Embed Size (px)

Citation preview

Report No. 14375-TUN

Republic of TunisiaTowards the 21 st CenturyCountry Economic Memorandum(In Two Volumes) Volume II Annexes

October 1995

Country Operations DivisionCountry Department IMiddle East and North Africa Department

h-'I', '', ''<,i' WCk '' 7.'.~~~~~~~~~~-'~

;. ~ ~~~ .. F _ 1i 9et ' '-- X, - _ , - '

~W V

7,~ ~ ~ ~ ~~~- %~ '

-- ;- .-~~~* _-

"N x 7~f

* -.- , -,-~~~~~~~~~~~~~~~~~~~~~.

"e7

4~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Pub

lic D

iscl

osur

e A

utho

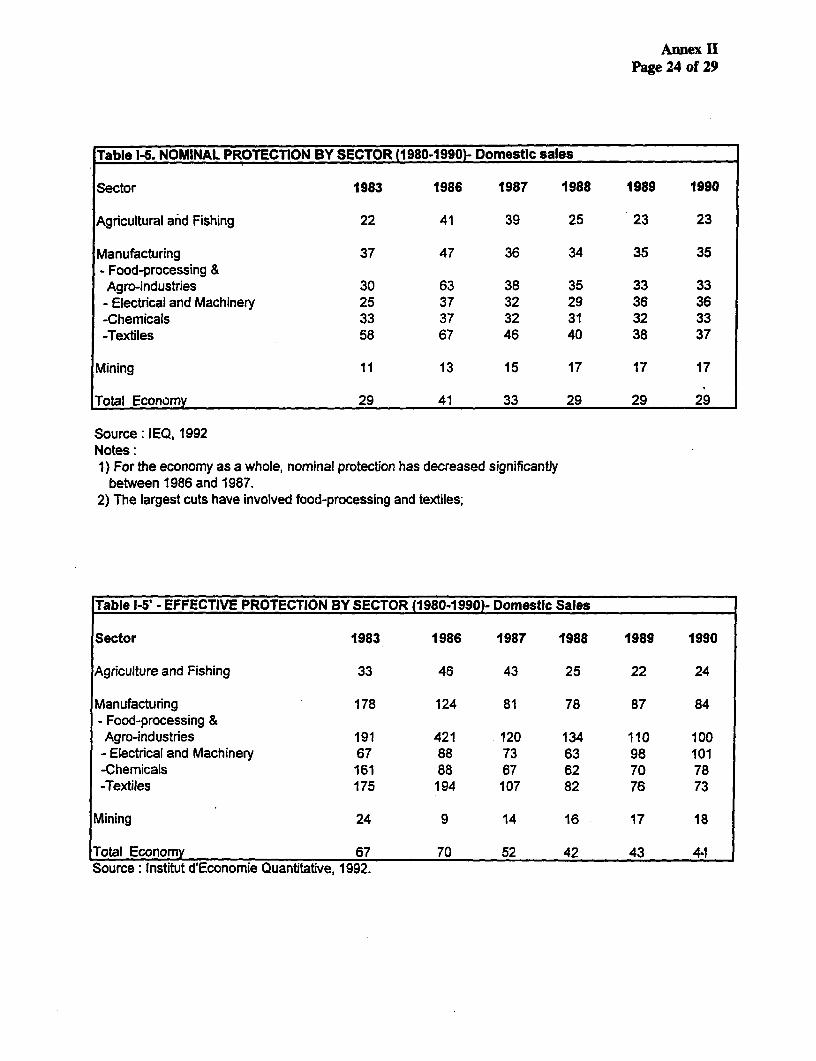

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Currency and Exchange Rates

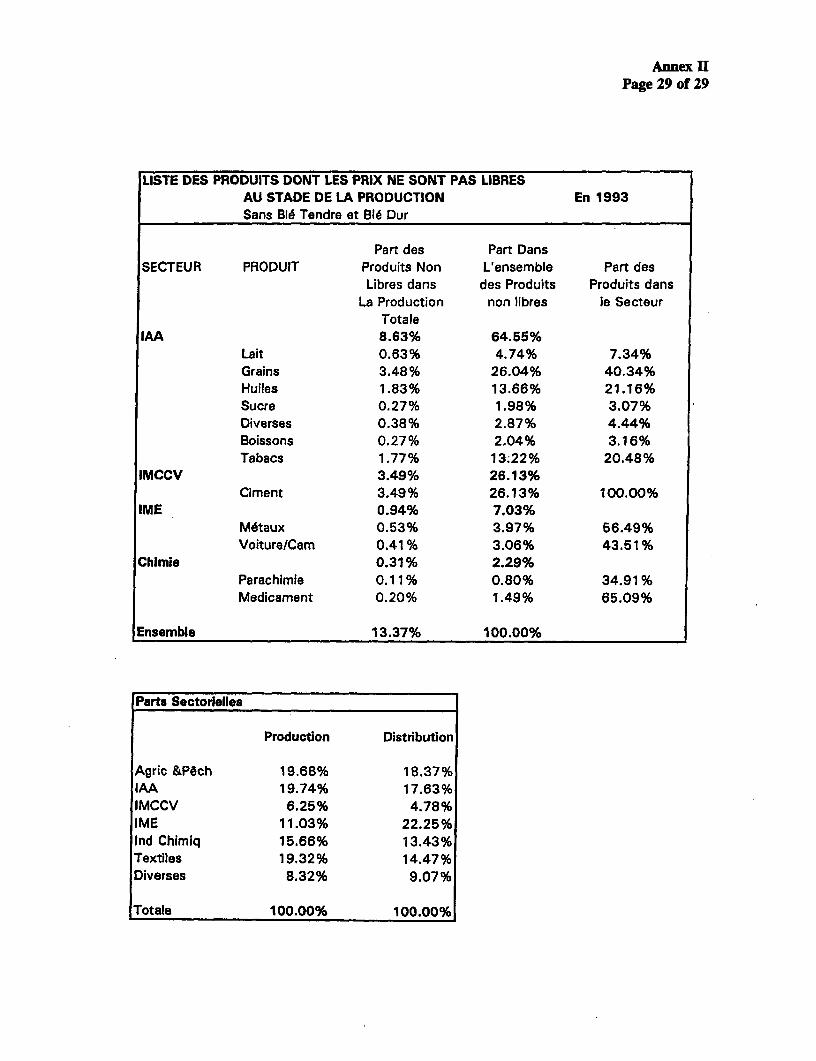

Currency Unit: Tunisian Dinar (TD)

TD per US$

Period Averages

1980=0.40501981 =0.49381982=0.59071983 =0.67881984=0.77681985 =0.83451986 =0.79401987 =0.82871988 =0.85781989=0.94931990=0.87831991 =0.92461992 =0.88441993 = 1.0037

1994=1.0126 (est.)

Fiscal Year

January 1st - December 31st

Weights and Measures

Metric System

ABBREVIATIONS AND ACRONYMS

ANPE Agence Nationale de Protection de l'Environnement (Environment National Agency)BCT/CBT Banque Centrale de Tunisie (Central Bank of Tunisia)BNA Banque Nationale Agricole (Agricultural National Bank)CDs Certificates of Deposits (Certificats de Dep6t)CNSS Caisse Nationale de Securite Sociale (National Social Security Fund)CPI Consumer Price Index (Index des Prix a la Consommation)CTN Compagnie Tunisienne de Navigation (Tunisian shipping company)EPA Etablissement Public Administratif (administrative entity)EPIC Etablissement Public Industriel et Commercial (quasi-commercial entity)EU European Union (Union Europeenne)FDI Foreign Direct Investment (Investissement Direct Etranger)FODEP Fonds de Depollution (Anti-Pollution Fund)FTA Free Trade Agreement (Accord de Libre Echange)FTZ Free Trade Zone (Zone de Libre Echange)GATT General Agreement on Tariffs and Trade (Accord General sur les Tarifs Douaniers et le

Commerce)GDI Gross Domestic Investment (Investissement Interieur Brut)GOT Government of Tunisia (Gouvernement de Tunisie)IDF Institutional Development Fund (Fonds de Developpement Institutionnel)INNORPI Institut National pour la Normalisation des Produits Industriels (National Institute for

Industrial Products Normalization)INS Institut National de Statistiques (National Institute of Statistics)MEAT Ministere de l'Environnement et de l'Amenagement du Territoire

(Ministry of Environment and Regional Planning)MMR Money Market Rate (Taux du Marche Monetaire)MOA Ministry of Agriculture (Ministere de l'Agriculture)MOH Ministry of Health (Ministere de la Sante)NIE Newly Industrializing Economies (Economies Nouvellement Industrialisees)OC Office des Cereales (National Agency for Cereal Marketing)OECD Organization for Economic and Cooperation Development

(Organisation de Cooperation et de Developpement Economiques - OCDE)ONAS Societe Nationale d'Assainissement (National Sewerage Company)ONH Office National de l'Huile (National Agency for Edible Oil)O&M Operation and Maintenance (Exploitation et Entretien)QRs Quantitative Restrictions (restrictions quantitatives)SICAF Societe d'Investissement a Capital Fixe (closed-end mutual fund)SICAV Societe d'Investissement a Capital Variable (open-end mutual fund)SME Small-Medium Sized Enterprises (Petites et Moyennes Entreprises)SONEDE Societe Nationale d'Exploitation et de Distribution des Eaux

(National Water Supply Utility Company)STAM Societe Tunisienne d'Affretement Maritime (Tunisian cargo-handling company)STIL Societe Tunisienne d'Industrialisation Laitiere (National Company for Milk Marketing)VAT Value-Added Tax (taxe a la valeur ajoutee)WTO World Trade Organization (Organisation Mondiale du Commerce)

List of Definitions

Accord de place Informal agreement between commercial banks not to compete for depositsbased on interest rates.

Appel d 'oifres A weekly auction by the Central Bank of a fixed amount of seven-day fundsprovided to commercial banks. The appel d 'oifres operations are based onprecisely defined collateral (loans to priority sectors, e.g. agriculture,micro-enterprises.

Bon d'equipement Treasury bonds mandatorily placed by the Government.Bon du Tresor Treasury Bills at market-related interest rates.Bon du Tresor negociable Treasury Bills negotiable (NTB) on the bourse and set at maturities of five

years or more.Contrat de liquidite ou Obligation for commercial banks to repurchase the securities sold toAccord de liquidite customers virtually on demand regardless of maturity.

Enprunts nationaux "National loans", borrowing of the Government through bond issues.Prise en pension A seven-day repurchase facility at a higher interest rate than the appel

d'offres, designed to provide banks with additional liquidity.

The report is a product of a team consisting of Linda Likar (Task Manager), Norman Loayza (Macroeconomic Policyand Policies for Higher Growth), Aziz Bouzaher and Sarah Forster (Environmental Issues), Mohamed Lahouel(Competition Policies) and Guillermo Hakim (Labor Policies), Laura Burakreis and Richard Brun (Banking and FinancialSector Reforms), Faycal Lakhoua (Role of the State in the Economy) and Juan Lopez (Comparator Country Analysis andMacroeconomic support). The main report was prepared by Linda Likar and Norman Loayza. Several working papers(listed in the bibliography) were prepared by staff from the sector divisions and by Tunisian consultants. Valuable inputsand comments were received by Laurie Effron and David Tarr. Fataneh Semsarzadeh provided research assistance.

The cooperation of the Government of Tunisia, particularly the Ministry of Plan and the Institut d 'Economie Quantitative,is gratefully acknowledged. Local consultants, Professors Mohamed Lahouel and Faygal Lakhoua of the University ofTunis and the SIDES consulting firm, made significant contributions to the report.

REPUBLIC OF TUNISIATOWARDS THE 21ST CENTURY

COUNTRY ECONOMIC MEMORANDUM

VOLUME 11 - ANNEXES

Contents

ANNEX I - ECONOMIC GROWTH AND ENVIRONMENTAL SUSTAINABILITYIN TUNISIA: LINKAGES AND IMPLICATIONS

I - Overview

II - The Government's Environmental Strategy & Institutional Framework

A. Environmental Priorities and StrategyB. Government ProgramsC. Institutional Framework

III - Sectoral Environmental Issues and Economic Linkages

A. AgricultureB. Industry and EnergyC. Tourism

IV - The Social Cost of Environmental Pollutionand Natural Resource Degradation

A. Public Health and the EnvironmentB. The Costs of Natural Resource Degradation

V - Conclusions: Macroeconomic Linkages and Sustainable Development

ANNEX II - COMPETITION POLICIES

I - Trade Liberalization

Quantitative RestrictionsTariff Barriers

II - Competition Policies and Differentiated Support Measures

The Old Investment Incentive SystemThe New Incentive SystemSpecific Incentives and Distortions

Contents (cont'd)

The Removal of Capacity LicensingIndustrial Support MeasuresAbsorption of Technology and Support ServicesPublic Procurement PoliciesTransparency of RulesTendering ProceduresDifferentiated Treatment of Firms

III - Pricing and Deregulation Policies

Price and Distribution ControlsMajor Shifts in 1991Procedure and Pace of Price LiberalizationPrice Control at the Producer StagePrice Control at the Distribution StageDeregulation: The Transport Sector

ANNEX III - FINANCIAL SECTOR IN TUNISIA

CHAPTER I - THE BANKING SYSTEM

A - OverviewB - Banking RegulationsC - Sources of Funding and Composition of AssetsD - Intermediation and Efficiency of the Banking SystemE - Concluding Recommendations

CHAPTER 11 - FINANCING OF THE TREASURY, MONETARY POLICYAND FINANCIAL MARKETS

A - The Financing of the Treasury and the Managementof the Monetary Policy

I - The Financing of the Treasury (Primary Market)and the Management of Domestic Public Debt (Secondary Market)

11 - The Management of the Monetary Policy

B - The Modernization of the Stock and Bond MarketsI - The Legal Environment and the Market OrganizationII - Evolution of Market Activity and Present Issues

C - Recommendations

ANNEX 1

ECONOMIC GROWTH AND ENVIRONMENTAL SUSTAINABILITY INTUNISIA: LINKAGES AND IMPLICATIONS

I. OVERVIEW

1. For the last ten years, Tunisia has experienced relatively steady economic growth based on adevelopment strategy focussed on three principal sectors: irrigated agriculture, manufacturing industry andtourism (Table 1). GDP growth has averaged around 5 percent for the last five years. Growth has notbeen steady, however, but rather reflects the economy's dependancy on the agricultural sector, the output ofwhich varies dramatically depending on rainfall.

Table 1. Sectoral Share of GDP and Growth Rates (in percentages)

1987 1988 1989 1990 1991 1992 1993 1994

GDP growth rate 6.7 0.1 3.7 7.6 3.8 8.0 2.6 6.1

Agriculture GDP share 15.3 11.7 12.1 14.4 15.7 15.5 14.1 14.1

Growth rate 20.5 -25.8 5.7 27.7 14.3 6.6 -7.0 5.1

Industry GDP share 27.8 28.1 29.0 28.2 28.0 27.1 26.5 26.4

Growth rate 0.4 2.3 5.4 6.2 5.1 5.6 1.8 7.2

(Manufacturing) GDP share 13.1 13.9 14.4 15.0 15.1 15.0 15.0 15.3

Growth rate 4.4 6.5 6.0 11.3 4.0 8.1 3.0 7.4

Services GDP share 32.5 35.8 35.3 34.0 32.0 33.1 34.4 34.6

Growth rate 8.6 9.0 2.2 3.3 -1.3 11.9 5.9 6.1

(Tourism) GDP share 3.8 4.3 4.2 3.9 2.9 3.8 4.0 4.0

Growth rate 37.2 11.6 -2.8 -0.8 -25.0 44.8 7.0 6.5

Source: World Bank data

2. In recent years increasing concerns have emerged about the environmental costs of thisdevelopment strategy. Pursuit of development objectives in these priority sectors, combined with a growingshift of the population to the coastal areas (where over 77 percent of the population are concentrated in lessthan 25 percent of the total land area), has placed increasing pressures on the natural resource base,particularly coastal land and water resources which are relatively limited. This is leading to environmentaldegradation which is manifested in three main ways:

* land degradation -- over 60 percent of the country's usable land resources are estimated to beaffected by degradation. This is leading to the permanent loss of the equivalent of 24,000 hectaresof agricultural land (about 0.5 percent of cultivated land) a year putting even more pressures onrangeland resources, whose productivity continues to decline at an average of 2 percent per year.

Annex 1Page 2

* water scarcity -- almost all Tunisia's available water resources will be fully developed by theyear 2000. Continued growth of agriculture, industry and tourism at current rates is likely to putincreasing pressures on existing water resources, leading to a deterioration of water quality due todomestic, industrial and agricultural pollution, increasing intersectoral competition for scarcesupply and potentially constraints to long-term economic growth.

* coastal degradation -- industrial and oil pollution problems, coastal erosion and overdevelopmentare worsening long the coast as urban, industrial and tourism areas continue to grow rapidly. Inthe next 10 years, Tunisia's population will grow by an estimated 3.15 million, the vast majority ofwhich will live along the coast, if current trends continue, further increasing pressures on marineand coastal resources.

3. The Government is well aware of these problems and has made significant progress in developinginstitutions, policies and programs to deal with them.' To date their approach to environmentalmanagement has been investment-based, with significant resources going to sanitation infrastructure andsoil and water conservation, in particular. Less attention has been paid to developing incentives to reducewaste and encourage conservation, though progress is now being made on key pricing policy reforms toencourage more sustainable use of natural resources -- water pricing, energy pricing and reduction ofagrochemical subsidies. A more integrated approach to land and water use management, however, is yet tobe developed.

4. The purpose of this report is to examine the nature and extent of these environmental problems andtheir economic implications. The report first discusses the evolution and current status of theGovernment's overall environmental strategy and institutional framework for environmental management.Second, it provides an analysis of the environmental issues related to Tunisia's three main sectors:agriculture, industry and tourism. Third, to the extent possible, given the time and data constraints of thisreport, a rough estimate is made of the costs, both social and economic, to the economy of theseenvironmental problems, particularly the cost of natural resource degradation, air pollution and lack of safewater and sanitation. Finally, the report provides initial conclusions and recommendations as to how toreconcile the objectives of economic development and environmental protection.

5. This paper will be followed-up by further analysis of the potential natural resource constraints toeconomic development in Tunisia. A more detailed study is to be carried out in close collaboration with theTunisian Government which will provide a more extensive and systematic economic analysis of the issuesrelated to the competing demands on water and coastal land and their environmental and economicimplications.

'See Annex 2 and 3 for selected economic and environmental indicators for Tunisia and comparable countries.

Annex 1Page 3

II. THE GOVERNMENT'S ENVIRONMENTAL STRATEGY ANDINSTITUTIONAL FRAMEWORK

A. ENVIRONMENTAL PRIORITIES AND STRATEGY

6. Environmental protection has long been a concern of the Government of Tunisia, however, it isonly in the last few years that the understanding of environmental issues, their relation to development andtheir translation into action have been approached in a systematic and effective fashion. In 1990, with thesupport of the World Bank, the Government developed a National Environmental Action Plan whichrepresented the first step in an ongoing process of environmental policy-making. Environmentalmanagement was a central objective of the Eighth Plan for Social and Economic Development (1992-96)which devoted a chapter specifically to environmental protection, the first plan to do so, and set out thefollowing environmental priorities2:

* ensure the rational and sustainable use of the country's natural resources* keep pollution within acceptable limits* clean-up polluted areas* involve citizens in the effort to protect the environment

7. To achieve these objectives the Government has a three-part strategy, implementation of which isunder the overall responsibility of the Ministry of Environment and Regional Planning (MEAT):

a Prevention - this is based on the Government's realization that a strategy of grow now andclean-up later is no longer acceptable and is unnecessarily expensive. It is thereforeplacing emphasis on designing and implementing policies and mechanisms to preventpollution and the wasteful use of natural resources. A key tool is the use of environmental

3impact assessments.

Inspection and monitoring of environmental conditions - monitoring of environmentalconditions is essential to control compliance with pollution control regulations. Thestrategy aims to increase the capacity of research and analytical laboratories, monitoringstations and technical and scientific staff.

* Curative actions - though the main thrust of the Government's strategy is prevention ofpollution and natural resource degradation, in certain areas serious damage has alreadybeen done. According to the Government's strategy, this damage will be rectified.Attention should be paid to the costs and benefits of such clean-up programs, and prioritygiven to cleaning-up areas where environmental degradation is causing a serious risk tohuman health or economic activity and the greatest benefits can be achieved. In the long-term, it is hoped that a preventative approach will reduce the need for costly clean-upprograms.

2Ministry of Environment and Regional Planning (MEAT), 1994. Environment and Sustainable Development: AReview of the Tunisian Strategy, report of Tunisia to the Tunis Conference on Sustainable Development in theMediterranean.

3Environmental assessments have formed the centerpiece of environmental policy in many countries, particularlythe U.S.

Annex IPage 4

B. GOVERNMENT PROGRAMS

8. To implement the strategy, MEAT has launched seven programs:

(i) Urban and rural sanitation. The objective of this program is to extend the sewage network anddisposal system in order to increase the percentage of households connected to the collection system,to increase the treatmnent capacity by putting new treatment plants into operation, and to increase thereuse of treated effluents, especially in the agricultural sector.

(ii) Protection of the coastal zone (program "Main Bleue"). This program consists of activities toensure that the beaches along Tunisia's coastline are fit for swimming; to protect the marineenvironment from oil spills and pollution; to reduce the impacts of urbanization along the coast --both in terms of aesthetics as well as liquid and solid wastes; and to implement the necessary landuse planning measures to achieve these objectives.

(iii) Solid waste management, the "PRONAGDES" program, aims to improve the worseningsituation of the collection, treatment and ultimate use of household waste, industrial waste andspecial waste (from hospitals, slaughterhouses etc.). In the short-term, the program is gearedtowards improving waste disposal; in the longer term, the goal is to reduce the overall volume ofwaste generated and maximize recycling of solid waste.

(iv) Industrial pollution control. This program has two components: prevention and pollutionreduction. Prevention is put into effect primarily through (a) environmental impact assessments,which are now mandatory for all new projects; (b) creation of a depollution fund (FODEP) tofinance pollution control (para. 11); (c) encouraging non-polluting industrial processes; and (d) thecreation of industrial zones which allow easier pre-treatment of industrial effluent. Polluhonreduction involves identifying sectors and regions with particularly severe pollution problems anddesigning and implementing action plans to reduce or eliminate the pollution based on considerationof pollution reduction options.

(v) Desertification control (program "Main Jaune") consists of a broad range of activitiesimplemented by different ministries and coordinated by MEAT, including family planning in ruralzones, integrated rural development, forestry, soil and water conservation programs and researchactivities carried out by the Institute for Arid Regions.

(vi) Natural resource management and biodiversity conservation ("Main Verte"). The objectives ofthis program are to conserve biological resources, rare and endangered species and their ecosystems;to sensitize the public to the need for nature conservation; and to promote ecological tourism.

(vii) Environmental awareness and education. This program involves environmental education and anawareness-building effort aimed primarily at children and young people. The program isimplemented in collaboration with other ministries and NGOs.

9. Financing. The Government budget allocated to environmental protection has increased over thelast ten years, from 260 million dinars in the Seventh Development Plan (1987-1991), roughly 0.3 percentof GDP, to 600 million dinars in the Eighth Plan (1992-1996), around 0.4 percent of GDP. This figurerises to 1,400 million dinars, or about 1 percent of GDP if financing for environmental protection at themunicipal level and for safeguarding natural resources, such as water, forests and soils are added. This iscomparable to the expenditure of industrial nations on environmental management, which is between 0.8and 2 percent of GDP, though the budgetary allocation for environmental programs is still below the

Annex 1Page 5

4investment needs proposed by MEAT which amount to 3 percent of GDP. Much of the budget forenvironmental protection is financed by external aid which is not yet assured for the total investmentprogram. Table 2 presents budget allocations for the above mentioned environmental programs and otherenvironmentally-related investments.

Table 2. Government Budget Allocations for Environmentally-related Investments.

Planned Enviroinmental Investments

Eighth Plan for Economic and SocW Development (1992-1996)

Environmental Investments Dinars % of budget %(millions) disbursed

Environmental Protection Programs 259 25 35

- industrial pollution control 157

- solid waste management 53

- oil pollution prevention 20

-protection of natural and cultural heritage 16

- institutional support 8

-public awareness and research 5

Sanitation 299 28 55

Flood control 40 4 35

Soil and Water Conservation 196 19 94

Forestry 259 25 71

TOTAL 1,053

Source: Ministry of Environment and Regional Planning (MEAT), 1994. Environment and SustainableDevelopment: A Review of the Tunisian Strategy, report of Tunisia to the Tunis Conference on SustainableDevelopment in the Mediterranean.

10. Though budget allocations remain below proposed investment needs, operational problems are amajor constraint to disbursing existing funds. A Bank analysis on the implementation of the TunisianNEAP found that only 17 percent of the proposed projects had been completed on target.5 The quality ofproject design and institutional factors appear to be key determinants of disbursement rates and projectcompletion. Many projects are selected and included in the investment program before pre-feasibilitystudies had been done. Institutional arrangements are another important factor determining the success rateof projects. Overall, for example, there is very little delay of municipal sewerage and wastewater treatmentprojects which are handled by a very competent institution (ONAS), whereas programs to addressmounting solid waste problems have been seriously delayed. These are handled by municipalities whichhave limited institutional capacity.

4Ministry of Environment and Regional Planning, 1993. Rapport National: L 'Etat de I 'Environnement, 1993.

5World Bank, 1994. 1990 National Environmental Action Plan Update Sector Note (draft), prepared by MNlIN.

Annex 1Page 6

11. Depollution Fund (FODEP). The Government is developing new mechanisms to financeenvironmental investments in the form of environmental funds. The most important fund is the depollutionfund (FODEP) established under the 1993 investment law to finance investments in pollution control. Anyindustrial enterprise, public or private, can receive up to 20 percent of the investment cost of depollutionactivities. At least 30 percent of the financing must be covered by the enterprise itself and the remaining 50percent can benefit from bank financing obtained through lines of credit earmarked for environmentalprotection. FODEP is a very new creation and several outstanding issues need further clarification duringimplementation including (i) the treatment of public and private firms; (ii) how the Government will dealwith polluting firms that are financially non-viable, and (iii) the treatment of old versus new firms.

Box 1: Policy Tools for Environmental Management - Lessons from OECD Experience

In most OECD countries a combination of command and control (CAC) and economic incentives are used tomanage environmental problems. The experience with economic incentives, though in theory the most efficientmechanism by which to ensure the costs of environmental degradation are internalized into developmentactivities, is fairly limited and it is too early to draw very concrete lessons.

Pollution fees are the most commonly used economic instrument and are part of environmental managementsystems in many European countries and the U.S. Most of these programs are in the areas of water protection,waste disposal and noise abatement. However, the majority of fees are set too low to function as economic.incentives, due for the most part to resistance by industry and fears of the adimiinistrative complexity of suchsystems. Use of marketable permits has been limited and has been mostly confined to the U.S. All permitprograms exist within a larger CAC framework and their experience has been mixed. A number of countries:have used outright subsidies to induce polluters to make the investments required to bring them intoenvironmental compliance, despite it being contrary to the polluter pays principle. In Gennany, in particular,credit guarantees and subsidies drawn from revolving funds are used to speed the implementation of stricterenvironmental standards, especially among small and medium size firmns, which could experience cash flow,problems because of the sudden capital investments required to comply with mandatory enviromnentalstandards. Tax incentives have proven successful for. encouraging the use of "clean" cars and unleaded fuelsIn the U.K., for example, a 10% differential in fuel prices resulted in a doubling of the use of lead free fuel in 12months.

All incentive systems to date are add-ons to pre-existing CAC regulations. A pure economic incentive system isunlikely to ever exist, so the basic challenge is to determnine the most appropriate mix taking into accounteconomic and political realities. Whatever the instrument selected, the regulator must Xmonitor and enforce the

: environmental management system. If agencies lack necessary. equipment or trained manpower to ensurecompliance, CAC regulations and monitoring of initial compliance may be the best interim approach untilbetter resources are available.

Source: Patterns of Environmental Management, paper prepared for the World Bank, 1994.

12. Many similar funds have been established in OECD countries and Eastern Europe (see Box 1).Some of these are financed utilizing revenues raised from pollution charges, which is more in line with thepolluter pays principle (PPP). Tunisia has yet to introduce a system of pollution taxes. FODEP subsidizesdepollution activities, essentially violating the PPP and arguably providing a disincentive to polluters tointernalize the cost of pollution. In the short term, however, FODEP may prove a useful mechanism duringthe transitional stage of environmental policy implementation to ease the financial pressures on enterprisesassociated with complying with stricter pollution standards. FODEP can also help speed up thereplacement of old plants by cleaner technologies. In the medium to long-term, the role of more efficientpolicy instruments, such as pollution taxes, should be strengthened and the need for subsidies reduced.

Annex 1Page 7

13. Policy Reform. In addition to the above programs, the Governnent is undertaking a number of policyreforms, including water and energy pricing, that will encourage the conservation of natural resources andreduce waste and pollution (summarized in Table 3). Many of these policy reforms were made for economicreasons -- primarily to increase govemment revenue by improving cost recovery of public services -- however,they represent so-called "win-win" policies that will also bring environmental improvements

Table 3. Key Policy Reforms

Policy Objective Progress to date Expected Environmental Impact

Macroeconomic and Sectoral Policies Land Water Air Waterdegradation scarcity pollution Pollution

Water Improve Despite regular price increases, waterpricing water use is still being subsidized particularly for

efficiency agriculture and domestic use by an + ++ ++and cost estimated 83 MD6 Tariffs charged are (oncerecovery based on the volume of water tariffs are

consumed. 1994 tariffs range from D brought in

0.095-0.585 per i 3. The consolidated aIe withrnational average revenue is D co)l

0.326/m3 ($1.46/1,000 gallons). l

Energy Improve After several delays in increasingpricing economic electricity and petroleum prices, in

and energy 1990 the Government started to + ++use efficiency implement tariff adjustments. Prices

are now in line with LRMC.

Agrochemic To encourage Subsidies for fertilizer have beenal subsidies use of substantially reduced over the last ten

fertilizer and years'. The gross amount of subsidy + ++pesticides. peaked in 1989 at 20 MD but had been

reduced to 0.9 MD by 1993. Data onagrochemical subsidies is lacking.

Livestock To assist Animal feed continues to befeed livestock subsidized2, particularly duringsubsidies owners drought years. Subsidies for animal

maintain feed peaked in the drought year of 3herd sizes 1989 at 50 MD (plus a further 20 MD_during subsidy for fertilizer, some of it fordrought years feed production) before falling to 4so stabilizing MD in 1993. Overall levels of subsidyincomes. were higher in the 80s than in the 70s.

Legend: + +: positive, direct impact; - -: negative, direct impact+ positive, indirect impact; - negative, indirect impact.' Subsidies have been eliminated for 3 of the 4 main types of fertilizers used.2 Maize and soybean meal subsidies have been eliminated; subsidies remain mostly for barley.3 Maintaining herd sizes during drought years can put unsustainable pressures on grazing lands.

6This figure represents an implicit subsidy based on the difference between cost and price of water. Table 14presents the issue from a public expenditure point of view.

Annex IPage 8

14. Legal Framework There are over 350 existing legal texts related to environmental issues inTunisia which are often overlapping, provide a sectoral approach to the environment and fall within nooverall guiding framework. The most important laws are the Forestry Code (1988), the Water Code(1975), the Urban Planning Code (1979) and the Labour Code (1966), which currently regulates pollution.A new soils code is awaiting legislative approval. MEAT aims to consolidate all environmentally-relatedtexts within a coherent framework based on an integrated cross-sectoral, cross-media environmental policy.To this end, ANPE has inventoried and classified all existing legal texts concerning the environment.Based on this, the legal framework for environmental protection is being thoroughly revised.

C. INSTITUTIONAL FRAMEWORK

15. After a series of institutional reforms, the Tunisian government now has three well-establishedinstitutions to take the lead on designing and implementing environmental policy:

The National Sanitation Board (ONAS) which was created in 1974 to control water pollutionand protect the country's water resources. ONAS manages the entire sanitation system beingresponsible for the design, construction, operation and maintenance of all sanitation works fromcollection to treatmnent. There are plans under discussion, however, to privatize certain aspects ofONAS' operations. The institution has accomplished a remarkable amount in its twenty years ofexistence. Over 80 percent of Tunisia's urban population is now connected to the sanitationsystem, though rural sanitation is still lacking. Over 100 million m3 of water are treated each year,and the quality of treated water meets international standards. Increased reutilization of treatedwater has also provided savings in the use of fresh water.

The National Environmental Protection Agency (ANPE), created in 1988, has a two-foldmandate: to analyze and monitor the state of the country's environment and to combat all sourcesof damage to and degradation of the natural environment. ANPE carries out a number ofpreventative measures: (i) evaluating and approving environmental impact assessments which arenow compulsory for all new investments; (ii) drawing up environmental standards; (iii) promotingpublic awareness; and (iv) training and environmental education. It also undertakes curativemeasures including (i) inspection of industrial plants and their pollution treatment facilities and (ii)enforcing legislation. ANPE is legally empowered to bring court action against any entity found tobe in contravention of the law and it can conclude agreements with offending enterprises regardingmeasures to remedy pollution problems.

The Ministry of Environment and Regional Planning (MEAT), created in 1991, wasestablished to complete the institutional structures dealing with environment and to lend greaterpolitical weight and importance to environmental policy. The Ministry, in collaboration with otherministries, is responsible for proposing policies regarding protection of the environment,improvement of living conditions and land planning. It is also responsible for legislation related tothe environment. Structures with authority in the environmental domain continue to exist in otherministries, as for example the Department of Environmental Hygiene and Protection in the Ministryof Health, but MEAT is responsible for ensuring overall coordination among them.

In addition, a National Coastal Zone Agency ("Agence Nationale du Littoral") has recently beencreated and will be another agency of MEAT.

16. Institutional Capacity. The Ministry of Environment and Regional Planning (MEAT) has arelatively high degree of political power and resources compared to many other environmental institutions

Annex 1Page 9

elsewhere in the world. However, according to an assessment of environmental management systems indeveloping countries (see Table 4), though Tunisia's institutional framework is now integrated, the fact thatline ministries still keep control over environmental management issues means that the envirommentalmanagement system itself defacto remains fragmented. This constrains the ability of MEAT to have a realimpact on the various sector activities and on facilitating the integration of environmental policy intogeneral development iniatives. Continued efforts will need to be made to strengthen MEAT and theenvironmental units in sectoral ministries, while improving coordination between them.

Table 4: Nature of Environmental Management Systems in Selected Countries

Country Institutional Framework EnvironmentalManagement

Tunisia Integrated Fragmented

Morocco Coordinated Fragmented

Thailand Quasi-integrated Fragmented

Indonesia Integrated Fragmented

Argentina Coordinated Fragmented

Chile Coordinated Fragmented

Mexico Quasi-integrated Integrated

Nigeria Integrated Integrated

Germany Integrated Fragmented

U.S.A. Integrated Integrated

Definitions:Fragmented: enviromnental protection functions are carried out by sectoral and media agencies, based on laws

and regulations primarily addressing the sectoral or media issues.Coordinated: environmental protection functions are still assigned to several sector ministries and agencies,

however, environmental policy formulation is coordinated through an inter-ministerial body.Quasi-integrated: one of the line ministries is assigned responsibility for environmental protection issues.

Potential conflicts of interest with the ministry's main function, however, are not eliminated.Integrated: a separate environmental protection agency or ministry is established and administrative

functions and resources for environmental management are transferred to this agency.

Source: Lovei M., 1994. Institutional Issues of Environmental Management and the Bank's Approach inDevelopment Countries, ENVPE, World Bank.

17. Monitoring. Though Tunisia now has a well-organized institutional framework in place,monitoring and enforcement capacity still need considerable strengthening. Current staff numbers areinadequate to properly evaluate all environmental impact assessments and monitor pollution trends. Todate, attention has been focused on financing and irnplementing environmental programs, such as soilconservation and pollution control programs, without paying adequate attention to the importance ofmonitoring natural resource degradation and pollution trends. As a result, information on ambientenvironmental conditions and trends is lacking. Several steps are being taken to address this, including thesetting-up of an environmental monitoring observatory and the decentralization of MEAT -- MEAT plans

Annex 1Page 10

to set up regional ANPE offices which will be responsible for monitoring and enforcement authority at theregional level (see Map 1). In addition, a monitoring capacity of inland surface waters has been put inplace. These efforts should improve the quality and consistency of environmental data. The ability tomonitor environmental progress is essential to keep track of the marginal costs and benefits ofenvironmental investments with the associated implications for resource allocation at the national level.

18. Enforcement. Enforcement is constrained by the lack of realistic norms (though the Governmentis in the process of establishing new norms for air, water, toxic and noise pollution) and institutionalcapacity to enforce existing norms. The Government's commitment to enforcing environmental standards atall costs is questionable. Though ANPE officially has the legal mandate to take strict measures againstpolluters, such as temporary closure of polluting plants, there is still much reluctance to implement suchmeasures, particularly against public enterprises. Worldwide the most successful approach toenvironmental management is an integrated, permit-based approach involving the polluters in settingrealistic and achievable standards.

III. SECTORAL ENVIRONMENTAL ISSUES AND ECONOMICLINKAGES

A. AGRICULTURE

19. Sector strategy. Tunisia's strategy for agricultural development is clearly spelled out at thebeginning of the 8th Plan (1992-96). Agriculture was the first sector to undergo a structural adjustmentprocess (1987) and is still considered the basis of the national economy ("le fondement de 1'economienationale"). Although the sector's annual growth rate during the 7th Plan averaged 3.8 percent, thegovernment has projected a 6 percent average annual growth for the period 1995-2001. The developmentstrategy of the sector will cost close to 4 billion DT (in current prices), 50 percent of which will come fromthe state budget, and will include five major components under which key elements are summarized below:

v Mobilization and efficient use of water resources. About 1.4 billion m3 of water (about 200 millionm3 of which are treated water) are expected to be mobilized at a cost ofjust under 2 billion DT(corresponding to an average cost of 0.15-0.20 DT/m3), bringing the rate of mobilization of known waterresources to 90 percent by 2001.

* Land and natural resource conservation. An ambitious program of soil conservation andafforestation, projected to cost over 1.5 billion DT, will focus on watershed management (600,000hectares), soil conservation practices on 400,000 hectares of land suitable for cereal production,maintenance of conservation work previously done on one million hectares, afforestation of 300,000hectares, development of forage crops on 400,000 hectares, and rangeland management of 2.2 millionhectares.

* Improvement in agricultural productivity through investment in applied research and the developmentof high quality seed production, and fanming systems adapted to dryland and semi-arid climateconditions. In addtion, agricultural extension will be enhanced through more support for l"Agence de laVulgansation et de la Formation Agricoles," which was created in 1990.

* Intensification of production and development of agro-industries to achieve three main objectives: (i)self-sufficiency in hard wheat, barley, and meat production; (ii) reduction of imports of sugar, milk, and

Annex 1Page 11

soft wheat; and (iii) increasing exports of olive oil, fruits, vegetables, and fish products. To achieve theseobjectives, an additional 100,000 hectares will be managed for intensive irrigation (at 5,000-6,000m3/ha, this implies an additional 550 miilion m3) and 77,000 hectares of cereal crops will be managed for"irrigation d'appoint." Other key actions will be designed to increasing olive oil, livestock; sugar beet,fruits, vegetables, and fish production and associated agro-industries.

Improvement in the institutional framework through reforms in land tenure, agriculural credit and taxsystems, and development of subsidized crop insurance schemes (through "le Fonds National deGarantie"). Water conservation will be promoted through the continued gradual increase of water pricesand the support of water user associations (700 new AIC for irrigation water will be created by 2001).Additional support to the sector will also come from continued subsidies for cereals, milk, and olive oil,deregulation of input and output markets, and continued development of rural infrastructure (electricity,water supply, and rwal roads).

20. Land distribution. Tunisia has a total land area of 15.6 million hectares, 62 percent of which isclassified as suitable for agriculture and livestock production ("surface agricole utile"). The cultivated areais 5 mnillion hectares, of which 2.1 million hectares are used for annual crops, 1.9 million hectares forperennial crops (68 percent olives, the rest fruits and vignards), and 1.0 million hectares are fallowed(Figure 1).

21. Farm structure and land tenure. The Tunisian farm sector is characterized by an asymmetricfarm size distribution with a large number of small operators (47% hold only 8% of the land) and a largeconcentration of land within the hands of a few (less than 2% hold over 28% of the land). The averagefarm size is less than 14 ha, with 85% of the farms having less than 20 ha (Figure 2).

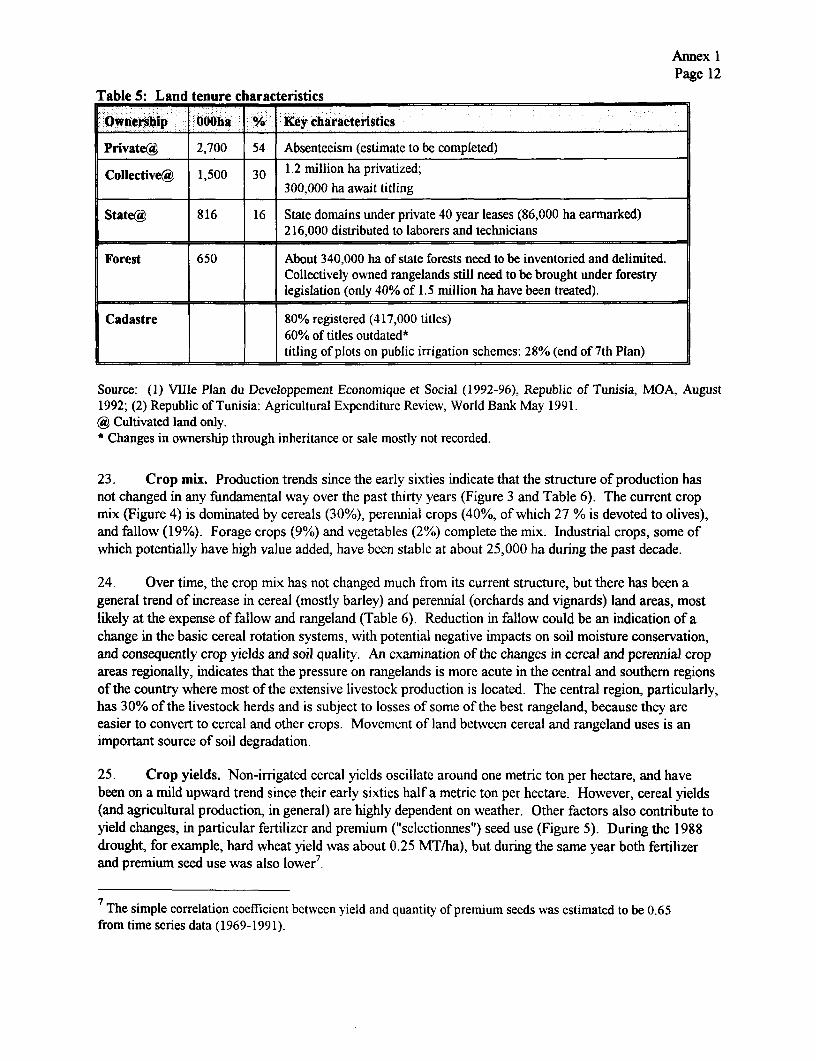

22. The land tenure system is emerging as a major constraint to the further development of theagricultural sector. The major characteristics of the land tenure system are fragmentation, absenteeism,and lack of clear and secure property rights. In addition, there is a need for a cadastral system andnecessary institutions to support the smooth functioning of land markets. With 1.2 million land parcels, the380,000 farm operations average 3.2 parcels per average operation. This trend is amplified by inheritanceand socio-cultural factors. Absenteeism, often associated with extensive agricultural practices, is animpediment to investment and intensification, partly because absentees are engaged in other economicactivities. Out of the 5 million hectares of cultivated land, about 54 percent are privately owned, 30percent are collectively owned and managed, and 16 percent are state held lands. Some key indicators ofthe land tenure system are shown in Table 5.

Annex 1Page 12

Table 5: Land tenure characteristics

ilOwnership ... 000Oha. Key characteristics

PrivateC#, 2,700 54 Absenteeism (estimate to be completed)

Collective* 1,500 30 1.2 million ha privatized;300,000 ha await titling

State@¢ 816 16 State domains under private 40 year leases (86,000 ha earmarked)216,000 distributed to laborers and technicians

Forest 650 About 340,000 ha of state forests need to be inventoried and delimited.Collectively owned rangelands still need to be brought under forestrylegislation (only 40% of 1.5 million ha have been treated).

Cadastre 80% registered (417,000 titles)60% of titles outdated*titling of plots on public irrigation schemes: 28% (end of 7th Plan)

Source: (1) Vllle Plan du Developpement Economique et Social (1992-96), Republic of Tunisia, MOA, August1992; (2) Republic of Tunisia: Agricultural Expenditure Review, World Bank May 1991.@ Cultivated land only.* Changes in ownership through inheritance or sale mostly not recorded.

23. Crop mix. Production trends since the early sixties indicate that the structure of production hasnot changed in any fundamental way over the past thirty years (Figure 3 and Table 6). The current cropmix (Figure 4) is dominated by cereals (30%), perennial crops (40%, of which 27 % is devoted to olives),and fallow (19%). Forage crops (9%) and vegetables (2%) complete the mix. Industrial crops, some ofwhich potentially have high value added, have been stable at about 25,000 ha during the past decade.

24. Over time, the crop mix has not changed much from its current structure, but there has been ageneral trend of increase in cereal (mostly barley) and perennial (orchards and vignards) land areas, mostlikely at the expense of fallow and rangeland (Table 6). Reduction in fallow could be an indication of achange in the basic cereal rotation systems, with potential negative impacts on soil moisture conservation,and consequently crop yields and soil quality. An examination of the changes in cereal and perennial cropareas regionally, indicates that the pressure on rangelands is more acute in the central and southern regionsof the country where most of the extensive livestock production is located. The central region, particularly,has 30% of the livestock herds and is subject to losses of some of the best rangeland, because they areeasier to convert to cereal and other crops. Movement of land between cereal and rangeland uses is animportant source of soil degradation.

25. Crop yields. Non-irrigated cereal yields oscillate around one metric ton per hectare, and havebeen on a mild upward trend since their early sixties half a metric ton per hectare. However, cereal yields(and agricultural production, in general) are highly dependent on weather. Other factors also contribute toyield changes, in particular fertilizer and premium ("selectionnes") seed use (Figure 5). During the 1988drought, for example, hard wheat yield was about 0.25 MT/ha), but during the same year both fertilizerand premium seed use was also lower7.

7The simple correlation coefficient between yield and quantity of premium seeds was estimated to be 0.65from time series data (1969-199 1).

Annex 1Page 13

26. The importance of cereal production in Tunisia (and throughout the region for that matter) stemsfrom its traditional role in the subsistence and economic conditions of small farmers (less than 20 ha, andrepresenting 85% of the operators), and from government subsidies and food security objectives. However,dryland cereal production is neither economical nor environmentally sustainable, particularly in areas ofunfavorable climatic and soil conditions. Overall yields are less that half the worldwide average andcompare favorably only with yields on the African continent. Granted there are important differences inlocal conditions, the long-run, extensive, non-sustainable forms of cereal production will exarcebate thewater and soil scarcity constraints. A targeted approach is needed to phase out non-sustainable cerealproduction in marginal and stagnating/declining yield areas and promote other farming systems whichbetter integrate crop and livestock production, using improved pastures and legume crops and areeconomically viable.

27. Livestock production. Several important factors characterize the livestock sector, and have adirect, although not easy to estimate, environmental impact. The country's general policy of increasing itsself-sufficiency in livestock products, has led to various pricing and subsidy schemes (Partow and Mink,World Bank, 1993), which are particularly evident during drought years. For example, during the 1988-89and 1993-94 drought years, herd sizes were not affected. Despite yearly fluctuations, two particular trendsare noteworthy because of their potential implications for the overall balance between livestock units andfeed supply, and consequently the carrying capacity of the land: (i) the increase in herd size (Table 7) and(ii) the increase in cultivated land (between 1986 and 1993, total animal units increased by over 15% at thesame time cultivated land increased by about 5%). Clearly, these general trends need to be examined indetail by species and at the regional level to determine more specifically where the pressure on rangelandresources is more acute. However, initial indications are, that the Center and South, where extensiverangeland-based livestock systems (mostly small animals) predominate, are the two regions where increasesin cultivated land have been more significant. Between 1980 and 1990, cultivated land increased by 4.8%,17.6%, and 9.0%, in the North, Center, and South regions, respectively (Msellati et al., 1994)8.

28. Three sources contribute about equally to overall feed supply: concentrates; cultivated forages; andpastures. Over time, however, the contribution of rangelands to the overall feed balance has decreaseddramatically, from 1,200 million feed units in 1964 to about 533 million feed units in 1990. Initialestimates indicate that, in addition to the conversion of pasture land to cultivated agriculture, the majorcause of this trend is a loss of productivity of rangelands, which can only be attributed to non-sustainableuses (Table 8, adapted from Msellati et al., 1994).

sThe results of this study ("Contribution to a Rangeland Strategy." December 1994) are preliminary andneed to be cleared with Laurent Msellati before they can be quoted.

Annex 1Page 14

Table 6. Trends in crop mix (1000 ha)

:1982 1986 1987 1990 1992

Cereals 1,197 1,278 1,710 1,551 1,499

Fallow 1,184 1,091 755 875 960

Forage crops* 428 419 407 449 432

Veetables 121 165 137 141 96

Industrial 9 24 27 30 24

Sub-total 2,939 2,977 3,036 3,046 3,011

Olive oil 1,306 1,294 1,379 1,327 1,327

Almonds 295 311 304 389 389

Other perr. 226 210 213 257 248

Sub-total 1,827 1,815 1,896 1,973 1,973

Total 4,777 4,792 4,932 5,019 4,975

Source: World Bank and Tunisia MOA and MOP. * Includes "cultures fourageres et legumineuse."

Table 7. Trends in Livestock Herds

1986 1993

Cattle 624,290 659,000

Sheep 5,409,080 7,110,000

Goats 1,046950 1,417,000

SAU (standard animal units) 1,770,000 2,085,000

Source: (1) Tunisia Small Farmers Potential and Prospects: A Technical Study, World Bank, March 1991; (2)Laurent Msellati et al. 1994.

Table 8. Sources of Degradation of Rangeland Resources

Million feed %units

Decrease in rangeland area (720,000 ha over 14 years) 145 21.7Decrease in forest-based rangeland area 30 4.5Productivity loss of existing rangelands (33% over 4 million ha) 270 40.5Rangelands not used in the South 138 20.7Rangelands under utilized because of land tenure constraints 84 12.6

0;iTotal :loss t:0: :: 0 0: 0 ;: 0 : :: 00: t: 00 0 ; ; : ; ;it tl: 0667:; ;:6 .100IO

Source: L. Mselati, 1994.

Annex IPage 15

29. The sustainability of irrigated agriculture. Tunisian irrigated agriculture contributes about 30percent of agricultural GDP. The sector uses about 82 percent of mobilized water resources9 and isexpected to continue at the same rate well beyond the year 2010 (Tunisia Water Sector Review, WorldBank, September 1994). Irrigated land has increased an average of 7,500 ha per year during the 80s,totalling 300,000 ha today. However, Tunisian statistics show that only about 250,000 ha are actuallyirrigated, corresponding to an 83 percent utilization rate. We examine in the next two sections the role oftwo important factors in the sustainability of agricultural production in Tunisia: water scarcity and waterpricing.

30. Water scarcity. Tunisia invested a great deal in the development of its water resources, and it isestimated that the country's traditional water sources will be fully developed by the year 2000 (TunisiaWater Sector Review, World Bank, September 1994). Because the country's water balance will becomeincreasingly small, and agriculture is slated for intensification and will continue to be the major user,nonpoint source pollution, mainly from agriculture, will add to the salinity of water resources andexacerbate the scarcity issue. In this light, by explicitly incorporating some form of quality'° constraints,and assuming that all potable water will have to be supplied from resources with salt concentration notexceeding 1.5 g/l, we can examine how constraining the water balance will be by the year 2010 based onsupply source, quality, and demand, separately or together, as follows:

Water supply (by 2010) = {demand}, {by source}, or {quality}

3,800 Mm3 = 3,200 Mm3 (demand/year) + 600 Mm3 (balance, assuming median rainfall)

3,800 Mm3 = 2,090 Mm3 (surface water) + 1,710 Mm3 (groundwater)

3,800 million m3 = 1,688 Mm3 (<1.5 g/l salt) + 1,044 Mm3 (1.5-3.0 g/l salt) +1,068 Mm3 (> 3.0 g/l salt)

3,800 million m3 = {625 Mm3 (<1.5 g/l salt, for domestic, industry, and tourism by 2010)+ 1,063 Mm3 (remaining supply with <1.5 g/l salt)} +

1,044 Mm3 (1.5-3.0 gA salt) + 1,068 Mm3 (> 3.0 g/l salt)

9Although the sector is allocated about 82 percent of water, it uses about 60 percent in an average year(Steve Mink, World Bank).

10 Given the lack of systematic data on water quality, we confine the analysis to salinity only, therebyunderestimating the scarcity constraint. The following salinity distribution is used, and assumed to be thesame until 2010:

Surface water: 74% < 1.5 g/l; 24% between 1.5 g/l and 3.0 g/l; and 2% > 3.0 g/lGroundwater: 8.4% < 1.5 g/l; 31.7% between 1.5 g/l and 3.0 g/l; and 60% > 3.0 g/l

Data sources: (1) Tunisia Water Sector Review, World Bank, September 1994) and (2) Developpement duTourisme et Preservation de l'Environnement en Tunisie, Volume II, METAP Project, February 1994).

Annex 1Page 16

31. The last relationship allows us to evaluate the availability of water for additional irrigation, byconsidering three scenarios (Table 9).

Table 9. Irrigation and water scarcity: 3 scenarios (assuming zero water balance by 2010

Scenario 1: Agriculture can only use water with salinity < 1.5 gAl

Amount of water available by 2010: 1,063 M m3

a. Maximum land area that can be irrigated at the current average rate (5250 m3/ha): 202,000 hab. Maximum water rate to maintain current level of irrigation (300,000 ha): 3,543 m3/hac. Maximum water rate to achieve new irrigation target (400,000 ha): 2,658 m3/ha

Scenario 2: Agriculture can only use water with salinity < 3.0 g/l

Amount of water available by 2010: 2,107 M m3

a. Maximum land area that can be irrigated at the current average rate (5250 m3/ha): 401,000 hab. Maximum water rate to achieve new irrigation target (400,000 ha): 5,268 m3/ha

Scenario 3: Agriculture can use water with no salinity restriction

Amount of water available by 2010: 3,175 M m3

a. Maximum land area that can be irrigated at the current average rate (5250 m3/ha): 605,000 ha

32. If reservoir siltation continues unabated at the current rate it will lead to storage capacity losses ofabout 500-600 Mm3 by 2010, which will wipe out the projected positive water balance, and severelyrestrict additional irrigation potential (Table 9) and will require even larger efficiency gains (Table 10).

Table 10. Irrigation implications of water scarcity

No salinity restriction Can potentially irrigate about 600,000 ha at current ratesIncreasing need for salt tolerant crop mixGreater potential impact of salinity on productivitySpecial precautions for irrigation

Irrigation water with salinity (1.5-3.0 g/l) Can potentially irrigate about 400,000 ha at current ratesIncreasing need for salt tolerant crop mixGreater potential impact of salinity on productivity

Irrigation water with salinity <1.5 g/l Can potentially irrigate about 200,000 ha at current rates;or, irrigate about 300,000 ha by achieving a 33% efficiencyin water use;or, irrigate about 400,000 ha by achieving a 50% efficiencyin water use;

33. From this analysis we can draw some general conclusions (summarized in Table 6) which clearlypoint to water scarcity (quantity and quality) as a major constraint to the future development of theagricultural sector, if not before, certainly beyond 2010, and that major gains in water use efficiency willhave to be achieved and maintained, although, as we suggest below, progress will be dependent on otherpolicy and institutional factors.

Annex 1Page 17

34. Water use efficiency. Efficient water management requires strict control of losses and water use;losses can be minimized with good pumping schemes and efficient distribution networks; use requires dosemanagement (quantity and timing); but the complex land tenure structure, the high degree of absenteeism,the credit system, and insufficient extension services together with relatively high efficiency levels combineto make the hypothesis of dramatic savings from irrigation efficiency not very likely in the foreseeablefuture.

35. The analysis also shows that important trade-offs need to be made between different uses, changesin crop mix patterns, and investment in water mobilization, treatment, and reuse. Addressing these trade-offs in systematic ways will require starting to think about water and land resources and related issues in astrategic and integrated way, but also to develop and use methodologies and decision support systems(incorporating benefit-cost or cost-effectiveness approaches) to guide government policy.

36. Water pricing. Based on available data sources, current estimates of the value, price, and cost ofwater are summarized in Table 11.

Table 11. Value, price, and cost of water

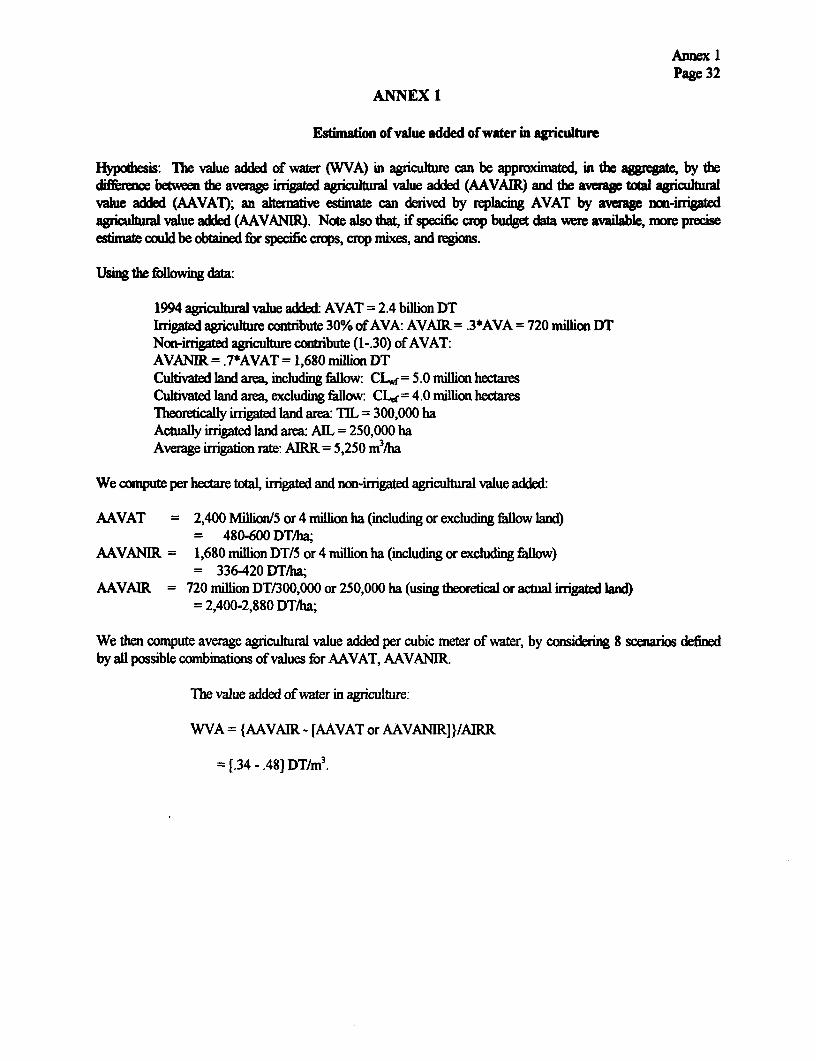

Use Value of water (DT per m3 ) Price of water (DT per m3) Cost of water (DT per mi)

Agriculture 0.34 - 0.48 0.04 (Annex 5, Water groundwater: 0.24 - 0.52*(details in Annex 1) Sector Review, May 1994 & surface water: 0.15 -0.39*

Mink) treated waste water: 0.25*Cost of additional water: 0.15-0.20 / (1996-2001) (see para.

_____________ ~~~~~~~~~~~~~~~19)

Domestic: 0.32 (1993 average over 0.45#Urban 1 - 14 (willingness to pay for SONEDE's tariff schedule) 0.86#Rural privately supplied water)&

Industry 0.59@ 0.59 (highest SONEDE rate) 0.45#

Tourism 0.59@ 0.59 (same as industry) 0.45#

* From Draft annex 4 (Rezebos): "The Value and Cost of Water," Tunisia Water Sector Review, World Bankmission 1993/94)& Draft annex 4: "The Value and Cost of Water," Tunisia Water Sector Review, World Bank mission 1993/94).Based on fragmented data and applying to irregular supplies of water.# "Etude Economique sur l'Eau Potable en Tunisie: Rapport, lere partie. M.L. Lahouel et al., November 1993.@ Because of lack of data, the value of water is assumed to be equal to SONEDE's water price for the highestquantity users (>151 m3/quarter). Discussions with Tunisian officials indicated that both in industry and tourismsome operators are starting to develop alternative sources of water supplies, deeming SONEDE's price too high, anindication of willingness to pay, which we use as a proxy for the value of water in the two sectors.

37. This shows that: (i) water is still being subsidized" (about 83 million DT per annum based on thedifference between average cost and price); (ii) the level of subsidy is even larger if willingness to pay is

1 If all the irrigation water is priced at 0.04 DT/m3 and costs an average of 0.22 DT/m3, the amount ofsubsidy would be about 284 million DT. However, according to Steve Mink, only 20 percent of irrigationwater is being subsidized, which would put the total subsidy level at about 52.1 million DT.

Annex IPage 18

taken into account; (iii) the average value added of water in agriculture (estimated in Annex 1 in the range0.34-.48 DT/m3), is about twice the current average cost of water mobilization; and (iv) as the marginalcost of supplying irrigation water increases (recall that by the year 2010 most available resources will havebeen mobilized), the value added of water will have to also increase, suggesting that a detailed analysis bycrop and region be undertaken to determine the most economically viable and environmentally sustainablecrop mix for the country. An important target would be to identify specific areas of the country whereproduction can be sustained without policy distortions and the underpriced of environment and naturalresource.

38. Soil degradation. Sixty percent of Tunisia's useful land resources (estimated between 8.5 and 10million hectares) are subject to different forms of degradation of varying intensities, under the combinedeffects of natural processes and human activity. The county's rainfall pattern (wide regional variations,timing, irregularity, heavy storms, and violent sporadic floods) and the hilly topography combine withsocio-economic factors (population pressure on vegetative cover, particularly cultivation of marginal landspreviously used for grazing and deforestation) and inadequate management practices (tilling up and downthe slope, stubble plowing, and mechanical operations) to produce significant soil erosion.

39. The 1992 Tunisia "National Report to the United Nations Conference on Environment andDevelopment" and the 1993 "State of the Environment Report" identify four major sources of landdegradation.

(i) Soil erosion due to water and flooding, results in soil losses equivalent to withdrawing11,000 ha permanently from production each year. This form of erosion predominates in the north(71%) and south (23%); estimated erosion rates are in the range 5-50 tlhalyr. Detailed regionaldata is not available, but the partial data presented in Table 12 provides an indication of thepervasiveness and the severity of the erosion problem in Tunisia.

Table 12. Erosion distribution in Northern Tunisia

Erosion class North West North East Total (Ha)

Ha % Ha %

Low 301,500 26.1 301,500

Moderate 242,800 21.0 183,000 19.9 425,800

Severe 148,200 12.8 27,000 2.9 232,200

Very severe 57,000 6.2

Region total 1,155,000 100 918,000 100 2,073,222

Source: Sols de Tunisie. Bulletin de la Division des Sols, No.11, 1980. Ministry of Agriculture, Tunisia.

(ii) Desertification, mostly due to wind erosion, salinity, and genetic weakening of rangelands,results in "the loss of 8,000 ha of relatively productive land each year.

(iii) Urban encroachment. It is estimated that the rapid urbanization that occurred between 1975and 1985 "took place mainly on farmland." An estimated 4,000 ha is permanently lost toagriculture each year.

Annex 1Page 19

(iv) Salinization, due to changes in the water table and irrigation practices, contributes to the lossof about 1,000 ha per year.

40. In addition, the degradation of rangeland resources (combined effects of land lost to cultivation,productivity loss and other factors) can be put at about 23 percent of the total feed demand (feed value for460,000 SAUs)'2. However, note that some of this loss is compensated by the gains from conversion of theland to other uses.

B. INDUSTRY AND ENERGY

41. Structure and Trends in the Industrial Sector. For the last few decades, industrial developmenthas been a central pillar of Tunisia's development strategy. The country now has an important industrialbase which accounted for 31% of GDP in 1992 compared to 24% in 197013. Manufacturing is the largestcomponent of the industrial sector (consisting primarily of agro-industry, construction materials,machinery, textiles and chemicals) followed by fuel production, gas and electricity, and mining (primarilyof phosphate and steel). Tunisia has performed well in terms of export growth, with manufactured exportsincreasing by 9% a year during 1980-92, though growth has slowed in recent years. This rate of growthwas achieved through a combination of policies that fostered macroeconomic stability and increased theoutward orientation of the economy.

42. Structure and Trends in the Energy Sector. The principal sources of primary energy in Tunisiaare oil and natural gas. The structure of energy consumption has changed dramatically over the past 30years in favor of gas which represented 30% of energy consumed in 1992 compared to only 7% in 1970.Ttraditional energy sources (primarily wood) are an important source of energy in the household sector,however, data on wood consumption is limited. Electricity demand is growing at 6% a year which willrequire an expansion of Tunisia's production capacity. Much of this demand is likely to be met fromincreased use of natural gas; the state electricity company (STEG) estimates that 80% of currentproduction capacity could use gas.

43. Environmental "Hotspots". Most industry and energy use occurs around urban centers wherepollution affects the health and well-being of large segments of the population. Industrial pollution hasincreased steadily in Tunisia over the last twenty years. Industrial activity is considerable and diverse,concentrated primarily around the large cities and along the coast. At least 12% of Tunisia's 10,000officially registered industrial establishments have been identified as major polluters. The environmental"hotspots" in Tunisia (areas where problems of air quality, industrial/municipal water pollution and solidwaste tend to converge) are major population centers on the coast: Tunis, Sousse, Sfax, Gabes, Gafsa andBizerte. These areas all contain major industries which are known point sources of water and air pollution,as well as port facilities and tourist development zones. Beaches in the Sfax and Gabes areas have beenclosed for a number of years due to industrial pollution. Though these are not tourist beaches and pollutiondoes not appear to have had a negative impact on the tourism trade, as yet, industrial pollution if notcontrolled could jeopardize tourism.

12 Assuming one standard animal unit requires 1450 feed units per year.

13World Development Report, 1994.

Annex 1Page 20

44. Land use regulations in these areas are, for the most part, poorly defined, with the consequentjuxtaposition of industrial zones, tourist beaches and residential areas. Very few industrial establishmentshave in-house pollution abatement facilities that are either operational or fully capable of treating planteffluents. Wastes are rarely pre-treated, nor are there centralized treatment plants where sewered wastescan be processed. Historical reasons, particularly the fast industrialization efforts in the 60s and 70s,explain why in the past pollution control was neglected.

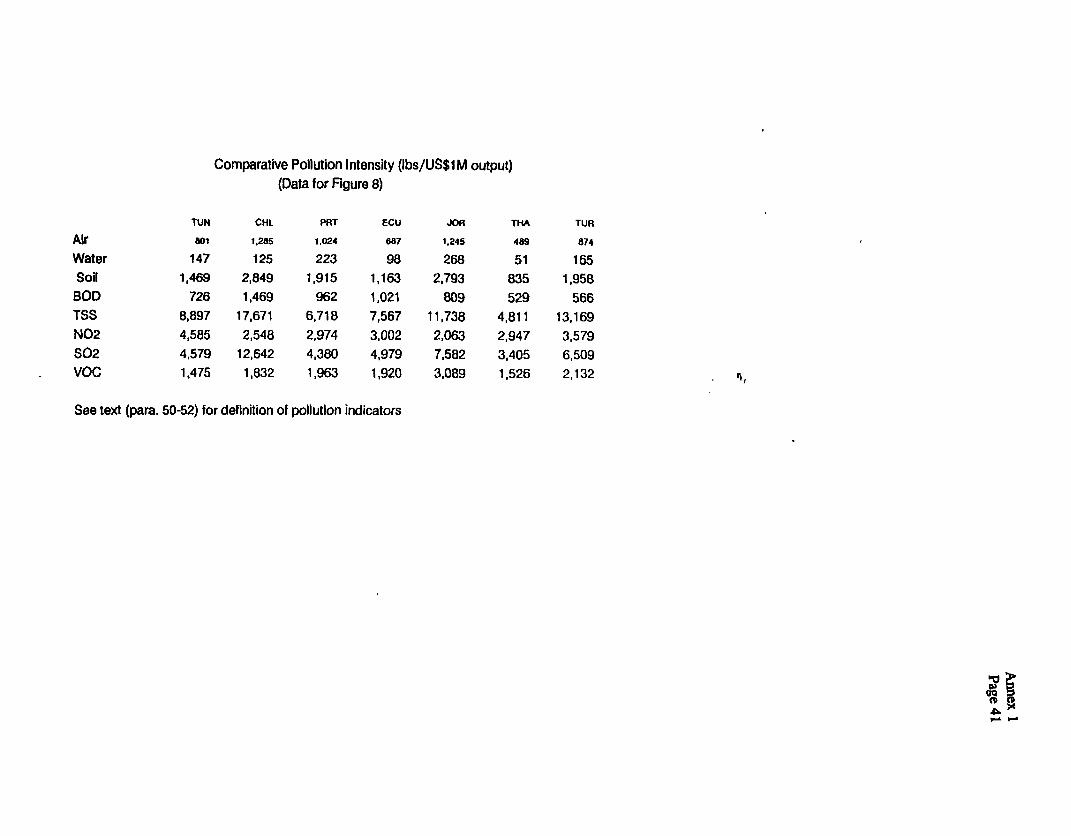

45. Industrial Pollution: Comparative Analysis. To assess the seriousness of Tunisia's pollutionproblems and its environmental progress, it is useful to compare its performance to a number of countriesfrom different regions and with similarities in either size of the economy or stage of economicdevelopement. Using data from the World Bank's industrial pollution projection system (IPPS)'4 , pollutionintensities and pollution loads were estimated for 28 sectors for Tunisia (TUN), Chile (ClL), Ecuador(ECU), Jordan (JOR), Portugal (PRT), Thailand (TMA), and Turkey (TUR). The IPPS system is based onthe premise that "industrial pollution is heavily affected by the scale of industrial activity, its sectoralcomposition, and the process technologies which are employed in production." Because industrial pollutiondata is not readily available for all countries, industry survey information on output is used to estimatepollution intensities (that is, pollution per unit of activity). A number of indicators are chosen to span therange of pollution impacts. First, three indicators are used for toxic pollution to air (Air), water (Water),and land (Soil); second, BOD (biological oxygen demand) and TSS (total suspended solids) are used forwater pollution intensity; and N02 (nitrogen dioxide), S02 (sulphur dioxide), and VOC (volatile organiccoumpounds) are used for air pollution intensity'5. The comparative results are summarized in Figure 6and accompanying tables.

46. Several important observations can be made. First, Tunisia exhibits the same pollution patterns,but compares favorably with other countries, particularly Portugal, Chile, Jordan, and Turkey; second, interms of water quality, the relatively high level of intensity of TSS and low level of BOD may reflect thefact that much more attention is given to wastewater treatment than to sedimentation and industrial wasteproblems; and third, Tunisia has the highest level of pollution intensity from NO2, usually associated withthe thermal combustion of fossil fuels, and indication perhaps of less efficient technologies in the industryand transportation sectors.

47. The distribution of pollution intensity within the Tunisian industrial sector also exhibits someinteresting patterns (see short and detailed tables at the end of the paper giving distribution of pollution).The chemical industry is the largest contributor to toxic pollution (respectively, 52% of air pollution, 70%of water pollution, and 60% of land pollution); other much smaller contributors are the paper, iron andsteel, and textile industries. Water pollution is almost entirely attributable to the food (53% of BOD), ironand steel (82% of TSS), paper (21% of BOD and 6% of TSS), and chemical (18% of BOD and 8% of

14 The Industrial Pollution Projection System, By H. Hetige, P. Martin, M. Singh, and D. Wheeler.December 1994.

15 Toxicity indicators are used because they incorporate heavy metals and are poisonous to humans. BODand TSS are traditional water quality indicators with direct implications for ecosystem health and levels ofwater treatment requirements; nitrates and total coliform are two other water quality indicators with moredirect linkage to human health, but were not available from IPPS. For air pollution, S02 and N02 arecaused by fossil fuel combustion in transportation and industrial activities, and VOC are particularlyimporant in the petrochemical and plastic industries; all these pollutants impact human health.

Annex 1Page 21

TSS) industries. The non-metallic mineral production, iron and steel, chemical, and petroleum refineryindustries are the major air pollutants.

48. Health Impacts of Pollution. What matters are not the total emissions of pollutants but rather thedamage that they cause to human health and the environment. A growing body of evidence points to aconsistent association between pollution and health. However, linkages between human health and/orecosystems damage, exposure, ambient pollution concentrations and emissions are complicated and requireconsiderable data and analysis to understand. There is very little data available on the impact of pollutionboth in terms of actual damage to and exposure of people and the environment to pollution in Tunisia.However, based on estimates done for the MENA region as a whole (MENA Environmental Strategy,World Bank, 1994), it is estimated that air pollution in Tunisia leads to the loss of 105,000 DALYs ordisability adjusted life years a year"6 .

49. Government Pollution Control Policies. Up until 1990, the government had no homogenous andintegrated industrial pollution policy. The body in charge of monitoring industrial pollution was not staffedor financed adequately to carry out a credible monitoring function. Inspections were made onlysporadically and even then enforcement was only partial given the absence of adequate environmentalquality standards. As of 1988, atmospheric emission limits did not exist and there were only partial normson liquid effluents with major pollutants with limits often so strict as to be impossible to observe.Regulations for waste disposal were absent as well.

50. With the creation of the National Environmental Protection Agency in 1988, the situation hasimproved considerably. The government is now in the process of developing new environmental norms anda pollution prevention policy framework that combines economic and environmental regulations, market-based incentives, monitoring, enforcement and negotiated agreements between enterprises and theauthorities based on a two part strategy:

clean-up highly polluted ("hot spot") areaspromote clean industrial growth where pollution is kept to acceptable norms.

51. Since 1992, a significant effort has been made to clean up "hot spots" and institutionalize the useof environmental impact assessments. Environmental action plans have been developed for the industrialzones of Bizerte, greater Tunis, Sousse, Sfax, Gabes and Gafsa. Two plans specific to tanneries and agro-processing industries have also been launched. Measures undertaken include the installation ofpretreatment and treatment plants. However, in general, industries still regard pollution control measuresas a burden that will undermine profitability. Though the Government espouses the "polluter paysprinciple", such a policy has yet to be implemented. The cost of pollution control and more importantly ofprevention have yet to be integrated into the concerns of industrialists since there are no pollution taxes.Certain other measures have been taken, however, that will help prevent pollution, including the creation ofFODEP (see para. 11). Water and energy tariffs have also been increased. The government startedincreasing electricity tariffs in 1990 and these are now considered to be in line with LRMC.'' Water tariffshave also risen sharply in recent years; however water consumption is charged on a sliding scale accordingto a category of users and volume of water consumed. While for large industries the price of water has

16A disability adjusted life year (DALY) is a measure of the loss of healthy life, based on years lost due topremature mortality combined with those lost as a result of disability.

17World Bank, 1994. Project Completion Report: Tunisia Fourth Power Project.

Annex IPage 22

already reached a level that covers the cost of supply, it is possible that small industries still do not seeenough incentives to conserve water.

52. Government's Energy Conservation Policy. The government's strategy to reduce theenvironmental impacts of energy is one of demand. For the next decade, the main thrusts of thegovernment's strategy are (i) launching an action program of energy efficiency in the main sectors; (ii)continuation of the policy of price adjustment and subsidy removal on energy products (except for keroseneand LPG); (iii) preparation of regulations to establish energy efficiency normns; and (iv) continueddevelopment of natural gas utilization in final energy use. This program is estimated to cost 65 MD duringthe period 1990-2001. It will pernit 300,000 tons of oil equivalent in energy savings by the year 2000,corresponding to 50MD.

53. The government is aiming for complete substitution to natural gas in the electricity stations whichwill reduce CO2 emissions and virtually eliminate SO2. Under a worst case scenario, S02 emissions wouldonly increase from 20% to 30% by the year 2000 while electricity demand will increase from 50 to 75%.These emissions could be completely eliminated if the price of gas became competitive with fuel oil. C02emissions would be reduced from 3 to 5% by 2000 due to the improved efficiency of the cycle combind andfrom 16 to 33% if maximum natural gas is used.

54. The government also plans to invest 100 MD in renewable energy development over the next tenyears for the following programs:

- development of biogas in rural areas -- actual potential is estimated at 30 million m3 a year, whichis equivalent to 50,000 m3 of wood

development of solar water heaters -- 800,000 households could be equipped with solar waterheaters which would save 300,000 tep per year. The GEF program has provided Tunisia with agrant of $4 million to subsidize the purchase price of water heaters so as to increase their uptake.

distribution of small-scale photovoltaic systems in rural areas far from the electricity grid.

55. Future industrial growth and its environmental implications. The industrial sector will play acentral role in the future economic growth of Tunisia. The Government intends to further liberalize itseconomy and has set itself a target of over 6% annual GDP growth for the next five years. Industry,particularly growth in manufactured exports, is considered a key economic sector in achieving this goal.Greater emphasis on privatization and export promotion is to be welcomed from an environmentalperspective as competition with EU countries is likely to require firms to comply with higher environmentalstandards. Inward looking economies, such as in Eastern Europe, China, and India, have historically hadmore severe pollution problems as they rely heavily upon state-owned enterprises and lack of competitionhas provided little incentive to firms to improve their environmental standards.

56. There are strong linkages between private sector development, economic liberalization, cleangrowth and human health benefits. If the Government wishes to capitalize on these poisitive linkages it isessential that it establish a policy and institutional framework that encourages rapid and clean growth. Keywill be removing impediments to the adoption of clean technology, including tariff and non-tariff barriers tothe importation of clean technology, and reducing and eventually eliminating input subsidies thatdiscourage resource conservation and efficiency improvements. These reforns should also be accompaniedby the introduction of pollution charges or taxes on polluting activities which will encourage resouce useefficiency and pollution abatements (see section para. 89).

Annex 1Page 23

C. TOURISM

57. Overview. Since the 1960s, tourism has witnessed explosive growth in Tunisia and today is one ofthe country's most important sources of foreign currency. In 1993, foreign exchange earnings from tourismreached nearly $1.3 billion, 30 percent of the income from merchandize exports, and the sector accountedfor 4 percent of GDP. Tourism is also a major source of direct and indirect employment, providing200,000 jobs of which 60,000 are direct, and has a positive effect on other parts of the economy, such asagriculture, and the manufacturing and construction industries.