Embed Size (px)

Citation preview

REDUCING REPORTING BURDEN ON EUROPEAN CORPORATIONS

Standard formats and IASCF-XBRL taxonomy

An experience from the European Commitee of Central Balance Sheet Data Offices (ECCBSO)

Manuel OrtegaHead of the Central Balance Sheet Data Office DivisionChairman of the IIIWG of the ECCBSO

10th XBRL International Conference

Brussels

17th November 2004

2STATISTICS AND CENTRAL BALANCE SHEET DATA OFFICE DEPARTMENT

REDUCING REPORTING BURDEN ON EUROPEAN CORPORATIONS

DO WE HAVE A PROBLEM OF COMMUNICATION?

YES

Standard formats and IASCF-XBRL taxonomy An experience from ECCBSO

3STATISTICS AND CENTRAL BALANCE SHEET DATA OFFICE DEPARTMENT

REDUCING REPORTING BURDEN ON EUROPEAN CORPORATIONS

QUESTION TO COMPANIES:

GORGED WITH STATISTICS, QUESTIONNAIRES AND SURVEYS?

YES

– Cost

– Redundancy

Standard formats and IASCF-XBRL taxonomy An experience from ECCBSO

4STATISTICS AND CENTRAL BALANCE SHEET DATA OFFICE DEPARTMENT

REDUCING REPORTING BURDEN ON EUROPEAN CORPORATIONS

QUESTION TO STATISTICIANS, INVESTORS, LENDERS, OTHER USERS:

ARE YOU REALLY DISAPPOINTED WITH INFORMATION RECEIVED?

YES

– Cost

– Inadequacy

– Lack of comparability

Standard formats and IASCF-XBRL taxonomy An experience from ECCBSO

5STATISTICS AND CENTRAL BALANCE SHEET DATA OFFICE DEPARTMENT

REDUCING REPORTING BURDEN ON EUROPEAN CORPORATIONS

FAITH AND HOPE, TO COMBINE BOTH POLES OF COMMUNICATION

IFRS: an option for homogeneization

XBRL: an opportunity for connecting supply and demand of information

Standard formats and IASCF-XBRL taxonomy An experience from ECCBSO

6STATISTICS AND CENTRAL BALANCE SHEET DATA OFFICE DEPARTMENT

REDUCING REPORTING BURDEN ON EUROPEAN CORPORATIONS

SOME LIMITS AND DANGERS. ABOUT IFRS:

-A common accounting system is needed, but

-What will happen with SME?

-Comparability inside countries

-Are IFRS biased towards a group of users (investors)?

-Some figures:

Standard formats and IASCF-XBRL taxonomy An experience from ECCBSO

Agents Employment (2)

Number Percentage Number PercentageAll legal forms 10.758.372 100,00 38.442.981 100,00Personally owned 5.995.513 55,73 8.172.856 21,26Corporations 4.789.859 44,52 30.270.125 78,74

of which, quoted corporations 3.816 0,04 na na(1) Data available for Denmark, Finland, Italy, Luxemburg, Norway, Portugal, Spain, Sweden and United Kingdom.

(2) Data not available for United Kingdom.

Eurostat and European Securities Exchange Statistics.

Non-financial enterprises

in Europe (9 countries) (1)

7STATISTICS AND CENTRAL BALANCE SHEET DATA OFFICE DEPARTMENT

REDUCING REPORTING BURDEN ON EUROPEAN CORPORATIONS

SOME LIMITS AND DANGERS. ABOUT XBRL:

-Regulators are becoming prepared for XBRL in Europe. Are companies prepared too?

-Easy access? It depends on the integration of the information in companies

TWO NEEDS:

-Continue with standard formats until XBRL is sufficiently used by corporations

-Involve IT corporations, which develop accounting software for SME, in order to assure a rapid use of XBRL

Standard formats and IASCF-XBRL taxonomy An experience from ECCBSO

8STATISTICS AND CENTRAL BALANCE SHEET DATA OFFICE DEPARTMENT

REDUCING REPORTING BURDEN ON EUROPEAN CORPORATIONS

WHY STANDARD FORMATS / XBRL TAXONOMIES?

-Good for users, that:

-Profits on comparability

-Reduce costs and make access to data easier

-But also for companies, that:

- They want to know their obligations

- Especially when an accounting change is approaching

-Best way to introduce IFRS in Europe

-It means a reduction on reporting burden (several users can reach an agreement on the format or on the taxonomy)

Standard formats and IASCF-XBRL taxonomy An experience from ECCBSO

9STATISTICS AND CENTRAL BALANCE SHEET DATA OFFICE DEPARTMENT

REDUCING REPORTING BURDEN ON EUROPEAN CORPORATIONS

EUROPEAN COMMITTEE OF CENTRAL BALANCE SHEET DATA OFFICES (ECCBSO)

-Infomal club of CBSO belonging to NIS and NCB

-Experience using accounting data for several purposes; some figures:

-Banque de France: 4.008 groups, 214.913 companies (74% coverage of employment in 2002)

-Banque de Belgique/Nationale Bank van België: 276.543 annual accounts (100% coverage in 2002)

-Banco de Portugal: 3.631 quarterly accounts (45,4% coverage in 2002)

-Banco de España: 209.007 annual accounts (45% coverage in 2002)

-Experience facing the problem of harmonization: BACH database

Standard formats and IASCF-XBRL taxonomy An experience from ECCBSO

10STATISTICS AND CENTRAL BALANCE SHEET DATA OFFICE DEPARTMENT

REDUCING REPORTING BURDEN ON EUROPEAN CORPORATIONS

III WG OF THE ECCBSO

Targets:

-Monitor and report to the ECCBSO on IFRS implementation process

-Analyze the foreseeable impact on databases and system of analysis

-Creation of an IFRS-based format

Standard formats and IASCF-XBRL taxonomy An experience from ECCBSO

11STATISTICS AND CENTRAL BALANCE SHEET DATA OFFICE DEPARTMENT

REDUCING REPORTING BURDEN ON EUROPEAN CORPORATIONS

IFRS-BASED STANDARD FORMAT: STRATEGIC PLAN

Use of XBRL-IASCF taxonomy (July 2003)Monitoring with real examples (13 listed groups)Methodological note: first draft finishedDefinition of “essential information”Reduction of the format to a common and essential format

Standard formats and IASCF-XBRL taxonomy An experience from ECCBSO

12STATISTICS AND CENTRAL BALANCE SHEET DATA OFFICE DEPARTMENT

REDUCING REPORTING BURDEN ON EUROPEAN CORPORATIONS

IFRS-based standard format: characteristics

Great level of detail, to allow subsequent reductionEach item provides IFRS reference and XBRL tag availableEmployment, even though not asked for in IFRSPresentation principles :

Use of net values

Non current / current presentation of balance sheet

Income statement by nature / by function

Statement of cash-flow (both methods)

Standard formats and IASCF-XBRL taxonomy An experience from ECCBSO

13STATISTICS AND CENTRAL BALANCE SHEET DATA OFFICE DEPARTMENT

REDUCING REPORTING BURDEN ON EUROPEAN CORPORATIONS

Contents of the extended format:

General characteristics

Options IAS

Business combinations

Consolidation

Employment (not required by any IFRS)

Balance sheet

Income statement (by function or by nature)

Statement of changes in equity

Cash-flow statement (direct, indirect or indirect alternative)

Notes

Standard formats and IASCF-XBRL taxonomy An experience from ECCBSO

14STATISTICS AND CENTRAL BALANCE SHEET DATA OFFICE DEPARTMENT

REDUCING REPORTING BURDEN ON EUROPEAN CORPORATIONS

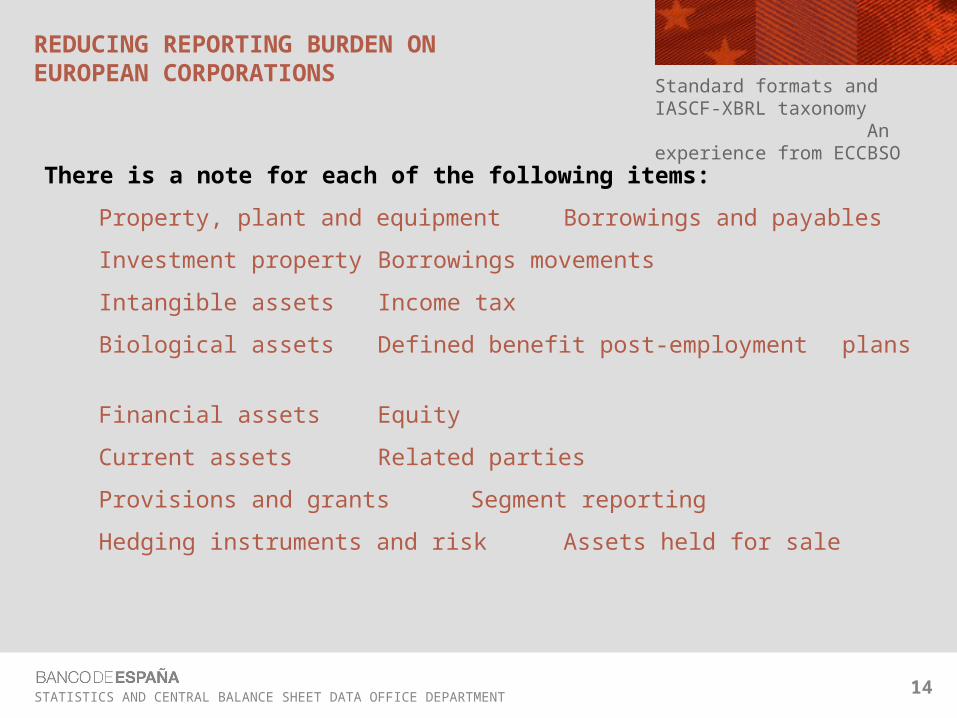

There is a note for each of the following items:

Property, plant and equipment Borrowings and payables

Investment property Borrowings movements

Intangible assets Income tax

Biological assets Defined benefit post-employment plans

Financial assets Equity

Current assets Related parties

Provisions and grants Segment reporting

Hedging instruments and risk Assets held for sale

Standard formats and IASCF-XBRL taxonomy An experience from ECCBSO

15STATISTICS AND CENTRAL BALANCE SHEET DATA OFFICE DEPARTMENT

REDUCING REPORTING BURDEN ON EUROPEAN CORPORATIONS

BEFORE THE PRESENTATION OF THE FORMAT AND ITS TAXONOMY EXAMPLE

THREE DEMANDS:

-It is convenient that IASB approves and updates the IASCF-XBRL taxonomy at the same pace IASB introduces changes

-If SME standards are developed by IASB, all users’ needs should be taken into account

-HOW AND WHEN: Asking for a more accessible channel (XBRL) to annual accounts is a fair demand. But:

-While XBRL is not used by SME, need of standard formats will remain.

-Why not asking for an early access, that is to say, an early deposit of the accounts?

Standard formats and IASCF-XBRL taxonomy An experience from ECCBSO

The ECCBSO Standard formatExample

Prepared with contributions of Banque Nationale de Belgique / Nationale Bank van België

REDUCING REPORTING BURDEN ON EUROPEAN CORPORATIONS ECCBSO Standard Format:

COUNTRY:

COMPANY:

IAS XBRLASSETS Paragraph Tag CBSO code Current Previous

I. NON-CURRENT ASSETS 1.51, 1.57 XBRL 0 0

A. Tangible assets 0 0

1. Property, plant and equipment 1.68.a XBRL 0 01.1. Land and buildings 16.37.b 0 0

1.1.1. Land 16.73,16.37.a XBRL1.1.2. Buildings 16.73 XBRL

1.2. Plant and equipment 16.73 XBRL1.3. Other elements 16.73 0 0

1.3.1. Motor vehicles 16.73,16.37.f XBRL1.3.2. Fixtures and fittings 16.73,16.37.g XBRL1.3.3. Leasehold improvements 16.73 XBRL1.3.4. Other property, plant and equipment (a) 16.73 XBRL

1.4. Construction in progress XBRL

2. Investment property 1.68.b XBRL 0 02.1. Land and buildings 40.76, 40.79 0 0

2.1.1. Land 40.76, 40.792.1.2. Buildings 40.76, 40.79

2.2. Other investment property (a) 40.76, 40.79

B. Intangible assets 0 0

Thousands €Year

REDUCING REPORTING BURDEN ON EUROPEAN CORPORATIONS

COUNTRY:

COMPANY:

INCOME STATEMENT BY NATURE IAS XBRLParagraph Tag CBSO code Current Previous

1. Operating revenue 1.81.a XBRL 0 0 1.1. Operating revenue 1.81.a XBRL 0 0

1.1.1. Turnover 0 01.1.1.1. Sale of goods 18.35.b.i XBRL1.1.1.2. Rendering of services 18.35.b.ii XBRL1.1.1.3. Revenue from construction contracts 11.39.a XBRL

1.1.2. Royalty income 18.35.b.iv XBRL1.1.3. Property rental income 40.75.f.i, CP XBRL1.1.4. Other miscellaneous operating revenue 1.91 XBRL

1.2. Other operating income 1.91, 1.92 XBRL 0 01.2.1. Interest income 18.35.b.iii XBRL1.2.2. Dividend income 18.35.b.v XBRL1.2.3. Income from government grants 20.39.b 0 0

1.2.3.1. Income from government grants related to income 20.311.2.3.2. Income from government grants related to assets 20.26

1.2.4. Remaining operating income 0 01.2.4.1. Foreign exchange gain from foreign currency borrowings related to interest costs 23.5.e XBRL1.2.4.2. Gain on redemption and extinguishment of debt CP XBRL1.2.4.3. Other operating income CP XBRL

Thousands €Year

ECCBSO Standard Format:

General presentation

WGIII Taxonomy

IFRS Taxonomy

Extension ifrs-gp-2004-06-15-WGIII.xsd

Presentation Link ifrs-gp-2004-06-15-WGIII-presentation.xml

ifrs-gp-2004-06-15-WGIII-label.xml

Label Link

Instance document

Stylesheet

Company-2003-12-31.xml

ifrs-gp-2004-06-15.xsd

ifrs-gp-2004-06-15-label.xml

Company-2003-12-31.html

Taxonomy - Extension

ExtensionElement list

Element attribute

DTS

Taxonomy - Presentation Link

Presentation tree

Instance document

Contexts

Data

StylesheetExcel sheet

Stylesheet

STATISTICS AND CENTRAL BALANCE SHEET DATA OFFICE DEPARTMENT

THANK YOU FOR YOUR ATTENTIONManuel Ortega