Embed Size (px)

Citation preview

Retirement

Not FDIC InsuredMay Lose ValueNot Bank Guaranteed

SIMPLE IRAA Guide for Business Owners

OppenheimerFunds is not undertaking to provide impartial investment advice or to provide advice in a fiduciary capacity.

1

A Simple Retirement Plan for Your Employees—and You

As a small business owner, saving for your retirement is probably one of your most important goals. Attract ing and keeping the best employees is also of critical importance. Sponsoring a retirement plan may be the perfect way to address both of these compelling needs.

For many small business owners, providing a standard 401(k) plan is simply too expensive and complex to be practical. OppenheimerFunds offers a SIMPLE IRA product. It is a cost-effective plan with minimal administrative oversight, to help you and your employees boost retirement savings potential.

A SIMPLE IRA may be an ideal vehicle for small businesses that wish to establish personal Individual Retirement Accounts (IRAs) for both owners and their employees. The plan provides the quality investments and outstanding service you and your staff need to work toward the long-term security you desire. It offers:

• Powerful advantages for small businesses• Generous, no-hassle features• Comprehensive investment options and support

2

OppenheimerFunds®

Filing Status/Adjusted Gross Income for 2018

Credit Individual Head of Household Married Filing Jointly

2018 50% $0–$19,000 $0–$28,500 $0–$38,001

20 $19,001–$20,500 $28,501–$30,750 $38,001–$41,000

10 $20,501–$31,500 $30,751–$47,250 $40,001–$63,000

0 More than $31,500 More than $47,250 More than $63,000

1. If the total value of the participant’s investments in retirement and/or non-retirement accounts in Oppenheimer funds, excluding OppenheimerFunds direct-sold 529 plans, is $50,000 or more, the annual maintenance fee is $0.

2. Students and dependents are not eligible for this credit. Credit amount equals a percentage of contributions permitted to be counted.

Powerful Advantages for Small Businesses

OppenheimerFunds’ SIMPLE IRA is a surprisingly easy and cost efficient way to give your business an edge. Because so few small businesses offer a retirement plan, a SIMPLE IRA can be a real plus in attracting—and holding onto—qualified workers.

Offering pretax salary deferrals and tax-deferred investment growth, a SIMPLE IRA gives small businesses the most desirable benefits of a corporate retirement plan, while eliminating the administrative burdens and expenses that typically accompany such programs.

In addition to helping employees save, SIMPLE IRAs provide several key benefits for business owners that 401(k) plans don’t:

• You can maximize your own salary deferral contributions, even if your employees participate at low levels or don’t contribute at all.

• Because SIMPLE IRAs don’t have complicated discrimination rules, they don’t require the various compliance tests that can be problematic for smaller companies.

• Maintaining a SIMPLE IRA costs far less than admini stering a 401(k) plan—each participant pays only $25 a year.1

Saver’s Credit

An employee who contributes to employer-sponsored retirement plans, including SIMPLE IRAs, may be eligible to receive a saver’s credit.

This credit is limited based on the income of the employee. The maximum saver’s credit is $2,000 for single filers and $4,000 for married couples; however, the amount could be less.2

3

The Right Way to Invest

Generous, No-Hassle Features

Generally, you may establish a SIMPLE IRA if your business has 100 or fewer employees and doesn’t already have another retirement plan. SIMPLE IRAs may also be appropriate for sole proprietors, independent contractors and freelancers.

Higher Employee Contribution Limits

To qualify for a SIMPLE IRA, employees must have completed two years of service during which they’ve earned at least $5,000 per year, and they must expect to earn at least $5,000 during the current year. While you may include more employees by lessening the above requirements, you may not exclude workers by making these requirements more restrictive.

All participants (including the business owner) may contribute as much as 100% of their compensation, up to $12,500 for 2018. In addition, participants age 50 or older may make catch-up contributions up to $3,000 (2018) annually. When the plan’s mandatory employer contributions are taken into account, the annual savings may be as high as $25,000, or $31,000 for participants who are age 50 or older. Participants are immediately 100% vested in the total value of their SIMPLE IRA accounts.

If You’re a Non-Profit Organization

Many non-profit organizations and government entities may establish a SIMPLE IRA. This includes trade associations, advocacy groups, charities, country clubs, business leagues and chambers of commerce.

If this description fits your organization, you’ll want to discuss a SIMPLE IRA with your financial advisor.

4

OppenheimerFunds®

3. These hypothetical examples are not intended to show the performance of any Oppenheimer fund for any period of time, or fluctuations in principal value or investment return. The persons portrayed in these examples are fictional. This material does not constitute a recommendation as to the suitability of any investment for any person or persons having circumstances similar to those portrayed, and a financial advisor should be consulted.

Flexible Employer Contribution Options

While you are required to make contributions on behalf of employees, you have the flexibility to choose between the following two formulas:

1. Matching contributions. You can match participant contributions, dollar for dollar, up to 3% of each indi-vidual’s compensation to a maximum of $12,500, or $15,500 for participants who are age 50 or older. This amount can be reduced to a minimum of 1% for any two years out of a five-year period.

2. Nonelective contributions. Alternatively, you can contribute the equivalent of 2% of compensation for all eligible employees (based on compensation up to $275,000 in 2018), including those employees who chose not to contribute through salary deferrals. This means an employer’s maximum 2018 contribution is $5,500 for each employee.

Please note: You may switch between the two for-mulas, but such changes will not take effect until the start of the next calendar year. In addition, you must give employees at least 60 days’ advance notice of the change. Therefore, the last day to switch contribution options for the following calendar year is November 1.

A Great Savings Opportunity for Those with a Side Business3

If you earn extra money through a business on the side, you can set up an OppenheimerFunds SIMPLE IRA and convert some of your self-employment income into tax-deferred savings—even if you already participate in a retirement savings plan, like a 401(k), through your regular employer.

Additional Savings

While your own salary deferral contri butions to both a 401(k) and SIMPLE IRA generally can’t total more than $18,500 for 2018, you may be able to gain additional savings through matching contributions.

Example: Let’s say you earn $80,000 a year at your job with ABC Company, which matches your 401(k) contributions dollar for dollar up to 6% of your compen sation—or $4,800. You also earn $60,000 a year as a part-time photographer. Here’s how a SIMPLE IRA can make a difference.

401(k) Only 401(k) with SIMPLE IRA

401(k) Contribution $ 18,500 401(k) Contribution $ 5,500

401(k) Match (6%) 4,800 401(k) Match (6%) 4,800

SIMPLE IRA Contribution 12,500

SIMPLE IRA Match (3%) 1,800

Total Annual Savings $23,300 $24,600

5

The Right Way to Invest

4. These hypothetical examples are not intended to show the performance of any Oppenheimer fund, for any period of time, or fluctuations in principal value or investment return. The persons portrayed in these examples are fictional. This material does not constitute a recommendation as to the suitability of any investment for any person or persons having circumstances similar to those portrayed, and a financial advisor should be consulted.

A Double Tax Advantage for Employers

Since both employer and employee contributions are tax-deductible business expenses, sponsoring a SIMPLE IRA gives your business an immediate tax break. In addition, your own pretax employee contributions reduce your current-year taxable income, providing a personal tax benefit as well.

Easy Administration

A SIMPLE IRA is virtually maintenance free. There’s no top-heavy or discrimi nation testing, no government filing and only minimal paperwork. And because employees control their own investments, you don’t have to worry about taking on any significant fiduciary responsibility for the performance of their accounts. For more infor mation on SIMPLE IRA administration, including deadlines, see “A Look at the Details” on page 10 of this brochure.

Spousal Savings4

What’s more, if you’re married and your spouse is on the payroll of your side business, a SIMPLE IRA will give him or her a chance to defer as much as $12,500 of income (depending on eligible earnings) as well as receive an employer contribution.

Example: Let’s continue the scenario from the pre-vious example, but this time we’ll assume that your spouse is employed as your photographic assistant, earning an annual salary of $20,000.

As this example illustrates, the addition of a SIMPLE IRA can give a married couple’s combined annual retirement savings a big boost. In this case, you and your spouse would have been able to put away $37,700 ($24,600 + $13,100) by adding a SIMPLE IRA, versus $24,600 if you were saving alone.

And if you’re concerned about your spouse meeting a SIMPLE IRA’s minimum eligibility requirements, don’t be. Remember that you, as the sponsor, can set less restrictive standards than required by law.

You Your Spouse

401(k) Contribution $ 5,500 N/A

401(k) Match (6%) 4,800 N/A

SIMPLE IRA Contribution 12,500 12,500

SIMPLE IRA Match (3%) 1,800 600

Combined Annual Account Savings

$24,600 + $13,100

= $37,700

6

OppenheimerFunds®

Generally, you should consider a SIMPLE IRA if you: Reason

Want a plan with minimal administration. Requires no testing or government filing and entails minimal paperwork.

Have 100 or fewer employees, particularly if you have 25 or under.

Mandatory contributions may make the plan cost prohibitive for businesses with a larger number of employees.

Can afford only a low cost plan. Relative to other types of plans, a SIMPLE IRA is one of the least expensive options available.

Can contribute significantly more money than your employees.

Allows you to maximize your own contributions, regardless of how much your employees make or contribute.

Have consistent earnings. Employer contributions on behalf of employees must be made annually.

Don’t have high turnover. Employees are immediately 100% vested in the plan.

Have employees who want to contribute to a retirement savings plan.

Employees may make elective salary deferral contributions.

Are in a competitive labor market. Very few small businesses offer a retirement plan.

You’ll want to look at other plan options if you: Reason

Have more than 100 employees. Businesses with over 100 eligible employees do not meet a SIMPLE IRA’s sponsorship requirements.

Have high employee turnover. You may want a plan that allows you to control eligibility and vesting, like a 401(k).

Can’t afford to fund the plan each year. Profit-sharing and SEP plans, for instance, give you the flexibility to reduce or stop employer contributions.

Already have some type of tax-advantaged retirement plan. Generally, a SIMPLE IRA can’t be paired with another qualified plan. However, individuals with self-employment income from a side business may establish a SIMPLE IRA, even if they’re participants in another company-sponsored retirement savings plan.

Want to tax-shelter the maximum amount of income possible. Other plans—e.g., profit-sharing plans—have higher contribution limits.

When Is a SIMPLE IRA the Best Choice?

As with all retirement plans, a SIMPLE IRA can be a better fit in some situations than in others.

7

The Right Way to Invest

SIMPLE IRA 401(k)

Plan size 100 or fewer eligible employees; 25 or under is optimal

25+ is optimal

Administration Low Higher

Cost Low Higher

Employer contributions Mandatory; must follow one of two plan formulas

Discretionary match

Maximum employee salary deferral 100% of gross compensation up to $12,500 (in 2018)

Catch-up contributions of up to $3,000 (in 2018) permitted for participants age 50 and older

100% of gross compensation up to $18,500 (in 2018)

Catch-up contributions of up to $6,000 (in 2018) permitted for participants age 50 and older

Vesting Participants are immediately 100% vested in all contributions

Choice of vesting schedule for employer contributions

Hardship withdrawals5 Not available Available

Loans Not available Available

Nondiscrimination testing Not available Required at least once a year

Additional fees No Yes

5. Withdrawals due to death, disability, divorce or those taken as substantially equal periodic payments over the participant’s life expectancy are not subject to the premature distribution penalty.

SIMPLE IRA or 401(k)? Which Is Best for You?

Debating between a SIMPLE IRA and a 401(k)? This chart comparing the key features of each type of plan may help you and your advisor decide.

8

OppenheimerFunds®

Comprehensive Investment Options and Support

When you or your employees establish a SIMPLE IRA account, you can select the funds in which your contributions will be invested. OppenheimerFunds, a market leader in SIMPLE IRAs, makes the process easier by offering the investment solutions and services you need to reach your retirement savings goals.

Comprehensive Investments

Founded in 1959, OppenheimerFunds is a global asset manager with decades of experience serving the needs of retirement plan participants and sponsors, as well as their advisors. We offer investments across every major asset class, including U.S. and international equity and fixed-income portfolios. We also provide innovative asset allocation strategies to help investors pursue specific investment and risk management objectives. In our view, The Right Way to Invest encompasses four key principles: make global connections, look to the long term, take intelligent risks and invest with experience.

Investor Services and Support

All SIMPLE IRA participants have access to our website, oppenheimerfunds.com, where you’ll find account information, fund descriptions and much more.

OppenheimerFunds Also Provides Participants

• Easy-to-read statements.• Comprehensive investment education

and enrollment support.• A toll-free number for account inquiries

and automated exchanges.

Technology-Based Solutions

You can make contributions online with our Contribution Processing System. This program provides you with greater control over changing contributions, changing fund allocations and submitting plan payments. Call 800 835 7305 for more information today.

9

The Right Way to Invest

How to Set Up an OppenheimerFunds SIMPLE IRA

Setting up an OppenheimerFunds SIMPLE IRA is easy. Just follow these five steps.

1. Read and complete the IRS Form 5304-SIMPLE.

2. Determine who is eligible to participate in your plan, then notify these eligible employees using the Notification to Eligible Employees form (contained in IRS Form 5304-SIMPLE). In addition, provide them with a copy of your completed IRS Form 5304-SIMPLE.

3. Encourage employees to enroll by giving each a SIMPLE IRA Participant Guide and applications (RB0000.051).

4. Ask employees to complete and return (to you)• The Model Salary Reduction Agreement (found

in their copy of IRS Form 5304-SIMPLE) which is provided by you from this guide.

• The appropriate forms in the SIMPLE IRA Participant Guide.

5. Send the following items to one of the addresses listed below

• The original completed IRS Form 5304-SIMPLE (please keep a copy for yourself).

• A completed SIMPLE IRA Application and/or SIMPLE IRA Transfer Request Form (if applicable) for each eligible employee.

Mail to:OppenheimerFunds Distributor, Inc. P.O. Box 5390 Denver, CO 80217-5390

If you are using an overnight delivery service, please send to:OppenheimerFunds Services 6803 S. Tucson Way Centennial, CO 80112-3924

10

OppenheimerFunds®

A Look at the Details

Who can sponsor a SIMPLE IRA?• Businesses that have 100 or fewer eligible employ-

ees and don’t maintain another retirement plan.• Non-profit organizations (including government

entities).• Individuals with any type of self-employment

income (including sole proprietors and moon-lighters), even if they already participate in another employer-sponsored retirement plan.

What about plan adoption and contribution deadlines?• The plan is maintained on a calendar-year basis

and must be set up by October 1.• Employer contributions must be made by employ-

er’s tax filing deadline, including extensions.• Employee salary deferral contributions must be

deposited into the employee’s account no later than the 30th day of the next month.

How do employers fund the plan?• Employer contributions are mandatory and may be

based on either one of the following two formulas: 1. A dollar-for-dollar match on employee deferrals

up to 3% of compensation, unless the employer elects a lower match of not less than 1% for two out of any five years. The match is not required if an eligible employee doesn’t participate in salary deferrals.

2. A contribution of 2% of compensation (limited to compensation of $275,000 in 2018 for each eligible employee who has $5,000 in wages for the year. The 2% nonelective contributions must be made for all eligible employees, regardless of their participation in salary deferrals.

• Employers may switch formulas in a new calendar year as long as employees are notified at least 60 days prior to January 1.

How much may employees contribute?• Employees may make elective salary deferral

contributions of up to $12,500 (in 2018) or 100% of their compensation after Social Security and unemployment taxes (FICA and FUTA) are paid, whichever is less.

• In addition, participants who are age 50 or older may make catch-up contributions of up to $3,000 (in 2018).

Which employees are eligible to participate?• Employees with two years of service during which

they have earned at least $5,000 and who are ex pect ed to earn at least $5,000 during the current year may participate. (Employer may set less res-tric tive eligibility standards.)

What about taxes?• Elective salary deferral contributions are made

on a pretax basis, reducing income subject to federal taxation.

• Earnings on account contributions grow tax deferred until withdrawal.

11

The Right Way to Invest

• Upon withdrawal, account assets are taxed as ordinary income, although early withdrawals (those taken prior to age 59½) are subject to an additional 25% tax penalty if taken within the first two years from first contribution and a 10% tax penalty if taken after the first two years. The penalty is waived for distributions received due to death, disability, qualified medical expenses, qualified health insurance payments, qualified higher education expenses, a qualified first-time home purchase and distributions taken as substantially equal periodic payments over the participant’s life expectancy.

• Tax-free rollovers from a SIMPLE IRA to another SIMPLE IRA are permitted at any time. Tax-free rollovers or transfers can be made from a SIMPLE IRA to a regular IRA, qualified plan, 403(b), SEP IRA and 457 after two years from first contribution in the SIMPLE IRA. Rollovers and transfers cannot be made from a regular IRA, qualified plan, 403(b), SEP IRA and 457 into a SIMPLE IRA. Please be sure to check if there are any restrictions associated with a provider’s plan before moving your plan.

• All employee contributions are tax deductible as a business expense.

• Lower-income employees may be eligible for a tax credit of up to $2,000 for contributions made to the SIMPLE IRA. Please talk to your financial advisor for more information.

When do employees become vested?• Participants are immediately 100% vested in all

contributions.

What are the administration and reporting requirements?• Minimal. Employees must be notified of their

option to participate no later than the first day the participant is eligible and each year given 60 days notice to change their deferral election. In addition, if you modify the contribution method or change eligibility requirements, you must notify employees 60 days prior to January 1 or the date designated by the employer in the Adoption Agreement if your plan is already established or 60 days prior to the effective date if you are establishing a new plan. For example, if you are establishing a SIMPLE IRA plan on April 1, 2018, you must give notice to employees by February 1, 2018.

• Employers must complete IRS Form 5304-SIMPLE and provide copies to employees.

• No IRS filing is required.• Participants must complete a SIMPLE IRA Appli-

cation, and if applicable, a SIMPLE IRA Transfer Request Form, as well as the Salary Reduction Agreement and return them to you before admission to the plan.

12

OppenheimerFunds®

Questions & Answers

Q. May I establish a SIMPLE IRA if I already have another retirement plan, such as a Money Purchase Pension plan?

A. No. A SIMPLE IRA is not available to employers who maintain another retirement plan for the same business. If you currently have another retirement plan, you must terminate or freeze it before establishing a SIMPLE IRA.

Q. Do I have to make a contribution on behalf of employees who don’t make any salary deferral contributions?

A. It depends on the formula you choose. If you decide to use the dollar-for-dollar 3% match, you need not contribute anything for participants who don’t defer a portion of their salary to the plan. If you choose the nonelective contribution equal to 2% of compensation, you must do so for all eligible employees, whether or not they participate in salary deferrals.

Q. Are employees required to contribute to a SIMPLE IRA?

A. No, employee contributions are discretionary.

Q. What are the deadlines for establishing a SIMPLE IRA?

A. A new SIMPLE IRA can be established up until October 1 and must be maintained thereafter on a calendar-year basis. Employees must be notified of their eligibility to make deferral elections on or before the day they become eligible, and give them 60 days to complete the salary deduction form to make deferral elections. For example, if you wish to establish a new SIMPLE IRA on January 1, 2018, you will need to notify employees who are eligible to participate by November 1, 2017.

Q. Can employees change the amount of their salary deferrals?

A. Yes. Employees may modify a salary reduction election during the 60-day period before January 1 of the effective year or the date designated by the employer in the Adoption Agreement. The Notifi cation to Eligible Employees is used to notify employees of their ability to modify their elections and to communicate the amount of employer contributions for the year.

Q. May I exclude any employees from a SIMPLE IRA?

A. Yes, union employees and nonresident aliens may be excluded.

Q. Are tax-exempt organizations able to establish a SIMPLE IRA?

A. Yes, tax-exempt organizations, including government entities, can establish one.

Q. Can I establish a SIMPLE IRA if I’m self-employed, but don’t have any employees?

A. Yes, a SIMPLE IRA is an appropriate alternative for a sole proprietor or independent contractor.

Q. If I put money into an IRA every year, does my IRA contribution count toward my SIMPLE IRA contributions?

A. No, you may still defer as much as $12,500 (in 2018) to your SIMPLE IRA account. In addition, participants age 50 and older may make catch-up contributions of up to $3,000 (in 2018).

Q. Can an employee who leaves or terminates service with an employer transfer SIMPLE IRA funds to other investments?

A. An employee who leaves or terminates service may transfer their SIMPLE IRA to another SIMPLE IRA without restriction. However, if rolling over to another retirement plan type, other than a SIMPLE IRA, the first contribution to the SIMPLE IRA plan must be 2-years-old or older.

13

The Right Way to Invest

Contribution Processing System (CPS) Information

What Is CPS?

OppenheimerFunds’ Contribution Processing System (CPS) is an Internet-based system that allows you to submit retirement plan contributions electronically and receive confirmation instantaneously.

Flexibility

• Submit contribution information to OppenheimerFunds at your convenience. The Automatic Contribution feature eliminates the need to send us instructions each payroll period. We simply deduct the designated amount from your business bank account on the specified date until instructed otherwise.

• Submit contribution information for multiple plans.• Customize plan screen settings to suit your

business needs.• Site available 24 hours a day, seven days a week.

Less Paperwork

• Submit contribution instructions electronically.• Update participant information online, including

fund allocations.

• View contribution history online.• Make payments using our flexible Automated

Clearing House (ACH) feature. OppenheimerFunds can deduct the funds directly from your bank account.

Security

• Secure website features Secured Socket Layer (SSL) encryption.

Ease of Use

• CPS self set-up feature.• Minimal data entry—employee information,

including name and Social Security number are already online. Simply enter the contribution amount for each employee.

• Contributions can be submitted using the online spreadsheet or by attaching a preformatted spreadsheet—e.g., Excel.

• Automatic contributions can be scheduled for fixed dollar amounts.

Interested?

Visit https://retire.oppenheimerfunds.com, click on “Contribution Processing System,” then click on “New? Register Here!” to set up your own user ID and password.

Please note: We need to have your employer ID in our system before you can set up CPS for your plan. Please contact us at 800 835 7305.

14

OppenheimerFunds®

Payment Options

• ACH funds deducted from your bank account. Funds can be deducted according to your instructions each payroll period or through the Automatic Contribution feature.

• ACH push• Check• Fed wire

Cost-Effective

• Free service• Saves mailing costs• Saves paper

CPS Questions & Answers

Can I create my own user ID and password?Yes. Visit https://retire.oppenheimerfunds.com, click on “Contribution Processing System,” then click on “New? Register Here!” button on the log in screen. You will need your employer’s name as it appears on the plan application, your employer’s tax ID # and one of the following:

• City• State• Zip code

Can I use CPS to view contribution history and verify contributions have been posted?Yes. CPS is designed to assist you with the mainte-nance of your plan. You will have the ability to view contribution history and verify when money has been posted to employee accounts.

Do participants have access to their retirement accounts through CPS?No. Participants in OppenheimerFunds-sponsored retirement plans can access their retirement accounts at oppenheimerfunds.com. Participants must have their Social Security number and an account number to establish online account access.

Is the website secure?Yes. The CPS system uses Secured Socket Layer (SSL) encryption to help ensure that all transferred data remains private.

What are the benefits of the Automatic Contribution feature?The Automatic Contribution feature eliminates the need to send us instructions each payroll period. We simply deduct the designated amount from your bank account through ACH on the specified date each payroll period until instructed otherwise. The frequency of your payroll period may be weekly, bi-weekly, monthly, month-end, semi-monthly, quarterly or quarter-end.

Will participants be able to update allocation instructions by contacting OppenheimerFunds?Yes. If participants wish to change fund allocations or contribute to a new fund, they must contact OppenheimerFunds by letter, fax 303 768 1500 or phone 800 835 7305.

15

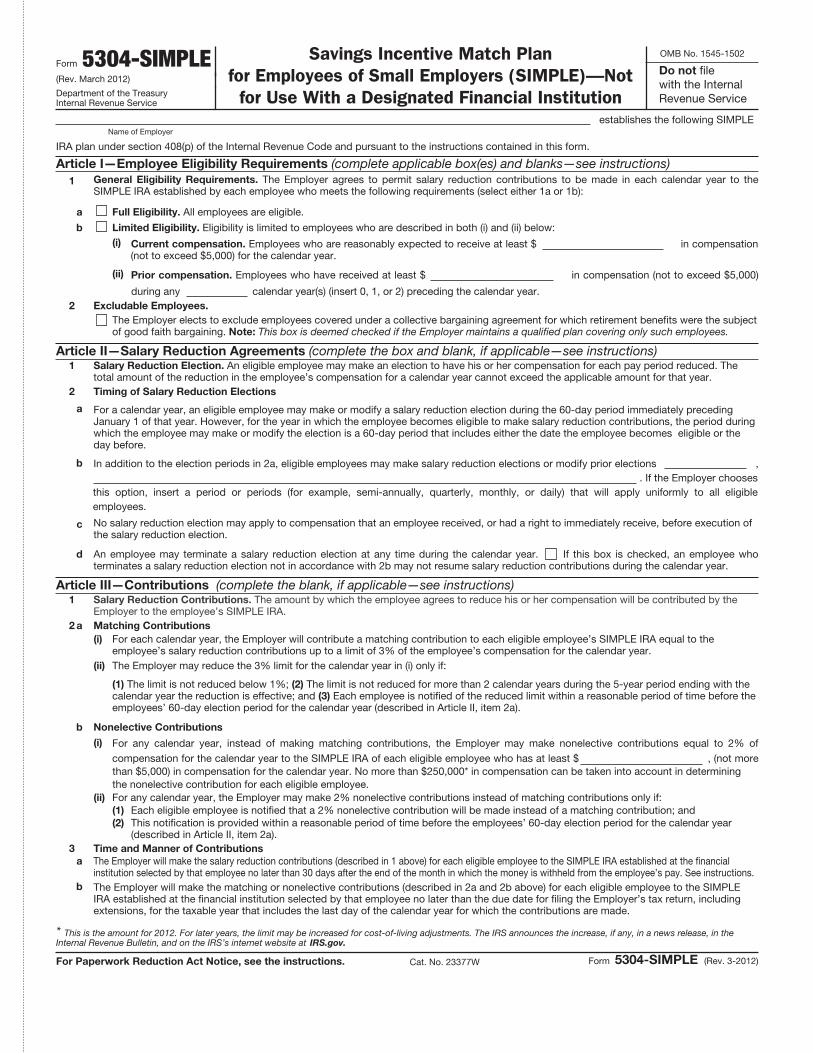

Form 5304-SIMPLE(Rev. March 2012)

Department of the Treasury Internal Revenue Service

Savings Incentive Match Plan for Employees of Small Employers (SIMPLE)—Not

for Use With a Designated Financial Institution

OMB No. 1545-1502

Do not file with the Internal Revenue Service

Name of Employer establishes the following SIMPLE

IRA plan under section 408(p) of the Internal Revenue Code and pursuant to the instructions contained in this form.

Article I—Employee Eligibility Requirements (complete applicable box(es) and blanks—see instructions) 1 General Eligibility Requirements. The Employer agrees to permit salary reduction contributions to be made in each calendar year to the

SIMPLE IRA established by each employee who meets the following requirements (select either 1a or 1b):

a Full Eligibility. All employees are eligible.

b Limited Eligibility. Eligibility is limited to employees who are described in both (i) and (ii) below: (i) Current compensation. Employees who are reasonably expected to receive at least $ in compensation

(not to exceed $5,000) for the calendar year.

(ii) Prior compensation. Employees who have received at least $ in compensation (not to exceed $5,000)

during any calendar year(s) (insert 0, 1, or 2) preceding the calendar year. 2 Excludable Employees.

The Employer elects to exclude employees covered under a collective bargaining agreement for which retirement benefits were the subject of good faith bargaining. Note: This box is deemed checked if the Employer maintains a qualified plan covering only such employees.

Article II—Salary Reduction Agreements (complete the box and blank, if applicable—see instructions) 1 Salary Reduction Election. An eligible employee may make an election to have his or her compensation for each pay period reduced. The

total amount of the reduction in the employee’s compensation for a calendar year cannot exceed the applicable amount for that year. 2 Timing of Salary Reduction Elections

a For a calendar year, an eligible employee may make or modify a salary reduction election during the 60-day period immediately preceding January 1 of that year. However, for the year in which the employee becomes eligible to make salary reduction contributions, the period during which the employee may make or modify the election is a 60-day period that includes either the date the employee becomes eligible or the day before.

b In addition to the election periods in 2a, eligible employees may make salary reduction elections or modify prior elections , . If the Employer chooses this option, insert a period or periods (for example, semi-annually, quarterly, monthly, or daily) that will apply uniformly to all eligible employees.

c No salary reduction election may apply to compensation that an employee received, or had a right to immediately receive, before execution of the salary reduction election.

d An employee may terminate a salary reduction election at any time during the calendar year. If this box is checked, an employee who terminates a salary reduction election not in accordance with 2b may not resume salary reduction contributions during the calendar year.

Article III—Contributions (complete the blank, if applicable—see instructions) 1 Salary Reduction Contributions. The amount by which the employee agrees to reduce his or her compensation will be contributed by the

Employer to the employee’s SIMPLE IRA. 2 a Matching Contributions

(i) For each calendar year, the Employer will contribute a matching contribution to each eligible employee’s SIMPLE IRA equal to the employee’s salary reduction contributions up to a limit of 3% of the employee’s compensation for the calendar year.

(ii) The Employer may reduce the 3% limit for the calendar year in (i) only if:

(1) The limit is not reduced below 1%; (2) The limit is not reduced for more than 2 calendar years during the 5-year period ending with the calendar year the reduction is effective; and (3) Each employee is notified of the reduced limit within a reasonable period of time before the employees’ 60-day election period for the calendar year (described in Article II, item 2a).

b Nonelective Contributions

(i) For any calendar year, instead of making matching contributions, the Employer may make nonelective contributions equal to 2% of compensation for the calendar year to the SIMPLE IRA of each eligible employee who has at least $ , (not more than $5,000) in compensation for the calendar year. No more than $250,000* in compensation can be taken into account in determining the nonelective contribution for each eligible employee.

(ii) For any calendar year, the Employer may make 2% nonelective contributions instead of matching contributions only if: (1) Each eligible employee is notified that a 2% nonelective contribution will be made instead of a matching contribution; and (2) This notification is provided within a reasonable period of time before the employees’ 60-day election period for the calendar year

(described in Article II, item 2a). 3 Time and Manner of Contributions

a The Employer will make the salary reduction contributions (described in 1 above) for each eligible employee to the SIMPLE IRA established at the financial institution selected by that employee no later than 30 days after the end of the month in which the money is withheld from the employee’s pay. See instructions.

b The Employer will make the matching or nonelective contributions (described in 2a and 2b above) for each eligible employee to the SIMPLE IRA established at the financial institution selected by that employee no later than the due date for filing the Employer’s tax return, including extensions, for the taxable year that includes the last day of the calendar year for which the contributions are made.

* This is the amount for 2012. For later years, the limit may be increased for cost-of-living adjustments. The IRS announces the increase, if any, in a news release, in the Internal Revenue Bulletin, and on the IRS’s internet website at IRS.gov.

For Paperwork Reduction Act Notice, see the instructions. Cat. No. 23377W Form 5304-SIMPLE (Rev. 3-2012)

Form 5304-SIMPLE (Rev. 3-2012) Page 2 Article IV—Other Requirements and Provisions

1 Contributions in General. The Employer will make no contributions to the SIMPLE IRAs other than salary reduction contributions (described in Article III, item 1) and matching or nonelective contributions (described in Article III, items 2a and 2b).

2 Vesting Requirements. All contributions made under this SIMPLE IRA plan are fully vested and nonforfeitable.

3 No Withdrawal Restrictions. The Employer may not require the employee to retain any portion of the contributions in his or her SIMPLE IRA or otherwise impose any withdrawal restrictions.

4 Selection of IRA Trustee. The Employer must permit each eligible employee to select the financial institution that will serve as the trustee, custodian, or issuer of the SIMPLE IRA to which the Employer will make all contributions on behalf of that employee.

5 Amendments To This SIMPLE IRA Plan. This SIMPLE IRA plan may not be amended except to modify the entries inserted in the blanks or boxes provided in Articles I, II, III, VI, and VII.

6 Effects Of Withdrawals and Rollovers

a An amount withdrawn from the SIMPLE IRA is generally includible in gross income. However, a SIMPLE IRA balance may be rolled over or transferred on a tax-free basis to another IRA designed solely to hold funds under a SIMPLE IRA plan. In addition, an individual may roll over or transfer his or her SIMPLE IRA balance to any IRA or eligible retirement plan after a 2-year period has expired since the individual first participated in any SIMPLE IRA plan of the Employer. Any rollover or transfer must comply with the requirements under section 408.

b If an individual withdraws an amount from a SIMPLE IRA during the 2-year period beginning when the individual first participated in any SIMPLE IRA plan of the Employer and the amount is subject to the additional tax on early distributions under section 72(t), this additional tax is increased from 10% to 25%.

Article V—Definitions 1 Compensation

a General Definition of Compensation. Compensation means the sum of the wages, tips, and other compensation from the Employer subject to federal income tax withholding (as described in section 6051(a)(3)), the amounts paid for domestic service in a private home, local college club, or local chapter of a college fraternity or sorority, and the employee’s salary reduction contributions made under this plan, and, if applicable, elective deferrals under a section 401(k) plan, a SARSEP, or a section 403(b) annuity contract and compensation deferred under a section 457 plan required to be reported by the Employer on Form W-2 (as described in section 6051(a)(8)).

b Compensation for Self-Employed Individuals. For self-employed individuals, compensation means the net earnings from self-employment determined under section 1402(a), without regard to section 1402(c)(6), prior to subtracting any contributions made pursuant to this plan on behalf of the individual.

2 Employee. Employee means a common-law employee of the Employer. The term employee also includes a self-employed individual and a leased employee described in section 414(n) but does not include a nonresident alien who received no earned income from the Employer that constitutes income from sources within the United States.

3 Eligible Employee. An eligible employee means an employee who satisfies the conditions in Article I, item 1 and is not excluded under Article I, item 2.

4 SIMPLE IRA. A SIMPLE IRA is an individual retirement account described in section 408(a), or an individual retirement annuity described in section 408(b), to which the only contributions that can be made are contributions under a SIMPLE IRA plan and rollovers or transfers from another SIMPLE IRA.

Article VI—Procedures for Withdrawals (The Employer will provide each employee with the procedures for withdrawals of contributions received by the financial institution selected by that employee, and that financial institution’s name and address (by attaching that information or inserting it in the space below) unless: (1) that financial institution’s procedures are unavailable, or (2) that financial institution provides the procedures directly to the employee. See Employee Notification in the instructions.)

Article VII—Effective Date

This SIMPLE IRA plan is effective . See instructions.

* * * * *

Name of Employer

Address of Employer

By: Signature Date

Name and title

Form 5304-SIMPLE (Rev. 3-2012)

Article VI—Procedures for Withdrawal (The employer will provide each employee with the procedures for withdrawals of contributions received by the financial institution selected by that employee, and that financial institution’s name and address (by attaching that information or inserting it in the space below) unless: (1) that financial institution’s procedures are unavailable, or (2) that financial institution provides the procedures directly to the employee. See Employee Notification on page 5.) Due to the unique nature of your participants’ financial circumstances and because of the possibility of tax penalties for failure to comply with IRS regulations on distributions from SIMPLE IRAs, your participants should consult with their tax advisor prior to requesting a distribution. To request a distribution from an OppenheimerFunds SIMPLE IRA account, go online at oppenheimerfunds.com or call OppenheimerFunds Services at 1.800.225.5677 to initiate a telephone distribution or request a copy of the OppenheimerFunds IRA Distribution Booklet. The completed form can be returned to OppenheimerFunds Services at P.O. Box 5390, Denver, Colorado 80217-5390 or by fax to 1.303.768.1500. If the distribution requested is in excess of $100,000, or if the requested redemption check is to be mailed to an address other than the address of record, then your signature on the IRA Distribution Request Form should be guaranteed by a financial institution of the type described in a current Oppenheimer fund prospectus and must be mailed. A beneficiary of a SIMPLE IRA account in any of the Oppenheimer funds may request a distribution by completing and returning the Inherited IRA Account Registration and Distribution Form with a copy of the Death Certificate of the account owner.

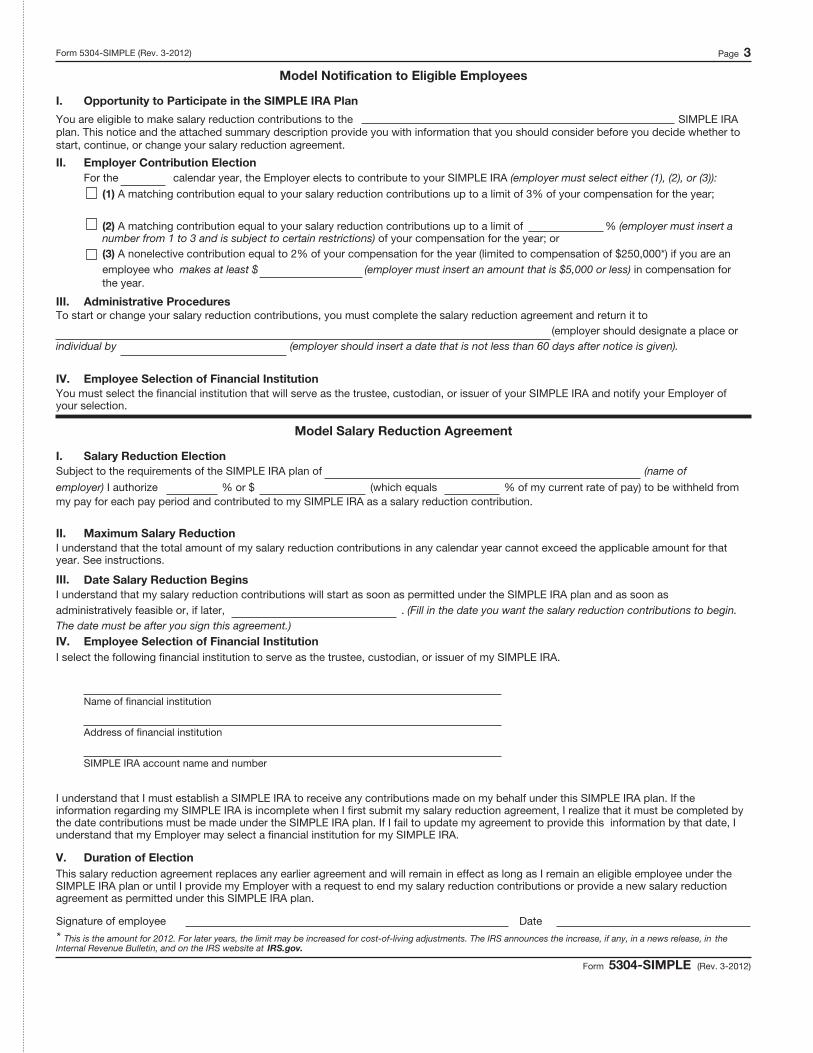

Form 5304-SIMPLE (Rev. 3-2012) Page 3

Model Notification to Eligible Employees

I. Opportunity to Participate in the SIMPLE IRA Plan

You are eligible to make salary reduction contributions to the SIMPLE IRA plan. This notice and the attached summary description provide you with information that you should consider before you decide whether to start, continue, or change your salary reduction agreement.

II. Employer Contribution Election For the calendar year, the Employer elects to contribute to your SIMPLE IRA (employer must select either (1), (2), or (3)):

(1) A matching contribution equal to your salary reduction contributions up to a limit of 3% of your compensation for the year;

(2) A matching contribution equal to your salary reduction contributions up to a limit of % (employer must insert a number from 1 to 3 and is subject to certain restrictions) of your compensation for the year; or (3) A nonelective contribution equal to 2% of your compensation for the year (limited to compensation of $250,000*) if you are an employee who makes at least $ (employer must insert an amount that is $5,000 or less) in compensation for the year.

III. Administrative Procedures To start or change your salary reduction contributions, you must complete the salary reduction agreement and return it to (employer should designate a place or individual by (employer should insert a date that is not less than 60 days after notice is given).

IV. Employee Selection of Financial Institution You must select the financial institution that will serve as the trustee, custodian, or issuer of your SIMPLE IRA and notify your Employer of your selection.

Model Salary Reduction Agreement

I. Salary Reduction Election Subject to the requirements of the SIMPLE IRA plan of (name of

employer) I authorize % or $ (which equals % of my current rate of pay) to be withheld from my pay for each pay period and contributed to my SIMPLE IRA as a salary reduction contribution.

II. Maximum Salary Reduction I understand that the total amount of my salary reduction contributions in any calendar year cannot exceed the applicable amount for that year. See instructions.

III. Date Salary Reduction Begins I understand that my salary reduction contributions will start as soon as permitted under the SIMPLE IRA plan and as soon as administratively feasible or, if later, . (Fill in the date you want the salary reduction contributions to begin. The date must be after you sign this agreement.) IV. Employee Selection of Financial Institution I select the following financial institution to serve as the trustee, custodian, or issuer of my SIMPLE IRA.

Name of financial institution

Address of financial institution

SIMPLE IRA account name and number

I understand that I must establish a SIMPLE IRA to receive any contributions made on my behalf under this SIMPLE IRA plan. If the information regarding my SIMPLE IRA is incomplete when I first submit my salary reduction agreement, I realize that it must be completed by the date contributions must be made under the SIMPLE IRA plan. If I fail to update my agreement to provide this information by that date, I understand that my Employer may select a financial institution for my SIMPLE IRA.

V. Duration of Election This salary reduction agreement replaces any earlier agreement and will remain in effect as long as I remain an eligible employee under the SIMPLE IRA plan or until I provide my Employer with a request to end my salary reduction contributions or provide a new salary reduction agreement as permitted under this SIMPLE IRA plan.

Signature of employee Date

* This is the amount for 2012. For later years, the limit may be increased for cost-of-living adjustments. The IRS announces the increase, if any, in a news release, in the Internal Revenue Bulletin, and on the IRS website at IRS.gov.

Form 5304-SIMPLE (Rev. 3-2012)

Form 5304-SIMPLE (Rev. 3-2012) Page 4

General Instructions Section references are to the Internal Revenue Code unless otherwise noted.

Purpose of Form Form 5304-SIMPLE is a model Savings Incentive Match Plan for Employees of Small Employers (SIMPLE) plan document that an employer may use to establish a SIMPLE IRA plan described in section 408(p), under which each eligible employee is permitted to select the financial institution for his or her SIMPLE IRA.

These instructions are designed to assist in the establishment and administration of the SIMPLE IRA plan. They are not intended to supersede any provision in the SIMPLE IRA plan.

Do not file Form 5304-SIMPLE with the IRS. Instead, keep it with your records.

For more information, see Pub. 560, Retirement Plans for Small Business (SEP, SIMPLE, and Qualified Plans), and Pub. 590, Individual Retirement Arrangements (IRAs).

Note. If you used the March 2002, August 2005, or September 2008 version of Form 5304-SIMPLE to establish a model Savings Incentive Match Plan, you are not required to use this version of the form.

Which Employers May Establish and Maintain a SIMPLE IRA Plan? To establish and maintain a SIMPLE IRA plan, you must meet both of the following requirements:

1. Last calendar year, you had no more than 100 employees (including self-employed individuals) who earned $5,000 or more in compensation from you during the year. If you have a SIMPLE IRA plan but later exceed this 100-employee limit, you will be treated as meeting the limit for the 2 years following the calendar year in which you last satisfied the limit.

2. You do not maintain during any part of the calendar year another qualified plan with respect to which contributions are made, or benefits are accrued, for service in the calendar year. For this purpose, a qualified plan (defined in section 219(g)(5)) includes a qualified pension plan, a profit-sharing plan, a stock bonus plan, a qualified annuity plan, a tax-sheltered annuity plan, and a simplified employee pension (SEP) plan. A qualified plan that only covers employees covered under a collective bargaining agreement for which retirement benefits were the subject of good faith bargaining is disregarded if these employees are excluded from

participating in the SIMPLE IRA plan. If the failure to continue to satisfy the 100-employee limit or the one-plan rule described in 1 and 2 above is due to an acquisition or similar transaction involving your business, special rules apply. Consult your tax advisor to find out if you can still maintain the plan after the transaction.

Certain related employers (trades or businesses under common control) must be treated as a single employer for purposes of the SIMPLE IRA requirements. These are: (1) a controlled group of corporations under section 414(b); (2) a partnership or sole proprietorship under common control under section 414(c); or (3) an affiliated service group under section 414(m). In addition, if you have leased employees required to be treated as your own employees under the rules of section 414(n), then you must count all such leased employees for the requirements listed above.

What Is a SIMPLE IRA Plan? A SIMPLE IRA plan is a written arrangement that provides you and your employees with an easy way to make contributions to provide retirement income for your employees. Under a SIMPLE IRA plan, employees may choose whether to make salary reduction contributions to the SIMPLE IRA plan rather than receiving these amounts as part of their regular compensation. In addition, you will contribute matching or nonelective contributions on behalf of eligible employees (see Employee Eligibility Requirements below and Contributions later). All contributions under this plan will be deposited into a SIMPLE individual retirement account or annuity established for each eligible employee with the financial institution selected by him or her.

When To Use Form 5304-SIMPLE A SIMPLE IRA plan may be established by using this Model Form or any other document that satisfies the statutory requirements.

Do not use Form 5304-SIMPLE if: 1. You want to require that all SIMPLE

IRA plan contributions initially go to a financial institution designated by you. That is, you do not want to permit each of your eligible employees to choose a financial institution that will initially receive contributions. Instead, use Form 5305-SIMPLE, Savings Incentive Match Plan for Employees of Small Employers (SIMPLE)—for Use With a Designated Financial Institution;

2. You want employees who are nonresident aliens receiving no earned income from you that is income from sources within the United States to be eligible under this plan; or

3. You want to establish a SIMPLE 401(k) plan.

Completing Form 5304-SIMPLE Pages 1 and 2 of Form 5304-SIMPLE contain the operative provisions of your SIMPLE IRA plan. This SIMPLE IRA plan is considered adopted when you have completed all applicable boxes and blanks and it has been executed by you.

The SIMPLE IRA plan is a legal document with important tax consequences for you and your employees. You may want to consult with your attorney or tax advisor before adopting this plan.

Employee Eligibility Requirements (Article I) Each year for which this SIMPLE IRA plan is effective, you must permit salary reduction contributions to be made by all of your employees who are reasonably expected to receive at least $5,000 in compensation from you during the year, and who received at least $5,000 in compensation from you in any 2 preceding years. However, you can expand the group of employees who are eligible to participate in the SIMPLE IRA plan by completing the options provided in Article I, items 1a and 1b. To choose full eligibility, check the box in Article I, item 1a. Alternatively, to choose limited eligibility, check the box in Article I, item 1b, and then insert “$5,000” or a lower compensation amount (including zero) and “2” or a lower number of years of service in the blanks in (i) and (ii) of Article I, item 1b.

In addition, you can exclude from participation those employees covered under a collective bargaining agreement for which retirement benefits were the subject of good faith bargaining. You may do this by checking the box in Article I, item 2. Under certain circumstances, these employees must be excluded. See Which Employers May Establish and Maintain a SIMPLE IRA Plan? above.

Salary Reduction Agreements (Article II) As indicated in Article II, item 1, a salary reduction agreement permits an eligible employee to make a salary reduction election to have his or her compensation for each pay period reduced by a percentage (expressed as a percentage or dollar amount). The total amount of

Form 5304-SIMPLE (Rev. 3-2012) Page 5

the reduction in the employee’s compensation cannot exceed the applicable amount for any calendar year. The applicable amount is $11,500 for 2012. After 2012, the $11,500 amount may be increased for cost-of-living adjustments. In the case of an eligible employee who is 50 or older by the end of the calendar year, the above limitation is increased by $2,500 for 2012. After 2012, the $2,500 amount may be increased for cost-of-living adjustments.

Timing of Salary Reduction Elections For any calendar year, an eligible employee may make or modify a salary reduction election during the 60-day period immediately preceding January 1 of that year. However, for the year in which the employee becomes eligible to make salary reduction contributions, the period during which the employee may make or modify the election is a 60-day period that includes either the date the employee becomes eligible or the day before.

You can extend the 60-day election periods to provide additional opportunities for eligible employees to make or modify salary reduction elections using the blank in Article II, item 2b. For example, you can provide that eligible employees may make new salary reduction elections or modify prior elections for any calendar quarter during the 30 days before that quarter.

You may use the Model Salary Reduction Agreement on page 3 to enable eligible employees to make or modify salary reduction elections.

Employees must be permitted to terminate their salary reduction elections at any time. They may resume salary reduction contributions for the year if permitted under Article II, item 2b. However, by checking the box in Article II, item 2d, you may prohibit an employee who terminates a salary reduction election outside the normal election cycle from resuming salary reduction contributions during the remainder of the calendar year.

Contributions (Article III) Only contributions described below may be made to this SIMPLE IRA plan. No additional contributions may be made.

Salary Reduction Contributions As indicated in Article III, item 1, salary reduction contributions consist of the amount by which the employee agrees to reduce his or her compensation. You must contribute the salary reduction contributions to the financial institution selected by each eligible employee.

Matching Contributions In general, you must contribute a matching contribution to each eligible employee’s SIMPLE IRA equal to the employee’s salary reduction contributions. This matching contribution cannot exceed 3% of the employee’s compensation. See Definition of Compensation, below.

You may reduce this 3% limit to a lower percentage, but not lower than 1%. You cannot lower the 3% limit for more than 2 calendar years out of the 5-year period ending with the calendar year the reduction is effective.

Note. If any year in the 5-year period described above is a year before you first established any SIMPLE IRA plan, you will be treated as making a 3% matching contribution for that year for purposes of determining when you may reduce the employer matching contribution.

To elect this option, you must notify the employees of the reduced limit within a reasonable period of time before the applicable 60-day election periods for the year. See Timing of Salary Reduction Elections above.

Nonelective Contributions Instead of making a matching contribution, you may, for any year, make a nonelective contribution equal to 2% of compensation for each eligible employee who has at least $5,000 in compensation for the year. Nonelective contributions may not be based on more than $250,000* of compensation.

To elect to make nonelective contributions, you must notify employees within a reasonable period of time before the applicable 60-day election periods for such year. See Timing of Salary Reduction Elections above.

Note. Insert “$5,000” in Article III, item 2b(i) to impose the $5,000 compensation requirement. You may expand the group of employees who are eligible for nonelective contributions by inserting a compensation amount lower than $5,000.

Effective Date (Article VII) Insert in Article VII the date you want the provisions of the SIMPLE IRA plan to become effective. You must insert January 1 of the applicable year unless this is the first year for which you are adopting any SIMPLE IRA plan. If this is the first year for which you are adopting a SIMPLE IRA plan, you may insert any date between January 1 and October 1, inclusive of the applicable year.

Additional Information Timing of Salary Reduction Contributions The employer must make the salary reduction contributions to the financial institution selected by each eligible employee for his or her SIMPLE IRA no later than the 30th day of the month following the month in which the amounts would otherwise have been payable to the employee in cash.

The Department of Labor has indicated that most SIMPLE IRA plans are also subject to Title I of the Employee Retirement Income Security Act of 1974 (ERISA). Under Department of Labor regulations at 29 CFR 2510.3-102, salary reduction contributions must be made to each participant’s SIMPLE IRA as of the earliest date on which those contributions can reasonably be segregated from the employer’s general assets, but in no event later than the 30-day deadline described previously.

Definition of Compensation “Compensation” means the amount described in section 6051(a)(3) (wages, tips, and other compensation from the employer subject to federal income tax withholding under section 3401(a)), and amounts paid for domestic service in a private home, local college club, or local chapter of a college fraternity or sorority. Usually, this is the amount shown in box 1 of Form W-2, Wage and Tax Statement. For further information, see Pub. 15, (Circular E), Employer’s Tax Guide. Compensation also includes the salary reduction contributions made under this plan, and, if applicable, compensation deferred under a section 457 plan. In determining an employee’s compensation for prior years, the employee’s elective deferrals under a section 401(k) plan, a SARSEP, or a section 403(b) annuity contract are also included in the employee’s compensation.

For self-employed individuals, compensation means the net earnings from self-employment determined under section 1402(a), without regard to section 1402(c)(6), prior to subtracting any contributions made pursuant to this SIMPLE IRA plan on behalf of the individual.

Employee Notification You must notify each eligible employee prior to the employee’s 60-day election period described above that he or she can make or change salary reduction elections and select the financial institution that will serve as the trustee, custodian, or

*This is the amount for 2012. For later years, the limit may be increased for cost-of-living adjustments. The IRS announces the increase, if any, in a news release, in the Internal Revenue Bulletin, and on the IRS’s website at IRS.gov.

Form 5304-SIMPLE (Rev. 3-2012) Page 6

issuer of the employee’s SIMPLE IRA. In this notification, you must indicate whether you will provide:

1. A matching contribution equal to your employees’ salary reduction contributions up to a limit of 3% of their compensation;

2. A matching contribution equal to your employees’ salary reduction contributions subject to a percentage limit that is between 1 and 3% of their compensation; or

3. A nonelective contribution equal to 2% of your employees’ compensation.

You can use the Model Notification to Eligible Employees earlier to satisfy these employee notification requirements for this SIMPLE IRA plan. A Summary Description must also be provided to eligible employees at this time. This summary description requirement may be satisfied by providing a completed copy of pages 1 and 2 of Form 5304-SIMPLE (including the information described in Article VI—Procedures for Withdrawals).

If you fail to provide the employee notification (including the summary description) described above, you will be liable for a penalty of $50 per day until the notification is provided. If you can show that the failure was due to reasonable cause, the penalty will not be imposed.

If the financial institution’s name, address, or withdrawal procedures are not available at the time the employee must be given the summary description, you must provide the summary description without this information. In that case, you will have reasonable cause for not including this information in the summary description, but only if you ensure that it is provided to the employee as soon as administratively feasible.

Reporting Requirements You are not required to file any annual information returns for your SIMPLE IRA plan, such as Form 5500, Annual Return/Report of Employee Benefit Plan, or Form 5500-EZ, Annual Return of One-Participant (Owners and Their Spouses) Retirement Plan. However, you must report to the IRS which eligible employees are active participants in the SIMPLE IRA plan and the amount of your employees’ salary reduction contributions to the SIMPLE IRA plan on Form W-2. These contributions are subject to social security, Medicare, railroad retirement, and federal unemployment tax.

Deducting Contributions Contributions to this SIMPLE IRA plan are deductible in your tax year containing the end of the calendar year for which the contributions are made.

Contributions will be treated as made for a particular tax year if they are made for that year and are made by the due date (including extensions) of your income tax return for that year.

Summary Description Each year the SIMPLE IRA plan is in effect, the financial institution for the SIMPLE IRA of each eligible employee must provide the employer the information described in section 408(l)(2)(B). This requirement may be satisfied by providing the employer a current copy of Form 5304-SIMPLE (including instructions) together with the financial institution’s procedures for withdrawals from SIMPLE IRAs established at that financial institution, including the financial institution’s name and address. The summary description must be received by the employer in sufficient time to comply with the Employee Notification requirements earlier.

There is a penalty of $50 per day imposed on the financial institution for each failure to provide the summary description described above. However, if the failure was due to reasonable cause, the penalty will not be imposed.

Paperwork Reduction Act Notice. You are not required to provide the information requested on a form that is subject to the Paperwork Reduction Act unless the form displays a valid OMB control number. Books or records relating to a form or its instructions must be retained as long as their contents may become material in the administration of any Internal Revenue law. Generally, tax returns and return information are confidential, as required by section 6103.

The time needed to complete this form will vary depending on individual circumstances. The estimated average time is: Recordkeeping . . . . 3 hr., 38 min.Learning about the law or the form . . . . 2 hr., 26 min.Preparing the form . . . . 47 min.

If you have comments concerning the accuracy of these time estimates or suggestions for making this form simpler, we would be happy to hear from you. You can write to the Internal Revenue Service, Tax Products Coordinating Committee, SE:W:CAR:MP:T:M:S, 1111 Constitution Ave. NW, IR-6526, Washington, DC 20224. Do not send this form to this address. Instead, keep it with your records.

RB0000.049.0812 September 10, 2012

This page intentionally left blank.

An OppenheimerFunds SIMPLE IRA can help you and your employees save for retirement by offering:

• Powerful advantages for small businesses• Generous, no-hassle features• Comprehensive investment options

and support

This brochure provides all the information and forms you need to set up an OppenheimerFunds SIMPLE IRA program for your business. Talk to your financial advisor today about how this program can fit into your personal financial plan.

Shares of Oppenheimer funds are not deposits or obligations of any bank, are not guaranteed by any bank, are not insured by the FDIC or any other agency, and involve investment risks, including the possible loss of the principal amount invested.

This material is provided for general and educational purposes only, is not intended to provide legal or tax advice, and is not for use to avoid penalties that may be imposed under U.S. federal tax laws. OppenheimerFunds is not undertaking to provide impartial investment advice or to provide advice in a fiduciary capacity. Contact your attorney or other advisor regarding your specific legal, investment or tax situation.

Talk to your financial advisor and consider whether or not an OppenheimerFunds IRA makes sense for you.

Before investing in any of the Oppenheimer funds, investors should carefully consider a fund’s investment objectives, risks, charges and expenses. Fund prospectuses and summary prospectuses contain this and other information about the funds, and may be obtained by asking your financial advisor, visiting oppenheimerfunds.com or calling 1 800 CALL OPP (225 5677). Read prospectuses and summary prospectuses carefully before investing.Oppenheimer funds are distributed by OppenheimerFunds Distributor, Inc. 225 Liberty Street, New York, NY 10281-1008© 2017 OppenheimerFunds Distributor, Inc. All rights reserved.

RB0000.046.1117 December 13, 2017

Visit Us oppenheimerfunds.com Call Us 800 835 7305 Follow Us

![NOTE PROCEDURES - Self-Directed IRA...PURCHASE NOTES WITH YOUR IRA! ... Roth IRA [ ] SEP IRA [ ] SIMPLE IRA [ ] Individual 401(k) [ ] HSA [ ] ESA Note: All investment paperwork must](https://img.dokumen.tips/doc/110x75/5f22e13b32debe6653035cf6/note-procedures-self-directed-ira-purchase-notes-with-your-ira-roth-ira.jpg)