Embed Size (px)

Citation preview

2013-11-15

OBJECTS AND REASONS

This Bill would provide for

the establishment of a regulatory framework to facilitate and encouragethe sustainable growth and development of cultural industries;

funding for cultural projects; and

duty free concessions and income tax benefits in respect of culturalprojects,

and for related matters.

(a)

(b)

(c)

Arrangement of Sections

Part IPreliminary

Short title

Interpretation

Part IIEstablishment, Composition and Administration of the Authority

Establishment of the Authority

Functions of the Authority

Establishment of Board of Directors

Appointment of Offices

Other Staff

Pension rights and service with Authority

Savings of pension

Directions of Minister

Fees

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

11.

2

Part IIIApproval of Cultural Project

Application for approval of cultural project

Further information to be furnished by the applicant

Interim approval of a cultural project

Notification

Form of interim approval

Suspension or revocation of interim approval

Order declaring approved cultural project

Licensing of cultural project

Effective date of licensing

Part IVDuty Free Concessions

Permit and exemption from duties and taxes

Suspension or revocation of permit

Incentives

Prohibited uses

Keeping of records of equipment, building material and supplies

12.

13.

14.

15.

16.

17.

18.

19.

20.

21.

22.

23.

24.

25.

3

Part VIncome Tax Concessions

Constructing and furnishing of a new building or refurbishment andfurnishing of an existing building

Set-off capital expenditure

Allowance in respect of artistic work

Marketing

Training

Investment

Dividends

Part VICultural Industries Development Fund

Establishment and resources of the Fund

Purposes of the Fund

Administration and management of Fund

Reports

Auditing of the Fund

Investment in the Fund

26.

27.

28.

29.

30.

31.

32.

33.

34.

35.

36.

37.

38.

4

PART VIIIncentives for Audio-Visual Production and Motion Pictures

Exemption from taxes

PART VIIIIncentives for Heritage Building and Conservation

Concessions in respect of heritage building and conservation

PART IXMiscellaneous

Regulations

Offences

Commencement

FIRST SCHEDULE

Constitution and Procedure of Board

SECOND SCHEDULE

Duty Free Concessions

39.

40.

41.

42.

43.

5

BARBADOS

A Bill entitled

An Act to provide for

the establishment of a regulatory framework to facilitate and encouragethe sustainable growth and development of cultural industries;

funding for cultural projects; and

duty free concessions and income tax benefits in respect of culturalprojects,

(a)

(b)

(c)

and for related matters.

ENACTED by the Parliament of Barbados as follows:

Part I

Preliminary

Short title

This Act may be cited as the Cultural Industries Development Act,2013.

Interpretation

In this Act,

“approved cultural agency” means an entity approved by the Minister for thepurposes of

registering cultural entrepreneurs and cultural practitioners;

obtaining funding for cultural entrepreneurs and cultural practitioners;and

obtaining concessions for cultural entrepreneurs and culturalpractitioners;

“approved cultural project” means a cultural industries project that has beendeclared to be an approved cultural project by the Minister undersection 12(2);

“approved producer of audio-visual content” or “approved producer ” means afilm production company incorporated under the Companies Act,Cap. 308, or registered under the Registration of Business Names Act,Cap. 317 that is controlled by a resident of Barbados;

“arts and heritage facilities” means any building, service or equipment utilisedfor the purpose of the arts or identified as having heritage value;

1.

2.(1)

(a)

(b)

(c)

8

“Authority” means the Cultural Industries Development Authority establishedunder section 3;

“Comptroller” means the Comptroller of Customs;

“conservation” means the maintenance, preservation, restoration orreconstruction of heritage buildings, structures and areas of historic oraesthetic, architectural, cultural or environmental significance according toguidelines established by the local World Heritage Committee incollaboration with the Town and Country Planning Department;

“cultural administrator” means a person who liaises between the artists and theconsumer to create an environment for the development of the culturalindustries sector;

“cultural entrepreneur” means a person who organises, manages and assumes therisk of a business or enterprise in the cultural industries sector;

“cultural goods and services” means goods which result from individual orcollective creativity and activities aimed at satisfying cultural interests orneeds;

“cultural heritage” encompasses several main categories of heritage andincludes

immovable cultural heritage such as buildings, monuments andarchaeological sites;

intangible cultural heritage such as oral traditions, performing arts andrituals;

natural heritage such as natural sites with cultural aspects - culturallandscapes, physical, biological or geological formations;

underwater cultural heritage such as shipwrecks, underwater ruins andcities;

(a)

(b)

(c)

(d)

9

“cultural industries” include those enterprises which provide the general publicwith commercially viable cultural goods and services that are developed forreproduction and distribution to mass audiences in the following areas:

arts and culture - the performing arts, visual arts, literary arts,photography, craft, culinary arts, libraries, museums, galleries,archives, heritage sites, festivals and art supporting enterprises;

design - advertising, architecture, web and software design, graphics,industrial design, fashion, communications, interior and environmentaldesign;

media - broadcast media including television, radio and cable, digitalmedia including software and computer services, film and video,recorded music and publishing and video games;

“cultural practitioner” means an individual, company, partnership orunincorporated body that

is involved in the business of the arts and cultural industries;

has been issued with a licence under section 19; or

is registered with a cultural agency;

“cultural project” means a cultural industries project undertaken by a culturalentrepreneur, cultural practitioner or governmental entity that assists in thedevelopment of cultural industries;

“cultural worker” means an individual whose technical or administrative labouris required to facilitate the production of goods and services in the culturaland creative industries;

“Fund” means the Cultural Industries Development Fund established undersection 32;

“governmental entity” means an agency of government established by statute orincorporated under the Companies Act, Cap. 308 for the purposes ofdeveloping culture, cultural industries or the arts;

(a)

(b)

(c)

(a)

(b)

(c)

10

“heritage building” means a building that possesses architectural, aesthetic,historical or cultural values and which is listed as such with the local WorldHeritage Committee, the Town and Country Planning Department, theBarbados Museum and Historical Society or the Barbados National Trust;

“interim approval” means the approval of a cultural industries project by theMinister under section 14;

“investor” means

an individual, company, partnership or unincorporated body that isincorporated under the Companies Act, Cap. 308 or registered underthe Registration of Business Names Act or , Cap. 317; or

a cultural entrepreneur or a cultural practitioner

who invests in a cultural project with the expectation of receiving a financialreturn;

“licence” means the licence issued by the Minister under section 12 in respect ofan approved cultural project;

“social media” means a group of internet and mobile based technologies thatsupport interactive dialogue and exchange of user generated content;

“supplies” means

goods that are imported, purchased from a bonded warehouse or thatare locally manufactured for the construction, development andoperation of an approved cultural project; and

the provision of services that directly relate to the construction of anapproved cultural project.

For the purposes of this Act, the term “resident of Barbados” means aperson who in an income year

spends in the aggregate more than 182 days in Barbados; or

is ordinarily resident in Barbados in the relevant income year.

(a)

(b)

(a)

(b)

(2)

(a)

(b)

11

For the purposes of subsection 2(b) a person shall be deemed to beordinarily resident in Barbados in an income year if that person

has a permanent home in Barbados; and

has given notice to the Commissioner of Inland Revenue that he intendsto reside in Barbados for a period of at least 2 consecutive years,including the income year in question.

For the purposes of subsection (3) “permanent home” meansaccommodation in Barbados which is permanently available for the use of theperson in question but does not include accommodation retained for his use inBarbados solely as a vacation property.

Part II

Establishment, Composition and Administration of the Authority

Establishment of the Authority

There is established an Authority to be known as the BarbadosCultural Industries Development Authority.

The Authority is a body corporate to which section 21 of the InterpretationAct, Cap. 1, applies.

Functions of the Authority

The Authority established under section 3 shall be responsible for

promoting, assisting and facilitating the efficient development of thecultural industries;

designing and implementing suitable marketing strategies for theeffective promotion of the cultural industries;

(3)

(a)

(b)

(4)

3.(1)

(2)

4.

(a)

(b)

12

maintaining a registry of the applications of cultural entrepreneurs orcultural practitioners submitted to the Minister and the approvalsgranted in respect of those applications;

determining the eligibility of cultural projects for funding;

processing the applications for concessions and benefits to be derivedunder this Act;

monitoring and inspecting each approved cultural project to ensure thecompliance of the cultural entrepreneur, cultural practitioner orgovernmental entity with the terms and conditions governing theproject and for this purpose may

cause the books, records and accounts of the cultural entrepreneur,cultural practitioner or governmental entity in relation to a culturalproject to be inspected;

request such information from the cultural entrepreneur, culturalpractitioner or governmental entity as the Authority considersnecessary to enable the inspection to be carried out; and

such other functions as are conferred on the Authority by the Minister.

Establishment of Board of Directors

There is established a Board of Directors of the Authority which shalladvise the Minister on any matter connected to cultural industries and beresponsible for the execution of the policy of the Authority.

The First Schedule has effect with respect to the constitution of the Boardand otherwise in relation thereto.

Appointment of Offices

The Authority shall, with the approval of the Minister, appoint suchpersons to such offices as may be designated by the Minister.

(c)

(d)

(e)

(f)

(i)

(ii)

(g)

5.(1)

(2)

6.(1)

13

The Chief Executive Officer of the Authority, by whatever name called, issubject to the directions of the Board for the execution of its policy and themanagement of its affairs.

Other Staff

The Authority may appoint and employ such officers, agents andservants as it considers necessary for the proper carrying into effect of theprovisions of this Act, at such remuneration and on such terms and conditions asthe Minister approves in writing.

Notwithstanding subsection (1) no post shall be established and no salaryin excess of such amount as the Minister may determine and may notify in writingto the Authority shall be assigned to any post without the prior approval of theMinister.

Subject to this Act and to the Statutory Boards (Pensions) Act, Cap. 384,no provision shall be made for the payment of any pension, gratuity or other likebenefit to any person employed by the Authority without the prior approval inwriting of the Minister.

Pension rights and service with Authority

Where a public officer is seconded or temporarily transferred from apensionable office within the meaning of section 2(1) of the Pensions Act,Cap. 25 to perform any service with the Authority, his service with the Authorityshall, unless the Governor-General otherwise decides, count for pension underthat Act as if the officer had not been so seconded or transferred.

Where the services of a person employed by the Authority are on loan tothe Government that person is entitled to such benefits and terms of employmentas are applicable to the post which he occupies, and the service with the Authorityshall be taken into account as continuous service with the Government and thePensions Act, Cap. 25 and the Pension Regulations 1947 (1947/20) shall applyto him as if his service with the Authority were service within the meaning ofthat Act.

(2)

7.(1)

(2)

(3)

8.(1)

(2)

14

Where a public officer is transferred to the service of the Authority inaccordance with subsection (1), the Authority shall refund to the ConsolidatedFund all moneys payable as pension in respect of the service of that officer withthe Authority.

Savings of pension

Where a public officer who has pensionable service is transferred toor becomes employed in the service of the Authority, his service with theAuthority shall, whether or not there was a break in service, be aggregated withhis service in the public service and his pension shall be calculated in accordancewith the Pensions Act, Cap. 25 and the Pensions Regulations, 1947 (1947/20).

Directions of Minister

The Minister may give the Authority directions of a general nature orspecific nature in respect of the policy to be followed by the Authority in theperformance of its functions under this Act, and the Authority shall comply withthose directions.

Fees

The Authority may charge such fees as are prescribed by order madeby the Minister responsible for Finance for

the issue of licences; and

any service performed by it.

(3)

9.

10.

11.

(a)

(b)

15

Part III

Approval of Cultural Project

Application for approval of cultural project

A cultural entrepreneur, cultural practitioner or governmental entitywho wishes to develop a cultural project may apply to the Minister to have thecultural project approved for the purposes of this Act.

For the purposes of this Act, a cultural project includes work in

arts and culture;

design;

media;

the use of new technologies and the development of the social mediaand data bases for the purpose of enhancing the operation andmanagement of the cultural industries sector;

the training and professional development of artists, artisans andstudents of the arts and cultural workers;

product design and the marketing and distribution of cultural goodsand services;

product design with respect to cultural goods and services;

the construction or renovation of arts and heritage facilities and theacquisition of specialised equipment for those purposes;

the promotion and presentation of programmes in the area of culturalheritage and artistic expression;

the restoration, preservation and conservation of natural sites;

the establishment, restoration, preservation and conservation ofmonuments, museums and other historical structures and sites; and

12.(1)

(2)

(a)

(b)

(c)

(d)

(e)

(f)

(g)

(h)

(i)

(j)

(k)

16

research work on culture and cultural industries,

aimed at stimulating economic activity and development.

The Minister may, with the approval of the Cabinet, declare by order anycultural project that meets the requirements of this Act to be an approved culturalproject for the purposes of this Act.

Further information to be furnished by the applicant

Upon receipt of an application under section 12, the Minister mayrequire that further information be submitted to him with respect to any matterrelevant to the applicant including

the estimated expenditure of the cultural project and the source of fundsto be used;

a project feasibility study forecasting the economic impact of thecultural project on the development of cultural industries in Barbados;

evidence of ownership of the cultural project, that is, the copyright,patent, trade mark, industrial design, or other such ownership of thecultural project;

a proposed marketing plan relevant to the completed cultural project;

where the applicant is not an individual, evidence of the legal status ofthe entity in respect of its authority to carry on its business;

the nature of the business carried on by the cultural entrepreneur orcultural practitioner;

information on the project such as the name and nature of the projectand expected duration of the project together with a description of theproject;

estimated projected cash flow of the cultural project;

estimated capital cost of the project;

an estimated annual operational budget of the project; and

(l)

(3)

13.

(a)

(b)

(c)

(d)

(e)

(f)

(g)

(h)

(i)

(j)

17

any other information including comments from the National CulturalFoundation or any other cultural agency, that may be required by theMinister.

Interim approval of a cultural project

Where the Minister is satisfied that the cultural project would assistin the development of culture and cultural industries, the Minister may with theapproval of the Cabinet, grant to the cultural entrepreneur, cultural practitioneror governmental entity an interim approval of the cultural project as the first stagein a two-stage authorisation procedure which would include

an interim approval of the cultural project based on the informationsubmitted in accordance with section 13 and the registration of thecultural entrepreneur, cultural practitioner or governmental entity withan approved cultural agency; and

a licence issued to the cultural entrepreneur, cultural practitioner orgovernmental entity under section 19 on the recommendation of theAuthority where the Authority is satisfied that all of the relevantprocedures, requisitions and statutes have been complied with, and thatthe cultural project is in a suitable form and is of a standard acceptableto the Authority.

Where the Minister grants an interim approval in accordance withsubsection (1) a notice to that effect shall be made by the Minister and publishedin the Official Gazette.

Notification

Where the Minister receives an application under section 12, theMinister shall within 90 days of the date of its receipt,

notify the applicant in writing of the approval or refusal of theapplication; or

(k)

14.(1)

(a)

(b)

(2)

15.

(a)

18

request that additional information be submitted in accordance withsection 13.

Form of interim approval

The interim approval granted under section 14(1) shall

be in such form and contain such particulars as may be prescribed;

specify the benefits that may be granted to the applicant in respect ofthe project; and

be subject to such conditions or terms as the Minister may attach.

Suspension or revocation of interim approval

An interim approval may be suspended or revoked by the Minister atany time where

any information submitted with respect to the application is false ormisleading; or

the applicant to whom the interim approval was granted has failed tocomply with any condition or term of the interim approval.

Where the Minister suspends or revokes an interim approval, the Ministershall in writing inform the person to whom the approval was granted of thereasons for the suspension or revocation.

Order declaring approved cultural project

Where a cultural project has been developed in accordance with theconditions of an interim approval, the Minister shall by order, declare theresulting project to be an approved cultural project for the purpose of this Act.

An order made under subsection (1)

shall be in such form and contain such particulars as may be prescribedby the Minister;

(b)

16.

(a)

(b)

(c)

17.(1)

(a)

(b)

(2)

18.(1)

(2)

(a)

19

shall specify the benefits to be granted to the applicant; and

may impose conditions or terms to be observed by the applicant.

Where an Order is made pursuant to subsection (1) and the applicant failsto comply with the conditions or terms imposed in the Order, the Minister mayrevoke the Order by a notice published in the Official Gazette.

Licensing of cultural project

Where a cultural project has been reviewed and assessed by theAuthority and has met the standards and requirements of the relevant culturalagency, the Minister shall issue to the cultural entrepreneur, cultural practitioneror governmental entity a licence in respect of the approved cultural project.

A licence issued under subsection (1)

shall be in such form and contain such particulars as may be prescribedby the Minister by order; and

may impose conditions to be observed by the cultural entrepreneur,cultural practitioner or governmental entity.

Where conditions are imposed in a licence issued under subsection (1) andthose conditions are not observed by the cultural entrepreneur, culturalpractitioner or governmental entity the Minister shall revoke the licence by anotice published in the Official Gazette.

Effective date of licensing

Where a licence is issued under section 19, the licence shall specifythe effective date from which the cultural entrepreneur, cultural practitioner orgovernmental entity will receive any tax benefit granted to the culturalentrepreneur, cultural practitioner or governmental entity pursuant to this Act.

The date specified in the licence under subsection (1) shall mark thebeginning of the initial year of assessment for the purpose of computing taxbenefits.

(b)

(c)

(3)

19.(1)

(2)

(a)

(b)

(3)

20.(1)

(2)

20

Part IV

Duty Free Concessions

Permit and exemption from duties and taxes

Where a cultural entrepreneur, cultural practitioner or governmentalentity has been granted an interim approval in respect of a cultural project, theMinister may grant to that cultural entrepreneur, cultural practitioner orgovernmental entity a permit for the importation of the items set out in the SecondSchedule.

A cultural entrepreneur, cultural practitioner or governmental entity of anapproved cultural project shall be exempt from the payment of import duty, stampduty and value added tax on

imports of equipment listed in Part I of the Second Schedule;

imports of operating non-capital supplies necessary for preparing fornational festivals listed in Part II of the Second Schedule;

building materials purchased locally; and

other capital assets.

For the purposes of subsection (2),

“capital assets” refer to items such as imports ofequipment, apparatus and materials; and

“imports of operating non-capital supplies” means goods used in thepreparation of festivals and approved cultural projects.

Where a governmental entity is a cultural entrepreneur or culturalpractitioner it shall be exempt from the payment of all duties and taxes on importsused for the construction and furnishing of a new building or for the renovationand furnishing of an existing building where such building is to be used primarilyfor cultural activities.

21.(1)

(2)

(a)

(b)

(c)

(d)

(3)

(a)

(b)

(4)

21

The exemption from the payment of duties and taxes referred to insubsection (2) shall be for a period of 15 years from the date of the importationof the imports or capital assets.

A permit granted under subsection (1) shall be in such form and subject tosuch terms and conditions as the Minister may prescribe.

The Minister may by order amend the Second Schedule.

Suspension or revocation of permit

Where the Minister is satisfied that the holder of a permit grantedunder section 21(1) has

obtained the permit by any false statement;

abused or misused the permit; or

breached or failed to comply with any condition stipulated in thepermit,

the Minister may by written notice to the holder of the permit, either suspend theoperation of the permit or revoke the permit and shall give reasons for thesuspension or revocation.

Incentives

A cultural entrepreneur, cultural practitioner or governmental entityis entitled to any one or more of the following incentives in respect of an approvedcultural project:

the payment of tax at the rate of 15 per cent on the profits of the project;

exemption from withholding tax on dividends and interest earned oninvestment in an approved cultural project;

exemption from the payment of stamp duty under the Stamp DutyAct, Cap. 91 on all documents related to the project where theregistration of these documents is required by law;

(5)

(6)

(7)

22.

(a)

(b)

(c)

23.

(a)

(b)

(c)

22

a deduction of tax of an amount equal to 20 per cent of the actualexpenditure incurred in respect of the use of technology, marketresearch and any other activity that is in the opinion of the Committeedirectly related to the development of the approved cultural project.

Prohibited uses

Every cultural entrepreneur or cultural practitioner and where thecultural entrepreneur or cultural practitioner is a government entity, every officerof the governmental entity, who imports building material, equipment andsupplies without payment of duties and taxes and who without the authorisationof the Minister, disposes of the equipment and supplies other than as providedfor in the permit is guilty of an offence and is liable on conviction on indictmentto

a fine of 3 times the value of the equipment and supplies in respect ofthe disposal; or

repayment of the duties and taxes refunded on the equipment andsupplies

or both.

Keeping of records of equipment, building material and supplies

The Comptroller shall require every cultural entrepreneur, culturalpractitioner or governmental entity who imports equipment, building materialand supplies or purchases equipment, building material and supplies locally to

keep records in such form and containing such particulars as may bespecified by the Comptroller in respect of the use or disposal of thesupplies, equipment and building materials; and

permit the Comptroller or any person authorised by him in writing, atall reasonable times, to inspect the records and to have access to anypremises for the purposes of examining any equipment, buildingmaterial and supplies which the Comptroller may believe to be therein,

(d)

24.

(a)

(b)

25.(1)

(a)

(b)

23

and of satisfying himself in respect of the accuracy of the particularsin relation to the equipment, building materials and supplies containedin the records.

The conditions imposed under paragraphs (a) and (b) of subsection (1)shall apply for a period of 5 years from

the date of the importation of the equipment, building material andsupplies without payment of the duties and taxes; or

the date of payment of the duties and taxes,

as the case may be.

A person who wilfully delays, hinders or obstructs the Comptroller or anyperson authorised by him in writing from inspecting the equipment, buildingmaterial and supplies or any records relating to the equipment, building materialor supplies is guilty of an offence and is liable on conviction on indictment to afine of $50 000 or 5 times the value of the equipment, building material andsupplies, whichever is greater.

Part V

Income Tax Concessions

Constructing and furnishing of a new building or refurbishment andfurnishing of an existing building

Where a cultural entrepreneur, cultural practitioner or a governmentalentity responsible for a cultural project

secures a loan from a private sector lending institution for the purposeof constructing and furnishing a new building or refurbishing anexisting building, where the building will be primarily used for culturalactivities; and

has in an income year incurred expenditure in relation to thatconstruction, furnishing or refurbishment,

(2)

(a)

(b)

(3)

26.(1)

(a)

(b)

24

then in calculating the assessable income of the cultural entrepreneur, culturalpractitioner or governmental entity for an income year, there shall be deductedan amount equal to 100 per cent of the interest paid on the loan in the incomeyear.

The cultural project referred to in subsection (1) shall not have a value thatis less than $15 000, and the portion of the loan on which the concession atsubsection (1) is granted shall be no more than 50 percent of the value of thecultural project to be constructed or refurbished.

Set-off capital expenditure

Where a cultural entrepreneur, cultural practitioner, a governmentalentity or investor is desirous of constructing and furnishing a new building or ofrenovating and furnishing an existing building and the building is to be usedprimarily for cultural activities, the cultural entrepreneur, cultural practitioner,governmental entity or investor shall be allowed to set off approved capitalexpenditure against income derived from cultural activities over a period of 10years commencing in the year following completion of the project.

Allowance in respect of artistic work

Where in an income year a cultural entrepreneur, cultural practitioneror a governmental entity incurs expenditure in respect of an artistic work,however defined, there shall be allowed as a deduction, in ascertaining thechargeable profit derived from the cultural activities of the cultural entrepreneur,cultural practitioner or the governmental entity for that year of income, anallowance equal to 150 per cent of the actual expenditure up to a maximum of$250 000.

The deduction referred to in subsection (1) may only be claimed in respectof the initial acquisition of the work and where the work is done by a resident ofBarbados.

The allowance referred to in subsection (1) shall apply in total to allpurchases of artistic work in the income year.

(2)

27.

28.(1)

(2)

(3)

25

Marketing

Where a cultural entrepreneur, cultural practitioner or governmentalentity has in an income year incurred expenditure for marketing, productdevelopment and research related to marketing and product development, thenin calculating the assessable income derived from the cultural activities of thatcultural entrepreneur, cultural practitioner or governmental entity for an incomeyear, there shall be deducted an amount equal to 150 per cent of the expenditureincurred.

Training

Where a cultural entrepreneur, cultural practitioner or governmentalentity has in an income year incurred for the purpose of training persons employedby the cultural entrepreneur, cultural practitioner or governmental entity,expenditure for marketing, product development and research related tomarketing and product development, then in calculating the assessable incomederived from the cultural activities of that cultural entrepreneur, culturalpractitioner or governmental entity for an income year, there shall be deductedan amount equal to 150 per cent of the expenditure incurred.

The cultural entrepreneur, cultural practitioner or governmental entityreferred to in subsection (1) may claim an additional 50 per cent of theexpenditure where the cultural project involves an employee share ownershipscheme that meets the criteria prescribed by the Minister.

For the purposes of this section “employee share ownership scheme”means a reward scheme or package in which employees are offered shares in acompany

at a full or discounted price or free of cost;

as equity in a publicly traded company;

to facilitate the acquisition and distribution of a company’s share to itsemployees.

29.

30.(1)

(2)

(3)

(a)

(b)

(c)

26

Investment

Where an investor makes an investment in a cultural practitioner orapproved cultural project, in calculating the assessable income of the investorthere shall be deducted an amount equal to 100 per cent from their assessableincome for the first five years from the commencement of this Act.

Dividends

Dividends paid to a shareholder by a corporate entity in respect of acultural project shall not be subject to withholding tax and the provisions ofsections 65(4) and 65(4A) of the Income Tax Act, Cap. 73 shall not apply.

Part VI

Cultural Industries Development Fund

Establishment and resources of the Fund

There is established a Cultural Industries Development Fund.

The resources of the Fund shall consist of

any money transferred to the Fund from the Arts and Sports PromotionFund, Cap. 39;

any money voted by Parliament for the Fund;

any money received from the private sector;

moneys arising from gifts, grants or donations; and

any other money received from such other sources as the Minister maydetermine.

31.

32.

33.(1)

(2)

(a)

(b)

(c)

(d)

(e)

27

Purposes of the Fund

The purposes of the Fund are to

finance cultural projects and programmes that are designed to developthe cultural industries sector and train cultural entrepreneurs, culturalpractitioners, cultural administrators and cultural workers;

provide cultural entrepreneurs or cultural practitioners with non-repayable grants to enable them to participate in local and overseasevents, workshops and seminars, and allow for training, marketing,export and product development;

provide repayable grants to support cultural projects on the conditionthat the grants be repaid out of the future business revenues;

provide loans which allow for easy and flexible repayment togetherwith interest;

provide equity financing to allow investors to inject funds into culturalbusinesses and in return to take an equity share in the capital of suchbusinesses; and

to defray the costs incurred in the administration of this Act.

Administration and management of Fund

The Fund shall be kept, administered and managed by the AccountantGeneral under the general control and direction of the Minister.

The initial expenditure required for, or in connection with, theestablishment of the Fund shall be defrayed out of moneys provided byParliament.

Any temporary insufficiency of the Fund to discharge its liabilities shallbe defrayed out of such moneys as each House of Parliament may by resolutionapprove by way of advance for this purpose to the Fund.

34.

(a)

(b)

(c)

(d)

(e)

(f)

35.(1)

(2)

(3)

28

Every advance referred to in subsection (3) shall as soon as possible berepaid to the Consolidated Fund out of the resources of the Cultural IndustriesDevelopment Fund.

Reports

The Accountant-General shall prepare quarterly reports of theaccounts and economic activity of the Fund and shall deliver those reports to theMinister not later than 21 days following the end of each quarter.

The Minister responsible for Culture shall, as soon as practicable afterreceiving a report referred to in subsection (1), cause a copy to be laid in bothHouses of Parliament.

Auditing of the Fund

The accounts of the Fund shall be audited at least once every financialyear by the Auditor-General.

Investment in the Fund

Where a cultural entrepreneur, cultural practitioner or governmentalentity has in any income year invested an amount of money in the Fund, then incalculating the assessable income of that cultural entrepreneur, culturalpractitioner or governmental entity for that income year, there shall be deductedan amount equal to 150 per cent of the actual amount invested.

The benefit described in subsection (1) may only be granted on thecertificate of the Accountant-General to the effect that the cultural entrepreneur,cultural practitioner or governmental entity claiming the benefit has contributedthat amount of money in respect of the Fund.

(4)

36.(1)

(2)

37.

38.(1)

(2)

29

PART VII

Incentives for Audio-Visual Production and Motion Pictures

Exemption from taxes

Where a cultural entrepreneur or cultural practitioner who is anapproved producer of audio-visual content imports

equipment, machinery and materials for the construction of facilitiesfor use in audio-visual and motion picture production; and

equipment for use in audio-visual and motion picture production,

the approved producer shall be exempt from the payment of all duties and taxespayable on such imports of equipment, machinery and materials referred to inparagraphs (a) and (b).

Where an approved producer referred to under subsection (1) is desirousof establishing facilities for the production of audio-visual and motion pictures,that person shall be

allowed to set off approved capital expenditure incurred on suchfacilities against income derived from the audio-visual and motionindustry over a period of 10 years commencing in the year followingcompletion of the facilities;

exempt from the payment of property transfer tax on the initialpurchase of any property acquired for the specific purpose of providingsuch facilities;

eligible for interest rate subsidies on funds borrowed from privatesector lending institutions for the establishment of such facilities.

Where an approved producer referred to in subsection (1) has in an incomeyear incurred expenditure for the purpose of the production and acquisition inrespect of local films, then in calculating the assessable income of the approvedproducer for an income year, there shall be a write-off of 100 per cent.

39.(1)

(a)

(b)

(2)

(a)

(b)

(c)

(3)

30

Where an approved producer referred to under subsection (1) has in anincome year incurred expenditure for the purpose of training persons employedby the approved producer, then in calculating the assessable income of theapproved producer for an income year, there shall be deducted an amount equalto 150 per cent of the expenditure incurred.

Where an approved producer referred to under subsection (1) has in anincome year incurred expenditure for marketing, product development andresearch related to an approved cultural project, then in calculating the assessableincome of the approved producer for an income year, there shall be deducted anamount equal to 150 per cent of the expenditure incurred.

Where in connection with an approved cultural project, an approvedproducer requires the services of a specially qualified individual to carry out itsbusiness effectively from within Barbados and it is unable to acquire thoseservices in Barbados; and it is unable to retain those services from outsideBarbados without special tax concessions, the Minister may grant a taxconcession in respect of the specially qualified individual retained from outsideBarbados.

The tax concession referred to in subsection (6) is one that allows aprescribed percentage of the qualified individual’s salary or fees to be

exempt from income tax in Barbados to an amount that is 60 per centof his accessable income;

paid in a foreign currency in a trust account without being liable to thepayment of income tax in Barbados as to the amount paid or any interestpaid or any interest earned thereon;

paid in some other prescribed manner in another currency or otherwisewithout being liable to income tax in Barbados.

(4)

(5)

(6)

(7)

(a)

(b)

(c)

31

PART VIII

Incentives for Heritage Building and Conservation

Concessions in respect of heritage building and conservation

A cultural entrepreneur, cultural practitioner or a governmental entitythat is in receipt of a licence issued under section 19 and who imports suppliesfor a cultural project in the area of heritage building and conservation shall beexempt from the payment of all duties and taxes on such imports where

these imports are used for the purposes of heritage building andconservation; and

the cultural entrepreneur, cultural practitioner or governmental entitycomplies with the provisions of section 25.

Where a cultural entrepreneur, cultural practitioner or a governmentalentity referred to in subsection (1)

secures a loan from a private sector lending institution for the purposesof financing a project concerning heritage building and conservation;and

has in an income year incurred expenditure in relation to the heritagebuilding and conservation

then in calculating the assessable income of the cultural entrepreneur, culturalpractitioner or governmental entity for an income year, there shall be deductedan amount equal to 150 per cent of the interest paid on the loan in the incomeyear.

Where a cultural entrepreneur, cultural practitioner or a governmentalentity referred to in subsection (1) expends money on an approved heritagebuilding and conservation project, the cultural entrepreneur, cultural practitioneror governmental entity shall be allowed to set off approved capital expenditureagainst income derived from the heritage building and conservation project over

40.(1)

(a)

(b)

(2)

(a)

(b)

(3)

32

a period of 10 years commencing in the year following the completion of theproject.

Where in an income year a cultural entrepreneur, cultural practitioner orgovernmental entity incurs expenditure in respect of a heritage building andconservation project, there shall be allowed as a deduction, in ascertaining thechargeable profits derived from the heritage building and conservation project ofthe cultural entrepreneur, cultural practitioner or governmental entity for that yearof income, an allowance equal to 150 per cent of the actual expenditure up to amaximum of $250 000.

The deduction referred to in subsection (4) may only be claimed in respectof the initial heritage building and conservation project, and where the project isimplemented by a resident of Barbados who is registered with a culturalagency.

PART IX

Miscellaneous

Regulations

The Authority may, with the approval of the Minister make regulations

prescribing

the form of application for a cultural project;

financial forecasts and specifications that are to accompany anapplication for the approval of a cultural project;

the form and content of interim approvals and the conditions tobe contained therein;

the form and content of the licence to be issued to the culturalentrepreneur, cultural practitioner or governmental entity inrespect of an approved cultural project;

(4)

(5)

41.

(a)

(i)

(ii)

(iii)

(iv)

33

the criteria for determining the projects that are to benefit fromthe Fund;

the fees to be paid in respect of any licence issued under this Act;

the fees for services charged by the Authority in connection witha cultural project; and

generally for the purpose of giving effect to this Act.

Offences

A person who contravenes any provision of this Act or the Regulationsmade pursuant to this Act is guilty of an offence and is liable on summaryconviction to a fine of $2 500 or to imprisonment for a term of 2 years or to both.

Commencement

This Act comes into operation on a date to be fixed by proclamation.

(v)

(vi)

(vii)

(b)

42.

43.

34

FIRST SCHEDULE

(Section 5(2))

Constitution and Procedure of Board

The Board shall comprise

The Board shall comprise

a Chairman and Deputy Chairman; and

such other members as the Minister may appoint by instrument inwriting.

Temporary appointment of Board

The Minister may, in accordance with paragraph 1(b), appoint anyperson to act temporarily in the place of any Director who is absent from Barbadosor is unable to act.

Tenure

A Director holds office for such period as the Minister determinesunless he resigns or his appointment is revoked before the end of that period.

Every Director is, on the expiration of the period of his appointment,eligible for re-appointment for a further period.

Where a vacancy is created by the death, resignation or removal from officeof a Director, a person may be appointed in accordance with paragraph 1(b) tofill that vacancy.

Resignation of Chairman or Deputy Chairman

The Chairman or Deputy Chairman may at any time resign his officeby instrument in writing addressed to the Minister and, upon the receipt by theMinster of the instrument, the Chairman or Deputy Chairman ceases to be

1.

(a)

(b)

2.

3.(1)

(2)

(3)

4.

35

Chairman or Deputy Chairman and, if the instrument so specifies, also ceases tobe a director.

Resignation of Director

A Director, other than the Chairman or Deputy Chairman may at anytime resign his office by instrument in writing addressed to the Minister andtransmit the instrument through the Chairman and, from the date of the receiptby the Minister of the instrument, the Director ceases to be a Director.

Automatic termination of memberships

Any Director who fails, without reasonable excuse, to attend 3consecutive meetings of the Board ceases to be a Director and is not eligible forappointment to the Board until the expiry of 3 years from the date when he ceasesto be a director.

Revocation of membership

The Minister may at any time by instrument in writing revoke theappointment of any Director.

Disqualification of director

A person is not qualified for appointment as a Director if he isemployed by the Authority.

Notice in Official Gazette

The appointment and the cessation of appointment of a Director shallbe notified in the Official Gazette.

Seal

The seal of the Authority shall be kept in the custody of the Chairmanor Deputy Chairman, or such officer of the Authority as the Authority approves,

5.(1)

6.

7.

8.

9.

10.(1)

36

and may be affixed to documents or instruments pursuant to a resolution of theAuthority in the presence of the Chairman or Deputy Chairman and the Secretary.

The seal of the Authority shall be authenticated by the signature of theChairman and the Secretary.

All documents or instruments, other than those required by law, to be underseal, and all decisions of the Authority may be signified under the hand of theChairman or Deputy Chairman.

Meetings

The Board shall meet at least once a month and at such other times asmay be necessary, or expedient for the transaction of its business.

Disclosure of directors interest

A Director who has any interest in a company or concern with whichthe Authority proposes to make a contract or otherwise transact business shalldisclose to the Authority the particulars of that interest, and details of thedisclosure shall be recorded in the minutes taken at the meetings at which thedisclosure is made.

A Director referred to in subsection (1) shall not take part in anydeliberation or discussion of the Board relating to that contract or business.

Special Meetings

The Chairman or, in the event of his absence from Barbados, orinability to act as such, the Deputy Chairman may at any time call a meeting ofthe Board and shall call a meeting within 7 days of the receipt by him of a requestfor that purpose addressed to him in writing and signed by 3 other Directors.

Presiding at meetings

The Chairman or, in his absence, the Deputy Chairman shall presideat all meetings of the Board and, in the case of the absence of both, the Directors

(2)

(3)

11.

12.(1)

(2)

13.

14.

37

present and constituting a quorum shall elect a temporary Chairman from amongtheir members who shall preside at the meeting.

Quorum

A majority of the Directors shall constitute a quorum.

Decisions

The decisions of the Board shall be by a majority of votes and, in anycase in which the voting is equal, the Chairman, the Deputy Chairman ortemporary Chairman presiding at the meeting has, in addition to an original vote,a second or casting vote.

Minutes

Minutes in proper form of each meeting shall be kept by the Secretaryor such officer as the Authority appoints for the purpose and shall be confirmedin writing at the next meeting by the Chairman or Deputy Chairman.

Confirmed minutes of meetings shall be submitted to the Minister withinone month of the date of the meeting at which they were confirmed.

Attendance of non-members at meetings

The Chairman may write any person to attend a meeting of the Boardwhere the Board considers it necessary to do so.

A person referred to in sub-paragraph (1) may take part in the deliberationsof the Board but shall not vote on any matter.

Validity of decisions of the Board

Any act done or proceeding taken by the Board under this Act or theregulations may not be questioned on the ground of

the existence of any vacancy in the membership of or of any defect inthe constitution of the Board;

15.

16.

17.(1)

(2)

18.(1)

(2)

19.

(a)

38

any omission, defect or irregularity that does not affect the merits ofthe case.

(b)

39

SECOND SCHEDULE

(Section 21(1))Duty Free Concessions

Part I

Equipment

SECTOR

AUDIO VISUALEQUIPMENT

TOOLS OF TRADE

Cameras and camera accessoriesEditing suites, editing equipmentElectrical equipmentGeneratorsGrip equipmentLighting equipmentMake up , make up toolsProduction office equipmentProduction vehicles: grip truck, generator truck,wardrobe truck , trailersSet pieces, props e.g prop gunsSound engineering equipmentSound recording and mixing equipmentStunt and special effects equipmentTapes, discs recording material

40

SECOND SCHEDULE - (Cont'd)

Duty Free Concessions - (Cont'd)

Part I - (Cont'd)

Equipment - (Cont'd)

SECTOR - (Cont'd)

CRAFT

TOOLS OF TRADE - (Cont'd)

Soldering ironsAnvilsWire cuttersDrilling machinesFiling toolsTape measuresMetal rolling millsTorches and accessoriesFlexible shaftsJewellery toolsFabricBeadsLeatherHooksFastenersGlueGlazesStainsMetal dyesJewellery suppliesWire (gold, copper, silver)LinoleumPaperSewing machinesKilns (electric or gas)Computer and softwareCredit card machinesJewellery display cases

41

SECOND SCHEDULE - (Cont'd)

Duty Free Concessions - (Cont'd)

Part I - (Cont'd)

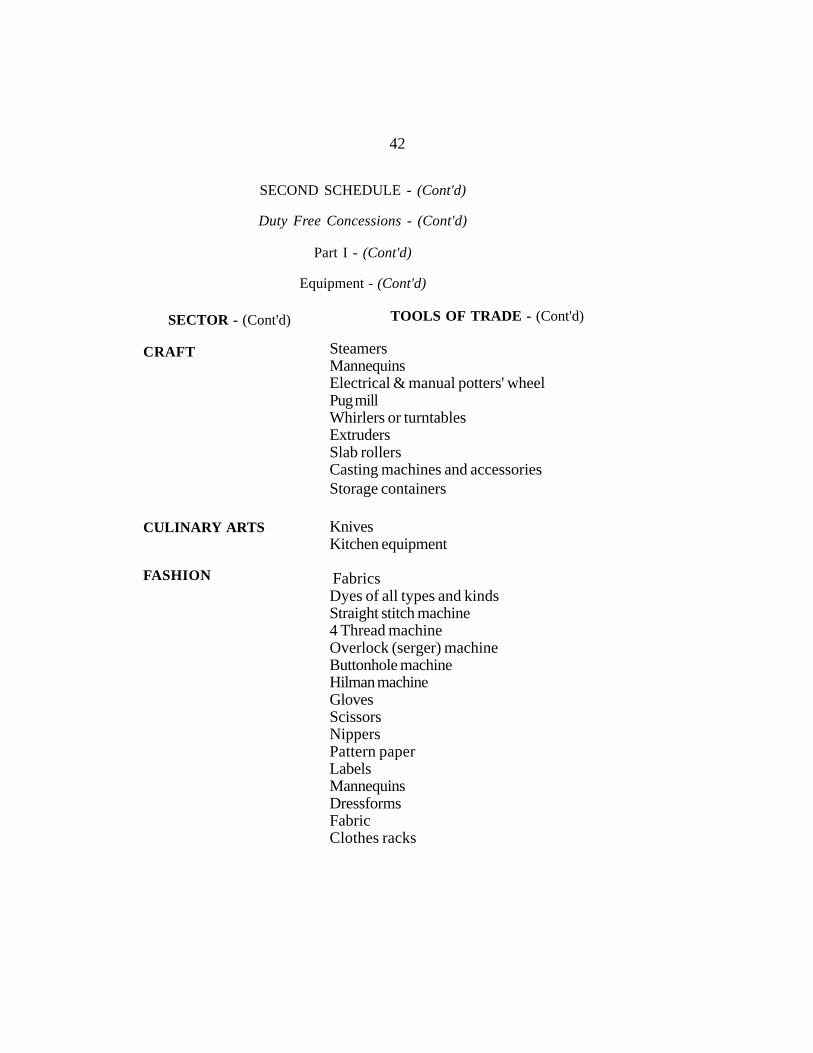

Equipment - (Cont'd)

SECTOR - (Cont'd)

CRAFT

CULINARY ARTS

FASHION

TOOLS OF TRADE - (Cont'd)

SteamersMannequinsElectrical & manual potters' wheelPug millWhirlers or turntablesExtrudersSlab rollersCasting machines and accessoriesStorage containers

KnivesKitchen equipment

FabricsDyes of all types and kindsStraight stitch machine4 Thread machineOverlock (serger) machineButtonhole machineHilman machineGlovesScissorsNippersPattern paperLabelsMannequinsDressformsFabricClothes racks

42

SECOND SCHEDULE - (Cont'd)

Duty Free Concessions - (Cont'd)

Part I - (Cont'd)

Equipment - (Cont'd)

SECTOR - (Cont'd)

FASHION - (Cont'd)

MUSIC

TOOLS OF TRADE - (Cont'd)

Wall fixtures for displaying garmentsThreadsYarnsNotionsSteamersDisplay racksIndustrial IronsNeedlesTape measuresRotary machineButton tacking machine

All types of acoustic guitarsAll types of electric guitarsGuitar accessoriesStraps, bags and casesSlides, caposPick and pick guardsAll types of stringElectric and battery powered tunersGuitar standsCleaning agentsKeyboards standsProfessional keyboardsKeyboard controllersKeyboard amplifiersSound modulesDrumsets

43

SECOND SCHEDULE - (Cont'd)

Duty Free Concessions - (Cont'd)

Part I - (Cont'd)

Equipment - (Cont'd)

SECTOR - (Cont'd)

MUSIC - (Cont'd)

TOOLS OF TRADE - (Cont'd)

Acoustic drum-kits and accessoriesElectronic drum machines or modulesSnare-Bass-drumsHand drums: Djembe, congas, maracasWooden bongosWooden and plastic tambourinesWooden and plastic jam blocksVibra slapsCabasasCowbellsGuirosStraps and belts for carrying drumsCarpetingBlank CDsSound proofing materialFlash drivesComputers & music production softwareDuplicating systemsDigital and analog mixersDigital multi-track recorders andaccessoriesPortable recordersCD/DVD flash recordersActive and passive monitorsHeadphonesHeadphone AmplifiersSingle- dual- and multi-channel preamplifiersand accessoriesAmplifiers

44

SECOND SCHEDULE - (Cont'd)

Duty Free Concessions - (Cont'd)

Part I - (Cont'd)

Equipment - (Cont'd)

SECTOR - (Cont'd)

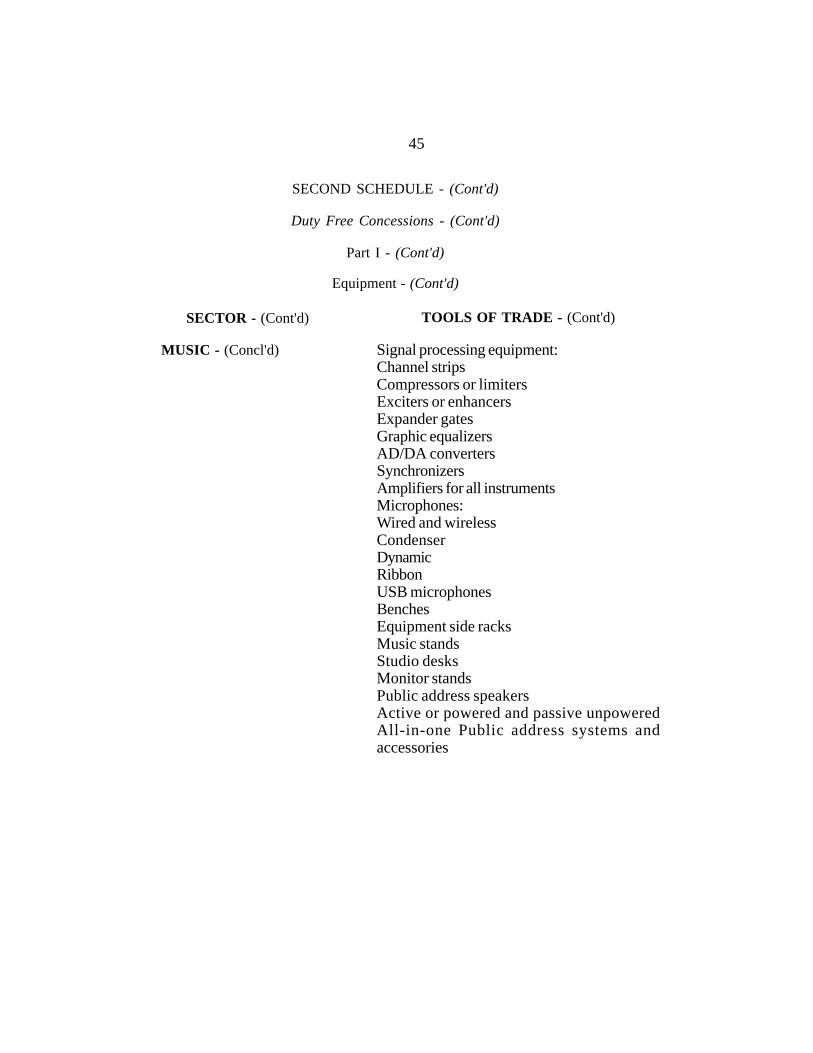

MUSIC - (Concl'd)

TOOLS OF TRADE - (Cont'd)

Signal processing equipment:Channel stripsCompressors or limitersExciters or enhancersExpander gatesGraphic equalizersAD/DA convertersSynchronizersAmplifiers for all instrumentsMicrophones:Wired and wirelessCondenserDynamicRibbonUSB microphonesBenchesEquipment side racksMusic standsStudio desksMonitor standsPublic address speakersActive or powered and passive unpoweredAll-in-one Public address systems andaccessories

45

SECOND SCHEDULE - (Cont'd)

Duty Free Concessions - (Cont'd)

Part I - (Cont'd)

Equipment - (Cont'd)

SECTOR - (Cont'd)

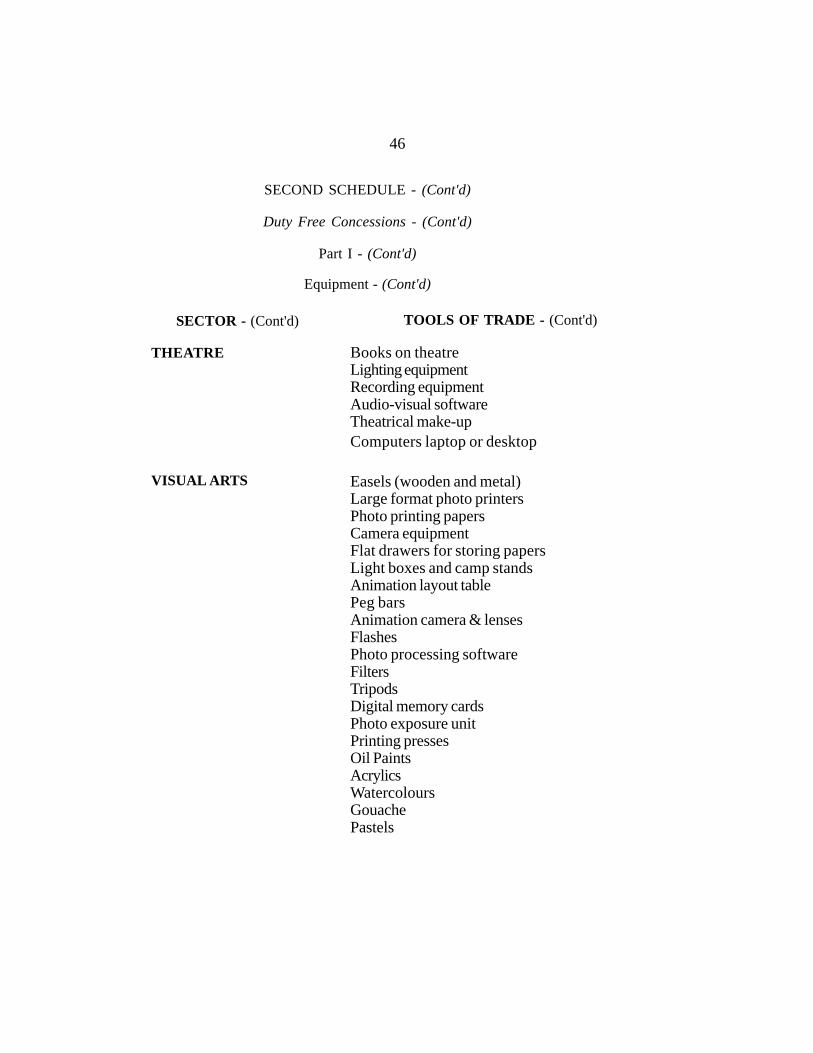

THEATRE

VISUAL ARTS

TOOLS OF TRADE - (Cont'd)

Books on theatreLighting equipmentRecording equipmentAudio-visual softwareTheatrical make-upComputers laptop or desktop

Easels (wooden and metal)Large format photo printersPhoto printing papersCamera equipmentFlat drawers for storing papersLight boxes and camp standsAnimation layout tablePeg barsAnimation camera & lensesFlashesPhoto processing softwareFiltersTripodsDigital memory cardsPhoto exposure unitPrinting pressesOil PaintsAcrylicsWatercoloursGouachePastels

46

SECOND SCHEDULE - (Cont'd)

Duty Free Concessions - (Cont'd)

Part I - (Cont'd)

Equipment - (Cont'd)

SECTOR - (Cont'd)

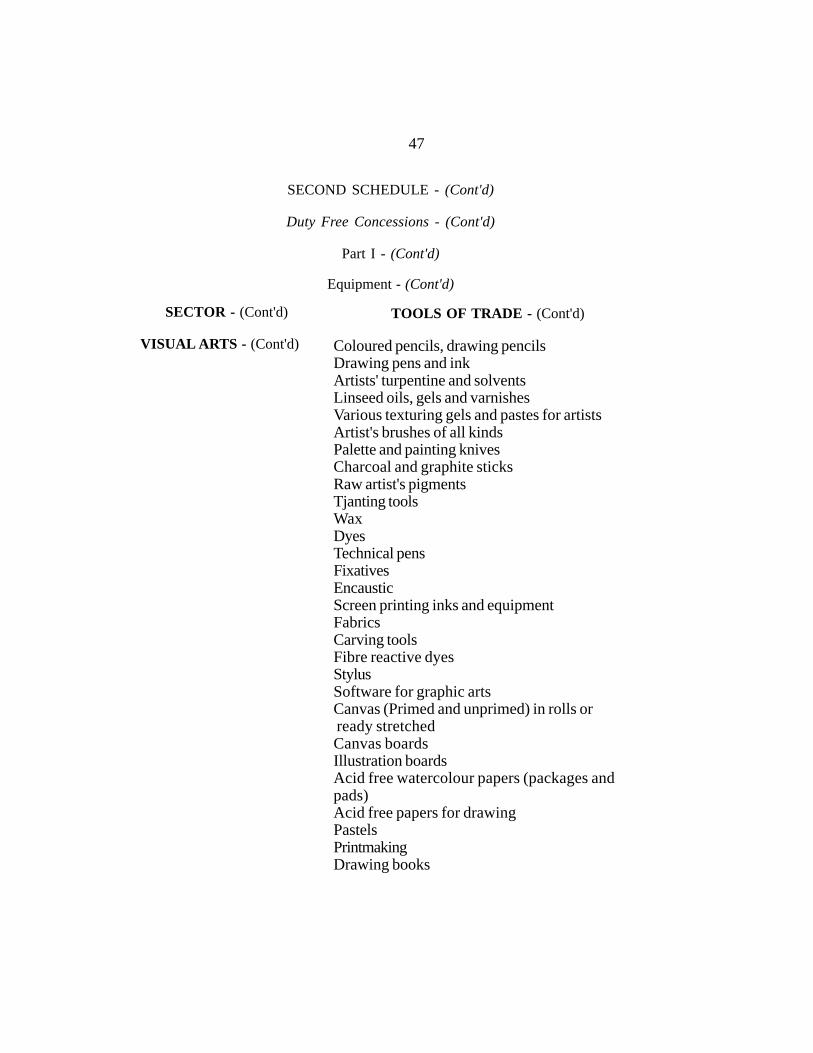

VISUAL ARTS - (Cont'd)

TOOLS OF TRADE - (Cont'd)

Coloured pencils, drawing pencilsDrawing pens and inkArtists' turpentine and solventsLinseed oils, gels and varnishesVarious texturing gels and pastes for artistsArtist's brushes of all kindsPalette and painting knivesCharcoal and graphite sticksRaw artist's pigmentsTjanting toolsWaxDyesTechnical pensFixativesEncausticScreen printing inks and equipmentFabricsCarving toolsFibre reactive dyesStylusSoftware for graphic artsCanvas (Primed and unprimed) in rolls or ready stretchedCanvas boardsIllustration boardsAcid free watercolour papers (packages andpads)Acid free papers for drawingPastelsPrintmakingDrawing books

47

SECOND SCHEDULE - (Cont'd)

Duty Free Concessions - (Cont'd)

Part I - (Cont'd)

Equipment - (Cont'd)

SECTOR - (Cont'd)

VISUAL ARTS - (Cont'd)

TOOLS OF TRADE - (Cont'd)

Matt boardsAnimation paperLayout padsStoryboard padsAnimation layout sheetsField guidesArt books and teaching aidsMatt cutter and bladesArtist portfoliosArtist presentation blocksContainers or tubes for canvasesGlazes and stainsSlab rollersCeramic pencils and crayonsHandtoolsPottery wheelsBlungers, jiggers, jolleyersPugmills and related productsSpecialists paper

48

SECOND SCHEDULE - (Cont'd)

Duty Free Concessions - (Cont'd)

Part I - (Cont'd)

Equipment - (Cont'd)

SECTOR - (Cont'd)

TECHNICAL

TOOLS OF TRADE - (Cont'd)

GeneratorsIntercom systems or walkie talkiesEvent planning softwareTicket countersTicket production systemsEvent themed itemsDécor itemsTressle tablesPlastic chairsSpecialised mirrorsSound boardsDrumsKeyboardsGuitars (rhythm and bass)percussion instrumentsWind instrumentsSpeakersMixers (analog and digital)Power ampsCables and snakesDirect boxesMicrophones and standsEquipment casesStage trussingDieselVehicles (vans and trucks)TarpaulinHand ToolsRopeStagesInstrument amplifiers

49

SECOND SCHEDULE - (Cont'd)

Duty Free Concessions - (Cont'd)

Part I - (Cont'd)

Equipment - (Cont'd)

SECTOR - (Cont'd)

TECHNICAL - (Cont'd)

TOOLS OF TRADE - (Cont'd)

Music standsMixing consolesCD burnersCompressorsPower toolsWoods, metals and paintsTapes, screws, nailsRigging toolsFabricsBlocks, cleatsStaplesFastenersFlagpolesFlutter flagsInflatablesSewing materialsTranspondersRepeatersBatteries of all typesSpeaker enclosuresDigital snakesCD replicating machineryProjectors and screensPlasma screensCounterweight systems:pulleys, roping systems, weights, shacklespipe and drape infrastructure (plastic andmetallic)Modular exhibition frameworks

50

SECOND SCHEDULE - (Cont'd)

Duty Free Concessions - (Concl'd)

Part I - (Concl'd)

Equipment - (Concl'd)

SECTOR - (Concl'd)

TECHNICAL - (Concl'd)

TOOLS OF TRADE - (Concl'd)

Modular signageComputers and softwareTabletsCamera and photography softwareSpeaker labelsGlue and other adhesivesLighting dimmersLighting gels and gel framesStagelighting unitsLighting consoles ladders CD playersCDsDesign softwareCanvasFibre optic cableSpeaker management systemsHydraulic lifts

51

SECOND SCHEDULE - (Cont'd)

PART II

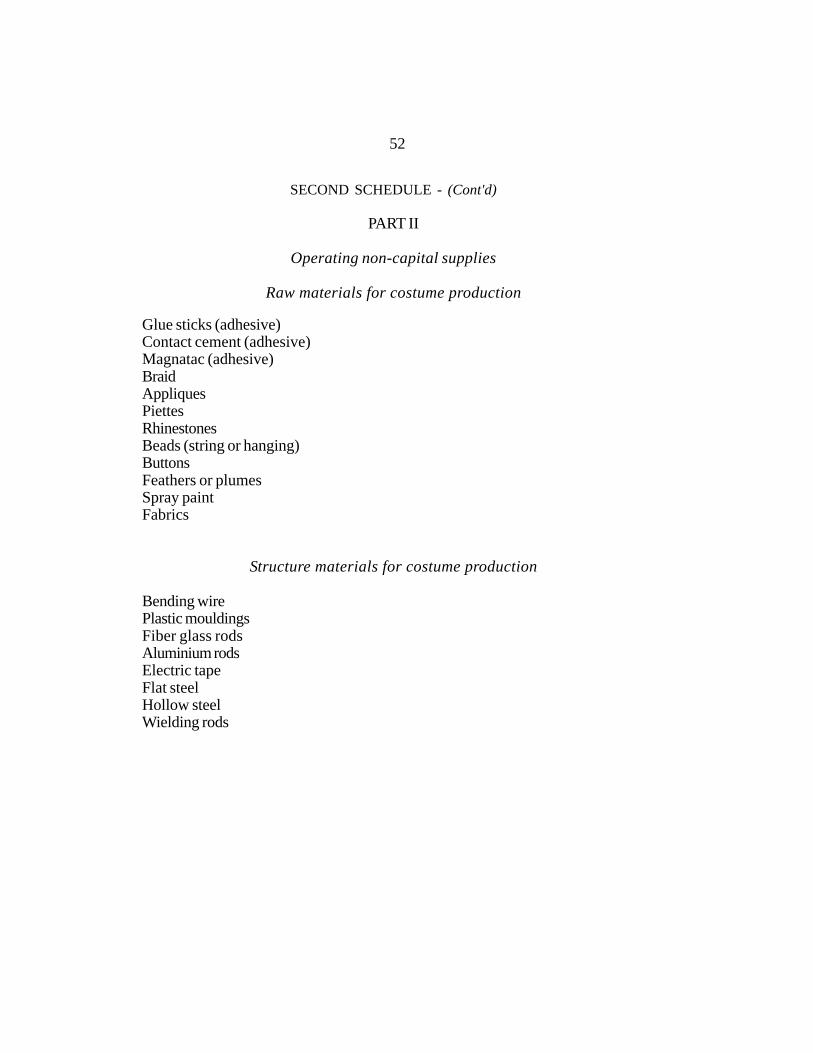

Operating non-capital supplies

Raw materials for costume production

Glue sticks (adhesive)Contact cement (adhesive)Magnatac (adhesive)BraidAppliquesPiettesRhinestonesBeads (string or hanging)ButtonsFeathers or plumesSpray paintFabrics

Structure materials for costume production

Bending wirePlastic mouldingsFiber glass rodsAluminium rodsElectric tapeFlat steelHollow steelWielding rods

52

SECOND SCHEDULE - (Concl'd)

PART II - (Concl'd)

Operating non-capital supplies - (Concl'd)

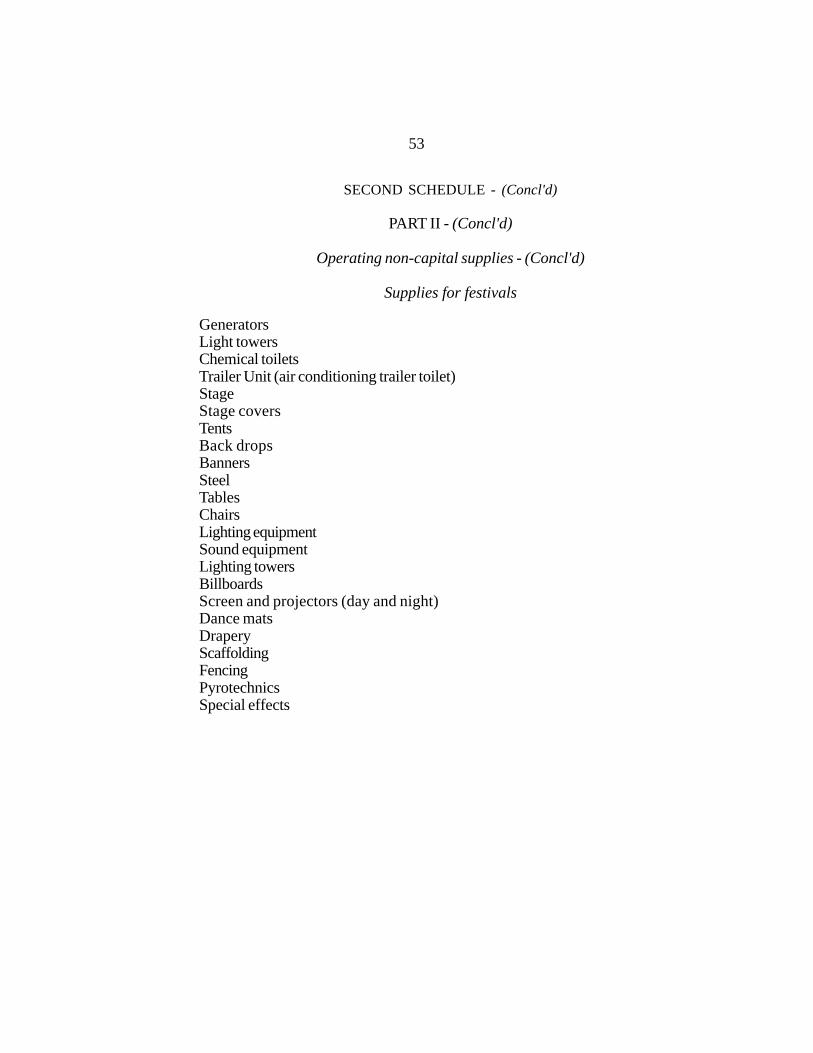

Supplies for festivals

GeneratorsLight towersChemical toiletsTrailer Unit (air conditioning trailer toilet)StageStage coversTentsBack dropsBannersSteelTablesChairsLighting equipmentSound equipmentLighting towersBillboardsScreen and projectors (day and night)Dance matsDraperyScaffoldingFencingPyrotechnicsSpecial effects

53

Read three times and passed the House of Assembly thisday of , 2013.

Speaker

Read three times and passed the Senate this day of , 2013.

President

54

CULTURAL INDUSTRIES DEVELOPMENT ACT, 2013

EXPLANATORY MEMORANDUM

PART I

Preliminary

states the short title by which the Act may be cited.

sets out the definitions of terms used in the legislation.

PART II

Establishment, Composition and Administration of the Authority

speaks to the establishment of the Authority and gives theAuthority a separate and distinct legal entity to which section21 of the Interpretation Act Cap. 1 applies.

states the functions of the Authority.

establishes the Board of Directors of the Authority. The Boardis responsible for advising the Minister on matters connectedwith cultural industries and for executing the policy of theAuthority. Sub-clause (2) speaks to the constitution of theBoard which is set out in the First Schedule.

provides for the appointment of persons to offices. The ChiefExecutive Officer is subject to the Board with respect to policyand the management of the affairs of the Authority.

gives the Authority, with the approval of the Minister, thepower to appoint officers, agents and servants and fix theirremuneration.

Clause 1:

Clause 2:

Clause 3:

Clause 4:

Clause 5:

Clause 6:

Clause 7:

i

speaks to the pension rights of a public officer who is secondedto the Authority.

provides for the savings of pensions of a public officer who istransferred or becomes employed with the Authority.

states that the Minister may give the Authority directions of ageneral or specific nature with respect to policy and theAuthority shall comply with the directions.

states that the Authority may charge fees for the issue oflicences and for any service performed, and these fees are tobe prescribed by the Minister responsible for Finance.

PART III

Approval of Cultural Project

states that a cultural entrepreneur, cultural practitioner orgovernmental entity may apply to the Minister to have acultural project approved. Sub-clause (2) states that theMinister may declare by order a cultural project to be anapproved cultural project.

states the additional information which an applicant may haveto furnish with respect to an application under section 12.

states that the Minister, with the approval of the Cabinet, maygrant to a cultural entrepreneur, cultural practitioner andgovernmental entity interim approval of a cultural project anda notice to that effect shall be made by the Minister andpublished in the Official Gazette.

gives the Minister 90 days after receiving an application tonotify the applicant in writing of the approval or refusal of the

Clause 8:

Clause 9:

Clause 10:

Clause 11:

Clause 12:

Clause 13:

Clause 14:

Clause 15:

Cultural Industries Development Act,2013

ii

application or request the submission of additionalinformation.

speaks to the form and characteristics of an interim approval.

states that an interim approval may be suspended or revokedby the Minister in certain circumstances and where it issuspended or revoked, the Minister shall in writing inform theperson to whom the approval was granted of the reason for thesuspension or revocation.

provides that where a cultural project has been developed theMinister may declare the project to be an approved culturalproject. This declaration shall take the form of an order. Theorder shall inter alia specify the benefits granted to theapplicant and the conditions to be observed. This order maybe revoked by a notice published in the OfficialGazette wherethe applicant fails to comply with conditions imposed in theorder.

states that a licence in respect of a cultural project shall beissued by the Minister where the cultural project has beenreviewed and assessed by the Authority and has met thestandards and requirements of the relevant cultural agency.Sub-clause (2) speaks inter alia to conditions that may beimposed on the cultural practitioner, cultural entrepreneur orgovernmental entity. Sub-clause (3) states that where thecultural entrepreneur, cultural practitioner or governmentalentity fails to observe the conditions set out in a licence, theMinister shall revoke the licence by a notice published in theOfficial Gazette.

speaks to the effective date of the licence from which thecultural entrepreneur, cultural practitioner or governmental

Clause 16:

Clause 17:

Clause 18:

Clause 19:

Clause 20:

Cultural Industries Development Act,2013

iii

entity may receive tax benefits. This date shall also mark thebeginning of the initial year of assessment for the purpose ofcomputing tax.

PART IV

Duty Free Concessions

provides for the cultural entrepreneur, cultural practitioner orgovernmental entity to be granted a permit to import the itemsset out in the Second Schedule. Sub-clause (2) exempts thesepersons from the payment of import duty, stamp duty andvalue added tax on the items listed in the Second Schedule,building materials purchased locally and other capital assets.Sub-clause (4) states that a governmental entity will be exemptfrom duties and taxes on imports used in the construction andfurnishing of a new building or the renovation and furnishingof an existing building where the building is to be usedprimarily for cultural activities.

provides that the Minister may by written notice to the holderof the permit, either suspend the operation of the permit orrevoke the permit and shall give reasons where he is satisfiedthat the holder obtained the permit by a false statement, heabused or misused the permit or breached or failed to complywith any condition stipulated in the permit.

provides for the incentives to which a cultural entrepreneur,cultural practitioner or governmental entity is entitled inrespect of an approved cultural project.

provides that where a cultural entrepreneur, culturalpractitioner or governmental entity imports building material,equipment and supplies without payment of duties and taxesand disposes of the equipment and supplies without the

Clause 21:

Clause 22:

Clause 23:

Clause 24:

Cultural Industries Development Act,2013

iv

authorisation of the Minister, that person is guilty of anoffence. The section provides for the requisite fine.

states that the Comptroller shall require that records be kept,and that the records be inspected. The records are to be keptfor 5 years from the date of importation or the date of thepayment of the duty. Sub-clause (3) speaks to an offence ofwilfully delaying, hindering or obstructing the Comptrollerfrom inspecting equipment and supplies and to the fine of $50000 or to 5 times the value of the equipment, building materialand supplies which ever is greater.

PART V

Income Tax Concessions

provides for an income tax deduction which a culturalentrepreneur, cultural practitioner or governmental entity mayreceive in respect of interest paid on a loan from a privatesector lending institution, for the purpose of constructing andfurnishing a new building or refurbishing an existing building.

states that the cultural entrepreneur, cultural practitioner,governmental entity or investor shall be allowed to set offapproved capital expenditure against income derived fromcultural activities and is exempt from the payment of propertytransfer tax where certain conditions are met.

states that where in an income year a cultural entrepreneur,cultural practitioner or governmental entity incursexpenditure in respect of artistic work, a deduction shall beallowed of 150 percent of the actual expenditure up to amaximum of $250 000. The deduction may only be claimedin resect of the initial acquisition of the artistic work wherethe work is done by a resident of Barbados. The allowance

Clause 25:

Clause 26:

Clause 27:

Clause 28:

Cultural Industries Development Act,2013

v

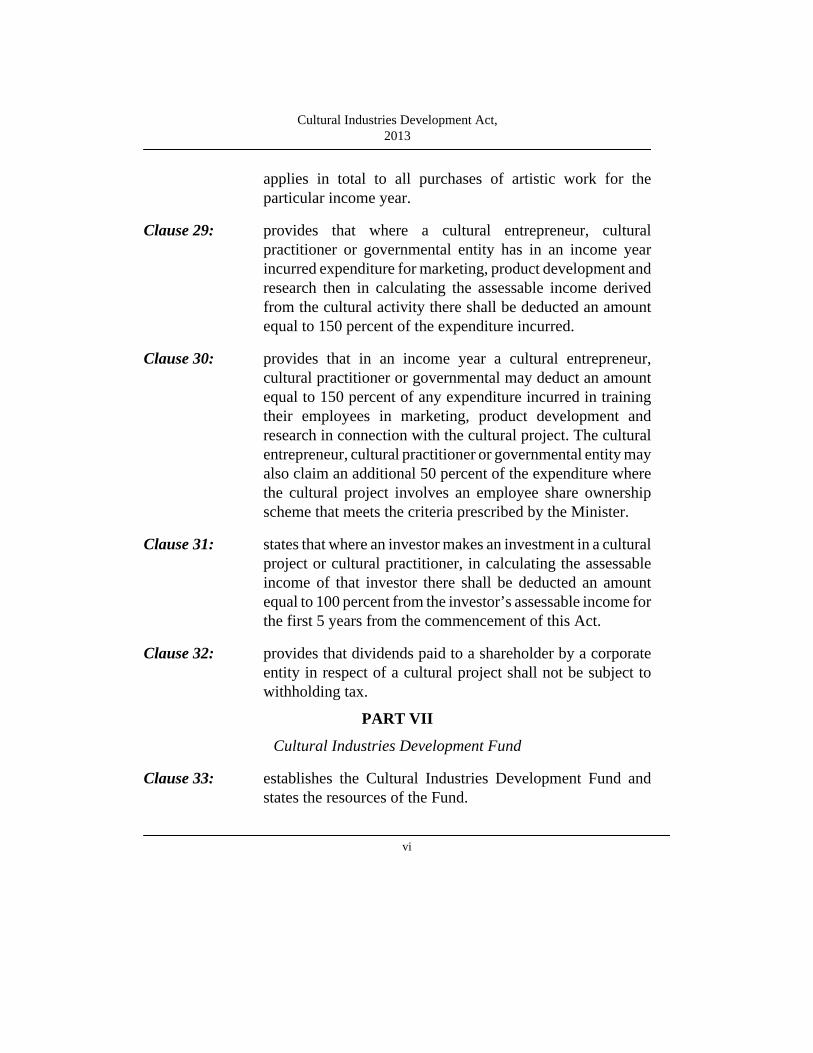

applies in total to all purchases of artistic work for theparticular income year.

provides that where a cultural entrepreneur, culturalpractitioner or governmental entity has in an income yearincurred expenditure for marketing, product development andresearch then in calculating the assessable income derivedfrom the cultural activity there shall be deducted an amountequal to 150 percent of the expenditure incurred.

provides that in an income year a cultural entrepreneur,cultural practitioner or governmental may deduct an amountequal to 150 percent of any expenditure incurred in trainingtheir employees in marketing, product development andresearch in connection with the cultural project. The culturalentrepreneur, cultural practitioner or governmental entity mayalso claim an additional 50 percent of the expenditure wherethe cultural project involves an employee share ownershipscheme that meets the criteria prescribed by the Minister.

states that where an investor makes an investment in a culturalproject or cultural practitioner, in calculating the assessableincome of that investor there shall be deducted an amountequal to 100 percent from the investor’s assessable income forthe first 5 years from the commencement of this Act.

provides that dividends paid to a shareholder by a corporateentity in respect of a cultural project shall not be subject towithholding tax.

PART VII

Cultural Industries Development Fund

establishes the Cultural Industries Development Fund andstates the resources of the Fund.

Clause 29:

Clause 30:

Clause 31:

Clause 32:

Clause 33:

Cultural Industries Development Act,2013

vi

provides for the purposes of the Fund.

states that the Fund is to be administered by theAccountant-General, and the initial expenditure required forthe Fund shall be defrayed out of the moneys provided byParliament. Any temporary insufficiency of the Fund todischarge its liabilities shall be defrayed by moneys voted byParliament by way of advance and every advance shall berepaid to the Consolidated Fund by resources from the Fund.

provides for the Accountant-General to prepare quarterlyreports of accounts and economic activity of the Fund andthese reports are to be delivered to the Minister who shall laya copy in both Houses of Parliament.

states that the accounts of the Fund shall be audited at leastonce every financial year by the Accountant- General.

provides for a cultural entrepreneur, cultural practitioner orgovernmental entity to invest in the Fund.

PART VII

Incentives for Audio-Visual Production and Motion Pictures

provides for exemption from taxes for a cultural entrepreneuror cultural practitioner who is an approved producer of audio-visual content. Some of the concessions granted in this areaextend to equipment, machinery and materials used in theconstruction of audio-visual facilities, equipment for use inaudio-visual and motion picture production, as well as anexemption from property transfer tax and from income tax.

Clause 34:Clause 35:

Clause 36:

Clause 37:

Clause 38:

Clause 39:

Cultural Industries Development Act,2013

vii

PART VIII

Incentives for Heritage Building and Conservation

speaks to concessions to be granted to a cultural entrepreneur,cultural practitioner or governmental entity in respect of aproject connected to heritage building and conservation.

PART IX

Miscellaneous

gives the Authority, with the approval of the Minister, thepower to make regulations.

provides for the offences under this Act.

provides for the Act to come into operation on a date to befixed by proclamation.

First Schedule: provides for the constitution and procedure of the Board.

Second Schedule: provides in Part I, for a list of tools of trade to be used by acultural entrepreneur, a cultural practitioner and a governmental entity. Part IIprovides for a list of operating non-capital supplies that are necessary forpreparing for national festivals.

Clause 40:

Clause 41:

Clause 42:

Clause 43:

Cultural Industries Development Act,2013

viii