Embed Size (px)

Citation preview

8/6/2019 Report Communication

http://slidepdf.com/reader/full/report-communication 1/24

Chapter-1

1.1 Introduction of the report:

The word ‘Bank’ is derived from the word ‘Bank’ or ‘Banquet’. Bank or

Banquet means a bench. The early bankers transected their money leading

activities sitting on the benches in a market place. According to others, the

word ‘Bank’ is originally derived from the German word ‘Back’ meaning a

joint stock fund. However, the term ‘Bank’ has been in use from the Middle

Ages in connection with the business of money leading.

Originally, `Banker’ or ‘Bank’ was defined as a person who carried on business

of receiving money, collecting of drafts, honoring checks drawn upon it. Over

the years the banking business has undergone many changes and now it covers

a wide range of activities. According to modern concept, banking is a business

which deals with borrowings, leading and remittances of fund as well as many

ancillary businesses connected thereto.

Modern banks play an important part in promoting economic development of a

country. Banks provide necessary funds for executing various programs

underway in the process of economic development. They collect savings of

large masses of people scattered through out the country, which in the absence

of banks would have remained ideal and unproductive. These scatteredamounts are collected, pooled together and made available to commerce and

industry for meeting the requirements. Economy of Bangladesh is in the group

of word‘s most underdeveloped economies. One of the reasons may be its

underdeveloped banking system. Government as well as different international

organizations have also identified that underdeveloped banking system causes

some obstacles to the process of economic development. So they have highly

recommended for reforming financial sector. Since 1990, Bangladesh

1

8/6/2019 Report Communication

http://slidepdf.com/reader/full/report-communication 2/24

Government has taken a lot of financial sector reform measurements for

making financial sector as well as banking sector transparent, formulation and

implementation of these reform activities has also been participated by

different international organization like World Bank, IMF etc.

1.2 Objective of the report:

The main objective of education is to make a complete man. No knowledge

becomes complete without practical exposure. To acquire knowledge

completely we must do some practical applications of it in addition to

theoretical knowledge. Thus the objectives of the report are:

1. To make myself more confident and active in future to handle my job.

2. To know about the Previous & present banking system of National Bank

Limited.

1.3 Methodology:

The methodology of the report includes direct observation, oral communication

with the employees of all departments of Mirpur Branch, studying files,

circulars etc and practical experience. The report includes both quantitative as

well as qualitative data. To make the report more meaningful and presentable,

two sources of data and information have been used as follows:

• Primary Sources of Information• Secondary Sources of Information

1.3.1. Primary Sources of Information:

Primary data are collected from the respective officers of various desk and files

studies.

2

8/6/2019 Report Communication

http://slidepdf.com/reader/full/report-communication 3/24

1.3.2. Secondary Sources of Information:

The Secondary Sources of Information are:

• Annual Report of NBL• Website of NBL.

1.4 Limitation of the Report:

Every thing has its limitations. My report is not also out of weakness. For some

certain causes, I could not effort to conduct my report properly. I have

considered the following causes as the limitations of the study. This Bank has

some policy for not disclosing some data and information for obvious reasons

that could be very much essential.

3

8/6/2019 Report Communication

http://slidepdf.com/reader/full/report-communication 4/24

8/6/2019 Report Communication

http://slidepdf.com/reader/full/report-communication 5/24

National Bank Limited was born as the first hundred percent Bangladeshi

owned Bank in the private sector. From the very inception, it was the firm

determination of National Bank Limited to play a vital role in the national

economy. We are determined to bring back the long forgotten taste of bankingservices and flavors. We want to serve each one promptly and with a sense of

dedication and dignity. The then President of the People's Republic of

Bangladesh Justice Ahsanuddin Chowdhury inaugurated the bank formally on

March 28, 1983 but the first branch at 48, Dilkusha Commercial Area, Dhaka

started commercial operation on March 23,1983. The 2nd Branch was opened

on 11th May 1983 at Khatungonj, Chittagong.

At present, NBL has been carrying on business through its 131 branches spread

all over the country. Since the very beginning, the bank has exerted much

emphasis on overseas operations and handled a sizable quantum of home

bound foreign remittance. It has drawing arrangements with 415

correspondents in 75 countries of the world, as well as with 37 overseas

Exchange Companies located in 13 countries. NBL was the first domestic bank

to establish agency arrangements with the world famous Western Union in

order to facilitate quick and safe remittance of the valuable foreign exchanges

earned by the expatriate Bangladeshi nationals.

This has meant that the expatriates can remit their hard-earned money to the

country with much ease, confidence, safety and speed. NBL was also the first

among domestic banks to introduce international Master Card in Bangladesh.In the meantime, NBL has also introduced the Visa Card and Power Card.

The Transparency and accountability of a financial institution are reflected in

its Annual Report containing its Balance Sheet and Profit & Loss Account. In

recognition of this, NBL was awarded Crest in 1999 and 2000, and Certificate

of Appreciation in 2001 by the Institute of Chartered Accountants of

Bangladesh. The bank has a strong team of highly qualified and experienced

5

8/6/2019 Report Communication

http://slidepdf.com/reader/full/report-communication 6/24

professionals, together with an efficient Board of Directors who play a vital

role in formulating and implementing policies.

2.2 Vision of National Bank Limited:Ensuring highest standard of clientele services through best application of latest

information technology, making due contribution to the national economy and

establishing ourselves firmly at home and abroad as a front ranking bank of the

country have been our cherished vision.

2.3 Mission of National Bank Limited:

Our mission is to continue our support for expansion of activities at home and

abroad by adding new dimensions to our banking services which have been

ongoing in an unabated manner. Alongside, we are also putting highest priority

in ensuring transparency, account ability, improved clientele service, as well as

our commitment to serve the society through which we want to get closer to the

people of all strata. Winning an everlasting seat in the hearts of the people as a

caring companion in uplifting the national economic standard through

continuous up gradation and diversification of our clientele services in line

with national and international requirements is the desired goal we want to

reach.

2.4 Function of National Bank Limited:

• To maintain all types of deposit A/Cs.

• To make investment.• To conduct of reign exchange business.

• To conduct other Banking services.

• To conduct social welfare activities.

• To work for continues business innovation and improvements.

• To bui1d up strong-based capita1ization of the country.

• To ensure the best uses of its creativity, well disciplined, well manages and

perfect growth.

6

8/6/2019 Report Communication

http://slidepdf.com/reader/full/report-communication 7/24

Chapter-3

3.1 Deposit Collection:

Deposit is the lifeblood of a bank. From the history and origin of the bankingsystem. We know that deposit collection is the main function of a bank.

3.1.1 Accepting deposits:

The deposits that are accepted by NBL like other banks may be classified in to-

a) Demand Deposits b) Time Deposits

3.1.2 Demand deposits:

These deposits are withdrawn able without notice, e.g. current deposits. National Bank Limited accepts demand deposits through the opening of, -a) Current account

b) Savings accountc) Call deposits from the fellow bankers

3.1.3 Time deposits:

A deposit which is payable at a fixed date or after a period of notice is a timedeposit.

National Bank Limited accepts time deposits through Fixed Deposit Receipt(FDR), Short Term Deposit (STD) and Beard Certificate Deposit (BCD) etc.

While accepting these deposits, a contract is done between the bank and thecustomer.

When the banker opens an account in the name of a customer, there arises acontract between the two. This contract will be valid one only when both the parties are competent to enter into contracts. As account opening initiates thefundamental relationship & since the banker has to deal with different kinds of

persons with different legal status, National Bank Limited officials remain verymuch careful about the competency of the customers.

7

8/6/2019 Report Communication

http://slidepdf.com/reader/full/report-communication 8/24

3.2 Deposits beehives of last five years:Deposits 2005 2006 2007 2008 2009Current

deposit& other

account

5,157,689,93

4

6,178,409,30

0

8,24,747,03

2

8,782,589,42

0

10,398,061,3

33

Bills

payable

455,124,300 665,728,459 1,343,146,1

24

1,23,527,712 1,285,541,18

3Savings

bank

deposit

8,002,250,85 10,023,258,1

2

11,423,416,

26

13,233,056,2

41

16,509,865,8

13

Fixeddeposits

13,305,103,800

15,502,105,700

17,608,092,14

24,554,075,165

31,605,724,061

Term

deposits

6,856,411,00

1

7,965,541,73

3

9,322,999,8

93

12,364,361,5

12

17,023,623,5

97Bearer

certificat

es of

deposit

15,825,000 15,825,000 15,825,000 15,825,000 15,825,000

3.2.1. Chart of deposit behavior

8

8/6/2019 Report Communication

http://slidepdf.com/reader/full/report-communication 9/24

0.00

10,000.00

20,000.0030,000.00

40,000.00

50,000.00

60,000.00

70,000.00

80,000.00

2005 2006 2007 2008 2009

deposits

Diagram: Deposits beehives of last five years

3.2.3. Table showing Deposits beehives of last five years

Deposits 2005 2006 2007 2008 2009Total

Deposits

32,984.05 40,350.87 47,961.22 60,187.89 76,838.64

3.3. Credit creation:

9

8/6/2019 Report Communication

http://slidepdf.com/reader/full/report-communication 10/24

As a continued process National Bank Ltd, followed the course of its own

credit policy within the framework and guidelines outlined by the Government,

Bangladesh Bank and Head office of National Bank Ltd. in respect of

deployment of its loan able fund. The Bank continued to explore and diversifythe area of its operation to extend credit facilities throughout the year to the

various productive sectors on priority basis.

3.3.1. Corporate Banking:Letter of Credit (LC), Letter of Guarantee (LG). Overdraft, Short Term Loan,

Lease Finance, Loan Against Trust Receipt (LATR), Work Order Finance,Emerging Business, Syndication, Term Loan, Project Finance, Bill Purchase,

Bank Guarantees.

3.3.2. Major Types of Loans and Advances:a) Home Loan

b) SME Loan

c) Consumer Loan

d) Trade Finance

10

8/6/2019 Report Communication

http://slidepdf.com/reader/full/report-communication 11/24

3.4 Credits of last five years

credits 2005 2006 2007 2008 2009Loans &

Advances

27,020.21 32,709.68 36,475.74 50,665.07 65,129.29

Provision

for

Unclassifiedloans

251.13 307.43 514.91 784.91 959.91

Provision

for

Classified

loans

716.07 854.18 947.74 1,121.76 1,195.86

Note: Taka in million.

3.4.1. Chart of loans & advances

11

8/6/2019 Report Communication

http://slidepdf.com/reader/full/report-communication 12/24

Overdrafts

Lease Finance

Home Loan

SME Loan

Consumer Loan

Trade Finance

3.4.2 Table showing Loan & Advance in different field

Loan &

Advance

Overdrafts Lease

Finance

Home

Loan

SME

LoanConsumer Loan

Trade

Finance2009 15372.9 12810.8 10248.6 7686.47 5124.31 5124.31

3.5 Income of National Bank Ltd:

12

8/6/2019 Report Communication

http://slidepdf.com/reader/full/report-communication 13/24

Income is essential for any kind of business National Bank Ltd earned profit by

their investment and the operating income of interest receivable, income on

investment, commission, exchange, & other incomes, at a glance with

comparing the actual result of previous year and the budgeted figure for thenext coming year which is distributed into two quarters.

3.5.1 Interest Income :

Income through the operating income of interest receivable, income on

investment .

3.5.2. Non –Interest Income:

Income through commission, exchange, & other incomes .

13

8/6/2019 Report Communication

http://slidepdf.com/reader/full/report-communication 14/24

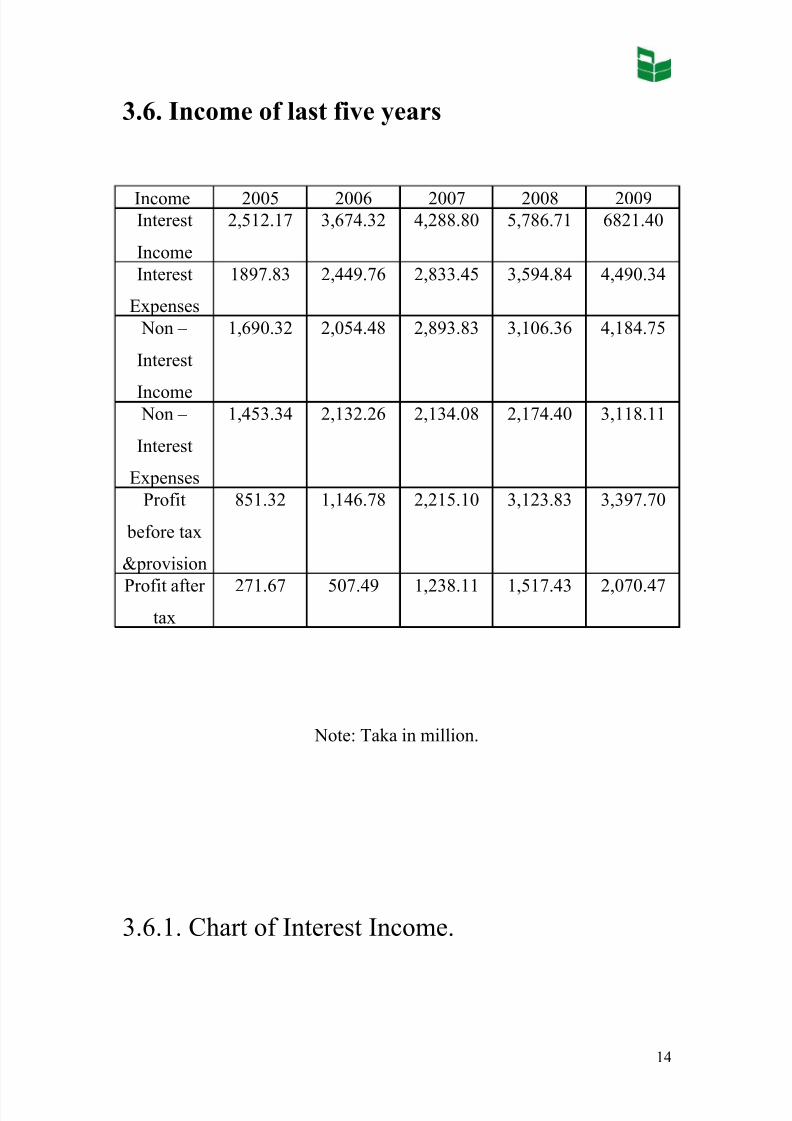

3.6. Income of last five years

Income 2005 2006 2007 2008 2009Interest

Income

2,512.17 3,674.32 4,288.80 5,786.71 6821.40

Interest

Expenses

1897.83 2,449.76 2,833.45 3,594.84 4,490.34

Non –

Interest

Income

1,690.32 2,054.48 2,893.83 3,106.36 4,184.75

Non –

Interest

Expenses

1,453.34 2,132.26 2,134.08 2,174.40 3,118.11

Profit

before tax

&provision

851.32 1,146.78 2,215.10 3,123.83 3,397.70

Profit after tax

271.67 507.49 1,238.11 1,517.43 2,070.47

Note: Taka in million.

3.6.1. Chart of Interest Income.

14

8/6/2019 Report Communication

http://slidepdf.com/reader/full/report-communication 15/24

0.00

1,000.00

2,000.00

3,000.00

4,000.00

5,000.00

6,000.00

7,000.00

2005 2006 2007 2008 2009

income

expenses

Diagram: Interest Income &Expenses of last five years

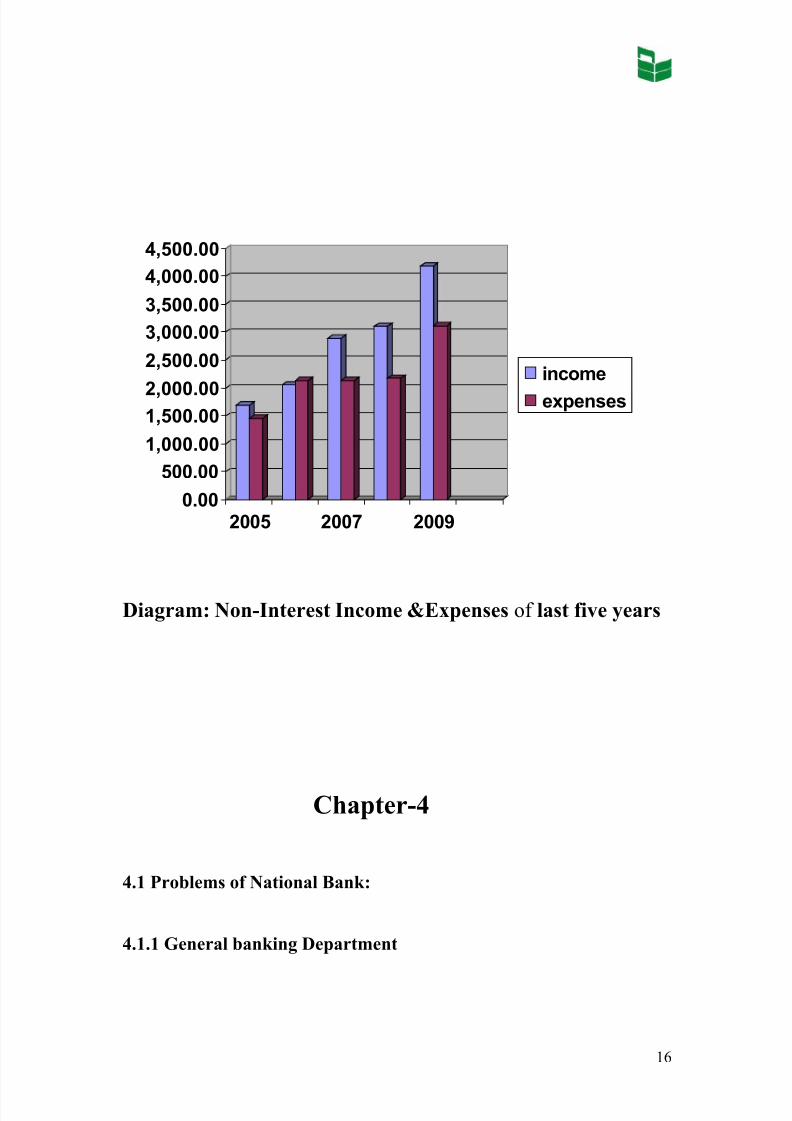

3.6.2. Chart of Non-Interest Income.

15

8/6/2019 Report Communication

http://slidepdf.com/reader/full/report-communication 16/24

0.00

500.001,000.00

1,500.002,000.00

2,500.00

3,000.003,500.00

4,000.004,500.00

2005 2007 2009

incomeexpenses

Diagram: Non-Interest Income &Expenses of last five years

Chapter-4

4.1 Problems of National Bank:

4.1.1 General banking Department

16

8/6/2019 Report Communication

http://slidepdf.com/reader/full/report-communication 17/24

• In general banking department they follow the traditional banking system, the

entire general banking procedure is not fully computerized.

• They are not using Data Base Networking in Information Technology (I)

Department. So they have to transfer data from branch to branch and branch tohead office by using floppy disk and sure it is not a good system.

• According to some clients opinion introducer is one of the problems to open

an account. If a person who is new of the city wants to open account, it is a

problem for him/her to arrange an introducer of SB or CD accounts holder.

4.1.2 Loans and Advances Department:

NBL uses numerical credit scoring model.

Sanction of all types of loan of NBL increasing day by day.

NBL loan business is really good than the other bank.

NBL time of repayment of installment is not sufficient for the

clients.

NBL want much more condition from the other bank.

NBL have the opportunity to introduce other types of loan likestudent loan, Teacher loan and agriculture loan etc.

The amount of NBL house loan is much lower than other bank.

Rate of interest of NBL is moderate.

Refinancing of household loan is moderate comparing to others

bank

NBL providing much higher car loan to the other bank.Down payment of car loan is very much lower.

NBL travel loan is much lower than other bank.

Down payment of travel loan is required for the NBL

The maximum amount of education loan is much lower than

other bank.

Rate of interest of education loan is moderate to the other bank

and it is vary comfortable to the other client.

17

8/6/2019 Report Communication

http://slidepdf.com/reader/full/report-communication 18/24

4.1.3 Other Problem:

• National Bank doesn't give their attention on advertisement. As a competitionmarket it is too much important for any organization to increasing their

advertisements procedure.

4.2 Recommendation:

4.2.1General Banking Department:

• If the enter general Banking system is fully computerized then they satisfy the

customer by provide fast service.

• If they establish networking system with their branches then it can easily

transfer data within short time.

• If they cancel the introducer system then they can collect more deposit

through new account and it also satisfied the customer.

4.2.2 Loan and Advance Department:

Interest rate should be decreased.

They should refinancing 100% of loan amount.

Down payment may be stopped for taking advantages to the other bank

They should offer some other types of loan. I.e. Student loan, Teacher

loan, Agriculture loan.

The clients of loan should be facilitated with online bank and other

benefits.

National Bank Ltd. should upgrade its website regularly and providing

details information of loan scheme.

The amount of household loan should be increased.

18

8/6/2019 Report Communication

http://slidepdf.com/reader/full/report-communication 19/24

For the successful handling of loan operation, proper monitoring and is

essential. Customer’s information should be uploaded regularly for the

proper supervision and monitoring.

The bank may also promote loan operation through different advertising.

The bank may charge flat interest rate to get a comparative advantages

over other bank.

The bank should requite some energetic executives to ensure timely

recovery of disbursed of loan.

4.2.3 Foreign Exchange Department:

• In Foreign Exchange Department it is require communicating with foreign

bank frequently and quickly. To make the process easy and quick the whole

system should be computerized and modern communication media for example

e-mail, fax, Internet should be used.

4.2.4 Other Problem:

• National Bank should give more attention to advertisement to create more

attraction among their customer, which is collect, more deposit and increase

investment scope.

4.3 Conclusion:

19

8/6/2019 Report Communication

http://slidepdf.com/reader/full/report-communication 20/24

We moved a long way from the time when the banks were deposit taking and

money-lending institution. The old concepts, attitudes and methods in banking

have undergone a marked change all over the world. Modern Banking is anoutcome development driven by changing financial activities and lifestyle.

Bangladesh has not lagged behind. Banks are required to participate in the

nation building activities and act as agent for bringing about socioeconomic

changes.

Reference:

National Bank Limited (2009), “ History of NBL” , Retrieved as December

05, 2009, from

www.nblbd.com. National Bank Limited (2009), “ NBL Products” , Retrieved as December

13, 2009, from

www.nblbd.com.

National Bank Limited (2009), “ Annual report” 2007-2008 , National

Bank Limited, Dhaka,

Bangladesh.

Appendix:NATIONAL BANK LIMITED

20

8/6/2019 Report Communication

http://slidepdf.com/reader/full/report-communication 21/24

Deposit Interest RateCircular Letter No. 2760

September 29, 2009.

3.5-2 Books and Ledger maintain by3.5-2 Books and Ledger maintain by Mirpur Branch(See theBranch(See the appendix)appendix)

Sl No Particulars Of Statement1 Marginal Deposit A/C

SlNo.

Category of Deposit Deposit Interest RateEffect from Oct. 01, 09

Remarks

1. Savings 4.50%2. Short Term Deposit: 1.00%

For Financial Institution and NonBank Financial Institution

4.00%

For Institutional deposit other thanFinancial Institute and Non-Banking Financial Institute(irrespective of slab/amount)

3.00%

3. FDR for 1 month and above butless than 3 months

4.50%

4. FDR for 3 months and above but less than6 months

Below25.00 7.50%25.00 lac & above 7.75%1.00 core & above 8.00%

5. FDR for 6 months & above but less than 1 year

Below25.00 7.50%25.00 lac & above 7.75%3.00 core & above 8.00%

6. FDR for 1 year and above Below25.00 7.50%25.00 lac & above 7.75%3.00 core & above 8.00%

21

8/6/2019 Report Communication

http://slidepdf.com/reader/full/report-communication 22/24

2 Summation & Balance Of Ledger 3 Fixed Deposit A/C4 Short Term Deposit A/C5 Call Deposit A/C6 Statement Of Demand Bill For Collection Outstanding7 Statement Of Usence Bill For Collection Outstanding8 Suspense A/C9 Sundry Deposit A/C10 Payment Order A/C11 Cash Certificate12 Statement Of Unclaimed Deposit13 Profit & Loss Entries14 Analysis Of Expenditure A/C (Revised)15 Closing Balance Of General Ledger(After Passing Of Closing Entries)16 Statement Of Dead Stock Article Supplied Vide Instruction Circular No.136

Dt.30-07-9717 Statement Of Stamps A/C18 Statement Of Interest Received & Paid19 Income Receivable A/C (Adjusting A/C Dr. Balance20 Unpaid Expenses A/C (Adjusting A/C Cr. Balance)21 Detail Statement Of Bank Guarantees Issued22 Branches Statistic23 Statement Showing The SHB Loan24 Cash Credit (Pledge)25 Cash Credit (Hypothecation)26 Overdrafts27 Loan A/C28 Inland Bills Purchased & Discounted29 Demand Drafts Purchased30 Postested Bills A/C31 Annual Return Of Particulars Of Advances.32 Suit Filed By The Bank 33 Suit Filed Against The Bank 34 Ancillary Statement-1 Relating To Particulars of Advances35 Ancillary Statement-11 Relating To Particulars Of Advances36 Ancillary Statement-111 Relating To Particulars Of Advances

37 Statement Of Interest Suspense A/C38 Advance Deposit And Advance Rent A/C39 Payment & Security Deposit A/C40 Drafts Payable A/C41 Statement Of Certificate Of Stock Of Stationary42 Stamped Certificate Of Balance With Other Banks (With Reconciliation

Statements)43 Statement Of Outstanding Foreign Import Usance Bills Received For

Collection.44 Revaluation Statement Of Foreign Currency Notes On Hand.45 Statement Of Contingent Liabilities As On 31-12-2002.46 Statement Of Import Letter Of Credits Outstanding.

22

8/6/2019 Report Communication

http://slidepdf.com/reader/full/report-communication 23/24

47 Statement Of Balance With Foreign Correspondent.48 Statement Of Export L/Cs Confirmed On Behalf Of Correspondents

Outstanding49 Statement Of Pad Outstanding.50 Statement Of Foreign Bills Purchased/Negotiated Outstanding.51 Statement Of Overdraft/Advances Against Export Bills Sent For Collection

Outstanding.52 Statement Of Packing Credit/OD Export Outstanding.53 Statement Of Lim.54 Statement Of Deposit Insurance Scheme For The Half Year Ended On 31 st

December 2002.55 Statement Of Depreciation Of Dead Stock Articles.56 Forward Sales Outstanding.57 Forward Purchased Outstanding58 Borrowing From Foreign Banks Outstanding

59 Outstanding Foreign Bills Rediscounted60 Wage Earners Development Bond.61 Statement Of Loans & Advances & Recovery Against Classified Loans &

Advances.62 Statement Of Advances By Lending Categories.63 Statement Of Loan & Advances Analysis Of Maturity Grouping.64 Statement Of Loan & Advances Analysis Under Board Categories.65 Statement Of Loan & Advances Analysis Under Significant Concentration

66 Statement Of Deposit Analysis(FDR,DPS,BCD,STD,BSCD,CA(CR),CC(CR),LA (CR), NECD Other Deposit Of Maturity Grouping.

Glossary:

AD : Authorize Dealer A/C : Account

23

8/6/2019 Report Communication

http://slidepdf.com/reader/full/report-communication 24/24

![UNISEL Nonverbal Communication: Communication Skill Assigment Report [COMPLETE]](https://img.dokumen.tips/doc/110x75/544df13bb1af9f2b638b4b66/unisel-nonverbal-communication-communication-skill-assigment-report-complete.jpg)