Embed Size (px)

Citation preview

Risk Management by banks financing agriculture and

rural enterprise:

African and Asian Experiences

Expert Meeting on Managing Risk in Financing Agriculture

Johannesburg,1-3 April, 2009

Ajai Nair, Consultant,

The World BankThe World Bank

Expert Meeting on Managing Risk in Financing Agriculture, 1-3 April 2009, Johannesburg

2

Presentation Outline

Study framework

Key Research Questions

Institutions Studied

Findings

Conclusions

Way Forward

Expert Meeting on Managing Risk in Financing Agriculture, 1-3 April 2009, Johannesburg

3

Study Framework

Cover major institutional types - Commercial banks, Development finance institutions, and supply chain organizations

Include only institutions with relatively large agricultural portfolios

Understand the policy environment and business model

Understand credit risk assessment and credit risk management.

Expert Meeting on Managing Risk in Financing Agriculture, 1-3 April 2009, Johannesburg

4

Key Research Questions

Agricultural Credit Risk Assessment What information is used to assess

credit applications?

How important is agricultural domain knowledge?

Is credit-risk quantified at the loan-level and at the portfolio level?

Does credit risk influence terms of credit?

Expert Meeting on Managing Risk in Financing Agriculture, 1-3 April 2009, Johannesburg

5

Key Research Questions

Agricultural Credit Risk Management Are collateral substitutes used?

Do lenders facilitate access to risk mitigation services for borrowers?

How diversified is the credit portfolio – within the agricultural portfolio / total portfolio?

Are risk transfer mechanisms used?

Are any special asset classification and provisioning mechanisms used?

Expert Meeting on Managing Risk in Financing Agriculture, 1-3 April 2009, Johannesburg

6

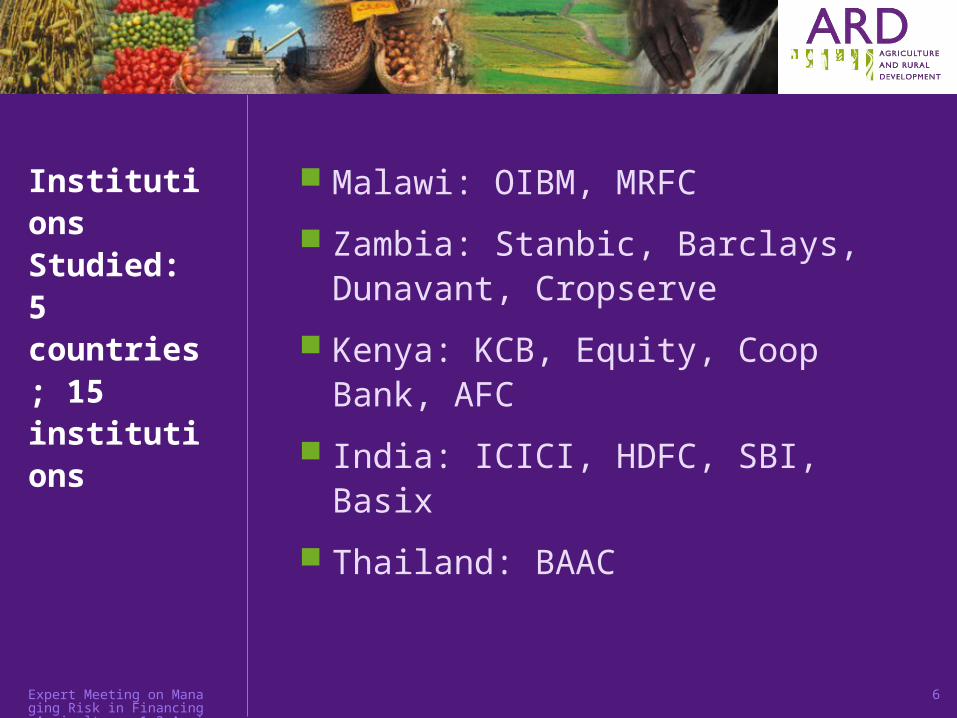

Institutions Studied: 5 countries; 15 institutions

Malawi: OIBM, MRFC

Zambia: Stanbic, Barclays, Dunavant, Cropserve

Kenya: KCB, Equity, Coop Bank, AFC

India: ICICI, HDFC, SBI, Basix

Thailand: BAAC

Expert Meeting on Managing Risk in Financing Agriculture, 1-3 April 2009, Johannesburg

7

Institutions Studied: 5 countries; 15 institutions

8 Commercial Banks 2 international and 6 national banks 7 traditional commercial banks and 1 microfinance

bank 4 provide retail services to small farmers; 4 provide

to retail services to large farmers and agribusinesses

1 apex bank lending to cooperatives

4 Development Finance Institutions 1 agricultural development bank 2 agricultural finance corporations 1 microfinance finance company

2 Supply-chain finance providers Produce buyer Input supplier

Expert Meeting on Managing Risk in Financing Agriculture, 1-3 April 2009, Johannesburg

8

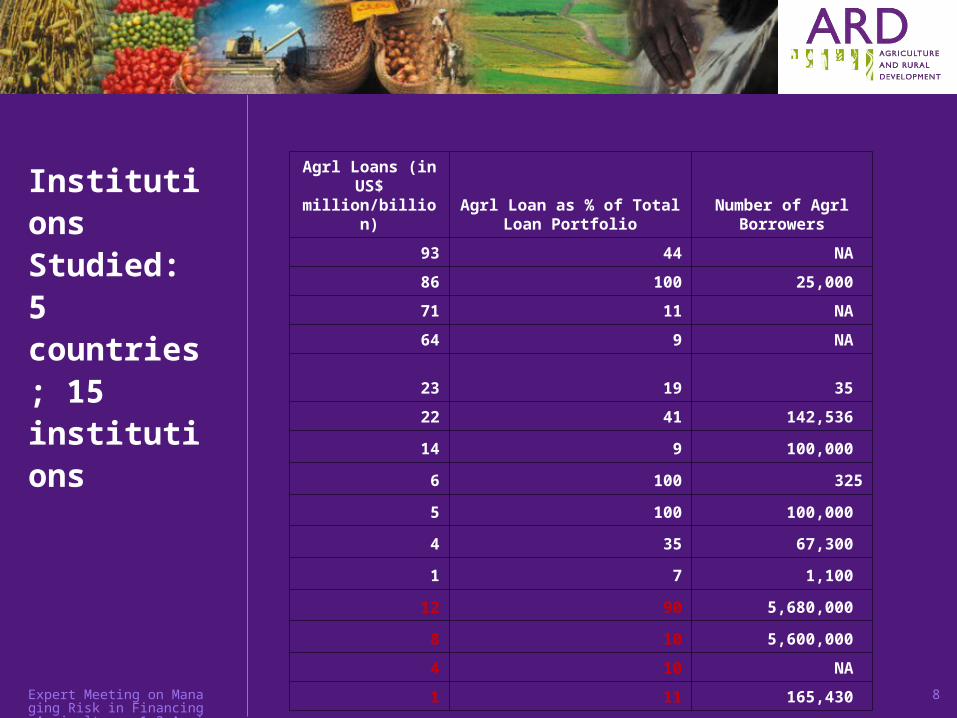

Institutions Studied: 5 countries; 15 institutions

Agrl Loans (in US$ million/billion)

Agrl Loan as % of Total Loan Portfolio

Number of Agrl Borrowers

93 44 NA

86 100 25,000

71 11 NA

64 9 NA

23 19 35

22 41 142,536

14 9 100,000

6 100 325

5 100 100,000

4 35 67,300

1 7 1,100

12 90 5,680,000

8 10 5,600,000

4 10 NA

1 11 165,430

Expert Meeting on Managing Risk in Financing Agriculture, 1-3 April 2009, Johannesburg

9

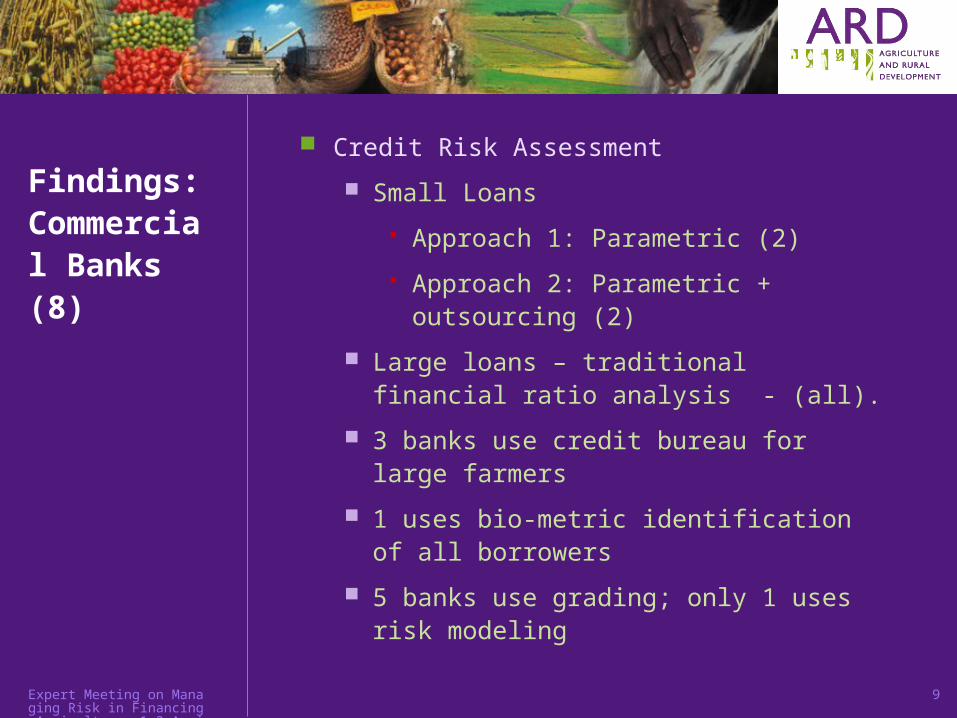

Findings: Commercial Banks (8)

Credit Risk Assessment

Small Loans

Approach 1: Parametric (2)

Approach 2: Parametric + outsourcing (2)

Large loans – traditional financial ratio analysis - (all).

3 banks use credit bureau for large farmers

1 uses bio-metric identification of all borrowers

5 banks use grading; only 1 uses risk modeling

Expert Meeting on Managing Risk in Financing Agriculture, 1-3 April 2009, Johannesburg

10

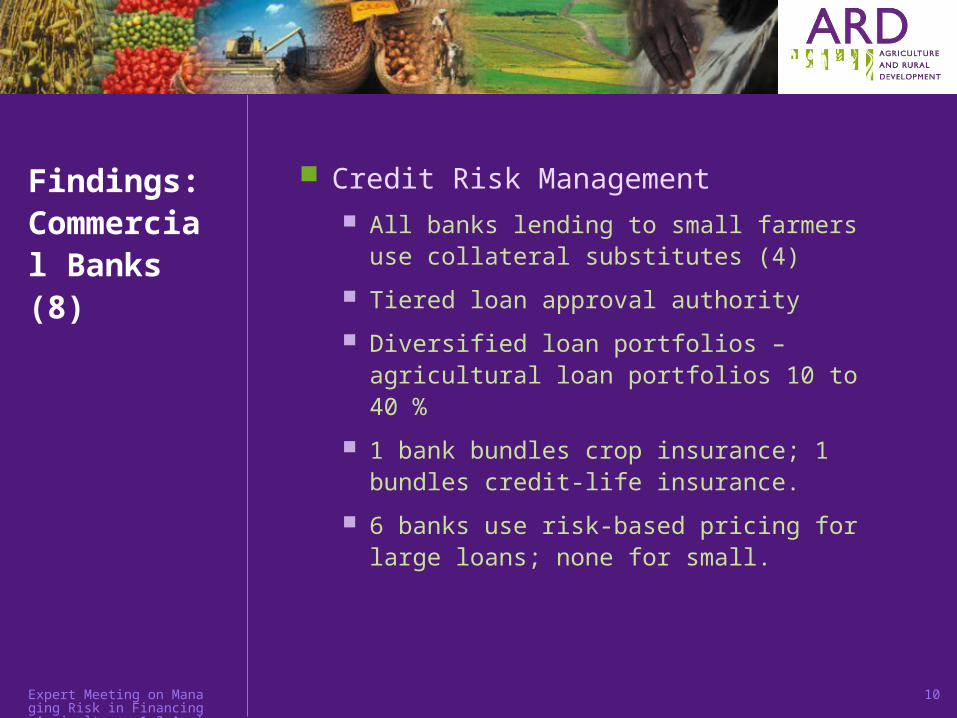

Findings: Commercial Banks (8)

Credit Risk Management All banks lending to small farmers use

collateral substitutes (4)

Tiered loan approval authority

Diversified loan portfolios – agricultural loan portfolios 10 to 40 %

1 bank bundles crop insurance; 1 bundles credit-life insurance.

6 banks use risk-based pricing for large loans; none for small.

Expert Meeting on Managing Risk in Financing Agriculture, 1-3 April 2009, Johannesburg

11

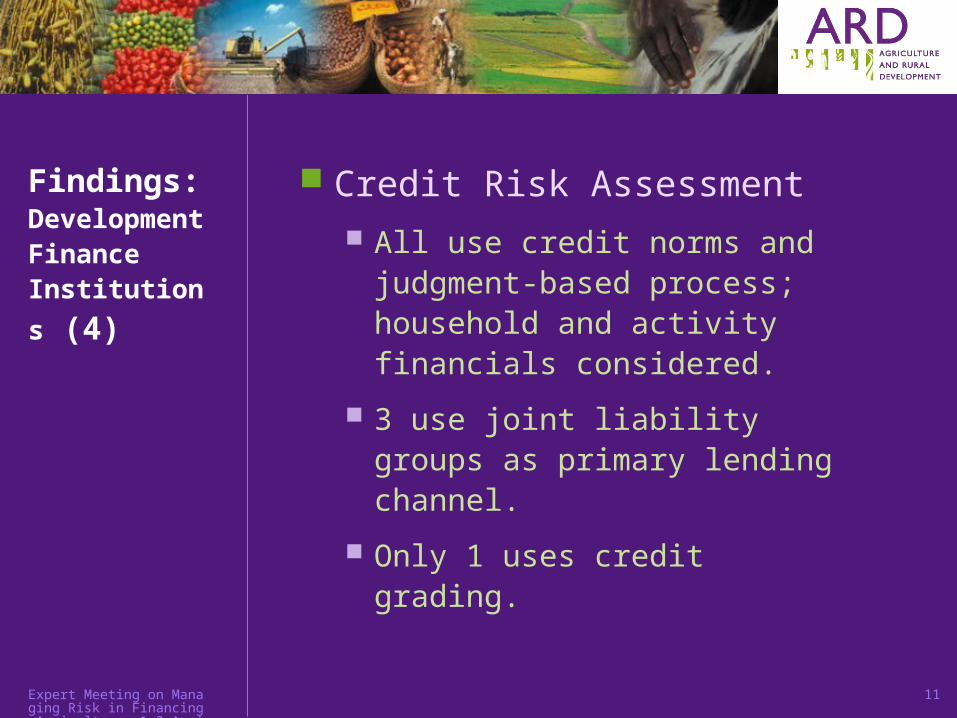

Findings: Development Finance

Institutions (4)

Credit Risk Assessment

All use credit norms and judgment-based process; household and activity financials considered.

3 use joint liability groups as primary lending channel.

Only 1 uses credit grading.

Expert Meeting on Managing Risk in Financing Agriculture, 1-3 April 2009, Johannesburg

12

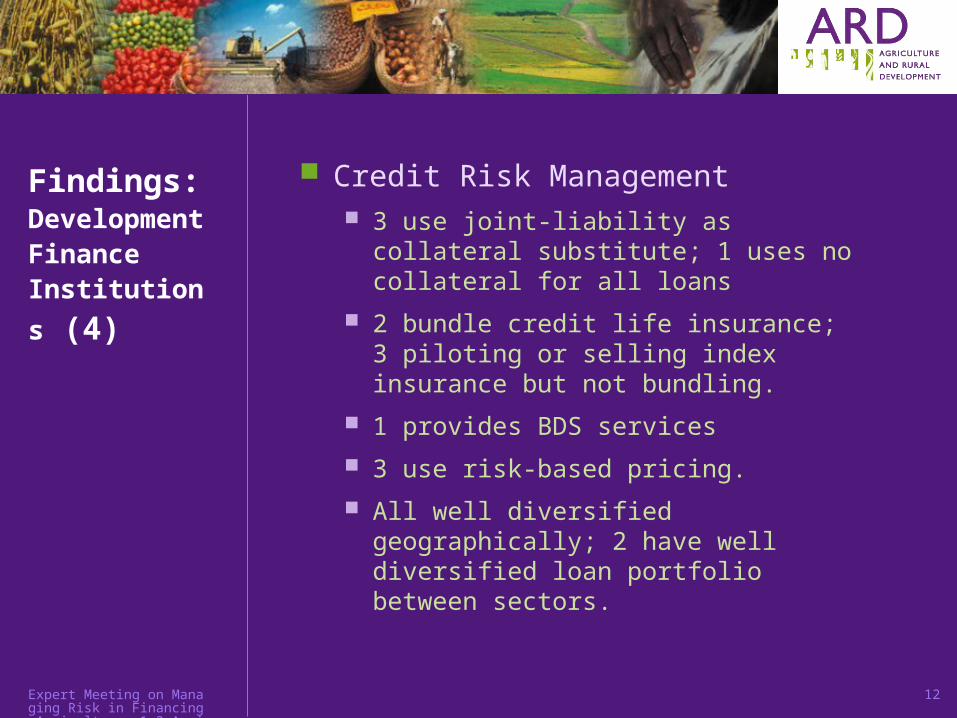

Findings: Development Finance

Institutions (4)

Credit Risk Management 3 use joint-liability as collateral

substitute; 1 uses no collateral for all loans

2 bundle credit life insurance; 3 piloting or selling index insurance but not bundling.

1 provides BDS services

3 use risk-based pricing.

All well diversified geographically; 2 have well diversified loan portfolio between sectors.

Expert Meeting on Managing Risk in Financing Agriculture, 1-3 April 2009, Johannesburg

13

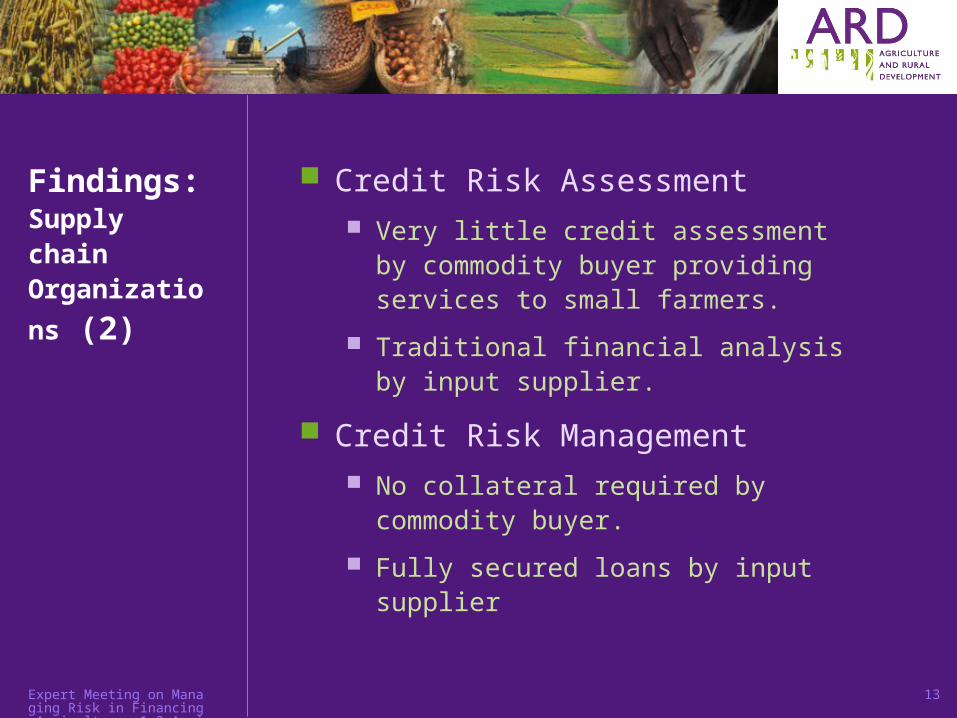

Findings: Supply chain

Organizations (2)

Credit Risk Assessment Very little credit assessment by

commodity buyer providing services to small farmers.

Traditional financial analysis by input supplier.

Credit Risk Management No collateral required by commodity

buyer.

Fully secured loans by input supplier

Expert Meeting on Managing Risk in Financing Agriculture, 1-3 April 2009, Johannesburg

14

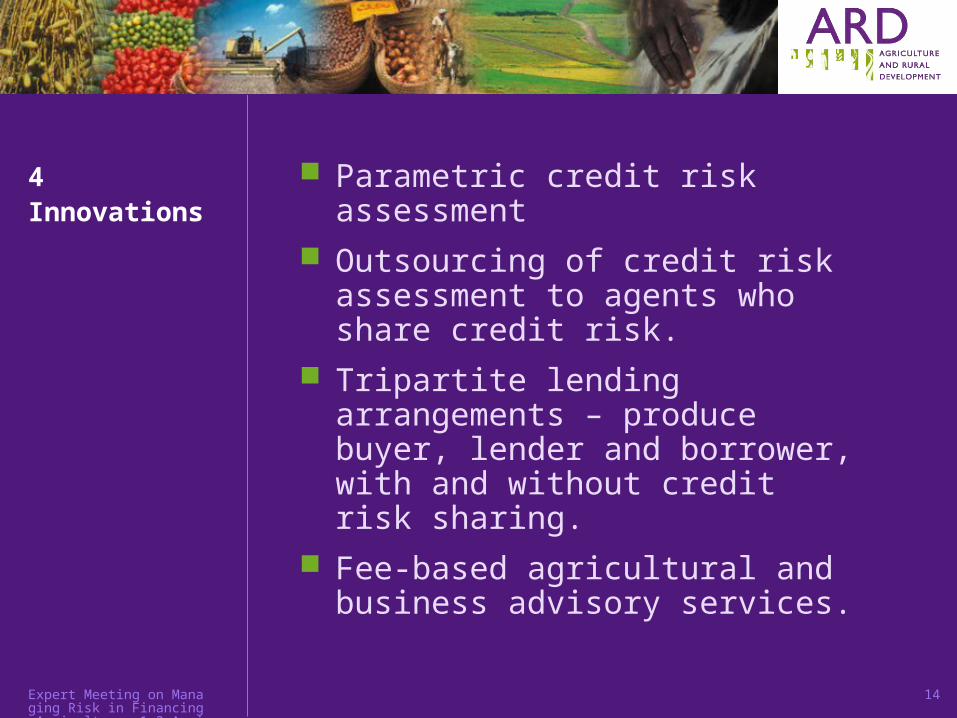

4 Innovations Parametric credit risk assessment

Outsourcing of credit risk assessment to agents who share credit risk.

Tripartite lending arrangements – produce buyer, lender and borrower, with and without credit risk sharing.

Fee-based agricultural and business advisory services.

Expert Meeting on Managing Risk in Financing Agriculture, 1-3 April 2009, Johannesburg

15

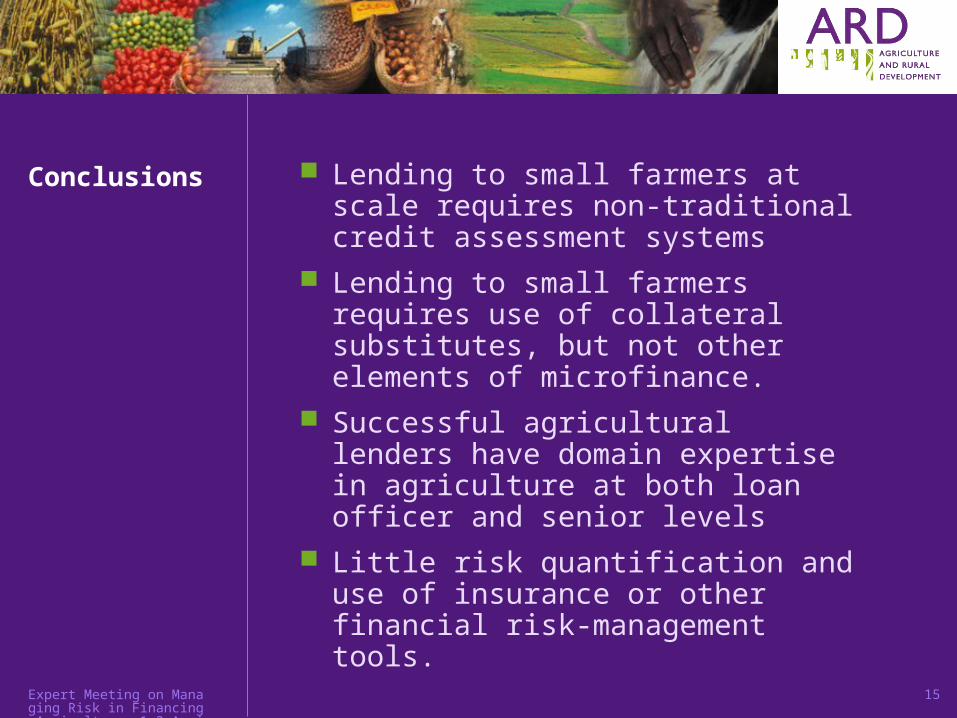

Conclusions Lending to small farmers at scale requires non-traditional credit assessment systems

Lending to small farmers requires use of collateral substitutes, but not other elements of microfinance.

Successful agricultural lenders have domain expertise in agriculture at both loan officer and senior levels

Little risk quantification and use of insurance or other financial risk-management tools.

Expert Meeting on Managing Risk in Financing Agriculture, 1-3 April 2009, Johannesburg

16

Some questions

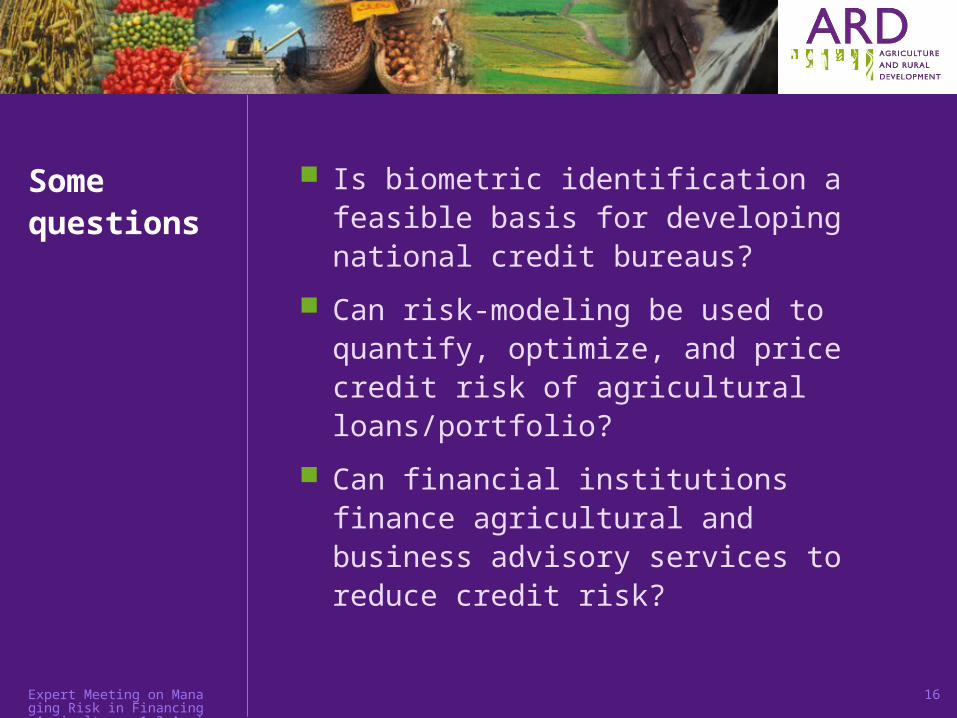

Is biometric identification a feasible basis for developing national credit bureaus?

Can risk-modeling be used to quantify, optimize, and price credit risk of agricultural loans/portfolio?

Can financial institutions finance agricultural and business advisory services to reduce credit risk?