Embed Size (px)

Citation preview

8 February 2013

Dear Shareholder, Re: Avalon Subscription Agreement Shareholder meeting to approve placement of 25 million shares for $3 million

On 28 November 2012, White Rock Minerals Ltd (‘White Rock’ or ‘the Company’) announced that a Subscription Agreement had been executed with Avalon Ventures Corporation (‘Avalon’) to raise $4.5M with the issue of 40M White Rock shares. The placement to Avalon comprises two tranches, with the first tranche of 15M shares issued in January at $0.10 per share raising $1.5M before costs. This represents a 14.6% shareholding in White Rock. Tranche two of the placement is for the issue of 25M shares at $0.12 per share, raising $3.0M. This comprises a further 16.7% of White Rock's diluted share capital (31% holding in aggregate) and provides for one Avalon-nominated Director to be appointed to the Board of White Rock following the completion of tranche two. As this aggregate holding by Avalon will be more than 20%, tranche two is conditional on White Rock shareholder approval. Accordingly, please find attached a Notice of Meeting with the supporting explanatory notes together with an Independent Expert’s Report, an Independent Geologist’s Report and valuation in order for you to make an informed decision on the placement to Avalon. The Independent Expert has determined that the placement to Avalon is not fair, but is reasonable. The Directors recommend that shareholders vote in favour of the proposed transaction, which will assist in executing the future plans of the Company. The General Meeting will be held on 15 March 2013. A Proxy Form is provided for your use if you are unable to attend the meeting.

White Rock is committed to unlocking the value that is emerging in our Mt Carrington gold-silver project in northern NSW. The recent 2012 scoping study identified the potential to develop a robust mining project with strong revenue, relatively low capital costs, a short payback period and conventional open pit mining at a low ore-waste strip ratio. Development of the project in a relatively short time frame is aided by the fact that the Mineral Resources are on granted mining leases with infrastructure including tailings storage, water and proximal power and road access.

The Company achieved a number of substantial goals on the project in 2012 which underpin our plans for 2013. The results of the scoping study were a pleasing outcome after working through 2011 to build the silver and gold Resource inventory, providing the basis to move to feasibility studies in 2013, along with an expanded exploration program designed to discover and define further shallow gold and silver resources. The goals we have set for 2013 are underpinned by the support we receive from both our long term shareholders and also our new major shareholder, Avalon. White Rock is pleased to welcome Avalon as a cornerstone investor and looks forward to a strong working relationship that will support the growth and development of the Mt Carrington gold-silver project through to a commercial operation. Yours sincerely

Geoffrey Lowe Managing Director

1

NOTICE OF MEETING Notice is given that a General Meeting of shareholders of White Rock Minerals Limited (the Company) will be held at the offices of Baker & McKenzie, Level 19, 181 William Street, Melbourne, at 10.00 am on Friday, 15 March 2013.

Resolution 1: Approval of Proposed Share Issue - Avalon (Tranche 2) To consider and, if thought fit, pass the following resolution as an ordinary resolution:

"That for the purposes of item 7 of section 611 of the Corporations Act and for all other purposes, the shareholders of the Company approve the issue of 25,000,000 fully paid ordinary shares in the capital of the Company to Avalon Ventures Corporation on the basis set out in the Explanatory Notes."

Resolution 2: Approval of Previous Share Issue - Avalon (Tranche 1) To consider and, if thought fit, pass the following resolution as an ordinary resolution:

"That for the purposes of ASX Listing Rule 7.4 and for all other purposes, the shareholders of the Company approve the previous issue of 15,000,000 fully paid ordinary shares in the capital of the Company on the basis set out in the Explanatory Notes."

Resolution 3: Approval of Proposed Share Issue - Titeline To consider and, if thought fit, pass the following resolution as an ordinary resolution:

"That for the purposes of ASX Listing Rule 7.1 and for all other purposes, the shareholders of the Company approve the proposed issue of 6,580,000 fully paid ordinary shares in the capital of the Company on the basis set out in the Explanatory Notes."

By order of the Board

Amber Rivamonte Company Secretary Dated: 8 February 2013

2

PROXY AND VOTING INSTRUCTIONS 1. A shareholder entitled to attend and vote at the meeting may appoint one or two proxies to attend and

vote on their behalf. Each proxy will have the right to vote on a poll and also to speak at the meeting.

2. A proxy need not be a member of the Company and a proxy can be either an individual or a body corporate.

3. The appointment of a proxy may specify the proportion or the number of votes that the proxy may

exercise. Where more than one proxy is appointed and the appointment does not specify the proportion or number of the shareholder’s votes each proxy may exercise, the votes will be divided equally among the proxies (i.e. where there are two proxies, each proxy may exercise half the votes).

4. If a proxy is not directed how to vote on an item of business, the proxy may vote or abstain from

voting on that resolution as they think fit. 5. If a proxy is instructed to abstain from voting on an item of business, they are directed not to vote on

the shareholder’s behalf on the poll and the shares that are the subject of the proxy appointment will not be counted in calculating the required majority.

6. Shareholders who return their proxy forms with a direction on how to vote but do not nominate the

identity of their proxy will be taken to have appointed the Chairman of the meeting as their proxy to vote on their behalf.

7. If a proxy form is returned but the nominated proxy does not attend the meeting, or does not vote on

the resolution, the Chairman of the meeting will act in place of the nominated proxy and vote in accordance with any instructions.

8. Proxy appointments in favour of the Chairman of the meeting, the secretary or any Director that do

not contain a direction on how to vote will be used where possible to support each of the resolutions proposed in this Notice of Meeting.

9. The proxy form (and the power of attorney or other authority, if any, under which the proxy form is

signed) or a copy which appears on its face to be an authentic copy of the proxy form (and the power of attorney or other authority) must be lodged at the share registry Security Transfer Registrars Pty Ltd, PO Box 535 Applecross WA 6153 or by facsimile +618 9315 2233 or by email to [email protected] not less than 48 hours before the time for holding the meeting, or adjourned meeting as the case may be, at which the individual named in the proxy form proposes to vote.

10. The proxy form must be signed by the member or his/her attorney duly authorised in writing or, if the

member is a corporation, in a manner permitted by the Corporations Act 2001 (Cth). A proxy given by a foreign corporation must be executed in accordance with the laws of that corporation’s place of incorporation.

A proxy form accompanies this Notice of Meeting.

Corporate Representatives Any corporation that is a shareholder of the Company may authorise (by a form of execution authorised by the laws of that corporation’s place of incorporation, or in any other manner satisfactory to the Chairman) a natural person to act as its representative at any general meeting. Voting Entitlement The Company has determined that for the purposes of the meeting, shares will be taken to be held by the persons who are registered as holding the shares at 7.00 pm on 13 March 2013. Accordingly, transfers registered after that time will be disregarded in determining entitlements to attend and vote at the meeting.

3

Explanatory Notes

These Explanatory Notes should be read in conjunction with the Notice of Meeting.

Resolution 1: Approval of Share Issue - Avalon (Tranche 2) The Company is seeking shareholder approval to issue 25,000,000 fully paid ordinary shares (Tranche 2 Shares) at 12 cents per share to Avalon Ventures Corporation (Avalon) to raise $3 million under Tranche 2 of the Subscription Agreement (Subscription Agreement) announced to ASX on 28 November 2012 (Tranche 2 Placement). Corporations Act Requirements Section 606 of the Corporations Act relevantly provides that, subject to limited specified exceptions, a person must not acquire a relevant interest in issued voting shares in a company, if as a result of the acquisition any person's voting power in the company would increase from less than 20% to more than 20%. In the absence of an applicable exception, the acquisition of relevant interests resulting in the increase in Avalon's voting power on account of the proposed issue of Tranche 2 shares would breach section 606(1) of the Corporations Act. Section 611 item 7 of the Corporations Act provides an exception to this prohibition, and allows a party to acquire a relevant interest if the proposed acquisition is approved in advance by a resolution passed at a general meeting. Accordingly, Resolution 1 seeks Shareholder approval for the purposes of section 611 item 7 of the Corporations Act for the Tranche 2 Shares to be issued to Avalon pursuant to the Subscription Agreement, the effect of which is that Avalon's voting power in the Company will be increased from 14.6% (15,000,000 shares) to 31.3% (40,000,000 shares).

The following information is provided in compliance with section 611 item 7 and ASIC guidance. The information below in relation to Avalon has been provided to the Company by Avalon, which takes responsibility for that information rather than the Company. (a) The identity of the person proposing to make the acquisition and their associates The Tranche 2 Shares are proposed to be acquired by Avalon. Avalon is principally an investment holding company with a focus on gold mining investments. Avalon currently holds a 30% shareholding in Mornington Offshore Inc (which itself owns mining interests through its wholly owned subsidiary Emas Mali S.A, a gold exploration company incorporated in the Republic of Mali).

The shareholders of Avalon are Tan Boon Kiat, who owns 90% of Avalon and is the sole director of the company, and Ismail Baba Cisse who owns 10% of Avalon. Mr Tan is a Malaysian citizen, who currently runs a company called Citral (M) Sdn Bhd in Kuala Lumpur. Mr Cisse is a former advisor to the President of Mali in relation to Malaysian investments and is the current director general of Emas Mali S.A, a gold exploration company incorporated in the Republic of Mali. Avalon does not have any associates in relation to the Tranche 2 Placement. (b) The maximum extent of the increase in Avalon's voting power in the Company that would result from the acquisition Avalon currently holds 15,000,000 shares in the Company which represents a 14.6% voting power in the Company. If Shareholders approve Resolution 1, following completion of the Tranche 2 placement, Avalon will have a 31.3% voting power in the Company after the issue of the Tranche 2 Shares (40,000,000 shares in total), being an increase of a 16.7% voting power from its current holding.

4

(c) The voting power that person will have as a result of the acquisition If the Tranche 2 Shares are issued to Avalon, it will have voting power of 31.3%. (d) The maximum extent of the increase in voting power of each of Avalon's associates that would result from the acquisition. 16.7% (25,000,000 shares) (e) The voting power that each of Avalon's associates would have as a result of the acquisition 31.3% (40,000,000 shares) (f) Reasons for proposed acquisition The purpose of the Tranche 2 Placement is to enable the Company to raise $3 million. This placement, together with the Tranche 1 Placement to Avalon which was completed in January 2013, is designed to assist the Company to develop the Mount Carrington gold-silver project. The funds are intended to be used by the Company to conduct pre-feasibility studies at Mount Carrington in 2013, resources and exploration drilling focused on defining new gold and silver resources at the Red Rock and Mozart prospects and for general working capital. (g) When the proposed acquisition is to occur Pursuant to the Subscription Agreement, the Tranche 2 Shares are expected be issued 5 business days after the satisfaction of all of the Tranche 2 Conditions Precedent. Each of the Conditions Precedent to Tranche 2 (other than shareholder approval as contemplated by Resolution 1) have been satisfied. (h) The material terms of the proposed acquisition The material terms of the proposed acquisition of Tranche 2 Shares are set out in the Subscription Agreement dated 28 November 2012. A summary of the key terms of the Subscription Agreement as they relate to Tranche 2 are set out below. This summary does not purport to be exhaustive or constitute a definitive statement of the rights and liabilities of each the Company and Avalon under the Subscription Agreement. The full terms of the Subscription Agreement were annexed to the ASX announcement issued by the Company on 28 November 2012 and is available from the ASX website. Conditions Precedent: Completion of Tranche 2 is conditional on Shareholder approval (as contemplated by this notice of meeting). Each of the other conditions relating to Tranche 2, being FIRB Approval and NSW Ministerial consent approval, have been satisfied. Avalon Board Nominee: The Company must take steps to appoint a proposed director nominated by Avalon to the board of the Company following Tranche 2 completion (refer below). Issue Price: The issue price of the Tranche 2 Shares is $0.12 per share. Capital Structure: Until the Tranche 2 Completion Date, the Company will not, except with the prior written consent of Avalon, issue or agree to issue any shares or other securities (with limited exceptions including to a third party under an agreement involving the provision of drilling services as contemplated by the proposed share issue in Resolution 3) or implement a share consolidation or subdivision, a capital reduction or a share buy-back or any other capital reconstruction. Warranties: The Company and Avalon have each given certain customary mutual warranties to each other including in relation to their authority and legal capacity. The Company has provided customary warranties to Avalon.

5

Termination: The Subscription Agreement may be terminated by either party by written notice to the other party, if the other party is in material breach of any clause of the Subscription Agreement and that breach is not remedied, or by agreement in writing between the parties. Cost reimbursement: If Tranche 2 completion does not occur for any reason (other than valid termination of the Subscription Agreement by Avalon), Avalon must reimburse the Company for any costs and expenses incurred by the Company in connection with obtaining an independent expert report (and any ancillary geological, technical or valuation reports) to be provided to Shareholders for the purposes of this meeting. (i) Details of the terms of any other relevant agreement between Avalon and the Company (or any of their associates) that is conditional on (or directly or indirectly depends on) Shareholders’ approval of the proposed acquisition There are such no agreements or proposed agreements. (j) Statement of Avalon's intentions regarding the future of the Company if Shareholders approve the acquisition Avalon has advised the Company that it currently intends that the Company's operations will continue unchanged in their current form and in a manner consistent with the Company's existing strategy and operation plan to progress the feasibility study on the Mount Carrington gold-silver project. Avalon has advised the Company that its current intentions are: • To be a strategic shareholder in the Company and to be a long-term shareholder of the

Company.

• Not to change the business of the Company, nor transfer assets between Avalon and the Company or their associates, nor redeploy fixed assets of the Company nor change the Company’s existing policies in relation to financial matters or dividend distribution.

• Not to change the employment of any present employee of the Company. (k) Does any Director of the Company have any interest in the acquisition or relevant agreement conditional upon the approval The Directors do not have an interest in the outcome of Resolution 1 other than in their capacity as holders of shares and options in the Company. (l) Details of the person intended to become a director if members approve the acquisition of shares Avalon propose to nominate Peter Lester, B.E (Mining), MAusIMM, MAICD. Mr Lester has over 35 years' experience in the mining industry, and has held senior executive positions with North Ltd, Newcrest Mining Limited, Oxiana Limited and Citadel Resource Group Limited. Mr Lester's experience covers operations, project and business development and general corporate activities. Mr Lester is a non-executive director of Chesser Resources Limited, Toro Energy Ltd, Castlemaine Goldfields Ltd, Accessio Resources Pty Ltd and Nord Gold NV. (m) Independent Expert's Report ASIC requires that the shareholders who are being asked to consider a proposal to pass a resolution under section 611 item 7 of the Corporations Act be provided with an analysis of whether the proposal is fair and reasonable when considered from the perspective of the shareholders of the Company other than Avalon and its associates. Directors may satisfy their obligation to provide an analysis and a valuation by those Directors not associated with the proposal commissioning an Independent Expert's Report. The Directors have commissioned RSM Bird Cameron Corporate Pty Ltd to prepare an Independent Expert's Report which assesses whether the proposed issue of the Tranche 2 Shares to Avalon is fair and reasonable

6

to Shareholders (which includes a Valuation Report and Independent Geologist Report prepared by Goldner & Associates and associated Independent Tenement Report). The Independent Expert Report is set out in Annexure A. The Independent Expert's Report has concluded that the issue of the Tranche 2 Shares is not fair but reasonable to Shareholders not associated with Avalon. Neither the Company nor the Directors are aware of any additional information not set out in these Explanatory Notes that would be relevant to Shareholders in deciding how to vote on this Resolution 1. (n) Voting Restriction The Company will disregard any votes cast on this resolution by Avalon or any of its associates. However, the Company need not disregard a vote if it is cast: • as proxy for a person who is entitled to vote, in accordance with the directions on the proxy

form; or

• by the person chairing the meeting as proxy for a person who is entitled to vote, in accordance with a direction on the form to vote as the proxy decides.

(o) Recommendation The Directors unanimously recommend that Shareholders vote in favour of this resolution. Resolution 2: Approval of Previous Share Issue - Avalon (Tranche 1) ASX Listing Rule 7.1 restricts the number of securities which a listed entity may issue in any 12 month period without the approval of shareholders of 15% of the number of securities on issue at the start of the period subject to certain adjustments and permitted exceptions. This resolution seeks shareholder approval to the previous issue of securities in the Company for the purposes of Listing Rule 7.4. The purpose of seeking shareholder approval of the issue of securities in this resolution is to "freshen up" the Company's placement capacity and ensure that the previous issue of shares as described below does not reduce the Company's placement capacity under the Listing Rules. As announced to ASX on 11 January 2013, the Company issued 15,000,000 fully paid ordinary shares in the Company to Avalon at a price of 10 cents each to raise $1.5 million. The Company proposes to use the funds for exploration activities including resource and exploration drilling, advancement of feasibility study activities and general working capital. Recommendation The Directors unanimously recommend that Shareholders vote in favour of this resolution. Voting Restriction The Company will disregard any votes cast on this resolution by Avalon or any of its associates. However, the Company need not disregard a vote if it is cast: • as proxy for a person who is entitled to vote, in accordance with the directions on the proxy

form; or

• by the person chairing the meeting as proxy for a person who is entitled to vote, in accordance with a direction on the form to vote as the proxy decides.

7

Resolution 3: Approval of Proposed Share Issue - Titeline This resolution seeks shareholder approval of the proposed issue of shares for the purposes of Listing Rule 7.1. The purpose of seeking shareholder approval of the issue of shares in this resolution is to ensure that the proposed issue of shares as described below does not reduce the Company's future placement capacity under the Listing Rules. As announced to ASX on 11 January 2013, the Company has entered into a drilling agreement with Titeline Drilling Pty Ltd (Titeline) under which Titleline has agreed to provide certain drilling services to the Company in consideration for the issue of 6,580,000 fully paid ordinary shares at 10 cents per share and total cash payments of $112,000. The purpose of the drilling agreement is to accelerate resource expansion, project development and exploration programs on the Company's 100% owned Mt Carrington gold-silver project. The shares under the drilling agreement are expected to be issued in or around late March 2013, and in any event within 3 months from the date of the meeting. Recommendation The Directors unanimously recommend that Shareholders vote in favour of this resolution. Voting Restriction The Company will disregard any votes cast on this resolution by Titeline and any person who might obtain a benefit, except a benefit solely in the capacity of a holder of ordinary securities, if this resolution is passed, or any of their associates. However, the Company need not disregard a vote if it is cast: • as proxy for a person who is entitled to vote, in accordance with the directions on the proxy

form; or

• by the person chairing the meeting as proxy for a person who is entitled to vote, in accordance with a direction on the form to vote as the proxy decides.

SECTION B: Voting Directions to your Proxy

SECTION A: Appointment of Proxy

SECTION C: Please Sign Below

REGISTERED OFFICE:24 SKIPTON STREETBALLARAT VIC 3350

SHARE REGISTRY:Security Transfer Registrars Pty Ltd

All Correspondence to:PO BOX 535,

APPLECROSS WA 6953 AUSTRALIA770 Canning Highway,

APPLECROSS WA 6153 AUSTRALIAT: +61 8 9315 2333 F: +61 8 9315 2233

E: [email protected]: www.securitytransfer.com.au

WHITE ROCK MINERALS LTDABN: 64 142 809 970

PROXY FORMTHIS DOCUMENT IS IMPORTANT. IF YOU ARE IN DOUBT AS TO HOW TO DEAL WITH IT, PLEASE CONTACT YOUR STOCK BROKER OR LICENSED PROFESSIONAL ADVISOR.

Holder Number:

I/We, the above named, being registered holders of the Company and entitled to attend and vote hereby appoint:

or failing the person named, or if no person is named, the Chairperson of the Meeting, as my/our Proxy to act generally at the meeting on my/our behalf and to vote in

accordance with the following directions (or if no directions have been given, as the Proxy sees fit) at the General Meeting of the Company to be held at 10.00am AEDSTon Friday 15 March 2013 at the offices of Baker & McKenzie, Level 19, 181 William Street, Melbourne VIC and at any adjournment of that meeting.

Code: WRM

OR

The name of the person you are appointing(if this person is someone other than the Chairperson of the meeting).

The meeting Chairperson (mark with an "X")

If no directions are given my proxy may vote as the proxy thinks fit or may abstain.* If you mark the Abstain box for a particular item, you are directing your Proxy not to vote on your behalf on a show of hands or on a poll and your votes will not be counted in computing the required majority on a poll.

WRM 1

Proxies must be received by Security Transfer Registrars Pty Ltd no later than 10.00AM AEDST on WEDNESDAY 13 MARCH 2013.

ONLINE PROXY SERVICEYou can lodge your proxy online at www.securitytransfer.com.au

1. Log into the Investor Centre using your holding details.2. Click on "Proxy Voting" and provide your Online Proxy ID to access the voting area.

Online Proxy ID:

This section must be signed in accordance with the instructions overleaf to enable your directions to be implemented.

Please mark "X" in the box to indicate your voting directions to your Proxy.

Resolution

1. Approval of Proposed Share Issue - Avalon (Tranche 2)

2. Approval of Previous Share Issue - Avalon (Tranche 1)

3. Approval of Proposed Share Issue - Titeline

For Against Abstain*

Individual or Security Holder Security Holder 2

Sole Director and Sole Company Secretary Director

Security Holder 3

Director / Company Secretary

9999666622226666111188881111999966668888

PRIVACY STATEMENTPersonal information is collected on this form by Security Transfer Registrars Pty Ltd as the registrar for securities issuers for the purpose of maintaining registers of securityholders,facilitating distribution payments and other corporate actions and communications. Your personal details may be disclosed to related bodies corporate, to external service providerssuch as mail and print providers, or as otherwise required or permitted by law. If you would like details of your personal information held by Security Transfer Registrars Pty Ltd or youwould like to correct information that is inaccurate please contact them on the address on this form.

TELEPHONE NUMBER

( )

NAME

My/Our contact details in case of enquiries are:

5. Signing InstructionsIndividual: where the holding is in one name, the Shareholder must sign.

Joint Holding: where the holding is in more than one name, all of theShareholders must sign.

Power of Attorney: to sign under Power of Attorney you must have alreadylodged this document with the Company's share registry. If you have not

previously lodged this document for notation, please attach a certifiedphotocopy of the Power of Attorney to this form when you return it.

Companies: where the Company has a Sole Director who is also the SoleCompany Secretary, this form must be signed by that person. If the Company

(pursuant to section 204A of the Corporations Act 2001) does not have aCompany Secretary, a Sole Director may sign alone. Otherwise this form mustbe signed by a Director jointly with either another Director or Company

Secretary. Please indicate the office held in the appropriate place.

If a representative of the corporation is to attend the meeting the appropriate"Certificate of Appointment of Corporate Representative" should be lodged

with the Company before the meeting or at the registration desk on the day ofthe meeting. A form of the certificate may be obtained from the Company's

share registry.

6. Lodgement of ProxyProxy forms (and any Power of Attorney under which it is signed) must bereceived by Security Transfer Registrars Pty Ltd no later than 10.00am AEDSTon Wednesday 13 March 2013, being 48 hours before the time for holding the

meeting. Any Proxy form received after that time will not be valid for thescheduled meeting.

Security Transfer Registrars Pty Ltd

PO BOX 535Applecross, Western Australia 6953

Street Address:Alexandrea House, Suite 1770 Canning HighwayApplecross, Western Australia 6153

Telephone +61 8 9315 2333

Facsimile +61 8 9315 2233

Email [email protected]

NOTES 1. Name and Address

This is the name and address on the Share Register of White Rock MineralsLtd. If this information is incorrect, please make corrections on this form.

Shareholders sponsored by a broker should advise their broker of anychanges. Please note that you cannot change ownership of your shares usingthis form.

2. Appointment of a ProxyIf you wish to appoint the Chairperson of the Meeting as your Proxy please

mark "X" in the box in Section A. Please also refer to Section B of this proxyform and ensure you mark the box in that section if you wish to appoint the

Chairperson as your Proxy.

If the person you wish to appoint as your Proxy is someone other than the

Chairperson of the Meeting please write the name of that person in Section A.If you leave this section blank, or your named Proxy does not attend the

meeting, the Chairperson of the Meeting will be your Proxy. A Proxy need notbe a Shareholder of White Rock Minerals Ltd.

3. Directing your Proxy how to voteTo direct the Proxy how to vote place an "X" in the appropriate box againsteach item in Section B. Where more than one Proxy is to be appointed and

the proxies are to vote differently, then two separate forms must be used toindicate voting intentions.

4. Appointment of a Second ProxyYou are entitled to appoint up to two (2) persons as proxies to attend the

meeting and vote on a poll. If you wish to appoint a second Proxy, an additional Proxy form may be obtained by telephoning the Company's share registry +61 8 9315 2333 or you may photocopy this form.

To appoint a second Proxy you must:

(a) On each of the Proxy forms, state the percentage of your voting rights ornumber of securities applicable to that form. If the appointments do not

specify the percentage or number of votes that each Proxy may exercise,each Proxy may exercise half of your votes; and

(b) Return both forms in the same envelope.

0000777788888888111188881111999966668888

White Rock Minerals Limited

Financial Services Guide and

Independent Expert’s Report 8 February 2013

We have concluded that the Proposed Transaction is NOT FAIR but IS REASONABLE to shareholders not associated with the Proposed Transaction

RSM Bird Cameron Corporate Pty Ltd Level 8 Rialto South Tower 525 Collins Street Melbourne VIC 3000 PO Box 248 Collins Street West VIC 8007 T +61 3 9286 1800 F +61 3 9286 1999 www.rsmi.com.au

RSM Bird Cameron Corporate Pty Ltd Level 8 Rialto South Tower 525 Collins Street Melbourne VIC 3000 PO Box 248 Collins Street West VIC 8007 T +61 3 9286 1800 F +61 3 9286 1999 www.rsmi.com.au

Financial Services Guide

RSM Bird Cameron Corporate Pty Ltd ABN 82 050 508 024 (“RSM Bird Cameron Corporate Pty Ltd” or “we” or “us” or “ours”

as appropriate) has been engaged to issue general financial product advice in the form of a report to be provided to you.

In the above circumstances we are required to issue to you, as a retail client, a Financial Services Guide (“FSG”). This FSG is

designed to help retail clients make a decision as to their use of the general financial product advice and to ensure that we

comply with our obligations as financial services licensees.

This FSG includes information about:

who we are and how we can be contacted;

the services we are authorised to provide under our Australian Financial Services Licence, Licence No 255847;

remuneration that we and/or our staff and any associates receive in connection with the general financial product advice;

any relevant associations or relationships we have; and

our complaints handling procedures and how you may access them.

Financial services we are licensed to provide

We hold an Australian Financial Services Licence, which authorises us to provide financial product advice in relation to:

deposit and payment products limited to:

(a) basic deposit products;

(b) deposit products other than basic deposit products.

interests in managed investments schemes (excluding investor directed portfolio services); and

securities (such as shares and debentures).

We provide financial product advice by virtue of an engagement to issue a report in connection with a financial product of

another person. Our report will include a description of the circumstances of our engagement and identify the person who has

engaged us. You will not have engaged us directly but will be provided with a copy of the report as a retail client because of

your connection to the matters in respect of which we have been engaged to report.

Any report we provide is provided on our own behalf as a financial services licensee authorised to provide the financial

product advice contained in the report.

General Financial Product Advice

In our report we provide general financial product advice, not personal financial product advice, because it has been prepared

without taking into account your personal objectives, financial situation or needs.

You should consider the appropriateness of this general advice having regard to your own objectives, financial situation and

needs before you act on the advice. Where the advice relates to the acquisition or possible acquisition of a financial product,

you should also obtain a product disclosure statement relating to the product and consider that statement before making any

decision about whether to acquire the product.

Benefits that we may receive

We charge fees for providing reports. These fees will be agreed with, and paid by, the person who engages us to provide the

report. Fees will be agreed on either a fixed fee or time cost basis.

Except for the fees referred to above, neither RSM Bird Cameron Corporate Pty Ltd, nor any of its directors, employees or

related entities, receive any pecuniary benefit or other benefit, directly or indirectly, for or in connection with the provision of

the report.

Remuneration or other benefits received by our employees

All our employees receive a salary.

Referrals

We do not pay commissions or provide any other benefits to any person for referring customers to us in connection with the

reports that we are licensed to provide.

Associations and relationships

RSM Bird Cameron Corporate Pty Ltd is beneficially owned by the partners of RSM Bird Cameron, a large national firm of

chartered accountants and business advisers. Our directors are partners of RSM Bird Cameron Partners.

From time to time, RSM Bird Cameron Corporate Pty Ltd, RSM Bird Cameron Partners, RSM Bird Cameron and / or RSM Bird

Cameron related entities may provide professional services, including audit, tax and financial advisory services, to financial

product issuers in the ordinary course of its business.

Complaints Resolution

Internal complaints resolution process

As the holder of an Australian Financial Services Licence, we are required to have a system for handling complaints from

persons to whom we provide financial product advice. All complaints must be in writing, addressed to The Complaints Officer,

RSM Bird Cameron Corporate Pty Ltd, P O Box R1253, Perth, WA, 6844.

When we receive a written complaint we will record the complaint, acknowledge receipt of the complaint within 15 days and

investigate the issues raised. As soon as practical, and not more than 45 days after receiving the written complaint, we will

advise the complainant in writing of our determination.

Referral to External Dispute Resolution Scheme

A complainant not satisfied with the outcome of the above process, or our determination, has the right to refer the matter to

the Financial Ombudsman Service (“FOS”). FOS is an independent company that has been established to provide free advice

and assistance to consumers to help in resolving complaints relating to the financial services industry.

Further details about FOS are available at the FOS website or by contacting them directly via the details set out below.

Financial Ombudsman Service

GPO Box 3

Melbourne VIC 3001

Toll Free: 1300 78 08 08

Facsimile: (03) 9613 6399

Email: [email protected]

Contact Details

You may contact us using the details set out at the top of our letterhead on page 1 of this FSG.

Independent Expert’s Report

TABLE OF CONTENTS Page

1. Introduction ................................................................................................................................................ 6

2. Summary and Conclusion .......................................................................................................................... 8

3. Summary of the Proposed Transaction ...................................................................................................10

4. Purpose of this Report .............................................................................................................................11

5. Profile of WRM .........................................................................................................................................13

6. Valuation Approach ..................................................................................................................................18

7. Valuation of WRM ....................................................................................................................................21

8. Is The Proposed Transaction Fair? ..........................................................................................................27

9. Is The Proposed Transaction Reasonable?.............................................................................................28

Appendix 1 – Declarations and Disclaimers .....................................................................................................31

Appendix 2 – Sources of Information ...............................................................................................................33

Appendix 3 – Glossary of Terms and Abbreviations ........................................................................................34

Appendix 4 – Profile of the Australian Silver Industry ......................................................................................37

Appendix 5 – Profile of the Australian Gold Industry ........................................................................................39

Appendix 6 – Independent Technical Review and Valuation of the Mt Carrington and Guyra Projects of White Rock Minerals Limited ......................................................................................................................................41

6

Direct Line: (03) 9286 1867 Email: [email protected]

8 February 2013

The Directors White Rock Minerals Limited 24 Skipton Street Ballarat VIC 3350 Dear Sirs

Independent Expert’s Report 1. Introduction

1.1. This Independent Expert‟s Report (the “Report” or “IER”) has been prepared to accompany the Notice of

Meeting and Explanatory Statement for Shareholders for the General Meeting of White Rock Minerals Limited (“WRM” or “the Company”) to be held in March 2013 at which Shareholder approval will be sought for Resolution 1 (“the Proposed Transaction”), as set out below:

Resolution 1: Approval of Proposed Share Issue – Avalon (Tranche 2)

To consider, and if thought fit, to pass the following resolution as an ordinary resolution:

“That for the purposes of item 7 section 611 of the Corporations Act and for all other purposes, the

shareholders of the Company approve the issue of 25,000,000 fully paid ordinary shares in the capital of

the Company to Avalon Ventures Corporation on the basis set out in the Explanatory Notes.”

1.2. On 28 November 2012, the Company entered into a share subscription agreement (“Share Subscription

Agreement”) with Avalon Ventures Corporation (“Avalon”) to issue 40 million ordinary shares to Avalon to raise $4.5 million in two tranches as follows:

Tranche 1 – $1.5 million comprising 15 million shares at 10 cents each. Tranche 1 shares were issued on 11 January 2013. The issue of Tranche 1 shares resulted in Avalon owning a 14.6% interest in WRM; and

Tranche 2 – $3 million comprising 25 million shares at 12 cents each, comprising a further 16.7% interest in the Company and will increase Avalon‟s interest in WRM to 31.4%.

1.3. Avalon is a Singapore-based special purpose company which also holds investments in mining interests in Mali. Neither Avalon nor its associates held any shares or options in WRM prior to the issue of the Tranche 1 shares.

1.4. The issue of a total of 25 million shares under Tranche 2 (the “Share Placement”) proposed in Resolution

1 will result in Avalon owning greater than 20% of the issued share capital of WRM, which under Section 611 Item 7, requires the approval of Shareholders in a general meeting.

7

1.5. The Directors of WRM have requested that RSM Bird Cameron Corporate Pty Ltd (“RSM”), being independent and qualified for the purpose, express an opinion as to whether Resolution 1 is fair and reasonable to Shareholders not associated with Avalon (“the Non-Associated Shareholders”).

1.6. The ultimate decision whether to approve the Proposed Transaction should be based on each Non- Associated Shareholder‟s assessment of their circumstances, including their risk profile, liquidity

preference, tax position and expectations as to value and future market conditions. If in doubt about the Proposed Transaction, or matters dealt with in this Report, the Non-Associated Shareholders should seek independent professional advice.

8

Low High Preferred$ $ $

Value per WRM share 0.188 0.450 0.257

Value of consideration for a WRM share 0.120 0.120 0.120

Source: RSM analysis

2. Summary and Conclusion

2.1. In our opinion, and for the reasons set out in sections 8 and 9 of this Report, the Proposed Transaction is Not Fair but Reasonable for the Non-Associated Shareholders of WRM.

Fairness

2.2. In order to assess the fairness of the Proposed Transaction, we have valued a share in WRM prior to the Proposed Transaction and compared it to the consideration of $0.12 per share offered for the Share Placement. Our assessed values are summarised in the table below.

Table 1: Valuation Summary

2.3. As the preferred value of a WRM share is greater than the consideration offered, we consider the Proposed Transaction to be not fair to the Shareholders.

Reasonableness

2.4. RG 111 establishes that an offer is reasonable if it is fair. If might also be reasonable if, despite not being fair, there are sufficient reasons for the security holders to accept the offer in the absence of any higher bid before the offer closes. In assessing the reasonableness of the Proposed Transaction, we have considered the following factors in our assessment:

the future prospects of the Company if the Proposed Transaction does not proceed;

alternative offers and sources of funds; and

any other commercial advantages and disadvantages to the Shareholders as a consequence of the Proposed Transaction proceeding.

2.5. In our opinion, in the absence of a superior offer, the position of Shareholders if Resolution 1 is approved is more advantageous than if it is not. The primary reasons for this assessment are set out below:

the $3 million in equity raised upon completion of the Proposed Transaction will increase the Company‟s current cash and liquidity position. As set out in further detail in section 5 of this Report, the Company‟s cash position has decreased from $5.3 million at 30 June 2011, to $1.1

million at 31 December 2012. The proceeds of $1.5 million raised from the issue of the Tranche 1 shares in January 2013, together with the Tranche 2 proceeds of $3 million will provide WRM with funding for the Company‟s operating expenses, as well as for the exploration and development of

the Company‟s properties and tenements, with the aim of the completion of a pre-feasibility study;

9

the consideration of $0.12 represents a 62.2% premium over the closing share price on 27 November 2012 of $0.074, 1 day before the announcement of the Proposed Transaction, and a 30.4% premium to the 30 day volume weighted average share price (“VWAP”) prior to the announcement of the Proposed Transaction of $0.092;

in the event that Resolution 1 is not approved, the Company will have to seek funding from alternative sources and may not be able to obtain funding on more favourable terms than currently offered by Avalon; and

WRM has undertaken a structured program seeking strategic investors or partnerships during the second half of 2012, meeting with local and international parties including other listed companies, capital funds, banks, broking firms, private investors and corporate advisory firms and, at the date of this Report, has not received any alternative offers that would offer a premium over the funding terms offered by Avalon.

2.6. The key disadvantages of the Proposed Transaction are as follows:

the Proposed Transaction is not fair;

the dilution of Shareholders‟ interests from 85.4% to 68.6% following the transaction set out in Resolution 1;

the likelihood of a future takeover of WRM may be reduced as Avalon would control a 31.4% interest in the Company; and

the dilution of existing shareholders‟ interests reduces the ability of existing shareholders to

influence the strategic direction of the Company, including acceptance or rejection of take-over or merger proposals.

2.7. We are not aware of any alternative proposals which may provide a greater benefit to the Non-Associated Shareholders of WRM at this time.

2.8. In our opinion, the position of the Shareholders of WRM if the Proposed Transaction is approved is more advantageous than the position if it is not approved. Therefore, in the absence of any other relevant information and/or a superior offer, we consider that the Proposed Transaction is reasonable for the Shareholders of WRM.

10

Number % of total

WRM Capital Structure Prior to the Proposed Transaction

Number of ordinary shares issued to Avalon under Tranche 1 15,000,000 14.6%Number of ordinary shares held by Non-Associated Shareholders 87,475,531 85.4%

Total number of shares prior to the Proposed Transaction 102,475,531 100.0%

WRM Capital Structure After the Proposed Transaction

Number of ordinary shares held by Non-Associated Shareholders 87,475,531 68.6%Number of ordinary shares held by Avalon after the issue of Tranche 1 and Tranche 2

40,000,000 31.4%

Total number of shares after the Proposed Transaction 127,475,531 100.0%

3. Summary of the Proposed Transaction

3.1. On 28 November 2012, the Company entered into a Share Subscription Agreement with Avalon to issue 40 million ordinary shares to Avalon in two tranches (Tranches 1 and 2) to raise $4.5 million.

3.2. Tranche 1 shares comprising 15 million shares with consideration of 10 cents per share were issued on 11 January 2013, resulting in Avalon owning a 14.6% interest in WRM.

3.3. Tranche 2 shares comprising 15 million shares with consideration of 12 cents per share, to raise a further $3 million, is subject to the approval of Resolution 1.

3.4. The Tranche 2 shares comprise a further 16.7% interest in the Company‟s share capital. In the event that

Resolution 1 is approved, completion of the issue of the Tranche 2 shares to Avalon is expected to take place in March 2013.

3.5. The effect of the Proposed Transaction on WRM‟s issued share capital is illustrated in the table below.

Table 2: WRM Capital Structure Before and After the Proposed Transaction

3.6. The Proposed Transaction would result in the dilution of Shareholders‟ interests from 85.4% to 68.6%.

3.7. As at the date of this Report, WRM had the following options on issue:

360,000 listed share options at an exercise price of $0.38, maturing 30 April 2014; and

6,050,000 listed share options at an exercise price of $0.38, maturing 1 August 2014.

3.8. As these options are all out of the money as at the date of this Report and, therefore, have no impact on our assessment of the fairness and reasonableness, we have excluded them from our analysis.

11

4. Purpose of this Report

Corporations Act

4.1. Section 606(1) of the Corporations Act provides that, subject to limited specified exemptions, a person must not acquire a “relevant interest” in issued voting shares in a public company if as a result of the acquisition any person‟s voting power in the company would increase from 20% or below to more than

20%. In broad terms, a person has a “relevant interest” in shares if that person holds shares or has the

power to control the right to vote or dispose of shares. A person‟s voting power in a company is the

number of voting shares in which the person (and its associates) has a relevant interest, compared with the total number of voting shares in a company.

4.2. Completion of the Proposed Transaction will result in Avalon having a 31.4% relevant interest in the Company.

4.3. Section 611, Item 7 of the Corporations Act provides an exemption to the rule noted in paragraph 4.1 above. Section 611, Item 7 allows a party (and its associates) to acquire a relevant interest in shares that would otherwise be prohibited under Section 606(1) of the Corporations Act if the proposed acquisition is approved in advance by a resolution passed at a general meeting of the company, and:

(i) no votes are cast in favour of the resolution by the proposed acquirer (Avalon) or respective associates; and

(ii) there was full disclosure of all information that was known to the persons proposed to make the acquisition or their associates or known to the company that was material to a decision on how to vote on the resolution.

4.4. This Report has been prepared to assist the Directors of WRM in making their recommendations to WRM Shareholders in relation to Resolution 1, and to assist the Non-Associated Shareholders of WRM to assess the merits of the Proposed Transaction. The sole purpose of this Report is to set out RSM‟s

opinion as to whether the Proposed Transaction is fair and reasonable.

4.5. Section 611 states that shareholders must be given all information that is material to the decision on how to vote at the meeting.

4.6. Regulatory Guide 111 Content of Expert Reports (“RG 111”) issued by ASIC advises the commissioning

of an Independent Expert‟s Report in such circumstances and provides guidance on the content.

Basis of Evaluation

4.7. In determining whether the Proposed Transaction is “fair and reasonable” we have given regard to the

views expressed by ASIC in RG 111.

4.8. RG 111 provides ASIC‟s views on how an expert can help security holders make informed decisions

about transactions. Specifically it gives guidance to experts on how to evaluate whether or not a proposed transaction is fair and reasonable.

12

4.9. RG 111 states that the expert report should focus on:

the issues facing the security holders for whom the report is being prepared; and

the substance of the transaction rather than the legal mechanism used to achieve it.

4.10. Where an issue of shares by a company otherwise prohibited under Section 606 is approved under Item 7 of Section 611 and the effect on the company‟s shareholding is comparable to a takeover bid, RG 111 states that the transaction should be analysed as if it were a takeover bid.

4.11. In assessing whether the Proposed Transaction is fair and reasonable to the Shareholders, the analysis undertaken is as follows:

Fairness

4.12. In assessing whether the Proposed Transaction is fair to Non-Associated Shareholders, a comparison of the following is undertaken:

the value of a WRM share (including a premium for control), prior to the Proposed Transaction; to

the consideration offered of $0.12 per share.

Reasonableness

4.13. In assessing whether the Proposed Transaction is reasonable to Non-Associated Shareholders, the following analysis has been undertaken:

a review of other significant factors which Non-Associated Shareholders might consider prior to approving the Proposed Transaction;

in particular, we have considered the advantages and disadvantages of the Proposed Transaction in the event that it proceeds or does not proceed, including the future prospects of the Company if the Proposed Transaction does not proceed; and

any other commercial advantages and disadvantages to Non-Associated Shareholders as a consequence of the Proposed Transaction proceeding.

4.14. Our assessment of the Proposed Transaction is based on economic, market and other conditions prevailing at the date of this Report.

4.15. Goldner and Associates (“GA”) has prepared a report providing an independent valuation of WRM‟s

interest in its gold and silver mineral assets. For the purpose of this Report, we have relied upon the valuation of WRM‟s mineral assets provided by GA in our assessment of the valuation of the Company.

13

Tonnes Gold SilverCategory Deposit Mt koz Au koz Ag

Silver dominant resources (25 g/t Ag cut-off grade)

Indicated Lady Hampden 1.84 37 4,056

Sub-total Indicated 1.84 37 4,056

Inferred Lady Hampden 2.47 27 4,023White Rock 4.08 - 8,194White Rock North 3.18 - 5,314Silver King 0.64 - 1,218

Sub-total Inferred 10.37 27 18,749

Gold dominant resources (0.5 g/t Au cut-off grate)

Indicated Strauss 1.24 57 153Kylo 1.59 59 133

Sub-total Indicated 2.83 116 286

Inferred Strauss 1.26 56 104Kylo 0.76 35 43Guy Bell 0.16 13 24

Sub-total Inferred 2.18 104 171

Total resources 284 23,262

Source: GA valuation (refer Appendix 6)

Contained metal

5. Profile of WRM

5.1. WRM is an Australian minerals exploration company focused on the discovery and development of shallow gold, silver and copper deposits in the New England Fold Belt of northern NSW.

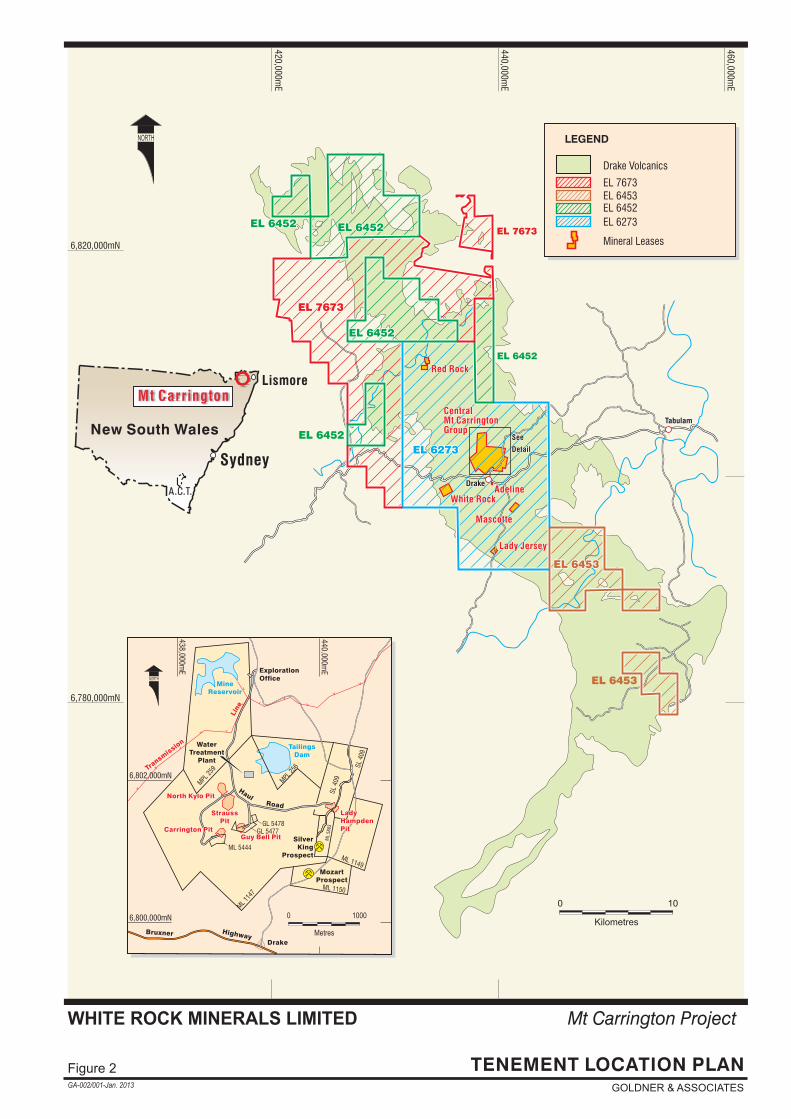

5.2. WRM‟s primary asset is the 100% owned Mt Carrington Project where shallow Indicated and Inferred Mineral Resources totalling 284koz gold and 23,262koz silver (750koz AuEq), have been defined in accordance with the JORC code. The Mt Carrington Project consists of four Exploration Licences (“ELs”)

and 22 assorted mining tenements covering a total area of approximately 467km2, and is located near the township of Drake, circa 100km west of Lismore.

5.3. The Company also owns the Guyra Project, comprising two ELs, one immediately east of Guyra town and the other near the township of Glencoe, 40km north of Guyra.

5.4. The table below sets out a summary of WRM‟s resources at the Mt Carrington Project.

Table 3: Resources Summary at Mt Carrington as at 4 February 2012

14

Period ended Year ended Year ended Year ended31-Dec-12 30-Jun-12 30-Jun-11 30-Jun-10

Unaudited Audited Audited Audited

Ref $ $ $ $

Finance income 5.6 51,232 194,319 385,988 20,396

Administrative expenses 5.7 (353,404) (441,720) (394,184) (36,931)Depreciation expense (18,904) (6,718) (2,934) -Employee benefits expense 5.7 (262,941) (597,936) (1,392,178) (19,960)Marketing expense 5.7 (106,995) (150,727) (140,325) (15,000)Write-down of capitalised exploration 5.8 - (1,238,103) - -

Loss before tax (691,012) (2,240,885) (1,543,633) (51,495)

Income tax benefit 771,945 202,346 -

Total loss for the period/year after tax 5.9 (691,012) (1,468,940) (1,341,287) (51,495)

Total comprehensive loss attributable to members of WRM 5.9 (691,012) (1,468,940) (1,341,287) (51,495)

Source: WRM audited financial statements for the three years ended 30 June 2012, and unaudited

management accounts for the six months ended 31 December 2012

Financial Performance

5.5. The financial performance of WRM for the three years ended 30 June 2012, and the six months ended 31 December 2012 is set out in the table below.

Table 4: Financial Performance for the three years ended 30 June 2012 and the period ended 31 December 2012

5.6. For the three years ended 30 June 2012 and the six months ended 31 December 2012, WRM has generated revenue comprising interest income from bank deposits. The Company has yet to generate operating revenue due to the current exploratory nature of WRM‟s activities.

5.7. The Company incurred $1.2 million and $723,000 in administrative, employee and marketing costs for the year ended 30 June 2012, and the six months ended 31 December 2012, respectively.

5.8. WRM undertook a review of the carrying values of capitalised exploration expenditure during the 2012 financial year. As a result of the review, the Company incurred impairment expenses of $1.2 million as a result of a write-down to the capitalised carrying value of exploration expenditure in relation to certain exploration tenements.

5.9. The Company incurred a loss of $1.5 million in the year ended 30 June 2012, compared to a loss of $1.3 million in the year ended 30 June 2011. WRM incurred losses of $691,000 for the period ended 31 December 2012.

15

As at As at As at As at31-Dec-12 30-Jun-12 30-Jun-11 30-Jun-10

Unaudited Audited Audited Audited

Ref $ $ $ $

Current assetsCash and cash equivalents 5.14 - 5.15 1,127,968 2,617,429 5,299,693 5,919,172Trade and other receivables 969,959 1,529,143 1,031,846 830,085Prepayments 39,416 107,391 4,982 42,626

Total current assets 2,137,343 4,253,963 6,336,521 6,791,883

Non-current assetsExploration and evaluation expenditure 5.12 18,836,720 17,609,850 12,419,305 7,502,411Property, plant and equipment 5.13 953,331 1,008,862 1,079,681 994,089

Total non-current assets 19,790,051 18,618,712 13,498,986 8,496,500

Total assets 21,927,394 22,872,675 19,835,507 15,288,383

Current liabilitiesTrade and other payables 126,524 447,223 371,825 187,810Employee benefits 133,020 98,591 51,775 911

Total current liabilities 259,544 545,814 423,600 188,721

Non-current liabilitiesEmployee benefits 38,682 38,682 - -Provision for rehabilitation 951,000 919,000 919,000 795,400Deferred tax liability 1,692,620 1,692,620 2,049,979 -

Total non-current liabilities 2,682,302 2,650,302 2,968,979 795,400

Total liabilities 2,941,847 3,196,116 3,392,579 984,121

NET ASSETS 5.11 18,985,547 19,676,559 16,442,928 14,304,262

EquityIssued capital 5.14 - 5.15 24,129,475 24,129,475 19,426,904 14,355,757Reserves 870,040 870,040 870,040 -Accumulated losses (6,013,968) (5,322,956) (3,854,016) (51,495)

TOTAL EQUITY 5.11 18,985,547 19,676,559 16,442,928 14,304,262

Source: WRM audited financial statements for the three years ended 30 June 2012, and the unaudited

management accounts for the six months ended 31 December 2012

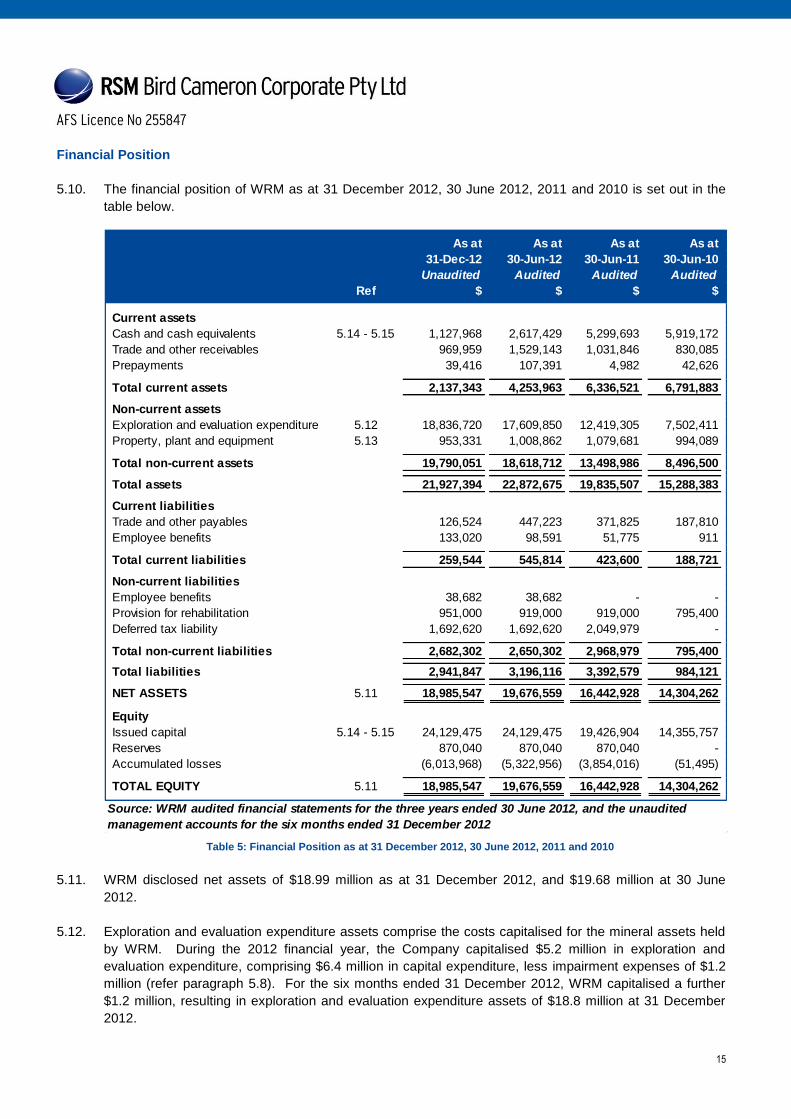

Financial Position

5.10. The financial position of WRM as at 31 December 2012, 30 June 2012, 2011 and 2010 is set out in the table below.

Table 5: Financial Position as at 31 December 2012, 30 June 2012, 2011 and 2010

5.11. WRM disclosed net assets of $18.99 million as at 31 December 2012, and $19.68 million at 30 June 2012.

5.12. Exploration and evaluation expenditure assets comprise the costs capitalised for the mineral assets held by WRM. During the 2012 financial year, the Company capitalised $5.2 million in exploration and evaluation expenditure, comprising $6.4 million in capital expenditure, less impairment expenses of $1.2 million (refer paragraph 5.8). For the six months ended 31 December 2012, WRM capitalised a further $1.2 million, resulting in exploration and evaluation expenditure assets of $18.8 million at 31 December 2012.

16

Shareholder Number of Shares %

AVALON VENTURES CORP 15,000,000 14.6%GREENSTONE PROP PL 8,441,919 8.2%SILVERSTONE INV HLDGS PL 5,203,333 5.1%GRAND SOUTH DVLMT LTD 3,033,334 3.0%S & S OLSEN PL 2,750,001 2.7%SELKIRK JAMES RONALD M 1,700,000 1.7%BANLONA PL 1,672,000 1.6%SILVERSTONE DRILLING SVCS 1,575,000 1.5%CITICORP NOM PL 1,453,820 1.4%JP MORGAN NOM AUST LTD 1,416,919 1.4%MELVILLE A G + E S 1,300,000 1.3%LAUFMANN NATALIE 1,287,501 1.3%STONE PONEYS NOM PL 984,999 1.0%LAUFMANN PHILIPPA 818,333 0.8%KATUT PL 810,000 0.8%HEWSON JOHN SUTTON + R A 800,000 0.8%STONE PONEYS NOM PL 750,000 0.7%GARDINER JAMES 750,000 0.7%OZGA S / F PL 684,999 0.7%YELLOWROCK PL 666,667 0.7%

51,098,825 49.9%Other Shareholders 51,376,706 50.1%

Total 102,475,531 100.0%

5.13. Property, plant and equipment primarily comprises machinery and motor vehicles, carried at cost less accumulated depreciation and asset impairment costs.

5.14. During the 2012 financial year and for the six months ended 31 December 2012, the Company issued a total of 30,658,332 new ordinary shares to raise $4.7 million (net of costs). Funds raised have primarily been utilised for WRM‟s exploration activities and to fund the Company‟s administrative, employment and marketing expenses. The Company‟s cash position has decreased from $5.3 million at 30 June 2011 to

$1.1 million at 31 December 2012.

5.15. The Company‟s issued share capital and cash position at 31 December 2012 does not reflect the

Tranche 1 shares issued to Avalon on 11 January 2013 to raise $1.5 million.

Capital Structure

5.16. As at 31 January 2013, WRM had 102,475,531 ordinary shares on issue, of which 49.9% were held by the top twenty shareholders. The top twenty Shareholders in WRM as at 31 January 2013 are set out in the table below.

Table 6: WRM Shareholder Summary

17

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

04

/01

/20

11

04

/02

/20

11

04

/03

/20

11

04

/04

/20

11

04

/05

/20

11

04

/06

/20

11

04

/07

/20

11

04

/08

/20

11

04

/09

/20

11

04

/10

/20

11

04

/11

/20

11

04

/12

/20

11

04

/01

/20

12

04

/02

/20

12

04

/03

/20

12

04

/04

/20

12

04

/05

/20

12

04

/06

/20

12

04

/07

/20

12

04

/08

/20

12

04

/09

/20

12

04

/10

/20

12

04

/11

/20

12

04

/12

/20

12

04

/01

/20

13

04

/02

/20

13

Volume tradedShare price ($)WRM Historical Share Price and Volume

Volume Price

28-Nov-12: WRM announces $4.5 million share placement with Avalon

8-May-12: WRM announces $0.5 million share placement with Greenstone Property Ltd and $0.56 million drilling services agreement with Silverstone Drilling Services Pty Ltd

22-May-12: The issue of shares to various substantial shareholders

3-Feb-11: WRM announces positive assay results from drilling completed at Gladstone Hill copper prospect within the Mt Carrington project

14-Nov-11: WRMannounces Entitlement Offer on a 1 share for 2 basis at an offer price of $0.15 per share

Share Price and Performance

5.17. The daily closing share price and traded volumes of WRM shares on the ASX from 1 January 2011 to 5 February 2013 is set out in the table below.

Chart 1: WRM Daily Closing Share Price and Traded Volumes from 1 January 2011 to 5 February 2013

(Source: Capital IQ)

5.18. WRM‟s share price has experienced a declining trend since the beginning of 2011. In 2011, the Company‟s share price fell from a high of $0.70 on 5 January 2011, to a low of $0.14 on 20 December 2011 and 22 December 2011.

5.19. The share price fell to $0.13 on 3 January 2012, before reaching a high $0.20 on 13 February 2012, and subsequently falling to $0.19 on 14 February 2012. Thereafter, the share price fluctuated between $0.135 and $0.175, before reaching a high of $0.180 on 4 May 2012, prior to the announcement of WRM‟s $0.5 million share placement with Greenstone Property Ltd and $0.56 million drilling services

agreement with Silverstone Drilling Services Pty Ltd.

5.20. WRM‟s share price declined from $0.18 on 4 May 2012 to reach a low of $0.074 on 27 November 2012, one day prior to the announcement of the Proposed Transaction. The share price increased to reach $0.091 on 30 November 2012, following the announcement of the Proposed Transaction.

5.21. Since the announcement of the Proposed Transaction to 5 February 2013, WRM‟s share price has

fluctuated from a low of $0.08 to a high of $0.094.

5.22. The liquidity of WRM shares is relatively low with circa 4.84% of the issued capital traded in the 60 trading days prior to the announcement of the Proposed Transaction.

18

6. Valuation Approach

Valuation Methodologies

6.1. In assessing the value of WRM prior to and immediately following the Proposed Transaction, we have considered a range of valuation methodologies. RG 111 proposes that it is generally appropriate for an expert to consider using the following methodologies:

the discounted cash flow (“DCF”) method and the estimated realisable value of any surplus assets;

the application of earnings multiples to the estimated future maintainable earnings or cashflows added to the estimated realisable value of any surplus assets;

the amount which would be available for distribution on an orderly realisation of assets;

the quoted price for listed securities; and

any recent genuine offers received.

6.2. We consider that the valuation methodologies proposed by RG 111 can be split into three valuation methodology categories, as follows:

Market Based Methods;

Discounted Cash Flow Methods; and

Asset Based Methods.

Market Based Methods

6.3. Market based methods estimate the fair market value by considering the market value of a company‟s

securities or the market value of comparable companies. Market based methods include;

capitalisation of maintainable earnings;

the quoted price for listed securities; and

industry specific methods.

6.4. The capitalisation of earnings methodology is generally considered a short form DCF, where an estimation of the Future Maintainable Earnings (“FME”) of the business, rather than a stream of cash

flows is capitalised based on an appropriate capitalisation multiple. Multiples are derived from the analysis of transactions involving comparable companies and the trading multiples of comparable companies.

6.5. The recent quoted price for listed securities method provides evidence of the fair market value of a company‟s securities where they are publicly traded in an informed and liquid market.

6.6. Industry specific methods usually involve the use of industry rules of thumb to estimate the fair market value of a company and its securities. Generally rules of thumb provide less persuasive evidence of the fair market value of a company than other market based valuation methods because they may not account for company specific risks and factors.

19

Discounted Cash Flow Methods

6.7. The DCF technique has a strong theoretical basis, valuing a business on the net present value of its future cash flows. It requires an analysis of future cash flows, the capital structure and costs of capital and an assessment of the residual value or the terminal value of the company‟s cash flows at the end of the forecast period. This method of valuation is appropriate when valuing companies where future cash flow projections can be made with a reasonable degree of confidence.

Asset Based Methods

6.8. Asset based methodologies estimate the fair market value of a company‟s securities based on the

realisable value of its identifiable net assets. Asset based methods include:

orderly realisation of assets method;

liquidation of assets method; and

net assets on a going concern basis.

6.9. The value achievable in an orderly realisation of assets is estimated by determining the net realisable value of the assets of a company which would be distributed to security holders after payment of all liabilities, including realisation costs and taxation charges that arise, assuming the company is wound up in an orderly manner. This technique is particularly appropriate for businesses with relatively high asset values compared to earnings and cash flows.

6.10. The liquidation of assets method is similar to the orderly realisation of assets method except the liquidation method assumes that the assets are sold in a shorter time frame, reflecting a distressed liquidation value. The liquidation of assets method will result in a value that is lower than the orderly realisation of assets method, and is appropriate for companies in financial distress or when a company is not valued on a going concern basis.

6.11. The net assets on a going concern method estimates the market values of the net assets of a company but unlike the orderly realisation of assets method, it does not take into account realisation costs. Asset based methods are appropriate when companies are not profitable, a significant proportion of the company‟s assets are liquid, or for asset holding companies.

Valuation methodology of mineral assets utilised by GA

6.12. GA has utilised the Comparable Transactions and the Multiple of Past Expenditure methodologies to value the Mt Carrington and Guyra Projects.

6.13. Recent comparable transactions can be relevant to the valuation of projects and tenements. GA notes that while it can be difficult to determine the extent transactions are comparable, the comparable transactions method can provide a useful benchmark for valuation purposes, further noting that the timing of comparable transactions must be considered as there can be substantial change in value over time.

6.14. Past expenditure, or the amount spent on exploration of a tenement is commonly used as a guide in determining the value of exploration tenements, and „deemed expenditure‟ is frequently the basis of joint venture agreements. GA notes that it is assumed that well directed exploration has added value to the property. This is not always the case and exploration can also downgrade a property and therefore, a prospectivity enhancement multiplier (“PEM”), which commonly ranges from 0.5 – 3.0, is applied to the

20

effective expenditure. The selection of the appropriate multiplier is a matter of experience and judgement. GA has applied a scale of PEM ranges to the exploration expenditure as follows:

PEM 0.5 – 0.9 Previous exploration indicates the area has limited potential

PEM 1.00 – 1.4 The existing (historical and/or current) data consists of pre-drilling exploration and the results are sufficiently encouraging to warrant further exploration

PEM 1.5 – 1.9 The prospect contains one or more defined significant targets warranting additional exploration.

PEM 2.0 – 2.4 The prospect has one or more targets with significant drill hole intersections

PEM 2.5 – 2.9 Exploration is well advanced and infill drilling is required to define a resource

PEM 3.0 A resource has been defined but a (recent) pre-feasibility study has not yet been completed

Selection of Valuation Methodologies

Valuation of a WRM Share prior to the Proposed Transaction

6.15. In valuing a share in WRM prior to the Proposed Transaction we have utilised the net assets on a going concern methodology and relied upon the net book value of assets and liabilities as set out in WRM‟s

unaudited financial statements as at 31 December 2012, and the valuation of WRM‟s mineral assets as set out in GA‟s report (refer Appendix 6).

Quoted Price of Listed Securities

6.16. As a secondary method of valuing a WRM share prior to the Proposed Transaction we have also considered the quoted price for listed securities methodology. In accordance with RG 111, we have assessed the value of WRM‟s shares on the basis of a 100% controlling interest.

6.17. Prices at which a company‟s shares have been traded on the ASX can, in the absence of low liquidity or unusual circumstances, provide an objective measure of the value of the company, excluding a premium for control.

6.18. As a cross-check, we have considered the quoted market price by considering the historical VWAP of WRM share and the volatility of the share price prior to and post the announcement of the Proposed Transaction.

21

As at31-Dec-12

Unaudited Low High Preferred$ Ref $ $ $

Current assetsCash and cash equivalents 1,127,968 1,127,968 1,127,968 1,127,968Issue of Tranche 1 shares to Avalon - 7.5 1,500,000 1,500,000 1,500,000Trade and other receivables 969,959 969,959 969,959 969,959Prepayments 39,416 39,416 39,416 39,416

Total current assets 2,137,343 3,637,343 3,637,343 3,637,343

Non-current assetsExploration and evaluation expenditure / Value of the Mt Carrington and Guyra Projects assessed by GA

18,836,720 7.6 to 7.9

17,570,000 44,480,000 24,660,000

Property, plant and equipment 953,331 953,331 953,331 953,331

Total non-current assets 19,790,051 18,523,331 45,433,331 25,613,331

Total assets 21,927,394 22,160,674 49,070,674 29,250,674

Current liabilitiesTrade and other payables 126,524 126,524 126,524 126,524Employee benefits 133,020 133,020 133,020 133,020

Total current liabilities 259,544 259,544 259,544 259,544

Non-current liabilitiesEmployee benefits 38,682 38,682 38,682 38,682Provision for rehabilitation 951,000 951,000 951,000 951,000Deferred tax liability 1,692,620 1,692,620 1,692,620 1,692,620

Total non-current liabilities 2,682,302 2,682,302 2,682,302 2,682,302

Total liabilities 2,941,847 2,941,847 2,941,847 2,941,847

NET ASSETS 18,985,547 19,218,827 46,128,827 26,308,827

Number of shares on issue 87,475,531 7.5 102,475,531 102,475,531 102,475,531

Assessed value per share ($) 0.188 0.450 0.257

Source: RSM analysis and GA

Prior to the Proposed TransactionAssessed value

7. Valuation of WRM

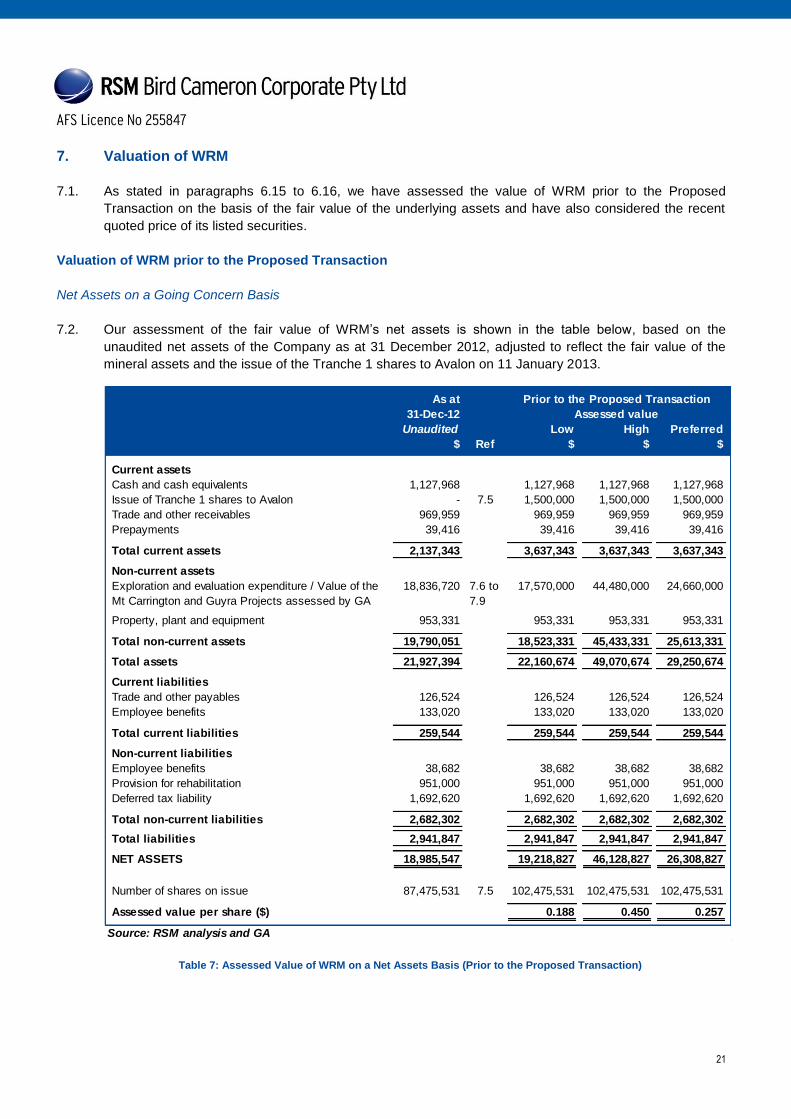

7.1. As stated in paragraphs 6.15 to 6.16, we have assessed the value of WRM prior to the Proposed Transaction on the basis of the fair value of the underlying assets and have also considered the recent quoted price of its listed securities.

Valuation of WRM prior to the Proposed Transaction

Net Assets on a Going Concern Basis

7.2. Our assessment of the fair value of WRM‟s net assets is shown in the table below, based on the unaudited net assets of the Company as at 31 December 2012, adjusted to reflect the fair value of the mineral assets and the issue of the Tranche 1 shares to Avalon on 11 January 2013.

Table 7: Assessed Value of WRM on a Net Assets Basis (Prior to the Proposed Transaction)

22

ComparableTransaction Low High Low High GA preferred

Project $'m $'m $'m $'m $'m $'m

Mt Carrington 17.11 40.29 43.62 17.11 43.62 24.00

Guyra 0.46 0.74 0.86 0.46 0.86 0.66

Total 17.57 41.03 44.48 17.57 44.48 24.66

Source: GA valuation (refer Appendix 6)

Multiple of Past Expenditure Valuation

7.3. As at the date of this Report, WRM had the following options on issue:

360,000 listed share options at an exercise price of $0.38, maturing 30 April 2014; and

6,050,000 listed share options at an exercise price of $0.38, maturing 1 August 2014.

7.4. As these options are all out of the money as at the date of this Report and, therefore, have no impact on our assessment of the fairness and reasonableness, we have excluded them from our analysis.

7.5. We have adjusted the Company‟s nets assets at 31 December 2012 to reflect the issue of the 15,000,000

Tranche 1 shares at an issue price of 10 cents per share to Avalon, to raise $1.5 million.

7.6. Exploration and evaluation expenditure are all related to expenditure on the mineral assets valued by GA. We have therefore excluded all capitalised exploration and evaluation expenditure as at 31 December 2012, and included GA‟s valuation of the Mt Carrington and Guyra Projects.

7.7. The table below sets out the range of values attributed to the Mt Carrington and Guyra Projects by GA using the Comparable Transactions and Multiple of Expenditure methodologies.

Table 8: Valuation of Mt Carrington and Guyra Projects

7.8. The range of values attributed to WRM‟s mineral assets comprising the Mt Carrington and Guyra Projects, by GA is $17.57 million to $44.48 million with a preferred value of $24.66 million.

7.9. GA considers that the Comparable Transactions method is a better guide to the value of the Mt Carrington Project than the valuation based on the Multiple of Past Expenditure. Consequently, GA‟s

preferred value for Mt Carrington is towards the lower end of the valuation range for the Mt Carrington Project as set out in Table 8 above.

7.10. We are not aware of any other indicators that the book value of assets and liabilities of WRM differ materially from their fair market value.

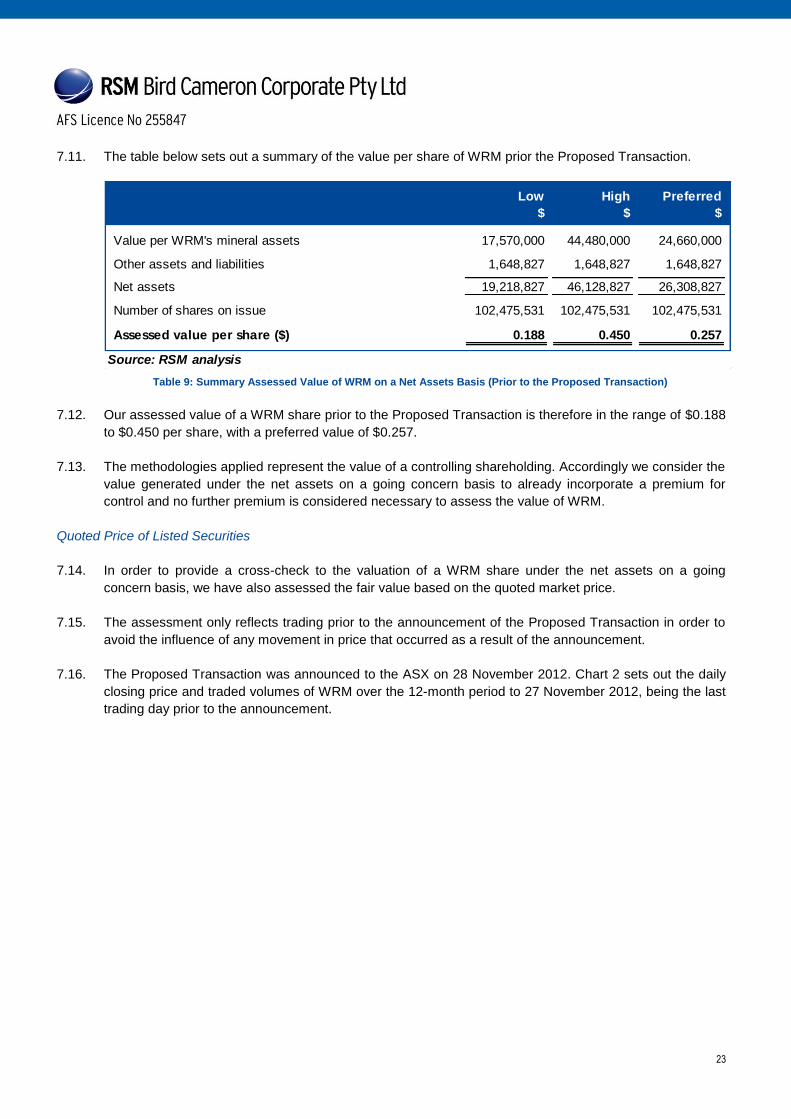

23

Low High Preferred$ $ $

Value per WRM's mineral assets 17,570,000 44,480,000 24,660,000

Other assets and liabilities 1,648,827 1,648,827 1,648,827

Net assets 19,218,827 46,128,827 26,308,827

Number of shares on issue 102,475,531 102,475,531 102,475,531

Assessed value per share ($) 0.188 0.450 0.257

Source: RSM analysis

7.11. The table below sets out a summary of the value per share of WRM prior the Proposed Transaction.

Table 9: Summary Assessed Value of WRM on a Net Assets Basis (Prior to the Proposed Transaction)