J. Onwumere who was the source of my inspiration

and motivator that made this work a reality. I also thank him in a most special way for his

support and concern for this work. My appreciation also goes to all members of my family

for their support, financially, morally and above all their prayers for me.

My regards goes to friends like Afamefuna Joseph, Gibson Eze and others for their

contributions in various degrees towards ensuring the success of this dissertation. I pray that

the good Lord reward you all abundantly.

ABSTRACT

This study examines the impact of risk management in two Nigerian Banks. Data were

obtained from the annual accounts and reports of the two banks (AfriBank Nigeria PLC and

Fidelity Bank Nigeria PLC). An event study methodology was employed to examine the

effects of deposit, asset quality and credit risk exposures on the growth and profitability of

Nigeria commercial banks.

Similarly, results shows the significant impact of asset on profit. On a whole, the study finds

the need for banks in Nigeria to devote enough attention to the management of financial risks

in the banking industry.

TABLE OF CONTENTS

Title Page----------------------------------------------------------------- i

Approval------------------------------------------------------------------- ii

Certification--------------------------------------------------------------- iii

Acknowledgment--------------------------------------------------------- iv

Abstract-------------------------------------------------------------------- v

Table of Content---------------------------------------------------------- vi

CHAPTER ONE

INTRODUCTION

1.1 Background of the Study---------------------------------------- 1

1.2 Statement of Problem---------------------------------------------- 3

1.3 Objectives of the Study----------------------------------------------- 3

1.4 Research Questions-------------------------------------------------- 3

1.5 Research Hypotheses------------------------------------------------ 4

1.6 The Scope and Limitations of the Study------------------------ -- 4

1.7 Significance of the Study----------------------------------------- -- 4

1.8 Definition of the Terms --------------------------------------- 6

References----------------------------------------------------------------- 9

CHAPTER TWO

REVIEW OF RELATED LITERATURE

2.1 Introduction-------------------------------------------------------- 9

2.2 Business Risks and Economic Globalization-------------------- 7

2.3 Meaning and Concept o risk Management--------------------- 8

2.4 Types of Risks Providing Banking Services-------------------- 10

2.5 Classification of risks---------------------------------------------- 13

2.6 Financial Risks Facing Nigerian Commercial Banks------------- 14

2.7 Design and Selection of Risk Management Strategic---------- 16

2.8 Portfolio Risk Analysis Management------------------------------ 17

2.9 Implication of Banking Risks on the Stability and

Soundness of the Financial System and the economy in General------ 18

2.10 Procedures for Adequate Bank Risk Management-------------- 20

2.11 Method of Monitoring Bank Risk--------------------------------- 13

2.12 Risk Control and Financing in Commercial Bank---------------- 24

2.13 Regulatory and Supervisory Frameworks------------------------ 28

2.14 Overview of the 1988 Accord------------------------------------- 29

2.15 Causes of Credit Risks to Commercial Banks------------------ 31

2.16 The Role of Liquidity in Commercial Bank Portfolio Management 33

2.17 Lending Polices of Commercial Banks----------------------------- 34

2.18 Summary of Literature Review------------------------------------- 36

References

CHAPTER THREE

RESEARCH DESIGN AND METHODOLOGY

3.1 Introduction----------------------------------------------------------- 40

3.2 Research Design----------------------------------------------------- 40

3.3 Population and Sample Size--------------------------------------- 40

3.4 Models of the Study------------------------------------------------ 41

3.5 Sources of Data----------------------------------------------------- 41

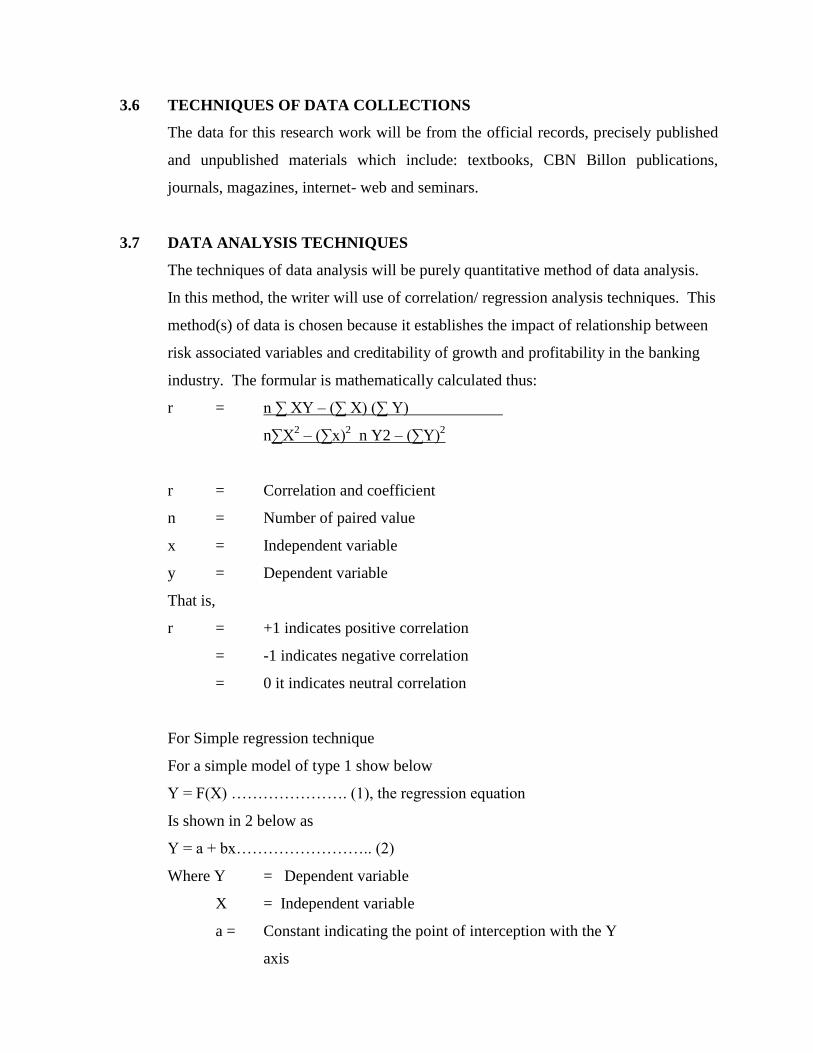

3.6 Techniques of Data Collections----------------------------------- 42

3.7 Data Analysis Techniques----------------------------------------- 42

References------------------------------------------------------------------ 44

CHAPTER FOUR

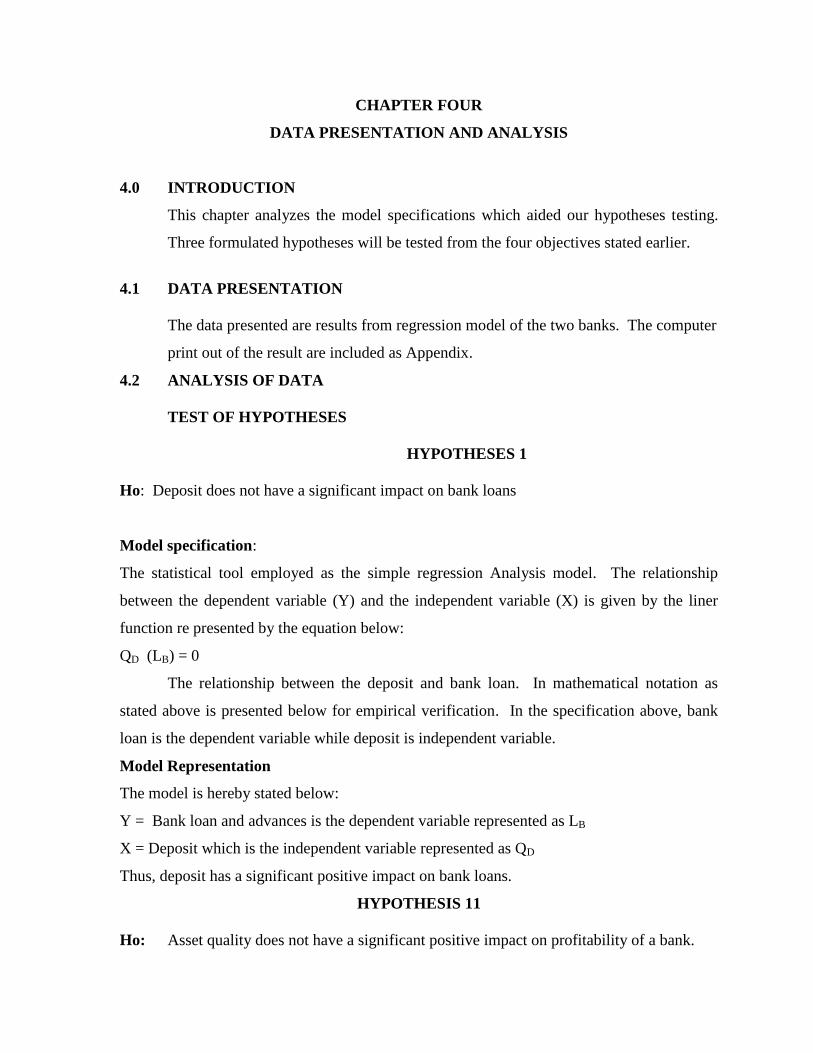

DATA PRESENTATION AND ANALYSIS

4.0 Introduction--------------------------------------------------------- 45

4.1 Data Presentation--------------------------------------------------- 45

4.2 Analysis of Data----------------------------------------------------- 45

CHAPTER FIVE

CONCLUSION AND RECOMMENDATIONS

5.1 Conclusion and Recommendations------------------------------ 48

5.2 Recommendations------------------------------------------------- 48

References----------------------------------------------------------------- 50

Bibliography---------------------------------------------------------------- 51

Appendix-------------------------------------------------------------------- 53

CHAPTER ONE

INTRODUCTION

1.1 BACKGROUND OF THE STUDY

The Nigerian Banking Industry for the past decades has witnessed series of Banking

distress and subsequent failures. Banks that had been doing well suddenly announced large

losses due to credit exposures that turned sour, interest rate position taken or derivate

exposures that may or may not have been assumed to hedge balance sheet risk. In response to

this, there is indeed urgent need for banks in Nigeria to devote enough attention to the

management of financial risks in the Nigerian Banking Industry. The 1989 annual report and

statement of account of NDIC revealed that classified loans and advances or bad debts

amounted to 9.4 billion which contributed 40.8 percent of total loans and advances and 280

percent of shareholders funds” (Hall, 1991:8). It is the development of his nature that have

led to the introduction of the CBN prudential guidelines for banks.

Cooker (1989:115), observes that “the main function of a bank is the collection of

deposits from those with surplus cash resources and the lending of these cash resources to

those with an immediate need for them” in fulfilling this:

It must be easily understood

It must be permanent

It must be able to absorb losses

These three features are expected to guide member countries, including Nigeria, in assessing

instruments to be used in raising bank capital. The bottom line in the debt capital is a risk

instrument for financing bank operations and should be discourage as much as possible. The

Basel Committee on banking supervision also introduced the “New Capital Accord” which

was implemented in 2007. The New Capital Accord required capital charges to be made for

credit, market and operational risks. This is aimed at protecting depositors, consumers, and

the general public against losses arising from bank fragility and failure (Umoh: 2005). Ever

since 1988, captains of the Nigerian Banking industry have shown keen interest in improving

the risk analysis, measurement and management capacity of firms in the banking sector.

Recently risk managers of major banks came together in Lagos to form an organization

named Credit Risk Association of Nigeria (CRAN). It is hoped that CRAN will offer them

opportunities for networking on issues of bank risk management. Concerted efforts are also

being made by captains of banking industry to reduce the risk exposure of banks in lending to

borrowers generally but especially to commercial bank, which is traditionally prone to

market and credit risk.

Coincidentally to this activity, and in part because of our recognition of the industry‟s

vulnerability to financial risk, the Wharton Financial Institutions center with the support of

the Slon Foundation, has been involved in an analysis of financial risk management

processes in the banking sector.

In the banking sector, system evaluation was conducted covering many of North

America‟s super regional and quasi money center commercial banks as well as a number

of major investment banking firms.

The Nigerian economy is increasing begin globalized by the deliberate government

actions since July 1986 when the federal government began the implementation of the

Structural Adjustment Programme (SAP). The SAP sought to deregulate and free the

economy from government control with a view to allowing market forces determine the

production and consumption decisions of economic agent within the country. The

deregulation process which was accompanied by privatization and commercialization

government enterprises, had far-reaching impacts on the entire economy. In particular,

deregulation of interest rates affected bank lending to the real sectors of the economy. In

more recent times, government adopted business consolidation strategies viz: merges,

acquisitions and taken over as part of its efforts to facilitate the ability of firms in financial

services industry to become global market Players.

According to the governor of the Central Bank of Niger (CBN), business

consolidation in the banking sector was to, among other things; make Nigeria banks complete

favourably in the global financial market” and to generate a high capital base that “will

provide banks with the resources to met the cost of compliance in the areas of credit and

market risk management” (Soludo, 2005:98-99).

1.2 STATEMENT OF PROBLEM

Risk management is at the core of lending in the banking industry. Many Nigerian banks had

failed in the past due to inadequate risk management exposure. This problem has continued

to affect the industry with serious adverse consequences. Banks are generally subject to wide

array of risks in the course of their business operations. Nwankwo (1990:15) observes that

„the subject of risks today occupies a central position in the business decisions of bank

management and it is not surprising that every institution is assessed an approached by

customers, investors and the general public to a large extent by the way or manner it presents

itself with respect to volume and allocation of risks as well as decision against them‟. Other

risks include insider abuse, poor corporate governance, liquidity risk, inadequate strategic

direction, among others. These risks have increased, „especially in recent times as banks

diversity their assets in the changing market. In particular, with the globalization of financial

markets over the years, the activities and operations of banks have expanded rapidly

including their exposure to risks.

1.3 OBJECTIVES OF THE STUDY

Basically; the main objective of this is to determine the effect of deposit on banks

lending and risk management.

Others are:

(i) To determine how asset quality can be efficiently and effectively monitored.

(ii) To examine the effects of credit risk exposure on growth and profitability of Nigeria

commercial banks.

1.4 RESEARCH QUESTIONS

The study will seek to answer the following questions:

(i) How does deposit of banks affect the portfolio of credit by banks?

(ii) How does the quality of banks assets in terms of risks exposures affect banks

profitability?

(iii) What are the effect of credit risk exposures on growth and profitability of banks?

1.5 RESEARCH HYPOTHESIS

The following alternative and null hypotheses will be formulated such as to uphold or

reject the preposition of the “risk management in two Nigerian commercial banks”.

(i) Ho: Deposit does not have a significant positive impact on

bank loans

(ii) Ho: Asset quality does not have a significant positive impact

on profitability of a bank

(iii) Ho: Credit risk exposures do not have a significant positive

impact on profitability of banks.

1.6 SCOPE OF THE STUDY

This study covers risk management in AfriBank Nigeria PLC and Fidelity Bank

Nigeria PLC. Pre and Post banking consolidation in Nigeria, specifically between

2003 and 2008.

1.7 SIGNIFICANCE OF THE STUDY

This study has a number of significant dimensions.

(i) The result of this study should provide information to the

commercial banks risk management department on the progress so far made in

identifying and evaluating risks as to enhance growth and profitability of the

financial institutions.

(ii) The result of this study should also reveal how much such progress has impacted on

the growth of the entire commercial banks in Nigeria.

(iii) Essentially, this work is a step in a right direction to assist and enlighten the general

public on what risk management in commercial banks is all about and hence guide

them in their immediate decision of handling risks.

(v) Furthermore, there is need to provide a reference document for further researchers

and evaluation of risk management conducted by other Nigerians/other Nations. This

research work will go a long way to increase the availability of literature in the field

of risk management in the banks and other related business associates that involve

risk in the day-to-day running of the businesses.

(vi) Finally, the study is of immense benefit to policy makers, investors, financial

managers lecturers and the general public.

1.8 DEFINITION OF THE TERMS

Portfolio Management: The process of making and carrying out a decision to

invest in securities (Anyafo, 2001 : 93).

Portfolio - Akinsulire (2002:357). Defined portfolio “as the combination or

collection of several securities on behalf of an investor.

Hedging: According to (Ebhalaghe, 1995 : 161) defined hedging as a system

employed to smoothen out unpredictable fluctuations in financial variables so as to

aid planning and avoid embarrassment induced by cash shortfalls.

Forward Contracts: This is a contract usually between a bank and customer to buy

or sell a specified quantity of foreign currency at an agreed future data (Akinsulire,

2002: 467).

Tenor Mismatch: Involves matching the tenor of an investment with the tenor of the

borrowed funds, so invested or a mismatch is said to occur when the tenor of

investments in aggregative exceeds the contractual tenor of the borrowed funds

(Ebhalaghe, 1995:144).

Currency Swap: This is a simultaneous borrowing and lending operation whereby

two parties exchange specific amount of two currencies on the outset at the sport rate

(Akinsulire, 2002:474).

REFERENCES

Anyafo, A. M. O. (2001), Investment Risk Evaluation: The State of the Art in Investment

and Project Analysis, Enugu: Banking and Financial Publication.

Akinsulure, O. (2002), Financial Management, Second Edition, Lagos, El-Toda Ventures

Limited.

Ebhalaghe, J. U. (1995), Corporate Financial Risk exposure Management, Lagos, Ronald

Printing Company Limited.

Hall J. A. (1999), “Banking Prudential Guidelines and their Impact on the Banking

Industry, being paper presented at the Bankers forum organized by CBN, June 5.

Nwankwo, G. O. (1990) “Prudential Regulation of Nigerian Banking” Institute of

European Finance, Lagos: University of Lagos publication.

Nigerian Deposit Insurance Corporation (1988), Annual Report and Statement of Accounts.

Soludo, C. (2005), Opening Remarks to Conference Participants, in CBN (ed), Consolidation

of Nigerian’s Banking Industry: Proceeding of Fourth Annual Monetary Policy

Conferences, Abuja, FCT.

CHAPTER TWO

REVIEW OF RELATED LITERATURE

2.1 INTRODUCTION

The review of related literature in this chapter will be reviewed under various sections

covering meaning and concept of risks, business risk and globalization, types of risks

managed by financial institutions (commercial banks), overview of the 1988 Accord

concerning risks, management, causes of credit risk to commercial banks, the role of liquidity

in commercial banks portfolio management, financial risk implication of securities, lending

policies of commercial banks. The regulatory and supervisory framework of CBN

concerning risk management in banks, risk control and financing in commercial banks,

financial risks facing commercial banks as a corporate body and techniques for monitoring

and managing financial risks exposure.

2.2 BUSINESS RISKS AND ECONOMIC GLOBALIZATION

In its general form, risk refers to variability around an expected value. The

probabilities of occurrence of the different outcomes are known, some of which are less

desirable than others and may entails a loss. Expected value is the outcome that would occur

on average over time if an individual or firm were repeatedly exposure to identifiable

conditions, decision or scenarios. Economists make a distinction between risk, in which a

random set of out comes can occur for which one known the probabilities, and uncertainty, in

which a random set of outcomes can occur for which one does not know the probabilities.

For a business enterprise, risk implies any thing that can cause variability in business value

such as unexpected increase in cash outflows or unexpected reduction in cash inflows. In

effect, business risk refers to variability in cash flow. The major business risks that give rise

to variability in cash flow. They are: price risk, credit risk. In recent times, these risks have

greatly increased as a result of economic globalization.

Globalization is the process by which national economics increasingly integrated and

dependent on one another. It is rooted in three technological revolutions.

In transportation, communication and information technology. Globalization has

drastically reduced economic transaction costs from afar and has tended to swallow up

inefficient production systems in developing countries with cheap imports from

industrialized nations (Shah, 2002).

Globalization ahs created huge concerns among government officials especially in

low-income countries as they lose sovereignty over their national economic policies. Also,

the combination of huge financial markets and flexible exchange rates makes it possible for

national economies to receive large shocks from abroad, some of which tend to be

destabilizing as demonstrated by the shocks in Indonesia and Argentina in the late 1990s. for

instance, the 1997 Asian currency crisis precipitated by hyper inflation and a 12% decline in

Indonesia GDP the following year (Friendman and Livensolhm 2002). This globalization

has capacity to greatly, increase the incidence of business risks, are sometimes classified in

economic literature as financial risks (Trieschamann et al, 2001).

2.3 MEANING AND CONCEPT OF RISK MANAGEMENT

Commercial banks are in the risk business. In the process of providing financial

services, they assume various kinds of financial risks. Over the decade our understanding of

the place of commercial banks within the financial sector has improved substantially. Over

this time, much has been written on the role of commercial banks in the financial sector both

in the academic literature (Santomero, 1997).

Suffice it to say that market participants seek the services of these financial

institutions because of the ability to provide market knowledge, transaction efficiency and

funding capacity. In performing these roles they generally act as a principal in the

transaction.

As such they use their own balance sheet to facilitate the transaction and to absorb the

risks associated with it.

To be sure, there are activities performed by banking firms which do not have direct

balance sheet implications. These services include agency and advisory activities such as:

Trust and investment management, “efforts” or facilitating contracts, standard underwriting

through sector 20 subsidiaries of the holding company or the packaging, securitizing,

distributing and servicing of loans in the areas of consumer and real estate debt primarily.

According to the Longman Dictionary of the English Language (1984 : 1284), risk is

the possibility of loss, injury, damage or peril. Defined in this way, risk is an inevitability of

life. No aspect of human endeavour is devoid of or can escape it. It is inherent in every day

lie and more so in the life of a banker because his business has business has been and

continues to be taking risks (Nwankwo; 1990:62). Managing risks like managing capital and

liquidity has therefore been the centre peace of banking (Nwankwo, 1990:63).

Umoh (1998:69), defined financial risk as the chance or probability that some

ufnavourable event will occur such that the financial position or cash flow stream of an

organization is adversely affected. One way of identifying the financial risks of an

organization is to recognize the sources of such risks. Another way is to see the risks as

either those the corporation can control and those that cannot.

Once a risk has been identified, the next stage is to estimate these frequency and

sovereignty of potential losses. In this way, risk managers obtain information for

determining the risks and selecting particular methods for managing them. In some cases, no

particular problems would arise if losses were incurred regularly (example, delay repayment

on small loans) because the potential size of each loss is small. But loses that occur

imprudently, yet are relatively large when they occur, need to be treated differently. It might

be a prudent policy to refuse loan application of the borrowers collateral of sufficient high

value that can be disposed without any legal entanglement. A good risk evolution system

should produce data on the following estimate: A good risk evaluation system should

produce data on the following estimate: Frequency of loss, maximum problem loss,

maximum possible loss expected loss, probability distribution of loss and standard deviation

of loss.

Risks in technical definitive terms to a situation where a project or investment

decision has a number of alternative possible outcomes and the probability of each occurring

is known. What is not known is which of the alternative outcomes will actually materialized

(Brown, 1988: 45 – 58).

the banking industries recognizes that an institution need not engage business in a

manner that unnecessarily imposes risk upon nor should it absorb risk that can be efficiently

transferred to other participants (Santomero, et all 1997).

2.4 TYPES OF RISKS PROVIDING BANKING SERVICES

In view of Nnanna (2003 : 30) observed that the risks associated with banking sector

can be grouped into the following types: Credit risk, Liquidity risk, interest rate risk, market

risk, currency risk, balance sheet structure, income structure and capital adequacy country

and transfer risk, legal risk. He further restated that the above type of risk, captures almost

all the risks arising from the normal day-to-day activities of a bank and are applicable to bank

that operate both internationally and locally. The based committee, however, noted that the

fundamental requirement for a good management of the above risks is the ability of banks to

identify and measure them accurately.

The risks associated with the provision of banking service differ by the types of

services rendered (Santomero; 1984:60). For the sector as a whole, however the risk

can be broken into five generic types: systematic/market risk, credit risk, counter part

risk, liquidity risk, and legal risks.

a. SYSTEMATIC RISK: This type of risk is referred as the risk arising

from asset value change associated with systematic factors (Old field et al,

1997: 61). It sometimes referred to as market risk, which is infact a some

what imprecise term. According to (Nnanna 2003:1) observed that market

risks is the risk arising from capital loss resulting from adverse market price

movement. By its nature, this risk can be hedged but cannot be diversified

complete away. Infact, systematic risk can be thought of an

undiverasifiable risk. All investors assume this type of risks, whenever

assets owned or claims issued can change in value as a result of broad

economic factors. Because of the bank‟s dependence on these systematic

factors, most try to estimate the impact of these particular risks on

performance.

b. CREDIT RISK: Credit risk refers to delinquency and default by

borrowers, that is, failure to make payment as at when due or make

payment by those owing the firm. The need to include delinquency derives

from the importance usually attached to the time of money in financial

analysis: one naira received today is worth more than one naira received in

the future. While delinquencies indicate delay in payment, default, denotes

non payment and the former is unchecked, leads to the latter

(Padmanaghan, 1988:14). The exposure to credit risk is particularly large

for financial institutions such as commercial and merchant banks. When

firms borrow money, they in turn, exposes under the credit risk.

However, credit risk arises from non-performance by a borrower. It may

arise from either an inability of unwillingness to perform in the pre-

committed contracted manner. This can affect the under holding the loan

contract as well as other lenders to the creditors. As a consequence,

borrowing exposes the firm‟s owners to the risk that the firm will be unable

to pay its debt and thus be forced into bankruptcy, and the firm generally

will have to pay more to borrow money because of credit risk (Harrington

and Niehaus, 1999:45).

It reduces the business value of the bank that granted the loan and

destabilizes the credit system.

Cost of administration of overdue local tends to the very sundry and

defaults push up lending costs without any corresponding increase in

loan turnover.

Default reduces the resources base for further lending, weaken staff

morale, and affect the borrower‟s confidence (Padmanabhan, 1998: 16)

The identification of credit risks and exposure to loss is perhaps the most

important element of the credit risk management process. Unless the

sources of possible losses delinquencies and defaults are recognized, it is

impossible to consciously choose appropriate, efficient methods for dealing

with those losses when they occur. The credit risk management unit of the

bank will need to draw a checklist of causes of delinquencies and default in

commercial bank financing.

c. COUNTER PARTY

Nnanna (2003:31) referred this type of risk arising from the economic, social

and political environment in the borrower‟s home country (Country risk) and

the risk present in loans that are not denominated in the borrower‟s local

currency (Transfer risk).

Moreover, counterparty risk comes from non performance of a trading

partner. The non performance may arise from a counter party‟s refusal to

perform due to an adverse price movement caused by systematic factor or from

some other political or legal constraint that was not anticipated by the principal

(Smith, 1990:59). Diversification is the major tool for controlling non

systematic counterparty risk. Counterparty risk is like credit risk, but generally

viewed as a more transient financial risk associated with trading than standard

creditor default risk.

d. LIQUIDITY RISK.

Nnanna (2003:31) defined liquidity risk as the risk arising form bank having

insufficient funds on hand to meet its current obligation. In view of Santomero

(1984:10) described liquidity risk as the risk of funding crisis. While some

would include the need to plan for growth and unexpected expansion of credit,

the credit here is seen more correctly as the potential for a funding crisis. Such

a situation would inevitably be associated with an unexpected event, such as a

large chares off, loss of confidence or a crisis of national proportion such as a

currency crisis.

One of management‟s fundamental responsibilities is to maintain sufficient

resources to meet liquidity requirements, as when cheque are presented for

payment, deposits mature and loan request are funded. Managing liquidity risk

forces a bank to estimate potential deposit losses and renew loan demanded.

e. LEGAL RISK:

Legal risks are endemic in financial contracting and are separate from the legal

ramification of credit, counter party and operational risk. Risk that a bank‟s

contract or claims will be enforceable or that court will impose judgment

against them. It covers the risk of legal uncertainty due to the lack of clarity of

laws in localities in which the bank does business (Nnanna, 2003:31);

examples of legal risk is fraud violation of regulation or laws and other actions

that can lead to catastrophic loss.

2.5 CLASSIFICATION OF RISKS

Generally, banking risks can be classified broadly into four categories: These are

financial risks, operational and event risks. Business risk and event risk.

a. Financial Risks:

Financial risks are further disaggregated into pure and speculative risks. Pure

risks which include liquidity, credit and solvency risks can result in a loss for bank, if

they are not properly managed. Speculative risks, based on financial arbitrage, can

result in a profit if the arbitrage is positive or a loss, if it is negative. The main

categories of speculative risks are interest rate, currency and market price (or

position) risks.

b. Operational risks:

Operational risks are related to a bank‟s overall organization and functioning of

internal systems, including: computer related and other technologies, compliance with

bank policies and procedure and measures against management and fraud.

c. Business risks

Business risk are associated with a bank business environment including:

macroeconomic and policy concern, legal and regulatory factors and the overall

financial sector infrastructure and payment system.

d. Event risks:

Event risks includes all type of exogenous risk which, if they are to materialize could

jeopardize a bank‟s operations or undermine its financial condition and capital

adequacy.

2.6 FINANCIAL RISKS FACING NIGERIA COMMERCIAL BANKS

Umoh (1988: 95) stated that one way of identifying the financial risks of an

organization/corporate body such as commercial bank is to categorize the sources of

such risks. He further observed that another way is to see the risks as either those the

corporation can control and those they cannot control consistent with these methods

one can classify financial risks into following sources: credit, interest rate, inflation,

exchange rate, investment, capital adequacy, liquidity, management and concentration

of asset risks: here the writer will examine sources of these financial risks briefly as

followings:

a. EXCHANGE RATE RISK

Exchange rate risk arises from the potential loss emanating from the inherent

fluctuation nature of exchange rates, particularly, since the Naira started

depreciating steadily against the major international currencies, cooperate

bodies that require foreign productive inputs have been exposed to loss arising

from changes in the relative value of the Naira vis-à-vis foreign currencies.

For the banking industry, exchange rate risks would arise if the naira rises in

value before a bank sell off its stock of foreign exchange. Conversely,

exchange gains are realized as the naira depreciates.

b. INFLATION/PURCHASING POWER RISK:

This risk arises from the changes in the price level. Since the Udeoji awards or

early 1970s the Nigerian economy, for the most part has lived with double

digit inflation. The inflation in the country has been linked mainly to excess

demand pressures, monetary and fiscal factors. One implication of purchasing

power risk for banks is that more funds must be raised to replace assets

resulting replacement.

c. INTEREST RATE RISKS:

Interest rate risk arises from changes in the prevailing rates of interest. For

example, if a merchant bank buy funds from a commercial bank at 27% and

before the merchant bank can place the funds, the market rate of interest falls

and the merchant bank can only get 25% of the funds placement, then a

financial loss will be sustained by a merchant. Bank‟s interest rate risk are

common in times of tight liquidity to financial market.

d. CAPITAL ADEQUACY RISKS:

This risk is particularly relevant in the banking business, where supervisory

authorities (CBN & NDIC) are demanding certain levels and types of capital

in order to maintain stability in the banking system and ensure the confidence

of depositors.

e. CONCENTRATION OF ASSETS RISK:

This is the probability that a corporate entity especially a financial house

would sustain financial losses if its funds are concentrated in one or only a

few asset portfolios. An example is that of a bank giving primarily real estate

loans and advances. If the market for real estate suffers a downturn, the bank

takes losses on the loans and advances portfolio. This kind of risk was

responsible for the much published savings and loan crisis in the Untied States

of America.

f. MANAGEMENT RISK:

This type of financial risk usually occur where the key management staff are

either incompetent or are pursuing goals other than those set for them by the

owners (shareholders) of the bank. Business literature has identified other

goals management may pursue to include market share, expense preference

and satisfying behaviour.

g. INVESTMENT RISK:

This is the change that the cash inflow from a given investment project when

put on a present value basis and aggregated may not be sufficient to cover the

cost of the project. Investment risk may arise from a number of factors most

of them may be outside the control of the investing bank (systematic risk).

For example, a down turn in the national economy may turn an otherwise

proof investment opportunity into a very risky one unpredictable government

policy such as ban on raw materials, importation can mar an otherwise

profitable investment opportunity. However, credit and liquidity risks have

been highlighted in our early discussions.

2.7 DESIGN AND SELECTION OF RISK MANAGEMENT STRATEGIES

This is the critical stage of fusion of risk management process and strategy. Three

basic strategies commonly employed in dealing with risks are: loss control, loss

financing and internal risk reduction. Loss control and internal risk reduction involve

decisions by firm to invest (or forego investing) resources in order to increase

business value. They are other conceptually equivalent to other decisions made by

firms. For instance, under loss control there are two basic methods loss prevention

and loss reduction. A commercial bank involved in Agriculture financing can only

bring its loss exposure to zero by refusing to grant loans to farmers. This is called

risk avoidance, the main cost being foregone benefits form agriculture financing. But

this is a non option in an environment where government insists that banks must grant

credit to their borrowers and provides the banks with incentives to do so. The

plausible option, therefore is one of loss reduction, whereby banks seek to reduce the

magnitude of losses from financing risks. The goal here is to make a safer and thus

reduce the frequency and severity of losses from delinquencies and defaults.

Investment in information on loan applicants, market research and diversification of

loan portfolio by funding different enterprises are internal risk reduction strategies

available to banks increased precaution in credit administration is very important and

can be achieved through two means:

- Demand for appropriate collateral security by banks before granting loan, and

- Effective loan supervision ad monitoring by credit officers of lending

agencies.

Loss financing refers to methods used to obtain funds to offset or pay for risks

related losses: retention, hedging and insurance.

With retention, the bank assumes obligation to pay for part or all of the credit

risk losses from available bank funds.

Hedging is employed to smoothen out unpredictable fluctuations in financial

variables so as to aid planning ad avoid embarrassment induced by cash shortfalls.

Unlike in diversification where securities/projects which are not closely correlated in

returns are sought. In hedging efforts should be made to find securities which are

perfectly correlated in returns. When one security is bought and other security with

perfectly correlated returns is sold so that the net position is safe. Hedging is used to

minimize interest rate risk and exchange rate risks.

Insurance is the third method for financing credit losses, and which tends to

spread out risk and consequently minimize the burden an individual lender/investor

has to bear.

2.8 PORTFOLIO RISK ANALYSIS MANAGEMENT

A portfolio is defined as a combination of assets and portfolio. A portfolio is

not merely a collection of unrelated assets but a carefully blended asset combination within a

unified framework. When investors make decisions with reference to their wealth positions,

they rationally should make them in a portfolio context. What constitutes a portfolio would

depend on whose perspective from which you are looking at it for an investor in the stock

market, the portfolio will be a collection of shareholdings in different companies. For a real

estate investor, his portfolio will be a collection of buildings. To a financial manager from

the industrial sector, his portfolio will be a collection of real capital projects.

The process of making and carrying out a decision to invest in securities is called

portfolio management. Proper portfolio management reduces investment risks. Portfolio

management has become a profession for delivery of investment counseling and

management services. Management of a portfolio of significant size is a time-consuming

and painstaking job. Historically, portfolio management progressed form traditional

to modern approach.

Traditional portfolio management expressed investment risk and its

relationship to returns in qualitative rather than in quantitative terms. Under the

approach, past returns could not be compared through the use of generally accepted

common denominator of risk. The uncertainty of expected return could not be

expressed with any degree of quantitative assurance.

Modern portfolio theory treats risk in quantitative terms. It focuses attention

beyond the tradition exhaustive analysis and evaluation of individual securities to the

problems of overall portfolio composition predicated on explicit risk return

parameters and on the identification and quantification of client objective.

Institutional investment polices are often a combination of the traditional and modern

approaches to portfolio management.

The basic elements of modern portfolio theory emanates form a series of

propositions concerning relational investor behaviour set forth in 1952 by Dr. Harry

Marketwise of the Rand Corporation and later in a more complete monograph

sponsored by the Cowls Foundation of the United States of America. Whether the

investor is an individual or an institution, the following factors influence investment

behaviour:

Security of capital invested: How secure is the investment given the state of

the economy?

Liquidity: the ease of convertibility of the capital invested into cash at short

notice

Return: The reward potentials of the investment

Risk: The risk content of the investment and the extent of its diversificability.

Growth prospects: The growth potentials of investment companies wishing to

attract investor‟s funds must ensure sufficient securities, liquidity, return and

growth prospects in order to enhance the marketability of the securities in the

capital market.

2.9 IMPLICATION OF BANKING RISKS ON THE STABILITY

AND SOUNDNESS OF THE FINANCIAL SYSTEM AND THE ECONOMY IN

GENERAL

Risks could result to bank distress, failure and financial crisis in an economy.

The worst problem associated with a bank crisis is that of contagion in which the

problems in one bank result to a run on the entire banking system. (Hilbers et al, 200:

52) depositors and other creditors who are worried about the safety of their money are

worried compelled to move their funds form those banks which are perceived to be

unhealthy, to the banks that are solvent. The panic withdrawal may not only be from

one bank to another, it could lead to total withdrawal of funds from the banking

system. Consequently, the loss of confidence of banks depositors on the banks can

establish the banking system and hence the economy as a whole.

2.10 PROCEDURES FOR ADEQUATE BANK RISK MANAGEMENT

It seems appropriate for an discussion or risk management procedures to

being with why these firms manage risk. According to standard economic

theory, managers of value maximizing firms ought to maximize expected profit

without regard to the variability around its expected value. However, there is

growing literature on the reasons for active risk management including in the

work of Stulz (1984), Smith, Smithson and Wolford (1990). Infact, the recent

review of risk management reposted in Santomero (1995) list dozen of

contributions to the area and at least four distinct rationals offered for active

risk management. These include managerial self interest, the non linearity of

the tax structure, the costs of financial distress and the existence of capital

market imperfections.

In the light of the above, what are the necessary procedures that must be

in place to carry out adequate risk management? And how they are

implemented in each area of risk control? The management of the banking

firm relies on a sequence of steps to implement a risk management system.

These can be seen as containing the following four parts:

- standards and reports

- position limit or rules

- investment guidelines or strategies

- incentives contracts and composition

In general, these tools are established to measure exposure, define procedures

to manage these exposures, limit individual positions to acceptable levels, and

encourage decision makers to manage risk in a manner that is consistent with the

firm‟s goals and objectives. To see how each of these four parastatals arts of basic

risk management techniques achieves these ends, we elaborate on each part of the

process below:

a. STANDARD AND REPORTS:

This involves two different conceptual activities, that is, standard setting and

financial reporting. They are list together because they are the sine qua non of

my risk system. Underwriting standards, risk categorizations, and standards of

review are all traditional tools of risk management and example is the great

depression of the 1930s, which originated in USA and affected many countries

across the world. The origin of the great depression is said to be traceable to

the initial crisis that began in the U.S. financial industry.

Empirical studies have shown that bank distress could affect the

economic growth of a country through the savings investment channel. For

instance, it has been proved that the mismanagement of contingent risks could

lead to panic withdrawals in the ailing bank, which could further deteriorate

into a run on the banking sector. The withdrawal of funds from the financial

sector implies a leakage in the system.

According to (Haynes, 2003:45) stated that in the process of managing

financial risks, and to safe-guard the banking industry in their business there is

need for banks to maintain and guide against risks losses as to ensure sound

and stable financial system in the following manners:

a. THE PURPOSE OF PRUDENTIAL REGULATIONS AND

SUPERVISION

The basic objectives of prudential regulation and supervision of banks

are to prevent systematic banking distress, protection of depositors,

savings and the encouragement of financial intimidation, specifically,

the objectives of prudential regulation as to:

enhance prudent portfolio management

ensure optimal risk diversification

prevent adverse selection and risk aversion

promote sound and stable financial system

b. REGULATORY AND SUPERVISORY FRAME WORKS

The international financial crisis of the second half of the 1990s

provoked much reflection on ways to strengthen the global financial system.

The international community identified a number of priorities including the

need to enhance its own ability to monitor the health of the financial system.

The ability to monitor the financial sector soundness presupposes the existence

of valid indicators which can measure the health and stability of the financial

systems. The general macro-prudential indicators as developed by the IMF for

assessing and supervising banks is embedded in the CAMELS frame control.

Consistent evaluating and rating of exposures of various types are essential to

understand the risk in the portfolio and the extent to which these risks must be

mitigated or absorbed.

Obviously, outside audits, regulatory reports and rating agency evaluations are

essential for investor to gauge asset quality and firm level or risk.

b. POSITION LIMITS AND RULES

A second technique for internal control of active management is the use of

position limits, and minimum standards for participation. In term of the latter,

the domain of risk taking is restricted to only those assets or counterparties that

pass some pre-specified quality standard. Then even for those investment that

are eligible limits are imposed to cover exposures to counterparties, credits and

overall position concentration relative to various types of risks.

c. INVESTMENT GUIDELINES AND STRATEGIES

Investment guidelines and recommended positions for the immediate future are the

third technique commonly in use. Here the strategies are outlined in term of

concentration and commitments to particular areas of the market, the extent of desired

asset/liability mismatching or exposure and the need to hedge against systematic risk

of a particular type.

The limit described above lead to passive risk avoidance and/or diversification,

because managers generally operate within position limits and prescribe rules.

d. INCENTIVE SCHEMES

To The extent that management can enter incentive compatible contracts with

the line managers and make companion related to the risk born by these

individuals, then the need for elaborate and costly control is lessened.

However, such incentive contracts require accurate position valuation and

proper internal control system (Santomero, 1995:4). Such tools which include

posting, risk analysis, the allocation of costs and setting of required returns to

various parts of the organization are not trivial. Notwithstanding the difficulty,

well designed system aligns the goals for managers with other stakeholders in a

most desirable way (Babble, et al, 1996:10). Infact, most financial decades can

be traced to the absence of incentive compatibility as the cases of deposit

insurance and maverick traders.

2.11 METHODS OF MONITORING BANK RISK

The banking industry has long viewed the problem of risk management as the

need to control four of the above risks mentioned earlier which make up most, if not all, of

their risk exposure, credit, interest rate, foreign exchange and liquidity risk. While they

recognize the counterparty, and legal risks, they view them as less central to their concerns

(Trester et al, 1997:45). Where counterparty risk is significant. It is evaluated using standard

credit risk procedures, and often within the credit department itself. Likewise, most bankers

would view legal risks as arising from their credit decisions, or more likely, proper process

and not employed in financial contraction. Accordingly, the study of bank risk management

process is essentially an investigation of how they manage these four risks. To illustrate how

this is achieved, this review of firm level risk management begins with a discussion of risk

management controls in each area as follows:

a. We begin with standards and reports. As noted earlier, each bank must

apply a consistent evaluation and rating scheme to all its investment

opportunities in order for credit decisions to be made in a consistent manner

and for the resultant aggregate reporting of credit risk exposure to be

meaningful. To facilitate this, a substantial degree of standardization of

process and documentation is required. The form reported here is a single

rating system where a single value is given to each loan, which relates to the

borrowers underlying credit quality. At some institution, a dual system is in

place where both the borrower and the credit facilities are rated.

There are various ways of trying to keep bad debts on loan to a tolerable

low level including:

avoiding loan to risky customers

monitoring loan repayment and

renegotiating loan when customers get unto difficulties.

Loans should be made only to borrowers who are likely to be able to

repay and who are unlikely to become insolvent. Credit analysis of

potential customers is carried out in order to judge the credit risk with

the borrower and to rich a lending decision. Loan payments are

monitored and action taken when a customer defaults.

There is some credit for customers in their dealing with bank more

commonly, borrowers are at some risk from the lending decisions of

their banks. The risk arises from taking credit rather than form giving it.

The borrower‟s risks can be listed briefly.

The interest rate charged by the bank will be dependent on the

bank‟s view of the borrower‟s credit worthiness

A bank might decide to reduce a customer‟s borrowing facility by

reducing an overdraft facilities

Lending covenants on an existing loan could restrict the ability of

the borrower to obtain further loans

A bank might refuse to extend a loan to support a company with

temporary cash flows.

Generally, accepted accounting principles require this monitoring. The

credit portfolio is subject to far value accounting standards, which have

recently be tightened by the financial Accounting shares board (FASB).

Commercial banks are required to have a loan loss reserve account (A

contra asset) which accurately represents the diminution in market value

from known or estimated credit losses. Bank loans have three sources

for repayment and these must be evaluated by the credit department of

the bank and they include:

The cash flow of the borrower

Security, in the form of a fixed or floating charge the borrower‟s

assets or a mortgage on property.

A guarantee from a third party, such as holding company

Credit management is concerned primary with managing debtors and

financing debts. The objectives of credit management can be stated as

safeguarding the company‟s investment in debtors and optimizing

operational cash flows. The objectives of credit management are

achieved primarily by means of health monitoring functions.

Assessing the credit risks and other risks such as currency risks

Negotiating and arranging credit terms appropriate to those risks.

Collecting payment in accordance with the agreed terms.

b. Interest Rate Monitoring Procedures

The area of interest rate risk is the second area of major concern and on-

going risk monitoring and management. However, the tradition has

been for the banking industry to diverge somewhat from other part of

the financial sector in their treatment of interest rate risk. Most

commercial bank make a clear distinction between their trading activity

and their balance sheet interest rate exposure. For large commercial

banks that have an active trading business, such systems have a required

part of the infrastructure. But, infact, these trading risk management

system vary substantially form bank to bank and generally are less real

than imagined.

For balance sheet exposure to interest rate risk, commercial banking

firms follow a different drummer or is it accountant? Given the

generally accepted accounting procedure (GAAP) established for bank

assets as well as the close correspondence of asset and liability

structures, commercial banks tend not to see market value reports

guidelines or limits. Rather, their approach relies on cash flow and

book value at the expense of market values.

Currently, many commercial banks are using balance sheet simulation

models to investigate the effect of interest rate variation on reported

earning over one, three and five years horizons.

c. Exchange Rate Monitoring Procedures

In this area, there is considerable difference in current practice. This can be

explained by the different franchise that co-exists in the banking industry.

Most banking institutions view activity in the foreign exchange market

beyond their frameless, while others are active participants; the former will

take virtually no principal risk, no forward open oppositions, and have

expectation of trade volume. Limits are the key elements of the risk

management systems in foreign trading as thy are for all trading business.

Incentive systems for foreign exchange traders are another area of significant

differences between the average commercial bank and its investment banking

counterpart.

d. Liquidity Risk Management Procedures

Two different nations of liquidity risk have evolved in the banking sector.

Each has some validity. The first and the easiest in most regards is a notion

of liquidity risk as a need for continued founding. The counterpart of standard

cash management, this liquidity need is forecast able and easily analysed.

Accordingly, attempt to analyze liquidity risk as a need for resources for

facilitate growth or honor outstanding credit lines are f little relevance to the

goal of risk management pursued here.

The liquidity risk that does present a real challenge is the need for funding

when and if a sudden crisis arises. In this review of literature we are

concerned with liquidity needs associated with a bank specific shock, which,

such as a severe loss, and a crisis that is system wide. The management of

risk in this aspect of our review tries to examine the extent to which it can be

self supporting in the event of a crisis and tries to estimate the speed with

which the shock will result in a funding crisis.

The regulatory authorities have increasingly mandated that a liquidity risk

plan be developed by members of the industries.

e. Risk Aggregation Procedures:

This method of risk management procedures measure, report, limit and

manage the risks of various types which have been earlier explained. A

process has been developed to measure particular risk considered and

techniques have been deployed to control each of them. In this procedure,

credit risk process is a quantitative review of the performance potential of

various borrowers. It result in rating, periodic re-evaluation at reasonable

intervals through time and on-going monitoring of various types of measures

of exposure interest rate risk rate is usually measured weekly, using on and off

balance sheet exposure. Limits are established and synthetic hedges are taken

on the basis of this cash flow earnings forecasts. Foreign exchange or general

trading risk is monitored in real time with strict limits and accountability.

As the organizational level, overall risk management is being centralized into

Risk management committee, headed by some one designated as the senior

risk manager. The purpose is to empower one individual or group with the

responsibility to evaluate overall firm level risk and determine the best interest

of the bank as a whole. At the analytical level, aggregate risk exposure is

receiving increase scrutiny. To do so, however, requires the summation of the

different types of risk outlined above. This is achieved in two district but

related ways: the first of these, pioneered by Bankers trust, is the RAROC

system of risk analysis (Wee et al, 1995:25). In this approach, risk is

measured in terms of variability of outcome, where possible, a frequency

distribution of returns is estimated, from the historical data and the standard

deviation of this distribution is estimated. Capital is allocated to activities as a

function of this credit or volatility measure.

A second approach is similar to the RAROC, but depends less on capital

allocation scheme and more on cash flow or earning effects of the implied

risky position. This was referred to as earnings. This method can be used to

analyze total firm level risk in a similar manner to the PAROC system.

2.12 RISK CONTROL AND FINANCING IN COMMERCIAL BANK

Identifying and measuring financial risks are only the preliminary steps in managing

and controlling financial risks. The next essential step is the strategy for controlling and

financing the risks. Control encompasses measures aimed at avoiding, eliminating or

reducing chances of loss, i.e. preventing events occurring or limiting the severity of the loses

when they occur (Naiyeju, 1989:15). Financing aims at spreading more evenly the costs of

the risks in order to reduce strains, financial and otherwise, and possible insolvency which

random occurrence of large losses may cause include three measures: risk avoidance and

minimization, risk transfer and risk retention (Naiyeju, 1989:25).

a. RISK AVOIDANCE AND MINIMIZATION

Banks make considerable use of this strategy which is inherent in the following areas:

Balance sheet strategy asset based and liability base approaches, particularly the

strong preference for short term self liquidating lending strategy.

Reinforced by regulator prohibitions through moral suasions and other limitations

that limit the scale of particular operations or contraction of risks in particular

areas.

Through off balance sheet activities such as currency and interest rate swaps and

other hedging devices

Internal control systems, efficiency in credit analysis and in assessing credit

worthiness and exposure limits.

Regulatory intervention by monetary authorities to keep the financial system upon

an even keel.

Overall improvements in quality of management.

Discount window and lender of last resort borrowing.

b. RISK TRANSFER STRATEGY

The management of banks especial the risk mangers in controlling and financing risks

should involve the following strategy in transferring risk.

Through an insurance system e.g. deposit insurance.

Collective guarantees of governments and their agencies e.g. international

lending.

Third party guarantees of government, wealth individuals.

c. RISK RETENTION

Assumption of risk that cannot be avoided or transferred a form of self insurance.

This is usually achieved through;

Charging losses as they occur against operations.

Adequate capital backing

Financing losses as they occur by obtaining loans from financial houses.

Providing for the loss through insurance, risk fund, contingency fund.

Interest margins on operations to cover operating expenses and some losses.

2.13 REGULATORY AND SUPERVISORY FRAMEWORKS

The international financial crisis of the second half of 1990s provided much reflection

on ways to strengthen the global financial system. The International community

identified a number of priorities, including the need to enhance its own ability to

monitor the health of the financial system. The ability to monitor the financial

system/sector soundness presupposes the existence of valid indicators which can

measure the health and stability of financial systems. The general macro-prudential

indicators as developed by the IMF for assessing and supervising bank embedded in

the CAMELS framework. CAMELS is acronym for capital (adequacy), Assets

quality, Management, Earrings, Liquidity and Sensitivity to market risks. The essence

of the CAMELS framework is explained as follows:

i. Capital: Capital adequacy ultimately determines how all financial

institutions can cope with shocks to their balance sheets, thus, it is

useful to track capital adequacy ratios that take into account the most

important financial risks, foreign exchange, credit, interest rate risks by

assigning risk weighting to the institution‟s assets.

ii. Assets Quality: The solvency of a bank is typically at risk when its

assets become impaired, so, it is important to monitor the indictor which

measures the quality of a bank‟s assets in terms of over exposure to

specific risks and the trends in non performing loans.

iii. Management: Sound management is the key to bank‟s performance,

though it could be difficult to measure. It is primarily a quantitative

factor applicable to individual institutions. Several indicators, however,

can serve for instance, efficiency measures can be applied as an indictor

of management soundness.

iv. Earnings: Chronically unprofitable financial institutions risk insolvency,

compared with other most indictors trends in profitability can be more

difficult to interpret of instance, usually; high profitability can reflect

excessive risk taking.

v. Liquidity: Initially, solvent institutions may be driven towards by poor

management of short-term liquidity indictors should cover funding

sources and capture large maturity mismatch.

vi. Sensitivity to market risk: Banks are increasingly involved in diversified

operations, all of which are subject to market risk, particularly in setting

of interest rates and the carrying out of foreign exchange transactions. In

countries that allow banks to trade in stock market or commodity

exchanges, there is also a need to monitor indictors, of equity and

commodity price risk.

2.14 OVERVIEW OF THE 1988 ACCORD

The 1988 capital accord, was a major development in bank‟s capital regulation. It

explicitly linked capital requirements to a bank quantum and degree of risks. It is also

established minimum capital requirements that were internationally comparable. It

required that banks should hold as capital, at least 80 percent of their weighted assets.

Four risk weights were introduced namely, claim on government (10 percent), claims

on banks (20 percent), residential mortgage claim (50 percent). The accord thus

provided a benchmark for the assessment of the banks by market participants.

The 1988 Accord however, has some weaknesses, some o which, at least, was a crude

measure of economic risk exposure were not sufficiently segmented to adequately

differentiate between true economic risk and the measured under the Accord.

The accord covered only credit risk.

While the 1988 Accord provided essentiality, only an option for

measuring, managing and mitigating risk, the new framework, on the other

hand provides a spectrum of approaches for the measurement of both

credit and operational risks in determining the capital requirement. It also

introduced the element of flexibility of the choice of measure, subject to

supervisory view.

Consequently, the new capital accord consists of three mutually

reinforcing pillars namely, the minimum capital requirement, supervisory

review and market discipline.

PILLAR 1: Minimum Capital Requirement:

The minimum capital requirements comprise three fundamental elements, viz

a definition of eligible regulatory capital, which remains the same as outlined

in the 1988 Accord, the risk weighted assets and the minimum capital to risk

weighted assets the fundamental; elements of 1988 Accord remain in change.

It is the measurement of risks embodied in the risk-weighted assets that the

new Accord addresses,

PILLAR 2: Supervisory Review Process

The supervisory review process is intended to ensure that the banks home

adequate capital to support all the risk in their business and also to encourage

them to develop and use better risk management techniques in monitoring and

managing risks.

PILLAR 3: Market Discipline:

This third pillar dealt with disclosure equipments and recommendations for

the market banks. The principle states that banks should have a formal

disclosure policy by the boards of directors. This policy should describe the

banks objective and strategy for the public disclosure of information on his

financial condition and performance. In addition, banks should implement a

process assessing the appropriateness of their disclosure including the

frequency of disclosure.

2.15 CAUSES OF CREDIT RISKS TO COMMERCIAL BANKS

Credit risk delinquency and fault is the main risk that commercial bank face in lending to

firms, individual, and corporate body. Empirical studies have produce a verity of reasons for

loan default,. Adeyemo (1984) identified the principal cause of loan default in Kwara state

as loss of production due to calamities. He found the educated borrowers and landlords or

landowners repaid loans more promptly than uneducated and tenant borrowers. Okorie

(1998) identified poor project supervision evaluation and management, ultimate loan

disbursements, diversion of funds, and dishonesty of loan beneficiaries as the cause of loan

default. A study in India found that default were by and large, willful and mostly large

borrowers were responsible (World Bank, 1975, Padmanabhan 1988). Given the variety of

reasons for credit risk in bank lending, it may be necessary to classify them into three broad

sources: Causes at borrower level, at financial institution level and at economy level. Such a

classification offers a quick checklist and guide to credit risk managers of bank in

management of commercial bank risks:

a. CAUSES OF LOAN DEFAULT AT BORROWERS LEVEL;

The causes of loan default the borrowers level include the following.

Failure of investment to generate sufficient income due to improper technical

advice, inadequate support services, marketing risks or natural disasters.

Diversion of loan business operations to non essential consumption which makes

it difficult to meet repayment commitment on time.

Existence of liabilities towards informal lenders, leading to delinquency and

default.

Contingencies at borrowers household, such as sickness, accident or death (pure

risk).

Absence of incentives for prompt repayment or penalties for delayed repayment.

Prevalence of low real rate of interest or pegging of interest rate far below the

market rate.

b. CAUSES OF LOAN DEFAULT AT FINANCIAL INSTITUTION

LEVEL:

At the financial institution level, loan default may be due to any or

combination of the following:

Inability or reluctance of lenders to ensure sanctions against conspicuous

defaulters.

Absence of a sound accounting and management information systems.

Defective procedures for loan appraisal which could lead to financing of

bad projects, thereby giving rise to delinquencies and default.

Quality of loan officers, their mobility in the field and their capacity to

judge borrowers as well as the incentive package available to them affect

repayment. When loan officers are assessed on the baisi of compliance

with lending targets than with recovery performance, it could lead to bad

loans, when targets than with recovery tends to decline.

Ultimate loan disbursement and inappropriate repayment schedules. In

addition, when the procedure for repayment is cumbersome, borrowers

tend to default.

c. CAUSES OF LOAN DEFAULT AT ECONOMY LEVEL

At the level of the economy, the causes of loan default include the following:

Excessive government regulations in the day to day administration of

financial institutions could result in difficult and bad debts.

Government indemnity or guarantee of banks against losses arising from

poor loan repayment, which could weaken the efforts of the banks in loan

collection.

Low real interest rate which makes borrowing and consumption more

profitable at the expense of savings and loan repayment.

Inappropriate monetary and fiscal policies that could induce inflation and

encourage borrowers to delay repayment in order to take advantage of the

fall in the value of monetary and

Poor planning and execution of development programmes by government

agencies, which could result in lack coordination between credit supported

activities and other support services.

2.16 THE ROLE OF LIQUIDITY IN COMMERCIAL BANK PORTFOLIO

MANAGEMENT

Liquidity is often measured in terms of balance sheet aggregate (Emekekwue,

1994:155) cash and government securities have continued to decline while loan

have been on the increase. The reason for decline in cash holding is because of

the sterility of cash, as for the government securities the income in the form of

interest rate is very negligible. On the other hand loan which are largely liquid

have been on the increase because of the huge profit potential from expending

prudent loans.

The loan deposit ratio measures, that extent to which the banks have used up

its resources in the extension of loans to its customers and as the ratio

continues to increase, the banks becomes very cautious and restrictive in their

lending activities. This is because their resources are tied up in liquid assets

and should assets and should there be serve pressure on the resources by

depositors.

The issue of liquidity is very crucial in the discussion of a bank to extent loans.

Liquid assets help to protect the bank against unexpected gyrations in the

amount of deposit held as some of those deposit could have been used in the

process of extending loans. When bank experience on unexpected loss of fund

through excessive with drawls of funds by depositors, part of this loss can be

met from liquid assets, (James, 1988:23). The ownership of liquid assets

reduces the profitability of a bank selling its loan under pressure at

unfavourable terms. In this way, when there is an unexpected flow of funds

into the bank, either because of depositors increasing the volume of deposit

they lodge at the bank, or through the repayment of loans on maturity, the

banker should exercise a lot of cautious in viewing such funds (George,

1973:133).

However, the amount of deposits held by bank can be influenced by

endogenous and exogenously influenced because the volume of loan demands

and deposit withdrawals cannot be predicted and the result is a diminution in

the amount of deposit in the bank. Similarly, the volume of deposits can be

enhanced by the sale of some assets of the bank and the sale of the certificate

of deposits (CDs) and the purchase of federal funds in the market.

2.17 LENDING POLICIES OF COMMERCIAL BANKS

The main preoccupation of banks is to extend loans to their customers.

Thus, the formulation and implementation of sound lending policies are

some important responsibilities of the directors and management of a

bank. If a bank is to execute its credit creation function properly, there

must be well articulated lending policy by the bank. The lending policy

of a bank must be specific on how much of loans will be made to whom,

when, for what period and for what purpose. Against this background,

lending policies should be well documents so that lending officers will be

able to know the area of prohibition and the areas where they can operate.

Even when the policies are established and documented, such policies

must be subject to periodic review to enabling the bank keep abreast with

the dynamic nature of the economy and complete effectively with other

banks in the system.

A bank‟s lending policy is simply a screening device that enables a bank

screen out poor loan applications and respond favourable tot eh good

ones, keeping in view its resources. We must emphasis that the character

of the loan is more important than its form. That is, it is more important

that a loan is sound and that the project can through of periodic incomes

large enough to service and extinguish the loan, than the mere fact that it

is a secured loan such as mortgage loan collateral loans consumer loans,

business loans etc.

Establishing policy guidelines for extending credits involves determining

well in advance how loans are to be made, how such loans will be

service, reviewed, and collected. In order to achieve this, the policy

makers must determine the organizational structure of the lending

function, delegate authority tot hose that will have to execute the polices

and to establish guidelines on how to review loan applications and

outstanding loans.

Most of the time, it is not proper to allow the directors to extend or

review loans to customers of the bank. This is because they not specialist

except executive directors) since they are not specialist they might over

emphasis the magnitude of the collaterals pledged as the sole basis of

extending credit. At times their social relationships might weigh heavily

in their decision making process. Against thus background the

responsibility for lending should be delegated to loan officers or credit

analyst.

Credit review is another guidelines for which commercial banks must be

put into consideration in making of lending to their customers. In order to