Embed Size (px)

Citation preview

RAO UES of Russia: Investment Stage of the Reform

9th Russian Economic Forum

London

24.04.2006

Anatoly Chubais Chairman of the Management Board

RAO “UES of Russia”

2

Maximum Load of Russian Power Plants

Source: RAO UES of Russia

143.5141.6

153.1

138.6142

139.1

133.5133.4130.3

135.3134.1

136.5

144.7148.3

157

160.1

100

125

150

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Th

sd M

WLoad of UES of Russia: Approaching a new consumption maximum

Electric Power Industry: New Trends

3

Regional Energy Systems : Exceeding the consumption maximum of the Soviet period

Source: RAO UES of Russia

102 104 105 106108 110 110

115121

124

160

100

110

120

130

140

150

160

170

180

Udmurti

a

Vologda

Karel

ia

Belgoro

d

Kuban

Astra

khan

Lenin

grad

Tyum

en

Kalin

ingra

d

Mosc

ow

Dages

tan

2006 vs. 1990, %

1990 = 100%

On March 28, 2006 the list of top-priority projects for 19 400 MW was approved.

Russian power industry needs badly full scale long term investments

4

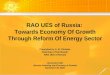

Electric Power Industry Reform: adjusting tactics while keeping strategy intact

Key Components of the Reform: Completion Status

200770% 4. Development of a markets system (for electric power, capacity, and ancillary services).

200770% 3. Setting up generation companies (WGCs and TGCs)

200770% 2. Consolidation of trunk grids and consolidation of the dispatching vertical

200690% 1. Split-up of vertically-integrated companies and separation of power generation from grids

Year of Completion% of completion Reform Components

The target of the Reform is not subject to change. The tactics for Reform completion require adjustment

The main initial target of the Reform is to launch the investment process

Main Point of Adjustment: Large-scale investments during the final stage of the Reform

rather than upon completion of the Reform.

Investments and the Reform

5

2005

2006

2007FINISH

The Finishing Line was close … Investments and the Reform

2006

2007

2008FINISH

Investment section of the road

but had to be pushed two years further along the road

6

Investments: Concept, sources and objects, volumes

Annual volumes of investments in RAO UES of Russia: 2005-2006 – about $5 bn, by 2008-2009 – about $15 bn.

Reform Concept

Investment Deployment Concept

Budgetinvestments

Competitive sectors (primarily – thermal powergeneration)

Private investments

Monopolistic sectors

Investment Deployment Concept

7

Thermal Power Generation: Mechanisms to attract investments

Investment Deployment Concept

Investment guarantee mechanism

Direct private investments

in local projects

Additional share issue of WGCs and TGCs

Private placement

Public placement

Project financing

Thermal power generation - a top priority object for investments

2/3 of electric power generation in Russia

8

Additional Share Issue of WGCs and TGCs

The logic and sequence of actionswas proposed by management and preliminarily approved by the Board of Directors.

It is up to the Russian Government to make key decision.

WGC-3, WGC-4, WGC-5, TGC-1, TGC-3, TGC-5, TGC-8, TGC-9, TGC-10

Selection of project consultants is starting as well as meetings with potential investors. Special conference for investors into above projects is planned for June 2006.

3-4 companies selected from the approved list of candidates will comprise a short list to make a decision on additional issue and placement of shares.

June 2006: RAO UES Board of Directors is expected to make a relevant decision on 3-4 companies to undergo share issue.

Long list of generation companies – top candidates for additional issue and placement of shares has been reviewed and approved by RAO UES management board In all cases,

placement of additionally issued shares is a tool for attracting investments in preselected projects with

total capacity of

6,700 MW

New Companies: Top-priority Projects

9

Additional Share Issue of WGCs and TGCs: Timeline

New Companies: Top-priority Projects

2006

'04 '05 '06 '07 '08 '09 '10-12'01-03

• Preparation and approval of the top candidates list

• Selection of consultants

• Consultations with potential investors

• Negotiations with shareholders

Preparation for share placement

Implementation of pilot projects

Selection of 3 to 4 pilot WGCs and TGCs from the top candidates list and approval of their share placement plans

10

WGC-5:Example of preparedness for share placement

Sources: MICEX; analysts reports (Aton, TroikaDialog, RenCap, MegatrustOil)

1.0

2.0

4.0

Current Mcap

19 Apr. 06

2.39

14 Sep. 05

(1st trading day)

Independent Appraiser’s evaluation

1.5

0.9

0.962

Analyst evaluation (min/max)

Prior to trading estimates

Current Mcap

$ bln

3.0 • Installed Capacity – 8,672 MW(5.53% of overall RAO UES’ installed capacity)

WGC 5

• Shares are traded on RTS, MICEX

• GDRs will be traded on London and Frankfurt stock exchanges

New Companies: Top-priority Projects

11

Reorganization of RAO UES of Russia:Pro rata principle for protection of shareholder rights

RAO UES of Russia

•Spin-off of 1-2 generation companies from the following candidates:

WGC-3, WGC-5, TGC-5

Shareholders Meeting (before the end of 2006)… Shareholders Meeting (in 2008)

• Reorganization of RAO UES of Russia by wayof split-up;• Pro rata distribution of the Company’s assetsamong shareholders;• Transfer of functions to the Government andinfrastructural entities of the energy industry

12

“The train departs in 2006-2008 . . .

. . . and the best seats are in the first car!”