Embed Size (px)

Citation preview

Past Presidents of Cement Manufacturers’ Association

Shri Dharamsey M. Khatau 1961 to 1964

Shri G.D. Somani 1965 to 1967

Shri V.H. Dalmia 1968 to 1969

Shri R.D. Shah 1970 to 1973

Shri P.K. Mistry 1974 to 1976

Shri A.K. Jain 1977 to 1978

Shri R.P. Nevatia 1979 to 1980

Shri S. Krishnaswamy 1981 to Aug’82

Shri V.L. Dutt Oct’82 to Oct’83

Shri J.R. Birla Nov’83 to Mar’87

Shri M.H. Dalmia Mar’87 to Jul’89

Shri M.N. Mehta Jul’89 to Jul’91

Shri N. Srinivasan Jul’91 to Aug’94

Shri M.C. Bagrodia Aug’94 to Sep’96

Shri N.S. Sekhsaria Sep’96 to Jun’98

Shri A.L. Kapur Jun’98 to Mar’99

Shri Y.H. Dalmia Mar’99 to Aug’99

Shri M. Karnani Aug’99 to Oct’00

Shri T.M.M. Nambiar Oct’00 to Oct’02

Shri B.L. Jain Oct’02 to Sep’04

Shri N. Srinivasan Sep’04 to Dec’06

Shri Manoj Gaur Dec’06 to Jul’07

Shri H.M. Bangur Jul’07 to Oct’09

Smt. Vinita Singhania Oct’09 to Jan’12

Shri M.A.M.R. Muthiah

President

Shri O.P. Puranmalka

Vice President

CEMENT MANUFACTURERS' ASSOCIATION

PRESIDENT

Shri M.A.M.R. Muthiah

VICE PRESIDENT

Shri O.P. Puranmalka

MEMBERS OF THE MANAGING COMMITTEE

Shri Harsh V. Lodha

Shri B.R. Nahar

Shri Rajendra Chamaria

Shri R.K. Vaishnavi

Shri Alok Patni

Shri P.S. Bakshi

Shri M.M.Venkateswar Rao

Ms. Rupa Gurunath

Shri T.S. Raghupathy

Shri Rakesh Singh

Shri V.M. Mohan

Shri R.K. Razdan

Shri Sunny Gaur

Shri Raghavpat Singhania

Dr. Shailendra Chouksey

Mrs. V.L. Indira Dutt

Shri K.C. Jain

Shri Uday Khanna

Shri P.R.R. Rajha

Shri K. Padmakumar

Shri Bhagwat Pandey

Shri M.S. Gilotra

Shri Mahendra Singhi

Shri Rajat Mukerjei

Thiru Ka. Balachandran, IAS

Shri Ratan K. Shah

Shri S.N. Jajoo

Shri K.C. Birla

Shri Krishna Srivastava

PERMANENT INVITEES

Smt. Vinita Singhania

Shri H.M. Bangur

Shri Manoj Gaur

Shri N. Srinivasan

Shri B.L. Jain

Shri Y.H. Dalmia

Shri M.N. Mehta

Shri M.H. Dalmia

Shri V.L. Dutt

SECRETARY GENERAL

Shri N. A. Viswanathan

52nd Annual Report

i

FOREWORD

The 52nd Annual Report of CMA for the year 2012-13 is in your hands. The Report covers

important developments in the Indian economy and reviews the performance of the

Cement Industry during the period under Report.

It has been yet another bad year (2012-13) for the Indian economy when its GDP growth

touched at 5%, an all-time low in the last decade as against 6.5% and 8.4% respectively in

the last two financial years. The Indian economy has been currently facing manifold

problems due to widening Current Account Deficit, increased interest rates, alarming

inflation, low investment climate particularly for infrastructure sector. Although,

Government has taken a number of bold and harsh steps to revive the economy, its

improvement in the current financial year, as per projections by certain expert agencies,

looks somewhat difficult to regain.

The gloomy scenario of the economy has severely dented the Cement Industry too as its

capacity utilization has tamed to around 72% from a comfortable level of 85% a couple of

years back. Today, the surplus cement capacity, due to mammoth mismatch between

demand and supply, is about 100 million tonnes. It means a dead investment of about

Rs.60,000/- crores, if calculated in today’s cost of setting up a million tonne cement plant.

In addition to sluggish cement demand, this Industry has been acutely suffering on

account of spiralling cost of inputs and their transportation, including cement and clinker.

The performance of the Cement Industry depends on regular and consistent supply of

Coal, Power and Railways. All these inputs are in the public sector over which the

Industry has no control.

Coal, being the main fuel, is an important input required in the manufacture of cement.

The Cement Industry continued to suffer on account of inadequate availability of coal.

Coal receipts against linkages have been showing a drop for the last 10 years while the

cement production capacity has been on the rise. The supply of linked coal during 2002-03,

which was as high as 75% of the total fuel consumption, has now come down to 35%. This

has resulted in increased dependence on costly open market purchase and coal imports. It

is, therefore, necessary for the Government that immediate steps are taken to ensure that

Cement Industry’s coal requirement, which is just 5% of the total coal production in the

country, is met in the overall interest of the Nation.

In the context of supply constraints of coal, already a few cement plants are using pet

coke, lignite and other alternate fuels in its place but are experiencing difficulties in their

ii

scaling up due to certain Technical, Policy and Regulatory and Finance related barriers

which need to be urgently addressed by the Government. The Thermal Substitution Rate

in India is very low at 0.5-1% as against 50-60% in other countries and hence usage of

alternate fuels, which entails huge investments, should be incentivized.

Logistics support has been another bottleneck. The Cement Industry has continued to

face the problems in transportation of cement, clinker, coal, fly ash etc. by Rail due to

supply constraints of Rail Wagons, lack of infrastructure facilities at Terminals and

Railway’s Policies not adequately addressing the interest of the Industry/Investors. These

factors have rendered overall transportation cost of cement by Rail costlier than road

transportation which, inter alia, resulted in sharp drop, over the last few years, in the Rail

share for cement to 35% from 57%. There is all the potential to enhance the Rail share

again to at least 50% provided the end transportation cost to the consumer is brought at

par with road transport.

Yet another major constraint for the Cement Industry is Power. Since cement production

is a continuous process, all efforts are being made by the cement plants to ensure

uninterrupted power supply and in that direction have added installed power generation

capacities to the extent of 60% of their requirement and even upto 100% in some cases.

To tide over the power shortages, cogeneration of power through Waste Heat Recovery

needs to be encouraged, and further, this technology should be granted ‘Renewable

Energy’ status for issuance of RE certificates.

Another impediment relates to supply of fly ash. Power plants which were supplying fly

ash to the Cement Industry free of cost as per the earlier Government Notification have

started charging significantly for fly ash from 2009. This has considerably enhanced the

production cost of Portland Pozzolana Cement. Cement Industry, which had already made

huge investments for effective utilization of fly ash by setting up ‘Grinding Units’ nearer

the Power Plants, deserves to be provided fly ash free of cost on the principle of ‘Polluter to

Pay’ basis, which has been adopted the world-over, in the overall interest of the Nation.

The Planning Commission’s Working Group on Cement Industry for the XIIth Five Year

Plan period 2012-17 has fixed the cement production target at 407 Mn.t. for the terminal

year (2016-17). To meet this huge and ambitions target, our Industry needs increased

Government support in respect of all inputs availability, logistics support and reduction in

the high taxation burden which currently rules at 60% of the ex-factory price. This

support to the Industry is all the more necessary if Government’s mission to enhance the

share of manufacturing in the GDP to 25% by 2020 from the present 16% is to be realized.

52nd Annual Report

iii

It gives me pleasure to mention here, that, both CMA and Cement Industry are not only

taking concrete and constructive measures for improving the performance of the Industry,

but are also finding ways to address the current burning issues of the Nation which could

also act as a ‘Growth Engine’ of the economy. One such measure, which has already been

appreciated and acknowledged by the Government, is the adoption of cement concrete

roads and white-topping in the country on large scale, as a Policy in place of the

conventional bitumen roads. What is now required is to allocate at least 50% of the total

road funds for construction of cement concrete roads and also to streamline the regular

and timely flow of funds and execution of cement concrete road projects on time. CMA,

which has brought out a considerable number of technical and promotional publications in

this field, would be happy to provide any technical help in the matter.

The Deptt. of Industrial Policy and Promotion, Ministry of Commerce and Industry, has

been highly supportive of our Industry for which, I am grateful to Secretary, Joint

Secretary, Director and Under Secretary. I am equally indebted to Secretary (Coal), Addl.

Secretary (Coal) and Joint Secretary, Ministry of Coal, Chairman, Railway Board, Member

Traffic, Advisor (T), Executive Director Traffic Transportation (S), Executive Director

Traffic Transportation (R), Ministry of Railways, Secretary, MoRT&H, Chairman, NHAI,

Secretary, Ministry of Environment and Forests, and Chairman, Central Pollution Control

Board, for their esteemed counsel, continued assistance and steady support. I also thank

the Senior Officers of various Ministries, Coal India, Singareni, Bureau of Energy

Efficiency (BEE), and Bureau of Indian Standards (BIS), Institute for Industrial

Productivity, World Business Council for Sustainable Development, Cement

Sustainability Initiative, for their co-operation.

I also wish to thank senior Members of the Managing Committee and various other CMA

Committees for their valuable advice.

Let me also take this opportunity to express my thanks to Shri N.A. Viswanathan,

Secretary General and other Officers and Staff of CMA for their valuable contribution and

continued and dedicated services in the interest of the Industry by providing various

representations, analytical reports, etc. I am sure that they will continue providing such

support in the years to come.

New Delhi (M.A.M.R. Muthiah) November 2013 PRESIDENT

Kind Attention ………

After the Order of June 2012 of the Competition Commission of India (CCI) slapping

huge fines on CMA and a few cement companies, without appropriately appreciating

the ground realities and hard facts presented to the CCI by CMA and concerned

member companies, the smooth and regular flow of statistical data to CMA by its

Members in respect of cement production and despatches became a causality and

the same came almost to a grinding halt.

This has happened for the first time in the history of CMA since its inception in

1961. As a result, CMA has not been able to compile any data concerning the

performance of its member companies for the year 2012-13 and incorporate the

information pertaining to addition of cement capacity and production of its

Members in the 52nd Annual Report of CMA.

However, in order to give a flavour of the Industry’s Pan India performance in

respect of cement production and despatches during the year under review, CMA

has drawn upon and analysed in the Report published/ web-hosted data of the Govt.

organisations, namely, Railways, Coal India, Office of the Economic Advisor, DIPP,

etc. in their respective Websites for the financial year 2012-13, which are available

in public domain.

While analysing this year’s all India cement production data of DIPP with their data

of previous year and also with CMA’s previous year’s data, as given in the Annual

Report, it will be observed that the %age growth in cement production, as per the

two sets of data, vastly differs owing to the difference in their published production

figures of last year. There is, therefore need to strengthen the process of effective

data collection base in the interest of both the Cement Industry and Govt. for their

short, medium and long-term planning.

***

52nd Annual Report

1

CEMENT MANUFACTURERS’ ASSOCIATION

52nd ANNUAL REPORT 2012-13 (Under Rule 49 – Rules & Regulations of CMA)

The Managing Committee is happy to

present its 52nd Annual Report for the

year 2012-13.

THE YEAR AT A GLANCE

Economy

The last two financial years were very

tough and challenging for the Indian

economy like other economies of the

world. In the year 2012-13, the

growth of the Indian economy

decelerated considerably and touched

an all-time low of 5% the lowest in the

last decade, as against 6.5% GDP

growth in 2011-12 and 8.4% in year

2010-11.

The country has been currently facing

widening Current Account Deficit

(CAD), which in turn has led to sharp

rupee depreciation against dollar with

its cascading effect on input costs.

India’s competitiveness, both in the

global and domestic markets, has also

been adversely impacted due to ‘high

cost’ structure arising from a host of

factors, namely, high interest rates,

increasing power and fuel costs, and

more particularly inadequate

infrastructure. With this cost

disadvantage, along with recent Free

Trade Agreements that India has

entered into with various countries,

the Indian Manufacturing Industry is

losing its edge.

The tardy growth of the economy had

impacted various segments of the

Industry. As per the Central Statistics

Office (CSO) data, industrial growth

dropped to 1% in 2012-13 as against

2.9% in 2011-12 and 8.2% in 2010-11.

Similarly, the manufacturing sector

grew by a mere 1% in 2012-13 as

compared to 2.7% in 2011-12 and

7.6% in 2010-11 respectively.

The growth on the Agricultural Sector

was also at a slower rate of 1.9% in

2012-13 as compared to 3.6% in

2011-12 and 7% in 2010-11.

The construction sector grew by 4.3% in

2012-13 as against 5.6% in 2011-12 and

8% in 2010-11.

Since India’s basic economic

fundamentals remain intact it is hoped

that growth will improve in the years

ahead, if bold and positive policy

measures are taken by the Govt.

2

Cement Industry’s Performance

The Cement Sector undeniably plays a

critical role in the economic growth of the

country and in its journey towards

inclusive growth. Cement is vital to the

construction sector and to all

infrastructural projects. The construction

sector alone contributes to over 7% of the

country’s GDP. Because of the lull in the

economy, the year 2012-13 was indeed

not a good year for the Cement Industry.

It may be recalled that the flow of

statistical feedback to CMA practically

dried up consequent upon the Order

dated 20th June 2012 of Competition

Commission of India (CCI) in Case No.

29/2010 “Builders Association of India Vs.

CMA & Ors.”. In the absence of inflow

of statistical data, CMA could not

compile and incorporate the

performance of Member Companies in

the Annual Report.

However, as per the data released by

the Office of the Economic Adviser,

Ministry of Commerce & Industry

(MoCI), the growth rate of the Cement

Industry was 8.9% in 2012-13 as

against 6.7% in the previous fiscal.

Incidentally, it needs to be highlighted

that when DIPP’s cement production

figures of 251.12 Mn.t. in 2012-13 are

compared with the 2011-12 cement

production figures of 247.45 Mn.t. of

CMA, the growth has gone up very

marginally by only 1.48%. This vast

difference in the growth rate between

the two sources only underscores, all

the more, the imperative need to

strengthen the collection and

compilation of the cement data system

in the overall interest of the cement

sector as the very basis of future

planning of the Cement Industry,

Infrastructure growth and

development of the country.

Cement Industry’s Outlook

(2013-14)

The cement sector continues to be

overwhelmed by problems such as under-

utilisation of cement capacity at around

72% due to mammoth mis-match between

the supply and cement demand, and

spiralling input costs in every area,

particularly of coal and diesel together

with the mounting transportation cost of

cement and clinker. This has significantly

enhanced the operating costs of the

Industry.

As per Prime Minister's Economic

Advisory Council (PMEAC) projections,

economic growth rate will be 5.0 - 5.5 per

cent in the current fiscal i.e. 2013-14 on

the expected improvement in the

performance of agriculture and

manufacturing sectors. Government is

also making efforts to remove the

bottlenecks that are delaying

infrastructure projects. If the

recommendations made by the Govt. in its

Twelfth Five Year Plan for National

Manufacturing Policy (NMP); Delhi

Mumbai Industrial Corridor (DMIC)

52nd Annual Report

3

Project and Policy reforms to promote

foreign direct investment (FDI) are

implemented on time, the projected

growth rate would be achieved.

Given the Government's thrust on

inclusive growth and the need to put

infrastructural projects on the Rail again,

cement demand is expected to remain firm

and rise in the near future. While the

short-term does present unique

challenges for the Industry, the mid to

long-term offers, good prospects, for the

cement growth.

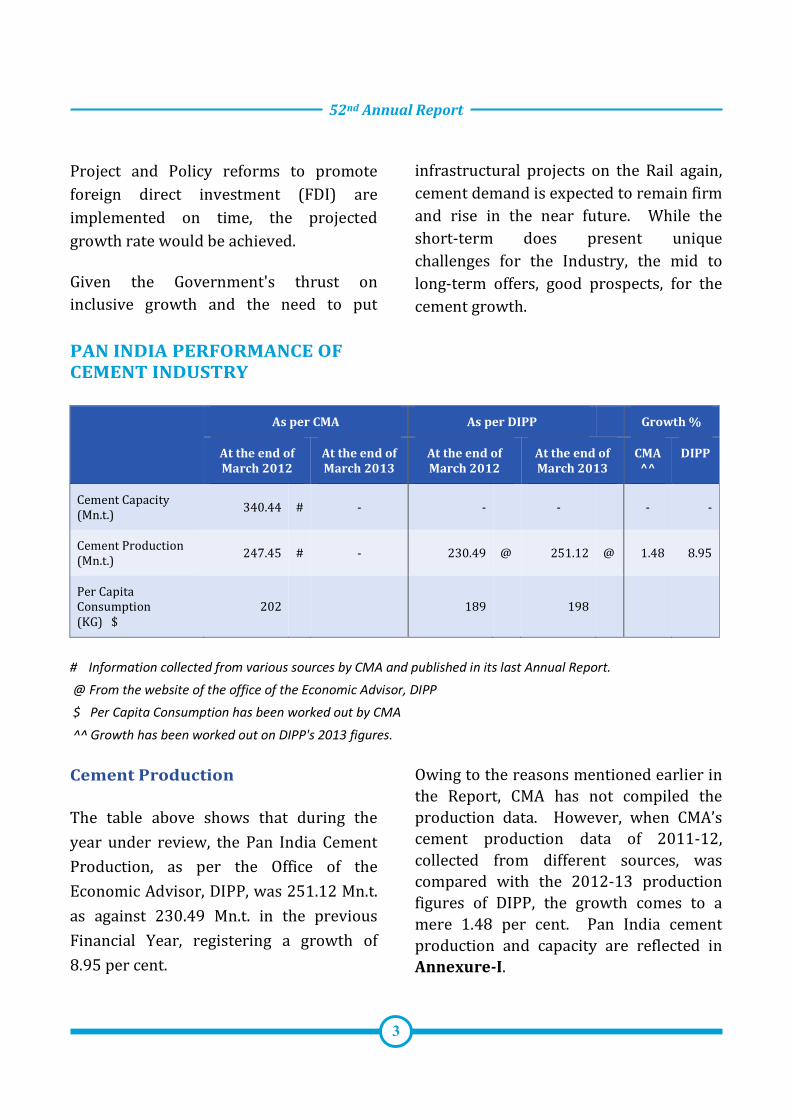

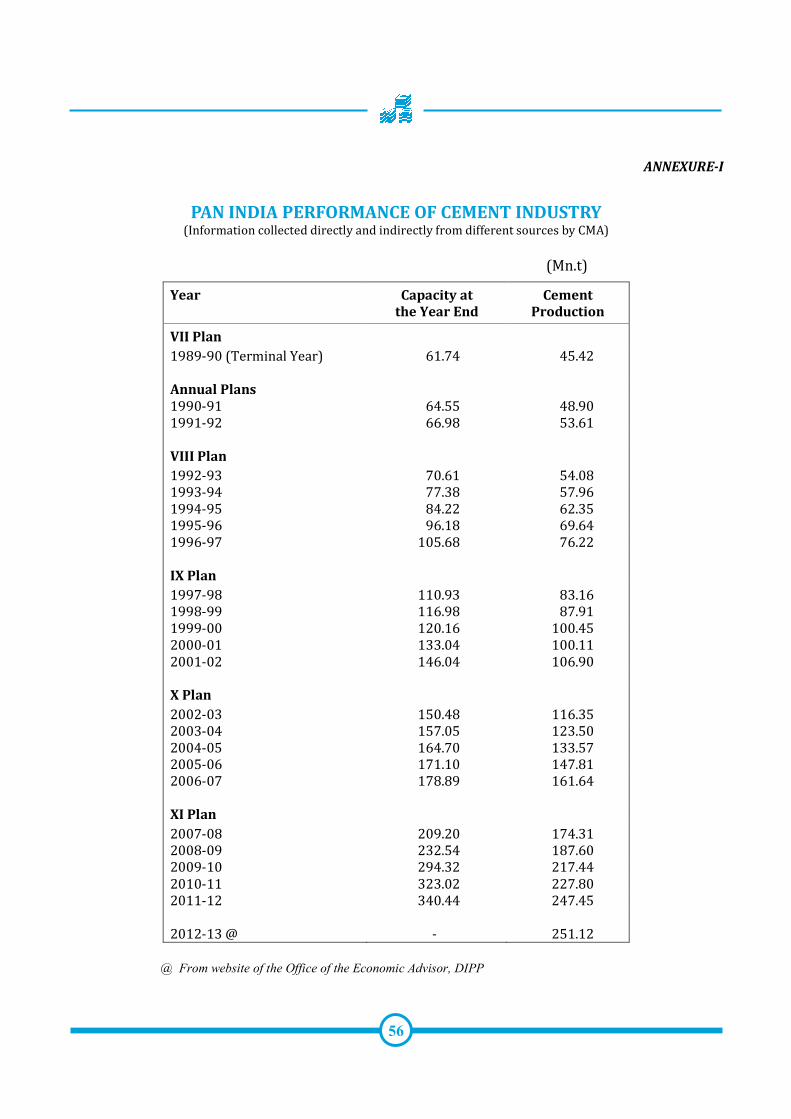

PAN INDIA PERFORMANCE OF

CEMENT INDUSTRY

As per CMA As per DIPP Growth %

At the end of

March 2012 At the end of

March 2013

At the end of

March 2012 At the end of

March 2013 CMA

^^

DIPP

Cement Capacity (Mn.t.)

340.44 # - -

-

- -

Cement Production (Mn.t.)

247.45 # - 230.49 @ 251.12 @ 1.48 8.95

Per Capita Consumption (KG) $

202

189

198

# Information collected from various sources by CMA and published in its last Annual Report.

@ From the website of the office of the Economic Advisor, DIPP

$ Per Capita Consumption has been worked out by CMA

^^ Growth has been worked out on DIPP's 2013 figures.

Cement Production

The table above shows that during the

year under review, the Pan India Cement

Production, as per the Office of the

Economic Advisor, DIPP, was 251.12 Mn.t.

as against 230.49 Mn.t. in the previous

Financial Year, registering a growth of

8.95 per cent.

Owing to the reasons mentioned earlier in

the Report, CMA has not compiled the

production data. However, when CMA’s

cement production data of 2011-12,

collected from different sources, was

compared with the 2012-13 production

figures of DIPP, the growth comes to a

mere 1.48 per cent. Pan India cement

production and capacity are reflected in

Annexure-I.

4

MEETINGS OF THE MANAGING

COMMITTEE AND HIGH POWER

COMMITTEE

In order to review and deliberate

on the issues relating to the

problems and growth of the

Cement Industry, Four meetings of

the Managing Committee and an

equal number of High Power

Committee meetings were held

during 2012–13.

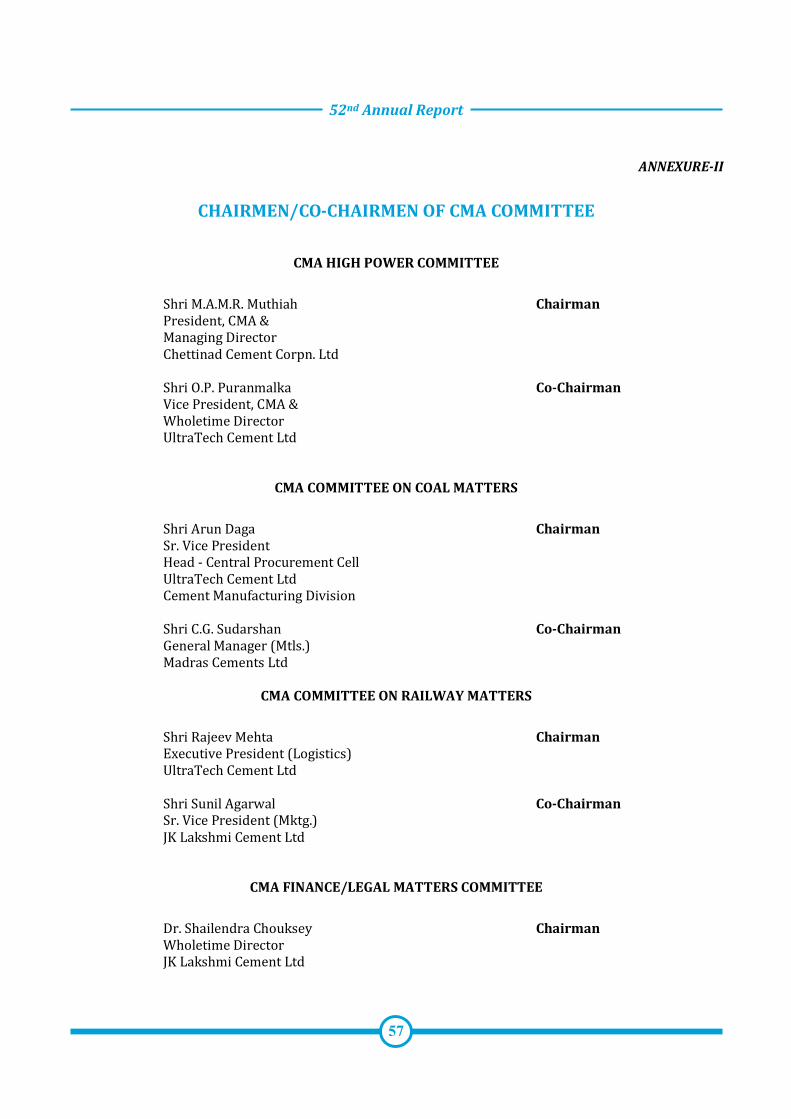

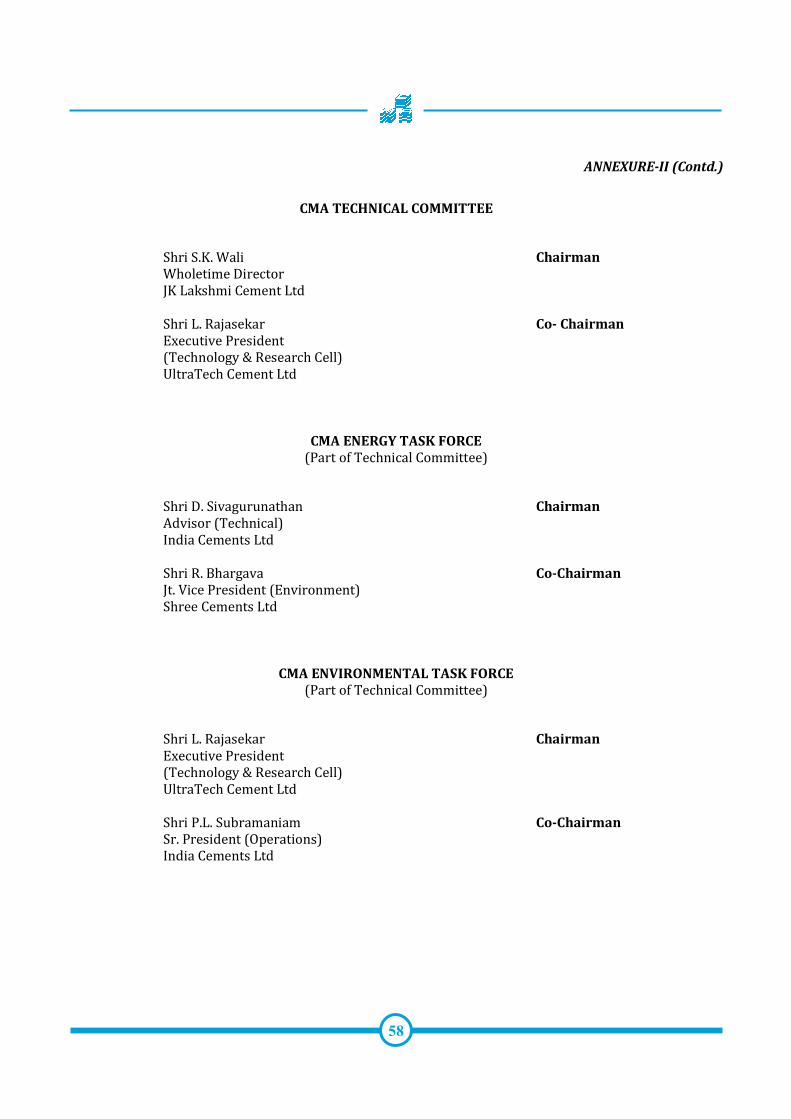

CMA COMMITTEES

The following Committees

continued to render assistance to

the Management of the Association

during the year 2012-13 to address

various emerging issues and

problems, affecting the Cement

Industry.

� CMA High Power Committee.

� CMA Committee on Coal

Matters.

� CMA Technical Committee.

� Energy Task Force.

� Environmental Task Force.

� CMA Finance/ Legal Matters

Committee.

� CMA Committee on Railway Matters.

Names of the Chairmen/Co-chairmen of

the above Committees are indicated in

Annexure-II.

MEETING WITH SECRETARY (DIPP),

MINISTRY OF COMMERCE AND

INDUSTRY

A delegation of CMA, led by our President,

Shri M.A.M.R. Muthiah, called on Shri

Saurabh Chandra, and had an interactive

meeting with him in May 2012, after his

taking over the reins of Secretary (DIPP),

Ministry of Commerce and Industry.

CMA Managing Committee Meeting

held on 16th September 2013

Seated on Dais ( L to R) Shri BL Jain, Past President, CMA, Shri OP Puranmalka,

Vice President, CMA, Shri MAMR Muthiah, President, CMA and Shri NA

Viswanathan, Secretary General, CMA

CMA Managing Committee Meeting

held on 18th December 2012

Seated on Dais ( L to R) Shri NA Viswanathan, Secretary General, CMA, Shri

MAMR Muthiah, President, CMA, Shri OP Puranmalka, Vice President, CMA and

Shri KC Jain, Sr. President, Kesoram and Vasavadatta Cement

52nd Annual Report

5

During the meeting, the President briefed

the Secretary about the overall scenario of

the Indian Cement Industry – Its problems

and prospects; the Industry’s role and

contribution to the infrastructure

development; economic growth and to the

National exchequer through various taxes

and levies and for the amelioration of the

conditions of the weaker sections of the

society through CSR activities in the field

of Education, Health, Environment, Water

Supply, Adoption of Villages, etc. In this

context, CMA had handed over a

“Presentation on Cement Industry” to the

Secretary.

CEMENT INDUSTRY’S PRE-BUDGET

MEMORANDUM – 2013-14

In November 2012, CMA submitted

comprehensive Pre-Budget Memorandum

2013-14 – Cement Industry to Shri P.

Chidambaram, Hon’ble Finance Minister.

The Memorandum covered

comprehensively various issues which are

briefly discussed hereunder:

Uniform and Specific Rate of Excise

Duty on Cement: Elaborating on the long

and established history of specific rate of

excise duty on cement which worked

efficiently up to 28.2.2011, CMA stressed

that the incidence of Excise Duty on

cement continued to be still on the higher

side for consumers, other than

industrial/institutional buyers, as an

additional specific rate of duty of Rs.120/-

per tonne is payable by them. Also the

basis of levying Excise Duty is different i.e.

12% on RSP less 30% of RSP (as

abatement) for packaged cement requires

MRP to be declared and 12% on

Transaction Value for sale to

industrial/institutional consumers. Thus,

the current regime makes for different

sets of duties per tonne of cement payable

by a producer on any given day. The

excise duty rates on Cement are one of the

highest and next only to luxury goods such

as cars. By contrast, other core industries

such as coal and steel attract duty at

around 5%.

It is well-known that the industry suffers

from excess of surplus capacity of cement

in the country and cement market is on a

bearish trend. In order to achieve the

expected growth of the Cement Industry

the Government may kindly reduce excise

Particulars New Duty Structure from

17.03.2012 vide Notification 12/2012

read with entry No. 52 of

Notification 12/2012

dated 22.03.2012

(Packaged

Cement)

- [ (RSP Less 30%

of RSP) x12%]

Add Rs.120 PMT

(Packaged

Cement on

which MRP is

not required to

be declared

and thus not

declared)

Cement cleared

in Bulk to

Industrial /

Institutional

buyers

12% of

Transaction Value

Loose Cement - 12% of

Transaction Value

Clinker - 12% of

Transaction Value

6

duty on cement and clinker and bring it at

par with other core and infrastructure

industries. The excise duty rate be

rationalized from 12% to 6-8% and scrap

the specific rate of duty of Rs. 120/- per

tonne in the interest of common man’s

housing needs. Besides, the duty structure

be simplified to be made applicable either

on specific rate per MT or on ad-valorem

basis and without relating to MRP etc.

Our submissions on other important

issues included:

• Excise Duty on Coal, Lignite, Coke, Fly

Ash etc.: Levy of this duty of

2%(except on Coal, on which duty is

1%) needs to be withdrawn or Cenvat

credit be made available for the duty

paid.

• Customs Duty on Pet Coke, Gypsum

& Other Inputs: Import duty on pet

coke, gypsum (2.5%) and other input

materials used in production of cement

be scrapped.

• Levy of Customs Duty on Cement

Imports: To provide a level-playing

field, basic customs duty be levied on

cement imports into India.

Alternatively, Import duties on goods

required for manufacture of cement be

abolished and freely allowed.

• Withdrawal of Excise Duty on Fly

Ash: There is no change in the process

of generation of fly ash viz. a waste

generated on burning coal in the boiler

(Supreme Court decision in the case of

Union of India Vs. Ahmedabad

Electricity Co. Ltd.). Therefore, the fly

ash generation should not be treated as

manufactured product and no Excise

Duty on fly ash be levied.

• Treatment of Waste Heat Recovery

as Renewable Energy Source: To help

the Industry in its endeavour to

produce more environment-friendly

energy, Waste Heat Recovery Plants

which need substantial capital

investments, be treated as Renewable

Energy Source, to enable Cement

Industry to derive more energy from

the same energy resource which is akin

to green energy.

• Abolition of Import Duty on Tyre

Chips : To increase supply of energy

sources as well as for conserving the

domestic energy sources it is necessary

that import of tyre chips be allowed by

removing it from the Negative list and

also reducing tyre chips by reducing

import duty on the same to ZERO in

the National interest.

• Classifying Cement as “Declared

Goods”: Cement be stipulated as

“Declared Goods” under Section 14 of

the Central Sales Tax Act, so that it is

put on an equal footing with other core

sector goods like coal and steel.

• Tax Exemption to Certified Emission

Reduction (CER) Credits Under

Clean Development Mechanism: To

motivate the corporate sector for

reduction in Carbon Emission, receipt

from the CER credit be exempted from

Tax.

52nd Annual Report

7

• Project Import: Basic Custom Duty rate in case of Project Import be brought down to 3% from the current 5%.

• Goods and Service Tax (GST): Before introduction of GST, Single Rate of Tax; any change in the statute of any state be made only with the concurrence of all states; Criteria/process for availing Input Tax Credit be made simple and unambiguous, Creation of a Common Dispute Resolution Mechanism throughout all the States and One Common Authority for all the States be established for Advance Ruling; after implementation of GST, Continuation of various Central/State Level exemptions and incentives currently being enjoyed under Excise/VAT laws for the remaining unexpired period be continued.

• Stimulus to the Sectors which are

Major Users of Cement:

Fiscal Support to Housing and Roads

- This could accelerate the demand for

cement quite substantially. Given the

housing shortages in rural and urban

areas and given the increase in the cost

of affordable house, income tax relief

for interest paid on the house building

loans be extended from Rs. 1.5 lakh to

Rs. 4 lakh per annum.

Using Cement Concrete Technology

for Roads - All new expansions in the

National and State Highways be made

of Cement Concrete as a Policy. To

begin with, this could be 30% of total

allocations. All existing city roads

having bitumen surface be converted

gradually to cement concrete and new

ones should preferably be constructed

with cement concrete technology. All

connecting roads in villages be done

with cement concrete technology.

Pre-Budget Meeting for Union Budget,

2013-14

The Department of Revenue convened

Pre-Budget meeting with Trade and

Industry Associations to discuss

suggestions/ recommendations in respect

of tax issues pertaining to different sectors

for the Budget 2013-14 under the

Chairmanship of Ms. Praveen Mahajan,

Chairperson of CBEC, Department of

Revenue, Ministry of Finance, Government

of India.

CMA delegation led by President,

Shri M.A.M.R. Muthiah accompanied by

representatives of JK Lakshmi Cement Ltd,

UltraTech Cement, Chettinad Cement,

CMA, India Cements Ltd, JK Cement, etc.

attended the meeting and put forth the

problems/issues and reiterated the

suggestions made in the comprehensive

Pre-Budget Memorandum submitted to

the Hon’ble Finance Minister in November

2012 referred to above.

Meeting by Chairman, CBEC,

regarding Revenue

Performance/Projections

In January, 2013 Chairman, CBEC, had

called a meeting of the representatives of

Cement Industry in the context of revenue

8

performance and provisional revenue

projections for the year 2012-13. The

meeting was attended by the

representatives of CMA, JK Lakshmi

Cement, UltraTech Cement, and Century

Textiles and Inds. Ltd. During the meeting,

conveying the concerns of Hon’ble Finance

Minister about the need for increased

revenue realization of 33% overall

compared to the previous year’s revenue,

Chairman mentioned that for the Cement

Industry the revenue has increased by

27% so far and requested that the

Industry may keep this in mind and co-

operate in increasing the excise revenue

as much as possible to achieve the target

of the Government.

CMA mentioned that CMA has stopped

compiling and providing information of

individual plants in view of the Orders of

Competition Commission of India and its

findings on the issue of cartelization

against CMA and Cement Industry and that

an Appeal against the Order is pending

with the Competition Appellate Tribunal.

CMA further took the opportunity to stress

on the difficulties in the current excise

regime and the reduced growth rate of

Cement Industry as a result of poor

demand due to poor growth in

infrastructure projects. It was also pointed

out that low GDP growth is impacting the

Cement Industry’s growth.

Union Budget 2013-14

Hon’ble Finance Minister, Shri P.

Chidambaram presented the Union Budget

2013-14 in the Parliament on 28th

February, 2013.

A view of CMA Managing Committee Meeting

52nd Annual Report

9

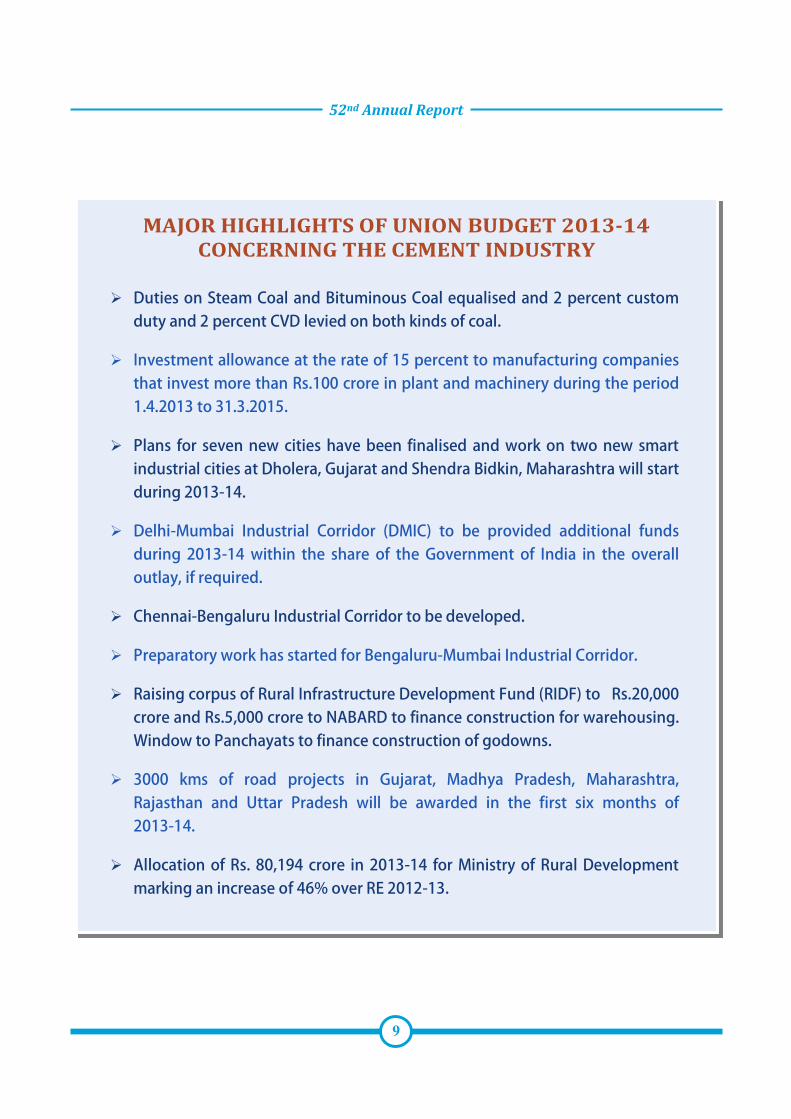

MAJOR HIGHLIGHTS OF UNION BUDGET 2013-14

CONCERNING THE CEMENT INDUSTRY

� Duties on Steam Coal and Bituminous Coal equalised and 2 percent custom duty and 2 percent CVD levied on both kinds of coal.

� Investment allowance at the rate of 15 percent to manufacturing companies that invest more than Rs.100 crore in plant and machinery during the period 1.4.2013 to 31.3.2015.

� Plans for seven new cities have been finalised and work on two new smart industrial cities at Dholera, Gujarat and Shendra Bidkin, Maharashtra will start during 2013-14.

� Delhi-Mumbai Industrial Corridor (DMIC) to be provided additional funds during 2013-14 within the share of the Government of India in the overall outlay, if required.

� Chennai-Bengaluru Industrial Corridor to be developed.

� Preparatory work has started for Bengaluru-Mumbai Industrial Corridor.

� Raising corpus of Rural Infrastructure Development Fund (RIDF) to Rs.20,000 crore and Rs.5,000 crore to NABARD to finance construction for warehousing. Window to Panchayats to finance construction of godowns.

� 3000 kms of road projects in Gujarat, Madhya Pradesh, Maharashtra, Rajasthan and Uttar Pradesh will be awarded in the first six months of 2013-14.

� Allocation of Rs. 80,194 crore in 2013-14 for Ministry of Rural Development marking an increase of 46% over RE 2012-13.

10

Post Budget Memorandum-2013-14

Your Association vide letter of 7th March

2013 to Shri P. Chidambaram, Hon’ble

Finance Minister while congratulating him

on his forward looking approach and the

bold measures announced in the Union

Budget to bring back the GDP on its

normal growth path, also re-stressed that

the overall tax burden on the Cement

Industry has been very high, more than

even luxury items (60% of the ex-factory

price). The Cement Industry was

expecting some taxation relief in the

Budget. However, additional burden has

been imposed on the Cement Industry by

levying 2 per cent custom duty and 2 per

cent CVD on steam coal, the prime raw

material needed in the manufacture of

cement. This levy would further increase

the cost of cement by around Rs. 16 per

tonne in case of units using imported coal.

CMA requested the Hon’ble Finance

Minister to withdraw this levy and also to lower the taxation burden of the Cement Industry by 20-25% from its present level of taxation in the interest of faster growth

of the economy.

It was also submitted that while a good measure has been introduced in Budget 2013-14 by way of investment allowance

of 15% on the assets (plant & machinery) acquired and installed in 2013-14 and 2014-15 and this will definitely help in taking investment decision and revamping of investment cycle in the Indian Economy, the Cement Industry will not be substantially benefited with the condition of assets being acquired and installed in

these two years period, since a cement plant normally takes 3-4 years period for commissioning. To boost the investment in the Cement Sector and to avoid any ambiguity, the Investment Allowance was urged to be made available for the assets (plant & machinery) installed during that year similar to the earlier provision of Section 32 (A), apart from increasing the investment period to 4 years.

It was further highlighted that any matter which goes to Excise/Customs Tribunal takes lot of time in disposal extending to 3-5 years. In a number of cases, the Tribunal gives the stay order up to the

disposal of the cases. However, with the new amendment, all the Stay Orders will stand vacated after 365 days, whether the appellate Tribunal has passed the final order or not. This creates hardship on the part of assessee. CMA, therefore,

requested that either there must be a provision that a matter referred to the Tribunal should be decided within a period of one year or if it is not decided by then, once the stay is granted, it should continue till the final disposal of appeal by the Tribunal, based on the original Stay Order passed by the Tribunal.

Welcoming the thrust and the

considerable fund allocations for the Road

development, including Industrial

Corridors and rural development, CMA

also urged that the funds allocated need to

be used for the construction of Techno-

economically superior Cement Concrete

Roads over conventional Bitumen Roads,

which deteriorate very fast, particularly

after the rains.

52nd Annual Report

11

INCREASE IN INPUT COSTS

Cement manufacturers had to shoulder

the burden of input cost hikes on account

of increase in Cost of Fuel, Railway Freight,

Customs Duty and CVD on Steam Coal, etc.

during the year 2012-13.

INFRASTRUCTURE

Cement is an important material for

any construction and is the most

essential infrastructure input.

Infrastructure development of roads,

housing, ports, airports, etc. heavily

depend on cement. However, there is

no gainsaying that the performance of

the Cement Industry itself depends

critically on regular and consistent

supply of Coal, Power and availability

of Rail transportation and these key

infrastructure inputs for the Cement

Industry are in the public sector

domain over which the Industry has

no control.

Coal is the main fuel required in the

production of cement and power is

essential for various operations of

plants. The Railways provide the

logistics support for inward

transportation of coal, gypsum and

other inputs to the cement factories

and for outward movement of cement

and clinker.

COAL

Coal is of vital importance to the

Cement Industry as coal is the

principal fuel and accounts for

25-30% of the total cost of cement

production.

During the year under review, CMA

and CMA Committee on Coal Matters

had regular interaction with various

Government Authorities on coal-

related issues. These are elaborated

below :

Signing Fuel Supply Agreements

(FSAs) against the Long Term

Linkages

A CMA delegation met with Chairman, CIL

on 8th April 2013 in Kolkata, wherein, the

signing of the FSA with SECL and other

related issues were discussed when other

senior officials were also present.

Chairman, CIL, assured that minor

procedural discrepancies could be

resolved with mutual discussion with

SECL.

As required, our Letter of Assurances

(LOA) holding Member companies/units,

had long back furnished all the necessary

documents against the specified

Milestones. Thereafter, even the revised

documents, as required vide CGM (S&M),

CIL’s letter dated 17.1.2011 were again

submitted in April/May 2011. This was

followed by one-on-one meeting between

the LOA holders and SECL between

1.10.2011 and 15.10.2011 at Bilaspur.

It was expected that after meeting with

Chairman, CIL on 8th April 2013. SECL

would have signed the FSAs with most of

the cement plants but regrettably this did

not happen and the FSAs against these

12

LOAs have not been concluded by SECL till

date. SECL further abruptly issued notices

for withdrawal/cancellation of LOAs and

encashment of “Commitment Guarantee”

and “Additional Commitment Guarantee”

without giving any opportunity to our

member units.

CMA took up this issue with CMD, SECL;

Secretary, DIPP; Secretary, Ministry of

Coal and also held meeting with Joint

Secretary, Ministry of Coal to seek

immediate relief in the matter and

requested for case-to-case review by SECL,

with the concerned LOA holders against

the Notice for withdrawal/cancellation of

LOA. It was also requested not to take any

coercive action for encashment of

“Commitment Guarantee” and “Additional

Commitment Guarantee” pending grant of

an opportunity for a meeting of CMA with

SECL for presentation of their case. The

affected member units also approached

the Hon’ble High Court at Bilaspur with

Writ Petitions. The Hon’ble Court

considered the matter on 10th July 2013

and stayed the operation of the notice of

forfeiture of “Commitment Guarantee” and

“Additional Commitment Guarantee” and

also passed the following order:

“The petitioners are at liberty to

make a fresh representation to

the Committee constituted for

examination of the

representations against

cancellation notices issued in

cement LOA cases, if so advised,

within a period of one week from

today. It is, thus, directed that till

the representations of the

respective petitioners are decided

by the Committee, the impugned

notices dated 11.06.2013 shall not

be enforced. It is for the

respondents to take appropriate

steps in accordance with law,

thereafter.”

Renewal of Fuel Supply Agreement

(FSA)

The FSAs which were signed by our

member Cement Companies with the Coal

Companies and remained in force for a

period of five years expired after March

2013 onwards. Latest Information/inputs

were provided to the Member Cement

Companies for renewal of FSA who were

also apprised of the terms of the FSA

towards their entitlement for the ACQ, in

respect of Cement and Captive Power

Plants.

Compulsory Purchase of 25%

Higher Grades of Coal

Cement plants, receiving the coal through

FSA, are being obliged to compulsorily

purchase 25% of higher Grades of coal for

their Kilns and CPPs and accordingly the

revised clauses are being included in the

renewed FSAs. For supply of higher grades

of coal of 1 tonne, adjustment of 1.5

tonnes of lower grades of coal shall be

made and the ACQ will be reduced

accordingly. Non acceptance of higher

52nd Annual Report

13

grades of coal shall be considered as

“Deemed Delivered Quantity” by the Coal

Company.

CMA raised this issue before CMD SECL,

Director Marketing, CIL, Kolkata, Secretary

(DIPP), Ministry of Commerce & Industry,

Secretary, Ministry of Coal, Cabinet

Secretary, & for modification of the

aforesaid directives of CIL and acceptance

of higher grades made optional for the

purchaser. CIL has since reviewed the

aforesaid clause of compulsory purchase

of 25% of higher grade of coal and

clarified to all the subsidiary companies

that no quantity adjustment for the supply

of higher grade of coal wherever available

to the non-power companies is to be

made. Thus, the obligation of compulsory

purchase of 25% higher grade of coal has

been modified.

Coal Supplies to the Extent of 80%

of the Entitled Quantity for Booking

of Coal by Cement Sector

SECL, Bilaspur, restricted coal supplies to

the extent of 80% of the entitled quantity

for booking of coal by Cement Sector with

effect from 1st April 2013. This issue was

taken up with Chairman, CIL; Director

(Mktg.), CIL; CMD, SECL; Ministry of

Commerce & Industry, DIPP; and Ministry

of Coal to review trigger/materialization

level for supplies to cement sector during

2013-14.

Your Association’s efforts in this regard

bore fruit and SECL was constrained to

restore 100% booking with effect from

1st June 2013.

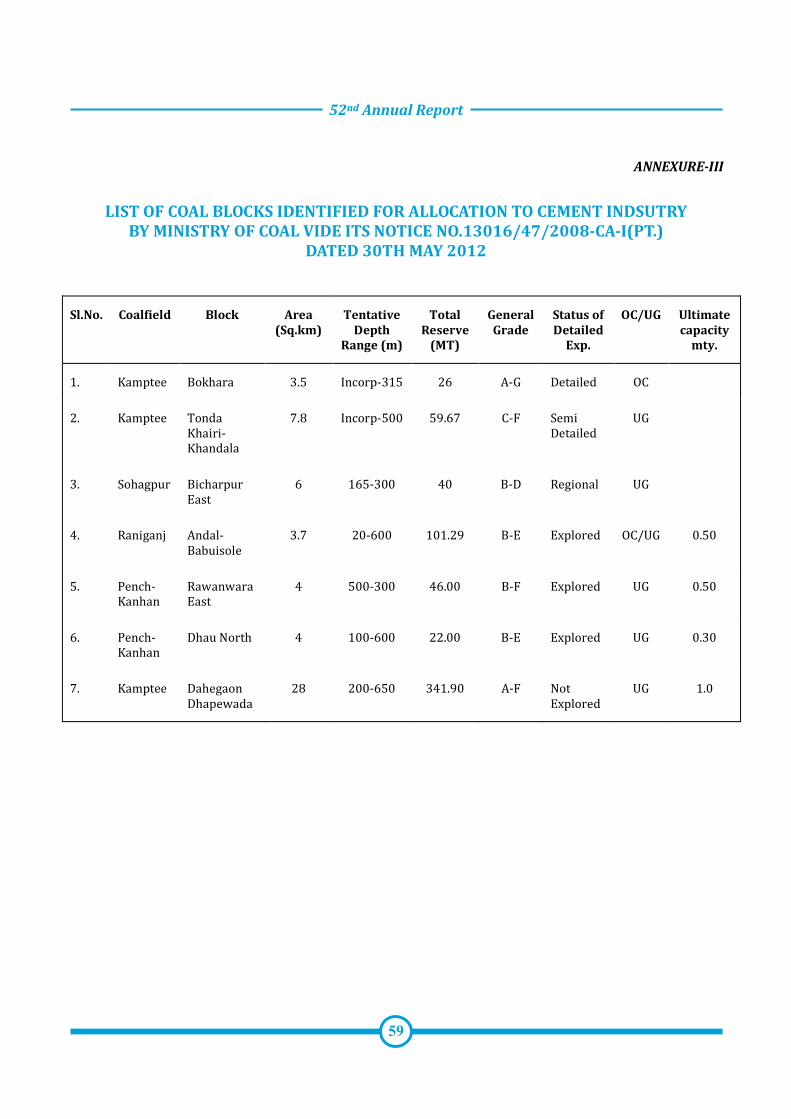

Coal Blocks for Cement Industry

CMA and the Cement Industry had taken

up with the Ministry of Coal and other

authorities, time and again, for specifically

earmarking coal blocks for allocation to

Cement Industry. Ministry of Coal by its

Notice of 30th May 2012 earmarked only 7

coal blocks for allocation exclusively for

the Cement Industry. These are listed at

Annexure-III.

Third Party Sampling Agency for

Sampling and Analysis of Coal for

the CMA’s Member Cement Cos.

In the Conference on “Power Sector – A

Way Forward” held in February 2013 at

New Delhi, Hon’ble Minister of State

(Independent Charge), Ministry of Power,

Shri Jyotiraditya Madhavarao Scindia

stated that there is a proposal of the

Ministry of Coal to engage independent

Third Party Sampling Agency for sampling

and analysis of coal in view of the demand

from the public sector power utilities and

power generating Companies.

In this context, CMA in its letter of March

2013 addressed to Secretary, Ministry of

Coal, highlighted the serious concern our

Member Cement Companies have been

consistently expressing about the poor

quality of coal being supplied by the coal

companies (Coal India Ltd., as also by

Singareni Collieries Co. Ltd)., and the

extensive variation in the declared GCV

14

and the actual GCV measured at the

cement plant being observed as a regular

feature.

CMA, therefore, requested the authorities

to extend the proposed facility of

engagement of independent third Party

Sampling Agency for sampling and

analysis of coal for cement sector

consumers as well, subject to their option,

for such facility without any embargo on

the minimum quantity of 4 lakh tonnes.

Strict Regulatory and Monitoring

Mechanism of Coal for Benefit of the

Consumers

In September 2012, Ministry of Commerce

& Industry sought CMA’s comments on the

“observations” made in the recent Report

of Comptroller and Auditor General of

India (CAG), “that there is need for strict

regulatory and monitoring mechanism to

ensure that the benefit of cheaper coal is

passed on to the consumers” in cases

where coal blocks have been allocated to

companies engaged in the production of

cement.

Based on the views of the Member

Companies, CMA replied on 26th

September 2012 as under :

• The assumption that the coal obtained

from coal block will be cheaper is not

correct; more so when against the

limited coal blocks allotted to Cement

Sector, clearances of various statutory

authorities are still pending at various

stages, despite deadlines having been

set by Ministry of Coal, for commencing

of production of cement from such coal

mines. The situation has been further

compounded by the coal companies

resorting to reduction in FSA quantity

by 25% by quoting a scheme of

tapering of linkages. Instead of taking

a realistic view about the ground

realities regarding delay in clearances,

the aforesaid cut on linkages has been

applied. In fact, compared to the

notified prices of coal supplied through

FSA, the coal from a coal block could

cost more and it may even vary from

time to time and area to area.

• In view of the short availability of

linked coal supplied under FSA, the

cement cos. have, presently, to source

more than 60% of its fuel requirement

in the form of E-auction coal, Imported

coal, and pet coke etc. The

procurement cost of fuel from other

sources is very high, as compared to

notified prices of CIL/SCCL.

Consequently, the input cost of fuel not

only becomes high but keeps on

fluctuating. Thus, the average cost of

fuel is much higher than the notified

price of coal supplied through FSA.

This aspect also needs to be kept in

mind.

• Cement is sold in open market and its

prices are accordingly governed by

market forces. Reduction in cost of

production of cement on account of

input costs, including transportation,

etc., will automatically bring a

downward impact on market prices in

a competitive market.

52nd Annual Report

15

In the light of the above, CMA contended

that any regulatory and monitoring

mechanism for such market driven

commodities does not appear feasible or

practicable.

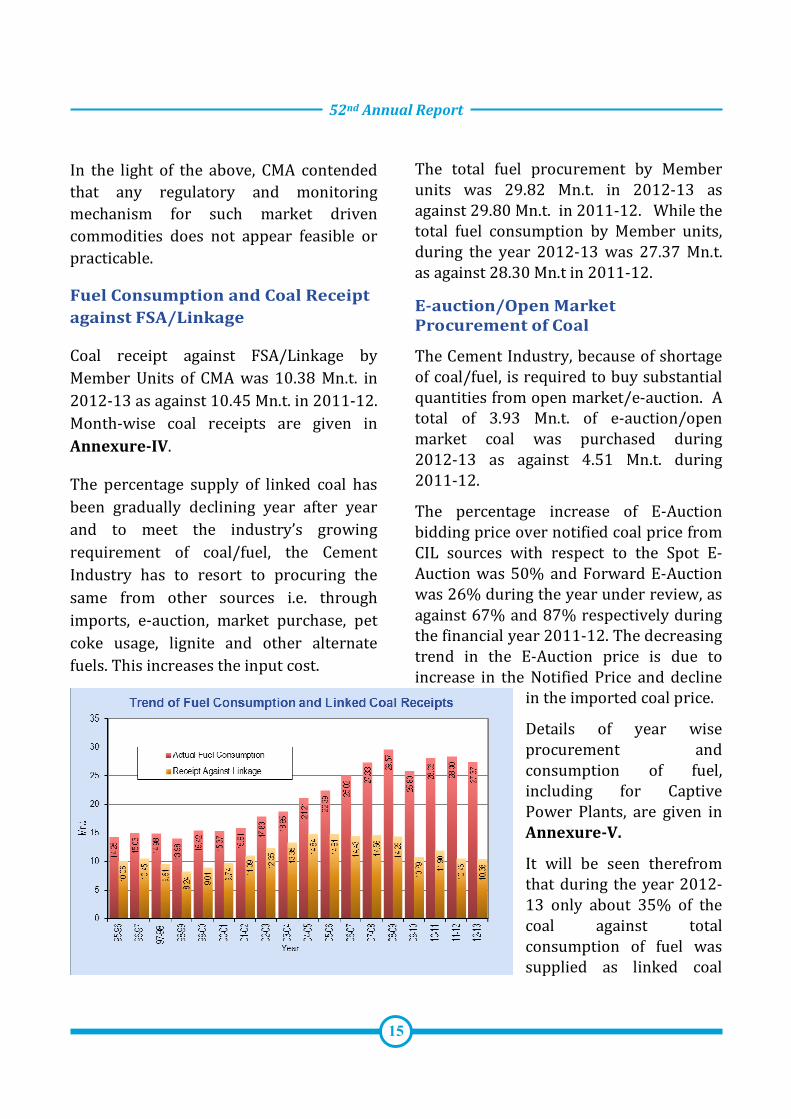

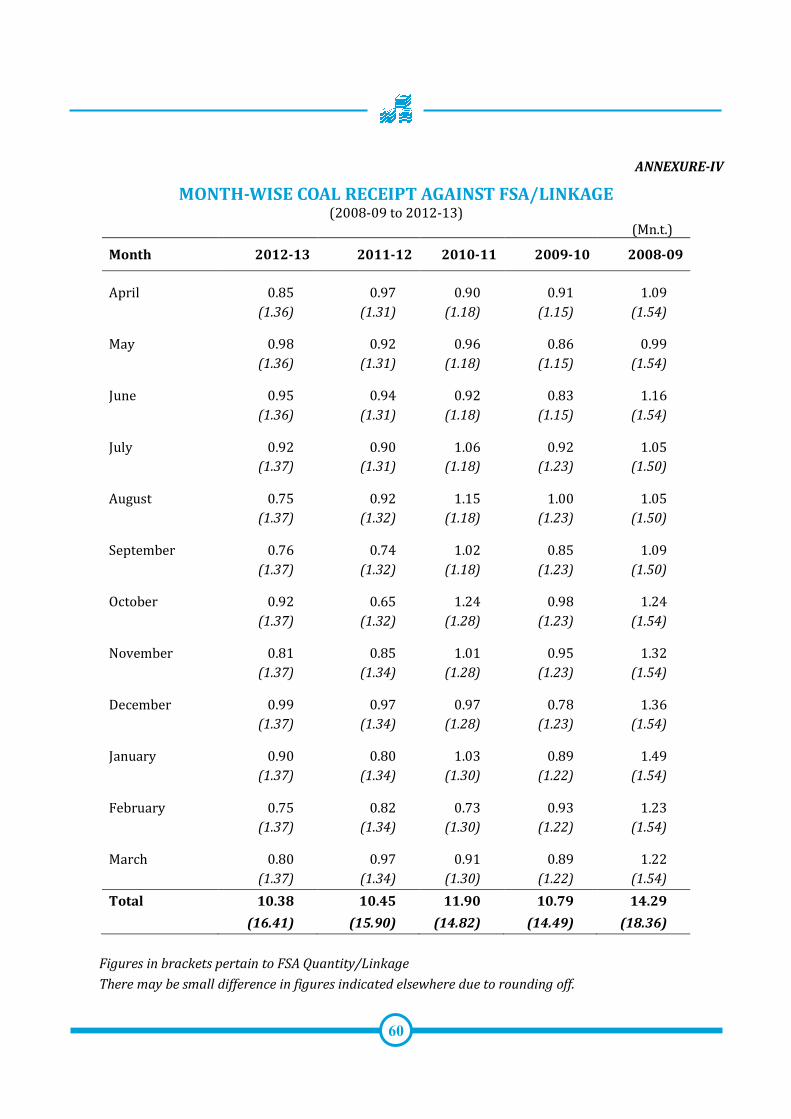

Fuel Consumption and Coal Receipt

against FSA/Linkage

Coal receipt against FSA/Linkage by

Member Units of CMA was 10.38 Mn.t. in

2012-13 as against 10.45 Mn.t. in 2011-12.

Month-wise coal receipts are given in

Annexure-IV.

The percentage supply of linked coal has

been gradually declining year after year

and to meet the industry’s growing

requirement of coal/fuel, the Cement

Industry has to resort to procuring the

same from other sources i.e. through

imports, e-auction, market purchase, pet

coke usage, lignite and other alternate

fuels. This increases the input cost.

The total fuel procurement by Member

units was 29.82 Mn.t. in 2012-13 as

against 29.80 Mn.t. in 2011-12. While the

total fuel consumption by Member units,

during the year 2012-13 was 27.37 Mn.t.

as against 28.30 Mn.t in 2011-12.

E-auction/Open Market

Procurement of Coal

The Cement Industry, because of shortage

of coal/fuel, is required to buy substantial

quantities from open market/e-auction. A

total of 3.93 Mn.t. of e-auction/open

market coal was purchased during

2012-13 as against 4.51 Mn.t. during

2011-12.

The percentage increase of E-Auction

bidding price over notified coal price from

CIL sources with respect to the Spot E-

Auction was 50% and Forward E-Auction

was 26% during the year under review, as

against 67% and 87% respectively during

the financial year 2011-12. The decreasing

trend in the E-Auction price is due to

increase in the Notified Price and decline

in the imported coal price.

Details of year wise

procurement and

consumption of fuel,

including for Captive

Power Plants, are given in

Annexure-V.

It will be seen therefrom

that during the year 2012-

13 only about 35% of the

coal against total

consumption of fuel was

supplied as linked coal

16

against FSA. The supply of

linked coal during 2002-03

was as high as 75% of the

total consumption.

The reduction in terms of

percentage of coal supply can

be attributable to (a) First,

change in Coal Distribution

Policy due to which only 75%

of the normative

requirement of the Cement

Industry is to be met through

FSA/linkage instead of 80%

earlier; (b) secondly, Delay in signing of

FSA between LOA Holders (cement

companies) and coal companies; and (c)

thirdly, Not holding Standing Linkage

Committee (LT) meeting since November

2007 for sanctioning of linkage to

new/enhanced cement capacities. The

decline in the supply of linked coal is also

due to increase in the fuel consumption

by 153.5%.

Coal Imports

The coal imported by Member units was

9.27 Mn.t. during 2012-13 as against 9.40

Mn.t. during 2011-12.

Steam coal was fully exempted from the

basic custom duty during the year

2011-12. Most of the steam coal imports

for cement companies are from South

Africa and Indonesia, which attracted

Basic Custom Duty (BCD) @ 5% and

Countervailing Duty (CVD) @ 1% up to

31.3.2012. The BCD was exempted with

effect from 1.4.2012 for steam coal.

Exemption on basic custom duty on steam

coal financially helped the Cement

Industry, which has now been abolished.

In the Union Budget 2013-14, applicability

of BCD and CVD on bituminous and steam

coal has been equalized to 2% each.

Pet Coke

Pet coke is widely used as a

supplementary fuel in the Cement

Industries in many countries, including

India. Pet coke (Petroleum Coke) is a

residual product of the crude oil refining

process. It has a high calorific value, but

low volatile content, thus leading to poor

ignition characteristics. It is a black solid

obtained as an end product from the

distillation of heavier petroleum crudes.

Pet coke has higher levels of sulphur and

nitrogen as compared to coal.

The main source of supply of pet coke is

from refineries of Reliance Industries Ltd.

(RIL) at Jamnagar, Gujarat and Indian Oil

Corporation (IOC) at Panipat and some

52nd Annual Report

17

quantity of imported pet

coke from USA (Gulf). Pet

coke is also now available

from the new refineries of

Essar at Jamnagar, Gujarat

and from Guru Govind Singh

Refinery at Bhatinda in

Punjab.

A large number of the

cement plants have now

been using pet coke as fuel

in the kilns as also in Captive

Power Plants to some extent.

During the year under

review, the Cement Industry consumed

5.18 Mn.t. of pet coke as against 4.70 Mn.t.

during 2011-12.

Lignite

A quantity of about 0.71 Mn.t. of Lignite

was used in the financial year 2012-13 as

fuel mainly in the cement plants of

Southern and Western Regions as against

0.48 Mn.t. during 2011-12. The trend is

expected to continue in coming years also.

Other Fuels

In view of the increasing requirement and

short availability of coal/fuel of the Cement

Industry, for using other alternative fuels

like husk/municipal wastes/biomass etc.

was kept a pace and the industry

consumed 0.35 Mn.t. in 2012-13 as against

0.28 Mn.t. in 2011-12.

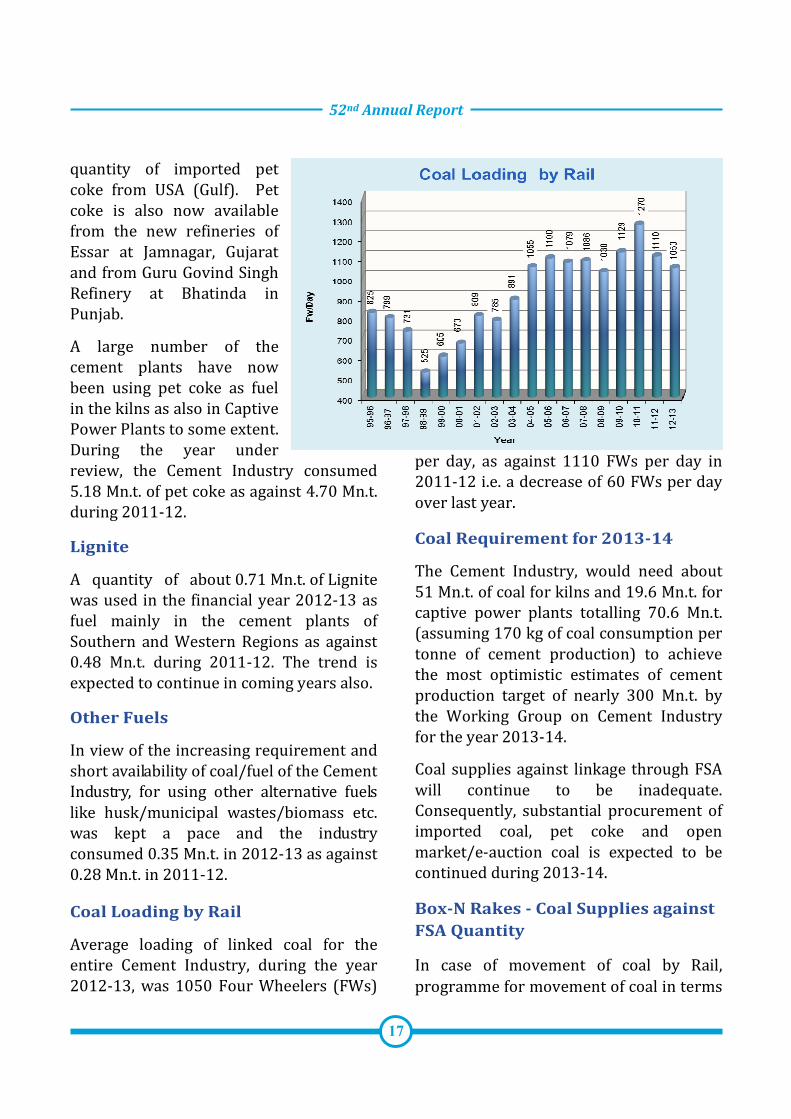

Coal Loading by Rail

Average loading of linked coal for the

entire Cement Industry, during the year

2012-13, was 1050 Four Wheelers (FWs)

per day, as against 1110 FWs per day in

2011-12 i.e. a decrease of 60 FWs per day

over last year.

Coal Requirement for 2013-14

The Cement Industry, would need about

51 Mn.t. of coal for kilns and 19.6 Mn.t. for

captive power plants totalling 70.6 Mn.t.

(assuming 170 kg of coal consumption per

tonne of cement production) to achieve

the most optimistic estimates of cement

production target of nearly 300 Mn.t. by

the Working Group on Cement Industry

for the year 2013-14.

Coal supplies against linkage through FSA

will continue to be inadequate.

Consequently, substantial procurement of

imported coal, pet coke and open

market/e-auction coal is expected to be

continued during 2013-14.

Box-N Rakes - Coal Supplies against

FSA Quantity

In case of movement of coal by Rail,

programme for movement of coal in terms

18

of rakes is submitted by the cement

companies. A quantity of 3894 tonnes

(59 x 66) is discounted from the monthly

quantity of FSA for each rake

programmed. In reality, however, the

actual quantity moved is generally much

less.

In its representation to Director

(Marketing), Coal India Ltd., in December

2012, CMA pointed out that in case of

supply by road the procedure is quite

simple as the delivery of coal is made

directly against the money deposited by

the cement plants with the Coal Cos. The

consumer lifts the entire quantity stated in

the delivery order in his own trucks. As

the FSA quantity is 7788 tonnes, the

consumer should receive the same

quantity to satisfy the provisions of the

FSA.

It was brought to the notice of the

authorities that there has been short

supply of coal in each rake dispatch from

the SECL colliery. Similar loss of

programmed-quantity is being

experienced in other Coal Companies/

Coalfields also. CMA proposed that the

difference between the notional rake

quantity of 3894 tonnes (59 x 66) and the

actual RR/Billed Quantity of that rake

should be accumulated over a period of

time and this accumulated quantity moved

as an additional rake to the

consumer/purchaser. Further, the mode

of movement of the differential quantities

could be allowed to be decided by the

purchaser as per his convenience.

Sanction of Long Term Coal

Linkages to New Capacities &

Resolution of the Pending Cases

Our Member cement plants were

sanctioned long term linkages in the last

SLC (LT) meeting held on 20th November

2007 for kilns. Since then, no meeting has

been held for the cement sector even to

review the status of the existing coal

linkages /LOAs and other related matters.

During this period a large number of

Cement plants have submitted their

applications for the Cement Kilns and

CPPs to Ministry of Coal for sanction of

new LT Linkages. As per the website of

Ministry of Coal, a total of 1590

applications for LOAs from Power Steel

and Cement have been received by the

Ministry of Coal as on December 2012, for

a coal requirement of 3200 Mt per annum.

Out of the total requirement, applications

for 164 Mt for Cement plants per annum

are pending with the Ministry of Coal. It

has been decided by the Ministry of Coal

that receipt of fresh application for LOAs

for power sector be kept in abeyance for a

period of two years.

While the Power Sector SLC (LT) meetings

are being held regularly to review the

status of existing coal linkages /LOAs and

other related matters and to see if the

directions /recommendations of SLC(LT)

are also implemented, Cement Sector,

regardless of being equally important in

building infrastructure, is being

completely ignored.

52nd Annual Report

19

In addition to letter to Secretary (DIPP),

Ministry of Commerce & Industry; and

Secretary, Ministry of Coal, Cabinet

Secretary has also been requested to issue

instructions to Ministry of Coal, for

holding SLC (LT) meeting for Cement

Sector at the earliest for sanction of Long-

Term Linkages against the pending

applications and also for resolution of

pending cases, which are already in

production but were required to come

through the LOA route due to

implementation of NCDP and for

developing a system of regular review of

the status of progress of the existing coal

linkages on similar lines as available to

Power Sector for Cement Sector as well.

TRANSPORTATION – RAILWAYS

During the year under review, Cement

Industry continued to face the problems in

transportation of Cement, Clinker, Coal,

Fly Ash, etc., by Rail due to a host of

reasons particularly with regard to supply

constraints of Rail Wagons, lack of

infrastructure facilities at Terminals and

Railways Policies not taking care of the

interest of the Industry/Investors. As a

result, the total logistics cost of Rail

Transportation continues to be much

higher than the Road Transport despite

the fact that Rail transport is an ideal

mode of transport for Cement Industry.

Cement and Clinker Transportation

by Rail and Revenue Generation

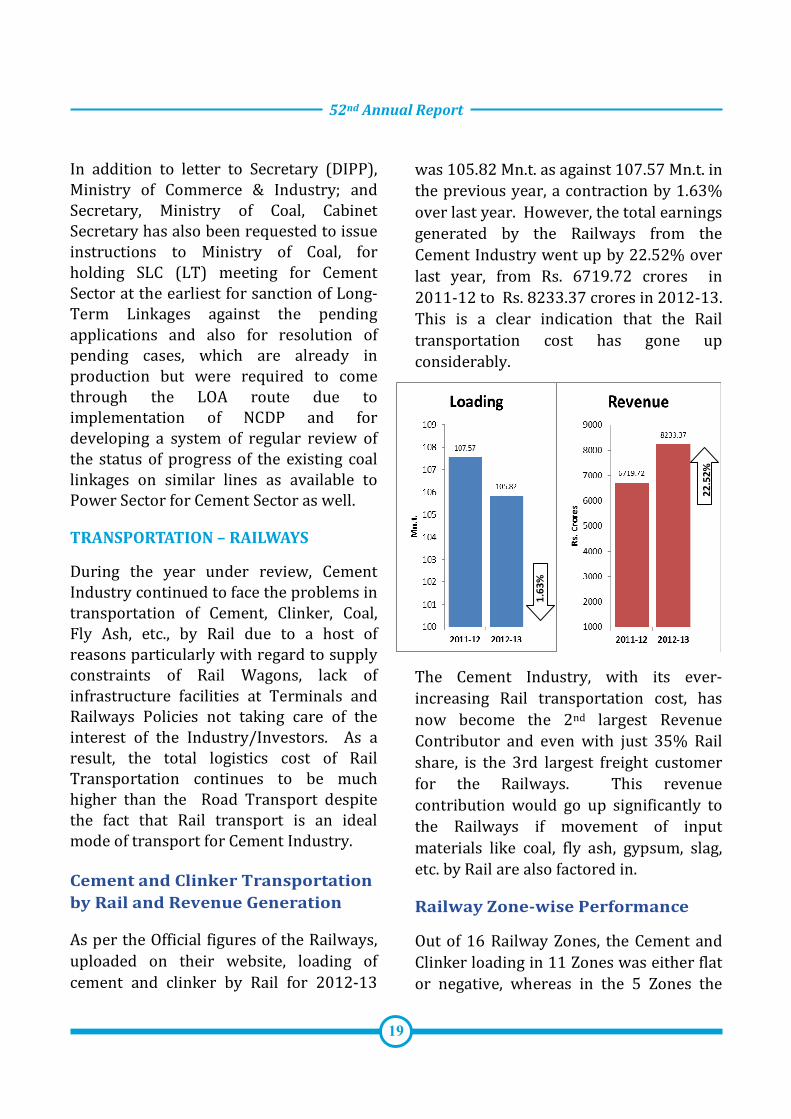

As per the Official figures of the Railways,

uploaded on their website, loading of

cement and clinker by Rail for 2012-13

was 105.82 Mn.t. as against 107.57 Mn.t. in

the previous year, a contraction by 1.63%

over last year. However, the total earnings

generated by the Railways from the

Cement Industry went up by 22.52% over

last year, from Rs. 6719.72 crores in

2011-12 to Rs. 8233.37 crores in 2012-13.

This is a clear indication that the Rail

transportation cost has gone up

considerably.

The Cement Industry, with its ever-

increasing Rail transportation cost, has

now become the 2nd largest Revenue

Contributor and even with just 35% Rail

share, is the 3rd largest freight customer

for the Railways. This revenue

contribution would go up significantly to

the Railways if movement of input

materials like coal, fly ash, gypsum, slag,

etc. by Rail are also factored in.

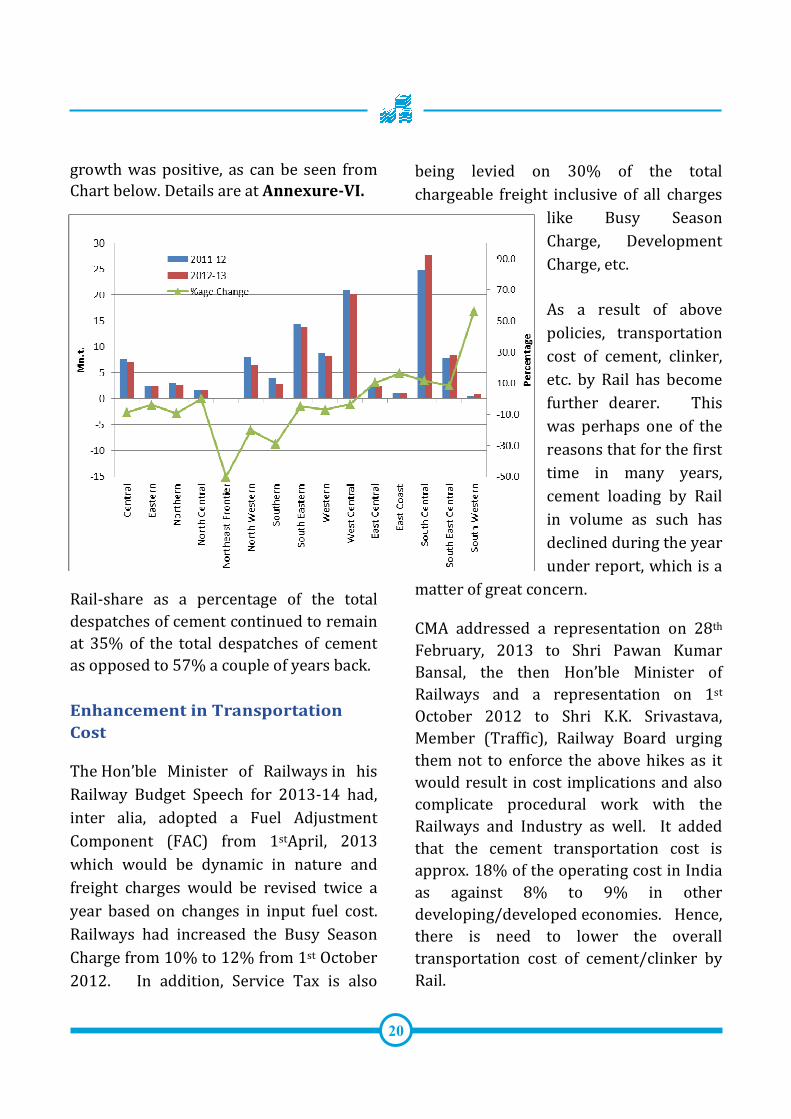

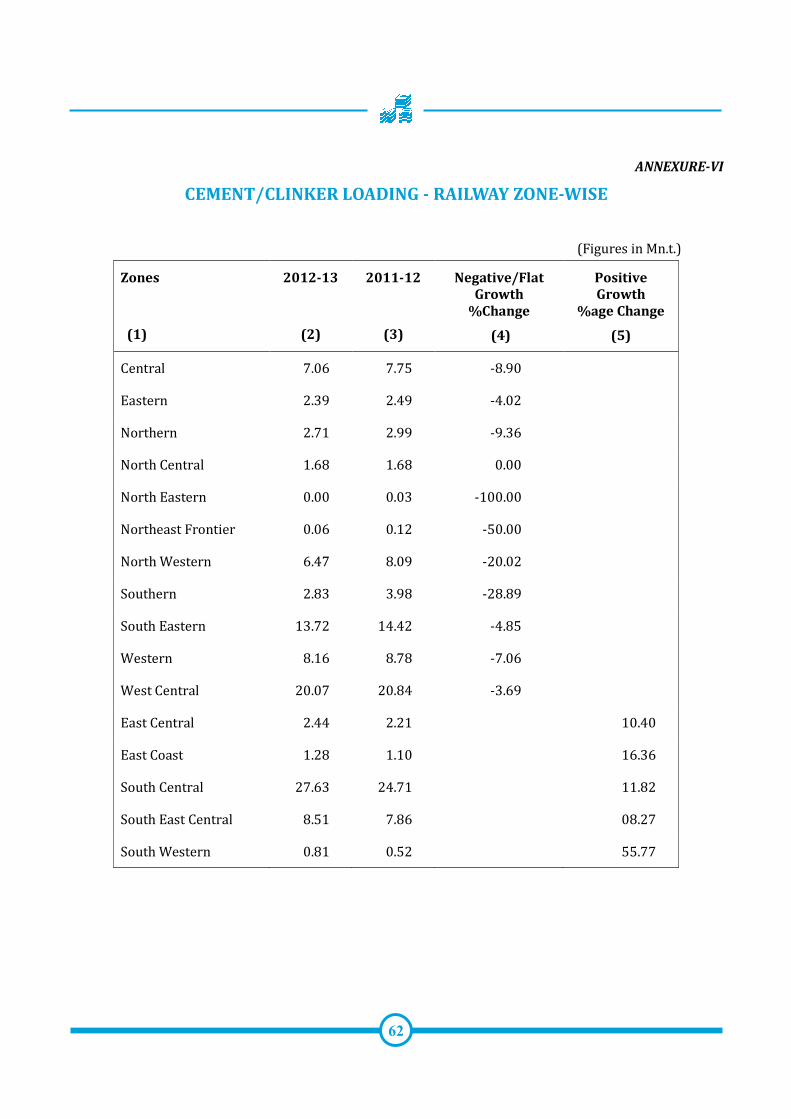

Railway Zone-wise Performance

Out of 16 Railway Zones, the Cement and

Clinker loading in 11 Zones was either flat

or negative, whereas in the 5 Zones the

1.6

3%

22

.52

%

20

growth was positive, as can be seen from

Chart below. Details are at Annexure-VI.

Rail-share as a percentage of the total

despatches of cement continued to remain

at 35% of the total despatches of cement

as opposed to 57% a couple of years back.

Enhancement in Transportation

Cost

The Hon’ble Minister of Railways in his

Railway Budget Speech for 2013-14 had,

inter alia, adopted a Fuel Adjustment

Component (FAC) from 1stApril, 2013

which would be dynamic in nature and

freight charges would be revised twice a

year based on changes in input fuel cost.

Railways had increased the Busy Season

Charge from 10% to 12% from 1st October

2012. In addition, Service Tax is also

being levied on 30% of the total

chargeable freight inclusive of all charges

like Busy Season

Charge, Development

Charge, etc.

As a result of above

policies, transportation

cost of cement, clinker,

etc. by Rail has become

further dearer. This

was perhaps one of the

reasons that for the first

time in many years,

cement loading by Rail

in volume as such has

declined during the year

under report, which is a

matter of great concern.

CMA addressed a representation on 28th

February, 2013 to Shri Pawan Kumar

Bansal, the then Hon’ble Minister of

Railways and a representation on 1st

October 2012 to Shri K.K. Srivastava,

Member (Traffic), Railway Board urging

them not to enforce the above hikes as it

would result in cost implications and also

complicate procedural work with the

Railways and Industry as well. It added

that the cement transportation cost is

approx. 18% of the operating cost in India

as against 8% to 9% in other

developing/developed economies. Hence,

there is need to lower the overall

transportation cost of cement/clinker by

Rail.

52nd Annual Report

21

CMA Committee on Railway Matters

In the last one year, CMA Committee on

Railway Matters, under the Chairmanship

of Shri Rajeev Mehta, Executive President

(Logistics), UltraTech Cement Ltd., had

Meetings with Chairman, Member

(Traffic), Member (Commercial), Advisors,

Executive Directors and other senior

officers of the Railway Board to keep them

abreast of Cement Industry’s Rail-related

problems along with suggestions for their

amicable solution. Some of the Meetings

were attended by senior officials from the

Zonal Railways also.

With the relentless efforts put in by the

Committee, CMA succeeded in getting the

Terminal Development Charges of Rs. 40/

pmt withdrawn from 1st April, 2013,

although the benefit of this was almost

negated by the imposition of upward

adjustments in freight rates from the same

date by the Railways. Further, the

Industry’s long-pending request for

reactivating the Rail Cement Co-ordination

Group had also been accepted by the

Railways.

Rail Cement Co-ordination Group

At the meeting of the Rail Cement Co-

ordination Group (RCCG), held under the

Chairmanship of Shri Manoj Akhori,

Executive Director – TT (F), Railway Board

on 17th June, 2013, Chairman sounded

positive. This was reflected in his

following replies to the issues raised by

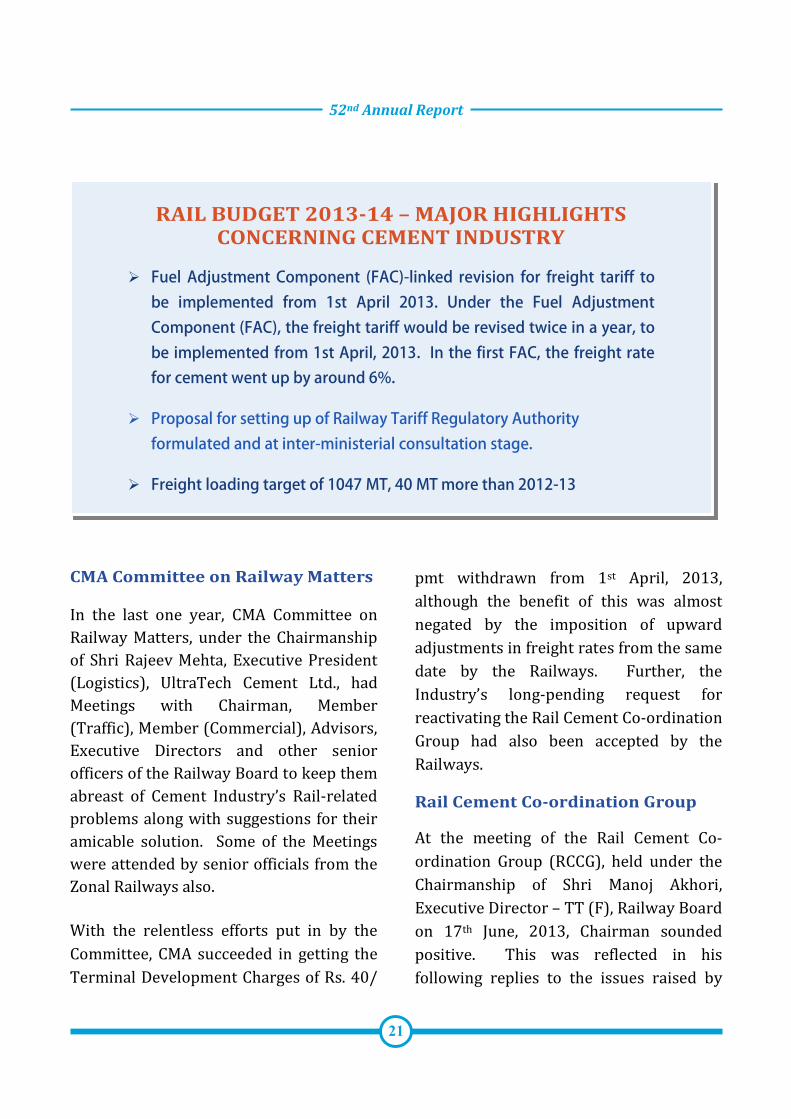

RAIL BUDGET 2013-14 – MAJOR HIGHLIGHTS CONCERNING CEMENT INDUSTRY

� Fuel Adjustment Component (FAC)-linked revision for freight tariff to

be implemented from 1st April 2013. Under the Fuel Adjustment

Component (FAC), the freight tariff would be revised twice in a year, to

be implemented from 1st April, 2013. In the first FAC, the freight rate

for cement went up by around 6%.

� Proposal for setting up of Railway Tariff Regulatory Authority

formulated and at inter-ministerial consultation stage.

� Freight loading target of 1047 MT, 40 MT more than 2012-13

22

the Industry representatives at the

meeting.

� Railways would consider and examine Industry’s request for 25 to 30% freight rebate for short-lead movement of cement say upto 450 kms. to encourage shifting of present cement traffic from Road to Rail which is about 40 to 50% of the total despatches.

� Before making any announcement of any Scheme whose implementation will impact the Cement Industry,

Railways would first invite the inputs from the Cement Industry and thereafter would also discuss with them the Draft Policy concerning cement.

� Terminals would be given priority for development.

� Retention as well as incremental traffic in cement loading by Rail would be given equal importance by the Railways for granting freight incentives.

Representations/Presentations to

the Railways

In order to encourage and enhance Rail

share for movement of cement, clinker and

input materials by Rail, CMA, on behalf of

the Cement Industry, made the following

submissions to the Railways, from time to

time, in its various meetings,

representations and presentations:

• Classification Slab for Cement and

Clinker be lowered to Slab 140 from

the present Slab 150.

• A freight incentive of at least 25-30%

be accorded to the cement dispatches

upto a distance of 450 kms. to enable

the Railways to capture huge cement

business from Road which is estimated

to be about 50% of the total cement

dispatches of the Industry.

• Freight Rates be fixed for a period of at

least one year and during this period

no outside adjustments i.e. Surcharge,

etc. should be made.

• Dynamic Pricing Freight Policy of the

Railways be scrapped for Cement

Industry as various Policy Decisions

under this Scheme have significantly

enhanced the overall transportation

cost of Cement by Rail. This has led to

steady shift to Road transportation.

• The Infrastructure facilities at

Terminals, handling cement, be made

world-class.

• The Railways should consider CMA’s

suggestion to give freight rebate for a

period of at least two years to capture

and retain the short lead cement

business.

• Two point and Mini rakes should be

considered even upto 500 kms. lead for

all important desired pair of points by

cement manufacturers.

• Steep penal and wharfage charges

being levied should be avoided to the

maximum extent.

• Immediate withdrawal of the increase

in Busy Season Surcharge.

52nd Annual Report

23

• The Modified Wagon Investment

Scheme (MWIS) and Liberalized Wagon

Investment Scheme (LWIS) would be

made more attractive; and

• Activation of Cement Rail Co-

ordination Committee on priority basis

for long term solution on freight

policies and infrastructure.

Problems in Claiming Cenvat Credit

on Service Tax on Cement

Transportation by Rail

The Railway Board by its Rate Circular of

28th September 2012 had issued

instructions to all Zonal Railways in the

matter of collection/documentation of

Service Tax on Transportation of Goods by

Rail. This has increased paper work

considerably and has impacted working of

member cement companies of CMA.

Accordingly, CMA made the following

submissions to the Railway Board:

• The Railways need not insist on

monthly written requests, as envisaged

in the Rate Circular from major

customers like cement, as this is a

recurring matter. Instead, the Railways

may routinely issue the Consolidated

Certificate for a given month, by the 3rd

of the following month, to enable

timely Cenvat Credit adjustment

against Service Tax paid by the

customer. This cut off time-line is

important as Central Excise Duty dues

of a given month are to be paid by

5th/6th of the following month.

• Alternately and preferably, the

Railways should issue an extra copy of

the “Railway Receipt”, which can be

treated as Service Tax Certificate. This

has already been envisaged by ED

(Accounts), Railway Board in his letter

of 29.6.2012 to FA&CACO’s of their

Zonal Railways.

• Apart from the primary Railway

Freight, other charges like Demurrage,

Wharfage, Under Charges, Penal

Charges, etc., also attract levy of

Service Tax. In the case of Demurrage

& Wharfage, the original “Money

Receipt” has to be submitted along

with Waiver Applications to the

Railways. As such, an extra copy of the

“Money Receipt” need to be provided

by the Railways, for the purpose of

available Cenvat Credit.

CMA brought the above submissions to the

notice of the Member (Traffic), Railway

Board in October 2012 and again in

November 2012 with a request, inter alia,

to recommend to the Ministry of Finance

that the Cement Industry be exempted

from the Service Tax for Transportation of

cement and clinker by Rail like other

essential commodities viz. petroleum

products and gases; food grains; chemical

manures; etc.

Bulk Movement of Cement

In order to encourage and enhance the

bulk movement of cement in the country,

which is about 2% of the total installed

24

capacity, CMA continued to request the

Railways to suitably bring down the Rail

Classification Slab for bulk cement and

also provide attractive freight discount to

all those who purchase Special Purpose

Wagons for bulk movement of cement and

fly ash, for the entire life of wagons, which

is 35-40 years.

POWER

Cement is a continuous process Industry

requiring un-interrupted power supply. As

a thumb rule, the requirement of power is

20 MW for a million tonne plant. Cement

plants are making all out efforts to ensure

availability of uninterrupted and quality

power in their manufacturing operations,

since power constitutes a major cost item

in cement manufacture.

Most of the cement units have now

installed captive power generation

capacities to the extent of 60% of their

requirement, and even 100% in some

cases. Normally, expansions and new

projects have also to be equipped with

captive power supply. Captive power

generation capacity which was approx.

118 MW in 1982-83 rose to nearly 3000

MW, both Diesel and Thermal in 2011-12

and has further gone up during the year

under review. In addition, the Cement

Industry has installed Wind Farms of

around 237 MW. Capacity of Waste Heat

Recovery (WHR) based power generation

was more than 115 MW during the year.

The Industry produced 0.78 Mn.t. or 3% of

total cement production in 1982-83 by

using captive power, which has

substantially gone upto nearly 145 Mn.t.

or 59% of total production in 2011-12.

This augurs well with the need to release

pressure on Grid Power. Unfortunately,

the data in respect of 2012-13 are not

available with CMA in the background of

the restraint Order of CCI dated 20.06.2012

in case No. 29/2010 “Builders Association of

India Vs. CMA & Ors.”.

The Industry has placed significant focus

on improving energy efficiency in plant

operation over the years and it is an

ongoing process. The Cement Industry’s

average electrical energy consumption is

expected to come down to 78 kWh/t

cement from 80 kWh/t cement and the

average thermal energy consumption to

about 710 kcal/kg clinker from 725

kcal/kg clinker by the terminal year of

XIIth Plan (Year 2016-17). The best

electrical energy consumption presently

achieved by the state-of-the-art cement

plants is nearly 67 kWh/t cement and

thermal energy of about 667 kcal/kg

clinker, which are comparable to the best

reported figures of 65 kWh/t cement and

660 kcal/kg clinker in a developed

country like Japan. The Industry’s

proactive participation in the ongoing

implementation of the PAT (Perform,

Achieve and Trade) Scheme of Bureau of

Energy Efficiency (under the National

Mission for Enhanced Energy Efficiency-

one of the Eight Missions of the Prime

Minister’s National Action Plan on Climate

52nd Annual Report

25

Change) is expected to drive further

reduction in energy consumption in our

cement plants.

Certain contentious issues that creep in

while the Industry makes efforts for

further energy efficiency improvement,

that merit due attention of the authorities,

are highlighted below:

(i) Use of Alternate Sources of

Energy: The Cement Industry is proactive and to tide over power requirement threatened by coal

supply constraints, has been using alternate/waste derived fuels (WDF) including hazardous combustible wastes (HCW). At present, a number of cement plants are already utilizing pet coke to the extent of 60-100% and agricultural wastes such as rice husk and bamboo dust to the extent of 10-15%, also for captive power generation. The Industry deserves suitable incentivisation for such usage of alternate fuels. In this regard, the Tariff Commission had conducted a study as desired by the Department Related Parliamentary Standing Committee on Commerce (DRPSC) on ‘Review of Performance

of Cement Industry’ for the year 2010-11, with special emphasis on the cost of production of cement including normative cost of production. The Chapter 8 on ‘Findings and Conclusions’ of the Study Report, uploaded on the website of DIPP under the link of ‘Discussion Papers’, seeking

views/comments of the stakeholders/public, has made similar observations, and stated, while there is a need to increase the linkage of domestic coal, use of alternative fuel in the kiln as a substitute will also reduce the dependence on coal, specifically suggesting in Para 8.5 that “policy measures like capital and interest

subsidy to cement units using bio-wastes/fuel in the manufacture of cement can be thought about to encourage such initiatives by the cement units, since use of bio-wastes/fuels in the cement manufacture is an environmental friendly measure”. Such constructive suggestion coming from an Apex Government Agency of the country greatly inspires and reinforces the initiatives the Industry has already taken in increasing the usage of alternative fuels and raw materials in Cement plants.

CMA, on the basis of feedback

received from its Member

Companies, responded to the

aforesaid observations and

suggestions made by the Tariff

Commission on ‘Use of Alternate

Fuel’ as sought for by DIPP,

submitted a representation to DIPP

on 16th August 2013. The key points

raised in our representation are:

• XII Plan Working Group Report

on Cement Industry has also

recommended an Incentive

Policy.

26

• A specially prepared ‘Technology Roadmap: Low-Carbon Technology for the Indian Cement Industry’ by Cement Sustainability Initiative/World Business Council for Sustainable Development-Geneva & International Energy Agency-Paris and released by them in New Delhi on 25th February 2013 has focused on the need for implementation of five major emissions reduction levers, namely, Co-processing of alternative fuels and raw materials, improved thermal and electrical efficiency, clinker substitution, waste heat recovery, and newer technologies.

• We have requested

incentivisation for alternative

fuels usage in the Cement sector,

in respect of huge capital

investment as well as higher

regular expenses in the areas of

AFR pre-processing, storage,

handling & feeding system, for

hassle-free import of alternate

fuels, for considering promotion

of ‘Polluters’ Pay’ principle, and

for providing an enabling

environmental regulatory

mechanism to facilitate

increased usage of alternative

fuels.

(ii) Cogeneration of Power through

Waste Heat Recovery System:

Another noteworthy effort the

Cement Industry has been making is

the cogeneration of power through

Waste Heat Recovery (WHR).

Twelve cement plants have been

equipped with this technology to

generate power, and more are

initiating steps towards harnessing

WHR for cogeneration. The

potential exists in almost all cement