Embed Size (px)

Citation preview

Results Third Quarter 2008

CONFERENCE CALL, NOVEMBER 12, 2008, 16:00 CET

Harrie NoyChief Executive Officer

Imagine the result

Higher revenues

Profitability stable

Gross revenues Q3 +5%

Good organic growth despite slowing growth U.S. and U.K. markets

EBITA up 8%, high margin maintained

Net income from operations stable despite currencies and higher financing charges

Outlook FY2008: +10%

Focus on cost control and sales, anticipating changing conditions

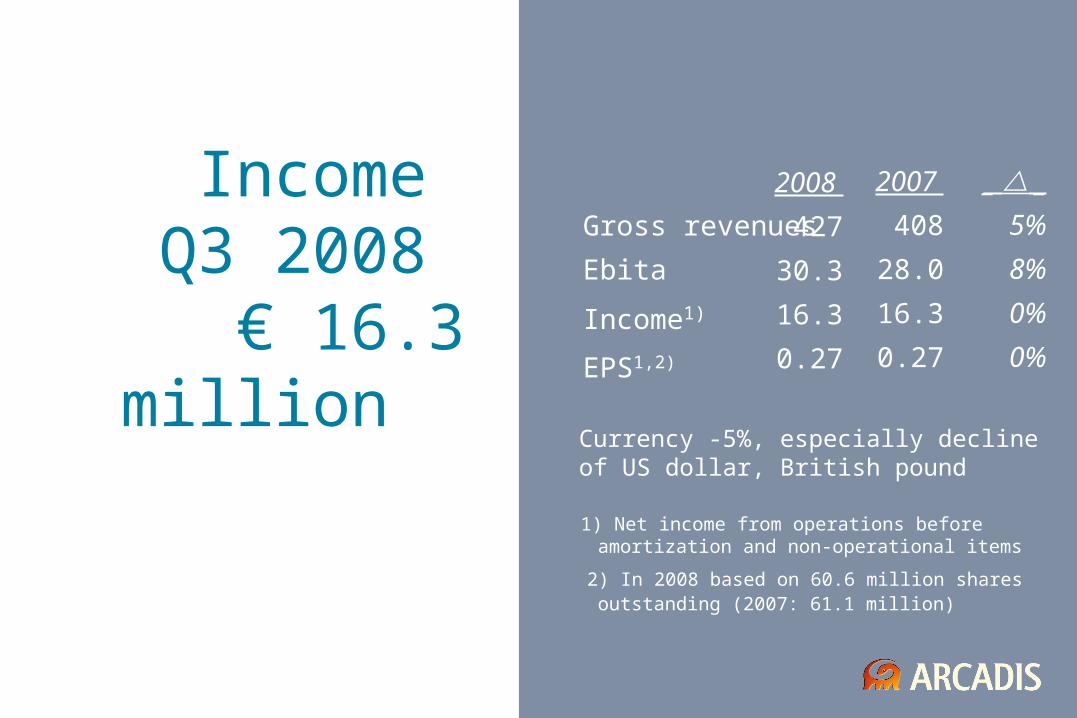

Gross revenues

Ebita

Income1)

EPS1,2)

2008

427

30.3

16.3

0.27

_ _

5%

8%

0%

0%

Income Q3 2008

€ 16.3 million

2007

408

28.0

16.3

0.27

1) Net income from operations before amortization and non-operational items

2) In 2008 based on 60.6 million shares outstanding (2007: 61.1 million)

Currency -5%, especially decline of US dollar, British pound

Gross revenues

Ebita

Income1)

EPS1,2)

2008

1,255

87.2

47.8

0.79

_ _

15%

17%

11%

12%

Income 9 months 2008 € 47.8 million

2007

1,088

74.4

43.1

0.71

1) Net income from operations before amortization and non-operational items

2) In 2008 based op 60.5 million shares outstanding (2007: 61.2 million)

Currency -6%, especially decline of US dollar, British pound

0%

2%

4%

6%

8%

10%

12%

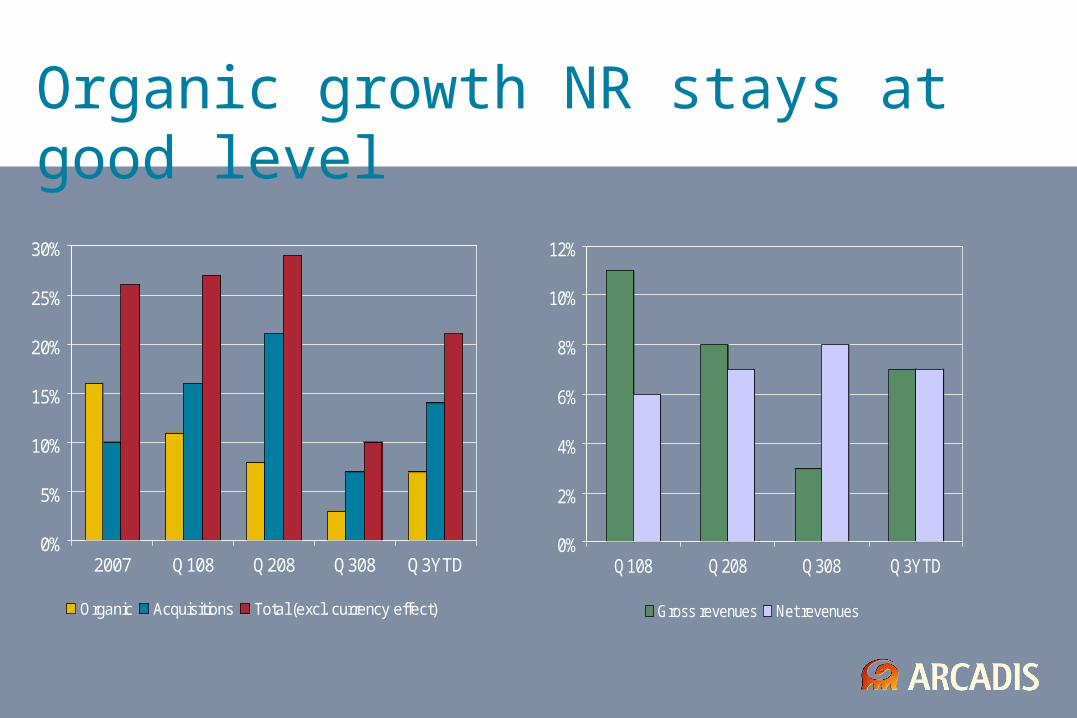

Q108 Q208 Q308 Q3YTD

Gross revenues Net revenues

Organic growth NR stays at good level

0%

5%

10%

15%

20%

25%

30%

2007 Q108 Q208 Q308 Q3YTD

Organic Acquisitions Total (excl. currency effect)

Main facts Till now impact credit crisis limited

UK property market remains difficult

Slowing growth in U.S. environmental market, partly due to completion large projects

Nevertheless organic growth NR 8%

Margin maintained at 10.7% (Q32007: 10.8% )

Dutch infra solid; Poland, Czech strong

Brazil and Chile continue strong growth

SET (Italy) acquired, Copijn divested

Figures relate to third quarter

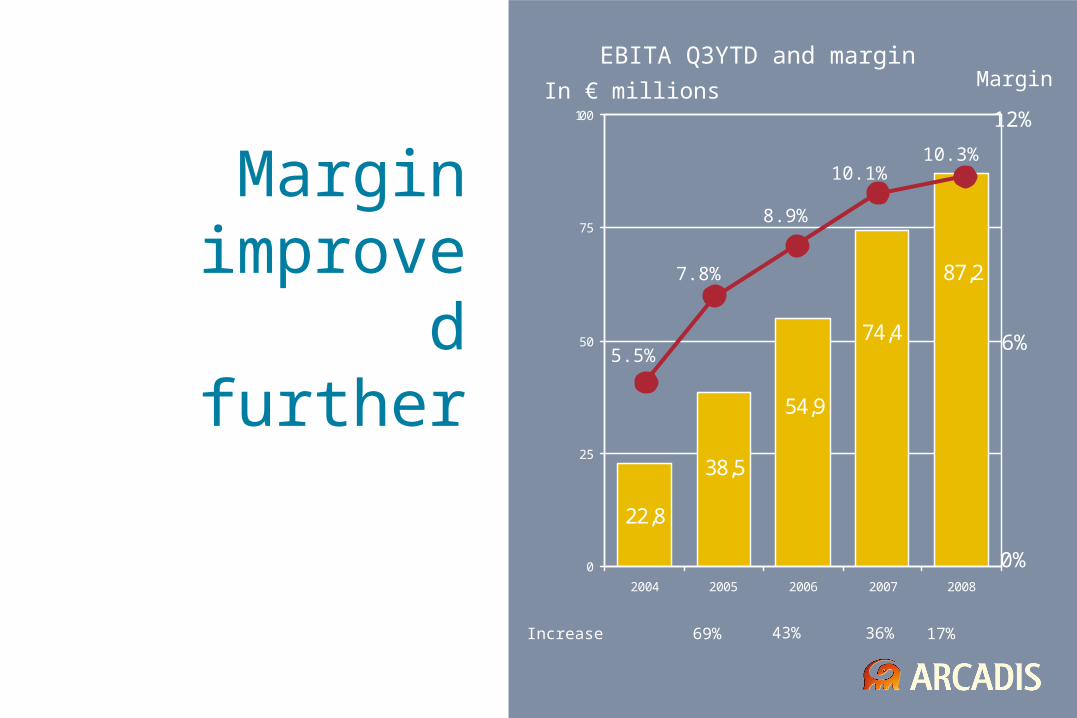

87,2

74,4

54,9

38,5

22,8

0

25

50

75

100

2004 2005 2006 2007 2008

Margin improved

further

In € millions

69%Increase

7.8%

Margin

12%

6%

0%

8.9%

43%

10.1%

36%

10.3%

17%

EBITA Q3YTD and margin

5.5%

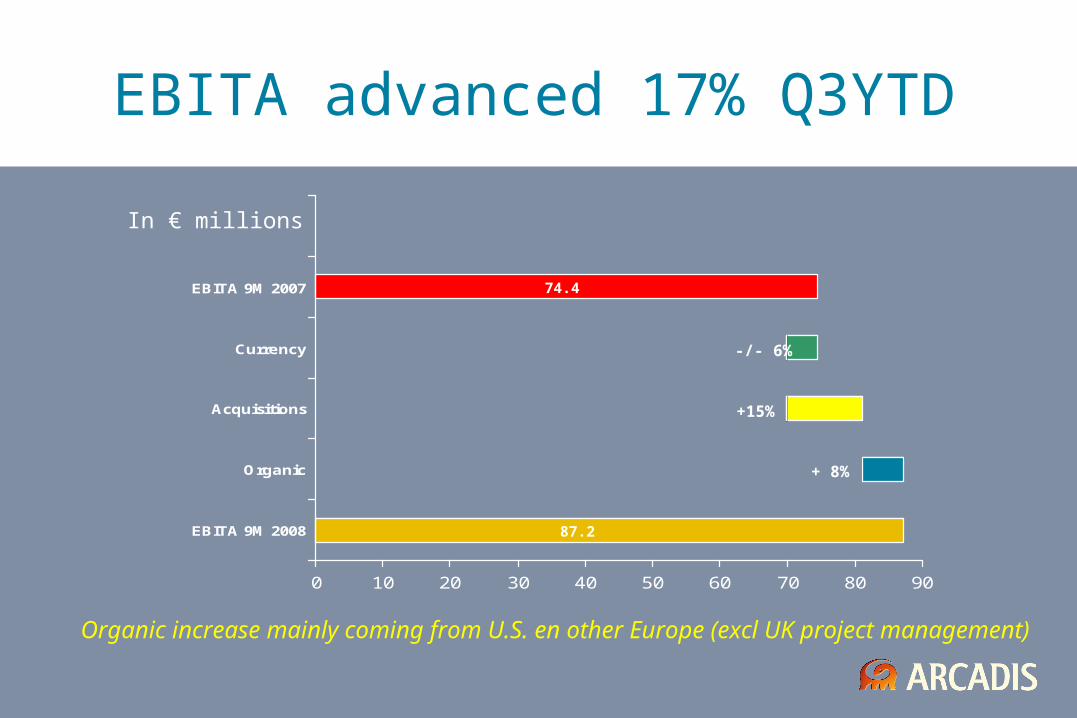

EBITA advanced 17% Q3YTD

0 10 20 30 40 50 60 70 80 90

EBITA 9M 2008

Organic

Acquisitions

Currency

EBITA 9M 2007

In € millions

+ 8%

-/- 6%

74.4

87.2

Organic increase mainly coming from U.S. en other Europe (excl UK project management)

+15%

Some financial

details Q3

Carbon credits contribute € 1.0 million to EBITA (2007: € 0.6 million)

Carbon credits from two landfills in Brazil; approx. 750K ton per year price 10-20 EUR; 1/3 for Logos

Again large impact derivatives on financing charges

Excl this impact financing charges increase to € 5.4 million (2007: € 2.6 million) as a result of acquisitions, higher interest rates and impact from Brazilian loans

ARCADIS

financially healthy

Balance sheet healthy: Net debt/Ebitda end 08 approx. 1.3

USD 350 million long term financing; repayment March 2011 – Jan 2015

End Q3 working capital up to 16.3% (Q307: 13.7%) due to reorganization billing in US and Poland

Cash flow expected to recover in Q4

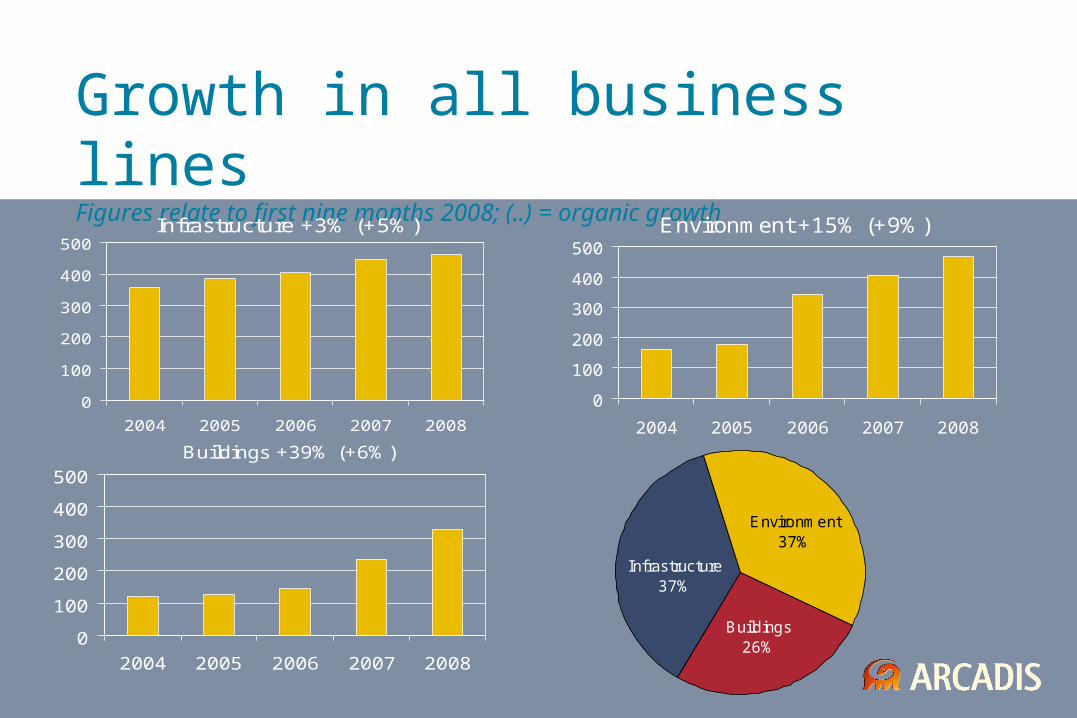

The business linesInfrastructureEnvironment Buildings

Growth in all business linesFigures relate to first nine months 2008; (..) = organic growth

Buildings +39% (+6%)

0

100

200

300

400

500

2004 2005 2006 2007 2008

Infrastructure +3% (+5%)

0

100

200

300

400

500

2004 2005 2006 2007 2008

Environment +15% (+9%)

0

100

200

300

400

500

2004 2005 2006 2007 2008

Buildings26%

Environment37%

Infrastructure37%

INFRASTRUCTURE9 MONTHS 2008: +3% organic:+5%; acquisitions:0%; currency:-2%

Organic growth negatively impacted by earlier decline land development in U.S.

Excluding this effect organic growth 7%

Netherlands, Poland, Czech strong

Brazil and Chile driven by mining and energy

In Q3 accelerated growth in U.S. water market; this year $60 million orders from New Orleans

Project management contributed in U.K.

ENVIRONMENT9 MONTHS 2008: +15%organic:+9%; acquisitions:+16%; currency:-10%

Contribution acquisitions from LFR & Vectra

In Q3 slowing growth in the U.S. due to industrial clients economic woes

Combined with completion of projects with large subcontracting: light organic decline

Net revenue saw organic increase

Already $55 million in new GRiP® work YTD

In most of Europe and Brazil solid growth

BUILDINGS9 MONTHS 2008: +39%organic:+6%; acquisitions:+38%; currency:-5%

Acquisitions: RTKL and APS mid 2007

Continued strong growth in most European countries in management services

RTKL: solid growth from non-commercial and international work

U.K. lower due to decline in commercial real estate market, partly offset by infra & ME

Five year facility management contract with Van Lanschot – the first bank contract

Outlook

Outlook per business line

Infrastructure – relatively stable• Government investments in Europe & U.S. to boost economy• Long term investment programs, e.g. Central Europe • Climate change fuels water management: e.g. Dutch Delta plan• New Orleans solid basis for growth in US water market

Environment – a healthy foundation by sustainability and regulations• Focus on sectors with continued high demand: oil & gas, utilities• Cost effective solutions, vendor reduction and outsourcing: > market share• Interest in GRiP® increases, both in US and Europe• In US, environment & climate change on political agenda

Buildings – refocusing sales efforts• Delays and postponements in commercial projects in UK and US• RTKL focuses on US non-commercial and on international• Project management for infra and Middle East• Demand for FM is expected to grow

Outlook 2008

Economic conditions deteriorate

Sustainability, climate change, urban renewal, mobility and energy offer ample opportunity

Well positioned with a strong backlog and intensified sales efforts

Cost control and focus on higher added value to maintain margin

Looking for acquisitions with more prudence

Expected increase net income from operations 2008: 10%

(Barring unforeseen circumstances)

ARCADIS Building Global Leadership

Thank you