Embed Size (px)

Citation preview

April 16, 2007

Document of the World Bank

Report No. 39672-CL

ChileInvestment Climate Assessment

(In Two Volumes) Volume I: Executive Summary and PolicyRecommendations

Finance and Private Sector UnitPoverty Reduction and Economic Management UnitLatin America and the Caribbean Region

39672P

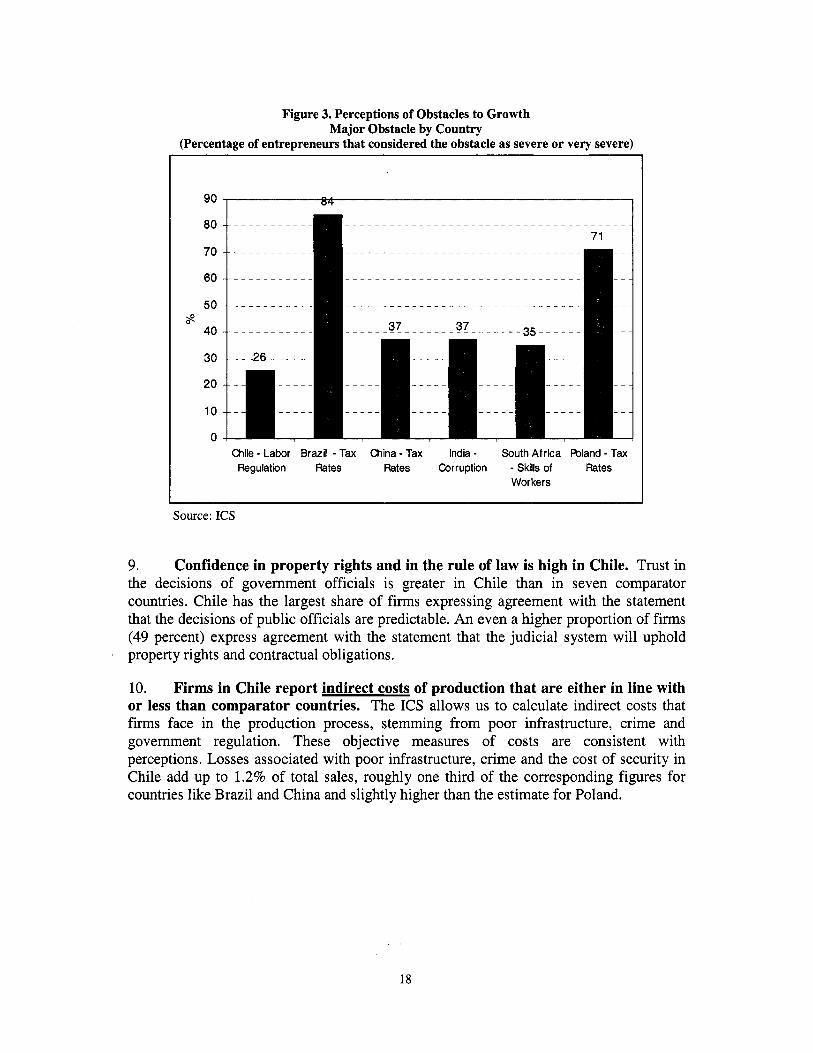

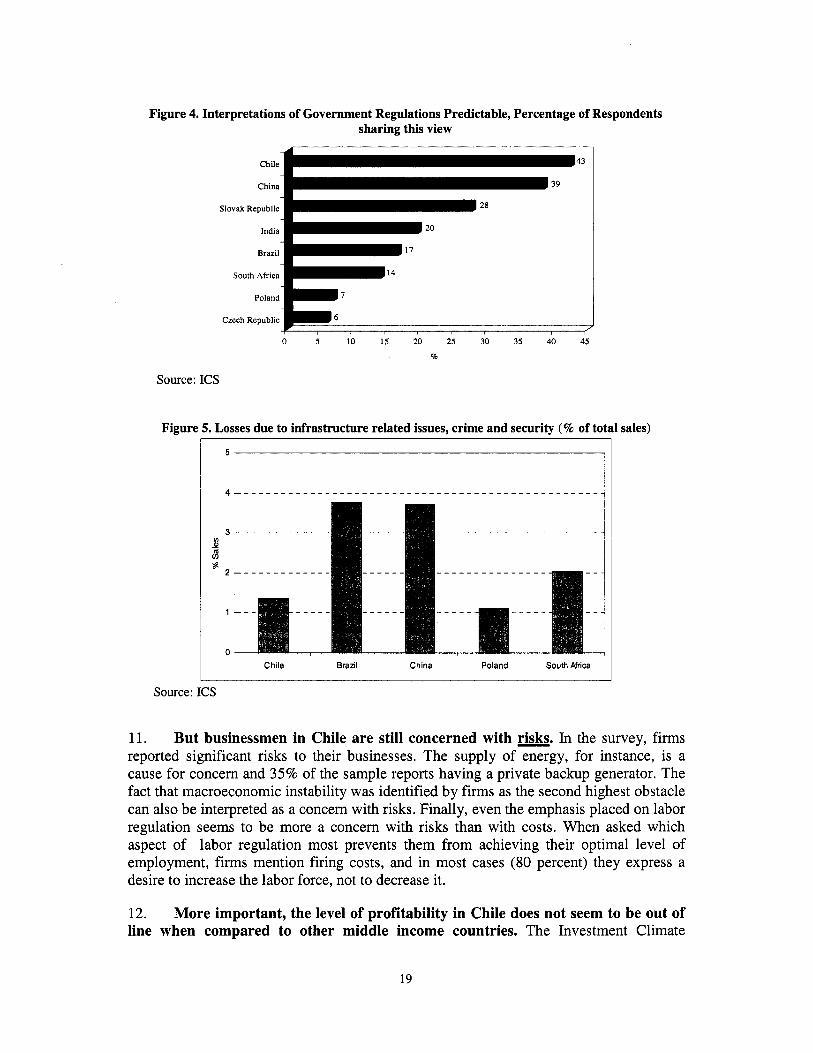

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

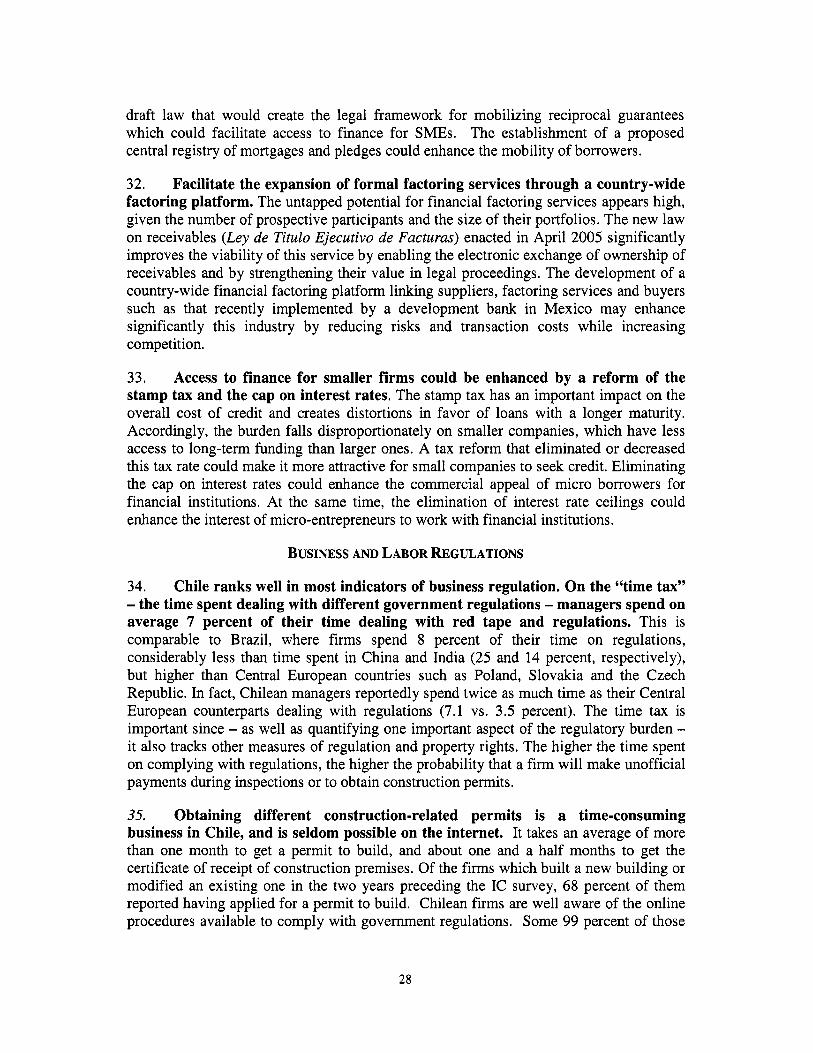

Aut

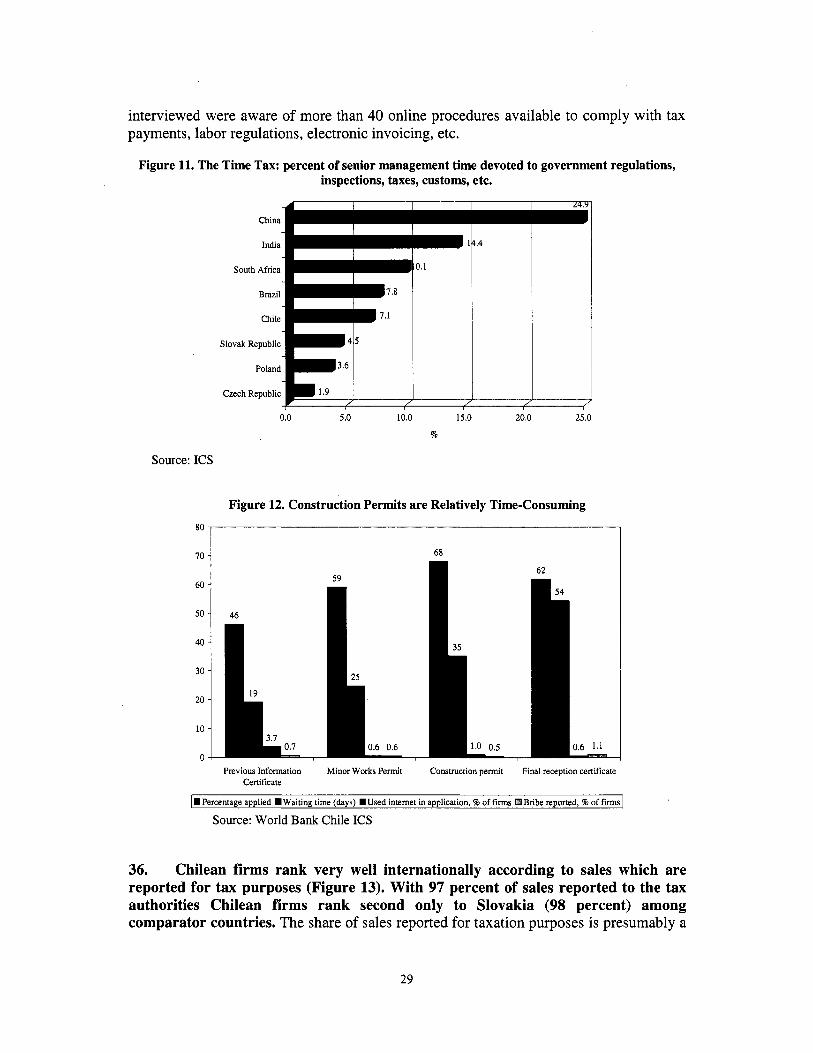

horiz

edP

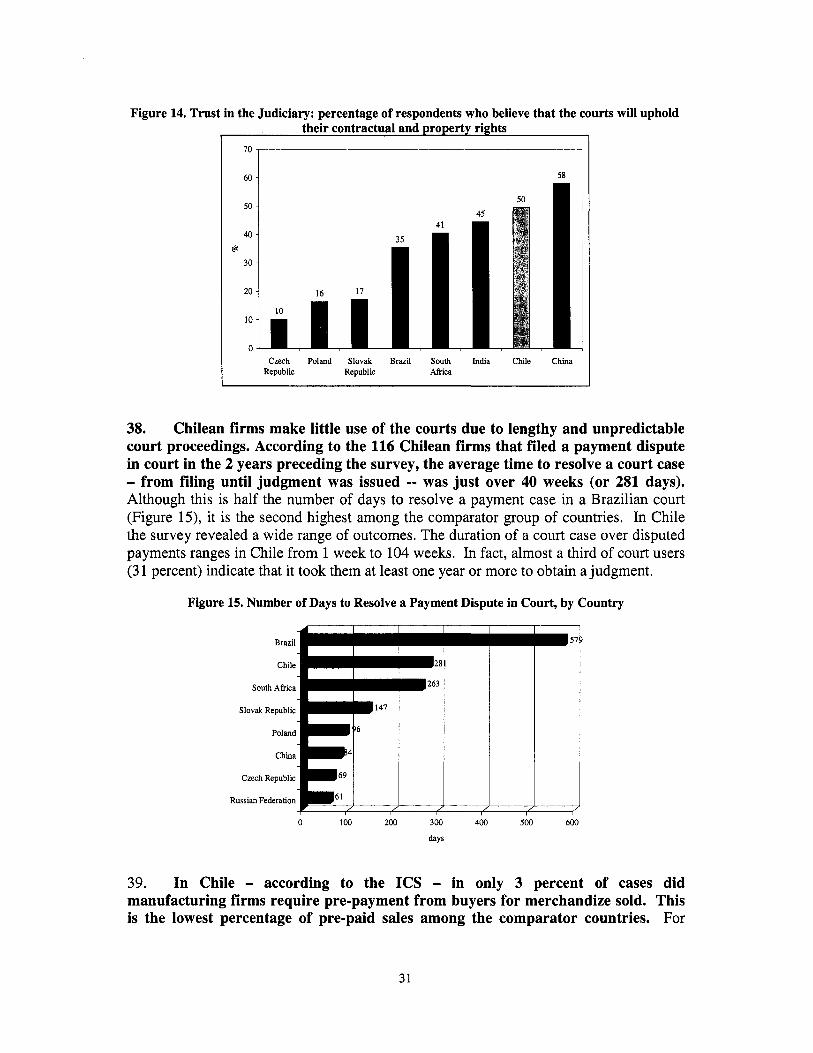

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

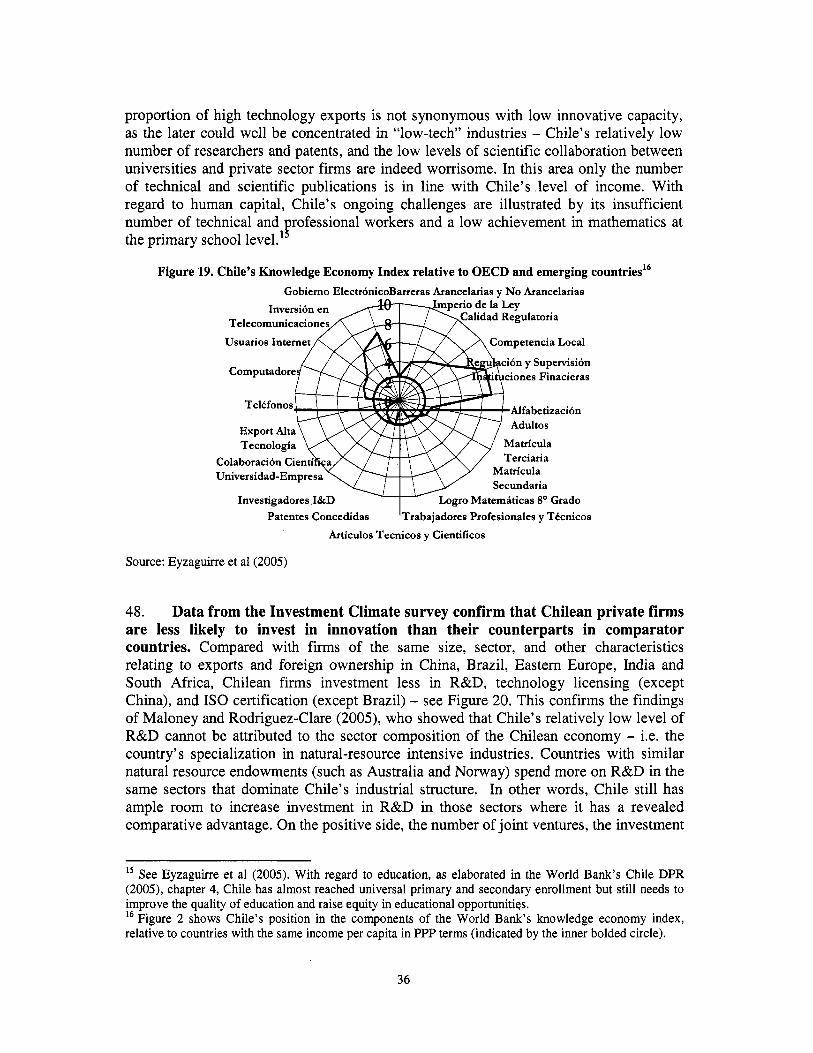

ure

Aut

horiz

edP

ublic

Dis

clos

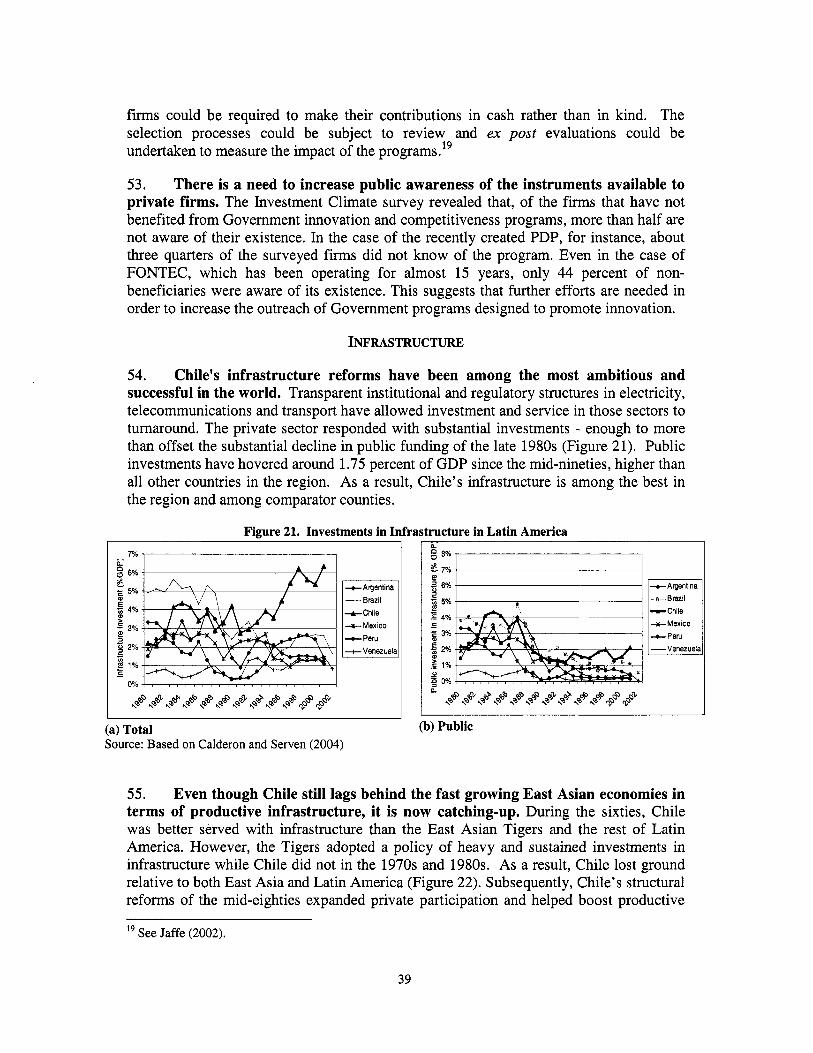

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

ed

ABBREVIATIONS AND ACRONYMS ACCIF ACHEL AUGE C A I CAS CASEN CONAF CONICYT CORFO DIPRES DPR ENIA EU FDI FECU FEDIT FIA FIDES FOGAPE FONASA FONTEC FOSIS FSSA FTAs FTE GDP IMF INE ISP L A C L D C MIDEPLAN MINEDUC MOPTT MPG NIS NSF OECD OMIL PASIS PAYGO PDP PEE PEPS PISA PRI SBIF SENCE

Average Country Citation Impact Factor Asociacion Chilena de Leasing Plan o f Universal Access with Explicit Guarantees Cuenta de Ahorro de Indemnizaci6n Country Assistance Strategy Chile’s National Household Survey Chile’s National Forest Corporation National Commission o f Science and Technology Industrial Development Corporation Budget Office, Ministry o f Finance Development Policy Review Encuesta Nacional Industrial Anual European Union Foreign Direct Investment Ficha Unica Codijicada Uniforme Spanish Federation o f Technological Innovation Entities Agrarian Innovation Foundation Fondos de Inversion de Desarrollo de Empresas Fondo de Garantia para la Pequeiia Empresa Publicly Run Social Health Insurance System Fondo Nacional de Desarrollo Tecnoldgico y Productivo Social Development Fund Financed by Chilean Government Financial Systems Stability Assessment Free Trade Agreements Full-Time Equivalent Gross Domestic Product International Monetary Fund National Statistics Institute Public Health Institute Latin America and the Caribbean Least Developed Countries Chile’s Ministry o f Planning and Cooperation Chile’s Ministry o f Education Ministerio de Obras Pu’blicas Minimum Pension Guarantee National Innovation system National Science Foundation (USA) Organization o f Economic co-operation and Development Ojicina Municipal de Intermediacidn Laboral Non Contributory, Social Assistance Benefit to Elderly Indigent Pay-as-you-go Financing for Social Insurance Institutions Program Desarrollo de Proveedores Plan Especial de Empleo Public Employment Programs Program for International Student Assessment Public Research Institute Superintendencia de Bancos e Instituciones Financieras Chile’s Social Risk Management Survey

1

SESMA SIC S I I SIMCE SING S M E svs SUBTEL TFP T M C USD VAT WB

Chile’s Environmental Metropolitan health Service Sistema Interconectado Central Servicio de Impuestos Internos Subsidies for Employment Creation Sistema Interconectado del Norte Grande Small and Medium Enterprise Superintendencia de Valores y Seguros Telecommunications Sub-secretariat Total Factor Productivity Tasa Mdxima Convencional United Sates Dollar Value Added Tax World Bank

2

ACKNOWLEDGEMENTS

This report was prepared by a team led by Jose Guilherme Reis and comprised of Stefka Slavova (Business Regulation), Pablo Fajnzylber (Technology and Innovation), Tito Yepes (Infrastructure), and Emanuel Salinas (Finance). The productivity analysis i s based on a background paper prepared by Alvaro Escribano, Jose Luis Guasch, Jorge Pena and Manuel de Orte. Leonid Koryukin also provided inputs for the productivity analysis and the analysis of the ENIA data base. Leyla Castillo, Mariam Dayoub and Patricia Melo provided valuable assistance in the preparation of the report. Peer reviewers Sara Calvo, William Maloney and Mary Hallward-Driemeier provided valuable comments and suggestions. Additional important inputs were received from Susan Goldmark, Marianne Fay, Jose Luis Guasch, Constantinos Stephanou, Raffaella Mota, James Parks, Daniel Oks, Phillippe Durand, Esperanza Lasagabaster, Juan Gaviria, Michael Goldberg and Francis J. Earwaker.

We would l i ke to acknowledge important contributions received from government officials in Chile, especially from the Subsecretaria de Economia, Ana Maria Correa, the former Subsecretario de Economia, Carlos Alvarez, as well as from Rosella Cominetti, Albert0 Ergas, Jaime Gre, Marisa Ernst, Andres Sanfuentes and Isabel Zuiiiga, a l l of them from Ministerio de Economia. The team also benefited from the insights provided in meetings with the Ministerio de Hacienda, led by the (then) economic policy coordinator, Marcel0 Tokman, as well as with Comision Nacional de Energia, Ministerio de Obras Pu'blicas, Transporte y Telecomunicaciones, Superintendencia de Electricidad y Combustibles (SEC), Fundacidn Chile, Corfo (Corporacidn de Foment0 de la Produccidn) and Sofofa (private sector manufacturing association).

The findings and views expressed here are exclusively those of the World Bank and do not represent the views of the government of Chile.

3

TABLE OF CONTENTS Abbreviations and Acronyms ......................................................................................................................... 1 Acknowledgements ........................................................................................................................................ 3 Table of Contents ............................................................................................................................................ 4 List of Figures ................................................................................................................................................. 5 List of Tables .................................................................................................................................................. 6 L i s t of Boxes ................................................................................................................................................... 6 Foreword ....................................................................................................................................................... 12

Background ............................................................................................................................................... 13

Finance ..................................................................................................................................................... 23 Business and Labor Regulations ............................................................................................................... 28 Innovation ................................................................................................................................................. 35 Infrastructure ............................................................................................................................................ 39

Annex: Productivity Analysis: A Summary of the Methodology ................................................................. 44 References ................................................................................................................................................ 46

General Findings ....................................................................................................................................... 16

4

LIST OF FIGURES

Figure 1 . GDP growth- International Comparison ...................................................................................... 13 Figure 2 . Entrepreneurs' perceptions of Obstacles to growth ....................................................................... 17 Figure 3 . Perceptions o f Obstacles to Growth .............................................................................................. 18 Figure 4 . Interpretations o f Government Regulations Predictable, Percentage o f Respondents sharing this view .............................................................................................................................................................. 19 Figure 5 . Losses due to infrastructure related issues. crime and security (% o f total sales) ......................... 19 Figure 6 . Profitability of the median firm in the manufacturing sector ....................................................... 20 Figure 7 . Productivity Elasticities and Semielasticities with respect to I C variables ................................... 21 Figure 8 . Average Productivity Impact (Gains and Losses) of Investment Climate Variables- Aggregate Level ............................................................................................................................................................. 22 Figure 9 . Domestic credit to private sector (% o f GDP) ............................................................................... 24 Figure 10 . Credit constraining by industry ................................................................................................... 27 Figure 1 1 . The Time Tax: percent of senior management time devoted to government regulations. inspections. taxes, customs, etc .................................................................................................................... 29 Figure 12 . Construction Permits Are Relatively Time-Consuming .............................................................. 29 Figure 13 . Percent of Sales Reported to Tax Authorities: An International Comparison ............................. 30 Figure 14 . Trust in the Judiciary: percentage of respondents who believe that the courts w i l l uphold their contractual and property rights ..................................................................................................................... 31 Figure 15 . Number o f Days to Resolve a Payment Dispute in Court. by Country ....................................... 31 Figure 16 . Chile: Minimum Wage. Mean wage and Productivity ................................................................ 33 Figure 17 . Productivity and Labor Cost in Manufacturing ........................................................................... 33 Figure 18 . Main Reasons for not changing the Size o f the Labor Force ....................................................... 34

Figure 20 . Differences with Chile in the fraction of firms with Investments in R&D. Technology Licensing. and I S 0 Certification (same sectors. size, export and FDI status) ................................................................ 37 Figure 21 . Investments in Infrastructure in Latin America .......................................................................... 39 Figure 22 . Composite Index of Productive Infrastructure ............................................................................ 40 Figure 23 . Investment in Transport Infrastructure ........................................................................................ 42 Figure 24 . Percentage of Firms that reported breakage or theft in transit ..................................................... 43

Figure 19 . Chile's Knowledge Economy Index relative to OECD and emerging countries ......................... 36

5

LIST OF TABLES

Table 1 . Chile at a Glance ............................................................................................................................... 7 Table 2 . Summary o f the Current Agenda and Main Messages of t h i s Report ............................................... 8

LIST OF BOXES

Box 1 . Productivity deceleration: cyclical or structural? .............................................................................. 15 Box 2 . What i s an Investment Climate Assessment? .................................................................................... 16

6

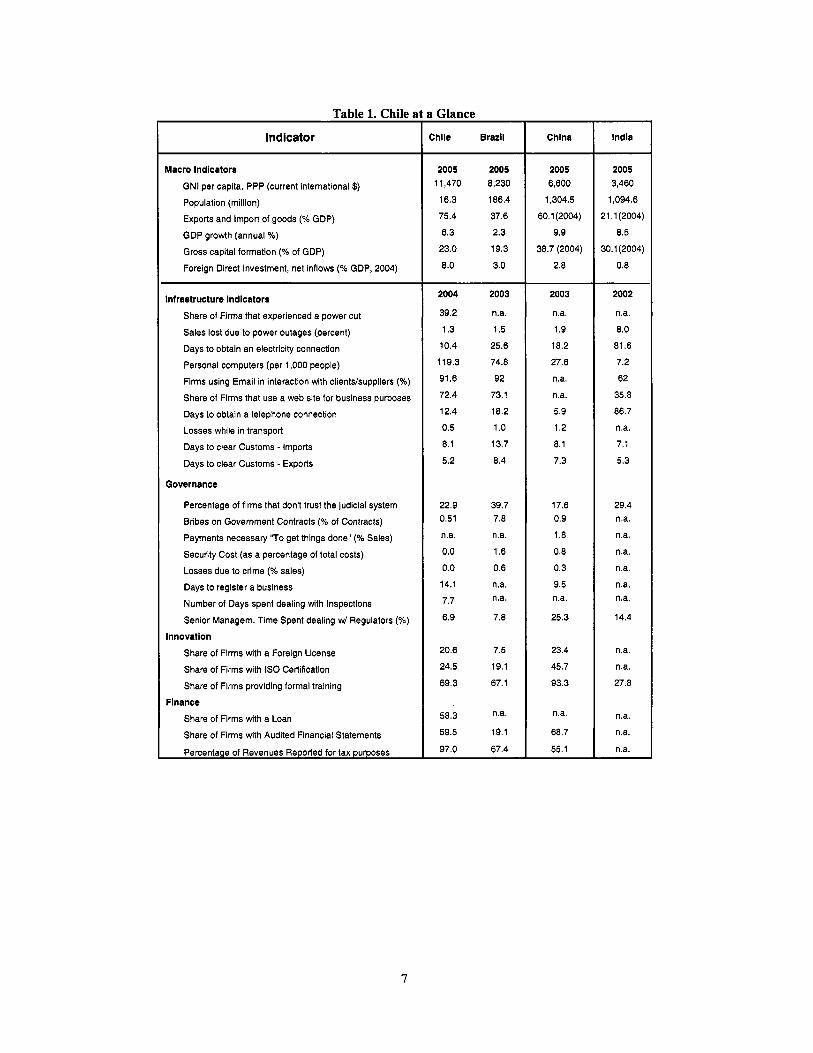

Table 1. Chile a

Indicator

Macro Indicators

GNI per capita, PPP (current international $)

Population (million)

Exports and Import of goods (“IO GDP) GDP growth (annual %)

Gross capital formation (?? of GDP) Foreign Direct Investment, net inflow (% GDP, 2004)

Infrastructure Indicators

Share of Firms that experienced a power cut

Sales lost due to power outages (percent) Days to obtain an electricity connection

Personal computers (per 1,000 people) Firms using Email in interaction with clients/suppliers (“IO)

Share of Firms that use a web site for business purposes Days to obtain a telephone connection Losses while in transport Days to clear Customs - Imports

Days to clear Customs - Exports

Governance

Percentage of firms that don’t trust the judicial system

Bribes on Government Contracts (% of Contracts) Payments necessary “To get things done” (% Sales)

Security Cost (as a percentage of total costs) Losses due to crime (% sales)

Days to register a business Number of Days spent dealing with Inspections

Senior Managem. Time Spent dealing w/ Regulators (“IO)

Innovation

Share of Firms with a Foreign License Share of Firms with IS0 Certification

Share of Firms providing formal training Flnance

Share of Firms with a Loan

Share of Firms with Audited Financial Statements

Percentage of Revenues Reported for tax purposes

I Glance

:bile Brazil

2005 2005 11,470 8,230

16.3 186.4

75.4 37.6

6.3 2.3

23.0 19.3

8.0 3.0

2004

39.2

1.3

10.4

119.3

91.6

72.4

12.4

0.5

8.1

5.2

22.9 0.51

n.a.

0.0

0.0

14.1

7.7

6.9

20.6

24.5

69.3

58.3

59.5

97.0

2003

n.a.

1.5

25.6

74.8

92

73.1

18.2

1 .o 13.7

8.4

39.7 7.8

n.a.

1.6

0.6

n.a. n.a.

7.8

7.5

19.1

67. I

n.a.

19.1

67.4

China

2005 6,600

1,304.5

60.1 (2004)

9.9

38.7 (2004)

2.8

2003

n.a.

1.9

18.2

27.6

n.a.

n.a. 5.9

1.2

8.1

7.3

17.6 0.9

1.8

0.8

0.3

9.5 n.a.

25.3

23.4

45.7

93.3

n.a.

68.7

55.1

India

2005 3,460

1,094.6

21.1(2004)

8.5

30.1 (2004)

0.8

2002

n.a.

8.0

81.6

7.2

62

35.8

86.7

n.a. 7.1

5.3

29.4 n.a. n.a.

n.a. n.a.

n.a. n.a.

14.4

n.a. n.a.

27.8

n.a. n.a.

ma.

7

E 0

1- 2

2 Y u

8 2 3

Y

m x e

$ ,n

.3 2 x E

0

0

.3 2 u

Summary and Overall Assessment

1. This study identifies constraints to private sector growth in Chile. Based on a survey covering 1,000 f i r m s and on other World Bank analytical work, this assessment focuses on the microeconomic and structural aspects o f the nation’s business environment, viewed from an international perspective. To this end, special attention has been given to factors constraining the efficiency o f product markets, financial and non- financial factor markets and infrastructure services including, in particular, weaknesses in the legal, regulatory and institutional framework.

2. The Investment Climate Assessment confirms the importance o f the investment climate for productivity in Chile. ICA results show that four aspects o f the investment climate (business regulation, infrastructure, finance and technology and innovation) affect Chilean firms in terms of their productivity. As may be expected, issues relating to infrastructure and business regulation affect total factor productivity negatively while ski l ls, technology and innovation have a positive impact.

3. Overall, Chile compares extremely well with other countries where the World Bank has made an Investment Climate Assessment. Both quantitative data and business perceptions support th i s conclusion. When asked about major obstacles to the growth of their businesses in Chile, f i r m s report fewer obstacles compared to other countries. In general, the percentage of entrepreneurs that consider the investment climate to be a major constraint to growth was lower than in other countries. Labor regulation was the obstacle most frequently identified but, even so, i t i s s t i l l not perceived as a major problem by 75 percent of f i r m s . The corresponding figure i s much lower in comparator countries. Confidence in property rights and in the ru le of law i s also high in Chile, as measured b y the proportion of f i r m s expressing agreement with the statement that the judicial system wi l l uphold property rights and contractual obligations. Finally, f i r m s also report indirect costs of production that are either in line with or less than comparator countries. Losses associated with poor infrastructure, crime and the cost of security in Chile add up to 1.2% of total sales, roughly one third o f the corresponding figure for countries l ike Brazil and China.

4. Business concerns mostly relate to uncertainty and risk. In the survey, f i r m s report significant risks to their businesses. The supply o f energy, for instance, i s an issue and 35 percent o f respondents report having a private generator. The fact that macroeconomic uncertainty was identified by f i r m s as the second highest obstacle to business growth can also be seen as reflecting a concern with risks. Specific measures related to weaknesses in the investment climate are summarized in table 1. Among these measures, access to finance, especially for micro- and small- f i r m s , seems particularly important. A more secure energy supply i s another important issue.

5. A second generation o f reforms i s seen as a challenge by businessmen in Chile. The priorities they identify clearly differ from the usual pattern observed in developing countries and in Latin America in particular. Labor regulation emerges as the principal concern for Chilean managers, especially the managers o f large f i rms. I t i s perceived as the foremost obstacle to a f i rm’s growth. As discussed later in t h i s report, firing costs are

10

identified as the main problem. This result seems to reflect the fact that labor market reforms are progressing only slowly in Chile, and they constrain the ability of f i r m s to compete in international and domestic markets. However, it also may reflect the fact that significant advance has already been made in other areas, such as regulatory policy and financial markets. The availability o f skilled workers also concerns Chilean businessmen. This i s an indication of the challenges faced by Chilean society in the area o f education, innovation and technology. These issues have been placed at the top of the agenda by government officials when focusing on prospects for long term growth in Chile.

6. Data from the Investment Climate survey confirms that Chilean private firms are less likely to invest in innovation than their counterparts from comparator countries. Compared with f i r m s of the same size, sector, export performance and foreign ownership profile operating in China, Brazil, Eastern Europe, India and South Africa, Chilean f i r m s invest less in R&D, technology licensing (except China), and I S 0 certification (except Brazil). Chile s t i l l has ample room for increasing i t s R&D investments in sectors where it has a revealed comparative advantage. On the positive side, the number o f joint ventures, the investment in fixed capital and the formal training offered to workers i s higher in Chile than in comparator countries - comparing f i r m s of the same size operating in the same industries.

7. Overall, the analysis confirms that an increased emphasis on innovation, technology and sk i l ls i s appropriate. In the econometric analysis, the estimated elasticities and the contribution to average productivity o f technology, innovation and sk i l l s are particularly significant. The results are consistent with business perceptions that the supply of sk i l l s as one of the most severe obstacles to growth. However, the outcome of this assessment suggests that the obstacles faced by f i rms in Chile are less severe than in other developing countries and that the profitability of f i r m s in Chile i s not particularly high (although not particularly low either). The evidence indicates that, while there are s t i l l obstacles to be dealt with in Chile, there i s room to focus more on engines of growth - and issues of technology, innovation and sk i l ls emerge as key focuses for public policy.

8. The government has been pursuing an active policy in this area, including the recent introduction o f a mining tax and an innovation fund. Nevertheless, additional measures could help promote higher private sector investments in innovation. They include complementary measures directed at facilitating private investment in innovation, such as reconfiguring the eligibility and selection criteria and the co-financing guidelines for existing matching grant programs. If there i s no demand for innovation on the part of the private sector, efforts to improve the S&T capacity on the supply side w i l l be ineffectual. Whi le matching grant schemes are an appropriate mechanism to promote private sector innovation, the effectiveness o f the schemes wi l l depend upon rigorous monitoring and evaluation, so that the eligibility and co-financing requirements may be adjusted if necessary. Finally, there i s a need to better inform private f i r m s of the available instruments. The Investment Climate survey revealed that, of the f i r m s that have not yet benefited from Government programs for innovation and competitiveness, more than half o f them are not aware that the programs exist. In the case o f the recently created PDP (Prograrna de Desarrollo de Proveedores), for instance, about three quarters o f the surveyed f i r m s did not know about the program.

11

FOREWORD The objective o f this study i s to evaluate constraints to private sector growth in Chile. Based on a survey covering 1,000 f i r m s and other Wor ld Bank analytical work, this assessment focuses on the microeconomic and structural dimensions o f the national business environment, viewed from an international perspective. T o this end, the study examines in detail factors constraining the efficiency o f product markets, financial and non-financial factor markets and infrastructure services including, in particular, weaknesses in the legal, regulatory and institutional framework.

In the simplest terms, the investment climate establishes the rules o f the game and the environment within which al l f i r m s must operate. This study focuses o n policies and institutions that influence the rate o f return and the risk associated with investment. I t includes regulatory policies, administrative procedures, infrastructure, as wel l as institutional issues such as the security o f property rights and the rule o f law.

This first volume presents the main results o f the analysis, including pol icy recommendations. More in-depth analyses are presented in Volume 11, which i s divided into seven chapters. The first chapter provides an overview o f the key questions and issues to be discussed and a background on methodology. The second chapter reviews recent economic trends in Chile. The third chapter presents a general statistical overview, including an econometric analysis o f the productivity o f f i r m s . The remaining chapters provide a detailed analysis o f four issues affecting the investment climate: access to and the cost o f finance, business and labor regulation, technology and innovation and infrastructure. There i s also a technical annex on the econometric methodology.

This assessment seeks to provide a diagnosis and policy recommendations for both the public and the private sectors in Chile. The Investment Climate Assessment (ICA) i s based on the Investment Climate Survey (ICs), but also goes beyond it. The report does not restrict itself to the results o f the survey-the I C s i s essentially a diagnostic tool that helps identify key bottlenecks to business growth. The report describes the main findings o f the survey and provides pol icy recommendations in selected areas. Other sources o f information are used to complement the analysis: background papers that were prepared in selected areas to complement the findings o f the I C s and other documents prepared by the World Bank, including the World Bank Country Assistance Strategy, the New Economy Study (2004) and the recent Development Policy Review (DPR).

To the extent possible, the views and the performance o f Chilean f i r m s are compared to those observed in fast growing economies and selected middle income countries. The I C s data base allows for international comparisons, because a core group o f questions i s asked in every country. China and India were chosen as comparators because they have been growing at a fast pace, at an annual average o f 5% in per capita terms, attracting a natural interest in the successful policies adopted by these countries. Benchmarking with Lat in America i s also important because o f the common institutional and economic background, and Brazi l was selected as a comparator. South Africa, Malaysia and selected countries o f East Europe (Czech Republic, Poland and Slovakia) were included as comparators as well.

12

BACKGROUND

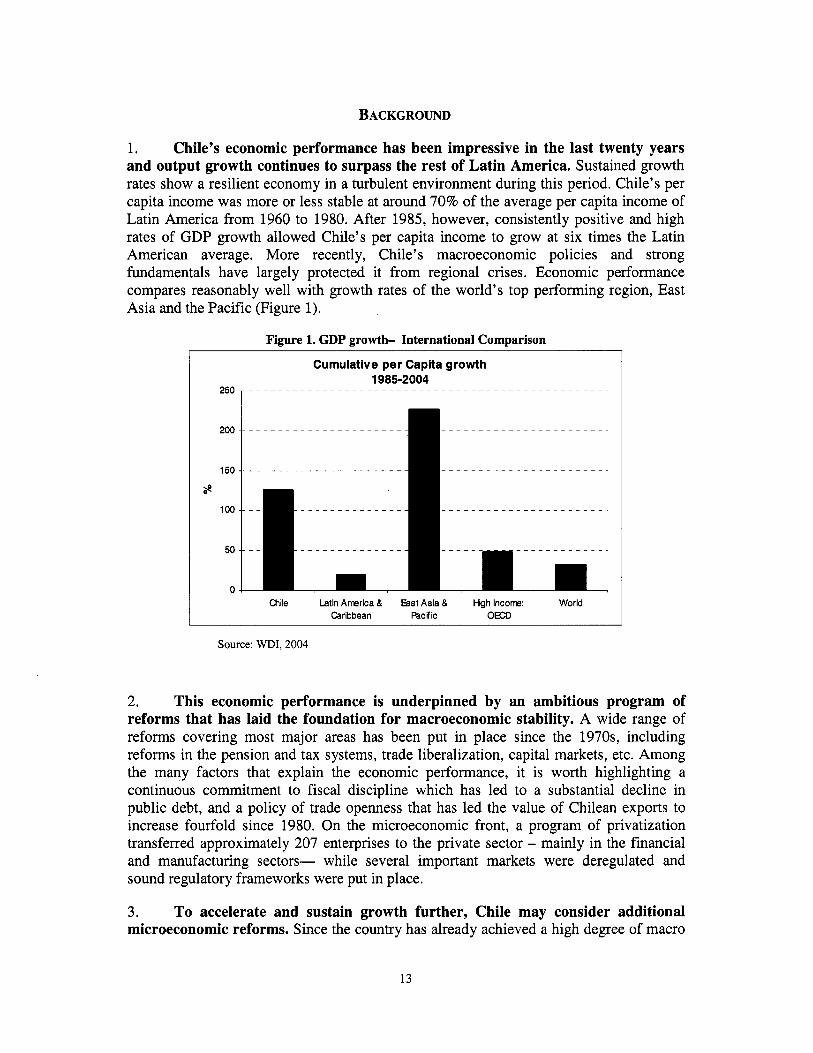

1. Chile’s economic performance has been impressive in the last twenty years and output growth continues to surpass the rest of Latin America. Sustained growth rates show a resilient economy in a turbulent environment during this period. Chile’s per capita income was more or less stable at around 70% of the average per capita income of Latin America from 1960 to 1980. After 1985, however, consistently positive and high rates of GDP growth allowed Chile’s per capita income to grow at six times the Latin American average. More recently, Chile’s macroeconomic policies and strong fundamentals have largely protected it from regional crises. Economic performance compares reasonably well with growth rates o f the world’s top performing region, East Asia and the Pacific (Figure 1).

Figure 1. GDP growth- International Comparison

250

200

150

ae 100

50

0 Chile Latin America & East Asia & Hgh income: World

Caribbean Pacific OECD

Source: WDI, 2004

2. This economic performance is underpinned by an ambitious program of reforms that has laid the foundation for macroeconomic stability. A wide range of reforms covering most major areas has been put in place since the 1970s, including reforms in the pension and tax systems, trade liberalization, capital markets, etc. Among the many factors that explain the economic performance, it i s worth highlighting a continuous commitment to fiscal discipline which has led to a substantial decline in public debt, and a policy of trade openness that has led the value o f Chilean exports to increase fourfold since 1980. On the microeconomic front, a program of privatization transferred approximately 207 enterprises to the private sector - mainly in the financial and manufacturing sectors- while several important markets were deregulated and sound regulatory frameworks were put in place.

3. To accelerate and sustain growth further, Chile may consider additional microeconomic reforms. Since the country has already achieved a high degree of macro

13

stability and an very good regulatory framework, it would be opportune to focus on a new round of microeconomic reforms aimed at further increasing long term economic growth. A new round of reforms may be needed as an additional impetus to growth because the macro and micro reforms initiated in the 1970s have already been fully deployed.

4. I n terms of human capital, Chile has almost achieved universal primary and secondary enrollment but still faces significant challenges. There i s urgent need to improve the quality of education and the equity o f education opportunities, as evidenced by comparing test scores with those o f countries with a similar per capita income, or a similar level of government expenditure per capita on primary and secondary education. Chile does not have a sufficient number o f technical and professional workers and achievement in primary school mathematics i s lagging.

5. Increasing emphasis has been placed on how to improve education and increase the adoption of innovatiodtechnology. Innovation has been placed at the top o f Government's priorities because greater innovation by both the public and private sectors wi l l not only increase long term growth but wi l l also help to reduce poverty and inequality. Despite major improvements in incentives and in infrastructure for innovation, international comparisons s t i l l reveal significant weaknesses in the areas o f education and innovative capacity. For a natural resource-rich country l i ke Chile, i t i s critical that sk i l ls and technology be in place to fully exploit i t s natural resources.

6. Building a sound environment for private sector growth requires a continuous program of reforms in several areas. Besides innovation, as discussed in a recent World Bank report, sustained high growth requires an efficient allocation of factors of production. As new f i r m s enter the market and less efficient ones leave it, a reallocation o f factors takes place and higher factor productivity i s achieved. The key i s having in place a private sector environment or investment climate that allows for the efficient entry and exit of f i r m s and the reallocation o f factors of production'. Chile has succeeded in improving the business environment in the last 25 years, and today it has an investment climate that compares favorably with many other countries. Nevertheless, there are opportunities for further improvement in areas such as labor regulation, competition policies, credit markets and the overall business regulatory environment. This report attempts to identify the remaining impediments and opportunities to stronger growth with new evidence from the Investment Climate Survey, which i s based on data collection from nearly 1000 f i r m s in 5 regions and 9 industries in Chile.

' World Bank (2005) DPR, p.62

14

Trends in Potential Output

s based on ENIA . Source: Ministry of Finance

See World Bank (2005) and chapter 2 o f volume I1 of this report.

15

te investment a

xperience 111 a range

en August and December 2004, with a

GENERAL FINDINGS

7. Chile compares extremely well with other countries where the World Bank has undertaken Investment Climate Assessments. Both quantitative data and business perceptions support that conclusion. When asked about the major obstacles to growth o f their businesses in Chile, f i r m s report fewer and less serious obstacles compared with other c ~ u n t r i e s . ~ In general, the percentage o f entrepreneurs that consider the investment climate to be a major constraint to grow was lower than in other countries. Labor regulation was the obstacle most frequently identified but, even so, it i s s t i l l not perceived as a major problem by 75 percent of firms. The corresponding figure i s much

Adapted from World Bank (2005), El Salvador Investment Climate Assessment,

In order to evaluate which are the most important investment climate constraints affecting Chilean firms, t h i s report uses both subjective and objective indicators. Greater emphasis i s placed on the latter. Perceptions, however, can help identify some constraints. A five-point scale i s used, ranging from extremely severe to not important. Figure 2 below sums up the findings, indicating the percentage o f firms that consider the obstacle as “severe” and “extremely severe”.

16

lower in comparator countries. The same applies to macroeconomic uncertainty which was ranked second by Chilean f i r m s . Yet only 25 percent o f f i r m s considered it a severe or very severe problem, while in Brazil, for instance, the percentage i s three times higher. Perception-based measures suggest that business managers in Chile are not greatly concerned about any o f the nineteen areas covered by the survey. No t surprisingly, the importance attached by respondents to the perceived obstacles to a f i r m s ’ growth in Chile clearly differs f rom the pattern observed in other developing countries and in Lat in America in particular. A greater weight i s given to problems l inked with a second generation o f reforms. That may suggest that Chile has already successfully tackled a first round o f micro reforms, but it also highlights the more complex challenges that l ie ahead.

Bectricity Cost of financing

Tax Addnistration

Figure 2. Entrepreneurs’ perceptions of obstacles to growth

17.8% 17.7%

15.4%

Source: ICs

8. Managers were more likely to be concerned about labor regulations, macroeconomic uncertainty, labor skills, informal practices, access to financing and tax rates than other aspects of the investment climate. Labor regulation emerges as the principal concern for Chilean managers, especially the managers o f large f i rms. As discussed later in this report, firing costs are identified as the key constraint. This result seems to confirm the fact that labor market reforms are progressing only slowly in Chile and are constraining firms in their ability to compete in international and domestic markets. However, fact that labor regulations are cited as the most important obstacle to company growth may indicate that significant advances have already been made in other areas, such as regulatory pol icy and financial markets.’ Macroeconomic uncertainty and four other issues fol low closely behind labor regulation as a concern for managers. Hence, it i s difficult to single out one key issue perceived by f i r m s to be an overriding concern.

Furthermore, the survey was made in 2004, when the issue of labor regulation was being widely debated.

17

Figure 3. Perceptions of Obstacles to Growth Major Obstacle by Country

(Percentage of entrepreneurs that considered the obstacle as severe or very severe)

90

80

70

60

50

40

30

20

10

0

a9

-. 04

Chile - Labor Brazil - Tax China - Tax India - South Africa Poland - Tax Regulation Rates Rates Corruption - Skills of Rates

Workers

Source: ICs

9. Confidence in property rights and in the rule of law i s high in Chile. Trust in the decisions of government officials i s greater in Chile than in seven comparator countries. Chile has the largest share of f i r m s expressing agreement with the statement that the decisions of public officials are predictable. An even a higher proportion of f i r m s (49 percent) express agreement with the statement that the judicial system wil l uphold

' property rights and contractual obligations.

10. Firms in Chile report indirect costs of production that are either in line with or less than comparator countries. The ICs allows us to calculate indirect costs that f i r m s face in the production process, stemming from poor infrastructure, crime and government regulation. These objective measures of costs are consistent with perceptions. Losses associated with poor infrastructure, crime and the cost of security in Chile add up to 1.2% of total sales, roughly one third of the corresponding figures for countries l ike Brazil and China and slightly higher than the estimate for Poland.

Figure 4. Interpretations of Government Regulations Predictable, Percentage of Respondents sharing this view

Source:

43 Chile

China 39

Slovak Republic 28

India 20

17 Brazil

South Africa 14

_ _ _ _ . . _ _ ~ _ _ _ r

0 5 I O 15 20 25 30 35 40 45

'KO

ICs

Figure 5. Losses due to infrastructure related issues, crime and security (% of total sales) I

5

4

3 a I * *

1

0 Chile Bradl China Poland South Africa

Source: ICs

11. But businessmen in Chile are still concerned with risks. In the survey, f i r m s reported significant risks to their businesses. The supply o f energy, for instance, i s a cause for concern and 35% of the sample reports having a private backup generator. The fact that macroeconomic instability was identified by f i r m s as the second highest obstacle can also be interpreted as a concern wi th risks. Finally, even the emphasis placed on labor regulation seems to be more a concern with r isks than with costs. When asked which aspect o f labor regulation most prevents them f rom achieving their optimal level o f employment, f i r m s mention firing costs, and in most cases (80 percent) they express a desire to increase the labor force, not to decrease it.

12. More important, the level of profitability in Chile does not seem to be out of line when compared to other middle income countries. The Investment Climate

19

Surveys permits a comparison o f profitability between countries. Profitability was estimated for manufacturing f i r m s in four comparator countries excluding indirect costs and depreciation because this data were not available for a l l countries. For the median Chilean enterprise, profitability was about 24.2 percent in 2004, higher than in Poland (17.4 percent), but lower than in South Africa (25 percent), Brazil (29.4 percent) and India (34.4 percent). These are approximate numbers, but the important point to note i s that profitability, while lower, i s comparable to that of other middle income countries where Investment Climate Surveys have been completed.

Figure 6. Profitability of the median firm in the manufacturing sector - International Comparison

Brazil' -I

0% 5% 10% 15% 20% 25% 30% 35% 40%

Profitability i s calculated as (Total Sales - Total Material Cost -Labor Cost - Electricity Cost)/ Sales * Estimate based on direct cost of materials instead of total material cost Source: ICs

13. Econometric analysis confirms the expected association between the investment climate and the productivity of firms. A number of investment climate indicators drawn from the Chile ICs were used as explanatory variables for productivity. Factors that enhance or detract from the competitiveness of manufacturing f i r m s in Chile were identified using statistically significant results from the regressions. The econometric methodology developed by Escribano and Guasch (2005) was employed in t h i s analysis. Different specifications of the production function were examined in order to get robust empirical elasticities for policy analysis. For purposes of the econometric analysis, the investment climate (IC) was separated into four component parts: (i) infrastructure; (ii) governance (including red tape and crime); (iii) finance; and (iv) quality, innovation and skil ls. Data was drawn from f i r m s having similar characteristics with respect to location, industry group, size, and other factors. The detailed results as well as details of the methodology are presented in the Annex.

20

14. The overall results of the ICs show that all four component parts of investment climate affect the productivity of Chilean firms. The results are summarized in Figure 7 and they indicate that three components of the investment climate in particular have a statistically significant association with productivity. Red tape, corruption and crime have, in general, a significant negative impact upon productivity. An increase of 1 percent in the number of inspections results in a decrease of 0.1 percent in productivity. Infrastructure shortcomings such as power outages and shipment losses have a strong negative effect. An increase o f 1 percent in the number o f days required for exports to clear customs reduces productivity by 0.1 percent. There i s strong evidence that labor training and innovation - as measured by the share of staff engaged in R&D - increase productivity, with a strong positive impact in the case of in- firm training. The experience o f the manager i s also important. Finally, with respect to finance, a l ine of credit was the only factor found to have a significant positive impact on the productivity o f f i r m s . Those f i r m s that have opened a l ine o f credit are 3 percent more productive.

Figure 7. Productivity Elasticities and Semielasticities with respect to I C variables- Average Levels of OLS Coefficients

In f rast ructures Qual i ty , Other Control Variables Red Tape,

Corruption and liInance Innovation and

0.3 0.25

0.2 0.15

0.1 0.05

0 -0.05

-0.1 -0.15

-0.2

Crime

nl I n

-0.05

1.1 1.2 1.3 1.4 2.1 2.2 2.3 2.4 3.1 1.1 Days to clear customs for exports. 1.2 Power outages. 1.3 Slipment losses. 1.4 Internet page. 2.1 Security. 2.2 Number o f inspections. 2.3 Cost o f entry. 2.4 Absenteeism. 3.1 Financing line program.

Labor S k i l l s U.26 r $4

0.005 ,ii',, u -0*01

-0.09

I

4.1 4.2 4.3 4.4 5.1 5.2 5.3 5.4 5.5 5.6 4.1 R + D . 4.2 Internal training. 4.3 University staff. 4.4 Experience o f the manager. 5.1 Incorporated company. 5.2 Foreign direct investment. 5.3 Exporter. 5.4 Capacity utilization. 5.5 Rent land. 5.6 Trade union.

*When the I C variable i s not expressed in log form, the estimated coefficient i s generally described as a productivity-IC semi-elasticity (in yellow). While the constant productivity-IC elasticity measures the percentage change in productivity induced by a percentage change in the I C variable, the semi-elasticity coefficient multiplied by 100, measures the percentage change in productivity induced by a unitary change in the I C variable. Source: Own Calculations based on ICs.

21

15. Quality, innovation and labor skills all have a significant positive impact on average productivity. Figure 8 shows the impact of average IC variables on average (log) productivity. The average impact of IC variables on productivity of Chilean f i r m s can be assessed by taking into account the elasticities and semielasticities of each variable measured at their sample mean (see Annex for details). For infrastructure the two most important factors affecting average productivity are power outages (-6.98 percent) and shipment losses (-6.91 percent). As far as business regulations are concerned, the cost of entry has the highest coefficient but it only represents -0.3 1 percent in terms of average productivity. Having a line of credit could account for 2 percent of average (log) productivity. Finally, with regard to quality, innovation and labor ski l ls , and staff with at least one year of university studies represents 6.51 percent of average productivity, despite presenting a very low coefficient (0.005), while having an experienced manager represents almost 30 percent of average productivity.

Figure 8. Average Productivity Impact (Gains and Losses) of Investment Climate Variables- Aggregate Level

%

Infrastructure

120

40

20

-20

-40

~i~~~~ Quality, Innovation and Other Control Variables Red Tape, Corruption and

Crime Labor s t i l l s

1.1 1.2 1.3 1.4 2.1 2.2 2.3 2.4 3.1 4.1 4.2 4.3 4.4 5.1 5.2 5.3 5.4 5.5 5.6

1.1 Days to clear customs to exports (log). 1.2 Average duration of power outages. 1.3 Shipment losses. 1.4 Internet page. 2.1 Security. 2.2 Number of inspections. 2.3 Cost of entry. 2.4 Absenteeism. 3.1 Financing Line Program.

4.1 R + D . 4.2 Internal training. 4.3 University staff. 4.4 Experience of the manager. 5.1 Incorporated company. 5.2 Foreign direct investment. 5.3 Exporter. 5.4 Capacity utilization. 5.5 Rent land. 5.6 Trade Union.

Source: Own Calculations. ICs data

16. I n addition, the investment climate affects the demand for labor and the prospects that a firm may become an exporter. The ICA supports the conclusion that that both exports and employment are directly and indirectly affected by the investment climate. A simultaneous equation model was employed to assess the impact of the investment climate on such factors as the probability of exporting, labor demand, the

22

probability of foreign direct investment and wages. In chapter 3 of volume 11, results are examined for exports and employment, two important objectives o f economic policy.

17. The conclusions of the econometric analysis are that investment climate significantly affects total factor productivity, the likelihood that firms will export and the labor demand in Chile. As mentioned before, Chile performs quite well in most investment climate indicators, compared to other countries. Notwithstanding this fact, there seems to be important areas in which reforms could significantly improve performance, including labor markets, access and cost of credit, and business regulation. In spite of the relatively good investment climate, the country could benefit from further improvements because indicators pertaining to a l l four areas are related to productivity, exports and labor demand.

18. ICA results seem to confirm that the increased emphasis on innovation, technology and skills i s appropriate. The econometric analysis reveals that technology, innovation and sk i l ls are particularly important for the productivity of f i r m s . These results are consistent with the perception of f i r m s that an insufficiency o f skilled labor i s one of the most severe obstacles to growth. This conclusion i s also important in light of the current concerns over equity in Chile. As discussed in previous World Bank reports, investments in education and returns to sk i l ls are interconnected and they constitute an area which might simultaneously help to address equality o f opportunity, human capital accumulation, innovation and growth.

19. The structure o f the report i s based on the four principal components of the investment climate: (i) finance; (ii) business regulation (including labor regulation); (iii) technology and innovation (including labor skills); and (iv) infrastructure. Finance and labor are key issues in the factor markets, while technology and innovation are the main drivers of economic growth. Infrastructure and business regulation can be either an obstacle or an engine of productivity and growth. Each one o f these areas i s analyzed below in more depth.

FINANCE

20. The financial system in Chile is the most robust in Latin America. The banking sector i s characterized by effective supervision, good capitalization and increasing sophistication of the participating institutions. Other sources of finance, including debt and equity markets, leasing and factoring companies and government finance programs provide further depth to the system. At the same time, a large pensions sector and a broad deposit base provide the system with an ample supply o f funds, far greater than that o f other Latin American economies. These factors result in a ratio of private-sector credit to GDP that compares very favorably with that of other economies in the region, and i s currently on a par with that of middle income countries (although considerably below that of European countries such as Ireland and Spain). After a significant contraction following the financial crisis in 1983, domestic credit to the private sector has been growing steadily since the early 1990s.

23

(%of GDP)

Domestic credit to private sector refers to financial resources provided to the private sector, such as through loans, purchases of non-equity securities, and trade credits and other accounts receivable, that establish a claim for repayment. For some countries these claims include credit to public enterprises. Source: World Bank WDI Database.

-Chile &High imome +Middie illcome +Latin Ametica

21. Financing of the corporate private sector i s highly dependent on bank credit, which has grown at a modest pace. The overall size of the banking sector’s credit portfolio has increased substantially over the past f ive years. However, this has been largely fuelled by growth in consumer credit and housing finance, while corporate credit has lagged behind. That i s due to the fact that large companies started to tap capital markets and external funding sources that offer cheaper finance than the domestic banking sector which, in turn, resulted in a significant reduction in bank lending. In addition, the banking sector has not been very active in seeking to increase lending to small and medium enterprises (SMES)~.

22. Funding through capital markets is largely closed to SMEs. The cost o f issuing domestic debt in Chile i s the highest among large Lat in American economies due, in part, to the stamp tax levied on financial transactions. As a result the smallest practical debt issue i s estimated at US$45 mi l l ion for domestic debt (US$200 mi l l ion for international issues), which was wel l above the financial capacity o f most Chilean f i rms. While many SMEs were listed in the stock market in the early 1990s, t h i s source o f funds has largely dried up for all but the largest companies, and n o new issues were made by SMEs from 1998 to 2004. That has been attributed to concerns over company profitability and deficiencies in corporate governance such as lack o f transparency and limited minority shareholder rights. By the same token, private equity i s s t i l l very limited,

The definition for firm size used in the present document corresponds to the standard World Bank classification based in the total number of permanent workers, Le. large (250+ workers); medium (50-249), small (16-49) and micro (<16). The sample covers establishments in nine industries and i s mainly concentrated in the manufacturing sector.

24

largely due to lack of interest of institutional investors following the poor track record of the sector.

23. Pension funds are the most important institutional investors in Chile, but their role as a source of finance is limited to large corporations. The investment portfolio of pension funds ( A F P s ) represents 70 percent of Chile’s GDP, making these funds the largest institutional investors, with a strong influence on the domestic debt and equity markets. However, their conservative investment requirements constrain the role of AFPs as direct suppliers of credit to private firms. In the bond market AFPs’ holdings are mostly concentrated on the highest-rated issues. Since AFPs build a buffer to protect against rating downgrades7, the universe of actual issuers i s limited to the very large f i rms. On the equity side, AFPs are allowed to invest only in companies listed as eligible. AFPs’ actual equity investments have been concentrated on the most liquid shares among those eligible, because investing in illiquid stocks could create price bubbles, or lock AFPs’ in their investments. A large proportion of the funds from AFPs to the private sector i s intermediated by banks, which receive considerable funding mainly through low-yield, short-term certificates of deposit acquired by AFPs. A judicious relaxation of the rigid investment regime of AFPs8, without undermining their financial integrity, may increase the flow of direct financing to the private sector although the impact would be gradual. Insurance companies, although smaller than the pension funds, also constitute important institutional investors, especially in instruments with longer term maturities.

24. Leasing and financial factoring appear to have considerable potential as sources of finance to the private sector, but their impact i s still very limited. The volume of leasing operations in Chile has grown substantially. In 2005, the leasing portfolio accounted for 4.3 percent of the total credit portfolio of banks, up from 2.1 percent in 1999. However, these operations appear to serve mainly large clients, while penetration into the SME sector i s s t i l l limited. By the same token, the volume of factoring transactions i s increasing although the industry i s s t i l l at an early development stage. There i s significant room for growth and competition, which would benefit clients. Proposed and recently introduced enhancements to the regulatory framework could help to expand the impact of both leasing and factoring as sources of finance to the private sector in Chile.

25. The Government of Chile participates actively in the provision of finance to the private sector. Banco Estado, a government-owned bank, i s the largest lender to smaller companies in Chile. I t focuses on those market segments that appear underserved by privately-owned commercial banks, such as small and micro enterprises, and f i r m s in higher-risk industries such as agriculture and fish farming. The government also provides financing indirectly through CORFO (a development entity that supports small and micro f i rms) and FOGAPE (a government fund that provides guarantees on loans to SMEs). The focus of FOGAPE and CORFO i s not particularly linked to innovative industries, but i s largely concentrated in domestic trade (both retail and wholesale) and on agriculture.

Since AFPs are not allowed to hold sub-inqestment grade bonds, holdings of debt rated at lower investment-grades creates the risk of substantial losses from illiquid bonds in case o f a downgrade. * For example, allowing a very moderate holding of sub-investment grade bonds, which would greatly reduce risks of holding lower investment-grade debt issues.

7

25

26. I f enacted, a proposed reform to the Capital Markets Law could strengthen the financial system. The proposed reform includes measures to improve corporate governance and enhance security for investors. It would strengthen the value o f a company’s collateral (especially important for smaller f i r m s that possess l imited assets to pledge as guarantees), and enhances prospects for the development of a venture capital sector.

27. Information gaps hamper access to credit, especially by SMJ3s. The inaccuracy and lack o f standardization o f financial information reported by SMEs has been cited as the reason why banks require collateral in order to lend. The introduction o f FECUPYME (a system that defines the reporting formats required for SMEs) in 2004 appears to be a step in the right direction. However, the full impact o f FECUPYME may take some time to materialize and so far i t s use has been very limited. Start-up requirements, the need to train companies in the use o f th i s reporting tool, and especially, the time required for banks to modify their credit processes are some o f the potential explanations for the limited use o f FECUPYME but there may be others that need to be investigated. At the same time, there may s t i l l remain issues related to the quality o f information because the accuracy and sufficiency o f the information self-reported by companies in the past has been questioned.

28. There i s plenty of short-term credit available, but collateral requirements constrain access to bank loans. Access to credit i s not just a question o f availability but also o f the terms and maturity needed by companies. While companies in Chile appear to have ample access to short-term credit, the availability o f longer term bank loans i s more restricted, and it does not appear to be strictly linked to the viability o f companies as measured by their profitability. Two major obstacles appear to limit access to longer-term credit. On the supply side there i s a lack o f transparency, especially among smaller companies, which impairs the ability o f banks to evaluate credit risk. Similarly, caps on interest rates can constrain the ability o f banks to correctly price credit to smaller f i rms . On the demand side, collateral i s an important consideration for banks to make credit available, and hence collateral requirements are perceived to be a major constraint for access to credit by companies surveyed.

29. Not surprisingly, firms in innovative industries find it more difficult to access credit. O n average, companies operating in industries that require constant innovation (e.g. biotechnology or IT) appear to have greater difficulty accessing bank loans than companies operating in more traditional industries. This may be explained by banks’ reliance on real estate as collateral. The assets o f f i r m s in innovative industries may be intangible (patents, software) and they may have a lower value as collateral. This problem i s exacerbated by the lack o f a wel l developed risk capital industry (which usually undertakes investments in innovative industries), and the l imited support f rom entities such as CORFO and FOGAPE. A recently created ‘Fund for Innovation and Competitiveness” may help to bridge the financing gap for these industries, fostering the development o f new forms o f venture capital.

26

Figure 10. Credit constraints by industry

Source: Investment Climate Survey Chile

Policy Recommendations

30. Enhance access to credit by underserved segments of the economy by mobilizing the positive experience with government programs. The guarantees program o f FOGAPE has facilitated access to credit for many companies that lack sufficient qualifying collateral. However, a significant proportion o f the guarantees are allocated to companies operating in retail and wholesale trade, while the data collected through the ICs shows that industrial sectors related to innovation face the most serious credit constrains. CORFO also supports a large number o f small and micro f i rms ' through second-tier financing and technical assistance. However, a large proportion of i t s operations" are concentrated in agriculture and livestock. I t would be helpful to review the economic sectors currently served by FOGAPE and CORFO in order to ensure that the government support targets those areas that a) are considered important for the economic development' in Chile, and b) are not already served by commercial financial institutions. Similarly, it would be useful to undertake an evaluation of the impact o f FOGAPE and CORFO's programs both in terms o f the benefit to client companies, and the effectiveness o f the programs as mechanisms to foster sustainable commercial financing to targeted sectors.

31. Enactment of the draft laws recently submitted to Congress would help enhance access to financing. The passing o f the Capital Markets 11 law would enhance the legal framework governing collateralized lending. I t would also facilitate access to credit by smaller prospective borrowers by enhancing the value of their collateral. Similarly, th i s law would probably make risk capital more readily available to SMEs (especially in areas related to innovation) by creating fiscal incentives for investors and enhancing the rules of corporate governance. B y the same token, the passing of another

Above 36,000 companies as o f March 2006. lo Estimated by the number o f companies, as opposed to the volume in monetary terms.

27

draft law that would create the legal framework for mobilizing reciprocal guarantees which could facilitate access to finance for SMEs. The establishment of a proposed central registry of mortgages and pledges could enhance the mobility of borrowers.

32. Facilitate the expansion of formal factoring services through a country-wide factoring platform. The untapped potential for financial factoring services appears high, given the number of prospective participants and the size of their portfolios. The new law on receivables (Ley de Titulo Ejecutivo de Fucturus) enacted in April 2005 significantly improves the viability of th i s service by enabling the electronic exchange of ownership of receivables and by strengthening their value in legal proceedings. The development of a country-wide financial factoring platform linking suppliers, factoring services and buyers such as that recently implemented by a development bank in Mexico may enhance significantly this industry by reducing risks and transaction costs while increasing competition.

33. Access to finance for smaller firms could be enhanced by a reform of the stamp tax and the cap on interest rates. The stamp tax has an important impact on the overall cost of credit and creates distortions in favor of loans with a longer maturity. Accordingly, the burden falls disproportionately on smaller companies, which have less access to long-term funding than larger ones. A tax reform that eliminated or decreased this tax rate could make it more attractive for small companies to seek credit. Eliminating the cap on interest rates could enhance the commercial appeal of micro borrowers for financial institutions. At the same time, the elimination of interest rate ceilings could enhance the interest of micro-entrepreneurs to work with financial institutions.

BUSINESS AND LABOR REGULATIONS

34. Chile ranks well in most indicators of business regulation. On the “time tax” - the time spent dealing with different government regulations - managers spend on average 7 percent of their time dealing with red tape and regulations. This i s comparable to Brazil, where f i r m s spend 8 percent of their time on regulations, considerably less than time spent in China and India (25 and 14 percent, respectively), but higher than Central European countries such as Poland, Slovakia and the Czech Republic. In fact, Chilean managers reportedly spend twice as much time as their Central European counterparts dealing with regulations (7.1 vs. 3.5 percent). The time tax i s important since - as well as quantifying one important aspect of the regulatory burden - it also tracks other measures of regulation and property rights. The higher the time spent on complying with regulations, the higher the probability that a firm wil l make unofficial payments during inspections or to obtain construction permits.

35. Obtaining different construction-related permits is a time-consuming business in Chile, and i s seldom possible on the internet. I t takes an average of more than one month to get a permit to build, and about one and a half months to get the certificate of receipt of construction premises. Of the f i r m s which built a new building or modified an existing one in the two years preceding the IC survey, 68 percent of them reported having applied for a permit to build. Chilean firms are well aware of the online procedures available to comply with government regulations. Some 99 percent of those

28

interviewed were aware of more than 40 online procedures available to comply with tax payments, labor regulations, electronic invoicing, etc.

Figure 11. The Time Tax: percent of senior management time devoted to government regulations, inspections, taxes, customs, etc.

China

India

South Africa

Brazil

Chile

Slovak Republic

Poland

Czech Republic

0.0 5.0 10.0 15.0 20.0 25.0

%

Source: ICs

Figure 12. Construction Permits are Relatively Time-Consuming 80

712 68 ,-

62 59

60 -

50 46

40 -

30 -

20 -

10 - 0.6 0.6

0 - Previous Information Minor Works Permit Construction permit Final reception certificate

Certificate

1 .Percentage applied Waiting time (days) W Used internet in application, % of firms c3 Bribe reported, 5% of firms 1 Source: World Bank Chile ICs

36. Chilean firms rank very well internationally according to sales which are reported for tax purposes (Figure 13). With 97 percent of sales reported to the tax authorities Chilean firms rank second only to Slovakia (98 percent) among comparator countries. The share of sales reported for taxation purposes i s presumably a

29

measure of the taxation burden and the efficiency of the tax administration system. The less complex the taxation system, with fewer exemptions and distortions, the better the compliance and the lower the opportunities to hide income (legally or illegally). Furthermore, the more efficient the collection, reporting and penalty system - the higher the degree of compliance. There i s not much variation in the share of sales reported by different types of f i r m s (classified by size and industry) - with al l f i r m s reporting between 96 and 98 percent of sales to the IRS. Therefore, the survey data suggest that there are no particular problems with the burden of corporate taxation - as perceived by the interviewed Chilean f i rms. However, tax rates are seen as problematic by 23 percent of interviewed f i r m s and are among the top five perceived constraints to business operation. In contrast, tax administration i s cited as a major or severe obstacle by only 14 percent of f i rms,

Figure 13. Percent of Sales Reported to Tax Authorities: A n International Comparison

97 Chile

South Afnca

Poland

I I I I I I I I I I

Brazil -61 I I China 5

/ / / / / / / / /

0 10 20 30 40 50 60 70 80 90 100

I

Source: ICs

37. One half of interviewed Chilean manufacturing companies express a strong degree of trust in the ability of the courts to defend their contractual and property rights. Confidence in the courts i s higher than in other comparator countries, and only a bit less than that expressed by Chinese ICs respondents (Figure 14). Conversely, only 14 percent of Chilean f i r m s distrust the courts - a share which i s the second lowest among the group of comparators. It i s also noteworthy that court users do not distrust the courts any more than non-users do. The share of either group that distrusts the courts i s a low 14 percent. The share of users that trust the courts i s lower than that of non-users (45 versus 52 percent), and the difference in means i s statistically significant at the 10 percent level. Court users are defined as f i r m s that report having been involved in a court case in the three years preceding the survey. Almost a third of manufacturing companies (31 percent) are court users according to t h i s definition, and so are 24 percent of surveyed non-manufacturing f i r m s .

30

Figure 14. Trust in the Judiciary: percentage of respondents who believe that the courts will uphold their contractual and property rights

7

_____

70 nn 58 -"

50

40 g

30

20

10

0 Czech Poland Slovak Brazil South India Chile China

Republic Republic Afr ica

38. Chilean firms make little use of the courts due to lengthy and unpredictable court proceedings. According to the 116 Chilean firms that filed a payment dispute in court in the 2 years preceding the survey, the average time to resolve a court case - from filing until judgment was issued -- was just over 40 weeks (or 281 days). Although t h i s i s half the number of days to resolve a payment case in a Brazilian court (Figure 15), it i s the second highest among the comparator group of countries. In Chile the survey revealed a wide range of outcomes. The duration of a court case over disputed payments ranges in Chile from 1 week to 104 weeks. In fact, almost a third of court users (3 1 percent) indicate that it took them at least one year or more to obtain a judgment.

Figure 15. Number of Days to Resolve a Payment Dispute in Court, by Country

-_

Chile

South Africa

Slovak Republic

Poland

China

Czech Republic 69

61 Russian Federation

0 100 200 300 400 500 600

days

39. In Chile - according to the ICs - in only 3 percent of cases did manufacturing firms require pre-payment from buyers for merchandize sold. This i s the lowest percentage of pre-paid sales among the comparator countries. For

31

example, the corresponding ratio for pre-payment i s 3 times higher for Czech manufacturing f i rms, and a 6 times higher in China. The share of sales paid at the moment of delivering merchandize in Chile i s also low by international standards, at 24 percent on average. In contrast, 56 percent of sales in China were paid at delivery. Consequently, the share of sales on credit i s very high in Chile - 73 percent of manufacturing sales were made on credit, i.e. with deferred payment by the buyer. This figure i s comparable to Brazil, and higher than other comparators. One possible interpretation of the relatively low usage of pre-payment and payment on the spot i s that f i r m s in Chile are more confident that they would eventually be able to collect their debts in the case of non-payment by the buyer.

40. Closing a business when faced with insolvency ranks as the most difficult aspect of the business environment in Chile according to the “Doing Business in 2007” database. There are important reforms under way, such as amendments to the Bankruptcy Law from 2005. Chile ranks 107” among 175 countries on the Closing a Business index -- worse than Poland, Slovakia, South Africa and China. Estimates indicate that it takes on average 5.6 years to close an insolvent company, at a cost of 15 percent of the value of the estate. For every dollar invested in the company, creditors may recover 20 cents. The low overall ranking in terms of Closing a Business i s largely explained by the slow process of insolvency proceedings - on which aspect alone Chile ranks 89* among 174 countries for which data are available. The duration of insolvency proceedings in Chile i s well above the 2.6-year average for LAC countries.

41. Labor market regulations are seen as a possible explanation for the behavior of the labor market, which did not follow macroeconomic performance. In Chile, the literature has highlighted two problem areas: one i s the institutional framework for wage setting, comprising both the minimum wage policy and backward looking schemes of wage readjustment. These two mechanisms have been blamed for the downward rigidity of real wages (Cowan, Micco and PagCs, 2004). The second problem relates to provisions for job security, especially firings costs, which are usually associated with a slow adjustment of the Chilean labor market to shocks.

42. Chile’s statutory minimum wage and long-term price-indexed wage contracts became increasingly binding in the years following the Asian crisis in 1997. Two studies covering the period to 2000 find that these two policies explained Chile’s slow adjustment to economic shocks of the late 1990s.” Infante, Marinakis, and Velasco (2002) compared trends in the real minimum wage with productivity and real average wages from 1990 to 2001 (Figure 16). Until 1998, the trends are similar. Starting in 1999, a gap favoring the minimum wage emerged, widening in the subsequent years to reach 17.1 percent in 2001. From ENIA data it can be seen that labor costs rose above the productivity trend (Figure 17) between 1996 and 1999 in the manufacturing sector, but the gap has been reduced more recently as productivity starts to pick up. Minimum wage regulations can also exacerbate inequity because some groups of unskilled workers,

l1 For more details, please, see Cowan, Mizala, Micco, Pages, and Romaguera (2003); and Cowan, Micco, and Pages (2004).

32

especially the youngest, are likely to be worse off in terms of employment, while others are better off in terms of income.

Figure 16. Chile: Minimum Wage, Mean wage and Productivity

1990-2001

Index

200

180

180

140

12Cl

1W

BU

- A 147.9 ?

we0 isgt 1.w 1083 1884 IQM 1006 i e w ~ B B B IQW 2wo 2001

Source: Infante, Marinakis and Velasco (2002)

Figure 17. Productivity and Labor Cost in Manufacturing

130

120

8 110 5-

@ 100

J - c 90 U

80

70 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

+Real value added per employeeday --.C Levinsohn-Petrin TFP estimate, value added-based + OLS TFP estimate, value added-based i - Total labor cost per employee-day -- Total labor cost per employee-day: unskilled -+T- Gross output per employee-day

Source: Own Calculations based on ENIA

33

43. The ICs indicates that firms see labor legislation, especially firing restrictions, as having a significant impact on the size of a firm's labor force. The ICs helps identify which aspect of labor regulation impacts most strongly on firms. ICs data show that 27 percent of f i r m s would l i ke to change the size of their labor force, while keeping constant the level of output. Among the 21 percent who wish to hire more people, 59 percent identify higher firing costs as a constraint to making the adjustment. This i s a greater issue than lack of flexibility in working hours (19 percent), minimum wages and obligatory benefits (10 percent) or union pressure (2.4 percent). Even though labor costs are felt principally when a worker i s fired, f i r m s cite that legislation i s a greater barrier to hiring workers. Similarly, of the 6 percent of f i r m s that wish to reduce the size of the labor force, nearly 77 percent cited firing restrictions. This result i s in l ine with a growing literature on labor market issues in Chile that identifies firing restrictions as one of the rigidities that affect labor market outcomes in Chile.I2

Figure 18. M a i n Reasons for not changing the Size of the Labor Force

High Firing Costs Deter Changes in Number of Permanent Employees

90 80 70 60 50 40 30 20 10 0

77

19

6 5 10

0

High firing costs Lack of flexibility High minimum Other laws and Others in working hours , salary and/or regulations about

obligatory contracting and benefits firing of workers

I Top reason to not increase current employment even if desired I Top reason to not decrease current employment even if desired

Source: ICs

Policy Recommendations

44. Chile has already made substantial efforts in making its national business environment conducive to opening and operating a business, especially in making government procedures available online and allowing for more transparency in the process of business regulation. As a result, Chile ranks 28' among 175 countries on the index of Ease of Doing Business (Doing Business in 2007). For instance, with respect to business registration - a process which tends to be time-consuming, procedurally burdensome and expensive in a number of comparator countries - Chile ranks 32nd. The

l2 See Gatica and Romaguera (2006), as well as Cowan and Micco (2006).

34

27 days needed to complete 9 procedures puts Chile above some OECD countries such as Switzerland and Belgium. Despite these very favorable international rankings, it i s worth noting that certain registrations - such as sanitary authorization or municipal licenses - are s t i l l rather time-consuming, taking more than 1 month to accomplish. Online compliance with those procedures i s very low - compared with the filing and payment of taxes, for example. One possible improvement may be to expand the use and the efficiency o f online procedures, and to provide more extensive public information about existing ones, which are underused at present (e.g. health permits by SESMA and ISP, registrations with the Labor Directorate, registration of trademarks with the Department of Industrial Property, etc.).

45. Problems remain in the area of construction permits - such as relatively long waiting times - and the Government could reduce those problems through better use of online processes. At present, less than 5 percent o f applicants for construction permits and licenses make use of online processes to get them.

46. In terms of labor regulation, redesigning the job security scheme seems to offer good prospects for increasing employment. The I C A reinforces the view that firing costs are the most important constraint for f i r m s in Chile as far as labor regulations are concerned. An option to be considered, as suggested in recent document^'^, would be to reduce the severance-payment component and to increase other components. This would maintain the overall amount of job security while avoiding distortions in f i r m s ’ hiring and firing decision^.'^

INNOVATION

47. Despite significantly better incentives regime and an improved infrastructure for innovation, international comparisons suggest that the country st i l l has relative weaknesses in the areas of education and capacity for innovation. The World Bank Knowledge Economy Index shows that Chile has an outstanding performance in the economic and incentive regime. Thus, compared to countries with similar levels of income, Chile gets very high marks for the quality o f regulations, the supervision of financial institutions, the degree of competition in the domestic market, and the prevalence of the rule of law (see upper right quadrant o f figure 19). Chile’s performance with regard to the infrastructure for innovation i s also outstanding, as confirmed by the development of electronic government, the use o f computers and the internet, and the investments in telecommunications (upper left quadrant o f figure 19). In contrast, the country underperforms in most indicators of innovative capacity (lower left quadrant) and human capital development (lower right quadrant). While some o f the corresponding indicators are potentially controversial - e.g. one could argue that having a low

l3 See (World Bank 2005), as well as Gatica and Romaguera (2006). As stated in this last paper (page 13), “. . ..parece razonable promover en el futuro una reforma que aumente progresivamente el seguro desempleo, a la vez que reduzca y mejore el disefio de las indemnizaciones.”

As mentioned by Fajnzylber and Reyes (2005), the benefits provided through the unemployment insurance mechanism introduced in 2002 are much smaller than mandatory severance payments. Workers that have been employed for less than a year - about 36 percent o f all salaried, as per the 2003 CASEN survey - are not eligible for severance payments.

14

35